Receivables with non-prime obligors have higher default rates than Receivables with prime obligors, which may affect the performance of the Receivables

[Some of] [Substantially all of] the Receivables are obligations of non-prime obligors who do not qualify for conventional motor vehicle financing as a result of, among other things, a lack of or adverse credit history, low income levels or the inability to provide adequate down payments. While Carvana’s underwriting criteria are designed to establish that the obligor would be a reasonable credit risk, the Receivables will nonetheless experience higher default rates than a portfolio of Receivables with all prime obligors. In the event of a default, repossession of the related financed vehicle is the most likely alternative for recovery. As a result, losses on Charged-Off Receivables are likely because net liquidation proceeds from the sale of repossessed vehicles are expected to be insufficient to satisfy amounts owed by the related obligors under the Receivables in full. See “The Receivables—Certain Legal Considerations of the Receivables.” In addition, the concentration of Receivables with non-prime obligors may also have the effect of heightening many of the other risks, including those relating to general macroeconomic forces and economic downturns, described in this “Risk Factors” section. If delinquencies and losses create shortfalls, which exceed the available credit enhancement, you may experience delays in payments due to you and you could suffer a loss on your Notes. [For information regarding non-prime obligors, see “Historical Performance—Delinquencies and Net Losses—Delinquency Experience (Non-Prime Obligors)” and “Historical Performance—Delinquencies and Net Losses—Net Loss Experience (Non-Prime Obligors).”]

Carvana’s proprietary credit scoring system may not perform as expected and may fail to properly quantify the credit risks associated with Carvana’s customers, resulting in higher than anticipated delinquencies and credit losses on the Receivables

Carvana has developed, and revises from time to time, complex proprietary credit scoring models that use traditional and non-traditional variables to assess credit risk and determine credit offer parameters. There is no guarantee that Carvana’s credit scoring models will perform as intended.

If Carvana made errors in developing or validating its credit scoring models, trained or validated its models on incomplete, inaccurate, or biased data sets, or used model development or validation techniques that result in bias or instability, Carvana may fail to gauge credit risk as expected and make credit decisions that result in higher delinquencies and credit losses.

Carvana’s credit scoring models are generally developed and validated on samples of consumer data and loan performance pertaining to a distinct period of time in the past. Changes in the macroeconomy, consumer behavior, creditor reporting behavior, and third party data reporting methods between a model’s development and validation periods and between a model’s development period and when the model is used by Carvana could materially impact the relationship between inputs to Carvana’s models and expected credit outcomes, resulting in a reduction of the ability of Carvana’s credit scoring models to assess credit risk as expected.

Carvana’s credit scoring models rely heavily on data obtained from third parties, including credit bureaus. If the data Carvana obtains from third parties for use in its models is incomplete, inaccurate, biased, or not provided consistent with the methods and practices used by such third parties during the time period of the sample upon which Carvana built or validated our models, the output of Carvana’s models may be unreliable and fail to properly quantify credit risk, resulting in it making credit decisions that result in higher delinquencies and credit losses.

Information provided to Carvana by customers, credit data partners, and others may be incorrect or fraudulent, and Carvana’s Verification Process may fail to ensure that reliable information is incorporated into the extension of credit offers to Carvana’s customers, resulting in higher than anticipated delinquencies and credit losses on the Receivables

In deciding whether to extend credit to customers and the parameters of such credit offers, Carvana relies heavily on information furnished to it by customers, credit data partners, and others, and such data may be incorrect or fraudulent. Carvana has developed a Verification Process that attempts to ensure that information considered by its proprietary financing technology belongs to the customer(s) receiving a credit offer, and that such information is reasonably accurate. There is no guarantee that Carvana’s Verification Process will perform as expected, detect fraudulent or incorrect data, or otherwise achieve its goals, which may result in credit loss and delinquency rates on the Receivables being higher than anticipated.

Further, Carvana utilizes identity and fraud checks based on customer provided documents and inputs, as well as data provided by external databases to authenticate each customer’s identity. There have been instances in the past in which these checks have failed or been ineffective, and there is a risk that these checks could also fail or be ineffective in the future, which could result in significant losses related to fraud being borne by investors in the Securities. Fraudulent activity or significant increases in fraudulent activity could also lead to regulatory intervention, negatively impacting the operating results and reputation of both Carvana and the Servicer.

Economic developments may adversely affect the performance of the Receivables and the market value of your Securities

The United States has in the past experienced and in the future may experience a recession or period of economic contraction. During the economic downturn following the 2008 financial crisis, elevated unemployment, decreases in home values, and reductions in available credit led to increased delinquency and default rates on retail installment contracts. If another financial crisis or economic downturn were to occur again, [including as a result of COVID-19,] delinquencies and losses with respect to motor vehicle receivables could increase, which could result in losses on your Securities. In addition, decreased consumer demand for motor vehicles and an increase in the inventory of used motor vehicles may depress the price at which repossessed motor vehicles may be sold or delay the timing of those sales. If the default rate on the Receivables increases and the price at which the related vehicles may be sold declines, you may experience losses with respect to your Securities.

Market factors may reduce the value of used vehicles, which could result in increased losses on the Receivables

[Obligors with lower FICO scores generally are less capable of making payments on their loans than obligors with higher FICO scores and are therefore more likely to experience repossession.] Vehicles that are repossessed are typically sold at vehicle auctions. The pricing of used cars is affected by the supply and demand for those cars, which, in turn, is affected by consumer demand and tastes, recalls, economic factors (including the price of gasoline and closure of dealerships), the introduction and pricing of new car models and other factors, including legislation related to emissions and fuel efficiency. Decisions by a manufacturer with respect to new vehicle production and brands, pricing and incentives may affect used car prices, particularly those for the same or similar models. Adverse changes in these factors may depress the price at which repossessed motor vehicles may be sold or delay the timing of those sales. An increase in the supply or a decrease in the demand for used cars may negatively impact the resale value of the vehicles securing the Receivables. Decreases in the value of those vehicles may, in turn, reduce the incentive of obligors to make payments on the Receivables and decrease the proceeds realized from vehicle repossessions, which could result in losses on the Securities.

Longer term Receivables may increase the frequency and amount of losses

The frequency and amount of losses may be greater for Receivables with longer terms, because these Receivables tend to have a somewhat greater frequency of delinquencies and defaults and because the slower rate of amortization of the principal balance of a longer term Receivable may result in a longer period during which the value of the related financed vehicle is less than the remaining principal balance of such Receivable. See “The Receivables—Distribution of the Receivables by Original Term to Maturity as of the [Initial] Cutoff Date” for the percentage of Receivables with original terms of greater than [72] months as of the [Initial] Cutoff Date.

Prepayments on and repurchases of the Receivables could shorten the average life of the Notes

Obligors may prepay the Receivables in full or in part at any time. We cannot predict the rate of prepayments on the Receivables. A variety of unpredictable economic, social, and other factors influence prepayment rates. In addition, the Receivables may be prepaid as a result of defaults, from credit life, disability or physical damage insurance, or, in limited circumstances, voluntarily by Carvana. Also, Carvana may be required to repurchase Receivables in specified circumstances and the Servicer (or its designee) may purchase all remaining Receivables pursuant to the optional redemption. See “The Transaction Documents—Sale and Assignment of Receivables.”

A prepayment, repurchase, purchase or liquidation of the Receivables, including liquidation of Charged-Off Receivables, could shorten the average life of the Notes.

[The yield on the Class N Notes will be more sensitive to prepayments and defaults on the Receivables, in particular prepayments and defaults on Receivables with a higher APR. If there are increased charge-offs, your yield or return on the Class N Notes will be reduced and may be less than your investment in the Class N Notes.]

You will bear all reinvestment risk resulting from a faster or slower rate of prepayment, repurchase or extension of the Receivables held by the [grantor] trust.

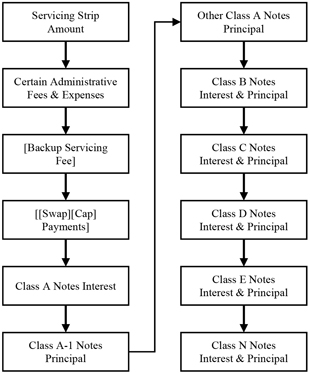

10