Table of Contents

As filed with the Securities and Exchange Commission on September 8, 2021

File No. 000-56274

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Amendment No. 4

to

FORM 10

GENERAL FORM FOR REGISTRATION OF SECURITIES

PURSUANT TO SECTION 12(b) OR 12(g) OF

THE SECURITIES EXCHANGE ACT OF 1934

VINEBROOK HOMES TRUST, INC.

(Exact name of registrant as specified in its charter)

| Maryland | 83-1268857 | |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification Number) | |

| 300 Crescent Court, Suite 700, Dallas, Texas | 75201 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (214) 276-6300

Copies to:

Brian Mitts Chief Financial Officer, Assistant Secretary and Treasurer VineBrook Homes Trust, Inc. 300 Crescent Court, Suite 700 Dallas, Texas 75201 (214) 276-6300 | Charlie Haag Justin Reinus Winston & Strawn LLP 2121 North Pearl Street, Suite 900 Dallas, Texas 75201 (214) 453-6500 |

Securities to be registered pursuant to Section 12(b) of the Act:

Title of each class to be so registered | Name of each exchange on which each class is to be registered | |

| None | None |

Securities to be registered pursuant to Section 12(g) of the Act:

Class A Common Stock, par value $0.01 per share

(Title of class)

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☑ | Smaller reporting company | ☑ | |||

| Emerging growth company | ☑ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Table of Contents

Table of Contents

VineBrook Homes Trust, Inc. (“we”, “us”, “our”, or the “Company”) is filing this fourth amendment, dated September 8, 2021 (“Amendment No. 4”), to its registration statement on Form 10, initially filed with the U.S. Securities and Exchange Commission on April 30, 2021 (the “Registration Statement”), solely to amend and restate the information in Item 1 of the Registration Statement and the first, second and third amendments thereto, filed on June 14, 2021 (“Amendment No. 1”), June 28, 2021 (“Amendment No. 2”) and July 27, 2021 (“Amendment No. 3”), respectively pursuant to Rule 12b-15 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

The Registration Statement, as amended, was automatically effective sixty days after it was initially filed with the Securities and Exchange Commission and the Company is currently subject to the requirements of the Exchange Act and the rules promulgated thereunder.

This Amendment No. 4 should be read in conjunction with the Registration Statement, Amendment No. 1, Amendment No. 2 and Amendment No. 3, and continues to speak as of the dates thereof. Accordingly, this Amendment No. 4 does not reflect events occurring after the filing of the Registration Statement, Amendment No. 1, Amendment No. 2 and Amendment No. 3, or modify or update any related or other disclosures or amend any items included therein, other than Item 1 as set forth herein.

1

Table of Contents

We are filing this Form 10, as amended, to register shares of our Class A common stock, par value $0.01 per share (our “common stock”), pursuant to Section 12(g) of the Exchange Act. We are subject to the registration requirements of Section 12(g) of the Exchange Act because as of December 31, 2020, the aggregate value of our assets exceeded the applicable threshold and our common stock was held of record by 2,000 or more persons. As a result of the registration of our common stock pursuant to the Exchange Act, following the effectiveness of this Form 10 (as amended), we will be subject to the requirements of the Exchange Act and the rules promulgated thereunder. In particular, we will be required to file Quarterly Reports on Form 10-Q, Annual Reports on Form 10-K, and Current Reports on Form 8-K and otherwise comply with the disclosure obligations of the Exchange Act applicable to issuers filing registration statements to register a class of securities pursuant to Section 12(g) of the Exchange Act.

General

VineBrook Homes Trust, Inc. (“VineBrook,” the “Company,” “we,” “us,” or “our”) was formed on July 16, 2018 as a Maryland corporation, and elected to be taxed as a real estate investment trust (“REIT”) beginning with its taxable year ended December 31, 2018. We are focused on acquiring, developing, renovating, leasing and operating single-family rental (“SFR”) properties primarily located in the midwestern, heartland and southern U.S. markets. Substantially all of our assets are owned by, and our operations are conducted through, our operating partnership, VineBrook Homes Operating Partnership, L.P. (our “Operating Partnership”). This structure is referred to as an Umbrella Partnership REIT or “UPREIT” structure. We own the majority of the issued and outstanding limited partnership interests of our Operating Partnership. As of March 31, 2021, we, through our Operating Partnership, owned and operated a portfolio of over 13,500 SFR assets located in 16 states (our “Portfolio”).

We are externally managed by our adviser, NexPoint Real Estate Advisors V, L.P. (our “Adviser”), through an amended and restated advisory agreement, dated May 4, 2020, between our Adviser and us (as amended from time to time, the “Advisory Agreement”), subject to the authority of our board of directors (our “Board”) over the management of the Company. Our Adviser’s responsibilities include, among other duties, recommending distributions to our Board, preparing our quarterly and annual consolidated financial statements in accordance with generally accepted accounting principles (“GAAP”), managing our annual audit, developing and maintaining appropriate internal accounting controls, maintaining our REIT status, recommending to the pricing committee of our board of directors our net asset value (“NAV”), processing purchases and redemptions of shares of our common stock, preparing public filings, preparing our tax filings, raising capital for us and procuring debt financing. See Item 5. “Directors and Executive Officers—Our Adviser—Advisory Agreement” for additional information regarding the terms of the Advisory Agreement. Additionally, certain employees of our Adviser serve as some of our directors and executive officers. For additional information regarding our Adviser’s key employees, see Item 5. “Directors and Executive Officers—Our Adviser—Key Employees of Our Adviser.”

Our Portfolio is managed by VineBrook Homes, LLC (our “Manager”), pursuant to the terms of a management agreement, dated November 1, 2018 (as amended from time to time, the “Original Management Agreement”), among our Manager and various wholly owned subsidiaries of our Operating Partnership that own the SFR properties and the amended and restated side letter, dated July 31, 2020, among our Manager, our Operating Partnership and other parties thereto (as amended from time to time, the “Side Letter”). Our Manager entered into two additional management agreements (as amended from time to time, the

2

Table of Contents

“TrueLane Management Agreements”) with other wholly owned subsidiaries of our Operating Partnership in connection with our acquisition of a bulk portfolio of SFR properties on September 30, 2019 (See “—Subsequent Material Acquisitions—TrueLane Acquisition” below for additional information). The TrueLane Management Agreements are on the same terms as the Original Management Agreement and are also subject to the terms of the Side Letter. Our Manager entered into an additional management agreement (as amended from time to time, the “Conrex Management Agreement”) with other wholly owned subsidiaries of our Operating Partnership in connection with our acquisitions of a bulk portfolio of SFR properties on January 22, 2021 and March 1, 2021 (See “—Subsequent Material Acquisitions—Conrex Acquisitions” below for additional information). The Conrex Management Agreement is on the same terms as the Original Management Agreement and is also subject to the terms of the Side Letter. From time to time, our Manager may enter into one or more additional management agreements with other wholly owned subsidiaries of our Operating Partnership in connection with future acquisitions of SFR properties on the same terms as the Original Management Agreement. The Original Management Agreement, the TrueLane Management Agreements, the Conrex Management Agreement and any future management agreements are collectively referred to herein as the “Management Agreements.” See Item 7. “Certain Relationships and Related Transactions, and Director Independence—Transactions with Related Persons—Management Agreements and Side Letter” for additional information regarding the terms of the Management Agreements.

Our Manager is responsible for the day-to-day management of the properties, renovating the homes, leasing the properties, managing tenant situations, collecting rents, paying operating expenses, managing maintenance issues, accounting for each property using GAAP, and other responsibilities customary for the management of SFR properties. In addition, subject to the limitations set forth in our Operating Partnership’s Amended and Restated Agreement of Limited Partnership (as amended from time to time, the “OP LPA”) and oversight from our Operating Partnership’s investment committee (the “Investment Committee”), our Manager is primarily responsible for the identification of potential SFR properties and the acquisition and disposition of SFR properties.

Our principal executive offices are located at 300 Crescent Court, Suite 700, Dallas, Texas 75201. Our telephone number is (214) 276-6300.

The Formation Transaction

On July 18, 2018, our Operating Partnership and its subsidiaries executed definitive agreements (the “Purchase Agreements”) to acquire the Initial Portfolio (defined below) through a series of restructurings and acquisitions of SFR properties from numerous partnerships and limited liability companies (such partnerships and limited liability companies are collectively referred to herein as the “VineBrook Companies,” and such acquisitions and related transactions are referred to herein as the “Formation Transaction”). The Formation Transaction closed on November 1, 2018, at which time we, through our Operating Partnership, acquired the equity interest in six special purpose entities (“SPEs”), which collectively owned approximately 4,129 SFR assets located in Ohio, Kentucky and Indiana (the “Initial Portfolio”) for a total purchase price of $330.2 million, including closing and financing costs of approximately $6.0 million. In connection with the Formation Transaction, NexPoint Real Estate Opportunities, LLC (“NREO”), an affiliate of NexPoint Advisors, L.P. (“NexPoint”), contributed an SPE which owned a portfolio of SFR properties located in Cincinnati included in the Initial Portfolio and cash in exchange for approximately $70.7 million in Class A units of our Operating Partnership (“OP Units”).

3

Table of Contents

Because we acquired substantially all of the VineBrook Companies’ assets and liabilities by purchasing (via a combination of cash and the issuance OP Units) all general partnership interests, limited partnership interests and equity interests of the VineBrook Companies in connection with the Formation Transaction, we consider the VineBrook Companies on a consolidated basis to be our predecessor.

Subsequent Material Acquisitions

TrueLane Acquisition

On September 30, 2019, we, through our Operating Partnership, acquired a portfolio of 954 SFR properties from an unaffiliated third-party for $73 million (the “TrueLane Acquisition”). The TrueLane Acquisition expanded our footprint to four additional active markets, including Pittsburgh, Pennsylvania, Jackson, Mississippi, Omaha, Nebraska and Little Rock, Arkansas. In connection with the TrueLane Acquisition, our Manager entered into the TrueLane Management Agreements with other wholly owned subsidiaries of our Operating Partnership. The TrueLane Management Agreements are on the same terms as the Original Management Agreement and are also subject to the terms of the Side Letter (See “—General” above and Item 7. “Certain Relationships and Related Transactions, and Director Independence—Transactions with Related Persons—Management Agreements and Side Letter” for additional information regarding the terms of the Management Agreements).

Conrex Acquisitions

On January 22, 2021, we, through our Operating Partnership, acquired a portfolio of 1,725 SFR properties from an unaffiliated third-party for $228.0 million (the “Conrex I Acquisition”). In addition to the $228.0 million purchase price, in connection with the Conrex I Acquisition, we paid an approximately $2.5 million acquisition fee to the Manager which was capitalized as a transaction cost. The Conrex I Acquisition expanded our footprint to seven additional markets in Alabama, Georgia, North Carolina and South Carolina. In connection with the Conrex I Acquisition, our Manager entered into the Conrex Management Agreement with wholly owned subsidiaries of our Operating Partnership. The Conrex Management Agreement is on the same terms as the Original Management Agreement and is also subject to the terms of the Side Letter (See “—General” above and Item 7. “Certain Relationships and Related Transactions, and Director Independence—Transactions with Related Persons—Management Agreements and Side Letter” for additional information regarding the terms of the Management Agreements). The Conrex I Acquisition was contemplated as one transaction and consisted of a portfolio acquisition and a simultaneous bulk disposition of approximately 8.5% of the homes in the portfolio for approximately $28 million to BSFR I Owner, L.P., an affiliate of the sellers (“BSFR I Owner”). The Company’s acquisition of the portfolio was not contingent on the simultaneous disposition but the disposition was contingent upon the Company’s acquisition. The purchase and bulk disposition was simultaneous, resulted in no GAAP gain or loss and references herein to the portfolio acquired in the Conrex I Acquisition refer only to homes actually acquired (i.e., net of the simultaneous disposition).

On March 1, 2021, we, through our Operating Partnership, acquired a portfolio of 2,170 SFR properties from an unaffiliated third-party for $282.9 million (the “Conrex II Acquisition”). In addition to the $282.9 million purchase price, in connection with the Conrex II Acquisition, we paid an approximately $3.0 million acquisition fee to the Manager which was capitalized as a transaction cost. The Conrex II Acquisition further expanded our presence in the midwest, heartland and southeast U.S. markets. In connection with the Conrex II Acquisition, our Manager entered into an amendment to the Conrex Management Agreement with wholly owned subsidiaries of our Operating Partnership. The Conrex Management Agreement is on the same terms as the Original Management Agreement and is also subject to the terms of the Side Letter (See “—General” above and Item 7. “Certain Relationships and Related Transactions, and Director Independence—Transactions with Related Persons—Management Agreements and Side Letter” for additional information regarding the terms of the Management Agreements). The Conrex II Acquisition was contemplated as one transaction and consisted of a portfolio acquisition and a simultaneous bulk disposition of approximately 4.0% of the homes in the portfolio for approximately $16.6 million to BSFR I Owner. The Company’s acquisition of the portfolio was not contingent on the simultaneous disposition but the disposition was contingent upon the Company’s acquisition. The purchase and bulk disposition was simultaneous, resulted in no GAAP gain or loss and references herein to the portfolio acquired in the Conrex II Acquisition refer only to homes actually acquired (i.e., net of the simultaneous disposition).

We entered into a 120-day agreement with an affiliate of Brookfield Asset Management for the management of a subset of homes purchased in the Conrex I Acquisition and Conrex II Acquisition on a transitional basis, which was mutually terminated early on April 27, 2021.

4

Table of Contents

The portfolio acquired in the Conrex I Acquisition had an occupancy rate of 96.5% and weighted average monthly effective rent per occupied home of $1,167 as of January 22, 2021. The portfolio acquired in the Conrex II Acquisition had an occupancy rate of 89.2% and weighted average monthly effective rent per occupied home of $1,158 as of March 1, 2021. At the time of the acquisition, 93% of the homes we acquired in the Conrex I Acquisition and the Conrex II Acquisition had in place leases and 99.6% of homes were generally in good condition with 99.6% being recently renovated and had minimal deferred maintenance. We intend to renovate less than 0.4% of the homes acquired and to sell less than 0.1% of the homes acquired.

The following table provides a summary of the number of homes, occupancy rate and average rent on a market basis of the 1,725 homes we acquired in the Conrex I Acquisition as of January 22, 2021:

| # of Homes | Occupancy | Avg Rent | ||||||||||

Birmingham | 309 | 91.6 | % | 1,104 | ||||||||

Columbia | 379 | 97.6 | % | 1,211 | ||||||||

Indianapolis | 276 | 98.2 | % | 1,196 | ||||||||

Augusta | 182 | 96.2 | % | 994 | ||||||||

Cincinnati | 117 | 98.3 | % | 1,270 | ||||||||

Dayton | 64 | 98.4 | % | 1,221 | ||||||||

Greenville | 138 | 99.3 | % | 1,228 | ||||||||

Kansas City | 130 | 94.6 | % | 1,164 | ||||||||

Triad | 52 | 98.1 | % | 1,159 | ||||||||

Columbus | 65 | 96.9 | % | 1,214 | ||||||||

Huntsville | 13 | 100.0 | % | 1,024 | ||||||||

|

|

|

|

|

| |||||||

Total | 1,725 | 96.5 | % | 1,167 | ||||||||

The following table provides a summary of the number of homes, occupancy rate and average rent on a market basis of the 2,170 homes we acquired in the Conrex II Acquisition as of March 1, 2021:

| # of Homes | Occupancy | Avg Rent | ||||||||||

Birmingham | 438 | 86.3 | % | 1,104 | ||||||||

Columbia | 305 | 88.5 | % | 1,191 | ||||||||

Indianapolis | 217 | 90.3 | % | 1,151 | ||||||||

Augusta | 186 | 91.4 | % | 990 | ||||||||

Cincinnati | 252 | 96.4 | % | 1,271 | ||||||||

Dayton | 125 | 95.2 | % | 1,244 | ||||||||

Greenville | 46 | 87.0 | % | 1,228 | ||||||||

Kansas City | 164 | 82.9 | % | 1,201 | ||||||||

Triad | 35 | 80.0 | % | 1,191 | ||||||||

Columbus | 81 | 91.4 | % | 1,196 | ||||||||

Huntsville | 121 | 95.0 | % | 1,074 | ||||||||

St. Louis | 31 | 80.6 | % | 1,188 | ||||||||

Montgomery | 61 | 85.2 | % | 1,061 | ||||||||

Jackson | 108 | 82.4 | % | 1,220 | ||||||||

|

|

|

|

|

| |||||||

Total | 2,170 | 89.2 | % | 1,158 | ||||||||

We included contractual provisions in both the acquisition agreements under which the sellers are obligated to provide us the books and records of the entities purchased, which would have allowed us to comply with Rule 3-14 by completing and auditing the required financial statements. We have, to date, exhausted all practical avenues by which to obtain the information necessary to provide Rule 3-14 financial statements. Consequently, we believe the essential information for the delivery of Rule 3-14 financial statements cannot be reasonably obtained. There is no affiliation between us and the sellers.

Our Adviser

Our Adviser is an affiliate of NexPoint Real Estate Advisors, L.P. (“NREA”), which is wholly owned by NexPoint. NREA was formed to manage real estate investments for NexPoint managed companies, funds and accounts. The NREA real estate team is led by Matt McGraner and Brian Mitts. Pursuant to the Advisory Agreement, our Adviser manages our business operations, subject to the authority of our Board. Additionally, certain employees of our Adviser serve on our Board, as our officers and on the Investment Committee. The Investment Committee was established pursuant to the terms of the OP LPA and is responsible for making decisions and approvals with respect to asset acquisitions and asset dispositions that exceed a pre-determined amount. The Investment Committee is comprised of three individuals, one appointed by our Adviser and two appointed by our Manager (so long as any Management Agreement remains in place). Currently, Matt McGraner, Dana Sprong and Ryan McGarry are members of the Investment Committee. In accordance with the OP LPA, the Investment Committee has delegated authority to the Manager to acquire or dispose of a limited number of homes. Acquisitions must satisfy the approved guidelines set forth in the Management Agreements, which may be updated from time to time.

For additional information regarding the Adviser’s key employees, see Item 5. “Directors and Executive Officers—Our Adviser—Key Employees of Our Adviser.”

5

Table of Contents

Our Manager

As part of the acquisition of the Initial Portfolio, the entity that managed the SFR properties owned by our predecessor since its inception in 2007 (the “Historical VineBrook Manager”) was not acquired. Instead, the beneficial owners of the Historical VineBrook Manager, which include Dana Sprong, Ryan McGarry, Dan Bathon and Tom Silvia (collectively, the “VineBrook Executives”) formed our Manager for the purpose of managing our Portfolio as an external manager.

Our Manager is led by Dana Sprong, Ryan McGarry, and Graham Strong and has a team of more than 350 professionals with experience in real estate investment, property management operations, construction management and comprehensive financial and metric-focused reporting. The VineBrook Executives have operated in the workforce SFR market since the inception of the VineBrook Companies in 2007, participating in several large acquisitions and financing transactions, demonstrating the ability to identify consolidation and growth opportunities and to subsequently integrate new properties into an existing portfolio. Pursuant to the Management Agreements, our Manager is generally the sole and exclusive manager for our properties (subject to the terms of the Management Agreements), responsible for managing, coordinating and supervising the ordinary and usual business and affairs pertaining to the renovation, operation, maintenance, leasing, and management of properties in an efficient manner satisfactory to us and in compliance with the Management Agreements. In addition, our Manager is primarily responsible for the identification of potential SFR properties and the acquisition and disposition of SFR properties, subject to oversight from the Investment Committee and the terms of the OP LPA. Additionally, certain employees of the Manager serve on our Board, as our officers and on the Investment Committee. From time to time, we may use an unaffiliated third party manager for limited periods to, for example, provide management while our Manager sets up an operations team in a market or to manage homes we acquired as part of a larger portfolio acquisition but plan to sell.

For additional information regarding our Manager’s key employees, see Item 5. “Directors and Executive Officers—Our Manager—Key Employees of Our Manager.”

Under the terms of the Side Letter, at any time, we and our Operating Partnership have the right and option (but not the obligation) to purchase all of the equity interests of our Manager, at a price calculated by a formula specified in the Side Letter (the “Call Right”). The purpose of the Call Right is to provide us, our Operating Partnership, and our and its respective permitted successors and assigns with the ability to perform the responsibilities and obligations of our Manager under the Management Agreements. It is not expected that the Call Right would be exercised, except in the event of our initial public offering or sale at our discretion. In addition, the equity interests of our Manager may not be transferred (directly or indirectly), or additional equity interests issued, without the consent of us and our Operating Partnership, which may be withheld in our discretion.

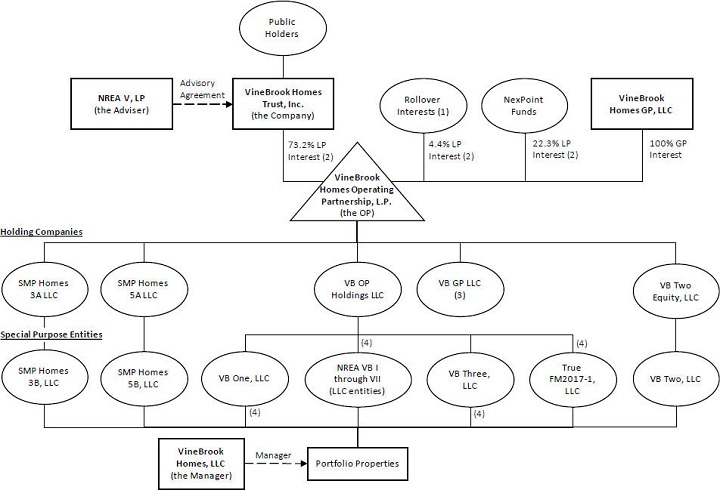

Our Ownership and Operation Structure

The following chart shows our current ownership structure and our relationship with our Adviser and our Manager.

6

Table of Contents

VineBrook REIT Structure Chart

| (1) | Also includes holdings of certain Company insiders. |

| (2) | Percentages may not total to 100% due to rounding. Percentages as of March 31, 2021. |

| (3) | VB GP LLC is the general partner for entities that are limited partnerships and subsidiaries of VB OP Holdings, LLC. VB OP Holdings LLC holds all of the limited partner interests for these limited partnerships. |

| (4) | One or more wholly owned intermediary entities are not displayed. |

7

Table of Contents

Our Portfolio

As of March 31, 2021, our homes average approximately 1,318 square feet with three bedrooms and one and a half bathrooms. Our homes benefit from high occupancy and low turnover rates due to our extensive renovation process and institutional management, generating stable, durable cash flows. Similarly, as of March 31, 2021, 93% of our Portfolio is comprised of standalone units, with only 7% of properties stemming from duplexes, triplexes, quad-plexes, villas, townhouses, courtyards and condominiums. As of March 31, 2021, 1,779 homes in our Portfolio (13% of our Portfolio) were unoccupied, including 1,331 recently purchased homes (10% of our Portfolio) in rehabilitation and 442 homes (3% of our Portfolio) in make-ready turnover. Vacant homes that have not undergone the Company’s rehabilitation program are categorized as “in rehabilitation.” While in rehabilitation, vacant homes undergo the Company’s initial rehabilitation program. Rehabilitated homes that are in between tenants are categorized as “make-ready turnover” until re-leased. While in the make-ready turnover category, homes are returned to their original rehabilitated state. Occupied homes, regardless of rehabilitation status, are categorized as “occupied.” As of March 31, 2021, the average length of leases in our Portfolio was 12 months and the average remaining length of leases in our Portfolio was seven months. We believe our turnover rate, or the rate, calculated as a percentage on an annualized basis, at which existing residents choose to not renew their lease upon expiration, is low (our renewal rate was 82.7% as of March 31, 2021) because of our institutional level of management, affordable pricing and available amenities not found in other SFR rental properties, including a large number of employees and 24/7 support. As of March 31, 2021, the average age of the homes in our Portfolio is 59 years, which we believe is materially similar to the average age of homes in the markets in which we operate.

The table below provides summary information regarding our Portfolio as of March 31, 2021:

Market | # of Homes | Portfolio Occupancy | Average Effective Rent | # of Stabilized Homes | Stabilized Occupany | Stabilized Average Monthly Rent | ||||||||||||||||||

Cincinnati | 2,738 | 92.9 | % | $ | 1,076 | 1,828 | 97.6 | % | $ | 1,066 | ||||||||||||||

Dayton | 2,432 | 93.3 | % | 961 | 2,097 | 98.2 | % | 940 | ||||||||||||||||

Columbus | 1,368 | 92.5 | % | 1,070 | 1,048 | 98.2 | % | 1,071 | ||||||||||||||||

St. Louis | 1,226 | 76.0 | % | 946 | 372 | 94.1 | % | 928 | ||||||||||||||||

Indianapolis | 1,059 | 89.6 | % | 1,070 | 403 | 96.8 | % | 976 | ||||||||||||||||

Birmingham | 759 | 87.1 | % | 1,126 | — | n/a | n/a | |||||||||||||||||

Columbia | 685 | 93.4 | % | 1,213 | — | n/a | n/a | |||||||||||||||||

Kansas City | 673 | 76.4 | % | 1,066 | 123 | 94.3 | % | 925 | ||||||||||||||||

Jackson | 494 | 58.9 | % | 1,040 | 46 | 93.5 | % | 1,079 | ||||||||||||||||

Memphis | 474 | 91.1 | % | 852 | 278 | 95.0 | % | 870 | ||||||||||||||||

Augusta | 374 | 86.6 | % | 998 | — | n/a | n/a | |||||||||||||||||

Milwaukee | 370 | 82.7 | % | 1,033 | 108 | 98.1 | % | 1,147 | ||||||||||||||||

Pittsburgh | 306 | 66.3 | % | 894 | 46 | 97.8 | % | 979 | ||||||||||||||||

Greenville | 190 | 90.5 | % | 1,242 | — | n/a | n/a | |||||||||||||||||

Little Rock | 137 | 54.7 | % | 822 | 33 | 100.0 | % | 885 | ||||||||||||||||

Huntsville | 134 | 95.5 | % | 1,144 | — | n/a | n/a | |||||||||||||||||

Omaha | 112 | 64.3 | % | 1,100 | 12 | 100.0 | % | 1,089 | ||||||||||||||||

Triad | 95 | 87.4 | % | 1,162 | — | n/a | n/a | |||||||||||||||||

Montgomery | 61 | 86.9 | % | 1,061 | — | n/a | n/a | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Sub-Total/Average | 13,687 | 87.0 | % | $ | 1,039 | 6,394 | 97.5 | % | $ | 1,001 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Held for Sale | 6 | n/a | n/a | n/a | n/a | n/a | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total/Average | 13,693 | 87.0 | % | $ | 1,039 | 6,394 | 97.5 | % | $ | 1,001 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Occupancy is calculated as the number of homes occupied as of the respective period end, divided by the total number of homes, expressed as a percentage. We use the definition of stabilized homes as established by the National Rental Home Council (the “NRHC”), a non-profit SFR home trade association. A stabilized home means a home that has had a rehabilitation completed and is either leased or 30 days have expired since the rehabilitation has been completed. In accordance with the NRHC definition of stabilized which allows management certain discretion in the inclusion of acquired homes, we currently do not include homes purchased with a tenant in place as stabilized until (1) we have owned them for an adequate period of time to allow for complete on-boarding to our operating platform and (2) the property has experienced tenant turnover at least once under our ownership, providing the opportunity for rehabilitation to meet our property standards. Since stabilized homes are expected to be held for at least one year, stabilized homes also excludes any assets held for sale. As of March 31, 2021, a total of 53.3% of our Portfolio was excluded from being a stabilized home, with 9.7% of our Portfolio being excluded because the homes were in rehabilitation and 43.6% of our Portfolio being excluded because the homes were purchased with tenants in place. As of March 31, 2021, on average, homes are in rehabilitation for 163 days and the average length of time from acquisition to stabilization for acquired homes is 222 days.

Investment Objectives and Strategy

Our primary investment objectives are to maximize the cash flow and value of properties owned, acquire properties with cash flow growth potential, provide quarterly cash distributions and achieve long-term capital appreciation for our stockholders through targeted management and a renovation program on

8

Table of Contents

the homes purchased. We predominately target markets that exhibit lower institutional competition, household formation growth, and superior revenue growth relative to national averages that still allow us to efficiently operate through market-level density. Our target markets include the following metropolitan statistical areas or MSAs: Cincinnati, Dayton (OH), Columbus (OH), St. Louis, Indianapolis, Birmingham (AL), Kansas City, Memphis, Montgomery (AL), Pittsburgh, Greenville (SC), Columbia (SC), Huntsville (AL), Milwaukee, Omaha, Little Rock, Jackson (MS), Augusta (GA) and the Triad (NC). We believe we can achieve this objective through active portfolio management to take advantage of market opportunities to achieve superior risk adjusted returns. Our Adviser and Manager regularly monitor and stress-test each market and the Portfolio as a whole under various scenarios, enabling us to make informed and proactive investment decisions.

Net Asset Value (“NAV”)

The sale price of the shares of our common stock sold in our ongoing private offering is equal to the most recent NAV in effect at the time a subscription agreement or funds are received, plus applicable fees and commissions. The purchase price at which shares of our common stock may be repurchased in accordance with the terms of the Share Repurchase Plan is generally based on the most recent NAV in effect at the time of repurchase, and shares of our common stock issued under the DRIP reflect a 3% discount to the then-current NAV.

NAV is calculated in accordance with the valuation methodology (the “Valuation Methodology”) approved by our Board. Our net assets are primarily comprised of our properties, debt and preferred equity. Other assets and liabilities included in our net asset valuation include cash, accounts payable, among others, and exclude intangible assets and liabilities. Our Adviser is responsible for performing the valuation process and computing our NAV. Our Adviser recommends our NAV to the pricing committee of the Board (the “Pricing Committee”). Based on this recommendation, the Pricing Committee determines our NAV.

Home Valuation

The value of our properties is calculated using pricing information obtained from independent, third-parties (the “Valuation Providers”) that are widely accepted industry leaders in the area of SFR asset valuation. The Valuation Providers are not responsible for determining the NAV. The Adviser will solicit valuations on each property on a monthly basis from multiple Valuation Providers. The Adviser will take an average of each valuation per property to determine the valuation for each specific property. However, in cases where the Adviser receives data from three or more Valuation Providers in a period that (1) reflects a change in value that is 20% higher (or more) than the last value received for the most recent NAV, the Adviser will use a value that is 15% greater than the last value used to calculate the most recent NAV, or (2) reflects a change in value that is 5% lower (or more) than the last value used to calculate the most recent NAV, the Adviser will use a value that is 95% of the previous value. Based on management’s experience in the market and to reduce periodic volatility in asset values, management may periodically recommend changes to the thresholds noted above to the Board, which may increase or decrease our asset values.

For homes purchased within the previous 90 days of the valuation date, the cost (purchase price plus any capital expenditures incurred after purchase) of the home will be used as the initial valuation as it represents the best data point available. Once the home has been held for greater than 90 days and has three or more valuations from Valuation Providers, the Adviser applies the home valuation process utilizing the Valuation Providers’ data as further described above. For homes that were purchased more than 90 days prior to the valuation date but do not have three or more valuations from Valuation Providers, the Company will use the prior valuation used for the calculation of the most recent NAV.

NAV Calculation

Monthly, the Adviser collects data from the Valuation Providers, combined with the cost for certain properties, and other adjustments as prescribed in the Valuation Methodology, to determine the value of our properties. The Adviser then values the remainder of our assets and liabilities using GAAP, excluding the value of interest rate swaps (to the extent the Company has sufficient debt to offset the notional amount of the swap), and including estimated transaction costs, to determine the NAV (subtracting estimated value of liabilities from estimated value of assets). The estimated transaction costs relate to an exit or initial public offering of the business. The Adviser estimates these transaction costs based on three separate scenarios that are weighted based on probable future outcome: (1) portfolio liquidation (2) private sale of the Company and (3) an initial public offering. The Adviser believes this is required to capture the true value of the Company. The NAV per share is then calculated on a fully diluted basis assuming all restricted stock unit grants and profit interest unit grants are fully vested and all units of the Operating Partnership are converted to common stock of the Company.

The factors management uses to determine the weightings is related to the practicality of each scenario. As the Portfolio grows larger, a pure liquidation of the portfolio (scenario 1) becomes less probable; furthermore, as the Company grows and continues to gain scale, it becomes more probable that an initial public offering (scenario 3) will be the most probable scenario. The below outlines the various components and general assumptions related to each scenario that comprise the transaction cost estimate which are subject to change in future NAV calculations based off management’s best estimates:

| 1. | Portfolio liquidation: |

| i. | Legal costs. |

9

Table of Contents

| ii. | Disposition costs, assumed at 3%. |

| iii. | Prepayment penalties on debt, assumed at 1%. |

| 2. | Private sale: |

| i. | Legal costs. |

| ii. | Brokerage costs, assumed to be 1.5%. |

| iii. | Prepayment penalties on debt, assumed at 1%. |

| 3. | Initial public offering: |

| i. | Legal costs. |

| ii. | Additional audit costs, including comfort letters and 3-14 audits. |

| iii. | Internalization fee of the Manager, assumed to be the maximum of 2.5% of outstanding consolidated equity. |

| iv. | Starting with the June 30, 2021 NAV estimation, internalization fee of the Adviser, assumed to be the maximum of 2.5% of outstanding consolidated equity. |

| v. | Underwriting costs, assumed to be 5% on equity raised which is estimated to be 20% of the current equity outstanding. |

| vi. | Listing and other fees associated with taking a company public. |

Currently, the NAV is reviewed and determined on a monthly basis by the Pricing Committee. The NAV calculation and application of the Valuation Methodology are reviewed and confirmed by an independent third-party valuation firm after the end of each fiscal quarter after that quarter-end’s NAV is determined by the Board. The most recent NAV per share in effect at any given point in time will be based on the NAV as of the most recent determination date. The NAV of $40.82 per share in effect as of July 27, 2021, was based on the NAV per share as of June 30, 2021. The NAV is applied to outstanding shares prospectively, and is used for sales, distribution reinvestment, and redemptions. For example, the purchase price for our common stock at each closing in the Private Offering is based on the most recent NAV per share in effect (currently our prior month calculated NAV) at the time a subscription agreement or funds are received, plus applicable fees and commissions. The determination of NAV under the Valuation Methodology involves significant judgment and estimation of the value of our properties by our Adviser. The Valuation Methodology allows our Adviser to use judgment in determining whether temporary market fluctuations are indicative of changes in core real estate values.

The following table presents our historical NAV as determined by the Pricing Committee (or our Board prior to the formation of the Pricing Committee) for all previous periods. We expect the Pricing Committee to determine NAV as of July 31, 2021 on or about August 15, 2021.

Date | NAV per share | |||

June 30, 2021 | $ | 40.82 | ||

May 31, 2021 | 38.68 | |||

April 30, 2021 | 37.85 | |||

March 31, 2021 | 36.82 | |||

February 28, 2021 | 36.68 | |||

January 31, 2021 | 36.56 | |||

December 31, 2020 | 36.56 | |||

November 30, 2020 | 34.38 | |||

October 31, 2020 | 34.18 | |||

September 30, 2020 | 34.00 | |||

August 31, 2020 | 32.91 | |||

July 31, 2020 | 31.47 | |||

June 30, 2020 | 31.24 | |||

May 31, 2020 | 31.08 | |||

April 30, 2020 | 30.82 | |||

March 31, 2020 | 30.59 | |||

December 31, 2019 | 30.58 | |||

September 30, 2019 | 29.85 | |||

June 30, 2019 | 28.88 | |||

March 31, 2019 | 28.75 | |||

December 31, 2018 | 28.27 | |||

November 1, 2018 | 25.00 | |||

10

Table of Contents

The following table provides a breakdown of the major components of our NAV per share amounts for all previous periods (in thousands, except per share amounts):

As of | Value of Homes (1) | Other assets (2) | Debt, net (3) | Preferred equity (4) | Other liabilities (5) | Transaction costs (6) | NAV | Fully diluted shares | NAV per share | |||||||||||||||||||||||||||

June 30, 2021 | $ | 1,787,597 | $ | 77,140 | $ (835,162) | $ (125,000) | $ | (67,322 | ) | $ (84,243) | $ 753,010 | 18,448 | $ | 40.82 | ||||||||||||||||||||||

May 31, 2021 | 1,641,514 | 70,400 | (834,361) | (125,000) | (55,923 | ) | (32,177) | 664,453 | 17,176 | 38.68 | ||||||||||||||||||||||||||

April 30, 2021 | 1,578,395 | 48,391 | (799,016) | (125,000) | (50,946 | ) | (30,622) | 621,202 | 16,411 | 37.85 | ||||||||||||||||||||||||||

March 31, 2021 | 1,517,321 | 59,320 | (799,229) | (125,000) | (39,134 | ) | (33,349) | 579,929 | 15,749 | 36.82 | ||||||||||||||||||||||||||

February 28, 2021 | 1,202,370 | 74,573 | (519,859) | (125,000) | (67,233 | ) | (33,547) | 531,304 | 14,484 | 36.68 | ||||||||||||||||||||||||||

January 31, 2021 | 1,162,439 | 67,724 | (524,088) | (125,000) | (41,275 | ) | (32,434) | 507,366 | 13,876 | 36.56 | ||||||||||||||||||||||||||

December 31, 2020 | 922,341 | 59,222 | (347,709) | (88,500) | (30,327 | ) | (29,358) | 485,669 | 13,283 | 36.56 | ||||||||||||||||||||||||||

November 30, 2020 | 842,960 | 29,900 | (311,057) | (61,000) | (32,735 | ) | (27,464) | 440,604 | 12,817 | 34.38 | ||||||||||||||||||||||||||

October 31, 2020 | 817,601 | 23,378 | (300,579) | (61,000) | (29,883 | ) | (26,494) | 423,023 | 12,376 | 34.18 | ||||||||||||||||||||||||||

September 30, 2020 | 799,042 | 14,968 | (346,262) | — | (36,871 | ) | (26,541) | 404,336 | 11,892 | 34.00 | ||||||||||||||||||||||||||

August 31, 2020 | 771,819 | 12,390 | (353,387) | — | (28,867 | ) | (25,107) | 376,848 | 11,452 | 32.91 | ||||||||||||||||||||||||||

July 31, 2020 | 739,817 | 17,402 | (360,852) | — | (24,249 | ) | (24,244) | 347,874 | 11,053 | 31.47 | ||||||||||||||||||||||||||

June 30, 2020 | 716,983 | 23,092 | (359,668) | — | (24,113 | ) | (23,740) | 332,554 | 10,646 | 31.24 | ||||||||||||||||||||||||||

May 31, 2020 | 697,750 | 33,339 | (357,472) | — | (28,979 | ) | (22,841) | 321,797 | 10,354 | 31.08 | ||||||||||||||||||||||||||

April 30, 2020 | 677,606 | 42,090 | (357,050) | — | (21,738 | ) | (22,607) | 318,301 | 10,329 | 30.82 | ||||||||||||||||||||||||||

March 31, 2020 | 650,844 | 50,319 | (356,928) | — | (19,011 | ) | (22,534) | 302,690 | 9,894 | 30.59 | ||||||||||||||||||||||||||

December 31, 2019 | 592,115 | 22,153 | (315,889) | — | (19,343 | ) | (21,283) | 257,753 | 8,428 | 30.58 | ||||||||||||||||||||||||||

September 30, 2019 | 540,918 | 22,232 | (304,497) | — | (17,724 | ) | (18,355) | 222,574 | 7,456 | 29.85 | ||||||||||||||||||||||||||

June 30, 2019 | 415,317 | 39,522 | (239,418) | — | (16,142 | ) | (15,577) | 183,702 | 6,360 | 28.88 | ||||||||||||||||||||||||||

March 31, 2019 | 386,576 | 35,470 | (239,339) | — | (13,127 | ) | (14,565) | 155,015 | 5,392 | 28.75 | ||||||||||||||||||||||||||

December 31, 2018 | 363,228 | 51,336 | (239,261) | — | (15,194 | ) | (13,694) | 146,415 | 5,179 | 28.27 | ||||||||||||||||||||||||||

November 1, 2018 | 330,173 | 27,030 | (239,209) | — | (9,836 | ) | — | 108,158 | 4,327 | 25.00 | ||||||||||||||||||||||||||

| (1) | As determined in accordance with the Valuation Methodology. |

| (2) | Includes cash, accounts receivable, prepaids and other assets calculated on a GAAP basis. |

| (3) | Presented net of unamortized deferred financing costs, in accordance with GAAP. |

| (4) | Presented at redemption value. |

| (5) | Includes accounts payable, accrued expenses and interest, security deposits and other liabilities calculated on a GAAP basis. |

| (6) | As estimated by management in accordance with the Valuation Methodology. |

While we believe our assumptions are reasonable, a change in these assumptions could materially impact the calculation of our NAV. For example, assuming all other factors remain unchanged, a 1% increase in the value of properties as of June 30, 2021 would result in a $0.93 increase in our NAV per share. Assuming all other factors remain unchanged, an increase in the estimated transaction costs as of June 30, 2021 of $1,000,000 would result in a $0.05 decrease in our NAV per share.

Our Valuation Methodology is based upon a number of estimates and assumptions, including the estimated value of our homes and estimated transaction costs that may not be accurate or complete. Different parties with different assumptions and estimates could derive a different NAV. Accordingly, we have disclosed the following risk factors relative to our NAV:

| • | The sale price of the shares of our common stock sold in the Private Offering and the purchase price at which the shares of our common stock may be repurchased under the Share Repurchase Plan are based on NAV as calculated in accordance with the Valuation Methodology, which is subject to certain risks and uncertainties and may be changed at any time in the sole discretion of our Board. |

| • | Valuations of our properties are estimates of value and may not necessarily correspond to realizable value. In addition, our Valuation Methodology and related policies may be changed at any time at the sole discretion of our Board. |

| • | Our NAV per share amounts may change materially if the appraised values of our properties materially change from prior appraisals or the actual operating results for a particular period differ from what we originally budgeted for that period. |

| • | It may be difficult to reflect, fully and accurately, material events that may impact our NAV. |

| • | We may change the frequency at which our NAV per share is calculated and may infrequently calculate our NAV per share. In addition, because our NAV per share is calculated periodically, our NAV per share may suddenly change on the day the newly calculated NAV per share is effective. |

| • | Purchases, reinvestments of distributions and repurchases of shares of our common stock are generally made at the most recent NAV per share in effect, which is based on a prior period (month or quarter) end and may not accurately reflect the current NAV per share. |

| • | NAV calculations are not governed by governmental or independent securities, financial or accounting rules or standards. |

Amended Valuation Methodology

On May 24, 2021, our Board approved a form of amendment and restatement of our Valuation Methodology (the “Green Street Valuation Methodology”). Once implemented, the Company expects Green Street Advisers, LLC (“Green Street”) to calculate a preliminary NAV by valuing the Portfolio in accordance with the Green Street Valuation Methodology. Green Street will then recommend the preliminary NAV to the Adviser. Based on this recommendation, the Adviser will then calculate transaction costs in the same process described above and make any other adjustments, including costs of internalization, determined necessary to recommend NAV to the Pricing Committee. Based off this recommendation, the Pricing Committee will then determine NAV. We expect that the new Green Street Valuation Methodology described further below will result in an increase to NAV compared to our prior Valuation Methodology. Green Street and our Advisor have not completed the initial valuation, and there can be no assurance as to the magnitude of the increase or that an increase will be realized at all.

11

Table of Contents

The Green Street Valuation Methodology includes an initial valuation (“Initial Valuation”) conducted by Green Street, which the Company expects to be completed by Green Street in the next few months, followed by monthly or quarterly ongoing valuations (“Ongoing Valuations”) as determined by the Board, which will also be conducted by Green Street.

Initial Valuation

The first quarterly valuation that Green Street conducts will ascribe values for both the stabilized and un-stabilized homes in our Portfolio. For purposes of the Green Street Valuation Methodology, a home will be considered un-stabilized if it is unoccupied and acquired-or-completed its renovation within the last twelve months. A home is also considered un-stabilized if the remaining renovation costs exceed 15% of cost basis (i.e., the acquisition price and completed renovation costs). Homes not meeting the criteria for un-stabilization are considered stabilized. The valuation of stabilized homes begins with the aggregation of third-party automated valuation model (“AVM”) estimates. Third-party automated valuation models calculate a property’s estimated value in real-time using mathematical algorithms combined with databases of existing properties and transactions. Green Street will assess the implied metrics stemming from AVM estimates, by triangulating between implied capitalization rates, anticipated operating margins, and sales values per square foot to ascribe an explicit value. Green Street will calculate a stabilized capitalization rate using an estimate of operating income over the ensuing twelve months (“Forward NOI”) divided by the AVM output. Provided that AVM estimates imply a capitalization rate that differs significantly from other market-level observations (i.e., greater than two standard deviations from the mean capitalization rate), further analysis will be conducted and manual/subjective adjustments may be warranted and applied.

Green Street will estimate the value of un-stabilized homes using the discounted cash flow method. The discounted cash flow method begins with an estimation of home value upon stabilization using the capitalized income approach. Capitalized income determines real estate value based on an estimate of Forward NOI and divides that income by a market-level capitalization rate. Market-level rent and operating margin estimates will be used to determine Forward NOI. Stabilized capitalization rates for each market will be determined using the implied capitalization rate of the Company’s existing stabilized portfolio. The projected stabilized home value is discounted at Green Street’s estimated unlevered required return to ascribe a current value. Unlevered required return estimates incorporate market-level cap rates, future NOI growth, and an adjustment for risk.

In addition to the home valuations, Green Street will value other assets and liabilities to arrive at a preliminary NAV. Cash, listed securities, receivables, prepaid expenses, and other current assets which have a defined and quantifiable market value are included in the gross asset value. Intangible assets without a quantifiable market value (i.e., goodwill) are excluded. Long-term fixed-rate liabilities are marked-to-market using a prevailing treasury yield of similar maturity and an appropriate spread to account for risk. Variable rate debt is listed at book value. Preferred equity obligations are accounted for at face value and listed as an addition to debt. Accounts payable and other current liabilities which have a defined and quantifiable market value are included at book value. The preliminary NAV per share is expected to be calculated on a fully diluted basis, assuming all restricted stock unit grants and profit interest unit grants are fully vested and all units of the Operating Partnership are converted to common stock of the Company.

Ongoing Valuations

Subsequent to the Initial Valuation, Green Street will determine stabilized home values by applying a proprietary appreciation index to Green Street’s estimate of beginning stabilized value. Beginning stabilized value for each home is determined either during the Initial Valuation or after an un-stabilized home becomes stabilized. The proprietary appreciation index utilizes a blend of Freddie Mac and Case-Schiller indices, the weighting of which is proprietary to Green Street. Green Street will estimate the value of homes that were un-stabilized during the Initial Valuation and transitioned to stabilization within the last three months (“Transition Homes”). Transition Homes will be valued using the capitalized income methodology. Green Street will estimate Forward NOI by reviewing Company’s in-place income and expense data and applying estimates for forward growth. Market-level stabilized capitalization rates will be determined using the implied capitalization rate of the Company’s existing stabilized assets. This value will serve as the starting point from which home price appreciation is applied in subsequent quarters. Un-stabilized homes will be the same as outlined in the Initial Valuation section above. As new homes are purchased each quarter, Green Street will assess the state of the asset (i.e., stabilized or un-stabilized) using occupancy figures, in-place rent relative to market (if occupied), and anticipated renovation costs. Value estimates for newly acquired assets will be determined according to Green Street’s Initial Valuation methodology for stabilized and un-stabilized assets. The ongoing valuations for the various other assets and liabilities will follow the same methodology as outlined in the Initial Valuation.

To assist Green Street in their analysis for the Initial Valuation and Ongoing Valuations, the Adviser sends the following information as of the valuation date to Green Street:

| • | A data tape that details the following information on each property in the Portfolio: |

| • | Address and geographic market location |

| • | Acquisition date |

| • | Management’s assessment of stabilization status |

| • | Rehab completion date |

| • | Tenant move-in date |

| • | Year built |

| • | Property type (i.e. single home or duplex) |

| • | Bedrooms and bathrooms |

| • | Square footage |

| • | Occupancy |

| • | Acquisition cost |

| • | Actual and projected capital expenditures |

| • | Market and actual rent |

| • | Net operating income detail |

| • | A preliminary unaudited consolidated balance sheet, subject to completion, including the completion of customary financial statement closing and review procedures for the period |

| • | Basic and diluted consolidated share counts |

| • | A debt schedule detailing the following for each note/facility: |

| • | Issuance date |

| • | Maturity date |

| • | Current outstanding balance |

| • | Maximum outstanding balance |

| • | Floating or fixed rate |

| • | Effective interest rate information (index and spread) |

Once the above information is provided by the Adviser to Green Street, Green Street analyzes the data and synthesizes it with their proprietary real estate data and calculations (as described above) to assess and estimate the growth, income, margin and risk of the Portfolio as a whole. These estimated inputs then factor into their preliminary NAV.

Our Financing Strategy

We intend to use leverage to provide additional funds to support our investment activities, with the expectation that this will enhance returns. Leverage allows us to make more investments than would otherwise be possible, resulting in a broader and more diverse portfolio with potentially higher returns but also with more risk.

We leverage our Portfolio by assuming or incurring secured or unsecured property-level or entity-level debt. An example of property-level debt is a mortgage loan secured by an individual property or portfolio of properties incurred or assumed in connection with the acquisition of such property or portfolio of properties. An example of entity-level debt is a line of credit obtained by us or our Operating Partnership or subsidiaries.

Our actual leverage level will be affected by a number of factors, some of which are outside our control. Significant inflows of proceeds from our ongoing private offering generally will cause our leverage as a percentage of net assets, or our leverage ratio, to decrease, at least temporarily. Our leverage ratio will also increase or decrease with decreases or increases, respectively, in the value of our Portfolio.

Our target leverage is 60-65% loan-to-value (“LTV”), with value being calculated as the value of our assets used to determine our NAV (see Item 2. “Financial Information—Management’s Discussion and Analysis of Financial Condition and Results of Operations—Overview”) and capital priced at one-month London InterBank Offered Rate (“LIBOR”) plus 150-325 bps, depending on whether the loan is secured or unsecured, the duration of the loan and specific provisions and covenants contained in the loan. We may additionally enter into interest rate swap contracts whereby we synthetically fix floating interest rates on loans.

The following table presents a summary of our current outstanding indebtedness as of March 31, 2021:

12

Table of Contents

| Type | Outstanding Principal as of March 31, 2021 | |||||||

Initial Mortgage | Floating | $ | 241,400 | |||||

Warehouse Facility | Floating | 100,000 | ||||||

JPM Facility | Floating | 320,000 | ||||||

MetLife Note | Fixed | 125,000 | ||||||

TrueLane Mortgage | Fixed | 10,526 | ||||||

Colony Note | Fixed | 9,318 | ||||||

CoreVest Note | Fixed | 2,364 | ||||||

|

| |||||||

| $ | 808,608 | |||||||

Debt premium, net | 563 | |||||||

Deferred financing costs, net of accumulated amortization of $1,794 | (9,942 | ) | ||||||

|

| |||||||

| $ | 799,229 | |||||||

|

| |||||||

Competition

We face competition from different sources in each of our two primary activities: developing/acquiring properties and renting our properties. We believe our primary competitors in acquiring our target properties through individual acquisitions are individual investors, small private investment partnerships looking for one-off acquisitions of investment properties that can either be rented or restored and sold, and larger investors, including private equity funds and other REITs, that are seeking to capitalize on the same market opportunity that we have identified as well as individuals looking to become homeowners. Our primary competitors in acquiring portfolios of properties or land assets include large and small private equity investors, public and private REITs, other sizeable private institutional investors and other homebuilders. These same competitors may also compete with us for tenants. Competition may increase the prices for properties and land that we would like to purchase, reduce the amount of rent we may charge at our properties, reduce the occupancy of our Portfolio and adversely impact our ability to achieve attractive yields. However, we believe that our acquisition platform, our extensive in-house property management infrastructure and market knowledge in markets that meet our selection criteria provide us with competitive advantages.

Private Offering

On August 28, 2018, we commenced a non-registered continuous private placement of up to 40,000,000 shares of our common stock (the “Private Offering”) pursuant to the safe harbor of Rule 506(b) of Regulation D under Section 4(a)(2) of the Securities Act of 1933, as amended (the “Securities Act”). The Private Offering will continue until the earlier of (i) the date when the maximum offering amount is sold, (ii) November 1, 2023, subject to two one-year extensions at the sole discretion of the Board or (iii) a decision by the Company to terminate the Private Offering. As of March 31, 2021, we have issued 11,533,512 shares of common stock through the Private Offering and under our DRIP resulting in gross offering proceeds of approximately $370.2 million, including 411,577 shares issued under our dividend reinvestment plan (“DRIP”). After fees, commissions and other offering expenses, we received net offering proceeds of approximately $352.4 million. We contributed a majority of the net proceeds from the Private Offering to our Operating Partnership in exchange for OP Units. Our Operating Partnership has used the net proceeds from the Private Offering primarily to acquire and renovate additional SFR properties in new and existing markets and maintain existing SFR properties in our Portfolio.

13

Table of Contents

Human Capital

We have one accounting employee. We are externally managed by our Adviser pursuant to the Advisory Agreement. In addition, our Manager is responsible for the day-to-day management of our Portfolio pursuant to the Management Agreements and Side Letter. We will not have any employees other than accounting and tax employees while the Advisory Agreement is in effect.

Regulation

General

Our properties are subject to various rules, laws and ordinances, and certain of our properties are also subject to the rules of the various HOAs where such properties are located. We believe that we are in material compliance with such covenants, laws, ordinances and rules, and we also require that our tenants agree to comply with such covenants, laws, ordinances and rules in their leases with us.

Fair Housing Act

The Fair Housing Act (“FHA”) and its state law counterparts, and the regulations promulgated by the U.S. Department of Housing and Urban Development and various state agencies, prohibit discrimination in housing on the basis of race or color, national origin, religion, sex, familial status (including children under the age of 18 living with parents or legal custodians, pregnant women and people securing custody of children under the age of 18), handicap or, in some states, financial capability. We believe that our properties are in substantial compliance with the FHA and other regulations.

Environmental Matters

As a current or prior owner of real estate, we are subject to various federal, state and local environmental laws, regulations and ordinances, and we could be liable to third parties as a result of environmental contamination or noncompliance at our properties, even if we no longer own such properties. See Item 1A. “Risk Factors—Risks Related to Our Business—Contingent or unknown liabilities could adversely affect our financial condition.” and Item 1A. “Risk Factors—Risks Related to the Real Estate Industry—Environmental hazards outside of our control and the cost of complying with governmental laws and regulations regarding these hazards may adversely affect our operations and performance.”

REIT Qualification

We have elected to be treated as a REIT under the Code, commencing with our taxable year ended on December 31, 2018. We believe that we have been organized and operate in such a manner as to continue to qualify for taxation as a REIT.

Qualification and taxation as a REIT depend on our ability to meet on a continuing basis, through actual operating results, distribution levels, and diversity of stock and asset ownership, various

14

Table of Contents

qualification requirements imposed upon REITs by the Code. Our ability to qualify as a REIT also requires that we satisfy certain asset tests, some of which depend upon the fair market values of assets that we own directly or indirectly. Such values may not be susceptible to a precise determination. Accordingly, no assurance can be given that the actual results of our operations for any taxable year will satisfy such requirements for qualification and taxation as a REIT.

If we fail to qualify as a REIT in any taxable year and do not qualify for certain statutory relief provisions, we will be subject to U.S. federal income tax at regular corporate rates and may be precluded from qualifying as a REIT for the subsequent four taxable years following the year during which we failed to qualify as a REIT. Even if we qualify for taxation as a REIT, we may be subject to some U.S. federal, state and local taxes on our income or property or REIT “prohibited transactions” taxes with respect to certain of our activities. Any distributions paid by us generally will not be eligible for taxation at the preferred U.S. federal income tax rates that apply to certain distributions received by individuals from taxable corporations. For additional information see Item 1A. “Risk Factors—Risks Related to Tax.”

Investment Company Act of 1940

We intend to conduct our operations so that neither we nor any of our subsidiaries are required to register as an investment company under the Investment Company Act of 1940.

Implications of Being an Emerging Growth Company and Smaller Reporting Company

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”) and we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a non-binding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

The JOBS Act permits an emerging growth company such as us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We have elected to take advantage of this extended transition period. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates for such new or revised standards. We may elect to comply with public company effective dates at any time, and such election would be irrevocable pursuant to Section 107(b) of the JOBS Act.

We could remain an “emerging growth company” until the earliest of (1) the end of the fiscal year following the fifth anniversary of the date of the first sale of our common stock pursuant to an effective registration statement, (2) the last day of the fiscal year in which our annual gross revenues exceed $1.07 billion, (3) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (4) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three year period.

15

Table of Contents

We are also a “smaller reporting company” as defined in the Exchange Act, and may elect to take advantage of certain of the scaled disclosures available to smaller reporting companies. We may be a smaller reporting company even after we are no longer an “emerging growth company.”

16

Table of Contents

SIGNATURES

Pursuant to the requirements of Section 12 of the Securities Exchange Act of 1934, the registrant has duly caused this registration statement to be signed on its behalf by the undersigned, thereunto duly authorized.

VineBrook Homes Trust, Inc. | ||||||

Date: September 8, 2021 | By: | /s/ Brian Mitts | ||||

Name: | Brian Mitts | |||||

Title: | Chief Financial Officer, Assistant Secretary and Treasurer | |||||