Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-228694

MERGER PROPOSED—YOUR VOTE IS VERY IMPORTANT

To the Stockholders of RTI Surgical, Inc. and the Unitholders of PS Spine Holdco, LLC:

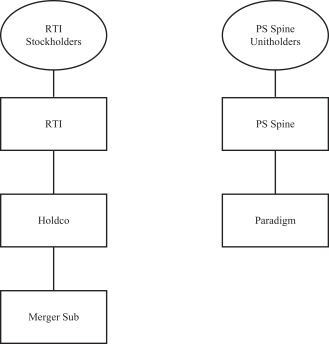

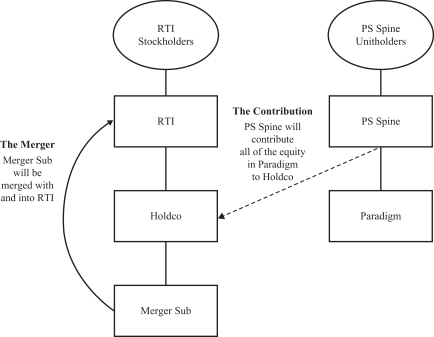

RTI Surgical, Inc., a Delaware corporation (“RTI”), PS Spine Holdco, LLC, a Delaware limited liability company (“PS Spine”), Bears Holding Sub, Inc., a Delaware corporation and direct wholly owned subsidiary of RTI (“Holdco”), and Bears Merger Sub, Inc., a Delaware corporation and direct wholly owned subsidiary of Holdco (“Merger Sub”), have entered into a Master Transaction Agreement, dated as of November 1, 2018 (as may be amended from time to time, the “Master Transaction Agreement”). Pursuant to the Master Transaction Agreement and subject to its terms and conditions, at the closing contemplated by the Master Transaction Agreement (the “closing”), Holdco will acquire all of the outstanding equity interests in Paradigm Spine, LLC, a Delaware limited liability company and wholly owned subsidiary of PS Spine (“Paradigm”), through a transaction in which: (i) PS Spine will contribute all of the issued and outstanding equity interests in Paradigm to Holdco (the “Contribution”), (ii) Merger Sub will be merged with and into RTI (the “Merger”), with RTI surviving as a wholly owned direct subsidiary of Holdco and (iii) Holdco will be renamed “RTI Surgical Holdings, Inc.” (collectively, the “Transaction”). The board of directors of RTI and the board of managers of PS Spine have each unanimously approved the Master Transaction Agreement and the transactions contemplated thereby, including the Merger and the Contribution.

If the Transaction is completed, as consideration for the Contribution, at closing Holdco will pay PS Spine $100.0 million in cash, subject to adjustment as described below (the “Cash Consideration Amount”), and will issue 10,729,614 fully paid andnon-assessable shares of Holdco common stock (as defined below) (the “Stock Consideration Amount”) in the aggregate to PS Spine and to the lenders under Paradigm’s existing senior secured credit agreement and their affiliates. The Stock Consideration Amount was determined by dividing $50.0 million by the volume weighted average closing price of common stock, par value $0.001 per share, of RTI (“RTI common stock”) for the five business days prior to the date of the Master Transaction Agreement (the “RTI Price”). The Cash Consideration Amount is subject to the following adjustments: (i) positive dollar-for-dollar adjustment based on the amount of Paradigm’s cash and cash equivalents at closing, (ii) negative dollar-for-dollar adjustment based on the amount of outstanding indebtedness and unpaid transaction expenses of Paradigm at closing and (iii) negative dollar-for-dollar adjustment to the extent that Paradigm’s working capital (excluding cash, cash equivalents, indebtedness and transaction expenses) at closing is less than the working capital target of $7.0 million. At the closing, due to the expected amount of Paradigm’s indebtedness and transaction expenses, all cash that would otherwise be paid at closing pursuant to the Master Transaction Agreement to PS Spine, as well as a portion of the Stock Consideration Amount, is expected to be used to satisfy Paradigm’s outstanding indebtedness and unpaid transaction expenses.

In addition to the Cash Consideration Amount and the Stock Consideration Amount payable at the closing, Holdco may be required to make further cash payments or issue additional shares of common stock, par value $0.001 per share, of Holdco (“Holdco common stock”) to PS Spine in an amount up to an additional $50.0 million of shares of Holdco common stock to be valued based upon the RTI Price and an additional $100.0 million of cash and/or Holdco common stock to be valued at the time of issuance (the “Earnout Consideration”), in each case, if certain revenue targets, which are described in the accompanying joint proxy and consent solicitation statement/prospectus, are achieved between closing and December 31, 2022. In certain circumstances, described in greater detail in the accompanying joint proxy and consent solicitation statement/prospectus, $10.0 million of the Earnout Consideration (which can take the form of cash, stock or a combination of both) will be paid to the lenders under Paradigm’s existing senior secured credit agreement and/or their affiliates.

If the Transaction is completed, (a) each share of RTI common stock issued and outstanding immediately prior to the effective time of the Merger (other than shares held by RTI as treasury shares or by Holdco or Merger Sub immediately prior to the effective time, which shall be automatically cancelled and cease to exist) will be converted automatically into one fully paid andnon-assessable share of Holdco common stock, (b) each share of Series A convertible preferred stock, par value $0.001 per share, of RTI issued and outstanding immediately prior to the effective time of the Merger (other than shares held by RTI as treasury shares or by

Table of Contents

Holdco or Merger Sub immediately prior to the effective time which shall be automatically cancelled and cease to exist) shall be converted automatically into one fully paid and non-assessable share of Series A preferred stock, par value $0.001 per share, of Holdco and (c) each stock option and restricted stock award granted by RTI will be converted into a stock option or restricted stock award, as applicable, of Holdco with respect to an equivalent number of shares of Holdco common stock on the same terms and conditions as were applicable prior to the closing.

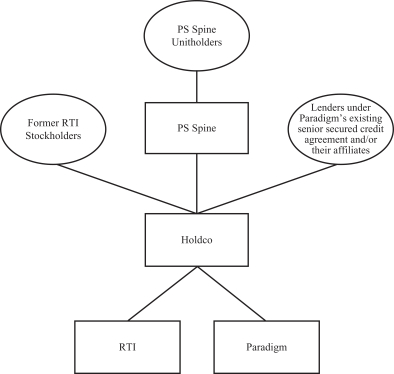

After the consummation of the Transaction, Holdco will own both RTI and Paradigm as wholly owned subsidiaries. Subject to certain assumptions set forth in the accompanying joint proxy and consent solicitation statement/prospectus, it is anticipated that, immediately upon completion of the Transaction, the former stockholders of RTI will own approximately 87.83% of Holdco and PS Spine will own approximately 5.31% of Holdco, and the lenders under Paradigm’s existing senior secured credit agreement and their affiliates will own approximately 6.86% of Holdco. We expect that Holdco common stock will be listed on the Nasdaq Global Market under the symbol “RTIX”.

The closing is subject to certain conditions, including (i) RTI stockholders approving a proposal to adopt the Master Transaction Agreement and approve the transactions contemplated thereby, including the Merger (the “Merger Proposal”) and to comply with applicable provisions of Nasdaq Stock Market LLC Listing Rule 5635, the potential issuance of more than twenty percent (20%) of Holdco’s issued and outstanding shares in connection with the Transaction (the “Share Issuance Proposal”) and (ii) PS Spine unitholders approving, by written consent, the Master Transaction Agreement and the transactions contemplated thereby, including the Contribution.To obtain these approvals, RTI will hold a special meeting of RTI stockholders (the “RTI special meeting”), and PS Spine will conduct a consent solicitation in order to obtain the requisite approval from PS Spine unitholders (the “PS Spine consent solicitation”). The RTI special meeting will be held on March 7, 2019 at 10:00 a.m., local time, at 520 Lake Cook Road, Suite 315, Deerfield, Illinois 60015.

Simultaneously with the execution of the Master Transaction Agreement, certain holders of 5% or more of the voting units of PS Spine, representing approximately 67.4% of the outstanding Common Units, Class A Common Units, Class A Preferred Units, Class B Preferred Units,Class E-1 Preferred Units and Class F Preferred Units, including a majority of the Class A Preferred Units and a majority of the Class B Preferred Units, of PS Spine have each entered into support agreements with RTI and Holdco pursuant to which, among other things, they have agreed to execute and return written consents approving the Master Transaction Agreement and the transactions contemplated thereby, including the Contribution. PS Spine expects that the written consents to be delivered by unitholders pursuant to the support agreements will represent a sufficient number of voting units of PS Spine to satisfy the approval requirement described above with respect to the approval of the Master Transaction Agreement and the transactions contemplated thereby, including the Contribution. Additionally, certain executive officers, directors and holders of five percent (5%) or more of the voting shares of RTI stock, representing approximately 2.08% of the outstanding RTI common stock and all of the outstanding RTI preferred stock as of the date of the Master Transaction Agreement, have each entered into support agreements with PS Spine pursuant to which, among other things, they have agreed to vote all of the shares of RTI common stock and RTI preferred stock owned by them in favor of (i) the Merger Proposal, (ii) the Share Issuance Proposal and (iii) a proposal to adjourn the RTI special meeting, if necessary or appropriate, to solicit additional proxies if there are not sufficient votes to approve the Merger Proposal or the Share Issuance Proposal.

At the RTI special meeting, RTI stockholders will be asked to vote on (i) the Merger Proposal, (ii) the Share Issuance Proposal and (iii) a proposal to adjourn the RTI special meeting, if necessary or appropriate, to solicit additional proxies if there are not sufficient votes to approve the Merger Proposal or the Share Issuance Proposal.

The RTI board of directors unanimously recommends that RTI stockholders vote “FOR” each of these proposals at the RTI special meeting.

The PS Spine board of managers unanimously recommends that PS Spine unitholders provide their written consent to the proposal to approve the Master Transaction Agreement and the transactions contemplated thereby, including the Contribution.

Table of Contents

The accompanying document is a proxy statement for RTI, as well as a consent solicitation statement for PS Spine, and provides you with important information about the RTI special meeting, the PS Spine consent solicitation and other matters contemplated by the Master Transaction Agreement. The accompanying document is also the prospectus of Holdco to register the shares of Holdco common stock and Holdco preferred stock to be issued in the Transaction.RTI and PS Spine encourage you to read this entire joint proxy and consent solicitation statement/prospectus carefully, including the section entitled “Risk Factors”, beginning on page38.

The Transaction cannot be completed unless RTI stockholders approve the Merger Proposal and the Share Issuance Proposal. Your vote is very important, regardless of the number of shares you own. Whether or not RTI stockholders plan to attend the RTI special meeting, we ask RTI stockholders to please promptly mark, sign and date the accompanying proxy card and return it promptly in the enclosed postage-paid envelope, or authorize the individuals named on your proxy card to vote your shares by calling the toll-free telephone number or by logging on to the Internet website specified in the instructions included with your proxy card. We ask PS Spine unitholders to please promptly complete the written consent furnished with this joint proxy and consent solicitation statement/prospectus and return it promptly to PS Spine.

Sincerely,

| Sincerely,

| |

| Curtis M. Selquist | Marc R. Viscogliosi | |

| Chairman | Chairman and Chief Executive Officer | |

| RTI Surgical, Inc. | PS Spine Holdco, LLC |

Neither the Securities and Exchange Commission nor any state or provincial securities regulator has approved or disapproved of the proposed transactions described in this joint proxy and consent solicitation statement/prospectus or the securities to be issued pursuant to the Master Transaction Agreement or determined if the information contained in this joint proxy and consent solicitation statement/prospectus is accurate or adequate. Any representation to the contrary is a criminal offense.

This joint proxy and consent solicitation statement/prospectus is dated February 6, 2019, and is being mailed to RTI stockholders and PS Spine unitholders on or about February 6, 2019.

Table of Contents

RTI SURGICAL, INC.

11621 Research Circle

Alachua, Florida 32615

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON MARCH 7, 2019

To the Stockholdersof RTI Surgical, Inc. (“RTI”):

RTI will hold a special meeting (the “RTI special meeting”) of stockholders of RTI at 520 Lake Cook Road, Suite 315, Deerfield, Illinois 60015, on March 7, 2019, at 10:00 a.m., local time, for the following purposes:

| 1. | To consider and vote upon a proposal to adopt the Master Transaction Agreement, dated as of November 1, 2018 (as may be amended from time to time, the “Master Transaction Agreement”), by and among RTI, PS Spine Holdco, LLC, a Delaware limited liability company (“PS Spine”), Bears Holding Sub, Inc., a Delaware corporation and direct wholly owned subsidiary of RTI (“Holdco”), and Bears Merger Sub, Inc., a Delaware corporation and direct wholly owned subsidiary of Holdco (“Merger Sub”), and approve the transactions contemplated thereby, including the merger of Merger Sub with and into RTI, with RTI surviving as a wholly owned subsidiary of Holdco (the “Merger”), (the “Merger Proposal”). |

| 2. | To consider and vote upon a proposal to approve, for purposes of complying with applicable provisions of Nasdaq Stock Market LLC Listing Rule 5635 (“Nasdaq Listing Rule 5635”), the potential issuance of more than twenty percent (20%) of Holdco’s issued and outstanding common stock in connection with the transactions contemplated by the Master Transaction Agreement (the “Share Issuance Proposal”). |

| 3. | To consider and vote upon a proposal to adjourn the RTI special meeting, if necessary or appropriate, including to permit further solicitation of proxies in favor of the Merger Proposal or the Share Issuance Proposal if there are insufficient votes at the time of the RTI special meeting to approve the Merger Proposal or the Share Issuance Proposal (the “Meeting Adjournment Proposal”). |

| 4. | To transact such other business as may properly come before the RTI special meeting or any adjournments or postponements of the RTI special meeting. |

The board of directors of RTI has fixed the close of business on February 1, 2019 as the record date for the determination of the stockholders of RTI entitled to receive notice of the RTI special meeting. Only RTI stockholders of record at the close of business on the record date for the RTI special meeting are entitled to notice of the RTI special meeting and any adjournment or postponements of the RTI special meeting. Only holders of record of RTI common stock and RTI preferred stock at the close of business on the record date for the RTI special meeting are entitled to vote at the RTI special meeting and any adjournment or postponements of the RTI special meeting. A complete list of RTI stockholders entitled to vote at the RTI special meeting will be available for review at the location of the RTI special meeting during the course of the meeting and at the executive offices of RTI during ordinary business hours for a period of ten (10) days before the RTI special meeting.

The board of directors of RTI unanimously recommends that RTI stockholders vote “FOR” the Merger Proposal, “FOR” the Share Issuance Proposal and “FOR” the Meeting Adjournment Proposal.

As holders of RTI stock, your vote is very important. We cannot complete the Transaction described in this joint proxy and consent solicitation statement/prospectus unless (A) the Merger Proposal receives (i) the affirmative vote of the holders of a majority of the outstanding shares of RTI common stock and RTI preferred stock (on a fully converted basis) entitled to vote thereon and (ii) the written consent or affirmative vote of the holders of a majority of the outstanding shares of RTI preferred stock entitled to vote thereon, voting separately as a class and (B) the Share Issuance Proposal receives (i) the affirmative vote of a majority of votes cast on the proposal by RTI common stock and RTI preferred stock (on a fully converted basis) and (ii) the written consent or affirmative vote of the holders of a majority of the outstanding shares of RTI preferred stock, voting

Table of Contents

separately as a class, in each case assuming a quorum is present. Abstentions and brokernon-votes will have the same effect as a vote “AGAINST” the Merger Proposal. Abstentions will have (i) the same effect as a vote “AGAINST” the Share Issuance Proposal for holders of RTI preferred stock, voting separately as a class and (ii) no effect on the Share Issuance Proposal for the holders of RTI common stock and RTI preferred stock (on a fully converted basis). Brokernon-votes will have (i) the same effect as a vote “AGAINST” the Share Issuance Proposal for holders of RTI preferred stock, voting separately as a class and (ii) no effect on the Share Issuance Proposal for the holders of RTI common stock and RTI preferred stock (on a fully converted basis).

It is important that your shares be represented and voted whether or not you plan to attend the RTI special meeting in person. Instructions regarding the different methods for voting your shares are provided under the section entitled “Questions and Answers about the Special Meeting of RTI Stockholders and the Consent Solicitation of PS Spine Unitholders.”

| By | Order of the Board of Directors

| |

Jonathon M. Singer Chief Financial and Administrative Officer, Corporate Secretary | ||

February 6, 2019

Table of Contents

PS SPINE HOLDCO, LLC

505 Park Avenue, 14th Floor

New York, New York 10022

NOTICE OF SOLICITATION OF WRITTEN CONSENT

To the Unitholdersof PS Spine Holdco, LLC (“PS Spine”):

Pursuant to a Master Transaction Agreement, dated as of November 1, 2018 (as may be amended from time to time, the “Master Transaction Agreement”), by and among RTI Surgical, Inc. a Delaware corporation (“RTI”), PS Spine, Bears Holding Sub, Inc., a Delaware corporation and direct wholly owned subsidiary of RTI (“Holdco”), and Bears Merger Sub, Inc., a Delaware corporation and direct wholly owned subsidiary of Holdco (“Merger Sub”), and subject to the terms and conditions of the Master Transaction Agreement, (i) PS Spine will contribute all of the issued and outstanding equity interests of Paradigm Spine, LLC, a Delaware limited liability company and wholly owned subsidiary of PS Spine, to Holdco (the “Contribution”), (ii) Merger Sub will be merged with and into RTI, with RTI surviving as a wholly owned subsidiary of Holdco, and (iii) Holdco will be renamed “RTI Surgical Holdings, Inc.” (collectively, the “Transaction”).

As more specifically described in the enclosed joint proxy and consent solicitation statement/prospectus, the approval of the Master Transaction Agreement and the transactions contemplated thereby, including the Contribution, by the unitholders of PS Spine requires the affirmative consent or vote of the holders of66-2/3% of the outstanding Common Units, Class A Common Units, Class A Preferred Units, Class B Preferred Units,Class E-1 Preferred Units and Class F Preferred Units of PS Spine, given in writing or by vote at a meeting, consenting or voting as a single class, as well as the affirmative consent or vote of the holders of a majority of the outstanding Class A Preferred Units and a majority of the outstanding Class B Preferred Units of PS Spine, given in writing or by vote at a meeting, each consenting or voting as a separate class.

The enclosed joint proxy and consent solicitation statement/prospectus is being delivered to you on behalf of the board of managers of PS Spine to request that unitholders of PS Spine, as of the record date of February 6, 2019, execute and return written consents to approve the Master Transaction Agreement and the transactions contemplated thereby, including the Contribution.

The joint proxy and consent solicitation statement/prospectus describes the proposed Transaction and the actions to be taken in connection with the Transaction and provides additional information about the parties involved. We encourage you to read carefully the entire joint proxy and consent solicitation statement/prospectus, including all its annexes, the documents incorporated by reference therein and the section entitled “Risk Factors”, beginning on page 38.

The board of managers of PS Spine has carefully considered the Master Transaction Agreement, the terms thereof and the transactions contemplated thereby, including the Contribution, and has declared that the Master Transaction Agreement, the terms thereof and the transactions contemplated thereby, including the Contribution, are advisable and fair to and in the best interests of PS Spine and its unitholders. Accordingly, the board of managers of PS Spine unanimously recommends that unitholders of PS Spine approve the Master Transaction Agreement and the transactions contemplated thereby.

After your review of the joint proxy and consent solicitation statement/prospectus and assuming your approval thereof,please sign and complete the written consent furnished with the enclosed joint proxy and consent solicitation statement/prospectus and return it to PS Spine by one of the means described under “The PS Spine Solicitation of Written Consents.”Time is of the essence, and, assuming your approval thereof, you must return the written consent by February 13, 2019.

Thank you for your prompt attention to these matters.

Table of Contents

Yours truly,

|

| Marc R. Viscogliosi |

| Chairman and Chief Executive Officer |

NO MEETING OF THE UNITHOLDERS OF PS SPINE IS BEING HELD IN CONNECTION WITH THE PROPOSED TRANSACTION. PS SPINE IS SOLICITING BY THE ENCLOSED CONSENT MATERIALS YOUR WRITTEN CONSENT TO THE MASTER TRANSACTION AGREEMENT AND THE TRANSACTIONS CONTEMPLATED THEREBY, INCLUDING THE CONTRIBUTION.

Table of Contents

ADDITIONAL INFORMATION

The accompanying joint proxy and consent solicitation statement/prospectus incorporates by reference important business and financial information about RTI from documents that are not included in or delivered with the accompanying joint proxy and consent solicitation statement/prospectus. You can obtain the documents that are incorporated by reference into the accompanying joint proxy and consent solicitation statement/prospectus (other than certain exhibits or schedules to those documents), without charge, by requesting them in writing or by telephone from RTI at the following addresses and telephone numbers, or through the Securities and Exchange Commission website at www.sec.gov:

RTI Surgical, Inc.

11621 Research Circle

Alachua, Florida 32615

Attn: Investor Relations, Molly Poarch

Telephone:(386) 418-8888

To obtain timely delivery of the documents, you must request them no later than five business days before the date of the RTI special meeting or the PS Spine deadline for submitting written consents. Therefore, if you would like to request documents from RTI, please do so by February 28, 2019 in order to receive them before the RTI special meeting or by February 6, 2019 in order to receive them before the PS Spine deadline for submitting written consents.

The accompanying joint proxy and consent solicitation statement/prospectus includes and contains calculations based upon shares of RTI common stock outstanding and entitled to vote and holders of record as of January 15, 2019, the most recent practicable date prior to the date of filing of the joint proxy and consent solicitation statement/prospectus. RTI does not believe such totals will change materially as of the RTI record date and undertakes to file a Current Report on Form 8-K with such updated totals promptly after the RTI record date.

In addition, if you have questions about the proposed transaction or the accompanying joint proxy and consent solicitation statement/prospectus, would like additional copies of the accompanying joint proxy and consent solicitation statement/prospectus or need to obtain proxy cards or other information related to the joint proxy and consent solicitation, please contact Georgeson LLC, the proxy solicitor for RTI, toll-free at (866)391-6921 or PS Spine toll-free at (888)273-9897 or by email at InvestorRelations@paradigmspine.com. You will not be charged for any of these documents that you request.

For more information, see the section entitled “Where You Can Find More Information”, beginning on page 187 of the accompanying joint proxy and consent solicitation statement/prospectus.

Unless otherwise indicated or as the context otherwise requires, all references in this joint proxy and consent solicitation statement/prospectus to:

| • | “combined company” refer collectively to Holdco, RTI and Paradigm, following completion of the Transaction; |

| • | “Contribution” refer to the contribution by PS Spine of all of the issued and outstanding equity interests in Paradigm to Holdco; |

| • | “Holdco” refer to Bears Holding Sub, Inc., a Delaware corporation and direct wholly owned subsidiary of RTI; |

| • | “Holdco common stock” refer to shares of common stock of Holdco, par value $0.001 per share; |

| • | “Holdco preferred stock” refer to shares of Series A preferred stock of Holdco, par value $0.001 per share; |

| • | “Master Transaction Agreement” refer to the Master Transaction Agreement, dated as of November 1, 2018, as it may be amended from time to time, by and among RTI, PS Spine, Holdco and Merger Sub, a copy of which is attached asAnnex A to this joint proxy and consent solicitation statement/prospectus and is incorporated herein by reference; |

| • | “Merger” refer to the merger of Merger Sub with and into RTI such that the separate corporate existence of Merger Sub will thereupon cease; |

Table of Contents

| • | “Merger Sub” refer to Bears Merger Sub, Inc., a Delaware corporation and direct wholly owned subsidiary of Holdco; |

| • | “Paradigm” refer to Paradigm Spine, LLC, a Delaware limited liability company and wholly owned subsidiary of PS Spine; |

| • | “PS Spine” refer to PS Spine Holdco, LLC, a Delaware limited liability company; |

| • | “PS Spine unitholders” refer to holders of PS Spine units; |

| • | “RTI” refer to RTI Surgical, Inc., a Delaware corporation; |

| • | “RTI common stock” refer to shares of common stock of RTI, par value $0.001 per share; |

| • | “RTI preferred stock” refer to shares of Series A preferred stock of RTI, par value $0.001 per share; |

| • | “RTI stockholders” refer to collectively to holders of RTI common stock and holders of RTI preferred stock; |

| • | “Transaction” refer collectively to the Merger and the Contribution; and |

| • | “we”, “our” and “us” refer to RTI and PS Spine, collectively. |

For an index of other defined terms used in this joint proxy and consent solicitation statement/prospectus, see “Index of Defined Terms”.

Table of Contents

ABOUT THIS JOINT PROXY AND CONSENT SOLICITATION STATEMENT/PROSPECTUS

This joint proxy and consent solicitation statement/prospectus, which forms part of a registration statement on FormS-4 filed with the U.S. Securities and Exchange Commission by Holdco (FileNo. 333-228694), constitutes a prospectus of Holdco under Section 5 of the Securities Act of 1933, as amended, with respect to the Holdco shares to be issued in connection with the transactions pursuant to the Master Transaction Agreement. This joint proxy and consent solicitation statement/prospectus also constitutes a proxy statement under Section 14(a) of the Securities Exchange Act of 1934, as amended. It also constitutes a notice of meeting with respect to the RTI special meeting and a notice of solicitation of written consent with respect to the PS Spine consent solicitation.

You should rely only on the information contained in or incorporated by reference into this joint proxy and consent solicitation statement/prospectus. No one has been authorized to provide you with information that is different from that contained in, or incorporated by reference into, this joint proxy and consent solicitation statement/prospectus. This joint proxy and consent solicitation statement/prospectus is dated February 6, 2019. You should not assume that the information contained in, or incorporated by reference into, this joint proxy and consent solicitation statement/prospectus is accurate as of any date other than the date of the applicable document that contains that information. Neither our mailing of this joint proxy and consent solicitation statement/prospectus to RTI stockholders and PS Spine unitholders, nor the issuance by Holdco of its common stock and preferred stock in connection with the transactions pursuant to the Master Transaction Agreement, will create any implication to the contrary.

This joint proxy and consent solicitation statement/prospectus does not constitute an offer to sell, or a solicitation of an offer to buy, any securities, or the solicitation of a proxy or a written consent, in any jurisdiction to or from any person to whom it is unlawful to make any such offer or solicitation in such jurisdiction. Information contained in this joint proxy and consent solicitation statement/prospectus regarding RTI and Holdco has been provided by RTI and Holdco and information contained in this joint proxy and consent solicitation statement/prospectus regarding PS Spine and Paradigm has been provided by PS Spine.

Table of Contents

| 1 | ||||

| 3 | ||||

| 3 | ||||

| 8 | ||||

| 13 | ||||

| 16 | ||||

| 16 | ||||

| 18 | ||||

| 20 | ||||

| 21 | ||||

| 21 | ||||

| 22 | ||||

| 22 | ||||

| 22 | ||||

| 23 | ||||

| 23 | ||||

Board of Directors and Management of Holdco after the Transaction | 23 | |||

| 23 | ||||

| 24 | ||||

| 25 | ||||

| 25 | ||||

| 25 | ||||

| 25 | ||||

| 26 | ||||

| 27 | ||||

| 27 | ||||

| 28 | ||||

| 28 | ||||

| 28 | ||||

Comparison of Rights of Holdco Stockholders, RTI Stockholders and the Paradigm Member | 29 | |||

Summary Selected Historical Consolidated Financial Data for RTI | 30 | |||

Summary Selected Historical Consolidated Financial Data for Paradigm | 32 | |||

Summary Selected Unaudited Pro Forma Condensed Combined Financial Information | 33 | |||

Unaudited Pro Forma Combined Per Share and Per Unit Information | 34 | |||

| 36 | ||||

i

Table of Contents

| 38 | ||||

| 38 | ||||

| 48 | ||||

| 48 | ||||

| 61 | ||||

| 61 | ||||

| 61 | ||||

| 61 | ||||

| 61 | ||||

| 62 | ||||

| 62 | ||||

| 62 | ||||

| 63 | ||||

| 64 | ||||

| 64 | ||||

| 65 | ||||

| 66 | ||||

| 68 | ||||

| 69 | ||||

| 69 | ||||

| 69 | ||||

| 69 | ||||

| 69 | ||||

| 69 | ||||

| 70 | ||||

| 70 | ||||

| 71 | ||||

PS SPINE PROPOSAL 1—APPROVAL OF THE MASTER TRANSACTION AGREEMENT | 72 | |||

| 73 | ||||

| 73 | ||||

| 73 | ||||

Recommendation of the RTI Board and Its Reasons for the Transaction | 79 | |||

Recommendation of PS Spine Board and Its Reasons for the Transaction | 80 | |||

| 84 | ||||

| 102 | ||||

| 108 | ||||

| 108 | ||||

| 109 | ||||

| 109 | ||||

ii

Table of Contents

| 109 | ||||

| 113 | ||||

| 113 | ||||

| 114 | ||||

Restrictions on Sales of Shares of Holdco Received in the Transaction | 114 | |||

Interests of PS Spine’s and Paradigm’s Managers and Executive Officers in the Transaction | 114 | |||

Board of Directors and Management of Holdco after the Transaction | 119 | |||

Board of Directors and Management of the Surviving Corporation after the Transaction | 119 | |||

| 119 | ||||

| 120 | ||||

| 121 | ||||

| 121 | ||||

| 121 | ||||

| 121 | ||||

| 123 | ||||

| 123 | ||||

| 123 | ||||

| 124 | ||||

| 124 | ||||

| 125 | ||||

| 126 | ||||

| 128 | ||||

| 130 | ||||

| 139 | ||||

| 141 | ||||

| 142 | ||||

| 144 | ||||

| 145 | ||||

| 147 | ||||

| 147 | ||||

| 147 | ||||

| 147 | ||||

| 149 | ||||

| 149 | ||||

| 149 | ||||

| 150 | ||||

| 150 | ||||

| 151 | ||||

iii

Table of Contents

| 151 | ||||

| 151 | ||||

| 152 | ||||

| 152 | ||||

| 152 | ||||

| 152 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF PARADIGM | 153 | |||

| 153 | ||||

Critical Accounting Policies and Significant Judgments and Estimates | 154 | |||

| 155 | ||||

| 156 | ||||

| 157 | ||||

| 159 | ||||

| 159 | ||||

| 159 | ||||

| 159 | ||||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT OF RTI | 160 | |||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT OF PS SPINE | 163 | |||

| 166 | ||||

| 166 | ||||

| 168 | ||||

| 168 | ||||

| 170 | ||||

COMPARISON OF RIGHTS OF HOLDCO STOCKHOLDERS, RTI STOCKHOLDERS AND THE PARADIGM MEMBER | 172 | |||

| 179 | ||||

NOTES TO UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION | 183 | |||

| 186 | ||||

| 186 | ||||

| 186 | ||||

| 186 | ||||

| 186 | ||||

| 186 | ||||

| 187 | ||||

| 187 | ||||

| 189 | ||||

| F-1 | ||||

iv

Table of Contents

Table of Contents

CAUTIONARY STATEMENT CONCERNINGFORWARD-LOOKING STATEMENTS

This joint proxy and consent solicitation statement/prospectus and the documents that are incorporated into this joint proxy and consent solicitation statement/prospectus by reference contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on the current expectations, estimates and projections of RTI, Holdco, PS Spine and Paradigm about their industry, the respective beliefs of the management of RTI, Holdco, PS Spine and Paradigm, and certain assumptions made by the management of RTI, Holdco, PS Spine and Paradigm. Words such as “anticipates,” “believes,” “estimates,” “expects,” “intends,” “plans,” “projects,” “seeks,” “targets,” variations of such words and similar expressions are intended to identify such forward-looking statements. In addition, except for historical information, any statements made in this joint proxy and consent solicitation statement/prospectus or any of the documents that are incorporated into this joint proxy and consent solicitation statement/prospectus by reference about: the respective financial condition of RTI, Holdco, PS Spine or Paradigm; expected financial results of the Transaction, including any projections or pro forma financial statements; the impact of the Transaction on the complexity of combined company’s operations; any benefits of scaling caused by the Transaction; the impact of the Transaction on the combined company’s growth rates; potential long-term growth for coflex® products; the impact of the Transaction on the combined company’s market share; the retention of current customers or the acquisition of additional customers; and the payment of any potential Earnout Consideration (as defined below) to PS Spine also are forward-looking statements. Many factors could affect the actual financial results of RTI, Holdco, PS Spine and Paradigm and cause them to vary materially from the expectations contained in the forward-looking statements, including those set forth in, or incorporated by reference into, this joint proxy and consent solicitation statement/prospectus. These statements are not guarantees of future performance and are subject to risks and uncertainties. In addition to the risk factors described under the section entitled “Risk Factors”, beginning on page38, these risks and uncertainties include, among other things:

| • | those identified and disclosed in Part I, Item 1.A., Risk Factors, of RTI’s Annual Report on Form10-K for the year ended December 31, 2017, as filed with the United States Securities and Exchange Commission (the “SEC”) on March 2, 2018; |

| • | the failure to obtain RTI stockholder approval of the proposed Transaction; |

| • | the failure to obtain PS Spine unitholder approval of the proposed Transaction; |

| • | the possibility that the closing conditions to the proposed Transaction may not be satisfied or may be waived, including that a governmental entity may prohibit, delay or refuse to grant a necessary regulatory approval and any conditions imposed in connection with consummation of the proposed Transaction; |

| • | delay in closing the proposed Transaction or the possibility ofnon-consummation of the proposed Transaction; |

| • | the risk that the cost savings and any other synergies from the proposed Transaction may not be fully realized or may take longer to realize than expected, including that the proposed Transaction may not be accretive within the expected timeframe or to the extent anticipated; |

| • | the occurrence of any event that could give rise to termination of the Master Transaction Agreement; |

| • | the risk that litigation in connection with the proposed Transaction may affect the timing or occurrence of the proposed Transaction or result in significant costs of defense, indemnification and liability; |

| • | risks related to the disruption of the proposed Transaction to RTI, Holdco or Paradigm and their management; |

| • | the effect of the announcement of the proposed Transaction on the ability of RTI, Holdco or Paradigm to retain and hire key personnel and maintain relationships with customers, suppliers, third-party distributors and other third parties; |

| • | RTI’s and Paradigm’s inability to pursue alternative business opportunities or make appropriate changes to their respective businesses because of requirements in the Master Transaction Agreement that they conduct their businesses in all material respects in the ordinary course of business consistent with past practice and not engage in certain activities prior to the completion of the Transaction; |

| • | delays or deferments of certain business decisions by RTI’s and Paradigm’s customers, suppliers, third-party distributors and other business partners; |

| • | the ability and timing to obtain required regulatory approvals and satisfy other closing conditions; |

1

Table of Contents

| • | the incurrence of significant costs, expenses and fees for professional services and other transaction costs associated with the Transaction; |

| • | the reduction in the ownership percentage of RTI’s stockholders and PS Spine in the combined company after the consummation of the Transaction; |

| • | the risk that RTI’s share price may fluctuate prior to the completion of the Transaction, and the combined company’s share price may fluctuate following the completion of the Transaction; |

| • | the risk that the monetary value of the Stock Consideration Amount (as defined below) and certain portions of the Earnout Consideration may change following the time of the signing of the Master Transaction Agreement or the date of this joint proxy and consent solicitation statement/prospectus due to a change in the value of Holdco common stock; |

| • | the risk that a significant portion of the consideration to be paid to PS Spine pursuant to the Master Transaction Agreement is contingent on the occurrence of certain events in the future; |

| • | the risk that the market price of the common stock of the combined company may be affected by factors different from those affecting the market price for shares of RTI common stock; |

| • | the risks associated with the incurrence of additional indebtedness to finance the Cash Consideration Amount (as defined below) and pay other costs and expenses incurred in connection with the Transaction, which may adversely affect the business, financial condition and operating results of the combined company; |

| • | the risk that a significant portion of the consideration that would otherwise be paid to PS Spine pursuant to the Master Transaction Agreement will be used to pay amounts owed to the lenders under Paradigm’s existing senior secured credit agreement and their affiliates; and |

| • | the risk that PS Spine and Paradigm managers and executive officers may have interests in the Transaction different from the interests of PS Spine unitholders. |

The areas of risk and uncertainty described above should be considered in connection with any written or oral forward-looking statements that may be made by RTI, Holdco, PS Spine or Paradigm or anyone acting for any or all of them. Except for their ongoing obligations to disclose material information under the U.S. federal securities laws, none of RTI, Holdco, PS Spine and Paradigm undertakes any obligation to release publicly any revisions to any forward-looking statements, to report events or circumstances after the date of this joint proxy and consent solicitation statement/prospectus or to report the occurrence of unanticipated events or actual outcomes.

For additional information about factors that could cause actual results to differ materially from those described in the forward-looking statements, see the note regarding forward-looking statements in Item 7 of RTI’s Annual Report on Form10-K for the year ended December 31, 2017, as filed with the SEC on March 2, 2018, and incorporated by reference in this joint proxy and consent solicitation statement/prospectus. See the sections entitled “Additional Information” and “Where You Can Find More Information”.

RTI, Holdco, PS Spine and Paradigm also caution you that undue reliance should not be placed on any forward-looking statements, which speak only as of the date of this joint proxy and consent solicitation statement/prospectus. Actual results may differ materially from the expected results reflected in forward-looking statements. Copies of RTI’s SEC filings may be obtained by contacting RTI or the SEC or by visiting RTI’s website at www.rtix.com or the SEC’s website at www.sec.gov.

2

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE SPECIAL MEETING OF RTI STOCKHOLDERS AND THE CONSENT SOLICITATION OF PS SPINE UNITHOLDERS

The following are some questions that you, as an RTI stockholder or a PS Spine unitholder, may have regarding the special meeting of RTI stockholders (the “RTI special meeting”) or the consent solicitation of PS Spine unitholders (the “PS Spine consent solicitation”), and brief answers to those questions. For more information about the matters discussed in these questions and answers, see the sections entitled “The RTI Special Meeting” and “The PS Spine Solicitation of Written Consents”, beginning on pages 61 and 69, respectively, of this joint proxy and consent solicitation statement/prospectus. RTI and PS Spine encourage you to read carefully the remainder of this joint proxy and consent solicitation statement/prospectus because the information in this section does not provide all of the information that might be important to you with respect to the matters being considered at the RTI special meeting or the PS Spine consent solicitation. Additional important information is also contained in the Annexes to, and in the documents incorporated by reference into, this joint proxy and consent solicitation statement/prospectus. See the section entitled “Where You Can Find More Information”, beginning on page 187 of this joint proxy and consent solicitation statement/prospectus. RTI and PS Spine are collectively referred to as “we,” “us,” and “our.”

| Q: | What is the proposed transaction on which RTI stockholders are being asked to vote and to which PS Spine unitholders are being asked to consent? |

| A: | RTI, PS Spine, Holdco and Bears Merger Sub, Inc., a Delaware corporation and direct wholly owned subsidiary of Holdco (“Merger Sub”), entered into the Master Transaction Agreement that is described in this joint proxy and consent solicitation statement/prospectus, and a copy of which is attached asAnnex A. Subject to the terms and conditions set forth in the Master Transaction Agreement, at the closing contemplated by the Master Transaction Agreement (the “closing”), Holdco will acquire all of the outstanding equity interests in Paradigm, a wholly owned subsidiary of PS Spine, through a transaction in which: (i) PS Spine will contribute all of the issued and outstanding equity interests in Paradigm to Holdco (i.e., the Contribution), (ii) Merger Sub will be merged with and into RTI (i.e., the Merger), with RTI surviving the Merger as a wholly owned direct subsidiary of Holdco and (iii) Holdco will be renamed “RTI Surgical Holdings, Inc.” (collectively, the “Transaction”). The Merger and the Contribution will become effective concurrently (such time as the Merger and the Contribution become effective, the “effective time”). |

If the Transaction is completed, as consideration for the Contribution, at the closing Holdco will pay PS Spine $100.0 million in cash, subject to adjustment as described below (the “Cash Consideration Amount”), and will issue 10,729,614 fully paid andnon-assessable shares of Holdco common stock in the aggregate (the “Stock Consideration Amount”) to PS Spine and to the lenders under Paradigm’s existing senior secured credit agreement and their affiliates. The Stock Consideration Amount was determined by dividing $50.0 million by the volume weighted average closing price of RTI common stock for the five business days prior to the date of the Master Transaction Agreement, which was $4.66 per share of RTI common stock (the “RTI Price”). The Cash Consideration Amount is subject to the following adjustments: (i) positive dollar-for-dollar adjustment based on the amount of Paradigm’s cash and cash equivalents at closing, (ii) negative dollar-for-dollar adjustment based on the amount of outstanding indebtedness and unpaid transaction expenses of Paradigm at closing and (iii) negative dollar-for-dollar adjustment to the extent that Paradigm’s working capital (excluding cash, cash equivalents, indebtedness and transaction expenses) at closing is less than the working capital target of $7.0 million. At the closing, due to the expected amount of Paradigm’s indebtedness and transaction expenses, all cash that would otherwise be paid at closing pursuant to the Master Transaction Agreement to PS Spine, as well as a portion of the Stock Consideration Amount, is expected to be used to satisfy Paradigm’s outstanding indebtedness and unpaid transaction expenses.

In addition to the Cash Consideration Amount and the Stock Consideration Amount payable at the closing, Holdco may be required to make further cash payments or issue additional shares of Holdco common stock to PS Spine in an amount up to an additional $50.0 million of shares of Holdco common stock to be valued based upon

3

Table of Contents

the RTI Price and an additional $100.0 million of cash and/or Holdco common stock to be valued at the time of issuance (the “Earnout Consideration”), in each case, if certain revenue targets, which are described in section entitled “The Master Transaction Agreement—Purchase Price—Contingent Consideration”, beginning on page 127, are achieved between closing and December 31, 2022. In certain circumstances, described in greater detail in this joint proxy and consent solicitation statement/prospectus, $10.0 million of the Earnout Consideration (which can take the form of cash, stock or a combination of both) will be paid to the lenders under Paradigm’s existing senior secured credit agreement and/or their affiliates.

If the Transaction is completed, (a) each share of RTI common stock issued and outstanding immediately prior to the effective time of the Merger (other than shares held by RTI as treasury shares or by Holdco or Merger Sub immediately prior to the effective time, which shall be automatically cancelled and cease to exist) will be converted automatically into one fully paid andnon-assessable share of Holdco common stock, (b) each share of RTI preferred stock issued and outstanding immediately prior to the effective time of the Merger (other than shares held by RTI as treasury shares or by Holdco or Merger Sub immediately prior to the effective time which shall be automatically cancelled and cease to exist) shall be converted automatically into one fully paid and non-assessable share of Holdco preferred stock and (c) each stock option and restricted stock award granted by RTI will be converted into a stock option or restricted stock award, as applicable, of Holdco with respect to an equivalent number of shares of Holdco common stock on the same terms and conditions as were applicable prior to the closing.

After the consummation of the Transaction, Holdco will own both RTI and Paradigm as wholly owned subsidiaries.

| Q: | Why am I receiving this joint proxy and consent solicitation statement/prospectus? |

| A: | If you are an RTI stockholder, you are receiving this joint proxy and consent solicitation statement/prospectus because you were a holder of record of RTI shares as of the close of business on February 1, 2019 (the “RTIrecord date”). RTI common stock and RTI preferred stock are collectively referred to as “RTI shares” or “RTI stock”. If you are a PS Spine unitholder, you are receiving this joint proxy and consent solicitation statement/prospectus because you were a holder of record of PS Spine units as of the close of business on February 6, 2019 (the “PS Spinerecord date”). |

This joint proxy and consent solicitation statement/prospectus serves as the proxy statement through which RTI will solicit proxies to obtain the necessary RTI stockholder approval of the Merger Proposal and the Share Issuance Proposal (each, as defined below) and as the consent solicitation statement for PS Spine to obtain the necessary written consent of its unitholders approving the Master Transaction Agreement and the transactions contemplated thereby, including the Contribution. It also serves as the prospectus of Holdco to register the shares of Holdco common stock and Holdco preferred stock to be issued in the Transaction.

RTI is holding a special meeting of its stockholders in order to obtain the stockholder approval necessary to approve the Merger Proposal and the Share Issuance Proposal. RTI stockholders will also be asked to approve the adjournment of the RTI special meeting (if necessary or appropriate to solicit additional proxies if there are not sufficient votes to adopt the Merger Proposal or the Share Issuance Proposal).

PS Spine is seeking the written consent of its unitholders to approve the Master Transaction Agreement and the transactions contemplated thereby, including the Contribution.

We will be unable to complete the Transaction unless, among other things, the RTI stockholders vote to adopt the Merger Proposal and the Share Issuance Proposal and the PS Spine unitholders provide their written consent to adopt the Master Transaction Agreement and the transactions contemplated thereby, including the Contribution.

This joint proxy and consent solicitation statement/prospectus contains important information about the Merger, the Contribution, the Master Transaction Agreement, the RTI special meeting and the PS Spine consent solicitation. You should read this information carefully and in its entirety. The enclosed voting materials allow RTI stockholders to vote RTI shares without attending the RTI special meeting. No meeting of the unitholders of PS Spine is being held in connection with the proposed Transaction. PS Spine is soliciting the consent of PS Spine unitholders by the enclosed consent materials.

4

Table of Contents

| Q: | What will RTI stockholders receive in connection with the Transaction? |

| A: | If the Transaction is completed, holders of RTI common stock will receive one share of Holdco common stock for each share of RTI common stock, and holders of RTI preferred stock will receive one share of Holdco preferred stock for each share of RTI preferred stock. |

| Q: | What will PS Spine receive in the Transaction? |

| A: | If the Transaction is completed, as consideration for the Contribution, Holdco will pay PS Spine $100.0 million in cash, subject to adjustment as described below, representing the Cash Consideration Amount, and will issue 10,729,614 fully paid andnon-assessable shares of Holdco common stock in the aggregate, representing the Stock Consideration Amount, to PS Spine and to the lenders under Paradigm’s existing senior secured credit agreement and their affiliates. The Stock Consideration Amount was determined by dividing $50.0 million by the RTI Price. The Cash Consideration Amount is subject to the following adjustments: (i) positive dollar-for-dollar adjustment based on the amount of Paradigm’s cash and cash equivalents at closing, (ii) negative dollar-for-dollar adjustment based on the amount of outstanding indebtedness and unpaid transaction expenses of Paradigm at closing and (iii) negative dollar-for-dollar adjustment to the extent that Paradigm’s working capital (excluding cash, cash equivalents, indebtedness and transaction expenses) at closing is less than the working capital target of $7.0 million. At the closing, due to the expected amount of Paradigm’s indebtedness and transaction expenses, all cash that would otherwise be paid at closing pursuant to the Master Transaction Agreement to PS Spine, as well as a portion of the Stock Consideration Amount, is expected to be used to satisfy Paradigm’s outstanding indebtedness and unpaid transaction expenses. |

In addition to the Cash Consideration Amount and the Stock Consideration Amount payable at the closing, Holdco may be required to make further cash payments or issue additional shares of Holdco common stock to PS Spine in an amount up to an additional $50.0 million of shares of Holdco common stock to be valued based upon the RTI Price and an additional $100.0 million of cash and/or Holdco common stock to be valued at the time of issuance, representing the Earnout Consideration, in each case, if certain revenue targets, which are described in the section entitled “The Master Transaction Agreement—Purchase Price—Contingent Consideration”, beginning on page 127, are achieved between closing and December 31, 2022. In certain circumstances, described in greater detail in this joint proxy and consent solicitation statement/prospectus, $10.0 million of the Earnout Consideration (which can take the form of cash, stock or a combination of both) will be paid to the lenders under Paradigm’s existing senior secured credit agreement and/or their affiliates.

PS Spine intends to distribute the consideration that it receives pursuant to the Master Transaction Agreement (net of transaction and other expenses and amounts due to its senior lenders and their affiliates) to its unitholders, in accordance with PS Spine’s organizational documents, as soon as reasonably practicable following its receipt thereof.

| Q: | What ownership percentage of Holdco will former RTI stockholders and PS Spine have after the Transaction is completed? |

| A: | If the Transaction occurs, 10,729,614 shares of common stock of Holdco will be issued at closing as partial consideration for the Contribution. A significant portion of these shares will be used, along with cash that would otherwise be paid at closing, to pay the amounts outstanding under Paradigm’s existing senior secured credit agreement. Assuming (i) the closing occurs on March 15, 2019, (ii) 62,245,112 shares of RTI common stock (based on the number of shares outstanding as of January 15, 2019) and 50,000 shares of RTI preferred stock are issued and outstanding immediately prior to the effective time and (iii) the amount of cash paid to the lenders under Paradigm’s existing senior secured credit agreement at closing does not exceed $95.0 million, and taking into account the $3.0 million Paradigm borrowed from the lenders under its existing senior secured credit agreement on December 6, 2018, approximately 85.30% of the issued and outstanding Holdco common stock and 100% of the issued and outstanding Holdco preferred stock immediately following the closing will be held by former RTI stockholders, approximately 6.42% of the issued and outstanding Holdco common stock immediately following the closing will be held by PS Spine and approximately 8.28% of the issued and outstanding Holdco common stock immediately following the closing will be held by the lenders under Paradigm’s existing |

5

Table of Contents

| senior secured credit agreement and their affiliates. Using the same assumptions set forth above and assuming the conversion of the RTI preferred stock, immediately following the closing, former holders of RTI common stock and RTI preferred stock will collectively hold 87.37% of the voting power of Holdco, PS Spine will hold 5.51% of the voting power of Holdco and the lenders under Paradigm’s existing senior secured credit agreement and their affiliates will hold 7.12% of the voting power of Holdco. As described in the section entitled “The Transaction—Interests of PS Spine’s and Paradigm’s Managers and Executive Officers in the Transaction—The Settlement Agreement”, the lenders under Paradigm’s existing senior secured credit agreement and their affiliates may receive a smaller or larger portion of the Stock Consideration Amount than as assumed for purposes of this example. If the lenders under Paradigm’s existing senior secured credit agreement and their affiliates receive a larger portion of the Stock Consideration Amount than as assumed for purposes of this example, the percentage of the issued and outstanding Holdco common stock immediately following the closing that will be held by the lenders under Paradigm’s existing senior secured credit agreement and their affiliates will be greater than set forth in this example and the percentage that will be held by PS Spine will be less than set forth in this example. If the lenders under Paradigm’s existing senior secured credit agreement and their affiliates receive a smaller portion of the Stock Consideration Amount than as assumed for purposes of this example, the percentage of the issued and outstanding Holdco common stock immediately following the closing that will be held by the lenders under Paradigm’s existing senior secured credit agreement and their affiliates will be less than set forth in this example and the percentage that will be held by PS Spine will be greater than set forth in this example. In addition, as described in greater detail herein, the earnout provisions of the Master Transaction Agreement provide for the possibility that PS Spine may receive additional shares of Holdco common stock, which would cause former RTI stockholders ownership of Holdco to be further diluted. |

For more information regarding the risk associated with RTI stockholders’ and PS Spine unitholders’ reduced ownership in the combined company, see “Risk Factors—Risks Related to the Transaction and the Combined Company—RTI stockholders and PS Spine unitholders will have a reduced ownership and voting interest after the Transaction and will each exercise less influence over management”.

| Q: | Should I, as an RTI stockholder, send in my stock certificates now for the exchange? |

| A: | RTI stockholders are not required to take any action to receive shares of Holdco stock. At the effective time, each share of RTI common stock will automatically be converted into a share of Holdco common stock. Similarly, at the effective time, each share of RTI preferred stock will automatically be converted into a share of Holdco preferred stock. At the effective time, each valid certificate or certificates which immediately prior to the effective time represented any such shares of RTI common stock or RTI preferred stock ornon-certificated shares of RTI common stock or RTI preferred stock held in book entry form, shall automatically represent an equivalent number of shares of Holdco common stock or Holdco preferred stock, as applicable (without any requirement for the surrender of any such certificates ornon-certificated shares). |

| Q: | Is there an exchange agent for the Transaction? |

| A: | No. Because each valid certificate of RTI stock shall, upon the effective time, automatically represent an equivalent number of shares of Holdco common stock or Holdco preferred stock, as applicable, no exchange of RTI stock certificates for Holdco stock certificates will take place. Therefore, an exchange agent is not needed for the Transaction. |

| Q: | When do you expect the Transaction to be completed? |

| A: | We are currently targeting completion of the Transaction by the end of the first quarter of 2019, subject to the required RTI stockholder approval, the required written consent of PS Spine unitholders and the satisfaction or waiver of the other closing conditions. It is possible that factors outside the control of RTI or PS Spine could result in the Transaction being completed at a later time, or not at all. |

6

Table of Contents

| Q: | What effects will the Transaction have on RTI and Paradigm? |

| A: | Upon completion of the Transaction, RTI will cease to be a publicly traded company. Merger Sub will merge with and into RTI, with RTI surviving as a wholly owned subsidiary of Holdco. In addition, upon completion of the Transaction, Holdco will own all of the outstanding equity interests in Paradigm. As a result of the Transaction, RTI stockholders will own shares of Holdco and will not directly own any shares of RTI, and PS Spine will own shares of Holdco and will not directly own any equity interest in Paradigm. |

Following the completion of the Transaction, the registration of the RTI common stock and RTI preferred stock and their respective reporting obligations under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) will be terminated. In addition, following the completion of the Transaction, shares of RTI common stock will no longer be listed on the Nasdaq Global Select Market (“Nasdaq”) or any other stock exchange or quotation system. However, as explained below, we expect that Holdco common stock will be listed on the Nasdaq Global Market under the symbol “RTIX”.

Although current RTI stockholders will no longer be stockholders of RTI after the Transaction, current RTI stockholders will have an indirect interest in both RTI and Paradigm through their ownership of Holdco common stock or Holdco preferred stock. Likewise, although PS Spine will no longer directly own any equity interest in Paradigm, PS Spine will have an indirect interest in both RTI and Paradigm through its ownership of Holdco common stock.

| Q: | What effects will the Transaction have on Holdco? |

| A: | Upon completion of the Transaction, Holdco will become the holding company of RTI and Paradigm, and Holdco will be renamed “RTI Surgical Holdings, Inc.” We expect that Holdco common stock will be listed on the Nasdaq Global Market under the symbol “RTIX”. |

| Q: | Who will manage the combined company after the Transaction? |

| A: | The executive officers of RTI immediately prior to the closing will become the executive officers of Holdco as of the effective time. Camille I. Farhat is anticipated to remain as Chief Executive Officer of Holdco. The directors of RTI immediately prior to the closing, as well as Jeffrey C. Lightcap, who is currently a manager of PS Spine and Paradigm, will become the directors of Holdco as of the effective time. |

| Q: | What will happen to outstanding RTI equity awards in the Transaction? |

| A: | At the effective time, each RTI Stock Option that is outstanding immediately prior to the effective time, whether vested or unvested, will be converted into a stock option in respect of shares of Holdco common stock, on the same terms and conditions as were applicable under such RTI Stock Option immediately prior to the effective time (including with respect to vesting). At the effective time, each RTI Restricted Stock Award that is outstanding immediately prior to the effective time will be converted into a restricted stock award with the same terms and conditions as were applicable under such RTI Restricted Stock Award immediately prior to the effective time (including with respect to vesting). For more information, see the section entitled “The Master Transaction Agreement—Treatment of RTI Equity Awards”. |

| Q: | Will RTI stockholders or PS Spine unitholders be paid dividends prior to the Transaction? |

| A: | Pursuant to the Master Transaction Agreement, RTI is not permitted to declare, set aside or pay dividends or other distributions (whether payable in cash, stock, property or a combination thereof) in respect of the stock of RTI prior to the closing of the Transaction without the consent of PS Spine. Under RTI’s current credit agreement with JPMorgan Chase Bank, N.A. (“JPM”), as lender, it is restricted from paying dividends on its common stock without the prior written consent of the administrative agent. Pursuant to the Master Transaction Agreement, PS Spine is not permitted to declare any equity dividend in respect of the PS Spine units prior to the closing of the |

7

Table of Contents

| Transaction without the consent of RTI. Under Paradigm’s existing senior secured credit agreement, PS Spine is restricted from paying dividends or distributions to its unitholders. Any future dividends following the closing of the Transaction will be at the discretion of the Holdco board of directors (the “Holdco board”). |

| Q: | Are there any risks in the Transaction that I should consider? |

| A: | Yes. There are risks associated with all business combinations, including the Transaction between RTI and Paradigm. These risks are discussed in more detail in the section entitled “Risk Factors”. |

| Q: | What is householding and how does it affect RTI stockholders? |

| A: | The SEC permits RTI to deliver a single copy of its proxy statements and annual reports to RTI stockholders who have the same address and last name, unless RTI has received contrary instructions from such RTI stockholders. Each RTI stockholder will continue to receive a separate proxy card. This procedure, called “householding”, will reduce the volume of duplicate information RTI stockholders receive and reduce RTI’s printing and postage costs. RTI will promptly deliver a separate copy of this joint proxy and consent solicitation statement/prospectus to any such RTI stockholder upon written or oral request. A stockholder wishing to receive a separate joint proxy and consent solicitation statement/prospectus can notify RTI at RTI Surgical, Inc., 11621 Research Circle, Alachua, Florida 32615, Attention: Investor Relations, Molly Poarch, telephone: (386)418-8888. Similarly, RTI stockholders currently receiving multiple copies of these documents can request the elimination of duplicate documents by contacting RTI as described above. |

| Q: | When and where will the RTI special meeting be held? |

| A: | The RTI special meeting will be held at 520 Lake Cook Road, Suite 315, Deerfield, Illinois 60015, on March 7, 2019, at 10:00 a.m., local time. |

| Q: | Who is entitled to vote at the RTI special meeting? |

| A: | Only holders of record of RTI common stock and RTI preferred stock at the close of business on the RTI record date are entitled to notice of, and to vote at, the RTI special meeting and at any adjournment or postponement of the RTI special meeting. |

| Q: | How can I, as an RTI stockholder, attend the RTI special meeting? |

| A: | All RTI stockholders are invited to attend the RTI special meeting. You may be asked to present a valid photo identification, such as a driver’s license or passport, before being admitted to the RTI special meeting. If you hold your RTI shares in “street name”, you also may be asked to present proof of ownership to be admitted to the RTI special meeting. A brokerage statement or letter from your broker, bank, trust company or other nominee proving ownership of the shares on the RTI record date are examples of proof of ownership. To help RTI plan for the RTI special meeting, please indicate whether you expect to attend by responding affirmatively when prompted during Internet or telephone proxy submission or by following the instructions included on your proxy card. |

| Q: | What proposals will be considered at the RTI special meeting? |

| A: | At the RTI special meeting, RTI stockholders will be asked: |

| • | to consider and vote on a proposal to adopt the Master Transaction Agreement, a copy of which is attached asAnnex A to this joint proxy and consent solicitation statement/prospectus, and to approve the transactions contemplated thereby, including the Merger (see the section entitled “RTI Proposal 1: Merger Proposal”); |

8

Table of Contents

| • | to consider and vote upon a proposal to approve, for purposes of complying with applicable provisions of Nasdaq Listing Rule 5635, the potential issuance of more than twenty percent (20%) of Holdco’s issued and outstanding common stock in connection with the transactions contemplated by the Master Transaction Agreement (see the section entitled “RTI Proposal 2: Share Issuance Proposal”); and |

| • | to consider and vote upon a proposal to adjourn the RTI special meeting, if necessary or appropriate, including to permit further solicitation of proxies in favor of the Merger Proposal or the Share Issuance Proposal if there are insufficient votes at the time of the RTI special meeting to approve the Merger Proposal or the Share Issuance Proposal (see the section entitled “RTI Proposal 3: Meeting Adjournment Proposal”). |

RTI will not transact other business at its special meeting, except such other business as may properly be brought before the RTI special meeting or any adjournments or postponements thereof.

| Q: | How does the RTI board of directors recommend that I vote? |

| A: | The RTI board of directors (the “RTI board”), on October 30, 2018, unanimously approved and adopted the Master Transaction Agreement and the transactions contemplated thereby, including the Merger, on the terms and subject to the conditions set forth therein, determined and declared that the terms of the Master Transaction Agreement and the transactions contemplated thereby, including the Merger, are advisable and in the best interests of RTI and its stockholders, and recommended that RTI stockholders approve and adopt the Master Transaction Agreement and the transactions contemplated thereby, including the Merger. The RTI board unanimously recommends that RTI stockholders vote “FOR” each of the Merger Proposal, the Share Issuance Proposal and the Meeting Adjournment Proposal. |

| Q: | How many shares of RTI common stock and RTI preferred stock are eligible to be voted? |

| A: | As of January 15, 2019, there were 62,245,112 shares of RTI common stock outstanding and entitled to vote at the RTI special meeting (including 1,056,028 unvested restricted shares of RTI common stock), held by approximately 291 holders of record. Each holder of RTI common stock is entitled to one vote for each share of RTI common stock owned as of the RTI record date. This joint proxy and consent solicitation statement/prospectus includes and contains calculations based upon shares of RTI common stock outstanding and entitled to vote and holders of record as of January 15, 2019, the most recent practicable date prior to the date of filing of this joint proxy and consent solicitation statement/prospectus. RTI does not believe such totals will change materially as of the RTI record date and undertakes to file a Current Report on Form 8-K with such updated totals promptly after the RTI record date. |

As of the RTI record date, there were 50,000 shares of RTI preferred stock outstanding and entitled to vote at the RTI special meeting, held by one holder of record. Each holder of RTI preferred stock is entitled to 239 votes for each share of RTI preferred stock owned as of the RTI record date.

| Q: | What vote is required to approve each RTI proposal? |

| A: | Assuming a quorum is present, the Merger Proposal requires (i) the affirmative vote of the holders of a majority of the outstanding shares of RTI common stock and RTI preferred stock (on a fully converted basis) entitled to vote thereon and (ii) the written consent or affirmative vote of the holders of a majority of the outstanding shares of RTI preferred stock entitled to vote thereon, voting separately as a class. Abstentions and brokernon-votes will have the same effect as a vote “AGAINST” the Merger Proposal. |

Assuming a quorum is present, the Share Issuance Proposal requires (i) the affirmative vote of a majority of votes cast on the proposal by RTI common stock and RTI preferred stock (on a fully converted basis) and (ii) the written consent or affirmative vote of the holders of a majority of the outstanding shares of RTI preferred stock, voting separately as a class. Abstentions will have (i) the same effect as a vote “AGAINST” the Share Issuance Proposal for holders of RTI preferred stock, voting separately as a class and (ii) no effect on the Share Issuance Proposal for the holders of RTI common stock and RTI preferred stock (on a fully converted basis). Brokernon-votes will have (i) the same effect as a vote “AGAINST” the Share Issuance Proposal for holders of RTI preferred stock, voting separately as a class and (ii) no effect on the Share Issuance Proposal for the holders of RTI common stock and RTI preferred stock (on a fully converted basis).

9

Table of Contents

Assuming a quorum is present, the Meeting Adjournment Proposal requires the affirmative vote of the holders of a majority of the shares having voting power present in person or represented by proxy at the RTI special meeting. Abstentions will have the same effect as a vote “AGAINST” the Meeting Adjournment Proposal, and brokernon-votes will not affect the outcome of the vote on the Meeting Adjournment Proposal.

| Q: | How do I, as an RTI stockholder, vote? |

| A: | If you are a holder of record of RTI shares as of the RTI record date, you may vote in person by attending the RTI special meeting. Shares held beneficially in street name may be voted by you in person at the RTI special meeting only if you obtain a legal proxy from the broker, trustee or nominee that holds your shares giving you the right to vote the shares. Even if you plan to attend the RTI special meeting, RTI recommends that you also submit your proxy or voting instructions as described below so that your vote will be counted if you later decide not to attend the special meeting. |

Whether you hold shares directly as the stockholder of record or beneficially in street name, you may direct how your shares are voted without attending the RTI special meeting. If you are an RTI stockholder of record, you may vote by submitting a proxy by one of the methods described below. If you hold shares beneficially in street name, you may vote by submitting voting instructions to your broker, trustee or nominee.

| • | By Internet- RTI stockholders of record with internet access may submit proxies by following the “Vote by Internet” instructions on their proxy cards. Most RTI stockholders who hold shares beneficially in street name may vote by accessing the web site specified on the voting instruction cards provided by their brokers, trustees or nominees. |

| • | By Telephone-RTI stockholders of record who live in the United States or Canada may submit proxies by following the “Vote by Phone” instructions on their proxy cards. Most RTI stockholders who hold shares beneficially in street name and live in the United States or Canada may vote by phone by calling the number specified on the voting instruction cards provided by their brokers, trustees or nominees. |

| • | By Mail- RTI stockholders of record may submit proxies by completing, signing and dating their proxy cards and mailing them in the accompanyingpre-addressed envelopes. RTI stockholders who hold shares beneficially in street name may vote by mail by completing, signing and dating the voting instruction cards provided by their brokers, trustees or nominees and mailing them in the accompanyingpre-addressed envelopes. |

| Q: | What will happen if I, as an RTI stockholder, abstain from voting? |

| A: | Assuming a quorum is present, abstentions will have (i) the same effect as (A) a vote “AGAINST” the Merger Proposal and the Adjournment Proposal, and (B) a vote “AGAINST” the Share Issuance Proposal for holders of RTI preferred stock, voting separately as a class and (ii) no effect on the Share Issuance Proposal for the holders of RTI common stock and RTI preferred stock (on a fully converted basis). Brokernon-votes will have no effect on the outcome of the proposals, assuming a quorum is present, except with respect (i) to the Merger Proposal and (ii) the vote of the RTI preferred stock, voting separately as a class, on the Share Issuance Proposal, in each case, whichbroker-non votes will have the same effect as a vote “AGAINST” such proposal. |

| Q: | What constitutes a quorum? |

| A: | The holders of a majority of the outstanding shares of RTI common stock and RTI preferred stock (on anas-converted basis) entitled to vote at the RTI special meeting, either present in person or represented by proxy, will constitute a quorum. Both abstentions and brokernon-votes are counted for the purpose of determining the presence of a quorum. |

| Q: | If my shares are held in “street name” by my broker, will my broker automatically vote my shares for me? |

| A: | No. If your brokerage firm, bank or other similar organization is the holder of record of your shares (i.e., your shares are held in “street name”), you may instruct the holder of record to vote your RTI shares by following the |

10

Table of Contents