Exhibit 99.1

Bringing medical inn vation to life Orchestra BioMed Corporate Presentation July 2022

Important Notice and Disclaimer This investor presentation (this “Presentation”) is for informational purposes only to assist interested parties in making their own evaluation with respect to the proposed business combination (the “Business Combination”) between Health Sciences Acquisitions Corporation 2 (“HSAC2”) and Orchestra BioMed, Inc. (“OBIO,” “Orchestra,” or the “Company”) and for no other purpose. The information contained herein does not purport to be all-inclusive and none of HSAC2, the Company or their respective affiliates makes any representation or warranty, express or implied, as to the accuracy, completeness or reliability of the information contained in this Presentation. Neither the Company nor HSAC2 has verified, or will verify, any part of this Presentation. The recipient should make its own independent investigations and analyses of the Company and its own assessment of all information and material provided, or made available, by the Company, HSAC2 or any of their respective directors, officers, employees, affiliates, agents, advisors or representatives. This Presentation does not constitute (i) a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the proposed Business Combination or (ii) an offer to sell, a solicitation of an offer to buy, or a recommendation to purchase any security of HSAC2, the Company, or any of their respective affiliates, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made expect by means of a prospectus meeting the requirements of the U.S. Securities Act of 1933, as amended (the “Securities Act”). You should not construe the contents of this Presentation as legal, tax, accounting or investment advice or a recommendation. You should consult your own counsel and tax and financial advisors as to legal and related matters concerning the matters described herein, and, by accepting this Presentation, you confirm that you are not relying upon the information contained herein to make any decision. The distribution of this Presentation may also be restricted by law and persons into whose possession this Presentation comes should inform themselves about and observe any such restrictions. The recipient acknowledges that it is (a) aware that the U.S securities laws prohibit any person who has material, non-public information concerning a company from purchasing or selling securities of such company or from communicating such information to any other person under circumstances in which it is reasonably foreseeable that such person is likely to purchase or sell such securities, and (b) familiar with the Securities Exchange Act of 1934, as amended, and the rules and regulations promulgated thereunder (collectively, the "Exchange Act"), and that the recipient will neither use, nor cause any third party to use, this Presentation or any information contained herein in contravention of the Exchange Act, including, without limitation, Rule 10b-5 thereunder. This Presentation and information contained herein constitutes confidential information and is provided to you on the condition that you agree that you will hold it in strict confidence and not reproduce, disclose, forward or distribute it in whole or in part without the prior written consent of HSAC2 and the Company and is intended for the recipient hereof only. Forward-Looking Statements This Presentation may contain forward-looking statements. Forward-looking statements include, without limitation, statements regarding the estimated future financial performance and financial position of the Company. Future results are not possible to predict. Opinions and estimates offered in this Presentation constitute the Company’s judgment and are subject to change without notice, as are statements about market trends, which are based on current market conditions. This Presentation contains forward-looking statements, including without limitation, forward-looking statements that represent opinions, expectations, beliefs, intentions, estimates or strategies regarding the future of the Company and its affiliates, which may not be realized. Forward-looking statements can be identified by the words, including, without limitation, “believe,” “anticipate,” “continue,” “estimate,” “may,” “project,” “expect,” “plan,” “potential,” “target,” “intend,” “seek,” “will,” “would,” “could,” “should,” “forecast,” or the negative or plural of these words, or other similar expressions that are predictions or indicate future events, trends or prospects but the absence of these words does not necessarily mean that a statement is not forward-looking. Any statements that refer to expectations, projections, indications of, and guidance or outlook on, future earnings, dividends or financial position or performance or other characterizations of future events or circumstances are also forward-looking statements. All forward-looking statements are based on estimates and assumptions that are inherently uncertain and that could cause actual results to differ materially from expected results. Many of these factors are beyond the Company’s ability to control or predict. Factors that may cause actual results to differ materially from current expectations include, but are not limited to: (1) the occurrence of any event, change or other circumstances that could give rise to the termination of any definitive agreements with respect to the Business Combination; (2) the outcome of any legal proceedings that may be instituted against HSAC2, the combined company or others following the announcement of the Business Combination and any definitive agreements with respect thereto; (3) the inability to complete the Business Combination due to the failure to obtain approval of the shareholders of HSAC2, or to satisfy other conditions to closing; (4) changes to the proposed structure of the Business Combination that may be required or appropriate as a result of applicable laws or regulations or as a condition to obtaining regulatory approval of the Business Combination; (5) the ability to meet stock exchange listing standards following the consummation of the Business Combination; (6) the risk that the Business Combination disrupts current plans and operations of the Company as a result of the announcement and consummation of the Business Combination; (7) the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition, the ability of the combined company to commercialize its product candidates, maintain relationships with physicians and suppliers and retain its management and key employees; (8) costs related to the Business Combination; (9) changes in applicable laws or regulations; (10) the possibility that the Company or the combined company may be adversely affected by other economic, business, and/or competitive factors; (11) the Company’s estimates of expenses and profitability; (12) the risks and uncertainties set forth on the slides titled “Summary of Risk Factors” located in the appendix to this Presentation; and (13) other risks and uncertainties set forth in the sections entitled “Risk Factors” and “Forward Looking Statements” in HSAC2’s Annual Report on Form 10-K filed with the Securities and Exchange Commission (the “SEC”) on March 31, 2022. There may be additional risks that neither HSAC2 nor the Company presently know or that HSAC2 and the Company currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. 2

Important Notice and Disclaimer (Cont’d) 3 You are cautioned not to place undue reliance upon any forward-looking statements. Any forward-looking statement speaks only as of the date on which it was made, based on information available as of the date of this Presentation, and such information may be inaccurate or incomplete. The Company undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. Information regarding performance by, or businesses associated with, our management team or businesses associated with them is presented for informational purposes only. Past performance by the Company’s management team and its affiliates is not a guarantee of future performance. Therefore, you should not rely on the historical record of the performance of the Company’s management team or businesses associated with them as indicative of the Company’s future performance of an investment or the returns the Company will, or is likely to, generate going forward. Industry and Market Data In this Presentation, the Company may rely on and refer to certain information and statistics obtained from third-party sources which they believe to be reliable. The Company has not independently verified the accuracy or completeness of any such third-party information. No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any such third-party information. Trademarks HSAC2 and the Company own or have rights to various trademarks, service marks and trade names that they use in connection with the operation of their respective businesses. This Presentation may also contain trademarks, service marks, trade names and copyrights of third parties, which are the property of their respective owners. The use or display of third parties’ trademarks, service marks, trade names or products in this Presentation is not intended to, and does not imply, a relationship with HSAC2 or the Company, or an endorsement or sponsorship by or of HSAC2 or the Company. Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in this Presentation may appear without the TM, SM, * or © symbols, but such references are not intended to indicate, in any way, that HSAC2 or the Company will not assert, to the fullest extent under applicable law, their rights or the right of the applicable licensor to these trademarks, service marks, trade names and copyrights. Additional Information In connection with the proposed Business Combination, HSAC2 intends to file a preliminary and definitive proxy statement/prospectus, which will be a part of a registration statement, and other relevant documents with the SEC relating to the proposed Business Combination . This Presentation does not contain all the information that should be considered concerning the proposed Business Combination and is not intended to form the basis of any investment decision or any other decision in respect of the Business Combination. HSAC2’s and the Company’s shareholders and other interested persons are advised to read, when available, the preliminary proxy statement/prospectus and the amendments thereto and the definitive proxy statement/prospectus and other documents filed in connection with the proposed Business Combination, as these materials will contain important information about HSAC2, the Company and the Business Combination. When available, the definitive proxy statement/prospectus and other relevant materials for the proposed Business Combination will be mailed to shareholders of HSAC2 as of a record date to be established for voting on the proposed Business Combination. Shareholders will also be able to obtain copies of the preliminary proxy statement/prospectus, the definitive proxy statement/prospectus and other documents filed with the SEC, without charge, once available, at the SEC’s website at www.sec.gov, or by directing a request to: Health Sciences Acquisitions Corporation 2; 40 10th Avenue, Floor 7, New York, NY 10014. Participants in the Solicitation HSAC2 and its directors and executive officers may be deemed participants in the solicitation of proxies from HSAC2’s shareholders with respect to the proposed Business Combination. A list of the names of those directors and executive officers and a description of their interests in HSAC2 is contained in HSAC2’s Annual Report on Form 10-K, which was filed with the SEC on March 31, 2022 and is available free of charge at the SEC’s web site at www.sec.gov, or by directing a request to Health Sciences Acquisitions Corporation 2; 40 10th Avenue, Floor 7, New York, NY 10014. Additional information regarding the interests of such participants will be contained in the proxy statement/prospectus for the proposed Business Combination when available. The Company and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from the shareholders of HSAC2 in connection with the proposed Business Combination. A list of the names of such directors and executive officers and information regarding their interests in the proposed Business Combination will be included in the proxy statement/prospectus for the proposed Business Combination when available. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

Transaction Overview 4 Transaction Summary Orchestra BioMed and Health Sciences Acquisitions Corporation 2 (“HSAC2”, Nasdaq: HSAQ) have entered into a definitive business combination agreement HSAC2 is a special purpose acquisition company sponsored by RTW Investments, LP Upon closing, HSAC2 will change its name to “Orchestra BioMed Holdings, Inc.” and is expected to trade under ticker “OBIO” Expected post transaction implied pro forma fully diluted equity value of $317 million and pro forma fully diluted enterprise value of $158 million1 Transaction expected to close Q4 2022 Cash in Trust Deal structured to provide a minimum of $70 million in gross cash to the combined company from HSAC2’s trust RTW is providing up to a $50 million commitment to backstop potential redemptions $20 million in total forward purchase agreements from Medtronic and RTW Assuming no redemptions are made, an additional $90 million may be available from HSAC2’s trust account, providing maximum gross proceeds from the business combination of $160 million Earnout for Orchestra Shareholders 8M shares subject to milestones being achieved 50% at 20-day VWAP of $15.00/sh and 50% at 20-day VWAP of $20.00/sh, any time in 5 years following business combination closing Opt-in requires an extended lock-up of 12 months Sponsor Shares and Private Placement Warrants Deferred Sponsor Shares Vesting 1M shares (25% of 4M sponsor shares) subject to vesting milestones being achieved 50% at 20-day VWAP of $15.00/sh and 50% at 20-day VWAP of $20.00/sh, any time in 5 years following business combination closing Sponsor Private Placement Warrants issued at IPO Sponsor agreed to extinguish 50% or 750,000 of its pre-paid Private Placement Warrants that have an exercise price of $11.50/sh and expire 5 years following completion of a business combination Use of Proceeds Orchestra BioMed expected to have a minimum total pro forma cash of $169 million, after expenses at announcement1 The combined company is expected to have sufficient capital into 2026 based on current plans and estimates 1Assumes company cash balance at 3/31/2022 pro forma for Avenue Capital Loan and Security Agreement and Series D preferred stock offering. Assumes minimum gross cash case of $70 million. If no redemptions, the company could have total pro forma cash of up to $259 million.

Terms of Transaction 5 Combination is structured to provide a minimum of $70 million in gross cash to the combined company Sources & Uses (Minimum G Sources ross Cash Case) Amount Pro Forma Valuation (Minimum Particulars Gross Cash Case) Amount Cash Held in Trust 1 $70,000,000 Share Price $10.00 Orchestra Fully Diluted Equity 2 3 213,000,000 Pro Forma Fully Diluted Shares Outstanding 2 3 31,750,000HSAC2 Sponsor Shares 34,500,000 P Forma Fully Diluted Equity Value $317,500,000 Total Sources $317,500,000 (-) Net Trust Cash 1 (58,000,000) (-) Existing Balance Sheet Cash (111,350,000) (+) Debt 10,000,000 Pro Forma Fully Diluted Enterprise Value $158,150,000 Pro Forma Basic Ownership Uses Amount Orchestra Fully Diluted Equity

Orchestra BioMed Executive Summary Strategic collaboration with Medtronic Strong balance sheet with significant financial runway and outstanding investors Medtronic Partnership-enabled business model designed to accelerate innovation to patients, drive strong partner and shareholder value, & yield exceptional future profitability Statistically significant double-blind, randomized preliminary trial efficacy data Plan to initiate pivotal trial H2 2023 Strategic partnership with Strong 3-year multi-center preliminary trial safety and efficacy data Plan to initiate pivotal trial H1 2023 6 BackBeat CNT™ targets >$10B annual hypertension market Firmware upgrade to exis:ng pacemaker Virtue® SAB targets ∼$3B annual artery disease markets Protected sirolimus delivery, non-coated balloon

Enable new growth opportunities Outsource development Minimize P&L dilution 7 Orchestra BioMed’s Partnership-enabled Model Benefits All Development Strategic Partners Commercializa0on Improve patient lives Accelerate development Leverage expertise & resources Secure high-margin long-term royalties Outsource commercialization Multiply pipeline opportunities Shared Benefits

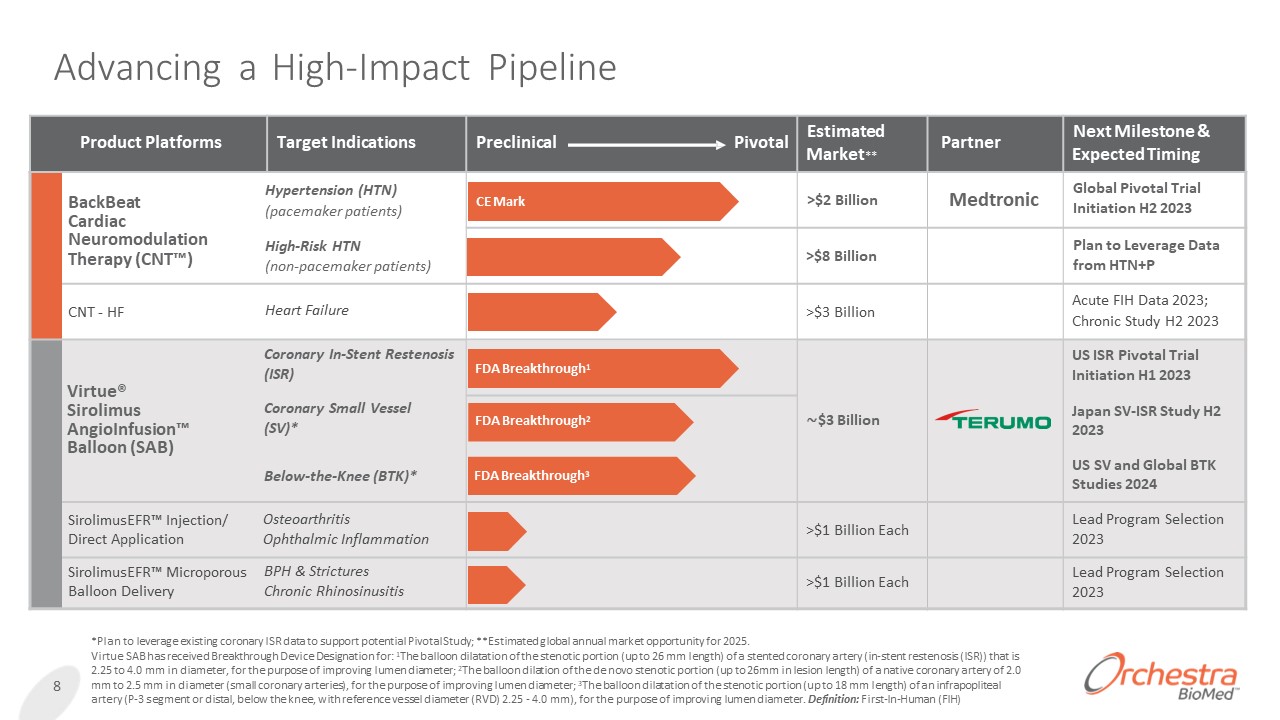

Advancing a High-Impact Pipeline 8 *Plan to leverage existing coronary ISR data to support potential Pivotal Study; **Estimated global annual market opportunity for 2025. Virtue SAB has received Breakthrough Device Designation for: 1The balloon dilatation of the stenotic portion (up to 26 mm length) of a stented coronary artery (in-stent restenosis (ISR)) that is 2.25 to 4.0 mm in diameter, for the purpose of improving lumen diameter; 2The balloon dilation of the de novo stenotic portion (up to 26mm in lesion length) of a native coronary artery of 2.0 mm to 2.5 mm in diameter (small coronary arteries), for the purpose of improving lumen diameter; 3The balloon dilatation of the stenotic portion (up to 18 mm length) of an infrapopliteal artery (P-3 segment or distal, below the knee, with reference vessel diameter (RVD) 2.25 - 4.0 mm), for the purpose of improving lumen diameter. Definition: First-In-Human (FIH) Product Platforms Target Indications Preclinical Pivotal Estimated Market** Partner Next Milestone & Expected Timing BackBeat Cardiac Neuromodulation Therapy (CNT™) Hypertension (HTN) (pacemaker patients) High-Risk HTN (non-pacemaker patients) CE Mark >$2 Billion Medtronic Global Pivotal Trial Initiation H2 2023 >$8 Billion Plan to Leverage Data from HTN+P CNT - HF Heart Failure >$3 Billion Acute FIH Data 2023; Chronic Study H2 2023 Virtue® Sirolimus AngioInfusion™ Balloon (SAB) Coronary In-Stent Restenosis (ISR) Coronary Small Vessel (SV)* Below-the-Knee (BTK)* FDA Breakthrough1 US ISR Pivotal Trial Initiation H1 2023 FDA Breakthrough2 ∼$3 Billion Japan SV-ISR Study H2 2023 FDA Breakthrough3 US SV and Global BTK Studies 2024 SirolimusEFR™ Injection/ Direct Application Osteoarthritis Ophthalmic Inflammation >$1 Billion Each Lead Program Selection 2023 SirolimusEFR™ Microporous Balloon Delivery BPH & Strictures Chronic Rhinosinusitis >$1 Billion Each Lead Program Selection 2023

George Papandreou Inessa R. Wheeler Bob Laughner Stephen A. Zielinski Ziv Belsky Juan Lorenzo Bill Baumbach, Ph.D. Eileen Bailey SVP, Quality VP, Strategy & VP, Regulatory Affairs VP, Product Dev., VP, Research, VP, Product Dev., VP, Scientific Affairs, VP, Quality, Focal Marketing Bioelectronic Therapies Bioelectronic Therapies Focal Therapies Focal Therapies Therapies Highly Accomplished Executive Team & Board Executive Team: >250 Years of Experience, ~25 Avg Industry Years, >100 Product Approvals & >600 Authored Patents David Hochman Chairman, CEO, Co-Founder Darren R. Sherman President, COO, Director, Co-Founder Michael Kaswan Chief Financial Officer Dennis Donohoe, M.D. Chief Medical Officer Yuval Mika, Ph.D. GM & CTO, Bioelectronic Therapies Hans-Peter Stoll, M.D., Ph.D. Chief Clinical Officer 9 Eric S. Fain, M.D. Board Member Eric A. Rose, M.D. Board Member Pamela Connealy Board Member Geoffrey W. Smith Board Member Jason Aryeh Board Member

10 BackBeat Cardiac Neuromodulation Therapy (CNT ™)

BackBeat CNT™ Overview 1Company estimates based on published sources, including National Inpatient Survey (NIS) and National Health and Nutrition Examination Survey 11 (NHANES); 2Kalaras et al. Journal of the American Heart Association. ahajournals.org/doi/10.1161/JAHA.120.020492; 3Burkhoff. MODERATO II Study 2- Year Results TCT 2021;. Definitions: Ambulatory Systolic Blood Pressure (aSBP) and Office Systolic Blood Pressure (oSBP) Opportunity Hypertension is #1 comorbidity in pacemaker population affecting over 70% of patients1 Older population at increased risk for major events & challenges with drug compliance Innovation Bioelectronic therapy designed to substantially & persistently lower blood pressure Compatible with standard pacemaker device & leverages existing treatment paradigm Compelling clinical data from double-blind randomized study: significant 8.1 mmHg net reduction in 24-Hr aSBP at 6 months & 17.5 mmHg reduction in oSBP at 2 years2,3 Collaboration with Medtronic Global pacemaker leader providing technology and development/clinical/regulatory support for Orchestra BioMed-sponsored global pivotal trial Following regulatory approval, Medtronic has exclusive global rights to commercialization in the pacemaker-indicated patient population with double-digit revenue sharing for Orchestra BioMed of BackBeat CNT-enabled pacemaker sales

Large Global Opportunity for Treating Hypertension in Target Populations *Total addressable market in 2025 based on company estimates; 1Company estimates based on published sources, including National Inpatient Survey (NIS) and National Health and Nutrition Examination Survey (NHANES); 2Known and well-characterized population, multiple references available; Definition: Hypertension (HTN) 12 >$10 Billion Potential Annual Global Market Opportunity* >3.1 M Addressable HTN Patients HTN + Pacemaker Over 70% of pacemaker patients have HTN1 Older, co-morbid population at increased risk of major events2 High Risk HTN (Non-pacemaker) Older patients with isolated systolic hypertension (ISH) and comorbidities 750,000 patients >$2 Billion Annual Global Opportunity 2,400,000 patients >$8 Billion HTN + Pacemaker High Risk HTN

Bioelectronic therapy designed to leverage standard rhythm management device procedures (dual-chamber pacemaker) Same implant procedure and lead positions Large trained physician pool Same target patient population Leverageable existing reimbursement Mechanism of action Designed to substantially reduce blood pressure by reducing preload through programmed pacing with short AV delays Designed to maintain reduction by modulating sympathetic tone and reducing afterload through programmed variable pressure patterns Designed to Substantially Lower BP & Maintain Reduction BackBeat CNT™ 13 Designed to Immediately, Substantially and Persistently Lower Blood Pressure 1. Reducing Preload Lowers BP 2. Modulating Sympathetic Tone Maintains Reduction in BP SBP (mmHg) 150 Time (s) 155 150 145 140 135 130 0 50 100. 200 250 300

MODERATO II Double-Blind, Randomized Results BackBeat CNT™ showed encouraging results in MODERATO II, a prospecQve, mulQ-center, randomized, (BackBeat CNT + Medical Therapy vs. ConQnued Medical Therapy), double-blind, pilot study of pacemaker paQents with persistent hypertension 1Kalaras et al. Journal of the American Heart Association. 2021;10:e020492 ahajournals.org/doi/10.1161/JAHA.120.020492; 2Burkhoff MODERATO II Study 2-Year Results TCT 2021; 324-Hr aSBP Control (n=19). 31 control patient could not be measured despite repeat measurement (patient had extremely high blood pressure); Definitions: Major Adverse Cardiac Events (MACE) included death, heart failure, clinically significant arrhythmias (i.e., persistent or increased atrial fibrillation, serious ventricular arrhythmias), myocardial infarction, stroke and renal failure in treatment group calculated per patient, Office Systolic Blood Pressure (oSBP), Ambulatory Systolic Blood Pressure (aSBP) 14 Significant Reduction in aSBP 24 Hours a Day -11.1 mmHg in 24-Hour aSBP at 6 months -17.5 mmHg in oSBP at 2 years 0% MACE vs. 9.5% in control group at 6 months 85% of patients with reduction in aSBP Significant Reduction in 24-Hr aSBP and oSBP1,2 oSBP 6 Months 24 Months aSBP 6 Months 0 -5 -10 -15 -20 -3.1 P = 0.17 -11.1 P < 0.001 -12.4 P < 0.001 -0.1 P = 0.94 -17.5 P < 0.01 Δ -12.3 P = 0.02 Δ -8.1 P = 0.01 Δ in BP (mmHg) 150 145 140 135 130 125 120 115 110 00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00 17:00 18:00 19:00 20:00 21:00 22:00 23:00 24-Hr aSBP (mmHg) P < 0.01 for all times of day Control (n=20)3 BackBeat CNT (n=26) Pre-activation (n=26) 6 months (n=26) 6 Month Mean Pre-activation Mean

BackBeat CNT™ Medtronic Collaboration Medtronic is the global leader in pacemakers >$1.5 billion annual pacemaker revenues1 Key Terms: (Hypertension + Pacemaker population) Orchestra BioMed drives and finances development as sponsor of global pivotal trial Medtronic provides certain development/clinical/regulatory resources funded by Orchestra to support integration into a Medtronic pacemaker and execution of the pivotal trial Medtronic has exclusive global rights for commercialization upon regulatory approval Orchestra BioMed will receive the higher of a fixed dollar amount per BackBeat CNT- enabled device, which varies by geography, or a percentage of the BackBeat CNT generated sales. The Orchestra BioMed revenue generated per sale of BackBeat CNT- enabled device is expected to be between $500 and $1,600 Medtronic invested $40 million in Orchestra BioMed’s $110 million Series D financing and will invest an additional $10M in HSAC2 merger transaction 15 Aligned with Global Market Leader in Pacemakers and Device-based Hypertension Treatment Medtronic 1Based on MDTs consolidated financial results for the fiscal year ended April 29, 2022

16 Virtue® Sirolimus AngioInfusion™ Balloon (SAB)

Virtue® SAB Overview 17 Opportunity Significant need for “leave nothing behind” treatment for coronary and peripheral indications representing an ∼$3B global market opportunity1 Drug-eluting stents (DES) carry risks of long-term restenosis and late thrombosis; require extended dual antiplatelet therapy; not effective/approved for select patients/lesions Innovation Highly-differentiated, non-coated drug/device combination product candidate designed to enable angioplasty with protected delivery of extended release sirolimus Compelling clinical results in multi-center coronary ISR clinical trial with 3-year follow-up2 FDA Breakthrough Device Designation received for indications in coronary ISR3, coronary SV4 and BTK5 Partnership with Global commercial leader with >$2.5B annual interventional cardiology revenue responsible for commercializing Virtue SAB as flagship therapeutic offering Collaboration driving multi-indication pivotal trial program starting with coronary ISR Orchestra BioMed to receive double-digit royalties and per unit drug payments 1Total addressable market is 2025 market data based on company estimates;; 2von Birgelen et al. JACC Vol. 59, No. 15, 2012 April 10, 2012:1350–61; Virtue SAB has received Breakthrough Device Designation for: 3The balloon dilatation of the stenotic portion (up to 26 mm length) of a stented coronary artery (in-stent restenosis (ISR)) that is 2.25 to 4.0 mm in diameter, for the purpose of improving lumen diameter; 4The balloon dilation of the de novo stenotic portion (up to 26mm in lesion length) of a native coronary artery of 2.0 mm to 2.5 mm in diameter (small coronary arteries), for the purpose of improving lumen diameter; 5The balloon dilatation of the stenotic portion (up to 18 mm length) of an infrapopliteal artery (P-3 segment or distal, below the knee, with reference vessel diameter (RVD) 2.25 - 4.0 mm), for the purpose of improving lumen diameter.

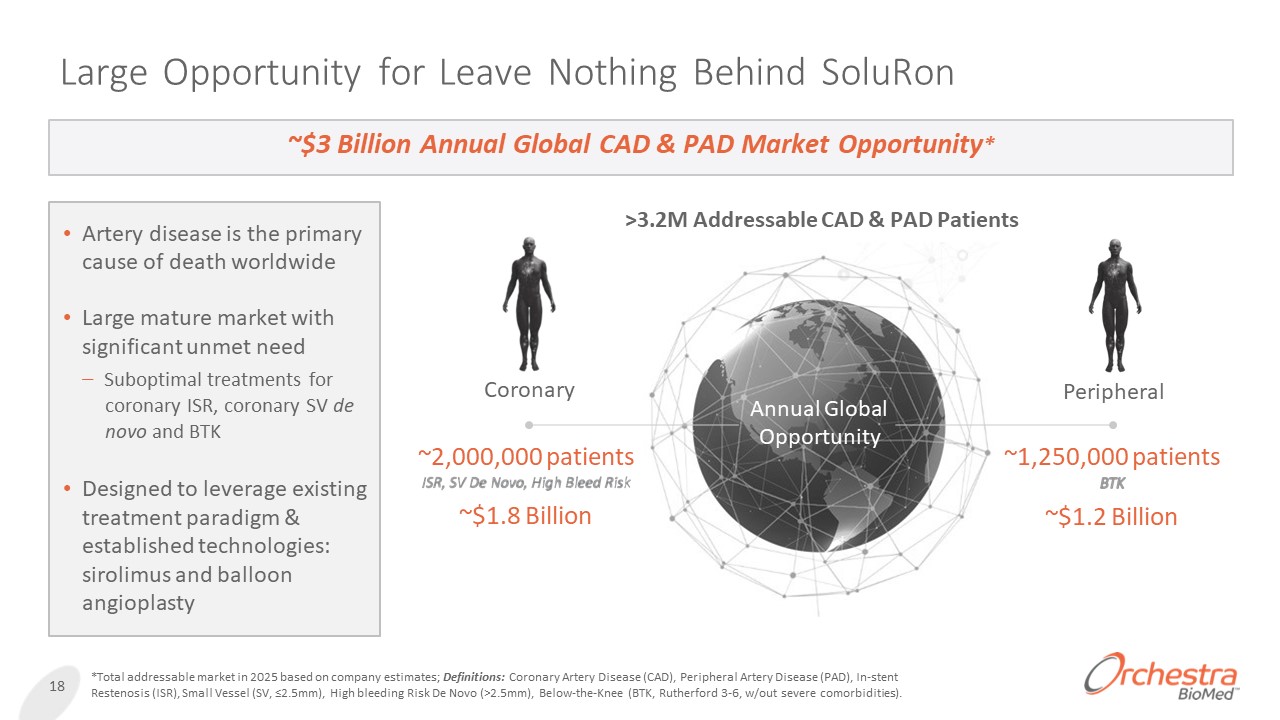

Large Opportunity for Leave Nothing Behind SoluRon 18 ~$3 Billion Annual Global CAD & PAD Market Opportunity* Artery disease is the primary cause of death worldwide Large mature market with significant unmet need – Suboptimal treatments for coronary ISR, coronary SV de novo and BTK Designed to leverage existing treatment paradigm & established technologies: sirolimus and balloon angioplasty >3.2M Addressable CAD & PAD Patients (2025 Estimate) ~2,000,000 patients ~$1.8 Billion Annual Global Opportunity ~1,250,000 patients ~$1.2 Billion Coronary Peripheral *Total addressable market in 2025 based on company estimates; Definitions: Coronary Artery Disease (CAD), Peripheral Artery Disease (PAD), In-stent Restenosis (ISR), Small Vessel (SV, ≤2.5mm), High bleeding Risk De Novo (>2.5mm), Below-the-Knee (BTK, Rutherford 3-6, w/out severe comorbidities).

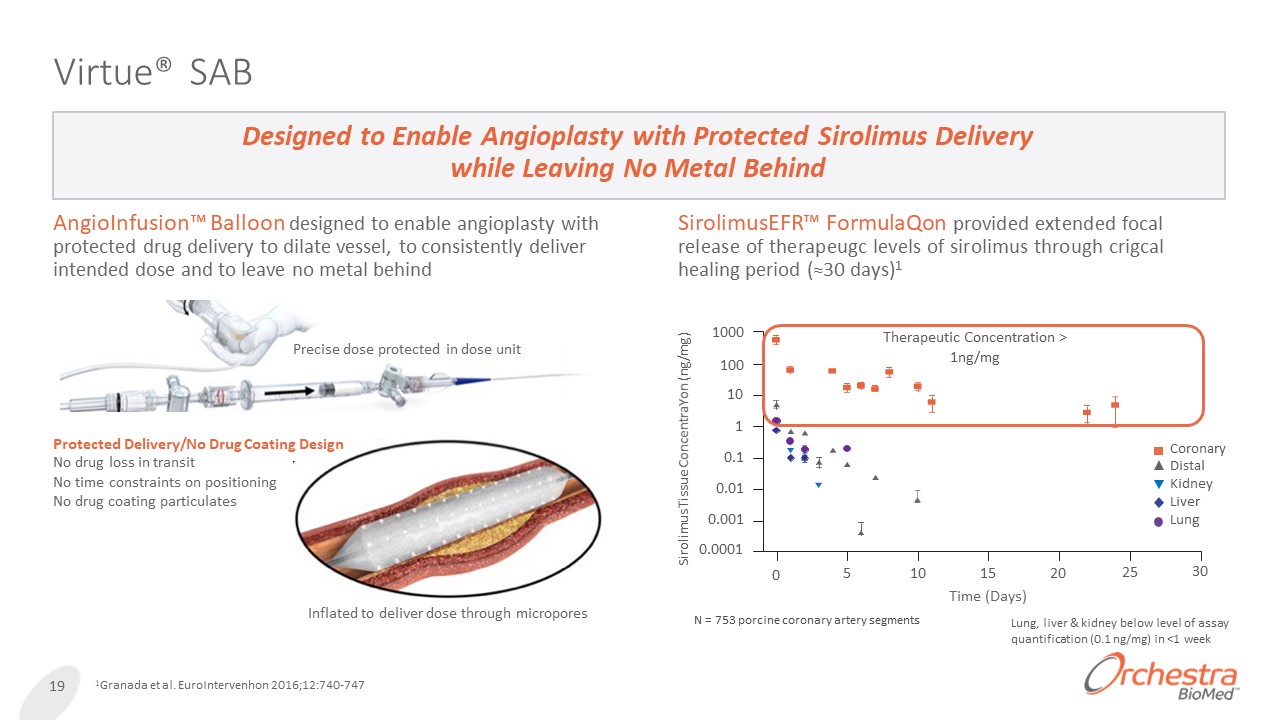

Virtue® SAB AngioInfusion™ Balloon designed to enable angioplasty with protected drug delivery to dilate vessel, to consistently deliver intended dose and to leave no metal behind Designed to Enable Angioplasty with Protected Sirolimus Delivery while Leaving No Metal Behind 19 1Granada et al. EuroIntervenhon 2016;12:740-747 Precise dose protected in dose unit Inflated to deliver dose through micropores SirolimusEFR™ FormulaQon provided extended focal release of therapeugc levels of sirolimus through crigcal healing period (≈30 days)1 1000 100 10 1 0.1 0.01 0.001 0.0001 Sirolimus Tissue ConcentraYon (ng/mg) Therapeutic Concentration > 1ng/mg Lung, liver & kidney below level of assay quantification (0.1 ng/mg) in <1 week 0 5 10 20 25 30 Coronary Distal Kidney Liver Lung 15 Time (Days) N = 753 porcine coronary artery segments Protected Delivery/No Drug Coating Design No drug loss in transit No time constraints on positioning No drug coating particulates

Compelling SABRE Trial Results in Coronary ISR Patients 1Verheye et al. JACC Cardiovasc Interv 2017 Oct 23;10(20):2029-2037. DOI: 10.1016/j.jcin.2017.06.021. 2Granada 3-Year Clinical Results TCT 2018. 3-Year SABRE Trial Clinical Report on file. 4Data is based on per protocol populahon criteria revised to be consistent with proposed Virtue ISR-US pivotal study populahon. Defini,ons: Target lesion failure (TLF), late lumen loss (LLL), target lesion revascularizahon (TLR) and Myocardial Infarchon (MI). 20 Virtue® SAB preliminarily demonstrated encouraging safety and efficacy results in patients with coronary in-stent restenosis (ISR) in prospective, multi-center SABRE Trial1 0.12mm LLL at 6-months 2.8% Target Lesion Failure at 1 year 0% New TLR between 1 to 3 years Preliminarily Demonstrated Safety with Low Event Rates Out to 3 Years Preliminary Efficacy Results Showed Low 0.12mm Late Loss 1RVD reported using Internormal values; 2Trial primary performance endpoint; 3Trial secondary performance endpoint (binary restenosis = >50% lumen diameter stenosis) Event Rates (%) TLR TLF 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% 30 days 1-year 3-years 0% 0% 0% 0% 0% Cardiac Death TV-MI 0% 0% 2.8% 2.8% 2.8% 2.8% 5.6% 4

Virtue® SAB Terumo Partnership Terumo is a global leader with >$2.5 billion annual interventional cardiology revenues1 Virtue SAB positioned as the flagship therapeutic offering with potential to drive significant future growth Key Terms: $30 million upfront and potential future clinical and regulatory milestones $5 million equity investment including participation in Series D financing Terumo responsible for clinical and regulatory expenses, excluding Virtue ISR-US study which Orchestra BioMed is sponsoring Terumo responsible for device supply chain and commercialization expenses Orchestra BioMed receives 10-15% royalty PLUS per unit payments for SirolimusEFR™ as exclusive supplier Orchestra BioMed retains rights to Virtue SAB in all clinical applications outside of vascular indications 21 MulLnaLonal Market Leader Provides Global Commercial Reach and Long-Term Alignment 1Based on Terumo’s consolidated financial results for the fiscal year ended March 31, 2022

Virtue® SAB – Coronary ISR US Pivotal Trial 22 Double-blind, mul_- center, prospec_ve, randomized controlled trial in pa_ents with single-layer coronary ISR Virtue® SAB N=200 R Target Lesion Failure (CD, TV-MI and TLR) at 12 months Primary Endpoint Statistical Assumption 90% powered for superiority Virtue SAB TLF ≤ 19% vs. PBA TLF ≥ 30% Success Considerations Virtue SAB: 2.8% TLF at 12 months in SABRE trial per protocol population PBA: 33-46% TLF at 12 months in coronary ISR published studies 12 Month Primary Endpoint 12-18 Months Enrollment Key Inclusion RVD 2.5 to 4.0 mm, <30% DS (vs. RVD 2.5 to 3.5, <40% DS SABRE1 Trial) 1Verheye S. JACC Cardiovasc Interv. 2017; 10: 2029-37. Definitions: Coronary In-stent Restenosis (ISR), Diameter Stenosis (DS), Plain Balloon Angioplasty (PBA). Revised per protocol analysis set meets the criteria of the proposed In-Stent Restenosis IDE study population. PBA N=100

Use of Proceeds 23 AcRvity Description Estimated Expenses H2 2022 - 2025 Research & Development General R&D enabling work for BackBeat CNT™ and Virtue® SAB BackBeat CNT Firmware integration into Medtronic device; testing and validation activities Clinical trial planning and preparation IDE preparation and submission Virtue SAB GLP and biocompatibility testing for IDE submission SirolimusEFR production and process scale-up activities Clinical trial materials (device and drug) manufacturing and testing IDE preparation and submission CNT-HF and SirolimusEFR feasibility work $35-45M Backbeat CNT & Virtue SAB Pivotal Trials Execution of multinational BackBeat CNT HTN+P pivotal trial (design, enrollment, data collection, analysis and monitoring) Execution of Virtue SAB ISR-US pivotal trial (design, enrollment, data collection, analysis and monitoring) $55-65M General & Administrative General overhead Includes public company expenses Minimal sales or marketing expenses; strategic partners drive commercialization ~$3M avg. per quarter H2 2022 - 2025 Expenses by Category Definitions: Coronary In-stent Restenosis (ISR), Research & Development (R&D), Investigation Device Exemption (IDE), Good Laboratory Practice (GLP)

24 Two Programs Targe0ng Large Markets Supported by Promising Trial Data Entering Pivotal Trials BackBeat CNT™ >$10 billion annual market Randomized, controlled study shows efficacy potengal Collaboragon with Medtronic Virtue® SAB ∼$3 billion annual market 3-year pilot study results show potengal safety & efficacy Partnered with Bringing Medical Inn vations to Life Through Partnerships Partnership-Enabled Business Model & Acc hip omplished Leaders Team – Designed to accelerate innovation to patients, enable pipeline expansion and drive strong partner and shareholder value – Highly experienced team with proven track record of innovation and execution Strong Balance Sheet with Significant Financial Runway and Committed Investors Medtronic

Partnership-Enabled Business Model 25

Significant Barriers Prevent Innovation From Reaching Patients 26 1Pitchbook – Analysis of 430 companies since 2015 that completed at least Series B financing 2SVB Healthcare Report 2019 3Capital IQ Startups often struggle for resources to reach commercial value inflection Large companies’ constrained R&D budgets limit innovation & acquisitions Increasing burden of cost, time, and work to bring medical innovation to patients Product Development Commercialization Avg $60M funding needed, 85% of acquisitions required commercial traction1 Avg 7% of revenue spent on R&D by top 20 med device vs. 20% in pharma2,3

Orchestra BioMed Can Accelerate Innovation to Patients 27 Risk-Reward Sharing Partnerships Can Overcome the Barriers to Innovation

28 SelecRng OpRmal OpportuniRes Develop for Partnership Pre-partnered Acquisitions Key Pipeline Criteria Large Market with Unmet Needs Large market, significant unmet needs, established distribution channels Potential for High Impact Designed to improve standard of care, fit existing treatment paradigm, disrupt market dynamics Favorable for Partnering Significant differentiation, attractive economics for partnership, durable IP protection Innovation Royalty-based R&D Programs

Orchestrating Inn vation 29 Created Pipeline, Pioneered Business Model and Established Partnerships Combined, our leadership team has Years of experience Average years of experience each New product approvals/clearances Authored patents 250+ 25 100+ 600+ Accomplished Leadership Team

Appendix: Summary of Risk Factors Risks Related to Orchestra’s Business and Products Orchestra has a history of net losses, expects to continue to incur losses for the foreseeable future and may never become profitable. If Orchestra does not achieve its projected development and commercialization goals, its business may be harmed. Even if Orchestra obtains all necessary FDA approvals and clearances, its product candidates may not achieve or maintain market acceptance. Orchestra may be unable to compete successfully with larger companies in its highly competitive industry. Orchestra may expend its limited resources to pursue a particular product or indication and fail to capitalize on products or indications that may be more profitable or for which there is a greater likelihood of success. Orchestra’s operating results may fluctuate significantly, which makes its future operating results difficult to predict and could cause operating results to fall below expectations or any guidance it may provide. A pandemic, such as the COVID-19 pandemic, could adversely impact our business, including our clinical trials and financial condition. Orchestra’s loan and security agreement contains operating covenants and restrictions that may restrict its business and financing activities. If Orchestra’s clinical trials are unsuccessful or significantly delayed, or if Orchestra does not complete its clinical trials, its business may be harmed. Interim, ‘‘top-line’’ and preliminary data from Orchestra’s clinical trials that it announces or publishes from time to time may change as more patient data become available and are subject to audit and verification procedures that could result in material changes in the final data. Orchestra’s product candidates may be associated with serious adverse events, undesirable side effects or have other properties that could halt their clinical development, prevent their regulatory approval, limit their commercial potential or result in significant negative consequences. Orchestra depends on attracting, retaining and developing key management, clinical, scientific and sales and marketing personnel, and losing these personnel could impair the development and sales of our products or product candidates. If Orchestra makes acquisitions, it could incur significant costs and encounter difficulties that harm its business. Product liability and other claims may reduce demand for Orchestra’s products or result in substantial damages. The misuse or off-label use of Orchestra’s products may harm its reputation in the marketplace, result in injuries that lead to product liability suits or result in costly investigations, fines or sanctions by regulatory bodies if Orchestra is deemed to have engaged in the promotion of these uses, any of which could be costly to its business. Orchestra’s internal computer systems, or those of any of its contract research organizations, manufacturers, other contractors, consultants, collaborators or potential future collaborators, may fail or suffer security or data privacy breaches or other unauthorized or improper access to, use of, or destruction of proprietary or confidential data, employee data, or personal data, which could result in additional costs, loss of revenue, significant liabilities, harm to Orchestra’s brand and material disruption of its operations. Economic conditions, including inflation caused by, among other things, the ongoing invasion of Ukraine by Russia, may adversely affect Orchestra’s business, financial condition and share price. Disruptions at the FDA and other government agencies caused by funding shortages or global health concerns could hinder their ability to hire, retain or deploy key leadership and other personnel, or otherwise prevent new or modified products from being developed, cleared or approved or commercialized in a timely manner or at all, which could negatively impact Orchestra’s business. In the future, we expect to be subject to a variety of risks associated with marketing and distributing our products internationally that could materially adversely affect our business. The sizes of the markets for product candidates have not been established with precision, and may be smaller than Orchestra estimates. Orchestra may in the future bring certain validation testing and pharmaceutical manufacturing capabilities in-house, and it may not be able to do so successfully or in compliance with FDA regulations. 30

Appendix: Summary of Risk Factors (Cont’d) Risks Related to Orchestra BioMed’s Reliance on Third Parties Orchestra expects to be highly dependent on partners and third-party vendors to manufacture and provide important materials and components for its products and product candidates. Orchestra may be unable to reach certain milestones under its agreement with Terumo by the dates specified or at all. Orchestra expects to be highly dependent on partners to drive the successful marketing and sale of our initial product candidates. Orchestra and its partners may be unable to sustain revenue growth. From time to time, Orchestra engages outside parties to perform services related to certain of its clinical studies and trials, and any failure of those parties to fulfill their obligations could cause costs and delays. The continuing development of many of Orchestra’s products and product candidates depends upon maintaining strong working relationships with physicians. Orchestra has limited pharmaceutical manufacturing experience and may experience development or manufacturing problems or delays in producing its products and planned or future products that could limit the potential growth of revenue or increase losses. Orchestra sources certain products from foreign suppliers, making it vulnerable to supply problems or price fluctuations caused by trade conflicts and other geopolitical events. The ongoing Russian invasion in Ukraine may have an adverse effect on the operations of our partners. Risks Related to Government Regulation and Orchestra BioMed’s Industry Healthcare reform initiatives and other administrative and legislative proposals may adversely affect Orchestra’s business. Orchestra may not obtain the necessary approvals and failure to obtain timely regulatory approval, if at all, would adversely affect its business. Orchestra’s medical device products must be manufactured in accordance with federal and state regulations, and it or any of its suppliers or third-party manufacturers could be forced to recall installed systems or terminate production if we or they fail to comply with these regulations. Even if Orchestra obtains regulatory approval for a product candidate, its products will remain subject to regulatory scrutiny and post-marketing requirements and failure to comply with post- marketing regulatory requirements could subject us to enforcement actions, including substantial penalties, and might require us to recall or withdraw a product from the market. Orchestra’s medical device products, if approved, may cause or contribute to adverse medical events or be subject to failures or malfunctions that Orchestra is required to report to the FDA, and if we fail to do so, we would be subject to sanctions that could harm our reputation, business, financial condition and results of operations. The discovery of serious safety issues with Orchestra’s products, or a recall of our products either voluntarily or at the direction of the FDA or another governmental authority, could have a negative impact on us. Virtue SAB is a drug/device combination, which may result in additional regulatory and other risks. If the FDA does not conclude that SirolimusEFR as a standalone product candidate satisfies the requirements for the Section 505(b)(2) regulatory approval pathway, or if the requirements for such product candidates under Section 505(b)(2) are not as Orchestra expects, the approval pathway for those product candidates may likely take significantly longer, cost significantly more and entail significantly greater complications and risks than anticipated, and in either case may not be successful. Changes in methods of product candidate manufacturing or formulation may result in additional costs or delay. Orchestra’s relationships with physicians, patients and payors in the United States and elsewhere may be subject, directly or indirectly, to applicable anti-kickback, fraud and abuse, false claims, transparency, and other healthcare laws and regulations. Healthcare cost containment pressures and legislative or administrative reforms resulting in restrictive coverage and reimbursement practices of third-party payors could decrease the demand for Orchestra’s products, the prices that customers are willing to pay for those products and the number of procedures performed using its devices, which could have an adverse effect on its business. Changes in and failures to comply with U.S. and foreign privacy and data protection laws, regulations and standards may adversely affect Orchestra’s business, operations and financial performance. Environmental and health safety laws may result in liabilities, expenses and restrictions on Orchestra’s operations. Orchestra is subject to anti-bribery, anti-corruption, and anti-money laundering laws, including the U.S. Foreign Corrupt Practices Act, and violations of these laws could result in substantial penalties and prosecution. 31