UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 1-K

ANNUAL REPORT

ANNUAL REPORT PURSUANT TO REGULATION A OF THE SECURITIES ACT OF 1933

For the fiscal year ended December 31, 2021

GolfSuites 1, Inc.

(Exact name of issuer as specified in its charter)

| Delaware | 83-2379196 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

2738 Falkenburg Road South Riverview, FL 33578 |

33578 | |

| (Address of principal executive offices) | (Zip Code) |

| (813) 621-5000 | ||

| (Phone) |

| Preferred Stock |

| (Title of each class of securities issued pursuant to Regulation A) |

TABLE OF CONTENTS

In this Annual Report, the term “GolfSuites,” “we,” “us,” “our,” or “the company” refers to GolfSuites 1, Inc. a Delaware corporation and its wholly-owned subsidiaries on a consolidated basis. The term “GolfSuites Lubbock” refers to GolfSuites Lubbock, LLC, the term “GolfSuites Tulsa” refers to GolfSuites Tulsa, LLC and the term “GolfSuites Baton Rouge” refers to GolfSuites Baton Rouge, LLC. GolfSuites Lubbock, GolfSuites Tulsa, and GolfSuites Baton Rouge are wholly owned subsidiaries of the company.

THIS ANNUAL REPORT MAY CONTAIN FORWARD-LOOKING STATEMENTS AND INFORMATION RELATING TO, AMONG OTHER THINGS, THE COMPANY, ITS BUSINESS PLAN AND STRATEGY, AND ITS INDUSTRY. THESE FORWARD-LOOKING STATEMENTS ARE BASED ON THE BELIEFS OF, ASSUMPTIONS MADE BY, AND INFORMATION CURRENTLY AVAILABLE TO THE COMPANY’S MANAGEMENT. WHEN USED IN THE ANNUAL REPORT, THE WORDS “ESTIMATE,” “PROJECT,” “BELIEVE,” “ANTICIPATE,” “INTEND,” “EXPECT” AND SIMILAR EXPRESSIONS ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS, WHICH CONSTITUTE FORWARD LOOKING STATEMENTS. THESE STATEMENTS REFLECT MANAGEMENT’S CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS AND UNCERTAINTIES THAT COULD CAUSE THE COMPANY’S ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE CONTAINED IN THE FORWARD-LOOKING STATEMENTS. INVESTORS ARE CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD-LOOKING STATEMENTS, WHICH SPEAK ONLY AS OF THE DATE ON WHICH THEY ARE MADE. THE COMPANY DOES NOT UNDERTAKE ANY OBLIGATION TO REVISE OR UPDATE THESE FORWARD-LOOKING STATEMENTS TO REFLECT EVENTS OR CIRCUMSTANCES AFTER SUCH DATE OR TO REFLECT THE OCCURRENCE OF UNANTICIPATED EVENTS.

ii

Overview

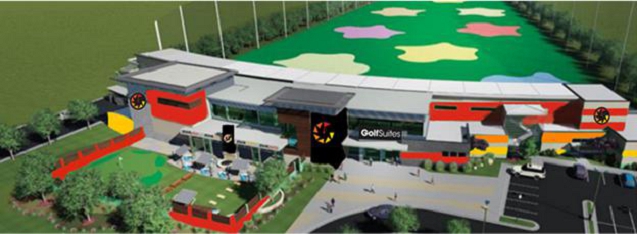

GolfSuites 1, Inc. (“GolfSuites”) owns, leases, and operates golf driving range entertainment centers in the United States. At its entertainment centers it aims to provide next generation hospitality and dining venues, high-tech gamified golf in climate-controlled suites, live entertainment, and spaces for both social and corporate functions. The company was incorporated in Delaware on October 25, 2018 as KGEM Golf Midwest, Inc. On January 15, 2019, the company changed its name to GolfSuites 1, Inc.

The company owns two wholly owned subsidiaries, GolfSuites Tulsa, LLC, an Oklahoma limited liability company, and GolfSuites Lubbock, LLC, a Texas limited liability company. The company owns 62.5% of GolfSuites Baton Rouge, LLC a Louisiana limited liability company. A third party owns the remaining 37.5% of GolfSuites Baton Rouge.

The company is a subsidiary of GolfSuites, Inc. (the “Parent Company”). The Parent Company was incorporated in 2018 as a successor entity to KGE, LLC, which was created in 2016 to develop and operate a national chain of golf driving range entertainment centers. GolfSuites, Inc. change its name from KGEM Golf, Inc. to GolfSuites, Inc. on December 3, 2020.

Timeline

Below is a timeline of the company’s operating history.

| ● | On October 25, 2018, the company was incorporated. | |

| ● | In September 2019, GolfSuites 3, Inc., an affiliate of the company, began operating an facility in Jenks, Oklahoma (the “Tulsa Facility”) pursuant to a lease agreement governing the Tulsa Facility and an additional agreement governing the land on which it is located. Both lease agreements were entered into by GolfSuite 3’s wholly owned subsidiary, GolfSuites Tulsa. | |

| ● | On August 6, 2020, GolfSuites Lubbock was formed. It is a wholly owned subsidiary of the company. | |

| ● | In November 2020, the company began discussions and drafting documents to acquire the Tulsa Facility and the land on which it is located. The company believes that it will acquire the facility and land by the end of Q2 2021. | |

| ● | On August 19, 2020, pursuant to the Membership Interest Purchase Agreement (“MIP Agreement”), GolfSuites Lubbock acquired 4ORE Golf, LLC, a Texas Limited Liability Company, (the “Lubbock Facility”). The Membership Interest Purchase Agreement is included as an Exhibit to this Form 1-K. | |

| ● | On August 19, 2020, GolfSuites Lubbock, pursuant to the MIP Agreement, assumed the lease agreement governing the land on which the Lubbock Facility is located. The related lease agreement is included as an Exhibit to this Form 1-K. | |

| ● | On December 30, 2020, the company acquired GolfSuites Tulsa from GolfSuites 3. | |

| ● | On February 9, 2021, the company entered into a lease agreement for an approximate 18-acre existing driving range located at 8181 Siegen Lane, Baton Rouge, Louisiana (the “Baton Rouge Facility”) and has a term of five years. The lease commenced on March 1, 2021. |

- 1 -

The Facilities

Below are statistics related to each facility.

| TULSA FACILITY | LUBBOCK FACILITY | BATON ROUGE FACILITY* | ||||

| ENTERTAINMENT AMENITIES | 60 golf suites. | 56 golf suites. | 40 golf suites planned. | |||

| These suites open up to the golf target field and incorporate comfortable seating, ball dispensers, club storage, gaming and media displays. | These suites open up to the golf target field and incorporate comfortable seating, ball dispensers, club storage, gaming and media displays. | It is intended that these suites open up to the golf target field and incorporate comfortable seating, ball dispensers, club storage, gaming and media displays. | ||||

| Private lessons available, pinball, pool and corn hole. | Private lessons available, pinball, pool and corn hole. | Private lessons will be made available, pinball, pool and corn hole will also be available. | ||||

| HOSPITALITY AMENITIES | 2 restaurants and 2 bars. | 2 restaurants and 2 bars. | 2 restaurants and 2 bars planned. | |||

| OPERATIONAL STATISTICS | Multi-floor facility. | Multi-floor facility. | Single floor facility. | |||

| Average weekly guests: Approximately 2,500 since September 2019 to present. | Average weekly guests: Approximately 2,500 since August 2020 to present. | N/A at this time. |

*Planned operations

Current Facilities

Currently, the company operates two facilities. The Tulsa Facility and the Lubbock Facility and has recently entered into a lease for a third facility, the Baton Rouge Facility. The company anticipates the Baton Rouge Facility will be operational in Q2 2022.

The Tulsa Facility: Overview

The Tulsa Facility is located at 600 Riverwalk Terrace in the City of Jenks, County of Tulsa, Oklahoma. The company believes the following to be the most appealing characteristics of the Tulsa Facility:

| ● | It is a mid-size venue consisting of approximately 53,102 rentable square feet and a driving range. | |

| ● | It is an entertainment facility, show casing live entertainment, gamified golf and various games such as pinball, pool and corn hole. It is also prides itself on its local chef inspired menus, craft cocktails and full-service restaurants. |

| ● | It is located in a metropolitan area with a mid-size population. |

| ● | Multiple university communities are a short distance away (less than ten miles). |

| ● | There is an established millennial population within the area which fosters a trade market. |

| ● | It is less than one mile to major highways, interstate access other large entertainment facilities, restaurant, and recreational attractions. |

- 2 -

During 2019, the company began re-branding and upgrading the facility. To date, the company has invested approximately $1,000,000 into the Tulsa Facility. The company believes that an additional $150,000 will be needed to complete the rebranding and necessary upgrades of the facility.

The Tulsa Facility: Lease Agreement

| ● | The term of the Tulsa Facility lease agreement is 25 years. |

| ● | Annual base lease payments are $360,000, adjustable throughout the terms of the lease. |

| ● | GolfSuites Tulsa is entitled to 50% of the net cash flow. The remaining 50% of the net cash flow is due and payable to Onefire Holding Company. |

- 3 -

- 4 -

The Lubbock Facility: Overview

The Lubbock Facility is located at 6909 Marsha Sharp Fwy, Lubbock, Texas 79407. The company believes the most appealing characteristics of the Lubbock Facility to be:

| ● | It is a mid-size venue with a driving range. |

| ● | It is an entertainment facility, show casing live entertainment, gamified golf and various games such as pinball, pool and corn hole. It is also prides itself on its local chef inspired menus, craft cocktails and full-service restaurants. |

| ● | It is located in a metropolitan area with a mid-size population. |

| ● | Multiple university communities are a short distance away (less than ten miles). |

| ● | There is an established millennial population within the area which fosters a trade market. |

| ● | It is less than one mile to major highways, interstate access other large entertainment facilities, restaurant and recreational attractions. |

The Lubbock Facility currently operates under the 4ORE! Golf brand, however, it is owned and operated by GolfSuites. The company plans to begin re-branding in the second half of 2022. The company believes the re-branding and necessary upgrades will cost approximately $350,000.

The Lubbock Facility: Lease Agreement

| ● | The lease agreement related to the land on which the facility is on is for a term of 20 years, terminating October 31, 2038. The beginning monthly rent is $13,000 annually and increases by 2% every year thereafter. The lease includes twenty 5 year options for renewal. |

| ● | In addition, the company maintains a nuisance (ingress/egress) lease. This lease was agreed to with the owner of the adjacent property because golf balls were going over the net surrounding the driving range and landing on the adjacent property. The lease expires on August 29, 2023. The company does not have plans to renew this lease. |

The Baton Rouge Facility: Overview

The Baton Rouge Facility, located at 8181 Siegen Lane, Baton Rouge, Louisiana. The company believes the most appealing characteristics of the Baton Rouge Facility to be:

| ● | It is a mid-size venue consisting of approximately 40 bays and a driving range. | |

| ● | It is an entertainment facility, show casing live entertainment, gamified golf and various games such as pinball, pool and corn hole. It is also prides itself on its local chef inspired menus, craft cocktails and full-service restaurants. |

| ● | It is located in a metropolitan area with a mid-size population. |

| ● | Multiple university communities are a short distance away (less than ten miles). |

| ● | There is an established millennial population within the area which fosters a trade market. |

| ● | It is less than one mile to major highways, interstate access other large entertainment facilities, restaurant and recreational attractions. |

The company believes the re-branding and upgrading of the facility will be complete by then end of Q2 2022.

The Baton Rouge Facility: Lease Agreement

| ● | The term of the Baton Rouge Facility lease agreement is 5 years, however the company has the option to extend the lease for 2 periods of 5 years. |

| ● | Annual base lease payments range from $15,000, for the first year, $39,600 for the second year and $60,000 for years 3-5. |

- 5 -

Future Facilities

Over the next year the company intends to: (i) continue to source existing facilities, and (ii) purchase land for future facilities where such opportunities exist.

The company is currently sourcing future facilities that will likely have the following characteristics:

| ● | Mid-size venue consisting of approximately 40 bays and a driving range. | |

| ● | It is an entertainment facility, show casing live entertainment, gamified golf and various games such as pinball, pool and corn hole. It is also prides itself on its local chef inspired menus, craft cocktails and full-service restaurants. |

| ● | It is located in a metropolitan area with a mid-size population. |

| ● | Multiple university communities are a short distance away (less than ten miles). |

| ● | There is an established millennial population within the area which fosters a trade market. |

| ● | It is less than one mile to major highways, interstate access other large entertainment facilities, restaurant and recreational attractions. |

Sourcing Facilities

When contemplating leasing already existing facilities, purchasing existing facilities, or building a facility from the ground up the company looks as the following factors to determine whether the project is suited for the company:

| ● | Location and size of each future facility. |

| ● | Large and mid-size populations within metropolitan areas. |

| ● | University communities with populations of at least 100,000. | |

| ● | Local millennial populations. | |

| ● | The proximity to major highway, interstate access other large entertainment facilities, restaurant, and recreational attractions. | |

| ● | Ongoing growth trends in the selected area. | |

| ● | Proximity of select population bases including: university students, types of housing developments and employment rates. | |

| ● | Whether a local government is cooperative and favors the development of leisure facilities. | |

| ● | Cost of land. | |

| ● | Availability and potential threat of competitor facilities within the vicinity. | |

| ● | Favorable mortgage/lender terms and relationships. |

Financing Facilities

The company intends to lease and/or purchase already existing facilities with a combination of the following:

| ● | The proceeds of the Regulation A offering. | |

| ● | Funds advanced to GolfSuites by the Parent Company. | |

| ● | Mortgage financing provided by banks, private equity funds, lending-REITs and/or other financial institutions. |

- 6 -

The company intends to purchase land to begin the construction of facilities with a combination of the following:

| ● | The proceeds of the Regulation A offering. | |

| ● | Funds advanced to GolfSuites by the Parent Company. | |

| ● | Mortgage financing provided by banks, private equity funds, lending-REITs and/or other financial institutions. |

Management of the Facilities

The Parent Company oversees the management of all of the company’s locations and will oversee the management of all future locations. We intend that all the facilities will operate similar to the Tulsa and Lubbock facilities, where the company and/or its subsidiaries employ management teams and staff to operate each facility whether it is leased facility, owned facility, or built from the ground up.

Market Sector

The company participates in the recreational sporting and entertainment facilities market. The company believes this market to be young, fast-growing and under-served. This market overlaps three growing, highly profitable markets: the golf market, the recreation/sporting entertainment sector and the food and beverage portion of the hospitality industry. The company competes for revenues from customer spending in each of these three sectors.

Target Audience

The company has five primary target audiences:

| ● | Families looking for a fun experience for their kids and friends. |

| ● | Experience Seekers, Millennials, Gen-Xers, Boomers seeking unique, fun night/weekend entertainment. |

| ● | Recreational and avid golfers. |

| ● | Businesses wanting team building, business gatherings, incentive rewards and corporate event venues with food and entertainment. |

| ● | Get together/Fundraiser planners looking for unique locations for parties, celebrations and fund-raising events. |

Management Services from GolfSuites

GolfSuites entered into a management services agreement with the Parent Company effective as of August 12, 2019 (the “Management Services Agreement”). Under that agreement, The Parent Company will manage the company and allow the company to use certain intellectual property and business concepts. The company will incur direct capitalized costs and overhead expenses.

Some direct capitalized costs and overhead expenses will be paid by the company directly (e.g., salaries, board of director and board of advisor fees, employee benefits, and general administrative costs) while other capitalized costs and overhead expenses will be paid by the Parent Company and then reimbursed by the company (e.g., architectural costs, engineering, land, zoning and permitting and other costs directly related to assets belonging to the company).

- 7 -

In addition, the company will pay the Parent Company monthly management fees as follows:

| ● | Operating facilities: 4% of gross operating revenues once facilities are opened. |

| o | Parent Company shall calculate 4% of gross revenue amount of the immediate past month, and the Parent Company shall invoice the company for the specific management fee amount on a monthly basis. |

| ● | Facilities that are not operational: 3% of all-in development costs. |

| o | The “in-development costs” shall be calculated as the total amount of the hard and soft development costs, which include, but are not limited to, the total costs of land, development and entitlement costs, all construction costs, engineering and design costs, and contractor fees (the “In-Development Costs”) paid by the company in the immediate past month. The Parent Company shall invoice the company for the specific management fee amount on a monthly basis. |

The Tulsa Facility and the Lubbock Facility are considered operating facilities.

The initial term of the Management Services Agreement is for ten years. Upon expiration of the agreement, it will automatically renew for another two years. Either party can terminate the agreement provided 120 days written notice has been given to the other party. The Management Services Agreement may also be terminated upon certain events of default, including but not limited to, material breaches of the agreement and also if one party files for bankruptcy or otherwise liquidates.

In the event the Parent Company were to file for bankruptcy or otherwise liquidate, the company would have to seek another provider of management services or make arrangements for such services to be provided in-house, including the hiring of additional personnel.

This agreement amended and replaced the agreement dated April 15, 2019. The company had previously accrued costs under that agreement.

For additional information please see the Management Services Agreement, which is an Exhibit to this Form 1-K.

Competition

Direct competitors

The company’s largest competitor in this emerging market is TopGolf. As of December 2021, there are 67 TopGolf locations in the United States. Its first facilities were developed less than 20 years ago, and according to public reporting TopGolf intends to add new venues annually. Other competitors include local and regional facilities as well as other national chains, including DriveShack, 1Up Golf, Big Shots, and Driv.

Indirect competitors

Indirect competitors include sports-themed entertainment facilities with food and beverage offerings that revolve around other sports including, but not limited to bowling, ping pong, baseball, NASCAR, etc. These include PINS Mechanical, Main Event (40+ locations), Lucky Strike, Bowl More, iDrive NASCAR, iFly, and Dave & Buster’s (139 locations as of December 2020), to name a few.

In addition, new entertainment themed centers are being developed within the US that merge retail, food and beverage, entertainment and hospitality into single, tightly packed mixed-use destinations of 1-3 million square feet. These new developments include American Dream (Miami) and American Dream (NYC), as well as numerous other smaller developments throughout the US. Facilities like these typically include entertainment amenities such as water parks, skydiving, surfing, ice-rinks, drive-in movie theatres, hybrid golf facilities, miniature golf, theme parks, observation wheels, climbing walls, X4D movie theatres, and aquariums.

- 8 -

Employees

The company does not have any full-time or part-time employees. The Tulsa Facility and the Lubbock Facility currently employ approximately 250 employees in the following roles: restaurant service, marketing, management, facilities management, event sales, golf instruction and retail.

In addition, the Parent Company employs eight individuals, all of whom spend up to half of their time working on matters related to the company and various related entities. The amount of time that an employee of the Parent Company will dedicate to GolfSuites will vary from week to week depending on the current needs of the company.

Regulation

Currently, the company has obtained a state liquor license in Oklahoma for the Tulsa Facility and a state liquor license in Texas for the Lubbock Facility. The company has not yet obtained a liquor license for the Baton Rogue Facility. In addition to the liquor licenses, certain other licenses that may be required for the company’s planned operations include:

| ● | State liquor license. | |

| ● | State reuse/resale tax for products including but not limited to golf clubs, and apparel. | |

| ● | County resale tax certificate. | |

| ● | “Doing Business As” certificates for applicable states. | |

| ● | Health department and food service license for each facility. | |

| ● | Elevator and Fire department certifications, required annually. |

Intellectual Property

The Parent Company has filed the following name trademarks and GolfSuites intends to enter into a license agreement with the Parent Company for use of the following trademarks:

| ● | GolfSuites | |

| ● | Off The Deck | |

| ● | FirstCut |

Litigation

The company has no litigation pending and the management team is not aware of any pending or threatened legal action relating to the company business, intellectual property, conduct or other business issues.

THE COMPANY’S PROPERTY

| ● | Tulsa Facility: o The company has entered into two lease agreements at the Tulsa Facility located at 600 Riverwalk Terrace Jenks, Oklahoma. One lease agreement relates to the facility. The second lease agreement relates to the land that the facility is on. |

| ● | Baton Rouge Facility: o The company has entered into one lease agreement for the property located at 8181 Siegen Lane, Baton Rouge, Louisiana. |

| ● | Lubbock Facility: o The company owns the facility located 6909 Marsha Sharp Fwy, Lubbock, Texas. The company leases the property at 6909 Marsha Sharp Fwy, Lubbock, Texas. |

- 9 -

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

You should read the following discussion and analysis of our financial condition and results of our operations together with our consolidated financial statements and related notes appearing at the end of this Annual Report. This discussion contains forward-looking statements reflecting our current expectations that involve risks and uncertainties. Actual results and the timing of events may differ materially from those contained in these forward-looking statements due to a number of factors, including those discussed elsewhere in this Annual Report.

Overview

GolfSuites 1, Inc. owns, leases and operates golf driving range entertainment centers in the United States. The entertainment centers aim to provide next generation hospitality and dining venues, high tech gamified golf in climate-controlled suites, live entertainment, and spaces for both social and corporate functions.

As of December 31, 2021, the company owns 100% of GolfSuites Tulsa, LLC and 100% of GolfSuites Lubbock, LLC. The Tulsa Facility was formerly operated under the FlyingTee brand, but now operates under the GolfSuites brand. The Lubbock Facility was formerly operated under the 4ORE! Golf brand, but now operates under 4ORE! Golf-Powered By GolfSuites brand, and will change to usage of the GolfSuites brand later in 2022. The company began recording revenues for the Lubbock Facility in August 2020. The financial statements include the operations of GolfSuites Tulsa for 2020 and 2021 and GolfSuites Lubbock since the acquisition date of mid-August 2020; however, minority interest in the loss related to GolfSuites Lubbock, LLC has been reflected in the financial statements of the company due to GolfSuites Lubbock’s partial ownership of the Lubbock facility from mid-August through mid-November 2020, when it took over 100% ownership.

On March 16, 2021, GS 1 formed GolfSuites Baton Rouge, LLC (“Baton Rouge”), a Louisiana limited liability company for the purpose of leasing an approximate 18-acre existing driving range that had been closed for operations. This site will be developed at an estimated total cost of $1,500,000. Upon completion it will operate as a 40-bay facility offering the same services as Tulsa and Lubbock. The expected completion of development and opening of Baton Rouge is the end of Q2 2022. Funding for this site is being provided by GS 1’s Regulation A share sales, private equity investment, advances from the Parent Company, and positive operating cash flows from existing operations. Minority interest in the loss of Baton Rouge has been reflected in the attached statements due to the allocation of the entire 2021 loss to the private equity investor. As of December 31, 2021, the private equity investor has invested $400,000 of his total commitment of $600,000.

To date, revenues have come from the following activities:

| ● | Suite rentals. |

| ● | Food and beverage sales. |

| ● | Coaching and instruction services. |

| ● | Individual and corporate membership sales. |

| ● | Retail sales. |

The company collects revenue upon sale of an item (including: membership sales, food and beverage sales, apparel etc.) and recognizes the revenue when the sale is made.

Operating expenses currently consist of advertising and marketing expenses and general administrative expenses.

- 10 -

Results of Operations

Year ended December 31, 2021 compared to the year ended December 31, 2020

For the year ended December 31, 2021, (“Fiscal 2021”) the company had $8,853,965 in revenues compared to the year ended December 31, 2020 (“Fiscal 2020”) the company had $4,547,636 a $4,306,329 increase (or 95%) increase. The increase in revenues is attributable to:

| · | a full year ownership of the both Lubbock and Tulsa Facilities; |

| · | the change in restrictions related to capacity constraints and public large-crowd-gatherings which were largely in place throughout 2020 but did not expire until March 2021, which led to an increase in group and corporate sales; and |

| · | an expanded offering of food and beverages. |

The company’s cost of revenues increased by $435,937 (or 54%) to $1,246,701 in Fiscal 2021 from $810,764 in Fiscal 2020 primarily due to the acquisition of the Lubbock Facility. Our gross profits increased to $7,607,264 from $3,736,872 for Fiscal 2021 and Fiscal 2020, respectively, by $3,870,392 (or 104%). Our gross margins increased to 86% from 82%, driven by increased efficiencies in purchasing food and beverages and improved sales performance incentives for employees.

Total operating expenses for the year ended December 31, 2021 increased to $6,427,854 from $3,778,474 for the year ended December 31, 2020, an increase of 2,649,380 (70%). The acquisition of the Lubbock Facility accounted for approximately $1,817,000 of the Fiscal 2021 operating expenses.

The primary drivers of the increase were:

| · | An increase of $1,157,707 in employee related costs (including salaries, employees and taxes) due to related to the labor costs associated with the Lubbock acquisition; and |

| · | An increase of $297,687 in equipment and repairs and gaming and software costs due to the additional expenses from the Lubbock acquisition. This expense is largely comprised of net repairs and gaming software licenses. |

Income from Covid 19 relief programs amounted to $1,404,856 for Fiscal 2021 compared to $893,400 for Fiscal 2020. The Covid 19 relief programs included: (i) PPP loan forgiveness in the amount of $1,073,100 for Fiscal 2021 compared to $893,400 for Fiscal 2020 and an (ii) Employee retention credit in the amount of $331,756 for Fiscal 2021. The employee retention credit was not available in Fiscal 2020.

Other income (expense) includes depreciation and amortization, interest expense, management fees to Parent Company, Regulation A share sale costs, and other income. Notably, depreciation and amortization increased $798,403 to $1,104,196 for Fiscal 2021 compared to $395,793 for Fiscal 2020. Interest expenses increased $383,445 to $644,222 for Fiscal 2021 compared to $260,777 for Fiscal 2020. For the first time, the company paid a management fee to the Parent Company in the amount of $667,036 for Fiscal 2021. Regulation A share sale costs increased $69,804 from $915,938 for Fiscal 2020 compared to $$985,742 for Fiscal 2021.

As a result of the foregoing, the company generated a net loss for Fiscal 2021 in the amount of $697,690 compared to a net loss for Fiscal 2020 in the amount of $684,513.

Liquidity and Capital Resources

The following table summarizes, for the periods indicated, selected items in our condensed Statements of Cash Flows:

| Year ended December 31, | ||||||||||||

| 2021 | 2020 | $ Change | ||||||||||

| Net cash (used in) provided by operating activities | $ | 382,166 | $ | 531,770 | $ | (149,604 | ) | |||||

| Net cash (used in) provided by investing activities | $ | (2,215,996 | ) | $ | (1,552,832 | ) | $ | (663,164 | ) | |||

| Net cash provided by financing activities | $ | 1,969,455 | $ | 1,526,715 | $ | 442,740 | ||||||

- 11 -

Cash provided by operating activities for the year ended December 31, 2021 was $382,166 as compared to cash provided by $531,770 in 2020. The decrease in cash provided by operating activities in 2021 was primarily due to the company having used $853,543 more in account receivable and accounts payable and accrued expenses in 2021 as compared to 2020 as 2021 reflected the employee retention credit, which was paid in 2022, and cash used to pay down prior expenses. However, the company also was provided $708,403 in 2021 related to depreciation in amortization costs due to the acquisition of the Lubbock Facility.

Cash used in investing activities for the year ended December 31, 2021 was $2,215,996, as compared to cash used by investing activities of $1,552,832 in 2020. In 2021, the company used $1,549,782 for the purchase of property and equipment related to ongoing costs for the Tulsa and Lubbock Facilities and $666,214 for capitalized development costs primarily related to the Baton Rouge Facility, while in 2020 the company used $1,550,517 for the acquisition of operating golf entities primarily related to the acquisition of Lubbock Facility.

Cash provided by financing activities was $1,969,455 for the year ended December 31, 2021, as compared to $1,526,715 in 2020. During 2021, we received $2,126,084 from the sale of Preferred Stock of $2,126,084 and $400,000 from the sale of the minority interest in the Baton Rouge Facility, while in 2020 we received $923,239 from the sale of Preferred Stock and $331,000 from proceeds from notes payable. Our shareholder and related party advances, net was $271,619 in 2021 compared with $1,278,694 in 2020. For proceeds net of principal payments on mortgages, equipment loans and leases, the company was provided $142,462 in 2021, which included the lease for the Baton Rouge Facility, compared with using $163,739 in 2020.

As of December 31, 2021, the company has cash and cash equivalents of $674,144. Since inception, our activities have been funded from our revenues, cash advances from its current parent entity and management as well as funds raised in the company’s offerings under Regulation A.

.

Since taking over the operations for the Lubbock Facility and the Tulsa Facility, the company has also been relying on revenues from those facilities and anticipates receiving revenues from the Baton Rouge Facility once it is operational. The company plans to continue to try to raise additional capital through: (i) additional offerings (ii) mortgage financing and (iii) revenues from the Tulsa Facility and the Lubbock Facility. Absent additional capital, the company may be forced to significantly reduce expenses and could become insolvent.

The company launched a Regulation A offering in May 2019, which terminated in May 2020. The total amount raised in the offering was approximately $1,334,218. The company has since launched a second Regulation A offering in February 2021 which terminated in March 2022. The total amount raised in the offering was approximately, $3,391,706.

Indebtedness

Advances from the Parent Company and its Shareholders

| ● | The company has received working capital to cover expenses and costs while preparing for the securities offering from the Parent Company. The balance of those advances at December 31, 2021 and December 31, 2020 was $2,143,058 and $1,691,239. The company has formalized some of these borrowings but expects to repay all of these amounts whether a formal promissory note exists of note. The agreements are between related parties. Therefore, there is no guarantee that the rates or terms are commensurate with arm’s-length arrangements. |

| ● | The company received advances from four shareholders of the Parent Company. The balance of these parent entity shareholder advances totaled $933,317 and 1,113,517 as of December 31, 2021 and December 31, 2020 respectively. These balances are recorded as liabilities of the company. These notes payable relate to the Lubbock Facility mortgage financing bear annual accruing interest rate of 12%. The notes were 90 day notes and the Company and the shareholders have yet to formalize the extension of the notes. The agreements are between related parties. Therefore, there is no guarantee that the rates or terms are commensurate with arm’s-length arrangements. These balances are recorded as liabilities of the company. |

- 12 -

Lease Obligations

| ● | Lubbock Facility |

| o | The company took over a construction loan with First United Bank, with an interest rate of 4% and a lease ended date of October 31, 2038. As of December 31, 2021, the company recorded $6,748,912 in liabilities for this mortgage; the mortgage was secured by a third party guarantor. |

| o | The company took over the Amended and Restated Ground Lease, executed on October 30, 2018, for a 20 year term. The beginning monthly rent is $13,000 annually and increases by 2% every year thereafter. The lease includes twenty 5 year options for renewal. |

| o | The company took over a lease with Hub City Main Street Investments, LLC. The lease provides for a 5 year term with monthly payments of $2,500. This lease is often referred to as a nuisance lease is with the owner of the adjacent property owner because golf balls were going over the net surrounding the driving range and landing on the adjacent property. The lease expires on August 29, 2023. |

| ● | Tulsa Facility |

| o | GolfSuites Tulsa is a party to a 25-year lease agreement, dated September 13, 2019, and entered into between GolfSuites Tulsa and Onefire Holding Company, LLC (“Onefire”) (the “Tulsa Lease Agreement”). Onefire is entitled to annual payments of $360,000 and 50% of net cash flow. The Tulsa Lease is included as an Exhibit to this Form 1-K. |

| o | On March 5, 2020 GolfSuites Tulsa entered into a Lease Amendment Agreement with Onefire. This agreement provides for the deferment of base rent and additional rent for the period from January 1, 2020, through March 31, 2020. The Lease Amendment Agreement is filed as an Exhibit to this Form 1-K. |

| o | On July 6, 2020, the company took out a loan for equipment financing with First Oklahoma Bank in the amount of $198,580. The loan bears an interest rate of 5.25% and expires on July 6, 2025. As of December 31, 2021, the outstanding principal and accrued interested on the loan was $147,580. |

| ● | Baton Rouge Facility |

| o | On February 9, 2021, the company entered into a lease agreement for an approximate 18-acre existing driving range located at 8181 Siegen Lane, Baton Rouge, Louisiana (the “Baton Rouge Facility”) and has a term of five years. The lease commenced on March 1, 2021. |

| ● | Unsecured Note Payable |

| o | The company also has $131,000 in an unsecured note payable. This is recorded as a current liability. |

| ● | Paycheck Protection Program |

| o | GolfSuites Tulsa and the GolfSuites Lubbock obtained Paycheck Protection Program (“PPP”) loans pursuant to two rounds of government loan funding. The first PPP loans were funded in 2020 and forgiven in Q1 2021, prior to the issuance of the 2020 consolidated financial statements. Therefore, forgiveness of these loans was reflected in the consolidated financial statements for 2020. |

| o | The second of the PPP loans were funded in Q1 2021. The company received official notice of forgiveness of these loans in the summer of 2021, forgiveness of these loans is reflected in the 2021 consolidated financial statements. GolfSuites Tulsa received $665,000 under this second PPP loan. The lender is First Oklahoma Bank. GolfSuites Lubbock received $408,100 under this second PPP. |

- 13 -

Trends

GolfSuites participates in the recreational sporting and entertainment facilities market. It believes this market to be young, fast-growing and under-served. This market overlaps three growing, highly profitable markets: the golf market, the recreation/sporting entertainment sector and the food and beverage portion of the hospitality industry. GolfSuites competes for revenues from customer spending in each of these three sectors. Since money spent in those sectors is discretionary income, the company believes it is reliant on economic trends in the United States.

COVID-19 pandemic has had an impact on the company’s plans and the operation of its facilities. For instance, while social distancing is still required, the Tulsa Facility and the Lubbock Facility have to limit the number of potential customers and limit their ability to function at capacity. However, due to the open air nature of our facilities, the limitations have been less restrictive than other sporting and entertainment facilities. To date, there have been limited restrictions on construction, so the company has been able to continue the rebranding of the Tulsa Facility and plan for the rebranding of the Lubbock Facility. In addition, the opening of the Baton Rouge Facility has been delayed due to the COVID-19 pandemic, we anticipate opening the facility in Q2 2022.

Since December 31, 2021:

| ● | Upon termination of the Regulation A Offering in February 2022, GolfSuites 1 sold a total of $3,391,706 of Preferred Stock, pursuant to the Regulation A offering. |

| ● | On August 16, 2021 GolfSuites Baton Rouge, the company and Shelchar Challa (the “Purchaser”) entered into an Membership Interest Purchase Agreement (the “MIP Agreement”). Pursuant to this MIP Agreement, the Purchaser intends to contribute $600,000 as an initial capital contribution. As of February 28, 2022, GolfSuites Baton Rouge has received the full $600,000. Under this agreement, the Purchaser will share in the profits of the Baton Rouge Facility. |

- 14 -

Item 3. Directors and Officers

Directors, Executive Officers and Significant Employees

The table below sets forth the officers and directors of the company.

| Name | Position | Employer | Age | Term of Office (If indefinite give date of appointment) | ||||||||

| Gerald Ellenburg | CEO, Director, Secretary, Treasurer | GolfSuites 1, Inc. | 72 | March 14, 2019 | ||||||||

The table below sets forth the officers and directors of the Parent Company.

| Name | Position | Employer | Age | Term of Office (If indefinite give date of appointment) | ||||||

| Gerald Ellenburg | Director Chairman Chief Executive Officer and Secretary | GolfSuites, Inc. | 72 | November 8, 2018 | ||||||

| Nicholas Flanagan | President, Chief Operating Officer | GolfSuites, Inc. | 56 | July 1, 2019 | ||||||

| Scott McCurry | VP Operations | GolfSuites, Inc. | 54 | |||||||

| David A. Morris III | Consulting CFO | GolfSuites, Inc. | 63 | November 8, 2018 | ||||||

| Michael Zylstra | VP, Chief Administrative Officer | GolfSuites, Inc. | 56 | July 1, 2019 | ||||||

| Ann England | VP, Human Resources | GolfSuites, Inc. | 51 | October 15, 2021 | ||||||

Gerald Ellenburg

Gerald Ellenburg (“Jerry”) is the Chairman and Chief Executive Officer of the Parent Company since November 2018 and GolfSuites since March 2019. Jerry also serves as the Chairman and Chief Executive Officer of ERC Communities, Inc., since March 2011. Jerry has a total of 35 years of experience in real estate ownership, management and financing of multi-family properties, management of over $750 million in debt and equity financing. Jerry graduated from the University of California, Berkeley in 1971, and is a California-licensed CPA (inactive).

Nicholas Flanagan

Nick Flanagan is the Chief Operating Officer of the Parent Company since July 1, 2019. Nick is a 30 year veteran of major restaurant and retail branded companies. From 1989 to 2004 he served in various roles with Steak & Ale Restaurant Corp. From 2004 to June 2019 Nick served in various roles at Cracker Barrel Old Country Store, Inc. (“Cracker Barrel”). Nick’s most recent role at Cracker Barrel was Senior Vice President of Restaurant & Retail Operations. While in this role, he served on the company’s executive team. Nick graduated from the University of Central Florida in 1989 with a Bachelor of Business Administration degree.

- 15 -

Scott McCurry

Scott McCurry has been the Vice President of Operations for the company since September 1, 2019. Scott is an operations executive with over 25 years of experience in the Hospitality and Entertainment Industry. Previously, Scott was the National Director of Operations for K1 Speed from September 2017 to September 2019, helping it grow in domestic and international size while adding food beverage to the brand while improving the guest experience. Prior to K1Speed, Scott was the National Director of Operations of Topgolf from February 2014 to September 2017. Prior to that Scott was their Director of Operations, a position he held since July 2012. At Topgolf, Scott helped build the brand from six venues to over 40 venues each averaging $20 million in revenue a year.

Ann England

Ann England is Vice-President of Human Resources, Organizational Development, and Employee Training since October 2021. Ann joins the Parent Company with over 30 years in the foodservice industry, including nearly 20 years in Human Resources, Organizational Development and Employee Training. From 1992 to October 2021, she served at Cracker Barrell in various roles, including Manager of Internal Communications and Guest Relations for 6 years and Director of Operational Strategy for the last 3 years there. In addition to her HR experience, Ann has led internal corporate communications, guest relations, strategic projects, and operational strategy. She is a graduate of Middle Tennessee State University.

David A. Morris III

David Morris is the Consulting Chief Financial Officer of the Parent Company since November 2018. David is also the Consulting Chief Financial Officer at ERC Communities, Inc., since March 2011 until present. David has over 30 years of experience in finance and financial forensics. During his tenure at GolfSuites, David oversees the following:

| ● | tax planning, | |

| ● | compliance, | |

| ● | accounting, | |

| ● | audit, | |

| ● | forecasts and | |

| ● | investment analysis. |

David’s’ career has included the Vice-Presidency of Finance at Belz Enterprises, a large real estate development and management company. David graduated from the University of Wisconsin, La Crosse, in 1980 and is a Tennessee-licensed CPA.

Michael Zylstra

Michael Zylstra is the Chief Administrative Officer of the Parent Company since July 1, 2019. From 1992 until 2017 Michael has worked extensively in the restaurant and retail industry with Cracker Barrel. In his most recent role at Cracker Barrel Michael served as VP, General Counsel & Corporate Secretary. Michael graduated from the University of Western Ontario in 1988 and from Cumberland School of Law at Samford University in 1991.

Compensation of Directors and Executive Officers

For the fiscal year ended December 31, 2021, the company did not pay its sole director in his capacity as director or its sole officer, in his capacity as CEO, secretary or treasurer.

In the future, the company will have to pay additional officers, directors and other employees, which will impact the company’s financial condition and results of operations, as discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The company may choose to establish an equity compensation plan for its management and other employees in the future. Further, as the company grows, the company intends to add other executives, including but not limited to, a General Manager, a Food and Beverage Manager and a Golf Manager.

- 16 -

Item 4. Security Ownership of Management and Certain Securityholders

The following table sets out, as of April 14, 2022, GolfSuites voting securities that are owned by its executive officers, directors and other persons holding more than 10% of the company’s voting securities.

| Title of class | Name and address of beneficial owner | Amount and nature of beneficial ownership | Amount and nature of beneficial ownership acquirable | Percent of class | ||||||||

| Class B Common Stock | GolfSuites, Inc. 2738 Falkenburg Road South, Riverview, FL 33578 | 18,000,000 | N/A | 100 | % | |||||||

There are currently no outstanding shares of the company’s Class A Common Stock and 687,489 shares outstanding of the company’s Preferred Stock.

The following table sets out, as of April 14, 2022 the Parent Company’s voting securities that are owned by the company’s executive officers, directors and other persons holding more than 10% of the company’s voting securities.

| Title of class | Name and address of beneficial owner | Amount and nature of beneficial ownership | Amount and nature of beneficial ownership acquirable | Percent of class | ||||||||

| Common Stock | Gerald Ellenburg | 215,000,000 | N/A | 22.83 | % | |||||||

| Nicholas Flanagan | 191,000,000 | N/A | 20.28 | % | ||||||||

| Michael & Gina Zylstra | 119,375,000 | N/A | 12.68 | % | ||||||||

| Michael J. Reiner & Associations, LP | 95,500,000 | N/A | 10.14 | % | ||||||||

| (1) | The address for all the executive officers, directors, and beneficial owners is c/o GolfSuites, Inc. 2738 Falkenburg Road South, Riverview, FL 33578. |

Item 5. Interest of Management and Others in Certain Transactions

Relationship with the Parent Company

The company has received working capital to cover expenses and costs while preparing for the securities offering from the Parent Company. The balance of those advances at December 31, 2021 and December 31, 2020 was $2,143,058 and $1,691,239. The company has formalized some of these borrowings but expects to repay all of these amounts whether a formal promissory note exists of note. The agreements are between related parties. Therefore, there is no guarantee that the rates or terms are commensurate with arm’s-length arrangements.

- 17 -

In addition, the company has received advances from shareholders of the Parent Company. The balance of these Parent Company shareholder advances at December 31, 2021 and December 31, 2020 was $933,317 and 1,113,517. The company has formalized some of these borrowings but expects to repay all of these amounts whether a formal promissory note exists of note. The agreements are between related parties. Therefore, there is no guarantee that the rates or terms are commensurate with arm’s-length arrangements.

The company has issued 18,000,000 shares of Class B Common Stock to the Parent Company, at par, in exchange for $180.

Management Services Agreement

The company has entered into a Management Services Agreement with the Parent Company. Pursuant to this agreement, the Parent Company will license all intellectual property and business concepts and design necessary for GolfSuites to conduct its business and under the direction of our Board of Directors, the Parent Company is to provide services to GolfSuites including: Supervision the operations of GolfSuites, and Management all necessary negotiations relating to the business, personnel, etc. In return for the aforementioned services GolfSuites agrees to pay the Parent Company a monthly management fee:

| ● | Operational facilities: 4% of gross operating revenues | |

| ● | Facilities that are not operational: 3% of all In-Development Costs |

The initial term of the agreement is for ten years. Upon expiration of the agreement it shall automatically renew for another two years. Either party can terminate the agreement provided 120 days written notice has been given to the other party. see “Item 1. Business – Management Services from GolfSuites.”

Relationship with ERC Communities, Inc.

Some of the parties involved with the operation and management of the company, including Gerald Ellenburg, and David Morris, have other relationships that may create disincentives to act in the best interest of the company and its investors. These parties are also involved with ERC Communities, Inc. and its subsidiaries in similar capacities. These conflicts may inhibit or interfere with the sound and profitable operation of the company.

Item 6. Other Information

None.

- 18 -

GolfSuites 1, Inc.

and Subsidiaries

Consolidated Financial Statements

As of, and for the Years Ended December 31, 2021 and 2020

F-1

INDEPENDENT AUDITOR’S REPORT

April 1, 2022

To: Board of Directors, GolfSuites 1, Inc.

Re: 2021 Consolidated Financial Statement audit

We have audited the accompanying consolidated financial statements of GolfSuites 1, Inc. and subsidiaries (the “Company”), which comprise the balance sheet as of December 31, 2021 and 2020, and the related statements of loss and comprehensive loss, changes in shareholders’ equity, and cash flows for the calendar year periods ended 2021 and 2020, and the related notes to such consolidated financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit of the Company’s financial statements in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion.

An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of the Company as of December 31, 2021 and 2020, and the results of its operations, shareholder equity and its cash flows for the calendar years thus ended in accordance with accounting principles generally accepted in the United States of America.

Going Concern

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in the notes to the financial statements, the Company has stated that substantial doubt exists about the Company's ability to continue as a going concern. Management's evaluation of the events and conditions and management's plans regarding these matters are also described in the Notes to the financial statements. The financial statements do not include any adjustments that might result from the outcome of this uncertainty. Our opinion is not modified with respect to this matter.

Sincerely,

IndigoSpire CPA Group

IndigoSpire CPA Group, LLC Aurora, Colorado

April 1, 2022

F-2

GolfSuites 1, Inc.

and Subsidiaries

Consolidated Financial Statements

As of, and for the Years Ended December 31, 2021 and 2020

Table of Contents

F-3

GolfSuites 1, Inc. and Subsidiaries

Consolidated Balance Sheets

As of December 31, 2021 and 2020

See accompanying Independent Auditor's report

| 2021 | 2020 | |||||||

| ASSETS | ||||||||

| Current assets | ||||||||

| Cash and cash equivalents | $ | 674,144 | $ | 538,519 | ||||

| Accounts receivable | 386,581 | 64,434 | ||||||

| Inventory | 105,856 | 88,286 | ||||||

| Prepaid expenses | 24,223 | 1,713 | ||||||

| Total current assets | 1,190,804 | 692,952 | ||||||

| Property, plant and equipment, net | ||||||||

| Land and building improvements | 6,867,239 | 6,867,239 | ||||||

| Furniture, fixtures and equipment | 3,742,864 | 3,524,920 | ||||||

| Construction in progress | 650,241 | - | ||||||

| Accumulated depreciation | (2,630,573 | ) | (1,917,002 | ) | ||||

| Property, plant and equipment, net | 8,629,771 | 8,475,157 | ||||||

| Right of use assets, net of accumulated amortization | 8,896,265 | 8,605,293 | ||||||

| Other assets | ||||||||

| Capitalized development costs | 666,214 | - | ||||||

| Other assets | 44,865 | 43,087 | ||||||

| Goodwill | 1,749,255 | 1,749,255 | ||||||

| Total other assets | 2,460,334 | 1,792,342 | ||||||

| TOTAL ASSETS | $ | 21,177,174 | $ | 19,565,744 | ||||

| LIABILITIES AND EQUITY | ||||||||

| Liabilities | ||||||||

| Current liabilities | ||||||||

| Notes payable, current portion | $ | 852,030 | $ | 396,853 | ||||

| Lease liabilities, current portion | 201,506 | 180,113 | ||||||

| Accounts payable and accrued expenses | 754,375 | 1,283,826 | ||||||

| EIDL loans payable | 298,900 | 149,900 | ||||||

| Total current liabilities | 2,106,811 | 2,010,692 | ||||||

| Non-current liabilities | ||||||||

| Notes payable, long-term portion | 6,044,462 | 6,862,858 | ||||||

| Lease liabilities, long-term portion | 8,954,141 | 8,469,853 | ||||||

| Advances from sharholders of Golfsuites, Inc. (parent company) | 933,317 | 1,113,517 | ||||||

| Advances from GolfSuites, Inc. (parent company) | 2,143,058 | 1,691,239 | ||||||

| Total non-current liabilities | 18,074,978 | 18,137,467 | ||||||

| TOTAL LIABILITIES | 20,181,789 | 20,148,159 | ||||||

| MINORITY INTEREST IN CONSOLIDATED SUBSIDIARY | 283,374 | - | ||||||

| Stockholders' equity | ||||||||

| Common stock, Class A: 132,000,000 shares authorized, $0.00001 par, no shares issued and outstanding | - | - | ||||||

| Common stock, Class B: 18,000,000 shares authorized, $0.00001 par, 18,000,000 shares issued and outstanding | 180 | 180 | ||||||

| Preferred stock, Class A: 10,000,000 shares authorized, 540,503 and 274,742 shares issued and outstanding, respectively | 3,430,618 | 1,304,534 | ||||||

| Preferred stock, Other: 40,000,000 shares authorized, no shares issued and outstanding | - | - | ||||||

| Retained earnings | (2,718,787 | ) | (1,887,129 | ) | ||||

| TOTAL EQUITY | 712,011 | (582,415 | ) | |||||

| TOTAL LIABILITIES AND EQUITY | $ | 21,177,174 | $ | 19,565,744 | ||||

The accompanying notes are an integral part of these financial statements.

F-4

GolfSuites 1, Inc. and Subsidiaries

Consolidated Statement of Operations

For the Years Ended December 31, 2021 and 2020

See accompanying Independent Auditor's report

| 2021 | 2020 | |||||||

| Revenues | $ | 8,853,965 | $ | 4,547,636 | ||||

| Cost of revenues | 1,246,701 | 810,764 | ||||||

| Gross profit | 7,607,264 | 3,736,872 | ||||||

| Operating expenses | ||||||||

| Advertising and marketing | 42,078 | 52,674 | ||||||

| Salaries - operational | 3,083,564 | 2,276,931 | ||||||

| Employee benefits and taxes | 576,154 | 225,080 | ||||||

| Property lease and affiliated costs | 90,550 | 56,872 | ||||||

| Equipment and repairs | 177,893 | 78,027 | ||||||

| Gaming, software and license fees | 315,060 | 117,239 | ||||||

| Utilities and telephone | 369,384 | 152,486 | ||||||

| Credit card fees | 240,301 | 65,210 | ||||||

| Insurance | 310,950 | 115,548 | ||||||

| Professional fees | 232,397 | 62,129 | ||||||

| Property and local taxes | 387,946 | 71,853 | ||||||

| Other selling, general and administrative | 601,577 | 504,425 | ||||||

| Total operating expenses | 6,427,854 | 3,778,474 | ||||||

| Net operating profit (loss) | 1,179,410 | (41,602 | ) | |||||

| Income from Covid 19 relief programs | ||||||||

| PPP loan forgiveness | 1,073,100 | 893,400 | ||||||

| Employee retention credit | 331,756 | - | ||||||

| Total Covid 19 relief programs | 1,404,856 | 893,400 | ||||||

| Net income before other income (expense) | 2,584,266 | 851,798 | ||||||

| Other income (expense) | ||||||||

| Depreciation and amortization | (1,104,196 | ) | (395,793 | ) | ||||

| Interest expense | (644,222 | ) | (260,777 | ) | ||||

| Management fees to GolfSuites, Inc. (parent company) | (667,036 | ) | - | |||||

| Reg A share sale costs | (985,742 | ) | (915,938 | ) | ||||

| Other income | 2,613 | 2,418 | ||||||

| Net other expense | (3,398,583 | ) | (1,570,090 | ) | ||||

| Net loss before minority interest | (814,317 | ) | (718,292 | ) | ||||

| Minority interest share of subsidiary loss | 116,627 | 33,779 | ||||||

| Net loss | $ | (697,690 | ) | $ | (684,513 | ) | ||

| Basic loss per common share | $ | (0.03876 | ) | $ | (0.03803 | ) | ||

| Diluted loss per common share | $ | (0.03798 | ) | $ | (0.03766 | ) | ||

The accompanying notes are an integral part of these financial statements.

F-5

GolfSuites 1, Inc. and Subsidiaries

Consolidated Statement of Stockholders' Equity (Deficit)

For the Years Ended December 31, 2021 and 2020

See accompanying Independent Auditor's report

| Class A | Class B | Class A | Other | Retained Earnings, | Total | |||||||||||||||||||||||||||||||||||

| Common Stock | Common Stock | Preferred Stock | Preferred Stock | Net of | Stockholders' | |||||||||||||||||||||||||||||||||||

| Shares | Value | Shares | Value | Shares | Value | Shares | Value | Dividends | Equity | |||||||||||||||||||||||||||||||

| Balance as of December 31, 2019 | - | $ | - | 18,000,000 | $ | 180 | 74,038 | $ | 381,295 | - | $ | - | $ | (1,126,175 | ) | $ | (744,700 | ) | ||||||||||||||||||||||

| Share issuance | - | - | - | - | 200,704 | 923,239 | - | - | - | 923,239 | ||||||||||||||||||||||||||||||

| Net loss | - | - | - | - | - | - | - | - | (684,513 | ) | (684,513 | ) | ||||||||||||||||||||||||||||

| Dividends | - | - | - | - | - | - | - | - | (76,441 | ) | (76,441 | ) | ||||||||||||||||||||||||||||

Balance as of December 31, 2020 | - | - | 18,000,000 | 180 | 274,742 | 1,304,534 | - | - | (1,887,129 | ) | (582,415 | ) | ||||||||||||||||||||||||||||

| Share issuance | - | - | - | - | 265,761 | 2,126,084 | - | - | - | 2,126,084 | ||||||||||||||||||||||||||||||

| Net income | - | - | - | - | - | - | - | - | (697,690 | ) | (697,690 | ) | ||||||||||||||||||||||||||||

| Dividends | - | - | - | - | - | - | - | - | (133,968 | ) | (133,968 | ) | ||||||||||||||||||||||||||||

Balance as of December 31, 2021 | - | $ | - | 18,000,000 | $ | 180 | 540,503 | $ | 3,430,618 | - | $ | - | $ | (2,718,787 | ) | $ | 712,011 | |||||||||||||||||||||||

The accompanying notes are an integral part of these financial statements.

F-6

GolfSuites 1, Inc. and Subsidiaries

Consolidated Statement of Cash Flows

For the Years Ended December 31, 2021 and 2020

See accompanying Independent Auditor's report

| 2021 | 2020 | |||||||

| Cash Flows from Operating Activities | ||||||||

| Net loss | $ | (697,690 | ) | $ | (684,513 | ) | ||

| Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | ||||||||

| Minority interest share of income (loss) | (116,627 | ) | (33,779 | ) | ||||

| Depreciation and amortization | 1,104,196 | 395,793 | ||||||

| Changes in operating assets and liabilities | ||||||||

| Accounts receivable | (322,147 | ) | (26,935 | ) | ||||

| Inventory | (17,570 | ) | (53,286 | ) | ||||

| Prepaid expenses | (22,510 | ) | 295 | |||||

| Accounts payable and accrued expenses | (529,450 | ) | 28,881 | |||||

| Other assets | (1,778 | ) | (10,624 | ) | ||||

| Reg A and Reg D share sale costs | 985,742 | 915,938 | ||||||

| Net cash provided by operating activities | 382,166 | 531,770 | ||||||

| Cash Flows from Investing Activities | ||||||||

| Acquisition of operating golf entities | - | (1,550,517 | ) | |||||

| Purchase of property and equipment | (1,549,782 | ) | (2,315 | ) | ||||

| Capitalized development costs | (666,214 | ) | - | |||||

| Net cash used in investing activities | (2,215,996 | ) | (1,552,832 | ) | ||||

| Cash Flows from Financing Activities | ||||||||

| Proceeds from issuance of common stock | - | - | ||||||

| Proceeds from issuance of preferred stock | 2,126,084 | 923,239 | ||||||

| Proceeds from minority interest investor in subsidiary | 400,000 | - | ||||||

| Proceeds from PPP and EIDL loans, net of forgiveness | 149,000 | 149,900 | ||||||

| Proceeds from notes payable | - | 331,000 | ||||||

| Proceeds net of principal payments on mortgages, equipment loans and leases | 142,462 | (163,739 | ) | |||||

| Shareholder and related party advances, net | 271,619 | 1,278,694 | ||||||

| Dividend payments | (133,968 | ) | (76,441 | ) | ||||

| Reg A and Reg D share sale costs | (985,742 | ) | (915,938 | ) | ||||

| Net cash provided by financing activities | 1,969,455 | 1,526,715 | ||||||

| Net Change In Cash and Cash Equivalents | 135,625 | 505,653 | ||||||

| Cash and Cash Equivalents, Beginning of Period | 538,519 | 32,866 | ||||||

| Cash and Cash Equivalents, End of Period | $ | 674,144 | $ | 538,519 | ||||

The accompanying notes are an integral part of these financial statements.

F-7

GolfSuites 1, Inc.

Notes to Consolidated Financial Statements

As of December 31, 2021 and 2020

See accompanying Independent Auditor's report

NOTE 1 - NATURE OF OPERATIONS

GolfSuites 1, Inc. (which may be referred to as “GS 1”, the “Company”, “we”, “us”, or “our”) is an early-stage company devoted to the development and operation of golf driving range and entertainment centers in the United States. The Company will operate under the brand GOLFSUITES. The Company will oversee the acquisition of land, zoning, entitlement, design, construction and operation of the planned facilities.

The Company owns 100% of GolfSuites Tulsa, LLC ("Tulsa") and 100% of GolfSuites Lubbock, LLC (“Lubbock”). Tulsa was formerly operated under the FlyingTee brand, but now operates under the GolfSuites brand. Lubbock was formerly operated under the 4ORE! Golf brand, but now operates under 4ORE! Golf-Powered By GolfSuites brand, and will change to usage of the GolfSuites brand later in 2022. The attached statement of operations includes the operations of Tulsa for 2021 and 2020, and Lubbock since the acquisition date in mid-August 2020. Minority interest in the 2020 loss of Lubbock has been reflected in the attached statements due to GS 1’s partial ownership of Lubbock from mid-August through mid-November 2020, when it took over 100% ownership.

On March 16, 2021 GS 1 formed GolfSuites Baton Rouge, LLC (“Baton Rouge”), a Louisiana limited liability company for the purpose of leasing an approximate 18-acre existing driving range that had been closed for operations. This site will be developed at an estimated total cost of

$1,500,000. Upon completion it will operate as a 40-bay facility offering the same services as Tulsa and Lubbock. The expected completion of development and opening of Baton Rouge is early spring of 2022. Funding for this site is being provided by GS 1’s Reg A share sales, private equity investment, advances from GolfSuites, Inc. (“GolfSuites”) (parent company), and positive operating cash flows from existing operations. Minority interest in the loss of Baton Rouge has been reflected in the attached statements due to the allocation of the entire 2021 loss to the private equity investor. As of December 31, 2021, the private equity investor has invested $400,000 of his total commitment of $600,000.

Securities Offering

On January 8, 2021 the Company re-filed its Reg A offering. The company was qualified by the Securities and Exchange Commission (“SEC”) on February 18, 2021 and began selling the securities. The Company engaged with various advisors and other professionals to facilitate the offering who are being paid customary fees and equity interests for their work.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accounting and reporting policies of the Company conform to accounting principles generally accepted in the United States of America ("GAAP"). The Company has adopted December 31 as the year end for reporting purposes.

Use of Estimates

The preparation of the financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and the footnotes thereto. Actual results could differ from those estimates. It is reasonably possible that changes in estimates will occur in the near term.

F-8

Risks and Uncertainties

The Company has a limited operating history. The Company's business and operations are sensitive to general business and economic conditions in the United States. A host of factors beyond the Company's control could cause fluctuations in these conditions. Adverse conditions may include: recession, economic downturn, local competition or changes in consumer taste. These adverse conditions could affect the Company's financial condition and the results of its operations. As of December 31, 2021, the Company is operating as a going concern.

Cash and Cash Equivalents

The Company considers short-term, highly liquid investments with original maturities of three months or less, at the time of purchase, to be cash equivalents. Cash consists of currency held in the Company’s checking accounts. As of December 31, 2021 and 2020, GS 1’s consolidated cash balances totaled $674,144 and $538,519, respectively.

Receivables and Credit Policy

Trade receivables from customers are uncollateralized customer obligations due under normal trade terms, primarily requiring payment before services are rendered. Trade receivables are stated at the amount billed to the customer. Payments of trade receivables are allocated to the specific invoices identified on the customer’s remittance advice or, if unspecified, are applied to the earliest unpaid invoice. The Company, by policy, routinely assesses the financial strength of its customer. As a result, the Company believes that its accounts receivable credit risk exposure is limited and it has not experienced significant write-downs in its accounts receivable balances. Balances due from credit card companies are included in accounts receivable. As of December 31, 2021, accounts receivable includes $331,756 related to Employee Retention Credits – see Note 9 for additional details.

Property and Equipment

Property and equipment are recorded at cost. Expenditures for renewals and improvements that significantly add to the productive capacity or extend the useful life of an asset are capitalized. Expenditures for maintenance and repairs are expensed as incurred. When equipment is retired or sold, the cost and related accumulated depreciation are eliminated from the balance sheet accounts and the resultant gain or loss is reflected in income.

Depreciation is provided using the straight-line method, based on useful lives of the assets. Depreciation for the years ended December 31, 2021 and 2020 totaled $713,571 and $258,670, respectively.

The Company reviews the carrying value of property and equipment for impairment whenever events and circumstances indicate that the carrying value of an asset may not be recoverable from the estimated future cash flows expected to result from its use and eventual disposition. In cases where undiscounted expected future cash flows are less than the carrying value, an impairment loss is recognized equal to an amount by which the carrying value exceeds the fair value of assets. The factors considered by management in performing this assessment include current operating results, trends and prospects, the manner in which the property is used, and the effects of obsolescence, demand, competition, and other economic factors. As of December 31, 2021 and 2020, net property, plant and equipment consisted of the following:

| 2021 | 2020 | |||||||

| By Asset Category: | ||||||||

| Land and building improvements | $ | 6,867,239 | $ | 6,867,239 | ||||

| Furniture, fixtures and equipment | 3,742,864 | 3,524,920 | ||||||

| Construction in progress | 650,241 | - | ||||||

| Acumulated depreciation | (2,630,573 | ) | (1,917,002 | ) | ||||

| Total | $ | 8,629,771 | $ | 8,475,157 | ||||

| Net Book Value By Entity: | ||||||||

| Tulsa | $ | 624,764 | $ | 534,946 | ||||

| Lubbock | 7,354,766 | 7,940,211 | ||||||

| Baton Rouge | 650,241 | - | ||||||

| Total | $ | 8,629,771 | $ | 8,475,157 | ||||

F-9

Capitalized Development Costs

The Company has capitalized development fees under contractual agreements with its parent company, GolfSuites. These costs totaled $666,214 as of December 31, 2021 and are not amortized for GAAP purposes.

Goodwill

The Company has recorded Goodwill related to the acquisition of its Tulsa and Lubbock golf operating entities in 2019 and 2020 respectively. Management has reviewed the amounts recorded as Goodwill in accordance with ASC 350-20-35-3C and has determined that the fair values of Tulsa and Lubbock are greater than carrying values, including Goodwill. Therefore, no impairment losses were recorded for 2021 or 2020. Following is a summary of the Goodwill values for Tulsa and Lubbock.

| Tulsa | Lubbock | Total | ||||||||||

| Acquisition cost | $ | 1,019,878 | $ | 1,550,517 | $ | 2,570,395 | ||||||

| Value of assets and liabilities acquired | 160,118 | 661,022 | 821,140 | |||||||||

| Goodwill | $ | 859,760 | $ | 889,495 | $ | 1,749,255 | ||||||

Income Taxes

Income taxes are provided for the tax effects of transactions reporting in the financial statements and consist of taxes currently due plus deferred taxes related primarily to differences between the basis of receivables, inventory, property and equipment, intangible assets, cryptocurrency valuation and accrued expenses for financial and income tax reporting. The deferred tax assets and liabilities represent the future tax return consequences of those differences, which will either be taxable or deductible when the assets and liabilities are recovered or settled. Deferred tax assets are reduced by a valuation allowance when, in the opinion of management, it is more likely than not that some portion or all the deferred tax assets will not be realized.

The Company is taxed as a C Corporation for federal and state income tax purposes. As the Company has recently been formed, no material tax provision exists as of the balance sheet date.

The Company evaluates its tax positions that have been taken or are expected to be taken on income tax returns to determine if an accrual is necessary for uncertain tax positions. As of December 31, 2021 and 2020 the Company had no uncertain tax positions requiring accruals.

The Company is current with its foreign, US federal and state income tax filing obligations and is not currently under examination from any taxing authority.

Revenue Recognition

In 2019, the Company adopted ASC 606, Revenue from Contracts with Customers, as of inception. There was no transition adjustment recorded upon the adoption of ASC 606. Under ASC 606, revenue is recognized when a customer obtains control of promised goods or services, in an amount that reflects the consideration which the entity expects to receive in exchange for those goods or services.

To determine revenue recognition for arrangements that an entity determines are within the scope of ASC 606, the Company performs the following steps: (i) identify the contract(s) with a customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction price, (iv) allocate the transaction price to the performance obligations in the contract and (v) recognize revenue when (or as) the entity satisfies a performance obligation. At contract inception, once the contract is determined to be within the scope of ASC 606, the Company assesses the goods or services promised within each contract and determines those that are performance obligations and assesses whether each promised good or service is distinct. The Company then recognizes as revenue the amount of the transaction price that is allocated to the respective performance obligation when (or as) the performance obligation is satisfied.

F-10

Advertising Expenses

The Company expenses advertising costs as they are incurred.

Organizational Costs

In accordance with GAAP, organizational costs, including accounting fees, legal fees, and costs of incorporation, are expensed as incurred.

Development & Management Fees

Pursuant to a Management Services Agreement (“MSA”) that exists between GolfSuites and GS 1, fees for development and management of assets are due and paid from GS 1 to GolfSuites. GS 1 pays 3% of the total cost of new assets acquired or developed as development fees on its facilities to GolfSuites, and it pays 4% of gross operating revenue as management fees to GolfSuites. Management fees are reflected on the GS 1 Statement of Operations – Other income (expense). Development fees are reflected on the Consolidated Balance Sheet of GS 1.

Earnings per Share

Earnings per share amounts are calculated based on the weighted-average number of shares of common stock outstanding in each year. The basic loss per share is based only on the weighted-average of common shares outstanding. The diluted loss per share is based on the weighted-average of common shares outstanding plus Class A preferred shares, which are convertible to one share of common stock.

Common and Preferred Share Sales and Affiliated Costs

GS 1 collected $2,126,084 in preferred share sales in 2021. The Company paid $985,742 in costs including direct compensation, platform facilitating, marketing, share issuance / administration, and advertising for the sale of such shares, accounting for an approximate 46.4% cost ratio. Accounting for approximately $150,000 of costs incurred in the current year for prior years’ share sales, the adjusted cost ratio approximates 39.3%.

Concentration of Credit Risk

The Company maintains its cash with major financial institutions located in the United States of America, which it believes to be credit worthy. The Federal Deposit Insurance Corporation insures balances up to $250,000. At times, the Company may maintain balances in excess of the federally insured limits. Management believes the risk of loss is minimal.

Recent Accounting Pronouncements