Use these links to rapidly review the document

TABLE OF CONTENTS

TABLE OF CONTENTS 2

TABLE OF CONTENTS

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

As confidentially submitted to the Securities and Exchange Commission on October 26, 2018

This draft registration statement has not been publicly filed with the Securities and Exchange Commission and all information herein remains strictly confidential.

Registration No. 333-[ · ]

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

AMCOR PLC

(Exact Name of Registrant as Specified in Its Charter)

| | | | |

Jersey (Channel Islands)

(State or other jurisdiction of

incorporation or organization) | | 3990

(Primary Standard Industrial

Classification Code Number) | | [·]

(I.R.S. Employer

Identification No.) |

83 Tower Road North

Warmley, Bristol BS30 8XP

United Kingdom

+44 117 9753200

(Address, including Zip Code, and Telephone Number, Including Area Code, of Registrant's Principal Executive Offices)

Julie McPherson

Group General Counsel and Company Secretary

83 Tower Road North

Warmley, Bristol BS30 8XP

United Kingdom

+44 117 9753200

(Name, Address, including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

| | | | |

| With a copy to: |

Eric L. Schiele, P.C.

Richard B. Aftanas, P.C.

Jonathan L. Davis, P.C.

Kirkland & Ellis LLP

601 Lexington Avenue

New York, New York 10022

(212) 446-4800 |

|

Sheri H. Edison

Senior Vice President, Chief Legal Officer and Secretary

Bemis Company, Inc.

2301 Industrial Drive

Neenah, Wisconsin 54956

(920) 727-4100 |

|

Michael A. Stanchfield

Amy C. Seidel

Brandon C. Mason

Faegre Baker Daniels LLP

90 South Seventh Street #2200

Minneapolis, Minnesota 55402

(612) 766-7000 |

Approximate date of commencement of proposed sale of the securities to the public:

As soon as practicable after this registration statement is declared effective and upon completion or waiver of all other conditions to the closing of the acquisition described herein.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, please check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, as amended (the "Securities Act"), check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | |

| Large accelerated filer o | | Accelerated filer o | | Non-accelerated filer ý | | Smaller reporting company o Emerging growth company o |

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. o

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) o

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) o

CALCULATION OF REGISTRATION FEE

| | | | | | | | |

| | | | | | | | |

| |

Title of each class of securities

to be registered

| | Amount to be

registered

| | Proposed maximum

offering price per

unit

| | Proposed maximum

aggregate offering

price

| | Amount of

registration fee

|

|---|

| |

Ordinary shares, par value $0.01 per share | | [·](1) | | N/A | | $[·](2) | | $[·](3) |

|

- (1)

- Represents the maximum number of ordinary shares, par value $0.01 per share (the "New Amcor Shares"), of Amcor plc ("New Amcor") to be issued upon completion of the merger described in the proxy statement/prospectus contained herein, based on [ · ] shares of common stock of Bemis Company, Inc. ("Bemis"), par value $0.10 per share (the "Bemis Shares"), estimated to be outstanding immediately prior to the merger described in the proxy statement/prospectus contained herein and an additional [ · ] Bemis Shares underlying outstanding stock-settled restricted stock units of Bemis, multiplied by 5.1, which is the exchange ratio for the holders of Bemis Shares under the Transaction Agreement, dated as of August 6, 2018, among New Amcor, Amcor Limited ("Amcor"), Arctic Corp., a wholly-owned Subsidiary of the registrant, and Bemis (the "Transaction Agreement").

- (2)

- Estimated solely for the purpose of calculating the registration fee required by Section 6(b) of the Securities Act and computed pursuant to Rules 457(c) and 457(f)(1) promulgated under the Securities Act. The proposed maximum aggregate offering price of the New Amcor Shares to be registered was calculated based on the product of (i) [ · ], representing the maximum number of New Amcor Shares to be issued to holders of Bemis Shares in connection with the transactions described herein and (ii) the average of the high and low sale prices of Bemis Shares as reported on the New York Stock Exchange on [ · ], 2018 ($[ · ]).

- (3)

- Determined in accordance with Section 6(b) of the Securities Act at a rate equal to $121.20 per $1,000,000 of the proposed maximum aggregate offering price.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the Securities and Exchange Commission ("SEC"), acting pursuant to said Section 8(a), may determine.

AMCO-001

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

The information in this proxy statement/prospectus is not complete and may be changed. Amcor plc may not distribute the securities offered by this proxy statement/prospectus until the registration statement filed with the Securities and Exchange Commission ("SEC") is effective. This proxy statement/prospectus is not an offer to sell these securities and Amcor plc is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY—SUBJECT TO COMPLETION, DATED , 2018

MERGER PROPOSED—YOUR VOTE IS VERY IMPORTANT

To our Shareholders:

You are cordially invited to attend a special meeting of shareholders of Bemis Company, Inc. ("Bemis") at the Bemis Innovation Center, 2301 Industrial Drive, Neenah, Wisconsin 54956, at [ · ] Central time on [ · ], 2019. Whether or not you plan to attend, please vote your shares as promptly as possible.

As you may be aware, on August 6, 2018, Bemis entered into a Transaction Agreement with Amcor Limited ("Amcor") providing for a combination of Amcor and Bemis (the "Transaction Agreement"). Together, Bemis and Amcor expect to create the global leader in consumer packaging with the footprint, scale, talent and capabilities to better serve customers around the world. Bemis and Amcor are a good fit, not just geographically, but also culturally as we share a similar customer-first philosophy, as well as strong commitments to integrity, safety and developing our people. We believe combining these two organizations will drive significant value for our respective shareholders, employees and customers over the long-term.

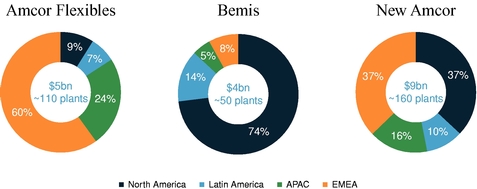

Bemis has a rich 160-year history and has evolved to its position today as a $4 billion plastic packager with a strong presence in the Americas. Our innovative products serve leading and emerging customers in food, consumer products, healthcare, and other industries. Our commitment to the growth and success of our customers is supported by our 16,000 employees across 56 plants in 12 countries. Over the past year and a half, Bemis has driven much positive change. We launched Agility—our plan to Fix, Strengthen, and Grow our business. For Bemis, this transaction is the next exciting chapter in our evolution, and our employees will carry forward the Bemis legacy as they showcase their talents, knowledge and passion for inspired packaging solutions as part of the global leader in consumer packaging that is being created through this transaction.

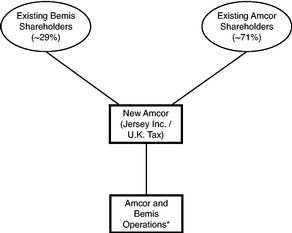

We believe this is a compelling transaction for Bemis shareholders, who will become owners of approximately 29% of the combined "New Amcor":

- •

- Significant Dividend Increase—New Amcor expects to maintain Amcor's competitive, progressive dividend, which is equivalent to $2.295 per Bemis share for calendar year 2018 (taking into account the 5.1 exchange ratio), a significant increase to Bemis' dividend of $1.24 per Bemis share for calendar year 2018. See "The Transaction—Amcor's Reasons for the Transaction —Financial Considerations—Dividend Policy and Capital Allocation."

- •

- Tax-free—The all-stock nature of this transaction is intended to allow the transaction to be tax-free to Bemis shareholders for U.S. federal income tax purposes. See "The Transaction —Material U.S., U.K. and Jersey Income Tax Considerations."

- •

- Synergy Benefits—Bemis shareholders will have the opportunity to benefit from value creation driven by the $180 million of estimated pre-tax annual net cost synergies by the end of the third year following closing of the transaction as well as additional potential revenue synergies. See "The Transaction—Recommendation of Bemis' Board of Directors; Bemis' Reasons for the Transaction."

AMCO-002

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

Bemis' board of directors unanimously approved the merger and is calling the upcoming special meeting at which Bemis shareholders can vote upon a proposal to approve the Transaction Agreement. Bemis' board of directors unanimously recommends that you vote "FOR" each of the proposals to be considered at the Bemis special meeting, including approval of the Transaction Agreement. The enclosed Notice of Special Meeting includes further details about the Bemis Special Meeting.

You are welcome to attend the Bemis special meeting in person on [ · ], 2019, but regardless of whether you plan to attend, please vote your shares via the instructions on page [ · ] of the enclosed proxy statement/prospectus and on the enclosed proxy or voting instruction card. Your vote is very important because the transaction cannot be completed unless holders of at least two-thirds of all of the outstanding Bemis Shares vote in favor of the proposal to approve the Transaction Agreement. A failure to vote your shares on the proposal to approve the Transaction Agreement will have the same effect as a vote against the proposal.

The enclosed proxy statement/prospectus provides you with detailed information about the Bemis special meeting, the Transaction Agreement and the transaction. A copy of the Transaction Agreement is attached as Annex A. I encourage you to read the proxy statement/prospectus, including its annexes and the documents incorporated by reference, carefully and in its entirety.

If you have any questions or need assistance in voting your shares, please contact Bemis' proxy solicitor, Innisfree M&A Incorporated, by calling toll-free at +1 888 750 5834.

Thank you for your continued support.

Sincerely,

William F. Austen

President and Chief Executive Officer

Neither the SEC nor any state securities commission has approved or disapproved of the transactions described herein, the issuance of New Amcor Shares in connection with the transactions described herein or determined that this proxy statement/prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

The date of this proxy statement/prospectus is [ · ] and it is first being sent to Bemis shareholders on or about [ · ].

AMCO-003

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

BEMIS COMPANY, INC.

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO THE SHAREHOLDERS OF BEMIS COMPANY, INC.:

You are cordially invited to attend a special meeting of shareholders (the "Bemis Special Meeting"), to be held at the Bemis Innovation Center, 2301 Industrial Drive, Neenah, Wisconsin 54956, at [ · ] Central time on [ · ], 2019. The purpose of the Bemis Special Meeting is to consider and vote upon the following proposals:

- 1.

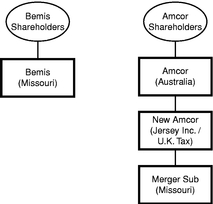

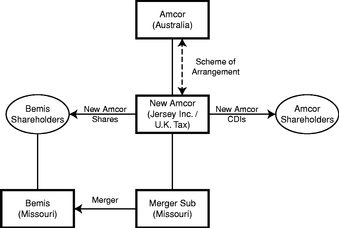

- Bemis Transaction Agreement Proposal. To approve the Transaction Agreement, dated as of August 6, 2018 (which, as it may be amended from time to time, we refer to as the "Transaction Agreement"), by and among Amcor Limited, Amcor plc (f/k/a Arctic Jersey Limited) ("New Amcor"), Arctic Corp. ("Merger Sub") and Bemis Company, Inc. ("Bemis"), pursuant to which, among other transactions, Merger Sub will merge with and into Bemis (the "merger"), with Bemis surviving the merger as a wholly-owned subsidiary of New Amcor, pursuant to which each share of common stock of Bemis, par value $0.10 per share (the "Bemis Shares"), other than certain excluded shares, will be converted into the right to receive 5.1 ordinary shares, par value $0.01, of New Amcor.

- 2.

- Bemis Compensation Proposal. To approve, in a non-binding advisory vote, certain compensation that may be paid or become payable to Bemis' named executive officers in connection with the transaction.

- 3.

- Bemis Amendments Proposals. To approve, in non-binding advisory votes, certain provisions of the New Amcor articles of association.

- 4.

- Bemis Adjournment Proposal. To approve one or more adjournments of the Bemis Special Meeting to a later date or dates for any purpose, including if necessary or appropriate to solicit additional proxies if there are insufficient votes to approve the Transaction Agreement at the time of the Bemis Special Meeting.

Accompanying this Notice of Special Meeting of Shareholders is a proxy statement/prospectus, which describes these proposals in more detail, and a form of proxy, which allows you to vote on these proposals. Please carefully review these materials, including the annexes to and information incorporated by reference into the proxy statement/prospectus.

We welcome you to attend the Bemis Special Meeting, but whether or not you plan to attend, please submit your completed proxy via phone, mail or internet as soon as possible. Proxies are revocable and will not affect your right to vote in person in the event that you revoke the proxy and attend the meeting. Instructions on how to vote are found in the sections titled "Information About the Bemis Special Meeting—Voting of Proxies; Incomplete Proxies" and "—Shares Held in Street Name and Broker Non-Votes" beginning on page [ · ] of the proxy statement/prospectus. Bemis' board of directors unanimously recommends that Bemis shareholders vote "FOR" each of these proposals.

AMCO-004

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

Only Bemis shareholders of record as shown on our books at the close of business on [ · ], [ · ] will be entitled to vote at the Bemis Special Meeting. Each Bemis shareholder is entitled to one vote per Bemis Share held by such Bemis shareholder on all matters to be voted on at the meeting.

| | | | |

| | | | | BY ORDER OF THE BOARD OF DIRECTORS, |

Dated: |

|

[·], [·]

Neenah, Wisconsin |

|

Sheri H. Edison

Senior Vice President, Chief Legal Officer and Secretary |

AMCO-005

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

ABOUT THIS PROXY STATEMENT/PROSPECTUS

This proxy statement/prospectus, which forms part of a registration statement on Form S-4 filed with the SEC by New Amcor, constitutes a prospectus of New Amcor under Section 5 of the Securities Act of 1933, as amended (the "Securities Act"), with respect to the New Amcor Shares to be issued to Bemis shareholders pursuant to the Transaction Agreement.

This document also constitutes a proxy statement of Bemis under Section 14(a) of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). It also constitutes a notice of meeting with respect to the Bemis Special Meeting, at which Bemis shareholders will be asked to consider and vote upon the Bemis Transaction Agreement Proposal, the Bemis Compensation Proposal, the Bemis Amendments Proposals and the Bemis Adjournment Proposal, each as described in more detail herein under "Information About the Bemis Special Meeting."

Amcor has supplied all information contained in this proxy statement/prospectus relating to Amcor and New Amcor, and Bemis has supplied all information contained in or incorporated by reference into this proxy statement/prospectus relating to Bemis.

You should rely only on the information contained in or incorporated by reference into this proxy statement/prospectus. New Amcor, Amcor and Bemis have not authorized anyone to provide you with information that is different from that contained in or incorporated by reference into this proxy statement/prospectus. This proxy statement/prospectus is dated [ · ], and you should not assume that the information contained in this proxy statement/prospectus is accurate as of any date other than such date. Further, you should not assume that the information incorporated by reference into this proxy statement/prospectus is accurate as of any date other than the date of the incorporated document. Neither the mailing of this proxy statement/prospectus to Bemis shareholders nor the issuance by New Amcor of New Amcor Shares pursuant to the Transaction Agreement will create any implication to the contrary.

A copy of this document has been delivered to the Jersey Registrar of Companies (the "Registrar") in accordance with Article 5 of the Companies (General Provisions) (Jersey) Order 2002, and the Registrar has given, and has not withdrawn, consent to its circulation. The Jersey Financial Services Commission ("JFSC") has given, and has not withdrawn, its consent under Article 2 of the Control of Borrowing (Jersey) Order 1958 to the issue of New Amcor Shares. The JFSC is protected by the Control of Borrowing (Jersey) Law 1947 against liability arising from the discharge of its functions under that law. It must be distinctly understood that, in giving these consents, neither the Registrar nor the JFSC takes any responsibility for the financial soundness of New Amcor or for the correctness of any statements made, or opinions expressed, with regard to it. If you are in any doubt about the contents of this document you should consult your stockbroker, bank manager, solicitor, accountant or other financial adviser. The current directors of New Amcor have taken all reasonable care to ensure that the facts stated in this document are true and accurate in all material respects, and that there are no other facts the omission of which would make misleading any statement in the document, whether of facts or of opinion. All such directors accept responsibility accordingly. It should be remembered that the price of securities and the income from them can go down as well as up.

Nothing in this document or anything communicated to holders or potential holders of the shares or CDIs in New Amcor is intended to constitute or should be construed as advice on the merits of, the purchase of or subscription for, the shares or CDIs in New Amcor or the exercise of any rights attached to them for the purposes of the Financial Services (Jersey) Law 1998.

AMCO-006

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

ADDITIONAL INFORMATION

This proxy statement/prospectus incorporates important business and financial information about Bemis from other documents that Bemis has filed with the SEC, and that are contained in or incorporated by reference into this proxy statement/prospectus. For a listing of documents incorporated by reference into this proxy statement/prospectus, please see the section entitled "Where You Can Find More Information" beginning on page [ · ] of this proxy statement/prospectus. This information is available for you to review at the SEC's public reference room located at 100 F Street, N.E., Room 1580, Washington, DC 20549, and through the SEC's website at www.sec.gov.

Any person may request copies of this proxy statement/prospectus and any of the documents incorporated by reference into this proxy statement/prospectus or other information concerning Bemis, without charge, by written or telephonic request directed to Bemis, 2301 Industrial Drive, Neenah, Wisconsin 54956, Telephone: +1 920 527 5000; or Innisfree M&A Incorporated, Bemis' proxy solicitor, by calling toll-free at +1 888 750 5834. Banks, brokerage firms and other nominees may call collect at +1 212 750 5833.

In order for you to receive timely delivery of the documents in advance of the Bemis Special Meeting to be held on [ · ], 2019 you must request the information no later than five business days prior to the date of the Bemis Special Meeting (i.e., by [ · ], 2019).

AMCO-007

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

CURRENCY EXCHANGE RATE DATA

References herein to "$" or "USD" are to U.S. dollars and references to "A$" or "AUD" are to Australian dollars.

The exchange rate for Australian dollars on [ · ], [ · ], the latest practicable date prior to the date of this proxy statement/prospectus, was $[ · ] per Australian dollar, as reported by Bloomberg.

The following table shows, for the periods indicated, the high, low, average and period end "Bloomberg Generic Composite Rate" expressed in AUD per USD. The Bloomberg Generic Composite Rate is a composite rate based on indicative rates contributed by market participants and compiled by Bloomberg.

| | | | | | | | | | | | | |

Month ended | | Period End | | Average(1) | | Low | | High | |

|---|

September 2018 | | | 1.38 | | | 1.38 | | | 1.37 | | | 1.41 | |

August 2018 | | | 1.39 | | | 1.37 | | | 1.34 | | | 1.39 | |

July 2018 | | | 1.35 | | | 1.35 | | | 1.34 | | | 1.37 | |

June 2018 | | | 1.35 | | | 1.34 | | | 1.30 | | | 1.36 | |

May 2018 | | | 1.32 | | | 1.33 | | | 1.31 | | | 1.35 | |

April 2018 | | | 1.33 | | | 1.30 | | | 1.28 | | | 1.33 | |

March 2018 | | | 1.30 | | | 1.29 | | | 1.26 | | | 1.31 | |

February 2018 | | | 1.29 | | | 1.27 | | | 1.24 | | | 1.29 | |

January 2018 | | | 1.24 | | | 1.26 | | | 1.23 | | | 1.28 | |

- (1)

- The average rate for a month is the arithmetic average of the Bloomberg Generic Composite Rates observed daily during the business days of that month.

| | | | | | | | | | | | | |

Year ended December 31, | | Period End | | Average(1) | | Low | | High | |

|---|

2017 | | | 1.28 | | | 1.30 | | | 1.23 | | | 1.40 | |

2016 | | | 1.39 | | | 1.35 | | | 1.28 | | | 1.46 | |

2015 | | | 1.37 | | | 1.33 | | | 1.21 | | | 1.45 | |

2014 | | | 1.22 | | | 1.11 | | | 1.05 | | | 1.24 | |

2013 | | | 1.12 | | | 1.04 | | | 0.94 | | | 1.13 | |

- (1)

- The average rate for a year is the arithmetic average of the Bloomberg Generic Composite Rates observed daily during the business days of that year.

AMCO-008

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

FREQUENTLY USED TERMS

Unless otherwise indicated or as the context otherwise requires, a reference in this proxy statement/prospectus to:

- •

- "Amcor" refers to Amcor Limited, an Australian public company limited by shares;

- •

- "Amcor Board" refers to the board of directors of Amcor;

- •

- "Amcor Shareholder Approval" refers to the approval of the scheme at the scheme meeting (or any adjournment of such meeting) by the Amcor Shareholders in accordance with the Australian Act by (1) a majority in number of Amcor shareholders that are present and voting at the scheme meeting (either in person or by proxy) and (2) 75% of the votes cast on the resolution, or, in each case, such other threshold as approved by the Court;

- •

- "Amcor Shares" refers to the ordinary shares of Amcor, no par value per share;

- •

- "AMVIG" refers to AMVIG Holdings Limited;

- •

- "Antitrust Division" refers to the Antitrust Division of the U.S. Department of Justice;

- •

- "Applicable Share Price" refers to the weighted average price of New Amcor Shares on the three trading days before settlement of any Bemis Equity Award;

- •

- "ASIC" refers to the Australian Securities and Investments Commission;

- •

- "ASX" refers to the ASX Limited;

- •

- "Australian Act" refers to the Australian Corporations Act 2001 (Cth);

- •

- "Bemis" refers to Bemis Company, Inc., a Missouri corporation;

- •

- "Bemis Cash-Settled RSUs" refers to the cash-settled restricted stock unit of Bemis;

- •

- "Bemis Equity Award" refers to any Bemis Cash-Settled RSU, Bemis PSU or Bemis RSU;

- •

- "Bemis Incentive Plan" refers to the Bemis Company, Inc. 2014 Stock Incentive Plan;

- •

- "Bemis Proposals" refers to, collectively, the Bemis Transaction Agreement Proposal, the Bemis Compensation Proposal, the Bemis Amendments Proposals and the Bemis Adjournment Proposal;

- •

- "Bemis PSUs" refers to the stock-settled performance stock units of Bemis;

- •

- "Bemis RSUs" refers to the stock-settled restricted stock units of Bemis that is not a Bemis PSU;

- •

- "Bemis Shareholder Approval" refers to the affirmative vote of at least two-thirds of the outstanding Bemis Shares entitled to vote on the approval of the Transaction Agreement at the Bemis Special Meeting in favor of adopting such proposal;

- •

- "Bemis Shares" refers to shares of common stock of Bemis, par value $0.10 per share;

- •

- "Bemis Special Meeting" refers to the special meeting of Bemis shareholders described in this proxy statement/prospectus;

- •

- "CDIs" refers to CHESS Depositary Interests, each representing a beneficial interest in one New Amcor Share, that are quoted and traded on the financial market operated by ASX;

- •

- "Cleary Gottlieb" refers to Cleary Gottlieb Steen & Hamilton LLP;

- •

- "closing" refers to the closing of the transaction;

- •

- "Code" refers to the Internal Revenue Code of 1986, as amended;

AMCO-009

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

- •

- "Court" refers to the Federal Court of Australia, or such other court of competent jurisdiction under the Corporations Act as may be agreed in writing by Amcor and Bemis;

- •

- "deed poll" refers to a deed poll under which New Amcor covenants in favor of the Amcor shareholders to perform the obligations attributed to New Amcor under the scheme;

- •

- "Developed Markets" refers to Amcor's businesses in Western Europe, North America and Australia and New Zealand;

- •

- "Dodd Frank Act" means the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010;

- •

- "effective time" refers to the effective time of the merger;

- •

- "Emerging Markets" refers to Amcor's businesses in Asia, Latin America, Eastern Europe (excluding certain operations in Poland) and Africa;

- •

- "end date" refers to August 6, 2019 (subject to extension by either party until February 6, 2020 in order to obtain antitrust or other regulatory approvals);

- •

- "ERISA" refers to the U.S. Employee Retirement Income Security Act of 1974, as amended;

- •

- "Exchange Act" refers to the Securities Exchange Act of 1934, as amended;

- •

- "FATA" refers to the Foreign Acquisitions and Takeovers Act 1975 (Cth);

- •

- "FIRB" refers to the Australian Foreign Investment and Review Board;

- •

- "First Court Hearing" refers to the hearing of the Court pursuant to Section 411(4)(a) of the Australian Act to consider and, if thought fit, approve the mailing of the Scheme Booklet (with or without amendment) and convene the scheme meeting;

- •

- "fiscal year 2016" refers, when used with respect to Amcor or New Amcor, to Amcor's fiscal year ended June 30, 2016 and, when used with respect to Bemis, to Bemis' fiscal year ended December 31, 2016;

- •

- "fiscal year 2017" refers, when used with respect to Amcor or New Amcor, to Amcor's fiscal year ended June 30, 2017 and, when used with respect to Bemis, to Bemis' fiscal year ended December 31, 2017;

- •

- "fiscal year 2018" refers, when used with respect to Amcor or New Amcor, to Amcor's fiscal year ended June 30, 2018 and, when used with respect to Bemis, to Bemis' fiscal year ending December 31, 2018;

- •

- "FTC" refers to the U.S. Federal Trade Commission;

- •

- "GAAP" or "U.S. GAAP" refers to accounting principles generally accepted in the United States of America;

- •

- "HSR Act" refers to the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended, and the rules and regulations promulgated thereunder;

- •

- "IFRS" refers to the International Financial Reporting Standards as issued by the International Accounting Standards Board;

- •

- "Intended Tax Treatment" refers to the condition that (i) the merger of Merger Sub into Bemis qualifies as a "reorganization" under Section 368(a) of the Code, (ii) the merger of Merger Sub into Bemis and the scheme, taken together, qualifies as an exchange described in Section 351(a) of the Code and (iii) the merger of Merger Sub into Bemis does not result in gain being recognized under Section 367(a)(1) of the Code (other than for any shareholder that would be a "five-percent transferee shareholder" (within the meaning of Treasury Regulations

AMCO-010

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

AMCO-011

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

- •

- "Transaction Agreement" refers to the Transaction Agreement, dated as of August 6, 2018, among New Amcor, Amcor, Merger Sub and Bemis;

- •

- "U.K." refers to the United Kingdom of Great Britain and Northern Ireland; and

- •

- "U.S." refers to the United States of America.

AMCO-012

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

TABLE OF CONTENTS

| | |

QUESTIONS AND ANSWERS ABOUT THE TRANSACTION AND THE BEMIS SPECIAL MEETING | | 1 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS | | 14 |

SUMMARY | | 16 |

RISK FACTORS | | 35 |

THE PARTIES TO THE TRANSACTION | | 65 |

INFORMATION ABOUT THE BEMIS SPECIAL MEETING | | 67 |

THE TRANSACTION | | 75 |

THE TRANSACTION AGREEMENT | | 135 |

SELECTED HISTORICAL CONSOLIDATED FINANCIAL DATA OF AMCOR | | 164 |

SELECTED HISTORICAL CONSOLIDATED FINANCIAL DATA OF BEMIS | | 165 |

UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION | | 168 |

COMPARATIVE HISTORICAL AND UNAUDITED PRO FORMA PER SHARE INFORMATION | | 182 |

MARKET PRICES OF AMCOR SHARES AND BEMIS SHARES AND DIVIDEND INFORMATION | | 183 |

BUSINESS OVERVIEW OF AMCOR | | 185 |

BUSINESS OVERVIEW OF NEW AMCOR | | 194 |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF THE FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF AMCOR | | 198 |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL HOLDERS, DIRECTORS AND MANAGEMENT OF BEMIS | | 223 |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL HOLDERS, DIRECTORS AND MANAGEMENT OF AMCOR | | 225 |

DESCRIPTION OF NEW AMCOR SHARES AND THE NEW AMCOR ARTICLES OF ASSOCIATION | | 226 |

COMPARISON OF THE RIGHTS OF HOLDERS OF BEMIS SHARES AND NEW AMCOR SHARES | | 234 |

MANAGEMENT AND CORPORATE GOVERNANCE OF NEW AMCOR | | 258 |

EXECUTIVE COMPENSATION | | 265 |

LEGAL MATTERS | | 277 |

EXPERTS | | 278 |

HOUSEHOLDING OF PROXY MATERIALS | | 279 |

WHERE YOU CAN FIND MORE INFORMATION | | 280 |

INDEX TO FINANCIAL STATEMENTS OF AMCOR LIMITED | | F-1 |

Annex A | | A-1 |

Annex B | | B-1 |

Annex C | | C-1 |

Annex D | | D-1 |

Annex E | | E-1 |

AMCO-013

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

QUESTIONS AND ANSWERS ABOUT THE TRANSACTION AND THE BEMIS SPECIAL MEETING

The following questions and answers are intended to briefly address some commonly asked questions regarding the transaction, the Transaction Agreement and the Bemis Special Meeting. These questions and answers may not address all questions that may be important to you as a Bemis shareholder. Please refer to the section entitled "Summary" beginning on page [ · ] of this proxy statement/prospectus and the more detailed information contained elsewhere in this proxy statement/prospectus, the annexes to and the information incorporated by reference into this proxy statement/prospectus, which you should read carefully and in their entirety. You may obtain the information incorporated by reference into this proxy statement/prospectus without charge by following the instructions under the section entitled "Where You Can Find More Information" beginning on page [ · ] of this proxy statement/prospectus.

Q: Why am I receiving this proxy statement/prospectus and proxy card?

Bemis has agreed to combine with Amcor under the terms of the Transaction Agreement that are described in this proxy statement/prospectus. The Transaction Agreement provides that, if the transaction is approved by Bemis' shareholders and the other conditions to closing the transaction are satisfied or waived at or prior to the closing of the transaction, each of Bemis and Amcor will become wholly-owned subsidiaries of New Amcor and each Bemis Share will be converted into the right to receive 5.1 New Amcor shares (which are expected to be listed and traded on the NYSE under the symbol "[ · ]"). Bemis is holding a special meeting of its shareholders (the "Bemis Special Meeting") to ask its shareholders to consider and vote upon a proposal to approve the Transaction Agreement (the "Bemis Transaction Agreement Proposal").

In addition to the Bemis Transaction Agreement Proposal, Bemis shareholders are also being asked (i) to consider and vote upon a proposal to approve, by non-binding, advisory vote, the compensation that may become payable to Bemis' named executive officers in connection with the transaction (the "Bemis Compensation Proposal"), (ii) to consider and vote upon proposals to approve, by non-binding advisory votes, certain provisions of the New Amcor articles of association (the "Bemis Amendments Proposals") and (iii) to approve one or more adjournments of the Bemis Special Meeting, if necessary or appropriate, including adjournments to permit further solicitation of proxies in favor of the proposal to approve the Transaction Agreement (the "Bemis Adjournment Proposal").

This proxy statement/prospectus includes important information about the transaction, the Transaction Agreement, a copy of which is attached as Annex A to this proxy statement/prospectus, and the Bemis Special Meeting. Bemis shareholders should read this information carefully and in its entirety. The enclosed voting materials allow shareholders to vote their Bemis Shares without attending the Bemis Special Meeting in person.

Q: How does Bemis' board of directors recommend that I vote at the Bemis Special Meeting?

- A:

- Bemis' board of directors unanimously recommends that Bemis shareholders vote "FOR" the Bemis Transaction Agreement Proposal, "FOR" the Bemis Compensation Proposal, "FOR" the Bemis Amendments Proposals and "FOR" the Bemis Adjournment Proposal. See the section entitled "The Transaction—Recommendation of Bemis' Board of Directors; Bemis' Reasons for the Transaction" beginning on page [ · ] of this proxy statement/prospectus.

Q: What is the vote required to approve each proposal at the Bemis Special Meeting?

- A:

- The approval of the Bemis Transaction Agreement Proposal requires the affirmative vote of the holders of at least two-thirds of the outstanding Bemis Shares entitled to vote at the Bemis Special Meeting. Because the affirmative vote required to approve the Bemis Transaction Agreement Proposal is based upon the total number of outstanding Bemis Shares, if you fail to submit a proxy

1

AMCO-014

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

or vote in person at the Bemis Special Meeting, you abstain or you do not provide your bank, brokerage firm or other nominee with instructions, as applicable, this will have the same effect as a vote "AGAINST" the Bemis Transaction Agreement Proposal.

The approval of the Bemis Compensation Proposal requires that the votes cast "FOR" the Bemis Compensation Proposal are of a number greater than the votes cast "AGAINST" the Bemis Compensation Proposal.

The approval of each of the Bemis Amendments Proposals require that the votes cast "FOR" such Bemis Amendments Proposal are of a number greater than the votes cast "AGAINST" the Bemis Amendments Proposals.

Approval of the Bemis Adjournment Proposal requires the affirmative vote of the holders of a majority of the voting power of the shares present or represented and entitled to vote on that item of business, whether or not a quorum is present.

For purposes of the Bemis Special Meeting, an abstention as to a particular matter occurs when either (a) a Bemis shareholder affirmatively votes to "ABSTAIN" as to that matter or (b) a Bemis shareholder attends the Bemis Special Meeting and does not vote as to such matter. For purposes of the Bemis Special Meeting, a failure to be represented as to particular Bemis Shares and a particular matter occurs when either (a) the holder of record of such Bemis Shares neither attends the meeting nor returns a proxy with respect to such Bemis Shares or (b) such Bemis Shares are held in "street name" and the beneficial owner does not instruct the owner's bank, broker or other nominee on how to vote such Bemis Shares with respect to such matter (i.e., a broker non-vote).

For the Bemis Transaction Agreement Proposal, an abstention or a failure to be represented will have the same effect as a vote cast "AGAINST" the proposal.

For the Bemis Compensation Proposal, an abstention will not have any effect on such proposal. If a Bemis shareholder fails to vote or instruct his or her bank, broker or other nominee on how to vote and is not present in person or by proxy at the Bemis Special Meeting, it will also have no effect on the vote count for the Bemis Compensation Proposal.

For each of the Bemis Amendments Proposals, an abstention will not have any effect on such proposal. If a Bemis shareholder fails to vote or instruct his or her bank, broker or other nominee on how to vote and is not present in person or by proxy at the Bemis Special Meeting, it will also have no effect on the vote count for the Bemis Amendments Proposals.

For the Bemis Adjournment Proposal, an abstention will have the same effect as a vote cast "AGAINST" the proposal, but a failure to be represented will not have any effect on this proposal.

Q: Does my vote matter?

- A:

- Yes. The transaction cannot be completed unless the Bemis Transaction Agreement Proposal is approved by the Bemis shareholders. For Bemis shareholders, if you fail to submit a proxy or vote in person at the Bemis Special Meeting, or vote to abstain, or you do not provide your bank, brokerage firm or other nominee with instructions, as applicable, this will have the same effect as a vote "AGAINST" the Bemis Transaction Agreement Proposal.

See the section entitled "Information About the Bemis Special Meeting" beginning on page [ · ] of this proxy statement/prospectus.

Q: What will I receive if the transaction is completed?

- A:

- If the transaction is completed, each outstanding Bemis Share (other than Bemis Shares held as treasury stock by Bemis or any of its subsidiaries and dissenting shares) will be converted into the

2

AMCO-015

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

right to receive 5.1 New Amcor Shares. The issuance of the New Amcor Shares to holders of Bemis Shares will be registered with the SEC and the New Amcor Shares are expected to be listed and traded on the NYSE under the symbol "[ · ]." See the section entitled "The Transaction Agreement—Transaction Consideration" beginning on page [ · ] of this proxy statement/prospectus.

Q: What equity stakes will former Bemis shareholders and former Amcor shareholders hold in New Amcor?

- A:

- Under the Transaction Agreement and pursuant to the exchange ratio, based on Amcor's and Bemis' respective fully diluted shares as of the date of the Transaction Agreement, it is expected that Amcor shareholders and Bemis shareholders will own approximately 71% and 29%, respectively, of the New Amcor Shares immediately following the effective time.

Q: How do I calculate the value of the transaction consideration?

- A:

- The value of the transaction consideration that Bemis shareholders receive will depend on the per share value of New Amcor Shares at the effective time. Prior to the effective time, there has not been and will not be an established public trading market for New Amcor Shares, and the market price of New Amcor Shares will be unknown until the commencement of trading following the effective time. The New Amcor Shares will reflect the combination of Amcor and Bemis based upon the respective exchange ratios for Amcor Shares and Bemis Shares, which in the case of Amcor is one New Amcor Share for each Amcor Share, and in the case of Bemis is 5.1 New Amcor Shares for each Bemis Share. The exchange ratios are fixed and will not fluctuate up or down based on the market price of Bemis Shares, the market price of Amcor Shares or changes in currency exchange rates prior to the completion of the transaction.

The implied value of the transaction consideration that Bemis shareholders will receive may be calculated, as of a specified date, as (i) the implied price of a New Amcor Share (ii) multiplied by the exchange ratio of 5.1 New Amcor Shares for each Bemis Share. The implied price of a New Amcor Share may be calculated, as of a specified date, as (A) Amcor's most recent closing share price as of such date, (B) multiplied by the current AUD:USD exchange rate on such date, (C) multiplied by the exchange ratio of one New Amcor Share for each Amcor Share. As the market price of Bemis Shares, the market price of Amcor Shares or currency exchange rates fluctuate, the implied value of New Amcor Shares will fluctuate too. As a result, the implied value of the transaction consideration that you will receive upon the completion of the transaction could be greater than, less than or the same as the implied value of the transaction consideration on the date of this proxy statement/prospectus or at the time of the Bemis Special Meeting. We urge you to obtain current market quotations and currency exchange rates before voting your Bemis Shares.

Q: After the transaction, where can I trade my New Amcor Shares?

- A:

- At and as of the closing of the transaction, it is expected that the New Amcor Shares will be listed and traded on the NYSE under the symbol "[ · ]."

Amcor Shares will not be traded on the ASX following the closing of the transaction, but interests in New Amcor Shares will be quoted and traded on the financial market operated by ASX in the form of CDIs under the ASX ticker symbol [ · ].

Q: What will holders of Bemis stock-based awards receive in the transaction?

- A:

- The Transaction Agreement generally provides for the cancellation of Bemis RSUs (which will automatically vest, to the extent previously unvested, at the effective time) and Bemis PSUs (which will automatically vest, to the extent previously unvested, at target levels at the effective time) in

3

AMCO-016

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

exchange for (i) a number of New Amcor Shares determined by multiplying the number of Bemis Shares subject to such vested Bemis RSUs and vested Bemis PSUs immediately prior to the effective time by the exchange ratio set forth in the Transaction Agreement, and (ii) any fractional consideration, in cash, payable to the holder of a cancelled Bemis RSU or Bemis PSU who would have been entitled to receive a fraction of a New Amcor Share upon conversion.

Each Bemis Cash-Settled RSU (which will automatically vest, to the extent previously unvested, at the effective time) will also be cancelled in exchange for an amount in cash equal to the product of (x) the number of Bemis Shares subject to the vested Bemis Cash-Settled RSU multiplied by (y) the exchange ratio set forth in the Transaction Agreement and (z) the Applicable Share Price. With respect to any Bemis RSU, Bemis PSU or Bemis Cash-Settled RSU that provides for the right to receive payments equivalent to the dividends paid on the underlying Bemis Shares, each holder of such rights will also receive an amount in cash equal to the aggregate amount of the dividends so payable. For additional information on the treatment of Bemis Equity Awards, see the section entitled "The Transaction—Treatment of Bemis Equity Awards" beginning on page [ · ] of this proxy statement/prospectus.

Q: Do any of the Bemis directors or officers have interests in the transaction that may differ from or be in addition to my interests as a Bemis shareholder?

- A:

- Bemis' directors and officers have certain interests in the transaction that may be different from, or in addition to, the interests of Bemis shareholders generally. See the section entitled "The Transaction—Interests of Bemis' Directors and Executive Officers in the Transaction" beginning on page [ · ] of this proxy statement/prospectus.

Q: How will I receive the transaction consideration to which I am entitled?

- A:

- After receiving the proper documentation from you, following the effective time, the exchange agent for the transaction will cause New Amcor Shares to be credited in book-entry form to the direct registered account maintained by New Amcor's transfer agent for the benefit of the respective holders (or, in the case of shares tendered through DTC, to the account of DTC so that DTC can credit the relevant DTC participant and such DTC participant can credit its respective account holders). Promptly following the crediting of shares to your respective direct registered account, you will receive a statement from New Amcor's transfer agent evidencing your holdings, as well as general information on the book-entry form of ownership.

Q: Will my New Amcor Shares acquired in the transaction receive a dividend?

- A:

- Once you exchange your Bemis Shares after the closing of the transaction, as a holder of New Amcor Shares, you will receive the same dividends on New Amcor Shares that all other holders of New Amcor Shares will receive with any dividend record date that occurs after the transaction is completed. Amcor has a history of paying a competitive, progressive dividend that is higher than the annual dividend received by Bemis' shareholders currently and it is expected that New Amcor will continue this dividend policy. Any dividend payments, or changes to New Amcor's dividend policy, will be made at the discretion of the board of directors of New Amcor and will depend upon many factors, including the financial condition of New Amcor, earnings, legal requirements, applicable restrictions in each of Amcor's and Bemis' debt agreements that limit their respective abilities to pay dividends to shareholders and other factors the board of directors of New Amcor may deem relevant. See "The Transaction—Amcor's Reasons for the Transaction" and "—Recommendation of Bemis' Board of Directors; Bemis' Reasons for the Transaction" for a discussion of Amcor's and Bemis' expectations with respect to the payment of dividends by New Amcor post-closing.

4

AMCO-017

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

Q: Will dividends paid by New Amcor be subject to tax withholding?

- A:

- Under U.S. federal tax withholding rules, dividends paid to a U.S. holder of New Amcor Shares should not be subject to withholding unless the holder is subject to backup withholding or fails to provide an accurate taxpayer identification number and make any other required certification. New Amcor is not required to withhold U.K. or Jersey tax at source from dividend payments made on the New Amcor Shares, irrespective of the residence of the New Amcor shareholders or their particular circumstances. For a more complete description of the material U.S. federal income tax consequences of the transaction to U.S. holders of Bemis Shares, please see the section entitled "The Transaction—Material U.S., U.K. and Jersey Income Tax Considerations" beginning on page [ · ] of this proxy statement/prospectus.

Q: What are the material U.S. federal income tax consequences of the transaction to U.S. holders of Bemis Shares?

- A:

- The parties intend the merger to be treated as a tax-free reorganization under Section 368(a) of the Code and the merger and the scheme, taken together, to be treated as an exchange described under Section 351 of the Code. In addition, assuming that the fair market value of Amcor, at the time of the transaction, equals or exceeds the fair market value of Bemis, as specially determined for purposes of Section 367 of the Code, the transaction should not result in gain being recognized under Section 367(a)(1) of the Code, other than for any "five-percent transferee shareholder" (within the meaning of Treasury Regulations Section 1.367(a)-3(c)(5)(ii)) of New Amcor that does not file with the IRS a gain recognition agreement, as described in applicable U.S. Treasury Regulations. In general, a five-percent transferee shareholder is a person who will own directly, indirectly or constructively through attribution rules, at least five percent of either the total voting power or total value of New Amcor immediately after the transaction.

As a condition to the scheme, Bemis will request that Cleary Gottlieb, or other nationally recognized tax counsel or a "Big 4" accounting firm, render its opinion or written advice to Bemis, which will be dated the Sanction Date and based on customary representations and assumptions, that there has been no Tax Law Change, the effect of which is to cause the merger and scheme to fail to qualify, at a "should" or higher level of comfort, for the Intended Tax Treatment.

Assuming that the transaction so qualifies, a U.S. holder of Bemis Shares that exchanges all of its Bemis Shares for New Amcor Shares in the transaction, and is not a "five-percent transferee shareholder" that does not file with the IRS a gain recognition agreement as described above, should not recognize any gain or loss with respect to its Bemis Shares, except to the extent of any cash such U.S. holder may receive in lieu of a fractional share.

For a more complete description of the material U.S. federal income tax consequences of the transaction to U.S. holders of Bemis Shares, please see the section entitled "The Transaction—Material U.S., U.K. and Jersey Income Tax Considerations" beginning on page [ · ] of this proxy statement/prospectus.

Q: What are the material U.S. federal income tax consequences of the transaction to U.S. holders of Amcor Shares?

- A:

- As described in the answer above, the parties intend the merger and the scheme, taken together, to be treated as an exchange described under Section 351 of the Code. As a condition to the scheme, Amcor will request that a nationally recognized tax counsel or a "Big 4" accounting firm render its opinion or written advice to Amcor, which will be dated the Sanction Date and based on customary representations and assumptions, that there has been no Tax Law Change, the effect of which is to cause the merger and the scheme to fail to qualify, at a "should" or higher level of comfort, for the Intended Tax Treatment.

5

AMCO-018

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

Assuming that the transaction so qualifies, a U.S. holder of Amcor Shares that exchanges all of its Amcor Shares for New Amcor Shares in the scheme, owns less than five percent (actually or constructively under attribution rules) of both the total voting power and the total value of the stock of New Amcor immediately after the transaction and does not file with the IRS a gain recognition agreement as described above, should not recognize any gain or loss with respect to its Amcor Shares.

For a more complete description of the U.S. federal income tax consequences of the transaction to U.S. holders of Amcor Shares, please see the section entitled "The Transaction—Material U.S., U.K. and Jersey Income Tax Considerations" beginning on page [ · ] of this proxy statement/prospectus.

Q: When is the transaction expected to be completed?

- A:

- Subject to the satisfaction or waiver of the closing conditions described under the section entitled "The Transaction Agreement—Conditions That Must Be Satisfied or Waived for the Transaction to Occur" beginning on page [ · ] of this proxy statement/prospectus, including the approval of the Bemis Transaction Agreement Proposal by Bemis shareholders at the Bemis Special Meeting, Amcor and Bemis expect that the transaction will be completed in the first calendar quarter of 2019 subject to the satisfaction of closing conditions. However, it is possible that factors outside the control of both companies could result in the transaction being completed at a different time or not at all.

Q: Who will serve on New Amcor's board of directors following the transaction?

- A:

- Upon the closing of the transaction, the board of directors of New Amcor will be comprised of 11 members. The members of the board are expected to be:

- •

- eight current Amcor directors (each of whom will be designated by Amcor and will be Graeme Liebelt, Ronald S. Delia, Dr. Armin Meyer, Paul Brasher, Eva Cheng, Karen Guerra, Nicholas (Tom) Long, and Jeremy Sutcliffe); and

- •

- three current Bemis directors (each of whom will be designated by Bemis prior to the closing date, subject to Amcor's prior written approval). The three Bemis designees have not been selected as of the date of this proxy statement/prospectus.

For more information on the governance of New Amcor following the completion of the transaction, see "Management and Corporate Governance of New Amcor" beginning on page [ · ] of this proxy statement/prospectus.

Q: Where will New Amcor be located, where will New Amcor be domiciled and who will serve in senior leadership roles following the transaction?

- A:

- Following the transaction, New Amcor will continue to maintain a critical presence in the same locations from which Amcor currently operates as well as at Neenah, Wisconsin and other key Bemis locations. New Amcor will be incorporated in Jersey, Channel Islands, with an intended tax domicile in the United Kingdom. Amcor's current Chairman, Mr. Graeme Liebelt, and current CEO, Mr. Ronald Delia, will continue in those roles for New Amcor after the transaction and Mr. Delia will continue to serve as the only Executive Director on New Amcor's board of directors. For additional information on New Amcor's senior leadership team, see "Management and Corporate Governance of New Amcor" beginning on page [ · ] of this proxy statement/prospectus.

6

AMCO-019

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

Q: How will my rights as a holder of New Amcor Shares following the transaction differ from my current rights as a holder of Bemis Shares?

- A:

- Pursuant to the terms of the Transaction Agreement, immediately prior to the closing of the transaction, New Amcor's memorandum of association and articles of association will be amended to be in substantially the forms attached as Annex B and Annex C, respectively, of this proxy statement/prospectus. As a result, the rights of Bemis shareholders who become shareholders of New Amcor following the transaction will be governed by the laws of Jersey, Channel Islands, the New Amcor Memorandum of Association and the New Amcor Articles of Association. For more information, see the section entitled "Comparison of the Rights of Holders of Bemis Shares and New Amcor Shares" beginning on page [ · ] of this proxy statement/prospectus.

Q: Who can vote at the Bemis Special Meeting?

- A:

- All holders of record of Bemis Shares as of the close of business on [ · ], [ · ], the record date for the Bemis Special Meeting (the "Record Date"), are entitled to receive notice of, and to vote at, the Bemis Special Meeting. Each holder of Bemis Shares is entitled to cast one vote on each matter properly brought before the Bemis Special Meeting for each Bemis Share that such holder owned of record as of the Record Date.

Q: When and where is the Bemis Special Meeting?

- A:

- The Bemis Special Meeting will be held on [ · ], 2019 at [ · ] Central time, at the Bemis Innovation Center, 2301 Industrial Drive, Neenah, Wisconsin 54956. All Bemis shareholders of record as of the close of business on the Record Date, their duly authorized proxy holders, and beneficial owners with proof of ownership are invited to attend the Bemis Special Meeting in person. Due to space constraints and other security considerations, we are not able to admit the guests of either shareholders or their legal proxy holders. To gain admittance you will need to obtain an admission ticket and you will need to bring valid photo identification, such as a driver's license or passport, with you to the Bemis Special Meeting. If your Bemis Shares are held through a bank, brokerage firm or other nominee, please bring proof of your beneficial ownership of such shares and legal proxy if you intend to vote at the Bemis Special Meeting. Acceptable proof could include an account statement showing that you owned Bemis Shares on the Record Date. If you are the representative of a corporate or institutional shareholder, you must present valid photo identification along with proof that you are the representative of such shareholder. Please note that cameras, recording devices and other electronic devices will not be permitted at the Bemis Special Meeting. For additional information about the Bemis Special Meeting, see the section entitled "Information About the Bemis Special Meeting" beginning on page [ · ] of this proxy statement/prospectus.

Q: Why am I being asked to consider and vote on a proposal to approve, by non-binding, advisory vote, the compensation that may become payable to Bemis' named executive officers in connection with the transaction?

- A:

- Under SEC rules, Bemis is required to seek a non-binding, advisory vote with respect to the compensation that may become payable to its named executive officers in connection with the transaction.

7

AMCO-020

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

Q: Why am I being asked to consider and vote on a proposal to approve, by non-binding, advisory votes, certain provisions of the New Amcor articles of association?

- A:

- Under SEC rules, Bemis is required to seek a non-binding, advisory vote with respect to certain provisions of the New Amcor articles of association that represent a change from the corresponding provisions of Amcor's current governing documents.

Q: What will happen if Bemis shareholders do not approve the transaction-related compensation or the amendments to the New Amcor articles of association?

- A:

- Approval of the Bemis Compensation Proposal and the Bemis Amendments Proposals is not a condition to completion of the transaction. Accordingly, you may vote against any or all of these proposals and vote in favor of the Bemis Transaction Agreement Proposal. The Bemis Compensation Proposal and the Bemis Amendments Proposals votes are each an advisory vote and will not be binding on Bemis or New Amcor following the transaction. If the transaction is completed, the transaction-related compensation may be paid to Bemis' named executive officers to the extent payable in accordance with the terms of their compensation agreements and arrangements even if Bemis' shareholders do not approve, by non-binding advisory vote, the Bemis Compensation Proposal and the provisions of New Amcor's articles of association will apply in accordance with their terms even if Bemis' shareholders do not approve, by non-binding advisory votes, any or all of the Bemis Amendments Proposals.

Q: What is the difference between holding shares as a shareholder of record and as a beneficial owner?

- A:

- If your Bemis Shares are registered directly in your name with the transfer agent of Bemis, EQ Shareowner Services, you are considered the shareholder of record with respect to those Bemis Shares. As the shareholder of record, you have the right to vote, or to grant a proxy for your vote directly to Bemis or to a third party to vote, at the Bemis Special Meeting.

If your Bemis Shares are held by a bank, brokerage firm or other nominee, you are considered the beneficial owner of shares held in "street name," and your bank, brokerage firm or other nominee is considered the shareholder of record with respect to those shares. Your bank, brokerage firm or other nominee will send you, as the beneficial owner, a package describing the procedure for voting your shares. You should follow the instructions provided by them to vote your Bemis Shares. If you are a beneficial owner of Bemis Shares, you are invited to attend the Bemis Special Meeting; however, you may not vote your shares held in street name in person at the Bemis Special Meeting unless you obtain a "legal proxy" from your bank, brokerage firm or other nominee that holds your shares, giving you the right to vote your Bemis Shares at the Bemis Special Meeting.

Q: If my Bemis Shares are held in "street name" by my bank, brokerage firm or other nominee, will my bank, brokerage firm or other nominee automatically vote those shares for me?

- A:

- No. If your Bemis Shares are held in "street name" in a stock brokerage account or by a bank or other nominee, your brokerage firm, bank or other nominee will only be permitted to vote your Bemis Shares if you instruct it how to vote. You must provide your brokerage firm, bank or other nominee with instructions on how to vote your Bemis Shares in order to vote. Please follow the voting instructions provided by your broker, bank or other nominee. Please note that you may not vote Bemis Shares held in street name by returning a proxy card directly to Bemis or by voting in person at the Bemis Special Meeting unless you obtain a "legal proxy," which you must obtain from your broker, bank or other nominee.

8

AMCO-021

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

Banks, brokerage firms and other nominees who hold Bemis Shares in street name for their customers have authority to vote on "routine" proposals when they have not received instructions from beneficial owners. However, banks, brokerage firms and other nominees are precluded from exercising their voting discretion with respect to non-routine matters when they have not received instructions from beneficial owners. It is expected that all proposals to be voted on at the Bemis Special Meeting are such "non-routine" matters. As a result, absent specific instructions from the beneficial owner of such shares, banks, brokerage firms and other nominees are not empowered to vote such shares, which we refer to as a broker non-vote. The effect of not instructing your broker how you wish your Bemis Shares to be voted will be the same as a vote "AGAINST" the Bemis Transaction Agreement Proposal, but will not have an effect on the Bemis Compensation Proposal, the Bemis Amendments Proposals or the Bemis Adjournment Proposal.

Q: How many votes do I have?

- A:

- Each Bemis shareholder is entitled to one vote for each Bemis Share held of record by such Bemis shareholder as of the Record Date. As of the close of business on the Record Date, there were [ · ] outstanding Bemis Shares.

Q: What constitutes a quorum for the Bemis Special Meeting?

- A:

- The representation, in person or by proxy, of a majority of the Bemis Shares issued and outstanding as of the close of business on the Record Date and entitled to vote is necessary to constitute a quorum for purposes of the Bemis Special Meeting. Votes to abstain are counted as present for the purpose of determining whether a quorum is present. If your Bemis Shares are held in "street name" and you do not instruct your bank, broker or other nominee on how to vote your shares with respect to any of the Bemis Proposals, your Bemis Shares will not be counted toward determining whether a quorum is present. Your shares will be counted toward determining whether a quorum is present if you instruct your bank, broker or other nominee on how to vote your shares with respect to one or more of the Bemis Proposals.

Q: How do I vote my shares?

- A:

- Shareholders of Record. If you are a shareholder of record, you may have your Bemis Shares voted on the matters to be presented at the Bemis Special Meeting in any of the following ways:

- •

- By Mail. Mark the enclosed proxy card, sign and date it and return it in the postage-paid envelope you have been provided. To be valid, your proxy by mail must be received by 11:59 p.m. Eastern time on the day preceding the Bemis Special Meeting.

- •

- By Telephone. The toll-free number for telephone proxy submission can be found on the enclosed proxy card. You will be required to provide your assigned control number located on the proxy card. Telephone proxy submission is available 24 hours a day. If you choose to submit your proxy by telephone, then you do not need to return the proxy card. To be valid, your telephone proxy must be received by 11:59 p.m. Eastern time on the day preceding the Bemis Special Meeting.

- •

- By Internet. The web address and instructions for internet proxy submission can be found on the enclosed proxy card. You will be required to provide your assigned control number located on the proxy card. Internet proxy submission via the web address indicated on the enclosed proxy card is available 24 hours a day. If you choose to submit your proxy by internet, then you do not need to return the proxy card. To be valid, your internet proxy must be received by 11:59 p.m. Eastern time on the day preceding the Bemis Special Meeting.

- •

- In Person. You may also vote your shares in person at the Bemis Special Meeting.

9

AMCO-022

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

Beneficial Owners.

If your Bemis Shares are held in "street name" through a bank, broker or other nominee, you should check the voting form used by that firm to determine whether you may give voting instructions by telephone or the internet and must instruct such bank, broker or other nominee on how to vote such shares by following the instructions that the bank, broker or other nominee provides you along with this proxy statement/prospectus. Your bank, broker or other nominee, as applicable, may have an earlier deadline by which you must provide instructions to it as to how to vote your Bemis Shares, so you should read carefully the materials provided to you by your bank, broker or other nominee.

You are not permitted to vote Bemis Shares held in "street name" by returning a proxy card directly to Bemis or by voting in person at the Bemis Special Meeting unless you provide a "legal proxy," which you must obtain from your broker, bank or other nominee. Further, banks, brokers or other nominees who hold Bemis Shares on behalf of their customers may not give a proxy to Bemis to vote those shares with respect to any of the Bemis Proposals without specific instructions from their customers, because banks, brokers and other nominees do not have discretionary voting power on any of the Bemis Proposals.

Q: How can I change or revoke my vote?

- A:

- You have the right to revoke a proxy, whether delivered over the internet, by telephone or by mail, at any time before it is exercised, by voting again at a later date through any of the methods available to you, by attending the Bemis Special Meeting and voting in person, or by giving written notice of revocation to Bemis prior to 11:59 p.m. Eastern time on the day preceding the Bemis Special Meeting. Attendance at the meeting, in itself, will not revoke a proxy. Written notice of revocation should be mailed to: Bemis Company, Inc., Bemis Innovation Center, 2301 Industrial Drive, Neenah, Wisconsin 54926, Attention: Corporate Secretary. If you hold Bemis Shares in "street name," you should follow the instructions provided by your bank, brokerage firm or other nominee in order to change or revoke your vote.

Q: If a shareholder gives a proxy, how are the Bemis Shares voted?

- A:

- Regardless of the method you choose to vote, the individuals named on the enclosed proxy card will vote your Bemis Shares in the way that you indicate. When completing the internet or telephone processes or the proxy card, you may specify whether your Bemis Shares should be voted for or against, or you may abstain from voting on, all, some or none of the specific items of business to come before the Bemis Special Meeting.

If you properly sign your proxy card but do not mark the boxes showing how your Bemis Shares should be voted on a matter, the Bemis Shares represented by your properly signed proxy card will be voted "FOR" the Bemis Transaction Agreement Proposal, "FOR" the Bemis Compensation Proposal, "FOR" the Bemis Amendments Proposals and "FOR" the Bemis Adjournment Proposal.

Q: What should I do if I receive more than one set of voting materials?

- A:

- If you hold Bemis Shares in "street name" and also directly as a record holder or otherwise or if you hold Bemis Shares in more than one brokerage account, you may receive more than one set of voting materials relating to the Bemis Special Meeting. Please complete, sign, date and return each proxy card (or cast your vote by telephone or internet as provided on your proxy card) or otherwise follow the voting instructions provided in this proxy statement/prospectus in order to ensure that all of your Bemis Shares are voted. If you hold your Bemis Shares in "street name" through a bank, brokerage firm or other nominee, you should follow the procedures provided by your bank, brokerage firm or other nominee to vote your shares.

10

AMCO-023

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

Q: What happens if I sell my Bemis Shares before the Bemis Special Meeting?

- A:

- The Record Date is earlier than both the date of the Bemis Special Meeting and the effective time of the transaction. If you transfer your Bemis Shares after the Record Date but before the Bemis Special Meeting, you will, unless the transferee requests a proxy from you, retain your right to vote at the Bemis Special Meeting but will transfer the right to receive the transaction consideration to the person to whom you transfer your Bemis Shares. In order to become entitled to receive the transaction consideration you must hold your Bemis Shares through the effective time of the transaction, which Amcor and Bemis expect will occur in the first quarter of 2019, subject to satisfaction of closing conditions.

Q: Who will solicit and pay the cost of soliciting proxies?

- A:

- Bemis has engaged Innisfree M&A Incorporated ("Innisfree") to assist in the solicitation of proxies for the Bemis Special Meeting. Bemis will pay Innisfree a base fee of $25,000 plus reasonable out-of-pocket expenses. Bemis also may reimburse banks, brokerage firms, other nominees or their respective agents for their reasonable expenses in sending proxy materials to beneficial owners of Bemis Shares. In addition to solicitations by mail, Bemis' directors, officers and regular employees may solicit proxies personally or by telephone without additional compensation.

Q: What do I need to do now?

- A:

- After carefully reading and considering the information contained in this proxy statement/prospectus, please vote promptly to ensure that your shares are represented at the Bemis Special Meeting. If you hold your Bemis Shares in your own name as the shareholder of record, you may submit a proxy to have your Bemis shares voted at the Bemis Special Meeting in one of four ways (described in detail in the response to the question "How do I vote my shares?"):

- •

- by returning a properly executed proxy card;

- •

- by telephone;

- •

- via the internet; or

- •

- in person at the Bemis Special Meeting.

If you decide to attend the Bemis Special Meeting and vote in person, your in-person vote will revoke any proxy previously submitted.

If your Bemis Shares are held in "street name" through a bank, broker or other nominee, you should check the voting form used by that firm to determine whether you may give voting instructions by telephone or the internet and must instruct such bank, broker or other nominee on how to vote such shares by following the instructions that the bank, broker or other nominee provides you along with this proxy statement/prospectus. Your bank, broker or other nominee, as applicable, may have an earlier deadline by which you must provide instructions to it as to how to vote your Bemis Shares, so you should read carefully the materials provided to you by your bank, broker or other nominee.

You are not permitted to vote Bemis Shares held in "street name" by returning a proxy card directly to Bemis or by voting in person at the Bemis Special Meeting unless you provide a "legal proxy," which you must obtain from your broker, bank or other nominee. Further, banks, brokers or other nominees who hold Bemis Shares on behalf of their customers may not give a proxy to Bemis to vote those shares with respect to any of the Bemis Proposals without specific instructions from their customers, because banks, brokers and other nominees do not have discretionary voting power on any of the Bemis Proposals.

11

AMCO-024

Table of Contents

Confidential Treatment Requested by AMCOR PLC

Pursuant to 17 C.F.R. Section 200.83

Q: Where can I find the voting results of the Bemis Special Meeting?

- A:

- The preliminary voting results will be announced at the Bemis Special Meeting, if available. In addition, within four business days following certification of the final voting results, Bemis will file the final voting results with the SEC on a Current Report on Form 8-K.

Q: Am I entitled to exercise appraisal or dissenters' rights instead of receiving the transaction consideration for my Bemis Shares?

- A: