As filed with the Securities and Exchange Commission on July 13, 2020

Registration No. 333-239291

Delaware | | | 6331 | | | 84-4512647 |

(State or other jurisdiction of incorporation or organization) | | | (Primary Standard Industrial Classification Code Number) | | | (I.R.S. Employer Identification Number) |

Dwight S. Yoo Skadden, Arps, Slate, Meagher & Flom LLP One Manhattan West New York, New York 10001 (212) 735-3000 | | | Richard D. Truesdell, Jr. Shane Tintle Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 |

Large accelerated filer | | | ☐ | | | Accelerated filer | | | ☐ |

Non-accelerated filer | | | ☒ | | | Smaller reporting company | | | ☐ |

| | | | | Emerging growth company | | | ☒ |

| | | Per Share | | | Total | |

Initial public offering price | | | $ | | | $ |

Underwriting discounts and commissions(1) | | | $ | | | $ |

Proceeds, before expenses, to us | | | $ | | | $ |

Proceeds, before expenses, to the selling stockholders | | | $ | | | $ |

| (1) | See “Underwriting” for a description of the compensation payable to the underwriters. |

Joint Book-Running Managers | ||||||

J.P. Morgan | | | Evercore ISI | | | William Blair |

Co-Manager | |||

JMP Securities |

| | | Page | |

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | |

(1) | Return on tangible equity is a non-GAAP financial measure. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of return on tangible equity to return on equity in accordance with U.S. generally accepted accounting principles (“GAAP”). |

(2) | Adjusted net income is a non-GAAP financial measure. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted net income to net income in accordance with GAAP. |

(3) | Adjusted return on equity is a non-GAAP financial measure defined as adjusted net income expressed on an annualized basis as a percentage of average beginning and ending members’ equity during the period. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted return on equity to return on equity in accordance with GAAP. |

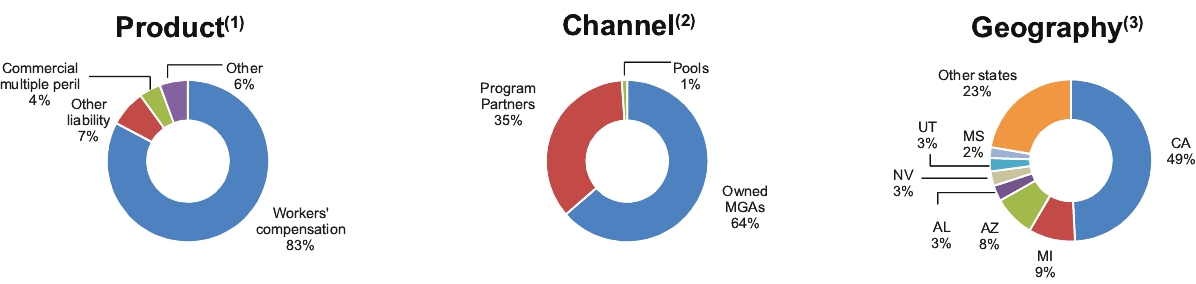

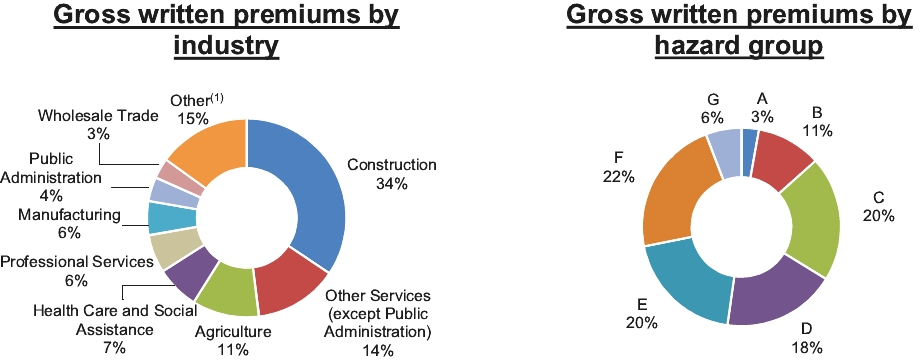

(1) | Other includes group accident & health, commercial auto liability, auto physical damage, private passenger auto liability, boiler and machinery, surety, fire and inland marine. |

(2) | Pools are state insurance pools. |

(3) | Other states include Montana, Tennessee, New Jersey and other U.S. geographical areas. |

| • | failure of our Program Partners or our Owned MGAs to properly market, underwrite or administer policies could adversely affect us; |

| • | we depend on a limited number of Program Partners for a substantial portion of our gross written premiums; |

| • | more than half of our gross written premiums are written in three key states; |

| • | a downgrade in the A.M. Best financial strength ratings of our insurance company subsidiaries may negatively affect our business; |

| • | if we are unable to accurately underwrite risks and charge competitive yet profitable rates to our clients and policyholders, our business, financial condition and results of operations may be materially and adversely affected; |

| • | adverse economic factors, including recession, inflation, periods of high unemployment or lower economic activity could result in the sale of fewer policies than expected or an increase in frequency or severity of claims and premium defaults or both, which, in turn, could affect our growth and profitability; |

| • | negative developments in the workers’ compensation insurance industry could adversely affect our business, financial condition and results of operations; |

| • | our failure to accurately and timely pay claims could harm our business; |

| • | we are subject to reinsurance counterparty credit risk and our reinsurers may not pay on losses in a timely fashion, or at all; |

| • | if we are unable to obtain reinsurance coverage at reasonable prices or on terms that adequately protect us, we may be required to bear increased risks or reduce the level of our underwriting commitments; |

| • | retention of business written by our Program Partners could expose us to potential losses; |

| • | our loss reserves may be inadequate to cover our actual losses; |

| • | we may not be able to manage our growth effectively; |

| • | any shift in our investment strategy could increase the riskiness of our investment portfolio and the volatility of our results, which, in turn, may adversely affect our profitability; |

| • | our results of operations, liquidity, financial condition and FSRs are subject to the effects of natural and man-made catastrophic events; |

| • | disruptions related to COVID-19, including economic impacts of the COVID-19-related governmental actions, could materially and adversely affect our business, financial condition and results of operations; |

| • | because our business depends on insurance brokers, we are exposed to certain risks arising out of our reliance on these distribution channels that could adversely affect our results; |

| • | regulators may challenge our use of fronting arrangements in states in which our Program Partners are not licensed; |

| • | our principal stockholders will be able to exert significant influence over us and our corporate decisions; |

| • | our principal stockholders could sell their interests in us to a third party in a private transaction, which may result in your not realizing any change-of-control premium on your shares and subject us to the influence of a currently unknown third party; and |

| • | we will incur significant increased costs as a result of operating as a public company, and operating as a public company will place additional demands on our management. |

| • | we may present as few as two years of audited financial statements and two years of related management’s discussion and analysis of financial condition and results of operations in this prospectus; |

| • | we are exempt from the requirement to obtain an attestation report from our auditors on management’s assessment of our internal control over financial reporting under the Sarbanes-Oxley Act of 2002 for up to five years or until we no longer qualify as an emerging growth company; |

| • | we are permitted to provide reduced disclosure regarding our executive compensation arrangements pursuant to the rules applicable to smaller reporting companies, which means we do not have to include a compensation discussion and analysis and certain other disclosures regarding our executive compensation; and |

| • | we are not required to hold non-binding advisory votes on executive compensation. |

| • | assumes that the initial public offering price of the common stock will be $14.00 per share (the midpoint of the price range set forth on the cover of this prospectus); |

| • | gives effect to the completion of the reorganization transactions; and |

| • | assumes no exercise of the option granted to the underwriters to purchase up to an additional 1,607,142 shares of our common stock to cover over-allotments. |

| | | Three months ended March 31, | | | Year ended December 31, | |||||||

| | | 2020 | | | 2019 | | | 2019 | | | 2018 | |

| | | (in thousands) | ||||||||||

Revenues: | | | | | | | | | ||||

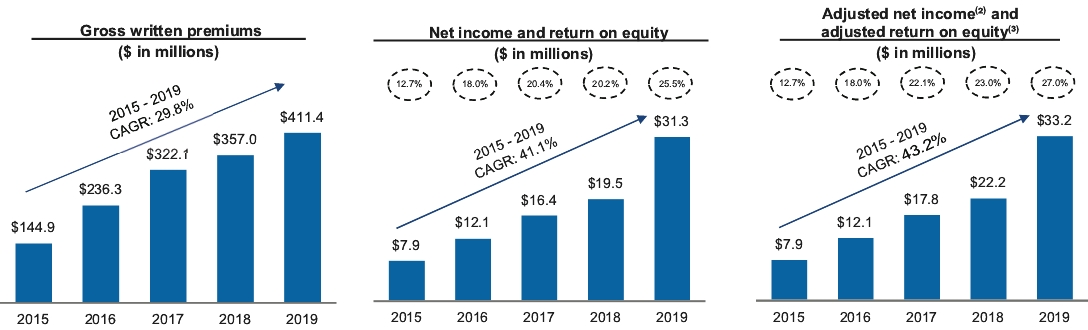

Gross written premiums | | | $107,859 | | | $101,534 | | | $411,401 | | | $357,007 |

Increase in gross unearned premiums | | | (7,373) | | | (10,952) | | | (13,598) | | | (16,862) |

Gross earned premiums | | | 100,486 | | | 90,582 | | | 397,803 | | | 340,145 |

Ceded earned premiums | | | (78,027) | | | (70,958) | | | (311,325) | | | (273,569) |

Net earned premiums | | | 22,459 | | | 19,624 | | | 86,478 | | | 66,576 |

Net investment income | | | 3,272 | | | 1,287 | | | 6,245 | | | 4,816 |

Net realized capital gains (losses) | | | 3,234 | | | 612 | | | 667 | | | (715) |

Other revenue | | | 4,392 | | | 3,595 | | | 9,125 | | | 7,826 |

Total revenue | | | 33,357 | | | 25,118 | | | 102,515 | | | 78,503 |

| | | | | | | | | |||||

Expenses: | | | | | | | | | ||||

Losses and loss adjustment expenses | | | 12,934 | | | 11,456 | | | 44,661 | | | 35,729 |

General and administrative expenses | | | 8,160 | | | 3,969 | | | 21,005 | | | 15,706 |

Interest expense | | | 461 | | | 624 | | | 2,169 | | | 1,557 |

Total expenses | | | 21,555 | | | 16,049 | | | 67,835 | | | 52,992 |

| | | | | | | | | |||||

Other income | | | 14 | | | 93 | | | 121 | | | 639 |

Income before taxes | | | 11,816 | | | 9,162 | | | 34,801 | | | 26,150 |

| | | | | | | | | |||||

Provision for income taxes | | | 2,912 | | | 1,319 | | | 7,074 | | | 5,546 |

Equity earnings (losses) in affiliates, net of tax | | | 702 | | | 608 | | | 3,558 | | | (1,082) |

Net income | | | $9,606 | | | $8,451 | | | $31,285 | | | $19,522 |

Adjusted net income(1) | | | $6,602 | | | $8,369 | | | $33,194 | | | $22,197 |

| | | Three months ended March 31, 2020 | | | Year ended December 31, 2019 | |

Pro forma per share data(2): | | | | | ||

Pro forma earnings (loss) per share outstanding | | | | | ||

Basic and diluted | | | $0.20 | | | $0.68 |

Pro forma weighted average shares outstanding | | | | | ||

Basic and diluted | | | 51,142,857 | | | 51,142,857 |

| (1) | Adjusted net income is a non-GAAP financial measure. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted net income to net income in accordance with GAAP. |

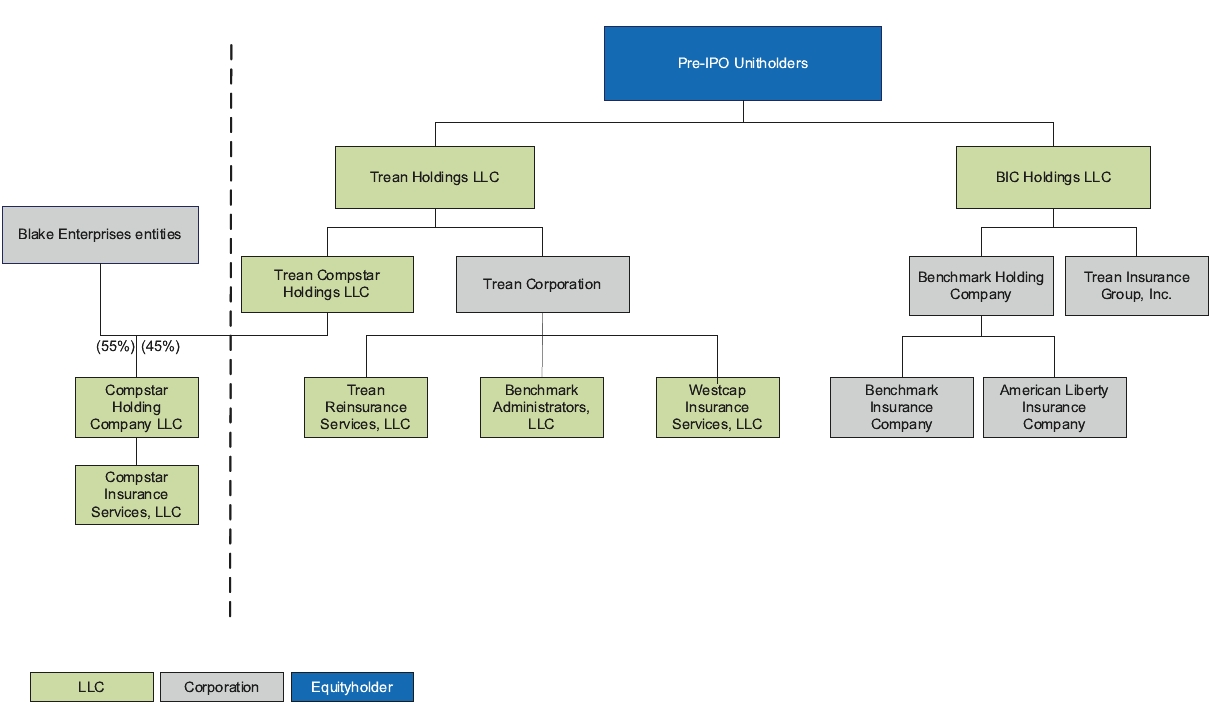

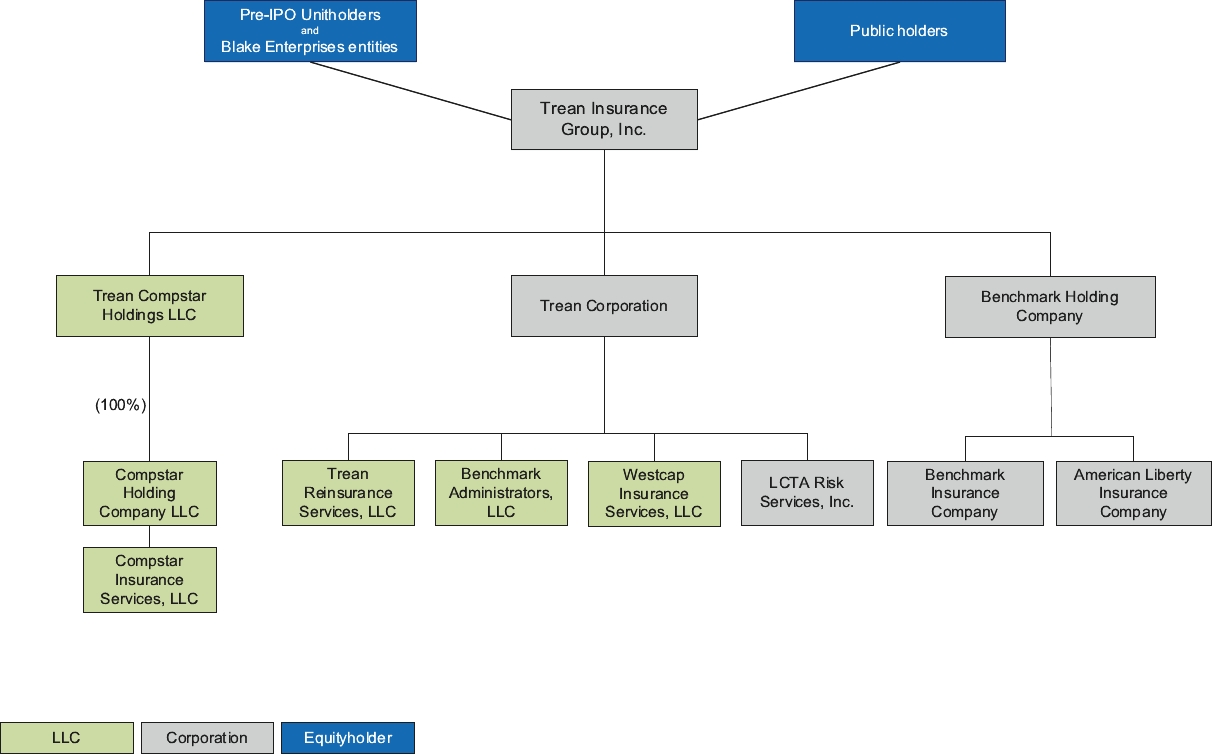

| (2) | Pro forma earnings per share outstanding gives pro forma effect to: (a) the issuance of 37,386,394 shares of our common stock to Trean Holdings and BIC Holdings in exchange for the contribution of all of their respective assets and liabilities to Trean Insurance Group, Inc., (b) the issuance of 6,613,606 shares of our common stock in connection with the acquisition from the Blake Enterprises entities of their 55% equity interest in Compstar, (c) the issuance of 7,142,857 shares of our common stock by us in the IPO and (d) equity in the net income of Compstar (net of tax) for the 55% that we do not currently own as if we had owned 100% of Compstar at the beginning of the period. See “Organizational structure.” See “Selected historical combined financial and other data” for the calculation of pro forma earnings per share outstanding. |

| | | At March 31, 2020 | | | At December 31, | ||||

| | | 2019 | | | 2018 | ||||

| | | (in thousands) | |||||||

Balance sheet data: | | | | | | | |||

Accrued investment income | | | $2,420 | | | $2,468 | | | $2,372 |

Premiums and other receivables | | | 67,773 | | | 62,460 | | | 62,400 |

Related party receivables | | | 21,871 | | | 22,221 | | | 15,934 |

Reinsurance recoverable | | | 313,760 | | | 307,338 | | | 257,509 |

Prepaid reinsurance premiums | | | 83,694 | | | 80,088 | | | 66,765 |

Deferred policy acquisition cost, net | | | 3,103 | | | 2,115 | | | 2,976 |

Property and equipment, net | | | 8,238 | | | 7,937 | | | 8,134 |

Deferred tax asset | | | 1,280 | | | 1,367 | | | 1,823 |

Goodwill | | | 2,822 | | | 2,822 | | | 2,822 |

Other assets | | | 7,572 | | | 3,277 | | | 1,963 |

Total assets | | | 954,583 | | | 919,034 | | | 800,119 |

Unpaid loss and loss adjustment expenses | | | 418,757 | | | 406,716 | | | 340,415 |

Unearned premiums | | | 111,162 | | | 103,789 | | | 90,074 |

Funds held under reinsurance agreements | | | 165,018 | | | 163,445 | | | 166,838 |

Reinsurance premiums payable | | | 48,099 | | | 53,620 | | | 40,135 |

Accounts payable and accrued expenses | | | 18,360 | | | 14,995 | | | 15,004 |

Total liabilities | | | 799,302 | | | 772,319 | | | 688,988 |

Redeemable preferred stock | | | 5,100 | | | 5,100 | | | 6,000 |

Total members’ equity | | | 150,181 | | | 141,615 | | | 105,131 |

Total liabilities and members’ equity | | | 954,583 | | | 919,034 | | | 800,119 |

| | | Three months ended March 31, | | | Year ended December 31, | |||||||

| | | 2020 | | | 2019 | | | 2019 | | | 2018 | |

Underwriting and other ratios: | | | | | | | | | ||||

Loss ratio(1) | | | 57.6% | | | 58.4% | | | 51.6% | | | 53.7% |

Expense ratio(2) | | | 36.3% | | | 20.2% | | | 24.3% | | | 23.6% |

Combined ratio(3) | | | 93.9% | | | 78.6% | | | 75.9% | | | 77.3% |

Return on equity(4) | | | 26.3% | | | 30.5% | | | 25.5% | | | 20.2% |

Adjusted return on equity(5) | | | 18.1% | | | 30.2% | | | 27.0% | | | 23.0% |

Return on tangible equity(6) | | | 26.9% | | | 31.4% | | | 26.1% | | | 20.6% |

Adjusted return on tangible equity(7) | | | 18.5% | | | 31.1% | | | 27.7% | | | 23.4% |

| (1) | The loss ratio is the ratio, expressed as a percentage, of losses and loss adjustment expenses to net earned premiums. |

| (2) | The expense ratio is the ratio, expressed as a percentage, of general and administrative expenses to net earned premiums. |

| (3) | The combined ratio is the sum of the loss ratio and the expense ratio. A combined ratio under 100% generally indicates an underwriting profit. A combined ratio over 100% generally indicates an underwriting loss. |

| (4) | Return on equity represents net income expressed on an annualized basis as a percentage of average beginning and ending members’ equity during the period. |

| (5) | Adjusted return on equity is a non-GAAP financial measure defined as adjusted net income expressed on an annualized basis as a percentage of average beginning and ending members’ equity during the period. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted return on equity to return on equity in accordance with GAAP. |

| (6) | Return on tangible equity is a non-GAAP financial measure defined as net income expressed on an annualized basis as a percentage of average beginning and ending tangible members’ equity during the period. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of return on tangible equity to return on equity in accordance with GAAP. |

| (7) | Adjusted return on tangible equity is a non-GAAP financial measure defined as adjusted net income expressed on an annualized basis as a percentage of average beginning and ending tangible members’ equity during the period. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted return on tangible equity to return on tangible equity in accordance with GAAP. |

| • | collect and properly analyze a substantial volume of data from our insureds; |

| • | develop, test and apply appropriate actuarial projections and ratings formulas; |

| • | closely monitor and timely recognize changes in trends; and |

| • | project both frequency and severity of our insureds’ losses with reasonable accuracy. |

| • | insufficient or unreliable data; |

| • | incorrect or incomplete analysis of available data; |

| • | uncertainties generally inherent in estimates and assumptions; |

| • | our failure to implement appropriate actuarial projections and ratings formulas or other pricing methodologies; |

| • | regulatory constraints on rate increases; |

| • | our failure to accurately estimate investment yields and the duration of our liability for losses and LAE; and |

| • | unanticipated court decisions, legislation or regulatory action. |

| • | judicial expansion of policy coverage and the impact of new theories of liability; |

| • | plaintiffs targeting property and casualty (“P&C”) insurers in purported class action litigation relating to claims-handling and other practices; |

| • | medical developments that link health issues to particular causes, resulting in liability claims; and |

| • | claims relating to unanticipated consequences of current or new technologies, including cyber-security related risks and claims relating to potentially changing climate conditions. |

| • | the terms of the reinsurance contract do not reflect the intent of the parties of the contract or there is a disagreement between the parties as to their intent; |

| • | the terms of the contract cannot be legally enforced; |

| • | the terms of the contract are interpreted by a court or arbitration panel differently than intended; |

| • | the reinsurance transaction performs differently than we anticipated due to a flawed design of the reinsurance structure, terms or conditions; or |

| • | a change in laws and regulations, or in the interpretation of the laws and regulations, materially affects a reinsurance transaction. |

| • | loss emergence and cedant reporting patterns; |

| • | underlying policy terms and conditions; |

| • | business and exposure mix; |

| • | trends in claim frequency and severity; |

| • | changes in operations; |

| • | emerging economic and social trends; |

| • | inflation; and |

| • | changes in the regulatory and litigation environments. |

| • | widespread claim costs associated with P&C and workers’ compensation claims; |

| • | losses resulting from a decline in the value of our invested assets; |

| • | losses resulting from actual policy experience that is adverse compared to the assumptions made in product pricing; |

| • | declines in value and/or losses with respect to companies and other entities whose securities we hold and counterparties with whom we transact business to whom we have credit exposure, including reinsurers, and declines in the value of investments; and |

| • | significant interruptions to our systems and operations. |

| • | Legislative or regulatory action seeking to retroactively mandate coverage for losses, which our policies would not otherwise cover or have been priced to cover; |

| • | Regulatory actions relaxing reporting requirements for claims, which may affect coverage under our claims made and reported policies; |

| • | Legislative actions prohibiting us from cancelling policies in accordance with our policy terms or non-renewing policies at their expiration date; |

| • | Legislative orders to provide premium refunds, extend premium payment grace periods and allow time extensions for past due premium payments; |

| • | We may have increased workers’ compensation loss expense and claims frequency if policyholder employees in high risk roles with essential businesses contract COVID-19 in the workplace; |

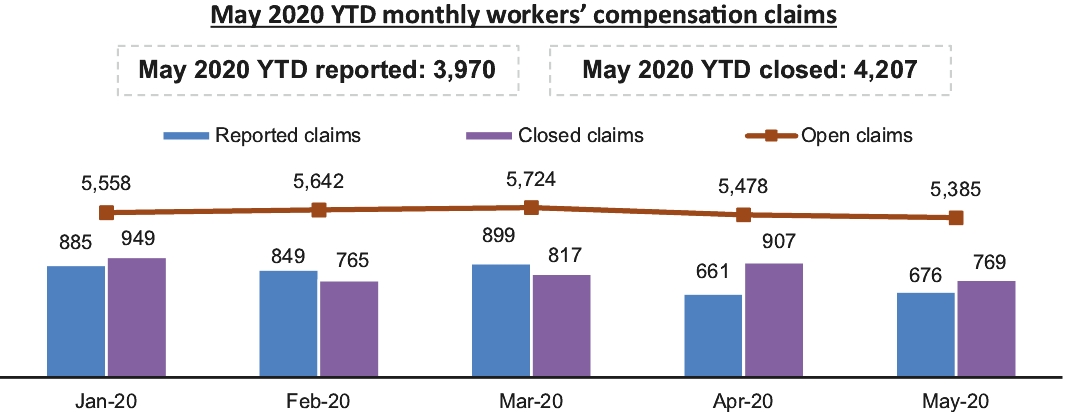

| • | While we have seen through the two months ended May 31, 2020 fewer claims reported despite insuring more employees and have not seen a significant impact on the average value of incurred losses due to the COVID-19 pandemic, high unemployment and low interest rates could adversely affect our profitability and declining payrolls could adversely affect our workers' compensation written premiums; |

| • | Travel restrictions and quarantines leading to a lack of in-person meetings, which would hinder our ability to establish relationships or originate new business; |

| • | Alternative working arrangements, including employees working remotely, which could negatively impact our business should such arrangements remain for an extended period of time; |

| • | We may experience elevated frequency and severity in our workers’ compensation lines as a result of legislative or regulatory action to effectively expand workers’ compensation coverage for certain types of workers; and |

| • | We may experience delayed reporting of losses, settlement negotiations and disputed claims resolution above our normal claims resolution trends. |

| • | approval of policy forms and premium rates; |

| • | standards of solvency, including risk-based capital measurements; |

| • | licensing of insurers; |

| • | challenging our use of fronting arrangements in states in which our Program Partner is not licensed; |

| • | imposing minimum capital and surplus requirements for insurance company subsidiaries; |

| • | restrictions on agreements with our large revenue-producing agents; |

| • | cancellation and non-renewal of policies; |

| • | restrictions on the nature, quality and concentration of investments; |

| • | restrictions on the ability of our insurance company subsidiaries to pay dividends to us; |

| • | restrictions on transactions between our insurance company subsidiaries and their affiliates; |

| • | restrictions on the size of risks insurable under a single policy; |

| • | requiring deposits for the benefit of policyholders; |

| • | requiring certain methods of accounting; |

| • | periodic examinations of our operations and finances; |

| • | prescribing the form and content of records of financial condition required to be filed; and |

| • | requiring reserves for unearned premium, losses and other purposes. |

| • | our operating and financial performance and prospects; |

| • | our announcements or our competitors’ announcements regarding new products or services, enhancements, significant contracts, acquisitions or strategic investments; |

| • | changes in earnings estimates or recommendations by securities analysts who cover our common stock; |

| • | fluctuations in our quarterly financial results or earnings guidance or the quarterly financial results or earnings guidance of companies perceived to be similar to us; |

| • | changes in our capital structure, such as future issuances of securities, sales of large blocks of common stock by our stockholders, including our principal stockholders, or the incurrence of additional debt; |

| • | departure of key personnel; |

| • | reputational issues; |

| • | changes in general economic and market conditions; |

| • | changes in industry conditions or perceptions or changes in the market outlook for the insurance industry; and |

| • | changes in applicable laws, rules or regulations, regulatory actions affecting us and other dynamics. |

| • | the ability of our board of directors to issue one or more series of preferred stock; |

| • | the filling of any vacancies on our board of directors by the affirmative vote of a majority of the remaining directors, even if less than a quorum, or by a sole remaining director or by the stockholders; provided, however, that after the first time when the principal stockholders cease to beneficially own, in the aggregate, at least 50% of our outstanding common stock, any vacancy occurring in our board of directors may only be filled by a majority of the directors then in office, although less than a quorum, or by a sole remaining director (and not by the stockholders); |

| • | certain limitations on convening special stockholder meetings; |

| • | advance notice for nominations of directors by stockholders and for stockholders to include matters to be considered at our annual meetings; and |

| • | stockholder action by written consent only until the first time when our principal stockholders cease to beneficially own, in the aggregate, 50% or greater of our outstanding common stock. |

| • | actual basis; |

| • | as adjusted basis giving effect to the reorganization transactions; and |

| • | as further adjusted basis giving effect to the issuance and sale by us of 7,142,857 shares of our common stock in this offering and the application of the net proceeds therefrom as described in “Use of proceeds,” based on an assumed initial public offering price of $14.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus. |

| | | As of March 31, 2020 | |||||||

| | | Actual | | | As adjusted | | | As further adjusted(1) | |

| | | (in thousands, except shares and per share data) | |||||||

Long-term debt | | | $28,721 | | | $48,981 | | | $20,989 |

Redeemable preferred stock,1,000,000 shares authorized; 51 shares issued and outstanding, actual and as adjusted; no shares issued and outstanding, as further adjusted | | | 5,100 | | | 5,100 | | | — |

Stockholders’ / members’ equity: | | | | | | | |||

Members’ equity | | | 78,458 | | | — | | | — |

Common stock, $0.01 par value per share, no shares authorized or issued and outstanding, actual; 600,000,000 shares authorized, 44,000,000 shares issued and outstanding, as adjusted; 51,142,857 shares issued and outstanding, as further adjusted | | | — | | | 440 | | | 511 |

Preferred stock, $0.01 par value per share, no shares authorized or issued and outstanding, actual; 100,000,000 shares authorized, no shares issued and outstanding, as adjusted and as further adjusted | | | — | | | — | | | — |

Additional paid-in capital | | | 17,995 | | | 188,604 | | | 276,795 |

Retained earnings | | | 49,967 | | | 114,468 | | | 114,468 |

Accumulated other comprehensive income | | | 3,761 | | | 3,761 | | | 3,761 |

Total stockholders’ / members’ equity | | | 150,181 | | | 307,273 | | | 395,535 |

Total capitalization(2) | | | $ 184,002 | | | $361,354 | | | $416,524 |

| (1) | Each $1.00 increase or decrease in the assumed initial public offering price of $14.00 per share of common stock (the midpoint of the price range set forth on the cover page of this prospectus) would increase (decrease) total stockholders’ equity by approximately $6.6 million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same, and after deducting the underwriting discount and commissions and estimated offering expenses payable by us. We may also increase or decrease the number of shares we are offering. Each 1,000,000 increase or decrease in the number of shares of common stock offered in this offering by us would increase or decrease total stockholders’ equity by approximately $13.0 million, assuming that the assumed initial public offering price remains the same, and after deducting the underwriting discount and commissions and estimated offering expenses payable by us. |

| (2) | Actual and As adjusted each include $5.1 million of redeemable preferred stock. |

Assumed initial public offering price per share | | | | | $14.00 | |

As adjusted net tangible book value per share as of March 31, 2020 | | | $2.67 | | | |

Increase in as adjusted net tangible book value per share attributable to new investors purchasing shares in this offering | | | 1.35 | | | |

As further adjusted net tangible book value per share immediately after this offering | | | | | $4.02 | |

Dilution per share to new investors in this offering | | | | | $9.98 |

| | | Shares Purchased | | | Total Consideration | | | Average Price Per Share | |||||||

| | | Number | | | Percent | | | Amount | | | Percent | | |||

Existing stockholders | | | 40,428,571 | | | 79.1% | | | $565,999,994 | | | 79.1% | | | $14.00 |

New investors in this offering | | | 10,714,286 | | | 20.9% | | | $150,000,004 | | | 20.9% | | | $14.00 |

Total | | | 51,142,857 | | | 100% | | | $715,999,998 | | | 100% | | | |

| | | Three months ended March 31, | | | Year ended December 31, | |||||||

| | | 2020 | | | 2019 | | | 2019 | | | 2018 | |

| | | (in thousands) | ||||||||||

Revenues: | | | | | | | | | ||||

Gross written premiums | | | $107,859 | | | $101,534 | | | $411,401 | | | $357,007 |

Increase in gross unearned premiums | | | (7,373) | | | (10,952) | | | (13,598) | | | (16,862) |

Gross earned premiums | | | 100,486 | | | 90,582 | | | 397,803 | | | 340,145 |

Ceded earned premiums | | | (78,027) | | | (70,958) | | | (311,325) | | | (273,569) |

Net earned premiums | | | 22,459 | | | 19,624 | | | 86,478 | | | 66,576 |

Net investment income | | | 3,272 | | | 1,287 | | | 6,245 | | | 4,816 |

Net realized capital gains (losses) | | | 3,234 | | | 612 | | | 667 | | | (715) |

Other revenue | | | 4,392 | | | 3,595 | | | 9,125 | | | 7,826 |

Total revenue | | | 33,357 | | | 25,118 | | | 102,515 | | | 78,503 |

| | | | | | | | | |||||

Expenses: | | | | | | | | | ||||

Losses and loss adjustment expenses | | | 12,934 | | | 11,456 | | | 44,661 | | | 35,729 |

General and administrative expenses | | | 8,160 | | | 3,969 | | | 21,005 | | | 15,706 |

Interest expense | | | 461 | | | 624 | | | 2,169 | | | 1,557 |

Total expenses | | | 21,555 | | | 16,049 | | | 67,835 | | | 52,992 |

| | | | | | | | | |||||

Other income | | | 14 | | | 93 | | | 121 | | | 639 |

Income before taxes | | | 11,816 | | | 9,162 | | | 34,801 | | | 26,150 |

| | | | | | | | | |||||

Provision for income taxes | | | 2,912 | | | 1,319 | | | 7,074 | | | 5,546 |

Equity earnings (losses) in affiliates, net of tax | | | 702 | | | 608 | | | 3,558 | | | (1,082) |

Net income | | | $9,606 | | | $8,451 | | | $31,285 | | | $19,522 |

Adjusted net income(1) | | | $6,602 | | | $8,369 | | | $33,194 | | | $22,197 |

| | | Three months ended March 31, 2020 | | | Year ended December 31, 2019 | |

Pro forma per share data(2): | | | | | ||

Pro forma earnings per share outstanding | | | | | ||

Basic and diluted | | | $0.20 | | | $0.68 |

Pro forma weighted average shares outstanding | | | | | ||

Basic and diluted | | | 51,142,857 | | | 51,142,857 |

| (1) | Adjusted net income is a non-GAAP financial measure. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted net income to net income in accordance with GAAP. |

| (2) | Pro forma earnings per share outstanding gives pro forma effect to: (a) the issuance of 37,386,394 shares of our common stock to Trean Holdings and BIC Holdings in exchange for the contribution of all of their respective assets and liabilities to Trean Insurance Group, Inc., (b) the issuance of 6,613,606 shares of our common stock in connection with the acquisition from the Blake Enterprises |

| | | Three months ended March 31, 2020 | | | Year ended December 31, 2019 | |

| | | (in thousands, except share and per share data) | ||||

Numerator: | | | | | ||

Net income | | | $9,606 | | | $31,285 |

Pro forma adjustment: 55% equity in net income of Compstar (net of tax) | | | 858 | | | 3,409 |

Pro forma net income | | | $10,464 | | | $34,694 |

| | | | | |||

Denominator: | | | | | ||

Issuance of our common stock to Trean Holdings and BIC Holdings in exchange for contribution | | | 37,386,394 | | | 37,386,394 |

| | | | | |||

Issuance of common stock in connection with acquisition from the Blake Baker Enterprises Entities of their 55% equity interest in Compstar Holding Company LLC | | | 6,613,606 | | | 6,613,606 |

Issuance of common stock by us in this offering | | | 7,142,857 | | | 7,142,857 |

Pro forma shares outstanding | | | 51,142,857 | | | 51,142,857 |

Pro forma earnings per share outstanding | | | | | ||

Basic and diluted | | | $0.20 | | | $0.68 |

| | | At March 31, 2020 | | | At December 31, | ||||

| | | 2019 | | | 2018 | ||||

| | | (in thousands) | |||||||

Balance sheet data: | | | | | | | |||

Accrued investment income | | | $2,420 | | | $2,468 | | | $2,372 |

Premiums and other receivables | | | 67,773 | | | 62,460 | | | 62,400 |

Related party receivables | | | 21,871 | | | 22,221 | | | 15,934 |

Reinsurance recoverable | | | 313,760 | | | 307,338 | | | 257,509 |

Prepaid reinsurance premiums | | | 83,694 | | | 80,088 | | | 66,765 |

Deferred policy acquisition cost, net | | | 3,103 | | | 2,115 | | | 2,976 |

Property and equipment, net | | | 8,238 | | | 7,937 | | | 8,134 |

Deferred tax asset | | | 1,280 | | | 1,367 | | | 1,823 |

Goodwill | | | 2,822 | | | 2,822 | | | 2,822 |

Other assets | | | 7,572 | | | 3,277 | | | 1,963 |

Total assets | | | 954,583 | | | 919,034 | | | 800,119 |

Unpaid loss and loss adjustment expenses | | | 418,757 | | | 406,716 | | | 340,415 |

Unearned premiums | | | 111,162 | | | 103,789 | | | 90,074 |

Funds held under reinsurance agreements | | | 165,018 | | | 163,445 | | | 166,838 |

Reinsurance premiums payable | | | 48,099 | | | 53,620 | | | 40,135 |

Accounts payable and accrued expenses | | | 18,360 | | | 14,995 | | | 15,004 |

Total liabilities | | | 799,302 | | | 772,319 | | | 688,988 |

Redeemable preferred stock | | | 5,100 | | | 5,100 | | | 6,000 |

Total members’ equity | | | 150,181 | | | 141,615 | | | 105,131 |

Total liabilities and members’ equity | | | $954,583 | | | $919,034 | | | $800,119 |

| | | Three months ended March 31, | | | Year ended December 31, | |||||||

| | | 2020 | | | 2019 | | | 2019 | | | 2018 | |

Underwriting and other ratios: | | | | | | | | | ||||

Loss ratio(1) | | | 57.6% | | | 58.4% | | | 51.6% | | | 53.7% |

Expense ratio(2) | | | 36.3% | | | 20.2% | | | 24.3% | | | 23.6% |

Combined ratio(3) | | | 93.9% | | | 78.6% | | | 75.9% | | | 77.3% |

Return on equity(4) | | | 26.3% | | | 30.5% | | | 25.5% | | | 20.2% |

Adjusted return on equity(5) | | | 18.1% | | | 30.2% | | | 27.0% | | | 23.0% |

Return on tangible equity(6) | | | 26.9% | | | 31.4% | | | 26.1% | | | 20.6% |

Adjusted return on tangible equity(7) | | | 18.5% | | | 31.1% | | | 27.7% | | | 23.4% |

| (1) | The loss ratio is the ratio, expressed as a percentage, of losses and loss adjustment expenses to net earned premiums. |

| (2) | The expense ratio is the ratio, expressed as a percentage, of general and administrative expenses to net earned premiums. |

| (3) | The combined ratio is the sum of the loss ratio and the expense ratio. A combined ratio under 100% generally indicates an underwriting profit. A combined ratio over 100% generally indicates an underwriting loss. |

| (4) | Return on equity represents net income expressed on an annualized basis as a percentage of average beginning and ending members’ equity during the period. |

| (5) | Adjusted return on equity is a non-GAAP financial measure defined as adjusted net income expressed on an annualized basis as a percentage of average beginning and ending members’ equity during the period. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted return on equity to return on equity in accordance with GAAP. |

| (6) | Return on tangible equity is a non-GAAP financial measure defined as net income expressed on an annualized basis as a percentage of average beginning and ending tangible members’ equity during the period. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of return on tangible equity to return on equity in accordance with GAAP. |

| (7) | Adjusted return on tangible equity is a non-GAAP financial measure defined as adjusted net income expressed on an annualized basis as a percentage of average beginning and ending tangible members’ equity during the period. See “Management’s discussion and analysis of financial condition and results of operations — Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted return on tangible equity to return on tangible equity in accordance with GAAP. |

| • | Addition and retention of Program Partners; |

| • | New business submissions to our Program Partners; |

| • | Binding of new business submissions into policies; |

| • | Renewals of existing policies; and |

| • | Average size and premium rate of bound policies. |

| • | frequency of claims associated with the particular types of insurance contracts that we write; |

| • | trends in the average size of losses incurred on a particular type of business; |

| • | mix of business written by us; |

| • | changes in the legal or regulatory environment related to the business we write; |

| • | trends in legal defense costs; |

| • | wage inflation; and |

| • | inflation in medical costs. |

| | | Three months ended March 31, | | | Change | | | Percentage Change | ||||

| | | 2020 | | | 2019 | | ||||||

| | | ($ in thousands) | | | | | ||||||

Revenues | | | | | | | | | ||||

Gross written premiums | | | $107,859 | | | $101,534 | | | $6,325 | | | 6% |

Increase in gross unearned premiums | | | (7,373) | | | (10,952) | | | (3,579) | | | (33) |

Gross earned premiums | | | 100,486 | | | 90,582 | | | 9,904 | | | 11 |

Ceded earned premiums | | | (78,027) | | | (70,958) | | | 7,069 | | | 10 |

Net earned premiums | | | 22,459 | | | 19,624 | | | 2,835 | | | 14 |

Expenses | | | | | | | | | ||||

Losses and loss adjustment expenses | | | 12,934 | | | 11,456 | | | 1,478 | | | 13 |

General and administrative expenses | | | 8,160 | | | 3,969 | | | 4,191 | | | 106 |

Underwriting income(1) | | | 1,365 | | | 4,199 | | | (2,834) | | | (67) |

Net investment income | | | 3,272 | | | 1,287 | | | 1,985 | | | 154 |

Net realized capital gains (losses) | | | 3,234 | | | 612 | | | 2,622 | | | 428 |

Other revenue | | | 4,392 | | | 3,595 | | | 797 | | | 22 |

Interest expense | | | (461) | | | (624) | | | 163 | | | 26 |

Other income | | | 14 | | | 93 | | | (79) | | | (85) |

Income before taxes | | | 11,816 | | | 9,162 | | | 2,654 | | | 29 |

Provision for income taxes | | | 2,912 | | | 1,319 | | | 1,593 | | | 121 |

Equity earnings (losses) in affiliates, net of tax | | | 702 | | | 608 | | | 94 | | | 15 |

Net income | | | $9,606 | | | $8,451 | | | $1,155 | | | 14% |

Adjusted net income(2) | | | $6,602 | | | $8,369 | | | $(1,767) | | | (21)% |

| (1) | Underwriting income is a non-GAAP financial measure. See “— Reconciliation of non-GAAP financial measures” for a reconciliation of underwriting income to net income in accordance with GAAP. |

| (2) | Adjusted net income is a non-GAAP financial measure. See “— Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted net income to net income in accordance with GAAP. |

| | | Three months ended March 31, | ||||

| | | 2020 | | | 2019 | |

Key metrics: | | | | | ||

Loss ratio | | | 57.6% | | | 58.4% |

Expense ratio | | | 36.3% | | | 20.2% |

Combined ratio | | | 93.9% | | | 78.6% |

Return on equity | | | 26.3% | | | 30.5% |

Adjusted return on equity(1) | | | 18.1% | | | 30.2% |

Return on tangible equity(2) | | | 26.9% | | | 31.4% |

Adjusted return on tangible equity(3) | | | 18.5% | | | 31.1% |

| (1) | Adjusted return on equity is a non-GAAP financial measure. See “— Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted return on equity to return on equity in accordance with GAAP. |

| (2) | Return on tangible equity is a non-GAAP financial measure. See “— Reconciliation of non-GAAP financial measures” for a reconciliation of return on tangible equity to return on equity in accordance with GAAP. |

| (3) | Adjusted return on tangible equity is a non-GAAP financial measure. See “— Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted return on tangible equity to return on tangible equity in accordance with GAAP. |

| | | Three months ended March 31, | | | Change | | | Percentage Change | ||||

| | | 2020 | | | 2019 | | ||||||

| | | (in thousands) | | | | | ||||||

Revenues: | | | | | | | | | ||||

Gross written premiums | | | $107,859 | | | $101,534 | | | $6,325 | | | 6% |

Increase in gross unearned premiums | | | (7,373) | | | (10,952) | | | (3,579) | | | (33) |

Gross earned premiums | | | 100,486 | | | 90,582 | | | 9,904 | | | 11 |

Ceded earned premiums | | | (78,027) | | | (70,958) | | | 7,069 | | | 10 |

Net earned premiums | | | $22,459 | | | $19,624 | | | $2,835 | | | 14% |

| | | Year ended December 31, | | | Change | | | Percentage Change | ||||

| | | 2019 | | | 2018 | | ||||||

| | | ($ in thousands) | | | | | ||||||

Revenues | | | | | | | | | ||||

Gross written premiums | | | $411,401 | | | $357,007 | | | $54,394 | | | 15% |

Increase in gross unearned premiums | | | (13,598) | | | (16,862) | | | (3,264) | | | (19) |

Gross earned premiums | | | 397,803 | | | 340,145 | | | 57,658 | | | 17 |

Ceded earned premiums | | | (311,325) | | | (273,569) | | | 37,756 | | | 14 |

Net earned premiums | | | 86,478 | | | 66,576 | | | 19,902 | | | 30 |

Expenses | | | | | | | | | ||||

Losses and loss adjustment expenses | | | 44,661 | | | 35,729 | | | 8,932 | | | 25 |

General and administrative expenses | | | 21,005 | | | 15,706 | | | 5,299 | | | 34 |

Underwriting income(1) | | | 20,812 | | | 15,141 | | | 5,671 | | | 38 |

Net investment income | | | 6,245 | | | 4,816 | | | 1,429 | | | 30 |

Net realized capital gains (losses) | | | 667 | | | (715) | | | 1,382 | | | 193 |

Other revenue | | | 9,125 | | | 7,826 | | | 1,299 | | | 17 |

Interest expense | | | 2,169 | | | 1,557 | | | (612) | | | (39) |

Other income | | | 121 | | | 639 | | | (518) | | | (81) |

Income before taxes | | | 34,801 | | | 26,150 | | | 8,651 | | | 33 |

Provision for income taxes | | | 7,074 | | | 5,546 | | | 1,528 | | | 28 |

Equity earnings (losses) in affiliates, net of tax | | | 3,558 | | | (1,082) | | | 4,640 | | | 429 |

Net income | | | $31,285 | | | $19,522 | | | $11,763 | | | 60% |

Adjusted net income(2) | | | $33,194 | | | $22,197 | | | $10,997 | | | 50% |

| (1) | Underwriting income is a non-GAAP financial measure. See “— Reconciliation of non-GAAP financial measures” for a reconciliation of underwriting income to net income in accordance with GAAP. |

| (2) | Adjusted net income is a non-GAAP financial measure. See “— Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted net income to net income in accordance with GAAP. |

| | | Year ended December 31, | ||||

| | | 2019 | | | 2018 | |

Key metrics: | | | | | ||

Loss ratio | | | 51.6% | | | 53.7% |

Expense ratio | | | 24.3% | | | 23.6% |

Combined ratio | | | 75.9% | | | 77.3% |

Return on equity | | | 25.5% | | | 20.2% |

Adjusted return on equity(1) | | | 27.0% | | | 23.0% |

Return on tangible equity(2) | | | 26.1% | | | 20.6% |

Adjusted return on tangible equity(3) | | | 27.7% | | | 23.4% |

| (1) | Adjusted return on equity is a non-GAAP financial measure. See “— Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted return on equity to return on equity in accordance with GAAP. |

| (2) | Return on tangible equity is a non-GAAP financial measure. See “— Reconciliation of non-GAAP financial measures” for a reconciliation of return on tangible equity to return on equity in accordance with GAAP. |

| (3) | Adjusted return on tangible equity is a non-GAAP financial measure. See “— Reconciliation of non-GAAP financial measures” for a reconciliation of adjusted return on tangible equity to return on tangible equity in accordance with GAAP. |

| | | Year ended December 31, | | | Change | | | Percentage Change | ||||

| | | 2019 | | | 2018 | | ||||||

| | | (in thousands) | | | | | ||||||

Revenues: | | | | | | | | | ||||

Gross written premiums | | | $411,401 | | | $357,007 | | | $54,394 | | | 15% |

Increase in gross unearned premiums | | | (13,598) | | | (16,862) | | | (3,264) | | | (19) |

Gross earned premiums | | | 397,803 | | | 340,145 | | | 57,658 | | | 17 |

Ceded earned premiums | | | (311,325) | | | (273,569) | | | 37,756 | | | 14 |

Net earned premiums | | | $86,478 | | | $66,576 | | | $19,902 | | | 30% |

| | | Three months ended March 31, | | | Change | | | Percentage Change | ||||

| | | 2020 | | | 2019 | | ||||||

| | | (in thousands) | | | | | ||||||

Cash, cash equivalents and restricted cash provided by (used in): | | | | | | | | | ||||

Operating activities | | | $7,428 | | | $9,332 | | | $(1,904) | | | (20)% |

Investing activities | | | (9,470) | | | (11,480) | | | 2,010 | | | 18 |

Financing activities | | | (344) | | | (372) | | | 28 | | | 8 |

Net increase in cash, cash equivalents and restricted cash | | | $(2,386) | | | $(2,520) | | | $134 | | | 5% |

| | | Year ended December 31, | | | Change | | | Percentage Change | ||||

| | | 2019 | | | 2018 | | ||||||

| | | (in thousands) | | | | | ||||||

Cash provided by (used in): | | | | | | | | | ||||

Operating activities | | | $52,173 | | | $75,266 | | | $(23,093) | | | (31)% |

Investing activities | | | (23,943) | | | (78,559) | | | 54,616 | | | 70 |

Financing activities | | | (8,125) | | | 14,282 | | | (22,407) | | | (157) |

Net increase in cash, cash equivalents and restricted cash | | | $20,105 | | | $10,989 | | | $9,116 | | | 83% |

| | | Payments Due by Period | |||||||||||||

| | | Total | | | Less than one year | | | One Year to Less Than Three Years | | | Three Years to Less Than Five Years | | | More Than Five Years | |

| | | ($ in thousands) | |||||||||||||

Reserve for losses and loss adjustment expenses | | | $406,716 | | | $94,765 | | | $157,806 | | | $60,194 | | | $93,951 |

Debt securities and credit agreements | | | 29,369 | | | 1,891 | | | 5,844 | | | 13,902 | | | 7,732 |

Interest payable(1) | | | 11,340 | | | 1,788 | | | 3,125 | | | 1,146 | | | 5,282 |

Operating lease obligations | | | 6,572 | | | 1,688 | | | 3,145 | | | 1,793 | | | (54) |

Total | | | $453,997 | | | $100,132 | | | $169,919 | | | $77,035 | | | $106,911 |

| (1) | Interest on the subordinated debt and the note payable under the Secured Credit Facility is calculated using 5.94% & 6.33%, respectively, in effect at December 31, 2019 with the assumption that interest rates remain flat over the remainder of the period that the note is outstanding. At our option, we may prepay the note payable in whole or in part without premium or penalty. |

The amortized cost and fair value on available-for-sale securities were as follows: | | | Cost or Amortized Cost | | | Fair Value | | | Cost or Amortized Cost | | | Fair Value |

| | | At March 31, 2020 | | | At December 31, 2019 | |||||||

| | | (in thousands) | ||||||||||

Fixed maturities: | | | | | | | | | ||||

U.S. government and government securities | | | $15,374 | | | $15,882 | | | $15,965 | | | $16,129 |

Foreign governments | | | 299 | | | 306 | | | 299 | | | 302 |

States, territories and possessions | | | 5,612 | | | 5,733 | | | 4,789 | | | 4,923 |

Political subdivisions of states, territories and possessions | | | 24,992 | | | 25,726 | | | 24,444 | | | 25,104 |

Special revenue and special assessment obligations | | | 64,694 | | | 67,326 | | | 59,149 | | | 61,405 |

Industrial and public utilities | | | 116,362 | | | 118,012 | | | 119,735 | | | 123,207 |

Commercial mortgage-backed securities | | | 15,547 | | | 16,334 | | | 15,586 | | | 16,312 |

Residential mortgage-backed securities | | | 55,492 | | | 57,351 | | | 53,467 | | | 54,109 |

Other loan-backed securities | | | 41,651 | | | 40,474 | | | 35,849 | | | 36,011 |

Hybrid securities | | | 357 | | | 353 | | | 357 | | | 363 |

Total fixed maturities | | | 340,380 | | | 347,497 | | | 329,640 | | | 337,865 |

Equity securities: | | | | | | | | | ||||

Preferred stock | | | 332 | | | 310 | | | 337 | | | 343 |

Common stock | | | 1,554 | | | 3,353 | | | 492 | | | 492 |

Total equity maturities | | | 1,886 | | | 3,663 | | | 829 | | | 835 |

Total securities available for sale | | | $ 342,266 | | | $ 351,160 | | | $ 330,469 | | | $ 338,700 |

| | | Three months ended March 31, | | | Change | | | Percentage Change | | ||||||

| | | 2020 | | | 2019 | | |||||||||

| | | (in thousands) | | | | | | | |||||||

Net income | | | $9,606 | | | $8,451 | | | $1,155 | | | 14% | | ||

Provision for income taxes | | | 2,912 | | | 1,319 | | | 1,593 | | | 121 | | ||

Equity (earnings) in affiliates, net of tax | | | (702) | | | (608) | | | 94 | | | 15 | | ||

Income before taxes | | | 11,816 | | | 9,162 | | | 2,654 | | | 29 | | ||

Other revenue | | | 4,392 | | | 3,595 | | | 797 | | | 22 | | ||

Net investment income | | | 3,272 | | | 1,287 | | | 1,985 | | | 154 | | ||

Net realized capital gains/(losses) | | | 3,234 | | | 612 | | | 2,622 | | | 428 | | ||

Interest expense | | | (461) | | | (624) | | | (163) | | | (26) | | ||

Other income | | | 14 | | | 93 | | | (79) | | | (85) | | ||

Underwriting income | | | $1,365 | | | $4,199 | | | $(2,834) | | | (67)% | | ||

| | | Year ended December 31, | | | Change | | | Percentage Change | ||||

| | | 2019 | | | 2018 | | ||||||

| | | (in thousands) | | | | | ||||||

Net income | | | $ 31,285 | | | $ 19,522 | | | $ 11,763 | | | 60% |

Provision for income taxes | | | 7,074 | | | 5,546 | | | 1,528 | | | 28 |

Equity (earnings) losses in affiliates, net of tax | | | (3,558) | | | 1,082 | | | 4,640 | | | 429 |

Income before taxes | | | 34,801 | | | 26,150 | | | 8,651 | | | 33 |

Other revenue | | | (9,125) | | | (7,826) | | | 1,299 | | | 17 |

Net investment income | | | (6,245) | | | (4,816) | | | 1,429 | | | 30 |

Net realized capital (gains)/losses | | | (667) | | | 715 | | | 1,382 | | | 193 |

Interest expense | | | 2,169 | | | 1,557 | | | 612 | | | 39 |

Other income | | | (121) | | | (639) | | | 518 | | | 81 |

Underwriting income | | | $20,812 | | | $15,141 | | | $5,671 | | | 37% |

| | | Three months ended March 31, | | | Change | | | Percentage Change | ||||

| | | 2020 | | | 2019 | | ||||||

| | | ($ in thousands) | | | ||||||||

Net income | | | $ 9,606 | | | $ 8,451 | | | $ 1,155 | | | 14% |

Net gain on purchase and disposal of subsidiaries | | | (3,116) | | | (634) | | | (2,482) | | | (391) |

FMV adjustment of remaining investment in subsidiary | | | (2,000) | | | — | | | (2,000) | | | (100) |

Expenses associated with Altaris management fee, including cash bonuses paid to unitholders | | | 441 | | | 441 | | | — | | | — |

Expenses associated with IPO, Compstar transaction and other one-time consulting expenses | | | 792 | | | 227 | | | 565 | | | 249 |

Expenses associated with debt issuance costs | | | 25 | | | 25 | | | — | | | — |

Expenses associated with the purchase accounting impact of the reorganization transactions | | | — | | | — | | | — | | | — |

Tax impact of adjustments | | | 854 | | | (141) | | | 995 | | | 706 |

Adjusted net income | | | $6,602 | | | $8,369 | | | $(1,767) | | | (21)% |

| | | Year ended December 31, | | | Change | | | Percentage Change | ||||

| | | 2019 | | | 2018 | | ||||||

| | | ($ in thousands) | | | ||||||||

Net income | | | $ 31,285 | | | $ 19,522 | | | $11,763 | | | 60% |

Net gain on purchase and disposal of subsidiaries | | | (600) | | | — | | | (600) | | | (100) |

Expenses associated with Altaris management fee, including cash bonuses paid to unitholders | | | 1,765 | | | 1,765 | | | — | | | — |

Expenses associated with IPO, Compstar transaction and other one-time consulting expenses | | | 1,292 | | | 785 | | | 507 | | | 65 |

Expenses associated with purchase of outstanding voting shares of ALIC | | | — | | | 770 | | | (770) | | | (100) |

Expenses associated with debt issuance costs | | | 101 | | | 75 | | | 26 | | | 35 |

Expenses associated with the purchase accounting impact of the reorganization transactions | | | — | | | — | | | — | | | — |

Tax impact of adjustments | | | (649) | | | (720) | | | 71 | | | 10 |

Adjusted net income | | | $33,194 | | | $22,197 | | | $ 10,997 | | | 50% |

| | | Year ended December 31, | | | Change | | | Percentage Change | ||||

| | | 2018 | | | 2017 | | ||||||

| | | ($ in thousands) | | | ||||||||

Net income | | | $ 19,522 | | | $ 16,408 | | | $ 3,114 | | | 19% |

Expenses associated with Altaris management fee, including cash bonuses paid to unitholders | | | 1,765 | | | 1,600 | | | 165 | | | 10 |

Expenses associated with IPO, Compstar transaction and other one-time consulting expenses | | | 785 | | | — | | | 785 | | | 100 |

Expenses associated with purchase of outstanding voting shares of ALIC | | | 770 | | | 385 | | | 385 | | | 100 |

Expenses associated with debt issuance costs | | | 75 | | | — | | | 75 | | | 100 |

Tax impact of adjustments | | | (720) | | | (622) | | | (98) | | | (16) |

Adjusted net income | | | $22,197 | | | $17,771 | | | $4,426 | | | 25% |

| | | Three months ended March 31, | ||||

| | | 2020 | | | 2019 | |

Adjusted return on equity calculation: | | | | | ||

Numerator: adjusted net income | | | $ 6,602 | | | $ 8,369 |

Denominator: average members’ equity | | | 145,898 | | | 110,717 |

Adjusted return on equity | | | 18.1% | | | 30.2% |

Return on equity | | | 26.3% | | | 30.5% |

| | | Year ended December 31, | |||||||

| | | 2019 | | | 2018 | | | 2017 | |

Adjusted return on equity calculation: | | | | | | | |||

Numerator: adjusted net income | | | $33,194 | | | $22,197 | | | $17,771 |

Denominator: average members’ equity | | | 122,873 | | | 96,648 | | | 80,589 |

Adjusted return on equity | | | 27.0% | | | 23.0% | | | 22.1% |

Return on equity | | | 25.5% | | | 20.2% | | | 20.4% |

| | | Three months ended March 31, | | | Year ended December 31, | |||||||

| | | 2020 | | | 2019 | | | 2019 | | | 2018 | |

Return on tangible equity calculation: | | | | | | | | | ||||

Numerator: net income | | | $9,606 | | | $8,451 | | | $31,285 | | | $19,522 |

Denominator: | | | | | | | | | ||||

Average members’ equity | | | 145,898 | | | 110,681 | | | 122,873 | | | 96,648 |

Less: Average goodwill and other intangible assets | | | 2,971 | | | 3,017 | | | 3,000 | | | 1,940 |

Average tangible members’ equity | | | 142,927 | | | 107,664 | | | 119,873 | | | 94,708 |

Return on tangible equity | | | 26.9% | | | 31.4% | | | 26.1% | | | 20.6% |

Return on equity | | | 26.3% | | | 30.5% | | | 25.5% | | | 20.2% |

| | | Three months ended March 31, | | | Year ended December 31, | |||||||

| | | 2020 | | | 2019 | | | 2019 | | | 2018 | |

Adjusted return on tangible equity calculation: | | | | | | | | | ||||

Numerator: adjusted net income | | | $6,602 | | | $8,369 | | | $33,194 | | | $22,197 |

Denominator: average tangible members’ equity | | | 142,927 | | | 107,664 | | | 119,873 | | | 94,708 |

Adjusted return on tangible equity | | | 18.5% | | | 31.1% | | | 27.7% | | | 23.4% |

Return on tangible equity | | | 26.9% | | | 31.4% | | | 26.1% | | | 20.6% |

| | | Year Ended December 31, 2019 | ||||||||||

| | | Gross | | | % of Total | | | Net | | | % of Total | |

| | | ($ in thousands) | ||||||||||

Case Reserves | | | $ 130,409 | | | 32% | | | $ 30,868 | | | 30% |

IBNR | | | 276,307 | | | 68% | | | 71,843 | | | 70% |

Total | | | $406,716 | | | 100% | | | $102,711 | | | 100% |

| | | Year Ended December 31, 2018 | ||||||||||

| | | Gross | | | % of Total | | | Net | | | % of Total | |

| | | ($ in thousands) | ||||||||||

Case Reserves | | | $ 104,953 | | | 31% | | | $ 26,262 | | | 32% |

IBNR | | | 235,462 | | | 69% | | | 56,732 | | | 68% |

Total | | | $340,415 | | | 100% | | | $82,994 | | | 100% |

| | | December 31, 2019 | | | Potential impact of 2019 | |||||||||||||

Sensitivity | | | Accident year | | | Net ultimate losses and LAE sensitivity factor | | | Net ultimate incurred losses and LAE | | | Net losses and LAE reserve | | | Pre-tax income | | | Stockholders’ equity |

Sample increases | | | 2019 | | | 5.0% | �� | | $53,009 | | | $43,081 | | | $(2,650) | | | $(2,094) |

| | | 2018 | | | 2.5% | | | 36,738 | | | 18,591 | | | (918) | | | (726) | |

| | | Prior | | | 1.0% | | | 179,010 | | | 41,039 | | | (1,790) | | | (1,414) | |

Sample decreases | | | 2019 | | | -5.0% | | | 53,009 | | | 43,081 | | | 2,650 | | | 2,094 |

| | | 2018 | | | -2.5% | | | 36,738 | | | 18,591 | | | 918 | | | 726 | |

| | | Prior | | | -1.0% | | | 179,019 | | | 41,039 | | | 1,790 | | | 1,414 | |

| | | Year ended December 31, | ||||||||||

| | | 2019 | | | 2018 | |||||||

| | | Gross Written Premiums | | | Net Written Premiums | | | Gross Written Premiums | | | Net Written Premiums | |

| | | (in thousands) | ||||||||||

Workers’ compensation | | | $ 340,444 | | | $ 73,287 | | | $ 277,291 | | | $ 59,764 |

Other liability – occurrence* | | | 20,129 | | | 5,269 | | | 20,923 | | | 7,089 |

Commercial multiple peril | | | 17,662 | | | 4,059 | | | 13,128 | | | 3,597 |

Commercial auto liability | | | 9,935 | | | 1,474 | | | 7,251 | | | 1,076 |

Group accident and health | | | 7,678 | | | 3 | | | 22,450 | | | 123 |

Products liability – occurrence* | | | 7,368 | | | — | | | 6,496 | | | — |

Auto physical damage | | | 4,843 | | | 874 | | | 4,404 | | | 651 |

Excess workers’ compensation* | | | 2,539 | | | 546 | | | 1,090 | | | 227 |

Boiler and machinery | | | 783 | | | — | | | 599 | | | — |

Fire | | | 64 | | | — | | | 42 | | | — |

Surety | | | 52 | | | 52 | | | 29 | | | 29 |

Inland marine | | | 4 | | | — | | | 3 | | | — |

Private passenger auto liability | | | (100) | | | — | | | 3,301 | | | — |

Total: | | | $ 411,401 | | | $85,564 | | | $357,007 | | | $72,556 |

| * | Included in other liability. |

| | | Year ended December 31, | ||||||||||

| | | 2019 | | | 2018 | |||||||

| | | Gross Written Premiums | | | Net Written Premiums | | | Gross Written Premiums | | | Net Written Premiums | |

| | | (in thousands) | ||||||||||

California | | | $ 202,446 | | | $ 39,066 | | | $ 153,611 | | | $ 32,259 |

Michigan | | | 38,174 | | | 7,990 | | | 37,084 | | | 7,741 |

Arizona | | | 34,215 | | | 5,394 | | | 28,350 | | | 6,227 |

Alabama | | | 12,946 | | | 5,551 | | | 11,907 | | | 5,694 |

Nevada | | | 11,869 | | | 2,918 | | | 9,225 | | | 2,417 |

Utah | | | 10,900 | | | 768 | | | 11,379 | | | 2,093 |

Mississippi | | | 8,910 | | | 4,399 | | | 7,143 | | | 3,705 |

Tennessee | | | 8,065 | | | 3,764 | | | 7,809 | | | 3,986 |

Indiana | | | 6,295 | | | 1,295 | | | * | | | * |

New Jersey | | | 6,222 | | | 82 | | | 7,580 | | | (292) |

Other geographical areas | | | 71,359 | | | 14,337 | | | 73,316 | | | 8,694 |

Total: | | | $411,401 | | | $85,564 | | | $357,007 | | | $72,556 |

| * | The amount for the state is relevant for 2019 but not in 2018 and therefore, was not presented in 2018. |

| • | small- to mid-sized books of business (less than $30 million of annual gross premiums at the inception of the relationship); |

| • | operating in markets where we believe we can leverage our distinctive expertise, multi-service offering and market relationships to create a competitive advantage; |

| • | track record of underwriting success supported with credible data; |

| • | proven ability to administer the program pursuant to agreed-upon underwriting and claims guidelines; |

| • | ability and willingness to assume a meaningful quota share risk participation in the program, typically through ownership of an insurance company or captive; |

| • | collaborative, entrepreneurial management team; and |

| • | willingness and ability for us to control the structuring and placement of reinsurance. |

Reinsurers: | | | A.M. Best Rating | | | Reinsurance Recoverables | | | Collateral | | | Net Recoverables |

| | | (in thousands) | ||||||||||

Markel Global Reinsurance Company | | | A | | | $ 70,510 | | | $ 4,617 | | | $ 65,893 |

Provistar Insurance Company, Limited | | | NR | | | 51,120 | | | 62,017 | | | (10,897) |

Arch Reinsurance Company (U.S.) | | | A+ | | | 40,021 | | | 3,313 | | | 36,708 |

Greenlight Reinsurance, Limited | | | A- | | | 39,624 | | | 56,510 | | | (16,886) |

Sunz Insurance Company | | | NR | | | 13,050 | | | 29,960 | | | (16,910) |

Synergy Comp. Insurance Company | | | NR | | | 12,238 | | | 15,409 | | | (3,171) |

VGM Insurance Companies Of America Limited | | | NR | | | 9,931 | | | 15,672 | | | (5,741) |

Employers National Insurance Company Inc. | | | NR | | | 9,599 | | | 13,423 | | | (3,824) |

First Insurance Company Of Oklahoma, Inc. | | | NR | | | 9,250 | | | 13,216 | | | (3,966) |

Steadpoint Insurance Company | | | NR | | | 6,611 | | | 8,815 | | | (2,204) |

Total | | | | | 261,954 | | | 222,952 | | | 39,002 | |

| | | | | | | | | |||||

All other reinsurers | | | | | 45,384 | | | 38,577 | | | 6,807 | |

Total recoverables | | | | | $307,338 | | | $261,529 | | | $45,809 | |

| • | type of loss; |

| • | severity of the injury or damage; |

| • | age and occupation of the injured employee; |

| • | estimated length of temporary disability; |

| • | anticipated permanent disability; |

| • | expected medical procedures, costs and duration; |

| • | our knowledge of the circumstances surrounding the claim; |

| • | insurance policy provisions, including coverage, related to the claim; |

| • | jurisdiction of the occurrence; and |

| • | other benefits defined by applicable statute. |

Incurred claims and allocated claim adjustment expenses, net of reinsurance For the years ended December 31, (in thousands) | | | As of December 31,2019 | |||||||||||||||||||||||||||||||||

Accident Year | | | 2010 | | | 2011 | | | 2012 | | | 2013 | | | 2014 | | | 2015 | | | 2016 | | | 2017 | | | 2018 | | | 2019 | | | Total of IBNR liabilities plus expected development on reported claims | | | Cumulative number of reported claims |

2010 | | | $11,800 | | | $11,580 | | | $12,396 | | | $12,806 | | | $12,730 | | | $13,557 | | | $13,972 | | | $13,976 | | | $13,777 | | | $13,754 | | | $874 | | | 3,871 |

2011 | | | | | 14,456 | | | 14,923 | | | 16,636 | | | 17,578 | | | 17,620 | | | 17,854 | | | 18,419 | | | 18,834 | | | 18,793 | | | 360 | | | 3,835 | |

2012 | | | | | | | 21,857 | | | 21,831 | | | 20,697 | | | 21,053 | | | 20,331 | | | 20,058 | | | 20,646 | | | 20,690 | | | 642 | | | 4,019 | ||

2013 | | | | | | | | | 24,661 | | | 24,755 | | | 24,280 | | | 21,361 | | | 21,342 | | | 21,506 | | | 21,465 | | | 902 | | | 4,364 | |||

2014 | | | | | | | | | | | 24,580 | | | 22,777 | | | 21,726 | | | 21,571 | | | 21,095 | | | 21,054 | | | 2,118 | | | 4,938 | ||||

2015 | | | | | | | | | | | | | 25,653 | | | 26,571 | | | 26,392 | | | 25,430 | | | 25,630 | | | 5,561 | | | 6,265 | |||||

2016 | | | | | | | | | | | | | | | 33,041 | | | 31,632 | | | 30,746 | | | 28,616 | | | 7,846 | | | 11,049 | ||||||

2017 | | | | | | | | | | | | | | | | | 39,295 | | | 31,462 | | | 29,008 | | | 8,410 | | | 16,396 | |||||||

2018 | | | | | | | | | | | | | | | | | | | 42,349 | | | 36,738 | | | 12,183 | | | 15,031 | ||||||||

2019 | | | | | | | | | | | | | | | | | | | | | 53,009 | | | 27,173 | | | 12,179 | |||||||||

Total | | | | | | | | | | | | | | | | | | | | | $268,757 | | | | | |||||||||||

Cumulative paid claims and allocated claim adjustment expenses, net of reinsurance For the years ended December 31, (in thousands) | ||||||||||||||||||||||||||||||

Accident Year | | | 2010 | | | 2011 | | | 2012 | | | 2013 | | | 2014 | | | 2015 | | | 2016 | | | 2017 | | | 2018 | | | 2019 |

2010 | | | $3,594 | | | $7,007 | | | $8,696 | | | $10,095 | | | $10,911 | | | $11,384 | | | $11,779 | | | $12,154 | | | $12,365 | | | $12,499 |

2011 | | | | | 3,954 | | | 8,815 | | | 12,631 | | | 14,107 | | | 15,405 | | | 16,347 | | | 17,085 | | | 17,515 | | | 18,091 | |

2012 | | | | | | | 6,143 | | | 11,996 | | | 14,480 | | | 16,249 | | | 17,196 | | | 18,188 | | | 19,098 | | | 19,399 | ||

2013 | | | | | | | | | 6,799 | | | 12,602 | | | 15,984 | | | 17,708 | | | 19,246 | | | 19,712 | | | 20,129 | |||

2014 | | | | | | | | | | | 6,011 | | | 12,005 | | | 14,814 | | | 16,666 | | | 17,260 | | | 18,238 | ||||

2015 | | | | | | | | | | | | | 6,269 | | | 13,770 | | | 16,493 | | | 18,026 | | | 18,903 | |||||

2016 | | | | | | | | | | | | | | | 7,509 | | | 15,516 | | | 18,182 | | | 19,286 | ||||||

2017 | | | | | | | | | | | | | | | | | 7,845 | | | 15,259 | | | 18,126 | |||||||

2018 | | | | | | | | | | | | | | | | | | | 8,326 | | | 18,905 | ||||||||

2019 | | | | | | | | | | | | | | | | | | | | | 11,813 | |||||||||

| | | | | | | | | | | | | | | | | | | | | 175,389 | ||||||||||

All outstanding liabilities before 2010, net of reinsurance | | | 4,811 | |||||||||||||||||||||||||||

Liabilities for claims and claim adjustment expenses, net of reinsurance | | | $98,179 | |||||||||||||||||||||||||||

| | | Three months ended March 31, 2020 | | | Year ended December 31, 2019 | |||||||||||||

| | | Cost or Amortized Cost | | | Fair Value | | | % of Total Fair Value | | | Cost or Amortized Cost | | | Fair Value | | | % of Total Fair Value | |

| | | ($ in thousands) | | | | | ($ in thousands) | | | |||||||||

Fixed maturities: | | | | | | | | | | | | | ||||||

U.S. government and government securities | | | $15,374 | | | $15,882 | | | 4.5% | | | $ 15,965 | | | $ 16,129 | | | 4.8% |

Foreign governments | | | 299 | | | 306 | | | 0.1% | | | 299 | | | 302 | | | 0.1% |

States, territories and possessions | | | 5,612 | | | 5,733 | | | 1.6% | | | 4,789 | | | 4,923 | | | 1.5% |

Political subdivisions of states, territories and possessions | | | 24,992 | | | 25,726 | | | 7.3% | | | 24,444 | | | 25,104 | | | 7.4% |

Special revenue and special assessment obligations | | | 64,694 | | | 67,326 | | | 19.2% | | | 59,149 | | | 61,405 | | | 18.1% |

Industrial and public utilities | | | 116,362 | | | 118,012 | | | 33.6% | | | 119,735 | | | 123,207 | | | 36.4% |

Commercial mortgage-backed securities | | | 15,547 | | | 16,334 | | | 4.7% | | | 15,586 | | | 16,312 | | | 4.8% |

Residential mortgage-backed securities | | | 55,492 | | | 57,351 | | | 16.3% | | | 53,467 | | | 54,109 | | | 16.0% |

Other loan-backed securities | | | 41,651 | | | 40,474 | | | 11.5% | | | 35,849 | | | 36,011 | | | 10.6% |

Hybrid securities | | | 357 | | | 353 | | | 0.1% | | | 357 | | | 363 | | | 0.1% |

Total fixed maturities | | | 340,380 | | | 347,497 | | | 98.9% | | | $329,640 | | | $337,865 | | | 99.8% |

| | | | | | | | | | | | | |||||||

Equity securities: | | | | | | | | |||||||||||

Preferred stock | | | 332 | | | 310 | | | 0.1% | | | 337 | | | 343 | | | 0.1% |

Common stock | | | 1,554 | | | 3,353 | | | 1.0% | | | 492 | | | 492 | | | 0.1% |

Total equity securities | | | 1,886 | | | 3,663 | | | 1.1% | | | 829 | | | 835 | | | 0.2% |

Total securities available for sale | | | $342,266 | | | $351,160 | | | 100.0% | | | $330,469 | | | $338,700 | | | 100.0% |

| | | Three months ended March 31, 2020 | | | Year ended December 31, 2019 | |||||||||||||

| | | Cost or Amortized Cost | | | Fair Value | | | % of Total Fair Value | | | Cost or Amortized Cost | | | Fair Value | | | % of Total Fair Value | |

| | | ($ in thousands) | | | | | ($ in thousands) | | | |||||||||

Available for sale: | | | | | | | | | | | | | ||||||

Due in one year or less | | | $19,827 | | | $19,897 | | | 5.7% | | | $ 17,822 | | | $ 17,872 | | | 5.3% |

Due after one year but before five years | | | 115,089 | | | 116,766 | | | 33.6% | | | 120,772 | | | 123,603 | | | 36.6% |

Due after five years but before ten years | | | 53,322 | | | 55,663 | | | 16.0% | | | 50,398 | | | 52,893 | | | 15.7% |

Due after ten years | | | 39,452 | | | 41,012 | | | 11.8% | | | 35,746 | | | 37,065 | | | 11.0% |

Commercial mortgage-backed securities | | | 15,547 | | | 16,334 | | | 4.7% | | | 15,586 | | ��� | 16,312 | | | 4.8% |

Residential mortgage-backed securities | | | 55,492 | | | 57,351 | | | 16.5% | | | 53,467 | | | 54,109 | | | 16.0% |

Other loan-backed securities | | | 41,651 | | | 40,474 | | | 11.7% | | | 35,849 | | | 36,011 | | | 10.6% |

Total | | | $340,380 | | | $347,497 | | | 100.0% | | | $329,640 | | | $337,865 | | | 100.0% |

| | | Three months ended March 31, 2020 | | | Year ended December 31, 2019 | |||||||

| | | Fair Value | | | % of Total Fair Value | | | Fair Value | | | % of Total Fair Value | |

| | | ($ in thousands) | | | ($ in thousands) | |||||||

Rating: | | | | | | | | | ||||

AAA | | | $57,569 | | | 16.6% | | | $ 52,571 | | | 15.6% |

AA | | | 164,382 | | | 47.3% | | | 153,838 | | | 45.5% |

A | | | 96,994 | | | 27.9% | | | 101,040 | | | 29.9% |

BBB | | | 27,060 | | | 7.8% | | | 30,245 | | | 9.0% |

BB | | | 1,443 | | | 0.4% | | | 119 | | | 0.0% |

NR | | | 49 | | | —% | | | 52 | | | 0.0% |

Total | | | $347,497 | | | 100.0% | | | $337,865 | | | 100.0% |

| • | Company Action Level Event. Total Adjusted Capital is greater than or equal to 150% but less than 200% of RBC or Total Adjusted Capital greater than or equal to 200% but less than 250% of RBC, and has a negative trend. If there is a Company Action Level Event, the insurer must submit a plan (an “RBC Plan”) outlining, among other things, the corrective actions it intends to take in order to remedy its capital deficiency. |

| • | Regulatory Action Level Event. Total Adjusted Capital is greater than or equal to 100% but less than 150% of RBC or the insurer has failed to comply with filing deadlines for its RBC Report or RBC Plan. If there is a Regulatory Action Level Event, the insurer is also required to submit an RBC Plan. In addition, the insurance regulator must undertake a comprehensive examination of the insurer’s financial condition and must issue any appropriate corrective orders. |

| • | Authorized Control Level Event. Total Adjusted Capital is below RBC but greater than or equal to 70% of RBC or the insurer has failed to respond to a corrective order. As noted above, if there is an Authorized Control Level Event, the insurance regulator may seek rehabilitation or liquidation of the insurer if it deems it to be in the best interests of the policyholders and creditors of the insurer and the public. |

| • | Mandatory Control Level Event. Total Adjusted Capital is below 70% of RBC. If there is a Mandatory Control Level Event, the insurance regulator must seek rehabilitation or liquidation of the insurer. |

Name | | | Age | | | Position |

Andrew M. O’Brien | | | 68 | | | President and Chief Executive Officer, Director |

Julie A. Baron | | | 54 | | | Chief Financial Officer, Treasurer and Secretary |

Joy N. Edler | | | 42 | | | Chief Operating Officer |

Nicholas J. Vassallo | | | 56 | | | Chief Accounting Officer |

Jill K. Johnson | | | 43 | | | General Counsel |

Steven B. Lee | | | 68 | | | Senior Vice President and Director |

Martin A. Ericson | | | 60 | | | Senior Vice President of Underwriting |

Matthew J. Spencer | | | 43 | | | Chief Information Officer |

Daniel G. Tully | | | 59 | | | Chairman |

David G. Ellison | | | 37 | | | Director |

Randall D. Jones | | | 66 | | | Director |

Terry P. Mayotte* | | | 60 | | | Director |

| * | Mr. Mayotte is currently a director nominee and will be appointed as a director upon consummation of this offering. |

| • | the quality and integrity of our combined financial statements and our financial reporting process; |

| • | internal and external auditing and the independent registered public accounting firm’s qualifications and independence; |

| • | the performance of our internal audit function and independent registered public accounting firm; |

| • | the integrity of our systems of internal accounting and financial controls; and |

| • | our compliance with legal and regulatory requirements. |

| • | identifying individuals qualified to become board members; |

| • | recommending to the board of directors the director nominees for the next annual meeting of stockholders; |

| • | leading the board of directors in its annual review of performance; and |

| • | recommending a code of conduct and, if deemed appropriate by the compensation, nominating and corporate governance committee, corporate governance guidelines, to the board of directors. |

| • | honest and ethical conduct, including the ethical handling of actual or apparent conflicts of interest between personal and professional relationships; |

| • | full, fair, accurate, timely and understandable disclosure in reports and documents that we file with, or submit to, the SEC and in other public communications made by us; |

| • | compliance with applicable governmental laws, rules and regulations; and |

| • | prompt internal reporting to an appropriate person or persons identified in the code of conduct of violations of the code of conduct; and accountability for adherence to the code of conduct. |

Name | | | Fees Earned or Paid in Cash ($)(1) | | | Stock Awards ($)(2) | | | Total ($) |

David G. Ellison | | | — | | | — | | | — |

Randall D. Jones | | | 75,000 | | | — | | | 75,000 |

Daniel G. Tully | | | — | | | — | | | — |

Terry P. Mayotte(3) | | | — | | | — | | | — |

| (1) | The amount in this column reflects the cash compensation earned by Mr. Jones, our only non-affiliated and non-employee director, during the fiscal year ended December 31, 2019. |

| (2) | None of our directors received stock awards during the fiscal year ended December 31, 2019. As of December 31, 2019, Mr. Jones held 5.43 Class C units in Trean Holdings (of which 2.7 Class C units were unvested as of December 31, 2019) and 393,169.29 Class C units in BIC Holdings (of which 196,584.6 Class C units were unvested as of December 31, 2019). As further described in the section titled “Our organizational structure” on page 12, upon the completion of the transfers, Trean Holdings and BIC Holdings will be dissolved and will distribute in-kind shares of our common stock to the Pre-IPO Unitholders, including Mr. Jones. With respect to each of his Class C units, Mr. Jones will receive an economically equivalent amount of fully-vested shares of our common stock determined based on the initial public offering price. Assuming an initial public offering price of $14.00 per share (the midpoint of the price range set forth on the cover page of this prospectus), Mr. Jones will receive 146,806 shares of our common stock, with a value of $2,055,284. |

| (3) | Mr. Mayotte is currently a director nominee and will be appointed as a director upon consummation of this offering. |

| • | an annual cash retainer in the amount of $75,000; |

| • | for the chairman of any committee of our board of directors, an additional annual cash retainer in the amount of $15,000; |

| • | for any member of a committee of our board of directors (not including the chairman), an additional cash retainer in the amount of $5,000; |

| • | an annual equity award in the form of service-based restricted stock units; and |

| • | reimbursement for all reasonable out-of-pocket expenses incurred in connection with service on our board of directors (including affiliated and employee directors). |

Name and principal position | | | Year | | | Salary ($) | | | Bonus ($)(1) | | | All other compensation ($)(2) | | | Total ($) |

Andrew M. O’Brien President, Chief Executive Officer and Director | | | 2019 | | | 400,000 | | | 600,000 | | | 8,058 | | | 1,008,058 |

Steven B. Lee Senior Vice President and Director | | | 2019 | | | 165,000 | | | 165,000 | | | 12,122 | | | 342,122 |

Julie A. Baron Chief Financial Officer, Treasurer and Secretary | | | 2019 | | | 202,833 | | | 80,000 | | | 7,093 | | | 289,926 |

| (1) | Amounts represent a discretionary cash bonus earned by each NEO with respect to performance during the fiscal year ended December 31, 2019. |

| (2) | Amounts represent the items listed in the following table: |

Name | | | 401(k) matching contributions ($) | | | Company-paid life insurance premiums ($) |

Andrew M. O’Brien | | | — | | | 8,058 |

Steven B. Lee | | | 4,152 | | | 7,970 |

Julie A. Baron | | | 5,071 | | | 2,022 |

| • | the amounts involved exceeded or will exceed the lesser of (i) $120,000 and (ii) 1% of the average of our total assets at year end for the last two completed fiscal years; and |

| • | any of our directors, director nominees or executive officers (in each case, including their immediate family members) or beneficial holders of more than 5% of any class of our voting securities had or will have a direct or indirect material interest. |

| • | each person or group whom we know to own beneficially more than 5% of our common stock; |

| • | each of the directors, the director nominee and named executive officers individually; |

| • | all directors, the director nominee and executive officers as a group; and |

| • | each of the other selling stockholders. |