Exhibit 99.1

JOHANNESBURG, 18 February 2021: Sibanye Stillwater Limited (Sibanye-Stillwater or the Group) (JSE: SSW & NYSE: SBSW) is pleased to report operating and financial results for the six months ended 31 December 2020, and reviewed condensed consolidated provisional financial statements for the year ended 31 December 2020.

SALIENT FEATURES FOR THE SIX MONTHS AND YEAR ENDED 31 DECEMBER 2020

| ● | Profit attributable to owners of Sibanye-Stillwater increased to R29,312m (US$1,781m) from R62m (US$5m) for 2019 |

| ● | Record adjusted Free Cash Flow (FCF) of R19.9bn (US$1.2bn) – 63x increase from R318m (US$22m) for 2019 |

| ● | Driven by larger diversified production base and robust recovery from COVID lockdown in SA |

| − | Proven ability to assess and respond to challenges |

| ● | Deleveraging achieved – net cash of R3.1bn (US$210m) at end 2020 |

| − | Shift in strategic focus to capital allocation |

| ● | Final dividend of R9.4bn (US$649m) for 2020 – 321cps (US88.8cents per ADR). Full year dividend yield of 8.7%* |

| ● | R6.8bn approved investment in high return SA PGM and gold projects securing operational sustainability and 7,000 jobs |

* Based on the average share price of R42.52 for the year end 31 December 2020

| | | | | | | | | | | | | ||

US dollar | | | | | | SA Rand | ||||||||

Year ended | Six months ended | | | | | | Six months ended | Year ended | ||||||

Dec 2019 | Dec 2020 | Dec 2019 | Jun 2020 | Dec 2020 | | KEY STATISTICS | | Dec 2020 | Jun 2020 | Dec 2019 | Dec 2020 | Dec 2019 | ||

| | | | | | UNITED STATES (US) OPERATIONS | | | | | | | ||

| | | | | | PGM operations1,2 | | | | | | | ||

593,974 | 603,067 | 309,202 | 297,740 | 305,327 | oz | 2E PGM2 production | kg | 9,497 | 9,261 | 9,617 | 18,758 | 18,475 | ||

853,130 | 840,170 | 431,681 | 397,472 | 442,698 | oz | PGM recycling1 | kg | 13,769 | 12,363 | 13,427 | 26,132 | 26,535 | ||

1,403 | 1,906 | 1,508 | 1,837 | 1,970 | US$/2Eoz | Average basket price | R/2Eoz | 32,026 | 30,621 | 22,150 | 31,373 | 20,287 | ||

504.2 | 794.8 | 295.9 | 360.0 | 434.8 | US$m | Adjusted EBITDA3 | Rm | 7,081.2 | 6,002.0 | 4,332.5 | 13,083.2 | 7,290.9 | ||

27 | 29 | 28 | 26 | 32 | % | Adjusted EBITDA margin3 | % | 32 | 26 | 28 | 29 | 27 | ||

784 | 874 | 795 | 866 | 882 | US$/2Eoz | All-in sustaining cost4 | R/2Eoz | 14,342 | 14,429 | 11,678 | 14,385 | 11,337 | ||

| | | | | | SOUTHERN AFRICA (SA) OPERATIONS | | | | | | | ||

| | | | | | PGM operations2,5 | | | | | | | ||

1,608,332 | 1,576,507 | 980,343 | 657,828 | 918,679 | oz | 4E PGM2 production | kg | 28,574 | 20,461 | 30,492 | 49,035 | 50,025 | ||

1,383 | 2,227 | 1,475 | 2,002 | 2,396 | US$/4Eoz | Average basket price | R/4Eoz | 38,954 | 33,375 | 21,671 | 36,651 | 19,994 | ||

608.3 | 1,766.5 | 464.5 | 542.8 | 1,223.7 | US$m | Adjusted EBITDA3 | Rm | 20,024.4 | 9,050.1 | 6,753.2 | 29,074.5 | 8,796.2 | ||

32 | 53 | 32 | 42 | 60 | % | Adjusted EBITDA margin3 | % | 60 | 42 | 32 | 53 | 32 | ||

1,027 | 1,111 | 1,074 | 1,156 | 1,082 | US$/4Eoz | All-in sustaining cost4 | R/4Eoz | 17,586 | 19,277 | 15,779 | 18,280 | 14,857 | ||

| | | | | | Gold operations | | | | | | | ||

932,659 | 982,559 | 587,908 | 403,621 | 578,939 | oz | Gold production | kg | 18,007 | 12,554 | 18,286 | 30,561 | 29,009 | ||

1,395 | 1,747 | 1,432 | 1,613 | 1,850 | US$/oz | Average gold price | R/kg | 967,229 | 864,679 | 676,350 | 924,764 | 648,662 | ||

(67.0) | 472.1 | 140.0 | 100.9 | 371.2 | US$m | Adjusted EBITDA3 | Rm | 6,087.4 | 1,682.9 | 1,967.7 | 7,770.3 | (969.4) | ||

(5) | 28 | 16 | 16 | 36 | % | Adjusted EBITDA margin3 | % | 36 | 16 | 16 | 28 | (5) | ||

1,544 | 1,406 | 1,347 | 1,493 | 1,347 | US$/oz | All-in sustaining cost4 | R/kg | 704,355 | 800,048 | 636,405 | 743,967 | 717,966 | ||

| | | | | | GROUP | | | | | | | ||

4.5 | 1,780.9 | 22.6 | 563.1 | 1,217.8 | US$m | Basic earnings | Rm | 19,926.9 | 9,385.0 | 316.8 | 29,311.9 | 62.1 | ||

(69.7) | 1,770.7 | 19.3 | 561.5 | 1,209.2 | US$m | Headline earnings | Rm | 19,785.1 | 9,360.4 | 254.9 | 29,145.5 | (1,008.2) | ||

1,034.3 | 3,000.4 | 892.4 | 990.4 | 2,010.0 | US$m | Adjusted EBITDA3 | Rm | 32,870.9 | 16,514.0 | 12,937.5 | 49,384.9 | 14,956.0 | ||

14.46 | 16.46 | 14.69 | 16.67 | 16.26 | R/US$ | Average exchange rate using daily closing rate | | | | | | | ||

| 1 | The US PGM operations’ underground production is converted to metric tonnes and kilograms, and performance is translated into SA rand (rand). In addition to the US PGM operations’ underground production, the operation treats recycling material which is excluded from the 2E PGM production, average basket price and All-in sustaining cost statistics shown. PGM recycling represents palladium, platinum and rhodium ounces fed to the furnace |

| 2 | The Platinum Group Metals (PGM) production in the SA operations is principally platinum, palladium, rhodium and gold, referred to as 4E (3PGM+Au), and in the US Region is principally platinum and palladium, referred to as 2E (2PGM) |

| 3 | The Group reports adjusted earnings before interest, taxes, depreciation and amortisation (EBITDA) based on the formula included in the facility agreements for compliance with the debt covenant formula. For a reconciliation of profit/loss before royalties and tax to adjusted EBITDA, see note 11.2 of the condensed consolidated provisional financial statements. Adjusted EBITDA margin is calculated by dividing adjusted EBITDA by revenue |

| 4 | See “Salient features and cost benchmarks” sections for the definition of All-in sustaining cost (AISC) |

| 5 | SA PGM operations’ results for the year ended 31 December 2019 include Marikana operations for the seven months since acquisition |

| | | |

Stock data for the six months ended 31 December 2020 | JSE Limited - (SSW) | ||

Number of shares in issue | | Price range per ordinary share (high/low) | R36.75 to R60.40 |

- at 31 December 2020 | 2,923,570,507 | Average daily volume | 16,587,898 |

- weighted average | 2,783,583,218 | NYSE - (SBSW); one ADR represents four ordinary shares | |

Free Float | 99% | Price range per ADR (high/low) | US$8.64 to US$16.30 |

Bloomberg/Reuters | SSWSJ/SSWJ.J | Average daily volume | 2,788,160 |

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 1

STATEMENT BY NEAL FRONEMAN, CHIEF EXECUTIVE OF SIBANYE-STILLWATER

Indisputably, 2020 has been a year of worldwide disruption, devastation and change. The global spread of the COVID-19 pandemic, which gained momentum in early 2020, was unexpected and the impact severe. The pandemic continues to wreak an immense toll on human lives, has transformed society, social engagement and lifestyles, with major impact for global economic activity. The world is steadily learning how to live and work with COVID-19 enabling social and economic activities to continue with reduced disruption, and we are encouraged by the roll out of vaccines and other preventative actions being taken, which may mitigate further negative consequences of the pandemic. There is no doubt that this pandemic has irrevocably changed life as we know it forever and many of the changes, whether enforced or accelerated, will persist long beyond COVID-19.

Paradoxically, while certain industries have been severely impacted by the virus and the global and national initiatives to manage health risks, other industries such as technology, healthcare and online retail have boomed, with global stock markets recovering to record highs. The commodity and mining sectors have largely recovered from the initial demand shock in H1 2020, as global economic recovery has been more rapid than initially expected, with murmurings of another commodities “super cycle” recently growing in volume. This positive outlook is supported by continued stimulus and expansionary monetary policy being maintained by many countries.

The improving outlook for commodities can also be attributed to a visible shift towards more socially and environmentally aware social and regulatory priorities worldwide. This swing towards prioritising a cleaner and greener global future is likely to drive future investment in infrastructure and renewable energy, which will be extremely positive for commodity prices, particularly the essential metals that Sibanye-Stillwater produces and is targeting.

SAFE PRODUCTION

The safe production journey continues and while we continue to make progress and have achieved some notable safety milestones, we are not yet attaining the intended standard of safety performance. We remain committed to prioritising health and safety in our daily activities.

It was pleasing to note that the key safe production metrics were relatively stable year on-year, despite having to develop and incorporate additional COVID-19 protocols throughout the Group. We also had to contend with the disruptive effect of the lockdown in South Africa in H1 2020 and the complexity of the subsequent safe production build-up following the easing of lockdown restrictions from May 2020. Although the Total Injury Frequency Rate (TIFR) for the Group increased from 8.40 to 8.52 year-on-year and the Serious Injury Frequency Rate (SIFR) ticked higher year-on-year from 3.03 to 3.14, the longer term trend is positive with the TIFR and SIFR significantly better than 2015 levels of 10.33 and 4.68 respectively.

In Q2 2020, the Group achieved the first fatality free quarter since Q4 2018, and the SA gold operations achieved a remarkable milestone of 13 million fatality free shifts over close to a two year period in August 2020. The loss of nine of our colleagues during the year due to fatal incidents at the SA operations caused significant distress throughout the Group. The Group suffered five fatalities at the SA gold and PGM operations during H2 2020, with four fatalities having occurred previously at the SA PGM operations in Q1 2020.

As per our usual protocols, these incidents have been fully investigated and appropriately managed. These fatalities occurred during periods of significant operational disruption and change (the integration of the Marikana operations in Q1 2020 and the post lockdown return to work from May 2020). At Sibanye-Stillwater, we are responsible for the well-being of more than 80,000 employees and we cannot accept our operating environment (deep level underground and labour intensive) as an inhibitor of excellent safety performance. We will improve overall safety at our operations by addressing behaviour related issues and real risk reduction, to ensure our safe production performance is comparable with international peers. Our values-based culture programme has been developed to address many of the high frequency risks and we believe that we will continue to see improved safe production outcomes as this programme continues to roll out.

ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG)

As mentioned, the COVID-19 pandemic, particularly the initial lockdown period at the beginning of 2020 has prompted increased awareness and focus on global responsibility, with ESG continuing to gain prominence and relevance.

At Sibanye-Stillwater, sustainability, which encompasses environmental, social and governance excellence, along with safety as an overriding priority, has always been prominent and woven into our approach to business and the way we interact and deal with all stakeholders.

Since the inception of the company in 2013, our CARES values (Commitment, Accountability, Respect, Enabling and Safety) have informed our strategy and business culture. We have been cognisant since the formation of the Group in 2013, that building a successful and sustainable business cannot be achieved without considering and incorporating the interests and needs of all stakeholders as a fundamental part of how we operate and in so doing, ensure that each derives appropriate benefit or value from our activities. This approach is captured in our vision of “creating superior value for all stakeholders”, which is unchanged and has proven to be prescient with companies across the globe beginning to recognise the importance of all stakeholders subscribing to an ethos of stakeholder capitalism and shunning the historical notion of shareholder primacy. Investors are increasingly recognising that companies need to have regard for all stakeholders in order to have the social legitimacy to operate that enables them to sustainably generate superior returns.

Our Group purpose is “Our mining improves lives” and this core mantra has become increasingly relevant as the Group has grown and evolved from a South African gold producer in 2013, to a global, diversified precious metals corporation today. We improve lives in a myriad of multi-faceted ways: from the jobs we provide, employing over 80,000 people worldwide, to the businesses we support and continue to develop and grow in our supply chain, to the communities we support and develop, to the critical financial contribution we make to local and national governments and to the importance of the metals we produce to ensure a cleaner, greener and more sustainable world for all.

From a social perspective, assisting stakeholders to manage the COVID-19 pandemic was a primary focus during 2020. The Group has continued to provide comprehensive support to employees and their families, local communities and regional and national government in the ongoing struggle with the COVID-19 pandemic (detail on these ongoing efforts was provided in the previous Operating and Financial Results for the six months ended 30 June 2020, which was published on 27 August 2020).

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 2

It is clear that we will be living and working in a COVID-19 affected world for the foreseeable future, although the availability of vaccines marks the start of a new phase in combatting the pandemic. While the roll out of the vaccines has commenced in Montana with mine employees prioritised as essential workers during an early phase of the state’s inoculation programme, the roll out of the vaccine in South Africa has just begun and a holistic vaccination programme to protect against severe disease and attain the goal of population immunity within a reasonable time frame, is in its early stages. The eventual role that the private sector will discharge in this programme remains unclear.

The SA mining industry has expressed its commitment to assist Government with the logistics of the vaccine roll out throughout the country. Significant Company resources are available to assist should it be required, including our 44 healthcare facilities and qualified healthcare professionals spread throughout the regions in which we operate. We have proven the capability and capacity of our systems to deliver health care services to our workforce and communities through the COVID-19 lockdown and subsequent return to work, which has been effectively managed.

Our analysis indicates that we should be able to vaccinate approximately 18,000 people per day, enabling us to cover our entire workforce within a week and extend the same benefit to their families and many people in our doorstep communities in a relatively short period. Board approval has already been granted to commit up to R200 million in direct and indirect funding/assistance to the vaccine roll out effort.

This represents a significant commitment and as such needs to be accompanied by specific conditions. These include:

| ● | The direct monetary contribution will be administered through the Solidarity Fund to coordinate proper and effective application |

| ● | We support the phased approach by Government, with the highest risk citizens such as healthcare workers in both the public and private sectors logically prioritised as a first phase. While we acknowledge classification of the mining industry as an essential service included in the second phase of the national vaccine roll out, we consider that vaccines acquired or financed directly by the company should be allocated for employees and their dependents (and communities if required) and preferably administered through our health care facilities by our qualified professionals |

| ● | We require full transparency on the commercial arrangements for vaccine procurement by Government and the management of logistical resources. |

With regard to environmental aspects, as the largest primary producer of PGMs worldwide and one of the largest recyclers of autocatalysts containing PGMs in the US, the Group already makes a significant contribution to ensuring a clean and safe environment. Due to their unique chemical and physical characteristics and catalytic qualities, for decades the PGMs have been essential metals utilised in catalytic converters in the exhausts of internal combustion engine automobiles in order to transform noxious exhaust gasses into more benign components. The Group is positioned to play an increasing role in the future green economy, via its battery and tech metal strategy and the growing potential of the hydrogen economy, which may significantly increase demand for PGMs.

In line with our commitment to ESG excellence and continual improvement throughout the business, a comprehensive review of the Group environmental and energy footprint was undertaken, which indicates that we should be able to achieve carbon neutrality by 2040. Considering the origins of the Sibanye-Stillwater Group with its deep level, energy intensive SA gold operations, which together with our other SA operations, are currently entirely dependent for their electricity needs on largely coal fired power from the South African state utility Eskom, this will be a commendable achievement. We aim to achieve this goal by, inter alia:

| • | Advocating for an enabling electricity supply industry in South Africa, supportive of decarbonisation |

-Direct representation on the Energy Intensive Users Group, BUSA electricity policy task team, and other sectoral forums

| • | Energy and decarbonisation governance through policy, strategy, target setting and performance management |

-Decarbonisation targets built into the LTI framework

| • | Improving energy efficiency |

-Targeted 2-3% year on year improvements minimum

-165,260tCO2e of emissions avoided in 2020

| • | Increasing renewables as part of our energy mix |

-50MW solar PV plant in development, with 200MW of additional solar PV, storage and wind projects under investigation

-20% renewable penetration at a minimum by 2040

We believe that we can accelerate the transition to carbon neutrality, and have an ambition to achieving a zero carbon footprint for the Group by 2040. We will ensure that stakeholders are kept appraised of our progress in this regard together with our ongoing efforts towards excellence in other environmental measures, on a regular basis.

OPERATING AND FINANCIAL REVIEW

2020 was a defining year for the Group, marking the end of the deleveraging phase that has prevailed over the past three years. Despite the significant challenges associated with the COVID-19 pandemic, the Group delivered a record financial performance and made notable progress towards delivery on many strategic targets. This performance is testament to benefits of the strategic growth and diversification undertaken in recent years and reflects the quality, depth and resilience of the Sibanye-Stillwater leadership. We have come out of this period strongly, and the Group is well positioned for the ongoing delivery of value for all stakeholders.

Despite the ongoing implementation and observance of COVID-19 protocols to support the health and wellbeing of our workforce, production from the three operating segments for 2020 was consistent with the prior year. The build-up to normalised production levels at the SA operations from the COVID-19 lockdown in Q2 2020 exceeded forecasts despite the adoption of a phased return to work in order to protect the health and safety of employees during this sensitive period. Both the SA gold and PGM operations reached normalised production rates in November 2020, positioning the Group for an improved operational performance in 2021.

The SA PGM operations produced 1,576,507 4Eoz in 2020 (including attributable ounces from Mimosa), exceeding the upper limit of revised annual guidance of between 1,350,000 4Eoz and 1,450,000 4Eoz by 9%, with PGM production of 918,679 4Eoz for H2 2020, 40%

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 3

higher than for H1 2020. Mined PGM production from the US PGM operations of 603,067 2Eoz in 2020 was marginally higher year-on-year, but below revised guidance of between 620,000 and 650,000 2Eoz, primarily due to the impact of a spike in COVID-19 infections at the US PGM operations in Q4 2020, associated with a severe wave of COVID-19 infections in Montana. Despite the COVID-19 disruptions, H2 2020 production of 305,327 2Eoz was 3% higher than for H1 2020, with most operating trends improving towards the end of the year. Production from the SA Gold operations (excluding DRDGOLD) of 25,190kg (809,877oz) was 3% above revised guidance of between 23,500 and 24,500kg (756,000oz and 788,000oz), with production of 15,023kg (483,001oz) for H2 2020, 48% higher than for H1 2020.

This solid operational performance underpinned the record financial results by obtaining full exposure to higher average precious metal prices. The average 4E PGM basket price increased by 83% to R36,651/4Eoz (US$2,227/4Eoz) for 2020 with the average 2E PGM basket price increasing by 36% to US$1,906/2Eoz (R31,373/2Eoz) and the average rand gold price increasing by 43% to R924,764/kg (US$1,747/oz). The average SA exchange rate depreciated by 14% to R16.46/US$ for the year.

Group revenue increased by 75% year-on-year to R127,392 million (US$7,740 million), with H2 2020 revenue of R72,374 million (US$4,439 million) on par with full year revenue of R72,925 million (US$5,043 million) for 2019. Group adjusted EBITDA for 2020 increased by 230% year-on-year to R49,385 million (US$3,000 million) compared to R14,956 million (US$1,034 million) for 2019.

This resulted in profit attributable to owners of Sibanye-Stillwater, increasing 472 fold from R62 million (US$5 million) for 2019 to R29,312 million (US$1,781 million). Basic earnings per share (EPS) of 1,074 cents (US 65 cents/US 261 cents/ADR) and headline earnings per share (HEPS) of R1,068 cents (US 65 cents/US 260 cents/ADR) increased by 53,600% and 2,770% respectively year-on year.

Sibanye-Stillwater’s economic contribution to the regions in which we operate grew commensurately to our profitability, with royalties increasing by 310% to R1,765 million (US$107million) for 2020 from R431 million (US$30 million) for 2019 and current mining tax increasing from R1,849 million (US$128 million) for 2019 to R5,374 million (US$327 million) for 2020. Along with other taxes, this R4,859 million (US$295 million) higher fiscal contribution is significant, particularly during a period when many countries have experienced economic devastation associated with the COVID-19 pandemic.

The Group deleveraging was successfully achieved during the year, with borrowings reducing by R5,354 million (US$444 million) to R18,383 million (US$1,251 million) and cash and cash equivalents increasing to R20,240 million (US$1,378 million). On a trailing 12 month basis, adjusted EBITDA increased by 230% to R49,385 million (US$3,000 million) resulting in a net cash: adjusted EBITDA ratio of 0.06x compared to net debt: adjusted EBITDA of 1.25x at the end of 2019.

This accelerated deleveraging has significantly de-risked the Group from a financial perspective, addressing what market analysts have continually highlighted as a primary concern and a justification for a relative discount in our investment rating since 2017. Completing this strategic priority allows for a shift in the strategic focus from deleveraging to capital allocation - securing an appropriate balance between consistent and sustained flows of value to stakeholders and allocating capital to ensure the sustainability of the Group and support strategic growth.

After giving due consideration to the successful resumption of operations to normalised operating levels during H2 2020 and the robust financial position of the Group, the Board declared a year-end dividend which delivers a full year dividend to shareholders at the top end of the Group policy range.

Normalised earnings** which are the basis for the declaration of dividends as per the Group dividend policy (see note 9 of the condensed consolidated provisional financial statements), increased by R28,247 million (US$1,696 million), to R30,607 million (US$1,860 million) for 2020 from R2,360 million (US$163 million) in 2019, resulting in the Board declaring full year dividends of R10,713 million (US$649 million) or 371 cents per share (US$25.15 cents per share or US$100.62 cents per ADR). This is equivalent to an approximate dividend yield of 6% at the prevailing share price, well ahead of most peers. Adjusting for the 50 cent per share interim dividend (US$2.94 cents per share or US$11.79 cents per ADR) results in a final dividend for 2020 of approximately R9,375 million (US$649 million) or 321 cents per share. (US$22.21 cents per share or US$88.83 cents per ADR)

** Normalised earnings is defined as earnings attributable to the owners of Sibanye-Stillwater excluding gains and losses on financial instruments and foreign exchange differences, impairments, gains and losses on disposal of property, plant and equipment, occupational healthcare expense, restructuring costs, transactions costs, share-based payment on BEE transaction, gain on acquisition, net other business development costs, share of results of equity-accounted investees, after tax, and changes in estimated deferred tax rate. This measure constitutes pro forma financial information in terms of the JSE Listings Requirements and is the responsibility of the board of directors (Board)

INVESTING FOR SUSTAINABLE VALUE

On 15 February 2020 Group Mineral Resources and Reserves were updated for the year ended 31 December 2020. Of primary significance was the 40% increase in the 4E PGM Mineral reserves at the SA PGM operations to 39.5M 4Eoz, primarily due to the inclusion of 12.7M 4Eoz PGM Mineral Reserves from the K4 project at the Marikana operation and the Klipfontein opencast project (0.1Moz) at the Kroondal operation. Gold Mineral Reserves at the SA gold operations and 2E PGM reserves at the US PGM operations remained stable at 11.3Moz and 26.9M 2Eoz respectively. Following the optimisation of the mining layout and scheduling at the Burnstone Project, combined with estimation model improvements, gold Mineral Reserves for the SA gold projects increased by 8% or 0.3Moz to 4.3Moz.

On 16 February 2021 the Board approved the development of the K4 and Klipfontein projects at the SA PGM operations and the resumption of capital development and equipping at the Burnstone gold project. This represents a significant capital investment of approximately R6.8 billion in high return organic projects in South Africa. The projects have a combined NPV of R5.1 biillion at conservative project prices assumed for the evaluations, which increases significantly to R26.9 billion at current spot prices. In addition to this value add for investors in Sibanye Stillwater, the ancillary benefits for communities and other stakeholders will be significant. Approximately 7,000 jobs will be created and sustained over the life of the projects, with significant financial benefits likely to accrue to local communities and regional and national government

The K4 project is a tier one, low cost, brownfields PGM expansion project at the Marikana operations. The project entails completion of the project, which was significantly advanced by Lonmin with R4.4bn of sunk capex before Lonmin suspended the project due to capital constraints. The K4 project has low execution risk and is expected to be brought into first production within 12 months and reach sustainable annual production of approximately 250,000 4Eoz and at average operating costs of approximately R16,000/4Eoz

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 4

achieved in approximately seven years. Project capital investment of R3.9 billion is relatively low for a project of this scale, resulting in superior NPV of R3 billion and an IRR of 33% with a six-year payback using conservative project price assumptions. The NPV increases seven fold to R21 billion with an IRR of 80% and a four year payback at current spot metal prices.

The Klipfontein project is a small robust open cast PGM opportunity, which will be developed in terms of the existing Pool and Share Agreement (PSA) with Anglo American Platinum at the Kroondal operations. The Klipfontein project will produce approximately 40,000 4Eoz per annum over a three year LoM of with low average operating cost around R9,000 4Eoz. Project capital is estimated at R66 million, predominantly in the first year, yielding a NPV of R738 million and an IRR of 70% using conservative project price assumptions. The NPV increases to R2.1 billion with an IRR of 110% at current spot metal prices.

These projects will deliver significant socio-economic benefits to the Rustenburg region, with the K4 project providing approximately 4,380 jobs at steady state and the Klipfontein project approximately 124 jobs. Both projects will create meaningful opportunities for local procurement, skills transfer and the provision of economic benefits to local SMMEs and local communities. The Klipfontein project will sustain the production profile of Kroondal for longer and the K4 project will ensure the sustainability of the Marikana operations for ~50 years.

The Burnstone project is a low cost, extensively pre-developed gold asset in the Balfour area, Mpumalanga which was previously operated under Great Basin Gold. The project will ramp up over five years to a steady state production of around 130,000oz per annum for 10 years with average operating costs of around R420,000/kg. Project capital investment of R2.3 billion returns an NPV of R1.4 billion and an IRR of 24% with a payback of seven years using conservative project price assumptions. The NPV increases to R3.8 billion with an IRR of 39% at the current spot rand gold price.

The Balfour community is an impoverished community in Mpumalanga facing severe socio-economic challenges, which will benefit significantly from economic investment in the region and the resultant employment. The mine will create 2,500 permanent jobs in an area faced with unemployment exceeding 30% and will create meaningful opportunities for local procurement and SMME development and the transfer of skills.

In addition to these projects approved by the Board, the Group has an extensive pipeline of organic projects including downstream beneficiation opportunities, primarily in South Africa, which could be developed under appropriate conditions. Amongst the projects identified and undergoing further assessment are:

| ● | At the SA PGM operations, the East 3 shaft, M5 project (old Marikana) decline and East 4 project (Pandora complex) at the Marikana operation, the Siphumelele 1 shaft UG2 project and below infrastructure Merensky extensions on the Thembelani and Khuseleka shafts at the Rustenburg operation and the Meccano chrome project at Kroondal |

| ● | At the SA gold operations the Bloemhoek project adjacent to the Beatrix operation is undergoing further evaluation with work on the secondary reef projects at the Kloof and Driefontein operations continuing |

Aside from the initial project capital, investment in organic projects of this nature would secure operational sustainability and deliver significant benefits for all stakeholders over many years, creating direct and indirect employment, fostering the development of supplier industries and SMMEs to support the operations, delivering community upliftment and support via SLPs and other social development projects and would contribute significantly to local and national Government in the form of rates, taxes and royalties.

Investing in capital intensive long life projects is not simply a commercially driven decision however, and is influenced by many other considerations other than the incentive pricing of commodities relative to operating costs. These factors include assumptions about the prevailing and future investment environment and the long term operating context, Government policy and regulatory efficiency and other factors which affect the required minimum rate of return or hurdle rate required to justify investment.

The commitment to invest approximately R6.8 billion in the three major capital projects approved by the Board should not be construed as a vote of confidence in the investment climate in South Africa. Continued policy uncertainty, combined with other risks, such as those related to the reliability of water and power availability and the uncertain outlook for electricity costs, as well as risks of social disruption and inefficient regulatory processes are ongoing deterrents to significant investment.

This has been apparent in previous commodity upcycles, where only projects with an extremely strong commercial case can be justified, resulting in SA lagging the rest of the world in terms of investment and growth of its mining sector. The projects we have approved are among the best in the industry due to specific characteristics, which enhance their attractiveness and supported the investment decision. These factors include significant pre-development by previous owners, resulting in relatively low capital to completion, a short lead time to first production and a quick payback on invested capital, which reduces the risk significantly and delivers superior returns. Few projects offer these characteristics and hence investment in the mining sector has been limited in recent years. Roger Baxter, CEO of the Minerals Council recently referred to potential investment of about R20 billion that could be approved by the SA mining industry in a supportive environment – as you can see from the investments we have just declared, this number is likely to be conservative.

A significant effort is going to be required to revitalise and reboot the mining industry and, with it, the national economy. The mining industry remains a critical component of the South African economy with strong multiplier effects into supporting industries and communities, and has the potential to catalyse and drive much needed growth, particularly with the increasingly positive outlook for a sustained period of higher commodity prices.

An example of this potential can be seen in recent reports which suggest that estimated South African tax revenue receipts for 2020 may be close to R300 billion, delivering a surplus of up to R100 billion more than prior projections of R200 billion for 2020. A significant component of this windfall can be attributed to increased royalty and tax receipts from the mining industry, which was the first to resume commercial activity after the lockdown in April 2020 and benefited from rising commodity prices in the latter part of the year. This is evident in a significant increase in royalties and taxes for the Group during 2020 as previously pointed out, which increased by 213% or R4,860 million (US$295 million) year on year, despite the impact of the COVID-19 pandemic. This surplus income is a welcome boon for the South African economy, which has been struggling financially for some time and was dealt a severe blow by COVID-19.

It is clear that the mining industry plays a critical role in the South African economy and could be the driver of much needed, but until now, absent economic growth. With an increasingly positive outlook for a sustained period of higher commodity prices, the

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 5

mining industry could be a strong driver of South Africa’s economic recovery. This potential will only be fully realised in a much more supportive environment however – one which incentivises, attracts and provides security for long term investment.

We have a significant opportunity as a country, which we cannot afford to squander. The private sector in South Africa has indicated its readiness to participate in the renewal of the economy. It will require significant courage and change from Government and other stakeholders to facilitate this.

OUTLOOK

The impact of the COVID-19 pandemic global economy during 2020 was profound and led to an approximate 14% decline in global demand for platinum, palladium and rhodium. The impact of this decline in demand on PGM prices was short lived however, with prices recovering rapidly at the end of Q1 2020, following the imposition of the countrywide lockdown in South Africa from late March 2020. The suspension of mining until May, followed by a gradual buildup of production during the remainder of the year, resulted in global primary platinum, palladium and rhodium supply declining by approximately 11% for 2020, largely offsetting the drop in demand. Secondary supply from recycling was also 10% lower due to COVID-19 related restrictions, which affected global recycling logistics, as well as fewer vehicles being scrapped. Converter plant failures at Anglo American Platinum’s processing operations in Q1 2020 and Q4 2020 exacerbated the supply shortfall from South Africa, with the second outage adding to an already tight market and driving PGM prices higher at year end and into 2021.

We expect sustained palladium deficits into 2024, supported by recovering auto sales and tightening emissions regulations in key markets, resulting in increased autocatalyst loadings. Thereafter, we forecast growing palladium surpluses as new mine supply comes online (from our US PGM operations and from Norilsk Nickel), and substitution of palladium with platinum in gasoline autocatalysts accelerates.

Conversely, we expect platinum market surpluses to narrow over the first half of the decade, with deficits forecast from 2024. This is largely due to the effect of substitution and declining production from SA. Our three-year investment into research and development (R&D) of a tri-metal catalyst for gasoline cars, together with BASF, has been successful. The tri-metal catalyst is able to replace palladium with platinum in a 1:1 ratio. Based on current uptake estimates substitution of palladium with platinum could increase to over 1Moz by 2025. Better alignment of the PGM basket demand with supply will provide longer-term sustainability and greater price stability. Growing acceptance of substitution in gasoline autocatalysts and increasing investment interest in the hydrogen economy has resulted in the platinum price achieving multi-year highs in 2021. We expect the platinum price to be well supported, with significant upside over the next 5 years.

Rhodium’s sustained market deficits and runaway prices are a growing concern in the absence of investment into new supply or alternative catalysts to meet tightening emissions regulation. We believe that R&D into substitution of rhodium must be considered over the near term.

The near to medium term fundamental outlook for PGMs is robust. As the largest primary producer and recycler of PGMs in the world, Sibanye-Stillwater’s investments into high return, organic growth projects positions us well to support PGM demand driven by increasing social pull and regulatory drive for a cleaner environment. Aspirational climate change targets in Europe and other parts of the world have raised investor interest in the hydrogen economy. Longer-term production of green hydrogen for industrial use is supportive of demand for both platinum and iridium.

With the medium term evolution of the automobile drive train from internal combustion engines (ICE) to greener technologies, such as battery electric, fuel cell electric and hybrid vehicles, we continue to monitor and evaluate the sector for entry points that meet our strategic objectives.

As our customers’ needs change, the opportunity for us to further build on our mining platform and diversify our offering will ensure that we remain a preferred supplier of strategic metals for tomorrow’s powertrains.

OPERATING GUIDANCE FOR 2021

A meaningful increase in mined 2E PGM production from the US PGM operations is forecast for 2021. Mined 2E PGM production is forecast to be between 660,000 2Eoz and 680,000 2Eoz, with AISC of between US$840/2Eoz to US$860/2Eoz. Capital expenditure is forecast to be between US$300 million and US$320 million, approximately 60% of which is growth capital in nature.

4E PGM production from the SA PGM operations for 2021 is forecast to be between 1,750,000 4Eoz and 1,850,000 4Eoz with AISC between R18,500/4Eoz and R19,500/4Eoz (US$1,230/4Eoz and US$1,295/4Eoz). Capital expenditure is forecast at R 3,800 million (US$ 253 million) with levels for 2021 elevated due to carry over of approximately R800 million (US$53 million) of capital from 2020 which was unspent due to the COVID-19 disruptions. In addition, R1,500 million (US$100 million) of project capital expenditure is expected following the approval of the K4 and Klipfontein projects.

Gold production from the SA gold operations for 2020 is forecast at between 27,500kg (884,000oz) and 29,500kg (948,000oz) with AISC between R760,000/kg and R815,000/kg (US$1,576/oz and US$1,690/oz). Capital expenditure is forecast at 4,025 million (US$268 million), including carry over of approximately R400 million (US$27 million) of capital from 2020 which was unspent due to the COVID-19 disruptions. R425 million (US$28 million) of project capital expenditure has been provided for the Burnstone project.

The dollar costs are based on an average exchange rate of R15.00/US$.

Neal Froneman

Chief Executive Officer

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 6

Safe PRODUCTION

Safe production is a Group imperative and the Group remains committed to achieving zero harm in the work place. Recent safe performance achievements suggest that this goal is attainable and we continue to refine and adapt our safe production strategy and protocols. The Group safety performance for 2020 was sound, considering the significant disruption and distractions caused by the COVID-19 pandemic, with the Group Serious Injury Frequency Rate continuing to decline, falling from 4.68 in 2015 to 3.03 in 2020 and the Total Injury Frequency Rate (TIFR) of 8.52 up from 8.40 in 2019, but showing an overall 18% improvement compared with 2015, despite the significant growth in the company since then.

The loss of nine of our colleagues during the year, due to fatal incidents at the SA operations, caused significant distress throughout the Group. After recording zero fatalities during Q2 2020 and the SA gold operations achieving a record and remarkable milestone of 13 million fatality free shifts (FFS) over a close to two year period prior, the Group suffered five fatalities at the SA gold and PGM operations during H2 2020, with four fatalities previously occurring at the SA PGM operations in Q1 2020.

The Board and management of Sibanye Stillwater extend their sincere condolences to the family and friends of our fallen colleagues at the SA Gold and PGM operations: Mr Jaoa Silindane, Mr Khulile Nashwa, Mr Emanoel Kaphe, Mr Rossofino Manhavele, Mr Mfuneko Manikela, Mr Bonginkosi Hlophe, Mr Hlopang Temeki, Mr Cebo Gungthwa and Mr Erens Mello. All incidents have been thoroughly investigated together with the relevant stakeholders to ensure that they are not repeated and appropriate support provided to the families.

The SA PGM operations also experienced a TIFR at 9.20, an increase from 7.84 for 2019, largely due to a regression in H2 2020, with the return to work from the COVID-19 lockdown, but in line with the figures going back to 2014. On 8 Dec 2020 the SA PGM operations plants and concentrators achieved a significant milestone of 13 million FFS.

The US PGM operations reported further improvement in safe production achieving a notable milestone of 3 million fatality free shifts having operated without any fatal incidents since October 2011.

An overall improvement in the safe production performance for the SA gold operations was marred by four fatal incidents in H2 2020 after close to two years’ operating without any fatalities. The TIFR for 2020 6.99 was the lowest level for the SA Gold operations since inception.

US PGM operations

Mined 2E PGM production for 2020 of 603,067 2Eoz, was 2% higher than for the comparable period in 2019, although 3% below the lower end of revised production guidance for 2020, with the state of Montana significantly impacted by the second wave of COVID-19 infections during Q4 2020. AISC for 2020 increased by 11% to US$874/2Eoz due to significantly higher sustaining capital which increased by 32% year-on-year to US$124 million; higher royalties, taxes and insurance which increased by approximately US$24 million (US$38/2Eoz of the AISC increase) due to a 36% higher 2E PGM average basket price at US$1,906/2Eoz and unbudgeted COVID-19 costs (approximately US$6 million or US$10/2Eoz). Despite COVID-19 challenges, total development increased by 3% year-on- year to 27,038m, with development rates improving towards year-end.

The Fill The Mill (FTM) project at the East Boulder mine was brought in on time achieving a sustainable annual run rate of 40,000 oz per annum in December 2020.

3E PGM recycling for 2020 decreased by 2% to 840,170 3Eoz primarily due to lower deliveries for Q2 2020 as a result of the disrupted supply chains earlier in the year. Recycling receipts increased significantly during Q4 as supply chains normalised.

The recycling operations fed an average of 26.4 tonnes per day of spent catalysts in 2020, 2% lower than 2019, but the rate picked up from 25.4 tonnes in H1 2020 to 27.5 tonnes per day in H2 2020, consistent with rates in H2 2019. Increased recycling receipts resulted in recycling inventory building to approximately 600 tonnes in Q3 2020 before being drawn down to approximately 400 tonnes by year end. Recycling inventory is expected to normalise to below 200 tonnes during H1 2021, with a resultant release of working capital.

The average 2E PGM basket price of US$1,906/2Eoz for 2020 was 36% higher than for 2019, resulting in adjusted EBITDA from US PGM operations of US$795 million, 58% higher than for 2019. The recycling operation contributed approximately US$53 million to this total.

Capital expenditure for 2020 was 15% higher than for 2019 at US$269 million with sustaining capital 32% higher at US$124 million and growth capital 3% higher at US$145 million mainly incurred at Stillwater East (SWE) and in completing the FTM project.

Mined PGM production of 305,327 2Eoz for H2 2020 was 1% lower than the comparable period in 2019 but 3% higher than H1 2020. Production from the Stillwater mine (including Stillwater West (SWW) and SWE) for H2 2020 was 194,461 2Eoz, 1% higher than the comparable period in 2019. East Boulder (EB) delivered 110,865 2Eoz for H2 2020, 5% lower than for 2019 due to lower grades and COVID-19 related production shortfalls.

There was an improvement in most operational metrics towards year end, with an increase of 16% in development rates in H2 2020 relative to H1 2020 and a 23% increase relative to H2 2019, consistent with the renewed focus on increasing operational flexibility at SWE. AISC of US$882/2Eoz for H2 2020 was 11% higher than for H2 2019 largely due to lower PGM production, higher ground support costs and higher sustaining capital. As a result of the 31% increase in the average basket price for H2 2020 to US$1,970/2Eoz, royalties and taxes increased, accounting for approximately US$42/2Eoz of the AISC increase. COVID-19 related expenditures of approximately US$3 million were incurred in H2 2020.

Blitz project update

As previously updated, the operating review on the Stillwater East (SWE)(Blitz) project has indicated a delay of up to two years, with production from SWE expected to reach the steady state run rate of approximately 300,000 2Eoz per annum in 2024. SWE has experienced various operational challenges and disruptions over the last 18 months, including:

| ● | ground conditions neccessitated modifications to mining methods and ground support to ensure safe extraction |

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 7

| ● | ventilation constraints temporarily resulted in concentrated mining fronts leading to sporadic elevated DPM levels that required ventilation modifications to remedy |

| ● | higher than expected water ingress requires extensive grouting campaigns negatively impacting primary and secondary development efficiencies |

| ● | COVID-19 negatively affected productivity and caused equipment and material delays as a result of associated supply chain challenges. As a consequence capital projects not on the project critical path, were delayed in the interest of contractor deployment efficiency. Key project build components were also negatively impacted by some suppliers of key project components declaring of force majeure |

Following a review, replanning and subsequent project optimisation undertaken during H2 2020, we are confident that a run rate of 300,000 2Eoz per annum will be achieved in 2024. The delay in the production build-up does impact on forecast capital and operating costs. Approximately US$375 million project capital will be required to reach steady state production in the next three years of with AISC for the total US PGM operations is forecast to reduce to an average of US$750/2Eoz (2021 monetary terms) once steady state production at SWE is achieved, including around US$210/oz of annual stay in business capital.

SA PGM operations

The operational performance from the SA PGM operations was commendable considering the sizeable challenges and operating adjustments required during the year. 4E PGM production of 1,576,507 4Eoz for 2020 (including attributable ounces from Mimosa), 9% above the upper limit of revised annual guidance of 1.35 – 1.45 million 4Eoz, production building back to pre COVID rates by November 2020, well ahead of expectations with PGM production for H2 2020 40% higher than for H1 2020. Production for 2020 was 2% lower than 2019 but due to the acquisition of Lonmin in June 2019 it is not directly comparable.

Considering the impact of COVID-19 on production and additional COVID-19 costs, costs for 2020 were well contained with AISC of R18,280/4Eoz (US$1,111/4Eoz) below revised market guidance of R18,500-R20,500/4Eoz. As a result of the transition of the Rustenburg operation from a purchase of concentrate (PoC) processing arrangement with Anglo American Platinum to toll processing (explained in 2019 in detail) as well as the inclusion of Marikana from June 2019, which significantly impacted AISC on a production weighted basis, full year AISC comparison for the full year 2020 with 2019 is not appropriate. Comparing AISC for H2 2020 with H2 2019 is more representative. AISC of R17,586/4Eoz (US$1,082/4Eoz) for H2 2020 was 11% higher than for H2 2019, primarily due to lower production year-on-year (6% lower due to the build-up after the COVID-19 lockdown) and higher royalties, which added R975 million or R1,061/4Eoz (US$65/4Eoz) to AISC.

Capital expenditure of R2,197 million (US$133 million) for 2020 was lower than guidance of R3,100 million (US$214 million) at the beginning of the year due to the impact of the COVID-19 lockdown on the operations. The capital underspend in 2020 will be caught up during 2021, including delayed equipment deliveries such as trackless mobile machinery rebuilds for mechanised operations, fire retardant belting and tailing facilities rehabilitation at Marikana operations.

Underpinned by the consistently strong operational performance and significantly higher PGM prices, with the average 4E PGM basket price of R36,651/4Eoz (US$2,227/4Eoz) for 2020, 83% higher than for 2019, profitability from the SA PGM operations was significantly higher. Adjusted EBITDA for 2020 of R29,075 million (US$1,767 million) was 231% higher than adjusted EBITDA of R8,796 million (US$608 million) for 2019, with the average adjusted EBITDA margin increasing from 32% for 2019 to 53% in 2020.

With the production from the SA PGM operations having returned to normalised pre-COVID -19 levels during Q4 2020 and with the PGM basket price continuing to increase during Q1 2021, the operating and financial outlook for 2021 is extremely positive. At spot price 15 February 2021, the SA PGM 4E revenue basket is around R47,300/4Eoz with Rhodium comprising 55%, palladium 23% and platinum 21% respectively of the basket revenue.

H2 2020 Chrome sales of 1,108k tonnes were lower than the 1,286k tonnes in H2 2019. Chrome revenue of R924 million (US$57 million) for H2 2020 was slightly higher than chrome revenue of R903 million (US$61 million) for H2 2019 despite the chrome price reducing from US$143/tonne in H2 2019 to US$140/tonne in H2 2020, as a result of the 11% weakening of the R/US$.

4E PGM production of 918,679 4Eoz for H2 2020 declined by 6% relative to the comparable period in 2019 with AISC 11% higher to R17,586/4Eoz (US$1,082/4Eoz). This was impressive given the controlled and phased production build-up, post the COVID-19 lockdown in Q2 2020. H2 2020 adjusted EBITDA increased by 197% to R20,024 million (US$1,224 million) with Marikana alone generating adjusted EBITDA of R8,901 million (US$544 million), an extraordinary feat given an acquisition price of R4,307 million (US$290 million) in June 2019. Capital expenditure of R1,383 million (US$85 million) for H2 2020 was 18% lower than H2 2019 with ORD 12% lower and sustaining capital 22% lower, due to the phased production build up.

4E PGM production from the Rustenburg operation of 337,392 4Eoz was 5% lower than for H2 2019. Underground production declined by 8% year-on-year to 303,489 4Eoz due to the phased build-up in production post COVID-19. A focus on surface production to offset lower underground production resulted in surface tons milled increasing by 23% to 2.81 million tons with 4E PGM production from surface sources increasing by 39% to 33,903 4Eoz. AISC at the Rustenburg operations increased by 18% year-on-year to R17,939/4Eoz (US$1,103/4Eoz), primarily due to lower production and R614 million (US$38 million) or R1,820/4Eoz (US$111/4Eoz) higher inventories than 2019. In addition there was a R390 million (US$24 million) or R1,156/4Eoz (US$71/4Eoz) increase in royalties due to higher PGM basket revenues.

Kroondal’s performance was solid considering the impact of the COVID-19 pandemic on the operations. Attributable 4E PGM production for H2 2020 of 114,412 4Eoz was 14% lower than for the comparable period in 2019, reflecting the phased production build-up after the COVID-19 lockdown. As a result of the mechanised and less labour intensive nature of underground mining at Kroondal, the operation was less impacted by the COVID-19 lockdown and able to ramp up production quicker than the conventional mines at the Rustenburg and Marikana operations. Kroondal’s AISC of R13,066/4Eoz (US$804/4Eoz) for H2 2020, was 16% higher than the comparable period in 2019, primarily due to lower production volumes as a result of COVID-19 disruptions higher royalties and COVID related costs.

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 8

The integration of the Marikana operation progressed smoothly notwithstanding the COVID-19 interruptions, delivering corporate and operational synergies of approximately R1.83 billion per annum by year end, well above initial transaction estimates of approximately R730 million per annum . 4E PGM production for H2 2020 of 381,838 4Eoz was 11% lower than for H2 2019, primarily due to the phased return to production following the COVID-19 lockdown in Q2 2020, which was achieved by November 2020.

Underground production was 14% lower year-on-year with surface operations granted a priority status during the lockdown period to compensate for reduced underground activity during the build-up. Surface production increased by 23% for H2 2020 relative to H2 2019 to 45,876 4Eoz. AISC of R18,970/4Eoz (US$1,167/4Eoz) was 7% higher than H2 2019 due to lower 4E PGM production. Similar to Rustenburg, higher royalties and inventory costs associated with higher PGM prices were partially offset by 36% and 19% lower sustaining capital and ORD respectively, relative to H2 2019. Marikana’s by-product credit was also R1,483 million (US$91 million) higher than H2 2019 due to toll and purchase of concentrate processing during the initial ACP failure. Marikana paid R583 million (US$36 million) higher royalties or R1,527/4Eoz (US$94/4Eoz) due to higher PGM basket revenues.

Attributable 4E PGM production from Mimosa of 62,417 4Eoz was 10% higher than for H2 2019 due to a mill breakdown during H2 2019. Mimosa has maintained a steady performance albeit with AISC increasing by 19% to US$900/4Eoz (R14,627/4Eoz) due to a 46% increase in sustaining capital.

The K4 and Klipfontein PGM projects

The K4 project is a tier one, low cost, brownfields PGM expansion project at the Marikana operations. The project entails completion of the project, which was significantly advanced by Lonmin with R4.4bn of sunk capex before Lonmin suspended the project due to capital constraints. The K4 project has low execution risk and is expected to be brought into first production within 12 months

The salient points of the K4 project include:

| ● | Steady state production of around 250,000 4Eoz per annum at an average operating cost of around R16,000/4Eoz |

| ● | Approximately 11.5M 4Eoz expected to be produced over a 50 year life of Mine (LoM), mining Merensky and UG2 reefs to a depth of 1,287m |

| ● | Project capital investment of R3.9 billion for infrastructure completion, on and off reef development and a tailings storage facility (TSF). Peak funding R1.67 billion |

| ● | Existing infrastructure: |

| − | Main vertical shaft equipped and functional to 1,332m |

| − | Ventilation shaft equipped and functional to 1,078m |

| − | Functional 130,000 tpm concentrator |

| − | Surface infrastructure such as offices, change houses, refrigeration plants and grout plants |

| − | Underground stations and station crosscuts |

| ● | The project returns a NPV (at a 15% real discount rate) of approximately R3 billion with an IRR of 33% and a six year payback on invested capital at long term assumed project prices of: platinum (US$880/oz), palladium (US$1,600/oz), rhodium (US$5,650/oz) and a R15,0/US$ exchange rate |

| ● | The NPV increases to approximately R21 billion with the IRR increasing to approximately 80% at spot prices on 9 February 2021 of: platinum (US$1,130/oz), palladium (US$2,340/oz), rhodium (US$21,800/oz) and a R15.00/US$ exchange rate |

The Klipfontein project is a small robust open cast PGM opportunity, which will be developed in terms of the existing Pool and Share Agreement (PSA) with Anglo American Platinum at the Kroondal operations.

The salient points of the Klipfontein project include:

| ● | Shallow open pit operation, producing approximately 40,000 4Eoz per annum over a three year LoM, with low average operating cost of around R9,000/4Eoz |

| ● | Mining UG2 reef to a depth of 45m |

| ● | Project capital investment of R66 million |

| ● | Ore will be mined by a contractor and treated at the K2 concentrator |

| ● | The project returns a NPV (15% real discount rate) of R738 million assuming the same project price parameters outlined above, an IRR of 70% and with a payback on invested capital of less than a year |

| ● | At spot metal prices on 9 February 2021 (as detailed above), the NPV increases to R2.1 billion and the IRR to 110% |

| ● | Awaiting S102 approval from the DMRE |

These projects will deliver significant socio-economic benefits to the Rustenburg region, with the K4 project providing approximately 4,380 jobs at steady state and the Klipfontein project approximately 124 jobs. Both projects will create meaningful opportunities for local procurement, skills transfer and the provision of economic benefits to local SMMEs and local communities. The Klipfontein project will sustain the production profile of Kroondal for longer and the K4 project will ensure the sustainability of the Marikana operations for ~50 years.

SA gold operations

Gold production for 2020 from the SA gold operations (including DRDGOLD) increased by 5% to 30,561kg (982,559oz) with production from the managed SA Gold operations (excluding DRDGOLD) of 25,190kg (809,877oz), 3% above the upper end of revised guidance for the year and only 13% below the lower end of initial pre-COVID-19 guidance for 2020. This was primarily due to the operations achieving normalised production levels from the COVID-19 lockdown sooner than expected.

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 9

Total tons milled for 2020 declined by 1% compared to 2019, with the yield increasing by 6% to 0.74g/t driven by an 8% increase in underground yield to 5.22g/t. This was a function of the preferential deployment of returning employees to higher grade areas in order to maximise revenue post lockdown. With underground operations back to full production in November 2020, we expect to see underground yields moderating to long term averages.

AISC for the SA gold operations (including DRD Gold) were well contained for 2020 despite the initial disruptive impact of COVID-19, increased by 4% to 743,967/kg (US$1,406/oz) compared to 2019 (9% lower in USD terms, from US$1,455/oz to US$1,406/oz). This was despite ORD expenditure and sustaining capital increasing by 34% and 88% respectively for 2020 compared with 2019, which was affected by the strike in the first half of the year. Capital spend on ORD and sustaining capital is likely to remain elevated until 2023 due to catch up from the 2019 and 2020 disruptions in order to maintain mining. In addition to the above costs which impacted AISC, royalties for the SA Operations (excluding DRD Gold) and community costs increased by 93% to R142 million and 138% to R135 million respectively.

This solid operational performance together with a 43% higher average gold price received of R924,764/kg (US$1,747/oz) for 2020, resulted in the adjusted EBITDA margin for the SA gold operations increasing to 28% for 2020 compared with a negative 5% adjusted EBITDA margin for 2019 and a significantly higher positive adjusted EBITDA of R7,770 million (US$472 million) compared with an adjusted EBITDA loss of R969 million (US$67 million) for 2019. Approximately 78% of adjusted EBITDA for 2020 was generated in H2 2020 which was a more representative period, suggesting significant upside for 2021.

Production for H2 2020 (including DRDGOLD) declined by 2% year-on-year to 18,007/kg (578,939oz) with production from the managed operations (excluding DRDGOLD) of 15,023kg (483,001oz) 1% lower as a result of the phased build-up post the COVID-19 lockdown. Total gold sold (excluding DRDGOLD) of 14,653kg (471,105oz) was 6% (991kg) lower than for the same period in 2019 with 695kg (2019: 219kg) of unsold gold at the end of the current financial period.

AISC for the SA gold operations (including DRDGOLD) increased by 11% to R704,355/kg (US$1,347/oz), primarily due to lower production and higher royalty and COVID-19 related costs. In addition ORD costs were 4% higher due to an increase in off-reef development as well as sustaining capital, which increased by 38% as a result of overhead cost reduction projects at the Kloof operation gaining momentum.

Capital expenditure for H2 2020 for SA gold Operations (including DRDGOLD) increased by 15% year-on-year to R1,889 million (US$116 million) largely driven by increased capital investment by DRDGOLD where capital expenditure increased by 363% to R202million (US$12million). Capital expenditure at SA gold operations (excluding DRDGOLD) increased by 6% to R1,687million (US104million) with ORD expenditure increasing by 4% year-on-year to R1,101 million (US$68 million) and sustaining capital by 10% to R443million (US$27million).

Underground production from the Driefontein operation increased by 11% to 4,931kg (158,535oz) year-on-year due to improved productivity and efficiencies despite crews being on average at a 20% lower complement than normal. Production from the Driefontein surface operation ceased in 2019, but surface material from the Kloof operations was toll treated at the Driefontein metallurgical plant during 2020. AISC for H2 2020 was 1% higher at R701,129/kg (US$1,341/oz) due to increased gold production offset by significantly higher royalties and community costs. Despite sustaining capital declining by 25% year-on-year, ORD spending increased by 8% year-on-year.

The Kloof operation performed solidly for H2 2020 with gold production increasing by 8% to 6,495kg (208,819oz). Underground production increased by 6% year-on-year to 5,493kg (177,604oz) with tons milled declining by 4% due to the gradual build-up in mining crews post lockdown. This was offset by underground yield increasing by 10% to 5.8g/t. Productivity increased with increased square meters mined despite the crews being on average 12% lower than the same period last year. The increase in grade can be attributed to crews initially being deployed to the highest-grade sections post lockdown following improved access to higher grade panels, which were unavailable in H2 2019 due to a fire and seismic events. Surface production at the Kloof operations increased by 20% to 1,002kg (32,215oz) with tons milled 9% higher for H2 2020 than for H2 2019 due to higher surface volumes being processed as a result of the additional capacity in the plants due to the slower start-up of underground mining and surface throughput from Kloof toll treated at the Driefontein and Ezulwini metallurgical plants. AISC at Kloof for H2 2020 1% higher at R722,845/kg (US$1,383/oz), due to increased gold production offsetting higher royalties and community cost and ORD and sustaining capital increases of 2% and 32% respectively.

Gold production from the Beatrix operation declined by 28% in H2 2020 compared to H2 2019 as a result of the slower start-up post lockdown with a high percentage of workers coming from neighbouring countries and restrictions at border posts. Underground gold production decreased by 31% to 2,799kg (89,990oz) with tons milled declining by 29% and yield declining 2% due to the slow start-up of the higher grade No 4 shaft. Gold production from surface sources increased by 127% to 150kg (4,823oz) as additional milling capacity was available for surface material and the higher gold price reduced the surface material pay limits. Beatrix’s AISC for H2 2020 increased 45% year-on-year to R812,018/kg (US$1,553/oz) largely due to the 31% decrease in gold sold coupled with higher sustaining capital which increased 17% year-on-year and higher royalties and community costs.

No underground material was processed in H2 2020 for the Cooke operations, which amounted to a drop of 16kg (514oz) from the previous period. Surface gold production increased by 2% to 648kg (20,834oz) with tons milled increasing by 20% and offsetting a 16% drop in yield. The volume increase is due to the higher percentage contribution from slimes following the depletion of the larger material on the sand and rock dumps. Care and maintenance cost at Cooke operations increased by 11% year-on-year to R315 million (US$19 million) as a result of the water purification project at Cooke 1 shaft and additional security cost to secure assets.

The Burnstone gold project

The Burnstone project is a low cost, extensively pre-developed gold asset in the Balfour area, Mpumalanga which was previously operated under Great Basin Gold.

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 10

The salient points of the Burnstone project include:

| ● | A relatively shallow underground operation, mining the Kimberley reef to an average depth of approximately 550m below surface |

| ● | Project capital investment of R2.3 billion primarily to complete underground infrastructure and acquire trackless mobile machinery |

| ● | Production of 2.03 Moz gold over a 20 year life |

| ● | The project will ramp up over five years to a steady state production of around 130,000 oz per annum for 10 years with average operating costs of around R420,000/kg |

| ● | Existing infrastructure includes: |

| − | A functional metallurgical facility |

| − | Established TSF |

| − | Equipped and functional vertical shaft and trackless decline |

| − | Surface infrastructure such as offices, workshops, compressors etc. |

| − | Extensive underground development and infrastructure |

| ● | The project NPV (15% real discount rate) is approximately R1.4 billion with an IRR of 24% and a payback of 7 years at an assume gold price of $1,500/oz and exchange rate of R15/US$ |

| ● | The NPV increases to approximately R3.8 billion with the IRR increasing to approximately 39% at spot prices on 9 February 2021 of: gold US$1,840/oz and a R15,0/US$ exchange rate |

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 11

FINANCIAL REVIEW OF THE SIBANYE-STILLWATER GROUP

FOR THE SIX MONTHS ENDED 31 DECEMBER 2020 (H2 2020) COMPARED WITH THE SIX MONTHS ENDED 31 DECEMBER 2019 (H2 2019)

The President of the Republic of South Africa announced a nation-wide lockdown from midnight 26 March 2020, which was amended through a notice published by the South African government on 16 April 2020 allowing for our South African mining operations to be conducted at a reduced capacity of not more than 50%. From 17 April 2020, management commenced implementing its strategy to mobilise the required employee complement to safely ramp up production at our South African operations to the initial restricted 50%. Subsequent directives issued by the Minister of Mineral Resources and Energy and the easing of lockdown restrictions allowed for the controlled ramp up of production under stringent regulations. As a result, significant differences between the periods include the lower production levels at the SA gold and SA PGM operations during H2 2020 while safely mobilising employees and ramping up production. By the end of H2 2020 the SA gold and SA PGM operations successfully reached near pre-COVID-19 production levels.

The reporting currency for the Group is SA rand (rand) and the functional currency of the US PGM operations is US dollar. Direct comparability of the Group results between the two periods is distorted as the results of the US PGM operations are translated to rand at the average exchange rate, which for H2 2020 was R16.26/US$ or 11% weaker than for H2 2019 (R14.69/US$).

The revenue, cost of sales, before amortisation and depreciation, net other cash costs, adjusted EBITDA and amortisation and depreciation are set out in the table below:

| | | |

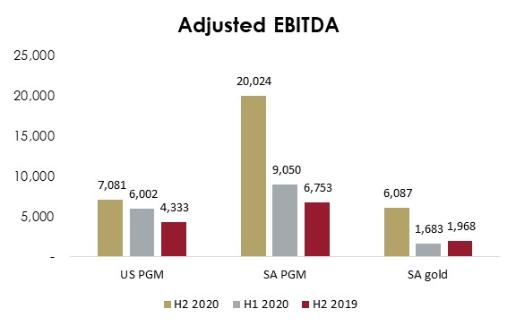

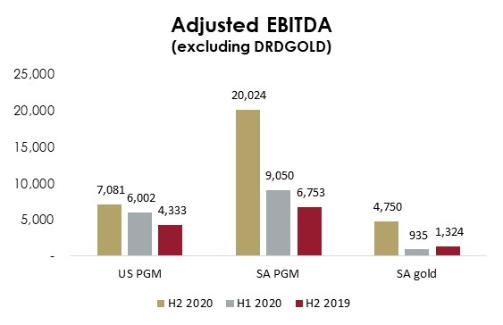

Figures in millions - SA rand | H2 2020 | H2 2019 | % change |

Revenue | 72,374 | 49,391 | 47 |

- US PGM operations | 22,138 | 15,541 | 42 |

- SA PGM operations | 33,477 | 21,340 | 57 |

- SA gold operations, excluding DRDGOLD | 14,103 | 10,515 | 34 |

- DRDGOLD | 2,978 | 2,111 | 41 |

- Group corporate1 | (322) | (116) | (178) |

Cost of sales, before amortisation and depreciation | (38,051) | (35,438) | 7 |

- US PGM operations | (15,038) | (11,236) | 34 |

- SA PGM operations | (12,648) | (14,080) | (10) |

- SA gold operations, excluding DRDGOLD | (8,739) | (8,678) | 1 |

- DRDGOLD | (1,626) | (1,444) | 13 |

Net other cash costs | (1,452) | (1,015) | 43 |

- US PGM operations | (19) | 28 | 168 |

- SA PGM operations | (805) | (507) | 59 |

- SA gold operations, excluding DRDGOLD | (614) | (513) | 20 |

- DRDGOLD | (14) | (23) | (39) |

Adjusted EBITDA | 32,871 | 12,937 | 154 |

- US PGM operations | 7,081 | 4,333 | 63 |

- SA PGM operations | 20,024 | 6,753 | 197 |

- SA gold operations, excluding DRDGOLD | 4,750 | 1,323 | 259 |

- DRDGOLD | 1,338 | 644 | 108 |

- Group corporate1 | (322) | (116) | (178) |

Amortisation and depreciation | (4,149) | (4,289) | (3) |

- US PGM operations | (1,398) | (1,193) | 17 |

- SA PGM operations | (1,168) | (1,202) | (3) |

- SA gold operations, excluding DRDGOLD | (1,488) | (1,810) | (18) |

- DRDGOLD | (95) | (84) | 13 |

| | | |

| 1. | The streaming transaction is not recognised in the Stillwater segment (see note 21 of the condensed consolidated provisional financial statements) |

Revenue

Revenue increased by 47% to R72,374 million (US$4,439 million), mainly due to higher commodity prices partially offset by lower sales volumes at the SA operations.

Revenue from the US PGM operations increased by 28% to US$1,363 million or 42% to R22,138 million in rand terms, due to a 31% increase in the average US dollar 2E basket price, a 1% increase in mined ounces sold and a 11% weaker rand, partially offset by a 19% decrease in recycled ounces. At the SA PGM operations, revenue increased by 57% to R33,477 million (US$2,050 million) due to a 80% higher average rand 4E basket price, partially offset by a 14% or 133,330 4Eoz decrease in PGMs sold. The lower sales volumes at our SA PGM operations in H2 2020 was mainly due to lower production volumes during Q3 2020 whilst ramping up to normal production levels post the COVID-19 lockdown.

Revenue from the SA gold operations excluding DRDGOLD increased by 34% to R14,103 million (US$864 million) mainly due to a 43% higher rand gold price, partially offset by 6% or 31,861oz decrease in gold sold. Revenue from DRDGOLD increased by 41% to R2,978 million (US$183 million) due to a 42% higher rand gold price received.

Cost of sales, before amortisation and depreciation

Cost of sales, before amortisation and depreciation increased by 7% to R38,051 million (US$2,341 million). Cost of sales, before amortisation and depreciation at the US PGM operations increased by 21% to US$927 million (R15,038 million) due to US$131 million (R3,001 million) higher recycling costs and higher royalties paid of approximately US$71/oz, both highly correlated to the increased PGM commodity prices. Cost of sales, before amortisation and depreciation at the SA PGM operations decreased by 10% to R12,648 million (US$778 million) due to a 6% or 61,664 4Eoz decline in production volumes and synergies realised following the integration of the Marikana operation.

Cost of sales, before amortisation and depreciation at the SA gold operations excluding DRDGOLD increased marginally by 1% or R61 million to R8,739 million (US$537 million) due to increased labour costs. Cost of sales, before amortisation and depreciation from DRDGOLD increased by 13% to R1,626 million (US$100 million) due to an increase in tons treated.

Sibanye-Stillwater Operating and financial results | Six months and year ended 31 December 2020 12

Adjusted EBITDA

Adjusted EBITDA includes other cash costs, care and maintenance costs; lease payments; strike costs and corporate social investment costs (CSI) (refer note 11.2 of the condensed consolidated provisional financial statements for a reconciliation of profit/(loss) before royalties and tax to adjusted EBITDA) . Care and maintenance costs for H2 2020 were R315 million (US$19 million) at Cooke (H2 2019: R283 million (US$19 million)); R56 million (US$3 million) at Marikana (H2 2019: R168 million (US$12 million)) and R41 million (US$3 million) at Burnstone (H2 2019: R10 million (US$1 million)). Lease payments of R75 million (US$5 million) (H2 2019: R81 million (US$6 million)) are included in line with the debt covenant formula. CSI costs were R165 million (US$10 million) (H2 2019: R91 million (US$6 million)) and for H2 2020 there were insignificant strike related costs (H2 2019: R27 million (US$2 million).

The adjusted EBITDA for all operations increased significantly due to higher average commodity prices achieved during H2 2020.

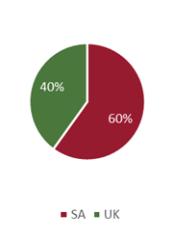

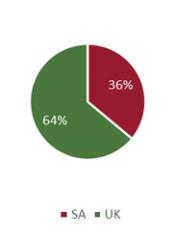

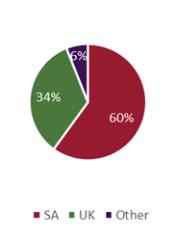

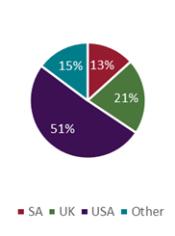

Adjusted EBITDA is shown in the graphs below:

Amortisation and depreciation

Amortisation and depreciation decreased by 3% to R4,149 million (US$255 million). Amortisation and depreciation at the US PGM operations increased by 6% in US dollar terms to US$86 million due to more capital items being placed into service and at the SA PGM operations decreased by 3% to R1,168 million (US$72 million) due to a decrease in production. Amortisation and depreciation at the SA gold operations excluding DRDGOLD decreased by 18% to R1,488 million (US$91 million) mainly due to a 1% decrease in production and the deferral of capital expenditure from H1 2020. Amortisation and depreciation at DRDGOLD increased by 13% to R95 million (US$6 million) due to increased capital expenditure during H2 2020 at the Far West Gold Recoveries tailings retreatment operation.

Finance expense

Finance expense decreased by R289 million (US$29 million) mainly due to a decrease in interest on borrowings of R227 million (US$14 million), decrease in the unwinding of amortised cost on borrowings of R17 million (US$1 million), decrease in the unwinding of the finance costs on the deferred revenue transactions of R33 million (US$2 million), decrease in interest on the occupational healthcare obligation of R13 million (US$1 million), decrease in the other interest of R14 million (US$1 million) and partly offset by an increase in the unwinding of the environmental rehabilitation obligation of R15 million (US$1 million). Refer to note 3 of the condensed consolidated provisional financial statements for a breakdown of finance expenses.

Sibanye-Stillwater’s outstanding gross debt at the end of H2 2020 was 23% lower at R18,383 million (US$1,251 million). The lower outstanding debt was mainly due to the settlement of the US$ convertible bond, a R2,500 million net repayment on the R5.5 billion RCF, partially offset by an increase of R1,266 million on the US$600 million RCF.

Loss on financial instruments