Table of Contents

As Filed with the Securities and Exchange Commission on August 12, 2019

Registration No. 333-229613

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 4

TO

FORMF-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

MODERN MEDIA ACQUISITION CORP. S.A.

(Exact name of Registrant as specified in its charter)

| Luxembourg | 7370 | Not Applicable | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

3414 Peachtree Road, Suite 480

Atlanta, Georgia 30326

(404)443-1182

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Lewis W. Dickey, Jr.

President and Chief Executive Officer

3414 Peachtree Road, Suite 480

Atlanta, Georgia 30326

(404)443-1182

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of communications to:

Mitchell S. Nussbaum, Esq. Loeb & Loeb LLP 345 Park Avenue New York, New York 10154 (212)407-4159 | Mark L. Hanson, Esq. Jones Day 1420 Peachtree Street, N.E., Suite 800 Atlanta, Georgia 30309 (404)521-3939 |

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this Registration Statement becomes effective and after all conditions under the Business Transaction Agreement are satisfied or waived.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule13e-4(i) (Cross-Border Issuer Tender Offer) ☐

Exchange Act Rule14d-1(d) (Cross-Border Third-Party Tender Offer) ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the Securities and Exchange Commission declares our registration statement effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction or state where the offer or sale is not permitted.

SUBJECT TO COMPLETION DATED AUGUST 12, 2019

PROXY STATEMENT FOR SPECIAL MEETING OF STOCKHOLDERS OF

MODERN MEDIA ACQUISITION CORP.

AND PROSPECTUS FOR ORDINARY SHARES AND WARRANTS

OF MODERN MEDIA ACQUISITION CORP. S.A.

Proxy Statement/Prospectus dated , 2019

and first mailed to Modern Media Acquisition Corp. stockholders on or about , 2019

To the Stockholders of Modern Media Acquisition Corp.:

You are cordially invited to attend the Special Meeting of the Stockholders of Modern Media Acquisition Corp. (“MMAC”), which will be held at , Eastern time, on , 2019, at (the “Special Meeting”).

MMAC has entered into a business transaction agreement, dated as of January 24, 2019 (as amended, the “Business Transaction Agreement”), which provides for a business combination (the “Business Combination”) between MMAC and Akazoo Limited, a private company limited by shares incorporated under the laws of Scotland (“Akazoo”). The Business Combination is structured to efficiently combine the assets and businesses of MMAC and Akazoo into one new, publicly traded entity. The Business Combination will result in (1) stockholders of MMAC, equityholders of Akazoo and certain other equity investors together holding all of the outstanding Ordinary Shares of PubCo (as defined below) and (2) Akazoo becoming a wholly owned subsidiary of PubCo.

Pursuant to the Business Transaction Agreement, the Business Combination will be effected in three steps: (i) subject to the approval and adoption of the Business Transaction Agreement by the stockholders of MMAC, MMAC will merge with and into Modern Media Acquisition Corp. S.A., a Luxembourg public limited company (société anonyme) (“PubCo”), with PubCo remaining as the surviving publicly traded entity (the “Merger”); (ii) Unlimited Music S.A., a Luxembourg public limited company (société anonyme) (“LuxCo”), will acquire the entire issued share capital of Akazoo in consideration for issuing ordinary shares of LuxCo (“LuxCo Shares”) to the Akazoo shareholders (the “Share Exchange”) and (iii) LuxCo will merge with and into PubCo, with PubCo remaining as the surviving publicly traded entity (the “Luxembourg Merger”). In addition to other customary closing conditions discussed herein, consummation of the Business Combination is conditioned upon there being not less than $53 million available between MMAC’s trust account and any additional capital otherwise available to MMAC at the time of consummation of the Business Combination, although such condition may be waived by Akazoo. As of June 30, 2019, MMAC had approximately $14.7 million in cash in its trust account. Given the amount currently in MMAC’s trust account, PubCo is in the process of securing binding commitments to purchase PubCo Units (as defined below) in a private placement offering on terms agreed to by the parties to the Business Transaction Agreement such that, together with cash available in MMAC’s trust account, PubCo would have at least an aggregate of $53 million of available cash after consummation of the Business Combination and the offering, before payment of any fees and expenses (such private placement offering, the “PIPE Financing”). The PIPE Financing is described in more detail in this proxy statement/prospectus. Based upon subscriptions and indications of interest received to date, MMAC and PubCo expect to successfully complete the PIPE Financing and the Business Combination. In addition, Akazoo may choose to waive the minimum cash condition. Nevertheless, there is no guarantee that the PIPE Financing or the other closing conditions will be satisfied or waived before September 17, 2019, the date on which MMAC must begin to liquidate its trust account pursuant to its Second Amended and Restated Certificate of Incorporation (the “MMAC Certificate of Incorporation”).

At the Special Meeting, MMAC stockholders will be asked to consider and vote upon a proposal, which is referred to herein as the “Business Combination Proposal,” to approve the Business Combination by the approval and adoption of the Business Transaction Agreement.

If MMAC stockholders approve the Business Combination Proposal and the parties consummate the Business Combination:

| (i) | Immediately prior to the consummation of the Merger, each MMAC right (“MMAC Rights”) entitling the holder to receiveone-tenth (1/10) of one share of MMAC’s common stock, par value $0.0001 per share (“MMAC Common Stock”) will be automatically converted into such fraction of MMAC Common Stock in accordance with the rights agreement governing such MMAC Rights; and |

| (ii) | Upon the consummation of the Merger: |

| a. | Each share of MMAC Common Stock issued and outstanding immediately prior to the effective time of the Merger (including shares that were automatically issued to holders of MMAC Rights pursuant to the conversion of such rights immediately prior to the Merger but excluding any redeemed shares), will convert into the right to receive one ordinary share of PubCo (a “PubCo Ordinary Share”); and |

| b. | Each warrant to purchase MMAC Common Stock (“MMAC Warrants”) (or portion thereof) issued and outstanding immediately prior to effective time of the Merger will convert into a warrant to purchase one PubCo Ordinary Share (each, a “PubCo Warrant”) (or equivalent portion thereof). The PubCo Warrants will have and will be subject to substantially the same terms and conditions set forth in the MMAC Warrants. |

i

Table of Contents

Immediately prior to the consummation of the Business Combination, all outstanding units of MMAC (each of which consists of one share of MMAC Common Stock, one MMAC Right andone-half of one MMAC Warrant) (the “MMAC Units”) will separate into their individual components of MMAC Common Stock, MMAC Rights and MMAC Warrants and will cease separate existence and trading.

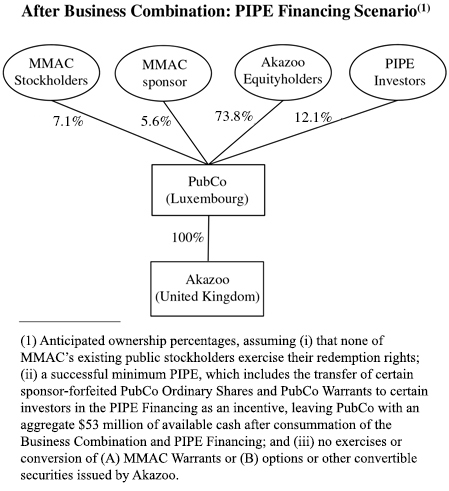

It is anticipated that, upon the consummation of the Business Combination and PIPE Financing on its expected terms, PubCo will issue up to 49,044,831 PubCo Ordinary Shares and 17,670,000 PubCo Warrants. Of these securities, MMAC’s existing stockholders, including the sponsor (as defined herein), would hold an ownership interest of approximately 6,297,374 PubCo Ordinary Shares (approximately 12.8% of the issued and outstanding PubCo Ordinary Shares), Akazoo’s current equityholders would own an ownership interest of approximately 36,196,428 PubCo Ordinary Shares (approximately 73.8% of the issued and outstanding PubCo Ordinary Shares) and the equity investors purchasing PubCo Ordinary Shares in the PIPE Financing would own an ownership interest of approximately 5,926,029 PubCo Ordinary Shares (approximately 12.1% of the issued and outstanding PubCo Ordinary Shares). These relative percentages assume that none of MMAC’s existing public stockholders exercise their redemption rights, as discussed herein, and assume a successful PIPE Financing which includes the transfer of certain sponsor-forfeited PubCo Ordinary Shares and PubCo Warrants to certain investors in the PIPE Financing as an incentive, leaving PubCo with an aggregate $53 million of available cash after consummation of the Business Combination and PIPE Financing, before payment of any fees and expenses. These percentages also do not include any exercise or conversion of (i) MMAC Warrants or (ii) options or other convertible securities issued by Akazoo. Pursuant to the Business Transaction Agreement, the number of PubCo Ordinary Shares that Akazoo’s current equityholders will also receive in the Business Combination is the quotient of (A) the Akazoo Enterprise Value, divided by (B) the Per Share Redemption Amount (each, as defined in the Business Transaction Agreement).

If any of MMAC’s existing public stockholders exercise their redemption rights, the anticipated percentage ownership of MMAC’s existing stockholders will be reduced.

In addition to being asked to approve the Business Combination Proposal, MMAC stockholders will also be asked to consider and vote upon a proposal relating to adjournment of the Special Meeting under certain circumstances, which is more fully described in this proxy statement/prospectus.

The MMAC Units, MMAC Common Stock, MMAC Rights and MMAC Warrants are currently listed on the NASDAQ Capital Market under the symbols “MMDMU,” “MMDM,” “MMDMR” and “MMDMW,” respectively. PubCo intends to apply to list the PubCo Ordinary Shares and PubCo Warrants on the NASDAQ Stock Market under the symbols “SONG” and “SONGW,” respectively, in connection with the closing of the Business Combination. MMAC cannot assure you that the PubCo Ordinary Shares and PubCo Warrants will be approved for listing on NASDAQ.

Investing in PubCo securities involves a high degree of risk. See “Risk Factors” beginning on page 35 for a discussion of information that should be considered in connection with an investment in PubCo securities.

Pursuant to the MMAC Certificate of Incorporation, MMAC is providing its public stockholders with the opportunity to redeem all or a portion of their shares of MMAC Common Stock at aper-share price, payable in cash, equal to the aggregate amount then on deposit in MMAC’s trust account as of two business days prior to the consummation of the Business Combination, including interest, less taxes payable, divided by the number of then outstanding shares of MMAC Common Stock that were sold as part of the MMAC Units in MMAC’s initial public offering (“IPO”), which are referred to collectively as “public shares,” subject to the limitations described herein.

On May 17, 2017, MMAC completed its initial public offering (“IPO”). In connection with its IPO, MMAC issued 20,700,000 public shares for gross proceeds to MMAC from the IPO totaling $207,000,000. After taking into account the concurrent sale of MMAC Warrants in a private placement and certain fees and expenses, the total amount deposited in the trust account totaled $209,070,000.

In connection with MMAC’s February 2019 stockholder vote to extend the date by which MMAC must consummate a business combination from February 17, 2019 to June 17, 2019 (the “First Extension”), public stockholders had the opportunity to redeem all or a portion of their public shares. In connection with the First Extension, a total of 5,942,681 public shares were redeemed for a total amount of approximately $61 million. Following the completion of such redemptions, MMAC had approximately $152 million in cash remaining in the trust account and 14,757,319 public shares issued and outstanding.

On June 14, 2019, at a special meeting of the stockholders of MMAC, the stockholders approved a further extension of the date by which MMAC must consummate a business combination from June 17, 2019 to September 17, 2019 (the “Second Extension”).

In connection with the approval of the Second Extension, stockholders elected to redeem an aggregate of 13,350,654 public shares. Following the completion of such redemptions, MMAC had approximately $14.7 million in cash remaining in the trust account and 6,581,665 shares of common stock issued and outstanding.

MMAC estimates that theper-share price at which public shares may be redeemed from cash held in the trust account will be approximately $10.35 at the time of the Special Meeting. Public stockholders may elect to redeem their shares even if they vote for the Business Combination Proposal or do not vote at all.

Holders of outstanding MMAC Warrants and MMAC Rights do not have redemption rights in connection with the Business Combination.

ii

Table of Contents

MMAC is providing this proxy statement/prospectus and accompanying proxy card to its stockholders in connection with the solicitation of proxies to be voted at the Special Meeting and at any adjournments or postponements of the Special Meeting. This proxy statement/prospectus is also being provided to persons who as at the date hereof hold equity securities, options or otherwise rights to be issued equity securities in the share capital of Akazoo, or LuxCo, as the case may be (“Akazoo equityholders”), as a prospectus in connection with their receipt of PubCo Ordinary Shares in the Business Combination.

Whether or not you plan to attend the Special Meeting, you are urged to read this proxy statement/prospectus (and any documents incorporated into this proxy statement/prospectus by reference) carefully and vote your shares of MMAC Common Stock using the accompanying proxy card.

MMAC’s board of directors (the “Board”) has approved the Business Combination and the Business Transaction Agreement and recommends that MMAC’s stockholders vote FOR each of the proposals to be presented to at the Special Meeting. When you consider the Board’s recommendation of these proposals, you should keep in mind that MMAC’s directors and officers have interests in the Business Combination that may conflict or differ from with your interests as a stockholder. See the section entitled “Proposal I — Approval of the Business Transaction Agreement and the Business Combination — Interests of MMAC Directors and Officers in the Business Combination”

Approval of the Business Combination Proposal requires the affirmative vote of holders of a majority of the outstanding shares of MMAC Common Stock. Approval of the adjournment proposal requires the affirmative vote of the holders of a majority of the shares of MMAC Common Stock represented in person or by proxy and entitled to vote thereon at the Special Meeting. The Board has already approved the Business Transaction Agreement and the Business Combination.

MMAC has no specified maximum redemption threshold under the MMAC Certificate of Incorporation. It is a condition to closing under the Business Transaction Agreement, however, that MMAC has, in the aggregate, not less than $53.0 million of available cash in MMAC’s trust account or additional capital otherwise available upon the consummation of the Business Combination. Given the amount currently in MMAC’s trust account, PubCo is in the process of securing binding commitments for the PIPE Financing to satisfy this condition, without which Akazoo will not be required to consummate the Business Combination, although Akazoo may waive this condition. In the event that Akazoo waives this condition, MMAC does not intend to seek additional stockholder approval or to extend the time period in which its public stockholders can exercise their redemption rights. In no event, however, will MMAC redeem more than approximately 445,850 (32%) of its currently outstanding public shares because redeeming more than that amount would cause its net tangible assets to be less than $5,000,001. The redemption thresholds discussed above are estimates for illustration only, and are based on an implied share price of $10.35 per share of MMAC Common Stock. Accordingly, if Akazoo determines to waive the condition that MMAC has, in the aggregate, not less than $53.0 million of available cash at the time of the Business Combination, then the parties may determine to consummate the Business Combination even if redemptions reduce MMAC’s net tangible assets to as low as $5,000,001. MMAC intends to notify MMAC stockholders by press release on or before consummation of the Business Combination that it has secured sufficient binding commitments for the PIPE Financing to satisfy the minimum cash condition under the Business Transaction Agreement or that Akazoo has otherwise waived this condition.

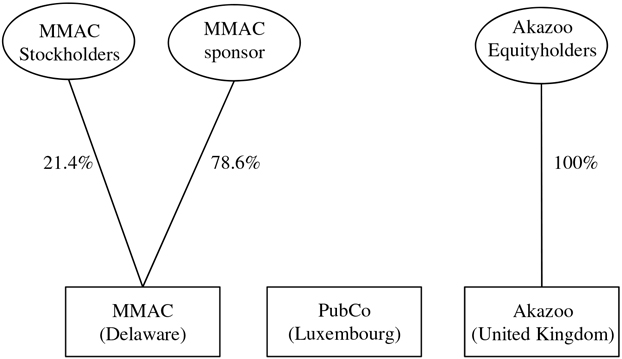

The sponsor and MMAC’s executive officers and independent directors have agreed to vote their shares of MMAC Common Stock in favor of the Business Combination Proposal. As of the date hereof, such persons are entitled to vote 5,175,000 shares of MMAC Common Stock, representing approximately 78.6% of all outstanding shares of MMAC Common Stock. Accordingly, stockholder approval of the Business Combination Proposal is assured. See “Special Meeting of MMAC Stockholders” and “Certain Agreements Related to the Business Combination – Voting Agreement.”

Your vote is very important. If you are a holder of record, you must vote by submitting the enclosed proxy card. Please vote as soon as possible to ensure that your vote is counted, regardless of whether you expect to attend the Special Meeting in person. Please complete, sign, date and return the enclosed proxy card in the postage-paid envelope provided.

If you hold your shares in “street name” through a bank, broker or other nominee, you will need to follow the instructions provided to you by your bank, broker or other nominee to ensure that your shares are represented and voted at the Special Meeting.

If you sign, date and return your proxy card without indicating how you wish to vote, your proxy will be voted in favor of each of the proposals presented at the Special Meeting. If you fail to return your proxy card or fail to instruct your bank, broker or other nominee how to vote, and do not attend the Special Meeting in person, the effect will be that your shares will not be counted for purposes of determining whether a quorum is present at the Special Meeting of stockholders and, if a quorum is present, will have the effect of a vote against the Business Combination Proposal and no effect on the adjournment proposal. If you are a stockholder of record and you attend the Special Meeting and wish to vote in person, you may withdraw your proxy and vote in person.

On behalf of the Board, I thank you for your support and we look forward to the successful consummation of the Business Combination.

iii

Table of Contents

Sincerely, |

Lewis W. Dickey, Jr. |

President, Chief Executive Officer and Chairman |

Neither the Securities and Exchange Commission nor any state securities commission has determined if this attached proxy statement/prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

iv

Table of Contents

Modern Media Acquisition Corp.

3414 Peachtree Road, Suite 480

Atlanta, Georgia 30326

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON , 2019

TO THE STOCKHOLDERS OF MODERN MEDIA ACQUISITION CORP.:

NOTICE IS HEREBY GIVEN that a Special Meeting of Stockholders of Modern Media Acquisition Corp., a Delaware corporation (“MMAC”), will be held at on , 2019 at (the “Special Meeting”), for the purpose of considering and acting upon the following proposals:

| I. | The Business Combination Proposal—to approve the adoption of the Business Transaction Agreement, dated as of January 24, 2019 (as amended, the “Business Transaction Agreement”) which provides for a business combination (the “Business Combination”) between MMAC and Akazoo Limited, a private company limited by shares incorporated under the laws of Scotland (“Akazoo”). Pursuant to the Business Transaction Agreement, the Business Combination will be effected in three steps: (i) MMAC will merge with and into Modern Media Acquisition Corp. S.A., a Luxembourg public limited company (société anonyme) (“PubCo”), with PubCo remaining as the surviving publicly traded entity (the “Merger”); (ii) Unlimited Music S.A., a Luxembourg public limited company (société anonyme) (“LuxCo”), will acquire the entire issued share capital of Akazoo in consideration for issuing ordinary shares of LuxCo (“LuxCo Shares”) to the Akazoo shareholders (the “Share Exchange”) and (iii) LuxCo will merge with and into PubCo, with PubCo remaining as the surviving publicly traded entity (the “Luxembourg Merger”). |

| II. | The Adjournment Proposal—to consider and vote upon a proposal to adjourn the Special Meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies in the event that, based upon the tabulated vote at the time of the Special Meeting, MMAC would not have been authorized to consummate the Business Combination (the “Adjournment Proposal”); and |

| III. | Such other business as may properly come before the meeting or any adjournment or postponement thereof. |

These proposals are described in the accompanying proxy statement/prospectus which you are urged to read in its entirety before voting.

The MMAC Board of Directors (the “Board”) has fixed the close of business on August 9, 2019, as the record date (the “Record Date”) for the determination of stockholders entitled to notice of and to vote at the Special Meeting and at any adjournment thereof. A list of the stockholders entitled to vote as of the Record Date at the Special Meeting will be open to the examination of any stockholder, for any purpose germane to the meeting, during ordinary business hours for a period of ten calendar days before the Special Meeting at the offices of MMAC, 3414 Peachtree Road, Suite 480, Atlanta, Georgia 30326, telephone number of (404)443-1182, General Counsel and Assistant Secretary: Adam Kagan, and at the time and place of the Special Meeting during the duration of the Special Meeting.

If MMAC does not consummate a business combination on or before September 17, 2019, and that date is not otherwise extended by MMAC’s stockholders, MMAC would be required to distribute the proceeds held in trust to its stockholders in accordance with the MMAC Certificate of Incorporation.

MMAC does not expect to transact any other business at the Special Meeting, except for business properly brought before the Special Meeting, or any adjournment or postponement thereof, by the Board.

Each MMAC stockholder who holds public shares of MMAC Common Stock has the right, regardless of such stockholder’s vote on the Business Combination Proposal, to demand that MMAC redeem such stockholder’s shares for aper-share price, payable in cash, equal to the aggregate amount then on deposit in the trust account as of two business days prior to the vote on the Business Combination Proposal, including interest earned on the trust account deposits (which interest shall be net of taxes payable), divided by the number of then outstanding public shares.

i

Table of Contents

MMAC estimates that theper-share price at which public shares may be redeemed from cash held in the trust account will be approximately $10.35 at the time of the Special Meeting. In no event will MMAC redeem its public shares in an amount that would cause MMAC’s net tangible assets to be less than $5,000,001 (so that MMAC is not subject to the SEC’s “penny stock” rules).

MMAC’s initial stockholders prior to the IPO, including the sponsor (collectively, the “initial stockholders”) have waived their rights to liquidating distributions from the trust account with respect to their shares of MMAC Common Stock acquired prior to the IPO (“founder shares”). As a consequence of such waivers, any liquidating distribution that is made will be only with respect to the public shares. There will be no distribution from the trust account with respect to MMAC Rights or MMAC Warrants, which will expire worthless in the event MMAC winds up.

Please sign, date and return your proxy card as soon as possible to make sure that your shares are represented at the Special Meeting. If you are a stockholder of record of MMAC Common Stock, you may also cast your vote in person at the Special Meeting. If your shares of MMAC Common Stock are held in an account at a brokerage firm or bank, you must instruct your broker or bank on how to vote your shares.

For purposes of the Business Combination Proposal, under the MMAC Certificate of Incorporation, approval of the Business Combination Proposal will require the affirmative vote of a majority of the shares of outstanding MMAC Common Stock. It is a condition to closing under the Business Transaction Agreement, however, that MMAC has, in the aggregate, not less than $53,000,000 of available cash upon the consummation of the Business Combination. Given the amount currently in MMAC’s trust account, PubCo is in the process of securing binding commitments for the PIPE Financing to satisfy this condition, without which Akazoo will not be required to consummate the Business Combination, although such condition may be waived by Akazoo. Accordingly, if Akazoo determines to waive the condition that MMAC has, in the aggregate, not less than $53.0 million of available cash at the time of the Business Combination, then the parties may determine to consummate the Business Combination, and in that case, redemptions could reduce MMAC’s net tangible assets to as low as $5,000,001. MMAC intends to notify MMAC stockholders by press release on or before consummation of the Business Combination that it has secured sufficient binding commitments for the PIPE Financing to satisfy the minimum cash condition under the Business Transaction Agreement or that Akazoo has otherwise waived this condition.

Since the Business Combination Proposal requires approval by a majority of the shares of outstanding MMAC Common Stock, abstentions or brokernon-votes will count as votes “AGAINST” the Business Combination Proposal. The holders of all founder shares have agreed to vote their shares of MMAC Common Stock owned or acquired by them during or after MMAC’s IPO in favor of the Business Combination Proposal. As of the date hereof, such persons are entitled to vote 5,175,000 shares of MMAC Common Stock, representing approximately 78.6% of all outstanding shares of MMAC Common Stock. Accordingly, stockholder approval of the Business Combination Proposal is assured. See “Special Meeting of MMAC Stockholders” and “Certain Agreements Related to the Business Combination – Voting Agreement.”

For purposes of the Adjournment Proposal, approval requires the affirmative vote of the holders of a majority of the shares of MMAC Common Stock represented in person or by proxy and entitled to vote at the Special Meeting.

WHETHER YOU PLAN TO ATTEND THE SPECIAL MEETING OR NOT, PLEASE SIGN, DATE AND RETURN THE ENCLOSED PROXY CARD AS SOON AS POSSIBLE IN THE ENVELOPE PROVIDED. IF YOU RETURN YOUR PROXY CARD WITHOUT AN INDICATION OF HOW YOU DESIRE TO VOTE, SINCE IT IS NOT AN AFFIRMATIVE VOTE IN FAVOR OF A RESPECTIVE PROPOSAL, IT: (I) WILL HAVE THE EFFECT OF A VOTE “AGAINST” THE BUSINESS COMBINATION PROPOSAL AND (II) WILL HAVE NO EFFECT ON THE VOTE REGARDING THE ADJOURNMENT PROPOSAL.

SUCH A VOTE WILL NOT HAVE THE EFFECT OF EXERCISING YOUR RIGHT TO REQUIRE MMAC TO REDEEM YOUR SHARES FOR A PRO RATA PORTION OF THE TRUST ACCOUNT IN WHICH A SUBSTANTIAL PORTION OF THE NET PROCEEDS OF MMAC’S IPO ARE HELD (IN ORDER FOR A STOCKHOLDER TO EXERCISE HIS OR HER RIGHT TO HAVE HIS OR HER SHARES REDEEMED, HE OR SHE MUST FOLLOW THE REDEMPTION PROCEDURES SET FORTH IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS).

SEE THE SECTION ENTITLED “RISK FACTORS” BEGINNING ON PAGE 35 FOR A DISCUSSION OF VARIOUS FACTORS THAT YOU SHOULD CONSIDER IN CONNECTION WITH THE BUSINESS COMBINATION.

The accompanying proxy statement/prospectus incorporates important business and financial information about MMAC that is not included in or delivered with this document. This information is available without charge to security holders upon written or oral request. The request should be sent to: the offices of MMAC, 3414 Peachtree Road, Suite 480, Atlanta, Georgia 30326, telephone number of (404)443-1182, Attention: General Counsel and Assistant Secretary Adam Kagan.

ii

Table of Contents

To obtain timely delivery of requested materials, security holders must request the information no later than five days before the date they submit their proxies or attend the Special Meeting. The latest date to request the information to be received timely is , 2019.

This proxy is being solicited on behalf of the Board, and MMAC will pay all costs of preparing, assembling and mailing the proxy materials. In addition to mailing out proxy materials, MMAC’s officers may solicit proxies by telephone or fax, without receiving any additional compensation for their services. MMAC has engaged the services of a professional proxy solicitation agent. Brokers, banks and other fiduciaries are requested to forward proxy materials to the beneficial owners of MMAC’s Common Stock.

The Solicitation Agent for the Special Meeting is:

Morrow Sodali LLC

You may obtain information regarding the Special Meeting

from the Solicitation Agent as follows:

470 West Avenue

Stamford, CT 06902

Tel: (800) 662-5200

Email: MMDM.info@morrowsodali.com

Banks and Brokerage Firms, please call: (203) 658-9400

The Board of Directors of Modern Media Acquisition Corp. unanimously recommends that you vote “FOR” Proposal I, the Business Combination Proposal, and “FOR” Proposal II, the Adjournment Proposal.

| By Order of the Board of Directors, |

| Lewis W. Dickey, Jr. |

President, Chief Executive Officer and Chairman , 2019 |

iii

Table of Contents

Table of Contents

ABOUT THIS PROXY STATEMENT/PROSPECTUS

This document, which forms part of a registration statement on FormF-4 filed by PubCo (File No. 333-229613) with the U.S. Securities and Exchange Commission (“SEC”), constitutes a prospectus of PubCo under Section 5 of the U.S. Securities Act of 1933, as amended (the “Securities Act”) with respect to the PubCo Ordinary Shares to be issued to MMAC stockholders and to Akazoo equityholders, as well as the PubCo Warrants to be issued to holders of MMAC Warrants and the PubCo Ordinary Shares underlying such PubCo Warrants, if the Business Combination is consummated. This document also constitutes a notice of meeting and a proxy statement under Section 14(a) of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”), with respect to the Special Meeting of MMAC stockholders at which MMAC stockholders will be asked to consider and vote upon a proposal to approve the Business Combination by the approval and adoption of the Business Transaction Agreement, among other matters.

This proxy statement/prospectus does not constitute an offer to sell, or a solicitation of an offer to buy, any securities, or the solicitation of a proxy, in any jurisdiction to or from any person to whom it is not lawful to make any such offer or solicitation in such jurisdiction.

WHERE YOU CAN FIND MORE INFORMATION

As a foreign private issuer, PubCo will be required to file its Annual Report on Form20-F with the SEC no later than 120 days following its fiscal year end. MMAC files reports, proxy statements and other information with the SEC as required by the Exchange Act. You can read MMAC’s SEC filings, including this proxy statement/prospectus, over the Internet at the SEC’s website at http://www.sec.gov. You may also read and copy any document MMAC files with the SEC at the SEC public reference room located at 100 F Street, N.E., Room 1580 Washington, D.C., 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at1-800-SEC-0330. You may also obtain copies of the materials described above at prescribed rates by writing to the SEC, Public Reference Section, 100 F Street, N.E., Washington, D.C. 20549.

Information and statements contained in this proxy statement/prospectus, or any annex to this proxy statement/prospectus, are qualified in all respects by reference to the copy of the relevant contract or other annex filed with this proxy statement/prospectus.

If you would like additional copies of this proxy statement/prospectus, or if you have questions about the Business Combination, you should contact MMAC’s proxy solicitor, Morrow Sodali, at (800) 662-5200 or by sending an e-mail to MMDM.info@morrowsodali.com.

All information contained in this proxy statement/prospectus relating to MMAC has been supplied by MMAC, and all such information relating to Akazoo, LuxCo or PubCo has been supplied by Akazoo. Information provided by either of MMAC or Akazoo does not constitute any representation, estimate or projection of the other party.

Neither MMAC, PubCo nor Akazoo has authorized anyone to give any information or make any representation about the Business Combination or their companies that is different from, or in addition to, that contained in this proxy statement/prospectus or in any of the materials that have been incorporated into this proxy statement/prospectus by reference. Therefore, if anyone does give you any such information, you should not rely on it. If you are in a jurisdiction where offers to exchange or sell, or solicitations of offers to exchange or purchase, the securities offered by this proxy statement/prospectus or the solicitation of proxies is unlawful, or if you are a person to whom it is unlawful to direct these types of activities, then the offer presented in this proxy statement/prospectus does not extend to you. The information contained in this proxy statement/prospectus speaks only as of the date of this proxy statement/prospectus unless the information specifically indicates that another date applies.

1

Table of Contents

IMPORTANT INFORMATION ABOUT IFRS ANDNON-IFRS FINANCIAL MEASURES

Akazoo’s audited financial statements are prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (the “IASB”). Akazoo refers in various places within this proxy statement/prospectus to EBITDA, EBITDA Margin, Adjusted Gross Profit and Free Cash Flow which arenon-IFRS measures. EBITDA is defined as Net Income before Net finance costs, Income tax expense and Depreciation and amortization. EBITDA Margin is a financial measure not prepared in accordance with IFRS and is defined as EBITDA as a percentage of Revenue. Adjusted Gross Profit is defined as Gross Profit with Media Costs added back to it. Free Cash Flow is defined as net cash from operating activities less capital expenditures. These measures are more fully explained in “Management’s Discussion and Analysis of Financial Condition and Results of Operations ofAkazoo—Non-IFRS Financial Measures.” The presentation of thisnon-IFRS information is not meant to be considered in isolation or as a substitute for Akazoo’s consolidated financial results prepared in accordance with IFRS.

In this proxy statement/prospectus, Akazoo relies on and refers to information and statistics regarding the markets in which it competes and other industry data. Akazoo obtained this information and these statistics from third-party sources, including reports by market research firms, such as the International Federation of the Phonographic Industry (“IFPI”), the GSM Association (“GSMA”) and MiDia Research, as well as financial firms. Akazoo has supplemented this information where necessary with its own internal estimates and information obtained from discussions with its customers, taking into account publicly available information about other industry participants and its management’s best view as to information that is not publicly available.

2

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This proxy statement/prospectus contains a number of forward-looking statements, including statements about the financial conditions, results of operations, earnings outlook and prospects of PubCo, Akazoo and/or MMAC and may include statements for the period following the consummation of the proposed business combination. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Forward-looking statements are typically identified by words such as “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements are based on the current expectations of the management of MMAC and Akazoo, as applicable, and are inherently subject to uncertainties and changes in circumstance and their potential effects and speak only as of the date of such statement. There can be no assurance that future developments will be those that have been anticipated. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described in “Risk Factors,” those discussed and identified in public filings made with the SEC by MMAC and the following:

| • | expectations regarding Akazoo’s strategies and future financial performance, including Akazoo’s future business plans or objectives, prospective performance and opportunities, and competitors, revenues, customer acquisition and retention, products and services, pricing, marketing plans, operating expenses, market trends, liquidity, cash flows and uses of cash, capital expenditures, and Akazoo’s ability to maintain access to content and manage license relationships, and to invest in growth initiatives and pursue acquisition opportunities; |

| • | the occurrence of any event, change or other circumstances that could give rise to the termination of the Business Transaction Agreement; |

| • | the outcome of any legal proceedings that may be instituted against Akazoo, MMAC and others following announcement of the Business Transaction Agreement and transactions contemplated therein; |

| • | the inability to complete the transactions contemplated by the Business Transaction Agreement due to the failure to secure sufficient binding commitments for the PIPE Financing or to satisfy other conditions necessary to consummate the Business Combination; |

| • | the risk that the proposed Business Combination disrupts current plans and operations of Akazoo as a result of the announcement and consummation of the transactions contemplated by the Business Transaction Agreement; |

| • | the ability to recognize the anticipated benefits of the combination of Akazoo and MMAC; |

| • | costs related to the proposed Business Combination; |

| • | the amount of any redemptions by holders of MMAC Common Stock; |

| • | the concentration of voting power among MMAC and Akazoo’s major shareholders who have had substantial control over the respective companies and will continue to have substantial control over PubCo; |

| • | the sources and uses of cash; |

| • | the management and board composition of PubCo following the proposed Business Combination; |

| • | the successful initial listing and continued listing of PubCo’s securities on NASDAQ; |

| • | the limited liquidity and trading of MMAC’s and PubCo’s securities; |

| • | geopolitical risk and changes in applicable laws or regulations in Akazoo’s varying markets; |

3

Table of Contents

| • | the possibility that Akazoo and/or MMAC may be adversely affected by other economic, business, and/or competitive factors; |

| • | financial performance; |

| • | operational risk; |

| • | litigation and regulatory enforcement risks, including the diversion of management time and attention and the additional costs and demands on Akazoo’s resources; |

| • | fluctuations in exchange rates between the foreign currencies in which Akazoo typically does business and the Euro; and |

| • | the risks that the consummation of the Business Combination is substantially delayed or does not occur. |

Should one or more of these risks or uncertainties materialize, or should any of the assumptions made by the management of MMAC and Akazoo prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements.

All subsequent written and oral forward-looking statements concerning the business combination or other matters addressed in this proxy statement/prospectus and attributable to Akazoo or MMAC or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this proxy statement/prospectus. Except to the extent required by applicable law or regulation, PubCo, Akazoo and MMAC undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date of this proxy statement/prospectus or to reflect the occurrence of unanticipated events.

4

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE BUSINESS COMBINATION AND THE SPECIAL MEETING

The following questions and answers briefly address some commonly asked questions about the Business Combination and the proposals to be presented at the Special Meeting. These questions and answers do not include all the information that be important to stockholders. MMAC stockholders are encouraged to read carefully this entire proxy statement/prospectus, including the Annex and other documents referred to herein.

Who is Modern Media Acquisition Corp.?

Modern Media Acquisition Corp. (“MMAC”) is a blank check company formed in 2014 for the purpose of entering into a merger, share exchange, asset acquisition, stock purchase, recapitalization, reorganization or other similar business combination with one or more businesses or entities in the media, entertainment or marketing services industries. In May 2017, MMAC consummated its IPO from which it derived gross proceeds of $207,000,000, which were placed in a trust account.

Who is PubCo?

Modern Media Acquisition Corp. S.A. (“PubCo”) is a newly formed Luxembourg public limited company (société anonyme), formed to facilitate the Business Combination. Upon the consummation of the transactions contemplated by the Business Combination (i) MMAC will merge with and into PubCo, with PubCo as the surviving publicly traded entity and (ii) Akazoo will become a wholly owned subsidiary of LuxCo through the Share Exchange and LuxCo will then merge with and into PubCo, such that Akazoo continues as a wholly owned subsidiary of PubCo. PubCo intends to apply to have its ordinary shares and warrants (“PubCo Ordinary Shares” and “PubCo Warrants”, respectively) listed on NASDAQ under the symbols “SONG” and “SONGW,” respectively.

MMAC and Akazoo agreed that PubCo would be incorporated in, and operate out of, Luxembourg to facilitate PubCo’s ongoing business operations. Specifically, as Akazoo currently generates, and PubCo expects to generate in the future, most of its revenue in Euros, it is important for the company to be based in a jurisdiction in the European Union. Given the economic and financial uncertainties surrounding the United Kingdom’s currently contemplated exit from the European Union, the parties believe that Akazoo’s current jurisdiction of incorporation does not provide the necessary long-term stability for PubCo’s operations. Furthermore, one of Akazoo’s key competitors that currently has U.S. publicly traded equity is incorporated in Luxembourg. The parties believe that, all else being equal, incorporating PubCo in Luxembourg would strengthen the appeal of PubCo Ordinary Shares in the U.S. equity market because the market is already comfortable with a similar company in the same space.

Who is Akazoo?

Akazoo Limited (“Akazoo”) is a private company limited by shares incorporated under the laws of Scotland that provides online media streaming services to customers in developing markets.

Who is LuxCo?

Unlimited Music S.A. (“LuxCo”), a Luxembourg public limited company (société anonyme), was formed to facilitate the merger of Akazoo with PubCo. As part of the Business Combination, LuxCo will acquire the entire issued share capital of Akazoo in consideration for issuing, on a 100-for-1 basis, LuxCo shares (“LuxCo Shares”) to the Akazoo shareholders (the “Share Exchange”), such that the shareholdings of LuxCo will be identical immediately following the Share Exchange to that of Akazoo prior to the Share Exchange; and on the calendar day following the effective date of the MMAC’s merger with and into PubCo, LuxCo will merge (the “Luxembourg Merger”) with and into PubCo in accordance with Luxembourg law, with PubCo remaining as the surviving publicly traded entity. In connection with the Luxembourg Merger, PubCo will issue 0.072803 PubCo Ordinary Shares for each LuxCo ordinary share then outstanding (assuming no redemptions of MMAC Common Stock). This transaction will result in Akazoo becoming a wholly owned subsidiary of PubCo.

Why am I receiving this proxy statement?

MMAC, Akazoo and PubCo have agreed to a transaction under the terms of a Business Transaction Agreement dated as of January 24, 2019 (as amended, the “Business Transaction Agreement”), pursuant to which MMAC and Akazoo will combine their businesses with PubCo, with PubCo remaining as the surviving publicly traded entity and Akazoo continuing as a wholly owned subsidiary of PubCo (the “Business Combination”). A copy of the Business Transaction Agreement, as amended is attached to this proxy statement/prospectus as “Annex A,” which we encourage you to review in its entirety.

The Business Combination is structured such that MMAC and LuxCo will each merge with and into PubCo, with PubCo remaining as the surviving publicly traded entity and Akazoo continuing as a wholly owned subsidiary of PubCo. If the stockholders of MMAC approve the Business Transaction Agreement and the transactions contemplated thereby, PubCo, will acquire each of MMAC and Akazoo in a series of steps as outlined below:

5

Table of Contents

| i. | in accordance with Luxembourg law and the Delaware General Corporation Law (the “DGCL”), MMAC will merge with and into PubCo, with PubCo remaining as the surviving publicly traded entity (the “Merger”); |

| ii. | no later than seven days prior to the effective date of the Merger, LuxCo will acquire the entire issued share capital of Akazoo in consideration for issuing LuxCo Shares to the Akazoo shareholders pursuant to the “Share Exchange”, acquire all outstanding convertible loan notes from the noteholders in Akazoo (the “Akazoo Noteholders”) in consideration for issuing convertible loan notes on materially the same terms in LuxCo and grant options to Akazoo optionholders (the “Akazoo Optionholders”) in LuxCo in consideration for the optionholders waiving their option to subscribe for equity in Akazoo such that the shareholdings of LuxCo will be identical immediately after the Share Exchange to that of Akazoo prior to the Share Exchange; and |

| iii. | on the calendar day following the effective date of the Merger, the Akazoo Noteholders will convert their convertible loan notes in LuxCo, the Akazoo Optionholders will exercise their options in LuxCo, and immediately thereafter LuxCo will merge with and into PubCo in accordance with Luxembourg law, with PubCo remaining as the surviving publicly traded entity (the “Luxembourg Merger”). |

Following the consummation of the Luxembourg Merger, Akazoo will be a direct, wholly owned subsidiary of PubCo, and the current security holders of MMAC and Akazoo will be shareholders of PubCo.

In order to consummate the Business Combination, a majority of the shares of MMAC Common Stock outstanding as of at the close of Business on August 9, 2019 (the “Record Date”) must vote to approve and adopt the Business Transaction Agreement and the transactions contemplated thereby (the “Business Combination Proposal”). MMAC’s executive officers, independent directors and sponsor have agreed to vote their shares of MMAC Common Stock in favor of the Business Combination Proposal. As of the date hereof, such persons are entitled to vote 5,175,000 shares of MMAC Common Stock, representing approximately 78.6% of all outstanding shares of MMAC Common Stock. Accordingly, stockholder approval of the Business Combination Proposal is assured. See “Special Meeting of MMAC Stockholders” and “Certain Agreements Related to the Business Combination – Voting Agreement.”

MMAC will hold a Special Meeting of its stockholders to obtain this approval. This proxy statement/prospectus contains important information about the proposed Business Combination.

This proxy statement/prospectus also contains important information about the proposed Adjournment. You should read it carefully; in particular the section entitled “Risk Factors.”

We encourage you to vote as soon as possible after carefully reviewing this proxy statement/prospectus.

What is being voted on at the Special Meeting?

There are two proposals on which you are being asked to vote. The Business Combination Proposal is to approve the Business Transaction Agreement and the transactions contemplated thereby. As a result of the Business Combination, MMAC will merge with and into PubCo in the Merger and Akazoo will become a wholly owned subsidiary of PubCo through (1) the Share Exchange with LuxCo and (2) the subsequent Luxembourg Merger.

The Adjournment Proposal is to approve the adjournment of the Special Meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies in the event that, based upon the tabulated vote at the time of the Special Meeting, MMAC would not have been authorized to consummate the Business Combination.

MMAC has agreed with the trustee to promptly liquidate if MMAC does not effect a business combination by September 17, 2019, unless that date is otherwise extended by MMAC’s stockholders.

Does the Board recommend voting for the approval of the proposals?

Yes. After careful consideration of the terms and conditions of these proposals, the Board has unanimously determined that each of the proposals are in the best interests of MMAC and its stockholders. The Board recommends that MMAC’s stockholders vote “FOR” each of the proposals.

How is management of MMAC voting?

MMAC’s initial stockholders, including all of its directors and officers, who purchased or received shares of MMAC Common Stock prior to MMAC’s IPO and may from time to time purchase MMAC Common Stock in the open market, together with their affiliates, owned an aggregate of approximately 78.6% of the outstanding shares of MMAC Common Stock (an aggregate of 5,175,000 shares of MMAC Common Stock) as of the Record Date. Because all of these persons have agreed to vote all of these shares in favor of the Business Combination Proposal, approval of the Business Combination is assured.

MMAC is not aware of any current plans for the sponsor or its directors, executive officers, advisors or their affiliates to purchase MMAC Common Stock from public stockholders in anticipation of the vote on the Business Combination Proposal.

6

Table of Contents

Because MMAC’s sponsor, directors and officers will also vote “FOR” the Adjournment Proposal, approval of the Adjournment Proposal is also assured.

Are any of the proposals conditioned on one another?

No. The Adjournment Proposal does not require the approval of the Business Combination Proposal to be effective. If MMAC does not consummate the Business Combination and fails to complete an initial business combination by September 17, 2019, and that date is not otherwise extended by MMAC’s stockholders, MMAC would be required to dissolve and liquidate its trust account by returning the then-remaining funds in such account to its public stockholders.

What is a quorum?

A quorum is the number of shares that must be represented, in person or by proxy, in order for business to be transacted at the Special Meeting.

More thanone-half of the total number of shares of MMAC Common Stock outstanding as of the Record Date (a quorum) must be represented, either in person or by proxy, in order to transact business at the Special Meeting. Abstentions and brokernon-votes are counted for purposes of determining the presence of a quorum. If there is no quorum, a majority of the shares present at the Special Meeting may adjourn the Special Meeting to another date.

Why is MMAC proposing the Business Combination?

MMAC is a blank check company formed specifically as a vehicle to effect a merger, capital stock exchange, asset acquisition, stock purchase, reorganization, recapitalization or similar business combination with one or more businesses in the media, entertainment or marketing services industries. In the course of MMAC’s search for a business combination partner, MMAC investigated the potential acquisition of many entities in the media, entertainment and marketing services industries, including Akazoo, and concluded that Akazoo was the best candidate for a business combination with MMAC. For more details on MMAC’s search for a business combination partner and the Board’s reasons for selecting Akazoo as MMAC’s business combination partner, see the sections titled “Background of the Business Combination” and “MMAC’s Reasons for the Business Combination and Recommendation of MMAC’s Board” included in this proxy statement/prospectus.

What vote is required in order to approve the Business Combination Proposal?

The approval of the Business Combination Proposal will require the affirmative vote of a majority of the shares of MMAC Common Stock outstanding on the Record Date. The founding stockholders of MMAC, representing approximately 78.6% of the shares of MMAC Common Stock outstanding on the Record Date, have agreed to vote their shares of MMAC Common Stock owned or acquired by them in favor of the Business Combination Proposal. Accordingly, approval of the Business Combination Proposal is assured.

Since the Business Combination Proposal requires the affirmative vote of a majority of the shares of MMAC Common Stock outstanding on the Record Date, abstentions or brokernon-votes will count as votes “AGAINST” the Business Combination Proposal.

What if I object to the Business Combination? Do I have appraisal rights?

Stockholders do not have appraisal rights in connection with the Business Combination under the DGCL.

Do I have redemption rights in connection with the Business Combination?

Pursuant to the MMAC Certificate of Incorporation, each MMAC stockholder who holds shares of MMAC Common Stock issued in MMAC’s initial public offering (the “IPO”) has the right to elect that MMAC redeem such stockholder’s shares for cash equal to a pro rata portion of the trust account. To properly elect redemption, MMAC stockholders must follow the procedures outlined in this proxy statement/prospectus under the heading “Special Meeting of MMAC Stockholders – Redemption Rights”. If the Business Combination is consummated and you properly complete the redemption procedures outlined herein, then your shares of MMAC Common Stock will be redeemed at aper-share price, payable in cash, equal to the aggregate amount then on deposit in MMAC’s trust account as of two business days prior to the consummation of the Business Combination, including interest, less taxes payable, divided by the number of then outstanding public shares, subject to certain limitations.

7

Table of Contents

MMAC estimates that theper-share price at which public shares may be redeemed from cash held in the trust account will be approximately $10.35 at the time of the Special Meeting.

In connection with tendering your shares for redemption, you must elect either to (x) physically tender your stock certificates to Continental Stock Transfer & Trust Company, MMAC’s transfer agent, at Continental Stock Transfer & Trust Company, 1 State Street, 30th Floor, New York, New York, 10004, Attn: Mark Zimkind, mzimkind@continentalstock.com, or (y) deliver your shares to the transfer agent electronically using The Depositary Trust Company’s (“DTC”) DWAC (Deposit/Withdrawal At Custodian) system, which election would likely be determined based on the manner in which you hold your shares. There may be a fee associated with this tendering process and the act of certificating the shares or delivering them through the DWAC system. The transfer agent will typically charge the tendering broker this fee, and the broker may or may not pass this cost on to you.You must tender your shares in the manner described above prior to 5:00 p.m. Eastern Time on , 2019 (two business days before the Special Meeting) in order to exercise your redemption rights in connection with the Business Combination.

Note that the delivery process can be accomplished by you, whether or not you are a record holder or your shares are held in “street name”, within a day, by simply contacting the transfer agent or your broker and requesting delivery of your shares through the DWAC system. MMAC believes this time period is sufficient for an average investor.

If you exercise your redemption rights, then you will be exchanging your shares of MMAC Common Stock for cash and will no longer own these shares of common stock and will not be entitled to receive any PubCo Ordinary Shares in connection with the Business Combination. If you redeem your shares of MMAC Common Stock but you remain in possession of any MMAC Warrants and have not sold or transferred them, you will still have the right to exercise the MMAC Warrants in accordance with the terms thereof, or, if the Business Combination is consummated, will receive PubCo Warrants in exchange for your MMAC Warrants, according to the terms of the Business Transaction Agreement.

If the Business Combination is not consummated: (i) then your shares will not be converted into cash at this time, even if you so elected, and (ii) assuming MMAC is unable to consummate another business combination by September 17, 2019, and that date is not otherwise extended by MMAC’s stockholders, then MMAC would be required to commence the liquidation process and you will be entitled to distribution upon liquidation. See the section titled “Redemption Rights” below in this proxy statement/prospectus.

Any request for redemption, once properly made, may be withdrawn at any time up to two days before the Special Meeting. Furthermore, if you delivered a certificate for redemption and subsequently decided prior to the Special Meeting not to elect redemption, you may simply request that the transfer agent return the certificate (physically or electronically) to you. The transfer agent will typically charge an additional fee for the return of the shares through the DWAC system.

If the Business Combination is not completed, your stock certificate will be automatically returned to you.

Holders of public shares of MMAC Common Stock have elected to redeem such shares such that MMAC currently has, in the aggregate, less than $53,000,000 of available cash. As such, MMAC is not currently able to satisfy a condition to consummation of the Business Combination and, unless the PIPE Financing is successful, Akazoo will not be required to consummate the Business Combination, although such condition to closing may be waived by Akazoo.

What are the interests of MMAC’s directors and executive officers in the Business Combination?

When you consider the recommendation of the Board to vote in favor of the approval of the Business Combination Proposal, you should keep in mind that MMAC’s directors and executive officers have interests in the Business Combination that are different from, or in addition to, your interests as a stockholder. For a full discussion of these interests, see the section titled “Interests of MMAC Directors and Officers in the Business Combination.” These interests include:

8

Table of Contents

| • | The MMAC Certificate of Incorporation provides that if MMAC does not complete an initial business combination by September 17, 2019, and that date is not otherwise extended by MMAC’s stockholders, MMAC would be required to dissolve and liquidate. In the event of a dissolution: |

| • | The founder shares would become worthless, as the initial stockholders have waived any right to redemption with respect to their founder shares. Such shares had an estimated aggregate market value of approximately $54,234,000, based upon the closing price of MMAC Common Stock of $10.48 on NASDAQ on the Record Date for the Special Meeting; |

| • | MMAC’s sponsor, which is partially owned by Mr. Dickey, may be liable for certain claims against MMAC; |

| • | MMAC’s sponsor, officers and directors may not receive reimbursement of certainout-of-pocket expenses to which they are entitled; and |

| • | Certain rights related to indemnification provided by MMAC to its directors and officers would no longer be available. |

| • | If the Business Combination is consummated, the current directors and officers of MMAC would have the right to continued indemnification, and to receive the benefit of directors’ and officers’ liability insurance; and |

| • | If the Business Combination is consummated, certain current directors or officers of MMAC may continue to serve as directors or officers of PubCo and may be compensated for such service. |

What vote is required in order to approve the Adjournment Proposal?

Adoption of the Adjournment Proposal requires the affirmative vote of the holders of a majority of the shares of MMAC Common Stock represented in person or by proxy and entitled to vote at the meeting. Accordingly, the failure to vote by proxy or to vote in person at the Special Meeting will not be counted for purposes of shares present to establish a quorum, and therefore will have no effect on the outcome of the vote. Abstentions will be counted in determining whether a quorum is present and therefore will have the same effect as a vote AGAINST the adjournment proposal. Adoption of the Adjournment Proposal is not conditioned upon the adoption of any of the other proposals.

If I am not going to attend the Special Meeting in person, should I return my proxy card instead?

Yes. Whether or not you plan to attend the Special Meeting, after carefully reading and considering the information contained in this proxy statement/prospectus, please complete and sign your proxy card. Then return the enclosed proxy card in the return envelope provided herewith as soon as possible, so that your shares may be represented at the Special Meeting.

What will happen if I abstain from voting or fail to vote at the Special Meeting?

MMAC will count a properly executed proxy marked ABSTAIN with respect to a particular proposal as present for purposes of determining whether a quorum is present. An abstention or failure to vote on the Business Combination Proposal count as a vote AGAINST the Business Combination Proposal, provided a quorum is present, and will have no effect on any redemption of your MMAC Common Stock. In order for a stockholder to convert his or her shares, he or she must follow the redemption procedures outlined below under the section entitled “Special Meeting of MMAC Stockholders — Redemption Rights.” An abstention on the Adjournment Proposal will have the same effect as a vote AGAINST that proposal.

What will happen if I sign and return my proxy card without indicating how I wish to vote?

Proxies received by MMAC without an indication of how the stockholders intend to vote on a proposal will be voted in favor of such proposal, in accordance with the Board’s unanimous recommendation.

9

Table of Contents

If my shares are held in “street name” by my broker, will my broker vote my shares for me?

If you hold your shares in “street name,” your bank or broker cannot vote your shares with respect to the Business Combination Proposal or the Adjournment Proposal without specific instructions from you, which are sometimes referred to in this proxy statement/prospectus as the broker“non-vote” rules. If you do not provide instructions with your proxy, your bank or broker may deliver a proxy card expressly indicating that it is NOT voting your shares; this indication that a bank or broker is not voting your shares is referred to as a “brokernon-vote.” Brokernon-votes will be counted for the purpose of determining the existence of a quorum, but will not count for purposes of determining the number of votes cast at the Special Meeting.

What do I do if I want to change my vote?

If you wish to change your vote, please send a later-dated, signed proxy card to MMAC’s General Counsel and Assistant Secretary, Adam Kagan, at MMAC’s corporate headquarters prior to the date of the Special Meeting or attend the Special Meeting and vote in person. You also may revoke your proxy by sending a notice of revocation to Adam Kagan at MMAC’s corporate headquarters, provided such revocation is received prior to the Special Meeting.

What consideration will be paid in connection with the Business Combination?

If the Business Combination is consummated and you do not otherwise properly elect to redeem your shares of MMAC Common Stock, your MMAC securities will be treated as follows:

| 1) | immediately before consummation of the Merger, you will automatically receiveone-tenth (1/10) of one share of MMAC Common Stock for each MMAC Right that you own; and |

| 2) | the MMAC Common Stock (including shares that were automatically issued to holders of MMAC Rights pursuant to the conversion of such rights immediately prior to the Merger but excluding any redeemed shares) and MMAC Warrants, as applicable, that you own will be exchanged, pursuant to the Business Transaction Agreement, for PubCo Ordinary Shares (in the case of MMAC Common Stock) or PubCo Warrants (in the case of MMAC Warrants) upon the completion of the Business Combination. |

If the Business Combination is consummated but you have elected and properly completed the procedures for a cash redemption, your shares of MMAC Common Stock will be redeemed at aper-share price, payable in cash, equal to the aggregate amount then on deposit in MMAC’s trust account as of two business days prior to the consummation of the Business Combination, including interest, net of taxes payable, divided by the number of then outstanding public shares, subject to certain limitations.

MMAC estimates that theper-share price at which public shares may be redeemed from cash held in the trust account will be approximately $10.35 at the time of the Special Meeting.

Existing Akazoo equityholders will receive an aggregate number of PubCo Ordinary Shares equal to an assumed Akazoo enterprise value of $380 million (less any cash payment to them, as discussed below) divided by the per share redemption price applicable to any redemptions by public stockholders of MMAC (such number of PubCo Ordinary Shares, the “Share Consideration”).

Additionally, subject to the terms of the Business Transaction Agreement, as consideration for the cancellation of the LuxCo Shares in exchange for PubCo Ordinary Shares in the Luxembourg Merger, (i) each issued and outstanding LuxCo Share will be cancelled, and (ii) each LuxCo shareholder will be entitled to receive its pro rata share of the Share Consideration. Also, each LuxCo shareholder will be entitled to receive its pro rata share of the Cash Payment (if any) as a compensatory payment under Luxembourg law to be payable 10 calendar days after the closing date of the Luxembourg Merger.

10

Table of Contents

Will I experience dilution as a result of the Business Combination?

Prior to the Business Combination, holders of the public shares owned approximately 21.4% of MMAC’s issued and outstanding common stock. After giving effect to the Business Combination and successful closing of the PIPE Financing such that PubCo has $53 million of available cash upon the consummation of the Business Combination, and giving effect to the PubCo Ordinary Shares to be issued to Akazoo in connection with the Business Combination, and assuming no MMAC stockholders exercise their redemption rights as discussed herein, the current holders of the public shares will own approximately 7.1% of PubCo.

MMAC has no specified maximum redemption threshold under the MMAC Certificate of Incorporation. It is a condition to closing under the Business Transaction Agreement, however, that MMAC has, in the aggregate, not less than $53.0 million of available cash upon the consummation of the Business Combination. Given the amount currently in MMAC’s trust account, PubCo is in the process of securing binding commitments for the PIPE Financing to satisfy this condition, without which Akazoo will not be required to consummate the Business Combination, although it may waive this condition.

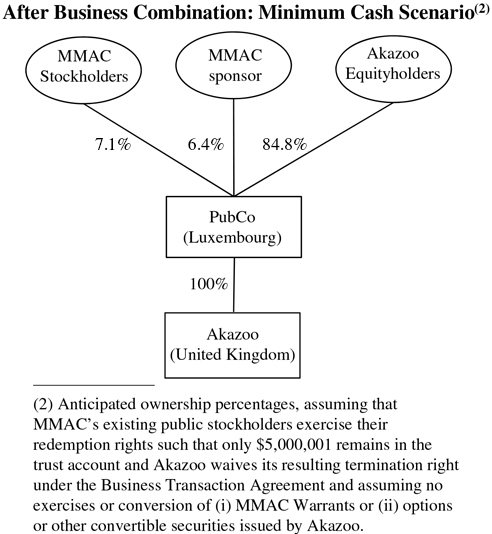

In no event, however, will MMAC redeem more than approximately 445,850 (32%) shares of MMAC Common Stock because redeeming more than that amount would cause its net tangible assets to be less than $5,000,001 (the “Minimum Cash Scenario”). The Minimum Cash Scenario would result in approximately 476,190 public shares being issued and outstanding at the time of the Business Combination. If the Business Combination were consummated under the Minimum Cash Scenario, Akazoo equityholders would own approximately 84.8% of outstanding PubCo Ordinary Shares, MMAC public stockholders would own approximately 7.1% and MMAC founders would own approximately 6.4%.

Are Akazoo’s equityholders required to approve the Business Combination?

Yes. However, holders of a majority of Akazoo’s voting power, in connection with the Business Transaction Agreement, have agreed to vote to approve the Business Combination.

Is the consummation of the Business Combination subject to any conditions?

Yes. The obligations of each of MMAC, Akazoo, LuxCo and PubCo to consummate the Business Combination are subject to conditions, as more fully described in the section entitled “The Business Transaction Agreement” in this proxy statement/prospectus.

What happens if I sell my shares of MMAC Common Stock before the Special Meeting?

The Record Date for the Special Meeting is earlier than the date that the Business Combination is expected to be consummated. If you transfer your shares of MMAC Common Stock after the Record Date, but before the Special Meeting, unless the transferee obtains from you a proxy to vote those shares, you would retain your right to vote at the Special Meeting. However, you would not be entitled to receive any PubCo Ordinary Shares on account of those shares of MMAC Common Stock following the consummation of the Business Combination because only MMAC’s stockholders at the time of the consummation of the Business Combination will be entitled to receive PubCo Ordinary Shares in connection with the Business Combination.

Do the laws governing companies in Luxembourg differ from those governing corporations in Delaware?

Yes. For a detailed description between the corporate law of Luxembourg and that of Delaware, see the section entitled “Comparison of Stockholders’ Rights” in this proxy statement/prospectus.

What are the U.S. federal income tax consequences of the Business Combination to MMAC and PubCo?

MMAC will recognize gain (but not loss) on the transfer of its assets to PubCo, to the extent that the fair market value of such assets exceeds MMAC’s adjusted basis in such assets. MMAC does not expect the amount of such gain to be material, but there is no certainty that that would be the case.

Although PubCo will be incorporated under the laws of Luxembourg, the Internal Revenue Service (the “IRS”) may assert that PubCo should be treated as a U.S. corporation for U.S. federal income tax purposes pursuant to section 7874 (“Section 7874”) of the Internal Revenue Code of 1986, as amended (the “Code”). If PubCo were to be treated as a U.S. corporation for U.S. federal income tax purposes, PubCo could be subject to substantial additional U.S. tax liability. However, as more fully described under “Material U.S. Federal Income Tax Consequences of the Business Combination — U.S. Federal Income Tax Consequences of the Business Combination to MMAC and PubCo,” based on certain representations of the parties and factual assumptions, PubCo does not expect that Section 7874 will cause it to be treated as a U.S. corporation for U.S. federal income tax purposes.

What are the U.S. federal income tax consequences of exercising my redemption rights?

A U.S. Holder (as defined below) who exercises his or her redemption rights will receive cash in exchange for the tendered shares, and either will be considered for U.S. federal income tax purposes to have made a sale or exchange of the tendered shares, or will be considered for U.S. federal income tax purposes to have received a distribution with respect to such shares that may be treated as (i) dividend income, (ii) a nontaxable recovery of basis in his investment in the tendered shares, or (iii) gain (but not loss) as if the shares with respect to which the distribution was made had been sold. See the section entitled “Material U.S. Federal Income Tax Consequences of the Business Combination — Certain U.S. Federal Income Tax Consequences of Exercising Redemption Rights.”

11

Table of Contents

Will holders of MMAC Common Stock, MMAC Rights or MMAC Warrants be subject to U.S. federal income tax on the PubCo Ordinary Shares or PubCo Warrants received in the Business Combination?

Subject to the limitations and qualifications described in “Material U.S. Federal Income Tax Consequences of the Business Combination,” the Merger should qualify as a “reorganization” within the meaning of Section 368 of the Code. As a result, a U.S. Holder should not recognize gain or loss on the automatic conversion of MMAC Rights to MMAC Common Stock immediately prior to the Merger in connection with the Business Combination, and the exchange of MMAC Common Stock or MMAC Warrants for PubCo Ordinary Shares or PubCo Warrants, as applicable, pursuant to the Merger. The discussion in “Material U.S. Federal Income Tax Consequences of the Business Combination” reflects the opinion of Jones Day as to the material U.S. federal income tax consequences of the Business Combination to U.S. Holders of MMAC securities and/or MMAC Rights, subject to the limitations, exceptions, beliefs, assumptions, and qualifications described therein and otherwise herein (including uncertainty as to whether the Business Combination will be taxable for such U.S. Holders). The rules under Section 367(a) and Section 368 of the Code are complex and there is limited guidance as to their application, particularly with regard to indirect stock transfers in cross-border reorganizations.