Table of Contents

As filed with the Securities and Exchange Commission on January 8, 2021.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

INTERIOR LOGIC GROUP HOLDINGS, LLC

to be converted as described herein to a corporation named

Interior Logic Group Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 1520 | 82-5478232 | ||

| (State or other jurisdiction of incorporation or organization | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

10 Bunsen

Irvine, California 92618

(800) 959-8333

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Alan K. Davenport

Chief Executive Officer and Chairman

Interior Logic Group Holdings, LLC

10 Bunsen

Irvine, California 92618

(800) 959-8333

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to

| Robin M. Feiner, Esq. Holland & Knight LLP 31 W. 52nd St. 12th floor New York, New York, 10019 (212) 513-3200 | Richard Strulson, Esq. Executive Vice President, General Counsel and Chief Compliance Officer Interior Logic Group Holdings, LLC 10 Bunsen Irvine, California 92618 (800) 959-8333 | Michael J. Zeidel, Esq. Skadden, Arps, Slate, Meagher & Flom LLP One Manhattan West New York New York 10001 (212) 735-3000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

| ||||

| Title of Each Class of Securities to be Registered | Proposed Maximum Offering Price(1)(2) | Amount of Registration Fee | ||

Common stock, $0.01 par value per share | $100,000,000 | $10,910 | ||

| ||||

| ||||

| (1) | Estimated solely for purposes of determining the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes the aggregate offering price of shares of common stock that may be purchased by the underwriters pursuant to their option to purchase additional shares of common stock. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

Interior Logic Group Holdings, LLC, the registrant whose name appears on the cover of this Registration Statement, is a Delaware limited liability company. Prior to the effectiveness of this Registration Statement, Interior Logic Group Holdings, LLC will convert into a Delaware corporation and be renamed Interior Logic Group Holdings, Inc. (the “Corporate Conversion”). Shares of common stock of Interior Logic Group Holdings, Inc. are being offered by the prospectus. Except as otherwise disclosed in the prospectus, the consolidated financial statements and selected historical financial data and other financial information included in this Registration Statement are those of Interior Logic Group Holdings, LLC and its respective subsidiaries, as the case may be, and do not give effect to the Corporate Conversion.

Table of Contents

The information contained in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION, DATED JANUARY 8, 2021 |

Shares

Interior Logic Group Holdings, Inc.

Common Stock

This is the initial public offering of our common stock. We are offering shares of our common stock.

No public market currently exists for our common stock. We have applied to list our common stock on the Nasdaq Global Select Market under the symbol “ILG.”

We currently expect the initial public offering price to be between $ and $ per share.

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 23 of this prospectus.

| Per Share | Total | |||||||

Public offering price | $ | $ | ||||||

Underwriting discounts and commissions(1) | $ | $ | ||||||

Proceeds, before expenses, to us | $ | $ | ||||||

| (1) | See “Underwriting” for a complete description of the compensation payable to the underwriters. |

The underwriters may also purchase up to an additional shares of our common stock from us at the public offering price, less underwriting discounts and commissions, within 30 days from the date of this prospectus. If the underwriters exercise this option in full, the total underwriting discounts will be $ , and the total proceeds, after underwriting discounts but before expenses, to us will be $ .

Neither the Securities and Exchange Commission nor any state securities commission or other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on or about , 2021.

| Citigroup | Goldman Sachs & Co. LLC | BofA Securities |

| Baird | Evercore ISI | Jefferies | RBC Capital Markets | Stephens Inc. | Truist Securities | UBS Investment Bank |

Table of Contents

You should rely only on the information contained in this prospectus and any free writing prospectus we may authorize to be delivered to you. We have not, and the underwriters have not, authorized anyone to provide you with information different from, or in addition to, that contained in this prospectus and any related free writing prospectus. We and the underwriters take no responsibility for, and can provide no assurances as to the reliability of, any information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is only accurate as of the date of this prospectus, regardless of the time of delivery of this prospectus and any sale of shares of our common stock.

| 1 | ||||

| 23 | ||||

| 56 | ||||

| 58 | ||||

| 59 | ||||

| 60 | ||||

| 62 | ||||

| 64 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 66 | |||

| 90 | ||||

| 109 | ||||

| 117 | ||||

| 132 | ||||

| 135 | ||||

| 137 | ||||

| 142 | ||||

| 144 | ||||

| 148 | ||||

| 155 | ||||

| 155 | ||||

| 155 | ||||

| F-1 |

Presentation of Market and Industry Data and Certain Definitions

We use market data and industry forecasts and projections throughout this prospectus, particularly in the sections entitled “Prospectus Summary,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Our Business.” The industry and market data are based on the good faith estimates of our management, research studies and surveys, independent industry publications and other publicly available information. Industry publications and research studies and surveys generally state that they have been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. These data involve a number of assumptions and limitations, and investors are cautioned not to give undue weight to such estimates. Although we have not independently verified the accuracy or completeness of any third-party information, we believe that the information from these publications and studies included in this prospectus is generally reliable, and the conclusions contained in the third-party information are reasonable. In addition, projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of

i

Table of Contents

factors, including those described in the section entitled “Risk Factors” and elsewhere in this prospectus. In particular, some of the market and industry estimates in this prospectus were prepared prior to the COVID-19 pandemic. These and other factors could cause results to differ materially from those expressed in the estimates made by independent parties and by us. We expect that the COVID-19 pandemic may continue to materially reduce the growth of various of the markets discussed in this prospectus, and we cannot predict the extent to which these estimates will be affected. These and other factors could cause results to differ materially from those expressed in, or implied by, the estimates made by independent parties and by us. Furthermore, we cannot assure you that a third party using different methods to assemble, analyze or compute industry and market data would obtain the same results. See “Information Regarding Forward-Looking Statements.”

In this prospectus, we present a variety of housing market indicators, including housing starts and home closings.

| • | A housing start is counted at the point in time excavation begins for the footings or foundation of a home. |

| • | A home closing is counted when the new homeowner takes title to the home. |

Housing starts are considered a leading indicator of the state of the housing market. Rankings of MSAs (as defined below) by 2019 single-family housing starts are based on estimated 2019 single-family housing starts per MSA published in Metrostudy’s September 2020 Builder Home Building Outlook.

References to a housing market mean a Metropolitan Statistical Area (“MSA”), which is an area that generally consists of at least one urbanized area of 50,000 or more inhabitants, plus adjacent territory that has a high degree of social and economic integration with the core area as measured by commuting ties. MSA boundaries are based on U.S. Census Bureau determinations as of March 2020. References to our “geographic markets” mean the MSAs we serve. References to our “turnkey” supply chain management and installation services mean the provision of both materials and workforce sold together.

References to the largest homebuilders are based on Builder Magazine’s 2020 Builder 100 list, which ranks U.S. homebuilders based on total number of home closings.

We calculate the size of the approximately $23 billion U.S. new home interior finish solutions industry by multiplying the average installed cost of flooring, cabinets and countertops in a new single-family home in 2019, which was approximately $25,500 according to the National Association of Homebuilders (the “NAHB”), by the number of 2019 single-family housing starts (approximately 887,700 based on U.S. Census Bureau data).

In this prospectus, we define a “direct” competitor as a company whose primary business is the provision of residential design services and the supply and installation of multiple categories of interior finishes.

In this prospectus, we refer to our “design studio solutions” and “builder direct solutions.” We define our design studio solutions as our full suite of design, supply chain management and installation services, including our dedicated builder-branded and shared ILG-branded design studios where we interface directly with homebuyers in the design process. We define our builder direct solutions as our supply chain management and installation services for homebuilders. Some of our customers start as builder direct customers and then convert to our design studio solutions.

Service Marks, Trademarks and Trade Names

This prospectus includes trademarks and service marks owned by us and our subsidiaries, as well as trademarks, trade names and service marks of other companies, which are the property of their respective owners. Solely for convenience, trademarks, trade names and service marks referred to in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these

ii

Table of Contents

trademarks, trade names and service marks. We do not intend our use or display of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

The Business Combination

On May 31, 2018, we consummated a business combination transaction (the “Business Combination”) where Interior Specialists, Inc. (“ISI”) acquired Interior Logic Group, Inc. (“ILG”) and combined under a new holding company, Interior Logic Group Holdings, LLC (“ILG Holdings”), pursuant to a Contribution Agreement (the “Contribution Agreement”) dated April 30, 2018, by and among Faraday Holdings, LLC (“Faraday”), Installation Services Holdings, LLC (“ISH”), ISI, Installation Services Holdings, Inc., (the parent company of ILG), and ILG Holdings.

We refer to the business of ISI prior to the Business Combination as “legacy ISI” and the business of ILG prior to the Business Combination as “legacy ILG.” Unless otherwise indicated, or the context otherwise requires, references to “we,” “us,” “our,” or the “Company” refer to (i) with respect to periods prior to the Business Combination, legacy ISI, (ii) with respect to periods beginning with the completion of the Business Combination and ending immediately before the completion of our Corporate Conversion (as defined below), Interior Logic Group Holdings, LLC and its subsidiaries, and (iii) with respect to periods beginning with the completion of our Corporate Conversion and thereafter, Interior Logic Group Holdings, Inc. and its consolidated subsidiaries. In accordance with Rule 3-05 of Regulation S-X, separate financial statements are not required for any of our acquisitions individually or in the aggregate.

Prior to the Business Combination, for the fiscal year ended December 31, 2017, legacy ILG had revenues of $566 million and nearly 1,600 employees, while legacy ISI had revenues of $852 million and nearly 2,600 employees. At the time of the Business Combination, legacy ILG was legacy ISI’s largest direct competitor.

Basis of Presentation

Our consolidated financial statements accompanying this prospectus have been prepared in accordance with accounting principles generally accepted in the United States of America, or GAAP, and include the accounts of the Company and its wholly-owned subsidiaries. All significant intercompany transactions have been eliminated in consolidation. Our consolidated financial statements are based on a fiscal year ending December 31.

Additional information regarding our financial performance and non-GAAP measures, including reconciliations of non-GAAP measures to their most directly comparable GAAP measure, is included in “Non- GAAP Financial Measures” and in “Summary Historical Financial Data.” In addition, such financial information should be read in conjunction with the disclosures set forth under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes appearing elsewhere in this prospectus.

Non-GAAP Measures

In addition to the results reported in accordance with GAAP, we have provided information in this prospectus relating to Adjusted EBITDA and Adjusted EBITDA margin.

We define EBITDA as earnings before interest, income taxes, depreciation and amortization. We define “Adjusted EBITDA” as EBITDA, adjusted for acquisition and integration costs, share-based compensation, management fees, pre-opening costs, refinancing costs and expenses associated with the submission of our prior draft registration statement to the SEC, which was discontinued. To calculate Adjusted EBITDA for the nine-month period ended September 30, 2020, we further adjusted EBITDA for direct COVID-19-related costs, which represent charges for severance costs, remote connectivity and health and safety modifications within our facilities, all of which are clearly and directly related to COVID-19 and are incremental and separable from

iii

Table of Contents

normal operations. To calculate Adjusted EBITDA for 2018, we further adjusted EBITDA for an impairment charge resulting from our rebranding in connection with our Business Combination. Adjusted EBITDA measures performance by adjusting EBITDA for certain income or expense items that are not considered part of our core operations.

Adjusted EBITDA margin takes Adjusted EBITDA and divides it by revenues. We believe that the presentation of these measures provides useful information to investors regarding our results of operations because it assists both investors and us in analyzing and benchmarking the performance and value of our business. We also believe these measures are useful to investors and us as measures of comparative operating performance from period to period, as they measure our changes in pricing decisions, cost controls and other factors that impact operating performance, and they remove the effect of our capital structure (primarily interest expense), asset base (primarily depreciation and amortization), items outside our control (primarily income taxes) and the volatility related to the timing and extent of other activities, such as asset impairments, and non-core income and expenses, such as acquisition and integration expenses. Accordingly, we believe that these measures are useful for comparing general operating performance from period to period. In addition, we use various Adjusted EBITDA- based measures in determining certain of our incentive compensation programs. Other companies may define Adjusted EBITDA and Adjusted EBITDA margin differently and, as a result, our measures may not be directly comparable to measures of other companies. In addition, Adjusted EBITDA may be defined differently for purposes of covenants contained in our Revolving Credit Facility or any future indebtedness.

Although we use these measures to assess the performance of our business, the uses of the measures are limited because they do not include certain material expenses, such as interest and taxes, necessary to operate our business. Adjusted EBITDA and Adjusted EBITDA margin should be considered in addition to, and not as substitutes for, net income (loss) in accordance with GAAP as a measure of performance. Our presentation of these measures should not be construed as an indication that our future results will be unaffected by unusual or non-recurring items.

These measures have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our results as reported under GAAP. Because of these limitations, these measures are not intended as alternatives to net income (loss) as indicators of our operating performance, as alternatives to any other measure of performance in conformity with GAAP or as alternatives to cash flow provided by operating activities as measures of liquidity. You should therefore not place undue reliance on these measures or ratios calculated using those measures.

iv

Table of Contents

This prospectus summary highlights certain information appearing elsewhere in this prospectus. As this is a summary, it does not contain all of the information that you should consider in making an investment decision.

You should read the entire prospectus carefully, including the information under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes thereto included elsewhere in this prospectus, before investing. This prospectus includes forward-looking statements that involve risks and uncertainties. See “Information Regarding Forward-Looking Statements.”

Our Vision

Our vision is to utilize our value-added technology platform combined with our national footprint and customer relationships to revolutionize the way homebuyers purchase and design their homes. By seamlessly connecting key constituents in the housing lifecycle, including homebuilders, homebuyers, suppliers and subcontractors, we believe we can unlock significant market opportunities.

Our Company

We are the leading national provider of technology-enabled sales and marketing, design and installation solutions for homebuilders. Our robust technology platform delivers interior design visualization, interior option selection, supply chain management and data analytics solutions from initial homebuyer engagement through the construction and delivery of homes. We are also the leading national installer for select high-value and aesthetically important interior finishes, such as flooring, cabinets and countertops, to our homebuilder customers, as well as multi-family, commercial and repair & remodel customers. Our scalable technology solutions enhance the homebuying experience, streamline the homebuying process and meaningfully drive homebuyer satisfaction, while improving homebuilders’ profitability, construction quality and cycle times. We serve a broad range of national, regional and local homebuilders across the home price spectrum, from entry-level to move-up and luxury homes, including each of the 20 largest U.S. homebuilders. We have the leading position in the estimated $23 billion U.S. new home interior finish solutions industry, and our technology solutions significantly expand our addressable market to other economic transactions associated with the housing lifecycle, including new construction pre-sales marketing, monetization of valuable consumer data and providing access to homebuyers for future design and renovation needs, amongst others. We generated 2019 revenues, net loss and Adjusted EBITDA of $1,785.4 million, $(15.8) million and $123.2 million, respectively.1

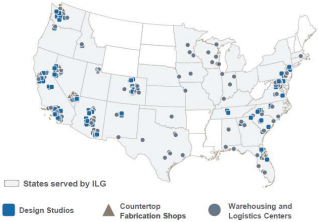

We have built the most expansive national footprint in our highly fragmented industry, which uniquely positions us to serve our national, regional and local homebuilding customers consistently and effectively across markets. Furthermore, we collect, analyze and report valuable data on over 100,000 new homes annually, creating the largest repository of homebuyer design preference data in our industry. Our national network is comprised of 110 design studios, 109 warehousing and logistics centers and nine countertop fabrication facilities, from which we serve approximately 285 Metropolitan Statistical Areas (“MSAs”), including 46 of the top 50 U.S. homebuilding markets based on 2019 single-family housing starts. We are more than three times the size of our next largest direct competitor, based on number of locations. With an estimated market share today of only 6% based on 2019 single-family residential revenues, we believe we have significant runway for growth.

Our design studios serve to manage a key part of the homebuying process where homebuyers design, select and upgrade the interior finishes of their new home. We operate 64 builder-branded design studios on behalf of

| 1 | For a definition of Adjusted EBITDA, as well a reconciliation to the most directly comparable GAAP measure, see “Non-GAAP Measures” and “—Summary Historical Financial Data.” |

1

Table of Contents

20 homebuilders across the country, as well as 46 ILG-branded design studios that provide the same profesionally-managed design experience for multiple homebuilders in a single location.

The following map illustrates our expansive national footprint.

We have an experienced team of approximately 4,200 employees, including approximately 300 design professionals and approximately 470 field managers, and utilize approximately 9,000 independent installation subcontractors. Additionally, our technology team includes approximately 140 software engineers, digital artists and technology specialists that facilitate the continual advancement of our industry-leading technology platform. In order to accelerate development of our technology solutions, we have added 40 new members to the technology team in 2020 alone and expect to continue to grow this group in 2021.

Our differentiated technology suite simplifies and enhances the home buying experience and has positioned us at the forefront of digitization in the homebuilding industry. Advancements in visualization technology and younger demographics reaching peak homebuying age have led to increasing demand for a more virtual homebuying and home design experience in recent years. Additionally, we believe the COVID-19 pandemic has been a catalyst for virtual engagement by homebuyers, resulting in a substantial increase in the use of our technology platform by our customers. We adapted our business model quickly to meet the increased demand for fully virtual offerings and we believe we will continue to benefit from our innovative business model. Many of our homebuilding customers are also reporting substantial increases in website traffic, virtual tours, and full virtual sales. Homebuyers are now spending, on average, four hours in our web-based design and option selection systems—a 24% increase in system usage in 2020 compared to 2019. Similarly, we have seen a notable increase in the percentage of our homebuyers who have completed their interior option selections via fully virtual appointments utilizing our technology platform in 2020 compared to 2019. Nearly 10% of all design sessions are now conducted virtually and the demand for online design appointments continues to increase. We believe we have the leading end-to-end technology platform that meets this demand and delivers a dynamic, digitally-enabled homebuying experience. Our engaging visualization technology allows homebuilders to offer photo-realistic virtual home tours as a marketing tool, eliminating the need to build costly model homes for every community, accelerating the pre-marketing window for each community and potentially shortening the overall sales cycle. Our cutting-edge option selection tools utilize visualization and real-time pricing technology to create a personalized, user-friendly design experience customized to the homebuyer’s community, floor plan and budget. Our streamlined integration with homebuilder back office systems creates valuable connectivity throughout the construction process, allowing us to improve construction quality, decrease cycle times and increase customer stickiness. In addition, our systems collect, analyze and report on vast quantities of valuable data, including homebuyer design preferences on over 100,000 new homes annually, which empowers

2

Table of Contents

homebuilders and suppliers with critical insight into evolving homebuyer preferences. Homebuilders use our proprietary analytics to tailor their product offerings and pricing by community to further drive incremental option sales and improve profitability. We have made significant technology investments to build our differentiated and scalable technology platform, which we believe will continue to further enhance our profitability and grow our revenue as we expand our footprint with existing and future customers and add new technology solutions.

We have grown considerably, more than doubling our business over the past three years, both organically and through acquisitions. Our organic growth has been driven by the addition of new design studios, new customer additions and increased penetration of existing customers, all of which is underpinned by our expanding technology offering. Technology-enabled solutions have further accelerated our organic growth, and adoption of these solutions by leading homebuilders has contributed to significant growth in our revenue generated by the top 10 U.S. homebuilders from 2015 to 2019. Our recent technology developments, including our photo-realistic visualization technology, have the potential to significantly accelerate the digitization of the homebuilding industry and drive further organic growth through increased adoption by new and existing homebuilders. In addition to our organic growth, we believe we are an acquirer of choice in our industry. We have completed over 18 acquisitions since 2013, which is more than any of our direct competitors, and we believe we have the opportunity to execute additional accretive acquisitions in our highly fragmented industry.

Historically, we have leveraged successful partnerships with homebuilders in specific markets to expand into additional geographies and product categories, which generally increases our profit margins by leveraging our infrastructure and personnel across a denser geographic footprint. We do not currently offer installation services for all three key product categories (i.e. flooring, cabinets and countertops) in all of our existing geographic markets. As such, we believe that expanding our service offering to capture incremental installation services offers significant growth opportunities. We also intend to drive margin expansion through purchasing efficiencies, economies of scale on both a local and national basis and the continued consolidation to a single integrated technology platform across our geographic markets.

3

Table of Contents

Our Value Proposition

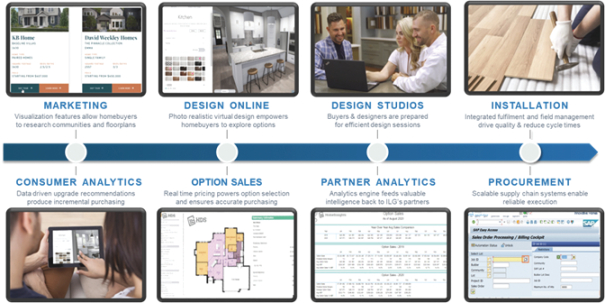

The chart and graphic below summarize our value proposition and the technology-enabled solutions we deliver to the key constituents in the homebuilding value chain.

Constituent | ILG Value Proposition | |

Homebuilders | • Streamline marketing, sales generation, and design process • Improved homebuyer satisfaction levels • Maximize option profitability • Improve cycle times • Provide valuable data analytics and insights | |

Homebuyers | • Fully customize their home design and furnishings • Improve homebuyer satisfaction • Leverage fully remote visualization tools for options selection • Access to designers to facilitate decision making | |

Designers | • Collaborate on home design process • Ability to work with homebuyers in virtual setting • Real-time pricing capabilities • Data analytics inform design decisions | |

Suppliers | • Predictive analytics on homebuyer trends • Ability to showcase products in a physical or virtual design studio • Integrated systems facilitate efficiencies • Real-time pricing capabilities | |

Installers | • Provide consistent, predictable work • Increase productivity through technology | |

4

Table of Contents

Our comprehensive suite of solutions provides meaningful value to each of the following constituencies:

Homebuilders

We have long-standing customer relationships with national, regional and local homebuilders as a result of our proven ability to drive increased homebuilder profitability through our technology solutions. We provide customized, value-added design studio solutions, critical insight into homebuyer demand trends and superior service, from pre-sale marketing to homebuyer option selection to supply chain management and installation. Homebuilders benefit from our valuable design expertise and installation capabilities, allowing them to focus on their core competencies in land procurement and development, home sales and construction management. Our visualization technology offers builders the ability to provide photo-realistic virtual tours of multiple floorplans to prospective homebuyers without needing to visit a physical model home. Our option selection technology, real-time pricing engine, and skilled design professionals enhance the homebuyer experience and drive homebuilder profitability by increasing sales of options and upgrades, while our turnkey supply chain management and installation services drive construction quality and process efficiencies. On average, buyers who use our online systems spend 25% more on interior options and upgrades compared to buyers that do not. We also offer supply chain management and installation services to homebuilders through our builder direct solutions, where our customers benefit from our extensive supplier relationships, service excellence and multi-product capabilities. Our streamlined integration with homebuilder back office systems helps our customers and our teams improve construction quality, decrease cycle times and increase customer stickiness. We complement our integration capabilities with extensive data analytics to offer insight into evolving design trends and homebuyer preferences and assist homebuilders in optimizing their option offerings and making home design and community investment decisions. Our ability to deliver fully-integrated services enhances our ability to retain customers over time.

We serve each of the top 20 U.S. homebuilders based on 2019 home closings. The top 20 U.S. homebuilders accounted for approximately 30% of total home closings in 2019, up from approximately 17% in 2000, according to Builder Magazine Online. We believe this increase in market share is due to the largest homebuilders benefiting from the financial and operational efficiencies associated with combining a national platform and local market concentration in the nation’s most attractive housing markets.

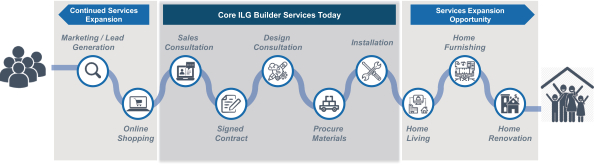

Approximately 80% of our 2019 revenues were derived from sales to the new single-family residential market. The following graphic illustrates the critical link we represent in the interior finish value chain for homebuilders.

Homebuyers

Our direct and personal interactions with homebuyers enable us to meaningfully drive homebuyer satisfaction. Our design studio solutions streamline the often disjointed and overwhelming option selection

5

Table of Contents

process by creating a personalized and well-organized design experience. We offer tailored option selection tools, ranging from self-guided web portals for browsing interior finishes to one-on-one appointments with trained design professionals, which can take place in strategically laid out and conveniently-located showrooms or through virtual meetings. Homebuyers benefit from our design expertise and user-friendly visual selection tools that allow them to experience photo-realistic interior finish options and compare real-time pricing for options that are customized to their community and floor plan. Once option selections are made, our turnkey installation services facilitate timely and high-quality completion for the homebuyer.

Suppliers and Installers

We maintain strong relationships with our broad supplier base and we are the largest new single-family residential customer for many of our suppliers. Our supplier relationships typically are negotiated at the national level but coordinated at the regional level, driving both local efficiency and overall cost-effectiveness. We provided interior finishes for more than 100,000 new single-family homes in 2019, which is more than any U.S. homebuilder; the breadth of our direct homebuyer interactions enables us to provide suppliers with valuable insight into homebuyers’ evolving preferences. Suppliers value our ability to help them optimize product offerings to be leaders in the latest design trends. In addition, we believe independent installers are eager to work with us due to our extensive customer-base, consistent job volumes and rapid payments, which we believe is a competitive advantage in an increasingly competitive workforce market.

Multi-Family, Commercial and Repair & Remodel Customers

In addition to single-family homebuilders, we are a critical partner to a broad range of multi-family, commercial and repair & remodel customers, including new multi-family and light commercial contractors, multi-family owners and operators, senior living operators, home improvement retailers, single-family rental operators and single-family repair & remodel customers, where homeowners spend over $330 billion annually to repair and renovate their homes according to the Joint Center for Housing Studies of Harvard University. We provide turnkey supply chain management and installation services for these customers across a wide range of project types and job sizes. Whether we are managing the interior finish installation process for a large new multi-family apartment complex or providing replacement flooring on a tight timeline for single-family rental home turnover, we offer a streamlined process and high-quality end result from a trusted provider. In addition, we provide customized technology solutions such as online ordering options for property managers. We leverage our infrastructure to cost-effectively serve this customer base across multiple markets with strong service levels, efficiency and valuable local expertise.

Our Industry

The interior finish solutions industry is a large, growing and highly fragmented market in which we are the leading national provider. We primarily serve the new single-family residential market, while also serving the new multi-family residential, commercial, and repair & remodel markets. The average installed cost of flooring, cabinets and countertops in a new single-family home was approximately $25,500 in 2019, according to the NAHB. Assuming 2019 U.S. single-family housing starts of approximately 887,700 based on U.S. Census Bureau data, this implies a potential addressable market of approximately $23 billion, with future upside through the addition of adjacent product categories, increases in interior finish spend per home and incremental housing volumes. Additionally, our technology solutions significantly expand our addressable market to include other economic transactions associated with the housing lifecycle including new construction pre-sales marketing, monetization of valuable consumer data and the provision of access to homebuyers for future design and renovation needs, amongst others.

Purchasing and designing or renovating a home has historically been facilitated by model homes and physical design studios. While our services today are largely delivered through physical design studios, we are

6

Table of Contents

seeing an increased shift towards digitization and a more virtual and technology-oriented model, driven by evolving homebuyer preferences. We believe that the long-term shift to digital solutions is fundamentally changing our market, with more homebuyers and homeowners preferring to review options and make design selections online. Beyond the convenience that comes with making selections virtually, our options selection tools, powered by our visualization technology, provide a more visual and real-time experience, allowing homebuyers and homeowners to see digital renderings of their designs rather than relying on samples and swatches. The ongoing shift in preference towards digital solutions is especially true for younger homebuyers and homeowners. In a recent survey from the National Association of Realtors, approximately 30% of those in younger demographics stated that they would be comfortable buying a house completely virtually. These long-term shifts have accelerated in the current COVID-19 pandemic with social distancing guidelines. We expect that these trends will lead to significant interest from both homebuilders and homeowners to increasingly implement digital solutions in the process of purchasing and designing a new home.

New Single-Family Residential Market

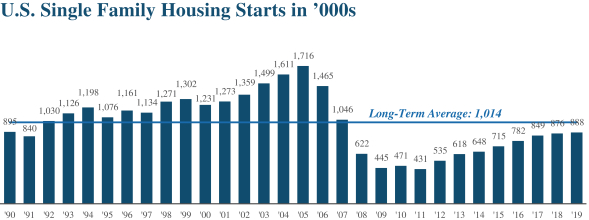

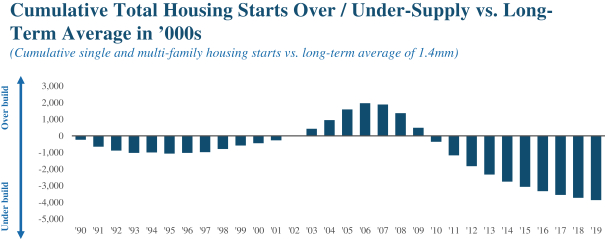

The new single-family residential market, valued at approximately $306 billion as of September 2020, is the primary market in which we operate. According to the NAHB and the U.S. Census Bureau, since 2011, cumulative net U.S. household formations have exceeded total housing starts by greater than 1.5 million units, leading to a significant backlog of demand for new housing. We expect the continued growth in the overall population, the aging of approximately 70 million millennials into their prime household formation and homeownership years, and the long-term effects of the COVID-19 pandemic to provide support for continued growth in new single-family residential construction. In addition to the long-term effects of COVID-19 on the industry, the public homebuilders are currently experiencing a significant rebound in net new orders. We typically benefit from an increase in net new orders once those homes are completed, which have historically averaged approximately 6 months after an initial order, and therefore we believe the current trends will benefit us in 2021. Furthermore, public homebuilding companies have reported increasing backlog value throughout 2020, which further supports increased deliveries in 2021.

Single-family housing starts remain below their long-term historical average and, according to the NAHB, are projected to grow at a 3.9% compound annual growth rate (CAGR) from 2020 to 2022. In addition, our large homebuilder customers have been gaining market share due to a long-term shift in the way homeowners approach the home purchasing process.

Source: U.S. Census Bureau Historical Data.

7

Table of Contents

Source: U.S. Census Bureau Historical Data.

Repair & Remodel, Multi-Family and Commercial Markets

The residential repair & remodel market has been growing at a 4% CAGR since 2014. According to the Joint Center for Housing Studies of Harvard University, homeowner improvement and repair spend is expected to be approximately $338 billion in 2020. As new home construction has lagged historical build averages over the last decade, the average home age has steadily increased to over 40 years in the U.S. which we expect to result in an increase in repair and remodel spend over time. The market is also supported in the near term by a greater portion of the population staying at home due to the COVID-19 pandemic and spending incremental income on home repairs and renovations. Our core categories (flooring, cabinets and countertops) are typically high-priority items for homeowners to renovate due to their high visibility. We also expect continued growth in the multi-family repair & remodel market, driven primarily by the age of the housing base, with approximately 80% of the multi-family housing base built before 2000 as well as growth in demand for multi-family housing.

We provide supply chain management and installation services to the commercial and multi-family construction market, primarily focusing on apartment buildings, hotels, senior living facilities and light commercial contractors. According to the American Institute of Architects (AIA), non-residential construction spend is estimated to be approximately $400 billion in 2020 and the NAHB is expecting 393,000 multi-family housing starts in 2020.

Our Strengths

We benefit from the following key competitive strengths:

Clear Market Leader with an Unrivaled National Network

We are the leading national provider of technology-enabled sales and marketing, design and installation solutions for homebuilders. We have the leading market position in the approximately $23 billion U.S. new home interior finish solutions industry, and our scale and technology differentiation provide unique capabilities that attractively position us relative to our competitors.

Amidst an increasingly consolidated homebuilder landscape, our national footprint, leading technology platform and execution capabilities position us as a preferred partner to large national and regional homebuilders

8

Table of Contents

across the U.S. In addition, our national scale, combined with leading local market positions, drive strong supplier and local workforce relationships that allow us to capture meaningful supply chain efficiencies and deliver consistent, high-quality installation services. We believe independent contractors are eager to work with us due to our extensive customer-base, consistent job volumes and rapid payments, which we believe is a competitive advantage in an increasingly competitive workforce market.

Differentiated Technology-Enabled Solutions

We have made significant investments to build a robust technology platform that we believe differentiates our value proposition to homebuilders and enhances the user experience for homebuyers. Our end-to-end technology suite starts with pre-sales marketing solutions, offering photo-realistic virtual tours of floor plans to prospective homebuyers, eliminating the need for time-consuming in-person tours and potentially eliminating the need for costly model homes. Once a homebuyer has purchased a home, we offer online option selection tools that utilize visualization technology to allow homebuyers to conveniently browse thousands of customized product options in advance of design appointments—whether in-person or virtual—and create an online “wish list” for their new home with real-time pricing. Our design professionals have access to this key information and use it during design appointments to focus on a particular homebuyer’s preferences and tailor their sales approach to maximize upgrade sales. Our technology integrates with homebuilder back office systems to help improve construction quality, decrease cycle times and increase customer stickiness. The wealth of data captured by our technology also offers critical insight to homebuilders that influences their product offerings and community design and investment decisions. The over 100,000 homes we serve annually vastly outnumbers the number of homes built by even the largest national homebuilders, which enhances the value of the data we collect. We continue to invest in technological innovation to create new opportunities for expansion, from additional visualization applications, such as supplier product selections, to market and data analytics for homebuilders and product manufacturers. We believe that our investments in technology will significantly expand our addressable market as we seek to capture additional economic transactions in the housing lifecycle.

Superior Customer Value Proposition

Our comprehensive suite of sales, marketing, design and installation solutions delivers a superior value proposition to our customers. Our design solutions drive increased homebuilder sales and profitability, improved operating efficiency and an enhanced homebuyer experience. Our ability to increase efficiency and profitability for our homebuilder customers is critical to our value proposition. Our builder-branded design studios offer a dedicated solution for larger homebuilders, while our ILG-branded design studios provide the same professionally-managed design experience for multiple regional homebuilders in a single location. We have also proven the ability to serve our customers digitally, as we have seen a notable increase in the percentage of our customers that have completed fully virtual design selections in 2020 compared to 2019. Our expanding technological capabilities, particularly around visualization, are accelerating the digitization of the homebuilding industry and enhancing the homebuyer experience for homebuyers across the size and price spectrum. Interior option sales are an important driver of homebuilder profitability, and we focus on high-touch products, such as flooring, cabinets and countertops, that homebuyers view as critical to the design aesthetic and overall home satisfaction. Our commitment to providing excellent service and quality from the design appointment through installation enhances the overall homebuyer experience, further benefitting our homebuilder customers. As a result of our strong value proposition and proven track record, we have developed long-standing customer relationships, as demonstrated by our minimal customer turnover, and we frequently benefit from exclusivity across specified products and geographic markets. In addition, we utilize our strong supplier and independent contractor relationships to serve as a valued provider of supply chain management and installation services for homebuilders through our builder direct solutions, as well as for a diverse range of multi-family, commercial and repair & remodel customers.

9

Table of Contents

Robust Supply Chain Capabilities

We are the largest new single-family residential customer for many of our suppliers, which we believe allows us to achieve superior pricing, product selection and supply chain efficiencies relative to our competitors. We manage the complex process of matching product supply to homebuyer demand for our customers, leveraging our data-driven insights to guide simplified product offerings that focus on high-demand options. Similar to our homebuilder customers, we also provide value-added insights and data analytics to our suppliers that we believe we can monetize over time.

Successful Track Record of Identifying, Executing and Integrating Acquisitions

We operate in a highly fragmented industry, where we believe our resources, experience and access to capital position us to capitalize on the significant opportunity to execute accretive acquisitions and enhance our market position. We have completed approximately 18 acquisitions since 2013, which is more than any of our direct competitors. We have completed both tuck-in and transformative acquisitions, with an average purchase multiple below seven times adjusted annualized EBITDA. Our senior management team has significant experience executing a disciplined acquisition strategy and has institutionalized best practices for successful integration and synergy realization. As a result of our management tenure, history of successful acquisitions and local entrepreneurial cultures, we have extensive relationships in our industry and are an acquirer of choice among potential acquisition targets.

Strong Balance Sheet and Free Cash Flow Generation

On a pro forma basis to reflect the net proceeds from this initial public offering, we expect our net leverage will be approximately times 2019 Adjusted EBITDA.2 The capital requirements of our business are relatively low, as our primary investments are focused on technology innovation, design studios and countertop fabrication equipment. We are focused on managing our working capital as part of our efficient supply chain operations, as evidenced by our inventory turning more than 15 times per year and an overall cash conversion cycle of fewer than 30 days. We believe our relatively low leverage compared to public company peers, coupled with our strong free cash flow generation and prudent capital management, provides us significant advantages in today’s environment, including the flexibility to continue to grow organically and through acquisitions, as well as maximize our asset efficiency.

Proven Management Team and Entrepreneurial Culture

Our senior management team, led by CEO, Alan Davenport, and President and COO, Jason Peel, has been instrumental in developing our innovative business model. The deep industry knowledge and customer and supplier relationships of our management team are a competitive advantage in executing our strategy. Our key executives have an in-depth understanding of how to best serve our customers as a result of their extensive experience in the interior finish solutions industry as well as other areas of the homebuilding and building products supply chain. Our entrepreneurial culture and deeply experienced local and regional management teams drive service excellence and nimble decision-making, empowering local collaboration with customers, suppliers and installers. Our vision is not attainable without our employees, and our future success will in large part be determined by the talent, skills and culture of our workforce. We strive to foster a diverse and inclusive workforce and we recognize a responsibility to advance our human capital management strategies to attract, develop and safeguard the well-being of our talented and dedicated workforce, including our employees, partners and suppliers. The board is also engaged with management to create a corporate culture that embodies the attributes and behaviors necessary to advance our vision and execute on our strategies.

| 2 | For a definition of Adjusted EBITDA and net leverage, as well a reconciliation to the most directly comparable GAAP measures, see “Non-GAAP Measures” and “—Summary Historical Financial Data.” |

10

Table of Contents

Demonstrated and Growing Commitment to Environmental, Social and Governance Matters (ESG)

We continue to increase our focus on ESG initiatives to ensure that we as well as our services and solutions promote a commitment to these important areas. Regarding social initiatives, we are constantly focused on the health and safety of our employees in all aspects of the workplace. In response to the ongoing COVID-19 pandemic, we have provided many of our employees with the ability to work remotely, increased the cleaning and sanitizing of our offices and facilities and have implemented strict safety and health measures at remote worksites. We also seek to promote community involvement and diversity in our organization. We encourage our employees to give back to the community and foster social change by providing them with a paid day off to get involved in charitable and community activities. We have established a diversity committee chaired by our female CFO. We have implemented and are continuing to implement important corporate governance and risk management practices as well, including compensation programs with increased focus on performance-based equity compensation.

Our Growth Strategy

Our objective is to achieve profitable growth and increase stockholder value through the following key strategies:

Gain Market Share Through Unique Visualization Tools Addressing Changing Customer Preferences

We have a proven ability to expand our solutions with existing homebuilder customers over time, layering design studio and technology solutions on top of existing installation services to grow our wallet share and enhance our customer stickiness due to our technology integration with homebuilder back office systems. Technology is one of the hallmarks of our solutions-oriented business model, and we plan to continue to invest in further differentiating our offering. We believe the homebuilding industry is still in the early stages of leveraging technology and data analytics to more efficiently design, market, sell and deliver homes. We believe we are one of the industry leaders in this area and our scale positions us to continue to invest more than our competitors in technology and innovation, as evidenced by our technology spend of over $60 million over the past three years. We intend to continue to develop leading-edge technology tools that enrich the user experience, optimize sales and profitability, and enhance service levels and operational efficiency for our customers.

One of our key development priorities has been to expand our visualization features, which we have accelerated through our recent acquisition of Roomored, a leading visualization SaaS provider. The market continues to shift towards a more virtual homebuying experience as younger demographics begin to enter their prime homebuying years. For example, according to Apartment List, 80% of millennials state that buying a home is an important personal goal, and approximately 30% of the younger demographic population would be willing to buy a home fully online, according to a recent survey from the National Association of Realtors. These tailwinds emphasize the importance of rich, real-time visualization capabilities and digital marketing platforms in the current environment. Our superior virtual capabilities and design tools will continue to position us to take advantage of these trends, while also enabling us to gain additional data insights to understand changing homeowner preferences and provide feedback to our homebuilder, supplier and installer partners.

Execute on Our Technology Roadmap to Increase Revenue Streams Throughout the Entire Lifecycle of a Home

Our technology strategy is to expand our total addressable market to capture incremental economic transactions associated with the housing lifecycle. We believe that our access to over 100,000 homebuyers annually leaves us uniquely positioned to capitalize on this opportunity. Our technology roadmap is focused on continued enhancement of our design and selection capabilities, monetization of our significant repository of

11

Table of Contents

homebuyer data, and creating a digital marketplace to connect homebuyers, suppliers and installers for any future repair and remodel needs. In addition, we plan to capitalize on artificial intelligence-driven technology to show homeowners products and solutions of interest, to the benefit of both the homeowners, homebuilders and product partners.

Expand Our Extensive Relationships with Leading Homebuilders

We have a proven track record of growing our business with key customers, with our revenues from the top 10 U.S. homebuilders more than tripling from 2015 to 2019 through organic growth and acquisitions. Furthermore, from 2017 to 2019, we grew organic revenue from multiple key customers by more than 20%. Today we serve many of the leading national and regional homebuilders in the U.S. in multiple markets. We have an opportunity to substantially expand these relationships over time. In 2019, we served approximately 75,000 homes to our national accounts, which represent key scaled homebuilding customers that management has strategically aligned with across core markets. These customers delivered approximately 250,000 new homes in total, providing an opportunity to meaningfully increase penetration within our existing customers. We intend to continue to leverage our national footprint, technology platform and strong reputation for consistently superior execution to serve these customers in additional markets. Today, we operate 64 builder-branded design studios on behalf of 20 homebuilders across the country, as well as 46 ILG-branded design studios that provide the same professionally-managed design experience for multiple homebuilders in a single location. Our larger design customers collectively have operations in over 250 MSAs that we do not serve with our builder-branded model, providing significant runway for continued expansion, particularly in high growth attractive housing markets in the South and Southeast. Likewise, we provide builder direct solutions to national and regional homebuilders in multiple markets today, and we look to further penetrate these relationships in many more of the markets they serve. In addition, we have been successful in converting a number of builder direct customers to our design studio solutions, and in expanding the scope of our technology solutions to our design studio customers. Our investments in technology also significantly enhance our ability to serve new customers remotely outside of our design studio footprint. As an example, we recently executed a multi-year agreement with one of our national homebuilder customers to serve as their sole-source visualization provider for all interior finishes, regardless of whether we provide their installation services in a given market.

Expand Product Installation Capabilities Across Additional Markets

We perform supply chain management and installation services for flooring products across substantially all of our geographic markets. However, we offer cabinet and countertop installation services in only approximately 38% and 35% of these markets, respectively. We believe there is significant opportunity to grow our business in these and other products, through both expansion across geographic markets and increased penetration of the markets we currently serve. By expanding our supply chain management and installation services to additional products, we believe we can increase our potential revenues and profit per home and deepen our homebuilder relationships.

Drive Margin Enhancement Through Scale, Operational Initiatives and Technology Investments

We have demonstrated a proven ability to expand our margins over time and achieve industry-leading returns on invested capital. Our favorable margin profile is in part due to increasing our scale in specific markets, as we typically generate the highest margins in regions where we maintain leadership positions. Local economies of scale allow us to better leverage field managers, warehouses, and installation crews on a per home basis; as such, we expect to enhance our profitability as we achieve additional regional scale. We have also meaningfully expanded our margins through operational efficiencies and our investments in technology to improve our integration with homebuilder back office systems. Today, we believe we are optimized in the markets that collectively represent approximately 41% of our revenues for the nine months ended September 30, 2020. Our optimized markets demonstrate the aforementioned characteristics and generate margins in excess of our

12

Table of Contents

corporate average. Finally, the monetization of our technology initiatives, such as our visualization capabilities, are generating revenue at significantly higher margins, with technology-enabled revenue generating gross margins more than 800 bps higher than our builder direct revenue. We believe we can materially increase our overall margins in the long term through our technology initiatives.

Pursue Value-Enhancing Acquisitions in a Highly Fragmented Market

We estimate that approximately 80% of the interior finishes solutions industry remains highly fragmented. Our successful and disciplined acquisition strategy has provided us access to new technology, customers and markets, expanded our product capabilities, deepened our management team and enhanced our operational best practices. We will continue to focus on acquisitions that meet our criteria for growth, returns, technological advancement, market expansion, customer and product expansion and synergistic operations at attractive valuations. We believe our scale and access to capital relative to our competition, together with our senior management team’s strong relationships and reputation and vast and talented workforce, position us to take advantage of the many acquisition opportunities in our fragmented industry.

Pursue Growth Opportunities in Multi-Family, Commercial and Repair & Remodel End Markets

We employ our scale and supply chain management and installation expertise to serve a broad range of customers in multi-family, commercial and repair & remodel end-markets. These customers collectively represented approximately 20% of our 2019 revenues and provide another channel of growth outside of the new single-family residential market. We expect to continue to expand existing and develop new relationships where we can efficiently and effectively leverage our existing supply chain management and installation services to enhance our growth and profitability. Within these end markets, additional revenue opportunities include multi-family and light commercial contractors, multi-family owners and operators, senior living operators, single-family rental operators and home improvement retailers, where the largest companies have grown extensively through industry consolidation since the housing recession.

Our Sponsors

Founded in 1996, Littlejohn & Co., LLC (together with its affiliates, “Littlejohn”) is an investment firm headquartered in Greenwich, Connecticut. The firm’s current portfolio consists of 17 companies (excluding non-control investments) in a variety of industries, including multiple investments in the building products space. Littlejohn’s current and historical investments in the building products sector include Cook & Boardman and Contech. In addition, from 2011 to 2015, Littlejohn maintained an investment in Installed Building Products Inc. (NYSE: IBP), one of the nation’s largest insulation installers for the new single-family residential market and a diversified installer of complementary building products, which completed its initial public offering in 2014. Littlejohn invests primarily in North American headquartered businesses, many of which have global operations. Littlejohn will beneficially own approximately % of our common stock immediately upon the consummation of this offering. See “Principal Stockholders” for additional information regarding beneficial ownership.

Founded in 1995, Platinum Equity is a global investment firm with approximately $23 billion of assets under management and a portfolio of approximately 40 operating companies that serve customers around the world. The firm’s portfolio companies generated more than $25 billion of revenue during the trailing twelve-month period ended June 30, 2020. Platinum Equity specializes in mergers, acquisitions and operations—a trademarked strategy it calls M&A&O®—acquiring and operating companies in a broad range of business markets, including manufacturing, distribution, transportation and logistics, equipment rental, metals services, packaging, media and entertainment, technology, telecommunications, healthcare and other industries. Platinum Equity’s current and historical investments in the building products and construction sector include PrimeSource,

13

Table of Contents

NILCO, United Site Services, Fabcon, CanWel Building Materials, and Yak Access. Over the past 25 years, Platinum Equity has completed more than 300 acquisitions. Certain affiliates of Platinum Equity, LLC (collectively, “Platinum” and, together with Littlejohn, the “Sponsors”) will beneficially own approximately % of our common stock immediately upon the consummation of this offering. See “Principal Stockholders” for additional information regarding beneficial ownership.

Corporate Conversion

We currently operate as a Delaware limited liability company under the name Interior Logic Group Holdings, LLC. Faraday, which is owned by, among others, Littlejohn and members of legacy ISI management, owns 53% of our Class A Units, and ISH, which is owned by, among others, Platinum and members of legacy ILG management, owns 47% of our Class A Units. Certain employees of the Company hold options to purchase our Class B Units.

Prior to the effectiveness of the registration statement of which this prospectus is a part, Interior Logic Group Holdings, LLC will convert into a Delaware corporation pursuant to a statutory conversion and change its name to Interior Logic Group Holdings, Inc. (the “Corporate Conversion”). As a result of the Corporate Conversion, the holders of Class A Units of Interior Logic Group Holdings, LLC and options to purchase Class B Units will become holders of shares of common stock of Interior Logic Group Holdings, Inc. and options to purchase shares of our common stock, respectively. The number of shares of our common stock and options to purchase shares of our common stock that holders of units and options to purchase units will be entitled to receive in the Corporate Conversion will be determined in accordance with the Plan of Conversion and our Second Amended and Restated Limited Liability Company Agreement, dated May 31, 2018 (the “LLC Agreement”). In connection with the Corporate Conversion, Faraday intends to undertake a series of restructuring actions such that each of Littlejohn and the other holders of the equity interests of Faraday will own our common stock or options to purchase shares of our common stock through a new holding company (“New Faraday”). Following the Faraday restructuring, Faraday will become a non-operating subsidiary of the Company.

The information in this prospectus is based on our estimate that, in the Corporate Conversion, shares of our common stock will be issued to holders of units and options to purchase shares of our common stock will be issued to holders of options to purchase units, in either case, based on an initial public offering price per share of common stock of $ , which is the midpoint of the price range set forth on the cover page of this prospectus. To the extent that the actual initial public offering price per share for this offering is greater or less than $ , the actual number of shares of common stock and options to be issued in connection with the Corporate Conversion will be adjusted accordingly. See “Description of Capital Stock” for additional information regarding our common stock following the Corporate Conversion.

In connection with the Corporate Conversion, Interior Logic Group Holdings, Inc. will continue to hold all property and assets of Interior Logic Group Holdings, LLC and will assume all of the debts and obligations of Interior Logic Group Holdings, LLC. Interior Logic Group Holdings, Inc. will be governed by a certificate of incorporation filed in the State of Delaware and bylaws, the material portions of which are described in “Description of Capital Stock.” On the effective date of the Corporate Conversion, the members of the board of managers of Interior Logic Group Holdings, LLC will become the members of the board of directors of Interior Logic Group Holdings, Inc., and the officers of Interior Logic Group Holdings, LLC will become the officers of Interior Logic Group Holdings, Inc.

14

Table of Contents

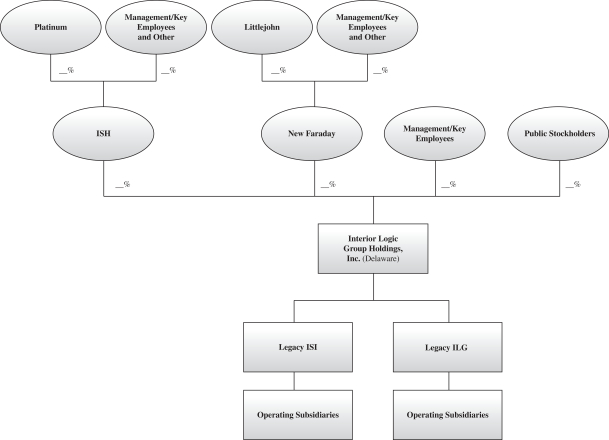

Our organizational and ownership structure, after giving effect to the Corporate Conversion and this offering, is presented below:

The purpose of the Corporate Conversion is to reorganize our corporate structure so that the entity that is offering our common stock to the public in this offering is a corporation rather than a limited liability company and so that our existing investors will own our common stock rather than equity interests in a limited liability company. References in this prospectus to our capitalization and other matters pertaining to our equity prior to the Corporate Conversion relate to the capitalization, equity and limited liability company interests of Interior Logic Group Holdings, LLC, and after the Corporate Conversion, to the capitalization, equity and shares of Interior Logic Group Holdings, Inc.

Corporate Information

Our principal executive offices are located at 10 Bunsen, Irvine, California 92618. Our main telephone number is (800) 959-8333. Our corporate internet website address is www.interiorlogicgroup.com. The information contained in, or that can be accessed through, our website is not incorporated by reference and is not a part of this prospectus.

Risk Factors Summary

Investing in our common stock involves a high degree of risk, which are discussed more fully under “Risk Factors.” You should carefully consider all the information in this prospectus, including the risks described in

15

Table of Contents

“Risk Factors,” before making a decision to invest in our common stock. If any of these risks are realized, our business, financial condition, results of operations and prospects could be materially and adversely affected. In that event, the trading price of our common stock could decline and you could lose part or all of your investment. Below is a summary of some of the principal risks we face:

| • | the negative impacts of the COVID-19 pandemic on our business; |

| • | decreased new single-family residential construction activity; |

| • | downturns in the economy and credit markets; |

| • | decreased demand for interior option upgrades; |

| • | decline in the rate of growth in the housing market, in our geographic markets or of the homebuilding industry; |

| • | loss of, or decreased construction activity by, significant customers; |

| • | pricing pressures from customers; |

| • | changes in the cost of the products we install or in our product mix; |

| • | increased tariffs and other changes in foreign trade policy; |

| • | dependence on our senior management team and other key personnel; |

| • | inability to attract and retain qualified employees and the risks associated with our workforce supply and costs; |

| • | risks associated with completing the implementation of our enterprise resource planning (“ERP”) system and implementing other new initiatives for operating software; |

| • | dependence on the availability and skill of subcontractors and the risks associated with our use of subcontractors; |

| • | inability to execute our growth strategy; |

| • | competitive pressures in our industry; |

| • | risks associated with acquisitions, including our ability to realize anticipated synergies or the costs of integrating acquisitions; |

| • | inability to expand into new geographic markets; |

| • | product shortages, loss of key suppliers, failure to develop relationships with qualified suppliers, material disruptions in our supply or substantial changes to supply terms; |

| • | reliance on third-party license agreements; |

| • | the effect of seasonality of our business, severe weather conditions and climate change; |

| • | cybersecurity risks; |

| • | disruptions in our IT systems and software; |

| • | changes in, or failure to comply with, federal, state, local and other laws and regulations; |

| • | exposure to claims and legal proceedings; |

| • | our failure to adequately protect our intellectual property rights; |

| • | risks related to our indebtedness; |

16

Table of Contents

| • | our inability to maintain an effective system of internal controls and produce timely and accurate financial statements or comply with applicable regulations; |

| • | the obligations and increased costs associated with being a public company; |

| • | the significant ownership of our common stock by our Sponsors, whose interests may conflict with those of our stockholders; and |

| • | additional factors discussed under the sections captioned “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Our Business.” |

17

Table of Contents

The Offering

Common stock offered by us | shares (or shares if the underwriters exercise their option to purchase additional shares in full). |

Common stock to be outstanding after this offering | shares (or shares if the underwriters exercise their option to purchase additional shares in full). |

Option to purchase additional shares. | We have granted the underwriters a 30-day option to purchase up to additional shares of our common stock. |

Use of proceeds | We expect to receive net proceeds from this offering of approximately $ million, or approximately $ million if the underwriters exercise their option to purchase additional shares of our common stock in full, assuming an initial public offering price of $ per share, which is the midpoint of the price range set forth on the on the cover page of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. We intend to use the net proceeds from this offering (including any additional proceeds that we may receive if the underwriters exercise their option to purchase additional shares of our common stock) to repay indebtedness under our Term Loan Facility and the balance for general corporate purposes, including working capital, operating expenses and capital expenditures. We may also use a portion of the net proceeds we receive from this offering for acquisitions or other strategic investments, although we do not currently have any specific transactions at this time. See “Use of Proceeds.” |

Dividend policy | We currently intend to retain any future earnings to finance the development and expansion of our business and, therefore, do not intend to pay dividends on our common stock after this offering and for the foreseeable future. Any future determination relating to dividend policy will be made at the discretion of our board of directors and will depend on a number of factors, including restrictions in our current and future debt instruments, our future earnings, capital requirements, financial condition, future prospects, and applicable Delaware law, which provides that dividends are only payable out of surplus or current net profits. See “Dividend Policy.” |

Proposed symbol | We have applied to list our common stock on the Nasdaq Global Select Market under the symbol “ILG.” |