UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-23425

CIM Real Assets & Credit Fund

(Exact Name of Registrant as Specified in Charter)

4700 Wilshire Boulevard

Los Angeles, California 90010

(Address of Principal Executive Offices)

David Thompson

Chief Executive Officer

CIM Real Assets & Credit Fund

4700 Wilshire Boulevard

Los Angeles, California 90010

(Name and Address of Agent for Service)

Registrant’s Telephone Number, Including Area Code: (323) 860-4900

Date of fiscal year end: September 30

Date of reporting period: September 30, 2023

Item 1. Reports to Stockholders.

Table of Contents

| Shareholder Letter | 1 |

| Portfolio Update | 4 |

| Consolidated Schedule of Investments | 6 |

| Consolidated Statement of Assets and Liabilities | 14 |

| Consolidated Statement of Operations | 16 |

| Consolidated Statements of Changes in Net Assets | 17 |

| Consolidated Statement of Cash Flows | 19 |

| Consolidated Financial Highlights | |

| Class A | 20 |

| Class C | 21 |

| Class I | 22 |

| Class L | 23 |

| Consolidated Notes to Financial Statements | 24 |

| Report of Independent Registered Public Accounting Firm | 42 |

| Additional Information | 43 |

| Trustee & Officers | 44 |

| Privacy Policy | 47 |

Important Notice Regarding Electronic Delivery

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you do not need to take any action. For shareholder reports and other communications from the Fund issued prior to 2023, you may elect to receive such reports and other communications electronically. If you own shares of the Fund through a financial intermediary, you may contact your financial intermediary to elect to receive materials electronically. This information is available free of charge by contacting us by mail at 4700 Wilshire Boulevard, Los Angeles, CA, 90010, by telephone at (866) 907-2653 or on our website at https://www.cimgroup.com/ public-investment-programs/current-public-programs/racr.

You may elect to receive all future reports in paper, free of charge. If you own shares of the Fund through a financial intermediary, you may contact your financial intermediary to elect to continue to receive paper copies of your shareholder reports in 2023. This information is available free of charge by contacting us by mail at 4700 Wilshire Boulevard, Los Angeles, CA, 90010, by telephone at (866) 907-2653 or on our website at https://www.cimgroup.com/public-investment-programs/current-public-programs/racr. If you make such an election through your financial intermediary, your election to receive reports in paper may apply to all funds held through your financial intermediary.

Dear Shareholders,

We are pleased to provide you with the 2023 annual report for CIM Real Assets & Credit Fund (“we,” “us,” “our,” “CIM RACR,” or the “Fund”). CIM RACR is a continuously-offered, closed-end interval fund registered under the Investment Company Act of 1940, as amended. The Fund primarily invests in credit (of both real assets and corporates) and real estate equity.

In October 2023, our Board of Directors declared monthly cash dividends representing an annualized distribution rate of 8.5% of net asset value per share (as of the close of business on October 12, 2023). This 21% increase in the distribution (from the prior distribution rate) rate reflects increasing income on CIM RACR’s floating rate real estate and credit investments and the expectation of improving net operating income on its real estate equity investments from recent strong leasing activity.1 In addition, a portion of RACR’s distribution may be tax deferred whereas income from bonds and credit funds are typically 100% ordinary income and taxed at the highest rate.

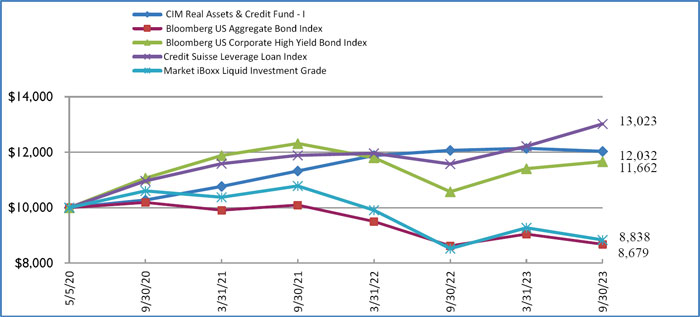

Since inception (May 2020), RACR’s Class I Common Shares have generated an annualized return of 5.58%, as of September 30, 2023, and have outperformed widely followed income alternatives such as the Bloomberg US Aggregate Bond Index, The Markit iBoxx USD Liquid Investment Grade Index and the Bloomberg US Corporate High Yield Bond Index.2

RACR’s returns since inception have primarily been driven by interest income from our real estate debt and corporate credit investments.

We believe the Fund is well positioned. In our view, it is an attractive environment to be a lender. Banks have reduced lending which has led to less competition and thus better terms for lenders like the Fund. Because of this dynamic, RACR has increased its allocation of investments higher in the capital stack (i.e. increased allocation to more senior debt investments and reduced allocation to more junior equity investments). For example, RACR’s real estate debt investments increased to 21.2% of the portfolio as of September 30, 2023, compared to 14.8% from the year-earlier period. And on the corporate credit side, we are focused on investing in 1st lien secured loans and CLO debt collateralized by 1st lien secured corporate loans, as opposed to 2nd lien or unsecured bonds.

RACR’s real estate equity investments decreased to 15.8% of the portfolio as of September 30, 2023, compared to 23.3% from the year-earlier period. However, we believe this asset class will be a source of compelling opportunities for the fund. The increase in interest rates and accompanying capitalization rates has led to a reduction in real estate values. As real estate owners seek to refinance their debt, the reduction in their asset value means they will likely need to either partially pay down their mortgage, sell their asset or partner with other equity providers. We believe this will present compelling deal flow for CIM RACR.

Fund Overview

The Fund’s investment objective is to generate current income through cash distributions and preserve shareholders’ capital across various market cycles, with a secondary objective of capital appreciation. However, there can be no assurance that the Fund will achieve its investment objective.

The Fund seeks to provide shareholders with income and capital appreciation, with lower volatility and correlation to the broader equity markets and other widely used income alternatives. We believe our real asset equity allocation may reduce volatility and correlation, while creating the potential for appreciation as well as allowing for the Fund to generate income used to pay distributions. This real asset equity allocation may also create a more tax efficient distribution for shareholders. Real estate investments

generate tax depreciation expenses. These tax depreciation expenses can be used to reduce the taxable income generated from credit investments, resulting in a lower current year taxable income.

The Fund’s innovative structure allows it to directly invest in real estate rather than private funds of other managers, and thus avoiding multiple layers of fees. To promote further alignment with other funds managed by affiliates of CIM Group, LLC (“CIM”) and OFS Capital Management, LLC (the “OFS Sub- Adviser” or “OFS”), the Fund has obtained exemptive relief from the U.S. Securities and Exchange Commission (“SEC”) that allows it to co-invest alongside funds managed by affiliates of CIM and OFS, in accordance with the conditions specified in the exemptive relief. The Fund seeks to provide investors with exposure to proprietary transactions, alongside large, sophisticated institutions, that otherwise may not be available to retail investors and that may have high investment minimums.

About the Advisor

CIM Capital IC Management, LLC (the “Adviser”), registered as an investment adviser with the SEC under the Investment Advisers Act of 1940, as amended (the “Advisers Act”), acts as the Fund’s investment adviser and is primarily responsible for determining the amount of the Fund’s total assets that are allocated to each of the Fund’s sub-advisers. The Adviser has engaged each of CIM Capital SA Management, LLC (the “CIM Sub-Adviser”) and the OFS Sub-Adviser, each a SEC-registered investment adviser, to act as an investment sub-adviser to the Fund. The CIM Sub-Adviser is responsible for identifying and sourcing investment opportunities with respect to investments in real assets held by the Fund. The OFS Sub-Adviser is responsible for identifying and sourcing credit and credit-related investment opportunities.

CIM is a vertically-integrated owner and operator of real assets for its own account and on behalf of its partners and co-investors, seeking exposure to real assets and associated credit strategies, with a principal focus on metropolitan areas across the Americas. Since inception, CIM, on behalf of itself and over 200 institutional partners and co-investors, has operated over 300 discretionary real estate and real estate-related equity, debt and infrastructure holdings (excluding net-lease).3 As of June 30, 2023, CIM owns and operates approximately $30.8 billion of assets4 across its products and has deployed assets for its Principals, partners and co-investors, which include U.S. and Non-U.S. public and corporate pension funds, endowments, foundations, sovereign wealth funds and other institutional and private partners and co- investors since 2000. As of September 30, 2023, CIM has over 1,000 employees and more than 600 professionals and 9 corporate offices worldwide. CIM also maintains additional offices across the United States as well as in Korea to support its platform.

OFS is a full-service provider of capital and levered financial solutions with $4.3 billion in assets under management as of June 30, 2023, with a focus on middle market lending, broadly syndicated loans, and structured credit. OFS serves as the investment adviser to business development companies, registered closed-end funds, and separately managed, proprietary and sub-advised accounts, as well as the collateral manager to various collateralized loan obligations.

Thank you for your investment in CIM RACR. If you have any questions, please contact the CIM Shareholder Relations team at 866.907.2653. We look forward to continuing our relationship in the years to come.

Sincerely,

Steve Altebrando

1st Vice President, Portfolio Oversight

David Thompson

Chief Executive Officer

| 1 | Based on current estimates, the Fund expects a portion of the distributions to be a return of capital. |

| 2 | The performance data quoted above represents past performance. Past performance does not guarantee future results. The investment return and principle value of an investment will fluctuate so that an investor’s shares, when sold or repurchased, may be worth more or less than the original cost. The current performance may be lower or higher than performance data quoted. The indices shown are for informational purposes only and are not reflective of any investment. Investors cannot invest directly in an index, and unmanaged index returns do no reflect any fees, expenses or sales charges. |

| 4 | “Assets Owned and Operated” represents the aggregate assets owned and operated by CIM on behalf of partners (including where CIM Group contributes alongside for its own account) and co-investors, whether or not CIM has discretion, in each case without duplication. |

Forward-Looking Statements

Statements in this letter regarding management’s future expectations, beliefs, intentions, goals, strategies, plans or prospects, including statements relating management’s belief that CIM RACR will benefit from CIM Group’s combined real assets, credit and transaction experience and deal-sourcing capabilities; the composition of CIM RACR’s portfolio of real assets and corporate credit assets and the potential benefits to investors, which may not be realized; opportunities for individuals to invest alongside institutional partners, and whether those opportunities will align the interests among sponsors, partners and shareholders; and other factors may constitute forward-looking statements for purposes of the safe harbor protection under applicable securities laws. Forward-looking statements can be identified by terminology such as “anticipate,” “believe,” “could,” “could increase the likelihood,” “estimate,” “expect,” “intend,” “is planned,” “may,” “should,” “will,” “will enable,” “would be expected,” “look forward,” “may provide,” “would” or similar terms, variations of such terms or the negative of those terms. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, including rising inflation and interest rates, the risk of recession, the ongoing war between Russia and Ukraine, the escalated conflict in the Middle East, supply chain disruptions, resource shortages, significant market volatility on our business, our industry, and the global economy, and those risks, uncertainties and factors referred to in CIM RACR’s Prospectus filed with the SEC under the section “Risks” and other documents that may be filed by CIM RACR from time to time with the SEC. As a result of such risks, uncertainties and factors, actual results may differ materially from any future results, performance or achievements discussed in or implied by the forward-looking statements contained herein. CIM RACR is providing the information in this letter as of this date and assumes no obligations to update the information included in this letter or revise any forward- looking statements, whether as a result of new information, future events or otherwise.

17646841-NLD-11282023

| CIM Real Assets & Credit Fund | Portfolio Update |

| | September 30, 2023 (unaudited) |

Performance as of September 30, 2023

| | | Annualized |

Annualized

Since |

| CIM Real Assets & Credit Fund | 1 Year | 3 Year | Inception |

| CIM Real Assets & Credit Fund - A-NAV | (0.58)% | 5.14% | 5.32% |

| CIM Real Assets & Credit Fund - A-Load | (6.29)% | 3.08% | 3.50% |

| CIM Real Assets & Credit Fund - C-NAV | (1.43)% | 4.31% | 4.49% |

| CIM Real Assets & Credit Fund - I-NAV | (0.31)% | 5.41% | 5.58% |

| CIM Real Assets & Credit Fund - L-NAV | (0.91)% | 4.84% | 5.02% |

| CIM Real Assets & Credit Fund - L-Load | (5.12)% | 3.33% | 3.69% |

| Bloomberg US Aggregate Bond Index (a) | (0.64)% | (5.21)% | (4.07)% |

| Bloomberg US Corporate High Yield Bond Index (b) | 10.28% | 1.75% | 4.62% |

| Credit Suisse Leverage Loan Index (c) | 12.47% | 5.91% | 8.04% |

| Market iBoxx Liquid Investment Grade (d) | 3.71% | (5.90)% | (3.56)% |

Comparison of the Change in Value of a $10,000 Investment

| (a) | Bloomberg US Aggregate Bond Index is a broad based, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. |

| | |

| (b) | The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded. |

| | |

| (c) | The Credit Suisse Leverage Loan Index tracks the investable market of the U.S. dollar denominated leveraged loan market. It consists of issues rated “5B” or lower, meaning that the highest rated issues included in this index are Moody’s/S&P ratings of Baa1/BB+ or Ba1/BBB+. All loans are funded term loans with a tenor of at least one year and are made by issuers domiciled in developed countries. |

| | |

| (d) | The Markit iBoxx USD Liquid Investment Grade Index is designed to reflect the performance of USD denominated investment grade corporate debt. The index rules aim to offer a broad coverage of the USD investment grade liquid bond universe. The index is market-value weighted with an issuer cap of 3%. |

The Fund previously compared its performance against the Morningstar LSTA US Leverage Loan index. The Fund decided to substitute the Morningstar LSTA US Leverage Loan Index with the Credit Suisse Leverage Loan USD index because of the costs associated with using the former index and the Fund’s belief that the replacement index is a close proximate of the original index.

Index performance is shown for illustrative purposes only as (i) all indices referenced above are unmanaged, (ii) index performance does not reflect the expenses associated with active management of an actual portfolio, (iii) the composition of each of the indices differs signficantly from that of the portfolio of the Fund and (iv) investors cannot invest directly in an index. The performance data quoted above represents past performance. Past performance does not guarantee future results. The investment return and principle value of an investment will fluctuate so that an investor’s shares, when sold or repurchased, may be worth more or less than the original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on any fund distributions or the sale of fund shares. The current performance may be lower or higher than performance data quoted. Please visit the Fund’s website at https://www.cimgroup.com/public-investment-programs/current-public-programs/racr for performance data current to the most recent month-end.

| CIM Real Assets & Credit Fund | Portfolio Update |

| | September 30, 2023 (unaudited) |

Top Ten Long Holdings as of September 30, 2023

| EPIC Dallas | | | 5.2 | % |

| Del Mar Terrace - Phoenix, AZ | | | 4.5 | % |

| Society Las Olas - PMG Greybook Riverfront I LLC | | | 3.3 | % |

| Sora Multifamily Residential Property | | | 3.0 | % |

| Extended Stay America Trust 2021-ESH, Class F | | | 2.9 | % |

| Elevation CLO 2022-16, Ltd., Class E | | | 2.8 | % |

| WMRK Commercial Mortgage Trust 2022-WMRK, Class E | | | 2.4 | % |

| 1902 Park Avenue (Los Angeles) Owner, L.P. | | | 2.3 | % |

| Regatta XXII Funding, Ltd., Class E | | | 2.2 | % |

| IENTC 2, LLC DDTL B-1 | | | 2.2 | % |

| | | | 30.8 | % |

Portfolio Composition as of September 30, 2023

| Collateralized Loan Obligations | | | 30.71 | % |

| Direct Real Estate | | | 20.49 | % |

| Commercial Mortgage-Backed Securities | | | 19.81 | % |

| Bank Loan | | | 21.27 | % |

| Real Estate-Related Securities | | | 7.66 | % |

| Common Stock | | | 2.66 | % |

| Loan Accumulation Facility | | | 0.52 | % |

| Cash, Cash Equivalents, & Other Net Assets | | | -3.12 | % |

| | | | 100.00 | % |

| CIM Real Assets & Credit Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

| Shares | | | | | | | | | | | Fair Value | |

| | | | | Common Stock - 2.66% | | | | | |

| | | | | Private - 2.16% | | | | | |

| | 580,645 | | | Boca Homecare Holdings, Inc. (Equity) (a),(b),(c),(d) | | | $ | 421,800 | |

| | 155,086 | | | CGA Holdings, Inc., Class A (a),(b),(c),(d) | | | | 154,820 | |

| | 3,763,895 | | | IENTC 1, LLC (a),(c),(d),(e) | | | | 6,212,460 | |

| | | | | | | | | | | | | | 6,789,080 | |

| | | | | Real Estate Investment Trust - .50% | | | | | |

| | 388,344 | | | Creative Media & Community Trust Corp. (b),(d),(h),(f) | | | | 1,572,793 | |

| | | | | | | | | | | | | �� | | |

| | | | | Total Common Stock (Cost $7,337,902) | | | | 8,361,873 | |

| | | | | | | | | | | | | |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | | |

| | | | | Bank Loans - 21.27% | | | | | | | | | | |

| | | | | Consumer Non-Cyclical - 2.56% | | | | | | | | | | |

| | 1,026,443 | | | Baart Programs, Inc., Second Lien Term Loan (a),(g),(h) | | 3M SOFR + 8.500% | | 14.150 | | 6/11/2028 | | | 964,856 | |

| | 500,000 | | | Bengal Debt Merger SUB, LLC TL 1L (a),(g) | | 3M SOFR + 6.000% | | 11.490 | | 1/24/2030 | | | 410,548 | |

| | 378,788 | | | MedMark Services, Inc., Second Lien Term Loan (a),(g) | | 3M SOFR + 8.500% | | 14.150 | | 6/11/2028 | | | 356,061 | |

| | 1,016,949 | | | RC Buyer, Inc., Second Lien Initial Term Loan (a),(g) | | 3M SOFR + 6.250% | | 11.920 | | 7/30/2029 | | | 948,305 | |

| | 2,985,000 | | | Spear Education Holdings, LLC Term A Loan (a),(b),(c),(g) | | 3M SOFR + 7.500% | | 12.548 | | 12/15/2027 | | | 2,952,165 | |

| | 430,240 | | | Spring Education Group, Inc., Second Lien Initial Term Loan (a),(g) | | 3M SOFR + 8.250% | | 13.680 | | 7/30/2026 | | | 414,966 | |

| | 1,985,000 | | | Tony’s Fresh Market / Cardenas Markets First lien Term Loan (g) | | 3M SOFR + 6.750% | | 12.240 | | 8/1/2029 | | | 1,990,796 | |

| | | | | | | | | | | | | | 8,037,697 | |

| | | | | | | | | | | | | | | |

| | | | | Electronic Equipment, Instruments & Components - 0.60% | | | | | | | | | | |

| | 2,000,000 | | | Idera, Inc. (a),(g),(h) | | 3M SOFR + 6.750% | | 11.880 | | 3/2/2029 | | | 1,900,000 | |

| | | | | | | | | | | | | | | |

| | | | | Financial Services - 0.64% | | | | | | | | | | |

| | 2,000,000 | | | PSB Group, LLC, Term Loan (Last Out) - May 2023 (a),(b),(c) | | 3M SOFR + 7.629% | | 12.935 | | 9/17/2026 | | | 1,996,000 | |

| | | | | | | | | | | | | | | |

| | | | | Financials - 0.16% | | | | | | | | | | |

| | 794,000 | | | Avison Young Canada, Inc., First Lien Term Loan (a),(g),(h) | | 3M SOFR + 7.000% | | 12.268 | | 1/31/2026 | | | 496,250 | |

| | | | | | | | | | | | | | | |

| | | | | Food Products - 0.22% | | | | | | | | | | |

| | 833,333 | | | BCPE North Star US Holdco 2, Inc. 2L TL (a),(g),(h) | | 3M SOFR + 7.250% | | 12.409 | | 6/8/2029 | | | 679,863 | |

| | | | | | | | | | | | | | | |

| | | | | Health Care Equipment & Supplies - 0.66% | | | | | | | | | | |

| | 163,043 | | | Kreg LLC, Revolver (a),(b),(c),(g),(i) | | 3M SOFR + 6.250% | | 0.500 | | 12/20/2026 | | | 151,467 | |

| | 2,064,011 | | | Kreg LLC, Term Loan (a),(b),(c),(g) | | 3M SOFR + 2.250% | | 7.298 | | 12/20/2026 | | | 1,917,466 | |

| | | | | | | | | | | | | | 2,068,933 | |

| | | | | Health Care Providers & Services - 6.78% | | | | | | | | | | |

| | 580,645 | | | Boca Home Care Holdings Revolver (a),(b),(c),(g),(i) | | 3M SOFR + 6.500% | | — | | 2/25/2027 | | | 559,161 | |

| | 5,001,895 | | | Boca Home Care Holdings, Inc Delayed Draw Term Loan (a),(b),(c),(g) | | 1M SOFR + 6.500% | | 11.648 | | 2/25/2027 | | | 4,816,824 | |

| | 1,183,256 | | | CVAUSA Management, LLC Primary DDTL (a),(b),(c),(g) | | 3M SOFR + 6.500% | | — | | 5/22/2029 | | | 1,165,507 | |

| | 495,316 | | | CVAUSA Management, LLC Secondary DDTL (a),(b),(c),(g) | | 3M SOFR + 6.500% | | — | | 5/22/2029 | | | 487,886 | |

| | 285,714 | | | CVAUSA Management, LLC, Revolver, TL (a),(b),(c),(g) | | 3M SOFR + 6.500% | | — | | 5/22/2028 | | | 281,429 | |

| | 1,991,747 | | | CVAUSA Management, LLC, Term Loan (a),(b),(c),(g) | | 3M SOFR + 6.500% | | 11.594 | | 5/22/2029 | | | 2,005,179 | |

| | 715,677 | | | Honor HN Buyer, Inc. Delayed Draw Term Loan (a),(b),(c),(g),(i) | | 3M SOFR + 5.750% | | 11.290 | | 10/15/2027 | | | 715,677 | |

| | 132,013 | | | Honor HN Buyer, Inc. Revolver (a),(b),(c),(g),(i) | | Prime + 5.000% | | 13.250 | | 10/15/2027 | | | 132,013 | |

| | 1,130,299 | | | Honor HN Buyer, Inc. Term Loan (a),(b),(c),(g) | | 3M SOFR + 5.750% | | 10.798 | | 10/15/2027 | | | 1,130,299 | |

| | 791,254 | | | Honor HN Buyer, Inc. Term Loan 1st Amendment Health Network (a),(b),(c) | | 6M SOFR + 6.000% | | 11.540 | | 10/15/2027 | | | 796,001 | |

| | 333,333 | | | One GI Intermediate LLC, Revolver Upsize (a),(b),(c),(g) | | 3M SOFR + 6.750% | | 11.961 | | 12/22/2025 | | | 313,667 | |

| | 1,723,750 | | | One GI Intermediate LLC, Tranche B Delayed Draw Term Loan (a),(b),(c),(g) | | 3M SOFR + 6.750% | | 12.003 | | 12/22/2025 | | | 1,622,049 | |

| | 914,390 | | | One GI Intermediate LLC, Tranche C Delayed Draw Term Loan (a),(b),(c),(g),(i) | | 3M SOFR + 6.750% | | 11.948 | | 12/22/2025 | | | 860,441 | |

| | 147,059 | | | Shiftkey, Revolver (a),(b),(c),(g),(i) | | 3M SOFR + 5.750% | | 10.616 | | 6/21/2027 | | | 143,382 | |

| | 2,329,412 | | | Shiftkey, Term Loan (a),(b),(c),(g) | | 3M SOFR + 5.750% | | 10.910 | | 6/21/2027 | | | 2,271,177 | |

| | 3,989,880 | | | Spectrum Vision Partners, LLC (a),(b),(c) | | 3M SOFR + 6.500% | | 12.150 | | 11/18/2024 | | | 3,977,910 | |

| | | | | | | | | | | | | | 21,278,602 | |

| | | | | Hotels, Restaurants & Leisure - 1.41% | | | | | | | | | | |

| | 1,440,000 | | | SS Acquisition LLC, Delayed Draw Term Loan (a),(b),(c),(g) | | 3M SOFR + 7.591% | | 12.625 | | 12/30/2026 | | | 1,440,000 | |

| | 3,000,000 | | | SS Acquisition LLC, Term Loan (a),(b),(c),(g) | | 3M SOFR + 6.751% | | 11.919 | | 12/30/2026 | | | 3,000,000 | |

| | | | | | | | | | | | | | 4,440,000 | |

| | | | | Household Durables - 0.17% | | | | | | | | | | |

| | 1,000,000 | | | Astro One Acquisition Corporation (a),(g),(h) | | 6M US L + 8.500% | | 13.663 | | 9/14/2029 | | | 521,665 | |

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | Bank Loans - 21.27% (Continued) | | | | | | | | | | |

| | | | | Industrial - 1.09% | | | | | | | | | | |

| | 2,545,527 | | | AIDC Intermediate Co. 2, LLC, Term Loan (a),(b),(c),(g) | | 3M SOFR + 6.250% | | 11.770 | | 7/22/2027 | | $ | 2,525,163 | |

| | 1,097,499 | | | Energy Acquisition LP, Second Lien Initial Term Loan (a),(g),(i) | | 3M SOFR + 8.500% | | 13.864 | | 6/26/2026 | | | 891,718 | |

| | | | | | | | | | | | | | 3,416,881 | |

| | | | | Personal Products - 0.60% | | | | | | | | | | |

| | 1,994,911 | | | Journey Personal Care Corp TL 1L (a),(i) | | 6M US L + 4.250% | | 9.980 | | 3/1/2028 | | | 1,883,944 | |

| | | | | | | | | | | | | | | |

| | | | | Retail - 0.97% | | | | | | | | | | |

| | 3,157,895 | | | LSF9 Atlantis Holdings, LLC (g),(h) | | 1M SOFR + 7.250% | | 12.640 | | 3/31/2029 | | | 3,033,555 | |

| | | | | | | | | | | | | | | |

| | | | | Services - 3.10% | | | | | | | | | | |

| | 4,286,957 | | | 24 Seven, Inc., Term Loan (a),(b),(c),(g) | | 3M SOFR + 6.000% | | 11.260 | | 11/16/2027 | | | 4,171,209 | |

| | 999,970 | | | Convergint Technologies LLC, Second Lien Term Loan (a),(g),(h) | | 3M SOFR + 6.750% | | 12.018 | | 3/30/2029 | | | 888,724 | |

| | 1,500,000 | | | EOS-Metasource Intermediate, Inc., DDC (a),(b),(c),(g),(i) | | 3M SOFR + 6.250% | | — | | 5/17/2027 | | | 1,413,000 | |

| | 3,456,250 | | | EOS-Metasource Intermediate, Inc., TL (a),(b),(c),(g) | | 3M SOFR + 6.250% | | 11.518 | | 5/17/2027 | | | 3,255,788 | |

| | | | | | | | | | | | | | 9,728,721 | |

| | | | | Technology - 1.65% | | | | | | | | | | |

| | 3,000,000 | | | Exponential Power, Inc., TL (a),(b),(c),(g) | | 3M SOFR + 6.500% | | 11.672 | | 5/12/2026 | | | 2,955,000 | |

| | 800,000 | | | Redstone HoldCo 2 LP, Second Lien Initial TL (a),(g),(h) | | 3M SOFR + 7.750% | | 13.042 | | 4/27/2029 | | | 527,000 | |

| | 500,021 | | | RumbleON, Inc. Delay Draw Term Loan (a),(b),(c),(g),(i) | | 3M SOFR + 8.250% | | 13.409 | | 8/31/2026 | | | 458,520 | |

| | 1,359,163 | | | RumbleON, Inc. TL (a),(b),(c),(g) | | 3M SOFR + 8.750% | | 13.409 | | 8/31/2026 | | | 1,246,353 | |

| | | | | | | | | | | | | | 5,186,873 | |

| | | | | Transportation - 0.66% | | | | | | | | | | |

| | 2,167,683 | | | Reception Purchaser, LLC (a),(g),(h) | | 3M SOFR + 6.000% | | 11.253 | | 3/24/2028 | | | 2,086,393 | |

| | | | | | | | | | | | | | | |

| | | | | Total Bank Loans (Cost$68,908,659) | | | | | | | | | 66,755,377 | |

| | | | | | | | | | | | | | | |

| | | | | Collateralized Loan Obligations - Debt - 24.18% | | | | | | | | | | |

| | 1,000,000 | | | Allegro CLO XII, Ltd., Class E (b),(g),(j) | | 3M SOFR+ 7.100% | | 12.695 | | 1/21/2032 | | | 943,848 | |

| | 4,000,000 | | | Atlas Senior Loan Fund XX, Ltd., Class (b),(g) | | 3M SOFR + 9.430% | | 14.750 | | 10/19/2035 | | | 3,992,857 | |

| | 1,000,000 | | | Barings Middle Market CLO, Ltd. 2021-I, Class D (g),(h),(j) | | 3M SOFR+ 8.650% | | 14.238 | | 7/20/2033 | | | 973,965 | |

| | 2,500,000 | | | Birch Grove CLO 6 Ltd Series 6A E (b),(g),(i),(j) | | 3M SOFR + 8.930% | | 14.468 | | 7/7/2035 | | | 2,524,141 | |

| | 430,442 | | | Brightwood Capital MM CLO 2023-1A D Ltd (g),(j) | | 3M SOFR + 6.460% | | 11.860 | | 10/15/2035 | | | 417,529 | |

| | 1,003,974 | | | Brightwood Capital MM CLO 2023-1A E Ltd (g),(j) | | 3M SOFR + 10.360% | | 15.760 | | 10/15/2035 | | | 903,577 | |

| | 4,250,000 | | | Carlyle US CLO 2022-4, Ltd., Class E (g),(h),(j) | | 3M SOFR + 8.150% | | 13.501 | | 7/22/2034 | | | 4,194,760 | |

| | 2,000,000 | | | Carlyle US CLO 2022-6, Ltd., Class E (b),(g),(h),(j) | | 3M SOFR + 8.630% | | 13.981 | | 10/25/2034 | | | 2,001,660 | |

| | 5,285,000 | | | CFIP CLO 2017-1, Ltd., Class ER (g),(h),(j) | | 3M SOFR+ 7.300% | | 12.872 | | 10/18/2034 | | | 4,807,605 | |

| | 9,100,000 | | | Elevation CLO 2022-16, Ltd., Class E (g),(h),(j) | | 3M SOFR + 8.300% | | 13.651 | | 7/25/2034 | | | 8,842,419 | |

| | 6,000,000 | | | Empower CLO 2022-1, Ltd., Class E (g),(h),(j) | | 3M SOFR + 8.550% | | 13.876 | | 10/20/2034 | | | 6,000,586 | |

| | 3,000,000 | | | Empower CLO 2023-1, Ltd., Class D (b),(g),(h),(j) | | 3M SOFR + 5.500% | | 10.568 | | 4/25/2036 | | | 3,033,929 | |

| | 500,000 | | | Flatiron CLO 20, Ltd., Class E (g),(h),(j) | | 3M SOFR+ 7.850% | | 13.229 | | 11/20/2033 | | | 497,920 | |

| | 2,000,000 | | | Ivy Hill Middle Market Credit Fund XVIII, Ltd., Class E (g),(j) | | 3M SOFR+ 7.750% | | 13.357 | | 4/22/2033 | | | 1,855,501 | |

| | 1,250,000 | | | LCM 31, Ltd., Class E (g),(h),(j) | | 3M SOFR + 7.08% | | 12.406 | | 1/20/2032 | | | 1,167,245 | |

| | 5,500,000 | | | LCM 38, Ltd., Class E (g),(h),(j) | | 3M SOFR+ 7.73% | | 13.064 | | 10/15/2036 | | | 5,382,153 | |

| | 600,000 | | | Madison Park Funding XLVII, Ltd., Class E (g),(h),(j) | | 3M SOFR+ 7.460% | | 13.042 | | 1/19/2034 | | | 595,793 | |

| | 2,500,000 | | | MCF CLO VII LLC, Class ER (g),(h),(j) | | 3M SOFR + 9.150% | | 14.738 | | 7/20/2033 | | | 2,466,017 | |

| | 3,500,000 | | | Monroe Capital Mml CLO X, Ltd., Class ER (b),(g),(h),(j) | | 3M SOFR + 8.750% | | 14.130 | | 5/20/2034 | | | 3,359,226 | |

| | 2,250,000 | | | Northwoods Capital 25, Ltd., Class E (g),(h),(j) | | 3M SOFR+ 7.140% | | 12.728 | | 7/20/2034 | | | 2,105,490 | |

| | 500,000 | | | OCP CLO 2020-20, Ltd., Class E (g),(h),(j) | | 3M SOFR+ 7.660% | | 13.203 | | 10/9/2033 | | | 495,269 | |

| | 3,000,000 | | | PennantPark CLO III, Ltd., Class E (g),(h),(j) | | 3M SOFR+ 8.140% | | 13.747 | | 10/22/2032 | | | 2,860,904 | |

| | 2,000,000 | | | PPM CLO 2022-6, Ltd., Class E (g),(h),(j) | | 3M SOFR + 8.210% | | 13.798 | | 1/20/2031 | | | 1,955,733 | |

| | 400,000 | | | Regatta Funding LP 2013-2A, Class DR2 (b),(g),(h),(j) | | 3M SOFR+ 6.950% | | 12.520 | | 1/15/2029 | | | 389,617 | |

| | 7,000,000 | | | Regatta XXII Funding, Ltd., Class E (b),(g),(h),(j) | | 3M SOFR + 7.190% | | 12.516 | | 7/20/2035 | | | 6,973,780 | |

| | 2,800,000 | | | Sandstone Peak II Ltd 2023-2 (b),(g),(j) | | 3M SOFR + 8.790% | | 13.938 | | 7/20/2036 | | | 2,782,700 | |

| | 2,000,000 | | | Saratoga Investment Corp. CLO 2013-1, Ltd., Class F1R3 (g),(h),(j) | | 3M SOFR+ 10.000% | | 15.250 | | 4/20/2033 | | | 1,678,971 | |

| | 500,000 | | | VCP CLO II, Ltd., Class E (b),(g),(h),(j) | | 3M SOFR+ 8.400% | | 13.970 | | 4/15/2031 | | | 484,397 | |

| | 3,000,000 | | | Venture 45 CLO, Ltd., Class E (b),(g),(j) | | 3M SOFR + 7.700% | | 13.026 | | 7/20/2035 | | | 2,240,373 | |

| | | | | Total Collateralized Loan Obligations - Debt (Cost$76,072,290) | | | | | | | | | 75,927,965 | |

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | Collateralized Loan Obligations - Equity - 6.53% | | | | | | | | | | |

| | 4,060,000 | | | Allegro CLO XV, Ltd., Class SUB (a),(b),(g),(j),(k) | | | | 21.47 | | 7/20/2035 | | $ | 3,083,397 | |

| | 2,980,000 | | | Apex Credit CLO 2021, Ltd., Class SUB (a),(b),(g),(j),(k) | | | | 19.97 | | 7/18/2034 | | | 1,899,699 | |

| | 3,000,000 | | | Atlas Senior Loan Fund XVII, Ltd., Class SUB (a),(b),(g),(j),(k) | | | | 23.46 | | 10/20/2034 | | | 1,705,177 | |

| | 2,585,233 | | | Brightwood Capital MM CLO 2023-1A Sub1 Ltd (a),(b),(g),(j),(k) | | | | 14.56 | | 10/15/2035 | | | 2,275,005 | |

| | 5,500,000 | | | Dryden 98 CLO, Ltd., Class SUB (a),(b),(g),(j),(k) | | | | 19.90 | | 4/20/2035 | | | 4,014,436 | |

| | 3,750,000 | | | Elevation CLO 2021-15, Ltd., Class SUB (a),(b),(g),(j),(k) | | | | 16.31 | | 1/5/2035 | | | 1,856,645 | |

| | 250,000 | | | LCM 31, Ltd., Class INC (a),(b),(g),(j),(k) | | | | 22.01 | | 1/20/2032 | | | 128,819 | |

| | 2,750,000 | | | Marble Point CLO XXI, Ltd., Class Inc (a),(b),(g),(j),(k) | | | | 17.29 | | 10/17/2051 | | | 1,573,534 | |

| | 5,000,000 | | | Steele Creek CLO 2022-1, Ltd., Class SUB (a),(b),(g),(j),(k) | | | | 19.80 | | 4/15/2035 | | | 3,280,832 | |

| | 2,300,000 | | | Trinitas CLO VIII, Ltd., Class SUB (a),(b),(g),(j),(k) | | | | 10.59 | | 7/20/2117 | | | 688,084 | |

| | | | | Total Collateralized Loan Obligations - Equity (Cost$25,031,461) | | | | | | | | | 20,505,628 | |

| | | | | | | | | | | | | | | |

| | | | | Commercial Mortgage-Backed Securities - 19.81% | | | | | | | | | | |

| | 391,000 | | | BPR Trust 2021-TY, Class D (g),(h),(j) | | 1M SOFR + 2.464% | | 7.655 | | 9/15/2038 | | | 367,107 | |

| | 1,785,235 | | | BX Trust 2022-PSB, Class E (g),(h),(j) | | 1M SOFR + 6.337% | | 11.669 | | 8/15/2039 | | | 1,787,825 | |

| | 3,570,470 | | | BX Trust 2022-PSB, Class F (g),(h),(j) | | 1M SOFR + 7.333% | | 12.665 | | 8/15/2039 | | | 3,559,738 | |

| | 1,380,514 | | | BX Trust 2023-VLT2, Class C (g),(h),(j) | | 1M SOFR + 4.176% | | 9.508 | | 6/15/2040 | | | 1,374,965 | |

| | 2,098,537 | | | BX Trust 2023-VLT2, Class D (g),(h),(j) | | 1M SOFR + 4.774% | | 10.106 | | 6/15/2040 | | | 2,091,679 | |

| | 520,949 | | | BX Trust 2023-VLT2, Class E (g),(h),(j) | | 1M SOFR + 5.871% | | 11.203 | | 6/15/2040 | | | 522,378 | |

| | 3,924,118 | | | Campus Drive Secured Lease-Backed Pass-Though Trust, Series C (a),(h),(j) | | | | 6.912 | | 6/15/2058 | | | 2,291,685 | |

| | 400,000 | | | CSMC 2020-TMIC, Class C (g),(h),(j) | | 1M SOFR + 7.365% | | 11.955 | | 12/9/2023 | | | 398,523 | |

| | 4,500,000 | | | CXP Trust 2022-CXP1, Class E (g),(h),(j) | | 1M SOFR + 4.545% | | 9.877 | | 12/15/2038 | | | 3,866,173 | |

| | 1,500,000 | | | CXP Trust 2022-CXP1, Class F (g),(h),(j) | | 1M SOFR + 5.461% | | 10.793 | | 12/15/2038 | | | 926,339 | |

| | 190,098 | | | Extended Stay America Trust 2021-ESH, Class D (g),(h),(j) | | 1M SOFR + 2.364% | | 7.455 | | 7/15/2038 | | | 186,774 | |

| | 2,946,512 | | | Extended Stay America Trust 2021-ESH, Class E (g),(h),(j) | | 1M SOFR + 2.964% | | 8.055 | | 7/15/2038 | | | 2,892,575 | |

| | 9,382,406 | | | Extended Stay America Trust 2021-ESH, Class F (g),(h),(j) | | 1M SOFR + 3.814% | | 8.905 | | 7/15/2038 | | | 9,193,940 | |

| | 4,034,600 | | | ILPT Commercial Mortgage Trust 2022-LPF2, Class E (g),(h),(j) | | 1M SOFR + 5.940% | | 11.272 | | 10/15/2039 | | | 4,035,713 | |

| | 4,037,768 | | | LAQ 2023-LAQ Mortgage Trust, Class D (g),(h),(j) | | 1M SOFR + 4.188% | | 9.499 | | 3/15/2036 | | | 4,036,172 | |

| | 3,710,000 | | | One New York Plaza Trust 2020-1NYP, Class B (g),(h),(j) | | 1M SOFR + 1.614% | | 10.244 | | 1/15/2036 | | | 3,385,793 | |

| | 3,400,000 | | | One New York Plaza Trust 2020-1NYP, Class C (g),(h),(j) | | 1M SOFR + 2.314% | | 6.884 | | 1/15/2036 | | | 2,933,634 | |

| | 1,500,000 | | | One New York Plaza Trust 2020-1NYP, Class D (g),(h),(j) | | 1M SOFR + 2.864% | | 6.162 | | 1/15/2036 | | | 1,159,329 | |

| | 2,900,000 | | | PGA National Resort Trust 2023-RSRT, Class C (g),(h),(j) | | 1M SOFR + 3.789% | | 9.121 | | 5/15/2033 | | | 2,897,646 | |

| | 1,370,000 | | | PGA National Resort Trust 2023-RSRT, Class D (g),(h),(j) | | 1M SOFR + 4.588% | | 9.923 | | 5/15/2033 | | | 1,377,136 | |

| | 1,811,000 | | | TWO VA Repack Trust Class B-2, Series B2 (a),(h),(j),(l) | | | | — | | 11/15/2033 | | | 604,874 | |

| | 177,084 | | | VA Gilbert AZ Subordinated Note Lease-Backed Pass -Through Trust (a),(h),(j) | | | | 12.997 | | 3/15/2034 | | | 200,814 | |

| | 4,010,000 | | | Wells Fargo Commercial Mortgage Trust 2021-FCMT, Class D (g),(h),(j) | | 1M SOFR + 3.614% | | 13.149 | | 5/15/2031 | | | 3,736,510 | |

| | 1,000,000 | | | Wells Fargo Commercial Mortgage Trust 2021-FCMT, Class F (g),(h),(j) | | 1M SOFR + 6.010% | | 11.105 | | 5/15/2031 | | | 929,468 | |

| | 7,500,000 | | | WMRK Commercial Mortgage Trust 2022-WMRK, Class E (g),(h),(j) | | 1M SOFR + 5.676% | | 11.008 | | 11/15/2035 | | | 7,448,690 | |

| | | | | Total Commercial Mortgage-Backed Securities (Cost$64,052,250) | | | | | | | | | 62,205,480 | |

| | | | | | | | | | | | | | | |

| Cost Basis ($) | | | | | | | | | | | | |

| | | | | Direct Real Estate - 20.49% | | | | | | | | | | |

| | 6,927,834 | | | 1902 Park Avenue (Los Angeles) Owner, L.P. (a),(d) | | | | 7,144,478 | |

| | 5,107,443 | | | 3816-3822 W Jefferson Blvd (a) | | | | 4,908,552 | |

| | 3,840,582 | | | 4707 W Jefferson Blvd (a),(e) | | | | 3,063,409 | |

| | 4,408,174 | | | 4901 W Jefferson Blvd - Los Angeles, CA (a),(e) | | | | 4,222,470 | |

| | 15,025,000 | | | Del Mar Terrace - Phoenix, AZ (a),(d) | | | | 14,202,188 | |

| | 13,671,116 | | | EPIC Dallas (a),(d) | | | | 16,374,709 | |

| | 16,876,244 | | | Sora Multifamily Residential Property (a) | | | | 9,463,484 | |

| | 5,141,761 | | | Vale at the Parks - DC (a),(d) | | | | 4,965,143 | |

| | | | | Total Direct Real Estate (Cost$70,998,154) | | | | 64,344,433 | |

| | | | | | | | | | | | | | | |

| Principal | | | | | | | | | | | | |

| Amount ($) | | | | | | | | | | | | |

| | | | | Loan Accumulation Facility - 0.52% | | | | | | | | | | |

| | 1,623,750 | | | Allegro CLO XVI, Ltd, Warehouse (a),(b),(c),(g) | | 3M SOFR + 14.500% | | 14.500 | | 5/5/2025 | | | 1,623,750 | |

| | | | | Total Loan Accumulation Facility (Cost$1,623,750) | | | | | | | | | | |

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | Real Estate-Related Securities - 7.66% | | | | | | | | | | |

| | | | | Other - 7.66% | | | | | | | | | | |

| | 1,645,000 | | | IENTC 2, LLC (a),(c),(d),(g) | | 1M SOFR + 9.750% | | 15.066 | | 3/31/2031 | | $ | 1,645,000 | |

| | 6,815,000 | | | IENTC 2, LLC DDTL B-1 (a),(c),(d),(g) | | 1M SOFR + 9.750% | | 15.066 | | 3/31/2031 | | | 6,815,000 | |

| | 10,381,385 | | | Society Las Olas - PMG Greybook Riverfront I LLC (a),(c),(d),(g) | | 1M SOFR + 1.470% | | 6.800 | | 10/7/2024 | | | 10,371,004 | |

| | 5,291,016 | | | Society Las Olas 301 - S 1st Avenue Holdings LLC (a),(c),(d),(g) | | 1M SOFR + 6.823% | | 12.151 | | 10/7/2024 | | | 5,226,752 | |

| | | | | Total Real Estate-Related Securities (Cost$24,130,979) | | | | | | | | | 24,057,756 | |

| | | | | | | | | | | | | | | |

| Shares | | | | | | | Expiration Date | | Strike Price | | | |

| | | | | Warrant — 0.0% (m) | | | | | | | | | | |

| | | | | Internet Media & Services - 0.0% (m) | | | | 6,970 | |

| | 7,576 | | | RumbleON, Inc. (a),(b),(c),(e) | | | | 8/14/2028 | | $33.00 | | | | |

| | | | | Total Warrant (Cost $83,469) | | | | | |

| | | | | | | | | | | | | | | |

| | | | | Short-Term Investments - 5.66% | | | | | |

| | | | | Money Market Funds - 5.66% | | | | | |

| | 39,249,639 | | | First American Treasury Obligations Fund, Class Z, 5.23% (n),(o) (Cost $17,770,670) | | | | 17,770,670 | |

| | | | | | | | | | | | | | | |

| | | | | Total Investments 108.78% (Cost $356,009,584) | | | $ | 341,559,902 | |

| | | | | Liabilities in Excess of Other Assets - (-8.78%) | | | | (27,573,821 | ) |

| | | | | Net Assets (100.00%) | | | $ | 313,986,081 | |

| (a) | Fair value of this security was determined using significant, unobservable inputs and was determined in accordance with Rule 2a-5 under the Investment Company Act of 1940, as amended (the “1940 Act”). |

| (b) | A co-investment, completed under an order for exemptive relief granted by the U.S. Securities and Exchange Commission (“SEC”) on August 4, 2020, that is advised by the OFS Adviser. |

| (d) | A co-investment, completed under an order for exemptive relief granted by the SEC on August 4,2020, that is advised by the CIM Sub-Adviser. |

| (e) | Non-income producing security. |

| (f) | Investment in affiliate. See also footnotes (b), (d) and (i). |

| (g) | Variable or floating rate security, the interest rate of which adjusts periodically based on changes in current interest rates and prepayments on the underlying pool of assets. |

| (h) | A co-investment under the “Mass Mutual” no action letters. |

| (i) | This Investment or portion thereof was not funded as of September 30, 2023. The Fund had $9,381,183 at par value in unfunded commitments as of September 30, 2023. |

| (j) | Security exempt from registration under Rule 144A or Section 4(2) of the Securities Act of 1933. The security may be resold in transactions exempt from registration, normally to qualified institutional buyers. As of September 30, 2023 the total market value of 144A securities is $154,646,216 or 49.26% of net assets. |

| (k) | Collateralized loan obligation (“CLO”) subordinated notes are residual positions in the CLO vehicle. CLO subordinated notes are entitled to distributions that are generally equal to the residual cash flows of the underlying securities less contractual payments to debt holders and fund expenses. The effective yield is estimated based upon the amount and timing of these distributions in addition to the estimated amount of terminal distribution. Effective yields for the CLO equity positions are updated generally once a quarter in connection with a transaction, such as an add-on purchase, refinancing or reset. The estimated yield and investment cost may ultimately not be realized. Estimated yields are periodically adjusted based on information reported by the CLO as of the date of determination. |

| (m) | Percentage rounds to less than 0.1%. |

| (n) | Rate disclosed is the seven day effective yield as of June 30, 2023. |

| (o) | A portion of this security is held as collateral for total return swaps. |

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Schedule of Investments |

Restricted Securities

| | | Acquisition | | | | | | | | Market Value as a | |

| Issuer Description | | Date | | Cost | | | Market Value | | | Percentage of Net Assets | |

| 24 Seven, Inc., Term Loan | | 1/28/2022 | | $ | 4,254,100 | | | $ | 4,171,209 | | | | 1.33 | % |

| AIDC Intermediate Co. 2, LLC, Term Loan | | 7/22/2022 | | | 2,499,398 | | | | 2,525,163 | | | | 0.80 | % |

| Allegro CLO XVI, Ltd, Warehouse | | 5/5/2023 | | | 1,623,750 | | | | 1,623,750 | | | | 0.52 | % |

| Boca Home Care Holdings Revolver | | 2/25/2022 | | | 574,839 | | | | 559,161 | | | | 0.18 | % |

| Boca Home Care Holdings, Inc. DDTL | | 2/25/2022 | | | 4,940,904 | | | | 4,816,824 | | | | 1.53 | % |

| Boca Homecare Holdings, Inc. (Equity) | | 2/25/2022 | | | 580,645 | | | | 421,800 | | | | 0.13 | % |

| CGA Holdings, Inc., Class A | | 3/3/2023 | | | 155,086 | | | | 154,820 | | | | 0.05 | % |

| CVAUSA Management, LLC Primary DDTL | | 5/22/2023 | | | 1,183,256 | | | | 1,165,507 | | | | 0.37 | % |

| CVAUSA Management, LLC Secondary DDTL | | 5/22/2023 | | | 495,316 | | | | 487,886 | | | | 0.16 | % |

| CVAUSA Management, LLC, Revolver, TL | | 5/22/2023 | | | 285,714 | | | | 281,429 | | | | 0.09 | % |

| CVAUSA Management, LLC, Term Loan | | 5/22/2023 | | | 1,991,747 | | | | 2,005,179 | | | | 0.64 | % |

| EOS-Metasource Intermediate, Inc., DDC | | 5/17/2022 | | | 1,485,000 | | | | 1,413,000 | | | | 0.45 | % |

| EOS-Metasource Intermediate, Inc., TL | | 5/17/2022 | | | 3,428,954 | | | | 3,255,788 | | | | 1.04 | % |

| Exponential Power, Inc., TL | | 5/17/2023 | | | 2,948,965 | | | | 2,955,000 | | | | 0.94 | % |

| Honor HN Buyer, Inc. Delayed Draw Term Loan | | 10/15/2021 | | | 715,677 | | | | 715,677 | | | | 0.23 | % |

| Honor HN Buyer, Inc. Revolver | | 10/15/2021 | | | 132,013 | | | | 132,013 | | | | 0.04 | % |

| Honor HN Buyer, Inc. Term Loan | | 10/15/2021 | | | 1,114,809 | | | | 1,130,299 | | | | 0.36 | % |

| Honor HN Buyer, Inc. Term Loan 1st Amendment Health Network | | 10/15/2021 | | | 791,254 | | | | 796,001 | | | | 0.25 | % |

| IENTC 1, LLC | | 3/31/2022 | | | 3,763,895 | | | | 6,212,460 | | | | 1.98 | % |

| IENTC 2, LLC | | 3/31/2022 | | | 1,645,000 | | | | 1,645,000 | | | | 0.52 | % |

| IENTC 2, LLC DDTL B-1 | | 3/31/2022 | | | 6,815,000 | | | | 6,815,000 | | | | 2.17 | % |

| Kreg LLC, Revolver | | 12/20/2021 | | | 162,228 | | | | 151,467 | | | | 0.05 | % |

| Kreg LLC, Term Loan | | 12/20/2021 | | | 2,052,469 | | | | 1,917,466 | | | | 0.61 | % |

| One GI Intermediate LLC, Revolver Upsize | | 12/13/2021 | | | 333,333 | | | | 313,667 | | | | 0.10 | % |

| One GI Intermediate LLC, Tranche B DDTL | | 12/13/2021 | | | 1,711,895 | | | | 1,622,049 | | | | 0.52 | % |

| One GI Intermediate LLC, Tranche C DDTL | | 12/13/2021 | | | 914,329 | | | | 860,441 | | | | 0.27 | % |

| PSB Group, LLC, Term Loan (Last Out) May 2023 | | 5/1/2023 | | | 1,981,985 | | | | 1,996,000 | | | | 0.64 | % |

| Rumbleon, INC. TL | | 8/31/2021 | | | 1,307,915 | | | | 1,246,353 | | | | 0.40 | % |

| RumbleOn, Inc., Delayed Draw Term Loan | | 8/31/2021 | | | 500,022 | | | | 458,520 | | | | 0.15 | % |

| RumbleON, Inc., Warrant | | 8/31/2021 | | | 83,469 | | | | 6,970 | | | | 0.00 | % |

| Shiftkey, Revolver | | 6/21/2022 | | | 147,059 | | | | 143,382 | | | | 0.05 | % |

| Shiftkey, Term Loan | | 6/21/2022 | | | 2,311,236 | | | | 2,271,177 | | | | 0.72 | % |

| Society Las Olas - PMG Greybook Riverfront I LLC | | 9/23/2021 | | | 10,379,962 | | | | 10,371,004 | | | | 3.30 | % |

| Society Las Olas 301 - S 1st Avenue Holdings LLC | | 6/7/2022 | | | 5,291,016 | | | | 5,226,752 | | | | 1.66 | % |

| Spear Education Holdings, LLC Term A Loan | | 2/10/2023 | | | 2,917,665 | | | | 2,952,165 | | | | 0.94 | % |

| Spectrum Vision Partners, LLC | | 5/5/2023 | | | 3,959,512 | | | | 3,977,910 | | | | 1.27 | % |

| SS Acquisition LLC, Delayed Draw Term Loan | | 12/30/2021 | | | 1,430,180 | | | | 1,440,000 | | | | 0.46 | % |

| SS Acquisition LLC, Term Loan | | 12/30/2021 | | | 2,976,874 | | | | 3,000,000 | | | | 0.96 | % |

| | | | | $ | 79,886,471 | | | $ | 81,238,289 | | | | 25.88 | % |

Other than as described above, we do not “control” and are not an “affiliate” of any of our portfolio investments, each as defined in the 1940 Act. In general, under the 1940 Act, we would be presumed to “control” a portfolio investment if we owned 25% or more of its voting securities and would be an “affiliate” of a portfolio investment if we owned 5% or more of its voting securities.

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Schedule of Investments |

TOTAL RETURN SWAP CONTRACTS (a)

| | | | | | | | | | | | | | | Net Unrealized | |

| | | | | Notional | | | | | Termination | | | | | Appreciation | |

| Counterparty | | Reference Entity/Obligation | | Amount | | | Fund Pays | | Date | | Value | | | Depreciation | |

| Citibank, N.A. | | ABG Intermediate Holdings 2 LLC TLB 1L, 1M SOFR + 4.00 | | $ | 690,848 | | | 3M SOFR + 1.80% | | 12/21/2028 | | $ | 700,466 | | | $ | 9,618 | |

| Citibank, N.A. | | ABG Intermediate Holdings 2 LLC, TL B 2 DDTL, 3M SOFR + 4.00 | | | 131,739 | | | 3M SOFR + 1.80% | | 12/21/2028 | | | 133,913 | | | | 2,174 | |

| Citibank, N.A. | | Academy, Ltd., 1M SOFR + 3.75 | | | 565,618 | | | 3M SOFR + 1.80% | | 11/5/2027 | | | 566,289 | | | | 671 | |

| Citibank, N.A. | | Acrisure LLC, 1M SOFR + 3.50 | | | 584,969 | | | 3M SOFR + 1.80% | | 2/15/2027 | | | 579,348 | | | | (5,621 | ) |

| Citibank, N.A. | | Acrisure LLC, 1M SOFR + 3.75 | | | 544,698 | | | 3M SOFR + 1.80% | | 2/15/2027 | | | 541,975 | | | | (2,723 | ) |

| Citibank, N.A. | | Acrisure LLC, 1M SOFR + 4.25 | | | 146,983 | | | 3M SOFR + 1.80% | | 2/15/2027 | | | 147,704 | | | | 721 | |

| Citibank, N.A. | | ADMI Corp. TLB3 1L, 1M SOFR + 3.75 | | | 789,478 | | | 3M SOFR + 1.80% | | 12/23/2027 | | | 741,118 | | | | (48,360 | ) |

| Citibank, N.A. | | Advantage Sales & Marketing, Inc., 3M SOFR + 4.50 | | | 748,967 | | | 3M SOFR + 1.80% | | 10/28/2027 | | | 731,840 | | | | (17,127 | ) |

| Citibank, N.A. | | Aegion Corp., 1M SOFR + 4.75 | | | 811,461 | | | 3M SOFR + 1.80% | | 5/17/2028 | | | 812,999 | | | | 1,538 | |

| Citibank, N.A. | | AHP Health Partners, Inc., 1M SOFR + 3.50 | | | 284,466 | | | 3M SOFR + 1.80% | | 8/24/2028 | | | 285,570 | | | | 1,104 | |

| Citibank, N.A. | | AI Aqua Merger Sub, Inc., 1M SOFR + 3.75 | | | 740,170 | | | 3M SOFR + 1.80% | | 7/31/2028 | | | 738,164 | | | | (2,006 | ) |

| Citibank, N.A. | | Allen Media LLC, 3M SOFR + 5.50 | | | 1,502,061 | | | 3M SOFR + 1.80% | | 2/10/2027 | | | 1,353,934 | | | | (148,127 | ) |

| Citibank, N.A. | | Allied Universal Holdco LLC, 1M SOFR + 3.75 | | | 489,388 | | | 3M SOFR + 1.80% | | 5/14/2028 | | | 475,311 | | | | (14,077 | ) |

| Citibank, N.A. | | Amentum Government Services Holdings LLC TLB 1L, 1M SOFR + 4.00 | | | 347,993 | | | 3M SOFR + 1.80% | | 2/15/2029 | | | 345,483 | | | | (2,510 | ) |

| Citibank, N.A. | | American Airlines, Inc. Seventh Amendment Extended Term Loan, 1M SOFR + 2.75 | | | 498,125 | | | 3M SOFR + 1.80% | | 2/7/2028 | | | 497,045 | | | | (1,080 | ) |

| Citibank, N.A. | | American Axle & Manufacturing, Inc., TL, 6M SOFR + 3.50 | | | 993,699 | | | 3M SOFR + 1.80% | | 12/13/2029 | | | 1,001,097 | | | | 7,398 | |

| Citibank, N.A. | | AMYNTA AGENCY BORROWER INC, TLB, 1M SOFR + 5.00 | | | 910,152 | | | 3M SOFR + 1.80% | | 2/28/2028 | | | 914,154 | | | | 4,002 | |

| Citibank, N.A. | | AP Core Holdings II LLC, 1M SOFR + 5.50 (b) | | | 1,097,877 | | | 3M SOFR + 1.80% | | 9/1/2027 | | | 1,090,761 | | | | (7,116 | ) |

| Citibank, N.A. | | AppLovin Corporation Aug-2023 TL, 1M SOFR + 3.10 | | | 691,031 | | | 3M SOFR + 1.80% | | 8/19/2030 | | | 692,624 | | | | 1,593 | |

| Citibank, N.A. | | Aramark Services, Inc. U.S. Term B-6 Loan, 1M SOFR + 1.75 | | | 130,375 | | | 3M SOFR + 1.80% | | 6/22/2030 | | | 131,846 | | | | 1,471 | |

| Citibank, N.A. | | Arches Buyer, Inc., 1M SOFR + 3.25 | | | 832,835 | | | 3M SOFR + 1.80% | | 12/6/2027 | | | 825,716 | | | | (7,119 | ) |

| Citibank, N.A. | | ASGN Incorporated Term Loan B, 1M SOFR + 2.25 (b) | | | 997,510 | | | 3M SOFR + 1.80% | | 8/31/2030 | | | 1,005,000 | | | | 7,490 | |

| Citibank, N.A. | | Asurion, LLC NEW B-11 TERM LOAN, 1M SOFR + 4.25 | | | 368,628 | | | 3M SOFR + 1.80% | | 8/19/2028 | | | 370,123 | | | | 1,495 | |

| Citibank, N.A. | | Asurion, LLC TLB 1L, 1M SOFR + 4.00 | | | 593,762 | | | 3M SOFR + 1.80% | | 8/21/2028 | | | 602,671 | | | | 8,909 | |

| Citibank, N.A. | | Athenahealth Group Inc. TLB 1L, 1M SOFR + 3.25 | | | 439,580 | | | 3M SOFR + 1.80% | | 2/15/2029 | | | 434,254 | | | | (5,326 | ) |

| Citibank, N.A. | | Athletico Physical Therapy TLB, 3M SOFR + 4.25 | | | 896,338 | | | 3M SOFR + 1.80% | | 2/15/2029 | | | 757,687 | | | | (138,651 | ) |

| Citibank, N.A. | | Autokiniton US Holdings, Inc., 1M SOFR + 4.50 | | | 1,077,527 | | | 3M SOFR + 1.80% | | 4/6/2028 | | | 1,056,409 | | | | (21,118 | ) |

| Citibank, N.A. | | Axalta Coating Systems US Holdings Repriced TL, 1M SOFR + 2.50 | | | 728,324 | | | 3M SOFR + 1.80% | | 12/20/2029 | | | 732,795 | | | | 4,471 | |

| Citibank, N.A. | | Bakemark Holdings, Inc., 1M SOFR + 4.00 | | | 490,632 | | | 3M SOFR + 1.80% | | 9/5/2028 | | | 488,806 | | | | (1,826 | ) |

| Citibank, N.A. | | Banijay Entertainment S.A.S., Banijay 1L, 1M SOFR + 3.75 | | | 358,278 | | | 3M SOFR + 1.80% | | 3/2/2028 | | | 362,277 | | | | 3,999 | |

| Citibank, N.A. | | Barnes Group First Lien TLB, 1M SOFR + 3.00 | | | 496,264 | | | 3M SOFR + 1.80% | | 8/11/2030 | | | 501,375 | | | | 5,111 | |

| Citibank, N.A. | | BCPE North Star US Holdco 2, Inc. TL 1L, 3M SOFR + 4.00 (b) | | | 946,917 | | | 3M SOFR + 1.80% | | 6/9/2028 | | | 855,829 | | | | (91,088 | ) |

| Citibank, N.A. | | BJ’s Wholesale Club, Inc., 1M SOFR + 2.75 | | | 198,427 | | | 3M SOFR + 1.80% | | 2/3/2027 | | | 199,320 | | | | 893 | |

| Citibank, N.A. | | BROOKFIELD WEC HOLDINGS INC TL 1L, 1M SOFR + 3.75 | | | 201,619 | | | 3M SOFR + 1.80% | | 8/1/2025 | | | 207,520 | | | | 5,901 | |

| Citibank, N.A. | | BROWN GROUP HOLDING, LLC TLB2 1L, 1M SOFR + 3.75 | | | 197,581 | | | 3M SOFR + 1.80% | | 7/2/2029 | | | 199,622 | | | | 2,041 | |

| Citibank, N.A. | | Burlington Coat Factory Warehouse Corp., 1M SOFR + 2.00 | | | 537,017 | | | 3M SOFR + 1.80% | | 6/26/2028 | | | 538,663 | | | | 1,646 | |

| Citibank, N.A. | | Buzz Merger Sub LTD. Initial Term Loan, 1M SOFR + 2.75 | | | 500,000 | | | 3M SOFR + 1.80% | | 1/29/2027 | | | 500,158 | | | | 158 | |

| Citibank, N.A. | | Cablevision Lightpath LLC Initial Term Loan, 1M SOFR + 3.25 | | | 737,126 | | | 3M SOFR + 1.80% | | 11/30/2027 | | | 742,500 | | | | 5,374 | |

| Citibank, N.A. | | CCRR Parent, Inc. TLB, 1M SOFR + 3.75 | | | 881,407 | | | 3M SOFR + 1.80% | | 3/5/2028 | | | 842,730 | | | | (38,677 | ) |

| Citibank, N.A. | | CDK GLOBAL, INC.TLB 1L, 3M SOFR + 4.25 | | | 247,877 | | | 3M SOFR + 1.80% | | 7/6/2029 | | | 254,087 | | | | 6,210 | |

| Citibank, N.A. | | Charlotte Buyer, Inc.; Curo Health Services, LLC, 1M SOFR + 5.25 | | | 936,497 | | | 3M SOFR + 1.80% | | 2/11/2028 | | | 986,025 | | | | 49,528 | |

| Citibank, N.A. | | Chart Industries, Inc., 1M SOFR + 3.75 (b) | | | 195,692 | | | 3M SOFR + 1.80% | | 3/15/2030 | | | 200,104 | | | | 4,412 | |

| Citibank, N.A. | | Charter Next Generation, Inc., 1M SOFR + 3.75 | | | 729,246 | | | 3M SOFR + 1.80% | | 12/1/2027 | | | 728,674 | | | | (572 | ) |

| Citibank, N.A. | | CHG Healthcare Services Inc TLB 2023, 1M SOFR + 3.75 | | | 247,500 | | | 3M SOFR + 1.80% | | 9/30/2028 | | | 250,156 | | | | 2,656 | |

| Citibank, N.A. | | CHG Healthcare Services, Inc., 1M SOFR + 3.25 | | | 345,450 | | | 3M SOFR + 1.80% | | 9/29/2028 | | | 345,761 | | | | 311 | |

| Citibank, N.A. | | City Brewing Co. LLC, 3M SOFR + 3.50 | | | 219,097 | | | 3M SOFR + 1.80% | | 4/5/2028 | | | 144,464 | | | | (74,633 | ) |

| Citibank, N.A. | | Clarios Global LP TL, 1M SOFR + 3.75 | | | 287,078 | | | 3M SOFR + 1.80% | | 5/6/2030 | | | 288,327 | | | | 1,249 | |

| Citibank, N.A. | | Clydesdale Acquisition Holdings, Inc., 1M SOFR + 4.18 | | | 789,100 | | | 3M SOFR + 1.80% | | 4/13/2029 | | | 802,454 | | | | 13,354 | |

| Citibank, N.A. | | Cogeco Communications Finance USA LP, Amendment No. 5 Incremental Term B Loan, 1M SOFR + 2.50 | | | 491,877 | | | 3M SOFR + 1.80% | | 9/1/2028 | | | 487,580 | | | | (4,297 | ) |

| Citibank, N.A. | | Compass Power Generation LLC, 1M SOFR + 4.25 | | | 921,302 | | | 3M SOFR + 1.80% | | 4/14/2029 | | | 933,440 | | | | 12,138 | |

| Citibank, N.A. | | Conduent Business Services LLC, 1M SOFR + 4.25 | | | 988,339 | | | 3M SOFR + 1.80% | | 10/15/2028 | | | 988,902 | | | | 563 | |

| Citibank, N.A. | | Connect Finco Sarl, 1M SOFR + 3.50 | | | 981,780 | | | 3M SOFR + 1.80% | | 12/12/2026 | | | 963,965 | | | | (17,815 | ) |

| Citibank, N.A. | | Core & Main LP, 1M SOFR + 2.50 | | | 407,580 | | | 3M SOFR + 1.80% | | 7/27/2028 | | | 408,895 | | | | 1,315 | |

| Citibank, N.A. | | Corel Corp., 3M SOFR + 5.00 | | | 609,177 | | | 3M SOFR + 1.80% | | 7/2/2026 | | | 608,623 | | | | (554 | ) |

| Citibank, N.A. | | CoreLogic, Inc., 1M SOFR + 3.50 | | | 204,267 | | | 3M SOFR + 1.80% | | 6/2/2028 | | | 189,898 | | | | (14,369 | ) |

| Citibank, N.A. | | CORGI BIDCO, INC.TL 1L, 3M SOFR + 5.00 | | | 172,674 | | | 3M SOFR + 1.80% | | 10/15/2029 | | | 180,950 | | | | 8,276 | |

| Citibank, N.A. | | Cornerstone Building Brands, Inc., 1M SOFR + 3.25 | | | 245,399 | | | 3M SOFR + 1.80% | | 4/12/2028 | | | 270,406 | | | | 25,007 | |

| Citibank, N.A. | | Cornerstone OnDemand, Inc., TL, 3M SOFR + 3.75 | | | 684,806 | | | 3M SOFR + 1.80% | | 10/16/2028 | | | 653,972 | | | | (30,834 | ) |

| Citibank, N.A. | | Covanta Holding Corporation, TLB, 1M SOFR + 3.00 | | | 525,375 | | | 3M SOFR + 1.80% | | 11/30/2028 | | | 526,584 | | | | 1,209 | |

| Citibank, N.A. | | Covanta Holding Corporation, TLC, 1M SOFR + 3.00 | | | 39,403 | | | 3M SOFR + 1.80% | | 11/30/2028 | | | 39,494 | | | | 91 | |

| Citibank, N.A. | | CP Atlas Buyer, Inc., 1M SOFR + 3.75 | | | 392,673 | | | 3M SOFR + 1.80% | | 11/23/2027 | | | 371,484 | | | | (21,189 | ) |

| Citibank, N.A. | | Dermatology Intermediate Holdings III, Inc. 1L, 3M SOFR +4.25 | | | 55,130 | | | 3M SOFR + 1.80% | | 3/26/2029 | | | 54,875 | | | | (255 | ) |

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Schedule of Investments |

TOTAL RETURN SWAP CONTRACTS (a)

| | | | | | | | | | | | | | | Net Unrealized | |

| | | | | Notional | | | | | Termination | | | | | Appreciation | |

| Counterparty | | Reference Entity/Obligation | | Amount | | | Fund Pays | | Date | | Value | | | Depreciation | |

| Citibank, N.A. | | Dermatology Intermediate Holdings III, Inc. TLB 1L, 3M SOFR + 4.25 | | | 289,494 | | | 3M SOFR + 1.80% | | 3/26/2029 | | | 293,025 | | | | 3,531 | |

| Citibank, N.A. | | DexKo Global Inc., TLB, 3M SOFR + 3.75 | | | 640,231 | | | 3M SOFR + 1.80% | | 10/4/2028 | | | 627,584 | | | | (12,647 | ) |

| Citibank, N.A. | | DG Investment Intermediate Holdings 2, Inc., 1M SOFR + 3.75 | | | 739,928 | | | 3M SOFR + 1.80% | | 3/31/2028 | | | 729,142 | | | | (10,786 | ) |

| Citibank, N.A. | | DIRECTV Financing LLC, 1M SOFR + 5.00 | | | 1,179,206 | | | 3M SOFR + 1.80% | | 8/2/2027 | | | 1,159,502 | | | | (19,704 | ) |

| Citibank, N.A. | | East West Manufacturing, LLC TLB 1L, 3M SOFR + 5.75 (b) | | | 641,258 | | | 3M SOFR + 1.80% | | 12/22/2028 | | | 560,906 | | | | (80,352 | ) |

| Citibank, N.A. | | Electrical Components International, Inc. Initial Term Loan (First Lien), 1M SOFR + 4.25 (b) | | | 497,539 | | | 3M SOFR + 1.80% | | 6/26/2025 | | | 496,250 | | | | (1,289 | ) |

| Citibank, N.A. | | Element Materials Tech Group US Holdings Delayed TL, 3M SOFR + 4.25 (b) | | | 55,449 | | | 3M SOFR + 1.80% | | 6/22/2029 | | | 54,941 | | | | (508 | ) |

| Citibank, N.A. | | Element Materials Tech Group US Holdings Inc. TL, 3M SOFR + 4.25 | | | 119,603 | | | 3M SOFR + 1.80% | | 6/22/2029 | | | 119,038 | | | | (565 | ) |

| Citibank, N.A. | | EnergySolutions, LLC 2023 TL, 1M SOFR + 4.00 (b) | | | 545,723 | | | 3M SOFR + 1.80% | | 9/18/2030 | | | 549,868 | | | | 4,145 | |

| Citibank, N.A. | | Fertitta Entertainment, LLC TLB 1L, 1M SOFR + 4.00 | | | 342,788 | | | 3M SOFR + 1.80% | | 1/29/2029 | | | 340,598 | | | | (2,190 | ) |

| Citibank, N.A. | | Gainwell Acquisition Corp., 1M SOFR + 4.25 | | | 490,965 | | | 3M SOFR + 1.80% | | 2/1/2029 | | | 495,542 | | | | 4,577 | |

| Citibank, N.A. | | Gainwell Acquisition Corp., 3M SOFR + 4.00 | | | 232,080 | | | 3M SOFR + 1.80% | | 10/1/2027 | | | 226,663 | | | | (5,417 | ) |

| Citibank, N.A. | | Garda World Security Corp., 1M SOFR + 4.25 | | | 593,103 | | | 3M SOFR + 1.80% | | 10/30/2026 | | | 593,182 | | | | 79 | |

| Citibank, N.A. | | GIP Pilot Acquisition Partners L.P. - 2023 TL 2023 TL, 1M SOFR + 3.00 (b) | | | 248,750 | | | 3M SOFR + 1.80% | | 9/19/2030 | | | 249,688 | | | | 938 | |

| Citibank, N.A. | | Gloves Buyer, Inc. Non-Fung Inc 1LTL, 1M SOFR + 5.00 (b) | | | 727,627 | | | 3M SOFR + 1.80% | | 12/29/2027 | | | 730,313 | | | | 2,686 | |

| Citibank, N.A. | | Great Outdoors Group, LLC TLB 1L, 1M SOFR + 3.75 | | | 1,469,713 | | | 3M SOFR + 1.80% | | 3/6/2028 | | | 1,476,262 | | | | 6,549 | |

| Citibank, N.A. | | Help/Systems Holdings, Inc., 3M SOFR + 4.00 | | | 488,636 | | | 3M SOFR + 1.80% | | 11/19/2026 | | | 469,499 | | | | (19,137 | ) |

| Citibank, N.A. | | Hunter Douglas Inc. TLB 1L, 3M SOFR +3.50 | | | 492,989 | | | 3M SOFR + 1.80% | | 2/25/2029 | | | 483,244 | | | | (9,745 | ) |

| Citibank, N.A. | | Hyperion Materials and Technologies Inc Initial Term Loans, 3M SOFR + 4.25 | | | 747,545 | | | 3M SOFR + 1.80% | | 8/30/2028 | | | 749,531 | | | | 1,986 | |

| Citibank, N.A. | | Indy US Holdco LLC, 1M SOFR + 6.25 | | | 813,093 | | | 3M SOFR + 1.80% | | 3/5/2028 | | | 887,877 | | | | 74,784 | |

| Citibank, N.A. | | Installed Building Products, Inc. Repriced TLB, 1M SOFR + 2.00 | | | 500,000 | | | 3M SOFR + 1.80% | | 12/14/2028 | | | 500,003 | | | | 3 | |

| Citibank, N.A. | | Ivanti Software, Inc., 3M SOFR + 4.25 | | | 657,114 | | | 3M SOFR + 1.80% | | 12/1/2027 | | | 571,519 | | | | (85,595 | ) |

| Citibank, N.A. | | Jadex, Inc., 1M SOFR + 4.75 (b) | | | 359,051 | | | 3M SOFR + 1.80% | | 2/11/2028 | | | 340,567 | | | | (18,484 | ) |

| Citibank, N.A. | | Janus International Group LLC, Amendment No. 6 Refinancing Term Loan, 1M SOFR + 3.25 | | | 235,755 | | | 3M SOFR + 1.80% | | 8/5/2030 | | | 237,649 | | | | 1,894 | |

| Citibank, N.A. | | KKR Apple Bidco, LLC, 1M SOFR + 2.75 | | | 945,663 | | | 3M SOFR + 1.80% | | 9/22/2028 | | | 942,143 | | | | (3,520 | ) |

| Citibank, N.A. | | KKR Apple Bidco, LLC, 1M SOFR + 4.00 | | | 224,138 | | | 3M SOFR + 1.80% | | 9/22/2028 | | | 236,312 | | | | 12,174 | |

| Citibank, N.A. | | KNS Midco Corp., 1M SOFR + 6.25 (b) | | | 573,750 | | | 3M SOFR + 1.80% | | 4/16/2027 | | | 490,556 | | | | (83,194 | ) |

| Citibank, N.A. | | LBM Acquisition LLC, 1M SOFR + 3.75 | | | 634,659 | | | 3M SOFR + 1.80% | | 12/17/2027 | | | 621,527 | | | | (13,132 | ) |

| Citibank, N.A. | | Liftoff Mobile, Inc., 1M SOFR + 3.75 | | | 489,890 | | | 3M SOFR + 1.80% | | 10/2/2028 | | | 470,718 | | | | (19,172 | ) |

| Citibank, N.A. | | LogMeIn, Inc. TLB, 3M SOFR + 4.75 | | | 684,225 | | | 3M SOFR + 1.80% | | 8/31/2027 | | | 457,318 | | | | (226,907 | ) |

| Citibank, N.A. | | LSF11 A5 HOLDCO LLC, TLB, 1M SOFR + 4.25 | | | 643,752 | | | 3M SOFR + 1.80% | | 10/15/2028 | | | 646,490 | | | | 2,738 | |

| Citibank, N.A. | | LSF9 ATLANTIS HOLDINGS, LLC, 3M SOFR + 7.25 | | | 1,146,461 | | | 3M SOFR + 1.80% | | 3/29/2029 | | | 1,137,582 | | | | (8,879 | ) |

| Citibank, N.A. | | Madison IAQ LLC, 1M SOFR + 3.25 | | | 639,847 | | | 3M SOFR + 1.80% | | 6/21/2028 | | | 634,194 | | | | (5,653 | ) |

| Citibank, N.A. | | Magenta Buyer LLC, 3M SOFR + 5.00 | | | 795,266 | | | 3M SOFR + 1.80% | | 7/27/2028 | | | 597,545 | | | | (197,721 | ) |

| Citibank, N.A. | | McAfee Corp. TLB 1L, 1M SOFR + 3.75 | | | 910,127 | | | 3M SOFR + 1.80% | | 3/1/2029 | | | 894,139 | | | | (15,988 | ) |

| Citibank, N.A. | | McGraw-Hill Education, Inc., 1M SOFR + 4.75 | | | 721,339 | | | 3M SOFR + 1.80% | | 7/28/2028 | | | 714,691 | | | | (6,648 | ) |

| Citibank, N.A. | | Medline Industries, LP, Term Loan, 1M SOFR + 3.25 | | | 861,990 | | | 3M SOFR + 1.80% | | 10/23/2028 | | | 862,736 | | | | 746 | |

| Citibank, N.A. | | Mega Broadband Investments LLC Initial Term Loan, 3M SOFR + 3.00 | | | 488,125 | | | 3M SOFR + 1.80% | | 11/12/2027 | | | 489,220 | | | | 1,095 | |

| Citibank, N.A. | | MH Sub I LLC, 1M SOFR + 4.25 | | | 677,053 | | | 3M SOFR + 1.80% | | 5/3/2028 | | | 677,675 | | | | 622 | |

| Citibank, N.A. | | Midwest Physician Administrative Services LLC, 3M SOFR + 3.25 | | | 720,775 | | | 3M SOFR + 1.80% | | 3/13/2028 | | | 678,543 | | | | (42,232 | ) |

| Citibank, N.A. | | Mitchell International, Inc., 1M SOFR + 3.75 | | | 654,558 | | | 3M SOFR + 1.80% | | 10/16/2028 | | | 648,649 | | | | (5,909 | ) |

| Citibank, N.A. | | Mosel Bidco SE TLB, 1M SOFR + 4.75 | | | 198,000 | | | 3M SOFR + 1.80% | | 8/1/2030 | | | 200,250 | | | | 2,250 | |

| Citibank, N.A. | | Naked Juice LLC 3M SOFR + 3.25 | | | 985,520 | | | 3M SOFR + 1.80% | | 1/24/2029 | | | 941,487 | | | | (44,033 | ) |

| Citibank, N.A. | | Olaplex, Inc TL 1L, 1M SOFR + 3.50 | | | 350,871 | | | 3M SOFR + 1.80% | | 2/17/2029 | | | 300,782 | | | | (50,089 | ) |

| Citibank, N.A. | | Oldcastle Building Envelope Inc TLB 1L, 3M SOFR + 4.50 | | | 730,052 | | | 3M SOFR + 1.80% | | 4/30/2029 | | | 741,922 | | | | 11,870 | |

| Citibank, N.A. | | OpenText Corporation Repriced TLB, 1M SOFR + 2.75 | | | 500,000 | | | 3M SOFR + 1.80% | | 1/31/2030 | | | 500,655 | | | | 655 | |

| Citibank, N.A. | | PetSmart LLC, 1M SOFR + 3.75 | | | 1,273,394 | | | 3M SOFR + 1.80% | | 2/11/2028 | | | 1,275,013 | | | | 1,619 | |

| Citibank, N.A. | | Pitney Bowes INC.TL, 1M SOFR + 4.00 (b) | | | 747,078 | | | 3M SOFR + 1.80% | | 3/17/2028 | | | 723,646 | | | | (23,432 | ) |

| Citibank, N.A. | | Primary Products Finance LLC, 3M SOFR+ 4.00 | | | 247,862 | | | 3M SOFR + 1.80% | | 4/2/2029 | | | 249,481 | | | | 1,619 | |

| Citibank, N.A. | | Proofpoint, Inc., 1M SOFR + 3.25 | | | 701,225 | | | 3M SOFR + 1.80% | | 8/31/2028 | | | 698,636 | | | | (2,589 | ) |

| Citibank, N.A. | | Quest Borrower Limited TL 1L, 3M SOFR + 4.25 | | | 981,999 | | | 3M SOFR + 1.80% | | 2/1/2029 | | | 828,610 | | | | (153,389 | ) |

| Citibank, N.A. | | Redstone Holdco 2 LP, 1M SOFR + 4.75 | | | 831,305 | | | 3M SOFR + 1.80% | | 4/27/2028 | | | 808,856 | | | | (22,449 | ) |

| Citibank, N.A. | | Ring Container Technologies Group LLC, 1M SOFR + 3.50 | | | 385,221 | | | 3M SOFR + 1.80% | | 8/12/2028 | | | 387,985 | | | | 2,764 | |

| Citibank, N.A. | | Roper Industrial Products Investment Co LLC, TL, 3M SOFR + 4.50 | | | 96,491 | | | 3M SOFR + 1.80% | | 11/22/2029 | | | 100,089 | | | | 3,598 | |

| Citibank, N.A. | | Rough Country, LLC 1L, 3M SOFR + 3.25(b) | | | 1,253,409 | | | 3M SOFR + 1.80% | | 7/26/2028 | | | 1,228,102 | | | | (25,307 | ) |

| Citibank, N.A. | | Ryan Specialty Group LLC, 1M SOFR + 3.00 | | | 194,713 | | | 3M SOFR + 1.80% | | 9/1/2027 | | | 194,900 | | | | 187 | |

| Citibank, N.A. | | Scientific Games Holdings LP TLB 1L, 3M SOFR + 3.50 | | | 698,631 | | | 3M SOFR + 1.80% | | 4/4/2029 | | | 698,069 | | | | (562 | ) |

| Citibank, N.A. | | Select Medical Corp. Tranche B-1 Term Loan, 1M SOFR + 3.00 | | | 331,731 | | | 3M SOFR + 1.80% | | 3/6/2027 | | | 332,917 | | | | 1,186 | |

| Citibank, N.A. | | Simon & Schuster TLB, 1M SOFR + 4.00 (b) | | | 99,000 | | | 3M SOFR + 1.80% | | 11/27/2030 | | | 99,500 | | | | 500 | |

| Citibank, N.A. | | Sinclair Television Group, Inc. TLB4 1L, 1M SOFR + 3.75 | | | 570,985 | | | 3M SOFR + 1.80% | | 4/13/2029 | | | 418,092 | | | | (152,893 | ) |

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Schedule of Investments |

TOTAL RETURN SWAP CONTRACTS (a)

| | | | | | | | | | | | | | | Net Unrealized | |

| | | | | Notional | | | | | Termination | | | | | Appreciation | |

| Counterparty | | Reference Entity/Obligation | | Amount | | | Fund Pays | | Date | | Value | | | Depreciation | |

| Citibank, N.A. | | Sitel Worldwide Corp., 1M SOFR + 3.75 | | | 671,183 | | | 3M SOFR + 1.80% | | 8/27/2028 | | | 658,872 | | | | (12,311 | ) |

| Citibank, N.A. | | Sovos Brands Intermediate, Inc., 1M SOFR + 3.50 | | | 351,455 | | | 3M SOFR + 1.80% | | 6/8/2028 | | | 353,516 | | | | 2,061 | |

| Citibank, N.A. | | Specialty Building Products Holdings LLC, 1M SOFR + 3.75 | | | 492,622 | | | 3M SOFR + 1.80% | | 10/15/2028 | | | 489,254 | | | | (3,368 | ) |

| Citibank, N.A. | | Spring Education Group, Inc., 3M SOFR + 4.50 | | | 136,991 | | | 3M SOFR + 1.80% | | 9/28/2030 | | | 136,991 | | | | — | |

| Citibank, N.A. | | SRS Distribution Inc., 1M SOFR + 3.50 | | | 175,996 | | | 3M SOFR + 1.80% | | 6/2/2028 | | | 175,416 | | | | (580 | ) |

| Citibank, N.A. | | Sunshine Luxembourg VII S.a r.l., 3M SOFR + 3.75 | | | 953,122 | | | 3M SOFR + 1.80% | | 10/2/2026 | | | 951,481 | | | | (1,641 | ) |

| Citibank, N.A. | | Star Parent, Inc. TLB, 3M SOFR + 4.00 | | | 175,892 | | | 3M SOFR + 1.80% | | 9/30/2030 | | | 174,863 | | | | (1,029 | ) |

| Citibank, N.A. | | Teneo Holdings LLC, 1M SOFR + 5.25 | | | 1,033,068 | | | 3M SOFR + 1.80% | | 7/12/2025 | | | 1,037,452 | | | | 4,384 | |

| Citibank, N.A. | | Tenneco Inc. Cov-Lite TLB, 1M SOFR + 5.00 | | | 426,377 | | | 3M SOFR + 1.80% | | 11/17/2028 | | | 425,783 | | | | (594 | ) |

| Citibank, N.A. | | Tony’s Fresh Market / Cardenas Markets TLB 1L, 1M SOFR + 6.75 | | | 939,773 | | | 3M SOFR + 1.80% | | 8/1/2029 | | | 995,398 | | | | 55,625 | |

| Citibank, N.A. | | Topgolf Callaway Brands Corp, TLB, 1M SOFR + 3.50 | | | 594,102 | | | 3M SOFR + 1.80% | | 3/15/2030 | | | 592,831 | | | | (1,271 | ) |

| Citibank, N.A. | | TransDigm Inc., TLH, 3M SOFR + 3.25 | | | 486,676 | | | 3M SOFR + 1.80% | | 2/22/2027 | | | 496,226 | | | | 9,550 | |

| Citibank, N.A. | | TricorBraun Holdings, Inc., 1M SOFR + 3.25 | | | 331,397 | | | 3M SOFR + 1.80% | | 3/3/2028 | | | 328,231 | | | | (3,166 | ) |

| Citibank, N.A. | | Tronox Finance LLC August 2023 Loan, 1M SOFR + 3.50 | | | 247,500 | | | 3M SOFR + 1.80% | | 8/10/2028 | | | 248,250 | | | | 750 | |

| Citibank, N.A. | | TruGreen LP, 1M SOFR + 4.00 | | | 362,155 | | | 3M SOFR + 1.80% | | 11/2/2027 | | | 359,241 | | | | (2,914 | ) |

| Citibank, N.A. | | TTM Technologies, Inc. TLB 1L, 1M SOFR + 2.75 (b) | | | 82,530 | | | 3M SOFR + 1.80% | | 5/30/2030 | | | 83,542 | | | | 1,012 | |

| Citibank, N.A. | | U.S. Anesthesia Partners, Inc., 1M SOFR + 4.25 | | | 930,304 | | | 3M SOFR + 1.80% | | 10/2/2028 | | | 859,484 | | | | (70,820 | ) |

| Citibank, N.A. | | U.S. Silica Company TLB, 1M SOFR + 4.75 | | | 628,335 | | | 3M SOFR + 1.80% | | 3/25/2030 | | | 640,584 | | | | 12,249 | |

| Citibank, N.A. | | Virtusa Corporation TL 1L, 1M SOFR + 3.75 | | | 790,697 | | | 3M SOFR + 1.80% | | 2/15/2029 | | | 793,463 | | | | 2,766 | |

| Citibank, N.A. | | Watlow Electric Manufacturing Co., 3M SOFR + 3.75 | | | 1,038,894 | | | 3M SOFR + 1.80% | | 3/2/2028 | | | 1,033,011 | | | | (5,883 | ) |

| Citibank, N.A. | | WildBrain Ltd Initial Term Loan, 1M SOFR + 4.25 | | | 748,135 | | | 3M SOFR + 1.80% | | 3/24/2028 | | | 738,750 | | | | (9,385 | ) |

| Citibank, N.A. | | Worldpay 1L Term Loan, 1M SOFR + 3.00 | | | 271,364 | | | 3M SOFR + 1.80% | | 9/19/2030 | | | 272,827 | | | | 1,463 | |

| Citibank, N.A. | | WW International, Inc., 1M SOFR + 3.50 | | | 1,171,950 | | | 3M SOFR + 1.80% | | 4/13/2028 | | | 891,220 | | | | (280,730 | ) |

| Citibank, N.A. | | Xperi Corporation TLB , 1M SOFR + 3.50 | | | 794,981 | | | 3M SOFR + 1.80% | | 6/8/2028 | | | 796,914 | | | | 1,933 | |

| Citibank, N.A. | | Zelis Payments Buyer, Inc., 1M SOFR + 3.50 | | | 978,332 | | | 3M SOFR + 1.80% | | 9/30/2026 | | | 981,227 | | | | 2,895 | |

| | | | | $ | 85,807,765 | | | | | | | $ | 83,770,466 | | | $ | (2,037,299 | ) |

| (a) | The Fund’s interest in the total return swap transactions are held through a wholly-owned subsidiary of the Fund, RACR-FS, LLC, a Delaware Limited Liability Company. |

| (b) | Security is classified as Level 3 in the Fund’s fair value hierarchy (see Note 2). |

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Statement of Assets and Liabilities |

| | September 30, 2023 |

| ASSETS | | | | |

| Investments: | | | | |

| Unaffiliated Investments at fair value (cost $284,495,278) | | $ | 267,030,375 | |

| Affiliated Investments at fair value (cost $71,514,306) | | | 74,529,527 | |

| Cash | | | 1,212,343 | |

| Cash collateral for total return swaps | | | 21,478,969 | |

| Interest receivable | | | 3,915,890 | |

| Receivable for investments sold | | | 7,043,143 | |

| Receivable for Fund shares sold | | | 1,211,071 | |

| Unrealized appreciation on total return swap contracts | | | 443,580 | |

| Prepaid expenses and other assets | | | 142,069 | |

| TOTAL ASSETS | | $ | 377,006,967 | |

| | | | | |

| LIABILITIES | | | | |

| Payable for securities purchased | | | 12,179,944 | |

| Line of credit payable (Note 7) | | | 45,000,000 | |

| Unrealized depreciation on total return swap contracts | | | 2,480,879 | |

| Due to Advisor | | | 527,318 | |

| Administrative fees payable (Note 8) | | | 683,589 | |

| Professional fees payable | | | 444,755 | |

| Trustee fees payable (Note 8) | | | 353,185 | |

| Payable for Fund shares repurchased | | | 270 | |

| Transfer agency fees payable (Note 8) | | | 212,241 | |

| Custody fees payable | | | 20,140 | |

| Distribution fee payable (Note 8) | | | 19,975 | |

| Shareholder Servicing fees payable (Note 8) | | | 8,411 | |

| Accrued expenses and other liabilities | | | 1,090,179 | |

| TOTAL LIABILITIES | | | 63,020,886 | |

| COMMITMENTS AND CONTINGENCIES (Note 2) | | | | |

| NET ASSETS | | $ | 313,986,081 | |

| | | | | |

| NET ASSETS CONSIST OF | | | | |

| Paid-in capital | | $ | 320,660,547 | |

| Accumulated earnings | | | (6,674,466 | ) |

| NET ASSETS | | $ | 313,986,081 | |

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Statement of Assets and Liabilities |

| | September 30, 2023 |

| PRICING OF SHARES | | | | |

| Class A | | | | |

| Net Assets | | $ | 10,364,407 | |

| Shares of beneficial interest outstanding (unlimited number of authorized shares, no par value common stock authorized) | | | 424,355 | |

| Net asset value | | $ | 24.42 | |

| Maximum offering price per share (Maximum sales load of 5.75%) | | $ | 25.91 | |

| Class C | | | | |

| Net Assets | | | | |

| Shares of beneficial interest outstanding (unlimited number of authorized shares, no par value common stock authorized) | | $ | 12,302,623 | |

| Net asset value (a) | | | 518,546 | |

| Maximum offering price per share | | $ | 23.73 | |

| Class I | | | | |

| Net Assets | | $ | 290,728,226 | |

| Shares of beneficial interest outstanding (unlimited number of authorized shares, no par value common stock authorized) | | | 11,824,907 | |

| Net asset value | | $ | 24.59 | |

| Maximum offering price per share | | | | |

| Class L | | | | |

| Net Assets | | $ | 590,825 | |

| Shares of beneficial interest outstanding (unlimited number of authorized shares, no par value common stock authorized) | | | 24,478 | |

| Net asset value | | $ | 24.14 | |

| Maximum offering price per share (Maximum sales load of 4.25%) | | $ | 25.21 | |

| (a) | Subject to early-withdrawal charge. Redemption price varies based on length of time held (Note 2). |

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Statement of Operations |

| | For the Year Ended September 30, 2023 |

| INVESTMENT INCOME | | | | |

| Interest income | | $ | 30,284,888 | |

| Income from affiliated investments | | | 2,351,186 | |

| Total Investment Income | | | 32,636,074 | |

| | | | | |

| EXPENSES | | | | |

| Management fees (Note 8) | | | 4,482,850 | |

| Incentive Fees (Note 8) | | | 3,897,500 | |

| Shareholder Servicing fees (Note 8) | | | | |

| Class A | | | 18,878 | |

| Class C | | | 29,006 | |

| Class L | | | 934 | |

| Distribution fees (Note 8) | | | | |

| Class C | | | 87,019 | |

| Class L | | | 934 | |

| Networking fees | | | | |

| Class I | | | 348,447 | |

| Interest expense (Note 7) | | | 3,267,891 | |

| Administrative fees (Note 8) | | | 2,753,343 | |

| Professional fees | | | 1,205,783 | |

| Transfer agency fees (Note 8) | | | 200,022 | |

| Trustees fees (Note 8) | | | 289,493 | |

| Printing fees | | | 234,123 | |

| Taxes | | | 159,125 | |

| Custody fees | | | 117,998 | |

| State Registration fees | | | 61,494 | |

| Insurance fees | | | 30,879 | |

| Other expenses | | | 870,533 | |

| Total Expenses | | | 18,056,252 | |

| Expenses reimbursed by Advisor (Note 8) | | | (4,024,557 | ) |

| Net Expenses | | | 14,031,695 | |

| Net Investment Income | | | 18,604,379 | |

| Net realized gain on investments | | | 575,609 | |

| Net realized loss on total return swap contracts | | | (224,905 | ) |

| Net change in unrealized depreciation on affiliated investments | | | (10,956,654 | ) |

| Net change in unrealized depreciation on unaffiliated investments | | | (12,387,359 | ) |

| Net change in unrealized appreciation on total return swap contracts | | | 3,298,067 | |

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | | | (19,695,242 | ) |

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (1,090,863 | ) |

See Notes to Consolidated Financial Statements.

| CIM Real Assets & Credit Fund | Consolidated Statements of Changes in Net Assets |

| | | For the Fiscal | | | For the Fiscal | |

| | | Year Ended | | | Year Ended | |