Description of Certain Components of Financial Data

Revenue

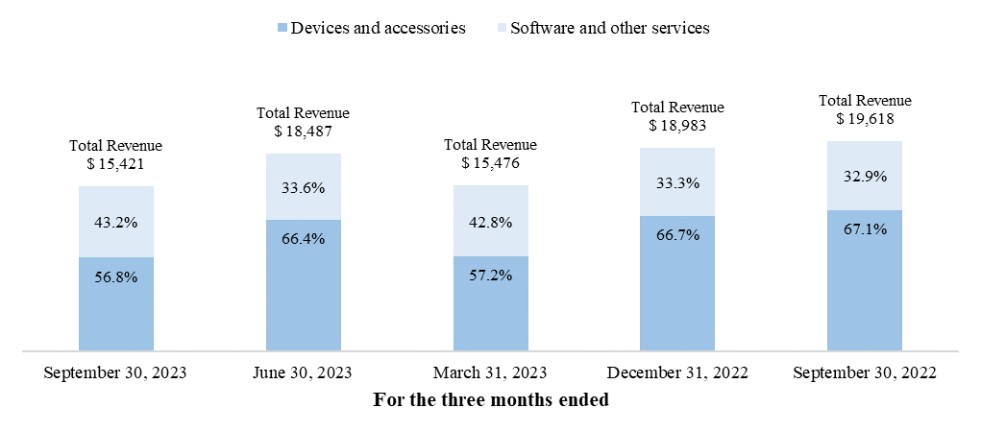

Revenue consists of revenue from the sale of products, such as medical devices and accessories, and the sale of software and related services, consisting of SaaS subscriptions and product support and maintenance (“Support”). SaaS subscriptions include licenses for teams and individuals as well as enterprise-level subscriptions. For sales of products, revenue is recognized at a point in time upon transfer of control to the customer. SaaS subscriptions and Support are generally recognized ratably over time.

Over time, as the adoption of our devices increases through further market penetration, and as practitioners continue using our devices and software platform, we expect our annual revenue mix to shift more toward software and other services. The quarterly revenue mix may be impacted by the timing of device sales.

To date, we have invested heavily in growing adoption at large-scale healthcare systems. As we expand our healthcare system software offerings and develop relationships with larger healthcare systems, we continue to expect a higher proportion of our revenue to come from direct sales to healthcare systems compared to eCommerce.

Cost of revenue

Cost of product revenue consists of product costs, including manufacturing costs, personnel costs and benefits, inbound freight, packaging, warranty replacement costs, payment processing fees, and inventory obsolescence and write-offs. We expect our cost of product revenue to fluctuate over time due to the level of units fulfilled in any given period, and we expect it to fluctuate as a percentage of product revenue over time as our focus on operational efficiencies in our supply chain may be offset by increased prices of certain inventory components.

Cost of software and other services revenue consists of personnel costs and benefits, cloud hosting costs and payment processing fees. Because the costs and associated expenses to deliver our SaaS offerings are less than the costs and associated expenses of manufacturing and selling our device, we anticipate an improvement in profitability and margin expansion over time as our revenue mix shifts increasingly towards software and other services. We plan to continue to invest resources to expand and further develop our SaaS and other service offerings.

Research and development

Research and development expenses primarily consist of personnel costs and benefits, facilities-related expenses and depreciation, fabrication services, and software costs. Most of our research and development expenses are related to developing new products and services that have not reached the point of commercialization and improving our products and services that have been commercialized. Fabrication services include certain third-party engineering costs, product testing, and test boards. Research and development expenses are expensed as incurred. We expect to continue to make substantial investments in our product and software development, clinical, and regulatory capabilities.

Sales and marketing

Sales and marketing expenses primarily consist of personnel costs and benefits, advertising, conferences and events, facilities-related expenses, and software costs. We expect to continue to make substantial investments in our sales capabilities.

General and administrative

General and administrative expenses primarily consist of personnel costs and benefits, outside services, insurance, software costs, and facilities-related expenses and depreciation. Outside services consist of professional services, legal fees, and other professional fees.

Other

Operating expenses classified as other are expenses which we do not consider representative of our ongoing operations. These other expenses primarily consist of employee severance and benefits costs related to our reductions in force, litigation costs, and legal settlements.