QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended:September 30, 2020

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to _____________

WETRADE GROUP INC

(Exact name of small business issuer as specified in its charter)

WYOMING

(State or other jurisdiction of

incorporation or organization)

(I.R.S. Tax. I.D. No.)

No 1 Gaobei South Coast, Yi An Men 111 Block 37, Chao Yang District,

Beijing City, People Republic of China

(Address of Principal Executive Offices)

(852) 67966335

(Registrant’s Telephone Number, Including Area Code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definition of “large accelerated filer,” accelerated filer” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer

☐

Accelerated filer

☐

Non-accelerated filer

☐

Smaller Reporting Company

☒

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of November 24, 2020, there were 305,451,498 shares of common stock outstanding.

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended, (the “Exchange Act”). These forward-looking statements are generally located in the material set forth under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations” but may be found in other locations as well. These forward-looking statements are subject to risks and uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from the results, performance or achievements expressed or implied by the forward-looking statements. You should not unduly rely on these statements.

We identify forward-looking statements by use of terms such as “may,” “will,” “expect,” “anticipate,” “estimate,” “hope,” “plan,” “believe,” “predict,” “envision,” “intend,” “will,” “continue,” “potential,” “should,” “confident,” “could” and similar words and expressions, although some forward-looking statements may be expressed differently. You should be aware that our actual results could differ materially from those contained in the forward-looking statements.

Forward-looking statements are based on information available at the time the statements are made and involve known and unknown risks, uncertainties and other factors that may cause our results, levels of activity, performance or achievements to be materially different from the information expressed or implied by the forward-looking statements in this report. These factors include, among others:

●

our ability to execute on our growth strategies;

●

our ability to find manufacturing partners on favorable terms;

●

declines in general economic conditions in the markets where we may compete;

●

our anticipated needs for working capital; and

Where we express an expectation or belief as to future events or results, such expectation or belief is expressed in good faith and believed to have a reasonable basis.

Forward-looking statements speak only as of the date of this report or the date of any document incorporated by reference in this report. Except to the extent required by applicable law or regulation, we do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date of this report or to reflect the occurrence of unanticipated events.

WeTrade Group Inc. was incorporated in the State of Wyoming on March 28, 2019.

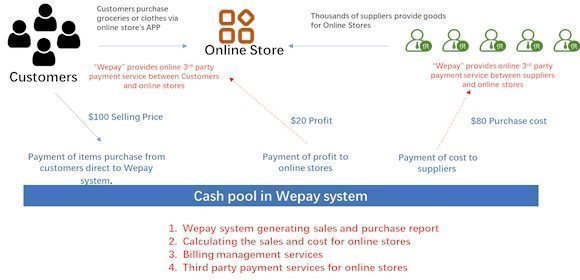

WeTrade Group Inc. is in the business of providing technical services and solutions via its membership-based social e-commerce platform and the Group is target to provided technical and auto-billing management services for 100 million micro-business users in China.

In January 2020, WeTrade have appointed 3rd party software company to develop an auto-billing management system (“Wepay System”) at the cost of RMB 400,000 in order to provide online payment services for its online store customers in PRC.

The main functions of Wepay System are user marketing relationship implementation, CPS commission profit management, multi-channel app data statistics and etc. Business applications cover the retail industry, tourism industry, hospitality and beauty industry.

WeTrade Group INC has conducted its business operations in mainland China and trial operation in Hong Kong, Philippines and Singapore. WeTrade has also formed the long-term technical cooperation with Yuetao App, Daren App, Yuebei App, Jingdong App, Yuedian App and Lvyue App.

In 2020, in order to better serve customers in mainland China, WeTrade reached an in-depth strategic partnership with Global Travelling Technology (Beijing) Co., Ltd., entrusting it to expand its business in China. As of the third quarter of 2020, WeTrade System has covered the e-commerce industry, tourism industry, hospitality industry, livestreaming/short video industry, etc.

As at September 30, 2020, the auto-billing management system of WeTrade group has more than 12 million micro-business users, 60,000 blog users and more than 2000 hotels direct booking suppliers in China. It is expected will be more than 12% of 100 million micro-business users in China by end of 2020.

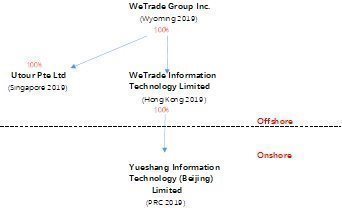

The following diagram sets forth the structure of the Company as of the date of this Current Report:

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of preparation of financial statements

The consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“GAAP”). The consolidated financial statements include the financial statements of the Company and its subsidiaries. All significant inter-company transactions and balances have been eliminated in consolidation.

The condensed consolidated financial statements of the Company as of and for the nine months ended September 30, 2020 and 2019 are unaudited. In the opinion of management, all adjustments (including normal recurring adjustments) that have been made are necessary to fairly present the financial position of the Company as of September 30, 2020, the results of its operations for the nine months ended September 30, 2020 and 2019, and its cash flows for the nine months ended September 30, 2020 and 2019. Operating results for the interim periods presented are not necessarily indicative of the results to be expected for a full fiscal year. The balance sheet as of December 31, 2019 has been derived from the Company’s audited financial statements included in the Form 10-K for the year ended December 31, 2019.

The statements and related notes have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission (the “SEC”). Accordingly, certain information and footnote disclosures normally included in financial statements prepared in accordance with U.S. GAAP have been omitted pursuant to such rules and regulations. These financial statements should be read in conjunction with the financial statements and other information included in the Company’s Annual Report on Form 10-K as filed with the SEC for the fiscal year ended December 31, 2019.

As of September 30, 2020, the details of the consolidating subsidiaries are as follows:

Place of

Attributable

Name of Company

incorporation

equity interest %

Utour Pte Ltd

Singapore

100

%

WeTrade Information Technology Limited (“WITL”)

Hong Kong

100

%

Yueshang Information Technology (Beijing) Co., Ltd. (“YITB”)

P.R.C.

100

%

Nature of Operations

WeTrade Group Inc. (the “Company” or or “We’ or “Us”) is a Wyoming corporation incorporated on March 28, 2019. The Company is an investment holding company that formed as a Wyoming corporation to use as a vehicle for raising equity outside the US.

As of September 30, 2020, the nature operation of its subsidiaries are as follows:

Place of

Nature of

Name of Company

incorporation

operation

Utour Pte Ltd

Singapore

Investment holding company

WeTrade Information Technology Limited (“WITL”)

Hong Kong

Investment holding company

Yueshang Information Technology (Beijing) Co., Ltd. (“YITB”)

P.R.C.

Providing of social e-commerce services, technical system support and services

COVID-19 outbreak

In March 2020 the World Health Organization declared coronavirus COVID-19 a global pandemic. The COVID-19 pandemic has negatively impacted the global economy, workforces, customers, and created significant volatility and disruption of financial markets. It has also disrupted the normal operations of many businesses, including ours. This outbreak could decrease spending, adversely affect demand for our services and harm our business and results of operations. It is not possible for us to predict the duration or magnitude of the adverse results of the outbreak and its effects on our business or results of operations at this time.

Revenue recognition

The Company follows the guidance of Accounting Standards Codification (ASC) 606, Revenue from Contracts. ASC 606 creates a five-step model that requires entities to exercise judgment when considering the terms of contracts, which includes (1) identifying the contracts or agreements with a customer, (2) identifying our performance obligations in the contract or agreement, (3) determining the transaction price, (4) allocating the transaction price to the separate performance obligations, and (5) recognizing revenue as each performance obligation is satisfied. The Company only applies the five-step model to contracts when it is probable that the Company will collect the consideration it is entitled to in exchange for the services it transfers to its clients.

The Company considers all highly liquid debt instruments purchased with a maturity period of three months or less to be cash or cash equivalents. The carrying amounts reported in the accompanying unaudited condensed consolidated balance sheets for cash and cash equivalents approximate their fair value. All of the Company’s cash that is held in bank accounts in Singapore and PRC is not protected by Federal Deposit Insurance Corporation (“FDIC”) insurance or any other similar insurance in the PRC, or Singapore.

Use of Estimate

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of expenses during the reporting periods. Actual results could differ from those estimates.

Concentration of Risk

Financial instruments that potentially subject the Company to concentrations of credit risk consist principally of cash. Cash on hand amounted to $6,787,535as of September 30, 2020.

Foreign currency translation and transactions

For the period ended September 30, 2020, the Company’s principal country of operations is the PRC. The accompanying consolidated financial statements are presented in US$. The functional currency of the Company is US$, and the functional currency of the Company’s subsidiaries is RMB. The consolidated financial statements are translated into US$ from RMB at year-end exchange rates as to assets and liabilities and average exchange rates as to revenues and expenses. Capital accounts are translated at their historical exchange rates when the capital transactions occurred. The resulting translation adjustments are recorded as a component of shareholders’ equity included in other comprehensive income. Gains and losses from foreign currency transactions are included in profit or loss.

As of

For the period

September 30,

2020

December 31,

2019

RMB: US$ exchange rate

6.79

7.00

Nine months ended

September 30,

2020

2019

RMB: US$ exchange rate

6.81

7.05

The RMB is not freely convertible into foreign currency and all foreign exchange transactions must take place through authorized institutions. No representation is made that the RMB amounts could have been, or could be, converted into US$ at the rates used in translation.

The balance sheet amounts, with the exception of equity, September 30, 2020 and December 31, 2019 were translated at 6.79 RMB and 7.00 RMB to $1.00, respectively. The equity accounts were stated at their historical rates. The average translation rates applied to statements of operations and comprehensive income (loss) accounts for the period ended September 30, 2020 and year ended December 31, 2019 were 6.81 RMB and 7.05 RMB to $1.00, respectively. Cash flows were also translated at average translation rates for the periods and, therefore, amounts reported on the statement of cash flows would not necessarily agree with changes in the corresponding balances on the consolidated balance sheet. The transactions dominated in SGD are immaterial.

Accounts receivable

Accounts receivable are presented net of allowance for doubtful accounts. The Group uses specific identification in providing for bad debts when facts and circumstances indicate that collection is doubtful and based on factors listed in the following paragraph. If the financial conditions of its customers were to deteriorate, resulting in an impairment of their ability to make payments, additional allowance may be required.

The Company maintains an allowance for doubtful accounts which reflects its best estimate of amounts that potentially will not be collected. The Company determines the allowance for doubtful accounts on general basis taking into consideration various factors including but not limited to historical collection experience and credit-worthiness of the customers as well as the age of the individual receivables balance. Additionally, the Company makes specific bad debt provisions based on any specific knowledge the Company has acquired that might indicate that an account is uncollectible. The facts and circumstances of each account may require the Company to use substantial judgment in assessing its collectability.

Intangible Asset

Intangible asset is software development cost incurred by the Company, it will be amortized on a straight line basis over the estimated useful life of 5 years.

Leases

On February 2016, the FASB established Topic 842, Leases, by issuing Accounting Standards Update (“ASU”) No. 2016-02, which requires lessees to recognize the rights and obligations created by leases on the balance sheet and disclose key information about leasing arrangements. Topic 842 was subsequently amended by ASU No. 2018-11, Targeted Improvements, ASU No. 2018-10, Codification Improvements to Topic 842, and ASU No. 2018-01, Land Easement Practical Expedient for Transition to Topic 842. The new standard establishes a right-of-use model (“ROU”) that requires a lessee to recognize a ROU asset and lease liability on the balance sheet for all leases with a term longer than 12 months. Leases will be classified as finance or operating, with classification affecting the pattern and classification of expense recognition in the statement of operations.

The new standard became effective April 1, 2019. A modified retrospective transition approach is required, applying the new standard to all leases existing at the date of initial application. An entity may choose to use either (1) its effective date or (2) the beginning of the earliest comparative period presented in the financial statements as its date of initial application. If an entity chooses the second option, the transition requirements for existing leases also apply to leases entered into between the date of initial application and the effective date. The entity must also recast its comparative period financial statements and provide the disclosures required by the new standard for the comparative periods. The Company adopted the new standard on July 1, 2019 using the modified retrospective transition approach as of the effective date of the initial application. The new standard provides a number of optional practical expedients in transition. The Company elected the “package of practical expedients”, which permits entities not to reassess under the new lease standard prior conclusions about lease identification, lease classification and initial direct costs. The Company does not expect to elect the use-of-hindsight or the practical expedient pertaining to land easements.

The most significant effects of the adoption of the new standard relate to the recognition of new ROU assets and lease labilities on our balance sheet for office operating leases and providing significant new disclosures about our leasing activities.

The new standard also provides practical expedients for an entity’s ongoing accounting. The Company has also elected the short-term leases recognition exemption for all leases that qualify. This means that the Company will not recognize ROU assets or lease liabilities, and this includes not recognizing ROU assets and lease liabilities, for existing short-term leases of those assets in transition. The Company also currently expects to elect the practical expedient to not separate lease and non-lease components for its leases. All existing leases are reported under this rule.

Under ASC 840, leases were classified as either capital or operating, and the classification significantly impacted the effect the contract had on the company’s financial statements. Capital lease classification resulted in a liability that was recorded on a company’s balance sheet, whereas operating leases did not impact the balance sheet. After the new adoption, $2,832,007 of operating lease right-of-use asset and $2,886,855 of operating lease liabilities were reflected on the Company’s September 30, 2020 financial statements.

ASU 2016-02 requires that public companies use a secured incremental browning rate for the present value of lease payments when the rate implicit in the contract is not readily determinable. We determine a secured rate on a quarterly basis and update the weighted average discount rate accordingly. Lease terms and discount rate follow:

Lease cost

In USD

Operating lease cost (included in general and admin in company’s statement of operations)

$

53,265

Other information

Cash paid for amounts included in the measurement of lease liabilities for the quarter ended 9/30/2020

-

Weighted average remaining lease term-operating leases (in years)

4.92

Average discount rate - operating leases

5

%

The supplemental balance sheet information related to leases for the period is as follows:

Operating leases

Long -term right-of-use assets

2,832,007

Total right-of-use assets

$

2,832,007

Short-term operating lease liabilities

365,274

Long-term operating lease liabilities

2,521,582

Total operating lease liabilities

$

2,886,855

Maturities of the Company’s lease liabilities are as follows:

Income taxes are determined in accordance with the provisions of ASC Topic 740, “Income Taxes” (“ASC Topic 740”). Under this method, deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax basis. Deferred tax assets and liabilities are measured using enacted income tax rates expected to apply to taxable income in the periods in which those temporary differences are expected to be recovered or settled. Any effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the period that includes the enactment date.

ASC 740 prescribes a comprehensive model for how companies should recognize, measure, present, and disclose in their financial statements uncertain tax positions taken or expected to be taken on a tax return. Under ASC 740, tax positions must initially be recognized in the financial statements when it is more likely than not the position will be sustained upon examination by the tax authorities. Such tax positions must initially and subsequently be measured as the largest amount of tax benefit that has a greater than 50% likelihood of being realized upon ultimate settlement with the tax authority assuming full knowledge of the position and relevant facts.

The Company has a subsidiary in Singapore and PRC. The Company is subject to tax in Singapore and PRC jurisdictions. As a result of its future business activities, the Company will be required to file tax returns that are subject to examination by the Inland Revenue Authority of Singapore and Tax Department of PRC.

Earning (Loss) Per Share

Basic net income (loss) per share of common stock attributable to common stockholders is calculated by dividing net income (loss) attributable to common stockholders by the weighted-average shares of common stock outstanding for the period. Potentially dilutive shares, which are based on the weighted-average shares of common stock underlying outstanding stock-based awards, warrants, options, or convertible debt using the treasury stock method or the if-converted method, as applicable, are included when calculating diluted net income (loss) per share of common stock attributable to common stockholders when their effect is dilutive.

Potential dilutive securities are excluded from the calculation of diluted EPS in profit periods as their effect would be anti-dilutive.

As of September 30, 2020, there were no potentially dilutive shares.

For the period

September

30, 2020

For the period

September

30, 2019

Statement of Operations Summary Information:

Net Income/ (Loss)

$

1,307,126

(255,010

)

Weighted-average common shares outstanding - basic and diluted

304,166,073

300,024,666

Net loss per share, basic and diluted

$

0.00

(0.00

)

Comprehensive income (loss)

Comprehensive income (loss) is defined to include all changes in shareholders’ equity except those resulting from investments by owners and distributions to owners. The Company presents items of net income (loss) and other comprehensive income (loss) in one continuous statement, the Consolidated Statements of Operations and Comprehensive income (loss). The components of other comprehensive income or loss consist solely of foreign currency translation adjustments.

Fair Value

The Company follows guidance for accounting for fair value measurements of financial assets and financial liabilities and for fair value measurements of nonfinancial items that are recognized or disclosed at fair value in the financial statements on a recurring basis. Additionally, the Company adopted guidance for fair value measurement related to nonfinancial items that are recognized and disclosed at fair value in the financial statements on a nonrecurring basis. The guidance establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value.

The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to measurements involving significant unobservable inputs (Level 3 measurements). The three levels of the fair value hierarchy are as follows:

Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that the Company has the ability to access at the measurement date.

Level 2 inputs are inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly.

Level 3 inputs are unobservable inputs for the asset or liability. The carrying amounts of financial assets such as cash approximate their fair values because of the short maturity of these instruments.

NOTE 3. RECENT ACCOUNTING PRONOUNCEMENTS

Recent accounting pronouncements issued by the FASB (including its Emerging Issues Task Force) and the United States Securities and Exchange Commission did not or are not believed by management to have a material impact on the Company’s present or future financial statements.

NOTE 4. REVENUE

The main functions of Wepay System is an online payment services, CPS profit management services, multi-channels App and data analysis, which is developed to provide payment and auto-billing services for online store customers from retail, tourism industry, hospitality and beauty industry.

We earn revenue primarily by completing payment transactions for customers through our “Wepay System” and from other value added services. Our revenues are classified into two categories: transaction revenues based on Gross Merchandise volume (“GMV”) of online stores and revenues from other value added services or online technical services from store customers. As per the services agreement , which will be 0.5% of the actual Gross Merchandise Volume (“GMV”) during trial period and subsequently 2% - 3.5% of GMV pay to the Company as the system service fee. As of nine months ended September 30, 2020, we generated revenues from a related party amounting $2,370,192. As of three months ended September 30, 2019, we generated revenues from a related party amounting $1,493,829.

As of September 30, 2020, the Company held cash in bank in the amount of $6,787,535 which consist of the following:

September 30,

2020

December 31,

2019

Bank Deposits-China

$

6,623,550

5,000,014

Bank Deposits-Singapore

163,985

1,591,114

6,787,535

6,591,128

NOTE 6. INTANGIBLE ASSET

Intangible asset is software development cost incurred by company, it will be amortized on a straight line basis over the estimated useful life of 10 years as follow:

September 30, 2020

Gross Carrying Amount

Accumulated Amortization

Net Carrying

Amount

Weighted Average Useful Life (Years)

Intangible assets:

Software development

$

57,143

$

(3,266

)

$

53,877

10

Software development in progress

$

21,014

-

21,014

Foreign currency translation adjustment

-

-

2,305

Intangible assets, net

$

78,157

$

(3,266

)

$

77,196

Amortization expense for intangible assets was $3,266 for the nine months ended September 30, 2020.

Expected future intangible asset amortization as of September 30, 2020 was as follows:

Management periodically reviews account balance. If any indication occurs, the allowance for doubtful debts would be recognized. No such allowance has been recognized during the nine months ended September 30, 2020.

NOTE 8. AMOUNT DUE TO DIRECTOR

As of September 30, 2020, amount due to related parties consist of the following:

As of

September 30,

2020

As of

December 31,

2019

Related parties payable

276,500

254,515

Related party loan

140,000

1,500,000

$

416,500

1,754,515

The related party balance of $416,500 represented an outstanding loan of $140,000 from the related company owned by Company’s director for daily business operation in Singapore, and professional expenses paid on behalf by Director of $276,500 and which consist of $224,500 advance from Dai Zheng, $42,000 advance from Li Zhuo and $10,000 from Che Kean Tat. It is unsecured, interest-free with no fixed payment term and imputed interest is consider to be immaterial.

The Company have settled related party loan of $650,000 and $710,000 in January 21, 2020 and March 2, 2020 respectively due to cost cutting in business operation in Singapore as a result of change in business plan. As of September 30, 2020, there were $140,000 of related party loan that are due to the company owned by Mr. Dai, the Chairman of the Board.

The Group’s PRC subsidiary is subject to the VAT rate of 6% of total revenue and statutory income tax rate of 25%.

NOTE 10. SHAREHOLDERS’ EQUITY (DEFICIT)

The company has an unlimited number of ordinary shares authorized, and has issued 305,451,498 shares with no par value as of September 30, 2020.

There are 26,000 shares issued at $3 per share to 2 new shareholders in July 10, 2020.

On September 15, 2020, the Wyoming Secretary of State approved the Company’s certificate of amendment to amend its Articles of Incorporation to effectuate a 3 for 1 forward stock split. The total issued and outstanding shares of the Company’s common stock has been increased from 10,322,660 to 305,451,498 shares, with the par value unchanged at zero.

On September 21, 2020, there are 151,500 shares issued at $5 per share to 303 new shareholders, the Company’s common stock issued has been increased to 305,451,498 shares as of September 30, 2020.

The following discussion and analysis of financial condition and results of operations should be read in conjunction with our financial statements and related notes included elsewhere in this report. This discussion contains forward-looking statements that involve risks, uncertainties and assumptions. See “Cautionary Note Regarding Forward-Looking Statements.” Our actual results could differ materially from those anticipated in the forward-looking statements as a result of certain factors discussed elsewhere in this report.

Overview

WeTrade Group Inc. is in the business of providing technical services and solutions via its membership-based social e-commerce platform and the Group is target to provided technical and auto-billing management services for 100 million micro-business online stores in China.

In January 2020, WeTrade have appointed 3rd party software company to develop an auto-billing management system (“Wepay System”) at the cost of RMB 400,000 in order to provide online payment services for its online store customers in PRC.

The main functions of Wepay System is an online payment services, CPS profit management services, multi-channels App and data analysis, which is developed to provide payment and auto-billing services for online store customers from retail, tourism industry, hospitality and beauty industry.

As at September 30, 2020, the auto-billing management system of WeTrade group has more than 12 million micro-business users, 60,000 blog users and more than 2000 hotels direct booking suppliers in China. It is expected will be more than 12% of 100 million micro-business users in China by end of 2020.

Results of Operations

The following tables provide a comparison of a summary of our results of operations for the nine months period ended September 30, 2020 and 2019.

Results of Operations for the Nine months period Ended September 30, 2020 and 2019

For the nine-month period ended September 30, 2020 and 2019, total revenue was $2,888,461 and $0, respectively. The increase was mainly from the service revenue generated from auto-billing management system from customers.

Cost of revenue

Cost of revenue is mainly consists of staff payroll, PRC central provident fund (“CPF”) and other staff benefits, the increase is mainly due to more staffs were recruited during the period. The increase is in line with the increase in revenue during the period.

General and Administrative Expenses

For the nine months period ended September 30, 2020 and 2019, general and administrative expenses were $617,216 and 255,010, respectively. The increase is mainly due to increase in the payroll expenses as a result of 77 new staffs were recruited during the period.

Net Income (Loss)

As a result of the factors described above, there was a net profit of $1,307,126 and net loss of $255,010 for the nine months period ended September 30, 2020 and 2019, respectively, the increase mainly due to revenue generated from auto-billing management system from related party.

Results of Operations for the Three months period ended September 30, 2020 and 2019.

2020

2019

Revenue

Service revenue, non-related party

$

518,269

$

-

Service revenue, related party

1,493,829

-

2,012,098

-

Cost of Revenue

(427,647

)

-

Gross Profit

1,584,451

-

General and Administrative Expense

(407,067

)

(110,921

)

Profit/ (Loss) from Operations

1,177,384

(110,921

)

Other revenue

38,939

-

Net Income/ (Loss) before income tax

1,216,323

(110,921

)

Income tax expenses

(475,431

)

-

Net Income/ (loss)

$

740,893

$

(110,921

)

Revenue from Operations

For the three-month period ended September 30, 2020 and 2019, total revenue was $2,012,098 and $0, respectively. The increase was mainly due to increase in service revenue generated from auto-billing management system from micro-business users.

Cost of revenue

Cost of revenue is mainly consists of staff payroll, PRC central provident fund (“CPF”) and other staff benefits, the increase is mainly due to more staffs were recruited during the period. The increase is in line with the increase in revenue during the period.

General and Administrative Expenses

For the three months period ended September 30, 2020 and 2019, general and administrative expenses were $407,067 and $110,921, respectively. The increase is mainly due to increase in the payroll expenses as a result of 77 new staffs were recruited during the period.

Net Income (Loss)

As a result of the factors described above, there was a net profit of $740,893 and net loss of $110,921 for the three months period ended September 30, 2020 and 2019, respectively. The increase mainly due to increase in revenue generated from auto-billing management system from customers.

As of September 30, 2020, we had cash on hand of $6,787,535. The increase is mainly due to the increase in revenue from auto-billing management services from customers. The increase is mitigated by the repayment of related party loan of $650,000 and $710,000 in January 21, 2020 and March 2, 2020 respectively as compare to the bank balance of $6,591,128 in December 31, 2019.

Operating activities

Our continuing operating activities used cash of $1,042,610 and $509 for the periods ended September 30, 2020 and 2019, respectively. The increase was mainly due to loan repayment of approximately $1.6 million to related parties.

Financing activities

Cash provided in our financing activities was increased to $835,500 and $220,020 for the periods ended September 30, 2020 and 2019, respectively. The increase was due to additional 1,896,166 shares issued to new 307 shareholders for cash in total amount of $757,500 during the period.

Inflation

Inflation does not materially affect our business or the results of our operations.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements.

Critical Accounting Policies

We prepare our financial statements in accordance with generally accepted accounting principles of the United States (“GAAP”). GAAP represents a comprehensive set of accounting and disclosure rules and requirements. The preparation of our financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Our actual results could differ from those estimates. We use historical data to assist in the forecast of our future results. Deviations from our projections are addressed when our financials are reviewed on a monthly basis. This allows us to be proactive in our approach to managing our business. It also allows us to rely on proven data rather than having to make assumptions regarding our estimates.

Recent Accounting Pronouncements

We have reviewed all the recently issued, but not yet effective, accounting pronouncements and we do not believe any of these pronouncements will have a material impact on the Company financial statements.

We are a “smaller reporting company” as defined by Item 10(f)(1) of Regulation S-K, and as such are not required to provide the information contained in this item pursuant to Item 305 of Regulation S-K.

The management of the Company is responsible for establishing and maintaining adequate internal control over financial reporting. The Company’s internal control over financial reporting is a process designed under the supervision of the Company’s Chief Executive Officer and Chief Financial Officer to provide reasonable assurance regarding the reliability of financial reporting and the preparation of the Company’s financial statements for external purposes in accordance with U.S. generally accepted accounting principles.

With respect to the period ending September 30, 2020, under the supervision and with the participation of our management, we conducted an evaluation of the effectiveness of the design and operations of our disclosure controls and procedures, as defined in Rules 13a-15(e) and 15d-15(e) promulgated under the Securities Exchange Act of 1934.

Based upon our evaluation regarding the period ending September 30, 2020, the Company’s management, including its Principal Executive Officer, has concluded that its disclosure controls and procedures were not effective due to the Company’s limited internal resources and lack of ability to have multiple levels of transaction review. Material weaknesses noted are lack of an audit committee, lack of a majority of outside directors on the board of directors, resulting in ineffective oversight in the establishment and monitoring of required internal controls and procedures; and management is dominated by two individuals, without adequate compensating controls. However, management believes the financial statements and other information presented herewith are materially correct.

The Company’s disclosure controls and procedures are designed to provide reasonable assurance of achieving their objectives. However, the Company’s management, including its Principal Executive Officer, does not expect that its disclosure controls and procedures will prevent all error and all fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefit of controls must be considered relative to their costs. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been detected.

Changes in Internal Control over Financial Reporting

There were no changes in our internal control over financial reporting that occurred during our most recently completed fiscal quarter that has materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

We were not subject to any legal proceedings during the nine months ended September 30, 2020, nor to the best of our knowledge and belief are any threatened or pending.

We are a “smaller reporting company” as defined by Item 10(f)(1) of Regulation S-K, and as such are not required to provide the information contained in this item.

Financial statements from the quarterly report on Form 10-Q of Wetrade Group Inc for the fiscal quarter ended September 30, 2020, formatted in XBRL: (i) the Balance Sheet; (ii) the Statement of Income; (iii) the Statement of Cash Flows; and (iv) the Notes to the Financial Statements Filed herewith

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

WETRADE GROUP INC

Date: December 2, 2020

By:

/s/ Pijun Liu

Pijun Liu

Chief Executive Officer

/s/ Kean Tat, Che

Kean Tat, Che

Chief Financial Officer

25

We use cookies on this site to provide a more responsive and personalized service. Continuing to browse, clicking I Agree, or closing this banner indicates agreement. See our Cookie Policy for more information.