Table of Contents

Exhibit 99.1

[Date]

Dear DowDuPont Stockholder:

As previously announced, DowDuPont Inc. (“DowDuPont”) intends to separate into three independent, publicly traded companies—one for each of its agriculture, materials science and specialty products businesses. We are pleased to deliver to you this information statement to inform you that on [●], our board of directors approved the first step in this plan: the separation of our materials science business, “Dow,” through the distribution to DowDuPont stockholders of all of the then issued and outstanding shares of common stock of Dow Holdings Inc. (“Dow common stock”), a wholly owned subsidiary of DowDuPont and the newly formed holding company for Dow. Completion of the separation will create the industry’s premier materials science solution provider focused on the high-growth market verticals of consumer care, infrastructure and packaging.

The separation is expected to be completed on [●], and will be effected by way of a pro rata dividend of Dow common stock to DowDuPont stockholders of record as of the close of business, Eastern Time, on [●], the record date. Each DowDuPont stockholder will receive [●] shares of Dow common stock for every [●] shares of DowDuPont common stock held on the record date.

Following the separation and distribution of Dow, DowDuPont (which we now refer to as “New DuPont”) will then separate Corteva, the subsidiary that will hold, at the time of its distribution, the assets and liabilities associated with DowDuPont’s agriculture business, by way of a pro rata distribution of Corteva’s common stock to New DuPont stockholders. Assuming both distributions are completed as anticipated, the remaining company, New DuPont, will hold only DowDuPont’s specialty products business. Following the distributions, DowDuPont will become known as DuPont. The separations are the first step toward creating three independent companies that are better positioned to capitalize on significant growth opportunities and to focus their respective resources on their particular business and strategic priorities.

We expect the distribution of Dow common stock to betax-free to you for U.S. federal income tax purposes, except for any cash received in lieu of fractional shares. You should consult your own tax advisor as to the particular tax consequences of the distribution of Dow common stock to you, including potential tax consequences under state, local andnon-U.S. tax laws.

Stockholder approval of the distribution is not required. In addition, you do not need to take any action to receive your Dow common stock and you do not need to pay any consideration or surrender or exchange your DowDuPont shares in order to receive your Dow common stock. Immediately following the distribution, you will own common stock in both New DuPont and Dow. The Dow common stock will be listed on the New York Stock Exchange under the symbol “DOW.”

We encourage you to carefully read the enclosed information statement, which is being mailed to all DowDuPont stockholders who held shares of DowDuPont common stock as of the record date for the distribution. The information statement describes the separation and distribution of Dow in detail and contains important information about Dow, including its business, financial condition and operations, and the distribution.

The DowDuPont board of directors believes that creating three focused companies will maximize value for all DowDuPont stockholders, and this separation is an exciting first step in this process. We want to thank you for your continued support of DowDuPont and we look forward to your support of Dow in the future.

Sincerely,

Edward D. Breen Chief Executive Officer DowDuPont Inc. | Jeff M. Fettig Executive Chairman DowDuPont Inc. |

Table of Contents

[Date]

Dear Dow Stockholder:

On behalf of Dow Holdings Inc., it is my great privilege to welcome you as a stockholder of our company.

When we announced Dow’s intention to merge with DuPont to form DowDuPont, we also announced the intention to separate the combined company into three independent, publicly traded companies. Today, we stand ready to deliver the first intended company—the new Dow.

We are proud of our more than120-year heritage. And we are equally excited for the opportunity that lies ahead, as we pursue our ambition to become the most innovative, customer-centric, inclusive and sustainable materials science company in the world.

The new Dow will be more focused, agile and market-oriented, with a portfolio comprised of six global business units organized into three operating segments: Performance Materials & Coatings; Industrial Intermediates & Infrastructure; and Packaging & Specialty Plastics. Through our deep materials science expertise, value chain understanding, global reach, scale and competitive capabilities, we will provide differentiated products and solutions to our customers. And we intend to direct our efforts primarily to three coreend-markets where we hold global leadership positions today—consumer care, infrastructure and packaging.

The new Dow will also be a financially disciplined company. We will be prudent stewards of our capital. Our focus will be to maximize value for our stockholders by driving profitable growth, higher returns on invested capital, increasing free cash flow and greater cash returns to you. In the long term, we are committed to maintaining and improving our leadership positions in our three key verticals—consumer care, infrastructure and packaging. Our near-term focus will be on incremental, less capital intensive, fast payback projects. As industry andend-market dynamics shift, we will continue to exercise disciplined portfolio management. And we intend to drive to abest-in-class cost structure.

Dow Holdings Inc.’s common stock will be listed on the New York Stock Exchange under the symbol “DOW.”

We invite you to learn more about our company, our strategy and how we are positioned to compete and win, by reviewing the enclosed information statement.

We value your ownership and look forward to growing together.

Best regards,

Jim Fitterling

Chief Executive Officer

Dow Holdings Inc.

Table of Contents

Information contained herein is subject to completion or amendment. A Registration Statement on Form 10 relating to these securities has been filed with the Securities and Exchange Commission under the Securities Exchange Act of 1934, as amended.

Preliminary and Subject to Completion, dated November 19, 2018

INFORMATION STATEMENT

Dow Holdings Inc.

Common Stock, Par Value $0.01 Per Share

This information statement is being furnished in connection with DowDuPont Inc.’s (“DowDuPont”) separation of its materials science business, “Dow,” through the distribution of shares of common stock of its subsidiary, Dow Holdings Inc. (“Dow NewCo,” and Dow NewCo’s common stock, the “Dow common stock”). The distribution will be effected by way of a pro rata dividend of Dow common stock to DowDuPont stockholders of record as of the close of business, Eastern Time, on [●], the record date. Dow NewCo is a newly formed holding company for Dow and at the time of the distribution will hold, directly or indirectly, DowDuPont’s materials science business, which includes DowDuPont’s Performance Materials & Coatings, Industrial Intermediates & Infrastructure and Packaging & Specialty Plastics segments.

As a DowDuPont stockholder, you will receive [●] shares of Dow common stock for every [●] shares of DowDuPont common stock that you hold of record as of the close of business on the record date. No fractional shares of Dow common stock will be issued. Instead, you will receive cash in lieu of any fractional shares. The distribution is intended to betax-free to DowDuPont stockholders for United States federal income tax purposes, except for any cash received in lieu of fractional shares, which will generally be taxable.

Dow common stock will be listed on the New York Stock Exchange (“NYSE”) under the symbol “DOW.” Dow expects DowDuPont will distribute the shares of Dow common stock to you on [●] prior to the opening of trading on the NYSE, subject to the satisfaction or waiver of certain conditions. Dow refers to the date of the distribution of the Dow common stock as the “distribution date.” Immediately after the distribution, Dow will be an independent, publicly traded company.

DowDuPont stockholders are not required to vote on or take any other action in connection with the separation or distribution. Therefore, Dow is not asking for a proxy to vote on the separation or the distribution, and Dow requests that you do not send Dow a proxy. DowDuPont stockholders will not be required to exchange or surrender their existing shares of DowDuPont common stock or take any other action to receive their applicable shares of Dow common stock, nor will they be required to pay any consideration for the shares of Dow common stock they receive in the distribution.

DowDuPont currently owns all of the outstanding shares of Dow NewCo. Accordingly, there is no current trading market for Dow common stock. Dow expects that a limited market, commonly known as a “when-issued” trading market, will develop on or shortly before the record date for the distribution, and Dow expects“regular-way” trading of Dow common stock to begin on the distribution date. As discussed under “The Distribution—Trading Between the Record Date and Distribution Date,” if you sell your DowDuPont common stock in the“regular-way” market after the record date and before the distribution, you also will be selling your right to receive shares of Dow common stock in connection with the separation and distribution.

In reviewing this information statement, you should carefully consider the matters described under the caption “Risk Factors” beginning on page 29.

Neither the U.S. Securities and Exchange Commission (“SEC”) nor any state securities commission has approved or disapproved these securities or determined if this information statement is truthful or complete. Any representation to the contrary is a criminal offense.

This information statement does not constitute an offer to sell or the solicitation of an offer to buy any securities.

References in this information statement to specific codes, legislation or other statutory enactments are to be deemed as references to those codes, legislation or other statutory enactments, as amended from time to time.

The date of this information statement is [●] and is first being mailed to

DowDuPont stockholders on or about [●].

Table of Contents

| Page | ||||

MERGER, INTENDED SEPARATIONS, REORGANIZATION AND FINANCIAL STATEMENT PRESENTATION | 3 | |||

| 6 | ||||

| 13 | ||||

| 18 | ||||

| 29 | ||||

| 44 | ||||

| 46 | ||||

| 54 | ||||

| 55 | ||||

| 56 | ||||

| 67 | ||||

| 90 | ||||

| 97 | ||||

| 99 | ||||

| 131 | ||||

| 138 | ||||

| 145 | ||||

| 148 | ||||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 149 | |||

DOW’S RELATIONSHIP WITH NEW DUPONT AND CORTEVA FOLLOWING THE DISTRIBUTION | 150 | |||

MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES OF THE DISTRIBUTION | 152 | |||

| 156 | ||||

| 157 | ||||

| 162 | ||||

| 163 | ||||

| F-1 | ||||

Table of Contents

The following is a summary of material information discussed in this information statement. This summary may not contain all the details concerning the separation and distribution or other information that may be important to you. To better understand the separation, distribution and Dow’s business and financial position, you should carefully review this entire information statement.

Unless otherwise indicated or the context otherwise requires, references in this information statement to:

| • | “Business Realignment” has the meaning set forth in the section titled “Merger, Intended Separations, Reorganization and Financial Statement Presentation”; |

| • | “distribution” refers to the transaction in which DowDuPont will distribute to its stockholders all of the then issued and outstanding shares of Dow common stock; |

| • | “distribution date” means the date of the distribution, which is expected to be [●]; |

| • | “Dow” refers to Dow NewCo, TDCC and their consolidated subsidiaries after giving effect to the Internal Reorganization and Business Realignment, resulting in Dow NewCo holding the materials science business of DowDuPont; |

| • | “Dow board of directors” refers to the board of directors of Dow NewCo following the distribution; |

| • | “Dow NewCo” refers to Dow Holdings Inc., the newly formed holding company for DowDuPont’s materials science business; |

| • | “Dow common stock” refers to the shares of common stock, par value $0.01 per share, of Dow NewCo; |

| • | “Dow stockholders” refers to holders of Dow common stock following the distribution; |

| • | “DowDuPont” refers to DowDuPont Inc., a Delaware corporation, and its consolidated subsidiaries, prior to the distribution of Dow; |

| • | “DowDuPont stockholders” refers to holders of record of the common stock of DowDuPont Inc. in their capacity as such; |

| • | “Historical Dow” refers to TDCC and its consolidated subsidiaries prior to the Business Realignment; |

| • | “Historical DuPont” refers to E. I. du Pont de Nemours and Company (“EID”) and its consolidated subsidiaries prior to the Business Realignment; |

| • | “Internal Reorganization” has the meaning set forth in the section titled “Merger, Intended Separations, Reorganization and Financial Statement Presentation”; |

| • | “New DuPont” refers to DowDuPont and its consolidated subsidiaries, (i) following the distribution of Dow, at which time New DuPont will continue to hold both DowDuPont’s agriculture and specialty products businesses, and (ii) following the distribution of Corteva, at which time New DuPont will hold only the specialty products business (following the distributions, DowDuPont will become known as DuPont); |

| • | “record date” means [●], the date set by the DowDuPont board of directors to determine the DowDuPont stockholders eligible to receive the distribution of Dow common stock; |

| • | “separation” refers to the transaction in which Dow will be separated from DowDuPont; and |

| • | “TDCC” refers to The Dow Chemical Company, exclusive of its subsidiaries. |

Unless otherwise indicated or the context otherwise requires, this information statement describes Dow as if the Internal Reorganization and Business Realignment have been completed and as if Dow held only the materials science business of DowDuPont during all periods described. As a result, references in this information statement to Dow’s historical assets, liabilities, products, businesses or activities are generally references to the

1

Table of Contents

applicable assets, liabilities, products, business or activities of Historical Dow and Historical DuPont on a pro forma basis as if the Internal Reorganization and Business Realignment had already occurred and Dow was a standalone company holding only DowDuPont’s materials science business. See the section entitled “Merger, Intended Separations, Reorganization and Financial Statement Presentation” for further information.

You should read this entire information statement carefully, including the consolidated financial statements of Historical Dow and notes thereto, which are incorporated by reference herein to the pertinent pages of the Historical Dow 2017 Form10-K (as defined in the section entitled “Unaudited Pro Forma Combined Financial Information”) and the Historical Dow Third Quarter 2018 Form10-Q (as defined in the section entitled “Unaudited Pro Forma Combined Financial Information”), which are filed as Exhibits 99.2 and 99.3, respectively, to the registration statement on Form 10 of which this information statement forms a part (the “Form 10”), the unaudited pro forma combined financial information for Dow and the notes thereto included elsewhere herein, and the sections entitled “The Business,” “Supplemental Pro Forma Segment Results for Dow,” “Selected Consolidated Financial Data of Historical Dow,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations of Historical Dow,” and “Risk Factors.” Some of the statements in this information statement constitute forward-looking statements. See “Cautionary Statement Concerning Forward-Looking Statements.”

You should not assume that the information contained in this information statement is accurate as of any date other than the date set forth on the cover. Changes to the information contained in this information statement may occur after that date, and Dow undertakes no obligation to update the information, except in the normal course of Dow’s public disclosure obligations.

2

Table of Contents

MERGER, INTENDED SEPARATIONS, REORGANIZATION AND

FINANCIAL STATEMENT PRESENTATION

Merger

DowDuPont is a Delaware corporation that was formed on December 9, 2015 for the purpose of effecting theall-stock merger of equals transaction between Historical Dow and Historical DuPont. On August 31, 2017, Historical Dow and Historical DuPont each merged with wholly owned subsidiaries of DowDuPont and, as a result, became subsidiaries of DowDuPont (the “Merger”).

Intended Separations

Prior to the Merger, Historical Dow and Historical DuPont were each publicly traded companies that were listed on the NYSE, with Historical Dow operating a global business that included agricultural sciences, consumer solutions, infrastructure solutions, performance materials and chemicals and performance plastics segments and Historical DuPont operating a global business that included agriculture, electronics and communications, industrial biosciences, nutrition and health, performance materials and protection solutions segments.In connection with the signing of the merger agreement for the Merger (the “merger agreement”), Historical Dow and Historical DuPont announced their intention to pursue, subject to the approval of the DowDuPont board of directors and any required regulatory approvals, the separation of the combined company, DowDuPont, into three independent, publicly traded companies—one for each of the combined company’s agriculture, materials science and specialty products businesses.

Internal Reorganization

In furtherance of DowDuPont’s planned separation into three independent, publicly traded companies, prior to, but in connection with, the separation and distribution, Historical Dow and Historical DuPont will undertake a series of internal reorganization transactions to align their respective businesses into three subgroups: agriculture, materials science and specialty products. DowDuPont has also formed two wholly owned subsidiaries: Dow NewCo, to serve as a holding company for Dow, and Corteva, Inc. (including, where context requires, its consolidated subsidiaries, “Corteva”), to serve as a holding company for its agriculture business. Following the distribution of Dow, the remaining company, which is referred to herein as “New DuPont,” will continue to hold DowDuPont’s agriculture and specialty products businesses. New DuPont is then expected to complete the distribution of Corteva, resulting in New DuPont holding only the specialty products business of DowDuPont. Following the distributions, DowDuPont will be known as DuPont.

This series of reorganization transactions, which we refer to in this information statement as the “Internal Reorganization,” will involve:

| • | the transfer or conveyance by Historical Dow of its assets and liabilities that are (i) aligned with DowDuPont’s agriculture business (including Historical Dow’s agriculture business) to legal entities that will be subsidiaries of Corteva following the Business Realignment (as defined below) (although certain transfers and conveyances to Corteva may occur after the Business Realignment but prior to the distribution of Dow), (ii) aligned with DowDuPont’s specialty products business (including those portions of Historical Dow’s business that are aligned with the specialty products business) to legal entities that will be subsidiaries of New DuPont following the Business Realignment (although certain transfers and conveyances to New DuPont may occur after the Business Realignment but prior to the distribution of Dow) and (iii) aligned with DowDuPont’s materials science business to legal entities that will remain with Dow; and |

| • | the transfer or conveyance by Historical DuPont of its assets and liabilities that are (i) aligned with DowDuPont’s agriculture business to legal entities that will remain with Corteva following the Business Realignment, (ii) aligned with DowDuPont’s specialty products business (including Historical |

3

Table of Contents

DuPont’s specialty products business) to legal entities that will be subsidiaries of New DuPont following the Business Realignment and (iii) aligned with DowDuPont’s materials science business (including Historical DuPont’s ethylene and ethylene copolymers businesses (other than its ethylene acrylic elastomers business)) to legal entities that will be subsidiaries of Dow following the Business Realignment. |

Following the Internal Reorganization, Historical Dow and Historical DuPont will then transfer or convey among Dow, Corteva and New DuPont all of the equity interests of the applicable subsidiaries such that, in addition to any assets and liabilities allocated to Dow, Corteva and New DuPont pursuant to the separation agreement (as defined below), Dow will hold only the assets and liabilities related to DowDuPont’s materials science business, Corteva will hold only the assets and liabilities related to DowDuPont’s agriculture business, and New DuPont will hold only the assets and liabilities related to DowDuPont’s specialty products business. These transfers and conveyances, which we refer to in this information statement as the “Business Realignment,” will involve:

| • | the transfer or conveyance of Historical Dow’s interests in the capital stock of, or any other equity interests in, the entities that are to be subsidiaries of Corteva or New DuPont to Corteva or New DuPont, as applicable; and |

| • | the transfer or conveyance of Historical DuPont’s interests in the capital stock of, or any other equity interests in, the entities that are to be subsidiaries of Dow or New DuPont to Dow or New DuPont (although certain transfers and conveyances to New DuPont may occur after the Business Realignment but prior to the expected distribution of Corteva), as applicable. |

In the case of Dow, as a result of the Internal Reorganization and Business Realignment, at the time of the separation and distribution, Dow NewCo will hold all of the outstanding common stock of TDCC as well as DowDuPont’s Performance Materials & Coatings, Industrial Intermediates & Infrastructure and Packaging & Specialty Plastics segments, which includes Historical DuPont’s ethylene and ethylene copolymers businesses (other than its ethylene acrylic elastomers business).

For further information, see the section entitled “Dow’s Relationship with New DuPont and Corteva Following the Distribution—Separation Agreement.”

Financial Statement Presentation

This information statement generally describes Dow as if the Internal Reorganization and Business Realignment have already been completed and Dow holds only the materials science business of DowDuPont that it will hold at the time of the distribution.Accordingly, this information statement includes an unaudited pro forma consolidated balance sheet for Dow as well as unaudited pro forma consolidated statements of income for Dow, which present Dow’s financial position and results of operations to give pro forma effect to the Internal Reorganization, the Business Realignment, the distribution, and the other transactions described under “Unaudited Pro Forma Combined Financial Information.” The unaudited pro forma combined financial statements are presented for illustrative purposes only and should not be viewed as an indication of current or future results of operations, financial position or cash flows as if Dow had been a separate, standalone company holding only DowDuPont’s materials science business during the periods presented.

This information statement also includes certain historical consolidated financial information related to and discusses the results of operations, financial condition and business of Historical Dow. For example, the historical financial statements incorporated by reference herein are the financial statements of Historical Dow and reflect Historical Dow’s business as it has been conducted prior to the Internal Reorganization and Business Realignment. These financial statements therefore reflect the business of Historical Dow, which includes those portions of Historical Dow’s business that form part of DowDuPont’s agriculture business and will be transferred to Corteva and those portions of Historical Dow’s business that form part of DowDuPont’s specialty products business and will be transferred to New DuPont. They also do not reflect the portions of Historical DuPont’s

4

Table of Contents

business related to DowDuPont’s materials science business that will be transferred to Dow. As such, Historical Dow’s financial information and results are not representative of the financial results that Dow would have achieved as a separate, publicly traded company holding only DowDuPont’s materials science business nor indicative of the results Dow expects for any future period. Information in this information statement that does not reflect Dow as it will be comprised at the time of the separation and distribution is generally identified by reference to “Historical Dow.” For further information, see the sections entitled “Selected Consolidated Financial Data of Historical Dow” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations of Historical Dow.”

Dow NewCo is a wholly owned subsidiary of DowDuPont that was formed on August 30, 2018 to serve as a holding company for Dow. Dow NewCo has engaged in no business operations to date and has no assets or liabilities of any kind, other than those incident to its formation.

5

Table of Contents

Distributing Company

DowDuPont is a holding company comprised of Historical Dow and Historical DuPont. DowDuPont conducts its operations worldwide through the following eight segments: Agriculture; Performance Materials & Coatings; Industrial Intermediates & Infrastructure; Packaging & Specialty Plastics; Electronics & Imaging; Nutrition & Biosciences; Transportation & Advanced Polymers; and Safety & Construction and collectively has approximately 98,000 employees.

In connection with the signing of the merger agreement, Historical Dow and Historical DuPont announced their intention, subject to the approval of the DowDuPont board of directors and any required regulatory approvals, to separate DowDuPont into three independent, publicly traded companies—one for each of the combined company’s agriculture, materials science and specialty products businesses.

The distribution of Dow, which at the time of the distribution will hold DowDuPont’s materials science business, is expected to be the first of the two distributions to effectuate DowDuPont’s plan to separate into three strong, independent, publicly traded companies. Following the distribution of Dow, the remaining company, which is referred to herein as “New DuPont,” will hold DowDuPont’s agriculture and specialty products businesses. It is expected that New DuPont will then complete, subject to the approval of its board of directors, the distribution of Corteva, which will hold the assets and liabilities associated with DowDuPont’s agriculture business, resulting in New DuPont holding only the specialty products business of DowDuPont. The separation of Corteva is expected to be completed by June 1, 2019 through the distribution to New DuPont stockholders of all of the common stock of Corteva. Following the distributions, DowDuPont will become known as DuPont. The DowDuPont board of directors believes that the completion of these separations will result in three independent, publicly traded companies that will lead their respective industries through productive, science-based innovation to meet the needs of customers and help solve global challenges and is the best available opportunity to unlock the value of DowDuPont’s businesses.

Dow Holdings Inc.

Dow will be a leading materials science company, combining science and technology to develop innovative solutions that are essential to human progress. Dow’s ambition is to be the most innovative, customer-centric, inclusive and sustainable materials science company in the world. Following the separation and distribution, Dow will employ its technology platforms, broad geographic reach and operational scale to deliver differentiated products and solutions through a focused business portfolio primarily aligned with three consumer-driven market verticals: consumer care, infrastructure and packaging.

With over 120 years of history, Dow’s knowledge of customers’ needs—and the eventual consumers’ needs—is at the core of its value proposition. Dow’s products serve as critical inputs used in a variety of high-performance applications, including coatings, home and personal care, durable goods, adhesives and sealants, and food and specialty packaging. These product offerings meet highly specialized customer needs and represent a critical component of customers’ products.

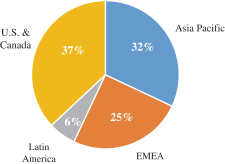

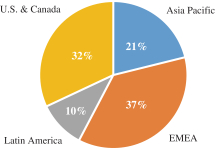

Dow’s products will be manufactured at 114 sites in 32 countries, reaching approximately 23,000 customers around the world. Dow’s global presence will allow it to serve a broad customer base, providing Dow with geographically diversified revenue and earnings streams. In addition, Dow will operate a global commercial and development network that features eightstate-of-the-art research and development (“R&D”) centers, covering each of the major geographies, with several additional laboratories and technical service centers around the world positioned to meet the growth and product development needs of customers.

In 2017, on a pro forma basis, Dow employed approximately 39,000 people and delivered pro forma sales of approximately $44.8 billion, pro forma net loss of $580 million and pro forma Operating EBIT of $5.6 billion.

6

Table of Contents

See the sections entitled “Unaudited Pro Forma Combined Financial Information” and “Supplemental Pro Forma Segment Results for Dow” for additional information, including a reconciliation of pro forma net income (loss) to pro forma Operating EBIT and pro forma Operating EBITDA.

Dow’s portfolio will be comprised of six global business units, organized into three operating segments: Performance Materials & Coatings, Industrial Intermediates & Infrastructure and Packaging & Specialty Plastics.

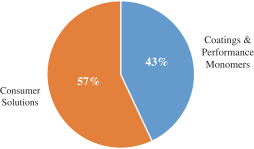

Performance Materials & Coatings includes industry-leading franchises that deliver a wide array of solutions into consumer and infrastructureend-markets. The segment consists of two global businesses: Coatings & Performance Monomers and Consumer Solutions. These businesses primarily utilize Dow’sacrylics-, cellulosics- and silicone-based technology platforms to serve the needs of the architectural and industrial coatings, home care and personal careend-markets. Both businesses employ materials science capabilities, global reach and unique products and technology to combine chemistry platforms to deliver differentiated offerings to customers.

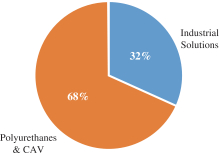

Industrial Intermediates & Infrastructureconsists of two customer-centric global businesses—Industrial Solutions and Polyurethanes & CAV—that develop important intermediate chemicals that are essential to manufacturing processes, as well as downstream, customized materials and formulations that use advanced development technologies. These businesses primarily produce and market ethylene oxide, propylene oxide derivatives, cellulose ethers, redispersible latex powders and acrylic emulsions that are aligned to market segments as diverse as appliances, coatings, infrastructure, oil and gas, and building and construction. The global scale and reach of these businesses, world-class technology and R&D capabilities and materials science expertise enable Dow to be a premier solutions provider offering customersvalue-add sustainable solutions to enhance comfort, energy efficiency, product effectiveness and durability across a wide range of home comfort and appliances, building and construction, adhesives and lubricant applications, among others.

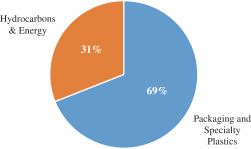

Packaging & Specialty Plasticsis a world leader in plastics and consists of two highly integrated global businesses: Hydrocarbons & Energy and Packaging and Specialty Plastics. The segment employs the industry’s broadest polyolefin product portfolio, supported by Dow’s proprietary catalyst and manufacturing process technologies, to work at the customer’s design table throughout the value chain to deliver more reliable and durable, higher performing, and more sustainable plastics to customers in food and specialty packaging; industrial and consumer packaging; health and hygiene; caps, closures and pipe applications; consumer durables; and infrastructure.

Dow’s Strategy

Dow strives to be the most innovative, customer-centric, inclusive and sustainable materials science company in the world—one that is driven by world-class talent and enabled by leading products and technologies.

Dow pursues this ambition with industry-leading materials science capabilities and competitive cost positions applied to three attractive markets: consumer care, infrastructure and packaging. These sectors have strong consumer-driven demand trends, including: urbanization; growing middle-class populations, particularly in the emerging world; increasing demand for sustainable solutions that support a circular economy and lower energy intensity; and faster value chain interactions that are driving demands for digital business models and sharper data insights.

Dow’s goal is to deliver profitable growth over the long-term by aligning its actions to a core set of strategic priorities:

| • | Maintain and improve Dow’s leadership positions in attractive growth markets where Dow’s leading materials science expertise, unparalleled global reach and customer and value chain understanding is recognized and rewarded; |

7

Table of Contents

| • | Focus on innovation and capitalizing on growth andvalue-add materials science opportunities between Dow’s technology platforms by leveraging Dow’s leading R&D and process technology capabilities to quickly adapt and innovate for the benefit of Dow’s customers and value chain partners through developing new and next generation products, formulations and novel solutions; |

| • | Maintain Dow’s foundation of operational excellence, exemplified by Dow’s long-standing hallmark performance in safe, reliable, and sustainable operations; |

| • | Exercise disciplined resource and capital allocation, focused on maintaining our leadership positions, driving profitable growth and improving return on invested capital. This includes a near-term focus on incremental, less capital intensive and fast payback investments that continue to drive organic growth and enhance Dow’s asset flexibility, reliability, and efficiency, without sacrificing Dow’s ability to evaluate the best long-term growth opportunities; |

| • | Drive continuous productivity, creating efficiency gains in Dow’s manufacturing and corporate operations in order to enhance Dow’s cost positions, increase throughput and maintain a streamlined corporate infrastructure, in part driven by integrating digitalization across our operations, businesses and work processes; |

| • | Disciplined portfolio management that continually assesses whether Dow’s portfolio is optimized to fit the company’s strategy and priorities based on return and competitive position criteria; |

| • | Commitment to sustainability in Dow’s products, operations and supply chains, which includes a continuation of Dow’s global industry leadership in transparency of sustainability reporting and goal setting; and |

| • | A fully inclusive organizationthat seeks to enhance Dow’s employee and customer experiences and strengthen Dow’s understanding of the communities it serves. |

In summary, Dow expects its strategy to further deepen its position as the industry’s leading materials science company and enhance the vitality of Dow’s customer relationships and the value Dow’s customers’ place on its product solutions—leading to higher returns on invested capital, increasing free cash flow (cash flows from operating activities less capital expenditures) and enhanced stockholder value.

Dow’s Competitive Strengths

Dow’s more than 120 years of history have enabled it to build a variety of competitive strengths that each support its strategic pillars and highlight how Dow is positioned to win with customers and in its core market verticals. These strengths include the following:

| • | Best-in-class manufacturing scale, with global reach and value chain knowledge; |

| • | Leading global market positions in growing, consumer-driven end markets; |

| • | Market-driven technology and intellectual property that enables Dow’s materials science expertise; |

| • | Diverse and deep customer relationships with a strong track record of collaboration; |

| • | A broad geographic footprint that is well-positioned to capture demand growth; |

| • | World-class safety and reliable operations; |

| • | Dow’s commitment to advancing sustainability; |

| • | Dow’s experienced management team with deep industry expertise; and |

| • | Dow’s inclusive, diverse and aligned business organization. |

8

Table of Contents

Detailed information on Dow’s competitive strengths can be found in “The Business—Dow’s Competitive Strengths.”

Although Dow expects these strengths to position Dow to execute on its business strategy and leverage its position as the industry’s leading materials science company in order to deliver profitable growth over the long-term, there are risks associated with Dow’s business as well as Dow’s separation from DowDuPont. For an overview of certain of these risks, please see the summary below under the caption “Risks Associated with Dow’s Business” as well as the information in the section entitled “Risk Factors.”

Risks Associated with Dow’s Business

An investment in Dow is subject to a number of risks. The following list of risk factors related to Dow’s business is not exhaustive. Please read the information in the section entitled “Risk Factors” for a more thorough description of these and other risks, including risks related to the separation and to Dow common stock.

| • | Conditions in the global economy and global capital markets—Dow operates in a global, competitive environment, which gives rise to operating and market risk exposure that could have a negative impact on Dow’s results of operations. |

| • | Financial commitments and exposure to credit markets—adverse conditions in economic markets could reduce Dow’s flexibility to respond to changing business conditions or to fund its capital needs. In addition, Dow will retain Historical Dow’s indebtedness following the separation and distribution, and if Dow is unable to generate sufficient funds to service this significant debt, Dow’s ability to fund working capital and/or expansion could be negatively impacted. |

| • | Raw materials requirements—Dow relies on the availability of purchased feedstocks and energy, the unavailability of these materials or volatility in their cost, could negatively impact Dow’s operating costs and add volatility to its earnings. |

| • | Changes in industry supply and demand—the ability of Dow to generate earnings varies in part based on the balance of supply relative to demand in Dow’s industries, and changes in capacity and disruptions in supply/demand balances could negatively impact Dow’s results of operations. |

| • | Litigation exposures and costs—in the ordinary course of its business, Dow is a party to a number of claims and lawsuits, including those related to product liability and patent infringement claims, employment matters, governmental tax and regulatory disputes, and contract and commercial litigation, for which Dow could have significant costs and incur significant liabilities. |

| • | Environmental compliance impacts—Dow is subject to extensive federal, state, local and foreign laws, regulations, rules and ordinances pertaining to environmental compliance and the costs of complying with these evolving regulatory requirements could negatively impact Dow’s financial results. In addition, actual or alleged violations of environmental laws or permitting requirements by Dow could result in restrictions or prohibitions on Dow’s plant operations, substantial civil or criminal sanctions, and/or the assessment of strict liability and/or joint and several liability, which could negatively affect Dow’s financial condition and results of operations. |

| • | Restrictions from health and safety regulations—increasing concerns regarding the safe use of chemicals and plastics in commerce (including concerns about environmental impact) have resulted and may result in new restrictive regulations, which may have a negative impact on Dow’s purchasing habits, regulatory compliance, product development and launches and potential litigation, all of which may impact Dow’s results of operations. |

| • | Significant operational disruption—as a diversified chemical manufacturing company, Dow’s operations may be disrupted by issues in the transportation of products, cyber attacks, or severe |

9

Table of Contents

weather events or natural phenomena, among other things, which events could significantly impact Dow’s production and operations and have a negative impact on its results of operations. Following the separation, Dow will also be subject to restrictions under certain intellectual property agreements with New DuPont and Corteva, which will limit Dow’s ability to develop and commercialize certain products and services. |

| • | Uncertainty in strategic implementation—the implementation of Dow’s strategy and development projects may be affected by a number of factors, including Dow’s operation in diverse markets and emerging geographies and the need to develop relationships with new customer and suppliers, and Dow’s financial condition, cash flows and results of operations may be adversely affected by its failure to successfully implement its strategy. |

| • | Restrictions on strategic flexibility—in order to preserve the tax-free nature of the distribution and related transactions, Dow will be restricted in its ability to undertake certain transactions in the future, including from entering into certain business combination and other transactions involving Dow’s assets and/or the Dow common stock, which could limit Dow’s strategic flexibility. |

| • | Impairments of goodwill—if Dow determines that it mustwrite-off a significant portion of its goodwill, Dow’s results of operations could be negatively impacted. |

| • | Changes in pension liabilities and obligations—increases in Dow’s obligations or funding requirements under its defined benefit pension plans and other postretirement benefit plans could negatively impact Dow’s cash flows and financial condition. |

Following the separation, Dow will be a pure-play materials science company and will not operate under the umbrella of DowDuPont. Dow’s business may be negatively impacted by this loss of operating diversity, including the purchasing power associated with operating as part of a larger organization. In addition, portions of Dow’s business were formerly part of Historical DuPont, which may be impacted by potential disruptions as a result of their transition to be a part of Dow and to the loss or dilution of their brand identities.

In addition, the financial information for Historical Dow that is incorporated by reference herein from the pertinent pages of Historical Dow’s financial statements, and the notes thereto, that are filed as Exhibits 99.2 and 99.3 to the Form 10 reflect the business of Historical Dow and not Dow’s business as it will be constituted following the separation and distribution, including after giving effect to the Internal Reorganization and Business Realignment. As a result, these historical financial statements may not be a reliable indicator of Dow’s financial condition or results of operations.

The Separation and Distribution

The separation and distribution of Dow is the first step in DowDuPont’s intended separation of its agriculture, materials science, and specialty products divisions into three independent, publicly traded companies.

On September 12, 2017, the DowDuPont board of directors announced the composition of the materials science business, Dow, which is expected to be the first business separated from DowDuPont, and will be comprised of DowDuPont’s Performance Materials & Coatings, Industrial Intermediates & Infrastructure and Packaging & Specialty Plastics (including Historical DuPont’s ethylene and ethylene copolymers businesses (other than its ethylene acrylic elastomers business)) segments.

On [●], the DowDuPont board of directors approved the distribution of all of the then issued and outstanding shares of common stock of Dow NewCo, the newly formed holding company for Dow that at the time of the distribution will hold DowDuPont’s materials science business, to DowDuPont stockholders on the basis of [●] shares of Dow common stock for every [●] shares of DowDuPont common stock held on [●], the record date for

10

Table of Contents

the distribution. As a result of the distribution, Dow will become an independent, publicly traded company. The distribution is intended to be generallytax-free to DowDuPont stockholders for U.S. federal income tax purposes, except for any cash received in lieu of fractional shares.

The distribution is subject to the satisfaction or waiver of certain conditions. The DowDuPont board of directors (and, following the distribution of Dow, with respect to the distribution of Corteva, the New DuPont board of directors) has the discretion to abandon one or both of the intended distributions and to alter the terms of each distribution. See the section entitled “The Distribution—Conditions to the Distribution.” As a result, Dow cannot provide any assurances that either distribution will be completed.

Internal Reorganization

In advance of the distribution, DowDuPont will undertake the Internal Reorganization and Business Realignment so that (1) Dow will hold, directly or indirectly, the entities, assets and liabilities associated with DowDuPont’s materials science business, which includes DowDuPont’s Performance Materials & Coatings, Industrial Intermediates & Infrastructure and Packaging & Specialty Plastics (including Historical DuPont’s ethylene and ethylene copolymers businesses (other than its ethylene acrylic elastomers business)) segments; (2) Corteva will hold, directly or indirectly, DowDuPont’s agriculture business and (3) New DuPont will hold, directly or indirectly, the specialty products business. See “Merger, Intended Separations, Reorganization and Financial Statements—Internal Reorganization” and “Dow’s Relationship with New DuPont and Corteva Following the Distribution—Separation Agreement” for further discussion.

Dow’s Relationship with New DuPont and Corteva Following the Distribution

Substantially simultaneously with the distribution, Dow will enter into a separation and distribution agreement with DowDuPont and Corteva, which is referred to in this information statement as the “separation agreement,” to effect the separation (including the Internal Reorganization and Business Realignment) and provide a framework for Dow’s relationship with New DuPont and Corteva after the separation and distribution. In connection with the separation and distribution, Dow will also enter into various other agreements with New DuPont and Corteva, including a tax matters agreement, an employee matters agreement, intellectual property cross-license agreements, trademark license agreements and certain services, manufacturing, supply and real estate-related agreements. These agreements will collectively provide for the terms of the allocation among Dow, New DuPont and Corteva of the assets, liabilities and obligations of DowDuPont and its subsidiaries (including investments, property and employee benefits andtax-related assets and liabilities) attributable to the periods prior to, at and after Dow’s and Corteva’s respective separations, and will govern certain relationships among Dow, New DuPont and Corteva after the separation and distribution. For a discussion of these arrangements, see the sections entitled “Risk Factors—Risks Related to the Separation” and “Dow’s Relationship with New DuPont and Corteva Following the Distribution.”

Regulatory Approvals

Dow must complete the necessary registration under U.S. federal securities laws of the Dow common stock to be issued in the distribution. Dow must also complete the applicable listing requirements of the NYSE for such shares.

Other than these requirements, Dow does not believe that any other material governmental or regulatory filings or approvals will be necessary to consummate the distribution.

DowDuPont stockholders will not have any appraisal rights in connection with the distribution.

11

Table of Contents

Corporate Information

Dow’s principal executive offices are located at 2211 H.H. Dow Way, Midland, Michigan 48674. Dow’s telephone number is (989)636-1000.

12

Table of Contents

SUMMARY OF THE SEPARATION AND DISTRIBUTION

The following is a summary of the material terms of the separation, distribution and other related transactions.

Distributing company | DowDuPont Inc. |

Distributed company | Dow Holdings Inc., a Delaware corporation and a wholly owned subsidiary of DowDuPont that will be the holding company for DowDuPont’s materials science business. Following the distribution, Dow NewCo will be an independent, publicly traded company. |

Distribution ratio | Each DowDuPont stockholder will receive [●] shares of Dow common stock for every [●] shares of DowDuPont common stock held on [●], the record date for the distribution. DowDuPont stockholders may also receive cash in lieu of any fractional shares, as described below. |

Distributed securities | In the distribution, DowDuPont will distribute to DowDuPont stockholders all of the then issued and outstanding shares of Dow common stock. Following the separation and distribution, Dow will be a separate company, and the remaining company, which is referred to herein as New DuPont, will not retain any ownership in Dow. |

| The actual number of shares of Dow common stock that will be distributed will depend on the number of shares of DowDuPont common stock outstanding on the record date. |

| Immediately following the distribution, DowDuPont stockholders will own shares in both Dow and New DuPont. |

Fractional shares | DowDuPont will not distribute any fractional shares of Dow common stock. Instead, if you are a registered holder, [●], the distribution agent, will aggregate all fractional shares that would have otherwise been issued in the distribution into whole shares and sell the whole shares in the open market at prevailing market prices on behalf of all DowDuPont stockholders entitled to receive a fractional share. The distribution agent will then distribute the aggregate cash proceeds of the sales, net of brokerage fees and other costs, pro rata to those stockholders (net of any required withholding for taxes applicable to each stockholder) who otherwise would have been entitled to receive a fractional share in the distribution. DowDuPont stockholders who receive cash in lieu of fractional shares will not be entitled to any interest on amounts paid in lieu of fractional shares. Any cash received in lieu of fractional shares generally will be taxable to DowDuPont stockholders as described in the section entitled “Material U.S. Federal Income Tax Consequences of the Distribution.” |

Record date | The record date for the distribution is the close of business on [●]. |

13

Table of Contents

Distribution date | The anticipated distribution date is [●]. |

Distribution | On the distribution date, DowDuPont will issue shares of Dow common stock to all DowDuPont stockholders as of the record date based on the distribution ratio. The shares of Dow common stock will be issued electronically in direct registration or book-entry form and no certificates will be issued. |

| Commencing on or shortly following the distribution date, the distribution agent will mail to stockholders who hold their shares directly with DowDuPont (registered holders) a direct registration account statement that reflects the shares of Dow common stock that have been registered in their name. |

| For shares of DowDuPont stock that are held through a bank, the bank will credit the stockholder’s account with the Dow common stock they are entitled to receive in the distribution. |

| DowDuPont stockholders will not be required to make any payment, to surrender or exchange their shares of DowDuPont common stock or to take any other action to receive their shares of Dow common stock in the distribution. |

| If you are a DowDuPont stockholder on the record date and decide to sell your shares on or before the distribution date, you may choose to sell your DowDuPont common stock with or without your entitlement to receive Dow common stock in the distribution. Beginning on or shortly before the record date and continuing through the last trading day prior to the distribution, it is expected that there will be two markets in DowDuPont common stock: a“regular-way” market and an“ex-distribution” market. Shares of DowDuPont common stock that are traded in the“regular-way” market will trade with the entitlement to receive the Dow common stock that is distributed pursuant to the distribution. Shares that trade in the“ex-distribution” market will trade without the entitlement to receive the shares of Dow common stock distributed pursuant to the distribution. Consequently, if you sell your shares of DowDuPont common stock in the“regular-way” market on or prior to the last trading day prior to the distribution date, you will also be selling your right to receive Dow common stock in the distribution. |

Conditions to the distribution | The distribution is subject to the satisfaction of the following conditions, among other conditions described in this information statement: |

| • | the SEC having declared effective the Form 10 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), no stop order relating to the Form 10 being in effect, no proceedings seeking such a stop order being pending before or threatened by the SEC and this information statement having been distributed to DowDuPont stockholders; |

14

Table of Contents

| • | the listing of the Dow common stock on the NYSE having been approved, subject to official notice of issuance; |

| • | the DowDuPont board of directors having received an opinion from a nationally recognized provider of such opinions, to the effect that, following the distribution, Dow and DowDuPont will each be solvent and adequately capitalized, and that DowDuPont has adequate surplus under Delaware law to declare the dividend of Dow common stock; |

| • | the Internal Reorganization and Business Realignment as they relate to Dow having been effectuated prior to the distribution date; |

| • | the DowDuPont board of directors having declared the dividend of Dow common stock to effect the distribution and having approved the distribution and all related transactions, which approval may be given or withheld in the board’s absolute and sole discretion (and such declaration or approval not having been withdrawn); |

| • | DowDuPont having elected the individuals to be members of the Dow board of directors following the distribution, and certain directors as set forth in the separation agreement having resigned from the DowDuPont board of directors; |

| • | each of Dow, DowDuPont and Cortevaand each of their applicable subsidiaries having entered into all ancillary agreements to which it and/or any such subsidiary is contemplated to be a party; |

| • | no events or developments having occurred or existing that make it inadvisable to effect the distribution or that would result in the distribution and related transactions not being in the best interest of DowDuPont or its stockholders; |

| • | no order, injunction or decree by any governmental entity of competent jurisdiction or other legal restraint or prohibition preventing consummation of the distribution or any of the related transactions, including the transfers of assets and liabilities contemplated by the separation agreement, shall be pending, threatened, issued or in effect; |

| • | the receipt (i) by DowDuPont of an opinion of Skadden, Arps, Slate, Meagher & Flom LLP, in form and substance satisfactory to DowDuPont (in its sole discretion) (the “DowDuPont Tax Opinion”) and (ii) by Dow of an opinion of each of Weil, Gotshal & Manges LLP and Ernst & Young LLP, in form and substance satisfactory to Dow (in its sole discretion) (the “Dow Tax Opinions” and, together with the DowDuPont Tax Opinion, the “Tax Opinions”), each substantially to the effect that, among other things, the distribution, together with certain related transactions, will qualify as atax-free transaction under Section 355 and Section 368(a)(1)(D) of the Internal Revenue Code of 1986, as amended (the “Code”) for U.S. federal income tax purposes; and |

15

Table of Contents

| • | the Internal Revenue Service (“IRS”) not having revoked the IRS Ruling (as described in the section entitled “Risk Factors—Risks Related to the Separation”). |

| The fulfillment of these conditions does not create any obligation on DowDuPont’s part to effect the distribution, and the DowDuPont board of directors has the ability, in its sole discretion, to amend, modify or abandon the distribution and related transactions at any time prior to the distribution date. |

Stock exchange listing | Dow intends to file an application to list the shares of Dow common stock on the NYSE under the symbol “DOW.” |

| Dow anticipates that on or shortly before the record date, trading in shares of Dow common stock will begin on a “when-issued” basis and that this “when-issued” trading market will continue through the last trading day prior to the distribution date. See the section entitled “The Distribution—Trading Between the Record Date and Distribution Date.” |

Transfer agent | [●] |

Dow’s indebtedness | Dow expects to retain Historical Dow’s long-term indebtedness. For additional information relating to Dow’s anticipated indebtedness following the separation and distribution, see the section entitled “Description of Material Indebtedness.” |

Risks relating to Dow, ownership of Dow common stock and the distribution | Dow’s business is subject to both general and specific risks, including risks relating to Dow’s business, Dow’s relationship with New DuPont and Corteva following the separation and distribution and to Dow being a separate, publicly traded company. You should read carefully the section entitled “Risk Factors.” |

Tax considerations | Assuming the distribution, together with certain related transactions, qualifies as atax-free transaction for U.S. federal income tax purposes under Section 368(a)(1)(D) and Section 355 of the Code, no gain or loss will be recognized by DowDuPont stockholders, and no amount will be included in the income of a DowDuPont stockholder, upon the receipt of shares of Dow common stock pursuant to the distribution. However, any cash payments made in lieu of fractional shares will generally be taxable to the stockholder. For a more detailed description, see the section entitled “Material U.S. Federal Income Tax Consequences of the Distribution.” |

Certain agreements with DowDuPont and Corteva | Substantially simultaneously with the distribution, Dow will enter into the separation agreement with DowDuPont and Corteva to effect the separation and distribution and provide a framework for Dow’s relationship with New DuPont and Corteva after the separation and distribution, Dow also intends to enter into various other agreements with DowDuPont and Corteva, including a tax matters agreement, an |

16

Table of Contents

employee matters agreement, intellectual property cross-license agreements, trademark license agreements and certain services, manufacturing, supply and real-estate agreements. These agreements will provide, among other things, for the allocation among Dow, New DuPont and Corteva of the assets, liabilities and obligations of DowDuPont (including its investments, property and employee benefits andtax-related assets and liabilities) attributable to periods prior to, at and after Dow’s and Corteva’s respective separations from DowDuPont and will govern certain relationships among Dow, New DuPont and Corteva. For a discussion of these arrangements, see the section entitled “Dow’s Relationship with New DuPont and Corteva Following the Distribution.” |

17

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE SEPARATION AND DISTRIBUTION

What is Dow and why is DowDuPont separating its materials science business and distributing Dow common stock? | Prior to the completion of the Merger on August 31, 2017, Historical Dow was a standalone, publicly traded company, operating a global business that included agricultural sciences, consumer solutions, infrastructure solutions, performance materials and chemicals, and performance plastics segments. As a result of the Merger, Historical Dow became a subsidiary of DowDuPont. In connection with their entry into the merger agreement, Historical Dow and Historical DuPont announced their intention to pursue the separation of DowDuPont into three independent, publicly traded companies—one for each of the combined company’s agriculture, materials science and specialty products businesses, subject to the approval of the DowDuPont board of directors and any required regulatory approvals. |

| The separation and distribution of DowDuPont’s materials science business, Dow, is the first step in this process. In connection with the separation of DowDuPont’s materials science business, DowDuPont will undertake the Internal Reorganization and Business Realignment, such that, at the time of the distribution, Dow will hold, directly or indirectly, only DowDuPont’s materials science business. Dow NewCo is a newly formed holding company for Dow and the separation will be effected by way of a pro rata dividend of Dow common stock to DowDuPont stockholders. Following the separation and distribution, Dow will be a separate company, and the remaining company, New DuPont, will not retain any ownership interest in Dow. |

| Following the separation and distribution of Dow, it is expected that the separation of DowDuPont’s agriculture business will be completed through the pro rata distribution to stockholders of the remaining company, New DuPont, of all of the then issued and outstanding shares of common stock of Corteva. The separations of Dow and Corteva from DowDuPont and the distributions of Dow common stock and Corteva common stock are each intended to provide DowDuPont stockholders with equity investments in separate companies that will be able to focus their respective businesses, with Dow being a leading, pure-play materials science company. DowDuPont and Dow expect that the separation will result in enhanced long-term performance of each business for the reasons discussed in the sections entitled “The Distribution—Background of the Distribution” and “The Distribution—Reasons for the Separation and Distribution.” |

Why am I receiving this document? | Dow is delivering this document to you because you are a DowDuPont stockholder as of the close of business on [●], the record date for the distribution. As a DowDuPont stockholder as of the record date, you are entitled to receive [●] shares of Dow common stock for every [●] shares of DowDuPont common stock that you hold at the close of business on such date. This document will help |

18

Table of Contents

you understand how the separation and distribution will affect your investment in DowDuPont and your investment in Dow after the separation and distribution. |

What are the reasons for the separation? | The DowDuPont board of directors believes that the separation of DowDuPont into three independent, publicly traded companies through the separation of DowDuPont’s agriculture, materials science, and specialty products businesses is in the best interests of DowDuPont and its stockholders and is the best available opportunity to unlock the value of DowDuPont’s business. |

| The DowDuPont board of directors, in consultation with its advisory committees (as described in the section entitled “The Distribution—Background of the Distribution”), considered a wide variety of factors in evaluating the planned separations and distributions and in deciding to proceed with the distribution of Dow, including the risk that one or more of the distributions is abandoned and not completed. Among other things, the DowDuPont board of directors and its advisory committees considered the following potential benefits of the separations and distributions: |

| • | Attractive Investment Profile.The creation of separate companies with strong, focused businesses and each with a distinct financial profile and clear investment thesis is expected to drive significant long-term value for all stockholders and also to reduce the complexities surrounding investor understanding, enabling investors to invest in each company separately based on its distinct characteristics. |

| • | Enhanced Means to Evaluate Financial Performance.Investors should be better able to evaluate the business condition, strategy and financial performance of each company within the context of its industry and markets. It is expected that, over time following the completion of the separations, the aggregate market value of Dow, Corteva and New DuPont will be higher, on a fully distributed basis and assuming the same market conditions, than if DowDuPont were to remain under its current configuration. |

| • | Distinct Position.The separations are expected to create three independent companies with tailored growth strategies and differentiated technologies, resulting in: Dow, a leading global materials science company that will be alow-cost, innovation-driven leader; Corteva, a leading global agricultural company with the most comprehensive and diverse portfolio in the industry; and New DuPont, a leading global specialty products company that will be a technology driven innovation leader. Each company will provide investors with a distinct investment option that may be more attractive to current investors and will allow the company to attract different investors than the current investment option available to DowDuPont stockholders of one combined company. |

19

Table of Contents

| • | Focused Capital Allocation. Each independent, publicly traded company will have a capital structure that is expected to be best suited to its specific needs and will be able to make capital allocation decisions that better align with its streamlined business. In addition, after the separation, the respective businesses within each company will no longer need to compete internally for capital and other corporate resources with businesses allocated to another company. |

| • | Ability to Adapt to Industry Changes. Each company is expected to be able to maintain a sharper focus on its core business and growth opportunities, which will allow each company to respond better and more quickly to developments in its industry. |

| • | Dedicated Management Team with Enhanced Strategic Focus. Each company’s management team will be able to design and implement corporate policies and strategies that are tailored to such company’s specific business characteristics and to focus on maximizing the value of its business. |

| • | Improved Management Incentive Tools. The separation will permit the creation of equity securities, including options and restricted stock units, for each publicly traded company with values more closely linked to the performance of such company’s business than would be readily available under the current configuration of businesses within DowDuPont as a single public company. The DowDuPont board of directors believes such equity-based compensation arrangements should provide enhanced incentives for performance and improve the ability for each publicly traded company to attract, retain and motivate qualified personnel. |

| • | Direct Access to Capital Markets and Ability to Pursue Strategic Opportunities.Each company’s business will have direct access to the capital markets, and is expected to be better situated to pursue future acquisitions, joint ventures and other strategic opportunities as well as internal expansion that is more closely aligned with such company’s strategic goals and expected growth opportunities. |

The DowDuPont board of directors also considered a number of potentially negative factors, including the loss of synergies and joint purchasing power from ceasing to operate as part of a larger, more diversified company, risks relating to the creation of a new public company, such as increased costs from operating as a separate public company, potential disruptions to the businesses and loss or dilution of brand identities, possible increased administrative costs andone-time separation costs, restrictions on each company’s ability to pursue certain opportunities that may have otherwise been available in order to preserve thetax-free nature of the distributions and related transactions for U.S. federal income tax purposes, the fact that each company will be less diversified than the current configuration of |

20

Table of Contents

DowDuPont’s businesses prior to the separations and distributions, and the potential inability to realize the anticipated benefits of the separations. |

| The DowDuPont board of directors concluded that the potential benefits of pursuing each separation and each distribution outweighed the potentially negative factors in connection therewith. For more information, see the sections entitled “The Distribution—Reasons for the Separation and Distribution” and “Risk Factors.” |

| The DowDuPont board of directors also considered these potential benefits and potentially negative factors in light of the risk that one or more of the distributions is abandoned or otherwise not completed, resulting in DowDuPont separating into fewer than the intended three separate publicly traded companies. The DowDuPont board of directors believes that the potential benefits to DowDuPont stockholders discussed above apply to the separation of each of the intended three businesses and that the creation of each independent company, with its distinctive business and capital structure and ability to focus on its specific growth plan, will provide DowDuPont stockholders with greater long-term value than retaining one investment in the combined company. |

Why is the separation of Dow structured as a distribution? | DowDuPont currently believes the separation by way of distribution is the most efficient way to separate its materials science business from DowDuPont for various reasons, including that a separation will (i) offer a high degree of certainty of completion in a timely manner, lessening disruption to current business operations; (ii) provide a high degree of assurance that decisions regarding Dow’s capital structure will align with its business objectives and provide the continued financial flexibility and financial stability to support its long-term growth and generate stockholder returns; and (iii) generally be atax-free distribution of shares of Dow common stock to DowDuPont stockholders for U.S. federal income tax purposes (except for any cash received in lieu of fractional shares). DowDuPont believes that atax-free separation will enhance the value of both DowDuPont and Dow. See the section entitled “The Distribution—Reasons for the Separation and Distribution.” |

What do I have to do to participate in the | You are not required to take any action to receive your shares of Dow common stock, although you are urged to read this entire document carefully.No approval of the distribution by DowDuPont stockholders is required and DowDuPont is not seeking your approval.Therefore, Dow is not asking for a proxy to vote on the separation or the distribution, and Dow requests that you do not send Dow a proxy.You will not be required to pay anything for the shares of Dow common stock you will receive in the distribution nor will you be required to surrender or exchange any shares of DowDuPont common stock to participate in the distribution. |

21

Table of Contents

What is the record date for the distribution? | DowDuPont will determine record ownership as of the close of business on [●], which Dow refers to as the “record date.” |

What will I receive in the distribution? | If you are a DowDuPont stockholder as of the record date, you will receive [●] shares of Dow common stock for every [●] shares of DowDuPont common stock you held on the record date, as well as a cash payment in lieu of any fractional shares (as discussed below). You will receive only whole shares of Dow common stock in the distribution. For a more detailed description, see the section entitled “The Distribution.” |

How will fractional shares be treated in the distribution? | No fractional shares of Dow common stock will be distributed. Consequently, you will not receive any fractional shares of Dow common stock and instead will receive a cash payment for any fractional shares you would otherwise have been entitled to receive in the distribution. |

| DowDuPont has engaged [●] as its distribution agent. The distribution agent will aggregate all fractional shares that would have otherwise been issued in the distribution into whole shares and will sell the whole shares in the open market at prevailing market prices on behalf of all DowDuPont stockholders entitled to receive a fractional share. The distribution agent will then distribute the aggregate cash proceeds of the sales, net of brokerage fees and other costs, pro rata to those stockholders (net of any required withholding for taxes applicable to such stockholder). You will not be entitled to any interest on the amount of payment made to you in lieu of fractional shares. |

Will the number of DowDuPont shares I own change as a result of the distribution? | No, the number of shares you own will not change as a result of the distribution. Immediately following the distribution, you will hold the same number of shares of DowDuPont, which will now be New DuPont, that you held immediately prior to the distribution. Your proportionate interest will also not change, so you will own the same proportionate amount of New DuPont immediately following the separation and distribution that you owned of DowDuPont immediately prior to the separation and distribution. |

How many shares of Dow common stock will be distributed? | The actual number of shares of Dow common stock that will be distributed will depend on the number of shares of DowDuPont common stock outstanding on the record date. The shares of Dow common stock that are distributed will constitute all of the then issued and outstanding shares of Dow common stock immediately prior to the distribution and DowDuPont will not retain any ownership interest in Dow following the distribution. For more information on the shares being distributed, see the section entitled “Description of Dow’s Capital Stock.” |

22

Table of Contents

When will the distribution occur? | It is expected that the distribution will be effected prior to the opening of trading on the NYSE on [●], which Dow refers to as the “distribution date,” subject to the satisfaction or waiver of certain conditions. On or shortly after the distribution date, the whole shares of Dow common stock will be credited in book-entry accounts for each stockholder entitled to receive shares of Dow common stock in the distribution. No share certificates will be issued with respect to the shares distributed in the distribution. Dow expects DowDuPont’s distribution agent to take approximately two weeks after the distribution date to fully distribute to stockholders any cash they are entitled to receive in lieu of fractional shares. See “—How will I receive my shares of Dow common stock?” for more information. |

If I sell my shares of DowDuPont common stock on or before the distribution date, will I still be entitled to receive shares of Dow common stock in the distribution? | If you are a DowDuPont stockholder on the record date and decide to sell your shares before the distribution date, you may choose to sell your DowDuPont common stock with or without your entitlement to receive Dow common stock in the distribution. Beginning on or shortly before the record date and continuing through the distribution, it is expected that there will be two markets in DowDuPont common stock: a“regular-way” market and an“ex-distribution” market. Shares of DowDuPont common stock that are traded in the“regular-way” market will trade with the entitlement to receive the Dow common stock that is distributed pursuant to the distribution. Shares that trade in the“ex-distribution” market will trade without the entitlement to receive the shares of Dow common stock distributed pursuant to the distribution. Consequently, if you sell your shares of DowDuPont common stock in the“regular-way” market on or prior to the last trading day prior to the distribution date, you are also selling your right to receive Dow common stock in the distribution. |