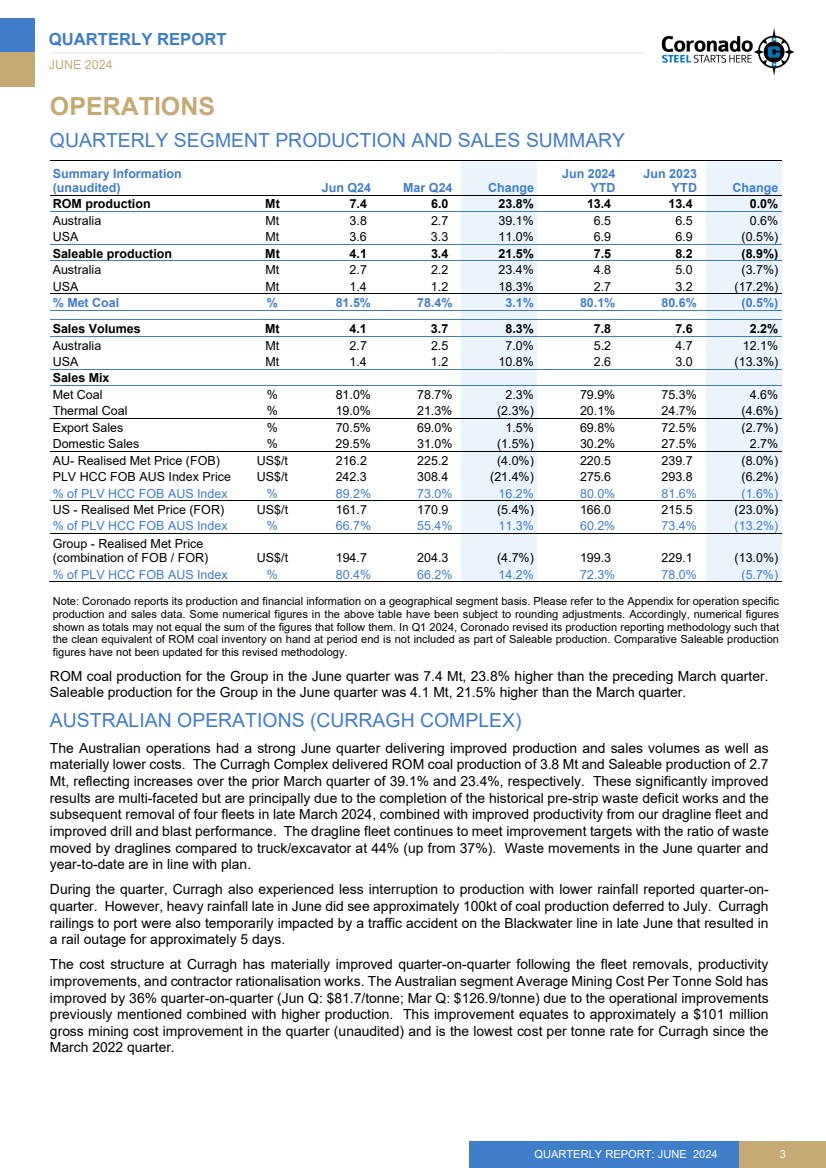

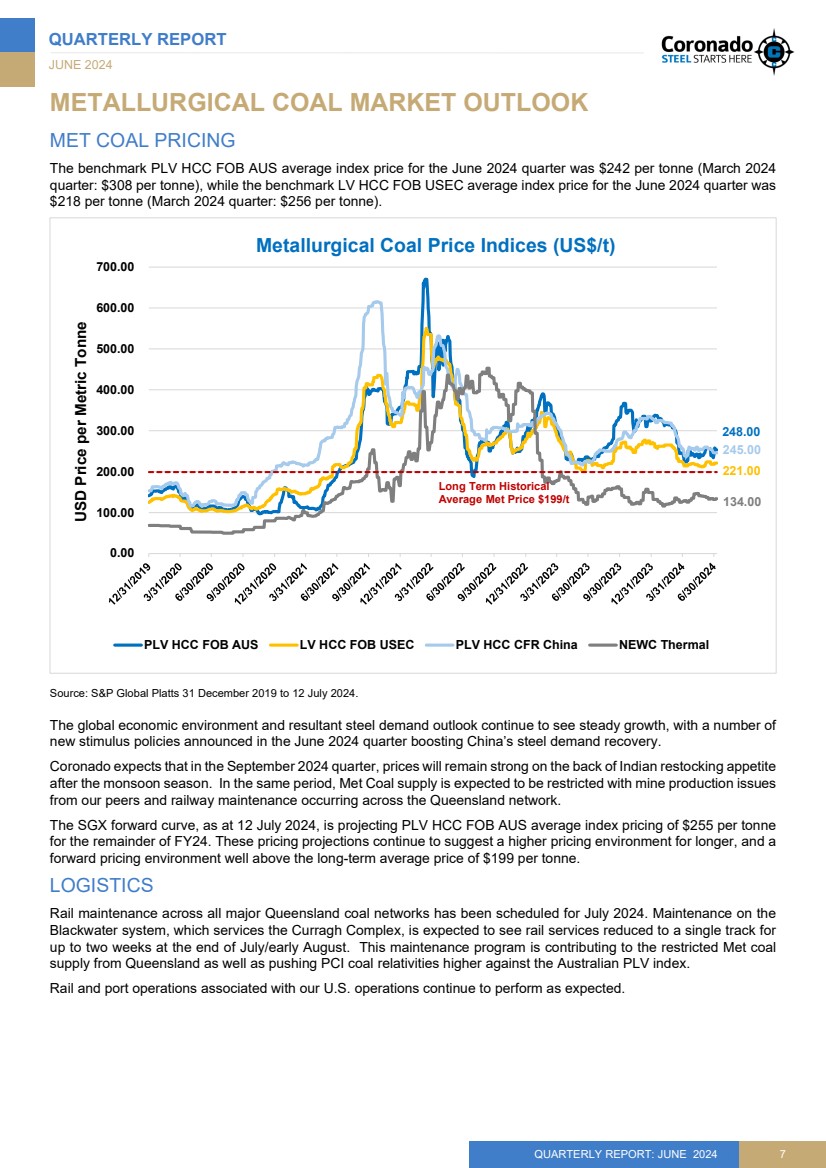

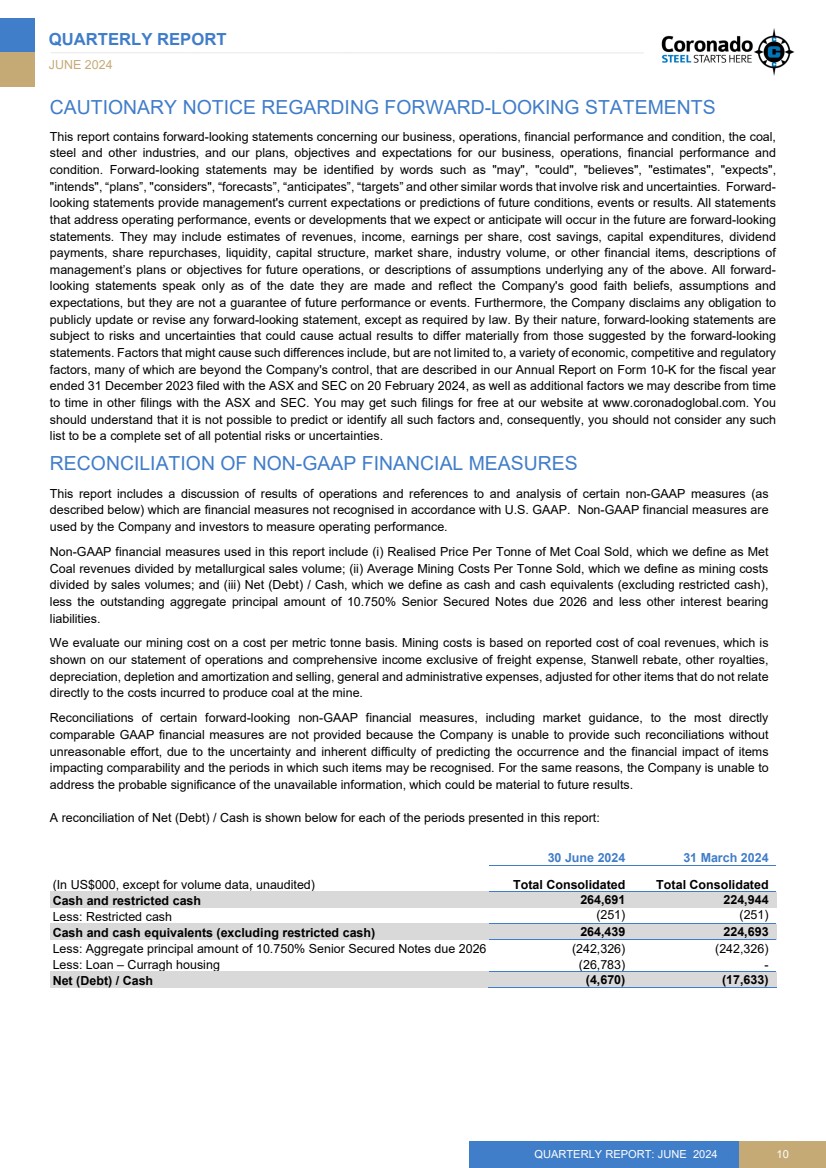

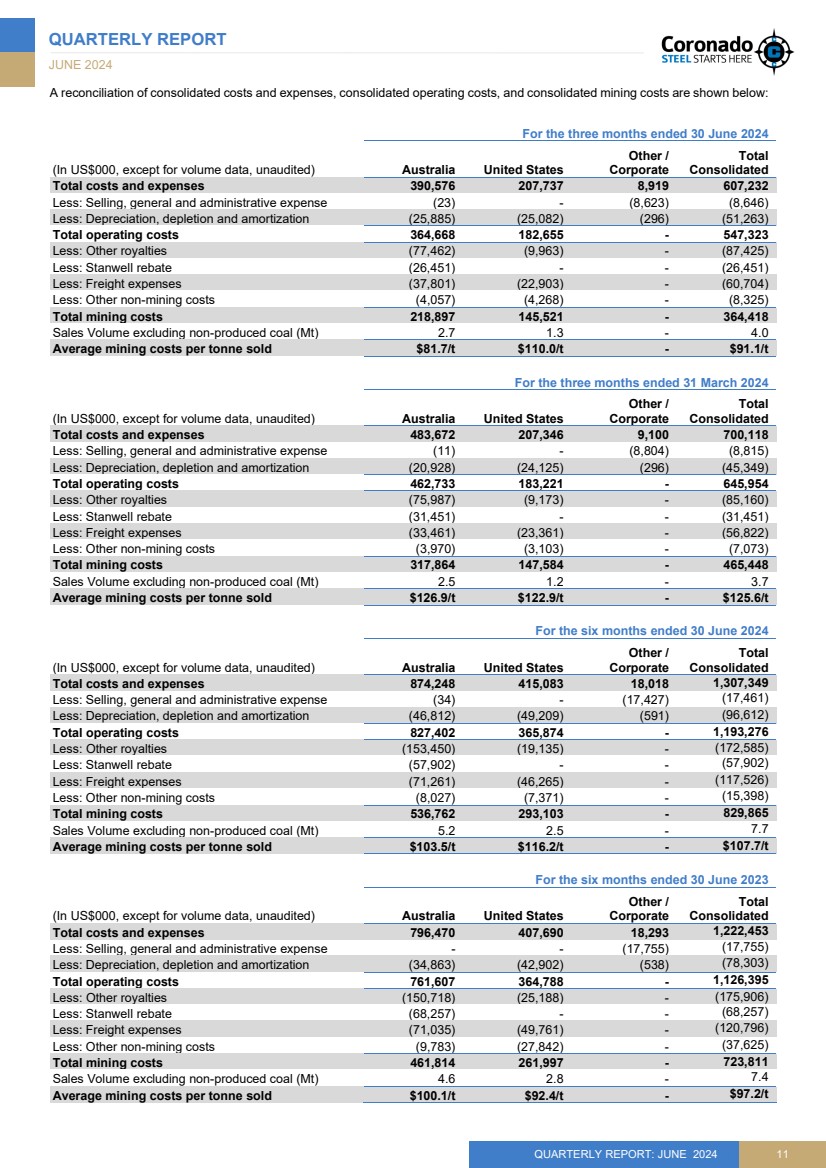

| QUARTERLY REPORT JUNE 2024 QUARTERLY REPORT: JUNE 2024 11 A reconciliation of consolidated costs and expenses, consolidated operating costs, and consolidated mining costs are shown below: For the three months ended 30 June 2024 (In US$000, except for volume data, unaudited) Australia United States Other / Corporate Total Consolidated Total costs and expenses 390,576 207,737 8,919 607,232 Less: Selling, general and administrative expense (23) - (8,623) (8,646) Less: Depreciation, depletion and amortization (25,885) (25,082) (296) (51,263) Total operating costs 364,668 182,655 - 547,323 Less: Other royalties (77,462) (9,963) - (87,425) Less: Stanwell rebate (26,451) - - (26,451) Less: Freight expenses (37,801) (22,903) - (60,704) Less: Other non-mining costs (4,057) (4,268) - (8,325) Total mining costs 218,897 145,521 - 364,418 Sales Volume excluding non-produced coal (Mt) 2.7 1.3 - 4.0 Average mining costs per tonne sold $81.7/t $110.0/t - $91.1/t For the three months ended 31 March 2024 (In US$000, except for volume data, unaudited) Australia United States Other / Corporate Total Consolidated Total costs and expenses 483,672 207,346 9,100 700,118 Less: Selling, general and administrative expense (11) - (8,804) (8,815) Less: Depreciation, depletion and amortization (20,928) (24,125) (296) (45,349) Total operating costs 462,733 183,221 - 645,954 Less: Other royalties (75,987) (9,173) - (85,160) Less: Stanwell rebate (31,451) - - (31,451) Less: Freight expenses (33,461) (23,361) - (56,822) Less: Other non-mining costs (3,970) (3,103) - (7,073) Total mining costs 317,864 147,584 - 465,448 Sales Volume excluding non-produced coal (Mt) 2.5 1.2 - 3.7 Average mining costs per tonne sold $126.9/t $122.9/t - $125.6/t For the six months ended 30 June 2024 (In US$000, except for volume data, unaudited) Australia United States Other / Corporate Total Consolidated Total costs and expenses 874,248 415,083 18,018 1,307,349 Less: Selling, general and administrative expense (34) - (17,427) (17,461) Less: Depreciation, depletion and amortization (46,812) (49,209) (591) (96,612) Total operating costs 827,402 365,874 - 1,193,276 Less: Other royalties (153,450) (19,135) - (172,585) Less: Stanwell rebate (57,902) - - (57,902) Less: Freight expenses (71,261) (46,265) - (117,526) Less: Other non-mining costs (8,027) (7,371) - (15,398) Total mining costs 536,762 293,103 - 829,865 Sales Volume excluding non-produced coal (Mt) 5.2 2.5 - 7.7 Average mining costs per tonne sold $103.5/t $116.2/t - $107.7/t For the six months ended 30 June 2023 (In US$000, except for volume data, unaudited) Australia United States Other / Corporate Total Consolidated Total costs and expenses 796,470 407,690 18,293 1,222,453 Less: Selling, general and administrative expense - - (17,755) (17,755) Less: Depreciation, depletion and amortization (34,863) (42,902) (538) (78,303) Total operating costs 761,607 364,788 - 1,126,395 Less: Other royalties (150,718) (25,188) - (175,906) Less: Stanwell rebate (68,257) - - (68,257) Less: Freight expenses (71,035) (49,761) - (120,796) Less: Other non-mining costs (9,783) (27,842) - (37,625) Total mining costs 461,814 261,997 - 723,811 Sales Volume excluding non-produced coal (Mt) 4.6 2.8 - 7.4 Average mining costs per tonne sold $100.1/t $92.4/t - $97.2/t |