Exhibit 99.2 Commercializing Aerial RidesharingExhibit 99.2 Commercializing Aerial Ridesharing

This investor presentation (this “presentation”) is for informational purposes only. This presentation has been prepared to assist interested parties in making their own evaluation with respect to the proposed transaction (the “Transaction”) between Reinvent Technology Partners (“Reinvent”) and Joby Aero, Inc. (the “Company”), as contemplated in the Agreement and Plan of Merger, dated as of February 23, 2021 (the “Merger Agreement”), by and among Reinvent, the Company and RTP Merger Sub Inc., and for no other purpose. The information contained herein does not purport to be all inclusive. Nothing herein shall be deemed to constitute investment, legal, tax, financial, accounting or other advice. This presentation is being provided for use only by the intended recipient. The information contained herein may not be reproduced or distributed in any format, in whole or in part, without the prior written consent of Reinvent and the Company. Neither Reinvent nor the Company makes any representation or warranty as to the accuracy or completeness of the information contained in this presentation. The information in this presentation and any oral statements made in connection with this presentation is subject to change and is not intended to be all-inclusive or to contain all the information that a person may desire in considering an investment in Reinvent and is not intended to form the basis of any investment decision in Reinvent. Certain information contained herein has been derived from sources prepared by third parties. While such information is believed to be reliable for the purposes used herein, none of the Company or Reinvent, or their respective affiliates, directors, officers, employees, members, partners, shareholders or agents makes any representation or warranty with respect to the accuracy of such information. Fo r ward-Looking Statements Some statements contained in this presentation are forward-looking in nature. Forward-looking statements include, but are not limited to, statements regarding the Company, its management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, ar e forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this presentation may include, for example, statements about the Company’s industry and market sizes; future opportunities; expectations and projections concerning future financial and operational performance and results; and the proposed Business Combination, including items such as the implied aggregate value, ownership structure and the likelihood and ability of the parties to successfully consummate the Business Combination. You should carefully consider the risks and uncertainties described in the “Risk Factors” section of Reinvent’s prospectus related to its initial public offering, the proxy statement/prospectus on Form S-4 relating to the Business Combination, which is expected to be filed by Reinvent with the Securities and Exchange Commission (the “SEC”) and other documents filed by Reinvent from time to time with the SEC. These filings identify and address other important risks an d uncertainties that could cause actual events and results to differ materially from those contained in the forward-looking statements. The forward-looking statements contained in this presentation are based on the Company’s current expectations and beliefs concer ning future developments and their potential effects on the Company taking into account information currently available. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond the control of Reinvent and the Company) or other assumptions that may cause the Company’s actual results or performance to be materially different from those expressed or implied by these forward-looking statements. Such risks, uncertainties and assumptions include, but are not limited to: the severity and duration of the COVID-19 pandemic; the pandemic’s impact on the U.S. and global economies; federal, state, and local governmental responses to the pandemic; the inability to create, maintain or grow volume and profitability; the inability to obtain relevant regulatory approvals for the operation of the mobility service; the inability to develop or source adequate infrastructure to support the scale of the intended operations; public reluctance in adopting this new form of mobility, or willingness to pay a premium price; inability of theCompany to ramp production adequately to support the scale of the intended operations; inability to reduce end-user pricing over time in order to stimulate sufficient demand to drive expected growth; changes in prevailing interest rates; the inability to obtain sufficient capital to meet operational financing requirements or comply with debt agreements; the inability to measure or estimate the fair value of assets and liabilities; the inability to compete in the highly competitive transportation industry; the inability to manage legal and regulatory examinations and enforcement investigations and proceedings, compliance requirements and related costs; the inability to prevent cyber intrusions and mitigate cyber risks; the inability to achieve or maintain initial and supplemental certifications; and the inability to maintain licenses and other regulatory approvals. Should one or more of these risks or uncertainties materialize, they could cause our actual results to differ materially from the forward-looking statements. Neither Reinvent nor the Company will undertake any obligation to update or revise any forward looking statements whether as a result of new information, future events or otherwise. You should not take any statement regarding past trends or activities as a representation that the trends or activities will continue in the future. Forward-looking statements speak only as of the date they are made. Accordingly, you should not put undue reliance on these statements. This presentation is not intended to constitute, and should not be construed as investment advice. An investment in the Company is not an investment in any of our founders’ past investments, companies or funds affiliated wit h them. The historical results of these investments are not indicative of future performance of the Company, which may differ materially from the performance of the founders. S t atement Regarding Non-GAAP Financial Measures This presentation includes EBITDA, which is a supplemental measure that is not required by, or presented in accordance with, accounting principles generally accepted in the United States (“GAAP”). As a Non-GAAP financial measure, EBITDA excludes items that are significant in understanding and assessing the Company’s financial results or position. Therefore, this measure should not be considered in isolation or as an alternative t o net income, cash flows from operations or other measures of profitability, liquidity or performance under GAAP. You should beware that the Company’s presentation of this measure may not be comparable to similarly-titled measures used by other companies. U se of Projections This presentation contains financial forecasts for the Company with respect to certain financial results for the Company’s fiscal years 2021 through 2026. Neither Reinvent’s nor Company’s independent auditors have audited, studied, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, they did not express an opinion or provide any other form o f assurance with respect thereto for the purpose of this presentation. These projections are forward-looking statements and should not be relied upon as being necessarily indicative of future results. In this presentation, certain of the above-mentioned projected information has been provided for purposes of providing comparisons with historical data. The assumptions and estimates underlying the prospective financial information are inherently uncert ain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. Accordingly, there can be no assurance that the prospective results are indicative of the future performance of the Company or that actual results will not differ materially from those presented in the prospective financial information. Inclusion of the prospective financial information in this presentation should not be regarded as a representation by any person that the results contained in the prospective financial information will be achieved. Important Information and Where to Find It Reinvent intends to file materials related to the proposed Business Combination with the SEC, including a registration statement on Form S-4, which will include a proxy statement/prospectus. The proxy statement/prospectus will be sent to all Reinvent share holders. Reinvent will also file other documents regarding the proposed transaction with the SEC. In vestors and security holders of Reinvent and the Company are urged to read the proxy statement/prospectus and other relevan t documents that will be filed with the SEC carefully and in their entirety when they become available because they will contain important information about the proposed Business Combination. Investors and security holders will be able to obtain free copies of the proxy statement , prospectus and other documents containing important information about Reinvent and the Company through the website maintained by the SEC at www.sec.gov. Copies of the documents filed with the SEC by Reinvent can be obtained free of charge by directing a written request to Reinvent at 215 Park Avenue, Floor 11, New York, NY. P articipation in Solicitation Reinvent and the Company and their respective directors and officers may be deemed to be participants in the solicitation of proxies from Reinvent shareholders in connection with the proposed Business Combination. Information about Reinvent’s directors and officers and their ownership of Reinvent’s securities is set forth in Reinvent’s filings with the SEC. Additional information regarding the interests of those persons and other persons who may be deemed participants in the proposed Buiness Combination may be obtained by reading the proxy statement/prospectus regarding the proposed Business Combination when it becomes available. You may obtain free copies of these documents as described in the preceding paragraph. Tr ademarks Reinvent and the Company own or have rights to various trademarks, service marks and trade names that they use in connection with the operation of their respective businesses. This presentation may also contain trademarks, service marks, trade names and copyrights of third parties, which are the property of their respective owners. The use or display of third parties’ trademarks, service marks, trade names or products in this presentation is not intended to, and does not imply, a relationship with Reinvent or the Company, or an endorsement or sponsorship by or of Reinvent or the Company. Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in this presentation may appear without the TM, SM, ® or © symbols, but such references are not intended to indicate, in any way, that Reinvent or the Company will not assert, to the fullest extent under applicable law, their rights or the right of the applicable licensor to these trademarks, service marks, trade names and copyrights.

Today's Presenters JoeBen Bevirt Paul Sciarra Michael Thompson CEO & Chief Architect Executive Chairman CEO & CFO Joby Joby Reinvent Serial Entrepenuer with Lifelong Passion for Co-Founder of Pinterest Founder / Portfolio Manager of BHR Aviation and Engineering Entrepreneur-in-Residence at Andreessen Capital Co-Founder of Velocity11 Horowitz 3Today's Presenters JoeBen Bevirt Paul Sciarra Michael Thompson CEO & Chief Architect Executive Chairman CEO & CFO Joby Joby Reinvent Serial Entrepenuer with Lifelong Passion for Co-Founder of Pinterest Founder / Portfolio Manager of BHR Aviation and Engineering Entrepreneur-in-Residence at Andreessen Capital Co-Founder of Velocity11 Horowitz 3

Reinvent is Proud to Sponsor Joby: A World-Changing Platform Investment Objectives Venture capital at scale – innovation driven company with uncapped growth potential ✓ At the nexus of impactful and attractive long-term technology trends where we have expertise and believe we can add value (autonomous transportation; clean energy ✓ infrastructure; electric vehicles; growth of marketplaces) Market-leading company delivering products and services that matter in people’s lives ✓ Visionary and bold founder and CEO ✓ Long-term shareholder alignment, including with strategic investors like Toyota and Uber ✓ Business model that benefits from sustained and defensible network effects at scale ✓ 4Reinvent is Proud to Sponsor Joby: A World-Changing Platform Investment Objectives Venture capital at scale – innovation driven company with uncapped growth potential ✓ At the nexus of impactful and attractive long-term technology trends where we have expertise and believe we can add value (autonomous transportation; clean energy ✓ infrastructure; electric vehicles; growth of marketplaces) Market-leading company delivering products and services that matter in people’s lives ✓ Visionary and bold founder and CEO ✓ Long-term shareholder alignment, including with strategic investors like Toyota and Uber ✓ Business model that benefits from sustained and defensible network effects at scale ✓ 4

DeSPAC Structure Aligns Interests for Long-Term Reid Hoffman will serve on the Board of Directors ✓ Up to five-year lock-up on founder shares ✓ Price-based vesting triggers of $12, $18, $24, $32 and $50 per share on founder shares ✓ Senior Joby management and material existing investors subject to lock-up arrangements substantially ✓ similar to the founder shares $100MM+ investment in PIPE from Reinvent investment vehicles ✓ Strong Alignment for Joby and Reinvent to Drive Significant Long-Term Value for Shareholders 5DeSPAC Structure Aligns Interests for Long-Term Reid Hoffman will serve on the Board of Directors ✓ Up to five-year lock-up on founder shares ✓ Price-based vesting triggers of $12, $18, $24, $32 and $50 per share on founder shares ✓ Senior Joby management and material existing investors subject to lock-up arrangements substantially ✓ similar to the founder shares $100MM+ investment in PIPE from Reinvent investment vehicles ✓ Strong Alignment for Joby and Reinvent to Drive Significant Long-Term Value for Shareholders 5

Transaction Summary Transaction Structure • Joby and Reinvent are in discussion to combine in order to grow the industry leading aerial ridesharing business as a public company and achieve commercialization for its eVTOL aircraft by 2024 • Restructured founder shares and private warrants to create long-term alignment Valuation • Transaction implies a fully diluted pro-forma aggregate value of $4.6Bn (2.3x AV / 2026E Revenue) (1)(2) • Existing Joby shareholders to roll 100% of their equity and expected to receive 76% of the pro-forma equity Capital Structure • The transaction will be funded by a combination of Reinvent cash held in a trust account and Committed Funding for an (1)(2) aggregate of up to $1.6Bn • Pro-forma for the transaction, Joby expects to have up to ~$2.0Bn of cash to fund growth and commercialize its operations No tes: 1. Pro-forma ownership based on $10.00 per share price and excludes potential dilution from out-of-the-money Reinvent warrants and out-of-of the-money founder shares. Pro-forma further assumes no redemptions by Reinvent's existing public shareholders 2. Committed Funding is inclusive of an $835MM fully committed PIPE and a $75MM Uber convertible note which converts immediately prior to transaction closing; the 7.5MM shares to be issued to Uber are excluded from the Equity Consideration to Joby's Existing Investors 6Transaction Summary Transaction Structure • Joby and Reinvent are in discussion to combine in order to grow the industry leading aerial ridesharing business as a public company and achieve commercialization for its eVTOL aircraft by 2024 • Restructured founder shares and private warrants to create long-term alignment Valuation • Transaction implies a fully diluted pro-forma aggregate value of $4.6Bn (2.3x AV / 2026E Revenue) (1)(2) • Existing Joby shareholders to roll 100% of their equity and expected to receive 76% of the pro-forma equity Capital Structure • The transaction will be funded by a combination of Reinvent cash held in a trust account and Committed Funding for an (1)(2) aggregate of up to $1.6Bn • Pro-forma for the transaction, Joby expects to have up to ~$2.0Bn of cash to fund growth and commercialize its operations No tes: 1. Pro-forma ownership based on $10.00 per share price and excludes potential dilution from out-of-the-money Reinvent warrants and out-of-of the-money founder shares. Pro-forma further assumes no redemptions by Reinvent's existing public shareholders 2. Committed Funding is inclusive of an $835MM fully committed PIPE and a $75MM Uber convertible note which converts immediately prior to transaction closing; the 7.5MM shares to be issued to Uber are excluded from the Equity Consideration to Joby's Existing Investors 6

77

Joby OverviewJoby Overview

Urban Traffic Networks Collapse Congestion is bad … and getting worse + Population urbanization and underfunded infrastructure + Ridesharing and delivery increasing ground traffic + LA traffic has increased 80% since 1990 + Average speed drops from 37km/h to 9km/h as congestion increases 9 Ambühl, L., et al. “The Collapse of Urban Traffic Networks.” Berkley Hemnet Lab, 2020Urban Traffic Networks Collapse Congestion is bad … and getting worse + Population urbanization and underfunded infrastructure + Ridesharing and delivery increasing ground traffic + LA traffic has increased 80% since 1990 + Average speed drops from 37km/h to 9km/h as congestion increases 9 Ambühl, L., et al. “The Collapse of Urban Traffic Networks.” Berkley Hemnet Lab, 2020

Massive Untapped Market Opportunity (1) $500 billion addressable market for the U.S. alone Total global addressable market is north of $1 trillion No tes: 1. Booz Allen Hamilton: Urban Air Mobility (UAM) Market Study – 2018 10Massive Untapped Market Opportunity (1) $500 billion addressable market for the U.S. alone Total global addressable market is north of $1 trillion No tes: 1. Booz Allen Hamilton: Urban Air Mobility (UAM) Market Study – 2018 10

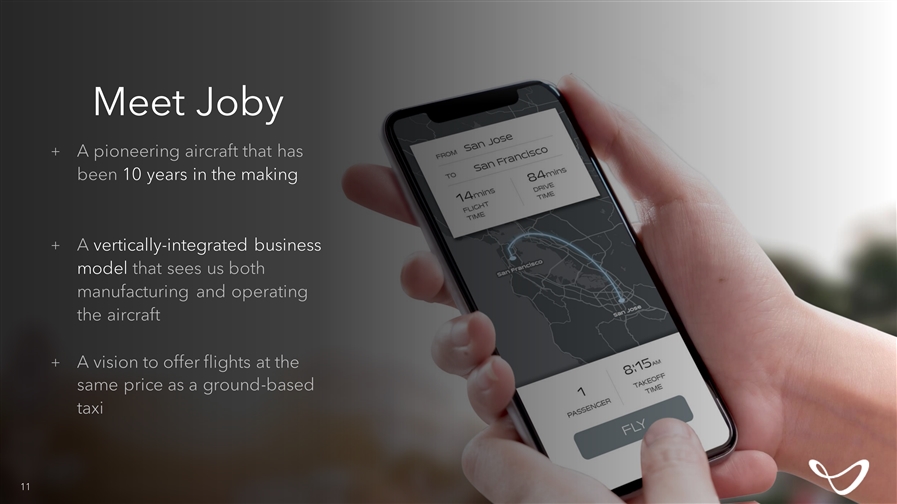

Meet Joby + A pioneering aircraft that has been 10 years in the making + A vertically-integrated business model that sees us both manufacturing and operating the aircraft + A vision to offer flights at the same price as a ground-based taxi 11Meet Joby + A pioneering aircraft that has been 10 years in the making + A vertically-integrated business model that sees us both manufacturing and operating the aircraft + A vision to offer flights at the same price as a ground-based taxi 11

1212

High level 10 years in 150+ mi range 5 Seats 200 mph 65 dBA (with 30 min VFR reserve) 1 pilot 4 passengers redundancy development top speed @ 100m (hover) 13High level 10 years in 150+ mi range 5 Seats 200 mph 65 dBA (with 30 min VFR reserve) 1 pilot 4 passengers redundancy development top speed @ 100m (hover) 13

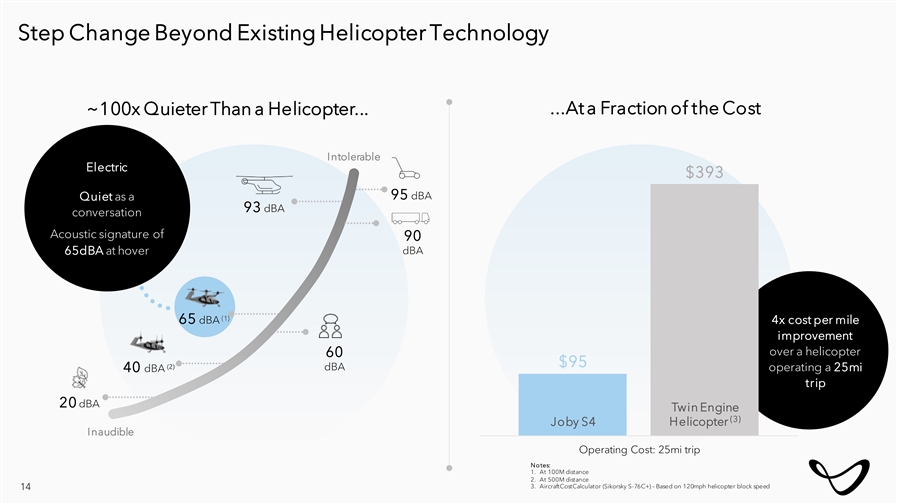

Step Change Beyond Existing Helicopter Technology ...At a Fraction of the Cost ~100x Quieter Than a Helicopter... Intolerable Electric $393 95 dBA Quiet as a 93 dBA conversation Acoustic signature of 90 dBA 65dBA at hover (1) 65 dBA 4x cost per mile improvement over a helicopter 60 $95 (2) dBA operating a 25mi 40 dBA trip 20 dBA Twin Engine (3) Joby S4 Helicopter Inaudible Operating Cost: 25mi trip No tes: 1. At 100M distance 2. At 500M distance 3. AircraftCostCalculator (Sikorsky S-76C+) – Based on 120mph helicopter block speed 14Step Change Beyond Existing Helicopter Technology ...At a Fraction of the Cost ~100x Quieter Than a Helicopter... Intolerable Electric $393 95 dBA Quiet as a 93 dBA conversation Acoustic signature of 90 dBA 65dBA at hover (1) 65 dBA 4x cost per mile improvement over a helicopter 60 $95 (2) dBA operating a 25mi 40 dBA trip 20 dBA Twin Engine (3) Joby S4 Helicopter Inaudible Operating Cost: 25mi trip No tes: 1. At 100M distance 2. At 500M distance 3. AircraftCostCalculator (Sikorsky S-76C+) – Based on 120mph helicopter block speed 14

Best-In-Class Energy Consumption Average Vehicle (1) Occupancy 4,600 (2) 4.0 (3) (4) ICE car 1.1 1,000 2.5 (4) EV car 1.1 - 20 40 60 80 100 Trip distance Miles No tes: 1. Average occupancy does not include pilot(s) 2. Assumes 4 passenger average occupancy in a 6-person helicopter 3. Internal combustion engine calculated at 32mpg 15 4. https://www.gocarma.com/news/2019/11/7/average-vehicle-occupancy-avo-as-a-key-performance-metric Energy consumption per passenger mile Watt-hour / Passenger mileBest-In-Class Energy Consumption Average Vehicle (1) Occupancy 4,600 (2) 4.0 (3) (4) ICE car 1.1 1,000 2.5 (4) EV car 1.1 - 20 40 60 80 100 Trip distance Miles No tes: 1. Average occupancy does not include pilot(s) 2. Assumes 4 passenger average occupancy in a 6-person helicopter 3. Internal combustion engine calculated at 32mpg 15 4. https://www.gocarma.com/news/2019/11/7/average-vehicle-occupancy-avo-as-a-key-performance-metric Energy consumption per passenger mile Watt-hour / Passenger mile

Los Angeles Malibu Santa Monica 15 min 6 min LAX 8 min Anaheim 12 min Long Beach + Aerial ridesharing unlocks the 12 min third dimension of transportation (1) + 5x faster than driving in major metros + Fraction of the infrastructure costs of rail Newport Beach and highway development 15 min + Replicable worldwide No tes: 1. Calculated based on average Joby S-4 speed of 125mph vs. 25mph speed in Los Angeles traffic per Google Maps average travel times at rush hour for each individual trip, averaged across all trips 16Los Angeles Malibu Santa Monica 15 min 6 min LAX 8 min Anaheim 12 min Long Beach + Aerial ridesharing unlocks the 12 min third dimension of transportation (1) + 5x faster than driving in major metros + Fraction of the infrastructure costs of rail Newport Beach and highway development 15 min + Replicable worldwide No tes: 1. Calculated based on average Joby S-4 speed of 125mph vs. 25mph speed in Los Angeles traffic per Google Maps average travel times at rush hour for each individual trip, averaged across all trips 16

Target Global Markets London Berlin Vancouver Paris Chicago San Francisco New York Seoul Dallas Tokyo Washington, D.C. Los Angeles Osaka Houston Miami Dubai Hong Kong Mexico City Bangkok Singapore Rio de Janeiro Sao Paulo Melbourne Key Criteria for Population Travel Distances Existing Airport O&D Fortune 1000 Per Capita GDP Evaluation Density and Congestion Infrastructure Traffic Presence 17Target Global Markets London Berlin Vancouver Paris Chicago San Francisco New York Seoul Dallas Tokyo Washington, D.C. Los Angeles Osaka Houston Miami Dubai Hong Kong Mexico City Bangkok Singapore Rio de Janeiro Sao Paulo Melbourne Key Criteria for Population Travel Distances Existing Airport O&D Fortune 1000 Per Capita GDP Evaluation Density and Congestion Infrastructure Traffic Presence 17

+ Joby Acquired Uber Elevate in January 2021 Combining Industry Leading eVTOL OEM & Operations De-risk go-to-market + Acquired tools, research and team + Market simulation tools will assist with launch planning + Work alongside a world leading operational launch team from UberCopter De-risk demand generation + Uber/Joby to partner in U.S. launch markets for demand generation + Joby to appear in Uber App on a nonexclusive basis, and vice versa 18+ Joby Acquired Uber Elevate in January 2021 Combining Industry Leading eVTOL OEM & Operations De-risk go-to-market + Acquired tools, research and team + Market simulation tools will assist with launch planning + Work alongside a world leading operational launch team from UberCopter De-risk demand generation + Uber/Joby to partner in U.S. launch markets for demand generation + Joby to appear in Uber App on a nonexclusive basis, and vice versa 18

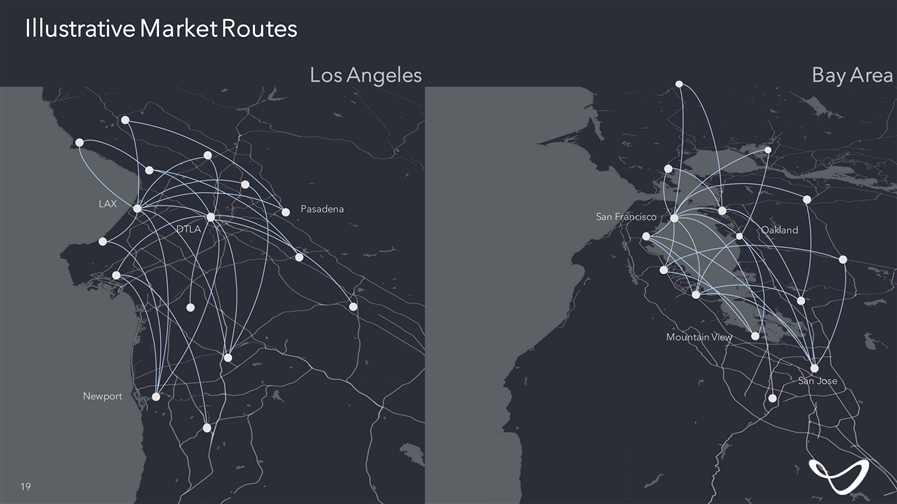

Illustrative Market Routes Los Angeles Bay Area LAX Pasadena San Francisco DTLA Oakland Mountain View San Jose Newport 19Illustrative Market Routes Los Angeles Bay Area LAX Pasadena San Francisco DTLA Oakland Mountain View San Jose Newport 19

Illustrative Market Routes Tri-State Area Miami Highland Beach Boca Raton Stamford White Greenwich Plans Andytown Weston Hollywood Fort Manhattan Lauderdale Miami Beach NEW YORK EWR JFK MIAMI Long Beach 20 Cutler BayIllustrative Market Routes Tri-State Area Miami Highland Beach Boca Raton Stamford White Greenwich Plans Andytown Weston Hollywood Fort Manhattan Lauderdale Miami Beach NEW YORK EWR JFK MIAMI Long Beach 20 Cutler Bay

Type Certificate FAA Part 23 Certification World Class Team Aircraft certified +25 Aircraft Greg Bowles Aggregate years of experience +275 Yrs. Head of Government and Regulatory Affairs Certification experts Former Co-Chairman of the FAA Part 23 +30 People Reorganization Aviation Rulemaking Designated engineer reps (DERs) Committee +17 People Joby Today 21 Unique Program RiskType Certificate FAA Part 23 Certification World Class Team Aircraft certified +25 Aircraft Greg Bowles Aggregate years of experience +275 Yrs. Head of Government and Regulatory Affairs Certification experts Former Co-Chairman of the FAA Part 23 +30 People Reorganization Aviation Rulemaking Designated engineer reps (DERs) Committee +17 People Joby Today 21 Unique Program Risk

Early Revenue Opportunity that Reduces Technology Risk Dual airworthiness tracks with the Department of Defense & the FAA + $40MM+ in Contracts secured with an estimated $120MM+ in progress + Operations in line with FAA certification & future commercial operations + Provides real-time operational data for FAA certification + 3 Government Entity Clients th + Military Flight Release Granted – December 10 ‘20 “We are announcing a world’s first. Joby Aviation is receiving the first military airworthiness approval for an electric vertical takeoff and landing aircraft.” – Dr. Will Roper, U.S. Air Force & Space Force Acquisition, Technology & Logistic Chief 22Early Revenue Opportunity that Reduces Technology Risk Dual airworthiness tracks with the Department of Defense & the FAA + $40MM+ in Contracts secured with an estimated $120MM+ in progress + Operations in line with FAA certification & future commercial operations + Provides real-time operational data for FAA certification + 3 Government Entity Clients th + Military Flight Release Granted – December 10 ‘20 “We are announcing a world’s first. Joby Aviation is receiving the first military airworthiness approval for an electric vertical takeoff and landing aircraft.” – Dr. Will Roper, U.S. Air Force & Space Force Acquisition, Technology & Logistic Chief 22

Preparation for Scaled Manufacturing + Identified facility locations + Acquired site for initial production + Developed in-house tooling + Strategic partnership since Series C in January 2020 brings world leading scaled manufacturing experience & quality to eVTOL sector + Scaled production setup experience + Deep understanding of automation + Technical resource for production 23Preparation for Scaled Manufacturing + Identified facility locations + Acquired site for initial production + Developed in-house tooling + Strategic partnership since Series C in January 2020 brings world leading scaled manufacturing experience & quality to eVTOL sector + Scaled production setup experience + Deep understanding of automation + Technical resource for production 23

2020 Received certification basis Aircraft design lock 2021 Anticipated timeline Certification component level testing to certification and commercialization FAA certification flight test 2022 Ahead of the Demonstration service in select markets competition Mass production facility comes online 2023 FAA Type Certification issued Commercial service launch in initial markets 2024 Global commercial service launched 242020 Received certification basis Aircraft design lock 2021 Anticipated timeline Certification component level testing to certification and commercialization FAA certification flight test 2022 Ahead of the Demonstration service in select markets competition Mass production facility comes online 2023 FAA Type Certification issued Commercial service launch in initial markets 2024 Global commercial service launched 24

Seasoned Management Team with Decades of Experience JoeBen Bevirt Bonny Simi Kate DeHoff Gregor Veble Rob Thodal CEO & Chief Head of Air Ops & General Counsel & Chief Aerodynamicist Head of Airframe Architect People Corporate Secretary Paul Sciarra Eric Allison Joe Brennan Jon Wagner Greg Bowles Executive Chairman Head of Product Head of Head of Powertrain Head of Government Manufacturing and Regulatory Affairs 25Seasoned Management Team with Decades of Experience JoeBen Bevirt Bonny Simi Kate DeHoff Gregor Veble Rob Thodal CEO & Chief Head of Air Ops & General Counsel & Chief Aerodynamicist Head of Airframe Architect People Corporate Secretary Paul Sciarra Eric Allison Joe Brennan Jon Wagner Greg Bowles Executive Chairman Head of Product Head of Head of Powertrain Head of Government Manufacturing and Regulatory Affairs 25

Strong Existing Investor Base 26Strong Existing Investor Base 26

Built Deep Competitive Moat + Expect to be first to market with the right aircraft + 4 passenger aircraft to optimize unit economics + Significant progress in certification + Well developed go-to-market strategy enhanced through Uber Elevate acquisition + World class engineering and certification team + FAA Part 23 general aviation certification enables global reach 27Built Deep Competitive Moat + Expect to be first to market with the right aircraft + 4 passenger aircraft to optimize unit economics + Significant progress in certification + Well developed go-to-market strategy enhanced through Uber Elevate acquisition + World class engineering and certification team + FAA Part 23 general aviation certification enables global reach 27

Financial OverviewFinancial Overview

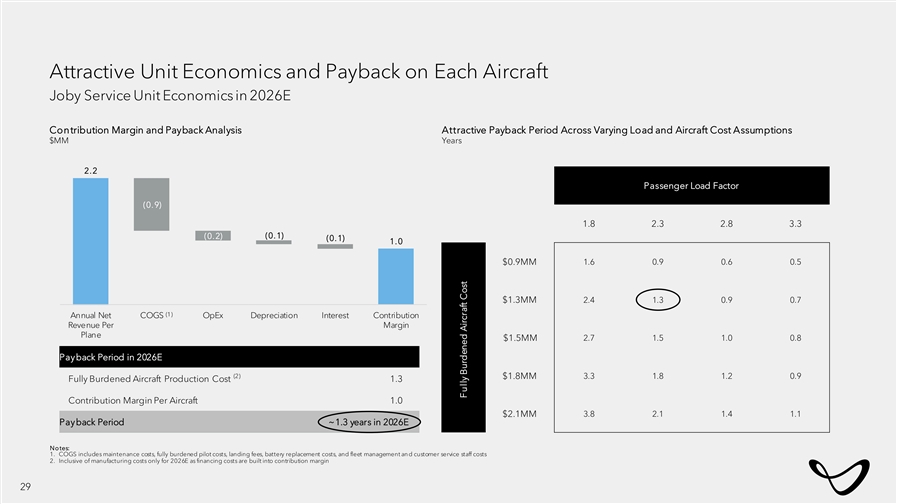

Attractive Unit Economics and Payback on Each Aircraft Joby Service Unit Economics in 2026E Contribution Margin and Payback Analysis Attractive Payback Period Across Varying Load and Aircraft Cost Assumptions $MM Years 2.2 Passenger Load Factor (0.9) 1.8 2.3 2.8 3.3 (0.1) (0.2) (0.1) 1.0 $0.9MM 1.6 0.9 0.6 0.5 $1.3MM 2.4 1.3 0.9 0.7 (1) Annual Net COGS OpEx Depreciation Interest Contribution Revenue Per Margin Plane $1.5MM 2.7 1.5 1.0 0.8 Payback Period in 2026E (2) $1.8MM 3.3 1.8 1.2 0.9 Fully Burdened Aircraft Production Cost 1.3 Contribution Margin Per Aircraft 1.0 $2.1MM 3.8 2.1 1.4 1.1 Payback Period ~1.3 years in 2026E No tes: 1. COGS includes maintenance costs, fully burdened pilot costs, landing fees, battery replacement costs, and fleet management an d customer service staff costs 2. Inclusive of manufacturing costs only for 2026E as financing costs are built into contribution margin 29 Fully Burdened Aircraft CostAttractive Unit Economics and Payback on Each Aircraft Joby Service Unit Economics in 2026E Contribution Margin and Payback Analysis Attractive Payback Period Across Varying Load and Aircraft Cost Assumptions $MM Years 2.2 Passenger Load Factor (0.9) 1.8 2.3 2.8 3.3 (0.1) (0.2) (0.1) 1.0 $0.9MM 1.6 0.9 0.6 0.5 $1.3MM 2.4 1.3 0.9 0.7 (1) Annual Net COGS OpEx Depreciation Interest Contribution Revenue Per Margin Plane $1.5MM 2.7 1.5 1.0 0.8 Payback Period in 2026E (2) $1.8MM 3.3 1.8 1.2 0.9 Fully Burdened Aircraft Production Cost 1.3 Contribution Margin Per Aircraft 1.0 $2.1MM 3.8 2.1 1.4 1.1 Payback Period ~1.3 years in 2026E No tes: 1. COGS includes maintenance costs, fully burdened pilot costs, landing fees, battery replacement costs, and fleet management an d customer service staff costs 2. Inclusive of manufacturing costs only for 2026E as financing costs are built into contribution margin 29 Fully Burdened Aircraft Cost

Base Financial Plan Underpinned by Significant Progress to Date Potential Upside Levers • More efficient scaling of manufacturing • Faster reduction in Revenue per Available Seat Mile ( RASM ) • Improvement in energy density for energy storage Base Case • Faster global adoption of advanced transportation technology than in the U.S. • Utilization upside to drive improvement in plane unit economics • 2-3 city initial rollout starting in 2024 and achieving scale by 2026 Significant Progress Towards Our Business Plan • Add newer cities only after meaningful • Significant data assets from Uber Elevate with leading operational launch team penetration of initial • World-class engineering and certification team rollout cities • Route-by-route demand analysis for target launch cities • Streamlined certification process with FAA under Part 23 that will have global acceptability • Identified and acquired manufacturing facilities including factory location and land • Majority of components and tooling designed in-house 30Base Financial Plan Underpinned by Significant Progress to Date Potential Upside Levers • More efficient scaling of manufacturing • Faster reduction in Revenue per Available Seat Mile ( RASM ) • Improvement in energy density for energy storage Base Case • Faster global adoption of advanced transportation technology than in the U.S. • Utilization upside to drive improvement in plane unit economics • 2-3 city initial rollout starting in 2024 and achieving scale by 2026 Significant Progress Towards Our Business Plan • Add newer cities only after meaningful • Significant data assets from Uber Elevate with leading operational launch team penetration of initial • World-class engineering and certification team rollout cities • Route-by-route demand analysis for target launch cities • Streamlined certification process with FAA under Part 23 that will have global acceptability • Identified and acquired manufacturing facilities including factory location and land • Majority of components and tooling designed in-house 30

Capital Raise Expected to Fund Commercialization in 2024 No Anticipated Further Capital Needs Beyond SPAC and PIPE Transaction to Begin Operations 2021E 2022E 2023E 2024E 2025E 2026E Income Statement Items Total Revenue – – – 131 721 2,050 Growth (%) 450% 185% (1) Recurring Aircraft Revenue – – – – 186 796 New Aircraft Revenue – – – 131 535 1,254 R ecurring Aircraft Revenue Contribution (%) 26% 39% (2) (-) Cost of Goods Sold – – – 55 304 867 Gross Profit––– 76 417 1,183 Gross Profit Margin (%) 58% 58% 58% (3) A djusted EBITDA (151) (190) (165) (69) 185 824 (3) Adjusted EBITDA Margin (%) 26% 40% Total Capex 58 68 166 552 903 1,444 Depreciation & Amortization 3 7 19 47 113 219 Assumptions Revenue Generating Aircraft (Average) 2 7 26 141 413 963 Number of Cities – – – 1 2 3 No tes: 1. Recurring Aircraft Revenue = Prior Year Average Aircraft * Current Year Revenue per Plane; Joby Service segment only 2. COGS includes pilot costs, maintenance labor and parts costs, fleet management and customer service staff costs, and battery replacement costs 31 3. Adjusted EBITDA is a non-GAAP financial metric defined by us as net loss or gain before interest expense, provision for income taxes, depreciation and amortization expense, and stock based compensationCapital Raise Expected to Fund Commercialization in 2024 No Anticipated Further Capital Needs Beyond SPAC and PIPE Transaction to Begin Operations 2021E 2022E 2023E 2024E 2025E 2026E Income Statement Items Total Revenue – – – 131 721 2,050 Growth (%) 450% 185% (1) Recurring Aircraft Revenue – – – – 186 796 New Aircraft Revenue – – – 131 535 1,254 R ecurring Aircraft Revenue Contribution (%) 26% 39% (2) (-) Cost of Goods Sold – – – 55 304 867 Gross Profit––– 76 417 1,183 Gross Profit Margin (%) 58% 58% 58% (3) A djusted EBITDA (151) (190) (165) (69) 185 824 (3) Adjusted EBITDA Margin (%) 26% 40% Total Capex 58 68 166 552 903 1,444 Depreciation & Amortization 3 7 19 47 113 219 Assumptions Revenue Generating Aircraft (Average) 2 7 26 141 413 963 Number of Cities – – – 1 2 3 No tes: 1. Recurring Aircraft Revenue = Prior Year Average Aircraft * Current Year Revenue per Plane; Joby Service segment only 2. COGS includes pilot costs, maintenance labor and parts costs, fleet management and customer service staff costs, and battery replacement costs 31 3. Adjusted EBITDA is a non-GAAP financial metric defined by us as net loss or gain before interest expense, provision for income taxes, depreciation and amortization expense, and stock based compensation

Key Assumptions and Performance Indicators in 2026 Joby Service Aircraft Utilization (1) • Average of 963 total aircraft (850 in Service segment)• ~7 hours spent in flight per day with ~12 operating hours • Fully loaded manufacturing cost of $1.3MM per aircraft• ~12.4MM total flights per year with ~35.4k flights per day • Average useful life of ~50k flight hours which equates to over 15 • Average trip length of 24 miles years • Load factor of 2.3 passengers per trip Bottoms-Up Cost Analysis Revenue & Payback • Fully loaded annual COGS, operating expense, depreciation, and • Net revenue of $2.2MM and $1.0MM annual profit per plane interest of $1.2MM per aircraft • Based on $1.3MM cost, payback period of ~1.3 years – COGS includes pilots, landing fees, customer service, and • Price point of $3.00 per seat mile ($1.73 RASM at full load maintenance factor) is cheaper than Uber Black for an individual – Operating expenses includes SG&A (2) • Fully burdened CASM of $0.86 No tes: 1. Assumes 14 operating hours per weekday and 8 operating hours per weekend day 2. CASM = (COGS plus operating expense plus depreciation) / Total Available Seat Miles of 1,188MM 32Key Assumptions and Performance Indicators in 2026 Joby Service Aircraft Utilization (1) • Average of 963 total aircraft (850 in Service segment)• ~7 hours spent in flight per day with ~12 operating hours • Fully loaded manufacturing cost of $1.3MM per aircraft• ~12.4MM total flights per year with ~35.4k flights per day • Average useful life of ~50k flight hours which equates to over 15 • Average trip length of 24 miles years • Load factor of 2.3 passengers per trip Bottoms-Up Cost Analysis Revenue & Payback • Fully loaded annual COGS, operating expense, depreciation, and • Net revenue of $2.2MM and $1.0MM annual profit per plane interest of $1.2MM per aircraft • Based on $1.3MM cost, payback period of ~1.3 years – COGS includes pilots, landing fees, customer service, and • Price point of $3.00 per seat mile ($1.73 RASM at full load maintenance factor) is cheaper than Uber Black for an individual – Operating expenses includes SG&A (2) • Fully burdened CASM of $0.86 No tes: 1. Assumes 14 operating hours per weekday and 8 operating hours per weekend day 2. CASM = (COGS plus operating expense plus depreciation) / Total Available Seat Miles of 1,188MM 32

Transaction Overview (1) Sources and Uses and Pro-Forma Ownership with $910MM of Committed Funding $MM, except per share data Sources Pro-Forma Valuation Rollover Equity $5,000 Share Price $10.00 (2) Reinvent Cash Held in Trust 690 Pro-Forma Shares Outstanding 660 (1) Committed Funding 910 Equity Value $6,600 Total Sources $6,600 + Debt 3 (3) - Net Cash (1,974) Uses Aggregate Value $4,629 (2) Cash Proceeds to Joby $1,528 (2) Illustrative Pro-Forma Ownership Equity Consideration to Joby Existing Investors 5,000 Estimated Transaction Costs 72 SPAC Public Holders Total Uses $6,600 10% (1) Existing Holders PIPE Holders 76% 14% No tes: 1. Committed Funding is inclusive of an $835MM fully committed PIPE and a $75MM Uber convertible note which converts immediately prior to transaction closing; the 7.5MM shares to be issued to Uber are excluded from the Equity Consideration to Joby's Existing Investors 2. Pro-forma shares outstanding based on $10.00 per share price and excludes potential dilution from out-of-the-money Reinvent warrants and out-of-of the-money founder shares. Pro-forma further assumes no redemptions by Reinvent's existing public shareholders. Private warrants restructured to match public warrant terms 3. Includes $446MM of existing Joby cash and cash equivalents as of December 31, 2020 and $1,528MM of net proceeds to be added t o Joby's balance sheet 33Transaction Overview (1) Sources and Uses and Pro-Forma Ownership with $910MM of Committed Funding $MM, except per share data Sources Pro-Forma Valuation Rollover Equity $5,000 Share Price $10.00 (2) Reinvent Cash Held in Trust 690 Pro-Forma Shares Outstanding 660 (1) Committed Funding 910 Equity Value $6,600 Total Sources $6,600 + Debt 3 (3) - Net Cash (1,974) Uses Aggregate Value $4,629 (2) Cash Proceeds to Joby $1,528 (2) Illustrative Pro-Forma Ownership Equity Consideration to Joby Existing Investors 5,000 Estimated Transaction Costs 72 SPAC Public Holders Total Uses $6,600 10% (1) Existing Holders PIPE Holders 76% 14% No tes: 1. Committed Funding is inclusive of an $835MM fully committed PIPE and a $75MM Uber convertible note which converts immediately prior to transaction closing; the 7.5MM shares to be issued to Uber are excluded from the Equity Consideration to Joby's Existing Investors 2. Pro-forma shares outstanding based on $10.00 per share price and excludes potential dilution from out-of-the-money Reinvent warrants and out-of-of the-money founder shares. Pro-forma further assumes no redemptions by Reinvent's existing public shareholders. Private warrants restructured to match public warrant terms 3. Includes $446MM of existing Joby cash and cash equivalents as of December 31, 2020 and $1,528MM of net proceeds to be added t o Joby's balance sheet 33

Analogous Autonomous Ridesharing Precedents Validates Valuation Upside Valuation Across Last Five Rounds Latest Valuation +Recent validations from $Bn $Bn autonomous ridesharing $30Bn 30 precedents +Large, untapped addressable $19Bn 20 markets $15Bn $31Bn $12Bn +Pre-commercialization phase 10 +Service-based models with $1Bn strong network effect - 2016 2018 2018 2019 2021 2020 L ead +Specialized hardware Investor: + Waymo and its autonomous taxi business was most recently valued at $31Bn +Significant ability to scale + Service based model, with limited vertical Employee integration 35 ~350 ~350+ 1,500 1,650+ Count: + Low margins given expectation for continued aggressive growth S o urce: PitchBook 34Analogous Autonomous Ridesharing Precedents Validates Valuation Upside Valuation Across Last Five Rounds Latest Valuation +Recent validations from $Bn $Bn autonomous ridesharing $30Bn 30 precedents +Large, untapped addressable $19Bn 20 markets $15Bn $31Bn $12Bn +Pre-commercialization phase 10 +Service-based models with $1Bn strong network effect - 2016 2018 2018 2019 2021 2020 L ead +Specialized hardware Investor: + Waymo and its autonomous taxi business was most recently valued at $31Bn +Significant ability to scale + Service based model, with limited vertical Employee integration 35 ~350 ~350+ 1,500 1,650+ Count: + Low margins given expectation for continued aggressive growth S o urce: PitchBook 34

Vertically Integrated Model Will Provide for Strong Growth and Margins Joby Boasts Substantial Scale of up to ~4x Other Emerging Technology Winners ’25E Revenue ($Bn) Revenue Growth Emerging Technology Winners Disruptive Transportation Vertically Integrated Platforms 2025E Peer Revenues and 2021E-2025E CAGR unless otherwise noted (2) 0.7 2.1 3.2 0.9 0.5 0.8 18.6 209.4 8.3 39.7 174.3 51.2 114.7 485% 512% Median: 174% 199% 185% 149% 132% Median: 32% Median: 14% 39% 38% 26% 22% 17% 14% 13% (2) 2025E 2026E (1) (3) EBITDA Margin 2025E Peer EBITDA Margin unless otherwise noted Median: 32% 40% 39% Median: 32% 37% 35% 28% 25% Median: 15% 32% 25% 26% 17% 17% 8% 13% (3) 2025E 2026E (1) (2) S o urce: Wall Street Research Estimates as of January 26 2021, Investor Presentations No tes: 1. Joby Revenue growth shown year-over-year for 2025E and 2026E. Revenue and Adjusted EBITDA margin as of 2025E and 2026E respectively. Adjusted EBITDA is a non-GAAP financial metric defined by us as net loss or gain before interest expense, provision for income taxes, depreciation and amortization expense, and stock based compensation 2. Revenue growth CAGR calculated from 2025E-2028E; revenue and EBITDA margin as of 2028E 35 3. Estimates based on investor presentation at time of transaction announcementVertically Integrated Model Will Provide for Strong Growth and Margins Joby Boasts Substantial Scale of up to ~4x Other Emerging Technology Winners ’25E Revenue ($Bn) Revenue Growth Emerging Technology Winners Disruptive Transportation Vertically Integrated Platforms 2025E Peer Revenues and 2021E-2025E CAGR unless otherwise noted (2) 0.7 2.1 3.2 0.9 0.5 0.8 18.6 209.4 8.3 39.7 174.3 51.2 114.7 485% 512% Median: 174% 199% 185% 149% 132% Median: 32% Median: 14% 39% 38% 26% 22% 17% 14% 13% (2) 2025E 2026E (1) (3) EBITDA Margin 2025E Peer EBITDA Margin unless otherwise noted Median: 32% 40% 39% Median: 32% 37% 35% 28% 25% Median: 15% 32% 25% 26% 17% 17% 8% 13% (3) 2025E 2026E (1) (2) S o urce: Wall Street Research Estimates as of January 26 2021, Investor Presentations No tes: 1. Joby Revenue growth shown year-over-year for 2025E and 2026E. Revenue and Adjusted EBITDA margin as of 2025E and 2026E respectively. Adjusted EBITDA is a non-GAAP financial metric defined by us as net loss or gain before interest expense, provision for income taxes, depreciation and amortization expense, and stock based compensation 2. Revenue growth CAGR calculated from 2025E-2028E; revenue and EBITDA margin as of 2028E 35 3. Estimates based on investor presentation at time of transaction announcement

Joby Valuation Consistent with High Growth, Disruptive Companies… …And Conservative on a Cash Flow Basis Current AV / 2025E Revenue x 18.5x 16.4x Median: 11.5x Median: 4.5x 6.4x Median: 3.5x 6.7x 5.3x 5.0x 4.5x 3.2x 4.6x 3.4x 2.5x 1.7x 2.3x (2) 2025E 2026E (3) (1) Current AV / 2025E EBITDA x 69.3x 67.1x Median: 35.2x 44.0x 36.6x Median: 25.6x Median: 13.7x 25.0x 26.4x 13.7x 14.4x 12.7x 14.7x 9.9x 8.7x 5.6x (2) 2025E 2026E (3) (1) Emerging Technology Winners Disruptive Transportation Vertically Integrated Platforms S o urce: Wall Street Research Estimates as of January 26, 2021, Investor Presentations No tes: 1. Assumes pro-forma aggregate value of $4.6Bn. Adjusted EBITDA is a non-GAAP financial metric defined by us as net loss or gain before interest expense, provision for income taxes, depreciation and amortization expense, and stock based compensation 2. Based on 2028E estimates 3. Aggregate value based on InterPrivate Acquisition Corp’s share price as of January 26, 2021, AEVA's pro-forma shares outstanding and net debt from the time of announcement. Revenue and EBITDA estimates based on investor presentation at time of transaction 36 announcementJoby Valuation Consistent with High Growth, Disruptive Companies… …And Conservative on a Cash Flow Basis Current AV / 2025E Revenue x 18.5x 16.4x Median: 11.5x Median: 4.5x 6.4x Median: 3.5x 6.7x 5.3x 5.0x 4.5x 3.2x 4.6x 3.4x 2.5x 1.7x 2.3x (2) 2025E 2026E (3) (1) Current AV / 2025E EBITDA x 69.3x 67.1x Median: 35.2x 44.0x 36.6x Median: 25.6x Median: 13.7x 25.0x 26.4x 13.7x 14.4x 12.7x 14.7x 9.9x 8.7x 5.6x (2) 2025E 2026E (3) (1) Emerging Technology Winners Disruptive Transportation Vertically Integrated Platforms S o urce: Wall Street Research Estimates as of January 26, 2021, Investor Presentations No tes: 1. Assumes pro-forma aggregate value of $4.6Bn. Adjusted EBITDA is a non-GAAP financial metric defined by us as net loss or gain before interest expense, provision for income taxes, depreciation and amortization expense, and stock based compensation 2. Based on 2028E estimates 3. Aggregate value based on InterPrivate Acquisition Corp’s share price as of January 26, 2021, AEVA's pro-forma shares outstanding and net debt from the time of announcement. Revenue and EBITDA estimates based on investor presentation at time of transaction 36 announcement

Cash Flows Support Attractive Entry Point for Investors Present Value of Future Aggregate Value at an Illustrative 20% Discount Rate + Applies a 25-30x AV / EBITDA multiple range to Joby’s 2026E EBITDA to arrive at an Implied Future Aggregate Value + The applied multiple range is representative of the long-term valuation of premier vertically integrated platforms + Implied Future Aggregate Value is discounted 4.75 years back at an illustrative 20% rate to arrive at an Implied Current Aggr egate Value Discounted Aggregate Value Analysis $Bn $24.7Bn $20.6Bn $10.4Bn $8.7Bn $4.6Bn (1) (1) 25-30x 2026E Adjusted EBITDA 25-30x 2026E Adjusted EBITDA 2.3x 2026E Revenue Implied Notional Aggregate Value Post-Money Aggregate Value Implied Current Aggregate Value at 20% Discount Rate Significant potential for continued value creation as market matures and Joby rolls out to additional cities No tes: 37 1. Adjusted EBITDA is a non-GAAP financial metric defined by us as net loss or gain before interest expense, provision for income t axes, depreciation and amortization expense, and stock-based compensationCash Flows Support Attractive Entry Point for Investors Present Value of Future Aggregate Value at an Illustrative 20% Discount Rate + Applies a 25-30x AV / EBITDA multiple range to Joby’s 2026E EBITDA to arrive at an Implied Future Aggregate Value + The applied multiple range is representative of the long-term valuation of premier vertically integrated platforms + Implied Future Aggregate Value is discounted 4.75 years back at an illustrative 20% rate to arrive at an Implied Current Aggr egate Value Discounted Aggregate Value Analysis $Bn $24.7Bn $20.6Bn $10.4Bn $8.7Bn $4.6Bn (1) (1) 25-30x 2026E Adjusted EBITDA 25-30x 2026E Adjusted EBITDA 2.3x 2026E Revenue Implied Notional Aggregate Value Post-Money Aggregate Value Implied Current Aggregate Value at 20% Discount Rate Significant potential for continued value creation as market matures and Joby rolls out to additional cities No tes: 37 1. Adjusted EBITDA is a non-GAAP financial metric defined by us as net loss or gain before interest expense, provision for income t axes, depreciation and amortization expense, and stock-based compensation

Long-Term Targets in Line with Joby’s Mission In Approximately 10 Years, Joby Estimates to Have + ~14K vehicles generating ~$20Bn Revenue + ~5Bn miles flown + Presence in over 20 cities worldwide + Adjusted EBITDA margin of ~35% + ~50%+ recurring aircraft revenue contribution Reinforcing Competitive Advantage Over Time + Joby is positioned to be the world’s leading operator of aerial ridesharing vehicles 38Long-Term Targets in Line with Joby’s Mission In Approximately 10 Years, Joby Estimates to Have + ~14K vehicles generating ~$20Bn Revenue + ~5Bn miles flown + Presence in over 20 cities worldwide + Adjusted EBITDA margin of ~35% + ~50%+ recurring aircraft revenue contribution Reinforcing Competitive Advantage Over Time + Joby is positioned to be the world’s leading operator of aerial ridesharing vehicles 38

+Key megatrends: sustainability, urbanization, and new mobility technologies +Massive global TAM +Vertically integrated on-demand business model generates recurring revenue +Zero emissions, quiet, electric, piloted aircraft in FAA certification process Joby exists to save +World class technical & certification team of 600+ employees a billion people an +Pre-service revenues from government contracts de-risk commercialization hour a day +Compelling unit economics: 45% contributionmargin & less than 2- year aircraft payback +Strong partners & investors: Toyota, Uber,Department of Defense,and more +Plan to commercialize aerial ridesharing in a phased roll-out by 2024 39+Key megatrends: sustainability, urbanization, and new mobility technologies +Massive global TAM +Vertically integrated on-demand business model generates recurring revenue +Zero emissions, quiet, electric, piloted aircraft in FAA certification process Joby exists to save +World class technical & certification team of 600+ employees a billion people an +Pre-service revenues from government contracts de-risk commercialization hour a day +Compelling unit economics: 45% contributionmargin & less than 2- year aircraft payback +Strong partners & investors: Toyota, Uber,Department of Defense,and more +Plan to commercialize aerial ridesharing in a phased roll-out by 2024 39

4040