Amryt is a global commercial-stage biopharmaceutical company focused on acquiring, developing and commercializing innovative treatments to help improve the lives of patients with rare and orphan diseases. Amryt comprises a strong and growing portfolio of commercial and development assets.

As used herein, references to “we,” “us,” “Amryt” or the “Group” in this annual report on Form 20-F shall mean Amryt Pharma plc and its global subsidiaries, collectively. References to the “Company” in this annual report shall mean Amryt Pharma plc.

This annual report includes the following historical financial information, presented in US Dollars:

All references in this annual report to “€” mean Euros, all references to “£” mean pounds sterling and all references to “$” mean U.S. dollars. Except as otherwise stated herein, all monetary amounts in this annual report have been presented in US Dollars. For presentation purposes all financial information, including comparative figures from prior periods, have been stated in round thousands, unless otherwise indicated.

This annual report contains forward-looking statements concerning our business, operations and financial performance and condition, as well as our plans, objectives and expectations for our business operations and financial performance and condition. Any statements contained herein that are not statements of historical facts may be deemed to be forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “aim,” “anticipate,” “assume,” “believe,” “contemplate,” “continue,” “could,” “due,” “estimate,” “expect,” “goal,” “intend,” “may,” “might,” “objective,” “plan,” “predict,” “potential,” “positioned,” “seek,” “should,” “target,” “will,” “would,” and other similar expressions that are predictions of or indicate future events and future trends, or the negative of these terms or other comparable terminology, although not all forward-looking statements contain these identifying words.

By their nature, forward-looking statements involve risk and uncertainty because they relate to future events and circumstances. Forward-looking statements are not guarantees of future performance and have not been reviewed by our auditors. Actual results and developments could differ materially from those expressed or implied by the forward-looking statements due to a variety of factors, including, but not limited to, those identified under the section titled “Risk Factors” in this annual report.

The preceding list is not intended to be an exhaustive list of all of our risks and uncertainties. As a result of these factors, we cannot assure you that the forward-looking statements in this annual report will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame, or at all.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this annual report, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely upon these statements.

The forward-looking statements and opinions contained in this annual report are based upon information available to us as of the date of this annual report and, while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. The forward-looking statements contained in this annual report speak only as of the date of this annual report, and we do not undertake any obligation to update them in light of new information or future developments or to release publicly any revisions to these statements in order to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

You should read this annual report and the documents referenced herein and have filed as exhibits to the registration statement, of which this annual report forms a part, completely and with the understanding that our actual future results may be materially different from expectations. We qualify all forward-looking statements in this annual report by these cautionary statements.

This annual report contains estimates, projections and other information concerning our industry, our business and the markets for our products and product candidates. Information that is based on estimates, forecasts, projections, market research or similar methodologies is inherently subject to uncertainties, and actual events or circumstances may differ materially from events and circumstances that are assumed in this information. Unless otherwise expressly stated, we obtained this industry, business, market and other data from our own internal estimates and research as well as from reports, research surveys, studies and similar data prepared by market research firms and other third parties, industry, medical and general publications, government data and similar sources. Management estimates are derived from publicly available information, our knowledge of our industry and assumptions based on such information and knowledge, which we believe to be reasonable.

In addition, assumptions and estimates of our and our industry’s future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors.” These and other factors could cause our future performance to differ materially from our assumptions and estimates. See “Special Note Regarding Forward-Looking Statements.”

The Amryt logo, Myalept®, Myalepta®, Juxtapid®, Lojuxta®, Episalvan®, Filsuvez®, Oleogel-S-10, Mycapssa®, TPE® and other trademarks or service marks of Amryt appearing in this annual report are the property of Amryt. This annual report includes trademarks, tradenames and service marks, certain of which belong to us and others that are the property of other organizations. Solely for convenience, trademarks, tradenames and service marks referred to in this annual report appear without the ®, TM and SM symbols, but the absence of those symbols is not intended to indicate, in any way, that we will not assert our rights or that the applicable owner will not assert its rights to these trademarks, tradenames and service marks to the fullest extent under applicable law. We do not intend our use or display of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply a relationship with, or endorsement or sponsorship of us by, these other parties.

Not applicable.

Not applicable.

The following selected historical consolidated financial data of Amryt Pharma as at December 31, 2021 and 2020 and for each of the years ended December 31, 2021, 2020 and 2019 have been derived from, and should be read in conjunction with, the audited consolidated financial statements and notes thereto set forth in Item 18 of this annual report. The selected historical consolidated financial data as at December 31, 2019 is derived from the audited consolidated financial statements not appearing in this annual report. This data should be read in conjunction with the financial statements, related notes and other financial information included elsewhere herein.

We have not included selected historical consolidated financial data for the years ended December 31, 2018, and 2017 in the table below as we qualify as an emerging growth company (an “Emerging Growth Company”) as defined in Section 2(a)(19) of the Securities Act and we make use of an accommodation for reduced reporting.

A. Selected Consolidated Financial Data of Amryt

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Our business is subject to a number of risks. You should carefully consider the risks and uncertainties described below and the other information in this annual report, including our consolidated financial statements and related notes. Our business, financial condition, results of operations or prospects could be materially and adversely affected if any of these risks occur, and as a result, the market price of our ADSs could decline.

We have incurred significant operating losses since our inception and we may not achieve or maintain profitability in the future.

To date, we have financed our operations primarily through a combination of revenues from sales of our commercialized products and the sale of our equity securities and convertible bonds. We have incurred operating losses since our inception, including net losses of $50.5 million, $46.5 million and $38.6 million for the years ended December 31, 2019, 2020 and 2021, respectively. Aegerion incurred losses since its inception, including net losses of $96.5 million and $30.9 million for the year ended December 31, 2018, and the six-month period ended June 30, 2019. Chiasma incurred losses since its inception, including net losses of $74,7 million and $50.4 million for the year ended December 31, 2020, and the six-month period ended June 30, 2021. We have devoted most of our financial resources to the acquisition of attractive commercial and near-commercial rare disease assets and research and development. We anticipate that we will continue to incur significant costs associated with the continued commercialization of lomitapide, Mycapssa® and metreleptin, and in connection with ongoing clinical development efforts and post-marketing commitments for these products as well as the continued development of our product candidates. The amount of our future net losses will depend, in part, on the rate of our future expenditures, our ability to continue generating adequate revenues from sales of lomitapide, Mycapssa® and metreleptin and from sales of Oleogel-S10 if approved, and our ability to obtain funding through equity or debt offerings, grant funding, collaborations, strategic partnerships and/or licensing arrangements. If we do become profitable, we may not be able to sustain or increase our profitability on a quarterly or annual basis.

Our future performance depends, in part, on our ability to successfully implement our strategy.

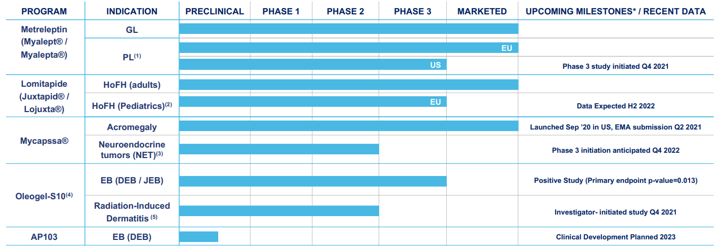

Our future success will depend on our ability to implement our strategy to develop and expand our existing portfolio of drugs to treat patients with rare diseases and to create a rare disease company with a diversified offering of multiple development stage and commercial assets that can provide us with scale to support future growth. The success of our strategy depends, in part, on our ability to drive growth in existing territories and access and drive growth in new territories and indications with existing commercial assets, build a franchise in EB through our lead product candidate, Oleogel-S10 (Filsuvez), and our product candidate AP103, based on our novel polymer-based topical gene therapy delivery platform, expand the indication of Mycapssa® (octreotide capsules) beyond acromegaly into carcinoid syndrome associated with neuroendocrine tumors and expand and diversify our product portfolio through acquisition and in-licensing opportunities. This strategy will require us to, among other things, identify suitable targets, conduct and complete clinical trials, obtain the necessary consents and authorizations for our products and any product candidates, conduct diligence, carry out any acquisition or in-licensing transaction and obtain suitable financing.

Implementing our strategy requires substantial time and resources from our management team. Our Board and management may not be able to successfully implement our strategy or other strategies to be developed by management, and implementing these strategies may not sustain or improve, and could even harm, our business, financial condition, results of operations and prospects. We may be unable to realize the anticipated benefits and synergies of our business strategies, which are based on assumptions about future demand for our current products and product candidates, as well as on our continuing ability to produce our products profitably. Consequently, any predictions made about our future success or viability may not be as accurate as they could be if we had a longer operating history or additional products on the market.

We are dependent primarily on three products, lomitapide, Mycapssa® and metreleptin, to generate revenue and these products may not be successful and may not generate sales at anticipated levels.

Our ability to meet expectations with respect to sales of lomitapide, Mycapssa® and metreleptin, and to generate revenues from such sales, and attain and maintain positive cash flow from operations, in the time periods anticipated, or at all, will depend on a number of factors, including, among others:

If we are unable to continue to generate revenue from our current commercial products, our business, financial condition, results of operations and prospects will be adversely affected.

We may not be successful in our efforts to build a pipeline of product candidates and develop additional marketable products.

We operate in the biopharmaceutical sector and have product candidates in various stages of clinical and preclinical development. In addition, we may continue to explore other opportunities within the sector in order to expand our present development pipeline. Industry experience indicates that there may be a very high incidence of delay or failure to produce valuable scientific results in relation to our present development pipeline. We will also face the risk that in developing new products we may spend substantial sums of money and the new products developed may not effectively meet the perceived need or may not be successfully commercialized. Our ability to develop new products relies on, among other things, the recruitment of sufficiently qualified research and development partners with expertise in the biopharmaceutical sector. We may not be able to develop relationships or recruit research partners of a sufficient caliber to satisfy the rate of growth and develop our future pipeline.

We may need to raise additional funding, which may not be available on acceptable terms, or at all, and failure to obtain this capital when needed may force us to delay, limit or terminate our product development efforts or other operations or to delay payment on future obligations.

On September 24, 2019, we entered into a five-year term loan facility (“Secured Credit Facility”) and issued 5% senior unsecured convertible notes (“Convertible Notes”). As of December 31, 2021, we had borrowings of $93.4 million under our Secured Credit Facility and $125.0 million under our Convertible Notes, for total debt of $218.4 million. The Secured Credit Facility includes an option to prepay the loan in whole or in part at any time subject to payment of an exit fee, which ranged from 0-5% of the principal amount then outstanding on the Secured Credit Facility. On February 18, 2022, the Secured Credit Facility was repaid in full and the Group secured a $125 million senior credit facility (“Senior Credit Facility”) from funds managed by the Credit Group of Ares Management Corporation (“Ares”) of which US$105 million was drawn down to facilitate the prepayment of the existing Secured Credit Facility. In repaying the Secured Credit Facility, Amryt incurred an exit fee of 5.00% of the outstanding principal amount as at the prepayment date. Furthermore, we may be required to satisfy payment obligations of up to $85 million to holders of contingent value rights (“CVRs”) issued to shareholders and option holders in connection with specified milestones, which we may elect to pay in ordinary shares or notes. If we elect to issue notes, we will settle such notes in cash 120 days after their issue. The specified milestones are related to the success of Oleogel-S10 and $50 million of the payment obligations are dependent on FDA and EMA approval. $35 million is due in respect of FDA approval and $15 million is due in respect of EMA approval if approval is obtained before December 31, 2021, with a sliding scale on a linear basis to zero if before July 1, 2022.

We have significant payment obligations in connection with our Senior Credit Facility, the Convertible Notes, the CVRs and royalty obligations under certain of our license agreements.

We have significant milestone and royalty payments payable under our material contracts if/when certain milestones are met, the terms of which are outlined in the “Material Contracts” section.

In addition, while we are currently commercializing our approved products, we are also advancing our product candidates through preclinical and clinical development. Developing product candidates is expensive, lengthy and risky, and we expect our research and development expenses to increase in connection with our ongoing activities, particularly as we advance our product candidates toward commercialization.

As of December 31, 2021, our unrestricted cash and cash equivalents were $113.0 million. We expect that our existing cash and cash equivalents will be sufficient to fund our current operations and our payment obligations to third parties for at least the next 12 months. However, these resources might be insufficient to conduct research and development programs, the cost of product in-taking and possible acquisitions, fully commercialize products and operate our business to the full extent currently planned, and our operating plan may change as a result of many factors currently unknown to us. As a result, we may need to seek additional funds sooner than planned, through public or private equity or debt financings, government or other third-party funding, marketing and distribution arrangements and other collaborations, strategic alliances and licensing arrangements or a combination of these approaches. Even if we believe we have sufficient funds for our current or future operating plans as well as to satisfy our payment obligations to third parties, we may seek additional capital if market conditions are favorable or if we have specific strategic considerations. Any additional fundraising efforts may divert our management from their day-to-day activities, which may adversely affect our ability to develop and commercialize our product candidates.

If we cannot obtain adequate funds, we may be required to significantly curtail our commercial plans or one or more of our research and development programs or obtain funds through additional arrangements with corporate collaborators or others that may require us to relinquish rights to some of our technologies or product candidates. In addition, we cannot guarantee that future financing will be available in sufficient amounts or on terms acceptable to us, if at all. Moreover, the terms of any financing may adversely affect the holdings or the rights of our shareholders and the issuance of additional securities, whether equity or debt, by us, or the possibility of such issuance, may cause the market price of our ADSs or ordinary shares to decline. The sale of additional equity or convertible securities may be dilutive to our shareholders. We may also enter into additional credit facilities from time to time, which may be secured, to fund certain of our operations. If we raise additional capital through debt financing, we would be subject to payment obligations and may be subject to security interests in our assets and covenants restricting our ability to take specific actions, such as incurring additional debt, making capital expenditures or declaring dividends. If we raise additional capital through marketing and distribution arrangements, sales of assets or other collaborations, or licensing arrangements with third parties, we may have to relinquish certain valuable rights to our product candidates, technologies, future revenue streams or research programs. We also could be required to seek collaborators for one or more of our current or future product candidates at an earlier stage than otherwise would be desirable or relinquish our rights to product candidates or intellectual property that we otherwise would seek to develop or commercialize ourselves. If we are unable to raise additional capital in sufficient amounts, at the right time, on favorable terms, or at all, we may have to significantly delay, scale back or discontinue the development or commercialization of one or more of our products or product candidates, or one or more of our other research and development initiatives. Any of the above events could significantly harm our business, prospects, financial condition and results of operations, cause the price of our ADSs and ordinary shares to decline, and negatively impact our ability to fund operations.

The terms of our debt and any requirements to incur further indebtedness or refinance our indebtedness in the future could have a material adverse effect on our business and results of operations.

Our level of indebtedness, together with any additional indebtedness we may incur in the future, could adversely affect our business, financial condition, results of operations and prospects. For example, our anticipated level of indebtedness or any additional financing may:

Any of the foregoing, alone or in combination, could have a material adverse effect on our business, financial condition, results of operations and prospects. A breach of, or the inability to comply with, the covenants in the Senior Credit Facility and the Convertible Notes could result in an event of default, in which case the lenders will have the right to declare all borrowings to be immediately due and payable, which would have a material adverse effect on our business, financial condition, results of operations and prospects and could lead to foreclosure on our assets.

In the future, we may need to refinance our indebtedness. However, additional financing may not be available on favorable commercial terms to us, or at all. If, at such time, market conditions are materially different or our credit profile has deteriorated, the cost of refinancing such debt may be significantly higher than our indebtedness existing at that time. Furthermore, we may not be able to procure refinancing at all. Any failure to meet any future debt service obligations through use of cash flow, refinancing or otherwise, could have a material adverse effect on our business, financial condition, results of operations and prospects.

Restrictive covenants in certain of the agreements and instruments governing our indebtedness may adversely affect our financial and operational flexibility.

The terms of our indebtedness as of the date of this annual report include covenants that, among other things, restrict our ability to: incur liens; dispose of our assets (both material assets and exclusive licensing transactions in material territories); consolidate and merge with other entities; make loans and investments; incur indebtedness; engage in transactions with affiliates; make specified payments; and engage in other customary business activities.

If we breach a restrictive covenant under the Senior Credit Facility or the Convertible Notes, or an event of default occurs with respect to such indebtedness, all amounts owing in respect of such indebtedness may be able to be declared due and payable immediately, which could have a material adverse effect on our business, prospects, liquidity, financial condition and results of operations. In addition, both our Senior Credit Facility and the Convertible Notes include cross-default provisions, which generally provide that a default under one facility also results in a default under the other. See “Item 7. Major Shareholders and Related Party Transactions—B. Related Party Transactions—Agreements with Principal Shareholders— Senior Credit Facility” and “Item 7. Major Shareholders and Related Party Transactions—B. Related Party Transactions—Agreements with Principal Shareholders—Convertible Notes.”

If we enter into future debt agreements, they may include similar or more restrictive provisions. These restrictions may also make more difficult or discourage a takeover of our company, whether favored or opposed by management or the Board. Our ability to comply with these covenants may be affected by events beyond our control, and any material deviations from our forecasts could require us to seek waivers or amendments of covenants or alternative sources of financing, or to reduce expenditures. We cannot guarantee that such waivers, amendments or alternative financing could be obtained or, if obtained, would be on terms acceptable to us. A breach of any of the covenants or restrictions in our debt agreements or instruments could result in an event of default. Such a default could allow our debt holders to accelerate repayment of the related debt, as well as any other debt to which a cross-acceleration or cross-default provision applies, or to declare all borrowings outstanding under these agreements to be due and payable. If our debt is accelerated, our assets may not be sufficient to repay such debt.

Holders of the Convertible Notes have the right to require the repurchase of their notes for cash upon the occurrence of a fundamental change, such as a change of control of our company, at a repurchase price equal to 100% of the respective principal amount, plus accrued and unpaid interest, if any. If a fundamental change occurs and the Convertible Notes are converted during the related fundamental change conversion period, then the conversion rate may be increased to a corresponding number of shares and share price set forth in the Convertible Notes. Subject to certain exceptions as provided in the indenture governing the Convertible Notes, a fundamental change includes (a) the acquisition of 50% or more of the voting interests in our company, (b) an event in which we merge or consolidate with another entity, (c) an event in which we convey, sell, transfer or lease all or substantially all of our assets to another entity, (d) our liquidation or (e) delisting of our ordinary shares. Among the exceptions provided in the indenture are for transactions described in (a), (b) or (c) in which (i) our stockholders immediately prior to the transaction have the right to exercise, directly or indirectly, 50% or more of the total voting power of the capital stock of the continuing or surviving entity or transferee or parent thereof following the transaction or (ii) 90% of the consideration paid for our ordinary shares in a transaction consists of stock that is or will be quoted on AIM, the New York Stock Exchange or the Nasdaq. Further, unless we elect to deliver our ordinary shares to settle any conversions of Convertible Notes, we would be required to settle a portion or all of the conversion obligation through the payment of cash. We may not have enough available cash or be able to obtain financing at the time it is required to make repurchases of Convertible Notes surrendered therefor or Convertible Notes being converted. The failure to repurchase Convertible Notes at a time when the repurchase is required by the indenture or to pay any cash payable on future conversions of the Convertible Notes as required by the indenture would constitute a default under the indenture. A default under the indenture or a fundamental change itself could also lead to a default under agreements governing our current and future indebtedness. If the repayment of such indebtedness were to be accelerated after any applicable notice or grace periods, we are unlikely to have sufficient funds to repay such indebtedness and repurchase the Convertible Notes or make cash payments upon conversions thereof or other required payments on its other indebtedness, which would materially and adversely affect our business, financial condition and results of operations on a consolidated basis.

We face potential product liability exposure, and if claims are brought against us, we may incur substantial liability.

The use of any product in clinical trials or early access programs, and the sale and use of any product for which we have obtained marketing approval exposes us to the risk of product liability claims. Product liability claims might be brought against us by consumers, healthcare providers or others selling or otherwise coming into contact with our products. If we cannot successfully defend against product liability claims, we could incur substantial liabilities. In addition, regardless of merit or eventual outcome, product liability claims may result in:

Although we have obtained product liability insurance coverage for both our clinical trials and our commercial exposure, this insurance coverage may not be sufficient to reimburse us for expenses or losses that we may suffer. Moreover, insurance coverage is becoming increasingly expensive, and in the future, we may not be able to maintain insurance coverage at a reasonable cost or in sufficient amounts to protect us against potential liability. If a claim is brought against us, we might be required to pay legal and other expenses to defend the claim, as well as pay uncovered damages awards resulting from a claim brought successfully against us and these damages could be significant and have a material adverse effect on our financial condition. On occasion, large judgments have been awarded in class action lawsuits relating to drugs that had unanticipated side effects or warnings found to be inadequate. The cost of any product liability litigation or other proceedings, even if resolved in our favor, could be substantial. A product liability claim or series of claims brought against us could harm our reputation and cause the price of our securities to decline and, if the claim is successful and judgments exceed our insurance coverage, it could have a material adverse impact on our business, financial condition, results of operations and prospects.

Adverse events involving any of our products and product candidates may lead the U.S. Food & Drug Administration (“FDA”), the European Medicines Agency (“EMA”) or other regulatory authorities to delay or deny clearance for our products or result in product recalls that could harm our reputation, business and financial results.

The FDA and the EMA, as well as similar governmental authorities in other jurisdictions, have the authority to require the recall of certain commercialized products in the event of adverse side effects, material deficiencies or defects in design or manufacture. Manufacturers may, under their own initiative, recall a product if any material deficiency in a product is found. A government-mandated recall or voluntary recall by us or one of our distributors could occur as a result of adverse side effects, impurities or other product contamination, manufacturing errors, design or labeling defects or other deficiencies and issues. Recalls of any of our products or product candidates would divert managerial and financial resources and have an adverse effect on our financial condition and results of operations. A recall announcement could harm our reputation with customers and negatively affect our sales, if any.

Our future success depends on our ability to hire and retain key executives and to attract, retain and motivate qualified personnel.

Our future success depends on our ability to attract and retain key management personnel, scientific and technical personnel, particularly in the biopharmaceutical industry. Our ability to continue our operations and implement our strategy depends upon retaining, recruiting and motivating employees, especially with respect to our management team and research personnel. Experienced employees in the biopharmaceutical and biotechnology industries are in high demand and competition for their talents can be intense, especially in Germany, Ireland, and Boston, Massachusetts, where we maintain our principal operations. We have entered into employment agreements with executive officers and other key employees, but any employee may terminate his or her employment at any time or may be unable to continue in his or her role. The loss of any executive or key employee, or an inability to recruit desirable candidates or find adequate third parties to perform such services on reasonable terms and on a timely basis, could have a material adverse effect on our business, financial condition, results of operations and prospects. If we are not able to attract, retain and motivate necessary personnel to accomplish our business objectives, we may experience constraints that could significantly impede our ability to achieve our development and commercial objectives, our ability to raise additional capital and our ability to implement our business strategy.

For U.S. federal income tax purposes, Amryt is treated as a surrogate foreign corporation, and there is a risk that Amryt may be treated as a U.S. corporation under certain circumstances, including as a result a change in law.

Section 7874 of the U.S. Internal Revenue Code of 1986, as amended (the “Code”) and the Treasury regulations promulgated thereunder contain two alternative sets of rules under which a U.S. target corporation may be subjected to certain additional U.S. federal income taxes or a non-U.S. acquiring corporation (such as Amryt) may be treated as a U.S. corporation for U.S. federal income tax purposes as a result of a transaction. Which set of rules applies depends on what percentage of the non-U.S. acquiring corporation’s stock the historic stockholders of the U.S. target corporation own or are treated as owning, under certain counting conventions, by reason of holding shares of the U.S. target corporation following the transaction (the “Section 7874 Percentage”). One set of rules imposes a tax on certain gain and income of the U.S. target corporation, and potentially certain other taxes, if (in addition to other requirements) the Section 7874 Percentage is at least 60 percent (by vote or value). The other set of rules under Section 7874 of the Code treats the non-U.S. acquiring corporation as a U.S. corporation for U.S. federal income tax purposes if (in addition to other requirements) the Section 7874 Percentage is at least 80 percent (by vote or value). If the Section 7874 Percentage is at least 60 percent (by vote or value), the non-U.S. acquiring corporation is considered a “surrogate foreign corporation,” and the U.S. target corporation is considered an “expatriated entity” with respect to the non-U.S. acquiring corporation.

Amryt believes that, as a result of Amryt’s acquisition of Aegerion in 2019 (the “Prior Acquisition”), Amryt is treated as a surrogate foreign corporation (the 60 percent test), but not as a U.S. corporation (the 80 percent test). As a result of Amryt’s status as a surrogate foreign corporation, dividends paid in respect of the Amryt ADSs or Ordinary Shares are not expected to be eligible to be taxed at favorable rates that otherwise are applicable to “qualified dividend income” received by non-corporate U.S. holders if certain additional conditions are satisfied.

Amryt believes that both Aegerion and Chiasma meet the definition of “expatriated entity” within the meaning of section 7874 of the Code. As expatriated entities, several limitations apply to both Aegerion and Chiasma, including, but not limited to, the prohibition, for a period of ten years from the closing date of the Prior Acquisition, of the use of net operating losses, foreign tax credits and other tax attributes to offset the income or gain recognized by reason of transfer of any property to a foreign related person or to offset any income received or accrued during such period by reason of Amryt’s license of any property to a foreign related person. Moreover, in such case, an additional minimum tax under Section 59A of the Code on certain “base eroding” payments to certain affiliates that are foreign corporations may be imposed.

Although Amryt does not expect to be treated as a U.S. corporation under currently applicable law and regulations, it is possible that a future change in law could expand the scope of Section 7874 of the Code on a retroactive basis. If Amryt were treated as a U.S. corporation, its entire net income would be subject to U.S. federal income tax on a net income basis and would be determined under U.S. federal income tax principles. Further, Amryt’s treatment as a U.S. corporation may have material adverse effects on the business, financial condition, results of operations and prospects of Amryt and its subsidiaries.

The application of Section 7874 of the Code is complex and subject to detailed regulations (the application of which is uncertain in various respects and could be impacted by changes in U.S. Treasury regulations with possible retroactive effect). Accordingly, there can be no assurance that the IRS will not challenge the status of Amryt as a non-U.S. corporation for U.S. federal income tax purposes under Section 7874 of the Code or that such challenge would not be sustained by a court. If the IRS were to successfully challenge under Section 7874 of the Code Amryt’s status as a non-U.S. corporation for U.S. federal income tax purposes, Amryt and certain Amryt Shareholders may be subject to significant adverse tax consequences, including a higher effective corporate income tax rate on Amryt, the recognition of gain by certain U.S. Amryt Shareholders upon the deemed conversion of Amryt from a non-U.S. corporation to a U.S. corporation, and future withholding taxes on certain Amryt Shareholders, depending on the application of any applicable income tax treaty that may apply to reduce such withholding taxes.

Our global operations subject us to significant tax risks.

We are subject to tax rules in the jurisdictions in which we operate. Changes in tax rates, tax relief and tax laws, changes in practice or interpretation of the law by the relevant tax authorities, increasing challenges by relevant tax authorities or any failure to manage tax risks adequately could result in increased charges, financial loss, penalties and reputational damage. Tax authorities may actively pursue additional taxes based on retroactive changes to tax laws which could result in a material restatement to its tax position. Any of these factors could have a negative impact on our business, financial condition, results of operations and prospects.

Fluctuations in currency exchange rates and increased inflation could materially adversely affect our financial condition and results of operations.

We have operations in Ireland, the United Kingdom, the United States, Germany, Switzerland, Brazil, France, Italy, Spain, Israel and other select markets throughout the world. As a result of the international scope of our operations, fluctuations in exchange rates, particularly between the U.S. dollar, our reporting currency, and the Euro, may adversely affect us. In the year ended December 31, 2021, 2.6% of our sales were denominated in pound sterling (£), 72.6% of our sales were denominated in U.S. dollars, 24.0% were denominated in Euros and the balance was denominated in other currencies. As a result, weakening of the Euro or pound sterling relative to the U.S. dollar presents the most significant risk to us. Any significant fluctuations in currency exchange rates may have a material impact on our business.

In addition, economies in Central European and Latin American countries have periodically experienced high rates of inflation. Periods of higher inflation may slow economic growth in those countries. As a substantial portion of our expenses (excluding currency losses and changes in deferred tax) is denominated in U.S. dollars or Euros, the relative movement of inflation significantly affects our results of operations. Inflation also is likely to increase some of our costs and expenses, including wages, rents, leases and employee benefit payments, which we may not be able to pass on to our customers and, as a result, may reduce our profitability. To the extent inflation causes these costs to increase, such inflation may materially adversely affect our business. Inflationary pressures could also affect our ability to access financial markets and lead to counter-inflationary measures that may harm our financial condition, or results of operations or materially adversely affect the market price of our securities.

The occurrence of cyber incidents, or a deficiency in cybersecurity, could negatively impact our business by causing a disruption to its operations, a compromise or corruption of confidential information, exposure to legal and regulatory action, or damage to our patient, partner or employee relationships, any of which could subject us to loss and reputational harm.

A cyber incident is considered to be any event that threatens the confidentiality, integrity or availability of information resources. More specifically, a cyber incident is an intentional attack or an unintentional event that can include gaining unauthorized access to systems to disrupt operations, corrupt data or steal confidential information about patients, suppliers, partners or employees. A number of companies have recently experienced serious cyber incidents and breaches of their information technology systems. Cyber incidents pose risks both to our internal systems and to those we have outsourced operations to, including the risk of operational interruption, damage to our reputation and relationships with patients, partners and employees, and private data exposure. We have implemented processes, procedures and controls to help mitigate these risks. However, these measures, as well as an increased awareness of the risk of a cyber incident, do not guarantee that our reputation, operations and financial results will not be adversely affected by such an incident.

In the ordinary course of business, we collect and store sensitive data, including intellectual property, proprietary business information and patient data. This data includes, where required or permitted by applicable laws, personally identifiable information. Certain third parties with whom we contract also collect and store data related to clinical trial subjects and patients. The secure maintenance of this information is critical to our operations and business strategy. Despite our current security measures, our information technology and infrastructure may be vulnerable to attacks by hackers or breaches due to employee error, malfeasance or other disruptions. Any such breach could compromise information stored on networks or those of our partners. Any access, disclosure or other loss of information could result in legal claims or proceedings, liability under laws that protect the privacy of personal information, recovery costs, disruption of operations, including delays in our regulatory approval efforts, and damage our reputation, which could adversely affect our business.

Risks Related to Acquisitions, Including our Acquisitions of Aegerion and Chiasma

We have faced, and we may continue to face, challenges integrating the businesses and operations of our company and Chiasma and Aegerion and, as a result, may not realize the expected benefits of the acquisitions.

Integrating the businesses of our company and the businesses of Aegerion and Chiasma is a complex process.. We cannot guarantee that the integration of our business with Aegerion and Chiasma’s will be completed successfully or that we will be able to achieve any of the anticipated benefits. In order for the integration to be successful, we must maintain prior regulatory relationships, clinical trials, product initiatives, license, service DOJ and Corporate Integrity agreement(s) and their related obligations, with violations of these agreements resulting in potential financial penalties, additional time added on to the current terms of the agreements and additional costs for the company. We must also undertake certain actions required to maintain manufacturing, supply and distribution processes. While we have made significant progress, we may not be able to successfully integrate the businesses of our company and Aegerion and Chiasma, and even if successful, the integration may be costly and time consuming, and the anticipated synergies may not be realized, either of which may have a material and adverse effect on our business, financial condition, results of operations and prospects.

Any future acquisitions we make may expose us, to risks that could adversely affect our business, and we may not achieve the anticipated benefits of acquisitions of businesses or technologies.

As a part of our growth strategy, we may make additional acquisitions of complementary businesses. Any future acquisition will involve numerous risks and operational, financial and managerial challenges, including the following, any of which could adversely affect our business, financial condition or results of operations:

| • | limited support and user knowledge for legacy systems of acquired companies; |

| • | problems maintaining uniform procedures, controls and policies with respect to our financial accounting systems; |

| • | difficulties in managing geographically dispersed operations, including risks associated with entering foreign markets in which we have no or limited prior experience; |

| • | underperformance of any acquired technology, product or business relative to our expectations and the price we paid; |

| • | negative near-term impacts on financial results after an acquisition, including acquisition-related earnings charges; |

| • | the potential loss of key employees, customers and strategic partners of acquired companies; |

| • | claims by terminated employees and shareholders of acquired companies or other third parties related to the transaction; |

| • | the assumption or incurrence of additional debt obligations or expenses, or use of substantial portions of our cash; |

| • | the issuance of equity securities to finance or as consideration for any acquisitions that dilute the ownership of our shareholders; |

| • | any collaboration, strategic alliance and licensing arrangement may require us to relinquish valuable rights to our technologies or product candidates, or grant licenses on terms that are not favorable to us; |

| • | risks and uncertainties associated with the other party to such a transaction, including the prospects of that party and their existing products or product candidates and regulatory approvals; |

| • | diversion of management’s attention and company resources from existing operations of the business; |

| • | inconsistencies in standards, controls, procedures and policies; |

| • | the impairment of intangible assets as a result of technological advancements, or worse-than-expected performance of acquired companies; |

| • | assumption of, or exposure to, historical liabilities of the acquired business, including unknown contingent or similar liabilities that are difficult to identify or accurately quantify; |

| • | our inability to generate revenue from acquired technology or products sufficient to meet our objectives in undertaking the acquisition or even to offset the associated acquisition and maintenance costs; |

| • | risks associated with acquiring intellectual property, including potential disputes regarding acquired companies’ intellectual property; and |

| • | future acquired products, employees policies and operations (including pricing/reimbursement) could be subject to Corporate Integrity Agreement compliance and review. |

There can be no assurance that any of the acquisitions we may make will be successful or will be, or will remain, profitable. Our failure to successfully address the foregoing risks may prevent us from achieving the anticipated benefits from any acquisition in a reasonable time frame, or at all.

If intangible assets and goodwill that we record in connection with our acquisitions become impaired, we may have to take significant charges against earnings.

In connection with the accounting for our acquisitions, a significant value may be recognized in respect of intangible assets, including developed technology and customer relationships relating to the acquired product lines, and goodwill. Under IFRS, we must assess, at least annually and potentially more frequently, whether the value of intangible assets and goodwill has been impaired. Intangible assets and goodwill will be assessed for impairment in the event of an impairment indicator. Any reduction or impairment of the value of intangible assets and goodwill will result in a charge against earnings, which could materially adversely affect our results of operations and shareholders’ equity in future periods.

Risks Related to the Commercialization of our Products

Our assumptions and estimates regarding prevalence and the addressable markets for our products and product candidates may be inaccurate. If there are fewer actual patients than estimated, or if any product approval is based on narrower definitions of patient populations, our revenues and cash position could be materially and adversely affected.

The patient population for the diseases that our products treat is very small, and networking, data gathering and support channels are not as established as those for more prevalent and researched disease indications. There are limited patient registries or methods of establishing with precision the actual number of Homozygous familial Hypercholesteraemia (HoFH), General Lipodystrophy (GL) and Partial Lipodystrophy (PL), acromegaly, Neuroendocrine Tumour (NET) or Epidermolysis Bullosa (EB) patients in any geography. Estimating the prevalence of a rare disease is difficult and we therefore must rely on assumptions, beliefs and an amalgam of information from multiple sources, resulting in potential under or over-reporting. There is no guarantee that our assumptions and beliefs are correct, or that the methodologies used and data collected have generated or will continue to generate accurate estimates. There is therefore uncertainty around the estimated total potential addressable patient population for treatment with lomitapide, Mycapssa, metreleptin or Oleogel-S10 worldwide.

In addition, the potential market opportunity for our product candidates that we may develop is difficult to estimate precisely, particularly given that the orphan drug markets which are targeted are, by their nature, relatively unknown. Our estimates of the potential market opportunity for each of these product candidates are predicated on several key assumptions, such as industry knowledge and publications, third-party research reports and other surveys. If any of our assumptions prove to be inaccurate, then the actual market for lomitapide, Mycapssa, metreleptin, Oleogel-S10 or AP103, or our other or future product candidates, could be smaller than our estimates of the potential market opportunity. If that turns out to be the case, our product revenue may be limited, and we may be unable to achieve or maintain profitability, which could have a material adverse effect on our business, financial condition, results of operations and prospects.

Our products may not gain market acceptance, in which case we may not be able to generate product revenues.

Physicians, healthcare providers, patients, payers or the medical community may not accept or use our approved products. Efforts to educate the medical community and third-party payers on the benefits of the products may require significant resources and may not be successful. Notwithstanding the level of revenues historically generated from the sale of lomitapide, Mycapssa® and metreleptin, if any of our existing marketed products or product candidates do not achieve an adequate level of acceptance, we may struggle to continue to generate significant product revenues and may not in the future generate any profits from operations. The degree of market acceptance will depend on a variety of factors, including, but not limited to:

| • | whether clinicians and potential patients perceive product candidates to have better efficacy, safety, tolerability profile and ease of use, when compared with the products marketed by our competitors and the prevailing standard of care (“SOC”); |

| • | the timing and location of market introduction of any approved products; |

| • | our ability to provide acceptable evidence of safety and efficacy; |

| • | the frequency and severity and causal relationships of any side effects and a continued acceptable safety profile following approval; |

| • | relative convenience and ease of administration; |

| • | patient diagnostics and screening infrastructure in each market; |

| • | marketing and distribution support; |

| • | the availability of healthcare coverage, reimbursement and adequate payment from health maintenance organizations and other third-party payers, both public and private; and |

| • | competition from other therapies. |

We face significant competition from other biotechnology and pharmaceutical companies.

The specific markets in which we operate are highly competitive and this competition could harm our results of operations, cash flows and financial condition. Our competitors include major international pharmaceutical companies as well as smaller or regional specialty pharmaceutical and biotechnology companies. We may be forced to either lower the selling prices of our products in response to competitor pricing or lose patients who choose lower-priced products. Many of our competitors are larger, have greater financial resources and a lower cost structure. As a result, our competitors may be better equipped to withstand changes in economic and industry conditions. These competitors currently engage in, have engaged in or may in the future engage in the development, manufacturing, marketing and commercialization of new pharmaceuticals, some of which may compete with our products. Competition may also arise from, among other things, other drug development technologies, methods of preventing or reducing the incidence of disease, including vaccines and new small molecule or other classes of therapeutic agents. Smaller or early-stage companies may also be significant competitors, particularly through collaborative arrangements with large, established companies. Key competitive factors affecting the commercial success of our products and any other products that we develop or acquire are likely to be safety, efficacy, tolerability profile, reliability, convenience of dosing, price and reimbursement. We may also face future competition from companies selling generic alternatives to our products in countries where we do not have patent coverage, Orphan Drug status or another form of data or marketing exclusivity or where patent coverage or data or marketing exclusivity has expired, is not enforced, or may, in the future, be challenged.

A significant competitor to our lomitapide product is a class of drugs known as PCSK9 inhibitors. Two main brands dominate the marketplace – Praluent and Repatha which are both approved in the European Union and the United States. Sales of PCSK9 inhibitors compete with sales of lomitapide and we expect that this product will continue to compete with lomitapide. In addition, one of our competitors, Regeneron Pharmaceuticals Inc., is developing Evinacumab, a human monoclonal antibody directed against the activity of angiopoietin-like 3 (“ANGPTL3”) for the treatment of HoFH. In August 2019, Regeneron announced positive topline data from its ongoing Phase 3 trial in HoFH and the FDA approved Evinacumab on February 11, 2021, for adults and pediatric patients 12 years and older for treatment of HoFH. EMA approved Evinacumab in June 2021 as an adjunct to diet and other low-density lipoprotein-cholesterol (LDL-C) lowering therapies for the treatment of adult and adolescent patients aged 12 years and older with homozygous familial hypercholesterolaemia (HoFH). Regeneron launched Evinacumab in the United States in March 2021. Evinacumab was licensed to Ultragenyx Pharmaceutical Inc in countries outside the US in January 2022. Although administered through intravenous infusion, physicians may now consider this product for HoFH patients as an alternative to lomitapide. Other competitors may succeed in developing, acquiring or licensing additional pharmaceutical products that are introduced into the market and that are more effective, have a more favorable safety profile or are less costly than our products.

Although Myalept is the first and only product approved in the United States for the treatment of complications of leptin deficiency in patients with GL, there are a number of therapies approved to treat these complications independently that are not specific to GL. Myalepta also faces competition in the European Union, both for the treatment of GL and PL. Our competitors are also developing products, which, if approved, and depending on the labelled indication, could potentially compete with metreleptin.

The acromegaly market has many established competitors, dominated by Novartis and Ipsen, who like the rest of the competition offer injectable SSA’s. Mycapssa® is the only oral SSA available on the market. Crinetics Pharmaceuticals are developing paltusotine, which if approved would be the second oral SSA to enter the market and compete directly with Mycapssa. Crinetics also have a Ph3 study to evaluate effect in treatment-naïve patients. If studies are successful, filings could take place at end of 2023 / early 2024.

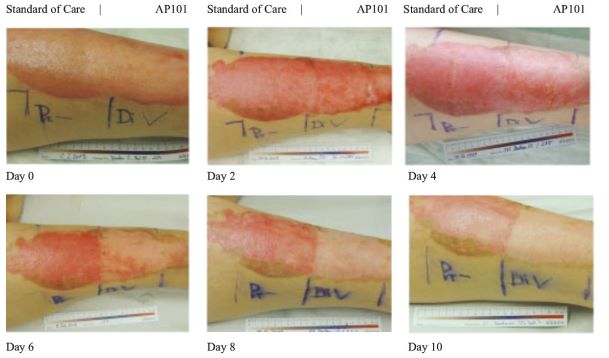

Although there are no approved products in the United States and the European Union for the treatment of EB, our competitors are developing products, which, if approved, and depending on the labelled indication, could potentially compete with Oleogel-S10. One such competitor on the near-term horizon is a potential competitor from Krystal Biotech – B-VEC. B-VEC is gene therapy delivered through a herpes simplex viral vector with studies focused on the narrower population of DEB patients. In November 2021 Kyrstal announced that its Ph3 GEM-3 study of B-VEC, known as Vyjuvek™, met its primary endpoint of complete wound healing at six-month timepoints and its secondary endpoint of complete wound healing at three-month timepoints. Additionally, Vyjuvek™ was shown to be well-tolerated, with no drug-related serious adverse events or discontinuations. They could file a Biologics License Application in Q2 2022, with potential approval in the second half of 2022 and file for MAA in EU in the second half of 2022. Although there is overlap with Oleogel-S10, Amryt believe that this lifelong condition will require multiple therapeutic options.

Other competitors may succeed in developing, acquiring or licensing additional pharmaceutical products that are introduced into the market and that are more effective, have a more favorable safety profile, or are less costly than our products. If we do not compete successfully, our operating margins, financial condition and cash flows could be adversely affected.

We commercialize our products through both a direct sales force and through strategic relationships with third parties for commercialization, distribution, sales and marketing in certain jurisdictions. If we are unable to adequately develop and maintain our sales, marketing and distribution capabilities or enter into business arrangements, we may not be successful in commercializing our product candidates.

We sell lomitapide, Mycapssa® and metreleptin directly in the United States using our own marketing and sales resources and also market and sell, or plan to market and sell, our products directly in certain key countries outside the United States where such products are, or may be, approved using country managers or local distributors to the extent rights to commercialize such products are not out-licensed. We also make our products available on a named patient basis as a result of the approval of our products in the United States or the European Union. We use third parties to provide sales, warehousing, shipping, third-party logistics, invoicing, collections and other distribution services on our behalf in connection with the sale of products globally. Metreleptin is also available in: Italy, Greece, France, Germany, Austria, Switzerland, United Kingdom, Denmark, Spain, Portugal, Serbia, Russia, Kazakhstan, Saudi Arabia, Israel, Turkey, Oman, Qatar, Bahrain, UAE, Colombia, Brazil and Argentina. Metreleptin was out-licensed to Shionogi & Co. Ltd. (“Shionogi”) in Japan. Lomitapide is also available in: the Netherlands, Germany, Austria, Spain, Greece, Italy, United Kingdom, Sweden, Norway, Denmark, France, Hungary, Czech Republic, Russia, Qatar, Kuwait, Saudi Arabia, Canada, Brazil, Colombia and Argentina. We also out-licensed lomitapide for sale by Recordati Rare Diseases Inc. (“Recordati”) in Japan. Mycapssa® is currently only sold in the United States.

For example, there is currently a contract with a single specialty pharmacy distributor in the United States for the distribution of lomitapide, Mycapssa® and metreleptin, a single distributor in Brazil for lomitapide and metreleptin, and single distributors, third-party logistics providers, importers and/or specialty pharmacies in certain other countries, including the European Union for lomitapide and metreleptin. We have entered into or may selectively seek to establish sales, distribution and similar forms of arrangements to grow revenue in existing territories and gain access to new territories and to reach patients in certain geographies that we do not believe can be cost-effectively addressed with our own sales and marketing capabilities. If we are unable to establish, maintain and finance the capabilities to sell, market and distribute our products, either through our own capabilities or through arrangements with third parties, and to effectively manage those third parties, or if we are unable to enter into distribution agreements in countries that we do not believe can be cost-effectively addressed with our own sales and marketing capabilities, we may not be able to successfully sell our products. We cannot guarantee that we will be able to establish, maintain and finance our own capabilities or to enter into and maintain favorable distribution agreements with third parties on acceptable terms, if at all.

To the extent that we enter into arrangements with third parties to perform sales, marketing or distribution services, the product revenues or the profitability of these product revenues may be lower than if we were to commercialize the products on our own. We will have limited control over such third parties, and any of them may fail to devote the necessary resources and attention to sell and market the products effectively, and may also, despite our compliance diligence reviews, audits and training, engage in non-compliant / illegal activities including U.S. Foreign Corrupt Practices Act of 1977 (“FCPA”) violative activity that, directly or indirectly, impact the use or sales of the products or damage our relationships with relevant stakeholders. Any performance failure, inability or refusal of our specialty pharmacy distributors, or third-party service providers to perform, or any failure to renew existing agreements on favorable terms, or at all, could cause serious disruption and impair our commercial or named patient sales of the products, which may have a material adverse effect on our business, financial condition and results of operations. Adverse actions with third parties and contract manufacturing organizations we enter into arrangements with including adverse regulatory actions could negatively impact the company. Furthermore, the expenses associated with maintaining sales force and distribution capabilities may continue to be substantial compared to the revenues we generate. If we are unable to establish and effectively maintain adequate sales, marketing and distribution capabilities, whether independently or with third parties, we may not be able to generate product revenues, which may have a material adverse effect on our business, financial condition, results of operations and prospects. See “—Risks Related to our Reliance on Third Parties.”

The successful commercialization of our product candidates will depend in part on the extent to which governmental authorities and health insurers establish adequate coverage, reimbursement levels and pricing policies. Failure to obtain or maintain coverage and adequate reimbursement for our product candidates, if approved, could limit our ability to market those products and decrease revenue generating ability.

The availability and adequacy of coverage and reimbursement by governmental healthcare programs such as Medicare and Medicaid, private health insurers and other third-party payers is essential for many patients to be able to afford prescription medications such as our products and potential product candidates, assuming regulatory approval is obtained. Our ability to achieve acceptable levels of coverage and reimbursement for products by governmental authorities, private health insurers and other organizations will affect the success of our approved products and product candidates. Assuming we obtain coverage for our product candidates by third-party payers, the resulting reimbursement payment rates may not be adequate or may require co-payments that patients find unacceptably high. We cannot be sure that coverage and reimbursement in the United States, the EU Member States, or elsewhere will be available for the product candidates or any product that we may develop, and any reimbursement that may become available may be decreased or eliminated in the future.

Further, it is possible that a third-party payer may consider our product candidates as substitutes and only offer to reimburse patients for a less expensive product. Even if we show improved efficiency or convenience of administration with our product candidates compared to products marketed by our competitors and the prevailing SOC, the pricing of existing therapies may still limit the amount we could charge. Third-party payers may deny or revoke the reimbursement status of any given product or establish new prices for existing marketed products that inhibit us from realizing an appropriate return on our investment in the product candidates. If reimbursement is not available or is available only at limited levels, we may not be able to successfully commercialize our product candidates and may not be able to obtain a satisfactory financial return on them.

Outside the United States, the success of our products and operations is subject to extensive governmental price controls and other market regulations which may materially and adversely affect our ability to generate commercially reasonable revenue and profits.

Our operations are subject to extensive governmental price controls and other market regulations in the United Kingdom and other countries outside of the United States. The increasing emphasis on cost-containment initiatives in the various EU Member States and other countries can put pressure on the pricing and usage of currently marketed products and product candidates in the future. In many countries, the prices of medical products are subject to varying price control mechanisms as part of national health systems. Some EU Member States have established free-pricing systems, but regulate the pricing for drugs, inter alia, through profit control schemes. However, the UK, which has implemented the most vigorous scheme, has officially left the European Union on January 31, 2020. Additional foreign price controls or other changes in pricing regulation could restrict the amount that we are able to charge for our product candidates. Accordingly, in markets outside the United States, the reimbursement for our currently marketed products and our product candidates in the future may be reduced and may be insufficient to generate sufficient revenues and profits. Moreover, increasing efforts by governmental and third-party payers in the United States and abroad to control healthcare costs may cause such organizations to limit both coverage and the level of reimbursement for newly approved products and, as a result, they may not cover or provide adequate payment for our products, or any other product candidates we may develop in the future.

A number of adverse effects have been reported in clinical trials for metreleptin, lomitapide, oral octreotide and Oleogel-S10, and the prescribing information for each of lomitapide, metreleptin and oral octreotide contains significant limitations on use and other important warnings and precautions, any of which could negatively affect the market acceptance, dropout rates and marketing approval for these products, and post-marketing commitments could identify additional adverse events and safety or efficacy risks, which could further harm our business.

The prescribing information for lomitapide in the United States and the European Union and in other countries in which lomitapide is approved contains significant limitations on use and other important warnings and precautions, including, but not limited to, a boxed warning in the Juxtapid U.S. labeling, additional monitoring which is identified by a black inverted triangle in the product information for Lojuxta in the European Union, warnings in the prescribing information for Lojuxta citing concerns over liver toxicity associated with use of lomitapide, European Risk Management Plan (RMP) materials for physicians and patients, and a U.S. Risk Evaluation Mitigation Strategy (“REMS”) program. The prescribing information for metreleptin in the United States and European Union contains important warnings and precautions, including but not limited to, a boxed warning on the Myalept label in the United States, citing the risk of anti-metreleptin antibodies with neutralizing activity, risk of lymphoma and a U.S. REMS program. As with the U.S. label, the Myalepta Summary of Product Characteristics in the European Union notes that the consequences of neutralizing antibodies with respect to the loss of efficacy or serious or severe infections is not well characterized but could reduce how well the leptin found naturally in the body works or how well Myalepta works.

Patients reported various adverse reactions in the Phase 3 study of lomitapide, including reports of gastrointestinal events by 93% of patients, and in the HoFH clinical trial, including diarrhea, nausea, vomiting, dyspepsia, abdominal pain, weight loss, abdominal discomfort, abdominal distension, constipation, flatulence, increased alanine aminotransferase, chest pain, influenza, nasopharyngitis, and fatigue. Elevations in liver enzymes and hepatic (liver) fat were also observed.

GL patients in the Phase 3 study of metreleptin reported various adverse drug reactions, including weight loss, hypoglycemia, decreased appetite, fatigue, neutralizing antibodies and alopecia. Additionally, although none were assessed as drug related, there were four reported treatment-emergent deaths over the course of the 14-year study duration. Upon further investigation, these reports were consistent with the underlying morbidity of lipodystrophy and included renal failure, cardiac arrest (with pancreatitis and septic shock), progressive end-stage liver disease (chronic hepatic failure), and hypoxic-ischemic encephalopathy. In the open-label, long-term, investigator-sponsored study of metreleptin for the treatment of metabolic disorders associated with lipodystrophy syndromes (initiated in 2000 and conducted at the National Institutes of Health (“NIH”)), there were two cases of peripheral T-cell lymphoma and one case of a localized anaplastic lymphoma (kinase-positive anaplastic large cell lymphoma, which is a type of T-cell lymphoma). Both of the cases of peripheral T-cell lymphoma were reported in patients with acquired GL, and both had evidence of pre-existing lymphoma and/or bone marrow/hematologic abnormalities before metreleptin therapy. A third case of anaplastic large cell lymphoma occurred in the context of a specific chromosomal translocation.

These adverse events, coupled with the boxed warnings and other label restrictions, could cause healthcare providers, regulators and patients or potential patients to view the risks associated with our products as outweighing the benefits. This could cause patients to discontinue use and limit the number of new patients, thereby negatively affecting our business, financial condition, results of operations and prospects. In addition, as part of the post-marketing commitment to the FDA for both lomitapide and metreleptin, we are conducting post-marketing registries to better understand their long-term safety and effectiveness. For lomitapide, we are conducting a long-term observational cohort study (product exposure registry) to better understand the long-term safety, patterns of use, compliance and long-term effectiveness of controlling LDL levels. For metreleptin, we are conducting a long-term, prospective, observational study (product exposure registry) to identify and better understand any serious risks related to the use of the product. Finally, we are conducting sequential programs to expand the understanding of metreleptin immunogenicity and manufacturing. The final program regarding the immunogenicity of metreleptin was initiated in 2018, and the final post-marketing study related to the manufacturing of metreleptin is expected to be completed by the deadlines agreed with the FDA. In addition, we are working to implement post-marketing commitments in the European Union for metreleptin, including a pediatric study in GL patients, an immunogenicity program, a post-approval study in PL and to enroll European patients in the product exposure registry. A failure to meet post-marketing commitments to the FDA, the EMA or other regulatory authorities could impact the ability to continue to market lomitapide or metreleptin, respectively, in countries where we are unable to meet such commitments. A Phase 3, randomized, multicenter, double-blind, placebo-controlled study of metreleptin in patients with partial lipodystrophy (PL) was initiated at the end of Q4 2021 with registration intent to include this population in the US label. In general, we may not be able to meet our post marketing commitments for our current approved products and those in development which could materially impact our ability to commercialize our products and therefore have a material impact on the success of our business.

In the course of conducting observational cohort studies, additional clinical studies (such as pursuant to a pediatric investigation plan (“PIP”) in the European Union), post-marketing surveillance, or re-evaluation of any completed clinical study data could identify, additional safety information on known or unknown side effects or new undesirable side effects caused by our products or product candidates, or the data may raise other issues with respect to the products. In such instances, a number of potentially significant negative consequences could result, including:

| • | we may experience a negative impact on market acceptance and increased dropout rates; |

| • | regulatory authorities may suspend, withdraw or alter their approval of the relevant product; |

| • | regulatory authorities may require the addition of labeling statements, such as warnings or contraindications or distribution and use restrictions such as, for example, the modifications to the Juxtapid label to include language instructing patients to cease therapy upon the occurrence of severe diarrhea; |

| • | regulatory authorities may issue, or require us to issue additional specific communications such as safety alerts, field alerts, or “Dear Doctor” letters to healthcare professionals; |

| • | regulatory authorities may require us to recall, withdraw, or stop selling a product or take other enforcement action; |

| • | we may receive negative publicity; |

| • | we may be required to change the way the relevant product is administered, conduct additional preclinical studies or clinical trials or restrict the distribution or use of the relevant product; |

| • | patients could suffer harm, and we could be sued and held liable for harm caused to patients; |

| • | the regulatory authorities may require us to amend the relevant REMS program, Risk Management Plan or comparable equivalent; and |

| • | our reputation may suffer. |

Mycapssa® (oral octreotide capsules) is approved in the US for use in patients who have responded to and tolerated octreotide or lanreotide, injectable somatostatin analogues (SSAs). Approval in the European Union is under review by the EMA with an anticipated approval date of Q3 2022. In the US, the prescribing information does not include any boxed warnings. The safety profile of Mycapssa® is consistent with that seen with injectable octreotide with the exception of the absence of injection site reactions. Warnings and precautions include the risks of cholelithiasis and complications of cholelithiasis, hypoglycemia or hyperglycemia, hypothyroidism bradycardia, arrhythmia, or cardiac conduction abnormalities, decreased Vitamin B12 Levels and an abnormal Schilling's Tests. There are no FDA post approval commitments for Mycapssa® in the treatment of Acromegaly patients but the company is conducting a 2 year observation registry study in patients with acromegaly receiving treatment with Mycapssa® as well as other drug treatments for acromegaly.