Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 31, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-12557

CASCADE CORPORATION

(Exact name of registrant as specified in its charter)

| Oregon | 93-0136592 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

2201 N.E. 201st Ave. Fairview, Oregon 97024-9718

(Address of principal executive office) (Zip Code)

Registrant’s telephone number, including area code:503-669-6300

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, par value $.50 per share

Name of exchange on which registered:New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files ). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of common stock held by non-affiliates of the registrant as of July 31, 2011 was $553,766,874, based on the closing sale price of the common stock on the New York Stock Exchange on that date.

The number of shares outstanding of the registrant’s common stock as of March 8, 2012 was 11,088,735.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement to be filed within 120 days after the registrant’s fiscal year end of January 31, 2012, to be delivered to shareholders in connection with the Annual Meeting of Shareholders to be held June 6, 2012 are incorporated by reference into Part III.

Table of Contents

| 4 | ||||||||

| Item 1. | 4 | |||||||

| Item 1A. | 8 | |||||||

| Item 1B. | 11 | |||||||

| Item 2. | 12 | |||||||

| Item 3. | 12 | |||||||

| Item 4. | 12 | |||||||

| 13 | ||||||||

| Item 5. | 13 | |||||||

| Item 6. | 15 | |||||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 16 | ||||||

| Item 7A. | 33 | |||||||

| Item 8. | 35 | |||||||

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 71 | ||||||

| Item 9A. | 72 | |||||||

| Item 9B. | 72 | |||||||

| 73 | ||||||||

| Item 10. | 73 | |||||||

| Item 11. | 73 | |||||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 73 | ||||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 74 | ||||||

| Item 14. | 74 | |||||||

| 75 | ||||||||

| Item 15. | 75 | |||||||

| 76 | ||||||||

NOTE: All references to fiscal years are defined as year ended January 31, 2012 (fiscal 2012), year ended January 31, 2011 (fiscal 2011) and year ended January 31, 2010 (fiscal 2010).

Table of Contents

Forward-looking Statements

This Annual Report on Form 10-K, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (Item 7) contains forward-looking statements that involve risks and uncertainties, as well as assumptions that, if they never materialize or prove incorrect, could cause our results to differ materially from those expressed or implied by such forward-looking statements. All statements other than statements of historical fact are statements that could be deemed forward-looking statements, including any projections of revenue, gross profit, expenses, earnings or losses from operations, synergies or other financial items; any statements of plans, strategies, and objectives of management for future operations; any statements regarding future economic conditions or performance; any statements of expectation or belief; and any statements of assumptions underlying any of the foregoing. The risks, uncertainties, and assumptions referred to above include, but are not limited to:

| • | General business and economic conditions globally and in particular in the Americas, Europe, the Asia Pacific region and China; |

| • | Competitive factors and the cyclical nature of the materials handling industry and lift truck orders; |

| • | Risks and complexities associated with international operations, including foreign currency fluctuations and international tax considerations; |

| • | Environmental matters; |

| • | Cost and availability of raw materials; |

| • | Effectiveness of our cost reduction initiatives; and |

| • | Impact of acquisitions. |

We undertake no obligation to publicly revise or update forward-looking statements to reflect events or circumstances that arise after the date of this report. See “Risk Factors” (Item 1A) for additional information on risk factors with the potential to impact our business.

3

Table of Contents

| Item 1. | Business |

General

Cascade Corporation (Cascade) was organized in 1943 under the laws of the state of Oregon. The terms “Cascade”, “we”, and “our” include Cascade Corporation and its subsidiaries. Our headquarters are located in Fairview, Oregon, a suburb of Portland, Oregon. We are one of the world’s leading manufacturers of materials handling load engagement devices and related replacement parts, primarily for the lift truck industry and to a lesser extent, the construction industry.

Products

We manufacture an extensive range of materials handling load engagement products that are widely used on lift trucks and, to a lesser extent, on construction and agricultural vehicles.

Our products are primarily manufactured and distributed under the Cascade name and symbol, for which we have secured trademark protection. The primary function of lift truck related products is to provide the lift truck with the capability of engaging, lifting, repositioning, carrying and depositing various types of loads and products. We offer a wide variety of functionally different products, each of which has numerous sizes, models, capacities and optional combinations. Lift truck related products are designed to handle loads with pallets and for specialized application loads without pallets. Examples of specialized products include devices specifically designed to handle loads such as appliances, carpet and paper rolls, baled materials, textiles, beverage containers, drums, canned goods, bricks, masonry blocks, lumber, plywood, and boxed, packaged and containerized products.

Certain construction related products allow vehicles such as loaders, backhoes and rough terrain lift trucks to move materials in much the same manner as conventional lift trucks. Our other construction related products are used on excavators and loaders for both conventional and specialized ground engagement applications.

Our products are subject to strict design, construction and safety requirements established by industry associations and the International Organization for Standardization (ISO). Our major manufacturing facilities are ISO certified. Product specifications and characteristics are determined by the expected capacity to be lifted, the characteristics of the load, the environment in which employed, the terrain over which the load will be moved and the operational life cycle of the vehicle. Accordingly, while there are some standard products, the market demands a wide range of products in custom configurations and capacities.

The manufacturing of our products includes the purchase of raw materials and components: principally rolled bar, plate and extruded steel products; unfinished castings and forgings; hydraulic cylinders and motors; and hardware items such as fasteners, rollers, hydraulic seals and hose assemblies. Certain purchased parts are provided worldwide by a limited number of suppliers. Difficulties in obtaining alternative sources of rolled bar, plate and extruded steel products and other materials from a limited number of suppliers could affect operating results. We are not currently experiencing any significant shortages in obtaining raw materials, purchased parts, or other steel products.

Markets

We market our products throughout the world. Our primary customers are companies and industries that use lift trucks for materials handling. Examples of these industries include pulp and paper, grocery products, textiles, recycling and general consumer goods. Additionally, our construction attachments are used on medium and heavy duty construction vehicles which are used in a variety of construction markets including infrastructure, demolition, recycling, forestry, utility and general construction. Our products are sold to the end-user customer through the retail lift truck dealer distribution channel and to lift truck manufacturers as original equipment manufacturer (OEM) equipment.

4

Table of Contents

In major industrialized countries, lift trucks are a widely utilized method of materials handling. In these markets, lift trucks are generally considered maintenance capital investment. This tends to subject the industry in general to the cyclical patterns similar to the broader capital goods economic sector.

Sales of our construction attachments are significantly influenced by levels of commercial, infrastructure and general construction activity, including housing construction.

However, many of our products measurably improve overall materials handling and lift truck productivity. Further, we are continually developing products to serve new types of materials handling applications to meet specific customer and industry requirements. In this sense, our products may also be generally considered a productivity enhancing investment. Historically, this has somewhat cushioned the negative impact of downward trends in the lift truck market on our net sales.

In emerging industrialized countries, China in particular, lift trucks are replacing manual labor and other less productive methods of materials handling. As such, lift trucks are generally considered productivity enhancing investments in these markets.

Competition

We are one of the leading global independent suppliers of load engagement products for industrial lift trucks. We compete with a number of companies in different parts of the world, including Bolzoni Auramo, an Italian public company, and privately-owned companies with a strong presence in local and regional markets. A small number of these competitors compete with us globally.

In addition, several lift truck manufacturers, who are customers of ours, are also competitors in varying degrees to the extent they manufacture a portion of their load engagement product requirements. Since we offer a broad line of products capable of supplying a significant part of the total requirements for the entire lift truck industry, our experience has shown that lower costs resulting from our relatively high unit volume would be difficult for any individual lift truck manufacturer to achieve for most products. We design and position our products to be the performance and service leaders in their respective product categories and geographic markets.

Our market share and gross profit throughout the world vary by geographic region due to the different competitive environments we face in each of these regions. Fluctuations in gross profit within a geographic region over time are generally due to a change in the competitive environment, such as new competitors entering a market or existing entities merging or otherwise leaving the market. Additionally, cyclical variations in product demand directly affect margins as higher manufacturing volumes generally result in greater fixed cost absorption and increased gross profit.

A further discussion of the competitive factors in each geographic region follows:

Americas—We are the leading manufacturer in North America and the preferred supplier of many OEMs as well as original equipment dealers (OEDs) and distributors. We compete in this region primarily with smaller regionally-based companies and a limited number of smaller foreign competitors. Our leading position is the result of our continued focus on providing high quality products and outstanding customer service. In South and Central America, we supply highly engineered, customized products that are sourced from various global Cascade manufacturing facilities.

Europe—While we are also a leading manufacturer in Europe, we compete with Bolzoni Auramo and several privately-owned companies with a strong presence in local and regional markets. Price competition in this region has historically resulted in lower gross profit margins than in other regions.

Asia Pacific—Our primary locations in this region include operations in Japan, Australia and Korea. The competitive environment varies somewhat from country to country, and competitors vary in size from smaller regionally-based private companies to some larger lift truck manufacturers. In general, we believe we have established a strong presence in most markets in this region.

5

Table of Contents

China—We have operated in China since 1987 and have established a strong presence in the lift truck market. As a result of the continued growth in China’s economy and the expanded use of lift trucks for various industrial purposes, we are seeing an increase in the number of competitors in the Chinese market, primarily Chinese OEMs and European based manufacturers.

Customers

Our products are marketed and sold primarily to lift truck OEDs, OEMs and distributors globally. In addition to sales to the lift truck market, we do sell products to OEMs who manufacture construction, mining, agricultural and industrial vehicles other than lift trucks.

While no single customer accounts for more than 10% of our consolidated net sales, our five largest customers comprise approximately 25% of our consolidated net sales. Our regional sales, as a percentage, to OEM customers and all other customers are distributed as follows for fiscal 2012:

| OEM Customers | OED Customers | |||||||||

Americas | 44 | % | 56 | % | ||||||

Europe | 28 | % | 72 | % | ||||||

Asia Pacific | 32 | % | 68 | % | ||||||

China | 69 | % | 31 | % | ||||||

Global | 42 | % | 58 | % | ||||||

Backlog

Our products are manufactured with short lead times of generally less than two months. Accordingly, the level of backlog orders is not a significant factor in evaluating our overall level of business activity.

Research and Development

Our research and development activities are conducted by a global engineering group with facilities in North America, Asia Pacific and Europe. Our engineering staff develops global designs to be customized and produced regionally based on our customers requirements. Products are being continually developed to meet new applications and the changing needs of the markets.

Environmental Matters

From time to time, we are the subject of investigations, conferences, discussions and negotiations with various federal, state, local and foreign agencies with respect to cleanup of hazardous waste and compliance with environmental laws and regulations. “Risk Factors” (Item 1A), Notes to Consolidated Financial Statements (Item 8) and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (Item 7) contain additional information concerning our environmental matters.

Foreign Operations

We have substantial operations outside the United States. There are additional business risks attendant to our foreign operations, including the risk that the relative value of the underlying local currencies may weaken when compared to the U.S. dollar. For further information about foreign operations, see “Risk Factors” (Item 1A), “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (Item 7) and Notes to Consolidated Financial Statements (Item 8).

Employees

At January 31, 2012, we had approximately 1,900 full-time employees throughout the world. The majority of these employees are not subject to collective bargaining agreements. Certain employees are subject to national labor agreements in foreign locations.

6

Table of Contents

Available Information

Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to reports filed or furnished pursuant to Sections 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available free of charge on or through our website atwww.cascorp.com when such reports are available on the Securities and Exchange Commission (SEC) website—www.sec.gov. Once filed with the SEC, such documents may be read and/or copied at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330.

Officers of the Registrant

Robert C. Warren, Jr.—Chief Executive Officer and President (1)—Mr. Warren, 63, has served as President and Chief Executive Officer of Cascade since 1996. He was President and Chief Operating Officer from 1993 until 1996 and was formerly Vice President—Marketing. Mr. Warren joined Cascade in 1972.

Richard S. Anderson—Senior Vice President and Chief Operating Officer (1)—Mr. Anderson, 64, has served as Chief Operating Officer since June 2008. Mr. Anderson has been employed by Cascade since 1972 and held several positions including his appointments as Chief Financial Officer from 2001 to 2008, Vice President—Material Handling Product Group in 1996 and Senior Vice President—International in 1999.

Frank R. Altenhofen, Vice President—Asia Pacific (1)—Mr. Altenhofen, 50, was appointed Vice President, Asia Pacific in June 2008 and was appointed Vice President, Americas in 2007. He started his career with Cascade in 1983 and held numerous manufacturing, marketing, and management positions including General Manager of Cascade’s operations in China, until his departure in 2001. Mr. Altenhofen’s experience from 2001 to 2007 includes four years as President of an international medical device company.

Peter D. Drake, Vice President—Americas (1)—Mr. Drake, 44, was appointed Vice President—Americas in June 2008. He started his career with Cascade in 1991 and has held a number of management positions including serving as Plant Manager for Cascade’s Portland facility from 2000 to 2008.

Kevin B. Kreiter, Vice President—Engineering and Marketing (1)—Mr. Kreiter, 58, has served in his current position since 2007. He has been employed by Cascade since 1979 and has held several positions within the engineering group, including his appointment as Vice President—Engineering in 2006.

Jeffrey K. Nickoloff, Vice President—Corporate Manufacturing (1)—Mr. Nickoloff, 56, has served in his current position since 2002. He has held several positions with Cascade, including his appointments as Director of North American Manufacturing in 2000 and Plant Manager in 1993. Mr. Nickoloff joined Cascade in 1979.

Joseph G. Pointer, Vice President and Chief Financial Officer (1)—Mr. Pointer, 51, has served as Chief Financial Officer since 2008. He was the Vice President—Finance from 2000 to 2008. Prior to joining Cascade in 2000, Mr. Pointer was a partner at PricewaterhouseCoopers LLP in Portland, Oregon.

Davide Roncari, Vice President—Europe (1)—Mr. Roncari, 39, was appointed Vice President—Europe in June 2008. He has held a number of management positions in Cascade’s European operations since 2003, including his most recent assignment as Director of Engineering—Europe and Director of Production for the Verona, Italy manufacturing operations.

Susan Chazin-Wright, Vice President—Human Resources (1)—Ms. Chazin-Wright, 59, was appointed as Vice President–Human Resources in March 2008. Prior to joining Cascade, Ms. Wright served as Director of Human Resources at the Stanford Graduate School of Business and as Vice President of Corporate Services at Denso Corporation, a Toyota affiliate automotive component manufacturer.

John A. Cushing—Treasurer—Mr. Cushing, 51, has served as Treasurer since 2001. He previously was Assistant Treasurer from 1999 until 2001. Prior to joining Cascade in 1999, Mr. Cushing was Assistant Treasurer for Fred Meyer, Inc., a retail company headquartered in Portland, Oregon.

(1)—These individuals are considered executive officers of Cascade Corporation.

7

Table of Contents

| Item 1A. | Risk Factors |

In addition to the other information contained in this Form 10-K, the following are certain risks that we believe should be considered carefully in evaluating Cascade’s business. Our business, financial condition, cash flows or results of operations could be materially adversely affected by any of these risks. The risks summarized

below do not represent an exhaustive list, and additional risks not presently known to us or that we currently consider immaterial may also impair our business and operations.

Economic or industry downturns

Our business has historically experienced periodic cyclical downturns generally consistent with economic cycles in the markets in which we operate. The level of sales of our products reflects to a significant extent the capital investment decisions of the customers who buy our products and the lift trucks and other vehicles on which our products are used. These customers tend to delay capital projects, including the purchase of new equipment or upgrades, during industry or general economic downturns. Past downturns have been characterized by diminished product demand, excess manufacturing capacity and erosion of gross profit and net income. Therefore, a significant downturn in the markets of our customers, including lift truck manufacturers and to a lesser extent construction equipment manufacturers, or in general economic conditions will result in a reduction in demand for our products and negatively affect our results of operations.

Economic, political and other risks associated with international operations

Foreign operations represent over 55% of our sales. In the future, we expect revenue from foreign markets to continue to represent a significant portion of our total sales. As noted in “Properties” (Item 2), we own or lease facilities in several foreign countries throughout the world. Since we manufacture and sell our products worldwide, our business is subject to risks associated with doing business internationally. Accordingly, our future results could be negatively affected by a variety of factors, including:

| • | Foreign currency exchange risks; |

| • | Difficulty in staffing and managing global operations; |

| • | Imposition of foreign exchange controls; |

| • | Changes in a specific country’s or region’s political or economic conditions, particularly in emerging markets such as China; |

| • | Seizure of our property or assets by a foreign government; |

| • | Tariffs, quotas, other trade protection measures and import or export licensing requirements; |

| • | Restrictions on our ability to own or operate or repatriate profits from our subsidiaries, make investments or acquire new businesses in foreign jurisdictions; |

| • | Potentially negative consequences from changes in tax laws; |

| • | Differing labor regulations; |

| • | Requirements relating to withholding taxes on remittances and other payments by subsidiaries; |

| • | Civil unrest or war in any of the countries in which we operate; |

| • | Unexpected transportation delays or interruptions; |

| • | Difficulty in enforcement of contractual obligations governed by non-U.S. law and complying with multiple and potentially conflicting laws; and |

| • | Unexpected changes in regulatory requirements. |

8

Table of Contents

Foreign currency fluctuations

Changes in economic or political conditions globally and in any of the countries in which we operate could result in exchange rate movements, new currency or exchange controls or other restrictions being imposed on our operations.

Because our combined financial results are reported in U.S. dollars, translation of sales or earnings generated in other currencies into U.S. dollars can result in a significant increase or decrease in the amount of those sales or earnings. For purposes of accounting, the assets and liabilities of our foreign operations, where the local currency is the functional currency, are translated using period-end exchange rates, and the revenues, expenses and cash flows of our foreign operations are translated using average exchange rates during each period.

In addition to currency translation risks, we incur currency transaction risk whenever we enter into a purchase or a sales transaction using a currency other than the local currency of the transacting entity. Given the volatility of exchange rates, we cannot be assured we will be able to effectively manage our currency transaction and/or translation risks. We have purchased and may continue to purchase foreign currency hedging instruments protecting or offsetting positions in certain currencies to reduce the risk of adverse currency fluctuations. We only purchase these instruments to cover currency exposures. We have in the past experienced and expect to experience at times in the future an impact on earnings as a result of foreign currency exchange rate fluctuations.

Reliance on customers

Approximately 58% of our products are sold to the end-user customer through OEDs. Therefore, a significant portion of our sales is dependent on the quality and effectiveness of these dealers, who are not subject to our control.

We sell approximately 42% of our products directly to OEMs, several of which are global manufacturers. The following actions taken by these OEMs could significantly affect our business:

| • | Adjusting their inventories of our finished products as part of ongoing operations; |

| • | Shifting from local or regional sourcing of products to lower cost global sourcing; |

| • | Altering the distribution channels of certain products by acquiring all or part of their dealer network or by exerting influence over their sale of replacement parts and attachments through their distribution channels; |

| • | Manufacturing their own attachments. |

Competition

Our products do not depend upon proprietary technology to any significant degree, and therefore can be subject to intense competition. Competitive characteristics of our products include overall performance, ease of use, quality, safety, customer service and support, manufacturing lead times, global reach, brand reputation, breadth of product line and price. Our customers increasingly demand more technologically advanced and integrated products in certain cases and we must continue to develop our expertise and technical capabilities in order to manufacture and market these products successfully. To retain our competitive position, we are continuously working to improve our manufacturing processes, marketing efforts, customer service and distribution networks.

Environmental compliance costs and liabilities

Our operations and properties are subject to stringent U.S. and foreign, federal, state and local laws and regulations relating to environmental protection. These laws and regulations govern the investigation and cleanup of contaminated properties as well as air emissions, water discharges, waste management and disposal and workplace health and safety. We can be held responsible under these laws and regulations whether or not the

9

Table of Contents

original actions were legal and whether or not we knew of, or were responsible for, the presence of such hazardous or toxic substances. We could be responsible for payment of the full amount of any liability, whether or not any other responsible party also is liable.

These laws and regulations affect a significant percentage of our operations, are different in every jurisdiction and can impose substantial fines and sanctions for violations. Further, they may require substantial clean-up costs for our properties, many of which are sites of long-standing manufacturing operations, and the installation of costly pollution control equipment or operational changes to limit pollution emissions and/or decrease the likelihood of accidental hazardous substance releases. We must conform our operations and properties to these laws and adapt to regulatory requirements in all jurisdictions as these requirements change.

We routinely deal with natural gas, oil and other petroleum products. As a result of our operations, we generate, manage and dispose of or recycle hazardous wastes and substances such as solvents, thinner, waste paint, waste oil, wash-down wastes and sandblast material. Hydrocarbons or other hazardous substances or wastes may have been disposed or released on, under or from properties owned, leased or operated by us or on, under or from other locations where such substances or wastes have been taken for disposal. These properties may be subject to investigatory, clean-up and monitoring requirements under U.S. and foreign, federal, state and local environmental laws and regulations.

In prior years, we entered into settlement agreements with various environmental insurance providers with respect to litigation of claims under insurance policies issued by the providers to recover expenses incurred in connection with environmental and related proceedings. As a part of these settlement agreements, we released all of our rights to any future recovery under these policies.

Impact of acquisitions

We have historically expanded our business through acquisitions and expect we will do so in the future if appropriate opportunities arise. If we are not successful in integrating acquisitions, we may not realize the operating results we anticipated at the time of acquisition. In addition, industry downturns in the markets the acquired companies serve and general economic conditions may adversely affect our financial results. Future acquisitions may require us to incur additional debt and contingent liabilities, which may materially and adversely affect our business, operating results, cash flows and financial condition. The acquisition and integration of businesses involve a number of risks, including:

| • | Doing business in industries outside our present material handling business; |

| • | Difficulties in integrating operations and systems, and matching the business culture of the acquired business with our culture; |

| • | Difficulties in the assimilation and retention of employees; |

| • | Difficulties in retaining customers and integrating customer bases; |

| • | Diversion of management’s attention from existing operations due to the integration of acquired businesses; and |

| • | Assumption of unexpected liabilities. |

We may, in a bid to conserve cash for operations, undertake acquisitions that would be financed in part through public offerings or private placements of debt or equity securities, or other arrangements. Such acquisition financing could result in a decrease of our ratio of earnings to fixed charges and adversely affect other leverage measures. If we were to undertake an acquisition by issuing equity securities, the issued securities may have a dilutive effect on the interests of the holders of our common shares.

Fluctuations in raw material costs and availability

To manufacture our products we purchase a variety of raw materials and components. These consist principally of rolled bar, plate and extruded specialty steel products, unfinished castings and forgings, hydraulic

10

Table of Contents

cylinders and motors and various hardware items. The price of steel is particularly significant to our manufacturing costs since most of our products are manufactured using specialty steel as a primary raw material and specialty steel based components as purchased parts. As a result, we are exposed to increases in the market prices of raw materials and components. We may not be able to mitigate these increases by changing the selling prices of our products or through other means.

We may also experience shortages of raw materials and purchased parts, which in certain cases are provided by a limited number of suppliers. Shortages may require us to curtail production, spend additional money to expedite product to our manufacturing locations, or to devote additional financial resources to maintaining inventories of raw materials and purchased parts in excess of our normal requirements.

Underfunded benefit plans

As of January 31, 2012, our accumulated postretirement benefit obligation under our postretirement benefit plan in the U.S., which is not funded, was $8.7 million. Fluctuations in the discount rate, health care cost trends, retirement and life expectancy rates and changes to participant contributions could cause our obligation under this plan to increase substantially. At some time in the future we may have to make significant cash payments to fund this plan, which would reduce the cash available for our business.

As of January 31, 2012, our projected benefit obligation under our defined benefit pension plans was $8.4 million which exceeds the fair value of plan assets of $8.1 million. The underfunding in our defined benefit pension plans is subject to fluctuations in the discount rate and financial markets that cause the valuation of assets to change. If our cash contributions are insufficient to adequately fund the plans to cover our future obligations, the performance of the pension plan assets do not meet our expectations or assumptions are modified, our contributions could be materially higher than we expect. This would reduce the cash available for our business.

We expect any required cash payments to our plans will be made from future cash flows from operations. Changes in U.S. or foreign laws governing these plans could require us to make additional contributions. Changes to generally accepted accounting principles in the United States could require the recording of additional costs related to these plans.

| Item 1B. | Unresolved Staff Comments |

None.

11

Table of Contents

| Item 2. | Properties |

We own and lease various types of properties located throughout the world. Our corporate office is located in Fairview, Oregon. We generally consider the productive capacity of our manufacturing facilities to be adequate and suitable to meet our requirements. Our primary locations are presented below:

Location | Primary Activity | Approximate Square Footage | Status | |||||||

AMERICAS | ||||||||||

Springfield, Ohio | Manufacturing | 200,000 | Owned | |||||||

Guelph, Ontario, Canada | Manufacturing | 125,000 | Owned | |||||||

Fairview, Oregon | Manufacturing | 112,000 | Owned | |||||||

Toronto, Ontario, Canada | Manufacturing | 73,000 | Leased | |||||||

Woodinville, Washington | Manufacturing | 68,000 | Leased | |||||||

Warner Robins, Georgia | Manufacturing | 65,000 | Owned | |||||||

Findlay, Ohio | Manufacturing | 52,000 | Owned | |||||||

Fairview, Oregon | Headquarters | 43,000 | Owned | |||||||

Lake Elsinore, California | Manufacturing | 24,000 | Leased | |||||||

Santos, Brazil** | Distribution | 15,000 | Leased | |||||||

EUROPE | ||||||||||

Almere, The Netherlands* | Distribution | 162,000 | Owned | |||||||

Verona, Italy | Manufacturing | 74,000 | Leased | |||||||

Manchester, England | Manufacturing | 44,000 | Owned | |||||||

Brescia, Italy | Manufacturing | 19,000 | Owned | |||||||

Dusseldorf, Germany | Sales | 3,000 | Leased | |||||||

Ancenis, France | Sales | 2,000 | Leased | |||||||

Vantaa, Finland | Sales | 500 | Leased | |||||||

ASIA PACIFIC | ||||||||||

Brisbane, Australia | Manufacturing | 46,000 | Leased | |||||||

Osaka, Japan | Sales/Distribution | 24,000 | Owned | |||||||

Inchon, Korea | Manufacturing | 12,000 | Owned | |||||||

Auckland, New Zealand | Sales/Distribution | 9,000 | Leased | |||||||

Johannesburg, South Africa | Sales | 9,000 | Leased | |||||||

Pune, India | Sales | 120 | Leased | |||||||

CHINA | ||||||||||

Xiamen, China | Manufacturing | 189,000 | Leased | |||||||

Hebei, China | Manufacturing | 88,000 | Leased | |||||||

Xiamen, China | Manufacturing | 87,000 | Leased | |||||||

Hebei, China | Manufacturing | 65,000 | Leased | |||||||

| * | Location is currently available for sale. |

| ** | Acquired March 2012 |

| Item 3. | Legal Proceedings |

Neither Cascade nor any of our subsidiaries are involved in any material pending legal proceedings. We believe we are adequately insured against product liability, personal injury and property damage claims, which may occasionally arise.

| Item 4. | Mine SafetyDisclosures |

Not applicable.

12

Table of Contents

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

As of March 8, 2012, there were 143 shareholders of record of Cascade’s common stock including blocks of shares held by various depositories. It is our belief that when the shares held by the depositories are attributed to the beneficial owners, the total exceeds 2,000.

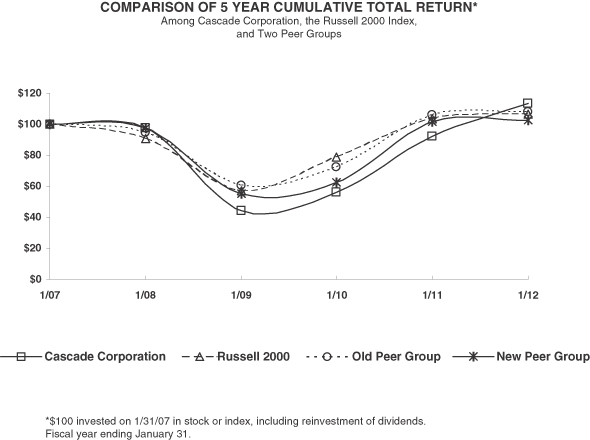

Performance Graph

The following graph compares the annual percentage change in the cumulative shareholder return on our common stock with the cumulative total return of the Russell 2000 Index and an industry group of peer companies, in each case assuming investment of $100 on January 31, 2007, and reinvestment of dividends. The stock price performance shown in the graph below is not necessarily indicative of future stock price performance. Notwithstanding anything to the contrary set forth in any of our filings under the Securities Act of 1933 or the Securities Exchange Act of 1934, the stock performance graph shall not be incorporated by reference into any such filings and shall not otherwise be deemed filed under such acts.

Old peer group is a historical group of companies which we share similar economic characteristics with and includes the following companies: Actuant Corporation, Alamo Group Inc., American Railcar Industries, Inc., Ampco-Pittsburgh Corporation, Astec Industries, Inc., Blount International Inc., Columbus-McKinnon Corporation, Foster (LB) Corporation, IDEX Corporation, Miller Industries Inc. and The Greenbrier Companies.

13

Table of Contents

New peer group is a group of companies, with characteristics similar to ours, that are used to evaluate our executive compensation and comprises the following companies: Accuride, Actuant Corporation, Alamo Group Inc., Altra Holdings Inc., American Railcar Industries, Inc., Astec Industries, Inc., Blount International Inc., Columbus-McKinnon Corporation, Foster (LB) Corporation, The Greenbrier Companies and Titan International Inc.

Market Information

The high and low sales prices of our common stock based on intra-day prices on the New York Stock Exchange for each quarter during the last two fiscal years were as follows:

| Year Ended January 31 | ||||||||||||||||

| 2012 | 2011 | |||||||||||||||

| High | Low | High | Low | |||||||||||||

First quarter | $ | 52.53 | $ | 42.15 | $ | 40.35 | $ | 25.33 | ||||||||

Second quarter | 55.67 | 37.90 | 43.36 | 27.34 | ||||||||||||

Third quarter | 51.30 | 31.30 | 40.65 | 27.55 | ||||||||||||

Fourth quarter | 58.33 | 37.30 | 51.82 | 34.65 | ||||||||||||

Dividends

The cash dividends declared during each quarter of the last two fiscal years were as follows:

| Year Ended January 31 | ||||||||

| 2012 | 2011 | |||||||

First quarter | $ | 0.20 | $ | 0.02 | ||||

Second quarter | 0.20 | 0.05 | ||||||

Third quarter | 0.25 | 0.10 | ||||||

Fourth quarter | 0.25 | 0.10 | ||||||

|

|

|

| |||||

| $ | 0.90 | $ | 0.27 | |||||

|

|

|

| |||||

Stock Exchange Listing and Transfer Agent

Cascade’s stock is traded on the New York Stock Exchange under the symbol CASC.

Cascade’s registrar and transfer agent is Computershare, P.O. Box 358015, Pittsburgh, P.A., 15252, (877) 268-3023.

Equity Compensation Plan Information

For information on our equity compensation plans, see Items 8 and 12 of this report.

14

Table of Contents

| Item 6. | Selected Financial Data |

The following selected financial data should be read in conjunction with our consolidated financial statements and accompanying notes contained in Item 8 of this Form 10-K.

| Year Ended January 31 | ||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| (In thousands, except per share amounts and employees) | ||||||||||||||||||||

Income statement data: | ||||||||||||||||||||

Net sales | $ | 535,767 | $ | 409,858 | $ | 314,353 | $ | 534,172 | $ | 558,073 | ||||||||||

Operating income (loss)(1) | $ | 87,415 | $ | 42,276 | $ | (31,494 | ) | $ | 11,477 | $ | 95,613 | |||||||||

Net income (loss)(2) | $ | 63,046 | $ | 21,406 | $ | (38,649 | ) | $ | 1,267 | $ | 60,147 | |||||||||

Cash flow data: | ||||||||||||||||||||

Cash flows from operating activities | $ | 54,219 | $ | 27,778 | $ | 45,413 | $ | 41,086 | $ | 53,326 | ||||||||||

Cash flows from investing activities | $ | (13,415 | ) | $ | (4,790 | ) | $ | (5,732 | ) | $ | (16,134 | ) | $ | (31,627 | ) | |||||

Cash flows from financing activities | $ | (45,357 | ) | $ | (20,930 | ) | $ | (44,659 | ) | $ | (20,382 | ) | $ | (33,432 | ) | |||||

Free cash flow(3) | $ | 40,802 | $ | 21,731 | $ | 39,479 | $ | 24,377 | $ | 30,518 | ||||||||||

Stock information: | ||||||||||||||||||||

Basic earnings (loss) per share(2) | $ | 5.74 | $ | 1.97 | $ | (3.57 | ) | $ | 0.12 | $ | 5.08 | |||||||||

Diluted earnings (loss) per share(2) | $ | 5.58 | $ | 1.93 | $ | (3.57 | ) | $ | 0.11 | $ | 4.88 | |||||||||

Dividends declared | $ | 0.90 | $ | 0.27 | $ | 0.12 | $ | 0.78 | $ | 0.70 | ||||||||||

Balance sheet information: | ||||||||||||||||||||

Cash and cash equivalents | $ | 24,928 | $ | 25,037 | $ | 20,201 | $ | 31,185 | $ | 21,223 | ||||||||||

Inventories | $ | 86,660 | $ | 67,041 | $ | 63,466 | $ | 90,806 | $ | 85,049 | ||||||||||

Working capital(4) | $ | 155,569 | $ | 135,124 | $ | 112,378 | $ | 161,718 | $ | 151,971 | ||||||||||

Property, plant and equipment, net | $ | 71,439 | $ | 66,978 | $ | 73,408 | $ | 93,826 | $ | 98,350 | ||||||||||

Total assets | $ | 394,559 | $ | 359,179 | $ | 341,931 | $ | 397,583 | $ | 462,500 | ||||||||||

Total debt | $ | 5,639 | $ | 42,337 | $ | 59,416 | $ | 102,763 | $ | 110,716 | ||||||||||

Shareholders’ equity | $ | 310,727 | $ | 248,556 | $ | 215,762 | $ | 236,967 | $ | 268,025 | ||||||||||

Other: | ||||||||||||||||||||

Capital expenditures | $ | 13,417 | $ | 6,047 | $ | 5,934 | $ | 16,709 | $ | 22,808 | ||||||||||

Depreciation | $ | 9,826 | $ | 9,980 | $ | 11,893 | $ | 13,801 | $ | 13,898 | ||||||||||

Amortization | $ | 156 | $ | 156 | $ | 403 | $ | 2,519 | $ | 3,214 | ||||||||||

Share-based compensation expense(5) | $ | 2,486 | $ | 2,654 | $ | 3,562 | $ | 4,421 | $ | 4,451 | ||||||||||

Interest expense, net of interest income | $ | 542 | $ | 1,803 | $ | 1,561 | $ | 3,475 | $ | 3,315 | ||||||||||

Diluted weighted average shares outstanding | 11,293 | 11,104 | 10,816 | 11,077 | 12,333 | |||||||||||||||

Number of employees | 1,900 | 1,800 | 1,700 | 2,100 | 2,400 | |||||||||||||||

| (1) | Amount includes $5,171 of net flood insurance proceeds in 2012, $5,145 of flood expense in 2011, $30,001 of restructuring costs in 2010, a $46,376 asset impairment charge in 2009 and a $15,977 insurance litigation recovery in 2008. |

| (2) | Amount includes after-tax net flood insurance proceeds of $3,620 ($0.32 per diluted share) in 2012, after-tax flood expense of $3,601 ($0.32 per diluted share) in 2011, an after-tax restructuring charge of $29,519 ($2.73 per diluted share) in 2010, an after-tax asset impairment charge in 2009 of $31,576 ($2.85 per diluted share) and an after-tax insurance litigation recovery in 2008 of $10,026 ($0.81 per diluted share). |

| (3) | A non-GAAP measure defined as cash flow from operating activities less capital expenditures. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (Item 7) for additional information on free cash flow. |

| (4) | Defined as current assets less current liabilities. |

| (5) | See Notes 2 and 13 to the Consolidated Financial Statements for additional information on share-based compensation. |

15

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following is a discussion and analysis of certain significant factors that have affected our financial condition as of January 31, 2012, and the results of operations and cash flows for the fiscal years ended January 31, 2012, 2011 and 2010. This information should be read in conjunction with our consolidated financial statements and notes thereto under Item 8, “Financial Statements and Supplementary Data” of this report.

OVERVIEW

Our businesses globally manufacture and distribute material handling load engagement products primarily for the lift truck industry and to a lesser extent the construction industry. We operate our business in four geographic segments: Americas, Europe, Asia Pacific and China. The Americas region includes activity in North, Central and South America. A further discussion of our business is contained in Item 1, “Business,” of this report.

RECENT TRENDS AND DEVELOPMENTS AFFECTING OUR RESULTS

Global Economic and Lift Truck Market Outlook

Over the last couple of years, we experienced the effects of the global recovery in the lift truck market, which led to increased sales and improved margins in most regions. However, during the later half of fiscal 2012 we started to experience a slower rate of growth in markets globally.

We expect the lift truck market for the Americas and Asia Pacific regions to experience modest growth during fiscal 2013. The outlook for Europe in fiscal 2013 appears to be stable, however, events surrounding the European debt crisis and other economic factors in Europe could have a dramatic affect on the market. China is currently experiencing a slowdown of lift truck shipments, which could result in lower lift truck shipment levels during fiscal 2013 than was experienced in fiscal 2012. It is difficult to predict the length and severity of the current slowdown in China.

The following table shows the year-over-year percent increase in global lift truck shipments over the past two fiscal years.

| Lift Truck Shipments | ||||||||||

| Fiscal 2012 vs 2011 | Fiscal 2011 vs 2010 | |||||||||

Americas | 41 | % | 3 | % | ||||||

Europe | 35 | % | 19 | % | ||||||

Asia Pacific | 22 | % | 30 | % | ||||||

China | 20 | % | 68 | % | ||||||

Global | 28 | % | 36 | % | ||||||

Currently, the lift truck market is the only direct economic or industrial indicator we have available for our markets. While results across this market do not correlate exactly with our business levels over the short term, since customers in the various end markets use our products to differing degrees, it does give us a good indication of trends over the year.

Additional information on lift truck industry trends can be found at www.cascorp.com/investor/industrytrends. This website address is intended to provide an inactive, textual reference only. The information at this website is not part of this Form 10-K and is not incorporated by reference.

Use of Cash

In recent years we used excess cash to reduce our outstanding debt balance. At January 31, 2012 our cash balance was $25 million and our outstanding debt balance was $6 million. Our revolving line of credit is expected to be completely paid off during the first quarter of fiscal 2013, leaving only our debt in Japan

16

Table of Contents

remaining. Given our liquidity position we are evaluating various growth opportunities, both within and outside the lift truck and construction equipment industries. Our board of directors will also continue to review our dividend policy periodically, in light of our cash flows and operating results.

COMPARISON OF FISCAL 2012, 2011 and 2010

Executive Summary

| Year Ended January 31 | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| (In thousands, except per share amounts) | ||||||||||||

Net sales | $ | 535,767 | $ | 409,858 | $ | 314,353 | ||||||

Gross profit % | 32 | % | 30 | % | 23 | % | ||||||

Operating income (loss) | $ | 87,415 | $ | 42,276 | $ | (31,494 | ) | |||||

Operating income % | 16 | % | 10 | % | (10 | %) | ||||||

Income (loss) before taxes | $ | 85,820 | $ | 39,535 | $ | (33,498 | ) | |||||

Provision for income taxes | $ | 22,774 | $ | 18,129 | $ | 5,151 | ||||||

Effective tax rate | 27 | % | 46 | % | (15 | %) | ||||||

Net income (loss) | $ | 63,046 | $ | 21,406 | $ | (38,649 | ) | |||||

Diluted earnings (loss) per share | $ | 5.58 | $ | 1.93 | $ | (3.57 | ) | |||||

The following summarizes consolidated financial results. All percentage comparisons to prior years exclude the impact of foreign currencies:

| • | Consolidated net sales increased 27% in fiscal 2012 and 29% in fiscal 2011 primarily as a result of higher sales volumes in all regions due to a stronger global lift truck market. |

| • | Our consolidated gross profit percentages in fiscal 2012 and 2011 reflect the benefits of cost absorption due to increased sales volumes and cost cutting measures implemented prior to fiscal 2011. The gross profit for fiscal 2011 was reduced by a charge of $2.2 million for inventory write-offs in Australia due to extensive flooding in the region during January 2011. |

| • | The lower gross profit percentage in fiscal 2010 was primarily a result of operational costs associated with our European restructuring, including costs associated with operational disruptions and inventory write-offs, and unabsorbed costs due to lower sales volumes, particularly in Europe and North America. |

| • | In January 2011, our facility in Australia was severely damaged by flooding. Our results were impacted, by this flood, during fiscal 2012 and 2011 as follows (in thousands): |

| Fiscal 2012 | Fiscal 2011 | |||||||

Insurance proceeds | $ | (8,081 | ) | $ | — | |||

Inventory write down (recovery), net | (413 | ) | 2,167 | |||||

Fixed asset write down (recovery), net | (299 | ) | 2,451 | |||||

Other flood related costs | 3,622 | 527 | ||||||

|

|

|

| |||||

Pre-tax net expense (recovery) | (5,171 | ) | 5,145 | |||||

Tax effect | (1,551 | ) | 1,544 | |||||

|

|

|

| |||||

After tax net expense (recovery) | $ | (3,620 | ) | $ | 3,601 | |||

|

|

|

| |||||

Net expense (recovery) per diluted share | $ | (0.32 | ) | $ | 0.32 | |||

|

|

|

| |||||

| • | We incurred European restructuring costs of $1.2 million and $30.0 million during fiscal 2011 and 2010, respectively. These costs related to closing certain European sales offices and shutting down production activities at our facilities located in France, Germany and The Netherlands. |

17

Table of Contents

| • | During fiscal 2010, we recorded a $1.3 million environmental charge primarily related to our Springfield, Ohio location. This expense was the result of formalizing a revised remediation plan with the Ohio Environmental Protection Agency, which will require additional cleanup activities related to groundwater contamination through fiscal 2019. |

| • | The effective tax rate of 27% in fiscal 2012 was lower than 2011 due to the release of $3.6 million of tax valuation allowances in The Netherlands. This release was due to improved financial performance in The Netherlands resulting from the restructuring of our manufacturing operations and sales agent model and the financial results of our parts business. |

| • | The effective tax rate of 46% in fiscal 2011 was higher due to our inability to recognize a tax benefit on losses incurred in several European countries and taxes on foreign dividends related to the repatriation of cash to the U.S. |

| • | The effective tax rate of (15%) in fiscal 2010 was impacted by our inability to recognize a tax benefit on losses incurred in several European countries and taxes due in countries where we generated income. |

Americas

| Year Ended January 31 | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| (In thousands) | ||||||||||||

Net sales | $ | 280,366 | $ | 206,079 | $ | 154,654 | ||||||

Transfers between areas | 27,826 | 24,611 | 15,086 | |||||||||

|

|

|

|

|

| |||||||

Net sales and transfers | 308,192 | 230,690 | 169,740 | |||||||||

Cost of goods sold | 213,656 | 160,862 | 120,933 | |||||||||

|

|

|

|

|

| |||||||

Gross profit | 94,536 | 69,828 | 48,807 | |||||||||

Gross profit % | 31 | % | 30 | % | 29 | % | ||||||

Selling and administrative | 48,924 | 43,785 | 41,251 | |||||||||

|

|

|

|

|

| |||||||

Operating income | $ | 45,612 | $ | 26,043 | $ | 7,556 | ||||||

|

|

|

|

|

| |||||||

Operating income % | 15 | % | 11 | % | 4 | % | ||||||

Details of the change in net sales compared to the prior year are as follows (in thousands):

| Fiscal 2012 vs 2011 | Fiscal 2011 vs 2010 | |||||||||||||||

| Change | Change % | Change | Change % | |||||||||||||

Net sales change | $ | 73,037 | 35 | % | $ | 49,728 | 32 | % | ||||||||

Foreign currency change | 1,250 | 1 | % | 1,697 | 1 | % | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | $ | 74,287 | 36 | % | $ | 51,425 | 33 | % | ||||||||

|

|

|

|

|

|

|

| |||||||||

The following summarizes financial results for the Americas. All percentage comparisons to prior years exclude the impact of foreign currencies:

| • | Net sales increased 35% in fiscal 2012 and 32% in fiscal 2011 primarily due to higher sales volumes as a result of improving economic conditions. |

| • | Shipments of product to other Cascade locations increased in fiscal 2012 and 2011 due to increased customer demand globally. |

| • | Our gross profit percentage steadily increased during the three year period ended January 31, 2012 due to improved cost absorption as a result of higher sales volumes. |

| • | During fiscal 2012, selling and administrative costs increased 11% primarily due to additional warranty expense, consulting fees and personnel costs. |

18

Table of Contents

| • | Selling and administrative costs increased 5% in fiscal 2011 primarily due to increased executive incentive compensation, sales commissions, reinstatement of previously frozen salary increases and other personnel costs as a result of improved financial performance. |

| • | During fiscal 2010, we recorded a $1.3 million environmental charge, in selling and administrative costs, primarily related to our Springfield, Ohio location. This expense was the result of formalizing a revised remediation plan with the Ohio Environmental Protection Agency, which required additional cleanup activities related to groundwater contamination. |

Europe

| Year Ended January 31 | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| (In thousands) | ||||||||||||

Net sales | $ | 109,551 | $ | 88,124 | $ | 81,068 | ||||||

Transfers between areas | 992 | 525 | 3,648 | |||||||||

|

|

|

|

|

| |||||||

Net sales and transfers | 110,543 | 88,649 | 84,716 | |||||||||

Cost of goods sold | 87,611 | 76,563 | 90,021 | |||||||||

|

|

|

|

|

| |||||||

Gross profit (loss) | 22,932 | 12,086 | (5,305 | ) | ||||||||

Gross profit (loss) % | 21 | % | 14 | % | (6 | %) | ||||||

Selling and administrative | 18,491 | 17,932 | 19,695 | |||||||||

European restructuring costs | 25 | 1,237 | 30,001 | |||||||||

|

|

|

|

|

| |||||||

Operating income (loss) | $ | 4,416 | $ | (7,083 | ) | $ | (55,001 | ) | ||||

|

|

|

|

|

| |||||||

Operating income (loss) % | 4 | % | (8 | %) | (65 | %) | ||||||

Details of the change in net sales compared to prior years are as follows (in thousands):

| Fiscal 2012 vs 2011 | Fiscal 2011 vs 2010 | |||||||||||||||

| Change | Change % | Change | Change % | |||||||||||||

Net sales change | $ | 16,298 | 18 | % | $ | 11,310 | 14 | % | ||||||||

Foreign currency change | 5,129 | 6 | % | (4,254 | ) | (5 | %) | |||||||||

|

|

|

|

|

|

|

| |||||||||

Total | $ | 21,427 | 24 | % | $ | 7,056 | 9 | % | ||||||||

|

|

|

|

|

|

|

| |||||||||

The following summarizes financial results for Europe. All percentage comparisons to prior years exclude the impact of foreign currencies:

| • | Net sales increased 18% in fiscal 2012 and 14% in fiscal 2011 primarily due to higher sales volumes as a result of a stronger lift truck market. |

| • | During fiscal 2012, the increase in our gross profit percentage was a result of increased cost absorption as a result of higher sales volumes, a continuing shift in sourcing more products from China, sales price increases for certain products and continuing efforts to reduce our overall cost structure. Our gross profit percentage improvement in fiscal 2011 was due to operational efficiencies as a result of significant restructuring activities and sales price increases. The gross loss in fiscal 2010 was due to costs associated with our significant European restructuring activities, including operational disruption costs and inventory write-offs. In addition, significantly lower sales volumes resulted in unabsorbed overhead costs, as all facilities operated under reduced work schedules during fiscal 2010. |

| • | Selling and administrative costs decreased 2% in fiscal 2012 and 5% in fiscal 2011 primarily due to lower personnel costs, as a result of headcount reductions made as part of our European restructuring activities. |

| • | During fiscal 2011, we incurred $1.2 million in restructuring costs primarily related to closure of certain sales offices and a building write-down in Germany. Restructuring costs of $30 million incurred |

19

Table of Contents

during fiscal 2010 were primarily a result of closing production facilities in Germany ($10.9 million), The Netherlands ($13.2 million) and France ($5.3 million). These costs included severance costs of $17.3 million, fixed asset write-downs of $9 million, costs for movement of equipment and facility shutdowns of $2.6 million and other restructuring costs of $1.1 million. |

Asia Pacific

| Year Ended January 31 | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| (In thousands) | ||||||||||||

Net sales | $ | 77,710 | $ | 59,676 | $ | 44,102 | ||||||

Transfers between areas | 127 | 128 | 147 | |||||||||

|

|

|

|

|

| |||||||

Net sales and transfers | 77,837 | 59,804 | 44,249 | |||||||||

Cost of goods sold | 53,896 | 45,797 | 32,972 | |||||||||

|

|

|

|

|

| |||||||

Gross profit | 23,941 | 14,007 | 11,277 | |||||||||

Gross profit % | 31 | % | 23 | % | 25 | % | ||||||

Selling and administrative | 11,216 | 9,538 | 7,487 | |||||||||

Australia flood costs (proceeds), net | (3,137 | ) | 2,978 | — | ||||||||

|

|

|

|

|

| |||||||

Operating income | $ | 15,862 | $ | 1,491 | $ | 3,790 | ||||||

|

|

|

|

|

| |||||||

Operating income % | 20 | % | 2 | % | 9 | % | ||||||

Details of the change in net sales compared to prior years are as follows (in thousands):

| Fiscal 2012 vs 2011 | Fiscal 2011 vs 2010 | |||||||||||||||

| Change | Change % | Change | Change % | |||||||||||||

Net sales change | $ | 11,397 | 19 | % | $ | 9,910 | 22 | % | ||||||||

Foreign currency change | 6,637 | 11 | % | 5,664 | 13 | % | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | $ | 18,034 | 30 | % | $ | 15,574 | 35 | % | ||||||||

|

|

|

|

|

|

|

| |||||||||

The following summarizes the financial results for Asia Pacific. All percentage comparisons to prior years exclude the impact of foreign currencies:

| • | Net sales increased 19% in fiscal 2012 and 22% in fiscal 2011 due to higher sales volumes as a result of strong lift truck markets. |

| • | Our gross profit percentage increased in fiscal 2012 primarily as a result of net flood insurance proceeds we received during fiscal 2012 and inventory write-offs in fiscal 2011 as a result of the Australia flood. The impact of the Australia flood on gross profit for fiscal 2012 and 2011 was as follows (in thousands): |

| Fiscal 2012 | Fiscal 2011 | |||||||

Gross profit | $ | 23,941 | $ | 14,007 | ||||

Flood costs (proceeds), net | (2,034 | ) | 2,167 | |||||

|

|

|

| |||||

Gross profit without flood costs (proceeds) | 21,907 | 16,174 | ||||||

|

|

|

| |||||

Gross profit % without flood costs (proceeds) | 28 | % | 27 | % | ||||

| • | Selling and administrative costs increased 7% in fiscal 2012 primarily due to higher personnel, warranty and professional fees. During fiscal 2011, selling and administrative costs increased 14% as a result of higher selling and personnel costs. |

20

Table of Contents

| • | In January 2011, our facility in Brisbane, Australia was severely damaged by flooding. During fiscal 2012 and 2011 our results in Asia Pacific were impacted by this flood as follows (in thousands): |

| Fiscal 2012 | Fiscal 2011 | |||||||

Operating income (loss) | $ | 15,862 | $ | 1,491 | ||||

Insurance proceeds | (8,081 | ) | — | |||||

Inventory write down (recovery), net | (413 | ) | 2,167 | |||||

Fixed asset write down (recovery), net | (299 | ) | 2,451 | |||||

Other flood related costs | 3,622 | 527 | ||||||

|

|

|

| |||||

Operating income without flood impact | $ | 10,691 | $ | 6,636 | ||||

|

|

|

| |||||

Operating income without flood impact % | 14 | % | 11 | % | ||||

China

| Year Ended January 31 | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| (In thousands) | ||||||||||||

Net sales | $ | 68,140 | $ | 55,979 | $ | 34,529 | ||||||

Transfers between areas | 32,569 | 23,517 | 10,549 | |||||||||

|

|

|

|

|

| |||||||

Net sales and transfers | 100,709 | 79,496 | 45,078 | |||||||||

Cost of goods sold | 72,831 | 52,729 | 28,787 | |||||||||

|

|

|

|

|

| |||||||

Gross profit | 27,878 | 26,767 | 16,291 | |||||||||

Gross profit % | 28 | % | 34 | % | 36 | % | ||||||

Selling and administrative | 6,353 | 4,942 | 4,130 | |||||||||

|

|

|

|

|

| |||||||

Operating income | $ | 21,525 | $ | 21,825 | $ | 12,161 | ||||||

|

|

|

|

|

| |||||||

Operating income % | 21 | % | 27 | % | 27 | % | ||||||

Details of the change in net sales compared to prior years are as follows (in thousands):

| Fiscal 2012 vs 2011 | Fiscal 2011 vs 2010 | |||||||||||||||

| Change | Change % | Change | Change % | |||||||||||||

Net sales change | $ | 9,062 | 16 | % | $ | 20,779 | 60 | % | ||||||||

Foreign currency change | 3,099 | 6 | % | 671 | 2 | % | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | $ | 12,161 | 22 | % | $ | 21,450 | 62 | % | ||||||||

|

|

|

|

|

|

|

| |||||||||

The following summarizes the financial results for China. All percentage comparisons to prior years exclude the impact of foreign currencies:

| • | Net sales increased in fiscal 2012 and fiscal 2011 primarily due to higher sales volumes as a result of growth in the Chinese economy and a strong lift truck market. The rate of growth has slowed in fiscal 2012 compared to 2011 due to a general slowdown in the Chinese economy which is also impacting lift truck shipments. |

| • | Transfers to other Cascade locations increased in fiscal 2012 and 2011 due to higher customer demand in Europe and Asia Pacific. |

| • | During fiscal 2012, our gross profit percentage decreased primarily due to strategic pricing reductions, product mix and higher overhead costs. Our gross profit percentage decrease in fiscal 2011 was due to changes in product mix and higher intercompany transfers mostly to the Europe and Asia Pacific regions, which carry lower gross margins. |

21

Table of Contents

| • | Selling and administrative costs increased 23% in fiscal 2012 primarily due to higher local taxes, personnel costs and selling expense. During fiscal 2011, selling and administrative costs increased 18% due to higher research and development costs and increased incentive and personnel costs as a result of improved financial performance. |

Non-Operating Items

The following are financial highlights for non-operating items:

| • | Interest expense decreased during fiscal 2012 as a result of paying down our debt and lower interest rates due to an amended loan agreement. |

| • | During fiscal 2012, foreign currency losses remained consistent as foreign currency rate trends were comparable to fiscal 2011. Foreign currency losses increased $0.5 million in fiscal 2011 as a result of greater volatility in foreign currency rates compared to fiscal 2010. |

| • | Our effective tax rate for fiscal 2012 was 27% primarily due to the release of a $3.6 million tax valuation allowance on deferred tax assets in The Netherlands. |

| • | Our effective tax rate for fiscal 2011 was 46% primarily due to recording of additional valuation allowances related to losses in Europe for which we were unable to realize tax benefits. |

| • | Our effective tax rate for fiscal 2010 was (15%) a result of our inability to realize a tax benefit for losses incurred in several European countries and taxes due in countries where we were generating income. |

| • | We repatriated cash to the U.S. and Canada from China of $17.1 million, $7.1 million and $23.4 million during fiscal 2012, 2011 and 2010, respectively. The repatriation did not result in additional cash taxes due to foreign tax credits. |

| • | Our debt balance at January 31, 2012 was $5.6 million. We reduced our outstanding debt by $36.7 million in fiscal 2012, $17.1 million in fiscal 2011 and $43.3 million in fiscal 2010. |

22

Table of Contents

Fourth Quarter Results

| Three Months Ended January 31 | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| (In thousands, except per share amounts) | ||||||||||||

Net sales | $ | 125,924 | $ | 110,348 | $ | 80,572 | ||||||

Cost of goods sold | 89,504 | 78,686 | 62,179 | |||||||||

|

|

|

|

|

| |||||||

Gross profit | 36,420 | 31,662 | 18,393 | |||||||||

Gross profit % | 29 | % | 29 | % | 23 | % | ||||||

Selling and administrative expenses | 20,759 | 20,545 | 17,891 | |||||||||

Environmental | — | — | 1,255 | |||||||||

Australia flood costs (proceeds), net | (2,871 | ) | 2,978 | — | ||||||||

European restructuring costs | — | 1,222 | 12,121 | |||||||||

|

|

|

|

|

| |||||||

Operating income (loss) | 18,532 | 6,917 | (12,874 | ) | ||||||||

Operating income (loss) % | 15 | % | 6 | % | (16 | %) | ||||||

Interest expense, net | 65 | 289 | 421 | |||||||||

Foreign currency loss, net | 16 | 186 | 159 | |||||||||

|

|

|

|

|

| |||||||

Income (loss) before provision for income taxes | 18,451 | 6,442 | (13,454 | ) | ||||||||

Provision for income taxes | 5,255 | 2,718 | 976 | |||||||||

|

|

|

|

|

| |||||||

Net income (loss) | $ | 13,196 | $ | 3,724 | $ | (14,430 | ) | |||||

|

|

|

|

|

| |||||||

Diluted earnings (loss) per share | $ | 1.16 | $ | 0.33 | $ | (1.33 | ) | |||||

|

|

|

|

|

| |||||||

Operating income (loss) by region: | ||||||||||||

Americas | $ | 9,438 | $ | 7,423 | $ | 1,403 | ||||||

Europe | 200 | (2,423 | ) | (18,750 | ) | |||||||

Asia Pacific | 5,045 | (3,458 | ) | 701 | ||||||||

China | 3,849 | 5,375 | 3,772 | |||||||||

|

|

|

|

|

| |||||||

| $ | 18,532 | $ | 6,917 | $ | (12,874 | ) | ||||||

|

|

|

|

|

| |||||||

The following summarizes the financial results for the fourth quarter. All percentage comparisons to prior years exclude the impact of foreign currencies:

| • | During the fourth quarter of fiscal 2012, our consolidated net sales increased 13% compared to an increase of 17% in global lift truck shipments. Our increase in sales was primarily due to higher sales volumes as a result of favorable economic conditions and a strong lift truck market in the regions of the Americas, Europe and Asia Pacific. Consolidated net sales increased 36% in 2011 primarily due to higher sales volumes as a result of improved economic conditions and a stronger global lift truck market Global lift truck shipments were up 38% in 2011 compared to the prior year. |

| • | Our consolidated gross profit percentage during fiscal 2012 was impacted by strategic pricing reductions in China, a higher percentage of lower margin products sold and increased overhead costs. Our consolidated gross profit percentage increased in fiscal 2011 primarily as a result of improved cost absorption due to increased sales volumes and the benefit of cost cutting measures implemented during fiscal 2010. This increase was partially offset by a charge of $2.2 million for inventory write-offs in Australia due to the flooding. In fiscal 2010, our consolidated gross profit percentage was lower primarily as a result of operational costs associated with our European restructuring, including considerable operational disruption costs and inventory writeoffs. |

| • | During fiscal 2011, selling and administrative expenses increased 8% due primarily to increased sales commissions, higher executive incentive compensation, the reinstatement of previously frozen salary increases and other personnel costs as a result of improved financial performance in the current year. |

23

Table of Contents

Selling and administrative expenses in fiscal 2010 included a $1.3 million environmental charge primarily related to our Springfield, Ohio location. This expense was the result of formalizing a revised remediation plan with the Ohio Environmental Protection Agency, which required additional cleanup activities related to groundwater contamination. |

| • | During fiscal 2012, we continued to incur costs and receive insurance proceeds, relating to the flood in Australia. Our results were impacted during the fourth quarter of fiscal 2012 and 2011 as follows (in thousands): |

| Fiscal 2012 | Fiscal 2011 | |||||||

Insurance proceeds | $ | (3,027 | ) | $ | — | |||

Inventory write down | — | 2,167 | ||||||

Fixed asset write down | — | 2,451 | ||||||

Other flood related costs | 156 | 527 | ||||||

|

|

|

| |||||

Net expense (recovery) | $ | (2,871 | ) | $ | 5,145 | |||

|

|

|

| |||||

| • | We incurred restructuring costs of $1.2 million in fiscal 2011 and $12.1 million in fiscal 2010, primarily related to the closure of certain European sales offices and shutting down production at our fork facility in Hagen, Germany. |

| • | The income tax rates in fiscal 2012, 2011 and 2010 were 28%, 42% and (7%), respectively. The fiscal 2011 and 2010 rates were due to our inability to realize a tax benefit in several European countries where we incurred losses. |

CASH FLOWS

Free Cash Flow

Free cash flow, a non-GAAP measure, is defined as cash flows from operating activities less capital expenditures. Free cash flow is considered a liquidity measure and provides useful information to management and investors about the amount of cash generated after capital expenditures, which can then be used for strategic opportunities including, among others, investing in our business, making strategic acquisitions and strengthening our balance sheet. A limitation of free cash flow is that it does not represent the total increase or decrease in the cash balance for the period.

In addition, management refers to these financial measures to facilitate internal and external comparisons to our historical operating results, in making operating decisions and for budget planning purposes. These measures should be considered in addition to, not as a substitute for, or superior to, gross profit, income from operations, cash flows from operating activities, or other measures of financial performance prepared in accordance with generally accepted accounting principles. The following table presents a summary of our free cash flow:

| Year Ended January 31 | ||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| (In thousands) | ||||||||||||||||||||

Cash flows from operating activities | $ | 54,219 | $ | 27,778 | $ | 45,413 | $ | 41,086 | $ | 53,326 | ||||||||||

Capital expenditures | (13,417 | ) | (6,047 | ) | (5,934 | ) | (16,709 | ) | (22,808 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Free cash flow | $ | 40,802 | $ | 21,731 | $ | 39,479 | $ | 24,377 | $ | 30,518 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

The increase in free cash flow during fiscal 2012 is primarily a result of higher net income, which was offset by higher levels of inventory and accounts receivable due to increased sales volumes. The decrease in free cash flow during fiscal 2011 is primarily a result of higher levels of accounts receivable due to increased sales volumes. Free cash flow levels in fiscal 2010 were primarily the result of reductions in accounts receivable and inventory during the economic downturn.

24

Table of Contents

Statements of Cash Flows

The statements of cash flows reflect the changes in cash and cash equivalents for the three years ended January 31, 2012 by classifying transactions into three major categories of activities: operating, investing and financing.

Our overall balance of cash and cash equivalents was $25 million at January 31, 2012 including a balance of $13 million in China. Legal restrictions and tax consequences in certain jurisdictions could limit our ability to repatriate cash to the United States. Certain repatriations of cash could result in negative tax consequences.

The following table presents net changes in cash and cash equivalents for the three years ended January 31, 2012.

| Year Ended January 31 | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| (In thousands) | ||||||||||||

Operating activities | $ | 54,219 | $ | 27,778 | $ | 45,413 | ||||||

Investing activities | (13,415 | ) | (4,790 | ) | (5,732 | ) | ||||||

Financing activities | (45,357 | ) | (20,930 | ) | (44,659 | ) | ||||||

Effect of exchange rate changes | 4,444 | 2,778 | (6,006 | ) | ||||||||

|

|

|

|

|

| |||||||

Net change in cash | $ | (109 | ) | $ | 4,836 | $ | (10,984 | ) | ||||

|

|

|

|

|

| |||||||

Operating