UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-23510

LORD ABBETT FLOATING RATE HIGH INCOME FUND

(Exact name of Registrant as specified in charter)

90 Hudson Street, Jersey City, New Jersey 07302-3973

(Address of principal executive offices) (Zip code)

Randolph A. Stuzin, Esq.

Vice President and Assistant Secretary

Member, Chief Legal Officer of Lord, Abbett & Co. LLC

90 Hudson Street, Jersey City, New Jersey 07302-3973

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888) 522-2388

Date of fiscal year end: 12/31

Date of reporting period: 12/31/2023

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1: | Report(s) to Shareholders. |

![]()

LORD ABBETT

ANNUAL REPORT

Lord Abbett

Floating Rate High Income Fund

For the period ended December 31, 2023

Table of Contents

Lord Abbett Floating Rate High Income Fund

Annual Report

For the period ended December 31, 2023

From left to right: Evelyn E. Guernsey, Independent Chair of the Lord Abbett Funds and Douglas B. Sieg, Trustee, President, and Chief Executive Officer of the Lord Abbett Funds. | Dear Shareholders: We are pleased to provide you with this overview of the performance of Lord Abbett Floating Rate High Income Fund for the period ended December 31, 2023. On this page and the following pages, we discuss the major factors that influenced period performance. For detailed and timely information about the Fund, please visit our website at www.lordabbett.com, where you can also access quarterly commentaries that provide updates on the Fund’s performance and other portfolio related updates. Thank you for investing in Lord Abbett Family of Funds. We value the trust that you place in us and look forward to serving your investment needs in the years to come.

Best regards,

Douglas B. Sieg Trustee, President and Chief Executive Officer |

The Lord Abbett Floating Rate High Income Fund returned 12.30%, reflecting performance at the net asset value (“NAV”) of Class I shares with all distributions reinvested, for the period starting January 10, 2023, the Fund’s performance inception, and ending December 31, 2023. The Fund’s benchmark, the Credit Suisse Leveraged Loan Index*, returned 11.68% during the same period.

Markets had to endure through a number of countervailing forces over the trailing 12 months, leading to periods of

volatility and a wide dispersion of returns. On the positive side, market expectations of a soft landing in the U.S. economy were backed by falling inflation data, a tight labor market, a resilient consumer, and optimism regarding the potential impacts of artificial intelligence. While there were concerns corporate earnings could deteriorate, aggregate earnings results were better than expected as cost-cutting measures, strength in services sectors, and supply chain improvements generally benefitted companies.2

1

Amid these positive trends, investors had concerns about aggressive U.S. Federal Reserve (the “Fed”) monetary policy and fear of a potential policy mistake leading to a recession. Investor sentiment was also negatively impacted by an underwhelming China recovery from the COVID-19 pandemic, geopolitical tensions, and rising energy prices. In addition, markets had to grapple with the ripple effects of the turmoil in the banking sector, which led to regulatory shutdowns and interventions by the Fed, FDIC, and U.S. Treasury.2

The dovish pivot by the Fed in December hinted at a potential policy easing, contributing to the market’s positive momentum and a fall in bond yields. A combination of additional factors also contributed to this positive market environment: a decline in core personal consumption expenditures (PCE) inflation, favorable Treasury refunding announcements, strong consumer resilience, and stable earnings expectations. These elements, along with a shift in market sentiment and positioning, buoyed by seasonality and increased corporate buybacks, culminated in a bullish sentiment across the equity markets.2

While there was significant rate volatility throughout the year, the 2-year Treasury yield2 moved lower from 4.42% to 4.25%, while the 10-year Treasury yield2 ended the year unchanged at 3.88%. Against this backdrop, the Bloomberg U.S. Aggregate Bond Index1 returned 5.53%, while high yield bonds3 outperformed investment grade corporate bonds4 (13.55% vs 8.52%,

respectively), partially due to the higher yield and lower duration of the high yield market.

Selection within floating rate bank loans contributed to outperformance, notably in the Healthcare and Information Technology sectors. In addition, Bohai Leasing Co., a global provider of aircraft, container, infrastructure and large equipment leasing, contributed to relative performance due to continued consumer strength coupled with bolstered demand for leisure and travel.

Due to the overall strength of the asset class throughout the period, performance at the sector level was also positive.

One notable detractor at the security level was Hurtigruten, an exotic cruise line, which faced headwinds due to an S&P downgrade based on liquidity shortfall; yet shareholders were nevertheless supportive as the company continued to improve its operational issues.

The Fund’s portfolio is actively managed and, therefore, its holdings and the weightings of a particular issuer or particular sector as a percentage of portfolio assets are subject to change. Sectors may include many industries.

* The Credit Suisse Leveraged Loan Index is designed to mirror the investable universe of the U.S. dollar-denominated leveraged loan market.

1 The Bloomberg U.S. Aggregate Bond Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Total return comprises price appreciation/depreciation and income as a percentage of the original investment.

2 Factset.

2

3 As represented by the ICE BofA U.S. High Yield Constrained Index as of 12/31/2023.

4 As represented by the Bloomberg US Corp Investment Grade Index as of 12/31/2023.

Unless otherwise specified, indexes reflect total return, with all dividends reinvested. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

Important Performance and Other Information

Performance data quoted in the following pages reflect past performance and are no guarantee of future results. Current performance may be higher or lower than the performance quoted. The investment return and principal value of an investment in the Fund will fluctuate so that shares, on any given day or when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by calling Lord Abbett at 888-522-2388 or referring to www.lordabbett.com.

Except where noted, comparative Fund performance does not account for the deduction of sales charges and would be different if sales charges were included. The Fund offers classes of shares with distinct pricing options. For a full description of the differences in pricing alternatives, please see the Fund’s prospectus.

During certain periods shown, expense waivers and reimbursements were in place. Without such expense waivers and reimbursements, the Fund’s returns would have been lower.

The annual commentary above discusses the views of the Fund’s management and various portfolio holdings of the Fund as of December 31, 2023. These views and portfolio holdings may have changed after this date. Information provided in the commentary is not a recommendation to buy or sell securities. Because the Fund’s portfolio is actively managed and may change significantly, the Fund may no longer own the securities described above or may have otherwise changed its position in the securities. For more recent information about the Fund’s portfolio holdings, please visit www.lordabbett.com.

A Note about Risk: See Notes to Consolidated Financial Statements for a discussion of investment risks. For a more detailed discussion of the risks associated with the Fund, please see the Fund’s prospectus.

Mutual funds are not insured by the FDIC, are not deposits or other obligations of, or guaranteed by, banks, and are subject to investment risks including possible loss of principal amount invested.

3

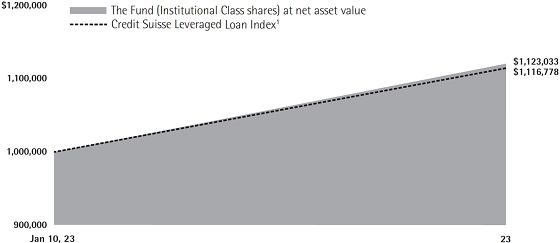

Floating Rate High Income Fund

Investment Comparison

Below is a comparison of a $1 million investment in Institutional Class shares with the same investment in the Credit Suisse Leveraged Loan Index, assuming reinvestment of all dividends and distributions. The performance of the other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursement of expenses, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns at Net Asset Value

for the Periods Ended December 31, 2023

| Life of Class | |||

| Institutional Class2 | 12.30% | ||

| Class A3 | 9.25% |

1 Performance for the unmanaged index does not reflect any fees or expenses. The performance of the index is not necessarily representative of the Fund’s performance.

2 Institutional Class shares commenced operations and performance began on January 10, 2023. Performance is at net asset value.

3 Class A shares commenced operations and performance began on January 10, 2023. Total return, which is the

percentage change in net asset value, after deduction of the maximum initial sales charge of 2.50% applicable to Class A shares, with all dividends and distributions reinvested for the periods shown ended December 31, 2023, is calculated using the SEC-required uniform method to compute such return.

4

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments (these charges vary among the share classes); and (2) ongoing costs, including management fees; distribution and service fees (these charges vary among the share classes); and other Fund expenses. You may also incur transaction costs in the form of a repurchase fee of up to 2% which the Fund may (but does not currently) impose on shares that have been accepted for repurchase that have been held for less than one year. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2023 through December 31, 2023).

Actual Expenses

For each class of the Fund, the first line of the table on the following page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading titled “Expenses Paid During Period 7/1/23 – 12/31/23” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class of the Fund, the second line of the table on the following page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

5

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value | Ending Account Value | Expenses Paid During Period† | |||||||||||

| 7/1/23 | 12/31/23 | 7/1/23 - 12/31/23 | |||||||||||

| Class I† | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,075.30 | $ | 12.34 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,013.31 | $ | 11.98 | |||||||

| Class A† | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,072.60 | $ | 15.10 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,010.64 | $ | 14.65 | |||||||

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (2.36% for Class I and 2.89% for Class A) multiplied by the average account value over the period, multiplied by 184/365 (to reflect one-half year period). |

Portfolio Holdings Presented by Sector

December 31, 2023

| Sector* | %** | |

| Asset-Backed Securities | 0.66 | % |

| Basic Materials | 1.81 | % |

| Communications | 6.88 | % |

| Consumer Cyclical | 20.37 | % |

| Consumer Non-cyclical | 11.05 | % |

| Energy | 4.24 | % |

| Financial | 14.75 | % |

| Industrial | 14.81 | % |

| Technology | 19.93 | % |

| Utilities | 1.30 | % |

| Repurchase Agreements | 4.20 | % |

| Total | 100.00 | % |

| * | A sector may comprise several industries. | |

| ** | Represents percent of total investments, which excludes derivatives. |

6

Consolidated Schedule of Investments

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| LONG-TERM INVESTMENTS 124.77% | ||||||||||||

| ASSET-BACKED SECURITIES 0.87% | ||||||||||||

| Automobiles | ||||||||||||

| CAL Receivables LLC Series 2022-1 Class B† (cost $97,490) | 9.688% (30 day USD SOFR Average + 4.35% | )# | 10/15/2026 | $ | 100,000 | $ | 99,593 | |||||

| CONVERTIBLE BONDS 0.43% | ||||||||||||

| Airlines | ||||||||||||

| JetBlue Airways Corp. (cost $59,349) | 0.50% | 4/1/2026 | 69,000 | 50,024 | ||||||||

| CORPORATE BONDS 8.26% | ||||||||||||

| Aerospace/Defense 1.21% | ||||||||||||

| Triumph Group, Inc. | 7.75% | 8/15/2025 | 140,000 | 139,654 | ||||||||

| Airlines 0.46% | ||||||||||||

| VistaJet Malta Finance PLC/Vista Management Holding, Inc. (Malta)†(a) | 9.50% | 6/1/2028 | 62,000 | 52,547 | ||||||||

| Diversified Financial Services 1.11% | ||||||||||||

| Global Aircraft Leasing Co. Ltd. (Cayman Islands)†(a) | 6.50% | 9/15/2024 | 138,000 | 127,215 | ||||||||

| Internet 0.62% | ||||||||||||

| EquipmentShare.com, Inc.† | 9.00% | 5/15/2028 | 69,000 | 71,077 | ||||||||

| Machinery-Diversified 0.89% | ||||||||||||

| Husky III Holding Ltd. (Canada)†(a) | 13.00% | 2/15/2025 | 103,000 | 102,806 | ||||||||

| Oil & Gas 1.99% | ||||||||||||

| Berry Petroleum Co. LLC† | 7.00% | 2/15/2026 | 92,000 | 89,103 | ||||||||

| Crescent Energy Finance LLC† | 7.25% | 5/1/2026 | 69,000 | 69,496 | ||||||||

| Crescent Energy Finance LLC† | 9.25% | 2/15/2028 | 28,000 | 29,074 | ||||||||

| Vital Energy, Inc. | 9.75% | 10/15/2030 | 40,000 | 41,497 | ||||||||

| Total | 229,170 | |||||||||||

| Pharmaceuticals 0.59% | ||||||||||||

| Herbalife Nutrition Ltd./HLF Financing, Inc.† | 7.875% | 9/1/2025 | 69,000 | 68,237 | ||||||||

| Retail 0.44% | ||||||||||||

| GPS Hospitality Holding Co. LLC/GPS Finco, Inc.† | 7.00% | 8/15/2028 | 69,000 | 50,433 | ||||||||

| See Notes to Consolidated Financial Statements. | 7 |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Telecommunications 0.96% | ||||||||||||

| Altice France SA(b) | 2.50% | 1/15/2025 | EUR | 103,000 | $ | 109,925 | ||||||

| Total Corporate Bonds (cost $934,543) | 951,064 | |||||||||||

| Shares | ||||||||||||

| EXCHANGE-TRADED FUND 3.26% | ||||||||||||

| Exchange-Traded Funds | ||||||||||||

| Invesco Senior Loan ETF (cost $373,425) | 17,699 | 374,865 | ||||||||||

| Principal Amount | ||||||||||||

| FLOATING RATE LOANS(c) 111.96% | ||||||||||||

| Advertising 0.59% | ||||||||||||

| Summer (BC) Holdco B SARL 2021 USD Term Loan B2 | 10.108% (3 mo. USD Term SOFR + 4.50% | ) | 12/4/2026 | $ | 68,649 | 68,123 | ||||||

| Aerospace 2.77% | ||||||||||||

| Cobham Ultra SeniorCo SARL USD Term Loan B | 9.363% (6 mo. USD Term SOFR + 3.50% | ) | 8/3/2029 | 72,818 | 71,944 | |||||||

| Peraton Corp. 2nd Lien Term Loan B1 | 13.222% (3 mo. USD Term SOFR + 7.75% | ) | 2/1/2029 | 137,679 | 137,313 | |||||||

| United Airlines, Inc. 2021 Term Loan B(d) | 9.22% (1 mo. USD Term SOFR + 3.75% | ) | 4/21/2028 | 108,998 | 109,543 | |||||||

| Total | 318,800 | |||||||||||

| Aerospace/Defense 2.39% | ||||||||||||

| Bleriot U.S. Bidco, Inc. 2023 Term Loan B | 9.61% (3 mo. USD Term SOFR + 4.00% | ) | 10/31/2028 | 68,477 | 68,838 | |||||||

| Dynasty Acquisition Co., Inc. 2023 Term Loan B1 | 9.356% (1 mo. USD Term SOFR + 4.00% | ) | 8/24/2028 | 95,620 | 95,987 | |||||||

| Dynasty Acquisition Co., Inc. 2023 Term Loan B2 | 9.356% (1 mo. USD Term SOFR + 4.00% | ) | 8/24/2028 | 40,980 | 41,137 | |||||||

| Vertex Aerospace Services Corp. 2021 First Lien Term Loan | 8.706% (1 mo. USD Term SOFR + 3.25% | ) | 12/6/2028 | 68,479 | 68,638 | |||||||

| Total | 274,600 | |||||||||||

| 8 | See Notes to Consolidated Financial Statements. |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Auto Parts & Equipment 1.25% | ||||||||||||

| RealTruck Group, Inc. 2023 Incremental Term Loan(d) | 10.47% (1 mo. USD Term SOFR + 5.00% | ) | 1/31/2028 | $ | 73,000 | $ | 73,000 | |||||

| Tenneco, Inc. 2022 Term Loan B | – | (e) | 11/17/2028 | 80,000 | 70,805 | |||||||

| Total | 143,805 | |||||||||||

| Automotive 0.60% | ||||||||||||

| Autokiniton U.S. Holdings, Inc. 2021 Term Loan B(d) | 9.97% (1 mo. USD Term SOFR + 4.50% | ) | 4/6/2028 | 68,649 | 68,998 | |||||||

| Banks 0.87% | ||||||||||||

| AqGen Ascensus, Inc. 2021 2nd Lien Term Loan | 12.176% (3 mo. USD Term SOFR + 6.50% | ) | 8/2/2029 | 104,000 | 100,425 | |||||||

| Building & Construction 0.70% | ||||||||||||

| Legence Holdings LLC 2021 Term Loan(d) | 8.956% (1 mo. USD Term SOFR + 3.50% | ) | 12/16/2027 | 80,250 | 80,459 | |||||||

| Building Materials 1.99% | ||||||||||||

| ACProducts, Inc. 2021 Term Loan B | 9.86% (3 mo. USD Term SOFR + 4.25% | ) | 5/17/2028 | 102,126 | 89,899 | |||||||

| Clay Holdco BV 2023 EUR Term Loan B2(b) | – | (e) | 12/31/2029 | EUR | 67,000 | 70,831 | (f) | |||||

| CP Atlas Buyer, Inc. 2021 Term Loan B(d) | 9.206% (1 mo. USD Term SOFR + 3.75% | ) | 11/23/2027 | $ | 68,828 | 67,889 | ||||||

| Total | 228,619 | |||||||||||

| Chemicals 3.92% | ||||||||||||

| Cyanco Intermediate 2 Corp. 2023 Term Loan B(d) | 10.106% (1 mo. USD Term SOFR + 4.75% | ) | 7/10/2028 | 69,000 | 69,316 | |||||||

| DCG Acquisition Corp. Term Loan B(d) | – | (e) | 9/30/2026 | 110,000 | 109,519 | |||||||

| LSF11 A5 Holdco LLC 2023 Incremental Term Loan B(d) | 9.706% (1 mo. USD Term SOFR + 4.25% | ) | 10/15/2028 | 68,828 | 69,143 | |||||||

| Olympus Water U.S. Holding Corp. 2021 USD Term Loan B(d) | 9.36% (3 mo. USD Term SOFR + 3.75% | ) | 11/9/2028 | 68,825 | 68,782 | |||||||

| Plaskolite LLC 2021 Term Loan | 9.645% (3 mo. USD Term SOFR + 4.00% | ) | 12/15/2025 | 69,000 | 66,154 | |||||||

| Starfruit Finco BV 2023 Term Loan B (Netherlands)(a) | 9.441% (1 mo. USD Term SOFR + 4.00% | ) | 4/3/2028 | 68,561 | 68,904 | |||||||

| Total | 451,818 | |||||||||||

| See Notes to Consolidated Financial Statements. | 9 |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Commercial Services 4.28% | ||||||||||||

| Allied Universal Holdco LLC 2023 Term Loan B(d) | – | (e) | 5/12/2028 | $ | 73,000 | $ | 73,165 | |||||

| AVSC Holding Corp. 2020 Term Loan B1 | 8.956% (1 mo. USD Term SOFR + 3.25% | ) | 3/3/2025 | 68,846 | 67,680 | |||||||

| CHG Healthcare Services, Inc. 2023 Incremental Term Loan(d) | 9.145% (3 mo. USD Term SOFR + 3.75% | ) | 9/29/2028 | 58,857 | 59,047 | |||||||

| Mavis Tire Express Services Corp. 2021 Term Loan B(d) | – | (e) | 5/4/2028 | 87,532 | 87,806 | |||||||

| Spring Education Group, Inc. Term Loan(d) | 9.848% (3 mo. USD Term SOFR + 4.50% | ) | 10/4/2030 | 102,193 | 102,615 | |||||||

| Verscend Holding Corp. 2021 Term Loan B(d) | 9.47% (1 mo. USD Term SOFR + 4.00% | ) | 8/27/2025 | 102,476 | 102,945 | |||||||

| Total | 493,258 | |||||||||||

| Construction & Engineering 0.60% | ||||||||||||

| Brand Industrial Services, Inc. 2023 Term Loan B | 10.877% (3 mo. USD Term SOFR + 5.50% | ) | 8/1/2030 | 69,058 | 68,818 | |||||||

| Containers & Packaging 2.24% | ||||||||||||

| Charter NEX U.S., Inc. 2021 Term Loan(d) | 9.22% (1 mo. USD Term SOFR + 3.75% | ) | 12/1/2027 | 115,557 | 116,225 | |||||||

| Pretium Packaging LLC Second Out Term Loan A1 | – | (e) | 10/2/2028 | 99,000 | 77,962 | |||||||

| Proampac PG Borrower LLC 2023 Term Loan(d) | 9.868% - 9.89% (3 mo. USD Term SOFR + 4.50% | ) | 9/15/2028 | 64,000 | 64,200 | |||||||

| Total | 258,387 | |||||||||||

| Distribution/Wholesale 0.60% | ||||||||||||

| BCPE Empire Holdings, Inc. 2023 Extended Term Loan(d) | 10.106% (1 mo. USD Term SOFR + 4.75% | ) | 12/11/2028 | 68,828 | 69,099 | |||||||

| Diversified Capital Goods 0.91% | ||||||||||||

| CeramTec AcquiCo GmbH 2022 EUR Term Loan B(b) | 7.455% (3 mo. EURIBOR + 3.50% | ) | 3/16/2029 | EUR | 95,078 | 104,421 | ||||||

| Diversified Financial Services 2.87% | ||||||||||||

| Advisor Group, Inc. 2023 Term Loan B(d) | 9.856% (1 mo. USD Term SOFR + 4.50% | ) | 8/17/2028 | $ | 124,836 | 125,392 | ||||||

| Minotaur Acquisition, Inc. Term Loan B(d) | 10.206% (1 mo. USD Term SOFR + 4.75% | ) | 3/27/2026 | 135,932 | 136,139 | |||||||

| NFP Corp. 2020 Term Loan(d) | 8.72% (1 mo. USD Term SOFR + 3.25% | ) | 2/16/2027 | 68,822 | 69,257 | |||||||

| Total | 330,788 | |||||||||||

| 10 | See Notes to Consolidated Financial Statements. |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Electric: Generation 1.17% | ||||||||||||

| EFS Cogen Holdings I LLC 2020 Term Loan B(d) | 9.11% (3 mo. USD Term SOFR + 3.50% | ) | 10/1/2027 | $ | 134,252 | $ | 134,244 | |||||

| Entertainment 1.93% | ||||||||||||

| ECL Entertainment LLC 2023 Term Loan B(d) | 10.106% (1 mo. USD Term SOFR + 4.75% | ) | 8/31/2030 | 150,000 | 150,600 | |||||||

| Motion Finco SARL 2023 EUR Term Loan B(b) | 7.925% (3 mo. EURIBOR + 4.00% | ) | 11/12/2029 | EUR | 64,384 | 71,132 | ||||||

| Total | 221,732 | |||||||||||

| Environmental Control 0.80% | ||||||||||||

| Heritage-Crystal Clean, Inc. Term Loan B(d) | 10.403% (3 mo. USD Term SOFR + 5.00% | ) | 10/17/2030 | $ | 92,000 | 92,345 | ||||||

| Financial 3.87% | ||||||||||||

| Acrisure LLC 2021 First Lien Term Loan B(d) | 9.90% (3 mo. USD LIBOR + 4.25% | ) | 2/15/2027 | 68,651 | 68,951 | |||||||

| AqGen Island Holdings, Inc. Term Loan(d) | 8.97% (1 mo. USD Term SOFR + 3.50% | ) | 8/2/2028 | 41,298 | 41,267 | |||||||

| AssuredPartners, Inc. 2020 Term Loan B | 8.97% (1 mo. USD Term SOFR + 3.50% | ) | 2/12/2027 | 68,289 | 68,528 | |||||||

| Asurion LLC 2021 Second Lien Term Loan B4(d) | 10.72% (1 mo. USD Term SOFR + 5.25% | ) | 1/20/2029 | 55,000 | 52,039 | |||||||

| Edelman Financial Center LLC 2018 2nd Lien Term Loan | 12.22% (1 mo. USD Term SOFR + 6.75% | ) | 7/20/2026 | 140,000 | 140,263 | |||||||

| OneDigital Borrower LLC 2021 Term Loan(d) | – | (e) | 11/16/2027 | 74,477 | 74,524 | |||||||

| Total | 445,572 | |||||||||||

| Food 1.59% | ||||||||||||

| Chobani LLC 2023 Incremental Term Loan(d) | 9.112% (3 mo. USD Term SOFR + 3.75% | ) | 10/25/2027 | 110,000 | 110,321 | |||||||

| Wm Morrison EUR Term Loan B1(b) | 8.752% (3 mo. EURIBOR + 4.75% | ) | 11/4/2027 | EUR | 69,000 | 72,542 | ||||||

| Total | 182,863 | |||||||||||

| Gaming/Leisure 4.27% | ||||||||||||

| 888 Acquisitions Ltd. USD Term Loan B (United Kingdom)(a) | 10.818% (6 mo. USD Term SOFR + 5.25% | ) | 7/1/2028 | $ | 182,624 | 177,797 | ||||||

| Fertitta Entertainment LLC 2022 Term Loan B | – | (e) | 1/27/2029 | 103,214 | 103,392 | |||||||

| Motion Finco Sarl Delayed Draw Term Loan B2 (Luxembourg)(a)(d) | 8.86% (3 mo. USD Term SOFR + 3.25% | ) | 11/12/2026 | 932 | 934 | |||||||

| See Notes to Consolidated Financial Statements. | 11 |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Gaming/Leisure (continued) | ||||||||||||

| Motion Finco Sarl USD Term Loan B1 (Luxembourg)(a)(d) | 8.86% (3 mo. USD Term SOFR + 3.25% | ) | 11/12/2026 | $ | 6,540 | $ | 6,554 | |||||

| Scientific Games Holdings LP 2022 USD Term Loan B | 8.664% (3 mo. USD Term SOFR + 3.25% | ) | 4/4/2029 | 99,248 | 99,409 | |||||||

| Silk Bidco AS EUR Term Loan B(b) | – | (e) | 2/28/2027 | EUR | 69,000 | 41,759 | ||||||

| United FP Holdings LLC 2019 1st Lien Term Loan | 9.645% (3 mo. USD Term SOFR + 4.00% | ) | 12/30/2026 | $ | 68,291 | 61,240 | ||||||

| Total | 491,085 | |||||||||||

| Gas Distribution 0.60% | ||||||||||||

| Freeport LNG Investments LLLP Term Loan B(d) | 9.177% (3 mo. USD Term SOFR + 3.50% | ) | 12/21/2028 | 68,473 | 68,541 | |||||||

| Health Care Products 0.54% | ||||||||||||

| Curia Global, Inc. 2021 Term Loan | 9.233% (3 mo. USD Term SOFR + 3.75% | ) | 8/30/2026 | 68,649 | 61,977 | |||||||

| Health Care Services 4.35% | ||||||||||||

| ADMI Corp. 2023 First Lean(d) | – | (e) | 12/23/2027 | 108,353 | 108,344 | |||||||

| ADMI Corp. 2023 Term Loan B5(d) | – | (e) | 12/23/2027 | 59,647 | 58,901 | (f) | ||||||

| Dermatology Intermediate Holdings III, Inc. 2023 Incremental Term Loan B | 10.878% (3 mo. USD Term SOFR + 5.50% | ) | 3/30/2029 | 102,000 | 100,343 | |||||||

| Heartland Dental LLC 2023 Term Loan B(d) | 10.358% (1 mo. USD Term SOFR + 5.00% | ) | 4/28/2028 | 139,293 | 139,250 | |||||||

| Star Parent, Inc. Term Loan B(d) | 9.348% (3 mo. USD Term SOFR + 4.00% | ) | 9/27/2030 | 95,000 | 94,116 | |||||||

| Total | 500,954 | |||||||||||

| Healthcare 9.61% | ||||||||||||

| Athenahealth Group, Inc. 2022 Term Loan B(d) | 8.606% (1 mo. USD Term SOFR + 3.25% | ) | 2/15/2029 | 61,004 | 60,821 | |||||||

| CCRR Parent, Inc. Term Loan B(d) | 9.22% (1 mo. USD Term SOFR + 3.75% | ) | 3/6/2028 | 72,290 | 70,393 | |||||||

| CNT Holdings I Corp. 2020 2nd Lien Term Loan | 12.176% (3 mo. USD Term SOFR + 6.75% | ) | 11/6/2028 | 138,950 | 139,689 | |||||||

| Covetrus, Inc. Term Loan(d) | 10.348% (3 mo. USD Term SOFR + 5.00% | ) | 10/13/2029 | 68,827 | 68,881 | |||||||

| eResearchTechnology, Inc. 2020 1st Lien Term Loan(d) | 9.97% (1 mo. USD Term SOFR + 4.50% | ) | 2/4/2027 | 135,946 | 135,978 | |||||||

| 12 | See Notes to Consolidated Financial Statements. |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Healthcare (continued) | ||||||||||||

| Hunter Holdco 3 Ltd. USD Term Loan B (United Kingdom)(a)(d) | 9.698% (3 mo. USD Term SOFR + 4.25% | ) | 8/19/2028 | $ | 69,000 | $ | 68,942 | |||||

| MedAssets Software Intermediate Holdings, Inc. 2021 Term Loan | 9.47% (1 mo. USD Term SOFR + 4.00% | ) | 12/18/2028 | 68,652 | 54,887 | |||||||

| Medical Solutions Holdings, Inc. 2021 1st Lien Term Loan(d) | 8.706% (1 mo. USD Term SOFR + 3.25% | ) | 11/1/2028 | 110,481 | 104,037 | |||||||

| Navicure, Inc. 2019 Term Loan B(d) | 9.47% (1 mo. USD Term SOFR + 4.00% | ) | 10/22/2026 | 68,468 | 68,810 | |||||||

| Physician Partners LLC Term Loan | – | (e) | 12/26/2028 | 56,020 | 53,089 | |||||||

| Southern Veterinary Partners LLC Term Loan(d) | 9.47% (1 mo. USD Term SOFR + 4.00% | ) | 10/5/2027 | 102,212 | 102,020 | |||||||

| Summit Behavioral Healthcare LLC 1st Lien Term Loan(d) | 10.40% (3 mo. USD Term SOFR + 4.75% | ) | 11/24/2028 | 179,222 | 179,266 | |||||||

| Total | 1,106,813 | |||||||||||

| Home Furnishings 0.26% | ||||||||||||

| AI Aqua Merger Sub, Inc. 2023 Incremental Term Loan | – | (e) | 7/31/2028 | 30,000 | 30,188 | |||||||

| Housewares 0.82% | ||||||||||||

| Springs Windows Fashions LLC 2021 Term Loan B | 9.47% (1 mo. USD Term SOFR + 4.00% | ) | 10/6/2028 | 104,468 | 93,859 | |||||||

| Housing 2.72% | ||||||||||||

| Cornerstone Building Brands, Inc. 2021 Term Loan B | 8.712% (1 mo. USD Term SOFR + 3.25% | ) | 4/12/2028 | 102,214 | 102,416 | |||||||

| Icebox Holdco III, Inc. 2021 2nd Lien Term Loan | 12.36% (3 mo. USD Term SOFR + 6.75% | ) | 12/21/2029 | 69,000 | 63,135 | |||||||

| LBM Acquisition LLC Term Loan B(d) | 9.106% (1 mo. USD Term SOFR + 3.75% | ) | 12/17/2027 | 80,444 | 79,677 | |||||||

| SRS Distribution, Inc. 2021 Term Loan B(d) | 8.97% (1 mo. USD Term SOFR + 3.50% | ) | 6/2/2028 | 68,301 | 68,501 | |||||||

| Total | 313,729 | |||||||||||

| Information Technology 5.09% | ||||||||||||

| AP Core Holdings II LLC High-Yield Term Loan B2(d) | 10.97% (1 mo. USD Term SOFR + 5.50% | ) | 9/1/2027 | 69,000 | 67,534 | |||||||

| Apttus Corp. 2021 Term Loan(d) | 9.47% (1 mo. USD Term SOFR + 4.00% | ) | 5/8/2028 | 68,301 | 68,564 | |||||||

| See Notes to Consolidated Financial Statements. | 13 |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Information Technology (continued) | ||||||||||||

| Cloud Software Group, Inc. 2022 USD Term Loan B | 9.948% (3 mo. USD Term SOFR + 4.50% | ) | 3/30/2029 | $ | 144,122 | $ | 141,141 | |||||

| ConnectWise LLC 2021 Term Loan B(d) | 9.11% (3 mo. USD Term SOFR + 3.50% | ) | 9/29/2028 | 68,477 | 68,477 | |||||||

| McAfee LLC 2022 USD Term Loan B | 9.193% (1 mo. USD Term SOFR + 3.75% | ) | 3/1/2029 | 103,564 | 103,413 | |||||||

| Project Boost Purchaser LLC 2019 Term Loan B(d) | 8.97% (1 mo. USD Term SOFR + 3.50% | ) | 6/1/2026 | 68,465 | 68,609 | |||||||

| Surf Holdings LLC USD Term Loan(d) | 8.974% (1 mo. USD Term SOFR + 3.50% | ) | 3/5/2027 | 68,470 | 68,701 | |||||||

| Total | 586,439 | |||||||||||

| Insurance 3.00% | ||||||||||||

| Amynta Agency Borrower Inc. 2023 1st Lien Term Loan B(d) | 9.606% (1 mo. USD Term SOFR + 4.25% | ) | 2/28/2028 | 146,174 | 146,540 | |||||||

| Asurion LLC 2023 Term Loan B11(d) | 9.706% (1 mo. USD Term SOFR + 4.25% | ) | 8/19/2028 | 55,000 | 54,882 | |||||||

| Jones Deslauriers Insurance Management, Inc. 2023 Term Loan B (Canada)(a) | 9.625% (3 mo. USD Term SOFR + 4.25% | ) | 3/15/2030 | 69,000 | 69,388 | |||||||

| Sedgwick Claims Management Services, Inc. 2023 Term Loan B(d) | 9.106% (1 mo. USD Term SOFR + 3.75% | ) | 2/24/2028 | 74,742 | 75,064 | |||||||

| Total | 345,874 | |||||||||||

| Internet 0.82% | ||||||||||||

| MH Sub I LLC 2021 2nd Lien Term Loan | 11.606% (1 mo. USD Term SOFR + 6.25% | ) | 2/23/2029 | 28,253 | 26,533 | |||||||

| MH Sub I LLC 2023 Term Loan(d) | 9.606% (1 mo. USD Term SOFR + 4.25% | ) | 5/3/2028 | 68,651 | 67,621 | |||||||

| Total | 94,154 | |||||||||||

| Internet Companies 0.59% | ||||||||||||

| NEXUS Buyer LLC 2021 Second Lien Term Loan | 11.706% (1 mo. USD Term SOFR + 6.25% | ) | 11/5/2029 | 69,000 | 67,577 | |||||||

| Investment Management Companies 1.14% | ||||||||||||

| Aragorn Parent Corporation Term Loan(d) | – | (e) | 6/15/2028 | 62,000 | 62,020 | |||||||

| NEXUS Buyer LLC 2023 Term Loan B2(d) | – | (e) | 12/13/2028 | 70,000 | 69,650 | |||||||

| Total | 131,670 | |||||||||||

| 14 | See Notes to Consolidated Financial Statements. |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Leisure Time 2.04% | ||||||||||||

| Amer Sports OYJ EUR Term Loan B(b) | 7.948% (3 mo. EURIBOR + 4.00% | ) | 3/30/2026 | EUR | 80,000 | $ | 88,660 | |||||

| Hurtigruten ASA EUR Term Loan A(b) | 11.932% (3 mo. EURIBOR + 8.00% | ) | 9/30/2024 | EUR | 7,301 | 7,576 | (g) | |||||

| Life Time Fitness, Inc 2023 1st Lien Term Loan B(d) | 10.111% (6 mo. USD Term SOFR + 4.25% | ) | 1/15/2026 | $ | 138,000 | 139,104 | ||||||

| Total | 235,340 | |||||||||||

| Lodging 0.85% | ||||||||||||

| Spectacle Gary Holdings LLC 2021 Term Loan B | 9.748% (3 mo. USD Term SOFR + 4.25% | ) | 12/11/2028 | 99,971 | 97,909 | |||||||

| Machinery: Diversified 3.54% | ||||||||||||

| Arcline FM Holdings LLC 2023 Incremental Term Loan B(d) | 10.86% (3 mo. USD Term SOFR + 5.25% | ) | 6/23/2028 | 147,000 | 147,368 | |||||||

| CPM Holdings, Inc. 2023 Term Loan | 9.843% (1 mo. USD Term SOFR + 4.50% | ) | 9/28/2028 | 21,000 | 21,096 | |||||||

| Engineered Machinery Holdings, Inc. 2021 USD 2nd Lien Term Loan | 11.61% (3 mo. USD Term SOFR + 6.00% | ) | 5/21/2029 | 69,977 | 66,128 | |||||||

| LSF12 Badger Bidco LLC Term Loan B | 11.356% (1 mo. USD Term SOFR + 6.00% | ) | 8/30/2030 | 103,326 | 103,261 | |||||||

| SPX Flow, Inc. 2022 Term Loan(d) | 9.956% (1 mo. USD Term SOFR + 4.50% | ) | 4/5/2029 | 69,000 | 69,316 | |||||||

| Total | 407,169 | |||||||||||

| Manufacturing 5.11% | ||||||||||||

| AMC Entertainment Holdings, Inc. 2019 Term Loan B | 8.474% (1 mo. USD Term SOFR + 3.00% | ) | 4/22/2026 | 110,000 | 92,194 | |||||||

| Chamberlain Group, Inc. Term Loan B | 8.706% (1 mo. USD Term SOFR + 3.25% | ) | 11/3/2028 | 102,220 | 102,110 | |||||||

| DirecTV Financing LLC Term Loan(d) | 10.65% (3 mo. USD Term SOFR + 5.00% | ) | 8/2/2027 | 109,378 | 109,577 | |||||||

| Frontier Communications Corp. 2021 1st Lien Term Loan(d) | 9.22% (1 mo. USD Term SOFR + 3.75% | ) | 10/8/2027 | 147,824 | 147,269 | |||||||

| Pro Mach Group, Inc. 2021 Term Loan B(d) | 9.47% (1 mo. USD Term SOFR + 4.00% | ) | 8/31/2028 | 68,477 | 68,763 | |||||||

| Univision Communications, Inc. 2022 First Lien Term Loan B | 9.598% (3 mo. USD Term SOFR + 4.25% | ) | 6/24/2029 | 68,480 | 68,754 | |||||||

| Total | 588,667 | |||||||||||

| See Notes to Consolidated Financial Statements. | 15 |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Metal Fabricate/Hardware 0.85% | ||||||||||||

| Tank Holding Corp. 2022 Term Loan | 11.206% (1 mo. USD Term SOFR + 5.75% | ) | 3/31/2028 | $ | 68,480 | $ | 65,741 | |||||

| Tank Holding Corp. 2023 Incremental Delayed Draw Term Loan(h) | 11.46% (1 mo. USD Term SOFR + 6.00% | ) | 3/31/2028 | 10,200 | 9,817 | (f) | ||||||

| Tank Holding Corp. 2023 Incremental Term Loan | 11.455% (1 mo. USD Term SOFR + 6.00% | ) | 3/31/2028 | 23,681 | 22,793 | |||||||

| Total | 98,351 | |||||||||||

| Mining & Metals 0.30% | ||||||||||||

| Arsenal AIC Parent LLC Term Loan | 9.856% (1 mo. USD Term SOFR + 4.50% | ) | 8/18/2030 | 34,883 | 35,079 | |||||||

| Office Furniture & Business Equipment 0.96% | ||||||||||||

| Xerox Holdings Corp. 2023 Term Loan B(d) | 9.356% (1 mo. USD Term SOFR + 4.00% | ) | 11/17/2029 | 110,000 | 110,344 | |||||||

| Oil & Gas 0.74% | ||||||||||||

| Parkway Generation LLC Term Loan B | 10.395% (3 mo. USD Term SOFR + 4.75% | ) | 2/18/2029 | 78,299 | 75,488 | |||||||

| Parkway Generation LLC Term Loan C | 10.395% (3 mo. USD Term SOFR + 4.75% | ) | 2/18/2029 | 10,349 | 9,977 | |||||||

| Total | 85,465 | |||||||||||

| Packaging 0.60% | ||||||||||||

| Clydesdale Acquisition Holdings, Inc. Term Loan B | 9.631% (1 mo. USD Term SOFR + 4.18% | ) | 4/13/2029 | 68,540 | 68,926 | |||||||

| Personal & Household Products 1.59% | ||||||||||||

| AI Aqua Merger Sub, Inc. 2021 1st Lien Term Loan B | 9.093% (1 mo. USD Term SOFR + 3.75% | ) | 7/31/2028 | 182,741 | 183,109 | |||||||

| Pharmaceuticals 1.46% | ||||||||||||

| Ceva Sante Animale 2023 USD Term Loan B (France)(a) | 9.616% (3 mo. USD Term SOFR + 4.25% | ) | 11/1/2030 | 31,000 | 31,092 | |||||||

| Packaging Coordinators Midco, Inc. 2020 1st Lien Term Loan | 9.11% (3 mo. USD Term SOFR + 3.50% | ) | 11/30/2027 | 136,595 | 136,852 | |||||||

| Total | 167,944 | |||||||||||

| 16 | See Notes to Consolidated Financial Statements. |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Pipelines 1.80% | ||||||||||||

| Brazos Delaware II LLC 2023 Term Loan B(d) | 9.108% (1 mo. USD Term SOFR + 3.75% | ) | 2/11/2030 | $ | 38,308 | $ | 38,445 | |||||

| Epic Crude Services LP Term Loan B | – | (e) | 3/2/2026 | 100,277 | 100,139 | |||||||

| Epic Y-Grade Services LP 2020 Term Loan | 11.371% - 11.49% (3 mo. USD Term SOFR + 6.00% | ) | 6/30/2027 | 70,000 | 68,561 | |||||||

| Total | 207,145 | |||||||||||

| Retail 4.22% | ||||||||||||

| Birkenstock GmbH & Co. KG USD Term Loan B (Germany)(a) | 8.894% (3 mo. USD Term SOFR + 3.25% | ) | 4/28/2028 | 27,305 | 27,421 | |||||||

| Evergreen Acqco 1 LP 2021 USD Term Loan(d) | 10.86% (3 mo. USD Term SOFR + 5.25% | ) | 4/26/2028 | 57,279 | 57,594 | |||||||

| Flynn Restaurant Group LP 2021 Term Loan B(d) | 9.72% (1 mo. USD Term SOFR + 4.25% | ) | 12/1/2028 | 69,209 | 69,642 | |||||||

| Fogo De Chao, Inc. 2023 Term Loan B | 10.106% (1 mo. USD Term SOFR + 4.75% | ) | 9/30/2030 | 103,000 | 101,240 | |||||||

| K-Mac Holdings Corp. 2021 Term Loan(d) | 8.72% (1 mo. USD Term SOFR + 3.25% | ) | 7/21/2028 | 102,737 | 102,801 | |||||||

| Peer Holding III BV 2023 USD Term Loan B4 (Netherlands)(a)(d) | –(e) | 10/28/2030 | 59,000 | 59,258 | ||||||||

| PetSmart, Inc. 2021 Term Loan B(d) | 9.206% (1 mo. USD Term SOFR + 3.75% | ) | 2/11/2028 | 68,301 | 67,653 | |||||||

| Total | 485,609 | |||||||||||

| Service 5.38% | ||||||||||||

| Amentum Government Services Holdings LLC 2022 Term Loan(d) | 9.358% (1 mo. USD Term SOFR + 4.00% | ) | 2/15/2029 | 68,480 | 68,634 | |||||||

| DTI Holdco, Inc. 2022 Term Loan(d) | 10.133% (3 mo. USD Term SOFR + 4.75% | ) | 4/26/2029 | 103,393 | 102,451 | |||||||

| Magnite, Inc. Term Loan(d) | 10.47% - 10.65% (1 mo. USD Term SOFR + 5.00% (3 mo. USD Term SOFR + 5.00% | ) ) | 4/28/2028 | 136,951 | 137,608 | |||||||

| Red Planet Borrower LLC Term Loan B(d) | 9.206% (1 mo. USD Term SOFR + 3.75% | ) | 10/2/2028 | 68,650 | 66,123 | |||||||

| Renaissance Holding Corp. 2023 Refi Term Loan(d) | 10.106% (1 mo. USD Term SOFR + 4.75% | ) | 4/5/2030 | 73,000 | 73,355 | |||||||

| Service Logic Acquisition, Inc. Term Loan(d) | 9.645% (3 mo. USD Term SOFR + 4.00% | ) | 10/29/2027 | 68,473 | 68,530 | |||||||

| See Notes to Consolidated Financial Statements. | 17 |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Service (continued) | ||||||||||||

| Sophia LP 2021 Term Loan B(d) | 8.956% (1 mo. USD Term SOFR + 3.50% | ) | 10/7/2027 | $ | 68,476 | $ | 68,706 | |||||

| SRS Distribution, Inc. 2022 Incremental Term Loan(d) | 8.956% (1 mo. USD Term SOFR + 3.50% | ) | 6/2/2028 | 33,742 | 33,795 | |||||||

| Total | 619,202 | |||||||||||

| Shipbuilding 1.08% | ||||||||||||

| LSF11 Trinity Bidco, Inc. 2023 Term Loan(d) | 9.358% (1 mo. USD Term SOFR + 4.00% | ) | 6/14/2030 | 123,017 | 123,939 | |||||||

| Software 7.51% | ||||||||||||

| Banff Merger Sub, Inc. 2021 USD 2nd Lien Term Loan | 10.97% (1 mo. USD Term SOFR + 5.50% | ) | 2/27/2026 | 137,992 | 137,992 | |||||||

| Central Parent, Inc. 2023 Term Loan B(d) | 9.348% (3 mo. USD Term SOFR + 4.00% | ) | 7/6/2029 | 68,483 | 68,950 | |||||||

| Cvent, Inc. 2023 Term Loan B(d) | 9.098% (3 mo. USD Term SOFR + 3.75% | ) | 6/17/2030 | 118,000 | 118,295 | |||||||

| Isolved, Inc. Term Loan B(d) | 9.484% (3 mo. USD Term SOFR + 4.00% | ) | 10/14/2030 | 78,000 | 78,244 | |||||||

| Mitchell International, Inc. 2021 2nd Lien Term Loan | – | (e) | 10/15/2029 | 110,000 | 108,316 | |||||||

| Mosel Bidco SE USD Term Loan B (Germany)(a) | 10.098% (3 mo. USD Term SOFR + 4.75% | ) | 9/16/2030 | 61,000 | 61,152 | |||||||

| Physician Partners LLC 2023 Incremental Term Loan B | 10.883% (3 mo. USD Term SOFR + 5.50% | ) | 12/23/2028 | 5,000 | 4,775 | |||||||

| Project Alpha Intermediate Holding, Inc. 2023 1st Lien Term Loan B | 10.106% (1 mo. USD Term SOFR + 4.75% | ) | 10/28/2030 | 73,000 | 73,540 | |||||||

| Quartz Acquireco LLC Term Loan B(d) | 8.856% (1 mo. USD Term SOFR + 3.50% | ) | 6/28/2030 | 68,370 | 68,669 | |||||||

| Rocket Software, Inc. 2023 USD Term Loan(d) | 10.106% (1 mo. USD Term SOFR + 4.75% | ) | 11/28/2028 | 147,000 | 144,703 | |||||||

| Total | 864,636 | |||||||||||

| Software/Services 0.94% | ||||||||||||

| Proofpoint, Inc. 2nd Lien Term Loan | 11.72% (1 mo. USD Term SOFR + 6.25% | ) | 8/31/2029 | 107,000 | 108,338 | |||||||

| Technology Hardware & Equipment 0.56% | ||||||||||||

| Atlas CC Acquisition Corp. Term Loan B | 9.90% (3 mo. USD Term SOFR + 4.25% | ) | 5/25/2028 | 56,901 | 53,145 | |||||||

| Atlas CC Acquisition Corp. Term Loan C | 9.90% (3 mo. USD Term SOFR + 4.25% | ) | 5/25/2028 | 11,573 | 10,809 | |||||||

| Total | 63,954 | |||||||||||

| 18 | See Notes to Consolidated Financial Statements. |

Consolidated Schedule of Investments (continued)

December 31, 2023

| Investments | Interest Rate | Maturity Date | Principal Amount | Fair Value | ||||||||

| Telecommunications 1.67% | ||||||||||||

| Carriage Purchaser, Inc. 2021 Term Loan B(d) | 9.72% (1 mo. USD Term SOFR + 4.25% | ) | 10/2/2028 | $ | 68,476 | $ | 67,385 | |||||

| Northwest Fiber LLC 2021 Term Loan(d) | 9.275% (1 mo. USD Term SOFR + 3.75% | ) | 4/30/2027 | 124,658 | 124,798 | |||||||

| Total | 192,183 | |||||||||||

| Utilities 0.46% | ||||||||||||

| Talen Energy Supply LLC 2023 Term Loan B | 9.869% (3 mo. USD Term SOFR + 4.50% | ) | 5/17/2030 | 52,735 | 53,109 | |||||||

| Utility 0.55% | ||||||||||||

| Compass Power Generation LLC 2022 Term Loan B2(d) | 9.72% (1 mo. USD Term SOFR + 4.25% | ) | 4/14/2029 | 62,720 | 63,096 | |||||||

| Total Floating Rate Loans (cost $12,694,269) | 12,889,548 | |||||||||||

| Total Long-Term Investments (cost $14,159,076) | 14,365,094 | |||||||||||

| SHORT-TERM INVESTMENTS 7.10% | ||||||||||||

| GOVERNMENT SPONSORED ENTERPRISES SECURITIES 1.56% | ||||||||||||

| Federal Home Loan Bank Discount Notes (cost $179,974) | Zero Coupon | 1/2/2024 | 180,000 | 179,895 | ||||||||

| REPURCHASE AGREEMENTS 5.54% | ||||||||||||

| Repurchase Agreement dated 12/29/2023, 2.800% due 1/2/2024 with Fixed Income Clearing Corp. collateralized by $317,700 of U.S. Treasury Note at 4.625% due 3/15/2026; value: $324,855; proceeds: $318,567 (cost $318,468) | 318,468 | 318,468 | ||||||||||

| Repurchase Agreement dated 12/29/2023, 5.280% due 1/2/2024 with TD Securities USA LLC collateralized by $507,000 of U.S. Treasury Bond at 1.125% due 08/15/2040; value: $323,925; proceeds: $319,829 (cost $319,641) | 319,641 | 319,641 | ||||||||||

| Total Repurchase Agreements (cost $638,109) | 638,109 | |||||||||||

| Total Short-Term Investments (cost $818,083) | 818,004 | |||||||||||

| Total Investments in Securities 131.87% (cost $14,977,159) | 15,183,098 | |||||||||||

| Less Unfunded Loan Commitments (0.06%) (cost $6,766) | (6,512 | ) | ||||||||||

| Net Investments in Securities 131.82% (cost $14,970,393) | 15,176,586 | |||||||||||

| Borrowings (29.97%) | (3,450,000 | ) | ||||||||||

| Other Assets and Liabilities – Net(i) (1.85)% | (213,519 | ) | ||||||||||

| Net Assets 100.00% | $ | 11,513,067 | ||||||||||

| See Notes to Consolidated Financial Statements. | 19 |

Consolidated Schedule of Investments (continued)

December 31, 2023

| EUR | Euro. |

| ETF | Exchange Traded Fund. |

| EURIBOR | Euro Interbank Offered Rate. |

| LIBOR | London Interbank Offered Rate. |

| SOFR | Secured Overnight Financing Rate. |

| † | Security was purchased pursuant to Rule 144A under the Securities Act of 1933 and, unless registered under such Act or exempted from registration, may only be resold to qualified institutional buyers. At December 31, 2023, the total value of Rule 144A securities was $759,581, which represents 6.60% of net assets. |

| # | Variable rate security. The interest rate represents the rate in effect at December 31, 2023. |

| (a) | Foreign security traded in U.S. dollars. |

| (b) | Investment in non-U.S. dollar denominated securities. |

| (c) | Floating Rate Loans in which the Fund invests generally pay interest at rates which are periodically re-determined at a margin above the Secured Overnight Financing Rate (“SOFR”) or the prime rate offered by major U.S. banks. The rate(s) shown is the rate(s) in effect at December 31, 2023. |

| (d) | All or part of this investment held as collateral for the Fund’s credit facility. |

| (e) | Interest Rate to be determined. |

| (f) | Level 3 Investment as described in Note 2(o) in the Notes to Consolidated Financial Statements. Floating Rate Loans categorized as Level 3 are valued based on a single quotation obtained from a dealer. Accounting principles generally accepted in the United States of America do not require the Fund to create quantitative unobservable inputs that were not developed by the Fund. Therefore, the Fund does not have access to unobservable inputs and cannot disclose such inputs in the valuation. |

| (g) | Level 3 Investment as described in Note 2(o) in the Notes to Consolidated Financial Statements. Floating Rate Loan fair valued by the Pricing Committee. |

| (h) | Security partially/fully unfunded. See Note (2(l)). |

| (i) | Other Assets and Liabilities – Net include net unrealized appreciation/depreciation on forward foreign currency exchange contracts and swap contracts as follows: |

Centrally Cleared Interest Rate Swap Contracts at December 31, 2023:

| Central Clearingparty | Periodic Payments to be Made By The Fund (Quarterly) | Periodic Payments to be Received By The Fund (Quarterly) | Termination Date | Notional Amount | Value/Unrealized Depreciation | |||||||||

| Bank of America(1) | 5.306% | 12-Month USD SOFR | 9/15/2024 | $ | 133,000 | $ | (214 | ) | ||||||

| Bank of America(1) | 4.791% | 12-Month USD SOFR | 8/15/2025 | 69,000 | (508 | ) | ||||||||

| Bank of America(1) | 4.552% | 12-Month USD SOFR | 2/15/2026 | 68,000 | (730 | ) | ||||||||

| Bank of America(1) | 4.523% | 12-Month USD SOFR | 2/15/2026 | 5,000 | (51 | ) | ||||||||

| Bank of America(1) | 4.481% | 12-Month USD SOFR | 5/1/2026 | 69,000 | (812 | ) | ||||||||

| Bank of America(1) | 4.041% | 12-Month USD SOFR | 2/15/2028 | 30,000 | (506 | ) | ||||||||

| Bank of America(1) | 4.013% | 12-Month USD SOFR | 5/15/2028 | 70,000 | (1,217 | ) | ||||||||

| Bank of America(1) | 4.007% | 12-Month USD SOFR | 6/1/2028 | 60,000 | (1,047 | ) | ||||||||

| Unrealized Depreciation on Centrally Cleared Interest Rate Swap Contracts | $ | (5,085 | ) | |||||||||||

| (1) | Central clearinghouse: Chicago Mercantile Exchange (CME). |

Total Return Swap Contracts at December 31, 2023:

| Swap Counterparty | Referenced Index* | Referenced Spread | Units | Position | Termination Date | Notional Amount | Upfront Payment(1) | Unrealized Appreciation | Value | |||||||||||||||||

| Morgan Stanley | IBOXX | 12-Month USD SOFR | 710 | Long | 3/20/2024 | $ | 140,000 | $– | $ | 3,237 | $ | 3,237 | ||||||||||||||

| Morgan Stanley | IBOXX | 12-Month USD SOFR | 2,265 | Long | 3/20/2024 | 450,000 | 1 | 6,998 | 6,999 | |||||||||||||||||

| Total | $ | 590,000 | $1 | $ | 10,235 | $ | 10,236 | |||||||||||||||||||

| * | iBoxx Leveraged Loan Index. |

| SOFR | Secured Overnight Financing Rate. |

| (1) | Upfront payments paid (received) are presented net of amortization. |

| 20 | See Notes to Consolidated Financial Statements. |

Consolidated Schedule of Investments (concluded)

December 31, 2023

Forward Foreign Currency Exchange Contracts at December 31, 2023:

| Forward Foreign Currency Exchange Contracts | Transaction Type | Counterparty | Expiration Date | Foreign Currency | U.S. $ Cost on Origination Date | U.S. $ Current Value | Unrealized Depreciation | |||||||||||||||

| Euro | Sell | State Street Bank and Trust | 2/28/2024 | 399,000 | $432,184 | $ | 441,449 | $ | (9,265 | ) | ||||||||||||

| Euro | Sell | Morgan Stanley | 2/28/2024 | 7,000 | 7,700 | 7,745 | (45 | ) | ||||||||||||||

| Total Unrealized Depreciation on Forward Foreign Currency Exchange Contracts | $ | (9,310 | ) | |||||||||||||||||||

The following is a summary of the inputs used as of December 31, 2023 in valuing the Fund’s investments carried at fair value(1):

| Investment Type(2) | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Long-Term Investments | ||||||||||||||||

| Asset-Backed Securities | $ | – | $ | 99,593 | $ | – | $ | 99,593 | ||||||||

| Convertible Bonds | – | 50,024 | – | 50,024 | ||||||||||||

| Corporate Bonds | – | 951,064 | – | 951,064 | ||||||||||||

| Exchange-Traded Fund | 374,865 | – | – | 374,865 | ||||||||||||

| Floating Rate Loans | ||||||||||||||||

| Building Materials | – | 157,788 | 70,831 | 228,619 | ||||||||||||

| Health Care Services | – | 442,053 | 58,901 | 500,954 | ||||||||||||

| Leisure Time | – | 227,764 | 7,576 | 235,340 | ||||||||||||

| Metal Fabricate/Hardware | – | 88,534 | 9,817 | 98,351 | ||||||||||||

| Remaining Industries | – | 11,826,284 | – | 11,826,284 | ||||||||||||

| Less Unfunded Commitments | – | – | (6,512 | ) | (6,512 | ) | ||||||||||

| Short-Term Investments | ||||||||||||||||

| Government Sponsored Enterprises Securities | – | 179,895 | – | 179,895 | ||||||||||||

| Repurchase Agreements | – | 638,109 | – | 638,109 | ||||||||||||

| Total | $ | 374,865 | $ | 14,661,108 | $ | 140,613 | $ | 15,176,586 | ||||||||

| Other Financial Instruments | ||||||||||||||||

| Centrally Cleared Interest Rate Swap Contracts | ||||||||||||||||

| Assets | $ | – | $ | – | $ | – | $ | – | ||||||||

| Liabilities | – | (5,085 | ) | – | (5,085 | ) | ||||||||||

| Total Return Swap Contracts | ||||||||||||||||

| Assets | – | 10,236 | – | 10,236 | ||||||||||||

| Liabilities | – | – | – | – | ||||||||||||

| Forward Foreign Currency Exchange Contracts | ||||||||||||||||

| Assets | – | – | – | – | ||||||||||||

| Liabilities | – | (9,310 | ) | – | (9,310 | ) | ||||||||||

| Total | $ | – | $ | (4,159 | ) | $ | – | $ | (4,159 | ) | ||||||

| (1) | Refer to Note 2(o) for a description of fair value measurements and the three-tier hierarchy of inputs. |

| (2) | See Consolidated Schedule of Investments for fair values in each industry and identification of foreign issuers and/or geography. The table above is presented by Investment Type. Industries are presented within an Investment Type should such Investment Type include securities classified as two or more levels within the three-tier fair value hierarchy. When applicable, each Level 3 security is identified on the Consolidated Schedule of Investments along with the valuation technique utilized. |

A reconciliation of Level 3 investments is presented when the Fund has a material amount of Level 3 investments at the beginning or end of the period in relation to the Fund’s net assets. Management has determined not to provide a reconciliation as the balance of Level 3 investments was not considered to be material to the Fund’s net assets at the beginning or end of the period.

| See Notes to Consolidated Financial Statements. | 21 |

Consolidated Statement of Assets and Liabilities

December 31, 2023

| ASSETS: | ||||

| Investments in securities, at fair value (cost $14,970,393) | $ | 15,176,586 | ||

| Cash | 290,223 | |||

| Deposits with brokers for forwards and swap contracts collateral | 11,533 | |||

| Foreign cash, at value (cost $2,098) | 2,103 | |||

| Receivables: | ||||

| Investment securities sold | 503,217 | |||

| Interest and dividends | 142,415 | |||

| Capital shares sold | 50,899 | |||

| From advisor (See Note 3) | 44,880 | |||

| Deferred financing costs | 8,381 | |||

| Variation margin for centrally cleared swap contracts agreements | 339 | |||

| Total return swap contracts, at fair value (including upfront payment of $1) | 10,236 | |||

| Prepaid expenses | 32,879 | |||

| Total assets | 16,273,691 | |||

| LIABILITIES: | ||||

| Payables: | ||||

| Credit Facility | 3,450,000 | |||

| Investment securities purchased | 1,059,414 | |||

| Interest payable | 20,275 | |||

| Distribution and Servicing Plan | 2,162 | |||

| Fund administration | 387 | |||

| Trustees’ fees | 282 | |||

| Unrealized depreciation on forward foreign currency exchange contracts | 9,310 | |||

| Unrealized depreciation on unfunded commitments | 254 | |||

| Distributions payable | 90,783 | |||

| Accrued expenses and other liabilities | 127,757 | |||

| Total liabilities | 4,760,624 | |||

| NET ASSETS | $ | 11,513,067 | ||

| COMPOSITION OF NET ASSETS: | ||||

| Paid-in capital | $ | 11,274,973 | ||

| Total distributable earnings (loss) | 238,094 | |||

| Net Assets | $ | 11,513,067 | ||

| Net assets by class: | ||||

| Class I Shares | $ | 6,406,229 | ||

| Class A Shares | $ | 5,106,838 | ||

| Outstanding shares by class: (unlimited number of authorized shares of beneficial interest): | ||||

| Class I Shares | 627,211 | |||

| Class A Shares | 500,000 | |||

| Net asset value, offering and redemption price per share (Net assets divided by outstanding shares): | ||||

| Class I Shares-Net asset value | $10.21 | |||

| Class A Shares-Net asset value | $10.21 | |||

| Class A Shares-Maximum offering price (Net asset value plus sales charge of 2.50%) | $10.47 |

| 22 | See Notes to Consolidated Financial Statements. |

Consolidated Statement of Operations

For the Period Ended December 31, 2023*

| Investment income: | ||||

| Dividends | $ | 5,393 | ||

| Interest and other | 1,256,561 | |||

| Total investment income | 1,261,954 | |||

| Expenses: | ||||

| Management fee | 100,691 | |||

| Distribution and Servicing plan–Class A | 24,909 | |||

| Interest expense and fees (See Note 10) | 198,556 | |||

| Professional | 92,241 | |||

| Reports to shareholders | 59,653 | |||

| Shareholder servicing | 29,917 | |||

| Registration | 9,846 | |||

| Custody | 7,502 | |||

| Fund administration | 4,199 | |||

| Trustees’ fees | 494 | |||

| Other | 42,451 | |||

| Gross expenses | 570,459 | |||

| Fees waived and expenses reimbursed (See Note 3) | (324,866 | ) | ||

| Net expenses | 245,593 | |||

| Net investment income | 1,016,361 | |||

| Net realized and unrealized gain (loss): | ||||

| Net realized gain (loss) on investments | 76,485 | |||

| Net realized gain (loss) on forward foreign currency exchange contracts | 7,793 | |||

| Net realized gain (loss) on swap contracts | (45,676 | ) | ||

| Net realized gain (loss) on foreign currency related transactions | (1,110 | ) | ||

| Net change in unrealized appreciation/depreciation on investments | 206,193 | |||

| Net change in unrealized appreciation/depreciation on forward foreign currency exchange contracts | (9,310 | ) | ||

| Net change in unrealized appreciation/depreciation on swap contracts | 5,150 | |||

| Net change in unrealized appreciation/depreciation on translation of assets and liabilities denominated in foreign currencies | (4,112 | ) | ||

| Net change in unrealized appreciation/depreciation on unfunded commitments | (254 | ) | ||

| Net realized and unrealized gain (loss) | 235,159 | |||

| Net Increase in Net Assets Resulting From Operations | $ | 1,251,520 | ||

| * | For the period January 4, 2023, commencement of operations, to December 31, 2023. |

| See Notes to Consolidated Financial Statements. | 23 |

Consolidated Statement of Changes in Net Assets

| INCREASE IN NET ASSETS | For the Period Ended December 31, 2023* | |||

| Operations: | ||||

| Net investment income | $ | 1,016,361 | ||

| Net realized gain (loss) on investments, forward foreign currency exchange contracts, swap contracts and foreign currency related transactions | 37,492 | |||

| Net change in unrealized appreciation/depreciation on investments, forward foreign currency exchange contracts, swap contracts, unfunded commitments and translation of assets and liabilities denominated in foreign currencies | 197,667 | |||

| Net increase in net assets resulting from operations | 1,251,520 | |||

| Distributions to shareholders: | ||||

| Class I | (552,175 | ) | ||

| Class A | (467,444 | ) | ||

| Total distributions to shareholders | (1,019,619 | ) | ||

| Capital share transactions (See Note 16): | ||||

| Net proceeds from sales of shares | 10,735,000 | |||

| Reinvestment of distributions | 546,166 | |||

| Net increase in net assets resulting from capital share transactions | 11,281,166 | |||

| Net increase in net assets | 11,513,067 | |||

| NET ASSETS: | ||||

| Beginning of period | $ | – | ||

| End of period | $ | 11,513,067 | ||

| * | For the period January 4, 2023, commencement of operations, to December 31, 2023. |

| 24 | See Notes to Consolidated Financial Statements. |

Consolidated Statement of Cash Flows

For the Period Ended December 31, 2023*

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||

| Net increase in net assets resulting from operations | $ | 1,251,520 | ||

| Adjustments to reconcile net increase in net assets resulting from operations to net cash used in operating activities: | ||||

| Investments Purchased | (59,927,552 | ) | ||

| Investments sold and principal repayments | 46,518,937 | |||

| Net increase in short-term investments | (818,004 | ) | ||

| Net amortization/(accretion) of premium (discount) | (104,165 | ) | ||

| Increase in receivable from advisor | (44,880 | ) | ||

| Increase in cash collateral held at broker | (11,533 | ) | ||

| Amortization of deferred financing costs | 4,119 | |||

| Increase in interest and dividends receivable | (142,402 | ) | ||

| Increase in prepaid expenses | (32,879 | ) | ||

| Increase in variation margin receivable for centrally cleared swap contracts agreements | (339 | ) | ||

| Increase in total return swap contracts, at fair value | (10,236 | ) | ||

| Increase in interest payable | 20,275 | |||

| Increase in distribution and servicing payable | 2,162 | |||

| Increase in fund administration payable | 387 | |||

| Increase in trustees’ fees payable | 282 | |||

| Increase in accrued expenses and other liabilities | 127,757 | |||

| Net realized (gain)/loss on: | ||||

| Net realized (gain)/loss on investments | (76,485 | ) | ||

| Net change in unrealized (appreciation)/depreciation on: | ||||

| Net change unrealized (appreciation)/depreciation on investments | (206,193 | ) | ||

| Net change in unrealized (appreciation)/depreciation on forward foreign currency exchange contracts | 9,310 | |||

| Net change in unrealized (appreciation)/depreciation on unfunded loan commitments | 254 | |||

| Net change in unrealized (appreciation)/depreciation on foreign currency translations | 4,112 | |||

| Net Cash Used in Operating Activities | (13,435,553 | ) | ||

| See Notes to Consolidated Financial Statements. | 25 |

Consolidated Statement of Cash Flows (concluded)

For the Period Ended December 31, 2023*

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||

| Cash provided by credit facility | $ | 3,450,000 | ||

| Repayments under credit facility | – | |||

| Deferred financing costs | (12,500 | ) | ||

| Distributions to shareholders | (382,670 | ) | ||

| Net proceeds from sales of shares | 10,684,101 | |||

| Net Cash Provided by Financing Activities | 13,738,931 | |||

| Effect of exchange rate changes on cash | 481 | |||

| Net change in cash | 303,859 | |||

| Cash at beginning period | $ | – | ||

| Cash at end of period | $ | 303,859 | ||

| Supplemental disclosure of cash flow information: | ||||

| Cash paid for interest expense and fees on credit facility | $ | 178,281 | ||

| Reinvestment of distributions | 546,166 | |||

| Reconciliation of restricted and unrestricted cash to the Consolidated Statement of Assets and Liabilities, ending balance: | ||||

| Cash | 290,223 | |||

| Foreign cash, at value | 2,103 | |||

| Deposits with brokers for forwards and swap contracts collateral | 11,533 | |||

| Total Reconciliation of restricted and unrestricted cash to the Consolidated Statement of Assets and Liabilities, ending balance | $ | 303,859 | ||

| * | For the period January 4, 2023, commencement of operations, to December 31, 2023. |

| 26 | See Notes to Consolidated Financial Statements. |

This page is intentionally left blank.

27

Consolidated Financial Highlights

| Per Share Operating Performance: | ||||||||||||||||||||||||

| Investment operations: | Distributions to shareholders from: | |||||||||||||||||||||||

| Net asset value, beginning of period | Net investment income (loss)(a) | Net realized and unrealized gain | Total from investment operations | Net investment income | Net asset value, end of period | |||||||||||||||||||

| Class I | ||||||||||||||||||||||||

| 1/4/2023 to 12/31/2023(e) | $10.00 | $0.99 | $0.16 | $1.15 | $(0.94 | ) | $10.21 | |||||||||||||||||

| Class A | ||||||||||||||||||||||||

| 1/4/2023 to 12/31/2023(e) | 10.00 | 0.93 | 0.17 | 1.10 | (0.89 | ) | 10.21 | |||||||||||||||||

| (a) | Calculated based on average shares outstanding during the period. |

| (b) | Total return for Class A does not consider the effects of sales loads and assumes the reinvestment of all distributions. |

| (c) | Not annualized. |

| (d) | Annualized. |

| (e) | Commenced on January 4, 2023. |

| 28 | See Notes to Consolidated Financial Statements. |

| Ratios to Average Net Assets: | Supplemental Data: | |||||||||||||||||||||||||

| Total return (%)(b)(c) | Total expenses after waivers and/or reim- bursements (includes interest expense) (%)(d) | Total expenses after waivers and/or reim- bursements (excludes interest expense) (%)(d) | Total expenses (%)(d) | Net investment income (loss) (%)(d) | Net assets, end of period (000) | Portfolio turnover rate (%)(c) | ||||||||||||||||||||

| 12.53 | 2.12 | 0.25 | 5.26 | 10.03 | $6,406 | 96 | % | |||||||||||||||||||

| 11.98 | 2.62 | 0.75 | 5.72 | 9.45 | 5,107 | 96 | % | |||||||||||||||||||

| See Notes to Consolidated Financial Statements. | 29 |

Notes to Consolidated Financial Statements

| 1. | ORGANIZATION |

Lord Abbett Floating Rate High Income Fund (the “Fund”) is registered under the Investment Company Act of 1940, as amended (the “Act”), as a non-diversified, closed-end management investment company that continuously offers its common shares (the “Shares”) and is operated as an interval fund. The Fund was organized as a Delaware statutory trust on January 30, 2020. The Fund had a sale to Lord, Abbett & Co. LLC (“Lord Abbett”) of 10,000 shares of common stock for $100,000 ($10.00 per share). The Fund commenced operations on January 4, 2023.

The Fund’s investment objective is to seek a high level of current income. The Fund currently offers three classes of Shares: Class A, Class I, and Class U. A front-end sales charge is normally added to the net asset value (“NAV”) for Class A shares. There is no front-end sales charge in the case of Class I and Class U shares. Class U shares has not commenced operations.

The Fund will not list its Shares for trading on any securities exchange. There is currently no secondary market for its Shares and the Fund does not expect any secondary market to develop for its Shares. Shareholders of the Fund are not able to have their Shares redeemed or otherwise sell their Shares on a daily basis because the Fund is an unlisted closed-end fund. In order to provide liquidity to shareholders, the Fund is structured as an interval fund and conducts quarterly repurchase offers for a portion of its outstanding Shares.

The preparation of the consolidated financial statements in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”) requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. The Fund is considered an investment company under U.S. GAAP and follows the accounting and reporting guidance applicable to investment companies.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

| (a) | Basis of Consolidation—The Fund’s consolidated financial statements and accompanying notes include balances of both the Fund and Lord Abbett FRHI Funding, LLC., a Delaware Limited Liability Company and wholly owned subsidiary of the Fund. All interfund transactions have been eliminated upon consolidation. |

| (b) | Investment Valuation—Under procedures approved by the Fund’s Board of Trustees (the “Board”), the Board has designated the determination of fair value of the Fund’s portfolio investments to Lord Abbett as its valuation designee. Accordingly, Lord Abbett is responsible for, among other things, assessing and managing valuation risks, establishing, applying and testing fair value methodologies, and evaluating pricing services. Lord Abbett has formed a Pricing Committee that performs these responsibilities on behalf of Lord Abbett, administers the pricing and valuation of portfolio investments and ensures that prices utilized reasonably reflect fair value. Among other things, these procedures allow Lord Abbett, subject to Board oversight, to utilize independent pricing services, quotations from securities, and financial instrument dealers and other market sources to determine fair value. |

| Securities actively traded on any recognized U.S. or non-U.S. exchange or on The NASDAQ Stock Market LLC are valued at the last sale price or official closing price on the exchange or system on which they are principally traded. Events occurring after the close of trading on non-U.S. |

30

Notes to Consolidated Financial Statements (continued)

| exchanges may result in adjustments to the valuation of foreign securities to reflect their fair value as of the close of regular trading on the New York Stock Exchange. When valuing foreign equity securities that meet certain criteria, the Pricing Committee uses a third-party fair valuation service that values such securities to reflect market trading that occurs after the close of the applicable foreign markets of comparable securities or other instruments that correlate to the fair-valued securities. Unlisted equity securities are valued at the last quoted sale price or, if no sale price is available, at the mean between the most recently quoted bid and ask prices. Fixed income securities are valued based on evaluated prices supplied by independent pricing services, which reflect broker/dealer supplied valuations and the independent pricing services’ own electronic data processing techniques. Forward foreign currency exchange contracts are valued using daily forward exchange rates. Swap contracts are valued daily using independent pricing services or quotations from broker/dealers to the extent available. | |

| Securities for which prices are not readily available are valued at fair value as determined by the Pricing Committee. The Pricing Committee considers a number of factors, including observable and unobservable inputs, when arriving at fair value. The Pricing Committee may use observable inputs such as yield curves, broker quotes, observable trading activity, option adjusted spread models and other relevant information to determine the fair value of portfolio investments. The Board or a designated committee thereof periodically reviews reports that may include fair value determinations made by the Pricing Committee, related market activity, inputs and assumptions, and retrospective comparison of prices of subsequent purchases and sales transactions to fair value determinations made by the Pricing Committee. | |

| Short-term securities with 60 days or less remaining to maturity are valued using the amortized cost method, which approximates fair value. | |

| (c) | Security Transactions—Security transactions are recorded as of the date that the securities are purchased or sold (trade date). Realized gains and losses on sales of portfolio securities are calculated using the identified-cost method. Realized and unrealized gains (losses) are allocated to each class of shares based upon the relative proportion of net assets at the beginning of the day. |

| (d) | Investment Income—Dividend income is recorded on the ex-dividend date. Interest income is recorded on the accrual basis as earned. Discounts are accreted and premiums are amortized using the effective interest method and are included in Interest and other, if applicable, in the Consolidated Statement of Operations. Investment income is allocated to each class of shares based upon the relative proportion of net assets at the beginning of the day. |

| (e) | Income Taxes—It is the policy of the Fund to meet the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies and to distribute substantially all taxable income and capital gains to its shareholders. Therefore, no income tax provision is required. |

| The Fund files U.S. federal and various state and local tax returns. No income tax returns are currently under examination. | |

| (f) | Expenses—Expenses, excluding class-specific expenses, are allocated to each class of shares based upon the relative proportion of net assets at the beginning of the day. Class A, Class I and Class U Shares bear their class-specific share of all expenses and fees relating to the Fund’s Distribution and Servicing Plan. |

31

Notes to Consolidated Financial Statements (continued)

| (g) | Foreign Transactions—The books and records of the Fund are maintained in U.S. dollars and transactions denominated in foreign currencies are recorded in the Fund’s records at the rate prevailing when earned or recorded. Asset and liability accounts that are denominated in foreign currencies are adjusted daily to reflect current exchange rates and any unrealized gain (loss), if applicable, is included in Net change in unrealized appreciation/depreciation on translation of assets and liabilities denominated in foreign currencies in the Fund’s Consolidated Statement of Operations. The resultant exchange gains and losses upon settlement of such transactions, if applicable, are included in Net realized gain (loss) on foreign currency related transactions in the Fund’s Consolidated Statement of Operations. The Fund does not isolate that portion of the results of operations arising as a result of changes in the foreign exchange rates from the changes in market prices of the securities. |

| The Fund uses foreign currency exchange contracts to facilitate transactions in foreign-denominated securities. Losses from these transactions may arise from changes in the value of the foreign currency or if the counterparties do not perform under the contracts’ terms. | |

| (h) | Forward Foreign Currency Exchange Contracts—The Fund may enter into forward foreign currency exchange contracts in order to reduce exposure to changes in foreign currency exchange rates on foreign portfolio holdings, or gain or reduce exposure to foreign currency solely for investment purposes. A forward foreign currency exchange contract is a commitment to purchase or sell a foreign currency at a future date at a negotiated rate. The contracts are valued daily at forward exchange rates and any unrealized gain (loss), if applicable, is included in Net change in unrealized appreciation/depreciation on forward foreign currency exchange contracts in the Fund’s Consolidated Statement of Operations. The gain (loss) arising from the difference between the U.S. dollar cost of the original contract and the value of the forward foreign currency in U.S. dollars upon closing of such contracts is included, if applicable, in Net realized gain (loss) on forward foreign currency exchange contracts in the Fund’s Consolidated Statement of Operations. |

| (i) | Futures Contracts—The Fund may purchase and sell futures contracts to enhance returns, to attempt to economically hedge some of its investment risk, or as a substitute position in lieu of holding the underlying asset on which the instrument is based. At the time of entering into a futures transaction, an investor is required to deposit and maintain a specified amount of cash or eligible securities called “initial margin.” Subsequent payments made or received by the Fund called “variation margin” are made on a daily basis as the market price of the futures contract fluctuates. The Fund will record an unrealized gain (loss) based on the amount of variation margin. When a contract is closed, a realized gain (loss) is recorded equal to the difference between the opening and closing value of the contract. |

| (j) | Credit Default Swap Contracts—The Fund may enter into credit default swap contracts in order to hedge credit risk or for speculation purposes. As a seller of a credit default swap contract (“seller of protection”), the Fund is required to pay the notional amount or other agreed-upon value of a referenced debt obligation to the counterparty in the event of a default by or other credit event involving the referenced issuer, obligation or index. In return, the Fund receives from the counterparty a periodic stream of payments over the term of the contract. |

| As a purchaser of a credit default swap contract (“buyer of protection”), the Fund would receive the notional amount or other agreed upon value of a referenced debt obligation from the counterparty in the event of default by or other credit event involving the referenced issuer, obligation or index. In return, the Fund makes periodic payments to the counterparty over the term of the contracts, provided no event of default has occurred. |

32

Notes to Consolidated Financial Statements (continued)