| Q2 2024 Financial Results August 6, 2024 Tara Living with narcolepsy Taking WAKIX since 2020 Exhibit 99.2 |

| 2 Forward-Looking Statements This presentation includes forward‐looking statements within the meaning of the Private Securities Reform Act of 1995. All statements other than statements of historical facts contained in these materials or elsewhere, including statements regarding Harmony Biosciences Holdings, Inc.’s (the “Company”) future financial position, business strategy and plans and objectives of management for future operations, should be considered forward-looking statements. Forward-looking statements use words like “believes,” “plans,” “expects,” “intends,” “will,” “would,” “anticipates,” “estimates,” and similar words or expressions in discussions of the Company’s future operations, financial performance or the Company’s strategies. These statements are based on current expectations or objectives that are inherently uncertain, especially in light of the Company’s limited operating history. These and other important factors discussed under the caption “Risk Factors” in the Company’s Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission (the “SEC”) on February 22, 2024 and its other filings with the SEC could cause actual results to differ materially and adversely from those indicated by the forward-looking statements made in this presentation. While the Company may elect to update such forward-looking statements at some point in the future, it disclaims any obligation to do so, even if subsequent events cause its views to change. This presentation includes information related to market opportunity as well as cost and other estimates obtained from internal analyses and external sources. The internal analyses are based upon management’s understanding of market and industry conditions and have not been verified by independent sources. Similarly, the externally sourced information has been obtained from sources the Company believes to be reliable, but the accuracy and completeness of such information cannot be assured. Neither the Company, nor any of its respective officers, directors, managers, employees, agents, or representatives, (i) make any representations or warranties, express or implied, with respect to any of the information contained herein, including the accuracy or completeness of this presentation or any other written or oral information made available to any interested party or its advisor (and any liability therefore is expressly disclaimed), (ii) have any liability from the use of the information, including with respect to any forward-looking statements, or (iii) undertake to update any of the information contained herein or provide additional information as a result of new information or future events or developments. |

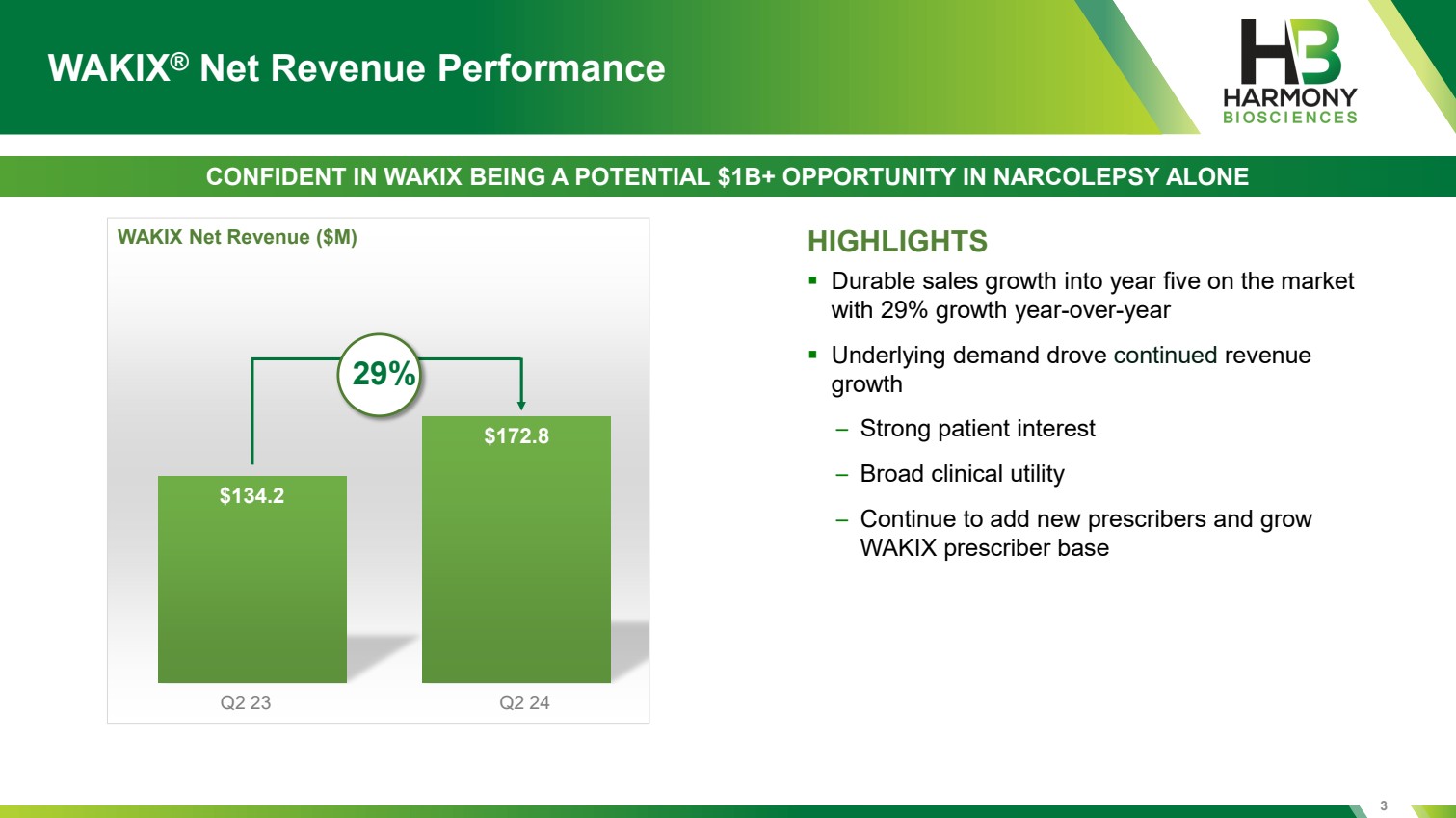

| $134.2 $172.8 HIGHLIGHTS ▪ Durable sales growth into year five on the market with 29% growth year-over-year ▪ Underlying demand drove continued revenue growth – Strong patient interest – Broad clinical utility – Continue to add new prescribers and grow WAKIX prescriber base Q2 23 Q2 24 WAKIX Net Revenue ($M) WAKIX® Net Revenue Performance CONFIDENT IN WAKIX BEING A POTENTIAL $1B+ OPPORTUNITY IN NARCOLEPSY ALONE 29% 3 |

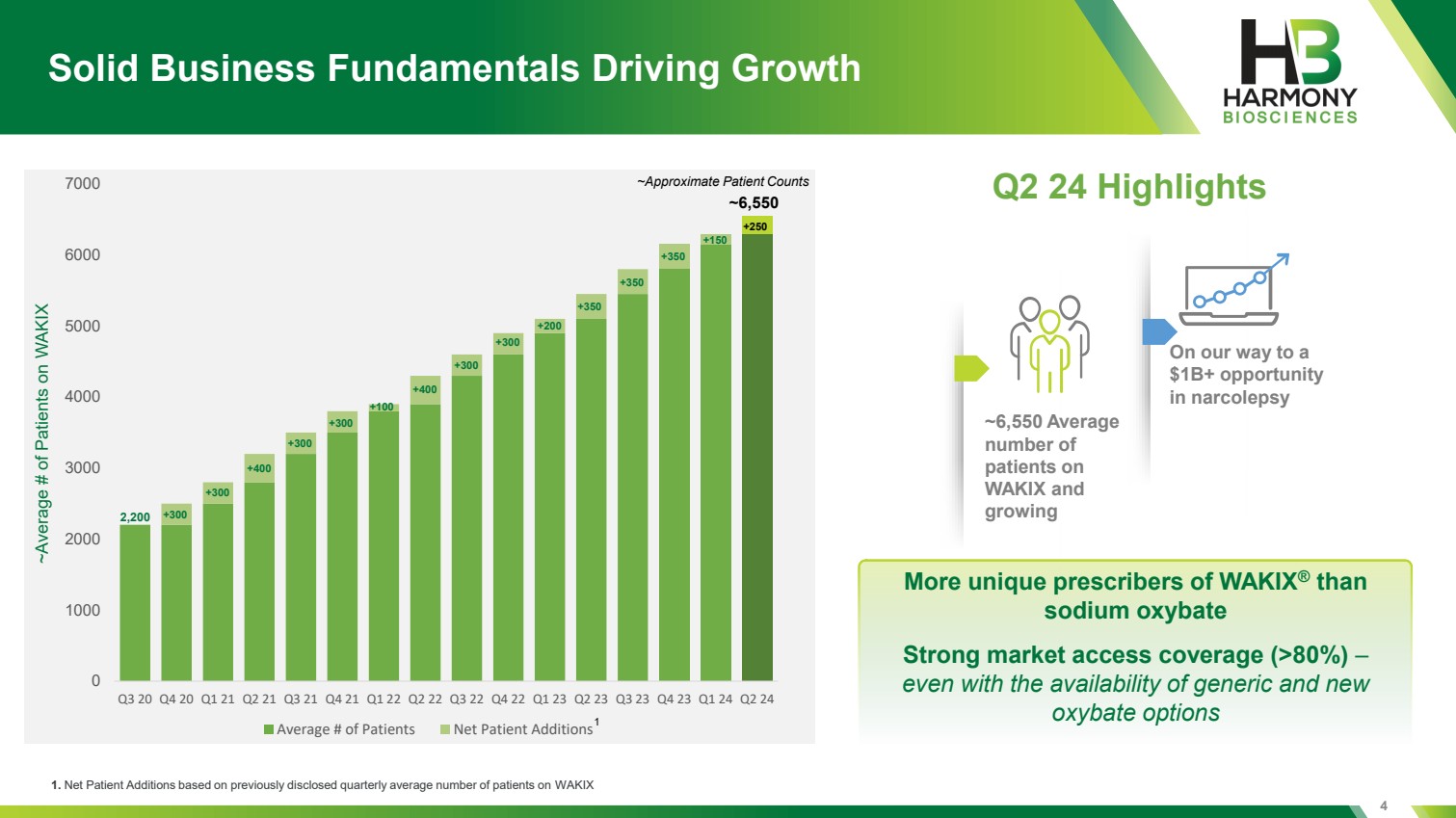

| 0 1000 2000 3000 4000 5000 6000 7000 Q3 20 Q4 20 Q1 21 Q2 21 Q3 21 Q4 21 Q1 22 Q2 22 Q3 22 Q4 22 Q1 23 Q2 23 Q3 23 Q4 23 Q1 24 Q2 24 Average # of Patients Net Patient Additions 4 Solid Business Fundamentals Driving Growth Q2 24 Highlights More unique prescribers of WAKIX® than sodium oxybate Strong market access coverage (>80%) – even with the availability of generic and new 1 oxybate options ~Average # of Patients on WAKIX ~Approximate Patient Counts 2,200 +300 +300 +400 +400 +300 +300 +300 +300 +350 +350 +350 +200 +100 ~6,550 1. Net Patient Additions based on previously disclosed quarterly average number of patients on WAKIX ~6,550 Average number of patients on WAKIX and growing On our way to a $1B+ opportunity in narcolepsy +250 +150 |

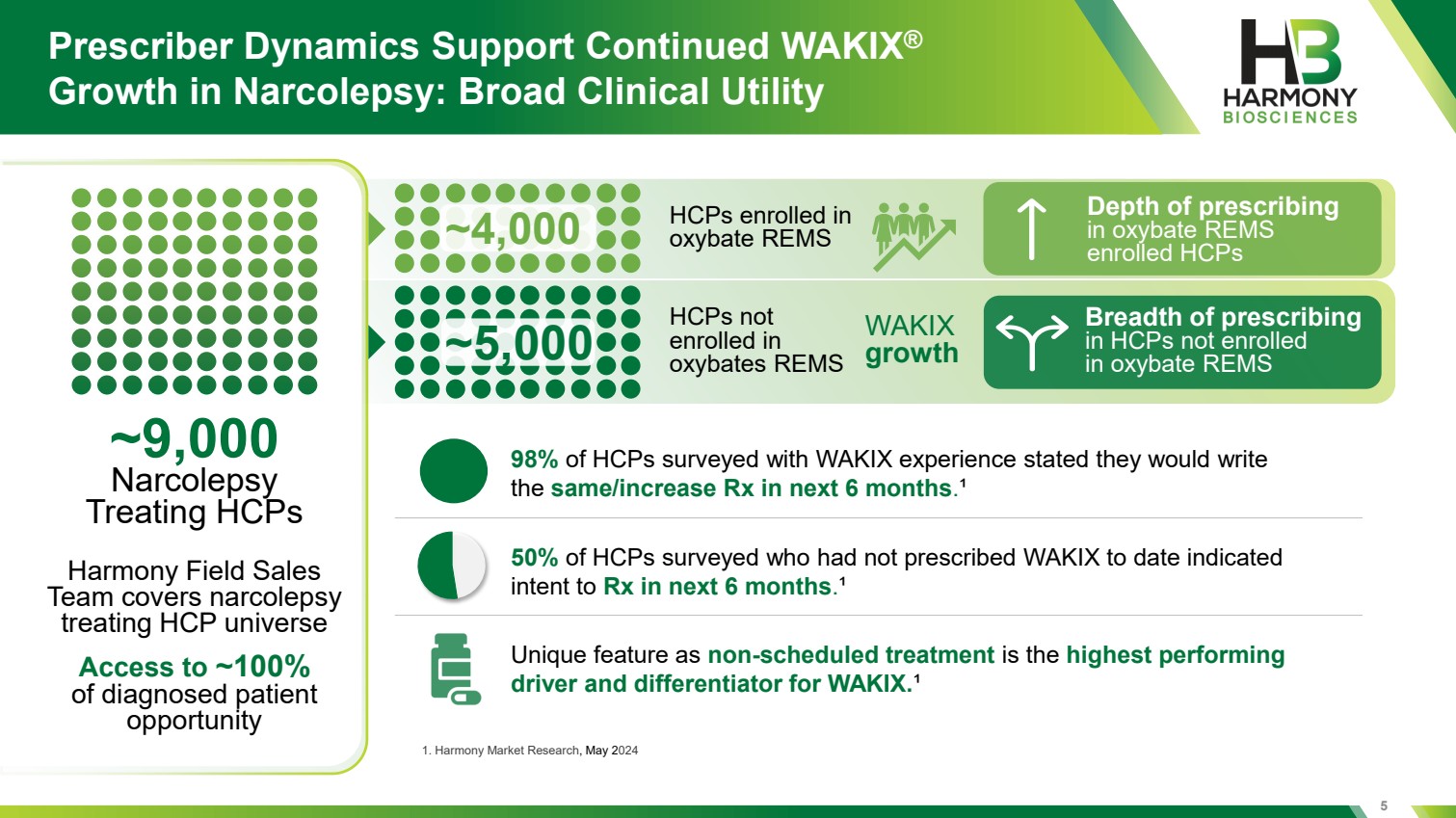

| 5 Prescriber Dynamics Support Continued WAKIX® Growth in Narcolepsy: Broad Clinical Utility ~9,000 Narcolepsy Treating HCPs HCPs enrolled in oxybate REMS HCPs not enrolled in oxybates REMS WAKIX growth Breadth of prescribing in HCPs not enrolled in oxybate REMS Harmony Field Sales Team covers narcolepsy treating HCP universe Access to ~100% of diagnosed patient opportunity 1. Harmony Market Research, May 2024 98% of HCPs surveyed with WAKIX experience stated they would write the same/increase Rx in next 6 months.¹ 50% of HCPs surveyed who had not prescribed WAKIX to date indicated intent to Rx in next 6 months.¹ Unique feature as non-scheduled treatment is the highest performing driver and differentiator for WAKIX.¹ Depth of prescribing in oxybate REMS enrolled HCPs ~5,000 ~4,000 |

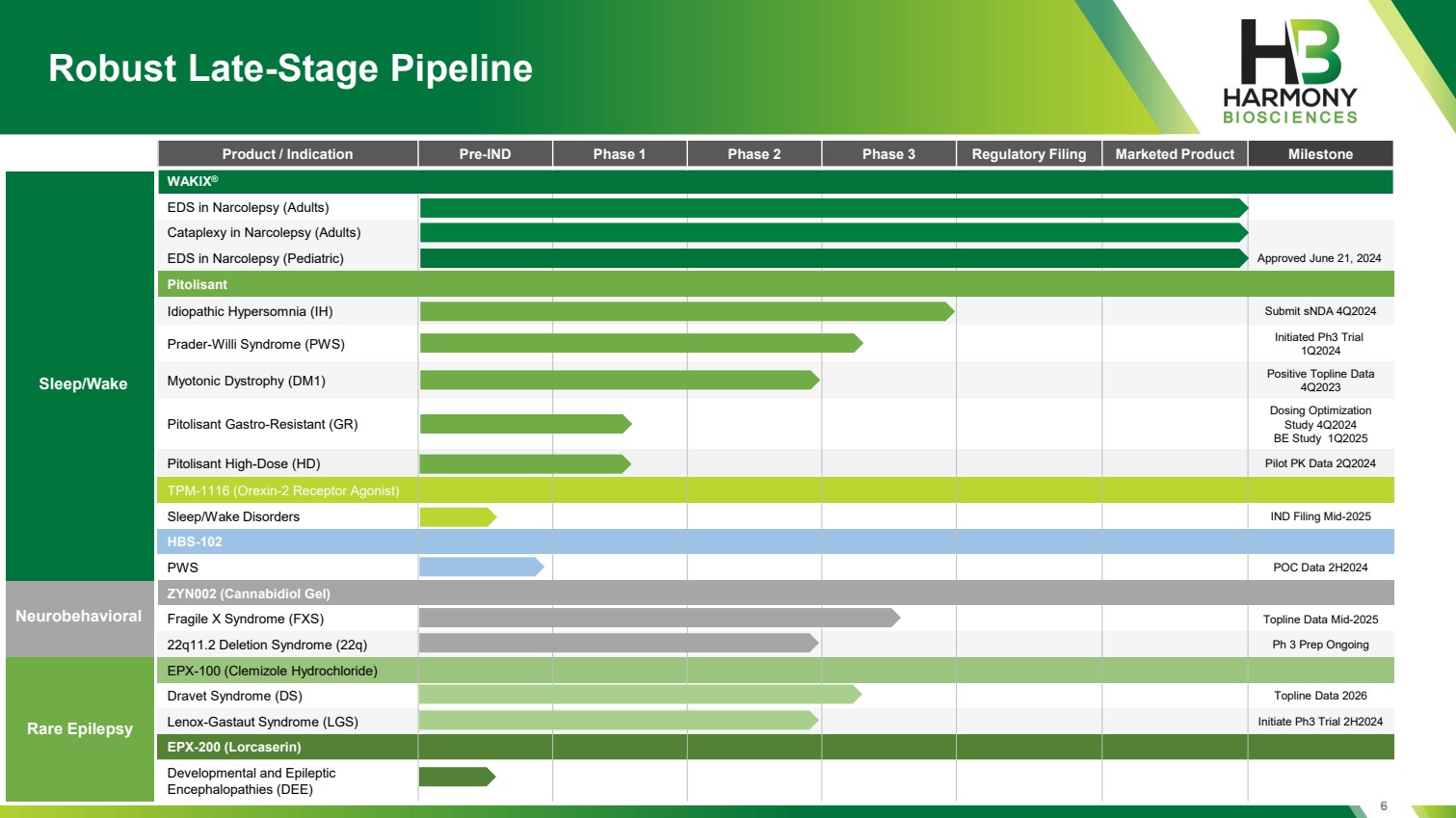

| 6 Robust Late-Stage Pipeline Product / Indication Pre-IND Phase 1 Phase 2 Phase 3 Regulatory Filing Marketed Product Milestone WAKIX® EDS in Narcolepsy (Adults) Cataplexy in Narcolepsy (Adults) EDS in Narcolepsy (Pediatric) Approved June 21, 2024 Pitolisant Idiopathic Hypersomnia (IH) Submit sNDA 4Q2024 Prader-Willi Syndrome (PWS) Initiated Ph3 Trial 1Q2024 Myotonic Dystrophy (DM1) Positive Topline Data 4Q2023 Pitolisant Gastro-Resistant (GR) Dosing Optimization Study 4Q2024 BE Study 1Q2025 Pitolisant High-Dose (HD) Pilot PK Data 2Q2024 TPM-1116 (Orexin-2 Receptor Agonist) Sleep/Wake Disorders IND Filing Mid-2025 HBS-102 PWS POC Data 2H2024 ZYN002 (Cannabidiol Gel) Fragile X Syndrome (FXS) Topline Data Mid-2025 22q11.2 Deletion Syndrome (22q) Ph 3 Prep Ongoing EPX-100 (Clemizole Hydrochloride) Dravet Syndrome (DS) Topline Data 2026 Lenox-Gastaut Syndrome (LGS) Initiate Ph3 Trial 2H2024 EPX-200 (Lorcaserin) Developmental and Epileptic Encephalopathies (DEE) Sleep/Wake Neurobehavioral Rare Epilepsy |

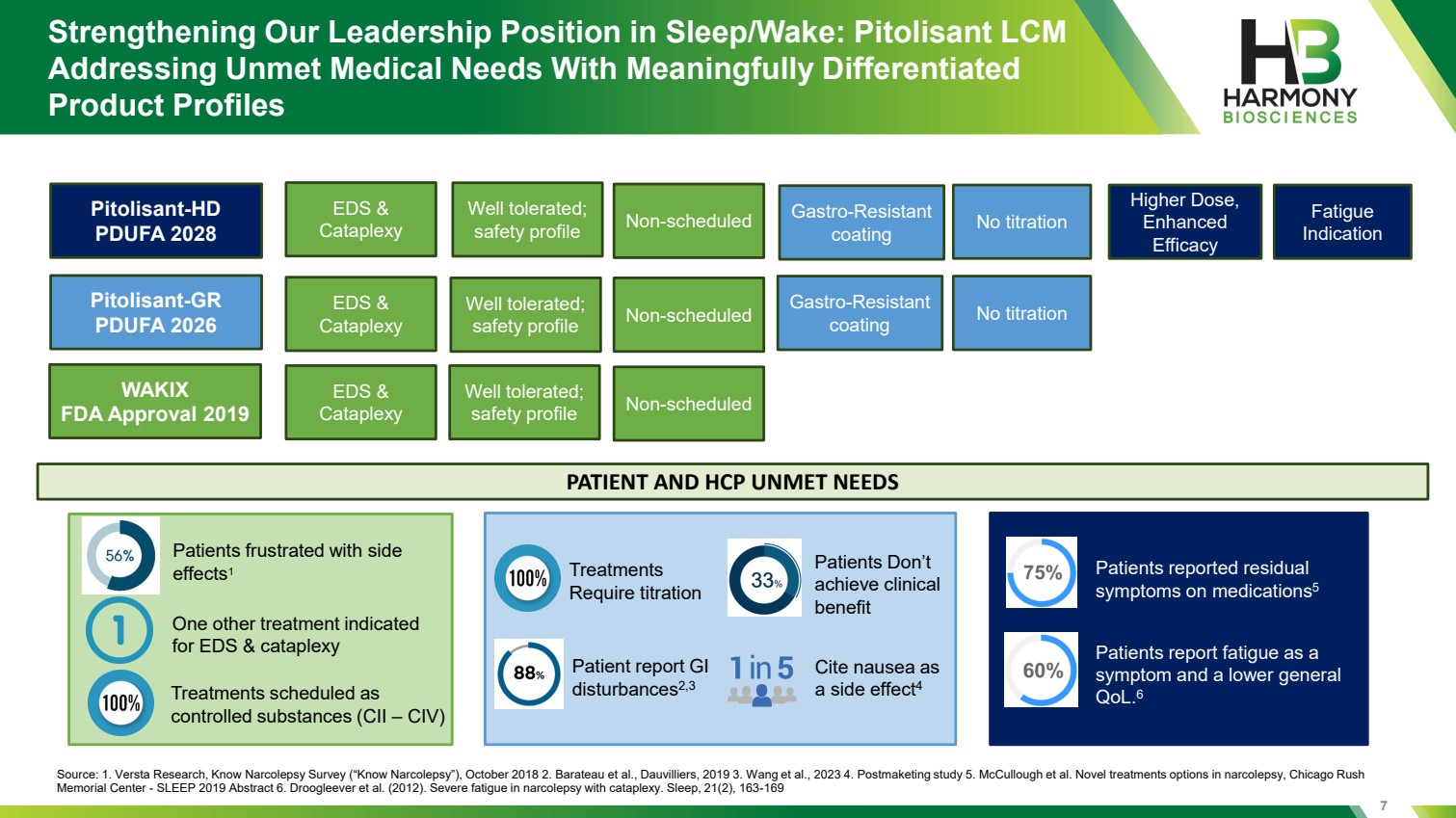

| 7 Strengthening Our Leadership Position in Sleep/Wake: Pitolisant LCM Addressing Unmet Medical Needs With Meaningfully Differentiated Product Profiles WAKIX FDA Approval 2019 Pitolisant-GR PDUFA 2026 Pitolisant-HD PDUFA 2028 Non-scheduled EDS & Cataplexy Well tolerated; safety profile Non-scheduled EDS & Cataplexy Well tolerated; safety profile Non-scheduled EDS & Cataplexy Well tolerated; safety profile Gastro-Resistant coating No titration Gastro-Resistant coating No titration Fatigue Indication Higher Dose, Enhanced Efficacy PATIENT AND HCP UNMET NEEDS Source: 1. Versta Research, Know Narcolepsy Survey (“Know Narcolepsy”), October 2018 2. Barateau et al., Dauvilliers, 2019 3. Wang et al., 2023 4. Postmaketing study 5. McCullough et al. Novel treatments options in narcolepsy, Chicago Rush Memorial Center - SLEEP 2019 Abstract 6. Droogleever et al. (2012). Severe fatigue in narcolepsy with cataplexy. Sleep, 21(2), 163-169 Treatments scheduled as controlled substances (CII – CIV) One other treatment indicated for EDS & cataplexy Patients frustrated with side effects1 Treatments Require titration Patient report GI disturbances2,3 Cite nausea as a side effect4 Patients Don’t achieve clinical benefit Patients report fatigue as a symptom and a lower general QoL.6 Patients reported residual symptoms on medications5 |

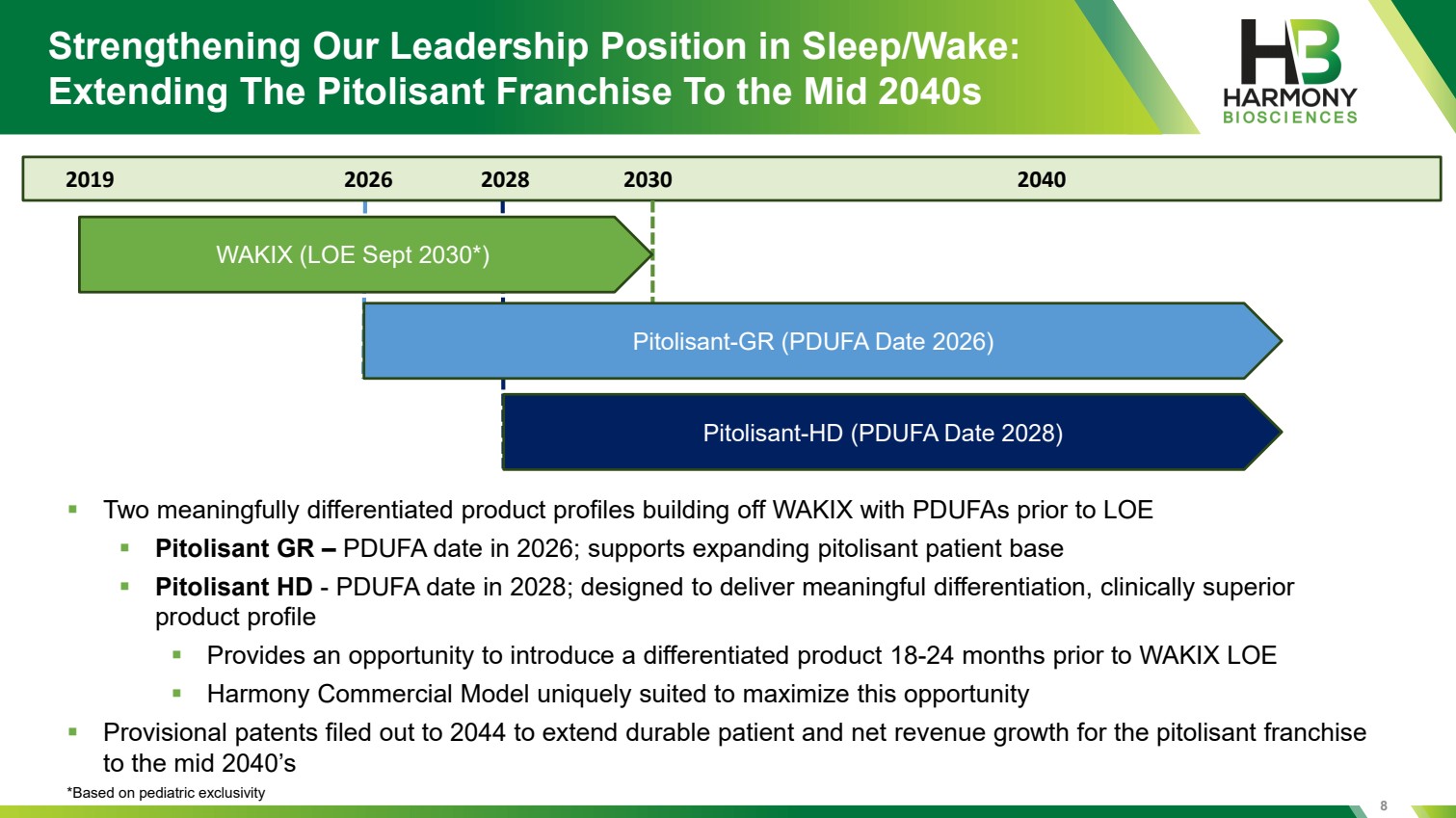

| 8 Strengthening Our Leadership Position in Sleep/Wake: Extending The Pitolisant Franchise To the Mid 2040s 2019 2026 2028 2030 2040 WAKIX (LOE Sept 2030*) Pitolisant-GR (PDUFA Date 2026) Pitolisant-HD (PDUFA Date 2028) ▪ Two meaningfully differentiated product profiles building off WAKIX with PDUFAs prior to LOE ▪ Pitolisant GR – PDUFA date in 2026; supports expanding pitolisant patient base ▪ Pitolisant HD - PDUFA date in 2028; designed to deliver meaningful differentiation, clinically superior product profile ▪ Provides an opportunity to introduce a differentiated product 18-24 months prior to WAKIX LOE ▪ Harmony Commercial Model uniquely suited to maximize this opportunity ▪ Provisional patents filed out to 2044 to extend durable patient and net revenue growth for the pitolisant franchise to the mid 2040’s *Based on pediatric exclusivity |

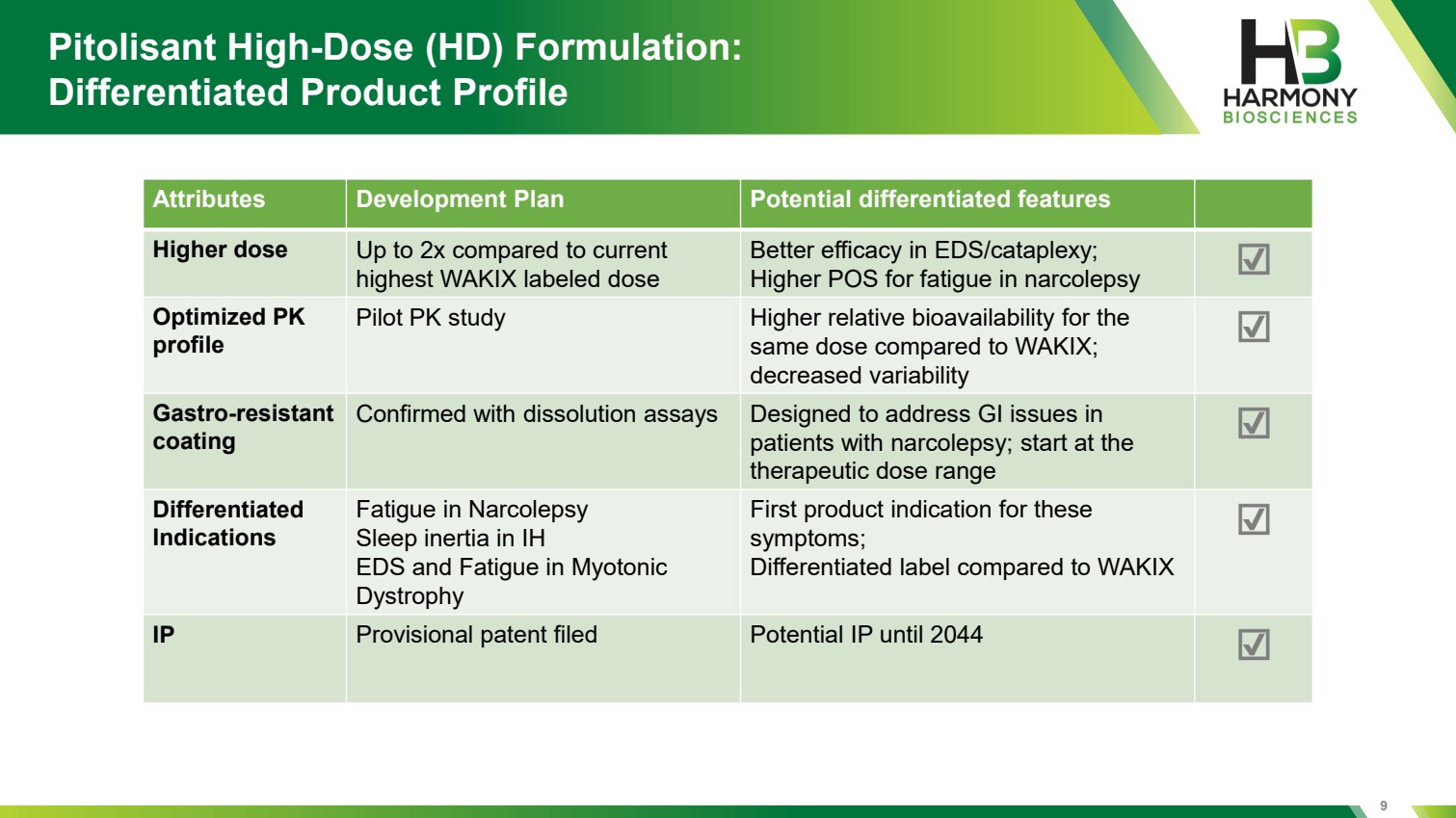

| Pitolisant High-Dose (HD) Formulation: Differentiated Product Profile 9 Attributes Development Plan Potential differentiated features Higher dose Up to 2x compared to current highest WAKIX labeled dose Better efficacy in EDS/cataplexy; Higher POS for fatigue in narcolepsy Optimized PK profile Pilot PK study Higher relative bioavailability for the same dose compared to WAKIX; decreased variability Gastro-resistant coating Confirmed with dissolution assays Designed to address GI issues in patients with narcolepsy; start at the therapeutic dose range Differentiated Indications Fatigue in Narcolepsy Sleep inertia in IH EDS and Fatigue in Myotonic Dystrophy First product indication for these symptoms; Differentiated label compared to WAKIX IP Provisional patent filed Potential IP until 2044 |

| 10 Financial Highlights Net Product Revenue Non-GAAP Adjusted Net Income(1) Cash, Cash Equivalents & Investments $134.2 $172.8 Q2 2023 Q2 2024 $45.9 $60.6 $253.3 $327.4 2023 YTD 2024 YTD $86.6 $111.3 2023 YTD 2024 YTD $429.6 $438.4 $425.6 $453.6 $434.1 Jun 30 '23 Sep 30 '23 Dec 31 '23 Mar 31 '24 Jun 30 '24 29% 29% 28% (1) Non-GAAP Adjusted Net Income= GAAP Net Income excluding non-cash interest expense, depreciation, amortization, stock-based compensation, other non-operating items and tax effect of these items (In millions, USD) Three Months Ended June 30, 2024 Six Month Ended June 30, 2024 Q2 2023 Q2 2024 32% |

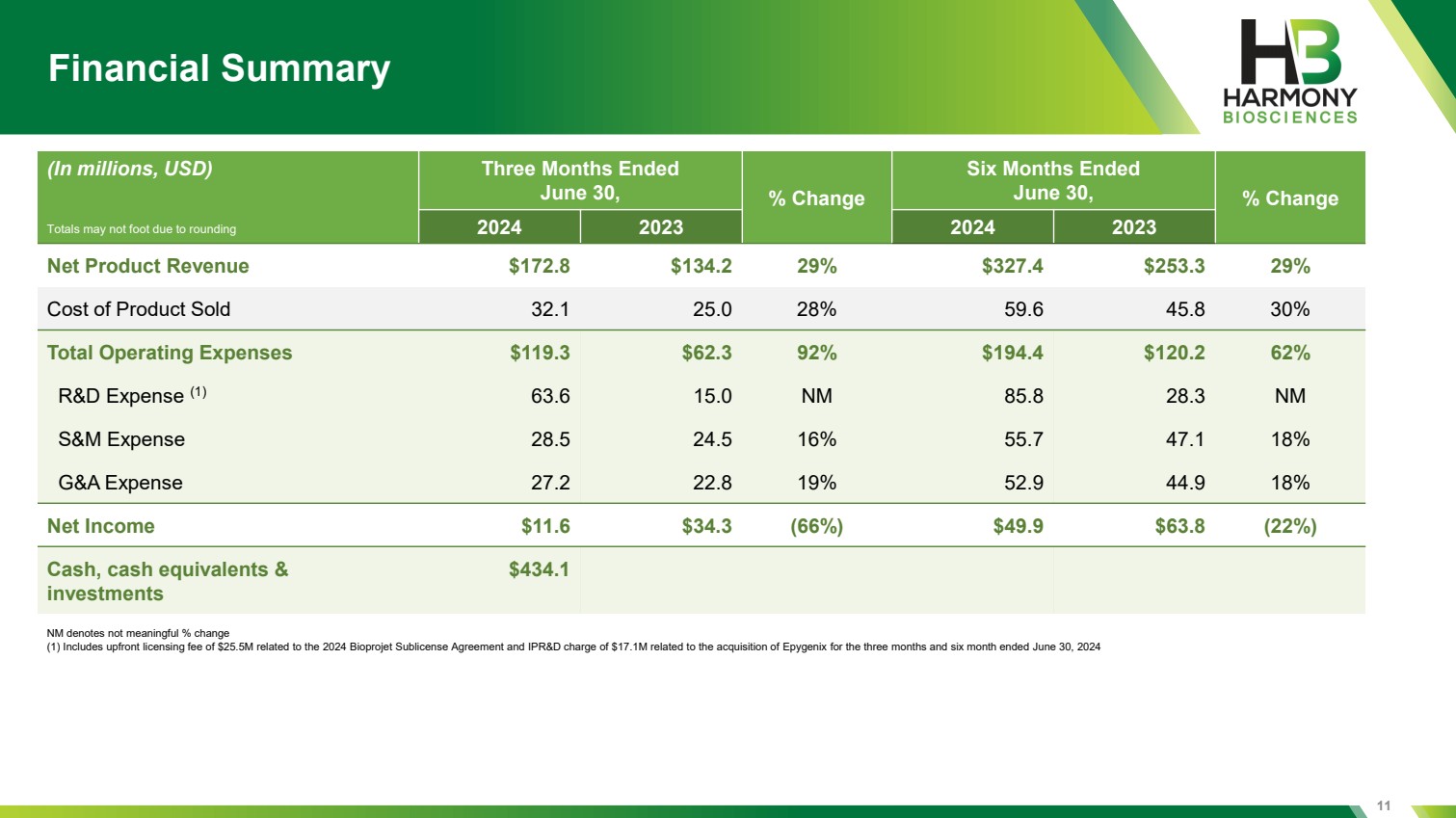

| 11 Financial Summary NM denotes not meaningful % change (1) Includes upfront licensing fee of $25.5M related to the 2024 Bioprojet Sublicense Agreement and IPR&D charge of $17.1M related to the acquisition of Epygenix for the three months and six month ended June 30, 2024 (In millions, USD) Three Months Ended June 30, % Change Six Months Ended June 30, % Change 2024 2023 2024 2023 Net Product Revenue $172.8 $134.2 29% $327.4 $253.3 29% Cost of Product Sold 32.1 25.0 28% 59.6 45.8 30% Total Operating Expenses $119.3 $62.3 92% $194.4 $120.2 62% R&D Expense (1) 63.6 15.0 NM 85.8 28.3 NM S&M Expense 28.5 24.5 16% 55.7 47.1 18% G&A Expense 27.2 22.8 19% 52.9 44.9 18% Net Income $11.6 $34.3 (66%) $49.9 $63.8 (22%) Cash, cash equivalents & investments $434.1 Totals may not foot due to rounding |

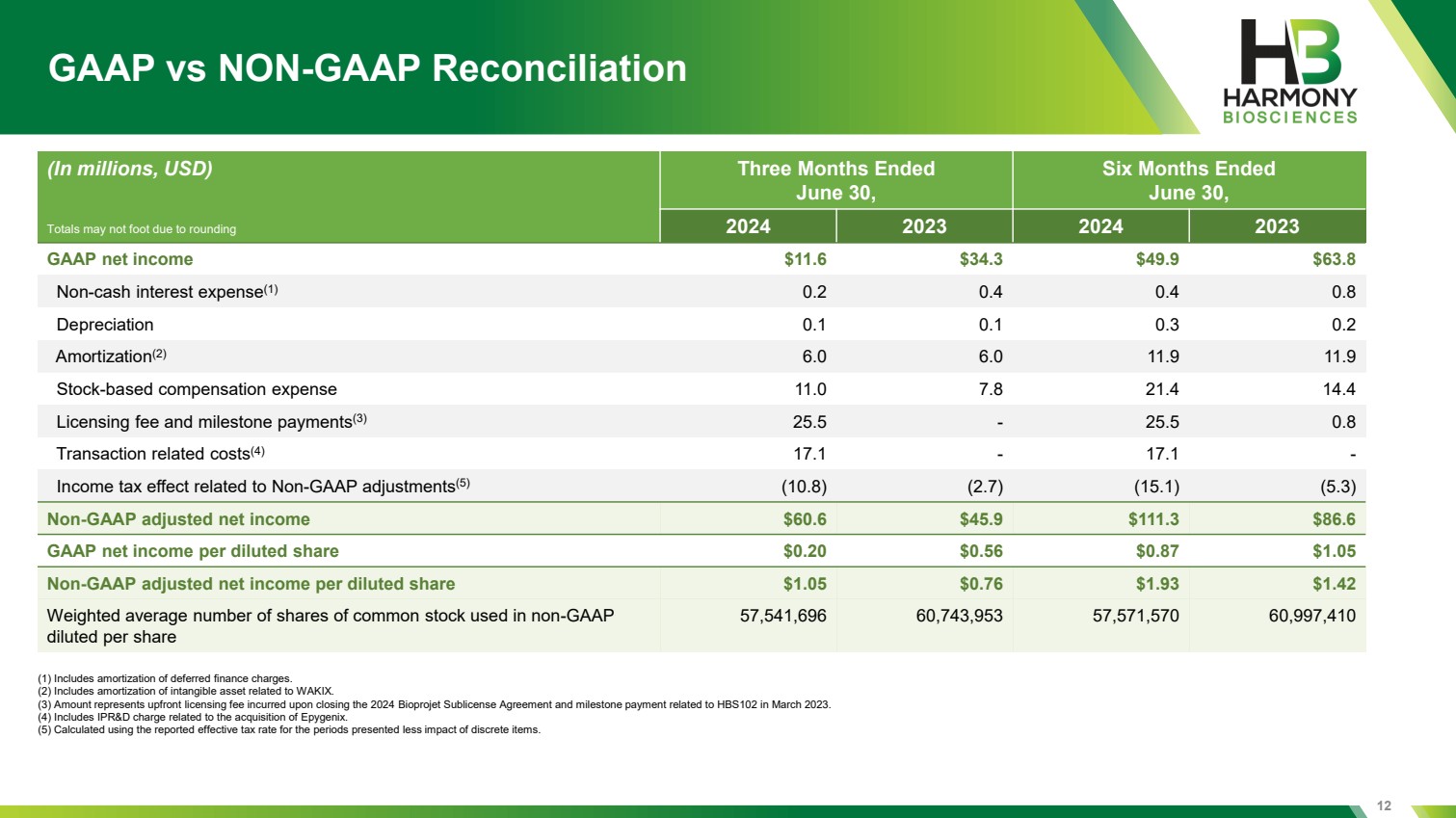

| 12 GAAP vs NON-GAAP Reconciliation (In millions, USD) Three Months Ended June 30, Six Months Ended June 30, 2024 2023 2024 2023 GAAP net income $11.6 $34.3 $49.9 $63.8 Non-cash interest expense(1) 0.2 0.4 0.4 0.8 Depreciation 0.1 0.1 0.3 0.2 Amortization(2) 6.0 6.0 11.9 11.9 Stock-based compensation expense 11.0 7.8 21.4 14.4 Licensing fee and milestone payments(3) 25.5 - 25.5 0.8 Transaction related costs(4) 17.1 - 17.1 - Income tax effect related to Non-GAAP adjustments(5) (10.8) (2.7) (15.1) (5.3) Non-GAAP adjusted net income $60.6 $45.9 $111.3 $86.6 GAAP net income per diluted share $0.20 $0.56 $0.87 $1.05 Non-GAAP adjusted net income per diluted share $1.05 $0.76 $1.93 $1.42 Weighted average number of shares of common stock used in non-GAAP diluted per share 57,541,696 60,743,953 57,571,570 60,997,410 (1) Includes amortization of deferred finance charges. (2) Includes amortization of intangible asset related to WAKIX. (3) Amount represents upfront licensing fee incurred upon closing the 2024 Bioprojet Sublicense Agreement and milestone payment related to HBS102 in March 2023. (4) Includes IPR&D charge related to the acquisition of Epygenix. (5) Calculated using the reported effective tax rate for the periods presented less impact of discrete items. Totals may not foot due to rounding |

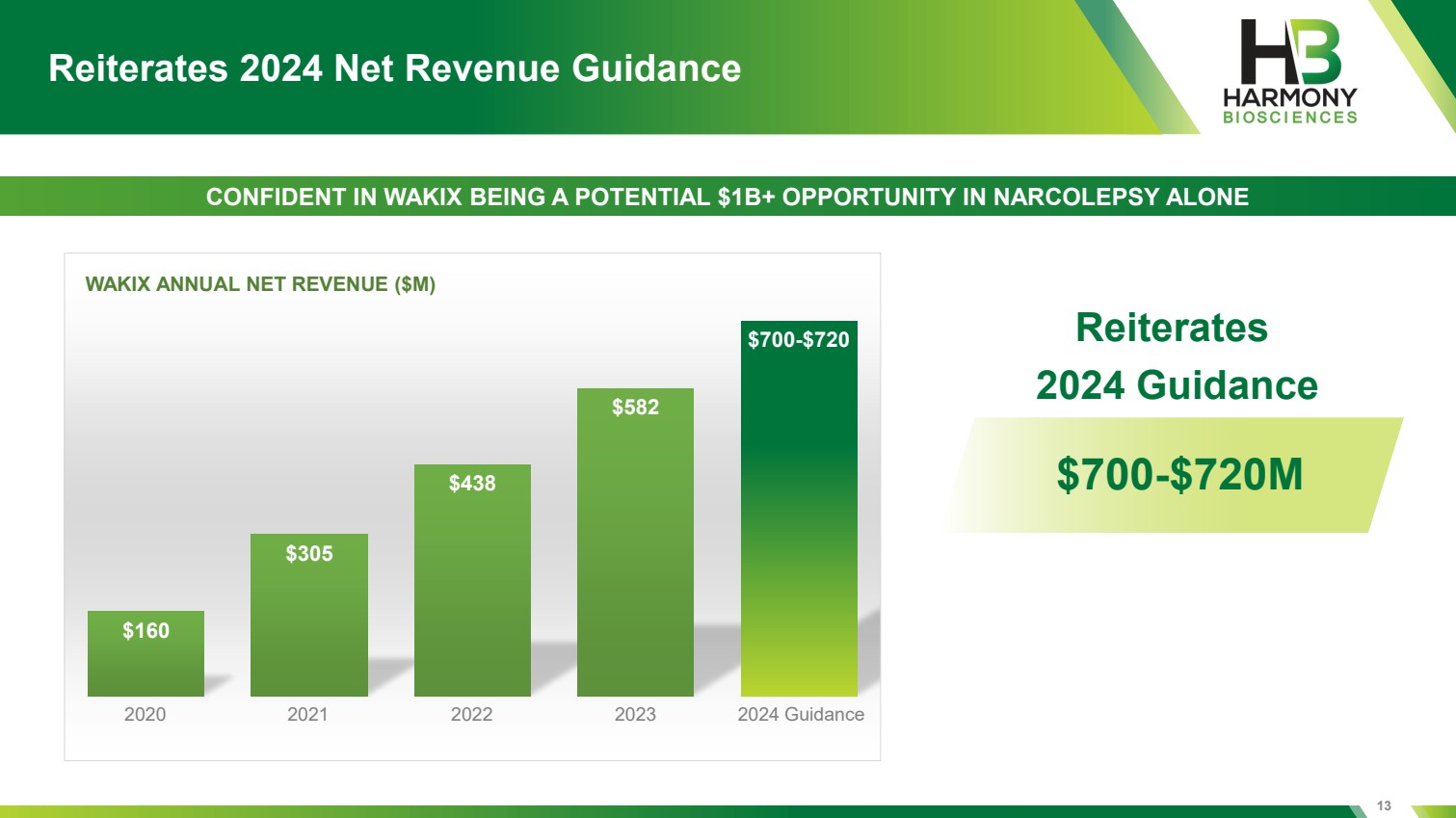

| 13 Reiterates 2024 Net Revenue Guidance $160 $305 $438 $582 $700-$720 WAKIX ANNUAL NET REVENUE ($M) 2020 2021 2022 2023 2024 Guidance CONFIDENT IN WAKIX BEING A POTENTIAL $1B+ OPPORTUNITY IN NARCOLEPSY ALONE $700-$720M Reiterates 2024 Guidance |

| Chris Living with narcolepsy Taking WAKIX since 2021 |