UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

Filed by the Registrant ☐

Filed by a Party other than the Registrant ☒

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material Under § 240.14a-12 |

LL FLOORING HOLDINGS, INC.

(Name of Registrant as Specified In Its Charter)

F9 INVESTMENTS, LLC

THOMAS D. SULLIVAN

JOHN JASON DELVES

JILL WITTER

(Name of Persons(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check all boxes that apply):

| ☒ | No fee required |

| ☐ | Fee paid previously with preliminary materials |

| ☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11 |

On May 31, 2024, F9 Investments, LLC, a Florida limited liability company (“F9”), launched a website in connection with the solicitation of shareholders of LL Flooring Holdings, Inc. (the “Company”), which is available at www.LLGroove.com (the “Website”). Copies of the materials posted to the Website are filed herewith as Exhibit 1.

On May 31, 2024, F9 issued a press release (the “Press Release”) and a letter to shareholders (the “Shareholder Letter” and, together with the Press Release, the “Materials”) related to Company, which F9 also simultaneously published to the Website. A copy of the Press Release is filed herewith as Exhibit 2 and a copy of the Shareholder Letter is filed herewith as Exhibit 3. From time to time, F9 or its fellow participants in the proxy solicitation may publish the Materials, or portions thereof, on social media channels relating to the Company and they may otherwise disseminate the Materials from time to time.

EXHIBIT 1

EXHIBIT 2

F9 INVESTMENTS HIGHLIGHTS LL FLOORING’S DANGEROUS PATTERN OF

UNDERPERFORMANCE AND FAILED OPERATIONAL STRATEGY

DUE TO INEFFECTIVE LEADERSHIP

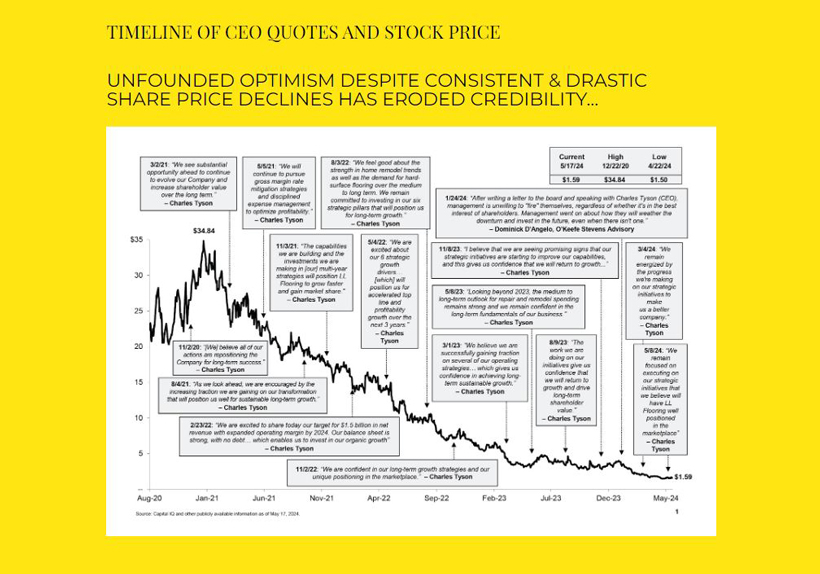

Under Current Board, LL’s Stock Price is Down More Than 63%, 93%, and 83% on a 1-, 3-, and 5-Year Basis, Respectively

F9 Urges Shareholders to Vote the GOLD Proxy Card “FOR” Its Three Highly Qualified Director Nominees – Tom Sullivan, Jason Delves, and Jill Witter – Who Are the Right Individuals

to Restore Value to LL Flooring

F9 Files Definitive Proxy Materials and Mails Letter to LL Flooring Shareholders

F9 Launches www.LLGroove.com

FRANKLIN, Tenn. – May 31, 2024 – F9 Investments, LLC (“F9”), which together with its affiliates collectively owns approximately 8.85% of LL Flooring Holdings, Inc. (“LL Flooring” or the “Company”) (NYSE: LL) common stock and is the Company’s largest shareholder, today filed definitive proxy materials with the Securities and Exchange Commission (“SEC”) for the election of three highly qualified, independent director candidates – Thomas D. Sullivan, John Jason Delves, and Jill Witter – to LL Flooring’s Board of Directors (the “Board”) at the Company’s 2024 Annual Meeting of Shareholders (the “Annual Meeting”) to be held on July 10, 2024.

In connection with the filing of definitive proxy materials, F9 is mailing a letter to LL Flooring’s shareholders urging them to hold the Board accountable for the Company’s abysmal stock price performance on an absolute and relative basis, an ineffective operational strategy, tremendous waste of capital, and flawed strategic review process, among many other failures. The letter also highlights F9’s three highly qualified director nominees, who will bring the experience, focus, relevant industry expertise and proper oversight required to put LL Flooring back on a path to success.

The full text of the letter is below and available at www.LLGroove.com.

May 31, 2024

Dear Fellow LL Flooring Shareholders,

As the largest shareholder in LL Flooring Holdings, Inc. (“LL Flooring” or the “Company”) (NYSE: LL), F9 Investments, LLC, together with its affiliates (collectively “F9” or “we”), owns approximately 8.85% of the Company’s common stock. We are deeply concerned about the severe value erosion of our investment and the utter lack of urgency and engagement demonstrated by the Company’s entrenched Board of Directors (the “Board”).

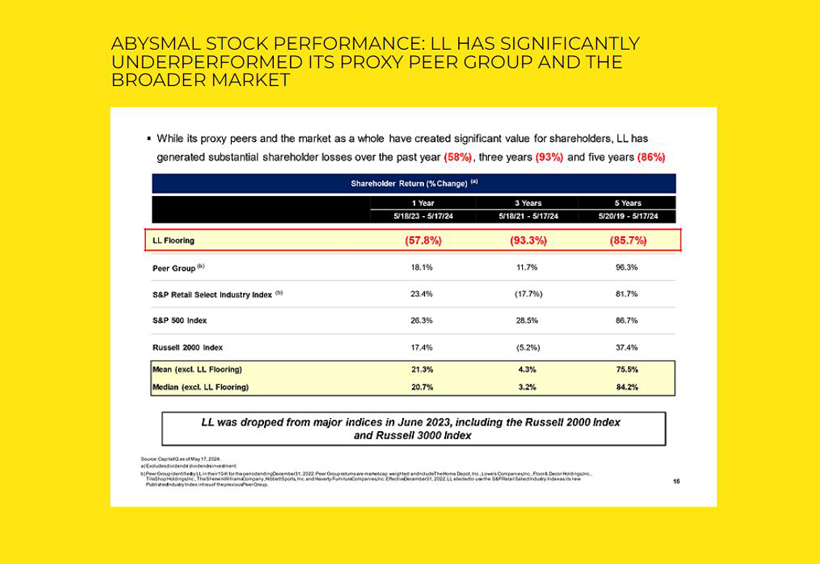

LL Flooring has vastly underperformed its peer group and broader market indices by a shockingly wide margin over all relevant time periods, and the Company’s stock price is down more than 57% this year alone. As a result of the Board’s many failures, the survival of this former industry leader is now in extreme peril, further evidenced by the negative “going concern” opinion recently issued by the Company’s auditors.

Simply put, shareholders deserve an immediate change of course. Accordingly, we have nominated three highly qualified directors to LL Flooring’s Board in connection with the upcoming 2024 Annual Meeting of Shareholders, scheduled for July 10, 2024.

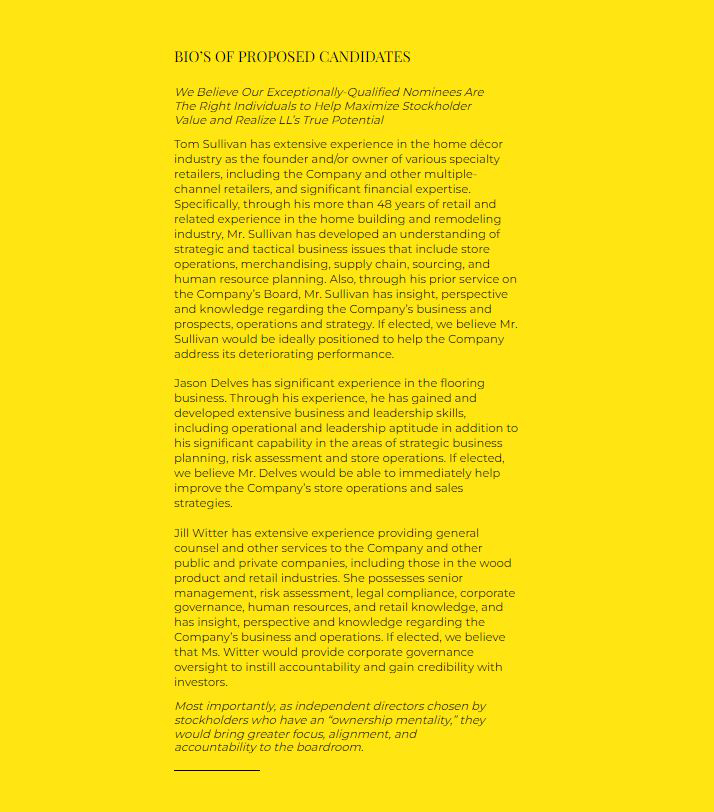

By way of background, F9 is a sophisticated private investment firm with a strong track record of creating enduring value at leading building products and home improvement businesses, including Cabinets To Go, Southwind Building Products and F9 Builder Services, which provides end-to-end solutions to builders. F9 was founded and is solely owned by industry veteran, serial entrepreneur and investor, Tom Sullivan. Mr. Sullivan is also the founder and former CEO and Chairman of Lumber Liquidators, LL Flooring’s predecessor company, which he grew into the largest hardwood flooring retailer in the United States. When Mr. Sullivan left the company in 2016, Lumber Liquidators had become a publicly traded company with a $430 million market cap, 383 outlet stores in 46 states and Canada, and more than 2,000 employees. Since his departure, LL Flooring’s market cap has astonishingly dwindled to approximately $50 million, whereas F9’s cost basis is $4.90 per share, ~200% above the current share price.

So, why are we here?

We are committed to halting the Company’s dangerous downward spiral and restoring the business to its former prominence and profitability by instituting meaningful change to LL’s Board. We are therefore nominating three highly qualified directors – Tom Sullivan, Jason Delves, and Jill Witter – who have a proven track record of successfully operating this and similar businesses under various market conditions. Moreover, they have an actionable, achievable plan to stabilize the business and position LL Flooring for long-term growth and shareholder value creation.

LL Flooring’s current Board has overseen abysmal stock price performance on an absolute and relative basis, an ineffective operational strategy, tremendous waste of capital, and flawed strategic review process, among many other failures.

LL Flooring’s financial performance continues to deteriorate rapidly across all metrics, including sales, profitability, and liquidity. Buried deep in its latest 10-Q filing with the SEC, the Company disclosed it has a “going concern” issue due to its inability to maintain compliance with its debt covenants. Rather than putting forth a plan to stop the bleeding, LL Flooring’s approach is to cover up its wounds with duct tape and hope things get better. Specifically, leadership’s primary solution is to sell a single distribution center and potentially other long-term assets and seek additional financing to meet its obligations. However, this will only serve to increase expenses and further dilute shareholders.

All the while, in 2023, LL Flooring paid its entrenched directors a total of over $1.6 million, including $287,500 to the long-tenured independent Board chair under whose leadership the Company’s stock price has declined an outrageous ~98%. Worse yet, the payments were not tied to performance and were approximately half in cash, furthering the misalignment with shareholders. In an unveiled, egregious display of atrocious corporate governance, on May 20, 2024, LL Flooring announced that the Board would forgo the equity component of its annual Board compensation but would continue to receive its cash payments.

Moreover, the Company’s August 14, 2023, announcement that it would explore strategic alternatives appears to be nothing more than a thinly veiled effort by the Board to buy time to execute its “hope and prayer” strategy, and save the Board and management’s lucrative jobs.

The Board has disclosed that it has received multiple premium offers from bona fide bidders, including F9, only to reject or ignore them as the Company’s share price craters.

WHAT IS GOING ON IN THE LL BOARDROOM?

We believe the only way to protect and enhance the value of your investment is to elect F9’s three director nominees – Tom Sullivan, Jason Delves, and Jill Witter – who have shareholders’ best interest at hand. This stands in stark contrast to the current boardroom where, appallingly, only one of nine directors complies with the Company’s self-imposed director ownership requirement and the scant remaining shareholder capital is being wasted on high-priced legal and financial advisors to protect incumbent directors.

F9’S NOMINEES ARE IDEALLY POSITIONED TO ADDRESS LL’S CONSIDERABLE STRATEGIC, FINANCIAL, OPERATIONAL, AND GOVERNANCE CHALLENGES

Most importantly, as independent directors chosen by shareholders who have an “ownership mentality,” the F9 nominees would bring greater focus, alignment, and accountability to the boardroom. We believe that the election of these three individuals will assist in holding management and the Board accountable for their actions and ensure that the Company operates with a long overdue focus on shareholders by committing to driving performance, maintaining strong corporate governance, and creating meaningful shareholder value.

F9’S NOMINEES PROVIDE EXPERTISE, EXPERIENCE AND A COLLABORATIVE APPROACH TO ASSIST LL’S BOARD IN RESTORING THE COMPANY TO PROMINENCE

LL Flooring is in dire need of a lifeline. Shareholders should not expect meaningful change from a Board that has failed to deliver on its promises for years. Now is the moment to have your voice heard and to protect your investment.

VOTE ON THE GOLD PROXY CARD TODAY “FOR” F9’S NOMINEES TOM SULLIVAN, JASON DELVES, AND JILL WITTER AND “WITHHOLD” ON ALL LL NOMINEES

Shareholders must act decisively to safeguard their investment. EVERY VOTE MATTERS NO MATTER HOW MANY SHARES YOU OWN. We urge shareholders to protect the value of their investment by voting for our nominees using the GOLD proxy card.

You can vote by Internet or by signing and dating the enclosed GOLD proxy card or GOLD voting instruction form and mailing it in the postage paid envelope provided. Do NOT vote using any white proxy card or voting instruction form you receive from LL Flooring. Please discard the white proxy card.

If you have any questions about how to vote your shares, please contact our proxy solicitor, Campaign Management, by telephone 1-(855) 264-1527 (shareholders) or (212) 632-8422 (banks & brokerages) or email at info@campaign-mgmt.com.

For more information, including voting instructions, visit our website www.LLGroove.com.

With your vote, we will be one step closer to ensuring LL Flooring is on a better path to creating lasting shareholder value.

We thank you for your support.

Sincerely,

Tom Sullivan Jason Delves Jill Witter

Solomon Partners Securities, LLC is serving as F9’s financial advisor and Dentons US LLP is serving as its legal advisor.

DISCLAIMER

Except as otherwise set forth in this press release, the views expressed in this press release reflect the opinions of F9 Investments, LLC and its affiliates (“F9”) and are based on publicly available information with respect to LL Flooring Holdings, Inc. (“LL” or the “Company”). F9 recognizes that there may be confidential information in the possession of the Company that could lead it or others to disagree with F9’s conclusions. F9 reserves the right to change any of its opinions expressed herein at any time as it deems appropriate and disclaims any obligation to notify the market or any other party of any such change, except as required by law. F9 disclaims any obligation to update the information or opinions contained in this press release, except as required by law. For the avoidance of doubt, this press release is not affiliated with or endorsed by LL.

This press release is provided merely as information and is not intended to be, nor should it be construed as, an offer to sell or a solicitation of an offer to buy any security nor as a recommendation to purchase or sell any security. Certain of the Participants (as defined below) currently beneficially own shares of the Company. The Participants and their affiliates may from time to time sell all or a portion of their holdings of the Company in open market transactions or otherwise, buy additional shares (in open market or privately negotiated transactions or otherwise), or trade in options, puts, calls, swaps or other derivative instruments relating to such shares.

Some of the materials in this press release contain forward-looking statements. All statements contained herein that are not clearly historical in nature or that necessarily depend on future events are forward-looking, and the words “anticipate,” “believe,” “expect,” “potential,” “could,” “opportunity,” “estimate,” “plan,” “once again,” “achieve,” and similar expressions are generally intended to identify forward-looking statements. The projected results and statements contained herein that are not historical facts are based on current expectations, speak only as of the date of these materials and involve risks, uncertainties and other factors that may cause actual results, performances or achievements to be materially different from any future results, performances or achievements expressed or implied by such projected results and statements. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of F9.

The estimates, projections and potential impact of the opportunities identified by F9 herein are based on assumptions that F9 believes to be reasonable as of the date of this press release, but there can be no assurance or guarantee (i) that any of the proposed actions set forth in this press release will be completed, (ii) that the actual results or performance of the Company will not differ, and such differences may be material, or (iii) that any of the assumptions provided in this press release are accurate.

F9 has neither sought nor obtained the consent from any third party to use any statements or information contained herein that have been obtained or derived from statements made or published by such third parties, nor has it paid for any such statements. Any such statements or information should not be viewed as indicating the support of such third parties for the views expressed herein. F9 does not endorse third-party estimates or research which are used herein solely for illustrative purposes.

Important Information

F9 Investments, LLC, Thomas D. Sullivan, John Jason Delves and Jill Witter (collectively, the “Participants”) filed a definitive proxy statement and accompanying form of gold proxy card (as supplemented and amended, the “Definitive Proxy Statement”) with the Securities and Exchange Commission (the “SEC”) on May 31, 2024 to be used in connection with the 2024 annual meeting of stockholders of the Company.

THE PARTICIPANTS STRONGLY ADVISE ALL STOCKHOLDERS OF THE COMPANY TO READ THE DEFINITIVE PROXY STATEMENT AND OTHER PROXY MATERIALS BECAUSE THEY CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS ARE AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT WWW.SEC.GOV AND F9’S WEBSITE AT WWW.LLGROVE.COM. THE DEFINITIVE PROXY STATEMENT AND ACCOMPANYING PROXY CARD WILL BE FURNISHED TO SOME OR ALL OF THE COMPANY’S STOCKHOLDERS. STOCKHOLDERS MAY ALSO DIRECT A REQUEST TO F9’S PROXY SOLICITOR, CAMPAIGN MANAGEMENT, 15 WEST 38TH STREET, SUITE #747, NEW YORK, NY 10018. STOCKHOLDERS CAN E-MAIL INFO@CAMPAIGNMANAGEMENT.COM OR CALL TOLL-FREE: (855) 264-1527.

Information about the Participants and a description of their direct or indirect interests by security holdings or otherwise can be found in the Definitive Proxy Statement.

INVESTOR AND MEDIA CONTACTS

Investors:

Michael Fein

Campaign Management

(212) 632-8422

michael.fein@campaign-mgmt.com

Media:

Jonathan Gasthalter/Nathaniel Garnick

Gasthalter & Co.

(212) 257-4170

F9Investments@gasthalter.com

EXHIBIT 3

May 31, 2024

Dear Fellow LL Flooring Shareholders,

As the largest shareholder in LL Flooring Holdings, Inc. (“LL Flooring” or the “Company”) (NYSE: LL), F9 Investments, LLC together with its affiliates (collectively “F9” or “we”), owns approximately 8.85% of the Company’s common stock. We are deeply concerned about the severe value erosion of our investment and the utter lack of urgency and engagement demonstrated by the Company’s entrenched Board of Directors’ (the “Board”).

LL Flooring has vastly underperformed its peer group and broader market indices by a shockingly wide margin over all relevant time periods, and the Company’s stock price is down more than 57% this year alone. As a result of the Board’s many failures, the survival of this former industry leader is now in extreme peril, further evidenced by the negative “going concern” opinion recently issued by the Company’s auditors.

Simply put, shareholders deserve an immediate change of course. Accordingly, we have nominated three highly qualified directors to LL Flooring’s Board in connection with the upcoming 2024 Annual Meeting of Shareholders, scheduled for July 10, 2024.

By way of background, F9 is a sophisticated private investment firm with a strong track record of creating enduring value at leading building products and home improvement businesses, including Cabinets To Go, Southwind Building Products and F9 Builder Services, which provides end-to-end solutions to builders. F9 was founded and is solely owned by industry veteran, serial entrepreneur and investor, Tom Sullivan. Mr. Sullivan is also the founder and former CEO and Chairman of Lumber Liquidators, LL Flooring’s predecessor company, which he grew into the largest hardwood flooring retailer in the United States. When Mr. Sullivan left the company in 2016, Lumber Liquidators

had become a publicly traded company with a $430 million market cap, 383 outlet stores in 46 states and Canada, and more than 2,000 employees. Since his departure, LL Flooring’s market cap has astonishingly dwindled to approximately $50 million, whereas F9’s cost basis is $4.90 per share, ~200% above the current share price.

So, why are we here?

We are committed to halting the Company’s dangerous downward spiral and restoring the business to its former prominence and profitability by instituting meaningful change to LL’s Board. We are therefore nominating three highly qualified directors – Tom Sullivan, Jason Delves, and Jill Witter – who have a proven track record of successfully operating this and similar businesses under various market conditions. Moreover, they have an actionable, achievable plan to stabilize the business and position LL Flooring for long-term growth and shareholder value creation.

LL Flooring’s current Board has overseen abysmal stock price performance on an absolute and relative basis, an ineffective operational strategy, tremendous waste of capital, and flawed strategic review process, among many other failures.

LL Flooring’s financial performance continues to deteriorate rapidly across all metrics, including sales, profitability, and liquidity. Buried deep in its latest 10-Q filing with the SEC, the Company disclosed it has a “going concern” issue due to its inability to maintain compliance with its debt covenants. Rather than putting forth a plan to stop the bleeding, LL Flooring’s approach is to cover up its wounds with duct tape and hope things get better. Specifically, leadership’s primary solution is to sell a single distribution center and potentially other long-term assets and seek additional financing to meet its obligations. However, this will only serve to increase expenses and further dilute shareholders.

All the while, in 2023, LL Flooring paid its entrenched directors a total of over $1.6 million, including $287,500 to the long-tenured independent Board chair under whose leadership the Company’s stock price has declined an outrageous ~98%. Worse yet, the payments were not tied to performance and were approximately half in cash, furthering the misalignment with shareholders. In an unveiled, egregious display of atrocious corporate governance, on May 20, 2024, LL Flooring announced that the Board would forgo the equity component of its annual Board compensation but would continue to receive its cash payments.

Moreover, the Company’s August 14, 2023, announcement that it would explore strategic alternatives appears to be nothing more than a thinly veiled effort by the Board to buy time to execute its “hope and prayer” strategy, and save the Board and management’s lucrative jobs.

The Board has disclosed that it has received multiple premium offers from bona fide bidders, including F9, only to reject or ignore them as the Company’s share price craters.

WHAT IS GOING ON IN THE LL BOARDROOM?

We believe the only way to protect and enhance the value of your investment is to elect F9’s three director nominees – Tom Sullivan, Jason Delves, and Jill Witter – who have shareholders’ best interest at hand. This stands in stark contrast to the current boardroom where, appallingly, only one of nine directors complies with the Company’s self-imposed director ownership requirement and the scant remaining shareholder capital is being wasted on high-priced legal and financial advisors to protect incumbent directors.

F9’S NOMINEES ARE IDEALLY POSITIONED TO ADDRESS LL’S CONSIDERABLE STRATEGIC, FINANCIAL, OPERATIONAL, AND GOVERNANCE CHALLENGES

Most importantly, as independent directors chosen by shareholders who have an “ownership mentality,” the F9 nominees would bring greater focus, alignment, and accountability to the boardroom. We believe that the election of these three individuals will assist in holding management and the Board accountable for their actions and ensure that the Company operates with a long overdue focus on shareholders by committing to driving performance, maintaining strong corporate governance, and creating meaningful shareholder value.

F9’S NOMINEES PROVIDE EXPERTISE, EXPERIENCE AND A COLLABORATIVE APPROACH TO ASSIST LL’S BOARD IN RESTORING THE COMPANY TO PROMINENCE

LL Flooring is in dire need of a lifeline. Shareholders should not expect meaningful change from a Board that has failed to deliver on its promises for years. Now is the moment to have your voice heard and to protect your investment.

VOTE ON THE GOLD PROXY CARD TODAY “FOR” F9’S NOMINEES TOM SULLIVAN, JASON DELVES, AND JILL WITTER AND “WITHHOLD” ON ALL LL NOMINEES

Shareholders must act decisively to safeguard their investment. EVERY VOTE MATTERS NO MATTER HOW MANY SHARES YOU OWN. We urge shareholders to protect the value of their investment by voting for our nominees using the GOLD proxy card.

You can vote by Internet or by signing and dating the enclosed GOLD proxy card or GOLD voting instruction form and mailing it in the postage paid envelope provided. Do NOT vote using any white proxy card or voting instruction form you receive from LL Flooring. Please discard the white proxy card.

If you have any questions about how to vote your shares, please contact our proxy solicitor, Campaign Management, by telephone 1-(855) 264-1527 (shareholders) or (212) 632-8422 (banks & brokerages) or email at info@campaign-mgmt.com.

For more information, including voting instructions, visit our website www.LLGroove.com.

With your vote, we will be one step closer to ensuring LL Flooring is on a better path to creating lasting shareholder value.

We thank you for your support.

Sincerely,

Tom Sullivan Jason Delves Jill Witter