| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-226943-05 | ||

|

November 12, 2019

FREE WRITING PROSPECTUS

STRUCTURAL AND COLLATERAL TERM SHEET

$1,024,298,346

(Approximate Total Mortgage Pool Balance)

$885,202,000

(Approximate Offered Certificates)

COMM 2019-GC44 |

Deutsche Mortgage & Asset Receiving Corporation

Depositor

German American Capital Corporation

Goldman Sachs Mortgage Company

Citi Real Estate Funding Inc.

Sponsors and Mortgage Loan Sellers

Deutsche Bank Securities | Citigroup | Goldman Sachs & Co. LLC |

Co-Lead Managers and Joint Bookrunners

Academy Securities | Drexel Hamilton |

Co-Managers

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-226943) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the Securities and Exchange Commission website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by emailing: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us. This free writing prospectus does not contain all information that is required to be included in the prospectus.

Capitalized terms used but not defined herein have the meanings assigned to them in the Preliminary Prospectus expected to be dated November 12, 2019 relating to the offered certificates (hereinafter referred to as the “Preliminary Prospectus”).

KEY FEATURES OF SECURITIZATION |

Offering Terms: |

|

Co-Lead Managers and Joint Bookrunners: | Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC and Citigroup Global Markets Inc. |

Co-Managers: | Academy Securities, Inc. and Drexel Hamilton, LLC |

Sponsors and Mortgage Loan Sellers: | German American Capital Corporation* (“GACC”) (26.9%), Goldman Sachs Mortgage Company (“GSMC”) (49.1%) and Citi Real Estate Funding Inc. (“CREFI”) (24.0%) *An indirect wholly owned subsidiary of Deutsche Bank AG |

Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

Operating Advisor: | Park Bridge Lender Services LLC |

Asset Representations Reviewer: | Park Bridge Lender Services LLC |

Special Servicer: | Rialto Capital Advisors, LLC |

Certificate Administrator: | Wells Fargo Bank, National Association |

Trustee: | Wells Fargo Bank, National Association |

Rating Agencies: | Moody’s Investors Service, Inc. (“Moody’s”), S&P Global Ratings, a Standard & Poor’s Financial Services LLC business (“S&P”) and Kroll Bond Rating Agency, Inc. (“KBRA”). |

Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements are being satisfied by GACC, as retaining sponsor, see “Credit Risk Retention” in the Preliminary Prospectus. Note that this securitization transaction is not being structured to satisfy EU risk retention and due diligence requirements. |

Determination Date: | 11th day of each month, or if such 11th day is not a business day, the immediately following business day, commencing in January 2020. |

Distribution Date: | 4th business day following the Determination Date in each month, commencing in January 2020. |

Cut-off Date: | With respect to each mortgage loan, the later of the related payment date of such mortgage loan in December 2019 (or, in the case of any mortgage loan that has its first due date subsequent to December 2019, the date that would have been its due date in December 2019 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month) and the date of origination of such mortgage loan. Unless otherwise noted, all mortgage loan statistics are based on balances as of the Cut-off Date. |

Closing Date: | On or about December 12, 2019 |

Settlement Terms: | DTC, Euroclear and Clearstream, same day funds, with accrued interest. |

ERISA Eligible: | All of the Offered Certificates are expected to be ERISA eligible. |

SMMEA Eligible: | None of the Offered Certificates will be SMMEA eligible. |

Day Count: | 30/360 |

Tax Treatment: | REMIC |

Rated Final Distribution Date: | August 2057 |

Minimum Denominations: | $10,000 (for each class of offered principal balance certificates) and $100,000 (for each class of offered interest-only certificates) and in each case in multiples of $1 thereafter. |

Clean-up Call: | 1% (with certain exceptions described under “Pooling and Servicing Agreement—Termination; Retirement of Certificates” in the Preliminary Prospectus) |

Distribution of Collateral by Property Type |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

COMM 2019-GC44 Mortgage Trust

|

TRANSACTION HIGHLIGHTS |

Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Pool Balance |

German American Capital Corporation | 9 | 10 | $275,840,769 | 26.9% |

Goldman Sachs Mortgage Company | 20 | 29 | $502,864,115 | 49.1% |

Citi Real Estate Funding Inc. | 14 | 16 | $245,593,462 | 24.0% |

Total: | 43 | 55 | $1,024,298,346 | 100.0% |

Collateral Facts |

|

Initial Outstanding Pool Balance: | $1,024,298,346 |

Number of Mortgage Loans: | 43 |

Number of Mortgaged Properties: | 55 |

Average Mortgage Loan Cut-off Date Balance: | $23,820,892 |

Weighted Average Mortgage Rate: | 3.5463% |

Weighted Average Mortgage Loan Original Term to Maturity Date or ARD (months): | 109 |

Weighted Average Mortgage Loan Remaining Term to Maturity Date or ARD (months): | 108 |

Weighted Average Mortgage Loan Seasoning (months): | 1 |

% of Mortgaged Properties Leased to a Single Tenant: | 13.0% |

Credit Statistics(1) |

|

Weighted Average Mortgage Loan U/W NCF DSCR: | 2.58x |

Weighted Average Mortgage Loan Cut-off Date LTV(2)(3): | 56.9% |

Weighted Average Mortgage Loan Maturity Date or ARD LTV(2): | 53.4% |

Weighted Average U/W NOI Debt Yield(3): | 10.5% |

Amortization Overview |

|

% Mortgage Loans with Amortization through Maturity Date or ARD: | 17.0% |

% Mortgage Loans which pay Interest Only through Maturity or ARD Date: | 66.3% |

% Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date or ARD: | 16.7% |

Weighted Average Remaining Amortization Term (months)(4): | 350 |

Loan Structural Features |

|

% Mortgage Loans with Upfront or Ongoing Tax Reserves: | 62.3% |

% Mortgage Loans with Upfront or Ongoing Replacement Reserves(5): | 78.2% |

% Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 33.7% |

% Mortgage Loans with Upfront or Ongoing TI/LC Reserves(6): | 59.9% |

% Mortgage Loans with In Place Hard Lockboxes(7): | 70.4% |

% Mortgage Loans with Cash Traps Triggered at DSCR Levels ≥ 1.05x: | 49.0% |

% Mortgage Loans with Cash Traps Triggered at Debt Yield Levels ≥ 5.0%: | 38.2% |

|

|

Prepayment Provisions |

|

% Mortgage Loans with Defeasance Only After a Lockout Period and Prior to an Open Period: | 72.9% |

% Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with a Yield Maintenance Charge: | 14.8% |

% Mortgage Loans with Prepayment with Yield Maintenance Charge or with Defeasance or Yield Maintenance Charge Prior to an Open Period(8): | 7.3% |

% Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with a Yield Maintenance Charge or After a Lockout Period with Defeasance or a Yield Maintenance Charge: | 5.0% |

(1) | The LTV, DSCR and Debt Yield calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

(2) | With respect to 5 mortgage loans (15.2%) (including Weston Kentucky Portfolio, 55 Green Street, Legends at Village West, Embassy Suites Laredo and Hampton Inn Summerlin), the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated using a value other than the “As Is” appraised values. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

(3) | With respect to the Weston Kentucky Portfolio mortgage loan (5.1%) the Cut-off Date LTV and U/W NOI Debt Yield are calculated based on the Cut-off Date Balance net of a related earnout reserve. |

(4) | Excludes mortgage loans which are interest only for the full loan term. |

(5) | Includes FF&E reserves. |

(6) | Represents the percent of the allocated Initial Outstanding Pool Balance of office, retail, industrial and mixed use properties only structured with TI/LC reserves. |

(7) | With respect to the Millennium Park Plaza mortgage loan (1.5%) there is an in place hard lockbox for the retail and office units and an in place soft lockbox for the multifamily units. |

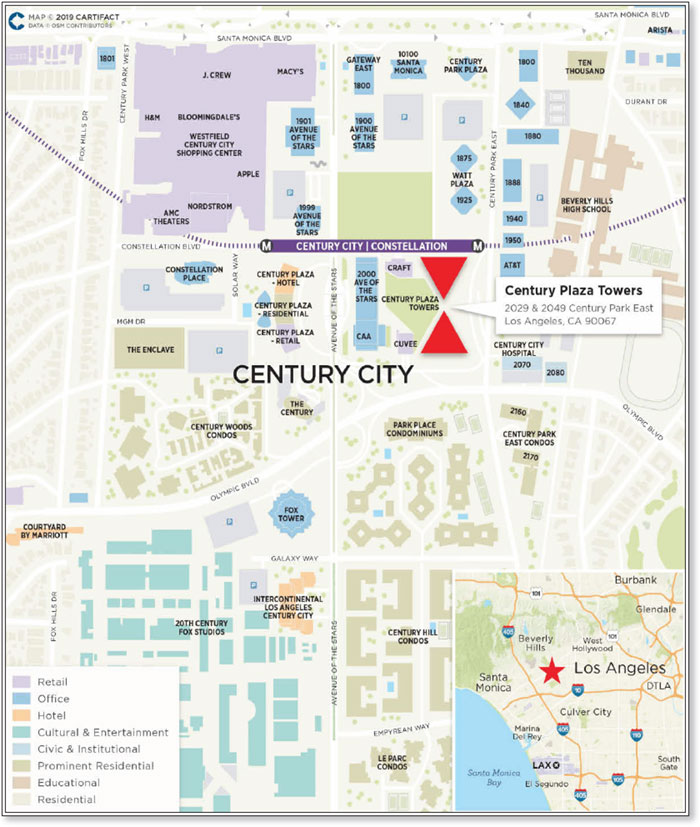

(8) | With respect to the Century Plaza Towers whole loan, prepayment in whole, but not in part, is permitted at any time prior to July 9, 2029 with the payment of a yield maintenance fee. Defeasance of the full $1.2 billion Century Plaza Towers whole loan is permitted after the date that is the earlier of (i) two years from the closing date of the securitization that includes the last pari passu note to be securitized and (ii) October 21, 2022. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

COMM 2019-GC44 Mortgage Trust

|

STRUCTURE SUMMARY |

OFFERED CERTIFICATES

Class(1) | Ratings | Initial Certificate | Initial Subordination | Weighted Average Life | Principal (months)(4) | Certificate | Certificate NOI Debt Yield(6) |

|

|

|

|

|

|

|

|

Class A-1 | Aaa(sf)/AAAsf/AAA(sf) | $23,338,000 | 30.000% | 2.82 | 1 – 59 | 39.8% | 15.0% |

Class A-2 | Aaa(sf)/AAAsf/AAA(sf) | $138,840,000 | 30.000% | 4.93 | 59 – 59 | 39.8% | 15.0% |

Class A-3 | Aaa(sf)/AAAsf/AAA(sf) | $55,469,000 | 30.000% | 6.93 | 83 – 83 | 39.8% | 15.0% |

Class A-SB | Aaa(sf)/AAAsf/AAA(sf) | $29,564,000 | 30.000% | 7.24 | 59 – 113 | 39.8% | 15.0% |

Class A-4 | Aaa(sf)/AAAsf/AAA(sf) | (7) | 30.000% | (7) | (7) | 39.8% | 15.0% |

Class A-5 | Aaa(sf)/AAAsf/AAA(sf) | (7) | 30.000% | (7) | (7) | 39.8% | 15.0% |

Class X-A(8) | NR/AAAsf/AAA(sf) | $808,764,000(9) | N/A | N/A | N/A | N/A | N/A |

Class A-M | Aa3(sf)/AAAsf/AAA(sf) | $118,356,000 | 18.000% | 9.93 | 119 – 119 | 46.7% | 12.8% |

Class B | NR/AA-sf/AA-(sf) | $40,685,000 | 13.875% | 9.93 | 119 – 119 | 49.0% | 12.2% |

Class C | NR/A-sf/A-(sf) | $35,753,000 | 10.250% | 9.93 | 119 – 119 | 51.1% | 11.7% |

NON-OFFERED CERTIFICATES

Class(1) | Ratings | Initial Certificate | Initial Subordination | Weighted Average Life | Principal (months)(4) | Certificate | Certificate NOI Debt Yield(6) |

|

|

|

|

|

|

|

|

Class X-B(8) | NR/A-sf/AAA(sf) | $76,438,000(9) | N/A | N/A | N/A | N/A | N/A |

Class X-D(8) | NR/BBB-sf/BBB-(sf) | $41,918,000(9) | N/A | N/A | N/A | N/A | N/A |

Class X-F(8)(10) | NR/BB-sf/BB-(sf) | $18,493,000(9) | N/A | N/A | N/A | N/A | N/A |

Class D | NR/BBBsf/BBB+(sf) | $23,425,000 | 7.875% | 9.93 | 119 – 119 | 52.4% | 11.4% |

Class E | NR/BBB-sf/BBB-(sf) | $18,493,000 | 6.000% | 9.93 | 119 – 119 | 53.5% | 11.2% |

Class F(10) | NR/BB-sf/BB-(sf) | $18,493,000 | 4.125% | 9.93 | 119 – 119 | 54.6% | 11.0% |

Class G-RR(10)(11) | NR/B-sf/B-(sf) | $9,863,000 | 3.125% | 9.93 | 119 – 119 | 55.1% | 10.8% |

Class H-RR(10)(11) | NR/NR/NR | $30,822,346 | 0.000% | 9.93 | 119 – 119 | 56.9% | 10.5% |

NON-OFFERED LOAN-SPECIFIC CERTIFICATES

Class(1) | Ratings | Initial Certificate | Initial Subordination | Weighted Average Life | Principal (months)(4) | Certificate | Certificate NOI Debt Yield(13) |

|

|

|

|

|

|

|

|

Class 180W-A(14) | Baa3(sf)/NR/NR | $33,155,000 | 34.943% | 4.93 | 59 – 59 | 38.2% | 8.8% |

Class 180W-B(14) | Ba3(sf)/NR/NR | $35,530,000 | 20.830% | 4.93 | 59 – 59 | 46.5% | 7.2% |

Class 180W-C(14) | B3(sf)/NR/NR | $42,940,000 | 3.774% | 4.93 | 59 – 59 | 56.5% | 5.9% |

Class 180W-D(14) | NR/NR/NR | $9,500,000 | 0.000% | 4.93 | 59 – 59 | 58.7% | 5.7% |

NON-OFFERED VERTICAL RISK RETENTION INTEREST

Non-Offered Vertical Risk | Ratings | Initial Certificate | Initial Subordination | Weighted Average Life | Principal (months)(15) | Certificate | Certificate NOI Debt Yield |

|

|

|

|

|

|

|

|

Class RR Certificates(16)(17) | NR/NR/NR | $25,800,000(18) | N/A | 8.77 | 1 – 119 | N/A | N/A |

RR Interest(16)(17) | NR/NR/NR | $12,200,000(18) | N/A | 8.77 | 1 – 119 | N/A | N/A |

180W-VRR Interest(14)(17)(19) | NR/NR/NR | $6,375,000 | N/A | 4.93 | 59 – 59 | N/A | N/A |

(1) | The pass-through rates applicable to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G-RR and Class H-RR certificates (the “Pooled Principal Balance Certificates”) will equal one of: (i) a fixed per annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which the related Distribution Date occurs (the “WAC Rate”), (iii) a rate equal to the lesser of a specified pass-through rate and the WAC Rate or (iv) the WAC Rate less a specified rate. The pass-through rates applicable to the Class 180W-A, Class 180W-B, Class 180W-C and Class 180W-D certificates, in each case, will equal one of the following per annum rates: (i) a fixed rate, (ii) the net mortgage rate on the Trust Subordinate Companion Loan, (iii) the lesser of a specified rate and the net mortgage rate on the Trust Subordinate Companion Loan, or (iv) the net mortgage rate on the Trust Subordinate Companion Loan less a specified rate. |

(2) | Approximate; subject to a permitted variance of plus or minus 5%. Neither the VRR Interest Balance of the VRR Interest nor the Certificate Balance of the 180W-VRR Interest is included in the Certificate Balance or Notional Amount of any Class of Certificates set forth under “Offered Certificates”, “Non-Offered Certificates” or “Non-Offered Loan-Specific Certificates” in the table above. In addition, the Certificate Balance of each Class of Pooled Principal Balance Certificates (and correspondingly, the initial Notional Amount of each Class of Class X Certificates) is subject to change as described in footnote (18) below. |

(3) | The initial subordination levels for the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-5 certificates are represented in the aggregate. The approximate initial credit support percentage for each class of Pooled Principal Balance Certificates does not include the subordination provided by the trust subordinate companion loan related to the 180 Water mortgage loan. None of the Class 180W-A, Class 180W-B, Class 180W-C, Class 180W-D certificates or the 180W-VRR Interest (the “Loan-Specific Certificates”) will provide credit support to any other class of certificates, except to the extent of the subordination of the trust subordinate companion loan (in which the Loan-Specific Certificates each represent an interest) to the 180 Water mortgage loan. The initial credit support percentages of the Loan-Specific Certificates are based on the 180 Water whole loan. The approximate initial credit support percentages shown in the table above do not take into account the VRR Interest or the 180W-VRR Interest. However, losses incurred on the mortgage loans will be allocated between the VRR Interest, on the one hand, and the Pooled Principal Balance Certificates, on the other hand, pro rata in accordance with their respective outstanding balances, and losses incurred on the trust subordinate companion loan will be allocated between the 180W-VRR Interest, on the one hand, and the Class 180W-A, Class 180W-B, Class 180W-C and Class 180W-D Certificates, on the other hand, pro rata in accordance with their respective outstanding Certificate Balances. |

(4) | The weighted average life and principal window during which distributions of principal would be received as set forth in the table with respect to each class of Pooled Principal Balance Certificates (and the Loan-Specific Certificates) are based on (i) modeling assumptions described in the Preliminary Prospectus and (ii) assumptions that there are no prepayments, delinquencies or losses on the mortgage loans (or, in the case of the Loan-Specific Certificates, the Trust Subordinate Companion Loan). The weighted average life and principal window of the Class A-4 and Class A-5 certificates are expected to be within the applicable ranges reflected in the chart set forth in footnote (7) below. |

(5) | “Certificate Principal to Value Ratio” for any class of Pooled Principal Balance Certificates is calculated as the product of (a) the weighted average mortgage loan Cut-off Date LTV of the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of the related class of Pooled Principal Balance Certificates and all other classes of Pooled Principal Balance Certificates (and the VRR Interest Balance of any portion of the VRR Interest that is considered to be pari passu or senior to such class), if any, that are senior to such class, and the |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

COMM 2019-GC44 Mortgage Trust

|

STRUCTURE SUMMARY |

denominator of which is the total initial Certificate Balance of all classes of Pooled Principal Balance Certificates and the initial VRR Interest Balance of the VRR Interest. The Certificate Principal to Value Ratios of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-5 certificates are calculated in the aggregate for those classes as if they were a single class.

(6) | “Certificate Underwritten NOI Debt Yield” for any class of Pooled Principal Balance Certificates is calculated as the product of (a) the weighted average Underwritten NOI Debt Yield for the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of all classes of Pooled Principal Balance Certificates and the initial VRR Interest Balance of the VRR Interest and the denominator of which is the total initial Certificate Balance of such class of Pooled Principal Balance Certificates and all other classes of Pooled Principal Balance Certificates, if any, that are senior to such class (and the VRR Interest Balance of any portion of the VRR Interest that is considered to be pari passu or senior to such class). The Underwritten NOI Debt Yields of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-5 certificates are calculated in the aggregate for those classes as if they were a single class. |

(7) | The exact initial Certificate Balances of the Class A-4 and Class A-5 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial Certificate Balances, weighted average lives and principal windows of the Class A-4 and Class A-5 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial Certificate Balance of the Class A-4 and Class A-5 certificates is expected to be approximately $443,197,000, subject to a variance of plus or minus 5.0%. |

Class of Certificates | Expected Range of Initial Certificate Balance | Expected Range of Weighted Avg. Life (years) | Expected Range of Principal Window (months) |

Class A-4 | $75,000,000 - $176,000,000 | 9.63 – 9.76 | 113-116 / 113-119 |

Class A-5 | $267,197,000 - $368,197,000 | 9.93 – 9.90 | 119-119 / 116-119 |

(8) | As further described in the Preliminary Prospectus, the pass-through rate applicable to the Class X-A, Class X-B, Class X-D and Class X-F certificates (collectively, the “Class X Certificates” and, together with the Pooled Principal Balance Certificates and the Class S Certificates, the “Pooled Certificates”) for each Distribution Date will generally be equal to the excess of (i) the WAC Rate over (ii)(A) with respect to the Class X-A certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5 and Class A-M certificates (based on their respective Certificate Balances immediately prior to such Distribution Date), (B) with respect to the Class X-B certificates, the weighted average of the pass-through rates of the Class B and Class C certificates (based on their respective Certificate Balances immediately prior to such Distribution Date), (C) with respect to the Class X-D certificates, the weighted average of the pass-through rates of the Class D and Class E certificates (based on their respective Certificate Balances immediately prior to such Distribution Date) and (D) with respect to the Class X-F certificates, the pass-through rate of the Class F certificates. |

(9) | The Class X Certificates will not have Certificate Balances. None of the Class X Certificates will be entitled to distributions of principal. The interest accrual amounts on the Class X-A certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5 and Class A-M certificates. The interest accrual amounts on the Class X-B certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class B and Class C certificates. The interest accrual amounts on the Class X-D certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class D and Class E certificates. The interest accrual amounts on the Class X-F certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class F certificates. The notional amount of each class of the Class X Certificates is subject to change depending upon the final pricing of the Pooled Principal Balance Certificates, as follows: (1) if as a result of such pricing the pass-through rate of any class of Pooled Principal Balance Certificates whose Certificate Balance comprises such notional amount is equal to the WAC Rate, the Certificate Balance of such class of Pooled Principal Balance Certificates may not be part of, and will reduce accordingly, such notional amount of the related Class X Certificates (or, if as a result of such pricing the pass-through rate of the related Class X Certificates is equal to zero, such Class X Certificates may not be issued on the Closing Date), and/or (2) if as a result of such pricing the pass-through rate of any class of Pooled Principal Balance Certificates that does not comprise such notional amount of the related Class X Certificates is equal to less than the WAC Rate, such class of Pooled Principal Balance Certificates may become a part of, and will increase accordingly, such notional amount of the related Class X Certificates. |

(10) | The initial Certificate Balance of each of the Class F, Class G-RR and Class H-RR certificates, and the notional amount of the Class X-F certificates, is subject to change based on final pricing of all Pooled Certificates, the final determination of the Class G-RR and Class H-RR certificates (collectively, the “HRR Certificates”) that will be retained by the retaining third-party purchaser and the final determination of the VRR Interest that will be retained as described under “Credit Risk Retention” in the Preliminary Prospectus to satisfy the U.S. risk retention requirements of German American Capital Corporation, as retaining sponsor. For more information regarding the methodology and key inputs and assumptions used to determine the sizing of the HRR Certificates, see “Credit Risk Retention” in the Preliminary Prospectus. |

(11) | The HRR Certificates are expected to be retained by RREF III-D AIV, LLC or its affiliate, in partial satisfaction of the retention obligations of German American Capital Corporation in its capacity as the retaining sponsor in accordance with the credit risk retention rules applicable to the pooled securitization transaction. For more information regarding the methodology and key inputs and assumptions used to determine the sizing of the HRR Certificates, see “Credit Risk Retention” in the Preliminary Prospectus. |

(12) | The “Certificate Principal to Value Ratio” for any class of Loan-Specific Certificates (other than the 180W-VRR Interest) is calculated as the product of (a) the Cut-off Date LTV of the180 Water Whole Loan, multiplied by (b) a fraction, the numerator of which is the sum of (i) the initial Certificate Balance of such class of Loan-Specific Certificates and all other classes of Loan-Specific Certificates, if any, that are senior to such class (including any portions of the 180W-VRR Interest that is considered to be pari passu or senior to such class) and (ii) the principal balance as of the Cut-off Date of the 180 Water Senior Loan, and the denominator of which is the total initial Certificate Balance of all classes of Loan-Specific Certificates (including the 180W-VRR Interest) and the principal balance as of the Cut-off Date of 180 Water Senior Loan. |

(13) | The “Certificate Underwritten NOI Debt Yield” for any class of Loan-Specific Certificates (other than the 180W-VRR Interest) is calculated as the product of (a) the Underwritten NOI Debt Yield for the 180 Water Whole Loan, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of all classes of Loan-Specific Certificates (including the 180W-VRR Interest) and the principal balance as of the Cut-off Date of 180 Water Senior Loan and the denominator of which is the total initial Certificate Balance of such class of Loan-Specific Certificates and all other classes of Loan-Specific Certificates (including any portions of the 180W-VRR Interest that is considered to be pari passu or senior to such class), if any, that are senior to such class and the principal balance as of the Cut-off Date of 180 Water Senior Loan. |

(14) | The Loan-Specific Certificates will only be entitled to receive distributions from, and will only incur losses with respect to, the Trust Subordinate Companion Loan. The Trust Subordinate Companion Loan will be included as an asset of the issuing entity but will not be part of the mortgage pool backing the Pooled Certificates. No class of Pooled Certificates will have any interest in the Trust Subordinate Companion Loan. See “Description of the Mortgage Pool—The Whole Loans—180 Water Whole Loan” in the Preliminary Prospectus. |

(15) | The weighted average life and principal window during which distributions of principal would be received as set forth in the foregoing table with respect to the VRR Interest (as defined below) and the 180W-VRR Interest are based on the assumptions set forth under “Yield and Maturity Considerations—Weighted Average Life” in the Preliminary Prospectus and on the assumptions that there are no prepayments, modifications or losses in respect of the mortgage loans or the Trust Subordinate Companion Loan, as applicable, and that there are no extensions or forbearances of maturity dates. |

(16) | German American Capital Corporation, as the retaining sponsor, is expected to acquire from the depositor, on the Closing Date, an “eligible vertical interest” (as defined in Regulation RR) in the form of a single vertical security comprised of the Class RR certificates and the RR interest (collectively, the “VRR Interest”), representing a specified percentage (to be determined as described in footnote (18) below) of all classes of Pooled Principal Balance Certificates and the VRR Interest. A portion of the VRR Interest will be retained by each of German American Capital Corporation or its “majority-owned affiliate” and GSMC and CREFI in accordance with the credit risk retention rules applicable to the pooled securitization transaction. See “Credit Risk Retention” in the Preliminary Prospectus. |

(17) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the VRR Interest will be the WAC rate. The effective interest rate for the 180W-VRR Interest will be the net mortgage rate of the Trust Subordinate Companion Loan. |

(18) | The initial VRR Interest Balance of the VRR Interest is subject to change depending on the final pricing of all classes of Pooled Certificates with the final VRR Interest Balance of the VRR Interest determined such that, upon initial issuance, the percentage of the fair value of the HRR Certificates and the percentage of the VRR Interest (in the aggregate) will equal at least 5. If the initial VRR Interest balance is reduced, the initial Certificate Balance of each class of Pooled Principal Balance Certificates (and correspondingly, the initial notional amount of each class of Class X Certificates) will be increased on a pro rata basis (based on the initial Certificate Balance set forth in the table above) in an aggregate amount equal to such reduction in the initial VRR Interest Balance of the VRR Interest. If the initial VRR Interest Balance of the VRR Interest is increased, the initial Certificate Balance of each class of Pooled Principal Balance Certificates (and correspondingly, the initial notional amount of each class of Class X Certificates) will be decreased on a pro rata basis (based on the initial Certificate Balance set forth in the table above) in an aggregate amount equal to such increase in the initial VRR Interest Balance of the VRR Interest. For a further description, see “Credit Risk Retention” in the Preliminary Prospectus. |

(19) | German American Capital Corporation, as the retaining sponsor, is expected to acquire from the depositor, on the Closing Date, an “eligible vertical interest” (as defined in Regulation RR) in the form of a single vertical security with an expected aggregate initial Certificate Balance of $6,375,000 (the “180W-VRR Interest”), which is expected to represent approximately 5.00% of all Classes of Loan-Specific Certificates. The 180W-VRR Interest will be retained by German American Capital Corporation or its “majority-owned affiliate” in accordance with the credit risk retention rules applicable to the securitization transaction relating to the Loan-Specific Certificates. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

COMM 2019-GC44 Mortgage Trust

|

STRUCTURE SUMMARY |

Class A-2 Principal Paydown(1) |

Class |

Mortgage Loan Seller | Mortgage Loan | Property Type | Cut-off Date | Remaining | Cut-off Date | U/W NCF DSCR | U/W NOI Debt Yield |

A-2 | GACC | 180 Water | Multifamily | $62,500,000 | 59 | 30.5% | 3.15x | 11.0% |

A-2 | GACC | 225 Bush | Office | $50,000,000 | 59 | 34.6% | 3.85x | 13.4% |

A-2 | CREFI | Legends at Village West | Retail | $34,948,301 | 59 | 53.3% | 1.67x | 9.5% |

(1) | This table reflects the mortgage loans whose balloon payments will be applied to pay down the Class A-2 certificates, assuming (i) that none of the mortgage loans experience prepayments, defaults or losses, (ii) there are no extensions of maturity dates and (iii) each mortgage loan is paid in full on its stated maturity date. See “Yield and Maturity Considerations—Yield Considerations” in the Preliminary Prospectus. |

(2) | With respect to the Legends at Village West mortgage loan, the Cut-off Date LTV has been calculated using a value other than the “As Is” appraised values. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

Class A-3 Principal Paydown(1) |

Class | Mortgage Loan Seller | Mortgage Loan | Property Type | Cut-off Date | Remaining | Cut-off Date | U/W NCF DSCR | U/W NOI Debt Yield |

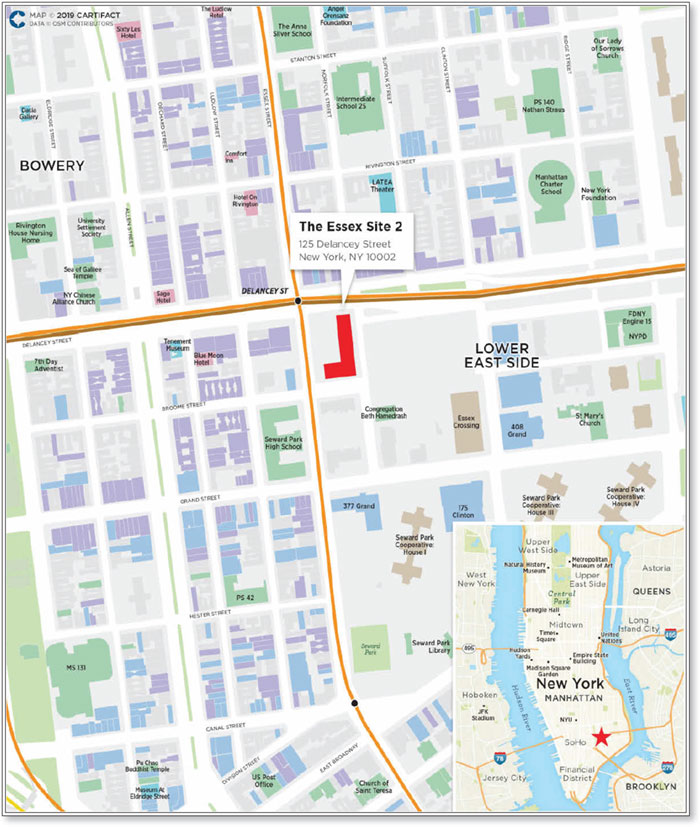

A-3 | GSMC | The Essex Site 2 | Mixed Use | $35,100,000 | 83 | 39.9% | 3.66x | 10.3% |

A-3 | GSMC | Cobb Place | Retail | $25,000,000 | 83 | 73.4% | 1.90x | 10.8% |

(1) | This table reflects the mortgage loans whose balloon payments will be applied to pay down the Class A-3 certificates, assuming (i) that none of the mortgage loans experience prepayments, defaults or losses, (ii) there are no extensions of maturity dates and (iii) each mortgage loan is paid in full on its stated maturity date. See “Yield and Maturity Considerations—Yield Considerations” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

COMM 2019-GC44 Mortgage Trust

|

OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Ten Largest Mortgage Loans | |||||||||

Mortgage Loan | Mortgage Loan Seller | City, State | Property Type | Mortgage Loan Cut-off Date | % of Initial | Cut-off Date | Cut-off | U/W NCF DSCR | U/W NOI Debt Yield(1)(3) |

Century Plaza Towers | GACC | Los Angeles, CA | Office | $75,000,000 | 7.3% | $375 | 39.1% | 4.09x | 13.5% |

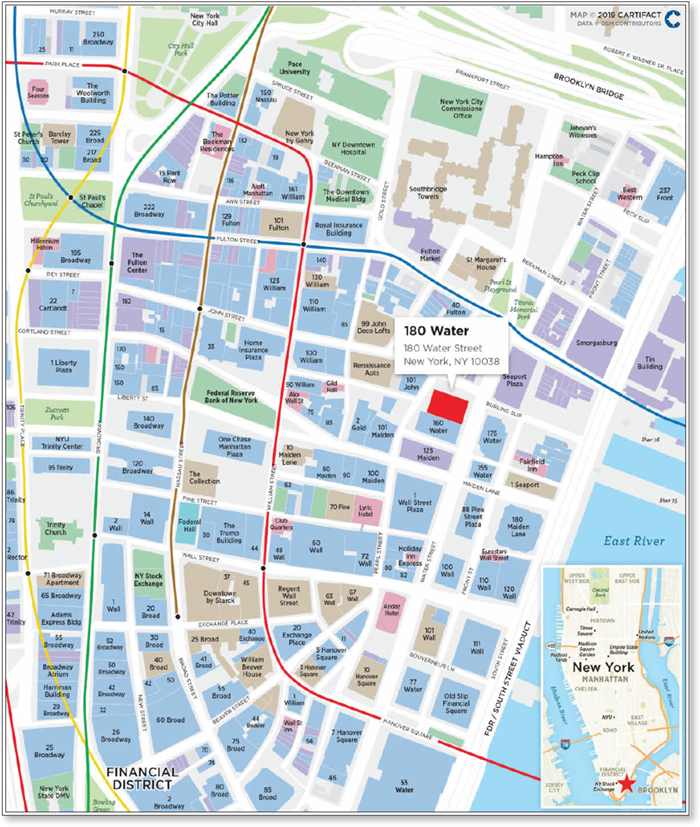

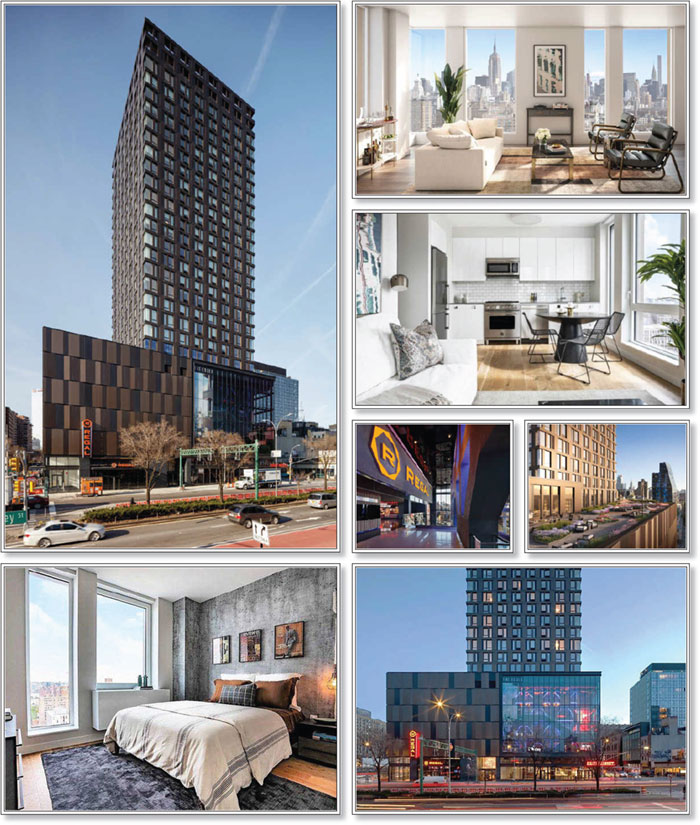

180 Water | GACC | New York, NY | Multifamily | 62,500,000 | 6.1% | $239,965 | 30.5% | 3.15x | 11.0% |

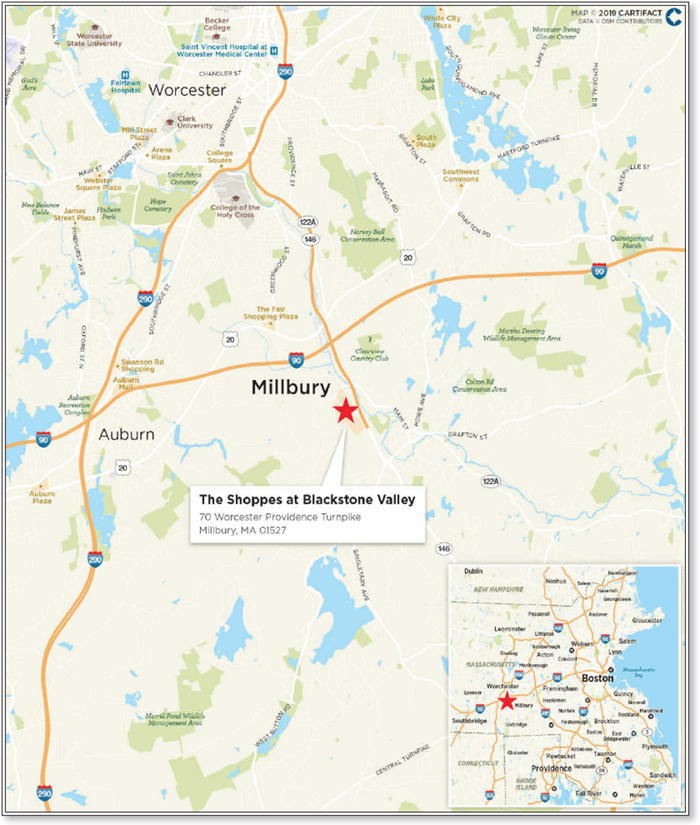

The Shoppes at Blackstone Valley | GSMC | Millbury, MA | Retail | 55,000,000 | 5.4% | $208 | 68.7% | 1.53x | 9.0% |

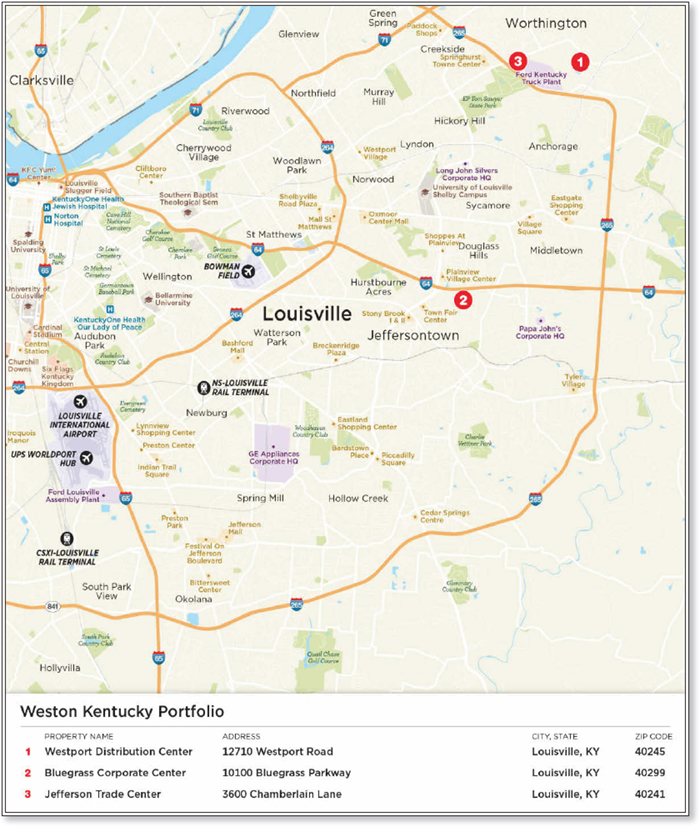

Weston Kentucky Portfolio | GSMC | Louisville, KY | Industrial | 52,253,500 | 5.1% | $36 | 59.5% | 3.06x | 12.3% |

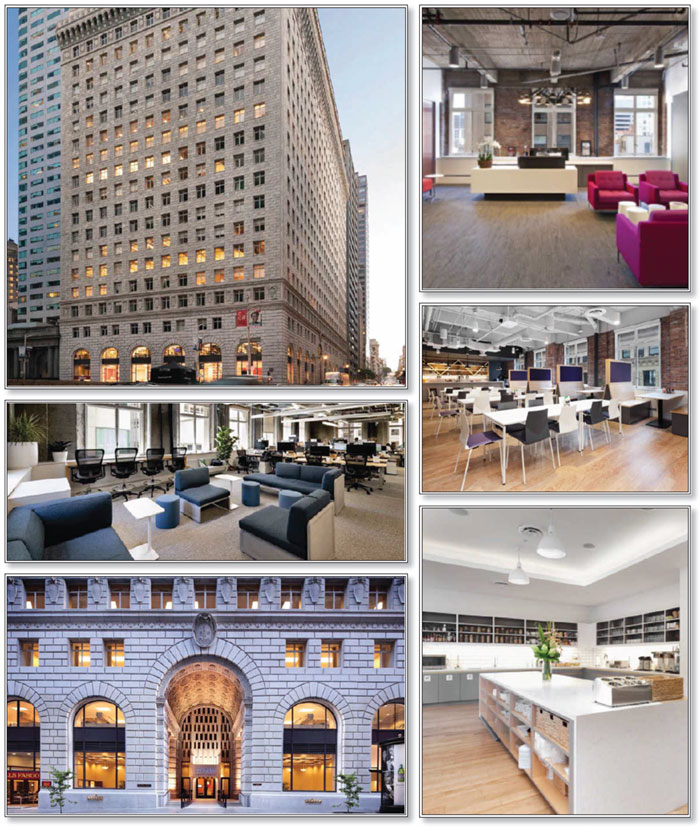

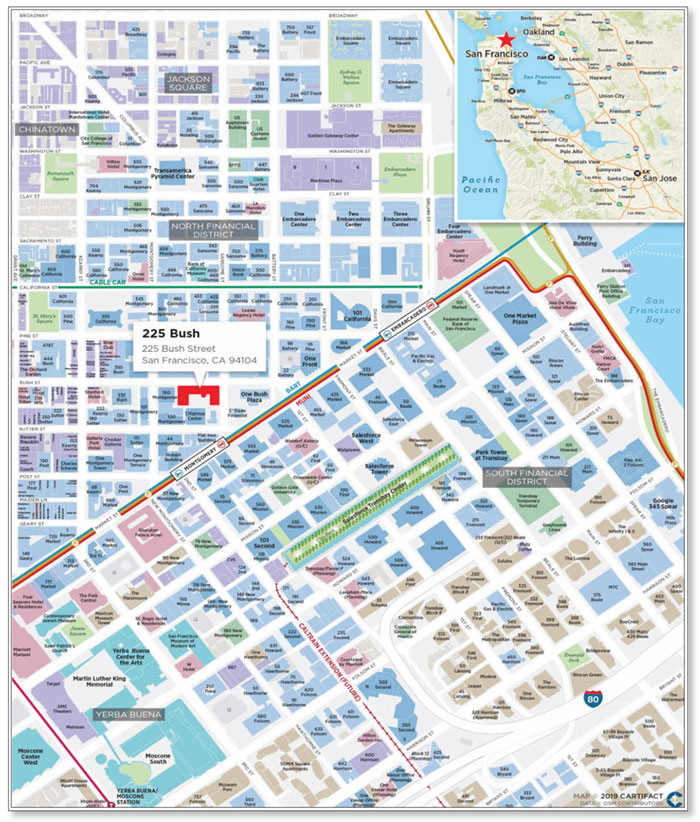

225 Bush | GACC | San Francisco, CA | Office | 50,000,000 | 4.9% | $351 | 34.6% | 3.85x | 13.4% |

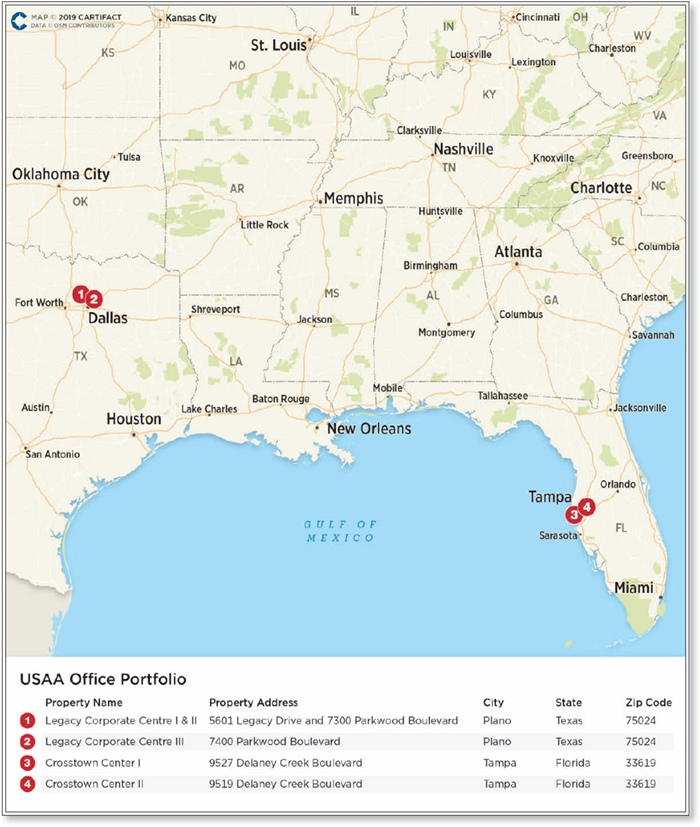

USAA Office Portfolio | GSMC | Various, Various | Office | 45,000,000 | 4.4% | $275 | 63.8% | 2.84x | 9.8% |

PCI Pharma Portfolio | GSMC | Various, Various | Various | 40,000,000 | 3.9% | $80 | 65.4% | 2.61x | 9.5% |

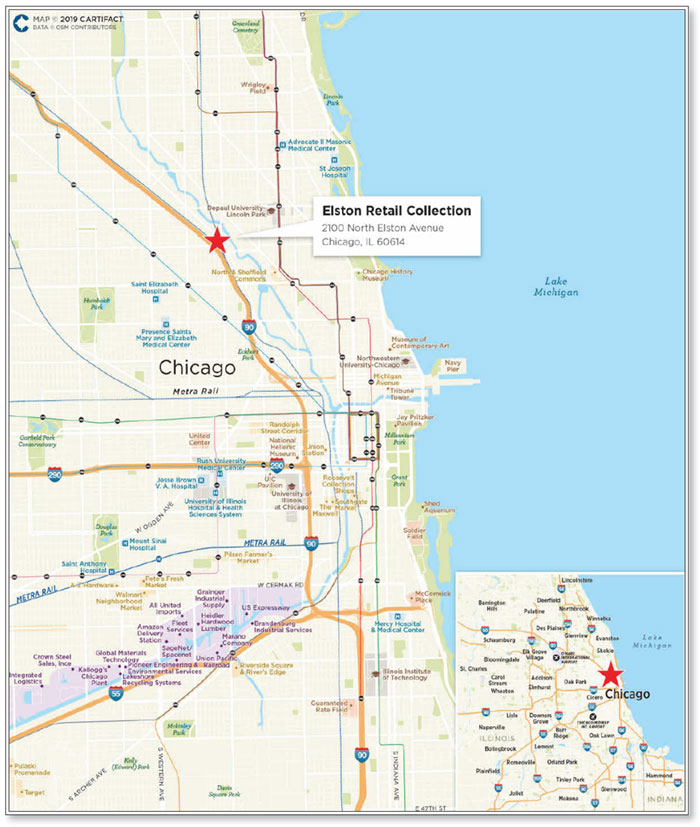

Elston Retail Collection | CREFI | Chicago, IL | Retail | 39,918,185 | 3.9% | $391 | 66.5% | 1.44x | 8.9% |

55 Green Street | GSMC | San Francisco, CA | Office | 36,600,000 | 3.6% | $673 | 56.9% | 2.46x | 8.8% |

The Essex Site 2 | GSMC | New York, NY | Mixed Use | 35,100,000 | 3.4% | $571 | 39.9% | 3.66x | 10.3% |

Total/Weighted Average |

|

|

| $491,371,685 | 48.0% |

| 51.0% | 2.95x | 10.9% |

(1) | The Cut-off Date Balance per NRA/Unit Cut-off Date LTV, U/W NCF DSCR after IO and U/W NOI Debt Yield calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

(2) | With respect to the Weston Kentucky Portfolio and 55 Green Street mortgage loans, the Cut-off Date LTV have been calculated based on the appraised values other than “As Is”. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

(3) | With respect to the Weston Kentucky Portfolio mortgage loan (5.1%) the Cut-off Date LTV and U/W NOI Debt Yield are calculated based on the Cut-off Date Balance net of a related earnout reserve. |

Existing Mezzanine Debt Summary | |||||||||

Mortgage Loan | Mortgage Loan |

Pari Passu/ | Mezzanine Debt | Trust | Total Debt | Trust | Total Debt | Trust | Total Debt |

180 Water | $62,500,000 | $202,500,000 | $100,000,000 | 3.15x | 0.85x | 30.5% | 80.8% | 11.0% | 4.1% |

The Essex Site 2 | $35,100,000 | $139,900,000 | $40,000,000 | 3.66x | 1.33x | 39.9% | 73.4% | 10.3% | 5.6% |

(1) | Total Debt U/W NCF DSCR, Total Debt Cut-off Date LTV and Total Debt U/W NOI Debt Yield calculations include any related pari passu companion loan(s), any related subordinate companion loan(s) and/or any related mezzanine loan(s). |

Subordinate Debt Summary | |||||||||

Mortgage Loan | Mortgage Cut-off Date |

Pari Passu | Subordinate Debt | Trust | Total Debt | Trust | Total Debt | Trust | Total Debt |

Century Plaza Towers | $75,000,000 | $825,000,000 | $300,000,000 | 4.09x | 3.07x | 39.1% | 52.1% | 13.5% | 10.1% |

180 Water | $62,500,000 | $75,000,000 | $127,500,000 | 3.15x | 0.85x | 30.5% | 80.8% | 11.0% | 4.1% |

225 Bush | $50,000,000 | $153,600,000 | $146,400,000 | 3.85x | 2.24x | 34.6% | 59.4% | 13.4% | 7.8% |

The Essex Site 2 | $35,100,000 | $81,900,000 | $58,000,000 | 3.66x | 1.33x | 39.9% | 73.4% | 10.3% | 5.6% |

Midtown Center | $32,525,000 | $349,475,000 | $143,000,000 | 3.98x | 2.90x | 39.8% | 54.7% | 12.6% | 9.1% |

(1) | Total Debt U/W NCF DSCR, Total Debt Cut-off Date LTV and Total Debt U/W NOI Debt Yield calculations include any related pari passu companion loan(s), related subordinate companion loan(s) and/or related mezzanine loan(s). |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

COMM 2019-GC44 Mortgage Trust

|

OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Companion Loan Summary |

Loan | Mortgage Loan | Note(s) | Original | Cut-off Date | Holder of Note(1) | Lead | Master | Special |

1 | Century Plaza Towers | A-1-S1, A-1-S2, A-1-S3, A-2-S1, A-2-S2, A-2-S3, A-2-C1, A-2-C3, A-2-C4, A-3-S1, A-3-S2, A-3-S3, A-3-C1, A-3-C3 | $525,000,000 | $525,000,000 | CPTS 2019-CPT | No |

|

|

|

| A-1-C1, A-1-C2, A-1-C6, A-1-C7 | $112,500,000 | $112,500,000 | DBRI | No |

|

|

|

| A-1-C3, A-1-C8 | $62,500,000 | $62,500,000 | JPMDB 2019-COR6 | No |

|

|

|

| A-1-C4, A-1-C5 | $75,000,000 | $75,000,000 | COMM 2019-GC44 | No |

|

|

|

| A-2-C2, A-2-C5, A-2-C6, A-2-C7 | $62,500,000 | $62,500,000 | MSBNA | No |

|

|

|

| A-3-C2, A-3-C4, A-3-C5 | $62,500,000 | $62,500,000 | WFBNA | No |

|

|

|

| Total Senior Notes | $900,000,000 | $900,000,000 |

|

|

|

|

|

| B-1, B-2, B-3 | $300,000,000 | $300,000,000 | CPTS 2019-CPT | Yes | Wells Fargo | CWCapital |

|

| Total | $1,200,000,000 | $1,200,000,000 |

|

|

|

|

2 | 180 Water | A-1 | $50,000,000 | $50,000,000 | Benchmark 2019-B14 | No |

|

|

|

| A-2, A-4, A-5 | $62,500,000 | $62,500,000 | COMM 2019-GC44 | No |

|

|

|

| A-3 | $25,000,000 | $25,000,000 | DBRI | No |

|

|

|

| Total Senior Notes | $137,500,000 | $137,500,000 |

|

|

|

|

|

| B | $127,500,000 | $127,500,000 | COMM 2019-GC44 | Yes(2) | Midland | Rialto |

|

| Total | $265,000,000 | $265,000,000 |

|

|

|

|

3 | The Shoppes at Blackstone Valley | A-1 | $55,000,000 | $55,000,000 | COMM 2019-GC44 | Yes | Midland | Rialto |

|

| A-2, A-3, A-4, A-5, A-6, A-7, A-8, A-9 | $109,000,000 | $109,000,000 | GS Bank | No |

|

|

|

| Total | $164,000,000 | $164,000,000 |

|

|

|

|

5 | 225 Bush | A-1, A-6 | $60,000,000 | $60,000,000 | Benchmark 2019-B14 | No |

|

|

|

| A-2 | $50,000,000 | $50,000,000 | COMM 2019-GC44 | No |

|

|

|

| A-3, A-4, A-5 | $93,600,000 | $93,600,000 | DBRI | No |

|

|

|

| Total Senior Notes | $203,600,000 | $203,600,000 |

|

|

|

|

|

| B | $146,400,000 | $146,400,000 | Benchmark 2019-B14 | Yes(3) | Midland | Midland |

|

| Total | $350,000,000 | $350,000,000 |

|

|

|

|

6 | USAA Office Portfolio | A-1 | $62,400,000 | $62,400,000 | CGCMT 2019-GC41 | Yes | Midland | CWCapital |

|

| A-2 | $45,000,000 | $45,000,000 | GSMS 2019-GC42 | No |

|

|

|

| A-3, A-4 | $75,000,000 | $75,000,000 | CGCMT 2019-GC43 | No |

|

|

|

| A-5 | $15,000,000 | $15,000,000 | GSMS 2019-GSA1 | No |

|

|

|

| A-6, A-7, A-8 | $45,000,000 | $45,000,000 | COMM 2019-GC44 | No |

|

|

|

| Total | $242,400,000 | $242,400,000 |

|

|

|

|

7 | PCI Pharma Portfolio | A-1 | $40,000,000 | $40,000,000 | COMM 2019-GC44 | Yes | Midland | Rialto |

|

| A-2, A-3, A-4, A-5, A-6, A-7 | $68,500,000 | $68,500,000 | GS Bank | No |

|

|

|

| Total | $108,500,000 | $108,500,000 |

|

|

|

|

8 | Elston Retail Collection | A-1 | $40,000,000 | $39,918,185 | COMM 2019-GC44 | Yes | Midland | Rialto |

|

| A-2 | $30,000,000 | $29,938,639 | CREFI | No |

|

|

|

| Total | $70,000,000 | $69,856,824 |

|

|

|

|

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

COMM 2019-GC44 Mortgage Trust

|

OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Loan | Mortgage Loan | Note(s) | Original | Cut-off Date | Holder of Note | Lead | Master | Special |

10 | The Essex Site 2 | A-1-1, A-1-3 | $56,900,000 | $56,900,000 | Benchmark 2019-B14 | No | Midland | Midland |

|

| A-1-2 | $25,000,000 | $25,000,000 | JPMCB | No |

|

|

|

| A-1-4 | $35,100,000 | $35,100,000 | COMM 2019-GC44 | No |

|

|

|

| Total Senior Notes | $117,000,000 | $117,000,000 |

|

|

|

|

|

| B-1-1 | $40,600,000 | $40,600,000 | JPMCB | Yes(4) |

|

|

|

| B-1-2 | $17,400,000 | $17,400,000 | GS Bank | Yes(4) |

|

|

|

| Total | $175,000,000 | $175,000,000 |

|

|

|

|

11 | Legends at Village West | A-1 | $50,000,000 | $49,926,144 | Benchmark 2019-B14 | Yes | Midland | Midland |

|

| A-2 | $35,000,000 | $34,948,301 | COMM 2019-GC44 |

|

|

|

|

| A-3 | $35,000,000 | $34,948,301 | CREFI |

|

|

|

|

| Total | $120,000,000 | $119,822,745 |

|

|

|

|

12 | Midtown Center | A-1-1, A-1-2, A-1-3 | $261,000,000 | $261,000,000 | DC Office Trust 2019-MTC | No |

|

|

|

| A-2-1, A-2-2, A-2-3, A-2-4, A-2-5 | $88,475,000 | $88,475,000 | BANK 2019-BNK22 | No |

|

|

|

| A-2-6, A-2-7 | $32,525,000 | $32,525,000 | COMM 2019-GC44 | No |

|

|

|

| Total Senior Notes | $382,000,000 | $382,000,000 |

|

|

|

|

|

| B-1-1, B-1-2, B-1-3 | $143,000,000 | $143,000,000 | DC Office Trust 2019-MTC | Yes | Wells Fargo | CWCapital |

|

| Total | $525,000,000 | $525,000,000 |

|

|

|

|

13 | Broadcasting Square | A-1 | $32,000,000 | $32,000,000 | COMM 2019-GC44 | Yes | Midland | Rialto |

|

| A-2 | $30,000,000 | $30,000,000 | CREFI | No |

|

|

|

| Total | $62,000,000 | $62,000,000 |

|

|

|

|

15 | Cobb Place | A-1 | $25,000,000 | $25,000,000 | COMM 2019-GC44 | Yes | Midland | Rialto |

|

| A-2 | $15,000,000 | $15,000,000 | GS Bank | No |

|

|

|

| Total | $40,000,000 | $40,000,000 |

|

|

|

|

18 | Wind Creek Leased Fee | A-4, A-5-2, A-6 | $41,600,000 | $41,441,447 | Benchmark 2019-B13 | Yes | Midland | CWCapital |

|

| A-1, A-2 | $40,000,000 | $39,847,545 | CD 2019-CD8 | No |

|

|

|

| A-3 | $45,000,000 | $44,828,489 | CGCMT 2019-GC41 | No |

|

|

|

| A-5-1 | $20,000,000 | $19,923,773 | COMM 2019-GC44 | No |

|

|

|

| Total | $146,600,000 | $146,041,254 |

|

|

|

|

28 | Millennium Park Plaza | A-1 | $70,000,000 | $70,000,000 | CGCMT 2019-GC41 | Yes | Midland | Rialto |

|

| A-2 | $30,000,000 | $30,000,000 | GSMS 2019-GC42 | No |

|

|

|

| A-3, A-5 | $60,000,000 | $60,000,000 | CGCMT 2019-GC43 | No |

|

|

|

| A-4 | $35,000,000 | $35,000,000 | GSMS 2019-GSA1 | No |

|

|

|

| A-6, A-7 | $15,000,000 | $15,000,000 | COMM 2019-GC44 | No |

|

|

|

| Total | $210,000,000 | $210,000,000 |

|

|

|

|

(1) | The identification of a securitization trust means we have identified another securitization trust that has closed or as to which a preliminary prospectus (or preliminary offering circular) or final prospectus (or final offering circular) has printed that has or is expected to include the identified Mortgage Note(s). |

(2) | With respect to the 180 Water Whole Loan, the initial Control Note is Note B. During the continuance of a 180 Water Appraisal Period, Note A-1 will be the Control Note. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—180 Water Whole Loan” in the Preliminary Prospectus. |

(3) | With respect to the 225 Bush Whole Loan, the initial Control Note is Note B. During the continuance of a 225 Bush Appraisal Period, Note A-1 will be the Control Note. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—225 Bush Whole Loan” in the Preliminary Prospectus. |

(4) | With respect to The Essex Site 2 Whole Loan, the controlling noteholder is the holder of a majority of the principal balance of the B notes. During the continuance of a The Essex Site 2 Control Appraisal Period, Note A-1-1 will be the Control Note. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—The Essex Site 2 Whole Loan” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

COMM 2019-GC44 Mortgage Trust

|

OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Distribution of Cut-off Date Balances(1) |

|

|

|

|

|

|

|

|

|

| Weighted Averages | ||||||||

Range of Cut-off Date Balances |

| Number of |

| Aggregate |

| % of Initial |

| Mortgage |

| Stated |

| U/W NCF |

| Cut-off Date |

| Maturity Date | ||

$5,000,000 | - | $7,499,999 |

| 6 |

| $35,740,000 |

| 3.5% |

| 3.6924% |

| 119 |

| 2.01x |

| 63.8% |

| 62.5% |

$7,500,000 | - | $14,999,999 |

| 9 |

| $106,667,523 |

| 10.4% |

| 3.6986% |

| 119 |

| 2.39x |

| 61.9% |

| 58.0% |

$15,000,000 | - | $24,999,999 |

| 13 |

| $234,545,837 |

| 22.9% |

| 3.9566% |

| 118 |

| 1.94x |

| 66.1% |

| 59.7% |

$25,000,000 | - | $49,999,999 |

| 10 |

| $352,591,485 |

| 34.4% |

| 3.3684% |

| 106 |

| 2.60x |

| 58.1% |

| 54.2% |

$50,000,000 | - | $75,000,000 |

| 5 |

| $294,753,500 |

| 28.8% |

| 3.3597% |

| 96 |

| 3.19x |

| 45.7% |

| 44.6% |

Total/Weighted Average |

| 43 |

| $1,024,298,346 |

| 100.0% |

| 3.5463% |

| 108 |

| 2.58x |

| 56.9% |

| 53.4% | ||

Distribution of Mortgage Rates(1) |

|

|

|

|

|

|

|

|

|

| Weighted Averages | ||||||||

Range of Mortgage Rates |

| Number of |

| Aggregate |

| % of Initial |

| Mortgage |

| Stated |

| U/W NCF |

| Cut-off Date |

| Maturity Date | ||

2.7590% | - | 3.9999% |

| 37 |

| $917,759,598 |

| 89.6% |

| 3.4577% |

| 107 |

| 2.67x |

| 55.7% |

| 52.7% |

4.0000% | - | 4.2499% |

| 3 |

| $50,981,269 |

| 5.0% |

| 4.0212% |

| 119 |

| 1.98x |

| 63.8% |

| 60.4% |

4.2500% | - | 4.7499% |

| 2 |

| $37,423,773 |

| 3.7% |

| 4.3426% |

| 117 |

| 1.54x |

| 72.4% |

| 62.0% |

4.7500% | - | 5.0500% |

| 1 |

| $18,133,706 |

| 1.8% |

| 5.0500% |

| 113 |

| 1.55x |

| 69.2% |

| 52.4% |

Total/Weighted Average |

| 43 |

| $1,024,298,346 |

| 100.0% |

| 3.5463% |

| 108 |

| 2.58x |

| 56.9% |

| 53.4% | ||

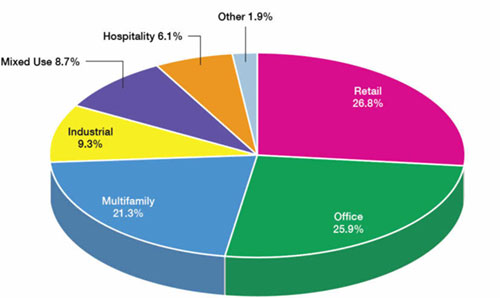

Property Type Distribution(1)(3) |

|

|

|

|

|

|

|

|

|

| Weighted Averages | ||||||||||||

Property Type |

| Number of |

| Aggregate |

| % of Initial |

| Number of |

| Cut-off Date |

| Mortgage |

| Stated |

| Occupancy |

| U/W NCF |

| Cut-off Date LTV(2)(4) |

| Maturity |

Retail |

| 10 |

| $274,463,498 |

| 26.8% |

| 2,985,464 |

| $272 |

| 3.6066% |

| 108 |

| 95.6% |

| 2.06x |

| 62.9% |

| 54.8% |

Anchored(5) |

| 8 |

| $249,763,498 |

| 24.4% |

| 2,944,852 |

| $197 |

| 3.6299% |

| 107 |

| 95.5% |

| 1.99x |

| 63.8% |

| 55.0% |

Unanchored |

| 2 |

| $24,700,000 |

| 2.4% |

| 40,612 |

| $1,032 |

| 3.3713% |

| 119 |

| 96.5% |

| 2.80x |

| 53.3% |

| 53.3% |

Office |

| 11 |

| $265,165,178 |

| 25.9% |

| 5,146,896 |

| $380 |

| 3.3454% |

| 107 |

| 97.1% |

| 3.38x |

| 47.8% |

| 46.7% |

CBD |

| 5 |

| $212,258,706 |

| 20.7% |

| 4,203,038 |

| $404 |

| 3.3389% |

| 104 |

| 96.3% |

| 3.52x |

| 43.8% |

| 42.4% |

Suburban/Suburban Flex |

| 6 |

| $52,906,472 |

| 5.2% |

| 943,858 |

| $287 |

| 3.3713% |

| 116 |

| 100.0% |

| 2.81x |

| 64.0% |

| 64.0% |

Multifamily |

| 17 |

| $218,045,000 |

| 21.3% |

| 1,478 |

| $255,689 |

| 3.6696% |

| 102 |

| 96.2% |

| 2.33x |

| 54.0% |

| 53.4% |

Garden |

| 6 |

| $71,155,000 |

| 6.9% |

| 582 |

| $147,443 |

| 3.6160% |

| 119 |

| 95.5% |

| 2.22x |

| 62.2% |

| 61.5% |

Mid Rise |

| 9 |

| $67,790,000 |

| 6.6% |

| 227 |

| $404,072 |

| 3.9054% |

| 119 |

| 96.0% |

| 1.90x |

| 64.0% |

| 64.0% |

High Rise |

| 1 |

| $62,500,000 |

| 6.1% |

| 573 |

| $239,965 |

| 3.4104% |

| 59 |

| 97.0% |

| 3.15x |

| 30.5% |

| 30.5% |

Townhomes |

| 1 |

| $16,600,000 |

| 1.6% |

| 96 |

| $172,917 |

| 3.9123% |

| 119 |

| 96.9% |

| 1.50x |

| 67.2% |

| 60.9% |

Industrial |

| 8 |

| $95,457,318 |

| 9.3% |

| 2,952,480 |

| $53 |

| 3.3879% |

| 119 |

| 98.8% |

| 2.87x |

| 62.1% |

| 65.1% |

Warehouse/Distribution |

| 2 |

| $38,221,105 |

| 3.7% |

| 1,458,560 |

| $40 |

| 3.3616% |

| 119 |

| 100.0% |

| 2.91x |

| 61.5% |

| 65.1% |

Flex |

| 4 |

| $37,821,967 |

| 3.7% |

| 968,500 |

| $40 |

| 3.4191% |

| 119 |

| 97.1% |

| 2.97x |

| 61.0% |

| 64.9% |

R&D/Flex |

| 1 |

| $18,102,929 |

| 1.8% |

| 447,000 |

| $110 |

| 3.3790% |

| 119 |

| 100.0% |

| 2.61x |

| 65.4% |

| 65.4% |

Warehouse |

| 1 |

| $1,311,317 |

| 0.1% |

| 78,420 |

| $45 |

| 3.3790% |

| 119 |

| 100.0% |

| 2.61x |

| 65.4% |

| 65.4% |

Mixed Use |

| 4 |

| $88,989,346 |

| 8.7% |

| 955,540 |

| $391 |

| 3.3037% |

| 104 |

| 98.2% |

| 2.75x |

| 56.2% |

| 53.4% |

Office/Retail |

| 2 |

| $38,889,346 |

| 3.8% |

| 190,387 |

| $235 |

| 3.6578% |

| 119 |

| 96.1% |

| 2.22x |

| 67.2% |

| 60.7% |

Multifamily/Retail |

| 1 |

| $35,100,000 |

| 3.4% |

| 205,070 |

| $571 |

| 2.7590% |

| 83 |

| 100.0% |

| 3.66x |

| 39.9% |

| 39.9% |

Multifamily/Office/Retail |

| 1 |

| $15,000,000 |

| 1.5% |

| 560,083 |

| $375 |

| 3.6600% |

| 116 |

| 99.2% |

| 2.01x |

| 65.8% |

| 65.8% |

Hospitality |

| 4 |

| $62,254,233 |

| 6.1% |

| 510 |

| $123,545 |

| 4.0267% |

| 119 |

| 79.4% |

| 2.00x |

| 63.9% |

| 51.5% |

Extended Stay |

| 2 |

| $30,481,269 |

| 3.0% |

| 229 |

| $134,299 |

| 4.1722% |

| 119 |

| 74.1% |

| 2.00x |

| 61.0% |

| 50.3% |

Full Service |

| 1 |

| $18,000,000 |

| 1.8% |

| 154 |

| $116,883 |

| 3.8390% |

| 118 |

| 89.4% |

| 2.18x |

| 69.8% |

| 58.5% |

Limited Service |

| 1 |

| $13,772,964 |

| 1.3% |

| 127 |

| $108,449 |

| 3.9500% |

| 119 |

| 78.1% |

| 1.76x |

| 62.6% |

| 45.1% |

Leased Fee |

| 1 |

| $19,923,773 |

| 1.9% |

| 2,608,541 |

| $56 |

| 4.3800% |

| 116 |

| NAP |

| 1.27x |

| 84.7% |

| 72.8% |

Total/Weighted Average |

| 55 |

| $1,024,298,346 |

| 100.0% |

|

|

|

|

| 3.5463% |

| 108 |

| 95.7% |

| 2.58x |

| 56.9% |

| 53.4% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

COMM 2019-GC44 Mortgage Trust

|

OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Geographic Distribution(1)(3) |

|

|

|

|

|

|

|

| Weighted Averages | ||||||||

State/Location |

| Number of |

| Aggregate Cut-off |

| % of Initial |

| Mortgage Rate |

| Stated |

| U/W NCF |

| Cut-off |

| Maturity Date |

California |

| 10 |

| $236,687,742 |

| 23.1% |

| 3.3566% |

| 106 |

| 3.24x |

| 47.3% |

| 46.6% |

Southern |

| 8 |

| $150,087,742 |

| 14.7% |

| 3.3514% |

| 119 |

| 3.22x |

| 49.2% |

| 48.1% |

Northern |

| 2 |

| $86,600,000 |

| 8.5% |

| 3.3655% |

| 84 |

| 3.26x |

| 44.0% |

| 44.0% |

New York |

| 9 |

| $127,390,000 |

| 12.4% |

| 3.3100% |

| 80 |

| 3.00x |

| 41.0% |

| 41.0% |

New York City |

| 9 |

| $127,390,000 |

| 12.4% |

| 3.3100% |

| 80 |

| 3.00x |

| 41.0% |

| 41.0% |

Massachusetts |

| 3 |

| $83,803,000 |

| 8.2% |

| 3.7375% |

| 119 |

| 2.01x |

| 65.9% |

| 58.6% |

Illinois |

| 5 |

| $73,430,414 |

| 7.2% |

| 3.5960% |

| 118 |

| 1.86x |

| 66.0% |

| 55.6% |

Pennsylvania |

| 3 |

| $70,026,701 |

| 6.8% |

| 3.5637% |

| 118 |

| 2.64x |

| 64.6% |

| 61.2% |

Kentucky |

| 3 |

| $52,253,500 |

| 5.1% |

| 3.3530% |

| 119 |

| 3.06x |

| 59.5% |

| 65.0% |

Other |

| 22 |

| $380,706,989 |

| 37.2% |

| 3.7149% |

| 110 |

| 2.21x |

| 62.7% |

| 57.1% |

Total/Weighted Average |

| 55 |

| $1,024,298,346 |

| 100.0% |

| 3.5463% |

| 108 |

| 2.58x |

| 56.9% |

| 53.4% |

Distribution of Cut-off Date LTVs(1)(2)(4) |

|

|

|

|

|

|

|

|

|

| Weighted Averages | ||||||||

Range of Cut-off Date LTVs |

| Number of |

| Aggregate Cut-off |

| % of Initial |

| Mortgage Rate |

| Stated |

| U/W NCF |

| Cut-off Date |

| Maturity Date | ||

30.5% | - | 54.9% |

| 10 |

| $361,496,301 |

| 35.3% |

| 3.2408% |

| 91 |

| 3.44x |

| 40.9% |

| 40.4% |

55.0% | - | 59.9% |

| 4 |

| $123,878,500 |

| 12.1% |

| 3.5719% |

| 119 |

| 2.58x |

| 58.5% |

| 59.6% |

60.0% | - | 64.9% |

| 13 |

| $166,014,523 |

| 16.2% |

| 3.6920% |

| 118 |

| 2.29x |

| 63.2% |

| 60.5% |

65.0% | - | 69.9% |

| 12 |

| $293,786,891 |

| 28.7% |

| 3.7498% |

| 118 |

| 1.91x |

| 67.5% |

| 60.0% |

70.0% | - | 84.7% |

| 4 |

| $79,122,131 |

| 7.7% |

| 3.8405% |

| 107 |

| 1.68x |

| 75.0% |

| 63.3% |

Total/Weighted Average |

| 43 |

| $1,024,298,346 |

| 100.0% |

| 3.5463% |

| 108 |

| 2.58x |

| 56.9% |

| 53.4% | ||

Distribution of Maturity Date or ARD LTVs(1)(2) |

|

|

|

|

|

|

|

|

|

| Weighted Averages | ||||||||

Range of Maturity Date or ARD LTVs |

| Number of |

| Aggregate Cut-off |

| % of Initial |

| Mortgage Rate |

| Stated |

| U/W NCF DSCR |

| Cut-off Date |

| Maturity Date or | ||

30.5% | - | 49.9% |

| 9 |

| $361,264,449 |

| 35.3% |

| 3.3523% |

| 91 |

| 3.12x |

| 43.4% |

| 39.7% |

50.0% | - | 54.9% |

| 6 |

| $102,537,976 |

| 10.0% |

| 3.6992% |

| 118 |

| 2.81x |

| 56.1% |

| 51.5% |

55.0% | - | 59.9% |

| 7 |

| $168,573,358 |

| 16.5% |

| 3.7226% |

| 119 |

| 1.92x |

| 65.4% |

| 57.3% |

60.0% | - | 72.8% |

| 21 |

| $391,922,563 |

| 38.3% |

| 3.6092% |

| 116 |

| 2.29x |

| 66.0% |

| 64.8% |

Total/Weighted Average |

| 43 |

| $1,024,298,346 |

| 100.0% |

| 3.5463% |

| 108 |

| 2.58x |

| 56.9% |

| 53.4% | ||

Distribution of Underwritten NCF Debt Service Coverages(1) |

|

|

|

|

|

|

|

|

|

| Weighted Averages | ||||||||

Range of Underwritten NCF Debt Service Coverages |

| Number of |

| Aggregate Cut-off |

| % of Initial |

| Mortgage Rate |

| Stated |

| U/W NCF DSCR |

| Cut-off Date |

| Maturity Date | ||

1.27x | - | 1.44x |

| 2 |

| $59,841,958 |

| 5.8% |

| 3.8930% |

| 118 |

| 1.38x |

| 72.6% |

| 55.8% |

1.45x | - | 1.74x |

| 6 |

| $149,406,019 |

| 14.6% |

| 3.9938% |

| 104 |

| 1.58x |

| 65.0% |

| 55.0% |

1.75x | - | 2.49x |

| 21 |

| $332,938,579 |

| 32.5% |

| 3.7187% |

| 116 |

| 2.08x |

| 64.8% |

| 60.5% |

2.50x | - | 3.49x |

| 9 |

| $257,486,790 |

| 25.1% |

| 3.4016% |

| 104 |

| 2.94x |

| 53.1% |

| 54.2% |

3.50x | - | 4.09x |

| 5 |

| $224,625,000 |

| 21.9% |

| 3.0664% |

| 100 |

| 3.87x |

| 40.1% |

| 40.1% |

Total/Weighted Average |

| 43 |

| $1,024,298,346 |

| 100.0% |

| 3.5463% |

| 108 |

| 2.58x |

| 56.9% |

| 53.4% | ||

Original Terms to Maturity or ARD(1) |

|

|

|

|

|

|

|

|

|

| Weighted Averages | ||||||||

Original Terms to Maturity or ARD |

| Number of |

| Aggregate Cut-off |

| % of Initial |

| Mortgage Rate |

| Stated |

| U/W NCF DSCR |

| Cut-off Date |

| Maturity Date | ||

60 | - | 84 |

| 5 |

| $207,548,301 |

| 20.3% |

| 3.3659% |

| 66 |

| 3.01x |

| 42.1% |

| 40.4% |

120 | - | 121 |

| 38 |

| $816,750,046 |

| 79.7% |

| 3.5921% |

| 119 |

| 2.47x |

| 60.7% |

| 56.7% |

Total/Weighted Average |

| 43 |

| $1,024,298,346 |

| 100.0% |

| 3.5463% |

| 108 |

| 2.58x |

| 56.9% |

| 53.4% | ||

Distribution of Remaining Terms to Maturity or ARD(1) |

|

|

|

|

|

|

|

|

|

| Weighted Averages | ||||||||

Range of Remaining Terms to Maturity or ARD |

| Number of |

| Aggregate Cut-off |

| % of Initial |

| Mortgage Rate |

| Stated |

| U/W NCF DSCR |

| Cut-off Date |

| Maturity Date | ||

59 | - | 83 |

| 5 |

| $207,548,301 |

| 20.3% |

| 3.3659% |

| 66 |

| 3.01x |

| 42.1% |

| 40.4% |

113 | - | 119 |

| 38 |

| $816,750,046 |

| 79.7% |

| 3.5921% |

| 119 |

| 2.47x |

| 60.7% |

| 56.7% |

Total/Weighted Average |

| 43 |

| $1,024,298,346 |

| 100.0% |

| 3.5463% |

| 108 |

| 2.58x |

| 56.9% |

| 53.4% | ||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

COMM 2019-GC44 Mortgage Trust

|

OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Distribution of Underwritten NOI Debt Yields(1)(4) |

|

|

|

|

|

|

|

|

|

| Weighted Averages | ||||||||

Range of Underwritten NOI Debt Yields |

| Number of |

| Aggregate Cut-off |

| % of Initial |

| Mortgage Rate |

| Stated |

| U/W NCF DSCR |

| Cut-off Date |

| Maturity Date | ||

7.1% | - | 8.9% |

| 16 |

| $251,736,958 |

| 24.6% |

| 3.7636% |

| 119 |

| 1.91x |

| 65.2% |

| 60.8% |

9.0% | - | 9.9% |

| 9 |

| $247,337,313 |

| 24.1% |

| 3.6061% |

| 110 |

| 2.18x |

| 62.9% |

| 58.5% |

10.0% | - | 12.4% |

| 11 |

| $304,661,100 |

| 29.7% |

| 3.4096% |

| 100 |

| 2.77x |

| 53.6% |

| 51.1% |

12.5% | - | 14.1% |

| 7 |

| $220,562,976 |

| 21.5% |

| 3.4200% |

| 105 |

| 3.50x |

| 45.4% |

| 42.4% |

Total/Weighted Average |

| 43 |

| $1,024,298,346 |

| 100.0% |

| 3.5463% |

| 108 |

| 2.58x |

| 56.9% |

| 53.4% | ||

Amortization Types(1) |

|

|

|

|

|

|

|

| Weighted Averages | ||||||||

Amortization Type |

| Number of |

| Aggregate Cut-off |

| % of Initial |

| Mortgage Rate |

| Stated |

| U/W NCF DSCR |

| Cut-off Date |

| Maturity Date |

Interest Only |

| 27 |

| $647,046,790 |

| 63.2% |

| 3.3923% |

| 106 |

| 2.98x |

| 52.2% |

| 52.7% |

Amortizing Balloon |

| 8 |

| $173,876,556 |

| 17.0% |

| 3.9903% |

| 106 |

| 1.62x |

| 66.5% |

| 52.7% |

Interest Only, then Amortizing |

| 7 |

| $170,850,000 |

| 16.7% |

| 3.7653% |

| 114 |

| 1.76x |

| 68.3% |

| 59.4% |

Interest Only, ARD |

| 1 |

| $32,525,000 |

| 3.2% |

| 3.0850% |

| 118 |

| 3.98x |

| 39.8% |

| 39.8% |

Total/Weighted Average |

| 43 |

| $1,024,298,346 |

| 100.0% |

| 3.5463% |

| 108 |

| 2.58x |

| 56.9% |

| 53.4% |

Footnotes:

(1) | The U/W NCF DSCR, Cut-off Date LTV Ratio, Maturity Date or ARD LTV, Underwritten NOI Debt Yield and Cut-off Date Balance per # of NRA/Units/Rooms calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

(2) | With respect to 5 mortgage loans (15.2%) (including Weston Kentucky Portfolio, 55 Green Street, Legends at Village West, Embassy Suites Laredo and Hampton Inn Summerlin), the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated using a value other than the “As Is” appraised values. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

(3) | Reflects allocated loan amount for properties securing multi-property Mortgage Loans. |

(4) | With respect to the Weston Kentucky Portfolio mortgage loan (5.1%) the Cut-off Date LTV and U/W NOI Debt Yield are calculated based on the Cut-off Date Balance net of a related earnout reserve. |

(5) | Anchored retail includes one power center property. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

COMM 2019-GC44 Mortgage Trust |

|

STRUCTURE OVERVIEW |

Allocation between VRR Interest and the Non-VRR Certificates: |

| The aggregate amount available for distribution to holders of the Pooled Certificates (including the VRR Interest) on each Distribution Date will be: (i) the gross amount of interest, principal, yield maintenance charges and prepayment premiums collected with respect to the Mortgage Loans in the applicable one-month collection period, net of specified expenses of the issuing entity, including fees payable therefrom to, and losses, liabilities, costs and expenses reimbursable or indemnifiable therefrom to, the Master Servicer, the Special Servicer, the Certificate Administrator, the Trustee, the Operating Advisor, the Asset Representations Reviewer and CREFC®; and (ii) allocated to amounts available for distribution to the holders of the VRR Interest, on the one hand, and amounts available for distribution to the holders of the remaining Pooled Certificates (the “Non-VRR Certificates”), on the other hand. On each Distribution Date, the portion of such pooled aggregate available funds allocable to: (a) the VRR Interest will be the product of such pooled aggregate available funds multiplied by a fraction, expressed as a percentage, the numerator of which is the initial VRR Interest Balance, and the denominator of which is the aggregate initial Certificate Balances of the Pooled Principal Balance Certificates and the initial VRR Interest Balance (the “VRR Percentage”); and (b) the Non-VRR Certificates will at all times be the product of such aggregate available funds multiplied by the difference between 100% and the VRR Percentage (such difference, the “Non-VRR Percentage”). See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus.

|

Principal Payments: |

| Payments in respect of the Non-VRR Percentage of principal on the Non-VRR Certificates will be distributed, first, to the Class A-SB certificates, until the Certificate Balance of such class is reduced to the planned principal balance for the related Distribution Date set forth on Annex F to the Preliminary Prospectus, then, to the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-SB, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G-RR and Class H-RR certificates, in that order, until the Certificate Balance of each such class is reduced to zero. Notwithstanding the foregoing, if the total Certificate Balance of the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G-RR and Class H-RR certificates have been reduced to zero as a result of loss allocation, payments in respect of principal of the certificates will be distributed, first, to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-5 certificates, on a pro rata basis, based on the Certificate Balance of each such class, then, to the extent of any recoveries on realized losses, to the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G-RR and Class H-RR certificates, in that order, in each case until the Certificate Balance of each such class is reduced to zero (or previously allocated realized losses have been fully reimbursed).

Each class of Class X Certificates will not be entitled to receive distributions of principal; however, (i) the notional amount of the Class X-A certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5 and Class A-M certificates; (ii) the notional amount of the Class X-B certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class B and Class C certificates; (iii) the notional amount of the Class X-D certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class D and Class E certificates; and (iv) the notional amount of the Class X-F certificates will be reduced by the principal distributions and realized losses allocated to the Class F certificates.

The holders of the Loan-Specific Certificates will only be entitled to distributions from amounts paid or advanced on and allocated to the Trust Subordinate Companion Loan in accordance with the co-lender agreement relating to the 180 Water Whole Loan and no class of Pooled Certificates will be entitled to distributions paid or advanced on and allocable to the Trust Subordinate Companion Loan.

|

Interest Payments: |

| On each Distribution Date, interest accrued for each class of Non-VRR Certificates at the applicable pass-through rate will be distributed in the following order of priority, to the extent of the Non-VRR Percentage of the pooled aggregate available funds (exclusive of any portion thereof that represents the Non-VRR Percentage of any yield maintenance charges and prepayment premiums): first, to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5, Class X-A, Class X-B, Class X-D and Class X-F certificates, on a pro rata basis, based on the accrued and unpaid interest on each such class and then, to the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G-RR and Class H-RR certificates, in that order, in each case until the interest payable to each such class is paid in full. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

COMM 2019-GC44 Mortgage Trust |

|

STRUCTURE OVERVIEW |

|

| The pass-through rates applicable to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G-RR and Class H-RR certificates for each Distribution Date will equal one of: (i) a fixed per annum rate, (ii) the WAC Rate, (iii) a rate equal to the lesser of a specified pass-through rate and the WAC Rate or (iv) the WAC Rate less a specified rate.

As further described in the Preliminary Prospectus, the pass-through rates applicable to the Class X Certificates for each Distribution Date will generally be equal to the excess of (i) the WAC Rate over (ii) (A) with respect to the Class X-A certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5 and Class A-M certificates (weighted based on their respective Certificate Balances immediately prior to that Distribution Date), (B) with respect to the Class X-B certificates, the weighted average of the pass-through rates of the Class B and Class C certificates (weighted based on their respective Certificate Balances immediately prior to that Distribution Date), (C) with respect to the Class X-D certificates, the weighted average of the pass-through rates of the Class D and Class E certificates (weighted based on their respective Certificate Balances immediately prior to that Distribution Date) and (D) with respect to the Class X-F certificates, the pass-through rate of the Class F certificates.

No class of Pooled Certificates will be entitled to distributions paid or advanced on and allocable to the Trust Subordinate Companion Loan. The holders of the Loan-Specific Certificates will only be entitled to distributions from amounts paid or advanced on and allocated to the Trust Subordinate Companion Loan in accordance with the co-lender agreement relating to the 180 Water Whole Loan.

|

Prepayment Interest Shortfalls: |

| Prepayment interest shortfalls will be allocated pro rata based on interest entitlements, in reduction of the interest otherwise payable with respect to each of the interest-bearing classes of certificates.

|

Loss Allocation: |

| The Non-VRR Percentage of losses on the Mortgage Loans will be allocated to each class of Non-VRR Certificates entitled to principal in reverse alphabetical order starting with Class H-RR certificates through and including Class A-M certificates and then to Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-5 certificates on a pro rata basis based on the Certificate Balance of each such class. The notional amount of any class of Class X Certificates will be reduced by the aggregate amount of realized losses allocated to the class(es) of certificates that are component(s) of the notional amount of such class of Class X Certificates.

Losses realized on the Trust Subordinate Companion Loan generally will be allocated to the Loan-Specific Certificates.

|

Prepayment Premiums:

|