UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-23410

FROST FAMILY OF FUNDS

(Exact name of registrant as specified in charter)

One Freedom Valley Drive

Oaks, PA 19456

(Address of Principal Executive Offices, Zip code)

Michael Beattie

c/o SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: 1-877-713-7678

Date of fiscal year end: July 31, 2024

Date of reporting period: July 31, 2024

Item 1. Reports to Stockholders.

(a) A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1), is attached hereto.

Frost Family of Funds - Institutional Class Shares - FICEX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about Institutional Class Shares of the Frost Growth Equity Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Growth Equity Fund, Institutional Class Shares | $76 | 0.67% |

How did the Fund perform in the last year?

For fiscal year 2024, the Frost Growth Equity Fund, Institutional Class posted a gain of 27.87%. Outperforming its benchmark, the Russell 1000 Growth Index, by 93 basis points, and its large growth peer group by 433 basis points. The Russell 1000 Growth Index remains more concentrated than the average Large Cap Growth Fund, often experiencing large relative swings based on a few (mega cap) stocks. Relative to our actively managed large growth peer group, the Fund ranked in the top quartile over the period.

Stock selection drove the Fund's performance, with consumer discretionary, communication services and health care as the top contributors, technology and industrials detracted the most. Sector allocation was an immaterial contributor.

In consumer discretionary, an underweight in Tesla and overweight in Amazon and Chipotle Mexican Grill were notable contributors. Tesla cut prices significantly to maintain volume targets, but vehicle sales have not recovered. What was formerly a 50% volume grower is struggling to stay flat. While we believe Tesla will remain a leader in electric vehicles, the stock looks expensive, and we maintain the position as a sizeable underweight in the Fund. Amazon was one of the top contributors driven by the uplift in tech stocks, profit and cash flow growth from cost management and interest in AI/data centers. Amazon was up almost 40% over the 12-month period.

In communication services, our investment in Spotify Technology was a solid contributor for the year. The stock benefitted from solid user growth, cost management, higher pricing and solidifying market leadership. Spotify, increasingly, controls its own destiny as its platform has grown and has branched out to podcasts and audiobooks. Revenue growth should be double digits for the next couple of years.

In health care, Eli Lilly, our top contributor for the year across sectors, rose 78% after a strong return last year. Lilly’s Mounjaro/Zepbound in diabesity is on pace to triple its revenues to more than $15 billion this year. More growth is expected before the end of the decade. Lilly has the most in-depth pipeline in diabesity with multiple follow-on molecules in the clinic currently. Lilly and Novo Nordisk will likely split this market, with a potential size in excess of $150 billion.

On the downside, relative performance in the technology sector was affected by an underweight in Broadcom and to a lesser extent, an underweight position in Apple. We believe Apple is one of the highest quality companies in the market and we have owned the stock for the past 15 years. However, we are underweight relative to the benchmark as we believe the valuation already reflects the quality and the growth prospects of the business. Software companies Microsoft and ServiceNow and the semiconductor company Advanced Micro Devices contributed positively to stock selection in the sector.

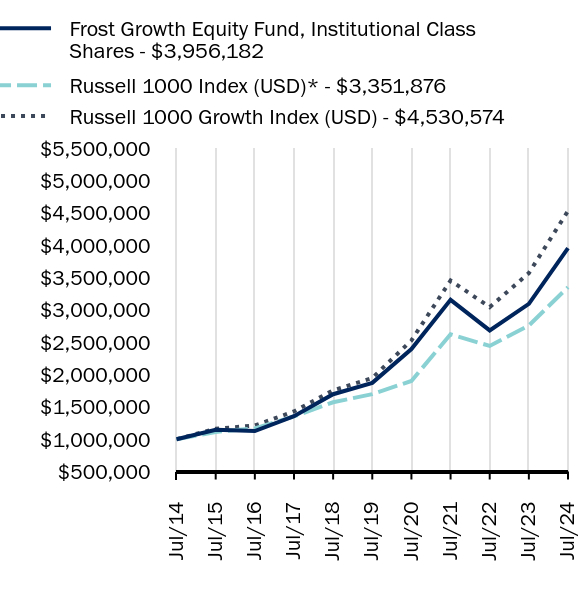

How did the fund perform during the last 10 years?

Total Return Based on $1,000,000 Investment

| Frost Growth Equity Fund, Institutional Class Shares - $3956182 | Russell 1000 Index (USD)* - $3351876 | Russell 1000 Growth Index (USD) - $4530574 |

|---|

| Jul/14 | $1000000 | $1000000 | $1000000 |

| Jul/15 | $1144533 | $1112351 | $1160821 |

| Jul/16 | $1124860 | $1166137 | $1211287 |

| Jul/17 | $1355878 | $1352137 | $1429944 |

| Jul/18 | $1695541 | $1571035 | $1756585 |

| Jul/19 | $1870940 | $1696725 | $1946708 |

| Jul/20 | $2393130 | $1900918 | $2527545 |

| Jul/21 | $3154861 | $2622618 | $3454593 |

| Jul/22 | $2682426 | $2442448 | $3042562 |

| Jul/23 | $3093990 | $2758701 | $3569204 |

| Jul/24 | $3956182 | $3351876 | $4530574 |

Average Annual Total Returns as of July 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Frost Growth Equity Fund, Institutional Class Shares | 27.87% | 16.16% | 14.74% |

| Russell 1000 Index (USD)* | 21.50% | 14.59% | 12.86% |

| Russell 1000 Growth Index (USD) | 26.94% | 18.41% | 16.31% |

The line graph represents historical performance of a hypothetical investment of $1,000,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 1-877-71-FROST or visit https://frostinv.com/ for current month-end performance.

Footnote Reference*As of July 2024, pursuant to the new regulatory requirements, this index replaced the prior index as the Fund's primary benchmark to represent a broad-based securities market index.

Key Fund Statistics as of July 31, 2024

| Total Net Assets | Number of Holdings | Total Advisory Fees Paid | Portfolio Turnover Rate |

|---|

| $240,759,686 | 57 | $1,271,123 | 17% |

What did the Fund invest in?

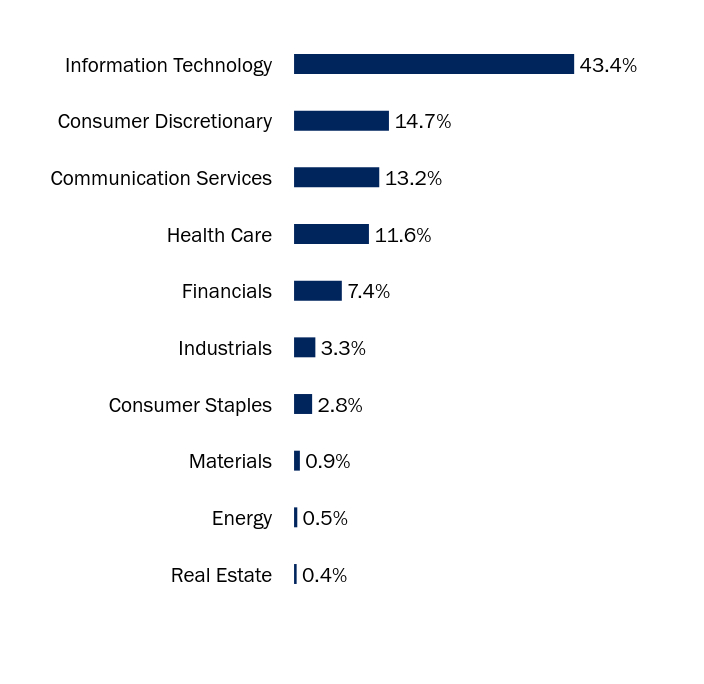

Sector WeightingsFootnote Reference*

| Value | Value |

|---|

| Real Estate | 0.4% |

| Energy | 0.5% |

| Materials | 0.9% |

| Consumer Staples | 2.8% |

| Industrials | 3.3% |

| Financials | 7.4% |

| Health Care | 11.6% |

| Communication Services | 13.2% |

| Consumer Discretionary | 14.7% |

| Information Technology | 43.4% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | | | Percentage of Total Net Assets |

|---|

| Microsoft | | | 12.3% |

| NVIDIA | | | 10.2% |

| Apple | | | 8.6% |

| Amazon.com | | | 7.1% |

| Meta Platforms, Cl A | | | 3.9% |

| Alphabet, Cl A | | | 3.8% |

| Eli Lilly | | | 3.7% |

| Alphabet, Cl C | | | 3.3% |

| Visa, Cl A | | | 2.9% |

| Mastercard, Cl A | | | 2.6% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund; including its prospectus, financial information, holdings, and proxy voting information, visit or call:

1-877-71-FROST

https://frostinv.com/

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds.

Frost Growth Equity Fund / Institutional Class Shares - FICEX

Annual Shareholder Report - July 31, 2024

FIA-AR-TSR-2024-5

Frost Family of Funds - Investor Class Shares - FACEX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about Investor Class Shares of the Frost Growth Equity Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Growth Equity Fund, Investor Class Shares | $104 | 0.91% |

How did the Fund perform in the last year?

For fiscal year 2024, the Frost Growth Equity Fund, Investor Class posted a gain of 27.55%. Outperforming its benchmark, the Russell 1000 Growth Index, by 61 basis points, and its large growth peer group by 401 basis points. The Russell 1000 Growth Index remains more concentrated than the average Large Cap Growth Fund, often experiencing large relative swings based on a few (mega cap) stocks. Relative to our actively managed large growth peer group, the Fund ranked in the top quartile over the period.

Stock selection drove the Fund’s performance, with consumer discretionary, communication services and health care as the top contributors, technology and industrials detracted the most. Sector allocation was an immaterial contributor.

In consumer discretionary, an underweight in Tesla and overweight in Amazon and Chipotle Mexican Grill were notable contributors. Tesla cut prices significantly to maintain volume targets, but vehicle sales have not recovered. What was formerly a 50% volume grower is struggling to stay flat. While we believe Tesla will remain a leader in electric vehicles, the stock looks expensive, and we maintain the position as a sizeable underweight in the Fund. Amazon was one of the top contributors driven by the uplift in tech stocks, profit and cash flow growth from cost management and interest in AI/data centers. Amazon was up almost 40% over the 12-month period.

In communication services, our investment in Spotify Technology was a solid contributor for the year. The stock benefitted from solid user growth, cost management, higher pricing and solidifying market leadership. Spotify, increasingly, controls its own destiny as its platform has grown and has branched out to podcasts and audiobooks. Revenue growth should be double digits for the next couple of years.

In health care, Eli Lilly, our top contributor for the year across sectors, rose 78% after a strong return last year. Lilly’s Mounjaro/Zepbound in diabesity is on pace to triple its revenues to more than $15 billion this year. More growth is expected before the end of the decade. Lilly has the most in-depth pipeline in diabesity with multiple follow-on molecules in the clinic currently. Lilly and Novo Nordisk will likely split this market, with a potential size in excess of $150 billion.

On the downside, relative performance in the technology sector was affected by an underweight in Broadcom and to a lesser extent, an underweight position in Apple. We believe Apple is one of the highest quality companies in the market and we have owned the stock for the past 15 years. However, we are underweight relative to the benchmark as we believe the valuation already reflects the quality and the growth prospects of the business. Software companies Microsoft and ServiceNow and the semiconductor company Advanced Micro Devices contributed positively to stock selection in the sector.

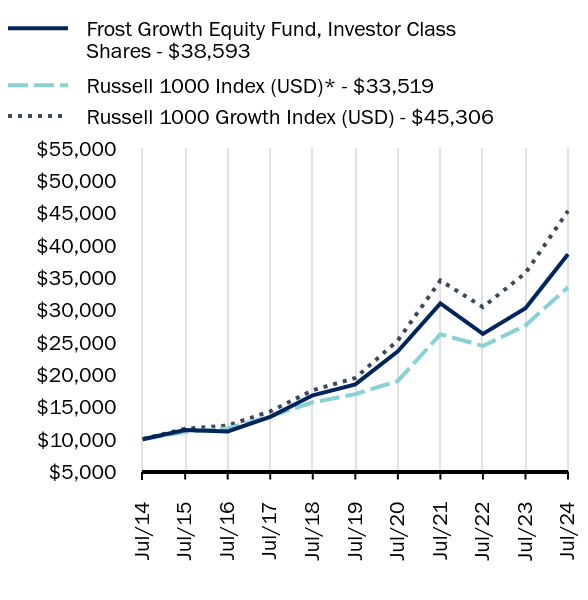

How did the fund perform during the last 10 years?

Total Return Based on $10,000 Investment

| Frost Growth Equity Fund, Investor Class Shares - $38593 | Russell 1000 Index (USD)* - $33519 | Russell 1000 Growth Index (USD) - $45306 |

|---|

| Jul/14 | $10000 | $10000 | $10000 |

| Jul/15 | $11417 | $11124 | $11608 |

| Jul/16 | $11188 | $11661 | $12113 |

| Jul/17 | $13462 | $13521 | $14299 |

| Jul/18 | $16789 | $15710 | $17566 |

| Jul/19 | $18476 | $16967 | $19467 |

| Jul/20 | $23579 | $19009 | $25275 |

| Jul/21 | $31010 | $26226 | $34546 |

| Jul/22 | $26285 | $24424 | $30426 |

| Jul/23 | $30256 | $27587 | $35692 |

| Jul/24 | $38593 | $33519 | $45306 |

Average Annual Total Returns as of July 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Frost Growth Equity Fund, Investor Class Shares | 27.55% | 15.87% | 14.46% |

| Russell 1000 Index (USD)* | 21.50% | 14.59% | 12.86% |

| Russell 1000 Growth Index (USD) | 26.94% | 18.41% | 16.31% |

The line graph represents historical performance of a hypothetical investment of $10,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 1-877-71-FROST or visit https://frostinv.com/ for current month-end performance.

Footnote Reference*As of July 2024, pursuant to the new regulatory requirements, this index replaced the prior index as the Fund's primary benchmark to represent a broad-based securities market index.

Key Fund Statistics as of July 31, 2024

| Total Net Assets | Number of Holdings | Total Advisory Fees Paid | Portfolio Turnover Rate |

|---|

| $240,759,686 | 57 | $1,271,123 | 17% |

What did the Fund invest in?

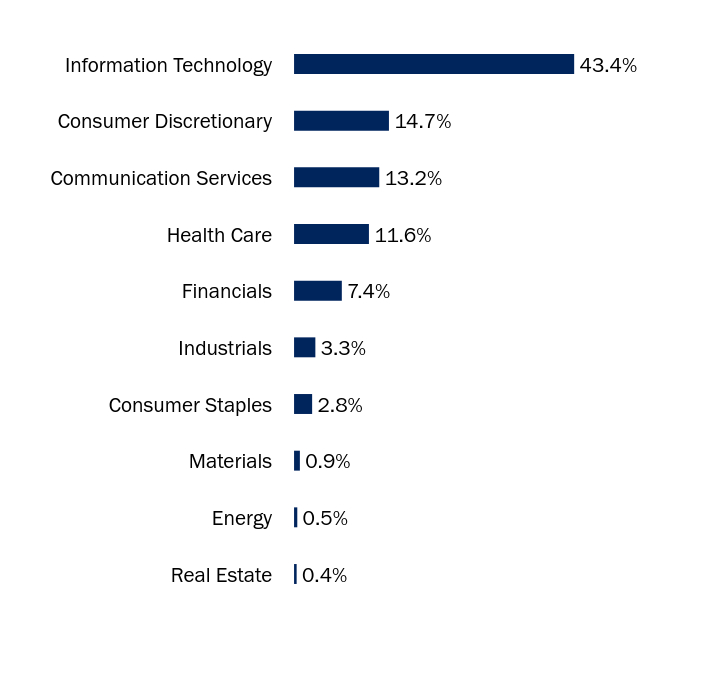

Sector WeightingsFootnote Reference*

| Value | Value |

|---|

| Real Estate | 0.4% |

| Energy | 0.5% |

| Materials | 0.9% |

| Consumer Staples | 2.8% |

| Industrials | 3.3% |

| Financials | 7.4% |

| Health Care | 11.6% |

| Communication Services | 13.2% |

| Consumer Discretionary | 14.7% |

| Information Technology | 43.4% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | | | Percentage of Total Net Assets |

|---|

| Microsoft | | | 12.3% |

| NVIDIA | | | 10.2% |

| Apple | | | 8.6% |

| Amazon.com | | | 7.1% |

| Meta Platforms, Cl A | | | 3.9% |

| Alphabet, Cl A | | | 3.8% |

| Eli Lilly | | | 3.7% |

| Alphabet, Cl C | | | 3.3% |

| Visa, Cl A | | | 2.9% |

| Mastercard, Cl A | | | 2.6% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund; including its prospectus, financial information, holdings, and proxy voting information, visit or call:

1-877-71-FROST

https://frostinv.com/

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds.

Frost Growth Equity Fund / Investor Class Shares - FACEX

Annual Shareholder Report - July 31, 2024

FIA-AR-TSR-2024-4

Frost Total Return Bond Fund

Frost Family of Funds - Institutional Class Shares - FIJEX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about Institutional Class Shares of the Frost Total Return Bond Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Total Return Bond Fund, Institutional Class Shares | $49 | 0.46% |

How did the Fund perform in the last year?

• The Bloomberg U.S. Aggregate Bond Index (the AGG) returned 5.10% over the year. The Frost Total Return Bond Fund (Institutional Share Class) returned 11.34% for the same period, bettering the benchmark by over 6.0%.

• Broadly, the Fund obtained outperformance relative to its benchmark from each of the four primary decisions the portfolio team utilizes – interest rate decisions, credit risk allocations, asset sector allocations and security selection.

• The Fund maintained its effective duration – a measure of interest rate risk – between 3.20% and 5.40% with the lower end of the range early in the year and increasing steadily throughout the year and finishing close to the high end of the range at the end of July 2024.

• With the benchmark’s average duration approximately 6.25%, the Fund’s underweight duration allocation resulted in positive outperformance relative to the benchmark. The primary benefit to the Fund’s interest rate profile, compared to the index, was the rise in yields for maturities over ten years due to the yield curve inversion. The Fund was strategically positioned throughout the year to take advantage of further yield curve inversion. The allocation to credit resulted in outperformance relative to the index as the credit markets outperformed U.S. government sectors. Risk asset sectors generally benefited from economic and credit cycle performance. The Fund throughout the year was slightly overweight the below investment grade securities and underweight government securities.

• The Fund outperformed due to individual security selection across several sectors. Individual security selection was the largest positive attribution metric relative to the benchmark during the year.

• The Fund held an average allocation of 5% to energy over the year. This resulted in positive relative performance. Several of the Fund’s oil holdings saw significant outperformance. The Fund held underweight allocations to Treasury, corporate and RMBS sectors and overweight ABS, CMBS and CLOs. Each of these sector allocations aided the Fund’s relative performance to the benchmark, even before any consideration to security selection.

• The Fund’s average allocations during the year were 29% Treasurys, 21% corporates, 17% RMBS, 10% CLOs, 10% ABS, and 6% CMBS.

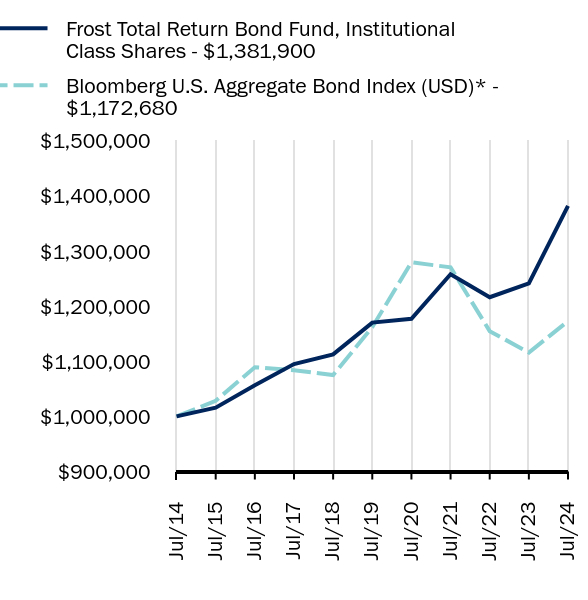

How did the fund perform during the last 10 years?

Total Return Based on $1,000,000 Investment

| Frost Total Return Bond Fund, Institutional Class Shares - $1381900 | Bloomberg U.S. Aggregate Bond Index (USD)* - $1172680 |

|---|

| Jul/14 | $1000000 | $1000000 |

| Jul/15 | $1015771 | $1028241 |

| Jul/16 | $1056573 | $1089267 |

| Jul/17 | $1094896 | $1083660 |

| Jul/18 | $1112464 | $1074990 |

| Jul/19 | $1170181 | $1161858 |

| Jul/20 | $1177173 | $1279452 |

| Jul/21 | $1257818 | $1270473 |

| Jul/22 | $1216266 | $1154652 |

| Jul/23 | $1241170 | $1115764 |

| Jul/24 | $1381900 | $1172680 |

Average Annual Total Returns as of July 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Frost Total Return Bond Fund, Institutional Class Shares | 11.34% | 3.38% | 3.29% |

| Bloomberg U.S. Aggregate Bond Index (USD)* | 5.10% | 0.19% | 1.61% |

The line graph represents historical performance of a hypothetical investment of $1,000,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 1-877-71-FROST or visit https://frostinv.com/ for current month-end performance.

Footnote Reference*As of July 2024, pursuant to the new regulatory requirements, this index replaced the prior index as the Fund's primary benchmark to represent a broad-based securities market index.

Key Fund Statistics as of July 31, 2024

| Total Net Assets | Number of Holdings | Total Advisory Fees Paid | Portfolio Turnover Rate |

|---|

| $3,373,875,556 | 392 | $10,281,854 | 48% |

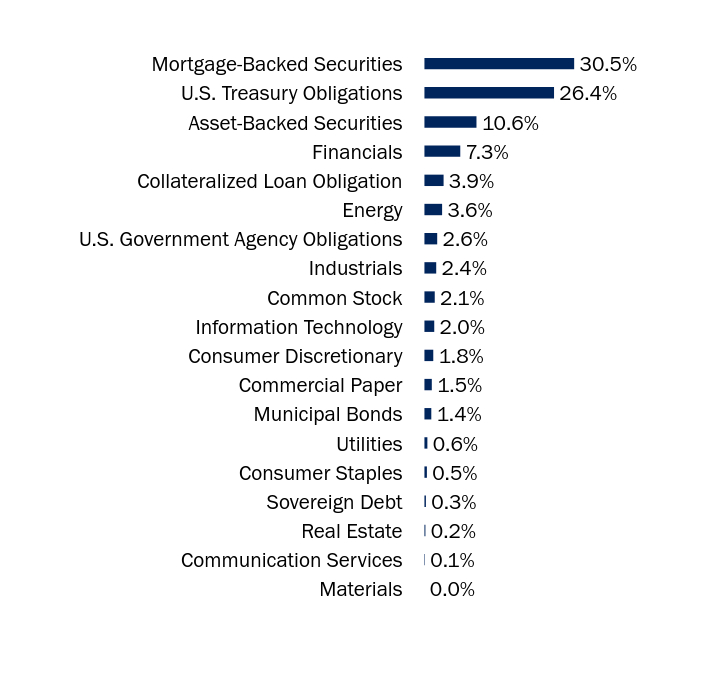

What did the Fund invest in?

Asset WeightingsFootnote Reference*

| Value | Value |

|---|

| Materials | 0.0% |

| Communication Services | 0.1% |

| Real Estate | 0.2% |

| Sovereign Debt | 0.3% |

| Consumer Staples | 0.5% |

| Utilities | 0.6% |

| Municipal Bonds | 1.4% |

| Commercial Paper | 1.5% |

| Consumer Discretionary | 1.8% |

| Information Technology | 2.0% |

| Common Stock | 2.1% |

| Industrials | 2.4% |

| U.S. Government Agency Obligations | 2.6% |

| Energy | 3.6% |

| Collateralized Loan Obligation | 3.9% |

| Financials | 7.3% |

| Asset-Backed Securities | 10.6% |

| U.S. Treasury Obligations | 26.4% |

| Mortgage-Backed Securities | 30.5% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | Coupon Rate | Maturity Date | Percentage of Total Net Assets |

|---|

| U.S. Treasury Bonds | 4.375% | 08/15/43 | 4.9% |

| U.S. Treasury Bonds | 3.250% | 05/15/42 | 3.2% |

| FHLMC, Ser 2024-5417, Cl JA | 5.500% | 08/25/44 | 2.9% |

| FHLMC, Ser 2024-5425, Cl A | 5.500% | 09/25/44 | 2.6% |

| U.S. Treasury Bonds | 3.875% | 05/15/43 | 2.3% |

| U.S. Treasury Bonds | 4.000% | 11/15/42 | 2.3% |

| U.S. Treasury Notes | 4.125% | 09/30/27 | 2.2% |

| Paratus Energy Services | 0.000% | — | 2.1% |

| U.S. Treasury Notes | 3.875% | 08/15/33 | 2.0% |

| U.S. Treasury Bonds | 4.000% | 11/15/52 | 1.5% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund; including its prospectus, financial information, holdings, and proxy voting information, visit or call:

1-877-71-FROST

https://frostinv.com/

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds.

Frost Total Return Bond Fund / Institutional Class Shares - FIJEX

Annual Shareholder Report - July 31, 2024

FIA-AR-TSR-2024-10

Frost Total Return Bond Fund

Frost Family of Funds - Investor Class Shares - FATRX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about Investor Class Shares of the Frost Total Return Bond Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Total Return Bond Fund, Investor Class Shares | $75 | 0.71% |

How did the Fund perform in the last year?

• The Bloomberg U.S. Aggregate Bond Index (the AGG) returned 5.10% over the year. The Frost Total Return Bond Fund (Investor Class Shares) returned 10.94% for the same period, bettering the benchmark by over 5.84%.

• Broadly, the Fund obtained outperformance relative to its benchmark from each of the four primary decisions the portfolio team utilizes – interest rate decisions, credit risk allocations, asset sector allocations and security selection.

• The Fund maintained its effective duration – a measure of interest rate risk – between 3.20% and 5.40% with the lower end of the range early in the year and increasing steadily throughout the year and finishing close to the high end of the range at the end of July 2024.

• With the benchmark’s average duration approximately 6.25%, the Fund’s underweight duration allocation resulted in positive outperformance relative to the benchmark. The primary benefit to the Fund’s interest rate profile, compared to the index, was the rise in yields for maturities over ten years due to the yield curve inversion. The Fund was strategically positioned throughout the year to take advantage of further yield curve inversion. The allocation to credit resulted in outperformance relative to the index as the credit markets outperformed U.S. government sectors. Risk asset sectors generally benefited from economic and credit cycle performance. The Fund throughout the year was slightly overweight the below investment grade securities and underweight government securities.

• The Fund outperformed due to individual security selection across several sectors. Individual security selection was the largest positive attribution metric relative to the benchmark during the year.

• The Fund held an average allocation of 5% to energy over the year. This resulted in positive relative performance. Several of the Fund’s oil holdings saw significant outperformance. The Fund held underweight allocations to Treasury, corporate and RMBS sectors and overweight ABS, CMBS and CLOs. Each of these sector allocations aided the Fund’s relative performance to the benchmark, even before any consideration to security selection.

• The Fund’s average allocations during the year were 29% Treasurys, 21% corporates, 17% RMBS, 10% CLOs, 10% ABS, and 6% CMBS.

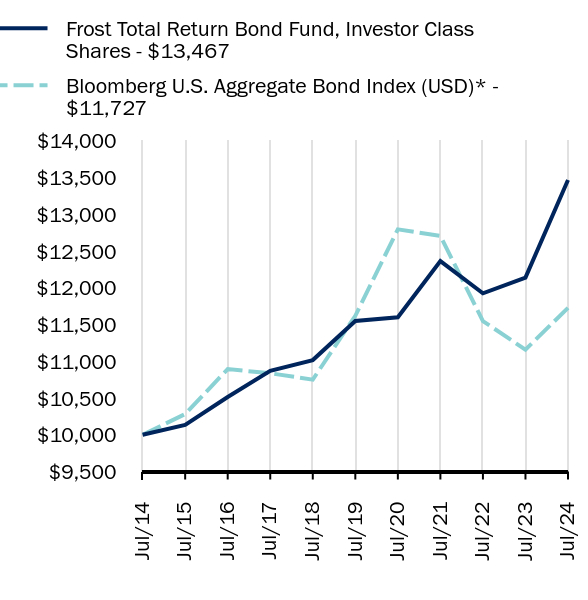

How did the fund perform during the last 10 years?

Total Return Based on $10,000 Investment

| Frost Total Return Bond Fund, Investor Class Shares - $13467 | Bloomberg U.S. Aggregate Bond Index (USD)* - $11727 |

|---|

| Jul/14 | $10000 | $10000 |

| Jul/15 | $10133 | $10282 |

| Jul/16 | $10514 | $10893 |

| Jul/17 | $10869 | $10837 |

| Jul/18 | $11016 | $10750 |

| Jul/19 | $11548 | $11619 |

| Jul/20 | $11599 | $12795 |

| Jul/21 | $12363 | $12705 |

| Jul/22 | $11925 | $11547 |

| Jul/23 | $12139 | $11158 |

| Jul/24 | $13467 | $11727 |

Average Annual Total Returns as of July 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Frost Total Return Bond Fund, Investor Class Shares | 10.94% | 3.12% | 3.02% |

| Bloomberg U.S. Aggregate Bond Index (USD)* | 5.10% | 0.19% | 1.61% |

The line graph represents historical performance of a hypothetical investment of $10,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 1-877-71-FROST or visit https://frostinv.com/ for current month-end performance.

Footnote Reference*As of July 2024, pursuant to the new regulatory requirements, this index replaced the prior index as the Fund's primary benchmark to represent a broad-based securities market index.

Key Fund Statistics as of July 31, 2024

| Total Net Assets | Number of Holdings | Total Advisory Fees Paid | Portfolio Turnover Rate |

|---|

| $3,373,875,556 | 392 | $10,281,854 | 48% |

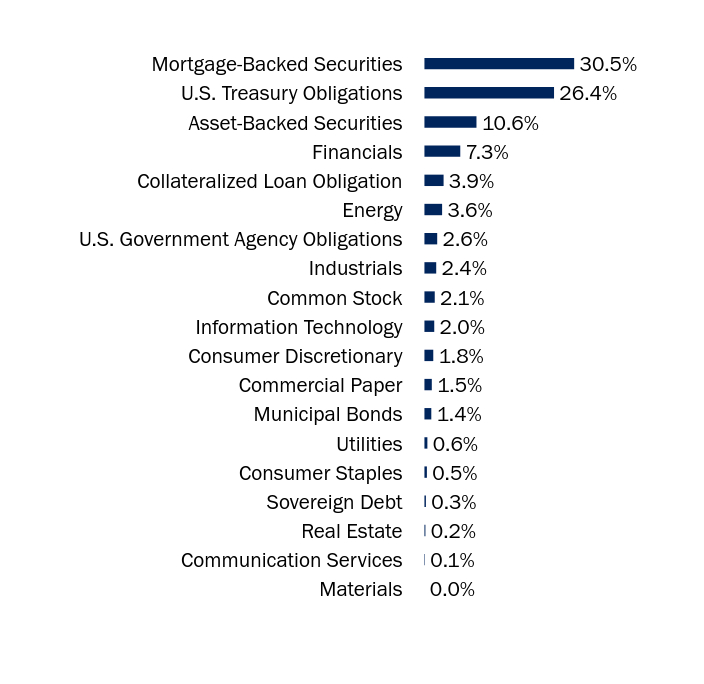

What did the Fund invest in?

Asset WeightingsFootnote Reference*

| Value | Value |

|---|

| Materials | 0.0% |

| Communication Services | 0.1% |

| Real Estate | 0.2% |

| Sovereign Debt | 0.3% |

| Consumer Staples | 0.5% |

| Utilities | 0.6% |

| Municipal Bonds | 1.4% |

| Commercial Paper | 1.5% |

| Consumer Discretionary | 1.8% |

| Information Technology | 2.0% |

| Common Stock | 2.1% |

| Industrials | 2.4% |

| U.S. Government Agency Obligations | 2.6% |

| Energy | 3.6% |

| Collateralized Loan Obligation | 3.9% |

| Financials | 7.3% |

| Asset-Backed Securities | 10.6% |

| U.S. Treasury Obligations | 26.4% |

| Mortgage-Backed Securities | 30.5% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | Coupon Rate | Maturity Date | Percentage of Total Net Assets |

|---|

| U.S. Treasury Bonds | 4.375% | 08/15/43 | 4.9% |

| U.S. Treasury Bonds | 3.250% | 05/15/42 | 3.2% |

| FHLMC, Ser 2024-5417, Cl JA | 5.500% | 08/25/44 | 2.9% |

| FHLMC, Ser 2024-5425, Cl A | 5.500% | 09/25/44 | 2.6% |

| U.S. Treasury Bonds | 3.875% | 05/15/43 | 2.3% |

| U.S. Treasury Bonds | 4.000% | 11/15/42 | 2.3% |

| U.S. Treasury Notes | 4.125% | 09/30/27 | 2.2% |

| Paratus Energy Services | 0.000% | — | 2.1% |

| U.S. Treasury Notes | 3.875% | 08/15/33 | 2.0% |

| U.S. Treasury Bonds | 4.000% | 11/15/52 | 1.5% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund; including its prospectus, financial information, holdings, and proxy voting information, visit or call:

1-877-71-FROST

https://frostinv.com/

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds.

Frost Total Return Bond Fund / Investor Class Shares - FATRX

Annual Shareholder Report - July 31, 2024

FIA-AR-TSR-2024-8

Frost Total Return Bond Fund

Frost Family of Funds - A Class Shares - FAJEX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about A Class Shares of the Frost Total Return Bond Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Total Return Bond Fund, A Class Shares | $85 | 0.81% |

How did the Fund perform in the last year?

• The Bloomberg U.S. Aggregate Bond Index (the AGG) returned 5.10% over the year. The Frost Total Return Bond Fund (A Class Shares) returned 10.96% for the same period, bettering the benchmark by 5.86%.

• Broadly, the Fund obtained outperformance relative to its benchmark from each of the four primary decisions the portfolio team utilizes – interest rate decisions, credit risk allocations, asset sector allocations and security selection.

• The Fund maintained its effective duration – a measure of interest rate risk – between 3.20% and 5.40% with the lower end of the range early in the year and increasing steadily throughout the year and finishing close to the high end of the range at the end of July 2024.

• With the benchmark’s average duration approximately 6.25%, the Fund’s underweight duration allocation resulted in positive outperformance relative to the benchmark. The primary benefit to the Fund’s interest rate profile, compared to the index, was the rise in yields for maturities over ten years due to the yield curve inversion. The Fund was strategically positioned throughout the year to take advantage of further yield curve inversion.The allocation to credit resulted in outperformance relative to the index as the credit markets outperformed U.S. government sectors. Risk asset sectors generally benefited from economic and credit cycle performance. The Fund throughout the year was slightly overweight the below investment grade securities and underweight government securities.

• The Fund outperformed due to individual security selection across several sectors. Individual security selection was the largest positive attribution metric relative to the benchmark during the year.

• The Fund held an average allocation of 5% to energy over the year. This resulted in positive relative performance. Several of the Fund’s oil holdings saw significant outperformance. The Fund held underweight allocations to Treasury, corporate and RMBS sectors and overweight ABS, CMBS and CLOs. Each of these sector allocations aided the Fund’s relative performance to the benchmark, even before any consideration to security selection.

• The Fund’s average allocations during the year were 29% Treasurys, 21% corporates, 17% RMBS, 10% CLOs, 10% ABS, and 6% CMBS.

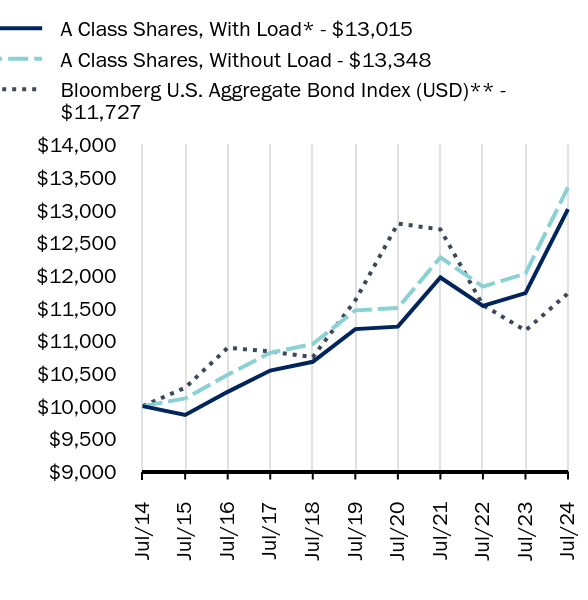

How did the fund perform during the last 10 years?

Total Return Based on $10,000 Investment

| A Class Shares, With Load* - $13015 | A Class Shares, Without Load - $13348 | Bloomberg U.S. Aggregate Bond Index (USD)** - $11727 |

|---|

| Jul/14 | $10000 | $10000 | $10000 |

| Jul/15 | $9865 | $10118 | $10282 |

| Jul/16 | $10219 | $10481 | $10893 |

| Jul/17 | $10545 | $10816 | $10837 |

| Jul/18 | $10679 | $10952 | $10750 |

| Jul/19 | $11179 | $11466 | $11619 |

| Jul/20 | $11217 | $11504 | $12795 |

| Jul/21 | $11969 | $12276 | $12705 |

| Jul/22 | $11534 | $11830 | $11547 |

| Jul/23 | $11730 | $12030 | $11158 |

| Jul/24 | $13015 | $13348 | $11727 |

Average Annual Total Returns as of July 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Frost Total Return Bond Fund | | | |

| A Class Shares, With Load* | 8.18% | 2.56% | 2.67% |

| A Class Shares, Without Load | 10.96% | 3.09% | 2.93% |

| Bloomberg U.S. Aggregate Bond Index (USD)** | 5.10% | 0.19% | 1.61% |

The line graph represents historical performance of a hypothetical investment of $10,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 1-877-71-FROST or visit https://frostinv.com/ for current month-end performance.

Footnote Reference*Reflects Sales charge of 2.50%

Footnote Reference**As of July 2024, pursuant to the new regulatory requirements, this index replaced the prior index as the Fund's primary benchmark to represent a broad-based securities market index.

Key Fund Statistics as of July 31, 2024

| Total Net Assets | Number of Holdings | Total Advisory Fees Paid | Portfolio Turnover Rate |

|---|

| $3,373,875,556 | 392 | $10,281,854 | 48% |

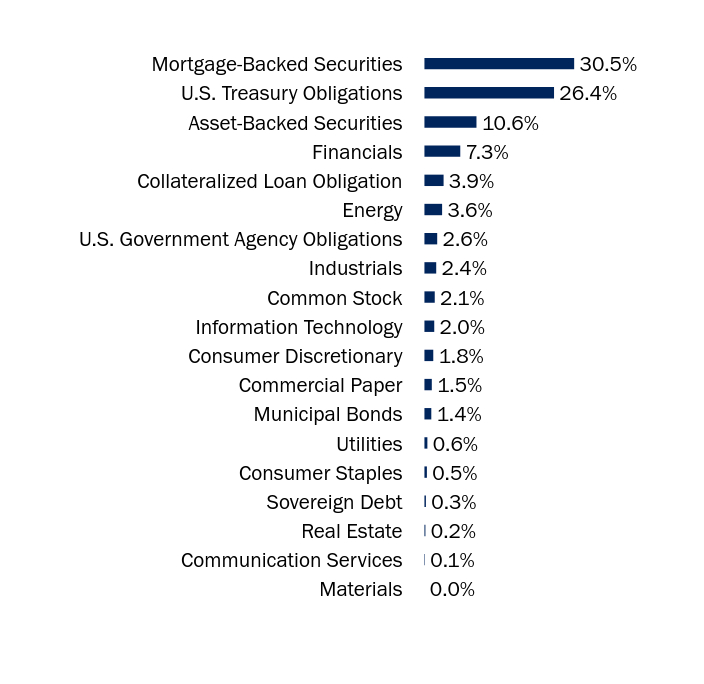

What did the Fund invest in?

Asset WeightingsFootnote Reference*

| Value | Value |

|---|

| Materials | 0.0% |

| Communication Services | 0.1% |

| Real Estate | 0.2% |

| Sovereign Debt | 0.3% |

| Consumer Staples | 0.5% |

| Utilities | 0.6% |

| Municipal Bonds | 1.4% |

| Commercial Paper | 1.5% |

| Consumer Discretionary | 1.8% |

| Information Technology | 2.0% |

| Common Stock | 2.1% |

| Industrials | 2.4% |

| U.S. Government Agency Obligations | 2.6% |

| Energy | 3.6% |

| Collateralized Loan Obligation | 3.9% |

| Financials | 7.3% |

| Asset-Backed Securities | 10.6% |

| U.S. Treasury Obligations | 26.4% |

| Mortgage-Backed Securities | 30.5% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | Coupon Rate | Maturity Date | Percentage of Total Net Assets |

|---|

| U.S. Treasury Bonds | 4.375% | 08/15/43 | 4.9% |

| U.S. Treasury Bonds | 3.250% | 05/15/42 | 3.2% |

| FHLMC, Ser 2024-5417, Cl JA | 5.500% | 08/25/44 | 2.9% |

| FHLMC, Ser 2024-5425, Cl A | 5.500% | 09/25/44 | 2.6% |

| U.S. Treasury Bonds | 3.875% | 05/15/43 | 2.3% |

| U.S. Treasury Bonds | 4.000% | 11/15/42 | 2.3% |

| U.S. Treasury Notes | 4.125% | 09/30/27 | 2.2% |

| Paratus Energy Services | 0.000% | — | 2.1% |

| U.S. Treasury Notes | 3.875% | 08/15/33 | 2.0% |

| U.S. Treasury Bonds | 4.000% | 11/15/52 | 1.5% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund; including its prospectus, financial information, holdings, and proxy voting information, visit or call:

1-877-71-FROST

https://frostinv.com/

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds.

Frost Total Return Bond Fund / A Class Shares - FAJEX

Annual Shareholder Report - July 31, 2024

FIA-AR-TSR-2024-9

Frost Family of Funds - Institutional Class Shares - FCFIX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about Institutional Class Shares of the Frost Credit Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Credit Fund, Institutional Class Shares | $74 | 0.70% |

How did the Fund perform in the last year?

• The Fund’s hybrid benchmark (50% Bloomberg U.S. Credit Index/50% Bloomberg U.S. Corporate High Yield Index) returned 8.79% for the year. The Fund returned 11.30% over the same period (the Institutional Share Class), representing a 2.51% of outperformance.

• The Fund was underweight interest rate risk throughout the year by maintaining its overall effective duration less than that of the benchmark. However, the Fund was also positioned for an expectation of a steeper yield curve (i.e., increasing yields as bond maturities increase) as the year progressed.

• The Fund’s effective duration was between 2.50% and 3.50%, with the low end of the range occurring early in the year and the high end of the range closer to the end of the year. This is compared to the 5.0% effective duration of the benchmark.

• Overall, the Fund saw very little overall performance attribution relative to the benchmark due to its interest rate risk profile. Overall Treasury yields declined somewhat over the year (for example the five-year Treasury Note yield decreased 4.25% to 3.75% in the year) but the yield curve steepened marginally as yields for shorter maturities declined and longer maturities increased. The Fund saw slight underperformance due to the shift in the yield curve but a largely offsetting outperformance in the yield curve twisting steeper as expected. These two interest rate profiles largely offset one another leading to very little performance attribution (positive or negative) for the Fund relative to the benchmark for the full year.

• The Fund was overweight the securitized market sectors (ABS, CMBS and CLOs) and underweight the investment-grade and high-yield corporate sector. These allocation positions resulted in relative outperformance as all three sectors delivered total returns over 12.0% in the year. The CLO sector delivered the best returns with almost 14.0% returns.

• The Fund was underweight credit risk such as high-yield sector, resulting in slight relative underperformance. Riskier sectors such as high yield outperformed during the year.

• The Fund slightly outperformed due to positive security selection. The Fund obtained slightly less than 1.0% of relative outperformance in the year based on security selection.

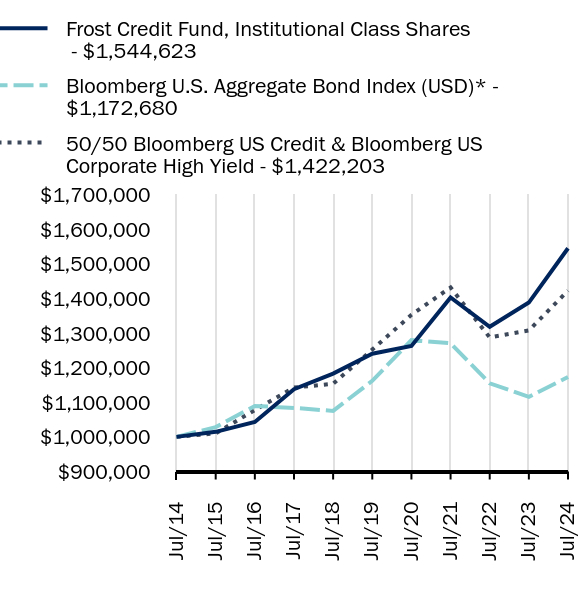

How did the fund perform during the last 10 years?

Total Return Based on $1,000,000 Investment

| Frost Credit Fund, Institutional Class Shares - $1544623 | Bloomberg U.S. Aggregate Bond Index (USD)* - $1172680 | 50/50 Bloomberg US Credit & Bloomberg US Corporate High Yield - $1422203 |

|---|

| Jul/14 | $1000000 | $1000000 | $1000000 |

| Jul/15 | $1014536 | $1028241 | $1010179 |

| Jul/16 | $1042848 | $1089267 | $1077583 |

| Jul/17 | $1137533 | $1083660 | $1142341 |

| Jul/18 | $1182571 | $1074990 | $1153392 |

| Jul/19 | $1240253 | $1161858 | $1252023 |

| Jul/20 | $1262413 | $1279452 | $1352360 |

| Jul/21 | $1402749 | $1270473 | $1431346 |

| Jul/22 | $1317850 | $1154652 | $1287269 |

| Jul/23 | $1387813 | $1115764 | $1307295 |

| Jul/24 | $1544623 | $1172680 | $1422203 |

Average Annual Total Returns as of July 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Frost Credit Fund, Institutional Class Shares | 11.30% | 4.49% | 4.44% |

| Bloomberg U.S. Aggregate Bond Index (USD)* | 5.10% | 0.19% | 1.61% |

| 50/50 Bloomberg US Credit & Bloomberg US Corporate High Yield | 8.79% | 2.58% | 3.58% |

The line graph represents historical performance of a hypothetical investment of $1,000,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 1-877-71-FROST or visit https://frostinv.com/ for current month-end performance.

Footnote Reference*As of July 2024, pursuant to the new regulatory requirements, this index replaced the prior index as the Fund's primary benchmark to represent a broad-based securities market index.

Key Fund Statistics as of July 31, 2024

| Total Net Assets | Number of Holdings | Total Advisory Fees Paid | Portfolio Turnover Rate |

|---|

| $317,464,023 | 177 | $1,032,438 | 26% |

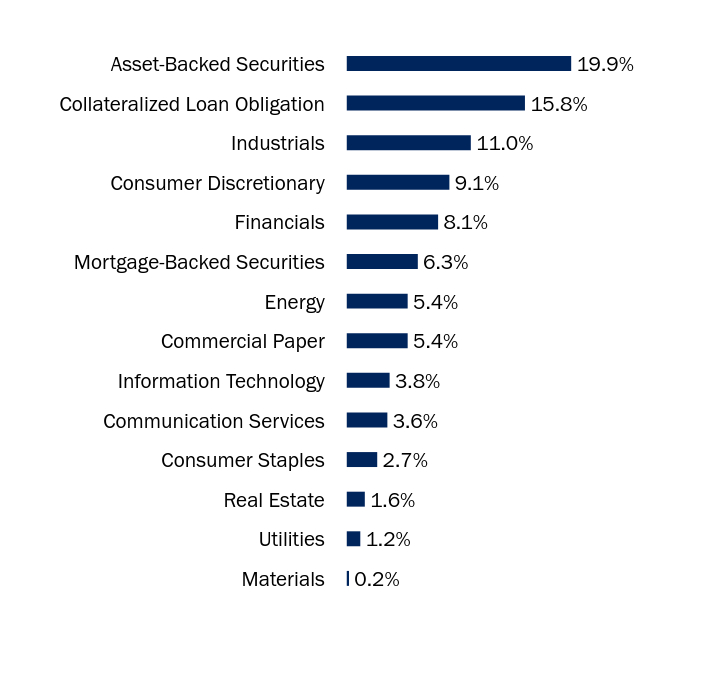

What did the Fund invest in?

Asset WeightingsFootnote Reference*

| Value | Value |

|---|

| Materials | 0.2% |

| Utilities | 1.2% |

| Real Estate | 1.6% |

| Consumer Staples | 2.7% |

| Communication Services | 3.6% |

| Information Technology | 3.8% |

| Commercial Paper | 5.4% |

| Energy | 5.4% |

| Mortgage-Backed Securities | 6.3% |

| Financials | 8.1% |

| Consumer Discretionary | 9.1% |

| Industrials | 11.0% |

| Collateralized Loan Obligation | 15.8% |

| Asset-Backed Securities | 19.9% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | Coupon Rate | Maturity Date | Percentage of Total Net Assets |

|---|

| Apidos CLO XL, Ser 2024-40A, Cl CR, TSFR3M + 1.950% | 7.235% | 07/15/37 | 1.6% |

| GoldenTree Loan Management US CLO 14, Ser 2024-14A, Cl CR, TSFR3M + 1.900% | 7.182% | 07/20/37 | 1.6% |

| Battalion CLO 17, Ser 2024-17A, Cl CR, TSFR3M + 2.250% | 7.532% | 03/09/34 | 1.6% |

| Burlington Northern Santa Fe | 5.500% | 03/15/55 | 1.3% |

| Cruise Yacht Upper HoldCo | 11.875% | 07/05/28 | 1.3% |

| Brundage-Bone Concrete Pumping Holdings | 6.000% | 02/01/26 | 1.3% |

| Concentrix | 6.850% | 08/02/33 | 1.3% |

| Race Point IX, Ser 2017-9A, Cl BR, TSFR3M + 2.412% | 7.713% | 10/15/30 | 1.3% |

| Kyndryl Holdings | 4.100% | 10/15/41 | 1.2% |

| Aircastle | 5.750% | 10/01/31 | 1.1% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund; including its prospectus, financial information, holdings, and proxy voting information, visit or call:

1-877-71-FROST

https://frostinv.com/

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds.

Frost Credit Fund / Institutional Class Shares - FCFIX

Annual Shareholder Report - July 31, 2024

FIA-AR-TSR-2024-1

Frost Family of Funds - Investor Class Shares - FCFAX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about Investor Class Shares of the Frost Credit Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Credit Fund, Investor Class Shares | $100 | 0.95% |

How did the Fund perform in the last year?

• The Fund’s hybrid benchmark (50% Bloomberg U.S. Credit Index/50% Bloomberg U.S. Corporate High Yield Index) returned 8.79% for the year. The Fund returned 11.05% over the same period (the Investor Share Class), representing a 2.27% of outperformance.

• The Fund was underweight interest rate risk throughout the year by maintaining its overall effective duration less than that of the benchmark. However, the Fund was also positioned for an expectation of a steeper yield curve (i.e., increasing yields as bond maturities increase) as the year progressed.

• The Fund’s effective duration was between 2.50% and 3.50%, with the low end of the range occurring early in the year and the high end of the range closer to the end of the year. This is compared to the 5.0% effective duration of the benchmark.

• Overall, the Fund saw very little overall performance attribution relative to the benchmark due to its interest rate risk profile. Overall Treasury yields declined somewhat over the year (for example the five-year Treasury Note yield decreased 4.25% to 3.75% in the year) but the yield curve steepened marginally as yields for shorter maturities declined and longer maturities increased. The Fund saw slight underperformance due to the shift in the yield curve but a largely offsetting outperformance in the yield curve twisting steeper as expected. These two interest rate profiles largely offset one another leading to very little performance attribution (positive or negative) for the Fund relative to the benchmark for the full year.

• The Fund was overweight the securitized market sectors (ABS, CMBS and CLOs) and underweight the investment-grade and high-yield corporate sector. These allocation positions resulted in relative outperformance as all three sectors delivered total returns over 12.0% in the year. The CLO sector delivered the best returns with almost 14.0% returns.

• The Fund was underweight credit risk such as high-yield sector, resulting in slight relative underperformance. Riskier sectors such as high yield outperformed during the year.

• The Fund slightly outperformed due to positive security selection. The Fund obtained slightly less than 1.0% of relative outperformance in the year based on security selection.

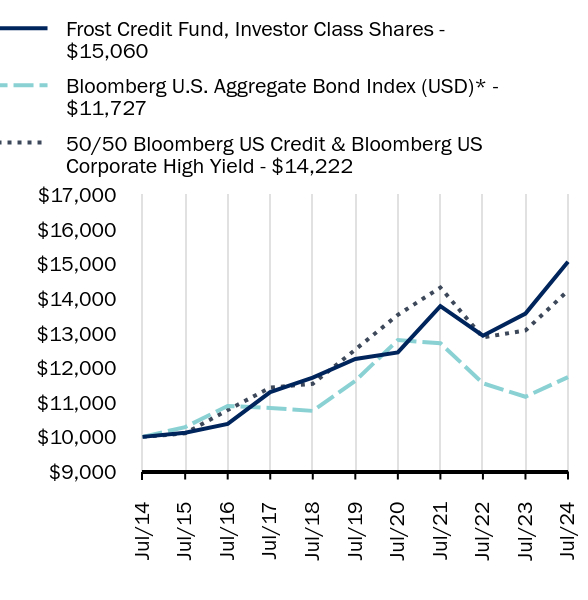

How did the fund perform during the last 10 years?

Total Return Based on $10,000 Investment

| Frost Credit Fund, Investor Class Shares - $15060 | Bloomberg U.S. Aggregate Bond Index (USD)* - $11727 | 50/50 Bloomberg US Credit & Bloomberg US Corporate High Yield - $14222 |

|---|

| Jul/14 | $10000 | $10000 | $10000 |

| Jul/15 | $10119 | $10282 | $10102 |

| Jul/16 | $10376 | $10893 | $10776 |

| Jul/17 | $11292 | $10837 | $11423 |

| Jul/18 | $11710 | $10750 | $11534 |

| Jul/19 | $12251 | $11619 | $12520 |

| Jul/20 | $12439 | $12795 | $13524 |

| Jul/21 | $13775 | $12705 | $14313 |

| Jul/22 | $12922 | $11547 | $12873 |

| Jul/23 | $13561 | $11158 | $13073 |

| Jul/24 | $15060 | $11727 | $14222 |

Average Annual Total Returns as of July 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Frost Credit Fund, Investor Class Shares | 11.05% | 4.21% | 4.18% |

| Bloomberg U.S. Aggregate Bond Index (USD)* | 5.10% | 0.19% | 1.61% |

| 50/50 Bloomberg US Credit & Bloomberg US Corporate High Yield | 8.79% | 2.58% | 3.58% |

The line graph represents historical performance of a hypothetical investment of $10,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 1-877-71-FROST or visit https://frostinv.com/ for current month-end performance.

Footnote Reference*As of July 2024, pursuant to the new regulatory requirements, this index replaced the prior index as the Fund's primary benchmark to represent a broad-based securities market index.

Key Fund Statistics as of July 31, 2024

| Total Net Assets | Number of Holdings | Total Advisory Fees Paid | Portfolio Turnover Rate |

|---|

| $317,464,023 | 177 | $1,032,438 | 26% |

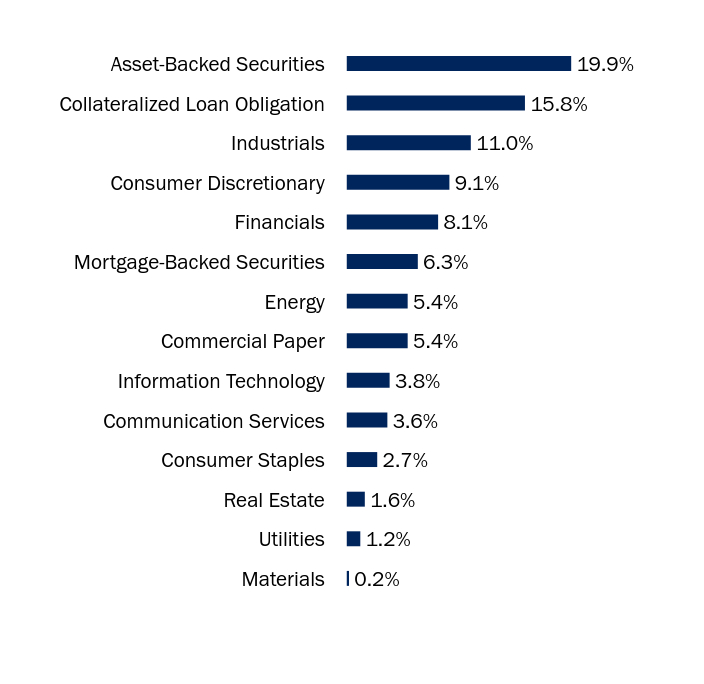

What did the Fund invest in?

Asset WeightingsFootnote Reference*

| Value | Value |

|---|

| Materials | 0.2% |

| Utilities | 1.2% |

| Real Estate | 1.6% |

| Consumer Staples | 2.7% |

| Communication Services | 3.6% |

| Information Technology | 3.8% |

| Commercial Paper | 5.4% |

| Energy | 5.4% |

| Mortgage-Backed Securities | 6.3% |

| Financials | 8.1% |

| Consumer Discretionary | 9.1% |

| Industrials | 11.0% |

| Collateralized Loan Obligation | 15.8% |

| Asset-Backed Securities | 19.9% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | Coupon Rate | Maturity Date | Percentage of Total Net Assets |

|---|

| Apidos CLO XL, Ser 2024-40A, Cl CR, TSFR3M + 1.950% | 7.235% | 07/15/37 | 1.6% |

| GoldenTree Loan Management US CLO 14, Ser 2024-14A, Cl CR, TSFR3M + 1.900% | 7.182% | 07/20/37 | 1.6% |

| Battalion CLO 17, Ser 2024-17A, Cl CR, TSFR3M + 2.250% | 7.532% | 03/09/34 | 1.6% |

| Burlington Northern Santa Fe | 5.500% | 03/15/55 | 1.3% |

| Cruise Yacht Upper HoldCo | 11.875% | 07/05/28 | 1.3% |

| Brundage-Bone Concrete Pumping Holdings | 6.000% | 02/01/26 | 1.3% |

| Concentrix | 6.850% | 08/02/33 | 1.3% |

| Race Point IX, Ser 2017-9A, Cl BR, TSFR3M + 2.412% | 7.713% | 10/15/30 | 1.3% |

| Kyndryl Holdings | 4.100% | 10/15/41 | 1.2% |

| Aircastle | 5.750% | 10/01/31 | 1.1% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund; including its prospectus, financial information, holdings, and proxy voting information, visit or call:

1-877-71-FROST

https://frostinv.com/

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds.

Frost Credit Fund / Investor Class Shares - FCFAX

Annual Shareholder Report - July 31, 2024

FIA-AR-TSR-2024-2

Frost Family of Funds - A Class Shares - FCFBX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about A Class Shares of the Frost Credit Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Credit Fund, A Class Shares | $100 | 0.95% |

How did the Fund perform in the last year?

• The Fund’s hybrid benchmark (50% Bloomberg U.S. Credit Index/50% Bloomberg U.S. Corporate High Yield Index) returned 8.79% for the year. The Fund returned 10.94% over the same period (the A Share Class), representing a 2.15% of outperformance.

• The Fund was underweight interest rate risk throughout the year by maintaining its overall effective duration less than that of the benchmark. However, the Fund was also positioned for an expectation of a steeper yield curve (i.e., increasing yields as bond maturities increase) as the year progressed.

• The Fund’s effective duration was between 2.50% and 3.50%, with the low end of the range occurring early in the year and the high end of the range closer to the end of the year. This is compared to the 5.0% effective duration of the benchmark.

• Overall, the Fund saw very little overall performance attribution relative to the benchmark due to its interest rate risk profile. Overall Treasury yields declined somewhat over the year (for example the five-year Treasury Note yield decreased 4.25% to 3.75% in the year) but the yield curve steepened marginally as yields for shorter maturities declined and longer maturities increased. The Fund saw slight underperformance due to the shift in the yield curve but a largely offsetting outperformance in the yield curve twisting steeper as expected. These two interest rate profiles largely offset one another leading to very little performance attribution (positive or negative) for the Fund relative to the benchmark for the full year.

• The Fund was overweight the securitized market sectors (ABS, CMBS and CLOs) and underweight the investment-grade and high-yield corporate sector. These allocation positions resulted in relative outperformance as all three sectors delivered total returns over 12.0% in the year. The CLO sector delivered the best returns with almost 14.0% returns.

• The Fund was underweight credit risk such as high-yield sector, resulting in slight relative underperformance. Riskier sectors such as high yield outperformed during the year.

• The Fund slightly outperformed due to positive security selection. The Fund obtained slightly less than 1.0% of relative outperformance in the year based on security selection.

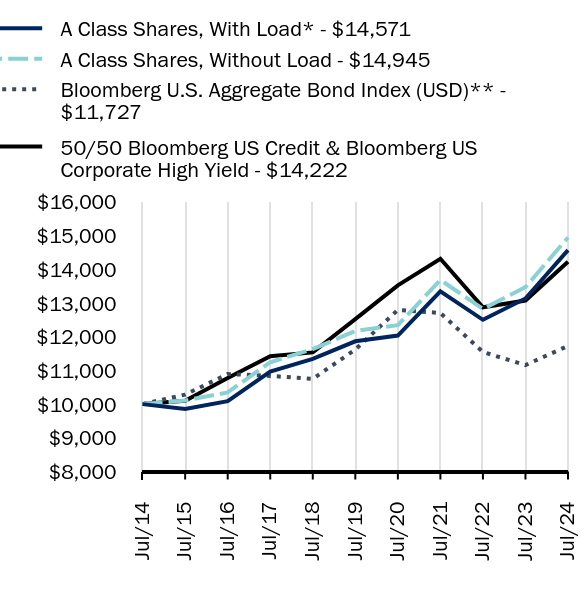

How did the fund perform during the last 10 years?

Total Return Based on $10,000 Investment

| A Class Shares, With Load* - $14571 | A Class Shares, Without Load - $14945 | Bloomberg U.S. Aggregate Bond Index (USD)** - $11727 | 50/50 Bloomberg US Credit & Bloomberg US Corporate High Yield - $14222 |

|---|

| Jul/14 | $10000 | $10000 | $10000 | $10000 |

| Jul/15 | $9855 | $10108 | $10282 | $10102 |

| Jul/16 | $10087 | $10346 | $10893 | $10776 |

| Jul/17 | $10962 | $11243 | $10837 | $11423 |

| Jul/18 | $11342 | $11633 | $10750 | $11534 |

| Jul/19 | $11864 | $12168 | $11619 | $12520 |

| Jul/20 | $12035 | $12343 | $12795 | $13524 |

| Jul/21 | $13343 | $13685 | $12705 | $14313 |

| Jul/22 | $12502 | $12823 | $11547 | $12873 |

| Jul/23 | $13135 | $13472 | $11158 | $13073 |

| Jul/24 | $14571 | $14945 | $11727 | $14222 |

Average Annual Total Returns as of July 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Frost Credit Fund | | | |

| A Class Shares, With Load* | 8.18% | 3.67% | 3.84% |

| A Class Shares, Without Load | 10.94% | 4.20% | 4.10% |

| Bloomberg U.S. Aggregate Bond Index (USD)** | 5.10% | 0.19% | 1.61% |

| 50/50 Bloomberg US Credit & Bloomberg US Corporate High Yield | 8.79% | 2.58% | 3.58% |

The line graph represents historical performance of a hypothetical investment of $10,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 1-877-71-FROST or visit https://frostinv.com/ for current month-end performance.

Footnote Reference*Reflects Sales charge of 2.50%

Footnote Reference**As of July 2024, pursuant to the new regulatory requirements, this index replaced the prior index as the Fund's primary benchmark to represent a broad-based securities market index.

Key Fund Statistics as of July 31, 2024

| Total Net Assets | Number of Holdings | Total Advisory Fees Paid | Portfolio Turnover Rate |

|---|

| $317,464,023 | 177 | $1,032,438 | 26% |

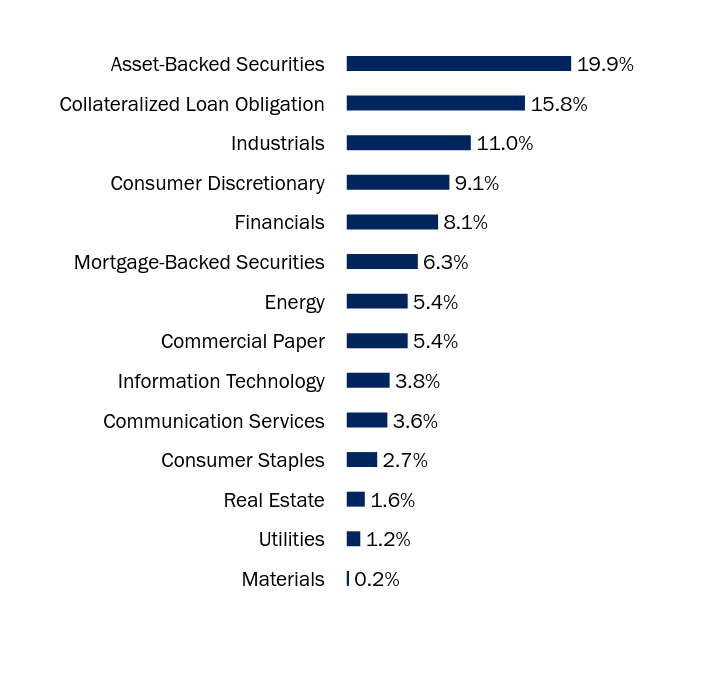

What did the Fund invest in?

Asset WeightingsFootnote Reference*

| Value | Value |

|---|

| Materials | 0.2% |

| Utilities | 1.2% |

| Real Estate | 1.6% |

| Consumer Staples | 2.7% |

| Communication Services | 3.6% |

| Information Technology | 3.8% |

| Commercial Paper | 5.4% |

| Energy | 5.4% |

| Mortgage-Backed Securities | 6.3% |

| Financials | 8.1% |

| Consumer Discretionary | 9.1% |

| Industrials | 11.0% |

| Collateralized Loan Obligation | 15.8% |

| Asset-Backed Securities | 19.9% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | Coupon Rate | Maturity Date | Percentage of Total Net Assets |

|---|

| Apidos CLO XL, Ser 2024-40A, Cl CR, TSFR3M + 1.950% | 7.235% | 07/15/37 | 1.6% |

| GoldenTree Loan Management US CLO 14, Ser 2024-14A, Cl CR, TSFR3M + 1.900% | 7.182% | 07/20/37 | 1.6% |

| Battalion CLO 17, Ser 2024-17A, Cl CR, TSFR3M + 2.250% | 7.532% | 03/09/34 | 1.6% |

| Burlington Northern Santa Fe | 5.500% | 03/15/55 | 1.3% |

| Cruise Yacht Upper HoldCo | 11.875% | 07/05/28 | 1.3% |

| Brundage-Bone Concrete Pumping Holdings | 6.000% | 02/01/26 | 1.3% |

| Concentrix | 6.850% | 08/02/33 | 1.3% |

| Race Point IX, Ser 2017-9A, Cl BR, TSFR3M + 2.412% | 7.713% | 10/15/30 | 1.3% |

| Kyndryl Holdings | 4.100% | 10/15/41 | 1.2% |

| Aircastle | 5.750% | 10/01/31 | 1.1% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund; including its prospectus, financial information, holdings, and proxy voting information, visit or call:

1-877-71-FROST

https://frostinv.com/

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds.

Frost Credit Fund / A Class Shares - FCFBX

Annual Shareholder Report - July 31, 2024

FIA-AR-TSR-2024-3

Frost Low Duration Bond Fund

Frost Family of Funds - Institutional Class Shares - FILDX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about Institutional Class Shares of the Frost Low Duration Bond Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Low Duration Bond Fund, Institutional Class Shares | $47 | 0.45% |

How did the Fund perform in the last year?

• The Bloomberg U.S. Government Credit One to Five Year Bond Index returned 5.83% during the year that ended July 31, 2024. The Frost Low Duration Bond Fund (Institutional Share Class) returned 6.94% over the same period, outperformance of 1.10%.

• The Fund maintained an underweight allocation to interest rate risk, with an effective duration profile of between 2.0% and 2.40% compared to the benchmark’s average duration of approximately 2.65%.

• Short-term interest rates, while volatile, finished the year ever so slightly lower than where they began the year as the Federal Reserve largely made no significant changes to monetary policy and the US economy remained solid.

• In turn, the Fund saw little relative performance attribution (neither positive nor negative) from its interest rate profile compared to its benchmark.

• The Fund’s primary relative outperformance was positive sector allocations. The Fund held a meaningful overweight to the ABS sector (40%) and an underweight to the Treasury sector (26%). The ABS sector during the year meaningfully outperformed, before taking into account security selection, both the investment grade corporate and the Treasury sectors. The Treasury sector delivered the lowest aggregate returns as well. Overall, the Fund obtained approximately 1.0% of its outperformance relative to the benchmark from these sector allocation decisions.

• The Fund obtained approximately 0.25% of outperformance do to solid individual security selection in the year. Most of these results came in the Fund’s investment grade corporate sector.

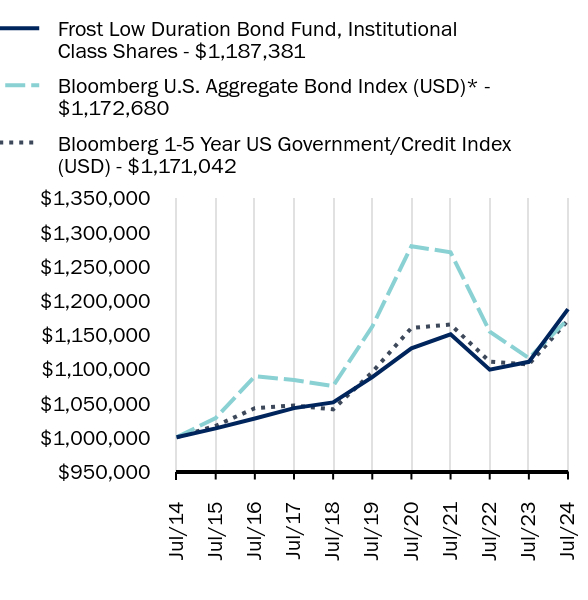

How did the fund perform during the last 10 years?

Total Return Based on $1,000,000 Investment

| Frost Low Duration Bond Fund, Institutional Class Shares - $1187381 | Bloomberg U.S. Aggregate Bond Index (USD)* - $1172680 | Bloomberg 1-5 Year US Government/Credit Index (USD) - $1171042 |

|---|

| Jul/14 | $1000000 | $1000000 | $1000000 |

| Jul/15 | $1013015 | $1028241 | $1016817 |

| Jul/16 | $1027478 | $1089267 | $1042602 |

| Jul/17 | $1042698 | $1083660 | $1046542 |

| Jul/18 | $1051007 | $1074990 | $1040877 |

| Jul/19 | $1088009 | $1161858 | $1095239 |

| Jul/20 | $1130030 | $1279452 | $1159926 |

| Jul/21 | $1150561 | $1270473 | $1164863 |

| Jul/22 | $1098858 | $1154652 | $1110767 |

| Jul/23 | $1110356 | $1115764 | $1106545 |

| Jul/24 | $1187381 | $1172680 | $1171042 |

Average Annual Total Returns as of July 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Frost Low Duration Bond Fund, Institutional Class Shares | 6.94% | 1.76% | 1.73% |

| Bloomberg U.S. Aggregate Bond Index (USD)* | 5.10% | 0.19% | 1.61% |

| Bloomberg 1-5 Year US Government/Credit Index (USD) | 5.83% | 1.35% | 1.59% |

The line graph represents historical performance of a hypothetical investment of $1,000,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 1-877-71-FROST or visit https://frostinv.com/ for current month-end performance.

Footnote Reference*As of July 2024, pursuant to the new regulatory requirements, this index replaced the prior index as the Fund's primary benchmark to represent a broad-based securities market index.

Key Fund Statistics as of July 31, 2024

| Total Net Assets | Number of Holdings | Total Advisory Fees Paid | Portfolio Turnover Rate |

|---|

| $320,433,457 | 75 | $902,705 | 72% |

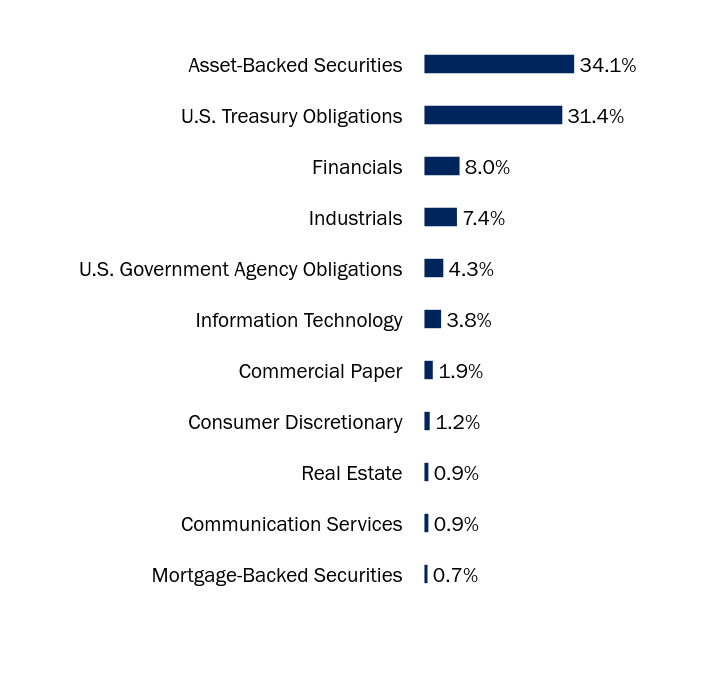

What did the Fund invest in?

Asset WeightingsFootnote Reference*

| Value | Value |

|---|

| Mortgage-Backed Securities | 0.7% |

| Communication Services | 0.9% |

| Real Estate | 0.9% |

| Consumer Discretionary | 1.2% |

| Commercial Paper | 1.9% |

| Information Technology | 3.8% |

| U.S. Government Agency Obligations | 4.3% |

| Industrials | 7.4% |

| Financials | 8.0% |

| U.S. Treasury Obligations | 31.4% |

| Asset-Backed Securities | 34.1% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | Coupon Rate | Maturity Date | Percentage of Total Net Assets |

|---|

| U.S. Treasury Notes | 4.000% | 01/31/29 | 14.1% |

| U.S. Treasury Notes | 4.375% | 11/30/28 | 7.9% |

| U.S. Treasury Notes | 4.000% | 02/29/28 | 7.8% |

| Molex Electronic Technologies | 3.900% | 04/15/25 | 3.1% |

| Verizon Master Trust, Ser 2023-4, Cl C | 5.650% | 06/20/29 | 3.1% |

| Fifth Third Bancorp, SOFRINDX + 2.192% | 6.361% | 10/27/28 | 2.6% |

| Prestige Auto Receivables Trust, Ser 2023-1A, Cl B | 5.550% | 04/15/27 | 2.5% |

| Kyndryl Holdings | 2.050% | 10/15/26 | 2.3% |

| Westlake Automobile Receivables Trust, Ser 2022-3A, Cl D | 6.680% | 04/17/28 | 2.2% |

| Charles Schwab, SOFRRATE + 2.210% | 5.643% | 05/19/29 | 1.6% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund; including its prospectus, financial information, holdings, and proxy voting information, visit or call:

1-877-71-FROST

https://frostinv.com/

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds.

Frost Low Duration Bond Fund / Institutional Class Shares - FILDX

Annual Shareholder Report - July 31, 2024

FIA-AR-TSR-2024-7

Frost Low Duration Bond Fund

Frost Family of Funds - Investor Class Shares - FADLX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about Investor Class Shares of the Frost Low Duration Bond Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Low Duration Bond Fund, Investor Class Shares | $71 | 0.69% |

How did the Fund perform in the last year?

• The Bloomberg U.S. Government Credit One to Five Year Bond Index returned 5.83% during the year that ended July 31, 2024. The Frost Low Duration Bond Fund (Investor Share Class) returned 6.64% over the same period, outperformance of 0.81%.

• The Fund maintained an underweight allocation to interest rate risk, with an effective duration profile of between 2.0% and 2.40% compared to the benchmark’s average duration of approximately 2.65%.

• Short-term interest rates, while volatile, finished the year ever so slightly lower than where they began the year as the Federal Reserve largely made no significant changes to monetary policy and the US economy remained solid.

• In turn, the Fund saw little relative performance attribution (neither positive nor negative) from its interest rate profile compared to its benchmark.

• The Fund’s primary relative outperformance was positive sector allocations. The Fund held a meaningful overweight to the ABS sector (40%) and an underweight to the Treasury sector (26%). The ABS sector during the year meaningfully outperformed, before taking into account security selection, both the investment grade corporate and the Treasury sectors. The Treasury sector delivered the lowest aggregate returns as well. Overall, the Fund obtained approximately 1.0% of its outperformance relative to the benchmark from these sector allocation decisions.

• The Fund obtained approximately 0.25% of outperformance do to solid individual security selection in the year. Most of these results came in the Fund’s investment grade corporate sector.

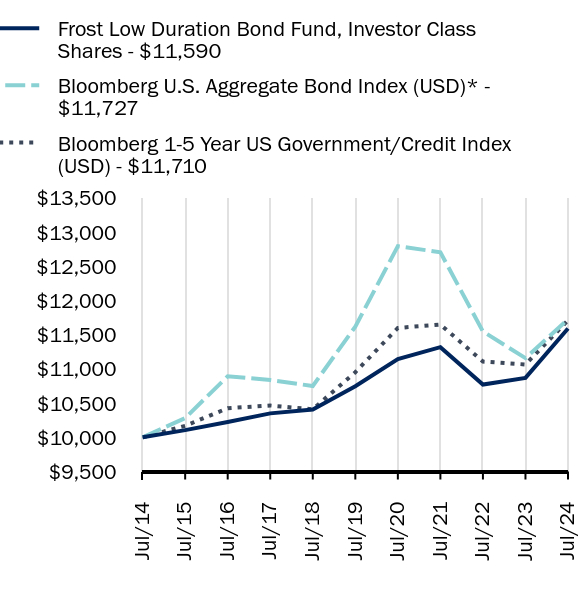

How did the fund perform during the last 10 years?

Total Return Based on $10,000 Investment

| Frost Low Duration Bond Fund, Investor Class Shares - $11590 | Bloomberg U.S. Aggregate Bond Index (USD)* - $11727 | Bloomberg 1-5 Year US Government/Credit Index (USD) - $11710 |

|---|

| Jul/14 | $10000 | $10000 | $10000 |

| Jul/15 | $10105 | $10282 | $10168 |

| Jul/16 | $10224 | $10893 | $10426 |

| Jul/17 | $10350 | $10837 | $10465 |

| Jul/18 | $10407 | $10750 | $10409 |

| Jul/19 | $10746 | $11619 | $10952 |

| Jul/20 | $11144 | $12795 | $11599 |

| Jul/21 | $11318 | $12705 | $11649 |

| Jul/22 | $10772 | $11547 | $11108 |

| Jul/23 | $10869 | $11158 | $11065 |

| Jul/24 | $11590 | $11727 | $11710 |

Average Annual Total Returns as of July 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Frost Low Duration Bond Fund, Investor Class Shares | 6.64% | 1.52% | 1.49% |

| Bloomberg U.S. Aggregate Bond Index (USD)* | 5.10% | 0.19% | 1.61% |

| Bloomberg 1-5 Year US Government/Credit Index (USD) | 5.83% | 1.35% | 1.59% |

The line graph represents historical performance of a hypothetical investment of $10,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 1-877-71-FROST or visit https://frostinv.com/ for current month-end performance.

Footnote Reference*As of July 2024, pursuant to the new regulatory requirements, this index replaced the prior index as the Fund's primary benchmark to represent a broad-based securities market index.

Key Fund Statistics as of July 31, 2024

| Total Net Assets | Number of Holdings | Total Advisory Fees Paid | Portfolio Turnover Rate |

|---|

| $320,433,457 | 75 | $902,705 | 72% |

What did the Fund invest in?

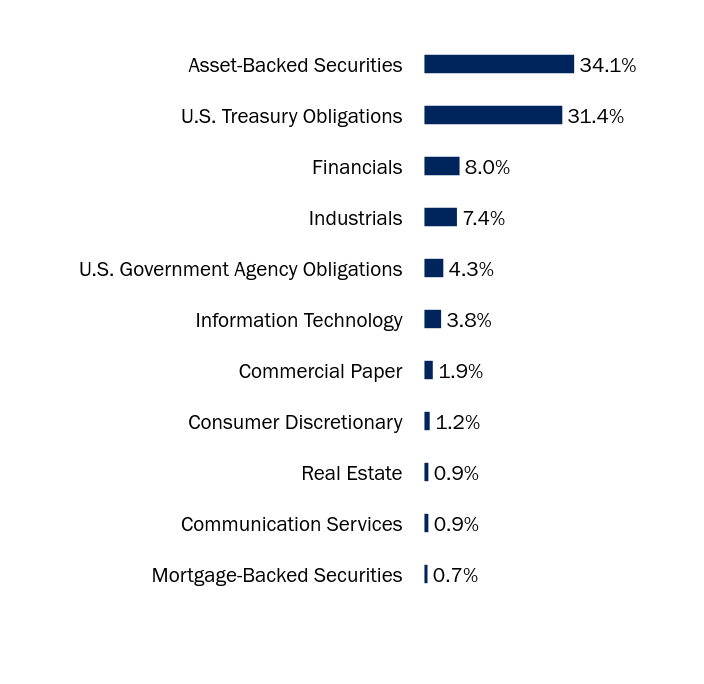

Asset WeightingsFootnote Reference*

| Value | Value |

|---|

| Mortgage-Backed Securities | 0.7% |

| Communication Services | 0.9% |

| Real Estate | 0.9% |

| Consumer Discretionary | 1.2% |

| Commercial Paper | 1.9% |

| Information Technology | 3.8% |

| U.S. Government Agency Obligations | 4.3% |

| Industrials | 7.4% |

| Financials | 8.0% |

| U.S. Treasury Obligations | 31.4% |

| Asset-Backed Securities | 34.1% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | Coupon Rate | Maturity Date | Percentage of Total Net Assets |

|---|

| U.S. Treasury Notes | 4.000% | 01/31/29 | 14.1% |

| U.S. Treasury Notes | 4.375% | 11/30/28 | 7.9% |

| U.S. Treasury Notes | 4.000% | 02/29/28 | 7.8% |

| Molex Electronic Technologies | 3.900% | 04/15/25 | 3.1% |

| Verizon Master Trust, Ser 2023-4, Cl C | 5.650% | 06/20/29 | 3.1% |

| Fifth Third Bancorp, SOFRINDX + 2.192% | 6.361% | 10/27/28 | 2.6% |

| Prestige Auto Receivables Trust, Ser 2023-1A, Cl B | 5.550% | 04/15/27 | 2.5% |

| Kyndryl Holdings | 2.050% | 10/15/26 | 2.3% |

| Westlake Automobile Receivables Trust, Ser 2022-3A, Cl D | 6.680% | 04/17/28 | 2.2% |

| Charles Schwab, SOFRRATE + 2.210% | 5.643% | 05/19/29 | 1.6% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund; including its prospectus, financial information, holdings, and proxy voting information, visit or call:

1-877-71-FROST

https://frostinv.com/

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds.

Frost Low Duration Bond Fund / Investor Class Shares - FADLX

Annual Shareholder Report - July 31, 2024

FIA-AR-TSR-2024-6

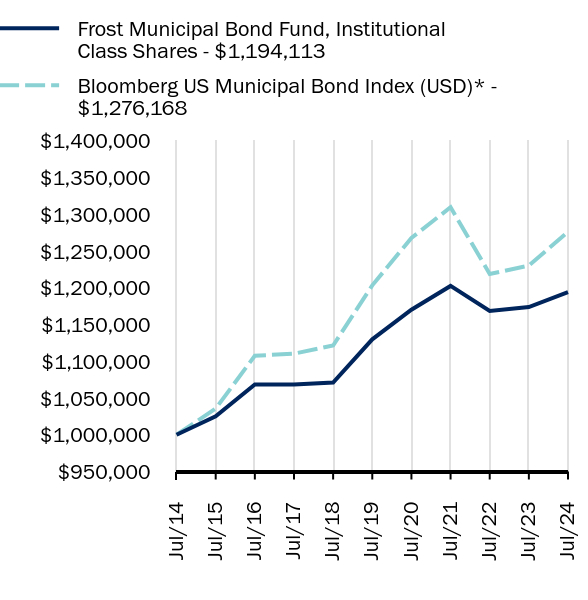

Frost Municipal Bond Fund

Frost Family of Funds - Institutional Class Shares - FIMUX

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about Institutional Class Shares of the Frost Municipal Bond Fund (the "Fund") for the period from August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://frostinv.com/. You can also request this information by contacting us at 1-877-71-FROST. This annual shareholder report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Frost Municipal Bond Fund, Institutional Class Shares | $105 | 1.04% |

How did the Fund perform in the last year?