UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

________________________________________________

FORM 10-K

________________________________________________

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2024

OR | | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 001-39220

________________________________________________

CARRIER GLOBAL CORPORATION

(Exact name of registrant as specified in its charter)

________________________________________________

| | | | | | | | |

| Delaware | | 83-4051582 |

| (State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

13995 Pasteur Boulevard, Palm Beach Gardens, Florida 33418

(Address of principal executive offices, including zip code)

(561) 365-2000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Stock ($0.01 par value) | | CARR | | New York Stock Exchange |

| 4.125% Notes due 2028 | | CARR28 | | New York Stock Exchange |

| 4.500% Notes due 2032 | | CARR32 | | New York Stock Exchange |

| | | | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒. No ☐.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☒ | Accelerated filer | ☐ | Emerging growth company | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting Common Stock held by non-affiliates of the Registrant as of June 30, 2024, the last business day of the Registrant's most recently completed second fiscal quarter, was approximately $53.2 billion, based on the New York Stock Exchange closing price for such shares on that date. Solely for purposes of this disclosure, shares of Common Stock held by executive officers and directors of the Registrant as of such date have been excluded because such persons may be deemed to be affiliates. This determination of executive officers and directors as affiliates is not necessarily a conclusive determination for any other purpose.

As of January 31, 2025, there were 868,339,902 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III hereof incorporates by reference portions of the Registrant's definitive proxy statement related to its 2025 annual meeting of shareowners.

Index

Carrier Global Corporation and its subsidiaries' names, abbreviations thereof, logos and product and service designators are all either the registered or unregistered trademarks or trade names of Carrier Global Corporation and its subsidiaries. Names, abbreviations of names, logos and products and service designators of other companies are either the registered or unregistered trademarks or trade names of their respective owners. As used herein, the terms "we," "us," "our," "the Company" or "Carrier," unless the context otherwise requires, mean Carrier Global Corporation and its subsidiaries. References to internet websites in this Annual Report on Form 10-K (the "Annual Report") are provided for convenience only. Information available through these websites is not incorporated by reference into this Annual Report.

CAUTIONARY NOTE CONCERNING FACTORS THAT MAY AFFECT FUTURE RESULTS

This Annual Report contains statements which, to the extent they are not statements of historical or present fact, constitute "forward-looking statements" under the securities laws. From time to time, oral or written forward-looking statements may also be included in other information released to the public. These forward-looking statements are intended to provide management’s current expectations or plans for our future operating and financial performance, based on assumptions currently believed to be valid. Forward-looking statements can be identified by the use of words such as "believe," "expect," "expectations," "plans," "strategy," "prospects," "estimate," "project," "target," "anticipate," "will," "should," "see," "guidance," "outlook," "confident," "scenario" and other words of similar meaning in connection with a discussion of future operating or financial performance. Forward-looking statements may include, among other things, statements relating to future sales, earnings, cash flow, results of operations, uses of cash, share repurchases, tax rates and other measures of financial performance or potential future plans, strategies or transactions of Carrier, Carrier's plans with respect to our indebtedness and other statements that are not historical facts. All forward-looking statements involve risks, uncertainties and other factors that may cause actual results to differ materially from those expressed or implied in the forward-looking statements. For those statements, we claim the protection of the safe harbor for forward-looking statements contained in the U.S. Private Securities Litigation Reform Act of 1995. Such risks, uncertainties and other factors include, without limitation:

•the effect of economic conditions in the industries and markets in which Carrier and our businesses operate in the U.S. and globally and any changes therein, including financial market conditions, inflationary cost pressures, fluctuations in commodity prices, interest rates and foreign currency exchange rates, levels of end market demand in construction, the impact of weather conditions, pandemic health issues, natural disasters and the financial condition of our customers and suppliers;

•challenges in the development, production, delivery, support, performance and realization of the anticipated benefits of advanced technologies and new products and services;

•future levels of capital spending and research and development spending;

•future availability of credit and factors that may affect such availability, including credit market conditions and Carrier's capital structure and credit ratings;

•the timing and scope of future repurchases of Carrier's common stock, including market conditions and the level of other investing activities and uses of cash;

•delays and disruption in the delivery of materials and services from suppliers;

•cost reduction efforts and restructuring costs and savings and other consequences thereof;

•new business and investment opportunities;

•the outcome of legal proceedings, investigations and other contingencies;

•the impact of pension plan assumptions on future cash contributions and earnings;

•the impact of the negotiation of collective bargaining agreements and labor disputes;

•the effect of changes in political conditions in the U.S. and other countries in which Carrier and our businesses operate, including the effect of changes in U.S. trade policies, on general market conditions, global trade policies, the imposition of tariffs, and currency exchange rates in the near term and beyond;

•the effect of changes in tax, environmental, regulatory (including among other things import/export) and other laws and regulations in the U.S. and other countries in which we and our businesses operate;

•the ability of Carrier to retain and hire key personnel;

•the scope, nature, impact or timing of acquisition and divestiture activity, such as our acquisition of the VCS Business (as defined below) and our portfolio transformation transactions, including among other things integration of acquired businesses into existing businesses and realization of synergies and opportunities for growth and innovation and incurrence of related costs;

•a determination by the U.S. Internal Revenue Service ("IRS") and other tax authorities that the Distribution (as defined below) or certain related transactions should be treated as taxable transactions; and

•risks associated with current and future indebtedness, as well as our ability to reduce indebtedness and the timing thereof.

This Annual Report includes important information as to risks, uncertainties and other factors that may cause actual results to differ materially from those expressed or implied in the forward-looking statements. See the Notes to the Consolidated Financial Statements in this Annual Report under the heading "Note 23 – Commitments and Contingent Liabilities," the sections entitled "Management's Discussion and Analysis of Financial Condition and Results of Operations" under the headings "Business Overview," "Results of Operations," "Liquidity and Financial Condition," and "Critical Accounting Estimates," and the section entitled "Risk Factors." This Annual Report also includes important information as to these factors in the "Business" section under the headings "General," "Other Matters Relating to Our Business as a Whole," and in the "Legal Proceedings" section. The forward-looking statements speak only as of the date of this report or, in the case of any document incorporated by reference, the date of that document. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by applicable law. Additional information as to factors that may cause actual results to differ materially from those expressed or implied in the forward-looking statements is disclosed from time to time in our other filings with the United States Securities and Exchange Commission ("SEC").

This Annual Report and our Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports are available free of charge through the Investors section of our Internet website (http://www.corporate.carrier.com) under the heading "SEC Filings" as soon as reasonably practicable after these reports are electronically filed with, or furnished to, the SEC. In addition, the SEC maintains an Internet website (http://www.sec.gov) containing reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

PART I

ITEM 1. BUSINESS

General

Carrier Global Corporation ("we" or "our" or the "Company") is a global leader in intelligent climate and energy solutions with a focus on providing differentiated, digitally-enabled lifecycle solutions to our customers. Our portfolio includes industry-leading brands such as Carrier, Viessmann, Toshiba, Automated Logic and Carrier Transicold that offer innovative heating, ventilating and air conditioning ("HVAC"), refrigeration and cold chain transportation solutions to help make the world safer and more comfortable. We also provide a broad array of related building services, including audit, design, installation, system integration, repair, maintenance and monitoring.

Through our performance-driven culture, we anticipate creating long-term shareowner value by investing strategically to strengthen our product position in homes, buildings and across the cold chain in order to drive profitable growth. We believe our business segments are well positioned to benefit from favorable secular trends, including the mega-trends of urbanization, population growth and demographic shifts, food security and safety, digitalization, global connectivity and energy efficiency. Coupled with our industry-leading brands and track record of innovation, we continue to provide market-leading solutions for our customers.

In addition, we continue to invest in product and technology innovation within our offerings as well as invest in new business models including Carrier Energy, our solution to reduce demands on power grids and energy infrastructure by better managing energy consumption and reducing end-customer energy costs. This new business model is also expected to provide a digital connection between the end-customers and Carrier, providing us with opportunities to offer services and aftermarket parts and components over the life of a product.

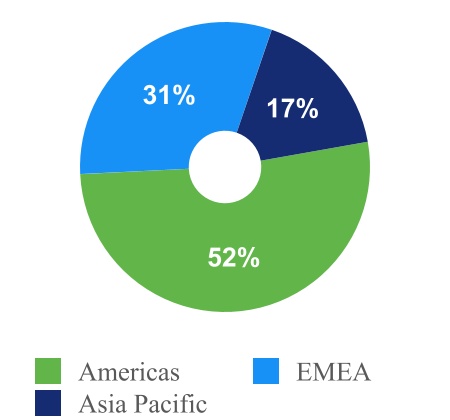

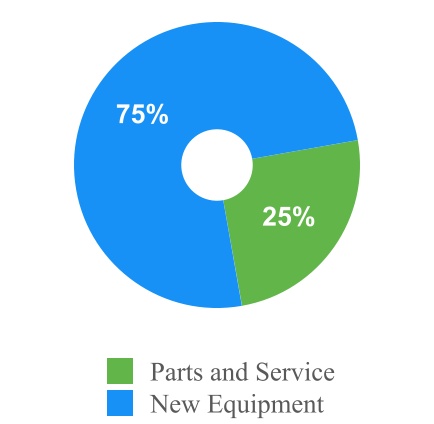

For the year ended December 31, 2024, our net sales were $22.5 billion and our operating profit was $2.6 billion. Our net sales for 2024 were derived from the Americas (52%), Europe, Middle East and Africa ("EMEA") (31%) and Asia-Pacific (17%). Our international operations, including U.S. export sales, represented approximately 50% of our net sales for 2024. During the same period, new equipment comprised 75% and parts and service comprised 25% of our net sales.

| | | | | | | | | | | | | | |

| Sales by Segment * | | Net Sales by Region | | Sales by Type |

* Segment sales include inter-company sales.

Separation from United Technologies Corporation

On April 3, 2020 (the "Distribution Date"), United Technologies Corporation, ("UTC"), since renamed RTX Corporation ("Raytheon Technologies Corporation" or "RTX") completed the spin-off of Carrier into an independent publicly traded company (the "Separation") through a pro rata distribution (the "Distribution") on a one-for-one basis of all of the outstanding shares of common stock of Carrier to UTC shareowners who held shares of UTC common stock as of the close of business on March 19, 2020, the record date of the Distribution. In addition, we entered into several agreements with UTC and Otis Worldwide Corporation ("Otis") that govern various aspects of the relationship among us, UTC and Otis following the Separation and Distribution. As of December 31, 2024, only certain portions of the Tax Matters Agreement ("TMA") remain in effect.

Business Segments

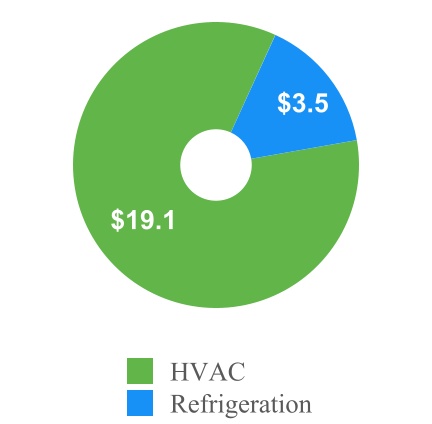

We globally manage our business operations through two segments: HVAC and Refrigeration. Each respective segment's major products, services and distribution methods are as follows:

The HVAC segment provides products, controls, services and solutions to meet the heating, cooling and ventilation needs of our customers while enhancing building performance, health and energy efficiency. Products and services include air conditioners, heating systems, heat pumps, building automation systems, aftermarket components, repair and maintenance services and rentals as well as modernization and upgrades through the product lifecycle. Our products and services cover a wide range of customers, including in the residential, commercial, education, healthcare, technology, retail, hospitality, data center, and infrastructure markets, among others. Products and solutions are sold directly to building contractors and owners and indirectly through joint ventures, independent sales representatives, distributors, wholesalers, dealers and retail outlets. Our established brands include Carrier, Viessmann, Toshiba, Automated Logic, Bryant, CIAT, Day & Night, Heil, NORESCO and Riello which offer an innovative and complete portfolio of products that provide numerous solutions for our customers. These products, in addition to the markets they serve, provide future service opportunities including replacement components, preventative and on-demand contractual maintenance and repair, digital monitoring and modifications/upgrades.

The Refrigeration segment provides products, services and monitoring for reliable transport and preservation of food, medicine and other perishable cargo. Products include trucks, trailers, shipping containers and intermodal applications to meet customer needs for both ground transport and ocean freight, while services include maintenance, repair, and monitoring. Products and services are sold directly to transportation companies and indirectly through joint ventures, independent sales representatives, distributors, wholesalers and dealers. Products and services are sold under established brand names, including Carrier Transicold and Sensitech. We provide customers the flexibility to select solutions from a very broad range of technologies including fossil fuel applications and electric solutions to best adhere to their objectives and preferences as well as regulatory requirements. In addition, our focus on digitalization and innovation is expanding our offering of service and aftermarket solutions, including on-demand and subscription-based monitoring of customer cargo. Through the lifecycle of the product, we also offer modifications and upgrades to the current installed base, improving energy efficiency, noise or other customer requirements.

Portfolio Transformation

In 2023, we began the journey to further simplify our company and accelerate our business strategy. Our actions transformed our business portfolio in an effort to establish us as a pure-play, global leader in intelligent climate and energy solutions. We believe that our greater focus on breakthrough innovation, electrification, energy-efficient solutions, the use of environmentally friendly refrigerants and connected ecosystems will further strengthen our global leadership position in our end-markets and provide responsible solutions for our customers.

On April 25, 2023, we announced that we entered into a Share Purchase Agreement (the “Agreement”) to acquire the climate solutions business (the "VCS Business") of Viessmann Group GmbH & Co. KG (“Viessmann”), a privately-held company. The VCS Business develops intelligent, integrated and sustainable technologies, including heat pumps, boilers, photovoltaic systems, home battery storage and digital solutions, primarily for residential customers in Europe. The acquisition was completed on January 2, 2024 and reported within our HVAC segment.

On June 2, 2024, we completed the sale of our Access Solutions business ("Access Solutions") to Honeywell International Inc. ("Honeywell") for cash proceeds of $5.0 billion. Access Solutions, historically reported in our Fire & Security segment, is a global supplier of physical security and digital access solutions supporting the hospitality, commercial, education and military markets. We recognized a net gain on the sale of $1.8 billion.

On July 1, 2024, we completed the sale of our Industrial Fire business ("Industrial Fire") for cash proceeds of $1.4 billion. Industrial Fire, historically reported in our Fire & Security segment, is a leading manufacturer of a full spectrum of fire detection and suppression solutions and services in critical high-hazard environments, including oil and gas, power generation, marine and offshore facilities, automotive, data centers and aircraft hangars. We recognized a net gain on the sale of $319 million.

On October 1, 2024, we completed the sale of our Commercial Refrigeration business ("CCR") for cash proceeds of $679 million. CCR, historically reported in our Refrigeration segment, is a global supplier of turnkey solutions for commercial refrigeration systems and services, with a primary focus on serving food retail customers, cold storage facilities and warehouses. We recognized a net gain on the sale of $292 million. The net proceeds received are subject to working capital and other adjustments provided in the stock purchase agreement.

On December 2, 2024, we completed the sale of our Commercial and Residential Fire business ("CRF Business") for cash proceeds of $2.9 billion. The CRF Business, historically reported in our Fire & Security segment, is a leading manufacturer of fire detection and alarm solutions for both commercial and residential applications. We recognized a net gain on the sale of $1.4 billion. The net proceeds received are subject to working capital and other adjustments provided in the stock purchase agreement.

Business Strategy

Our vision is to be a global leader in intelligent climate and energy solutions with a focus on providing differentiated, digitally-enabled lifecycle solutions to our customers. To achieve our vision, our core business strategy is to create innovative, differentiated products and solutions to provide a fully-integrated customer experience in order to be our customer’s preferred provider. We believe our strategy is supported by significant favorable secular trends, our industry-leading brands and track record of innovation. Our business strategy is built around the following pillars to drive long-term growth and deliver shareholder value:

Differentiated Products, Channels and Brands

Our strategy involves driving organic growth by further enhancing our proven track record of innovation, which is focused on designing smarter, more connected and more efficient sustainable systems and solutions. Our strategy also relies on our iconic, industry-leading brands and on strengthening our long-term relationships with channel partners and customers by offering solutions that anticipate customer needs with a focus on technologies related to energy efficiency, emissions, air quality, electrification, refrigerants with lower global warming potential and noise reduction.

Digitally-Enabled Lifecycle Solutions

We are focused on offering a comprehensive and differentiated suite of sustainable technologies and services. We expect that these solutions increase our total available market opportunity, enhance our predictive service and maintenance capabilities, strengthen our customer intimacy and increase aftermarket growth. Beginning with product design, our product offerings are moving towards digitally-enabled solutions that connect us to our customers throughout the product’s full lifecycle and help us grow our aftermarket sales. We plan to meet our customer’s needs by offering a wider-range of aftermarket products and services including replacement components, preventative and on-demand maintenance and repair, digital monitoring and modifications/upgrades. Our digitally-enabled lifecycle solutions include Abound, a cloud-based building platform that unlocks and unites building data to create healthy, sustainable and intelligent solutions for indoor spaces. It gathers data from disparate systems, sensors and sources; identifies opportunities to optimize performance; and works with healthy building solutions to improve occupant experiences. In addition, our Lynx digital platform, developed in collaboration with Amazon Web Services (“AWS”), allows customers to leverage data to enhance visibility, resiliency, agility and efficiency in the cold chain to reduce loss of cargo, lower operations costs and support real-time decisions.

Expand Portfolio with Energy Management Solutions

As power grids and transportation infrastructure shift from fossil fuels to renewables, we will continue to position ourselves as a leader in innovative solutions that reduce emissions and energy consumption and promote power grid stability. Our solutions range from residential home energy management to sustainable solutions for commercial and industrial buildings to optimized low noise and low gas emission transport solutions. With the addition of the VCS Business on January 2, 2024, we are well positioned to provide complete energy solutions globally. Our portfolio includes environmentally friendly refrigerants, high temperature heat pumps for use in industrial and commercial applications, natural refrigerant heat pumps for residential buildings and a connected ecosystem for homes including solar PV, batteries and a differentiated digital platform, all supported by extensive service and aftermarket offerings.

Strategic Capital Allocation

Our priorities for capital deployment include funding organic growth, acquisitions and capital returns to shareowners through a growing and sustainable dividend and share repurchases. We pursue potential acquisitions to complement existing products and services and to expand the range of technologies and solutions available to our customers. We leverage our global operations, the strength of our iconic, industry-leading brands and our success in creating valuable partnerships to focus on targeted expansion into new locations and channels where we believe that we can drive profitable growth. These drivers are supported by research and development activities with a focus on new product development and new technology innovation. In addition, Carrier Ventures, our global venture capital wholly-owned subsidiary, focuses on investments to accelerate the development of sustainable innovations and disruptive technologies to transform future building and cold chain management. It engages in strategic partnerships with high growth organizations as they invest in the development of technologies to innovate and commercialize the next generation of integrated offerings.

Other Matters Relating to Our Business as a Whole

Competitive Conditions

Each of our businesses is subject to significant competition from a number of companies throughout the world. Due to the nature of our products and services and the markets we serve, our competition can vary from regional or specialized companies to larger public or private companies.

The most significant competitive factors we face are technology differentiation, product performance, service, delivery schedule and price. Brand reputation, service to customers and quality are also important competitive factors for our products and services. While our competitive position varies among our products and services, we are a significant competitor with respect to each of our major product and service offerings. We believe that the loss of any individual contract or customer would not have a material adverse effect on our results.

Raw Materials and Supplies

We rely on suppliers and commodity markets to secure components and raw materials such as copper, aluminum and steel. In addition, we also use semi-conductors and other electronic components in the manufacture of our products. To maximize our buying effectiveness and leverage our scale, we have a central strategic sourcing group that consolidates purchases of certain materials and components across our business segments. We work closely with our suppliers to ensure availability of products and implement other cost savings initiatives. In addition, we continue to invest in our supply chain to improve its resilience with a focus on automation, dual sourcing of critical components and localized manufacturing when feasible.

Intellectual Property

We maintain a broad portfolio of patents, trademarks, copyrights, trade secrets, licenses and franchises related to our business to protect our research and development investments and to maintain our competitive advantages. We hold approximately 12,000 active patents and pending patent applications worldwide. From time to time, we take actions to protect our business by asserting our intellectual property rights against third-party infringement. We believe that we have taken reasonable measures to build and protect this portfolio of intellectual property rights, but we cannot be assured that these rights will not be challenged, found invalid or unenforceable.

Operating System

We plan to continue to foster operational, financial and commercial excellence to drive sales and earnings growth. With roots in our legacy manufacturing and business processes, the Carrier operating system — Carrier Excellence — is our continuous improvement framework that is expected to drive operational excellence across our businesses. Our Supplier Excellence program is intended to apply these same operating principles to our supply base and we continue to focus on strategic cost reductions through operational efficiency, digitalization, automation and supply chain productivity.

Joint Ventures and Strategic Relationships

Our joint ventures and strategic relationships are an important part of our business. We hold direct ownership interests in approximately 55 joint ventures, the financial results of which are accounted for by the equity method of accounting or the cost basis of accounting, of which 97% of such investments are in our HVAC segment. These relationships engage in distribution, manufacturing and product development activities and are integral to our business operations and growth strategy.

Seasonality

Demand for certain of our products and services is seasonal and can be impacted by weather conditions. For instance, sales and services of our HVAC products to residential customers have historically been higher in the second and third quarters of the calendar year, which represent the peak seasons for air conditioning-related sales in North America markets. A change in building and remodeling activity also can affect our financial performance. In addition, our financial performance may be influenced by the production and utilization of transport equipment, including truck production cycles in North America and Europe.

Compliance with the Regulation of our Business and Operations

We operate our businesses and sell our products all over the world. As a result, rapid changes in legislation, regulations and government policies affect our operations and business in the countries, regions and localities in which we operate and sell our products. International accords such as the Paris Agreement and the subsequent U.S. climate policies to meet its nationally determined contributions as well as local regulations in the U.S. reducing the use of fossil fuels in buildings all have the potential to impact our products and service offerings. Such changes, which can render our products and technologies non-compliant, involve refrigerants, noise levels, product and fire safety, hydrofluorocarbon emissions, fluorinated gases, hazardous substances and electric and electronic equipment waste. Increased fragmentation of regulatory requirements changes the manner in which we conduct our business and increases our costs because it necessitates the development of country or regional specific variants, monitoring of and compliance with those regulations and additional testing and certifications. In addition, our operations are subject to and affected by environmental regulations promulgated by federal, state and local authorities in the U.S. and by authorities with jurisdiction over our foreign operations. We have made, and will be required to continue to make, capital expenditures to design and upgrade our products to comply with or exceed environmental and other regulations and energy efficiency standards. However, we believe that the costs related to compliance requirements for environmental or other government regulations will not have a material adverse effect on our capital expenditures, financial results or competitive position.

Environmental Goals

As a global leader in intelligent climate and energy solutions, we are committed to making the world safer, sustainable and more comfortable. We have set ambitious sustainability goals to be reached by 2030, which include the following:

•Invest over $4 billion to develop intelligent climate and energy solutions that reduce environmental impacts,

•Avoid more than 1 gigaton of customer greenhouse gas emissions,

•Achieve carbon neutral operations,

•Reduce energy intensity by 10% across our operations,

•Develop water stewardship programs across our global operations, prioritizing water-scarce locations, and

•Promote sustainability and positively impact communities and our workforce through education, partnerships, programs and volunteering our time and talent.

Human Capital Management

At Carrier, we strive to connect our people to our purpose, our vision, our strategic priorities, our culture and each other, with the ultimate goal to engage our teams, drive success and create value for our customers and shareowners.

Culture and People

Our operating fundamentals - The Carrier Way, Leading People The Carrier Way, and Carrier Excellence – serve as a basis for how we operate our company and drive success, as One Team. The Carrier Way outlines our vision, values, and cultural behaviors. Leading People The Carrier Way sets expectations for people leaders and how we build the best teams. Carrier Excellence is our continuous improvement operating system, a mindset that focuses the organization on enhancing efficiency, and delivering high-quality outcomes across all facets of our business.

Our employees collaborate as one team across more than 50 countries. We develop and deploy best-in-class programs and practices, provide enriching career opportunities, listen to employee feedback and always challenge ourselves to do better. As of December 31, 2024, we had approximately 48,000 employees worldwide, of which 35% are located in the Americas, 36% are located in EMEA and 29% are located in Asia Pacific.

We are an employer of choice and we focus on our Build Best Teams cultural behavior priority through the deployment of our talent ecosystem that connects strategy, embeds talent in our culture and activates it through people programs, processes and leadership. One of our core values in The Carrier Way, inclusion, is fundamental to who we are and what we do. We aspire to have an inclusive culture where each and every employee can come to work, every day, feeling like they _belong, and can contribute to their fullest and greatest potential. We continuously evaluate, modify and enhance our recruitment and retention strategies as part of the overall management of our business.

Aligned to our fundamentals and talent ecosystem, we promote learning and development through technical and leadership programs, as well as tuition assistance to enhance our employees’ skills and abilities. Our offerings include an online platform, strategic partnerships and on-site technical training centers. We conduct annual leadership development reviews to identify future leaders and foster succession planning. We also renew our talent pipeline with internships and early career rotational programs. Through a strategic approach to human capital, we are creating an environment where employees thrive, belong, and contribute to a more sustainable and resilient world.

Employee Well-being, Health and Safety

Creating an environment where employees thrive includes prioritizing health, safety, and overall well-being. We are committed to maintaining world-class standards.

Our Environmental, Health and Safety program is focused on eliminating the risk of serious injuries, illness and fatalities to employees, contractors and customers during manufacturing, installation, servicing and other business activities. We apply rigorous standards to ensure that our operations and premises comply with national and local regulations and our incident reporting requirements. For 2024, our total recordable incident rate ("TRIR"), based upon the number of employee injuries per 200,000 hours worked, was 0.32 and our lost time incident rate ("LTIR") was 0.15.

Our global well-being programs support employees’ physical, mental and financial health, offering flexible benefits, mental health resources, hybrid-work and financial planning tools. Our total rewards philosophy is designed to align the compensation of our employees with individual and company performance and to provide the appropriate market-competitive incentives to attract, retain and motivate employees to achieve superior results.

We measure the Pulse of our workforce three times per year through company-wide employee surveys to help us understand how employees feel about working at Carrier and what we can do to improve their experience.

As of December 31, 2024, in the U.S., 90% of our approximately 4,000 production and maintenance employees were covered under six collective bargaining agreements with expiration dates ranging from 2025 to 2027. In Europe, approximately 16,200 employees are represented by a European Works Council and, at national and local levels, we inform and consult with 49 local works councils and with unions representing employees at approximately 40 sites. Relations with our labor unions and works councils are generally positive.

Corporate Information

Carrier was incorporated in Delaware in connection with the Separation on March 15, 2019. Our principal executive offices are located at 13995 Pasteur Boulevard, Palm Beach Gardens, Florida 33418, and our telephone number is (561) 365-2000. We maintain an Internet website at www.corporate.carrier.com.

ITEM 1A. RISK FACTORS

RISK FACTOR SUMMARY

Risks Related to Our Business

•Risks associated with our international operations could adversely affect our competitive position, results of operations, cash flows or financial condition.

•We are party to joint ventures and other strategic relationships, which may not be successful and may expose us to unique risks and restrictions.

•Risks associated with climate events, government regulations and incentives associated with climate events and mitigation efforts could adversely affect our business.

•Demand for our HVAC products and services is influenced by weather conditions and seasonality.

•Our business and financial performance depend on continued and substantial investments in our information and operational technology infrastructure, which may not yield anticipated benefits and which may be vulnerable to cyber-attacks.

•Cybersecurity incidents could disrupt business operations, result in the loss of critical and confidential information, and adversely impact our reputation and results of operations.

•We engage in acquisitions and divestitures and may encounter difficulties integrating acquired businesses with, or disposing of businesses from, our current operations; therefore, we may not realize the anticipated benefits of these acquisitions and divestitures.

•We incurred debt obligations, and we may incur additional debt in the future, which could adversely affect our business and profitability and our ability to meet other obligations.

•We depend on our intellectual property and have access to certain intellectual property and information of our customers and suppliers. Infringement of or the failure to protect that intellectual property could adversely affect our future growth and success.

•We use a variety of raw materials, supplier-provided parts, and third-party service providers in our business. The ability of suppliers to deliver materials, parts, components and manufacturing equipment to our manufacturing facilities, and our ability to manufacture without disruption, could affect our business performance. Significant shortages, supplier capacity constraints or production disruptions, price increases, duties, tariffs or other government actions could increase our operating costs, disrupt our operations and adversely impact the competitive positions of our products.

•We design, manufacture and service products that incorporate advanced technologies. The introduction of new products and technologies involves risks, and we may not realize the degree or timing of benefits initially anticipated.

•We operate in a competitive environment and our profitability and competitive position depend on our ability to accurately estimate the costs and timing of providing our products and services.

•Customers and others may take disruptive actions.

•Labor matters may impact our business.

•Our defined benefit pension plans are subject to financial market risks that could adversely affect our results.

•We may not realize expected benefits from our cost reduction and restructuring efforts, and our profitability or our business otherwise might be adversely affected.

•Failure to achieve and maintain a high level of product and service quality could damage our reputation with customers and negatively impact our results.

•We are subject to litigation, environmental and other legal and compliance risks.

•We are subject to risks arising from doing business with the U.S. government.

•We may recognize impairment charges for our goodwill and intangible assets.

•Failure to maintain a satisfactory credit rating could adversely affect our liquidity, capital position, borrowing costs and access to the capital markets.

Risks Related to the Separation from UTC

•After the Separation and the Distribution, certain members of management, directors and shareowners own stock in UTC, Carrier and Otis and as a result may face actual or potential conflicts of interest.

•In connection with the Separation into three independent public companies, each of UTC, Carrier and Otis has agreed to indemnify the other parties for certain liabilities. If we are required to pay UTC and/or Otis under these indemnities, our financial results could be negatively impacted. Also, the UTC or Otis indemnities may not be sufficient to hold us harmless from the full amount of liabilities for which UTC and Otis have been allocated responsibility, and UTC and/or Otis may not be able to satisfy their respective indemnification obligations in the future.

•In certain circumstances, we could be required to indemnify UTC for material taxes and other related amounts pursuant to indemnification obligations under the TMA.

•Potential liabilities may arise due to fraudulent transfer considerations, which would adversely affect our financial condition and results of operations.

Risks Related to Our Common Stock

•The market price and trading volume of our common stock may fluctuate significantly.

•Shareowner's percentage of ownership in our common stock may be diluted in the future.

•Quarterly cash dividends may be discontinued or modified, are subject to a number of uncertainties and may affect the price of our common stock.

•Our amended and restated bylaws designate the courts within the State of Delaware as the sole and exclusive forum for certain types of actions and proceedings that may be initiated by our shareowners, which could discourage lawsuits against Carrier and our directors and officers.

•Anti-takeover provisions could enable our Board of Directors to resist a takeover attempt by a third party and limit the power of our shareowners.

General Risks

•Natural disasters, epidemics or other unexpected events may disrupt our operations, adversely affect our results of operations, cash flows or financial condition, and may not be fully covered by insurance.

•We may be affected by global economic, capital market and political conditions, and conditions in the energy, construction, transportation and infrastructure industries in particular. Uncertainty in U.S. trade policy, including uncertainty surrounding changes in tariffs, trade agreements or other trade restrictions imposed by the U.S. or other governments, as well as political conditions in and between the United States and foreign countries in which we operate, could significantly and adversely affect our business and financial results.

•Our business success depends on attracting and retaining key personnel and other talent throughout the Company.

•Additional tax expense or additional tax exposures could affect our future profitability.

•Failure to maintain effective internal controls over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act could materially and adversely affect us.

RISK FACTORS

Our business, financial condition, operating results and cash flows can be impacted by the factors set forth subsequently, any one of which could cause our actual results to vary materially from recent results or from our anticipated future results.

Risks Related to Our Business

Risks associated with our international operations could adversely affect our competitive position, results of operations, cash flows or financial condition.

Approximately 50% of our net sales for the year ended December 31, 2024, are derived from international operations, including U.S. export sales. As a result, changes in local and regional economic conditions, including fluctuating exchange rates, may adversely affect demand for our products and the profits generated by our non-U.S. operations because a significant portion of our sales and expenses are denominated in currencies other than U.S. dollars. While we attempt to manage our exchange rate risks, we are not completely insulated from that exposure. Exchange rates can be volatile and a substantial weakening of foreign currencies against the U.S. dollar could reduce our operating margins in various locations outside of the U.S., which would adversely impact the comparability of our results from period to period.

Our international sales and operations are also subject to the risks associated with changes in local government regulations and policies regarding investments, employment, taxation, incentives, foreign exchange and capital controls and the repatriation of earnings. Moreover, government regulations and policies regarding international trade, such as import quotas, punitive taxes or tariffs or similar trade barriers, whether imposed by individual governments or regional trade blocs, can affect demand for our products and services, impact the competitive position of our products or services or encumber our ability to manufacture or sell or procure products in certain countries. The implementation of more restrictive trade policies, including tariffs, by the U.S. or by other countries, such as China and Mexico, where we sell or produce our products and services or procure materials, including as a result of trade conflict between the U.S. and other countries, could negatively impact our business, results of operations and financial condition. Our international sales and operations are also sensitive to political and economic instability, changes in foreign national priorities and government budgets, and the risks associated with differing legal systems and customs in foreign countries.

We expect that sales to emerging markets will continue to account for a significant portion of our sales as developing nations around the world increase their demand for our products. In addition, as part of our globalization strategy, we have invested in certain countries, including Mexico, Brazil, China, India, Saudi Arabia and other countries in the Middle East. Emerging markets can present many risks, including cultural differences (such as employment and business practices), compliance risks, economic and government instability, exchange rate fluctuations and the imposition of foreign exchange and capital controls. While these factors and their impact are difficult to predict, any one or more of them could have a material adverse effect on our competitive position, results of operations, cash flows or financial condition.

We are party to joint ventures and other strategic relationships, which may not be successful and may expose us to unique risks and restrictions.

Our business operations, particularly in our HVAC segment, depend on various strategic relationships, namely, joint ventures and non-wholly owned subsidiaries. We sell our products and services through certain key distributor, joint venture and similar relationships, including the Carrier Enterprise joint ventures with Watsco, Inc., AHI-Carrier FZC, a United Arab Emirates-based joint venture and various joint ventures with members of the Midea Group.

Some of our strategic relationships engage in manufacturing and/or product development. Loss of a key channel partner, or a significant downturn or deterioration in the business or financial condition of a key channel partner, joint venture or similar relationship, whether related to, among other things, a labor strike, diminished liquidity or credit unavailability, weak demand for products or delays in the launch of new products, could adversely affect our results of operations in a particular period or the value of our equity investment. If we are not successful in maintaining our strategic distribution relationships, our financial condition, results of operations and cash flows may be adversely affected.

In addition, our ability to apply our internal controls and governance and compliance policies to our minority-held joint ventures is limited and can expose us to additional financial and reputational risks. We seek to take proactive steps to mitigate these concerns, including through audits and similar reviews.

Joint ventures and strategic relationships inherently involve certain other risks. Whether or not we hold a majority interest or maintain operational control in such arrangements, our partners and similar business associates may, for example: (1) have economic or business interests or objectives that are inconsistent with or contrary to our own; (2) exercise veto or other rights, to the extent available, to block actions that we believe are in our or the joint venture’s best interests; (3) act contrary to our policies or objectives; or (4) be unable or unwilling to fulfill their obligations.

In addition, there can be no assurance that any particular joint venture or strategic relationship will continue to be beneficial to us in the long term. For example, some of our joint ventures or other strategic agreements prohibit us from competing in certain geographic markets or product and services channels, and these restrictions may apply to other products and services we develop or businesses we acquire in the future.

Risks associated with climate events, government regulations and incentives associated with climate events and mitigation efforts could adversely affect our business.

The effects of climate events, including increased frequency and intensity of extreme weather conditions and water scarcity, create financial risks to our business. The potential impacts of climate events on our operations are highly uncertain and depend upon the unique geographic and environmental factors present; for example rising sea levels at certain of our facilities, changing storm patterns and intensities and changing temperature levels. The effects of climate events could disrupt our operations by impacting the availability and cost of materials and by increasing insurance and other operating costs. The effects of climate events also may impact our decisions to construct new facilities or maintain existing facilities in the areas most prone to physical risks, which could similarly increase our operating and material costs. We could also face indirect financial risks passed through the supply chain that could result in higher prices for our products and the resources needed to produce them. Potential adverse impacts from climate events may create health and safety issues for employees operating at our facilities and may lead to an inability to maintain standard operating hours.

There is a general consensus that greenhouse gas emissions are linked to climate events, and that these emissions must be reduced dramatically to avert its worst effects. Increased public awareness and concern about climate events may continue to: (1) generate more international, regional and/or national requirements to curtail the use of high global warming potential refrigerants (e.g., the Kigali Amendment to the Montreal Protocol and the American Innovation and Manufacturing ("AIM") Act of 2020, which are essential to many of our products); (2) increase building energy and cold chain efficiency; (3) cause a shift away from the use of fossil fuels as an energy source, including natural gas prohibitions; and (4) lead to the adoption of additional rules and regulations surrounding public disclosures relating to greenhouse gas emissions, including those adopted in California and the European Union. In some instances, these requirements may render our existing technology, particularly some of our HVAC and refrigeration products, non-compliant or obsolete and we may be required to make increased capital expenditures to meet new regulations and standards, changing interpretations and stricter enforcement of current laws and regulations. Furthermore, our customers and the markets we serve may impose emissions or other environmental standards through regulation, market-based emissions policies or consumer preferences that we may not be able to timely meet due to our required level of capital investment and technology advancement. While we are committed to pursuing sustainable solutions for our products, there can be no assurance that our development efforts will be successful, that our products will be accepted by the market, that proposed regulations or deregulation will not have an adverse effect on our competitive position, or that economic returns will justify our investments in new product development.

At the same time, U.S. energy and climate policy may not align with the above trends. Inconsistent international, regional and/or national requirements associated with climate regulations, such as U.S. participation in the Paris Climate Agreement, also create economic and regulatory uncertainty. There is also regulatory and budgetary uncertainty associated with government incentives, which, if discontinued or materially reduced, could adversely impact the demand for energy-efficient buildings and homes and could increase costs of compliance. Further, the retraction of existing and implementation of new U.S. energy and/or climate policy and incentives could significantly and adversely impact our business, strategic direction and growth plans.

We have set sustainability goals to be achieved by 2030, which include investing over $4 billion to develop intelligent climate and energy solutions that reduce environmental impacts, avoiding more than 1 gigaton of customer greenhouse gas emissions, achieving carbon neutral operations and reducing energy intensity by 10% across our operations. Although we intend to meet these goals, we may be required to expend significant resources to do so, which could increase our operational costs. Further, there can be no assurance of the extent to which any of our goals will be achieved, or that any future expenditures or investments we make in furtherance of achieving such goals will be available, effective, meet investor expectations or any binding or non-binding legal standards regarding sustainability performance. For example, to make substantial progress toward or to meet some of these goals, we may need to purchase or deploy a combination of renewable energy utility contracts, carbon credits or offsets, energy-efficient or low-emission products or operations, or carbon sequestration technologies, and there can be no assurance of the extent to which such contracts, credits, offsets, products, operations or technologies will be available or effective in reducing emissions or energy intensity. As global regulatory reporting obligations continue to emerge and evolve, we strive to align our sustainability disclosures to global reporting requirements, standards, and best practices. To the extent that reporting gaps exist as reporting standards change over time, this could result in increased compliance costs and risks.

Moreover, we may determine that it is in the best interest of our company and our shareowners to prioritize other business, social, governance or sustainability investments over the achievement of our current goals based on economic, regulatory and social factors, business strategy or pressure from investors, activist groups or other stakeholders. If we are unable to make substantial progress toward or meet these goals, then we could incur adverse publicity and reaction from investors, activist groups or other stakeholders, which could adversely impact the perception of us and our products and services by current and potential customers, as well as investors, which could in turn adversely impact our results of operations. Differing views of environmental, social and governance issues may also increase the risk that our goals or actions taken to meet our goals would be viewed unfavorably by investors, activist groups, current and potential customers, employees and other stakeholders.

Demand for our HVAC products and services is influenced by weather conditions and seasonality.

Demand for our HVAC products and services, representing our largest segment by sales, is seasonal and affected by the weather. Cooler than normal summers depress sales of our replacement air conditioning products and services and warmer than normal winters have the same effect on our heating products. Historically, sales to residential HVAC customers tend to be higher in the second and third quarters of the year because, in the U.S. and other northern hemisphere regions, spring and summer are the peak seasons for sales of air conditioning systems and services. In these circumstances, the results of any quarterly period may not be indicative of expected results for a full year, and unusual weather patterns or events could positively or negatively affect our business and impact overall results of operations.

Our business and financial performance depend on continued and substantial investments in our information and operational technology infrastructure, which may not yield anticipated benefits and which may be vulnerable to cyber-attacks.

The efficient operation of our business requires continued and substantial investments in information technology ("IT") and operational technology (“OT”, together, “Technology”) infrastructure systems. The failure to design, develop, maintain and implement Technology infrastructure systems in an effective and timely manner or to maintain these systems could divert management’s attention and resources. Our information systems may also become obsolete because of inadequate investments, requiring an unplanned transition to a new platform that could be time consuming, costly, and damaging to our competitive position and could require additional management attention. Repeated or prolonged interruptions of service because of poor execution, inadequate investments or obsolescence could have a significant adverse impact on our reputation and our ability to sell products and services.

Cybersecurity incidents could disrupt business operations, result in the loss of critical and confidential information, and adversely impact our reputation and results of operations.

Our business has been and may again in the future be impacted by disruptions to our or third-party providers’ Technology infrastructure, which have resulted and could in the future result from (among other causes) cyber-attacks, infrastructure failures or compromises to our physical security. Cyber-based risks are evolving and include attacks: (i) on our Technology infrastructure; (ii) targeting the security, integrity and/or availability of hardware and software; (iii) exploiting weaknesses or vulnerabilities in our products, or capturing information installed, stored or transmitted in our products (including after the purchase of those products and when they are installed into, or into environments using, third-party products); and (iv) on facilities or similar infrastructure. Such attacks could disrupt our systems (or those of third parties) and business operations, impact the ability of our products to work as intended or result in the unauthorized access, use, disclosure, modification or destruction of information in violation of applicable law and/or contractual obligations. We continue to make investments and adopt measures to enhance our protection, detection, response and recovery capabilities, and to mitigate potential risks to our technology, products, services, operations and confidential data. However, depending on the nature, sophistication and scope of cyber-attacks, it is possible that potential vulnerabilities could go undetected for an extended period. As a result, we could potentially experience: (i) production downtimes; (ii) operational delays or other detrimental impacts on our operations; (iii) destruction or corruption of our data (or data at or third-party providers); (iv) security breaches; (v) manipulation or improper use of our or third-party systems, networks or products; and (vi) financial losses from remedial actions, loss of business, liability, penalties, fines and/or damage to our reputation, any of which could have a material adverse effect on our competitive position, results of operations, cash flows or financial condition. Due to the evolving nature of such risks, the impact of any potential incident cannot be predicted.

In addition, because of the global nature of our business, our internal systems and products must comply with applicable laws, regulations and standards in a number of jurisdictions, and government enforcement actions and violations of data privacy and cybersecurity laws could be costly or interrupt our business operations. Any disruption to our business arising from such issues, or an increase in our costs to cover these issues that is greater than what we have anticipated, could have an adverse effect on our reputation, competitive position, results of operations, cash flows or financial condition.

These risks are heightened by the increasingly connected nature of our products and services as we continue to focus on providing digitally-enabled lifecycle solutions to our customers, including due to the use of third-party products to connect these products and services to the internet, which may be subject to additional vulnerabilities beyond our control.

We engage in acquisitions and divestitures and may encounter difficulties integrating acquired businesses with, or disposing of businesses from, our current operations; therefore, we may not realize the anticipated benefits of these acquisitions and divestitures.

We seek to grow through strategic acquisitions in addition to organic growth. In the past several years, we have acquired consolidated and minority-owned businesses in an effort to complement and expand our business, including the acquisition of the VCS Business, which we completed on January 2, 2024. We expect to continue such pursuits in the future. Our due diligence reviews may not identify all of the issues necessary to accurately estimate the cost and potential loss contingencies of a particular transaction, including potential exposure to regulatory sanctions resulting from an acquisition target’s historical activities.

In connection with these acquisitions, we have in the past incurred, and expect to incur in the future, significant costs, including in connection with the integration of such businesses. For example, in connection with the integration of the VCS Business, we incurred transaction fees and costs related to formulating integration plans and achieving cost synergies, and the execution of our integration plans may lead to additional unanticipated costs, including costs related to employee retention, redeployment, relocation or severance fees, as well as costs necessary to maintain employee morale and to attract, motivate or retain management personnel and other key employees. Furthermore, integrating a business, including the VCS Business, may result in material challenges, including the diversion of management’s attention from ongoing business concerns; retaining key management and other employees; retaining or attracting business and operational relationships; managing the expenses and operational challenges of the integration process; consolidating corporate and administrative infrastructures; coordinating geographically separate organizations; loss of customers, distributors, suppliers, and other business partners of the acquired business; unanticipated issues in integrating information technology, communications, internal controls and other systems; as well as potential unknown liabilities and unforeseen expenses related to integration. We ultimately may not realize, and have sometimes not realized, the degree or timing of benefits or cost synergies we anticipate when we first enter into a transaction.

We also may incur - and have incurred - unanticipated costs or expenses, including asset impairment and other charges and expenses associated with litigation and other liabilities. In addition, in connection with certain acquisitions including the acquisition of the VCS Business, we have disclosed and may from time to time disclose, unaudited pro forma financial information. This pro forma financial information is presented for illustrative purposes only and is not necessarily indicative of what our actual financial position or results of operations would have been had the acquisition been completed on the dates indicated therein. Further, our actual results and financial position may differ materially and adversely from the unaudited pro forma financial information, including due to certain adjustments made by our management, and due to changes between preliminary estimates of the fair value of assets to be acquired and liabilities to be assumed, and the final acquisition accounting. Additionally, accounting requirements relating to business combinations, including the requirement to expense certain acquisition costs as incurred, may cause us to incur greater earnings volatility and generally lower earnings subsequent to periods in which we acquire new businesses. Any of the foregoing could adversely affect our business and results of operations.

We also make strategic divestitures from time to time, including the dispositions during 2024 of Access Solutions, Industrial Fire, CCR and the CRF Business. These and other divestitures may result in continued financial exposure to the divested businesses, such as through guarantees, other financial arrangements, continued supply and services arrangements or through the retention of liabilities, such as for environmental and product liability claims. Under these arrangements, nonperformance by those divested businesses or claims against retained liabilities could result in the imposition of obligations that could have a material adverse effect on our results of operations, cash flows or financial condition.

The success of future acquisitions, divestitures and joint ventures will depend on the satisfaction of conditions precedent to such transactions, which will depend in part on the ability of the parties to secure any required regulatory approvals in a timely manner, among other things.

We incurred debt obligations, and we may incur additional debt in the future, which could adversely affect our business and profitability and our ability to meet other obligations.

As of December 31, 2024, we had approximately $12.3 billion in aggregate principal amount of outstanding indebtedness, including debt incurred to close the acquisition of the VCS Business on January 2, 2024. See Note 7 – Borrowings and Lines of Credit in the accompanying Notes to the Consolidated Financial Statements and the section entitled "Liquidity and Financial Condition" in this Annual Report for additional information. We may also incur additional indebtedness in the future, including via issuance of commercial paper, under our Revolving Credit Facility.

Our debt obligations could potentially have important consequences to us and our debt and equity investors, including: (1) requiring a substantial portion of our cash flows from operations to make debt service payments or to refinance our indebtedness as it becomes due, making it more difficult for us to satisfy our other priorities and obligations; (2) increasing the risk of a future credit ratings downgrade of our debt, which could increase future debt costs and limit the future availability of debt financing; (3) increasing our vulnerability to general adverse economic and industry conditions; (4) reducing the cash flows available to fund capital expenditures and other corporate purposes and to grow our business; (5) limiting our flexibility in pursuing strategic opportunities or planning for, or reacting to, changes in our business and the industry; (6) placing us at a competitive disadvantage relative to our competitors that may not be as highly leveraged; and (7) limiting our ability to borrow additional funds as needed or take advantage of business opportunities as they arise, pay cash dividends or repurchase shares.

Our ability to make scheduled payments of the principal of, to pay interest on or to refinance our indebtedness depends on our future performance, which is subject to economic, financial, competitive, regulatory factors, and other factors beyond our control. Our cash flow from operations in the future may be insufficient to service our indebtedness because of factors beyond our control, including if our actual cash requirements in the future are greater than expected. If we are unable to generate the necessary cash flow, we may be required to adopt one or more alternatives, such as selling assets, restructuring debt or obtaining additional equity capital on terms that may be onerous or highly dilutive. Our ability to refinance our indebtedness will depend on the capital markets and our financial condition at such time. We may not be able to engage in any of these activities or engage in these activities on desirable terms, which could result in a default on our debt obligations.

As described in Note 7 – Borrowings and Lines of Credit in the accompanying Notes to the Consolidated Financial Statements and "Liquidity and Financial Condition," the agreements governing our indebtedness contain covenants restricting our financial flexibility in a number of ways, including, among other things, restrictions on our ability and the ability of certain of our subsidiaries to incur liens, to make certain fundamental changes and to enter into sale and leaseback transactions. In addition, some of the agreements governing our indebtedness require that we not exceed a maximum consolidated total leverage ratio and contain certain customary events of default, including related to changes of control. As of the date of this report, we were in compliance with the covenants under the agreements governing our outstanding indebtedness. Our ability to comply with such restrictions and covenants, some of which have already been amended as described above, may be affected by events beyond our control. If we breach any of these restrictions or covenants and do not obtain a waiver from the lenders or holders, as applicable, then, subject to the applicable cure periods and conditions, any outstanding indebtedness could be declared immediately due and payable.

Apart from these covenants, neither we nor any of our subsidiaries are restricted from incurring additional unsecured debt or liabilities, and to the extent that we incur additional indebtedness, the foregoing risks could increase.

We depend on our intellectual property and have access to certain intellectual property and information of our customers and suppliers. Infringement of or the failure to protect that intellectual property could adversely affect our future growth and success.

Our intellectual property rights are important to our business and include numerous patents, trademarks, copyrights, trade secrets, proprietary technology, technical data, business processes and other confidential information. Although we consider our intellectual property rights in the aggregate to be valuable, we do not believe that our business is materially dependent on a single intellectual property right or any group of them. We nonetheless rely on a combination of patents, trademarks, copyrights, trade secrets, nondisclosure agreements, customer and supplier agreements, license agreements, Technology security systems, internal controls and compliance systems and other measures to protect our intellectual property. We also rely on nondisclosure agreements, Technology security systems and other measures to protect certain customer and supplier information and intellectual property that we have in our possession or to which we have access. Our efforts to protect such intellectual property and proprietary information may not be sufficient, however.

We cannot be sure that our pending patent applications will result in the issuance of patents, that patents issued to or licensed by us in the past or in the future will not be challenged or circumvented by competitors, or that these patents will be found to be valid or sufficiently broad to preclude our competitors from introducing technologies similar to those covered by our patents and patent applications.

In addition, we may be the target of competitor or other third-party patent enforcement actions seeking substantial monetary damages or seeking to prevent the sale and marketing of certain of our products. Our competitive position also may be adversely impacted by limitations on our ability to obtain possession, ownership or necessary licenses concerning data important to the development or sale of our products or service offerings, or by limitations on our ability to restrict the use by others of data related to our products or services. Any of these events or factors could subject us to judgments, penalties and significant litigation costs or temporarily or permanently disrupt our sales and marketing of the affected products or services and could have a material adverse effect on our competitive position, results of operations, cash flows or financial condition.

We use a variety of raw materials, supplier-provided parts, and third-party service providers in our business. The ability of suppliers to deliver materials, parts, components and manufacturing equipment to our manufacturing facilities, and our ability to manufacture without disruption, could affect our business performance. Significant shortages, supplier capacity constraints or production disruptions, price increases, duties, tariffs or other government actions could increase our operating costs, disrupt our operations and adversely impact the competitive positions of our products.

Our reliance on suppliers and commodity markets to secure components (such as motors and valves) and raw materials (such as copper, aluminum and steel), and on service providers to deliver our products, exposes us to volatility in the prices and availability of these materials and services. We use a wide range of materials and components in the global production of our products, which come from numerous suppliers around the world. Because some key parts may be available only from a single supplier or a limited group of suppliers, we are subject to supply and pricing risk. In addition, certain proprietary component parts used in some of our products are provided by single-source unaffiliated third-party suppliers. We would be unable to obtain these proprietary components for an indeterminate period of time if these single-source suppliers were to cease or interrupt production or otherwise fail to supply these components to us, which could adversely affect our product sales and operating results. Our supply chain could be impacted by climate events through extreme weather, resulting in delivery or production disruptions and increased material costs. In addition, other issues with suppliers (such as capacity constraints, quality issues, consolidations, closings or bankruptcies), price increases, raw material/component shortages, regulatory limitations, or the decreased availability of trucks and other delivery services could also have a material adverse effect on our ability to meet our commitments to customers or increase our operating costs. Periodic disruptions in our supply chains have resulted, and may continue to result, in sufficient inventory not being available in a timely manner or during the appropriate season as well as higher freight and other logistic costs, including increased carrier rates, which could have a material adverse effect on our business.