Exhibit 99.1

FINANCIAL STATEMENTS

GUARDFORCE AI CO., LIMITED AND SUBSIDIARIES

UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE SIX MONTHS ENDED JUNE 30, 2021 and 2020

F-1

Guardforce AI Co., Limited and Subsidiaries

Unaudited Interim Condensed Consolidated Statements of Financial Position

(Expressed in U.S. Dollars)

Note | As at June 30, 2021 | As at December 31, 2020 | ||||||||

| (Unaudited) | ||||||||||

| Assets | ||||||||||

| Current assets: | ||||||||||

| Cash and cash equivalents | 4 | $ | 7,725,129 | $ | 8,414,044 | |||||

| Accounts receivable, net | 6 | 5,790,229 | 5,468,911 | |||||||

| Withholding taxes receivables | 7 | - | 690,487 | |||||||

| Other current assets | 8 | 2,462,654 | 1,584,884 | |||||||

| Deferred costs | 38,880 | - | ||||||||

| Inventory | 5 | 2,553,957 | 495,081 | |||||||

| Amount due from related parties | 21 | 7,422 | 373,268 | |||||||

| Total current assets | 18,578,271 | 17,026,675 | ||||||||

| Restricted cash | 4 | 1,667,081 | 1,715,866 | |||||||

| Fixed assets, net | 9 | 9,075,078 | 7,884,354 | |||||||

| Right-of-use assets | 10 | 2,868,604 | 4,190,351 | |||||||

| Intangible assets, net | 11 | 189,438 | 223,408 | |||||||

| Goodwill | 3 | 329,534 | - | |||||||

| Withholding taxes receivable, net | 7 | 3,359,752 | 3,534,552 | |||||||

| Deferred costs | 68,040 | - | ||||||||

| Deferred tax assets, net | 15 | 972,384 | 1,038,346 | |||||||

| Other non-current assets | 8 | 330,416 | 361,275 | |||||||

| Total Assets | $ | 37,438,598 | $ | 35,974,827 | ||||||

| Liabilities and (Deficit) Equity | ||||||||||

| Current liabilities: | ||||||||||

| Trade and other payables | 12 | $ | 3,050,006 | $ | 1,540,411 | |||||

| Short-term borrowings from financial institutions | 13 | 1,700,473 | 494,994 | |||||||

| Current portion of operating lease liabilities | 1,556,425 | 2,211,984 | ||||||||

| Current portion of finance lease liabilities, net | 14 | 790,704 | 632,105 | |||||||

| Other current liabilities | 12 | 1,349,427 | 1,249,106 | |||||||

| Deferred revenue | 43,200 | - | ||||||||

| Income tax payables | - | 284,627 | ||||||||

| Amount due to related parties | 21 | 4,396,317 | 1,670,469 | |||||||

| Total current liabilities | 12,886,552 | 8,083,696 | ||||||||

| Long-term borrowings from financial institutions | 13 | 986,584 | 993,869 | |||||||

| Operating lease liabilities | 10 | 1,482,152 | 2,106,429 | |||||||

| Long-term borrowings from related parties | 21 | 18,127,706 | 19,085,812 | |||||||

| Finance lease liabilities, net | 14 | 825,841 | 1,023,366 | |||||||

| Deferred revenue | 75,600 | - | ||||||||

| Provision for employee benefits | 16 | 6,547,498 | 6,841,673 | |||||||

| Total liabilities | 40,931,933 | 38,134,845 | ||||||||

| Commitments and Contingencies | ||||||||||

| (Deficit) Equity | ||||||||||

| Ordinary shares* – par value $0.003 authorized 100,000,000 shares, issued and outstanding 17,587,388 shares at June 30, 2021; par value $0.003 authorized 100,000,000 shares, issued and outstanding 17,356,090 shares at December 31, 2020 | 52,763 | 52,069 | ||||||||

| Subscription receivable | (50,000 | ) | (50,000 | ) | ||||||

| Additional paid in capital | 2,409,864 | 2,082,795 | ||||||||

| Legal reserve | 20 | 223,500 | 223,500 | |||||||

| Deficit | (6,277,568 | ) | (4,722,294 | ) | ||||||

| Accumulated other comprehensive income | 98,352 | 204,249 | ||||||||

| Total deficit attributable to equity holders of the Company | (3,543,089 | ) | (2,209,681 | ) | ||||||

| Total equity attributable to non-controlling interests | 49,754 | 49,663 | ||||||||

| Total deficit | (3,493,335 | ) | (2,160,018 | ) | ||||||

| Total Liabilities and Equity | $ | 37,438,598 | $ | 35,974,827 | ||||||

| * | Giving retroactive effect to the reverse split on August 20, 2021. |

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

F-2

Guardforce AI Co., Limited and Subsidiaries

Unaudited Interim Condensed Consolidated Statements of Profit or Loss

(Expressed in U.S. Dollars)

Note | For the six months ended June 30, | |||||||||

| 2021 | 2020 | |||||||||

| Revenue | 2.8 | $ | 18,405,025 | $ | 18,728,786 | |||||

| Cost of revenue | 2.9 | (16,346,463 | ) | (15,441,180 | ) | |||||

| Gross margin | 2,058,562 | 3,287,606 | ||||||||

| Provision for withholding taxes receivable | (98,226 | ) | - | |||||||

| Administrative expenses | 19 | (3,271,608 | ) | (4,094,532 | ) | |||||

| Loss from operations | (1,311,272 | ) | (806,926 | ) | ||||||

| Other income, net | 237,178 | 32,452 | ||||||||

| Foreign exchange loss, net | (40,137 | ) | (310,207 | ) | ||||||

| Finance costs | (440,952 | ) | (435,713 | ) | ||||||

| Loss before provision for income taxes | (1,555,183 | ) | (1,520,394 | ) | ||||||

| Provision for income taxes | 15 | - | (58,368 | ) | ||||||

| Net loss for the period | (1,555,183 | ) | (1,578,762 | ) | ||||||

| Less: net loss (profit) attributable to non-controlling interests | (91 | ) | 5,420 | |||||||

| Net loss attributable to equity holders of the Company | $ | (1,555,274 | ) | $ | (1,573,342 | ) | ||||

| Loss per share | ||||||||||

| Basic and diluted (loss) profit for the period attributable to ordinary equity holders of the Company* | $ | (0.09 | ) | $ | (0.09 | ) | ||||

| Weighted average number of shares used in computation: | ||||||||||

| Basic and diluted* | 17,486,264 | 17,090,926 | ||||||||

| * | Giving retroactive effect to the reverse split on August 20, 2021. |

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

F-3

Guardforce AI Co., Limited and Subsidiaries

Unaudited Interim Condensed Consolidated Statements of Comprehensive Loss

(Expressed in U.S. Dollars)

| For the six months ended June 30, | ||||||||||

| Note | 2021 | 2020 | ||||||||

| Net loss for the period | $ | (1,555,183 | ) | $ | (1,578,762 | ) | ||||

| Currency translation differences | 2.5 | (105,897 | ) | (414,098 | ) | |||||

| Total comprehensive income (loss) for the period | $ | (1,661,080 | ) | $ | (1,992,860 | ) | ||||

| Attributable to: | ||||||||||

| Equity holders of the Company | $ | (1,661,171 | ) | $ | (1,987,440 | ) | ||||

| Non-controlling interests | 91 | (5,420 | ) | |||||||

| $ | (1,661,080 | ) | $ | (1,992,860 | ) | |||||

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

F-4

Guardforce AI Co., Limited and Subsidiaries

Unaudited Interim Condensed Consolidated Statements of Changes in Equity (Deficit)

(Expressed in U.S. Dollars)

| Number of Shares* | Amount ($0.003 par*) | Subscription Receivable | Addition Paid-in Capital | Legal Reserve | Accumulated Other Comprehensive Income | Deficit | Non- controlling Interests | Total | ||||||||||||||||||||||||||||

| Balance as at December 31, 2019 (Note 17) | 16,666,663 | $ | 50,000 | $ | (50,000 | ) | $ | 2,360,204 | $ | 223,500 | $ | 273,579 | $ | (1,596,270 | ) | $ | 65,894 | $ | 1,326,907 | |||||||||||||||||

| Currency translation adjustments | - | - | - | - | - | (414,098 | ) | - | - | (414,098 | ) | |||||||||||||||||||||||||

| Stock-based compensation expenses | 689,427 | 2,069 | 16,757 | 18,826 | ||||||||||||||||||||||||||||||||

| Net loss for the period | - | - | - | - | - | - | (1,573,342 | ) | (5,420 | ) | (1,578,762 | ) | ||||||||||||||||||||||||

| Balance as at June 30, 2020 (Unaudited) | 17,356,090 | $ | 52,069 | $ | (50,000 | ) | $ | 2,376,961 | $ | 223,500 | $ | (140,519 | ) | $ | (3,169,612 | ) | $ | 60,474 | $ | (647,127 | ) | |||||||||||||||

| Balance as at December 31, 2020 (Note 17) | 17,356,090 | $ | 52,069 | $ | (50,000 | ) | $ | 2,082,795 | $ | 223,500 | $ | 204,249 | $ | (4,722,294 | ) | $ | 49,663 | $ | (2,160,018 | ) | ||||||||||||||||

| Currency translation adjustments | (105,897 | ) | (105,897 | ) | ||||||||||||||||||||||||||||||||

| Stock-based compensation expenses | 187,598 | 563 | (563 | ) | - | |||||||||||||||||||||||||||||||

| Issued shares for acquisition of a subsidiary | 43,700 | 131 | 327,632 | 327,763 | ||||||||||||||||||||||||||||||||

| Net loss for the period | (1,555,274 | ) | 91 | (1,555,183 | ) | |||||||||||||||||||||||||||||||

| Balance as at June 30, 2021 (Unaudited) | 17,587,388 | $ | 52,763 | $ | (50,000 | ) | $ | 2,409,864 | $ | 223,500 | $ | 98,352 | $ | (6,277,568 | ) | $ | 49,754 | $ | (3,493,335 | ) | ||||||||||||||||

| * | Giving retroactive effect to the reverse split on August 20, 2021. |

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements

F-5

Guardforce AI Co., Limited and Subsidiaries

Unaudited Interim Condensed Consolidated Statements of Cash Flows

(Expressed in U.S. Dollars)

| For the six months ended June 30, | ||||||||

| 2021 | 2020 | |||||||

| Operating activities | ||||||||

| Net loss | $ | (1,555,183 | ) | $ | (1,578,762 | ) | ||

| Adjustments to reconcile net (loss) profit to net cash provided by operating activities: | ||||||||

| Depreciation and Amortization of intangible assets | 2,542,432 | 2,486,283 | ||||||

| Stock-based compensation | - | 18,826 | ||||||

| Interest expense | 341,123 | 220,992 | ||||||

| Deferred tax | - | 11,269 | ||||||

| Recovery of doubtful accounts, net | - | (2,842 | ) | |||||

| Provision for withholding taxes receivable | 98,226 | - | ||||||

| (Gain) Loss from fixed assets disposal | (2,189 | ) | 43 | |||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts and other receivables | (673,605 | ) | (148,074 | ) | ||||

| Other current assets | (1,005,395 | ) | 88,282 | |||||

| Inventory | (2,105,633 | ) | (70,808 | ) | ||||

| Amount due from related parties | 365,594 | 129,256 | ||||||

| Other non-current assets | (98,693 | ) | 186,250 | |||||

| Trade and other payables | 872,339 | (592,783 | ) | |||||

| Other current liabilities | 28,428 | (5,404 | ) | |||||

| Income tax payables | - | (47,099 | ) | |||||

| Amount due to related parties | 2,566,716 | 422,211 | ||||||

| Withholding taxes receivable | 522,688 | (356,170 | ) | |||||

| Provision for employee benefits | 146,100 | 107,961 | ||||||

| Net cash provided by operating activities | 2,042,948 | 869,431 | ||||||

| Investing activities | ||||||||

| Purchase of property and equipment | (2,251,341 | ) | (188,890 | ) | ||||

| Proceeds from fixed assets disposal | 2,598 | 165 | ||||||

| Purchase of intangible assets | - | (5,524 | ) | |||||

| Cash acquired from acquisition of a subsidiary | 24,276 | - | ||||||

| Net cash used in investing activities | (2,224,467 | ) | (194,249 | ) | ||||

| Financing activities | ||||||||

| Proceeds from borrowings | 1,622,855 | 3,516,143 | ||||||

| Repayment of borrowings | (378,046 | ) | (1,207,112 | ) | ||||

| Interest paid | (269,389 | ) | (72,823 | ) | ||||

| Lease payments | (977,073 | ) | (1,401,490 | ) | ||||

| Net cash (used in) provided by financing activities | (1,653 | ) | 834,718 | |||||

| Effect of exchange rate changes on cash | (554,528 | ) | (178,352 | ) | ||||

| Net (decrease) increase in cash and cash equivalents, and restricted cash | (737,700 | ) | 1,331,548 | |||||

| Cash and cash equivalents, and restricted cash at beginning of year | 10,129,910 | 7,687,721 | ||||||

| Cash and cash equivalents, and restricted cash at end of period | $ | 9,392,210 | $ | 9,019,269 | ||||

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

F-6

Guardforce AI Co., Limited and Subsidiaries

Notes to the Unaudited Interim Condensed Consolidated Financial Statements

(Expressed in U.S. Dollars)

| 1. | NATURE OF OPERATIONS |

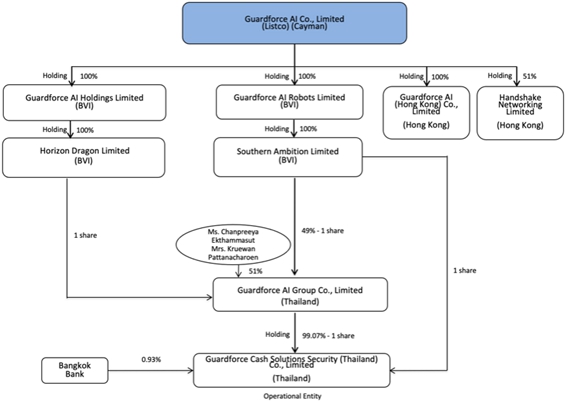

Guardforce AI Co., Limited (“Guardforce”) is a company incorporated and domiciled in the Cayman Islands under the Companies Act on April 20, 2018. The address of its registered office is 10 Anson Road, #28-01 International Plaza, Singapore 079903. Guardforce is controlled by Guardforce AI Technology Limited (“AI Technology”).

Guardforce AI Holding Limited (“AI Holdings”) was incorporated in the British Virgin Islands under the BVI Business Companies Act, 2004, on May 22, 2018. AI Holdings is a 100% owned subsidiary of Guardforce. AI Holdings’ registered office is located in British Virgin Islands.

Guardforce AI Robots Limited (“AI Robots”) was incorporated in the British Virgin Islands under the BVI Business Companies Act, 2004, on May 22, 2018. AI Robots is a 100% owned subsidiary of Guardforce.

Guardforce AI (Hong Kong) Co., Limited (“AI Hong Kong”) was incorporated in Hong Kong under the Hong Kong Companies’ Ordinance (Chapter 622), on May 30, 2018. AI Hong Kong is a 100% owned subsidiary of Guardforce. Beginning March 2020, AI Hong Kong commenced robotic AI solution business of selling robots.

Southern Ambition Limited (“Southern Ambition”) was incorporated in the British Virgin Islands under the BVI Business Companies Act, 2004, on August 3, 2018. Southern Ambition is a 100% owned subsidiary of AI Robots.

Horizon Dragon Limited (“Horizon Dragon”) was incorporated in the British Virgin Islands under the BVI Business Companies Act, 2004, on July 3, 2018. Horizon Dragon is a 100% owned subsidiary of AI Holdings.

Guardforce AI Group Co., Limited (“AI Thailand”) was incorporated in Thailand under the Civil and Commercial Code at the Registry of partnerships and Companies, Bangkok Metropolis, Thailand, on September 21, 2018 and has 100,000 ordinary plus preferred shares outstanding. 48,999 of the shares in AI Thailand are owned by Southern Ambition Limited, with one share being held by Horizon Dragon Limited, for an aggregate of 49,000 ordinary shares, or 49%, and 51,000 cumulative preferred shares are owned by two individuals of Thailand. The 49,000 ordinary shares with a value of approximately $16,000 and the value of the cumulative preferred shares of approximately $17,000 has not been received as of December 31, 2018. The cumulative preferred shares are entitled to dividends of $0.03 per share when declared. The cumulative unpaid dividends of the preferred shares as of December 31, 2020 is approximately $1,700. Pursuant to article of associates of AI Thailand, the holder of an ordinary share may cast one vote per share at a general meeting of shareholders, the holder of preferred shares may cast one vote for every 20 preferred shares held at a general meeting of shareholders. Southern Ambition is entitled to cast more than 95% of the votes at a general meeting of shareholders. No dividends were declared during the six months ended June 30, 2021 and 2020.

Guardforce Cash Solutions Security Thailand Co., Limited (“GF Cash (CIT)”) was incorporated in Thailand under the Civil and Commercial Code at the Registry of partnerships and Companies, Bangkok Metropolis, Thailand, on July 27, 1982 and has 3,857,144 outstanding shares. 3,799,544 ordinary shares and 21,599 preferred shares of the outstanding shares in GF Cash (CIT) (approximately 99.07% of the shares in GF Cash (CIT)) are owned by AI Thailand with one share being held by Southern Ambition and 33,600 ordinary shares and 2,400 preferred shares (approximately 0.933% of the shares in GF Cash (CIT)) being held by Bangkok Bank Public Company Limited. Pursuant to the articles of associates a shareholder may cast one vote per one share at a general meeting of shareholders. AI Thailand is entitled to cast 99.07% of the votes at a general meeting of shareholders. GF Cash (CIT)’s head office is located at No. 96 Vibhavadi-Rangsit Road, Talad Bang Khen Sub-District, Laksi District, Bangkok, Thailand. Beginning March 2020, GF Cash (CIT) commenced robotic AI solution business of selling and leasing of robots. No dividends were declared during the six months ended June 30, 2021 and 2020.

F-7

97% of the shares of GF Cash (CIT) are owned by AI Thailand and Southern Ambition, which were previously held by Guardforce TH Group Co., Ltd and Guardforce 3 Limited, with the same majority shareholder.

The reorganization of Guardforce and its subsidiaries (collectively referred to as the “Company) was completed on December 31, 2018. Pursuant to the reorganization, Guardforce became the holding company of the companies, which were under the common control of the controlling shareholder before and after the reorganization. Accordingly, the Company’s financial statements have been prepared on a consolidated basis by applying the predecessor value method as if the reorganization had been completed at the beginning of the earliest reporting period. The Company engages principally in providing cash management and handling services located in Thailand.

The following diagram illustrates the Company’s legal entity ownership structure as of June 30, 2021:

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

The accounting policies applied are consistent with those of the audited consolidated financial statements for the years ended December 31, 2020 and 2019, as described in those audited consolidated financial statements, except for the adoption of new and amended International Financial Reporting Standards (“IFRS”) effective for the year ending December 31, 2021 which are relevant to the preparation of the unaudited interim condensed consolidated financial statements.

The financial statements were approved by the board of directors and authorized for issuance on December 15, 2021.

F-8

| 2.1 | Basis of presentation |

The accompanying unaudited interim condensed consolidated financial statements have been prepared in accordance with International Accounting Standard (“IAS”) 34, “Interim Financial Reporting”. These statements should be read in conjunction with the audited consolidated financial statements for the years ended December 31, 2020 and 2019, which have been prepared in accordance with IFRS. The unaudited interim condensed consolidated financial statements have been prepared on a historical cost basis. In the opinion of management, all adjustments necessary for a fair presentation have been included in the accompanying unaudited condensed consolidated financial statements and consist of only normal recurring adjustments, except as disclosed herein. The results of operations for the six months ended June 30, 2021 are not necessarily indicative of the results that may be expected for the full year ended December 31, 2021.

All amounts are presented in United States dollars (“US $” or “USD”) and have been rounded to the nearest US $.

| 2.2 | Basis of consolidation |

The consolidated statements of profit or loss and other comprehensive loss, changes in equity (deficit) and cash flows of the Company for the relevant periods include the results and cash flows of all companies now comprising the Company from the earliest date presented or since the date when the subsidiaries and/or businesses first came under the common control of the controlling shareholders, wherever the period is shorter.

The unaudited interim condensed consolidated statements of financial position of the Company as at June 30, 2021 and 2020 have been prepared to present the assets and liabilities of the subsidiaries using the existing book values from the controlling shareholders’ perspective.

Equity interests in subsidiaries held by parties other than the controlling shareholders are presented as non-controlling interests in equity.

All intra-group and inter-company transactions and balances have been eliminated on consolidation.

| 2.3 | Business combinations under common control |

IFRS 3 Business combinations does not include specific measurement guidance for transfers of businesses or subsidiaries between entities under common control. Accordingly, the Company has accounted for such transactions taking into consideration other guidance in the IFRS framework and pronouncements of other standard-setting bodies. The Company recorded assets and liabilities recognized as a result of transactions between entities under common control at the carrying value on the transferor’s financial statements, and to have the consolidated statements of financial position, profit or loss, comprehensive income, changes in equity and cash flows reflect the results of combining entities for all periods presented for which the entities were under the transferor’s common control, irrespective of when the combination takes place.

| 2.4 | Non-controlling interest |

The non-controlling interest represents the portion of the equity (net assets) in the subsidiary not directly or indirectly attributable to the Company. Non-controlling interests are presented as a separate component of equity on the consolidated statements of financial position, profit or loss, comprehensive income and changes in equity attributed to controlling and non-controlling interests.

| 2.5 | Foreign currency translation |

The reporting currency of the Company is the U.S. dollar (“USD”). The functional currency of Guardforce, AI Holdings, AI Robots, Horizon Dragon, Southern Ambition, is the USD. The functional currency of AI Hong Kong and Handshake is the Hong Kong dollar. The functional currency of AI Thailand and GF Cash (CIT) is the Thai Baht (“Baht” or “THB”).

F-9

The currency exchange rates that impact our business are shown in the following table:

| Period End Rate | Average Rate | |||||||||||||||

| June 30, | December 31, | For the six months ended June 30, | ||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Thai Baht | 0.0312 | 0.0324 | 0.0325 | 0.0316 | ||||||||||||

| Hong Kong Dollar | 0.1282 | 0.1282 | 0.1282 | 0.1282 | ||||||||||||

| 2.6 | Use of estimates |

The preparation of consolidated financial statements requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets and liabilities, income and expense. Actual results may differ from these estimates.

In preparing the unaudited interim condensed consolidated financial statements, the significant judgments made by management in applying the Company’s accounting policies and the key sources of estimation uncertainty were the same as those that applied to the consolidated financial statements for the year ended December 31, 2020.

| 2.7 | Financial risk management |

| 2.7.1 | Financial risk factors |

The Company’s activities expose it to a variety of financial risks: foreign exchange risk, interest rate risk and liquidity risk. The Company’s overall risk management program focuses on the unpredictability of financial markets and seeks to minimize potential adverse effects on the Company’s financial performance.

The unaudited interim condensed consolidated financial statements do not include all financial risk management information and disclosures required in the audited financial statements, and should be read in conjunction with the Company’s audited consolidated financial statements as at December 31, 2020 and 2019.

| 2.7.2 | Liquidity risk |

Prudent liquidity management implies maintaining sufficient cash and cash equivalents and the availability of funding through an adequate amount of committed credit facilities.

The Company’s primary cash requirements are for operating expenses and purchases of fixed assets. The Company mainly finances its working capital requirements from cash generated from operation and proceeds from bank borrowings and finance leases.

The Company’s policy is to regularly monitor current and expected liquidity requirements to ensure it maintains sufficient cash and cash equivalents and an adequate amount of committed credit facilities to meet its liquidity requirements in the short and long term.

At the reporting date, the contractual undiscounted cash flows of the Company’s current financial liabilities approximate their respective carrying amounts due to their short maturities.

| 2.7.3 | Capital risk management |

The Company’s objectives on managing capital are to safeguard the Company’s ability to continue as a going concern and support the sustainable growth of the Company in order to provide returns for shareholders and benefits for other stakeholders and to maintain an optimal capital structure to enhance shareholders’ value in the long term.

F-10

In order to maintain or adjust the capital structure, the Company may adjust the amount of dividends paid to shareholders, return of capital to shareholders, issue new shares or sell assets to reduce debt.

In the opinion of the directors of the Company, the Company’s capital risk is low.

| 2.7.4 | Impact of COVID-19 |

The Coronavirus Disease (COVID-19) outbreak and the measures taken to contain the spread of the pandemic have created a high level of uncertainty to global economic prospects and this has impacted the Company’s operations and its financial performance in year 2021 and 2020. As COVID-19 continues to evolve with significant level of uncertainty, management of the Company is unable to reasonably estimate the full financial impact of COVID-19 on the Company’s financial results in year 2021. The Company is monitoring the situation closely and to mitigate the financial impact, it is conscientiously managing its cost by adopting an operating cost reduction strategy and conserving liquidity by working with major creditors to align repayment obligations with receivable collections. Based on the Company’s most recent projections for year 2021 and with over $9 million in cash and cash equivalents, management of the Company believes that the Company will be able to continue to operate as a going concern in the foreseeable future for at least the next 12 months.

| 2.8 | Revenue from contracts with customers |

The Company generates its revenue primarily from rendering the following services: (i) Cash-In-Transit - Non Dedicated Vehicle (Non-DV); (ii) Cash-In-Transit - Dedicated Vehicle (DV); (iii) ATM management; (iv) Cash Processing (CPC); (v) Cash Center Operations (CCT); (vi) Cheque Center Service (CDC); (vii) Express Cash; (viii) Coin Processing Service; (ix) Cash Deposit Management Solutions and (x) Robotics AI Solutions.

The Company recognizes revenue when it has transferred to its customer control over the service rendered. Control refers to the ability of the customer to direct and obtain substantially all the transferred service’s benefits. Also, it implies that the customer has the ability to prevent a third-party from directing the use and obtaining substantially all the benefits of the transferred service. The Company’s management applies the following considerations to analyze the moment in which the control of the service is transferred to the customer.

| ● | Identify the contract or quotation with the agreed service price. |

| ● | Evaluate the services engaged in the customer’s contract and identify the related performance obligations. |

| ● | Consider the contract terms and commonly accepted practices in the business to determine the transaction price. The transaction price is the consideration that the Company expects to be entitled for delivering the services engaged with the customer. The consideration engaged in a customer’s contract is generally a fixed amount. |

| ● | Allocate the transaction price, if necessary, to each performance obligation (to each good or service that is different) for an amount that represents the part of the benefit that the Company expects to receive in exchange for the right of delivering the services engaged with the customer. |

| ● | Recognize revenue when the Company satisfied the performance obligation through the rendering of services engaged. |

All of the conditions mentioned above are accomplished normally when the services are rendered to the customer and revenue is recognized when the Company satisfied the performance obligation over time or point in time depending on the service type. The reported revenue reflects services delivered at the contract or agreed-upon price.

F-11

Revenue is recognized when the related performance obligation is satisfied.

Disaggregation information of revenue by service type is as follows:

| For the six months ended June 30, | ||||||||||||||||

| 2021 | Percentage of Total | 2020 | Percentage of Total | |||||||||||||

| Service Type | $ | Revenue | $ | Revenue | ||||||||||||

| Cash-In-Transit – Non-Dedicated Vehicles (CIT Non-DV) | $ | 5,939,614 | 32.3 | % | $ | 5,964,178 | 31.8 | % | ||||||||

| Cash-In-Transit - Dedicated Vehicle to Banks (CIT DV) | 2,380,880 | 12.9 | % | 2,438,017 | 13.0 | % | ||||||||||

| ATM Management | 5,806,020 | 31.5 | % | 6,267,452 | 33.5 | % | ||||||||||

| Cash Processing (CPC) | 1,401,421 | 7.6 | % | 1,443,220 | 7.7 | % | ||||||||||

| Cash Center Operations (CCT) | 1,540,291 | 8.4 | % | 1,595,889 | 8.5 | % | ||||||||||

| Cheque Center Service (CDC) | 31,081 | 0.2 | % | 30,285 | 0.2 | % | ||||||||||

| Others ** | 251,890 | 1.4 | % | 223,342 | 1.2 | % | ||||||||||

| Cash Deposit Management Solutions (GDM) | 849,956 | 4.6 | % | 637,877 | 3.4 | % | ||||||||||

| Robotics AI solutions | 203,872 | 1.1 | % | 128,250 | 0.7 | % | ||||||||||

| Total | $ | 18,405,025 | 100.0 | % | $ | 18,728,786 | 100.0 | % | ||||||||

| ** | Others include primarily revenue from express cash and coin processing services. |

| 2.9 | Cost of revenue |

Cost of revenue consists primarily of internal labor costs and related benefits, and other overhead costs that are directly attributable to services provided.

| 2.10 | Recent Accounting Pronouncements |

All new standards and amendments that are effective for annual reporting period commencing January 1, 2021 have been applied by the Company for the six months ended June 30, 2021. The adoption of these new and amended standards did not have material impact on the consolidated financial statements of the Company. A number of new standards and amendments to standards have not come into effect for the year beginning January 1, 2021, and they have not been early adopted by the Company in preparing these consolidated financial statements. None of these new standards and amendments to standards is expected to have a significant effect on the consolidated financial statements of the Company.

| 3. | BUSINESS COMBINATION |

On the February 4, 2021, the Company announced the acquisition of a majority stake in information security consultants Handshake Networking Ltd (“Handshake”), a Hong Kong-based company specializing in penetration testing. A total of 43,700 shares were issued and valued at $7.50 per share in consideration for 51% of Handshake.

Accordingly, the acquisition has been accounted for in accordance with IFRS 3 guidelines, whereby the Company recognized the assets and liabilities of Handshake transferred at their carrying amounts with a carry-over basis.

The following represents the purchase price allocation at the dates of the acquisition:

| March 25, 2021 | ||||

| Cash and cash equivalents | $ | 24,276 | ||

| Other current assets | 32,250 | |||

| Current liabilities | (58,297 | ) | ||

| Goodwill | 329,534 | |||

| Total purchase price | $ | 327,763 | ||

| 4. | CASH, CASH EQUIVALENTS AND RESTRICTED CASH |

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| Cash on hand | $ | 368,117 | $ | 392,803 | ||||

| Cash in bank | 7,357,012 | 8,021,241 | ||||||

| Subtotal | 7,725,129 | 8,414,044 | ||||||

| Restricted cash | 1,667,081 | 1,715,866 | ||||||

| Cash, cash equivalents, and restricted cash | $ | 9,392,210 | $ | 10,129,910 | ||||

F-12

| 5. | INVENTORY |

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| Robots at warehouse | $ | 2,553,957 | $ | 252,411 | ||||

| Robots in transit | - | 242,670 | ||||||

| Inventory | $ | 2,553,957 | $ | 495,081 | ||||

No allowance for slow moving or obsolete inventory was recorded for the six months ended June 30, 2021 and 2020.

| 6. | ACCOUNTS RECEIVABLE, NET |

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| Accounts receivable | $ | 5,790,229 | $ | 5,468,911 | ||||

| Allowance for doubtful accounts | - | - | ||||||

| Accounts receivable, net | $ | 5,790,229 | $ | 5,468,911 | ||||

| 7. | WITHHOLDING TAX RECEIVABLES, NET |

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| Current portion | $ | - | $ | 690,487 | ||||

| Non-current portion | 3,359,752 | 3,534,552 | ||||||

| Withholding tax receivables, net | $ | 3,359,752 | $ | 4,225,039 | ||||

During the second half of year 2020, the Company received a withholding taxes refund in connection with the Company’s 2013 to 2015 withholding taxes refund applications. The Company wrote off the difference between the receivable recorded and amount of known refund from the Thai Revenue Department. The Company did not have any write offs during the six months ended June 30, 2021 and 2020.

Out of prudence, based on amount written off for the receivable related to year 2013 to 2015, the Company recorded an allowance of $98,226 against its withholding taxes receivable for the six months ended June 30, 2021.

| 8. | OTHER CURRENT AND OTHER NON-CURRENT ASSETS |

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| Input VAT receivable | $ | 325,208 | $ | 134,746 | ||||

| Prepayments - office rental | 1,515,585 | 952,616 | ||||||

| Prepayments - insurance | 503,978 | 292,095 | ||||||

| Prepayments - others | 17,709 | 51,920 | ||||||

| Uniforms | 15,450 | 17,954 | ||||||

| Tools and supplies | 84,724 | 135,553 | ||||||

| Other current assets | $ | 2,462,654 | $ | 1,584,884 | ||||

| Deposits | $ | 330,416 | $ | 361,275 | ||||

| Other non-current assets | $ | 330,416 | $ | 361,275 | ||||

F-13

| 9. | FIXED ASSETS, NET |

| Leasehold improvements | Machinery and equipment | Office decoration and equipment | Vehicles | Assets under construction | GDM machines | Robots | Total | |||||||||||||||||||||||||

| Cost | ||||||||||||||||||||||||||||||||

| At December 31, 2020 | $ | 3,649,107 | $ | 5,713,840 | $ | 5,951,808 | $ | 17,885,762 | $ | - | $ | 1,883,116 | $ | 884,950 | $ | 35,968,583 | ||||||||||||||||

| Additions | 4,284 | 47,695 | 54,330 | 399,639 | 23,027 | - | 2,385,878 | 2,914,853 | ||||||||||||||||||||||||

| Disposals | - | (33,571 | ) | (3,136 | ) | (115,471 | ) | - | (7,443 | ) | (159,621 | ) | ||||||||||||||||||||

| Exchange differences | (231,811 | ) | (362,976 | ) | (378,093 | ) | (1,136,207 | ) | - | (119,627 | ) | (26,570 | ) | (2,255,284 | ) | |||||||||||||||||

| At June 30, 2021 (Unaudited) | 3,421,580 | 5,364,988 | 5,624,909 | 17,033,723 | 23,027 | 1,763,489 | 3,236,815 | 36,468,531 | ||||||||||||||||||||||||

| Accumulated Depreciation | ||||||||||||||||||||||||||||||||

| At December 31, 2020 | 2,923,013 | 5,390,966 | 5,124,622 | 14,004,064 | - | 616,280 | 25,284 | 28,084,229 | ||||||||||||||||||||||||

| Depreciation charged for the year | 78,674 | 89,833 | 111,429 | 611,225 | - | 174,897 | 178,999 | 1,245,057 | ||||||||||||||||||||||||

| Disposals | - | (33,568 | ) | (3,091 | ) | (115,471 | ) | - | (248 | ) | (152,378 | ) | ||||||||||||||||||||

| Exchange differences | (185,685 | ) | (342,465 | ) | (325,546 | ) | (889,619 | ) | - | (39,150 | ) | (990 | ) | (1,783,455 | ) | |||||||||||||||||

| As June 30, 2021 (Unaudited) | 2,816,002 | 5,104,766 | 4,907,414 | 13,610,199 | - | 752,027 | 203,045 | 27,393,453 | ||||||||||||||||||||||||

| Net book value | ||||||||||||||||||||||||||||||||

| At June 30, 2021 (Unaudited) | $ | 605,578 | $ | 260,222 | $ | 717,495 | $ | 3,423,524 | $ | 23,027 | $ | 1,011,462 | $ | 3,033,770 | $ | 9,075,078 | ||||||||||||||||

There was no impairment of fixed assets recorded for the six months ended June 30, 2021 and 2020. No fixed assets were pledged as security for bank borrowings.

| 10. | RIGHT-OF-USE ASSETS AND OPERATING LEASE LIABILITIES |

The carrying amounts of right-of-use assets are as below:

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| As at January 1 | $ | 4,190,351 | $ | 6,173,590 | ||||

| New leases | 120,399 | 532,978 | ||||||

| Depreciation expense | (1,223,282 | ) | (2,506,446 | ) | ||||

| Exchange difference | (218,864 | ) | (9,771 | ) | ||||

| Net book amount | $ | 2,868,604 | $ | 4,190,351 | ||||

Lease liabilities were measured at the present value of the remaining lease payments, discounted using the lessee’s incremental borrowing rate. The weighted average incremental borrowing rate applied to new leases during six months ended June 30, 2021 was 3.25%.

During the six months ended June 30, 2021, interest expense of $125,245 arising from lease liabilities was included in finance costs. Depreciation expense related to right-of-use assets was $1,223,282 during the six months ended June 30, 2021.

| 11. | INTANGIBLE ASSETS, NET |

Intangible assets represent computer software. The intangible assets are recorded at historic acquisition costs, and amortized on a straight-line basis over their estimated useful lives.

Costs associated with maintaining computer software programs are recognized as an expense as incurred. Development costs that are directly attributable to the design and testing of identifiable and unique software products controlled by the Company will be recognized as intangible assets when the criteria of intangible assets are met.

F-14

Intangible assets are not amortized where their useful lives are assessed to be indefinite. The useful life of an intangible asset that is not being amortized is reviewed annually to determine whether events and circumstances continue to support the indefinite useful life assessment for that asset. Otherwise, the change in useful life assessment from indefinite to finite is accounted for prospectively from the date of change and in accordance with the policy for amortization of intangible assets with finite lives as set out above. As of June 30, 2021 and December 31, 2020, the Company had no indefinite lived intangible assets.

| Computer software | ||||

| Cost | ||||

| At December 31, 2020 | $ | 995,045 | ||

| Additions | 4,782 | |||

| Exchange difference | (63,211 | ) | ||

| At June 30, 2021 (Unaudited) | 936,616 | |||

| Accumulated amortization | ||||

| At December 31, 2020 | 771,637 | |||

| Amortization charged for the year | 24,559 | |||

| Exchange difference | (49,018 | ) | ||

| As June 30, 2021 (Unaudited) | 747,178 | |||

| Net book value | ||||

| At June 30, 2021 (Unaudited) | $ | 189,438 | ||

| 12. | TRADE AND OTHER PAYABLES AND OTHER CURRENT LIABILITIES |

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| Trade accounts payable – third parties | $ | 2,396,957 | $ | 1,366,482 | ||||

| Accrued salaries and bonus | 547,114 | 140,321 | ||||||

| Accrued customer claims, cash loss and shortage, others** | 105,935 | 33,608 | ||||||

| Trade and other payables | $ | 3,050,006 | $ | 1,540,411 | ||||

| Output VAT | $ | 134,296 | $ | 114,877 | ||||

| Accrued Expenses | 575,935 | 375,815 | ||||||

| Payroll Payable | 359,222 | 560,051 | ||||||

| Other Payables | 279,974 | 198,363 | ||||||

| Other current liabilities | $ | 1,349,427 | $ | 1,249,106 | ||||

| ** | Includes a provision for penalty for failure to meet certain performance indicators as stipulated in certain customer contracts for approximately $45,700 and $14,600 respectively. |

| 13. | BORROWINGS FROM FINANCIAL INSTITUTIONS |

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| Current portion of long-term borrowings | $ | 1,700,473 | $ | 494,994 | ||||

| Long-term borrowings | 986,584 | 993,869 | ||||||

| Borrowings from financial institutions | $ | 2,687,057 | $ | 1,488,863 | ||||

F-15

The Company’s borrowings are mainly used to support its business in Thailand. Those borrowings carry interest at the rate varies from 2% to MLR minus 1% per annum. Maturity date of borrowings is made and repayable on various dates from November 5, 2021 to April 7, 2025. For the six months ended June 30, 2021 and 2020, the interest expense was $22,212 and $47,918, respectively.

As of June 30, 2021, the Company has unused bank overdraft availability of approximately $312,000 (THB10 million) and unused trust receipts availability of approximately $1,560,000 (THB50 million).

| 14. | FINANCE LEASE LIABILITIES |

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| Current portion | $ | 790,704 | $ | 632,105 | ||||

| Non-current portion | 825,841 | 1,023,366 | ||||||

| Finance lease liabilities | $ | 1,616,545 | $ | 1,655,471 | ||||

For the six months ended June 30, 2021 and 2020, interest expense was $46,102 and $52,499, respectively.

The minimum lease payments under finance lease agreements are as follows:

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| Within 1 year | $ | 320,700 | $ | 701,796 | ||||

| After 1 year but within 5 years | 1,440,400 | 1,074,047 | ||||||

| Less: Finance charges | (144,555 | ) | (120,372 | ) | ||||

| Present value of finance lease liabilities, net | $ | 1,616,545 | $ | 1,655,471 | ||||

Finance leased assets comprise primarily vehicles and office equipment as follow:

| As at June 30, 2021 | As at December 31, 2020 | |||||||

| Cost | $ | 3,370,741 | $ | 8,459,215 | ||||

| Less: Accumulated depreciation | (1,029,460 | ) | (4,226,875 | ) | ||||

| Net book value | $ | 2,341,282 | $ | 4,232,340 | ||||

| 15. | TAXATION |

Value added tax (“VAT”)

The Company is subject to a statutory VAT of 7% for services in Thailand. The output VAT is charged to customers who receive services from the Company and the input VAT is paid when the Company purchases goods and services from its vendors. The input VAT can be offset against the output VAT. The VAT payable is presented on the statements of financial position when input VAT is less than the output VAT. A recoverable balance is presented on the statements of financial position when input VAT is larger than the output VAT.

F-16

Deferred taxes

Current income taxes are provided on the basis of net income for financial reporting purposes, adjusted for income and expense items which are not assessable or deductible for income tax purposes, in accordance with the regulations of the relevant tax jurisdictions. Deferred income taxes are accounted for using an asset and liability method. Under this method, deferred income taxes are recognized for the tax consequences of temporary differences by applying enacted statutory rates applicable to future years to differences between the financial statement carrying amounts and the tax bases of existing assets and liabilities. The tax base of an asset or liability is the amount attributed to that asset or liability for tax purposes. The effect on deferred taxes of a change in tax rates is recognized in the consolidated statements of profit or loss in the period of change. A valuation allowance is provided to reduce the amount of deferred tax assets if it is considered more likely than not that some portion of, or all of the deferred tax assets will not be realized.

The Company offsets deferred tax assets and deferred tax liabilities if and only if it has a legally enforceable right to set off current tax assets and current tax liabilities and the deferred tax assets and deferred tax liabilities relate to income taxes levied by the same taxation authority on either the same taxable entity or different taxable entities which intend either to settle current tax liabilities and assets on a net basis, or to realize the assets and settle the liabilities simultaneously, in each future period in which significant amounts of deferred tax liabilities or assets are expected to be settled or recovered.

| 16. | PROVISION FOR EMPLOYEE BENEFITS |

The Company has a defined benefit plan based on the requirement of the Thailand Labor Protection Act B.E.2541 (1988) to provide retirement benefits to employees based on pensionable remuneration and length of service which are considered as unfunded. There were no plan assets set up and the Company will pay benefits when needed.

| Provision for employee benefits | ||||

| Defined benefit obligations at December 31, 2020 | $ | 6,841,673 | ||

| Estimate for the six months period | $ | (294,175 | ) | |

| Defined benefit obligations at June 30, 2021 (Unaudited) | $ | 6,547,498 | ||

| 17. | SHAREHOLDERS’ EQUITY |

On August 20, 2021, the shareholders of the Company approved a 1 for 3 reverse split of the Company’s authorized and issued ordinary shares whereby every three shares were consolidated into one share (the “Reverse Split”). In addition, the par value of each ordinary share increased from $0.001 to $0.003. The interim financial statements and all share and per share amounts have been retroactively restated to reflect the Reverse Split.

In addition to the Reverse Split, the shareholders of the Company also approved a proposal to resolve fractional entitlements to the Company’s issued ordinary shares resulting from the Reserve Split – under the proposal, fractional shares will be disregarded and will not be issued to the shareholders of the Company but all such fractional shares shall be redeemed in cash for the fair value of such fractional share, with fair value being defined as the closing price of the ordinary shares on a post-reverse split basis on the applicable trading market on the first trading date of the Company’s ordinary shares following the effectiveness of the Reverse Split; and an increase in the Company’s authorized ordinary shares from 100,000,000 to 300,000,000.

As of December 31, 2020, 17,356,090 ordinary shares were issued at par value of $0.003, equivalent to share capital of $52,069. In March 2021, the Company issued 187,598 ordinary shares (see Note 18) and 43,700 ordinary shares (see Note 3) at par value. Total ordinary shares issued as of June 30, 2021 was 17,587,388, equivalent to share capital of approximately $52,763. As of June 30, 2021 and December 31, 2020, subscription receivable for these shares was $50,000.

F-17

| 18. | STOCK-BASED COMPENSATION |

On December 16, 2019, the Company entered into an agreement and plan of merger (the “Merger Agreement”) with VCAB Eight Corporation, a Texas corporation (“VCAB”). As consideration for the Merger, the Company agreed to issue an aggregate of 877,025 shares of capital stock (“Plan Shares’) to VCAB’s claim holders. As of December 31, 2020, the Company has issued, 689,427 of the Plan Shares to approximately 670 designated and Bankruptcy Court approved claim holders. In March 2021, the Company issued 187,598 of the Plan Shares to additional claim holders upon their approval by the Bankruptcy Court. Following the completion of this process, the Company has approximately 1,300 holders of its outstanding ordinary shares. During the year ended December 31, 2020, the Company recorded the fair value of the shares in connection to the 877,025 shares issued in the merger transaction of $18,826 as stock-based compensation expense.

| 19. | ADMINISTRATIVE EXPENSES |

| For the six months ended June 30, | ||||||||

| 2021 | 2020 | |||||||

| Staff expense | $ | 1,248,056 | $ | 1,193,864 | ||||

| Rental expense | 340,752 | 703,011 | ||||||

| Depreciation and amortization expense | 235,604 | 84,288 | ||||||

| Utilities expense | 81,255 | 85,467 | ||||||

| Travelling and entertainment expense | 77,747 | 45,436 | ||||||

| Professional fees | 331,522 | 488,504 | ||||||

| Repairs and maintenance | 26,226 | 40,774 | ||||||

| Employee benefits | 353,358 | 566,561 | ||||||

| Other service fees | 153,906 | 368,397 | ||||||

| Other expenses** | 423,182 | 518,230 | ||||||

| $ | 3,271,608 | $ | 4,094,532 | |||||

| ** | Other expenses mainly comprised of stock-based compensation, office expenses, stamp duties, training costs, etc. |

| 20. | LEGAL RESERVE |

Under the provisions of the Civil and Commercial Code, GF Cash (CIT) is required to set aside as a legal reserve at least 5% of the profits arising from the business of the Company at each dividend distribution until the reserve is at least 10% of the registered share capital. The legal reserve is non-distributable. The Company reserve has met the legal reserve requirement of $223,500 as of June 30, 2021 and December 31, 2020.

F-18

| 21. | RELATED PARTY TRANSACTIONS |

The principal related party balances and transactions as at and for the six months ended June 30, 2021 and 2020 are as follows:

The principal related party balances and transactions as of and for the years ended December 31, 2020 and 2019 are as follows:

Amounts due from related parties:

| As at June 30, 2021 | As at December 31, 2020 | |||||||||

| Quantum Infosec Inc (“Quantum”) | (a, b) | $ | 357 | $ | - | |||||

| Guardforce TH Group Company Limited | (b) | 6,593 | 6,026 | |||||||

| Guardforce AI Technology Limited | (b) | 236 | - | |||||||

| Guardforce AI Service Limited | (b) | 236 | - | |||||||

| Bangkok Bank Public Company Limited | (c) | - | 443 | |||||||

| Guardforce Limited | (d) | - | 20,647 | |||||||

| Shenzhen Intelligent Guardforce Robot Technology Co., Limited | (e) | - | 346,152 | |||||||

| $ | 7,422 | $ | 373,268 | |||||||

| (a) | Quantum Infosec Inc is related with the Company since March 2021 when the Company acquired Handshake. Quantum owns 49% of Handshake and the shareholders of Quantum are the directors of Handshake. |

| (b) | Amounts due from Quantum Infosec Inc, Guardforce TH Group Company Limited, Guardforce AI Technology Limited, Guardforce AI Service Limited were business advances for operational purposes. |

| (c) | Amounts due from Bangkok Bank Public Company Limited represents trade receivables for service provided by the Company. |

| (d) | Amounts due from Guardforce Limited represents primarily trade receivables for the sale of robots. The balance was fully settled in January 2021. |

| (e) | Amounts due from Shenzhen Intelligent Guardforce Robot Technology Co., Limited comprised of $187,665 advance to suppliers for the purchase of robots and $158,487 commission receivable. |

Amounts due to related parties:

| As at June 30, 2021 | As at December 31, 2020 | |||||||||

| Tu Jingyi | (b) | $ | 88,047 | $ | 88,047 | |||||

| Profit Raider Investment Limited | (b) | 1,253,814 | 1,136,664 | |||||||

| Shenzhen Intelligent Guardforce Robot Technology Co., Limited | (d) | 2,881,698 | - | |||||||

| Guardforce Holdings (HK) Limited | (c) | 156,782 | 156,782 | |||||||

| Richard Hall | (e) | 15,976 | - | |||||||

| Shenzhen Junwei Investment Development Company Limited (“Junwei”) | (a) | - | 225,085 | |||||||

| Guardforce Aviation Security Company Limited | (d) | - | 1,224 | |||||||

| Guardforce Security (Thailand) Company Limited | (d) | - | 62,667 | |||||||

| $ | 4,396,317 | $ | 1,670,469 | |||||||

| (a) | Amounts due to Shenzhen Junwei Investment Development Company Limited represent non-interest bearing advances from related parties. In January 2021, the amount due to Junwei was forgiven. |

| (b) | Amounts due to Tu Jingyi and Profit Raider Investment Limited represented interest accrued on the respective loans. |

| (c) | Amounts due to Guardforce Holdings (HK) Limited comprised of $99,998 advances made and $56,784 accrued interests on the loans. |

| (d) | Amounts due to Shenzhen Intelligent Guardforce Robot Technology Co., Limited , Guardforce Aviation Security Company Limited and Guardforce Security (Thailand) Company Limited represent accounts payable for the products or services provided by related parties. |

| (e) | Richard Hall is related to the Company since March 2021 when the Company acquired Handshake. Richard is one of the shareholders of Quantum which owns 49% of Handshake and Richard is the director of Handshake. Amount due to Richard represent advances made to Handshake. |

F-19

Long-term borrowings from related parties:

| As at June 30, 2021 | As at December 31, 2020 | |||||||||

| Guardforce Holdings (HK) Limited | (a) | $ | 4,040,500 | $ | 4,140,500 | |||||

| Tu Jingyi | (b) | 1,437,303 | 1,437,303 | |||||||

| Profit Raider Investment Limited | (c) | 12,649,903 | 13,508,009 | |||||||

| $ | 18,127,706 | $ | 19,085,812 | |||||||

| (a) | From time to time, the Company borrowed from Guardforce Holdings (HK) Limited whereby as of June 30, 2021, total loan amount from Guardforce Holdings (HK) Limited was $4,648,498. These loans bear interest rate of 2% and are due on various dates from December 22, 2022 to September 8, 2023. |

| (b) | On September 1, 2018, the Company entered into an agreement with Mr. Tu Jingyi whereby he lent $1,437,303 (RMB10 million) to the Company. The loan is due on August 31, 2022 with an interest rate at 1.5%. |

| (c) | The loan with Profit Raider Investment Limited is due on December 31, 2022. As of June 30, 2021, the outstanding principal amount due was $12,649,903 and the amount of interest accrued on the loan, calculated up to June 31, 2021 was $1,253,814. |

Related party transactions:

| For the six months ended June 30, | ||||||||||

| Nature | 2021 | 2020 | ||||||||

| Service/ Products received from related parties: | ||||||||||

| Shenzhen Intelligent Guardforce Robot Technology Co., Limited – Purchases | (a) | $ | 4,652,125 | $ | 150,185 | |||||

| Service/ Products delivered to related parties: | ||||||||||

| Guardforce Limited – Sales | (b) | $ | 111,564 | $ | 128,410 | |||||

Nature of transactions:

| (a) | The Company purchased robots from Shenzhen Intelligent Guardforce Robot Technology Co., Limited; |

| (b) | The Company sold robots to Guardforce Limited. |

| 22. | COMMITMENTS AND CONTINGENCIES |

Executives/directors agreements

The Company has several employment agreements with executives and directors with the latest expiring in 2024. All agreements provide for automatic renewal options with varying terms of one year or three years unless terminated by either party. Future payments for employment agreements as of June 30, 2021, are as follows:

| Amount | ||||

| Twelve months ending June 30: | ||||

| 2022 | $ | 1,048,214 | ||

| 2023 | 740,372 | |||

| 2024 | 110,000 | |||

| Total minimum payment required | $ | 1,898,586 | ||

F-20

Contracted expenditure commitments

The Company’s contracted expenditures commitments as of June 30, 2021 but not provided in the consolidated financial statements are as follows:

| Payments Due by Period | ||||||||||||||||||||||

| Less than | 1-3 | 4-5 | More than | |||||||||||||||||||

| Contractual Obligations | Nature | Total | 1 year | years | years | 5 years | ||||||||||||||||

| Service fee commitments | (a) | $ | 804,992 | $ | 368,175 | $ | 436,817 | $ | - | $ | - | |||||||||||

| Operating lease commitments | (b) | 403,656 | 362,233 | 41,423 | - | - | ||||||||||||||||

| $ | 1,208,648 | $ | 730,408 | $ | 478,240 | $ | - | $ | - | |||||||||||||

| (a) | The Company has commitments to pay certain service fees to Stander Information Company Limited, as its service provider to provide technical services for operating systems, that comprise a monthly fixed amount and certain other fees as specified in the agreement. | |

| (b) | The Company has leased offices and various low value items with various lease terms. |

Bank guarantees

As of June 30, 2021, the Company had commitments with banks for bank guarantees in favor of government agencies and others of approximately $7,000,000.

| 23. | SUBSEQUENT EVENTS |

Subsequent events have been reviewed through the date the consolidated financial statements were issued and required no adjustments or disclosures.

F-21