EXHIBIT 99.2

4Q24 Earnings Presentation

2 Important Disclosure IN REVIEWING THE INFORMATION CONTAINED IN THIS PRESENTATION, YOU ARE AGREEING TO ABIDE BY THE TERMS OF THIS DISCLAIMER . THIS INFORMATION IS BEING MADE AVAILABLE TO EACH RECIPIENT SOLELY FOR ITS INFORMATION AND IS SUBJECT TO AMENDMENT . This presentation is prepared by XP Inc . (the “Company,” “we” or “our”), is solely for informational purposes . This presentation does not constitute a prospectus and does not constitute an offer to sell or the solicitation of an offer to buy any securities . In addition, this document and any materials distributed in connection with this presentation are not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction . This presentation was prepared by the Company . Neither the Company nor any of its affiliates, officers, employees or agents, make any representation or warranty, express or implied, in relation to the fairness, reasonableness, adequacy, accuracy or completeness of the information, statements or opinions, whichever their source, contained in this presentation or any oral information provided in connection herewith, or any data it generates and accept no responsibility, obligation or liability (whether direct or indirect, in contract, tort or otherwise) in relation to any of such information . The information and opinions contained in this presentation are provided as at the date of this presentation, are subject to change without notice and do not purport to contain all information that may be required to evaluate the Company . The information in this presentation is in draft form and has not been independently verified . The Company and its affiliates, officers, employees and agents expressly disclaim any and all liability which may be based on this presentation and any errors therein or omissions therefrom . Neither the Company nor any of its affiliates, officers, employees or agents makes any representation or warranty, express or implied, as to the achievement or reasonableness of future projections, management targets, estimates, prospects or returns, if any . The information contained in this presentation does not purport to be comprehensive and has not been subject to any independent audit or review . Certain of the financial information as of and for the periods ended December 31 , 2019 , 2018 and 2017 has been derived from audited financial statements and all other financial information has been derived from unaudited interim financial statements . A significant portion of the information contained in this presentation is based on estimates or expectations of the Company, and there can be no assurance that these estimates or expectations are or will prove to be accurate . The Company’s internal estimates have not been verified by an external expert, and the Company cannot guarantee that a third party using different methods to assemble, analyze or compute market information and data would obtain or generate the same results . Statements in the presentation, including those regarding the possible or assumed future or other performance of the Company or its industry or other trend projections, constitute forward - looking statements . These statements are generally identified by the use of words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “estimate” and “potential,” among others . By their nature, forward - looking statements are necessarily subject to a high degree of uncertainty and involve known and unknown risks, uncertainties, assumptions and other factors because they relate to events and depend on circumstances that will occur in the future whether or not outside the control of the Company . Such factors may cause actual results, performance or developments to differ materially from those expressed or implied by such forward - looking statements and there can be no assurance that such forward - looking statements will prove to be correct . These risks and uncertainties include factors relating to : ( 1 ) general economic, financial, political, demographic and business conditions in Brazil, as well as any other countries we may serve in the future and their impact on our business ; ( 2 ) fluctuations in interest, inflation and exchange rates in Brazil and any other countries we may serve in the future ; ( 3 ) competition in the financial services industry ; ( 4 ) our ability to implement our business strategy ; ( 5 ) our ability to adapt to the rapid pace of technological changes in the financial services industry ; ( 6 ) the reliability, performance, functionality and quality of our products and services and the investment performance of investment funds managed by third parties or by our asset managers ; ( 7 ) the availability of government authorizations on terms and conditions and within periods acceptable to us ; ( 8 ) our ability to continue attracting and retaining new appropriately - skilled employees ; ( 9 ) our capitalization and level of indebtedness ; ( 10 ) the interests of our controlling shareholders ; ( 11 ) changes in government regulations applicable to the financial services industry in Brazil and elsewhere ; ( 12 ) our ability to compete and conduct our business in the future ; ( 13 ) the success of operating initiatives, including advertising and promotional efforts and new product, service and concept development by us and our competitors ; ( 14 ) changes in consumer demands regarding financial products, customer experience related to investments and technological advances, and our ability to innovate to respond to such changes ; ( 15 ) changes in labor, distribution and other operating costs ; ( 16 ) our compliance with, and changes to, government laws, regulations and tax matters that currently apply to us ; ( 17 ) the negative impacts of the COVID - 19 pandemic on global, regional and national economies and the related market volatility and protracted economic downturn ; and ( 18 ) other factors that may affect our financial condition, liquidity and results of operations . Accordingly, you should not place undue reliance on forward - looking statements . The forward - looking statements included herein speak only as at the date of this presentation and the Company does not undertake any obligation to update these forward - looking statements . Past performance does not guarantee or predict future performance . Moreover, the Company and its affiliates, officers, employees and agents do not undertake any obligation to review, update or confirm expectations or estimates or to release any revisions to any forward - looking statements to reflect events that occur or circumstances that arise in relation to the content of the presentation . You are cautioned not to unduly rely on such forward - looking statements when evaluating the information presented and we do not intend to update any of these forward - looking statements . Market data and industry information used throughout this presentation are based on management’s knowledge of the industry and the good faith estimates of management . The Company also relied, to the extent available, upon management’s review of industry surveys and publications and other publicly available information prepared by a number of third party sources . All of the market data and industry information used in this presentation involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates . Although the Company believes that these sources are reliable, there can be no assurance as to the accuracy or completeness of this information, and the Company has not independently verified this information . The contents hereof should not be construed as investment, legal, tax or other advice and you should consult your own advisers as to legal, business, tax and other related matters concerning an investment in the Company . The Company is not acting on your behalf and does not regard you as a customer or a client . It will not be responsible to you for providing protections afforded to clients or for advising you on the relevant transaction . This presentation also includes certain non - GAAP financial information . We believe that such information is meaningful and useful in understanding the activities and business metrics of the Company’s operations . We also believe that these non - GAAP financial measures reflect an additional way of viewing aspects of the Company’s business that, when viewed with our International Financial Reporting Standards (“IFRS”) results, as issued by the International Accounting Standards Board, provide a more complete understanding of factors and trends affecting the Company’s business . Further, investors regularly rely on non - GAAP financial measures to assess operating performance and such measures may highlight trends in the Company’s business that may not otherwise be apparent when relying on financial measures calculated in accordance with IFRS . We also believe that certain non - GAAP financial measures are frequently used by securities analysts, investors and other interested parties in the evaluation of public companies in the Company’s industry, many of which present these measures when reporting their results . The non - GAAP financial information is presented for informational purposes and to enhance understanding of the IFRS financial statements . The non - GAAP measures should be considered in addition to results prepared in accordance with IFRS, but not as a substitute for, or superior to, IFRS results . As other companies may determine or calculate this non - GAAP financial information differently, the usefulness of these measures for comparative purposes is limited . A reconciliation of such non - GAAP financial measures to the nearest GAAP measure is included in this presentation . For purposes of this presentation : “Active Clients” means the total number of retail clients served through our XP Investimentos, Rico, Clear, XP Investments and XP Private (Europe) brands, with Client Assets above R $ 100 . 00 or that have transacted at least once in the last thirty days . For purposes of calculating this metric, if a client holds an account in more than one of the aforementioned entities, such client will be counted as one “active client” for each such account . For example, if a client holds an account in each of XP Investimentos and Rico, such client will count as two “active clients” for purposes of this metric . “Client Assets” means the market value of all client assets invested through XP’s platform, including equities, fixed income securities, mutual funds (including those managed by XP Gestão de Recursos Ltda . , XP Advisory Gestão Recursos Ltda . and XP Vista Asset Management Ltda . , as well as by third - party asset managers), pension funds (including those from XP Vida e Previdência S . A . , as well as by third - party insurance companies), exchange traded funds, COEs (Structured Notes), REITs, and uninvested cash balances (Floating Balances), among others .

Index 4Q24 Financials and Main KPIs 02 Final Remarks 03 01 Key Highlights Q&A 04 Appendix 05

01. Key Highlights

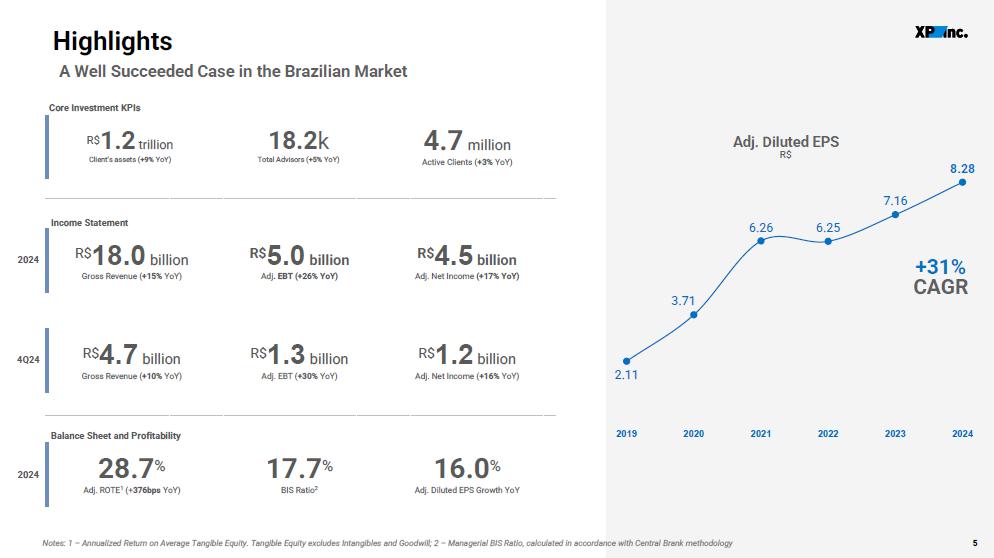

5 Highlights Notes: 1 – Annualized Return on Average Tangible Equity. Tangible Equity excludes Intangibles and Goodwill; 2 – Managerial BIS Ratio, c alculated in accordance with Central Brank methodology A Well Succeeded Case in the Brazilian Market 2.11 3.71 6.26 6.25 7.16 8.28 2019 2020 2021 2022 2023 2024 Adj. Diluted EPS R$ R$ 1.2 trillion Client’s assets ( + 9 % YoY) Core Investment KPIs 1 8 .2 k Total Advisors ( +5% YoY) 4.7 million Active Clients ( +3% YoY) 28.7 % Adj. ROTE 1 (+ 376bps YoY) 17.7 % BIS Ratio 2 16.0 % Adj. Diluted EPS Growth YoY Balance Sheet and Profitability R$ 18.0 billion Gross Revenue ( +15% YoY) R$ 5.0 billion Adj . EBT (+26% YoY) R$ 4.5 billion Adj. Net Income (+1 7 % YoY) Income Statement 2024 R$ 4.7 billion Gross Revenue ( +10% YoY) R$ 1.3 billion Adj. EBT ( +30% YoY) R$ 1.2 billion Adj. Net Income ( +16% YoY) 4Q24 +31% CAGR 2024

6 Strategy Tracker 2024 Current Status CAGR vs. 3Q23 LTM CAGR Guidance 2026 1 R$bn 18.0 a 17% 14% - 20% Gross Revenue 14.2 a 13% 11% - 15% Investments 2.6 a 32% 26% - 35% New Verticals 1.3 a 50% 28% - 47% Corporate & SMB 29% 283 bps 30% - 34% EBT Margin 14.8 18.0 3Q23 LTM @ ID 2024 2026 Guidance 26.8 Gross Revenue R$ Billion EBT Margin 30% - 34% 29% 26% 12% CAGR 22% CAGR 22.8 17% CAGR On Track to Deliver 2026 Guidance

7 Strategy Tracker Retail Investments Leadership in Core Business Our main goal is to achieve leadership in the investment market, our core business. To do this, we need to maintain and expand our differentials and continue to grow in all customer segments . Retail Cross - Sell Grow with Our Clients’ Needs Starting from our clients’ needs, we will expand our offer to serve their complete financial needs , aiming to break the link of investors with the incumbent banks once and for all. Corporate & SMB Premier Service with Unique Value We want to fully explore the synergy of a Wholesale Bank offer with the investment universe, deepening our relationship with the main economic groups in Brazil.' Quality Financial planning at scale, a new competitive advantage that enhances both the engagement and experience of our investor cli ent s. ]

8 Retail Investments – Consistent Net New Money Notes: 1 – Excluding Inorganic Net New Money from Modal’s acquisition in 3Q23. Net New Money (1) R$ Billion Serving Clients Wherever and However They Want 12 25 20 7 6 6 4Q23 3Q24 4Q24 19 31 25 +37% 60 81 10 22 2023 2024 71 103 +45% Ability To Grow In Our Core Business Retail Corporate Retail Strategy – Keeping Our Moats Expanding and Protecting our Core Business Multi - Channel Distribution and Expansion Through Internal Advisors and RIAs 2 Product Platform Best Investment Options – from Fixed - Income to Alternative Investments 1 Segmentation with Accurate Value Proposition Competitive Pricing, Services and Product Range to each client segment 3 Value - Added Services Through Large - Scale Financial Planning 4

9 Retail Investments Strategy Multi - Channel Distribution and Expansion Through Internal Advisors and RIAs 2 Product Platform Best Investment Options 1 Segmentation with Accurate Value Proposition Competitive Pricing, Services and Product Range 3 Value - Added Services Through Large - Scale Financial Planning 4 Largest Maket Maker in All Fixed Income Instruments Innovative Structuring & Technology Market Share in Secondary Markets Market Leadership Bank Notes, Corporate Credit and Sovereign Bonds Diverse Product Offering Over 18k Investment Specialists Robust Distribution Network 181 266 334 387 -5,000 0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 0 50 100 150 200 250 300 350 400 4Q20 4Q21 4Q22 4Q23 4Q24 106 …While Keeping a Consistent Traded Volume to Client Assets Ratio Through the Years Growing Fixed Income Client Assets… Product Innovation Diversification Beyond Equities Retail Fixed Income Platform Evolution Activity Reached a New Structural Level Fixed Income Client Assets (R$bn) Daily Avg Fixed Income Trades (Fixed Income DATs) Retail Fixed Income Traded Volume as a % of Total Fixed Income Client Assets Fixed Income Powerhouse Distribution and Technology Capabilities ~ 40 thousand A vg Daily Fixed Income Trades in our Secondary Market Platform 38% CAGR since 2020 Liquidity Provider To Illiquid Bank Notes Secondary Market Platform Most Active Platform in the Market

10 Retail Investments Strategy Multi - Channel Distribution and Expansion Through Internal Advisors and RIAs 2 Product Platform Best Investment Options 1 Segmentation with Accurate Value Proposition Competitive Pricing, Services and Product Range 3 Value - Added Services Through Large - Scale Financial Planning 4 Proprietary Tools XP HUB XP CRM Data & Intelligence Daily Preparation & Review Relationship Management & Execution ▪ Performance reports ▪ Client satisfaction tracking ▪ Educational content ▪ A.I. portfolio recommendations ▪ Client task management ▪ Prospect dashboard ▪ Client portfolio reports ▪ Portfolio simulation & performance forecasting Way of Work & Service Model Expansion & Diversification Service Model 11x increase in average number of daily Activities performed by Advisors & Adherence to Tasks is now an important KPI for Advisor’s Compensation 2024 IFAs Wealth Managers RIAs B2C B2B Internal Advisors Self - Directed Private New New New 2020 IFAs Self - Directed Private New Distribution Channels Represented ~60% of Net New Money in 2024

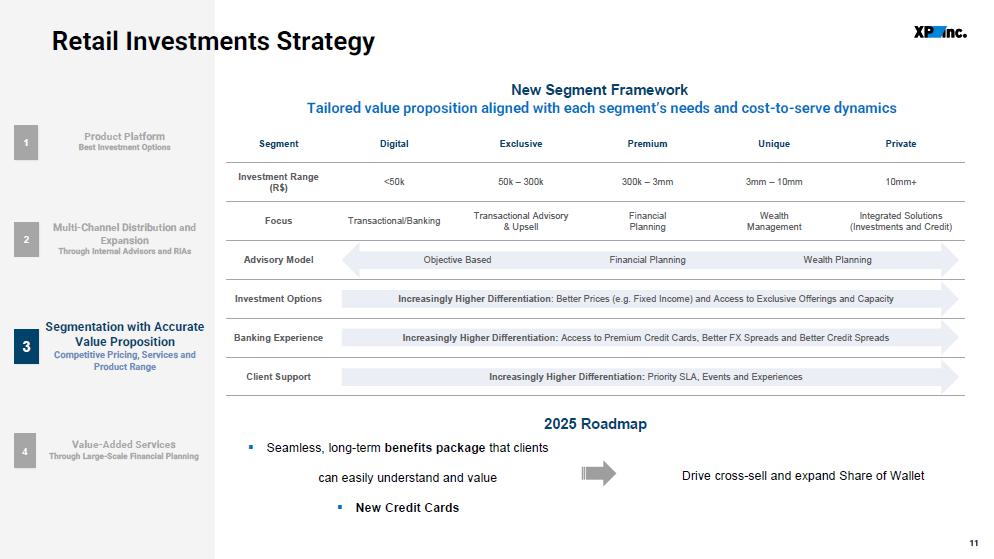

11 Private Unique Premium Exclusive Digital Segment 10mm+ 3mm – 10mm 300k – 3mm 50k – 300k <50k Investment Range (R$) Integrated Solutions (Investments and Credit) Wealth Management Financial Planning Transactional Advisory & Upsell Transactional/Banking Focus Wealth Planning Financial Planning Objective Based Advisory Model Investment Options Banking Experience Client Support Retail Investments Strategy Multi - Channel Distribution and Expansion Through Internal Advisors and RIAs 2 Product Platform Best Investment Options 1 Segmentation with Accurate Value Proposition Competitive Pricing, Services and Product Range 3 Value - Added Services Through Large - Scale Financial Planning 4 New Segment Framework Tailored value proposition aligned with each segment’s needs and cost - to - serve dynamics ▪ Seamless, long - term benefits package that clients can easily understand and value ▪ New Credit Cards 2025 Roadmap Drive cross - sell and expand Share of Wallet Increasingly Higher Differentiation : Better Prices (e.g. Fixed Income) and Access to Exclusive Offerings and Capacity Increasingly Higher Differentiation: Access to Premium Credit Cards, Better FX Spreads and Better Credit Spreads Increasingly Higher Differentiation: Priority SLA, Events and Experiences

12 Retail Investments Strategy Multi - Channel Distribution and Expansion Through Internal Advisors and RIAs 2 Product Platform Best Investment Options 1 Segmentation with Accurate Value Proposition Competitive Pricing, Services and Product Range 3 Value - Added Services Through Large - Scale Financial Planning 4 XP is the Only Player Providing Financial Planning at Scale Insurance 2x higher conversion Retirement Plans from 30% to 41% conversion Net New Money 43% higher Strong Early Indicators for clients with Financial Planning

13 Strategy Tracker Retail Investments Leadership in Core Business Our main goal is to achieve leadership in the investment market, our core business. To do this, we need to maintain and expand our differentials and continue to grow in all customer segments . Retail Cross - Sell Grow with Our Clients’ Needs Starting from our clients’ needs, we will expand our offer to serve their complete financial needs , aiming to break the link of investors with the incumbent banks once and for all. Corporate & SMB Premier Service with Unique Value We want to fully explore the synergy of a Wholesale Bank offer with the investment universe, deepening our relationship with the main economic groups in Brazil.' Quality Financial planning at scale, a new competitive advantage that enhances both the engagement and experience of our investor cli ent s.

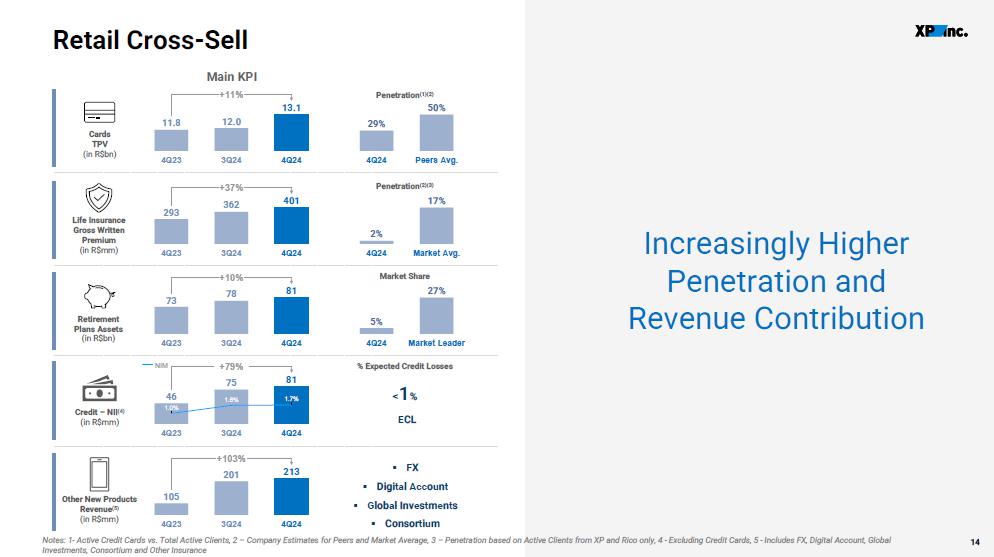

14 Retail Cross - Sell Notes: 1 - Active Credit Cards vs. Total Active Clients, 2 – Company Estimates for Peers and Market Average, 3 – Penetration base d on Active Clients from XP and Rico only, 4 - Excluding Credit Cards, 5 - Includes FX, Digital Account, Global Investments, Consortium and Other Insurance Penetration (2)(3) Cards TPV (in R$bn ) Main KPI 11.8 12.0 13.1 4Q23 3Q24 4Q24 +11% 4Q24 Peers Avg. 29% 50% 293 362 401 4Q23 3Q24 4Q24 +37% 4Q24 Market Avg. 2% 17% 73 78 81 4Q23 3Q24 4Q24 +10% 4Q24 Market Leader 5% 27% 46 75 81 0 2 4 0 50 100 1.0% 4Q23 1.6% 3Q24 1.7% 4Q24 +79% Other New Products Revenue (5) (in R$mm ) 105 201 213 4Q23 3Q24 4Q24 +103% Life Insurance Gross Written Premium (in R$mm ) Retirement Plans Assets (in R$bn ) Credit – NII (4) (in R$mm ) ▪ FX ▪ Digital Account ▪ Global Investments ▪ Consortium Market Share Penetration (1)(2) % Expected Credit Losses NIM < 1 % ECL Increasingly Higher Penetration and Revenue Contribution

15 Quality Financial planning at scale, a new competitive advantage that enhances both the engagement and experience of our investor cli ent s. Strategy Tracker Retail Investments Leadership in Core Business Our main goal is to achieve leadership in the investment market, our core business. To do this, we need to maintain and expand our differentials and continue to grow in all customer segments . Retail Cross - Sell Grow with Our Clients’ Needs Starting from our clients’ needs, we will expand our offer to serve their complete financial needs , aiming to break the link of investors with the incumbent banks once and for all. Corporate & SMB Premier Service with Unique Value We want to fully explore the synergy of a Wholesale Bank offer with the investment universe, deepening our relationship with the main economic groups in Brazil.

16 Wholesale 3,153 3,662 2023 2024 Institutional, Corporate and Issuer Services Gross Revenue R$ Million +16% YoY Investment Banking DCM Volume 1 (in R$bn ) Main KPI 7.1 8.6 9.3 4Q23 3Q24 4Q24 +31% 2024 Market Leader 13% 23% 488 481 3Q24 4Q24 - 1% 4Q24 Market Leader 16% 18% 16 23 32 4Q23 3Q24 4Q24 +104% Institutional Broker Dealer – Traded Volume 2 (in R$bn ) Corporate Securities (in R$bn ) OTC Derivatives Ranking 3 FX Ranking 4 15 th 41 st 2020 4Q24 10 th 2022 4 th 4Q24 Market Share 1 st in CRA and FII 3 rd in DCM Market Share ▪ Interest Rate Swaps #1 4Q24 Market Leader 8% 16% 4Q24 Market Leader 1% 13% Market Share Market Share 1 st Corporate Credit Broker in Brazil Note 1 - Source: Anbima, Distribuição de RF & Híbridos ; 2 – Source: Bloomberg; 3 – Source: B3; 4 – Source: Central Bank, considers primary activity only

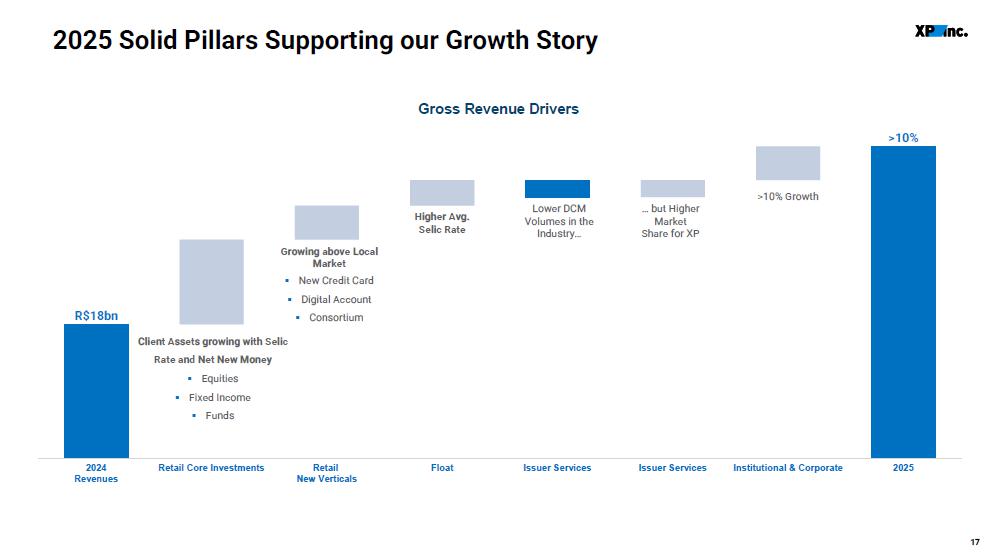

17 2025 Solid Pillars Supporting our Growth Story 2024 Revenues Retail Core Investments Retail New Verticals Float Issuer Services Issuer Services Institutional & Corporate 2025 R$ 18 bn >10% Client Assets growing with Selic Rate and Net New Money ▪ Equities ▪ Fixed Income ▪ Funds Growing above Local Market ▪ New Credit Card ▪ Digital Account ▪ Consortium Higher Avg. Selic Rate Lower DCM Volumes in the Industry… … but Higher Market Share for XP >10% Growth Gross Revenue Drivers

02. 4 Q24 Financials

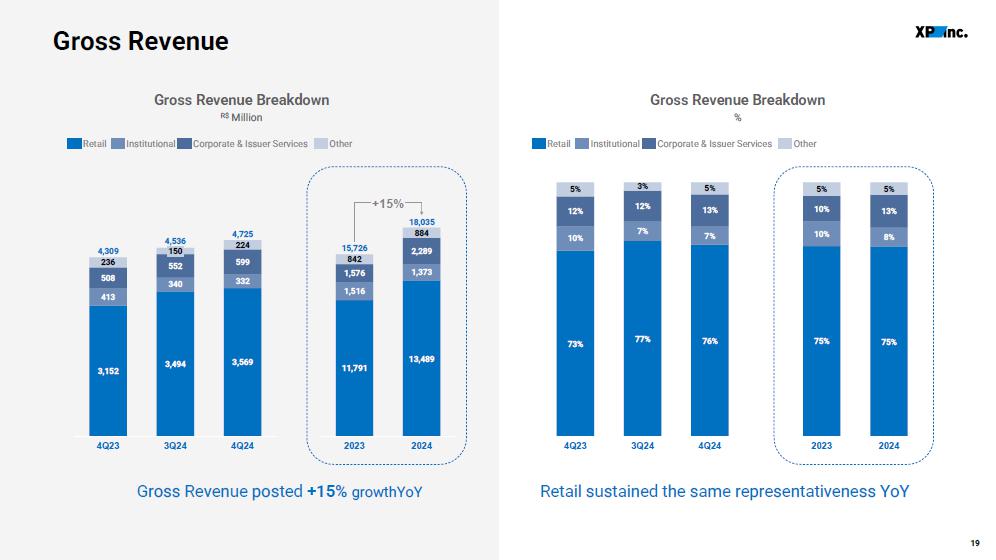

19 Gross Revenue 3,152 3,494 3,569 413 340 332 508 552 599 236 224 4Q23 150 3Q24 4Q24 4,309 4,536 4,725 Retail Institutional Corporate & Issuer Services Other 73% 77% 76% 10% 7% 7% 12% 12% 13% 5% 3% 5% 4Q23 3Q24 4Q24 Retail Institutional Corporate & Issuer Services Other Gross Revenue posted +15% growthYoY Retail sustained the same representativeness YoY 11,791 13,489 1,516 1,373 1,576 2,289 842 884 2023 2024 15,726 18,035 +15% 75% 75% 10% 8% 10% 13% 5% 5% 2023 2024 Gross Revenue Breakdown R$ Million Gross Revenue Breakdown %

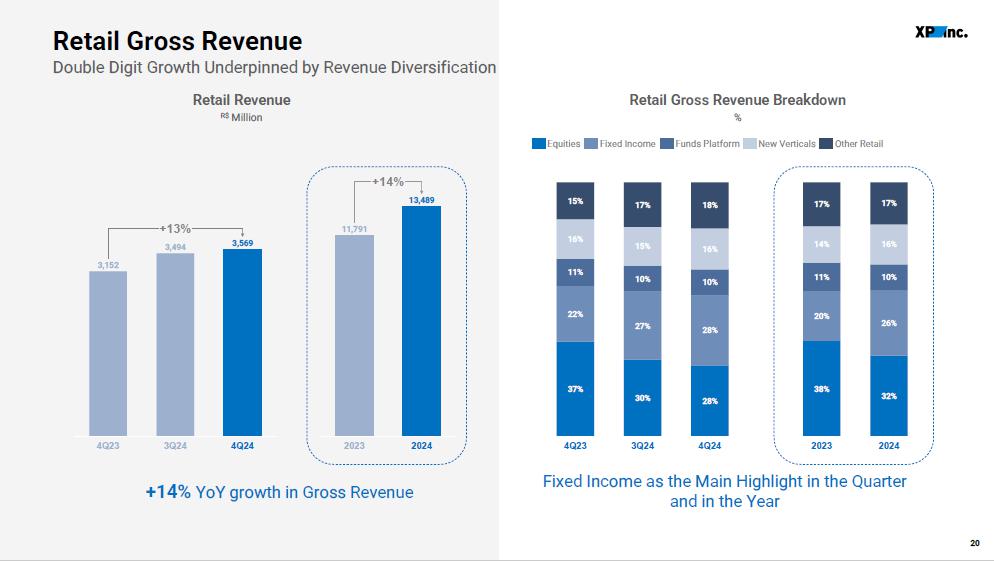

20 Retail Gross Revenue Double Digit Growth Underpinned by Revenue Diversification 3,152 3,494 3,569 4Q23 3Q24 4Q24 +13% 37% 30% 28% 22% 27% 28% 11% 10% 10% 16% 15% 16% 15% 17% 18% 4Q23 3Q24 4Q24 Equities Fixed Income Funds Platform New Verticals Other Retail +14% YoY growth in Gross Revenue Fixed Income as the Main Highlight in the Quarter and in the Year 11,791 13,489 2023 2024 +14% 38% 32% 20% 26% 11% 10% 14% 16% 17% 17% 2023 2024 Retail Revenue R$ Million Retail Gross Revenue Breakdown %

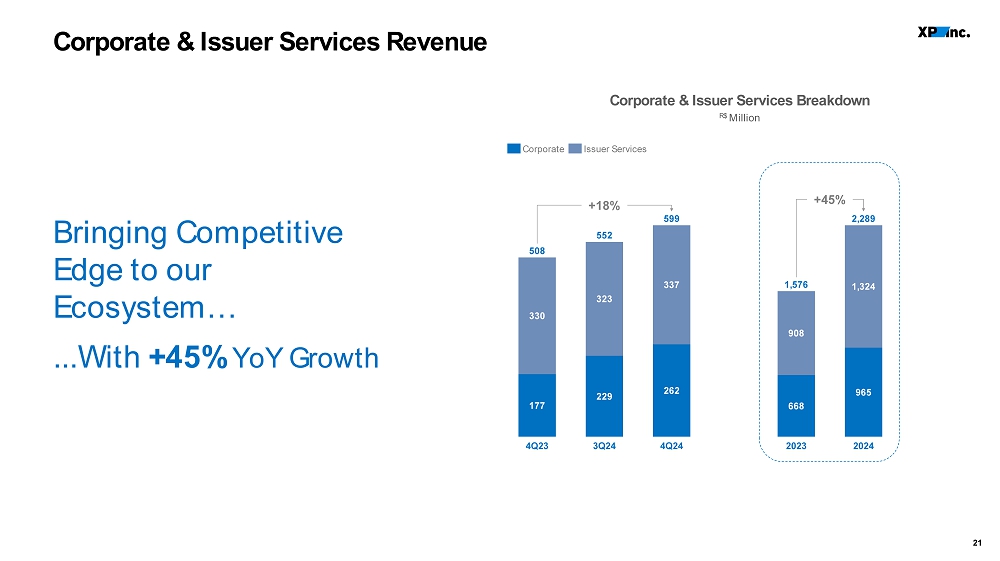

21 Corporate & Issuer Services Revenue Bringing Competitive Edge to our Ecosystem… ...With +45% YoY Growth 177 229 262 330 323 337 4Q23 3Q24 4Q24 508 552 599 +18% Corporate Issuer Services 668 965 908 1,324 2023 2024 1,576 2,289 +45% Corporate & Issuer Services Breakdown R$ Million

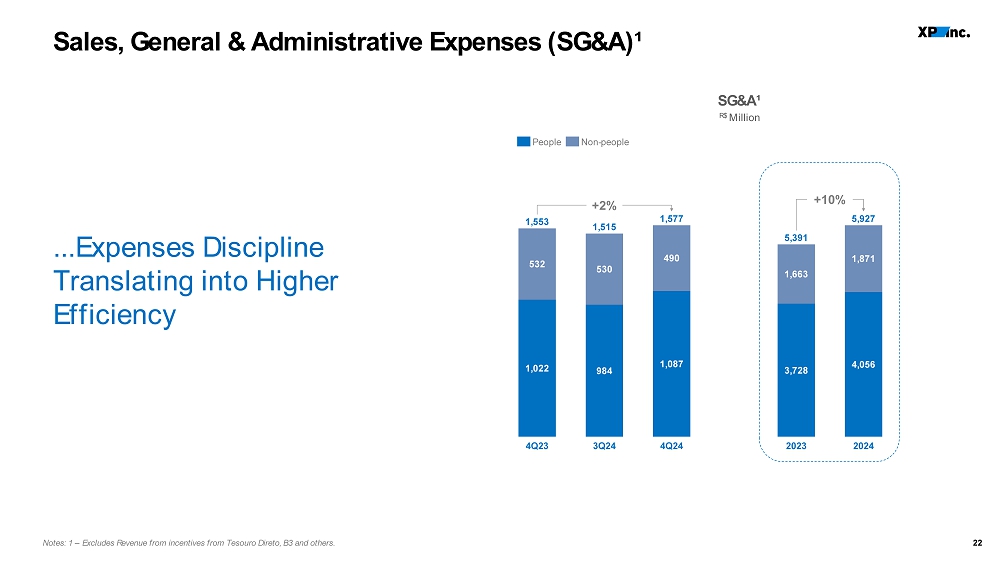

22 1,022 984 1,087 532 530 490 4Q23 3Q24 4Q24 1,553 1,515 1,577 +2% Sales, General & Administrative Expenses (SG&A)¹ Notes: 1 – Excludes Revenue from incentives from Tesouro Direto , B3 and others. People Non - people ...Expenses Discipline Translating into Higher Efficiency 3,728 4,056 1,663 1,871 2023 2024 5,391 5,927 +10% SG&A¹ R$ Million

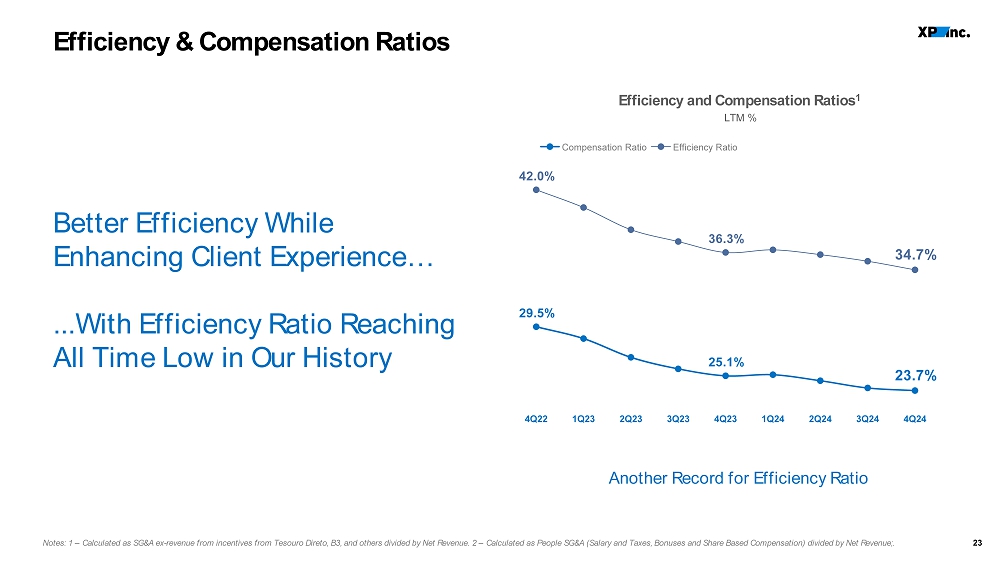

23 Efficiency and Compensation Ratios 1 LTM % Efficiency & Compensation Ratios Notes: 1 – Calculated as SG&A ex - revenue from incentives from Tesouro Direto , B3, and others divided by Net Revenue. 2 – Calculated as People SG&A (Salary and Taxes, Bonuses and Share Based Compensation) divided by Net Revenue;. 29.5% 25.1% 23.7% 42.0% 36.3% 34.7% 4Q22 1Q23 2Q23 3Q23 4Q23 1Q24 2Q24 3Q24 4Q24 Another Record for Efficiency Ratio Compensation Ratio Efficiency Ratio Better Efficiency While Enhancing Client Experience… ...With Efficiency Ratio Reaching All Time Low in Our History

24 EBT 1 R$ Million 1 - Please refer to the Non - GAAP Reconciliation in the appendix. C onsiders the adjustment in Net Revenue of +R$47mm and SG&A of - R$59mm. Our Strategy Resulted an Unprecedented Performance… Margin EBT Expanded +260bps During the Year Earning Before Taxes (EBT) 995 1,212 1,289 0 5 10 15 20 25 30 35 40 45 400 500 600 700 800 900 1,000 1,100 1,200 1,300 24.6% 4Q23 28.1% 3Q24 28.7% 4Q24 30% EBT Margin 3,936 4,974 0 5 10 15 20 25 30 35 40 45 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 26.5% 2023 29.1% 2024 +26%

25 1 – Please refer to the Non - GAAP Reconciliation in the appendix All Time High Results in the Quarter… … With 17% Growth in the Year Adjusted Net Income 1,040 1,187 1,210 0 5 10 15 20 25 30 35 40 45 0 200 400 600 800 1,000 1,200 1,400 25.7% 4Q23 27.5% 3Q24 27.0% 4Q24 16% Adjusted Net Margin 3,899 4,544 0 5 10 15 20 25 30 35 40 45 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 26.2% 2023 26.4% 2024 +17% Adjusted Net Income 1 R$ Million

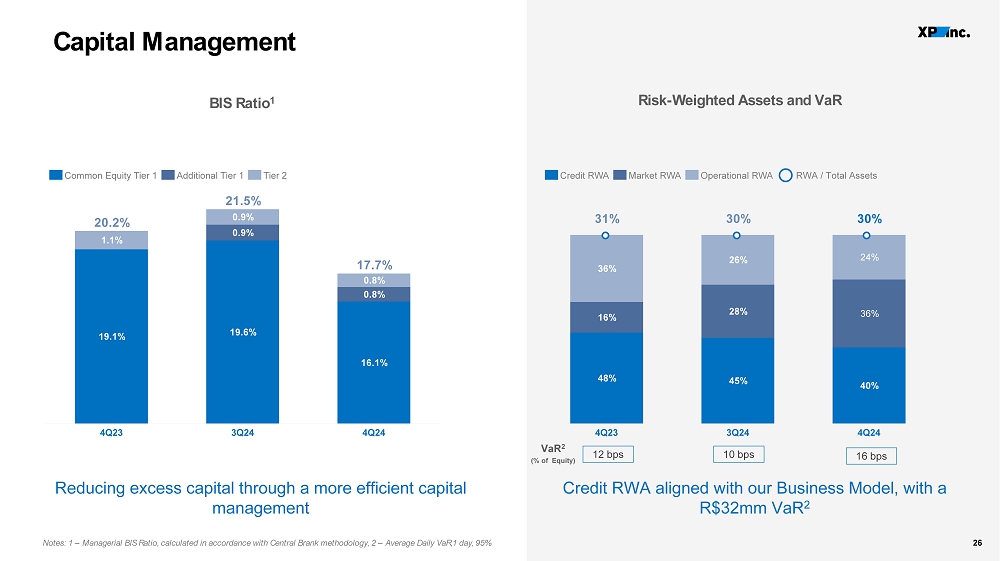

26 RWA / Total Assets 31% 30% 30% 19.1% 19.6% 16.1% 1.1% 0.9% 0.8% 0.9% 0.8% 4Q23 3Q24 4Q24 20.2% 21.5% 17.7% Credit RWA aligned with our Business Model, with a R$32mm VaR 2 Risk - Weighted Assets and VaR Capital Management Notes: 1 – Managerial BIS Ratio, calculated in accordance with Central Brank methodology, 2 – Average Daily VaR,1 day, 95% BIS Ratio 1 48% 45% 40% 16% 28% 36% 36% 26% 24% 4Q23 3Q24 4Q24 Reducing excess capital through a more efficient capital management Common Equity Tier 1 Additional Tier 1 Tier 2 Credit RWA Market RWA Operational RWA VaR 2 (% of Equity) 12 bps 10 bps 16 bps

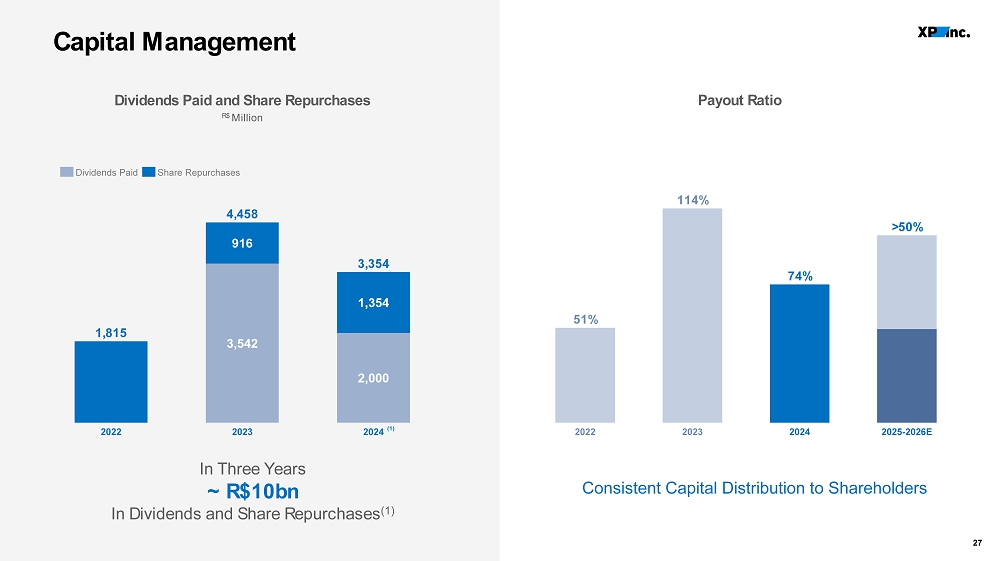

27 Consistent Capital Distribution to Shareholders Payout Ratio 1,815 3,542 2,000 916 1,354 2022 2023 2024 4,458 3,354 Capital Management In Three Years ~ R$10bn In Dividends and Share Repurchases (1) Dividends Paid Share Repurchases Dividends Paid and Share Repurchases R$ Million 2022 2023 2024 2025 - 2026E 51% 114% 74% >50% (1)

28 25.0% 28.7% 21.4% 23.0% 2023 2024 25.6% 28.4% 29.2% 21.1% 23.0% 23.4% 4Q23 3Q24 4Q24 3,899 4,543 8.28 0 1 2 3 4 5 6 7 8 9 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 7.16 2023 2024 Adjusted Annualized ROTE¹ and ROAE² % EPS and Return on Tangible Equity Notes: 1 – Annualized Return on Average Tangible Equity. Tangible Equity excludes Intangibles and Goodwill; 2 – Annualized Retur n on Average Equity; 3 – Net Income Attributable to Owners of Parent Company. 4 – Calculated based on Adjusted Net Income ROTE ROAE Adjusted EPS 4 ROTE of 29.2%, driven by 17% YoY growth in Net Income and a R$2 billion dividend in 4Q24 1,042 1,186 1,210 1.88 2.18 2.23 0.0 0.5 1.0 1.5 2.0 2.5 0 200 400 600 800 1,000 1,200 1,400 1,600 4Q23 3Q24 4Q24 Net Income Diluted EPS (R$)

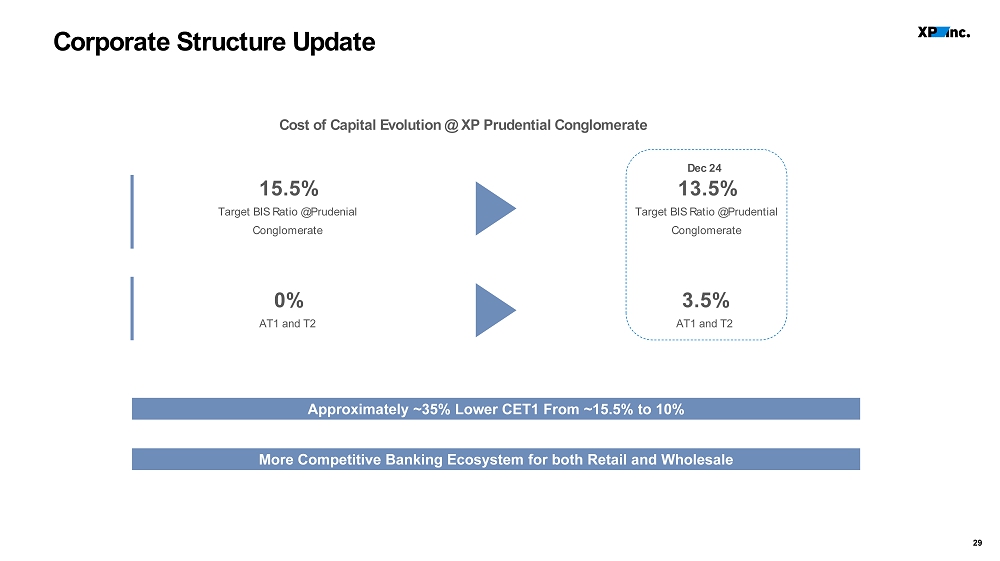

29 Cost of Capital Evolution @ XP Prudential Conglomerate Corporate Structure Update Approximately ~35% Lower CET1 From ~15.5% to 10% 15.5% Target BIS Ratio @Prudenial Conglomerate 13.5% Target BIS Ratio @Prudential Conglomerate 0 % AT1 and T2 3.5% AT1 and T2 More Competitive Banking Ecosystem for both Retail and Wholesale Dec 24

03. Final Remarks

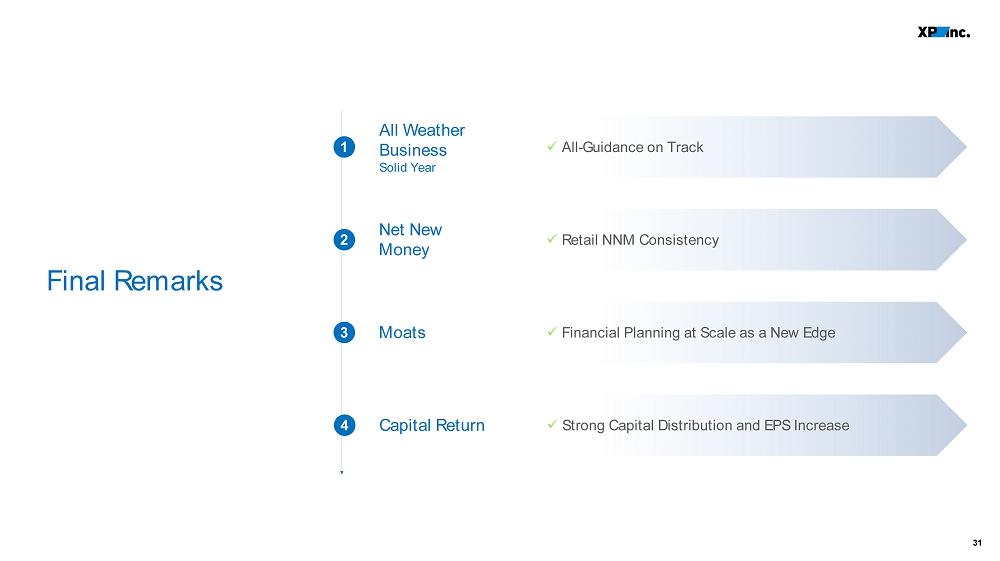

31 All Weather Business Solid Year x All - Guidance on Track 1 2 x Retail NNM Consistency Net New Money 3 x Financial Planning at Scale as a New Edge Moats Final Remarks 4 x Strong Capital Distribution and EPS Increase Capital Return

04. Q&A

33 Total Loan Portfolio¹ Note: 1 – Gross of Expected Credit Losses. Total Unsecured Secured R$ billion 21.2 4.1 17.2 Loans 8.4 2.4 6.0 Credit Card 31.9 26.3 5.6 Corporate Securities 61.5 32.7 28.8 Credit Portfolio Main Activities • Investment Banking • Fixed Income Distribution • Corporate Credit

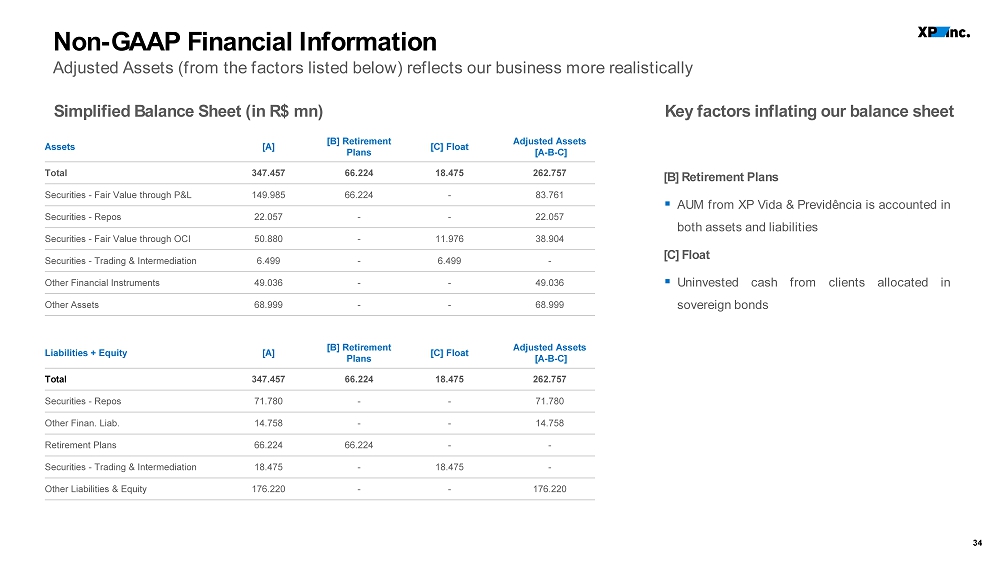

34 Adjusted Assets [A - B - C] [C] Float [B] Retirement Plans [A] Assets 262.757 18.475 66.224 347.457 Total 83.761 - 66.224 149.985 Securities - Fair Value through P&L 22.057 - - 22.057 Securities - Repos 38.904 11.976 - 50.880 Securities - Fair Value through OCI - 6.499 - 6.499 Securities - Trading & Intermediation 49.036 - - 49.036 Other Financial Instruments 68.999 - - 68.999 Other Assets Adjusted Assets [A - B - C] [C] Float [B] Retirement Plans [A] Liabilities + Equity 262.757 18.475 66.224 347.457 Total 71.780 - - 71.780 Securities - Repos 14.758 - - 14.758 Other Finan. Liab. - - 66.224 66.224 Retirement Plans - 18.475 - 18.475 Securities - Trading & Intermediation 176.220 - - 176.220 Other Liabilities & Equity Non - GAAP Financial Information Adjusted Assets (from the factors listed below) reflects our business more realistically [B] Retirement Plans ▪ AUM from XP Vida & Previdência is accounted in both assets and liabilities [C] Float ▪ Uninvested cash from clients allocated in sovereign bonds Key factors inflating our balance sheet Simplified Balance Sheet (in R $ mn )

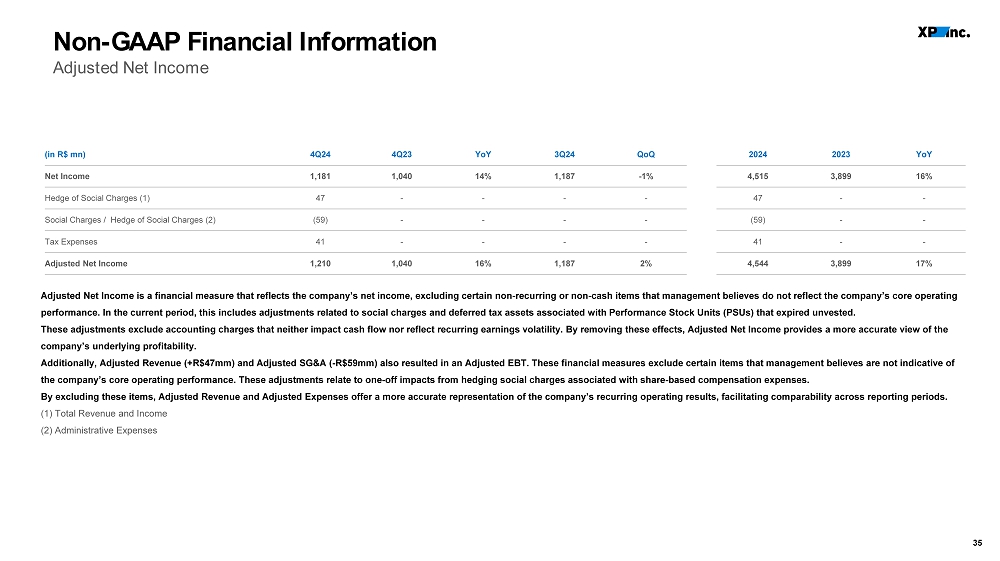

35 Non - GAAP Financial Information Adjusted Net Income YoY 2023 2024 QoQ 3Q24 YoY 4Q23 4Q24 (in R$ mn) 16% 3,899 4,515 - 1% 1,187 14% 1,040 1,181 Net Income - - 47 - - - - 47 Hedge of Social Charges (1) - - (59) - - - - (59) Social Charges / Hedge of Social Charges (2) - - 41 - - - - 41 Tax Expenses 17% 3,899 4,544 2% 1,187 16% 1,040 1,210 Adjusted Net Income Adjusted Net Income is a financial measure that reflects the company’s net income, excluding certain non - recurring or non - cash i tems that management believes do not reflect the company’s core operating performance. In the current period, this includes adjustments related to social charges and deferred tax assets associated wi th Performance Stock Units (PSUs) that expired unvested. These adjustments exclude accounting charges that neither impact cash flow nor reflect recurring earnings volatility. By remo vin g these effects, Adjusted Net Income provides a more accurate view of the company’s underlying profitability. Additionally, Adjusted Revenue (+R$47mm) and Adjusted SG&A ( - R$59mm) also resulted in an Adjusted EBT. These financial measures exclude certain items that management believes are not indicative of the company’s core operating performance. These adjustments relate to one - off impacts from hedging social charges associated wit h share - based compensation expenses. By excluding these items, Adjusted Revenue and Adjusted Expenses offer a more accurate representation of the company’s recurr ing operating results, facilitating comparability across reporting periods. (1) Total Revenue and Income (2) Administrative Expenses

3Q24 Earnings Presentation Investor Relations ir@xpi.com.br https://investors.xpinc.com/