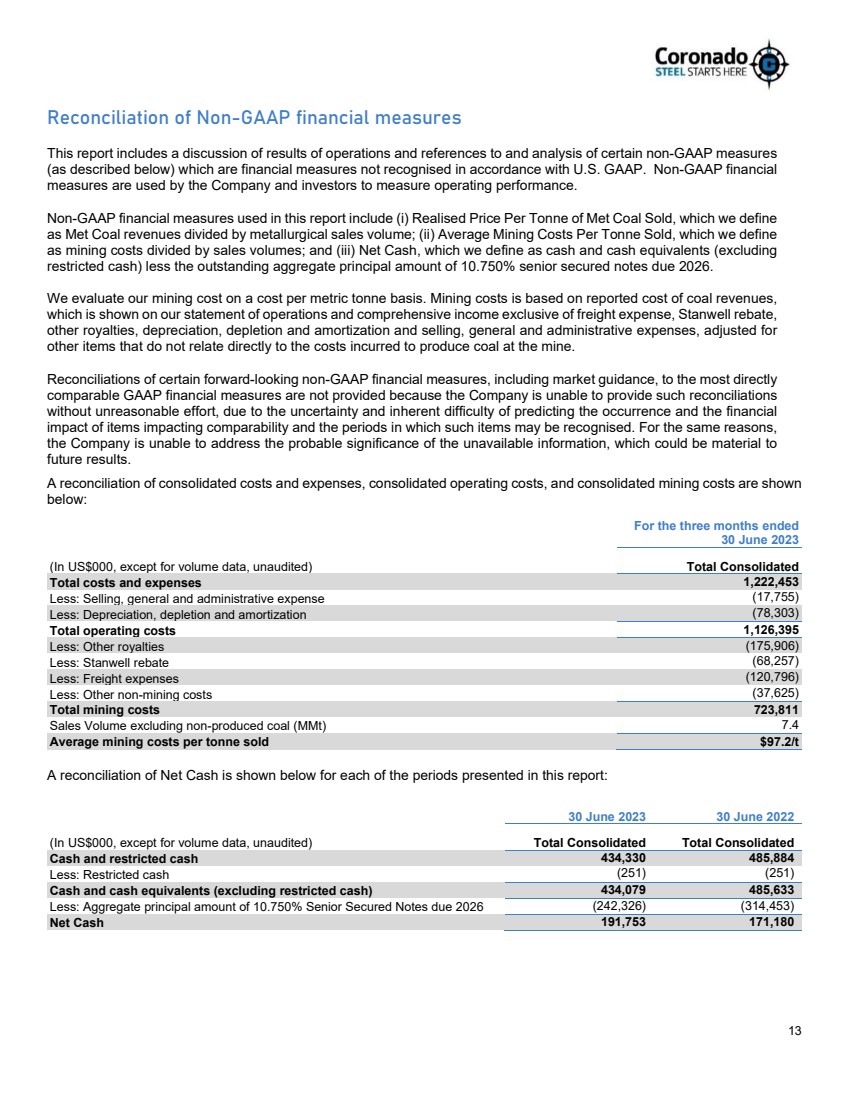

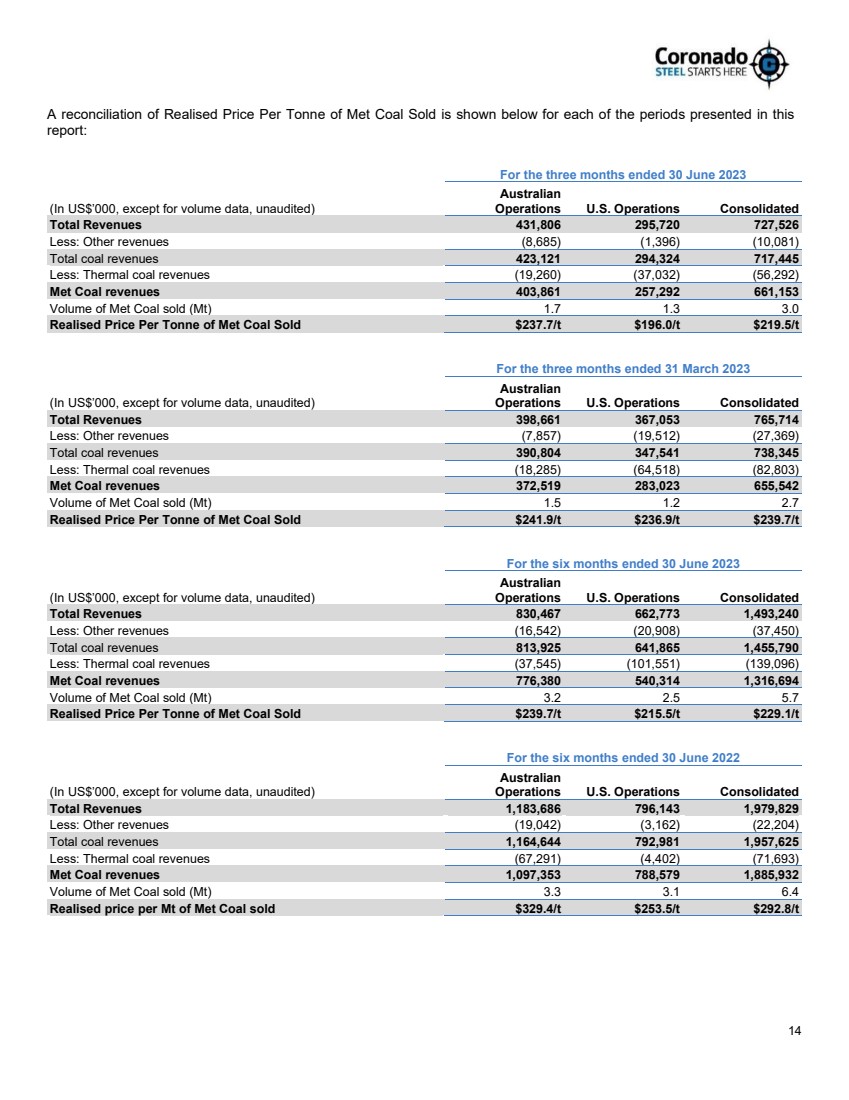

| 14 A reconciliation of Realised Price Per Tonne of Met Coal Sold is shown below for each of the periods presented in this report: For the three months ended 30 June 2023 (In US$’000, except for volume data, unaudited) Australian Operations U.S. Operations Consolidated Total Revenues 431,806 295,720 727,526 Less: Other revenues (8,685) (1,396) (10,081) Total coal revenues 423,121 294,324 717,445 Less: Thermal coal revenues (19,260) (37,032) (56,292) Met Coal revenues 403,861 257,292 661,153 Volume of Met Coal sold (Mt) 1.7 1.3 3.0 Realised Price Per Tonne of Met Coal Sold $237.7/t $196.0/t $219.5/t For the three months ended 31 March 2023 (In US$’000, except for volume data, unaudited) Australian Operations U.S. Operations Consolidated Total Revenues 398,661 367,053 765,714 Less: Other revenues (7,857) (19,512) (27,369) Total coal revenues 390,804 347,541 738,345 Less: Thermal coal revenues (18,285) (64,518) (82,803) Met Coal revenues 372,519 283,023 655,542 Volume of Met Coal sold (Mt) 1.5 1.2 2.7 Realised Price Per Tonne of Met Coal Sold $241.9/t $236.9/t $239.7/t For the six months ended 30 June 2023 (In US$’000, except for volume data, unaudited) Australian Operations U.S. Operations Consolidated Total Revenues 830,467 662,773 1,493,240 Less: Other revenues (16,542) (20,908) (37,450) Total coal revenues 813,925 641,865 1,455,790 Less: Thermal coal revenues (37,545) (101,551) (139,096) Met Coal revenues 776,380 540,314 1,316,694 Volume of Met Coal sold (Mt) 3.2 2.5 5.7 Realised Price Per Tonne of Met Coal Sold $239.7/t $215.5/t $229.1/t For the six months ended 30 June 2022 (In US$’000, except for volume data, unaudited) Australian Operations U.S. Operations Consolidated Total Revenues 1,183,686 796,143 1,979,829 Less: Other revenues (19,042) (3,162) (22,204) Total coal revenues 1,164,644 792,981 1,957,625 Less: Thermal coal revenues (67,291) (4,402) (71,693) Met Coal revenues 1,097,353 788,579 1,885,932 Volume of Met Coal sold (Mt) 3.3 3.1 6.4 Realised price per Mt of Met Coal sold $329.4/t $253.5/t $292.8/t |