UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| |

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2024 or

| |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-40373

ENDEAVOR GROUP HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| |

Delaware | 83-3340169 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

9601 Wilshire Boulevard, 3rd Floor

Beverly Hills, CA 90210

(Address of principal executive offices) (Zip Code)

(310) 285-9000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Class A Common Stock, par value $0.00001 per share | EDR | The New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | |

Large accelerated filer | ☒ | Accelerated filer | ☐ |

Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, based on the closing price of the shares of Class A common stock on the New York Stock Exchange on June 30, 2024, was $5,738,547,955. Solely for the purposes of this disclosure, shares of common stock held by the registrant’s executive officers, directors and certain of its stockholders as of such date have been excluded because such holders may be deemed to be affiliates.

As of January 31, 2025, there were 325,544,007 shares of the registrant’s Class A common stock outstanding, 144,878,961 shares of the registrant's Class X common stock outstanding and 215,927,779 shares of the registrant's Class Y common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the registrant's Definitive Proxy Statement for the registrant's 2025 annual meeting of stockholders to be filed with the Securities and Exchange Commission no later than 120 days after the end of the fiscal year ended December 31, 2024 are incorporated herein by reference in Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (the "Annual Report") contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 27A of the Securities Act of 1933, as amended (the "Securities Act") and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). All statements other than statements of historical facts contained in this Annual Report, including without limitation, statements regarding the anticipated timing, benefits and costs associated with the Merger Agreement and Merger-Related Transactions (as defined below), our expectations surrounding the Merger Agreement and Merger-Related Transactions and its ability to maximize shareholder value, our expectations, beliefs, plans, strategies, objectives, prospects, assumptions, future events or expected performance, are forward-looking statements.

Without limiting the foregoing, you can generally identify forward-looking statements by the use of forward-looking terminology, including the terms "aim," "anticipate," "believe," "could," "mission," "may," "will," "should," "believe," "expect," "anticipate," "intend," "plan," "estimate," "project," "target," "predict," "potential," "contemplate," or, in each case, their negative, or other, variations or comparable terminology and expressions. The forward-looking statements in this Annual Report are only predictions and are based on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition, and results of operations. These forward-looking statements speak only as of the date of this Annual Report and are subject to a number of known and unknown risks, uncertainties and assumptions, including, but not limited to:

•risks related to the Merger, the Merger-Related Transactions, the TKO Asset Acquisition and the OpenBet Acquisition (as defined below);

•changes in public and consumer tastes and preferences and industry trends;

•impacts from changes in discretionary and corporate spending on entertainment and sports events due to factors beyond our control, such as adverse economic conditions, on our operations;

•our ability to adapt to or manage new content distribution platforms or changes in consumer behavior resulting from new technologies;

•our reliance on our professional reputation and brand name;

•our dependence on the relationships of our management, agents, and other key personnel with clients across many content categories;

•our ability to identify, recruit, and retain qualified and experienced agents and managers;

•our ability to identify, sign, and retain clients;

•our ability to avoid or manage conflicts of interest arising from our client and business relationships;

•the loss or diminished performance of members of our executive management and other key employees;

•our dependence on key relationships with television and cable networks, satellite providers, digital streaming partners, corporate sponsors, and other distribution partners;

•our ability to effectively manage the integration of and recognize economic benefits from businesses acquired, our operations at our current size, and any future growth;

•the conduct of our operations through joint ventures and other investments with third parties;

•immigration restrictions and related factors;

•failure to protect our IT Systems and Confidential Information against breakdowns, security breaches, and other cybersecurity risks;

•the unauthorized disclosure of sensitive or confidential client or customer information;

•our ability to protect our trademarks and other intellectual property rights, including our brand image and reputation, and the possibility that others may allege that we infringe upon their intellectual property rights;

•risks associated with the legislative, judicial, accounting, regulatory, political and economic risks and conditions specific to both domestic and international markets;

•fluctuations in foreign currency exchange rates;

•litigation and other proceedings;

•our ability to comply with the U.S. and foreign governmental regulations to which we are subject;

•our compliance with certain franchise and licensing requirements of unions and guilds and dependence on unionized labor, which exposes us to risks of work stoppages or labor disturbances;

•our ability to obtain additional financing;

•risks related to our sports betting businesses and applicable regulatory requirements;

•risks related to successful integration of the businesses of WWE and UFC;

•our control by Messrs. Emanuel and Whitesell, the Executive Holdcos, and the Silver Lake Equityholders;

•risk related to our organization and structure;

•conflicts of interests that could result due to the amendments to the Endeavor Operating Company LLC Agreement;

•cash required to service our indebtedness;

•risks related to tax matters;

•risks related to our Class A common stock;

•risks related to the TKO Transactions (as defined below);

•risks related to our paying quarterly cash dividends, including pursuant to the Merger Agreement;

•risks related to other dispositions we may contemplate; and

•other important factors that could cause actual results, performance or achievements to differ materially from those described in Part I, Item 1A. "Risk Factors" and Part II, Item 7. "Management’s Discussion and Analysis of Financial Condition and Results of Operations" in this Annual Report and in any subsequent filings with the Securities and Exchange Commission (the "SEC").

These risks could cause actual results to differ materially from those implied by forward-looking statements in this Annual Report. Moreover, we operate in an evolving environment. New risk factors and uncertainties may emerge from time to time, and it is not possible for management to predict all risk factors and uncertainties. Even if our results of operations, financial condition and liquidity and the development of the industry in which we operate are consistent with the forward-looking statements contained in this Annual Report, those results or developments may not be indicative of results or developments in subsequent periods.

You should read this Annual Report and the documents that we reference herein completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements. Except as required by applicable law, we have no obligation to update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise.

DEFINITIONS

As used in this Annual Report, unless we state otherwise or the context otherwise requires:

•"we," "us," "our," "Endeavor," the "Company," and similar references refer (a) after giving effect to the reorganization transactions, to Endeavor Group Holdings and its consolidated subsidiaries, and (b) prior to giving effect to the reorganization transactions, to Endeavor Operating Company and its consolidated subsidiaries.

•"Endeavor Group Holdings" and "EGH" refer to Endeavor Group Holdings, Inc.

•"Endeavor Manager" refers to Endeavor Manager, LLC, a Delaware limited liability company and a direct subsidiary of Endeavor Group Holdings following the reorganization transactions.

•"Endeavor Manager Units" refers to the common interest units in Endeavor Manager.

•"Endeavor Operating Company" and "EOC" refer to Endeavor Operating Company, LLC, a Delaware limited liability company and a direct subsidiary of Endeavor Manager’s and indirect subsidiary of ours following the reorganization transactions.

•"Endeavor Operating Company Units" refers to all of the existing equity interests in Endeavor Operating Company (other than the Endeavor Profits Units) that were reclassified into Endeavor Operating Company’s non-voting common interest units upon the consummation of the reorganization transactions.

•"Endeavor Profits Units" refers to the profits units of Endeavor Operating Company and that are economically similar to stock options (other than with respect to Endeavor Full Catch-Up Profits Units which, upon our achievement of a price per share that would have fully satisfied their preference on distributions, were converted into Endeavor Operating Company Units). Each Endeavor Profits Unit (other than Endeavor Full Catch-Up Profits Units) has a per unit hurdle price, which is economically similar to the exercise price of a stock option.

•"Executive Holdcos" refers to Endeavor Executive Holdco, LLC, Endeavor Executive PIU Holdco, LLC, and Endeavor Executive II Holdco, LLC, each a management holding company, the equity owners of which include current and former senior officers, employees, or other service providers of Endeavor Operating Company, and which are controlled by Messrs. Emanuel and Whitesell.

•"fully-diluted basis" means on a basis calculated assuming the full cash exercise (and not net settlement but, for the avoidance of doubt, including the conversion of the Convertible Notes (to the extent not converted prior to closing of the Transactions)) of all outstanding options, warrants, restricted stock units, performance stock units, dividend equivalent rights and other rights and obligations (including any promised equity awards and assuming the full issuance of the shares underlying such awards) to acquire voting interests of TKO Group Holdings (without regard to any vesting provisions and, with respect to any promised awards whose issuance is conditioned in full or in part based on achievement of performance goals or metrics, assuming achievement at target performance) and the full conversion, exercise, exchange, settlement of all issued and outstanding securities convertible into or exercisable, exchangeable or settleable for voting interests of TKO Group Holdings, not including any voting interests of TKO Group Holdings reserved for issuance pursuant to future awards under any option, equity bonus, share purchase or other equity incentive

plan or arrangement of TKO Group Holdings (other than promised awards described above), and any other interests or shares, as applicable, that may be issued or exercised. For the avoidance of doubt, this definition assumes no net settlement or other reduction in respect of withholding tax obligations in connection with the issuance, conversion, exercise, exchange or settlement of such rights or obligations to acquire interests of TKO Group Holdings as described in the foregoing.

•"Governing Body" means the Company’s governing body, which is exclusively vested with all of the powers of our board of directors (under applicable Delaware law) in the management of our business and affairs and that acts in lieu of our board of directors to the fullest extent permitted under Delaware law, SEC rules and the rules of the New York Stock Exchange ("NYSE"). Prior to a Triggering Event, the Executive Committee is the Governing Body and, any action by our board of directors requires the prior approval of the Executive Committee, except for matters that are required to be approved by the Audit Committee (or both the Executive Committee and the Audit Committee), or by a committee qualified to grant equity to persons subject to Section 16 of the Exchange Act for purposes of exempting transactions pursuant to Section 16b-3 thereunder, or as required under Delaware law, SEC rules and NYSE rules.

•"Merger Agreement" refers to the Agreement and Plan of Merger, entered into on April 2, 2024, by and among the Company, Endeavor Manager, Endeavor Operating Company (together with the Company and Endeavor Manager, the "Company Entities" and each, a "Company Entity"), Executive Holdcos, Wildcat EGH Holdco, L.P., a Delaware limited partnership ("Holdco Parent"), Wildcat OpCo Holdco, L.P., a Delaware limited partnership ("OpCo Parent" and, together with Holdco Parent, the "Parent Entities" and each, a "Parent Entity"), Wildcat PubCo Merger Sub, Inc., a Delaware corporation and wholly-owned subsidiary of Holdco Parent ("Company Merger Sub"), Wildcat Manager Merger Sub, L.L.C., a Delaware limited liability company and a wholly-owned subsidiary of Company Merger Sub ("Manager Merger Sub"), Wildcat OpCo Merger Sub, L.L.C., a Delaware limited liability company and wholly-owned subsidiary of OpCo Parent ("OpCo Merger Sub" and, together with Endeavor Manager Merger Sub and Company Merger Sub, the "Merger Subs" and each, a "Merger Sub").

•"Merger" and "Merger-Related Transactions" refers to the transactions contemplated by the terms of the Merger Agreement (as defined above) that, upon completion, will result in Endeavor’s common stock no longer being listed on any public market (referred to as, the "take-private transaction"). Pursuant to the Merger Agreement, (a) OpCo Merger Sub will merge with and into Endeavor Operating Company, with Endeavor Operating Company surviving the merger, collectively owned, directly or indirectly, by OpCo Parent, the Company, Endeavor Manager and certain Rollover Holders (the "OpCo Merger"), (b) immediately following the OpCo Merger, Manager Merger Sub will merge with and into Endeavor Manager, with Endeavor Manager surviving the merger, wholly-owned by the Company (the "Manager Merger") and (c) immediately following the Manager Merger, Company Merger Sub will merge with and into the Company, with the Company surviving the merger, collectively owned, directly or indirectly, by Holdco Parent and/or certain Rollover Holders (the "Company Merger" and, together with the Manager Merger and the OpCo Merger, the "Merger" and, together with the other transactions contemplated by the Merger Agreement, collectively, the "Merger-Related Transactions").

•"Other UFC Holders" refers to the other persons that hold equity interests in UFC Parent and certain of their affiliates.

•"reorganization transactions" refers to the internal reorganization completed in connection with our May 2021 initial public offering ("IPO"), following which Endeavor Group Holdings manages and operates the business and control the strategic decisions and day-to-day operations of Endeavor Operating Company through Endeavor Manager and includes the operations of Endeavor Operating Company in its consolidated financial statements.

•"Rollover Holders" refers to certain direct or indirect holders of equity interests in the Company and Endeavor Operating Company (each, a "Rollover Holder") each of which entered into a rollover agreement with the Parent Entities, pursuant to which each Rollover Holder has agreed, on the terms and subject to the conditions set forth in the rollover agreements, that certain of their equity interests in Endeavor Operating Company will remain outstanding in the OpCo Merger, and/or certain of shares of Common Stock they own will remain outstanding in the Company Merger.

•"Silver Lake Equityholders" refers to certain affiliates of Silver Lake that are our stockholders.

•"Triggering Event" means the earlier of (i) the date on which neither Messrs. Emanuel nor Whitesell is employed as our Chief Executive Officer or Executive Chairman and (ii) the date on which neither Messrs. Emanuel nor Whitesell own shares of our Class A common stock representing, and/or own securities representing the right to own (including Endeavor Profits Units), at least 25% of the shares of our Class A common stock and securities representing the right to own shares of our Class A common stock owned by Messrs. Emanuel and Whitesell, respectively, as of the completion of the IPO.

•"TKO" refers to TKO Group Holdings, Inc., a consolidated subsidiary of the Company, which, following the TKO Transactions, owns and operates the UFC and WWE.

•"TKO Asset Acquisition" refers to the transaction entered into by EOC, Endeavor and IMG Worldwide (collectively, the "EDR Parties") and TKO and TKO OpCo (the "TKO Parties"), pursuant to which TKO OpCo will acquire Professional Bull Riders ("PBR"), On Location, and certain of the IMG businesses for total consideration of $3.25 billion, based on the volume-weighted average sales price of TKO Class A common stock for the twenty-five trading days ending on October 23, 2024.

•The "TKO Transactions" refer to the combination of the UFC and WWE businesses into a new publicly listed company, TKO.

•"UFC" refers to the Ultimate Fighting Championship, the professional mixed martial arts ("MMA") organization.

•"UFC Parent" refers to Zuffa Parent LLC (n/k/a TKO Operating Company, LLC or "TKO OpCo").

•"WWE" refers to World Wrestling Entertainment, Inc. (n/k/a World Wrestling Entertainment, LLC).

•"Zuffa" refers to Zuffa Parent, LLC (n/k/a TKO Operating Company, LLC).

RISK FACTORS SUMMARY

Our business is subject to numerous risks and uncertainties, including those described in Part I, Item 1A. "Risk Factors" in this Annual Report. You should carefully consider these risks and uncertainties when investing in our securities. Principal risks and uncertainties affecting our business include the following:

•risks related to the Merger, the Merger-Related Transactions, the TKO Asset Acquisition and the OpenBet Acquisition;

•changes in public and consumer tastes and preferences and industry trends could reduce demand for our services and content offerings and adversely affect our business;

•our ability to generate revenue from discretionary and corporate spending on entertainment and sports events, such as corporate sponsorships and advertising, is subject to many factors, including many that are beyond our control, such as general macroeconomic conditions;

•we may not be able to adapt to or manage new content distribution platforms or changes in consumer behavior resulting from new technologies;

•because our success depends substantially on our ability to maintain a professional reputation, adverse publicity concerning us, one of our businesses, our clients, or our key personnel could adversely affect our business;

•we depend on the relationships of our agents, managers, and other key personnel with clients across many categories, including television, film, professional sports, fashion, music, literature, theater, digital, sponsorship and licensing;

•our success depends, in part, on our continuing ability to identify, recruit, and retain qualified and experienced agents and managers. If we fail to recruit and retain suitable agents or if our relationships with our agents change or deteriorate, it could adversely affect our business;

•our failure to identify, sign, and retain clients could adversely affect our business;

•our business involves potential internal conflicts of interest due to the breadth and scale of our platform;

•the markets in which we operate are highly competitive, both within the United States and internationally;

•we depend on the continued service of the members of our executive management and other key employees, as well as management of acquired businesses, the loss or diminished performance of whom could adversely affect our business;

•we depend on key relationships with television and cable networks, satellite providers, digital streaming partners and other distribution partners, as well as corporate sponsors;

•our failure to protect our IT Systems and Confidential Information against breakdowns, security breaches, and other cybersecurity risks could result in financial penalties, legal liability, and/or reputational harm, which would adversely affect our business, results of operations, and financial condition;

•we may be unable to protect our trademarks and other intellectual property rights, and others may allege that we infringe upon their intellectual property rights;

•we are subject to extensive U.S. and foreign governmental regulations, and our failure to comply with these regulations could adversely affect our business;

•we are signatory to certain franchise agreements of unions and guilds and are subject to certain licensing requirements of the states in which we operate. We are also signatories to certain collective bargaining agreements and depend upon unionized labor for the provision of some of our services. Our clients are also members of certain unions and guilds that are signatories to collective bargaining agreements. Any expiration, termination, revocation or non-renewal of these franchises, collective bargaining agreements, or licenses and any work stoppages or labor disturbances could adversely affect our business;

•our businesses in the sports betting industry are subject to strict government regulations;

•some of TKO’s executive officers and directors may have actual or potential conflicts of interest because of their equity interest in us. Also, certain of TKO’s current executive officers are our directors and officers, which may create conflicts of interest or the appearance of conflicts of interest;

•we are a holding company and our principal asset is our indirect equity interests in Endeavor Operating Company and, accordingly, we are dependent upon distributions from Endeavor Operating Company to pay taxes and other expenses;

•amendments to the Endeavor Operating Company LLC Agreement that allow us to limit tax distributions that would otherwise be made could result in conflicts of interest;

•we are controlled by Messrs. Emanuel and Whitesell, Executive Holdcos, and the Silver Lake Equityholders, whose interests in our business may be different than our holders of Class A common stock, and our board of directors has delegated significant authority to an Executive Committee and to Messrs. Emanuel and Whitesell;

•we require a significant amount of cash to service our indebtedness. Our ability to generate cash for, make payments on or refinance our indebtedness as it becomes due depends on many factors, some of which are beyond our control and could impact our ability to continue as a going concern;

•we are required to pay certain of our pre-IPO investors, including certain Other UFC Holders, for certain tax benefits we may claim (or are deemed to realize) in the future, and the amounts we may pay could be significant; and

•we cannot guarantee we will continue to pay dividends in any specified amounts or a particular frequency.

PART I

Item 1. Business

Endeavor Group Holdings, Inc. is a global sports and entertainment company. We own and operate premium sports and entertainment properties, including UFC and WWE through our majority ownership of TKO, produce and distribute sports and entertainment content, own and manage exclusive live events and experiences, and represent top sports, entertainment and fashion talent, as well as blue chip corporate clients. Founded as a client representation business, we expanded organically and through strategic mergers and acquisitions, investing in new capabilities, including sports operations and advisory, events and experiences management, media production and distribution, sports data and technology, brand licensing, and experiential marketing.

We believe that our unique business model gives us a competitive advantage in the industries in which we operate. Our ownership of premium sports properties allows us to benefit from the generally rising value and increasing scarcity of ownable, scalable sports assets. Our dual role as an intellectual property owner and a trusted advisor to clients and rights holders allows us to make connections across the Endeavor network, increasing the earnings of our clients and the value of our sports and entertainment properties. We generally participate in the upside related to the commercial success of content with limited risk and we benefit from demand from both traditional and next generation distributors. We own and manage a diverse mix of premium live events and experiences in the entertainment, sports, fashion, culinary and art categories. The insights we gain from our connectivity across the sports and entertainment ecosystem may enable us to spot trends before they emerge and make strategic investments to enhance our growth.

Recent Developments

In April 2024, following our review to evaluate strategic alternatives, we entered into the Merger Agreement, pursuant to which affiliates of Silver Lake agreed to acquire 100% of the outstanding shares of our stock that it does not already own (other than certain equity interests held by certain current directors and executive officers of the Company and any other Rollover Holders (the "Rollover Interests")). Pursuant to the Merger Agreement and subject to the satisfaction or waiver of certain conditions and on the terms set forth therein, equityholders of Endeavor, Endeavor Operating Company and Endeavor Manager are to receive $27.50 in cash per share or unit, as applicable. The Merger Agreement also requires us to, in each calendar quarter prior to the closing, declare and pay a dividend in respect of each issued and outstanding share of our Class A common stock at a price equal to $0.06 per share. The Merger-Related Transactions are expected to close by the end of the first quarter of 2025, subject to certain customary closing conditions, including required regulatory approvals. Upon completion, our common stock will no longer be listed on any public market. For a discussion of risks relating to the Merger-Related Transactions, see Part I, Item 1A., Risk Factors.

In October 2024, the EDR Parties entered into an agreement with the TKO Parties (the “TKO Transaction Agreement”), pursuant to which TKO OpCo will acquire PBR, On Location, and certain of the IMG businesses for total consideration of $3.25 billion, based on the volume-weighted average sales price of TKO Class A common stock for the twenty-five trading days ending on October 23, 2024. The EDR Parties will receive approximately 26.1 million common units of TKO OpCo and will subscribe for an equal number of shares of TKO Class B common stock, subject to purchase price adjustments to be settled in cash and equity. Upon the close of the TKO Asset Acquisition, the EDR Parties are expected to own approximately 61% of the voting power of TKO through its holdings of TKO Class A common stock and common units of TKO OpCo. The TKO Asset Acquisition is expected to close in the first quarter of 2025, subject to the satisfaction or waiver of certain customary closing conditions, including receipt of required regulatory approvals and the affirmative vote of holders of a majority of the voting power of TKO common stock in favor of adopting the transaction agreement (which has been satisfied by delivery of a written consent by such stockholders). The TKO Asset Acquisition will be accounted for as a common control transaction between the companies.

In October 2024, we commenced a review and potential sale of certain assets within our events portfolio, including but not limited to the Miami Open and the Madrid Open tennis tournaments and art platform, Frieze. We have not set a deadline or definitive timetable for the completion of any potential sales.

In November 2024, we entered into an agreement with WME IMG, OB Global Holdings LLC, an entity affiliated with Ariel Emanuel, our Chief Executive Officer, and certain members of OpenBet management, pursuant to which OB Global Holdings LLC will acquire OpenBet and IMG ARENA for total consideration of approximately $450.0 million (the "OpenBet Acquisition"), subject to certain adjustments, consisting of (i) a $100.0 million cash payment, subject to specified adjustments as set forth in the agreement, and (ii) an unsecured promissory note with a make-whole value of approximately $350.0 million upon the occurrence of certain events, including a voluntary prepayment or a change of control of OB Global Holdings LLC.

Segments

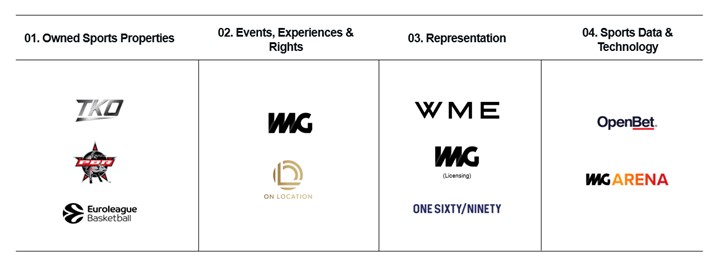

As a result of our Sports Data & Technology ("SD&T") segment being presented as discontinued operations (see Note 4, "Discontinued Operations and Held For Sale" to our annual consolidated financial statements included elsewhere in this Annual Report for further detail), we operate our business in three reportable segments in our continuing operations as of December 31, 2024: (i) Owned Sports Properties, (ii) Events, Experiences & Rights, and (iii) Representation, which are covered in greater detail in "Management’s Discussion and Analysis of Financial Condition and Results of Operation—Overview." Our segments are presented in the table below with select businesses:

We generate revenue in both a principal and an agency capacity and use risk mitigation strategies including pre-sales and licensing when we take on investment risk in content or sports rights. Our business has benefited from strong revenue visibility via sports rights fee payments, predictable client commissions, content rights payments, recurring annual, biennial, quadrennial or more frequent events, corporate client retainers, and licensing agreements. We believe that visibility into our performance provides us with a stable and growing revenue base.

Our Integrated Global Business

Across our segments, our global portfolio of premium owned assets and integrated set of capabilities, including client representation, media production & distribution, cultural and experiential marketing, and brand licensing drive revenue generation opportunities, improve client retention, and increase the flow of acquisition and investment opportunities.

Owned Sports Properties

We believe that our Company is distinguished by our ownership of intellectual property, including UFC, a global sports property and the premier mixed martial arts sports organization, and WWE, the recognized global leader in sports entertainment. UFC is among the most popular sports organizations in the world. As of December 31, 2024, UFC has more than 700 million fans who skew young and diverse, as well as approximately 299 million social media followers, and broadcasts its content to over 950 million households across more than 170 countries and territories. As of the same period, WWE has over 700 million fans and over 382 million social media followers. WWE counts more than 106 million YouTube subscribers, making it one of the most viewed YouTube channels globally, and its year-round programming is available in over one billion households across approximately 160 countries and territories. In total, our more than 300 live events across UFC and WWE have attracted more than two million attendees on an annual basis and serve as the foundation of our global content distribution strategy. In addition, we own PBR, the world's premier bull riding organization, featuring more than 1,000 bull riders competing in more than 250 events each year. PBR’s total live event attendance has increased by 125% since PBR was acquired by Endeavor in 2015. The organization has launched several event series since the acquisition and introduced a new league, PBR Teams, in 2022. In 2024, PBR entertained more than 1.4 million fans across its tour events and grossed its highest ever annual consumer ticketing revenue. As owners, we retain control over the organization, promotion and marketing of UFC, WWE, and PBR, as well as the monetization of their events, media distribution, licensing, and partnership sales. We also have a strategic partnership with Euroleague, which is expected to run through the 2035-2036 season.

Events, Experiences & Rights

We own, operate, or represent hundreds of global events annually, including live sports events covering more than 15 sports globally (e.g., Association of Tennis Professionals (ATP) and Women's Tennis Association (WTA) 1000 Tour Events, such as the Miami Open and Madrid Open), art fairs (e.g., Frieze Los Angeles, The Armory Show, and EXPO CHICAGO), music, culinary, and lifestyle festivals (e.g., The Big Feastival), and major attractions (e.g., Hyde Park Winter Wonderland and Barrett-Jackson). On Location, a leading provider of global premium live event experiences across sports and music, services more than 1,200 events and experiences built around major events, including the Super Bowl, FIFA World Cup 2026, the Aer Lingus Classic college football game, the Ryder Cup, the NCAA Final Four, Coachella and the 2024, 2026, and 2028 Olympic and Paralympic Games.

As one of the largest global distributors of sports programming, we manage, advise on, and/or sell media rights globally on behalf of more than 150 rights holders, such as the International Olympic Committee, the ATP and WTA Tours, CONMEBOL, and the National Hockey League ("NHL"), as well as for our owned assets, including UFC, WWE, and PBR. Our production business is one of the largest creators of sports programming in the world, responsible for more than 30,000 hours of content annually in more than 180 territories around the world, on behalf of federations, associations and events, including Major League Soccer ("MLS"), The R&A, Saudi Pro League, DP World Tour, and our owned assets, including UFC and WWE, as well as owned channel Sport 24. We broker and build commercial partnerships for owned properties and clients including The R&A, the All England Lawn and Tennis Club ("AELTC"), SailGP, Fédération Internationale de Football Association ("FIFA"), the Leagues Cup, and the Confederation of African Football ("CAF"). We provide a range of digital services and projects for clients, including the

National Football League ("NFL"), the NHL, Red Bull Racing, and multiple English Premier League clubs, NBA and NFL teams. We believe that our collective offering is more important than ever, as the demand for premium content and live experiences continues to be strong.

Representation

We represent many of the world’s greatest actors, writers, musicians, athletes, content creators, and notable figures across entertainment, sports, and fashion. In 2024, WME clients were involved in three of the top 10 grossing films at the U.S. box office, including summer blockbuster "Deadpool & Wolverine," which landed among the top three and premiered as the highest R-rated opening of all time.

WME also represents the creators behind some of the most-watched TV series across every major streaming service, including "The Bear" on Hulu, "House of the Dragon" on Max, "Avatar: The Last Airbender" on Netflix, "Percy Jackson" on Disney+, "Yellowstone" on Peacock, and "Masters of the Air" on Apple TV+. WME also sold more than 400 scripted and nonscripted projects across broadcast, streaming, and cable platforms.

WME closed deals for more than 300 new books, with WME represented authors debuting on The New York Times’ Best Seller list 65 times. WME closed over a thousand international book deals across the globe in 2024. WME also closed more than 120 audio deals with major podcast networks, including Khloe Kardashian’s new podcast "Khloé in Wonder Land" with X.

In theater, WME represented talent involved in 86% of the productions that opened during the 2023-24 Broadway season. Among many client wins at this year’s Tony Awards, David Adjmi’s "Stereophonic" won several awards, including Best Play, and became the most nominated play in Tony history.

In music, WME booked over 45,000 live shows in 2024. 328 clients played and 26 headlined or played top headline slots across 15 festivals including Coachella, Stagecoach, Lollapalooza and Glastonbury.

For the third consecutive year, WME Sports represented the most 2024 NBA Draft lottery picks of any agency with four, as well as five first round picks overall: Alex Sarr, Ron Holland II, Cody Williams, Devin Carter, and AJ Johnson. The 2024 WNBA season saw Sabrina Ionescu lead the New York Liberty to its first championship, marking three consecutive seasons in which a WME client has hoisted the trophy. With his victories at the French Open and Wimbledon, Carlos Alcaraz became a four-time grand slam winner, while Iga Świątek earned her fifth major championship at Roland-Garros.

Over 2,700 brand partnership deals were closed in 2024 including standout campaigns for Jeremy Allen White for Calvin Klein, Olivia Rodrigo for Lancôme, and John Legend for Montblanc.

Speakers bureau The Harry Walker Agency executed more than 1500 events globally in 2024. Top speakers included Tom Brady, Kim Kardashian, Rob Lowe, Ryan Reynolds, Mark Wahlberg, and Serena and Venus Williams.

We are dedicated to helping our clients increase the monetization potential of their intellectual property, build enduring brands, diversify and grow their businesses, and expand their geographic reach.

We are also a leading provider of licensing services to entertainment, sports, lifestyle, and consumer products brands, generating more than $17.2 billion in total retail sales for clients. For the sixth year in a row, our licensing business ranked No. 1 according to License Global magazine. We license our owned intellectual property, including the UFC, WWE, and PBR, and represent third-party brands and corporate trademarks across various industries including entertainment, gaming, automotive, fashion, sports, lifestyle, personalities, legends, corporate, and food and beverage. Our clients include McDonald’s, Jeep, Dolly Parton, Millie Bobby Brown, Volkswagen, Tetris, Claire’s, NFL, Harlem Globetrotters, Transport for London, Metropolitan Transport Authority, Lionsgate, Epic Games (Fortnite), and Gap.

Meanwhile, marketing services are delivered by 160over90, our full-service, global cultural marketing agency specializing in integrated marketing offerings spanning advertising and branding, strategy and creative, content and video production, creator marketing, digital services, entertainment marketing, experiential, media planning, partnerships, public relations/communications, and social media. 160over90 works on behalf of some of the world’s largest brands, including Amazon, Capital One, AB InBev, DP World, Marriott International, USAA and Visa. Through our owned and operated events and represented clients, 160over90 clients have access to unique content and activation opportunities, which we believe provides us with a competitive advantage, as well as access to the insights and intel brands are increasingly looking for in a rapidly changing marketing landscape.

Sports Data & Technology

The SD&T segment includes OpenBet, which specializes in betting engine products, services and technology, processing billions of bets annually, as well as trading, pricing and risk management tools; player account and wallet solutions; innovative front-end user experiences and user interfaces; and content offerings, such as BetBuilder, DonBest pricing feeds and a sports content aggregation platform. As part of OpenBet, IMG ARENA delivers live streaming and data feeds for more than 65,000 sports events annually to sportsbooks, rightsholders and media partners around the globe. This data also powers IMG ARENA's portfolio of on-demand virtual sports products and front-end solutions, including the UFC Event Centre. As contemplated in the Merger Agreement, we initiated a process to sell certain of our businesses. During the second quarter of 2024, we began to actively market the businesses comprising our SD&T segment, and in November 2024, signed a definitive agreement for the OpenBet Acquisition. As a result, the assets and liabilities are considered held for sale, and we determined the SD&T segment continued to meet the definition of a discontinued operation as of December 31, 2024; and, as such, we have recast our financial statements to present the SD&T segment as discontinued operations.

Intellectual Property and Other Proprietary Rights

We consider intellectual property to be very important to the operation of our business and to driving growth in our revenues, particularly with respect to professional engagements, sponsorships, licensing rights, and media distribution agreements. Our intellectual property includes, without

limitation, the "Endeavor," "WME," "William Morris Endeavor," "IMG," "UFC," "WWE", and "PBR" brands in addition to the trademarks and copyrights associated with our content and events, and the rights to use the intellectual property of our commercial partners. Substantially all of our intellectual property assets are protected through a combination of trademarks and copyrights, whether registered or unregistered.

Competition

The entertainment, sports, and content industries in which we participate are highly competitive. We face competition from alternative providers of the services, content, and events we and our clients and owned assets offer and from other forms of entertainment and leisure activities.

In our Events, Experiences & Rights segment, we face competition from other live, filmed, televised and streamed entertainment, including competition from other companies in the media rights industry. In our Representation segment, we compete with other agencies that represent and/or manage clients including talent and brands. In our Owned Sports Properties segment, we face competition from sports leagues, associations, promotions, and events. In our Sports Data & Technology segment, we compete with other technology and data companies that represent and/or manage clients including rightsholders. For a discussion of risks relating to competition, see Part I, Item 1A. "Risk Factors—The markets in which we operate are highly competitive, both within the United States and internationally."

Human Capital Resources

General

We believe the strength of our workforce is critical to our long-term success. Endeavor’s human capital management objectives include attracting, retaining, and developing high performing talent and empowering them with our guiding principles of persistence, collaboration, excellence, and inclusion.

As of December 31, 2024, we had approximately 10,000 employees in 40 countries, primarily in the U.S. and EMEA, with a smaller presence in other regions, including APAC. We have invested in and focused on the training and development of our employees, from both a personnel and technology perspective. We believe that our relations and engagement with our employees are good.

Talent Development

Endeavor recognizes that nurturing talent and embracing the constant evolution that leadership within our industry requires is crucial to our collective success. We have invested in multiple learning and development initiatives that strengthen the role of our leaders and people managers. Additionally, we offer learning programs for all employees to foster professional growth and skill development, including sessions on a variety of business and industry topics, on-demand digital learning resources, and mentorship programs.

Endeavor strives to create an inclusive work environment. To continue advancing our efforts to support qualified individuals of all backgrounds in succeeding across our company, we have launched and/or expanded upon the following initiatives in 2024:

•Initiated employee pulse surveys aimed at collecting actionable data on inclusion, belonging and wellness;

•Improved our recruitment practices to better result in qualified slates of candidates, and bolstered our network of recruitment partners;

•Established a program to support the retention and advancement of employees; used data from the program to identify key professional development areas for improvement and relaunched Empower, a retention program at WME;

•Grew the scope of our mentorship program aimed to result in career growth and development, an enhanced corporate culture, an increase in participants' confidence at work, and a widening of perspectives of all involved;

•Continued to grow and manage eight Employee Resource Groups (which are open to all employees) with 1,900+ employees across ten cities around the globe;

•Hosted frequent events globally for—or to celebrate—employees;

•Continued inclusive and impactful training programs.

Compensation and Benefits

The objective of our compensation and benefits programs is to provide a total rewards package that will attract, retain, motivate and reward the high-performing, qualified and skilled workforce necessary for our continued success across our diverse businesses. We seek to do this by linking compensation to company and business unit performance, as well as to each individual’s contributions to the results achieved. In addition to competitive base salaries, we accomplish this through annual cash-based bonus plans for eligible employees and long-term incentive plans for our executives.

Endeavor is committed to providing comprehensive benefit programs that enhance the total well-being of our people – and their families – both in and outside of work. Our programs are designed to inspire our people to prosper physically, mentally, socially, and financially. Some examples of our wide-ranging benefits offered include: health insurance, paid and unpaid leaves, a retirement plan, life insurance, disability/accident coverage, and mental health counseling and support.

Regulation and Legislation

We are subject to federal, state and local laws, both domestically and internationally, and at the state level by athletic commissions, governing matters such as:

•licensing laws for talent agencies, such as California’s Talent Agencies Act and the New York General Business Law;

•licensing laws for athletes;

•operation of our venues;

•licensing, permitting, and zoning;

•health, safety, and sanitation requirements;

•the service of food and alcoholic beverages;

•working conditions, labor, minimum wage and hour, citizenship, immigration, visas, harassment and discrimination, and other labor and employment laws and regulations;

•our employment of youth workers and compliance with child labor laws;

•compliance with the U.S. Foreign Corrupt Practices Act of 1977, as amended (the "FCPA"), the U.K. Bribery Act 2010 (the "Bribery Act") and similar regulations in other countries, as described in more detail below;

•antitrust and fair competition;

•data privacy and information security;

•environmental protection regulations;

•imposition by foreign countries of trade restrictions, restrictions on the manner in which content is currently licensed and distributed, ownership restrictions, or currency exchange controls;

•licensure and other regulatory requirements for the supply of sports betting data and software to gambling operators;

•licensing laws for the promotion and operation of MMA events; and

•government regulation of the entertainment and sports industry.

We monitor changes in these laws and believe that we are in material compliance with applicable laws. See Part I, Item 1A. "Risk Factors—Risks Related to Our Business—We are subject to extensive U.S. and foreign governmental regulations, and our failure to comply with these regulations could adversely affect our business."

Many of the events produced or promoted by our businesses are presented in venues which are subject to building and health codes and fire regulations imposed by the state and local governments in the jurisdictions in which the venues are located. These venues are also subject to zoning and outdoor advertising regulations and require a number of licenses in order for us to operate, including occupancy permits, exhibition licenses, food and beverage permits, liquor licenses, and other authorizations. In addition, these venues are subject to the U.S. Americans with Disabilities Act of 1990 and the U.K.’s Disability Discrimination Act 1995, which require us to maintain certain accessibility features at each of the facilities.

In various states in the United States and some foreign jurisdictions, we are required to obtain licenses for promoters, medical clearances and other permits or licenses for our athletes, and permits for our live events in order for us to promote and conduct those events. Generally, we or our employees hold promoters and matchmakers licenses to organize and hold certain of our live events. We or our employees hold these licenses in a number of states, including California, Nevada, New Jersey, and New York.

We are required to comply with the anti-corruption laws of the countries in which we operate, including the FCPA and the Bribery Act. These regulations make it illegal for us to pay, promise to pay, or receive money or anything of value to, or from, any government or foreign public official for the purpose of directly or indirectly obtaining or retaining business. This ban on illegal payments and bribes also applies to agents or intermediaries who use funds for purposes prohibited by the statute.

Our entertainment, sports, and content businesses are also subject to certain regulations applicable to our web sites and mobile applications. We maintain various web sites and mobile applications that provide information and content regarding our businesses and offer merchandise and tickets for sale. The operation of these web sites and applications may be subject to a range of federal, state, and local laws.

Gaming regulations in the jurisdictions in which we operate are established by statute and are administered by a regulatory agency with broad authority to interpret gaming regulations and to regulate gaming activities. Regulatory requirements vary among jurisdictions, but the majority of jurisdictions require licenses, permits, or findings of suitability for our company, individual officers, directors, major stockholders, and key employees. We believe we hold all of the licenses and permits necessary to conduct our business in this space, including the IMG ARENA and OpenBet businesses, which provide data technology and video for more than 65,000 sports events per year to sports betting platforms.

Available Information and Website Disclosure

We are required to file annual, quarterly and current reports, proxy statements and other information with the SEC. Our filings with the SEC are also available to the public through the SEC’s website at www.sec.gov.

You also can find more information about us online at our investor relations website located at www.investor.endeavorco.com. Filings we make with the SEC and any amendments to those reports are available free of charge on our website as soon as reasonably practicable after we electronically file such material with the SEC. The information posted on or accessible through our website is not incorporated into this Annual Report.

Investors and others should note that we announce material financial and operational information to our investors using press releases, SEC filings and public conference calls and call webcasts, and by postings on our investor relations site at investor.endeavorco.com. We may also use our website as a distribution channel of material Company information. In addition, you may automatically receive email alerts and other information about Endeavor when you enroll your email address by visiting the "Investor Email Alerts" option under the Resources tab on investor.endeavorco.com.

Item 1A. Risk Factors

Investing in our Class A common stock involves substantial risks. You should carefully consider the following factors and all other information in this Annual Report before investing in our Class A common stock. Any of the risk factors we describe below could adversely affect our business, financial condition or results of operations. The market price of our Class A common stock could decline if one or more of these risks or uncertainties develop into actual events, causing you to lose all or part of your investment. We cannot assure you that any of the events discussed below will not occur. While we believe these risks and uncertainties are especially important for you to consider, we may face other risks and uncertainties that could adversely affect our business. Please also see "Forward-Looking Statements" for more information.

Risks Related to the Merger and Other Strategic Transactions

The Merger, the pendency of the Merger or our failure to complete the Merger-Related Transactions could have a material adverse effect on our business, results of operations, financial condition and stock price.

As previously disclosed, on April 2, 2024, we entered into the Merger Agreement, providing for our acquisition by affiliates of Silver Lake. Completion of the Merger is subject to the satisfaction of various conditions, including: (1) the information statement having been mailed to the Company’s stockholders and at least 20 calendar days having elapsed since the completion of such mailing; (2) the absence of any law enjoining, restraining or otherwise prohibiting or making illegal the consummation of the Merger; (3) the expiration or termination of any applicable waiting period under the HSR Act, and the obtainment of regulatory clearances or approvals under certain specified foreign antitrust laws or foreign investment laws; (4) the clearance or obtainment of the applicable approvals by the Company Entities required by certain specified gaming authorities; (5) the accuracy of the other parties’ representations and warranties, subject to certain materiality standards set forth in the Merger Agreement; (6) compliance in all material respects with the other parties’ covenants, agreements and obligations under the Merger Agreement; (7) no Material Adverse Effect (as defined in the Merger Agreement) having occurred and being continuing since the date of the Merger Agreement; and (8) payment of quarterly dividends during the period between signing of the Merger Agreement and the closing of the Merger and, if applicable, payment of a catch-up dividend prior to closing of the Merger. There is no assurance that all of the various conditions will be satisfied, or that the Merger will be completed on the proposed terms, within the expected timeframe, or at all. Furthermore, there are additional inherent risks in the Merger, including the risks detailed below:

•the Merger-Related Transactions will not be consummated;

•the possibility that any or all of the various conditions to the consummation of the Merger-Related Transactions may not be satisfied or waived, including the failure to receive any required regulatory approvals from any applicable governmental entities (or any conditions, limitations or restrictions placed on such approvals), and the possibility that a Material Adverse Effect on our business would permit the Parent Entities not to close the Merger;

•the occurrence of any event, change or other circumstance that could give rise to the termination of the Merger Agreement;

•if the Merger Agreement is terminated in certain circumstances, we could be required to pay a termination fee of $288.5 million;

•the effect of the announcement or pendency of the proposed Merger-Related Transactions on the Company’s business relationships, operating results, and business generally;

•the inability to pursue certain business opportunities or strategic transactions pending the completion of the Merger, and other restrictions on our ability to conduct our business;

•risks that the proposed Merger-Related Transactions disrupts current plans and operations of the Company and potential difficulties in the Company’s employee retention as a result of the proposed Merger;

•there may be liabilities that are not known, probable or estimable at this time or unexpected costs, charges or expenses;

•the Merger-Related Transactions may result in the diversion of management’s time and attention to issues relating to the Merger-Related Transactions;

•there may be significant transaction-related costs in connection with the Merger-Related Transactions, whether or not the Merger closes;

•future stockholder litigation and other legal and regulatory proceedings that have been and that may in the future be instituted against the Company and Silver Lake following the announcement of the Merger-Related Transactions, which could delay or prevent the consummation of the Merger, and unfavorable outcome of such legal proceedings;

•the risk that our stock price may decline significantly if the proposed Merger-Related Transactions are not consummated;

•the amount of cash to be paid per share under the Merger Agreement is fixed and will not be adjusted for changes in our business, assets, liabilities, prospects, outlook, financial condition or operating results or in the event of any change in the market price of, analyst estimates of, or projections relating to, our common stock;

•risks associated with Merger-Related Transactions generally, such as the inability to obtain, or delays in obtaining, any required regulatory approvals or other consents; and

•we cannot assure you that our evaluation of strategic alternatives will result in any particular outcome, and the perceived uncertainties related to the Company could adversely affect our business and our stockholders.

We may fail to complete the TKO Asset Acquisition if certain required conditions, many of which are outside our control, are not satisfied.

The completion of the TKO Asset Acquisition is subject to various customary closing conditions, including, but not limited to, (i) the absence of any order, writ, judgment, injunction, decree, ruling, stipulation, directive, assessment, subpoena, verdict, determination or award issued, promulgated or entered, by or with any governmental entity that has the effect of making the TKO Asset Acquisition illegal or otherwise restraining or prohibiting the consummation of the TKO Asset Acquisition, (ii) subject to certain exceptions, the accuracy of the representations and warranties of the parties and (iii) compliance in all material respects by each party with its obligations under the transaction agreement. Despite the parties’ best efforts, we may not be able to satisfy the various closing conditions and obtain the necessary approvals in a timely fashion or at all.

We may fail to complete the OpenBet Acquisition if certain required conditions, many of which are outside our control, are not satisfied.

The completion of the OpenBet Acquisition is subject to various customary closing conditions, including, but not limited to, (i) the expiration of the waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended, (ii) obtaining applicable gaming authority approvals, (iii) the absence of any order or legal requirement that enjoins, restrains or otherwise prevents the consummation of the OpenBet Acquisition, and (iv) the consummation of the pre-closing reorganization contemplated by the OpenBet Acquisition. Despite the parties’ best efforts, we may not be able to satisfy the various closing conditions and obtain the necessary approvals in a timely fashion or at all.

Failure to complete the TKO Asset Acquisition, OpenBet Acquisition or other dispositions we may contemplate could negatively impact our stock price, future business and financial results.

If the TKO Asset Acquisition, OpenBet Acquisition or other dispositions we may contemplate are not completed, we will be subject to several risks, including the following:

•payment for certain costs, whether or not such transaction is completed, such as legal, accounting, financial advisor and printing fees;

•negative reactions from the financial markets, including potential declines in the price of our Class A common stock due to the fact that current prices may reflect a market assumption that the TKO Asset Acquisition, OpenBet Acquisition or other dispositions we announce will be completed;

•diverted attention of our management to the transactions rather than to our operations and pursuit of other opportunities that could have been beneficial to us; and

•negative impact on our future plans.

Risks Related to Our Business

Changes in public and consumer tastes and preferences and industry trends could reduce demand for our services and content offerings and adversely affect our business.

Our ability to generate revenues is highly sensitive to rapidly changing consumer preferences and industry trends, as well as the popularity of the talent, brands, and owners of intellectual property we represent, and the assets we own. Our success depends on our ability to offer premium content through popular channels of distribution that meet the changing preferences of the broad consumer market and respond to competition from an expanding array of choices facilitated by technological developments in the delivery of content. Our operations and revenues are affected by consumer tastes and entertainment trends, including the market demand for the distribution rights to live sports events, which are unpredictable and may be affected by factors such as changes in the social and political climate, global epidemics or general macroeconomic factors. Changes in consumers’ tastes or a change in the perceptions of our brands and business partners, whether as a result of the social and political climate or otherwise, could adversely affect our operating results. Our failure to avoid a negative perception among consumers or anticipate and respond to changes in consumer preferences, including in the form of content creation or distribution, could result in reduced demand for our services and content offerings or those of our clients and owned assets across our platform, which could have an adverse effect on our business, financial condition and results of operations.

Consumer tastes change frequently and it is a challenge to anticipate what offerings will be successful at any point in time. We may invest in our content and owned assets, including in the creation of original content, before learning the extent to which it will achieve popularity with consumers. For example, as of December 31, 2024, we have committed to spending approximately $2.5 billion in guaranteed payments for media, events, experiences or other representation rights and similar expenses, regardless of our ability to profit from these rights. A lack of popularity of these, our other content offerings, or our owned assets, as well as labor disputes, unavailability of a star performer, equipment shortages, cost overruns, disputes with production teams, or adverse weather conditions, could have an adverse effect on our business, financial condition and results of operations.

Our ability to generate revenue from discretionary and corporate spending on entertainment and sports events, such as corporate sponsorships and advertising, is subject to many factors, including many that are beyond our control, such as general macroeconomic conditions.

Our business depends on discretionary consumer and corporate spending. Many factors related to corporate spending and discretionary consumer spending, including economic conditions affecting disposable consumer income such as unemployment levels, fuel prices, interest rates, changes in tax rates, and tax laws that impact companies or individuals and inflation can significantly impact our operating results. While consumer and corporate spending may decline at any time for reasons beyond our control, the risks associated with our businesses become more acute in periods of a slowing economy or recession, which may be accompanied by reductions in corporate sponsorship and advertising, decreases in attendance at live entertainment and sports events, and purchases of pay-per-view ("PPV"), among other things. There can be no assurance that consumer and corporate spending will not be adversely impacted by current economic and geopolitical conditions, or by any future deterioration in such conditions, thereby possibly impacting our operating results and growth. A prolonged period of reduced consumer or corporate spending could have an adverse effect on our business, financial condition, and results of operations.

We may not be able to adapt to or manage new content distribution platforms or changes in consumer behavior resulting from new technologies.

We must successfully adapt to and manage technological advances in our industry, including the emergence of alternative distribution platforms and artificial intelligence. If we are unable to adopt or are late in adopting technological changes and innovations that other entertainment providers offer, it may lead to a loss of consumers viewing our content, a reduction in revenues from attendance at our live events, a loss of ticket sales, or lower ticket fees. It may also lead to a reduction in our clients’ ability to monetize new platforms. Our ability to effectively generate revenue from new distribution platforms and viewing technologies will affect our ability to maintain and grow our business. Emerging forms of content distribution may provide different economic models and compete with current distribution methods (such as television, film, and PPV) in ways that are not entirely predictable, which could reduce consumer demand for our content offerings. We must also adapt to changing consumer behavior driven by advances that allow for time shifting and on-demand viewing, such as digital video recorders and video-on-demand, as well as internet-based and broadband content delivery and mobile devices. If we fail to adapt our distribution methods and content to emerging technologies and new distribution platforms, while also effectively preventing digital piracy and the dilution of the value of our content resulting from the creation of similar or fake content on artificial intelligence applications, our ability to generate revenue from our targeted audiences may decline and could result in an adverse effect on our business, financial condition, and results of operations.

Because our success depends substantially on our ability to maintain a professional reputation, adverse publicity concerning us, one of our businesses, our clients, or our key personnel could adversely affect our business.

Our professional reputation is essential to our continued success and any decrease in the quality of our reputation could impair our ability to, among other things, recruit and retain qualified and experienced agents, managers, and other key personnel, retain or attract clients or customers, or enter into multimedia, licensing, and sponsorship engagements. Our overall reputation may be negatively impacted by a number of factors, including negative publicity concerning us, members of our management or our agents, managers, and other key personnel or individuals that participate in our events. In addition, we are dependent for a portion of our revenues on the relationships between content providers and the clients and key brands, such as sports leagues and federations, that we represent, many of whom are public personalities with large social media followings whose actions generate significant publicity and public interest. Any adverse publicity relating to such individuals or entities that we employ or represent or previously employed or represented, or have a contractual relationship with us or that otherwise occur at our locations or events, or to our company, including, for example, from reported or actual incidents or allegations of illegal or improper conduct, such as harassment, discrimination, or other misconduct, have resulted and could in the future result in significant media attention, even if not directly relating to or involving Endeavor, and could have a negative impact on our professional reputation. This could result in termination of licensing or other contractual relationships, or our employees’ ability to attract new customer or client relationships, or the loss or termination of such employees’ or contractors’ services, all of which could adversely affect our business, financial condition, and results of operations. Our professional reputation could also be impacted by adverse publicity relating to one or more of our owned or majority owned subsidiaries (including TKO), brands, events, or businesses.

We depend on the relationships of our agents, managers, and other key personnel with clients across many categories, including television, film, professional sports, fashion, music, literature, theater, digital, sponsorship and licensing.

We depend upon relationships that our agents, managers, and other key personnel have developed with clients across many content categories, including, among others, television, film, professional sports, fashion, music, literature, theater, digital, sponsorship, and licensing. The relationships that our agents, managers, and other key personnel have developed with studios, brands, and other key business contacts help us to secure access to sponsorships, endorsements, professional contracts, productions, events, and other opportunities for our clients. Due to the importance of those industry contacts to us, a substantial deterioration in these relationships, or substantial loss of agents, managers, or other key personnel who maintain these relationships, could adversely affect our business. In particular, our client management business is dependent upon the highly personalized relationships between our agent and manager teams and their respective clients. A substantial deterioration in the team managing a client may result in a deterioration in our relationship with, or the loss of, the clients represented by that agent or manager. The substantial loss of multiple agents or managers and their associated clients could have an adverse effect on our business, financial condition, and results of operations. Most of our agents, managers, and other key personnel are not party to long-term contracts and, in any event, can leave our employment with little or no notice. We can give no assurance that all or any of these individuals will remain with us or will retain their associations with key business contacts.

Our success depends, in part, on our continuing ability to identify, recruit, and retain qualified and experienced agents and managers. If we fail to recruit and retain suitable agents or if our relationships with our agents change or deteriorate, it could adversely affect our business.

Our success depends, in part, upon our continuing ability to identify, recruit, and retain qualified and experienced agents and managers. There is great competition for qualified and experienced agents and managers in the entertainment and sports industry, and we cannot assure you that we will be able to continue to hire or retain a sufficient number of qualified persons to meet our requirements, or that we will be able to do so under

terms that are economically attractive to us. Any failure to retain certain agents and managers could lead to the loss of sponsorship, multimedia, and licensing agreements, and other engagements and have an adverse effect on our business, financial condition, and results of operations.

Our failure to identify, sign, and retain clients could adversely affect our business.

We derive substantial revenue from the engagements, sponsorships, licensing rights, and distribution agreements entered into by the clients with whom we work. We depend on identifying, signing, and retaining as clients those artists, athletes, models, and businesses whose identities or brands are in high demand by the public and, as a result, are deemed to be favorable candidates for engagements. Our competitive position is dependent on our continuing ability to attract, develop, and retain clients whose work is likely to achieve a high degree of value and recognition as well as our ability to provide such clients with sponsorships, endorsements, professional contracts, productions, events, and other opportunities. Our failure to attract and retain these clients, an increase in the costs required to attract and retain such clients, or an untimely loss or retirement of these clients could adversely affect our financial results and growth prospects. We have not entered into written agreements with many of the clients we represent. These clients may decide to discontinue their relationship with us at any time and without notice. In addition, the clients with whom we have entered into written contracts may choose not to renew their contracts with us on reasonable terms or at all or they may breach or seek to terminate these contracts. If any of our clients decide to discontinue their relationships with us, whether they are under a contract or not, we may be unable to recoup costs expended to develop and promote them and our financial results may be adversely affected. Further, the loss of such clients could lead other of our clients to terminate their relationships with us.

We derive substantial revenue from the sale of multimedia rights, licensing rights, and sponsorships. A significant proportion of this revenue is dependent on our commercial agreements with entertainment and sports events. Our failure to renew or replace these key commercial agreements on similar or better terms could have an adverse effect on our business, financial condition and results of operations.

Our business involves potential internal conflicts of interest due to the breadth and scale of our platform.