While we have implemented security measures designed to protect against breaches of security and other interference with our systems and networks, our systems and networks may be, and at times are, subject to breaches or interference. Any such event may result in operational disruptions as well as unauthorized access to or the disclosure or loss of our proprietary information or our customers’ data and information, which in turn may result in legal claims, regulatory scrutiny and liability, reputational damage, the incurrence of costs to eliminate or mitigate further exposure, the loss of customers or affiliated advisors, reputational harm or other damage to our business. In addition, the trend toward general public notification of such incidents could exacerbate the harm to our business, financial condition and results of operations. Even if we successfully protect our technology infrastructure and the confidentiality of sensitive data, we could suffer harm to our business and reputation if attempted security breaches are publicized. We cannot be certain that advances in criminal capabilities, discovery of new vulnerabilities, attempts to exploit vulnerabilities in our systems, data thefts, physical system or network break-ins or inappropriate access, or other developments will not compromise or breach the technology or other security measures protecting the networks and systems used in connection with our business.

Recently, the majority of our employees have been working outside of our primary offices as a result of the Pandemic. We believe this additional remote work increases the need for our information technology and telecommunications systems to work properly and creates additional operational risk and difficulty should these systems fail.

Risks Related to Laws and Regulations

We are subject to extensive regulation, which may adversely affect our ability to achieve our business objectives. In addition, if we fail to comply with these regulations, we may be subject to penalties, including fines and suspensions, which may adversely affect our financial condition and results of operations.

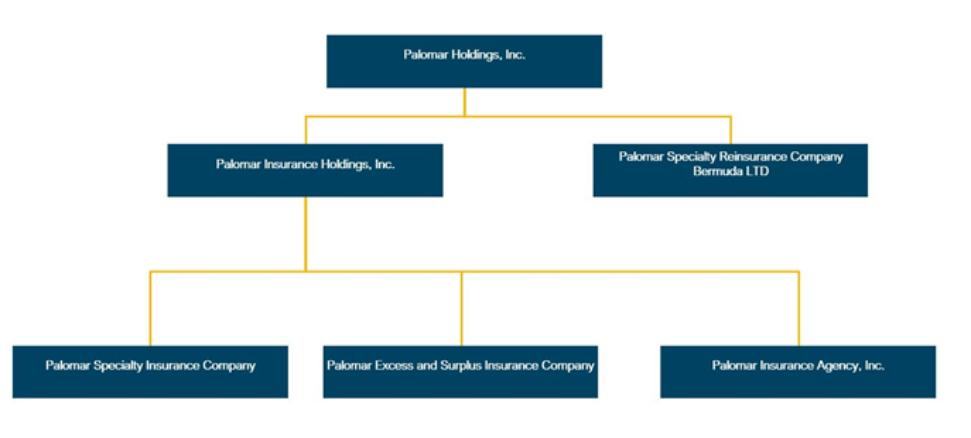

Palomar Specialty Insurance Company (“PSIC”) is subject to extensive regulation in Oregon, its state of domicile, California, where it is commercially domiciled, and to a lesser degree, the other states in which it operates. Palomar Excess and Surplus Insurance Company (‘‘PESIC’’) is subject to extensive regulation in Arizona, its state of domicile, and to a lesser degree, the other states in which it writes business. Our Bermuda based reinsurance subsidiary, Palomar Specialty Reinsurance Company Bermuda Ltd. (“PSRE”), is subject to regulation in Bermuda.

Most insurance regulations are designed to protect the interests of insurance policyholders, as opposed to the interests of investors or stockholders. These regulations generally are administered by a department of insurance in each state and relate to, among other things, capital and surplus requirements, investment and underwriting limitations, affiliate transactions, dividend limitations, changes in control, solvency and a variety of other financial and non-financial aspects of our business. Significant changes in these laws and regulations could further limit our discretion or make it more expensive to conduct our business. State insurance regulators and the Bermuda Monetary Authority (“the BMA”), also conduct periodic examinations of the affairs of insurance and reinsurance companies and require the filing of annual and other reports relating to financial condition, holding company issues and other matters. These regulatory requirements may impose timing and expense constraints that could adversely affect our ability to achieve some or all of our business objectives.

Our U.S. insurance subsidiaries are part of an “insurance holding company system” within the meaning of applicable California, Oregon and Arizona statutes and regulations. As a result of such status, certain transactions between our U.S. insurance subsidiaries and one or more of their affiliates, such as a tax sharing agreement or cost sharing arrangement, may not be effected unless the insurer has provided notice of that transaction to the California Department of Insurance, the Oregon Division of Financial Regulation, or the Arizona Department of Insurance, as applicable, at least 30 days prior to engaging in the transaction and the California Department of Insurance, the Oregon Division of Financial Regulation, or the Arizona Department of Insurance, as applicable, has not disapproved such transaction within the 30-day time period. These prior notification requirements may result in business delays and additional business expenses. If any of our U.S. insurance subsidiaries fail to file a required notification or fail to comply with other applicable insurance regulations in California, Oregon or Arizona, as applicable, we may be subject to significant fines and penalties and our working relationship with the California Department of Insurance, the Oregon Division of Financial Regulation, or the Arizona Department of Insurance, as applicable, may be impaired.