Filed by Apollo Strategic Growth Capital

Pursuant to Rule 425 under the Securities Act of 1933, as amended,

and deemed filed pursuant to Rule 14a-12 under the

Securities Exchange Act of 1934, as amended.

Subject Company: Apollo Strategic Growth Capital

File No.: 001-39576

Date: April 12, 2022

Beginning on April 12, 2022, representatives of GBT JerseyCo Limited and Apollo Strategic Growth Capital will meet with certain investors to discuss the proposed business combination. The presentation to be used during such meetings is set forth below.

Amex GBT Investor Day April 12, 2022

Legal Disclaimer This presentation (the “Presentation”) has been prepared by GBT JerseyCo Limited (“Amex GBT”) and Apollo Strategic Growth Capital (“APSG”) in connection with a potential business combination involvi ng Amex GBT and APSG (the “Business Combination”) and is preliminary in nature and solely for information and discussion purposes and must not be relie d u pon for any other purpose. This Presentation includes the slides that follow, the oral presentation of the slides by members of Amex GBT or APSG or any person on their behalf, the question - and - answer session that follows that oral presentatio n, copies of this document and any materials distributed at, or in connection with, that Presentation. By participating in the meeting, or by reading the Presentation slides, you will be deemed to have ( i ) agreed to the following limitations and notifications and made the following undertakings and (ii) acknowledged that you un der stand the legal and regulatory sanctions attached to the misuse, disclosure or improper circulation of this Presentation. Amex GBT is a joint venture that is not wholly owned by American Express or any of its subsidiaries. Forward - Looking Statements This Presentation contains certain “forward - looking statements” within the meaning of the Private Securities Litigation Reform A ct of 1995, Section 27A of the Securities Act of 1933 (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended. All statements other than statements of historical fact contained in this Presentation, inc lud ing market size and growth opportunities, are forward - looking statements. Some of these forward - looking statements can be identified by the use of forward - looking words, including “anticipate,” “expect,” “suggests,” “plan,” “believe ,” “intend,” “estimates,” “targets,” “predicts,” “projects,” “should,” “could,” “would,” “may,” “will,” “continue,” “forecast ” or other similar expressions. All forward - looking statements are based upon estimates and forecasts and reflect the views, assum ptions, expectations, and opinions of Amex GBT and APSG as of the date of this Presentation, and may include, without limitation, changes in general economic conditions as a result of COVID - 19, all of which are accordingly subjec t to change. Any such estimates, assumptions, expectations, forecasts, views or opinions set forth in this Presentation should be regarded as indicative, preliminary and for illustrative purposes only and should not be relied upon a s b eing necessarily indicative of future results. In some cases, forward - looking statements included in this Presentation, including financial projections, may be consistent with previously issued forward - looking statements, even in circ umstances where the assumptions underlying such statements have changed. The forward - looking statements contained in this Presentation are subject to a number of factors, risks and uncertainties, some of which are not currently k now n to APSG and Amex GBT. You should carefully consider the risks and uncertainties described in the “Risk Factors” section of APSG’s registration statement on Form S - 4 (file no. 333 - 261820), filed with the SEC on December 21, 2021 and amended on February 4, 2022 and March 21, 2022 (as amended from time to time, the “Registration Statement”). The Registration Statement identifies and addresses other important risks and uncertainties that could cause act ual events and results to differ materially from expected results contained in the forward - looking statements. Most of these factors are outside APSG’s and Amex GBT’s control and are difficult to predict. Factors that may cause such differen ces include, but are not limited to: (1) the outcome of any legal proceedings that may be instituted against APSG or Amex GBT following the announcement of the Business Combination; (2) the inability to complete the Business Combination, i ncl uding due to the inability to concurrently close the Business Combination and the PIPE or due to failure to obtain approval of the shareholders of APSG; (3) delays in obtaining, adverse conditions contained in, or the inability to ob tai n necessary regulatory approvals or complete regulatory reviews required to complete the Business Combination; (4) the risk that the Business Combination disrupts current plans and operations as a result of the announcement and consumma tio n of the Business Combination; (5) the inability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition, the ability of the combined company to grow and manag e g rowth profitably, maintain relationships with customers and suppliers and retain key employees; (6) costs related to the Business Combination; (7) changes in the applicable laws or regulations; (8) the possibility that the combined co mpany may be adversely affected by other economic, business, and/or competitive factors; (9) the impact of the global COVID - 19 pandemic; and (10) other risks and uncertainties described in the Registration Statement. APSG and Amex GBT caut ion that the foregoing list of factors is not exclusive and not to place undue reliance upon any forward - looking statements, which speak only as of the date made. Neither APSG nor Amex GBT undertakes or accepts any obligation to r ele ase publicly any updates, corrections or revisions to any other forward - looking statements to reflect any change in its expectations or existing circumstances or conditions or any subsequent change in events, conditions or circumst anc es on which any such statement is based, except as required by law. No Offer or Solicitation This Presentation is for informational purposes only and does not constitute an offer to sell or purchase, or a solicitation of an offer to sell, buy or subscribe for, any securities in any jurisdiction, or a solicitation of any proxy, vote, consent or approval relating to the Business Combination or otherwise in any jurisdiction, nor shall there be any sale of securities in any jurisdiction in which the offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such jurisdictions. Additional Information and Where to Find It In connection with the proposed Business Combination, APSG has filed with the SEC the Registration Statement, containing a pr eli minary prospectus and a preliminary proxy statement, and, after the Registration Statement is declared effective, APSG will mail a definitive proxy statement/prospectus relating to the proposed Business Combination to its shareh old ers. This Presentation does not contain all the information that should be considered concerning the proposed Business Combination and is not intended to form the basis of any investment decision or any other decision in respect of the Bu siness Combination. APSG’s shareholders and other interested persons are advised to read the Registration Statement, including the preliminary proxy statement/prospectus, and the amendments thereto, and, when available, the definit ive proxy statement/prospectus and other documents filed in connection with the proposed Business Combination, as these materials contain, or will contain, important information about Amex GBT, APSG and the proposed Busines s C ombination. When available, the definitive proxy statement/prospectus and other relevant materials for the proposed Business Combination will be mailed to shareholders of APSG as of a record date to be established for voting on the proposed Business Combination. Such shareholders will also be able to obtain copies of the preliminary proxy statement/prospectus, the definitive proxy statement/prospectus and other documents filed with the SEC, without charge, wh en available, at the SEC’s website at www.sec.gov, or by directing a request to Apollo Strategic Growth Capital, 9 West 57th Street, 43rd Floor, New York, NY 10019, Attention: James Crossen , (212) 515 - 3200. Participants in the Solicitation APSG, Amex GBT and their respective directors and executive officers may be deemed to be participants in the solicitation of pro xies from the shareholders of APSG with respect to the Business Combination. Information regarding APSG’s and Amex GBT’s respective directors and executive officers is contained in the Registration Statement. Free copies of the Registration Statement may be obtained as described in the preceding paragraph. 2

Legal Disclaimer Non - GAAP Financial Measures : We report our financial results in accordance with GAAP. Our non - GAAP financial measures are provided in addition to, and should not be considered as an alternative to, other performance or liquidity measure derived in accordance with GAAP. Non - GAAP financial measures have limitations as analytical tools, and you should not consider them either in isolation or as a substitute for analyzing our results as reported under GAAP. In addition, because not all companies use identical calculations, the presentations of our non - GAAP financial measures may not be comparable to other similarly titled mea sures of other companies and can differ significantly from company to company. Management believes that these non - GAAP financial measures provide users of our financial information with useful supplemental i nformation that enables a better comparison of our performance or liquidity across periods. In addition, we use certain of these non - GAAP financial measures as performance measures as they are important metrics used by management to eva luate and understand the underlying operations and business trends, forecast future results and determine future capital investment locations. We also use certain of our non - GAAP financial measures as indicators of our abili ty to generate cash to meet our liquidity needs and to assist our management in evaluating our financial flexibility, capital structure and leverage. These non - GAAP financial measures supplement comparable GAAP measures in the evalua tion of the effectiveness of our business strategies, to make budgeting decisions, and/or to compare our performance and liquidity against that of other peer companies using similar measures. We define Adjusted EBITDA as net loss before interest income, interest expense, benefit from (provision for) income taxes and de preciation and amortization excluding costs that management believes are non - core to the underlying business of Amex GBT, consisting of restructuring costs, integration costs, costs related to mergers and acquisitions, separa tio n costs, non - cash equity - based compensation, certain corporate costs, foreign currency gains (losses), non - service components of net periodic pension benefit (costs) and gains (losses) on disposal of businesses. Adjusted EBITDA is a supplemental non - GAAP financial measure of operating performance that does not represent and should not be considered as an alternative to net (loss) income or total operating expenses, as determined under GAAP. In addition, this measure may not be comparable to similarly titled measures used by other companies. This non - GAAP measur e has limitations as an analytical tool, and this measure should not be considered in isolation or as a substitute for analysis of Amex GBT’s results or expenses as reported under GAAP. Some of these limitations are that this mea sur e does not reflect: ▪ changes in, or cash requirements for, our working capital needs or contractual commitments; ▪ our interest expense, or the cash requirements to service interest or principal payments on our indebtedness; ▪ our tax expense, or the cash requirements to pay our taxes; recurring, non - cash expenses of depreciation and amortization of pro perty and equipment and definite - lived intangible assets and, although these are non - cash expenses, the assets being depreciated and amortized may have to be replaced in the future; ▪ the non - cash expense of stock - based compensation, which has been, and will continue to be for the foreseeable future, an importa nt part of how we attract and retain our employees and a significant recurring expense in our business; ▪ restructuring, mergers and acquisition and integration costs, all of which are intrinsic of our acquisitive business model; a nd ▪ impact on earnings or changes resulting from matters that we consider not to be indicative of our future operations. Adjusted EBITDA should not be considered as a measure of liquidity or as a measure determining discretionary cash available t o u s to reinvest in the growth of our business or as measures of cash that will be available to us to meet our obligations. We believe that the adjustments applied in presenting Adjusted EBITDA is appropriate to provide additional infor mat ion to investors about certain material non - cash and other items that management believes are non - core to the underlying business of Amex GBT. We use this measure as a performance measure as it is an important metric used by management to evaluate and understand the u nde rlying operations and business trends, forecast future results and determine future capital investment allocations. This non - GAAP measure supplements comparable GAAP measures in the evaluation of the effectiveness of our business s trategies, to make budgeting decisions, and to compare our performance against that of other peer companies using similar measures. We also believe that Adjusted EBITDA is helpful supplemental measures to assist potential i nve stors and analysts in evaluating our operating results across reporting periods on a consistent basis. We define Free Cash Flow as net cash (used in) from operating activities, less cash used for additions to property and equipm ent . We believe Free Cash Flow is an important measure of our liquidity. This measure is a useful indicator of our ability to gene rat e cash to meet our liquidity demands. We use this measure to conduct and evaluate our operating liquidity. We believe it typically presents an alternate measure of cash flows since purchases of property and equipment are a necessary co mpo nent of our ongoing operations and it provides useful information regarding how cash provided by operating activities compares to the property and equipment investments required to maintain and grow our platform. We believe Free Cas h F low provides investors with an understanding of how assets are performing and measures management’s effectiveness in managing cash. Free Cash Flow is a non - GAAP measure and may not be comparable to similarly named measures used by other companies. This measure has limitations in that it does not represent the total increase or decrease in the cash balance for the period, nor does it represent cash flow for discretionary expenditures. This measure should not be considered as a measur e o f liquidity or cash flows from operations as determined under GAAP. This measure is not measurement of our financial performance under GAAP and should not be considered in isolation or as alternative to net (loss) income or any othe r p erformance measures derived in accordance with GAAP or as an alternative to cash flows from operating activities as a measure of liquidity. 3

Legal Disclaimer Pro Forma Financial Information: This Presentation includes certain pro forma financial information. The pro forma adjustments assume that Amex GBT acquired E gen cia and the Business Combination was consummated as of January 1, 2021. The pro forma financial information is unaudited and is presented for illustrative purposes only and is not necessarily indicative of the operating r esu lts or financial position that would have occurred if the relevant transactions had been consummated on the date indicated, nor is it indicative of future operating results. The pro forma financial information presented is calculated in a ma nner similar to the pro forma financial statements prepared in accordance with Regulation S - X under the Securities Act as amended by the final rule, Release No. 33 - 10786 “Amendments to Financial Disclosures about Acquired and Disposed Business es.” No Representations and Warranties: Neither Amex GBT and APSG, nor any of their respective directors, officers, employees, advisors, representatives or agents ma ke any representation or warranty of any kind, express or implied, as to the value of Amex GBT or APSG or the accuracy or completeness of the information contained in this Presentation, and none of them shall have any liability bas ed on or arising from, in whole or in part, any information contained in, or omitted from, this Presentation or for any other written or oral communication transmitted to any person or entity in the course of its evaluation of Amex GBT or APSG. No warranty of any kind, implied, expressed or statutory, is given in conjunction with the information set forth herein. Amex GBT makes no representations or warranties, express or implied, as to the accuracy or completeness of any inform ati on, statements and estimates presented herein. Neither the SEC nor the securities regulatory authority of any state, foreign or other jurisdiction has passed upon the merits of, or the accuracy or adequacy of, any of the informatio n c ontained in this Presentation. Use of Projections: This Presentation contains projected financial information with respect to Amex GBT, including, but not limited to, estimated re sults for fiscal years 2021 through 2023. Such projected financial information constitutes forward - looking information and are presented as goals or an illustration of the results that could be generated given a set of hypothetical ass umptions that may prove to be incorrect. Such projected financial information should not be viewed as guidance and is not based on Amex GBT’s historical operating results and should not be relied upon as necessarily indicative of future re sults or Amex GBT’s actual economics. The assumptions and estimates underlying such financial forecast information are inherently uncertain and are subject to a wi de variety of significant business, economic, competitive and other risks and uncertainties, a number of which are beyond the control of either Amex GBT or APSG and subject to change, that could cause actual results to differ materially fro m t hose contained in the prospective financial information. Actual results may differ materially from the results contemplated by the financial forecast information contained in this Presentation, and the inclusion of such information in t his Presentation should not be regarded as a representation by any person that the results reflected in such forecasts will be achieved. Even if projected financial information remains unchanged from previously disclosed projected fi nan cial information, the assumptions underlying the information may have changed and may continue to change. Neither APSG’s nor Amex GBT’s independent auditors have audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this Presentation, and accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this Presentation. Moreo ver , Amex GBT operates in a very competitive and rapidly changing environment, and new risks may emerge from time to time. It is not possible to predict all risks, nor assess the impact of all factors on Amex GBT’s business or th e e xtent to which any factor, or combination of factors, may cause Amex GBT’s actual results, performance or financial condition to be materially different from the expectations of future results, performance of financial condition. Except to t he extent required by applicable federal securities law, neither APSG nor Amex GBT or any of their respective affiliates intends to update, revise or correct any projected financial information to reflect circumstances existing or arising after t he date such projected financial information was generated or to reflect the occurrence of future events. In addition, the analyses of Amex GBT and APSG contained herein are not, and do not purport to be, appraisals of the securities, assets or bus ine ss of Amex GBT, APSG or any other entity. Industry and Market Data: This Presentation also contains information, estimates and other statistical data derived from third party sources, including re search, surveys or studies, some of which are preliminary drafts, conducted by third parties, information provided by customers and/or industry or general publications. Such information involves a number of assumptions and limitations and d ue to the nature of the techniques and methodologies used in market research, none of Amex GBT, APSG or the third party can guarantee the accuracy of such information. You are cautioned not to give undue weight on such estimates. Am ex GBT and APSG have not independently verified any such third party information, and make no representation as to the accuracy of, such third - party information. Trademarks, Service Marks and Trade Names: Amex GBT and APSG own or have rights to various trademarks, service marks and trade names that they use in connection with th e o peration of their respective businesses. This Presentation also contains trademarks, service marks and trade names of third parties, which are the property of their respective owners. The use or display of third parties’ tradema rks , service marks, trade names or products in this Presentation is not intended to, and does not imply, a relationship with Amex GBT or APSG, or an endorsement or sponsorship by or of Amex GBT or APSG. Solely for convenience, the trademarks, se rvi ce marks and trade names referred to in this Presentation may appear with the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that Amex GBT or APSG will not assert, to the fullest extent un der applicable law, their rights or the right of the applicable licensor to these trademarks, service marks and trade names. 4

Transaction Update ▪ We signed the Business Combination Agreement with Apollo Strategic Growth Capital on Dec 2, 2021. $817M cash in trust ▪ PIPE process was well received, upsized and oversubscribed. Initial target for PIPE subscriptions was $200M. We allocated $335M, including sizeable investments by strategic investors Zoom and Sabre ▪ December 2021 new term loan facility provided $400M of incremental liquidity (including the currently undrawn delayed draw commitments), which may be used to backstop potential redemptions ▪ S - 4 filings: ‒ Filed on Dec 21, 2021 ‒ First amendment filed on Feb 4, 2022 ‒ Second amendment filed on Mar 21, 2022 ▪ Expected to close in May and trade on the New York Stock Exchange under the ticker symbol GBTG 5

Amex GBT Investor Day Intro Paul Abbott

Amex GBT Overview Why Amex GBT is a Compelling Investment Opportunity: 1. Travel Recovery Has Strong Momentum 2. A Significant Runway for Growth (Part 1) 3. A Significant Runway for Growth (Part 2) 4. Differentiated Value for Customers and Suppliers 5. Incremental M&A Opportunity and a Proven Track Record 6. Accelerating Earnings Power with Egencia Synergies & Permanent Cost Savings 7. Consistent History of Delivering Revenue and Earnings Growth Why Amex GBT is a Compelling Investment Opportunity – APSG’s Perspective Wrap Up and Q&A Today’s Agenda 7 1 2 4 3 Break Break

Evan Konwiser EVP Product, Strategy & Communications Michael Qualantone Chief Revenue Officer Martine Gerow Chief Financial Officer Paul Abbott Chief Executive Officer Andrew Crawley Chief Commercial Officer Boriana Tchobanova Chief Transformation Officer David Thompson Chief Technology Officer Eric Bock Chief Legal Officer, Global Head M&A Patricia Huska Chief People Officer Mark Hollyhead President, Egencia Management Team 8

Amex GBT Overview Paul Abbott

The Global Leader in B2B Travel ▪ 100 years of travel experience (carved out from American Express in 2014) ▪ Leading B2B travel platform by total spend with the largest concentration of high - value travelers ▪ Proprietary end - to - end digital solution and innovation hub powering omni - channel service platform ▪ Leading Meetings and Events solutions provider ▪ Leading Travel and Entertainment (“T&E”) and expense management software ▪ Acquisition of Egencia, the world leading B2B travel software platform, strengthens presence in the high - value U.S. Small and Medium Enterprise (“SME”) customer segment ▪ Industry - leading compliance and ESG program $1.4B+ (as of 2021) Total completed investment in product & platform 1 ~ 1 9K ( 20 21 ) Corporate customers 74 % (20 21 ) o f transactions through digital channels 3 $2. 8 B ( 2019 ) Total Revenue 2 , 11% CAGR 6 $ 502 M ( 2019) Adj. EBITDA 2 , 2 3 %+ CAGR 6 95% (2 0 21 ) Customer Retention 2 9 (as of 2021) Value - enhancing acquisitions since 2016 $ 39 B ( 2019) Total Transaction Value (TTV) 4,5 1. Includes purchase price for acquisition of Egencia 2. Excludes Egencia and Ovation 3. Includes transactions initiated through self - service on digital tools 4. Total Transaction Value (“TTV”) refers to the sum of the total price paid by travelers for air, hotel, rail, car rental and c rui se bookings, including taxes and other charges applied by suppliers at point of sale, less cancellations and refunds 5. Pro forma for 12 months of Egencia ownership 6. 2015 - 2019A CAGR; excludes Egencia 10

Supported by Strong Brand and Strategic Shareholders 11 Strategic Benefits to Amex GBT Brand halo created by one of the most recognized/trusted brands in the world Exclusive lead generation Joint customer initiatives and product development Other Key Shareholders with Strong Travel / Technology Experience 11 Year Brand Licensing Agreement 2 ~30% Pro Forma Ownership 3 ~$140B Market Cap 1 10 Year Strategic Commercial Partnership 5 ~14% Pro Forma Ownership 3 World’s 2 nd Largest Travel Company Strategic Benefits to Amex GBT Partnership with leading B2C travel platform Full access to Expedia’s proprietary hotel content and rates 1. As of 5 - Apr - 2022 2. Effective upon the consummation of the Business Combination, GBT will enter into an amended and restated brand license with A mer ican Express, effective upon the consummation of the Business Combination, for a term of 11 years.. 3. Reflects ownership at close pro forma for the Business Combination. Pro forma ownership based on transaction assumptions foun d o n page 73 4. Per American Express Company 2021 10 - K 5. Expedia strategic agreement effective at Egencia closing. Expires Q4 2031 6. ©2019 BlackRock, Inc. All Rights Reserved. BLACKROCK is a registered trademark of BlackRock, Inc. All other trademarks are th ose of their respective owners $1.3T Network volumes 4 Well - Known & Trusted Brand 6 New strategic investors participating in the PIPE

$ 23 $ 28 $ 39 ~$220 $ 6 $ 7 $ 8 ~$330 GMN ~$60B Managed SME ~$270B Unmanaged SME ~$ 675 B In - Destination ~$430B The Largest Player in a Massively Underpenetrated Industry 12 Long Tail of Vendors Total GBTS Managed ($B) 1 ~40% larger in TTV than the next closest competitor 60% 40% 94% 6% $23B 5 $16B 5 4 4 4 2019 Managed Global Business Travel Spend per TMC 1,2 Total Global Business Travel Spend of $1.4T 3 Source: Travel Weekly 2020 Power list, GBTA, JP Morgan T&E Benchmark, ARC, Phocuswright , Airlines for America, European Business Travel Barometer survey, iResearch China, CWT Public Filings 1. GBT includes ~$8B TTV from Egencia; BCD includes ~$11B TTV from affiliates; CTM pro forma for T&T acquisition 2. Not a comprehensive list of all TMCs, only TMCs known to have $5B+ TTV shown 3. $1.4T reflects 2019 worldwide corporate travel spend including in - destination spend per GBTA. Segment sizes are estimated 4. “GMN” represents Global Multinational Enterprises; “SME” represents Small & Medium Enterprises, which GBT generally defines a s h aving an expected annual spend on air travel of less than $20M. This criterion can vary by country and client needs; In - destination includes entertainment and meals 5. Amount is pro forma for 12 months of Egencia ownership

0.0 0.4 0.8 1.2 1.6 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 Business Travel Spend Has Historically Grown at 4%+ 13 Global Business Travel Spend, indexed to 100 for 2019 Global Business Travel Spend ($T) Decades of Consistent Growth in Worldwide Business Travel Spending Business Travel $1T+ Opportunity by 2023 Source: IATA (Mar - 2022), Global Business Travel Association (GBTA; Nov - 2021); USTA ( Nov - 2021), Fitch (Nov - 2021), Euromonitor (Sep - 2021) 1. IATA baseline travel projection (incl. leisure) for reference 2. Management estimate 20 40 60 80 100 120 '19A '20A '21E '22E '23E '24E '25E E xperts predict ~90 - 100% recovery by 2023; +10pts versus previous expectations Amex GBT is using a ~70% industry recovery in 2023 forecast 2 Fitch USTA (U.S. Domestic) Euromonitor GBTA IATA 1

Amex GBT Sits at the Center of the Business Travel Ecosystem ~19,000 customers globally 95% customer retention rate 1 No single customer or supplier over 6% of revenue Marketplace with the most comprehensive and competitive content in the industry Greatest concentration of high - value travelers GBT’s high value clients book 40% higher average ticket prices than the Travel Management Company (“TMC”) benchmark 3 16 year average tenure of top 100 customers 2 Relationships with 90+ global airlines and 100+ hotel groups 14 1. Excludes Egencia and Ovation 2. Tenure based on top 100 clients by 2019 FY TTV, with tenure calculated through December 2021 (excluding former HRG and Egenci a c lients) 3. Per IATA DDS IBM Microsoft BCG UPS Sanofi Dell KPMG GM IPG Aon Intel ITW Corning EY WorldBank Morgan Stanley Goldman Sachs Credit Suisse

The Platform Delivers Compelling Value to Customers & Suppliers… GBT’s leading position, best - in - class technology solutions and customer service create a highly compelling value proposition to customers and suppliers, making GBT the most valuable marketplace in corporate travel 1 Access to the largest set of premium corporate customers Business travelers are ~2x more valuable to suppliers vs. leisure travelers GBT’s high value clients book 40% higher average ticket prices than the TMC benchmark Cost - efficient, high ROI distribution channel Serve as an effective extension of suppliers’ sales and marketing functions Valuable insights and reporting on customer dynamics Enhance the customer experience Exceptional service, buying experience and disruption management Fully integrated travel and expense management platform Integrated end - to - end solutions enabling full travel spend visibility, control and compliance Detailed reporting and insights tools at customers’ fingertips, including sustainability metrics Complete traveler experience Global, high - touch, 24/7 service enables seamless search, booking and changing of travel, including disruption management Traveler location tracking based on real - time data to keep travelers safe and productive Savings through differentiated supplier content Access to GBT platform’s comprehensive content, value and relationships What We Do for Customers What We Do for Suppliers 15 1. Based on 2019 TTV pro forma to include 12 months of Egencia ownership

Amex GBT Generates Multiple Revenue Streams c Travel Revenues (76%) 1 GBT receives transaction fees for travel services Suppliers pay GBT for content distribution and promotion GBT is paid for each transaction booked through the GDS Product and Professional Services Revenues (24%) 1 GBT is paid fixed fees for staffing, including account management Subscription fees and professional service fees for value - added products and services Income received from suppliers for marketing, products and other professional services Customers Suppliers Net GDS Revenue 3 Transaction Fees 1 Products and Services Revenue 5 Management Fees 4 Fees, Incentives and Preferred Extras 2 Marketing and Other Revenue 6 GDS and New Distribution Capability (NDC) Content 6 5 4 3 2 1 16 1. Revenue split based on 2019 actual revenue, excluding Egencia

Revenue by Customer Segment 1 Revenue by Geography 1 by Revenue Stream 1 GMN , 55% SME , 45% US , 48% EMEA , 36% APAC and other , 9% Americas ex US , 6% Travel , 76% Product & Professional Services , 24% Revenue by Industry 1 IT , 16% Financial Services , 16% Healthcare , 14% Business Services , 13% Industrial , 11% Other , 31% No single customer or supplier accounts for greater than 6% of total revenues 2 Diversified Revenues Across Geography, Customer Segments and Industries 17 1. Revenue by geography and customer segment based on 2019 pro forma revenue, including Egencia. Revenue by industry based on 20 19 actual revenue, excluding Egencia and HRG; by revenue stream based on 2019 actual revenue, excluding Egencia 2. Based on 2019

Amex GBT’s Leadership Position 18 CORE PLATFORM 56 52 49 44 39 36 33 39 28 23 8 7 6 ~40% larger in TTV than the next closest competitor ▪ Global presence that serves clients 24/7 wherever and whenever they want ▪ Delivering superior customer and supplier value ▪ Efficient cost base and financial stability ▪ Differentiated investment capacity helps promote innovation and creates a unique competitive advantage ▪ $1.4B invested in purpose - built technology 2 ; infrastructure is less than six years old ▪ GBT’s Core Platform powers global travel programs at scale by connecting leading proprietary and third - party tools ▪ Leading solutions designed to address all needs of any travel program Business Travel , Meetings & Events for All Clients Solution of Choice for High Touch Clients Data Lake SUPPLY MARKETPLACE CONNECT PROFILE Œ GLOBAL TRIP RECORD Œ Neo Œ AI/Chat Agent Mobile Future channels Products & services TTV ($B) 1 Solution of Choice for Digital - First Clients 1. GBT includes ~$8B TTV from Egencia; BCD includes ~$11B TTV from affiliates; CTM pro forma for T&T acquisition. Not a comprehe nsi ve list of all TMCs, only TMCs known to have $5Bn+ TTV shown 2. $1.4B includes purchase price for acquisition of Egencia 3. Per July - August 2021 survey commissioned by APSG Leadership in Scale Leadership in Technology Leadership in Solutions NPS Scores 3

High Quality and Loyal Customer Base 19 $3.7B 2021 New Wins Value 1 95% 2021 Customer Retention Rate 2 16 Year Average Tenure for Top 100 Customers 3 40 of the Top 100 U.S. Companies by Travel Spend 4 5 of 10 Largest Health Care Companies 6 5 of 10 Largest U.S. banks 5 58% 2020 AM Law Top 100 3 of 4 Big Four Accounting Firms >45% of GBT Revenue Comes from SME 1. Pro forma for 12 months of Egencia ownership 2. Excludes Egencia and Ovation 3. Tenure based on top 100 clients by 2019 FY TTV, with tenure calculated until December 2021 (excluding former HRG clients) 4. Per BTN’s 2020 Corporate Travel 100 5. Per Federal Financial Institutions Examination Council, largest holding companies by total assets as of 30 - Jun - 2021 6. Per Pharm Exec / Evaluation Ltd. 2020 rankings of largest pharmaceutical companies by revenue

Delivering on Our Financial and Strategic Commitments: 2021 Results & Recent Highlights 20 Strengthened Customer Value Egencia Synergies & Accelerated SME 3 Growth Financial Results Well Above Forecast 1 Corporate Travel Recovery Accelerating ▪ 119% year - over - year growth in Q4 revenue ▪ Pro forma revenue and Adjusted EBITDA exceeded forecast in Registration Statement by $61M and $37M , respectively 1 ▪ Corporate travel transaction recovery reached 61% in the week ended April 2, up 33pts since mid - January ▪ TTV 2 recovery reached 59% in the week ended April 2 ▪ Compares to guidance for a 58% revenue recovery for the full year 2022 ▪ Doubled SME footprint to represent approximately 45% of revenue, based on 2019 ▪ On track to achieve $109M in total Egencia synergies and expect to deliver $25M synergies in 2022 ▪ Positioned for growth with 2021 new wins value 4 that represents 14% of 2019 pro forma 5 TTV for the SME customer segment ▪ Delivered $3.7B new wins value 4 ( 10% of 2019 pro forma 5 TTV) ▪ 95% customer retention rate 6 ▪ 92% customer satisfaction score 6 and major new customer wins 1. Apollo Strategic Growth Capital filed the registration statement on Form S - 4 (file no. 333 - 261820) with the SEC on December 21, 2021 as amended on February 4, 2022 and March 21, 2022 (as amended from time to time, the “Registration Statement”) 2. Total Transaction Value (“TTV”) refers to the sum of the total price paid by travelers for air, hotel, rail, car rental and c rui se bookings, including taxes and other charges applied by suppliers at point of sale, less cancellations and refunds 3. “SME” represents Small & Medium Enterprises, which Amex GBT generally defines as having an expected annual spend on air travel of l ess than $20 million. This criterion can vary by country and client needs. “GMN” represents Global & Multinational Enterprises 4. Expected annual average TTV over the contract term from new client wins based on 2019 spend; includes 12 months of Egencia ow ner ship 5. Pro forma for 12 months of Egencia ownership 6. Excludes Egencia and Ovation

Why Amex GBT is a Compelling Investment Opportunity Paul Abbott

Highly Attractive and Differentiated Investment Opportunity What You Need to Believe Proof Points Travel Recovery Has Strong Momentum Business travel has strong momentum. Transaction recovery was 61% of 2019 the week of April 2, a 33pt recovery since mid - January. A Significant Runway for Growth Global leader in a $1.4T addressable industry, delivering consistent share gains. Differentiated Value for Customers and Suppliers Our products, capabilities and premium scale deliver compelling value. Incremental M&A Opportunity and Proven Track Record Proven track record of delivering value through M&A in a highly fragmented and consolidating sector. Accelerating Earnings Power with Egencia Synergies & Cost Savings The Egencia acquisition and cost savings already actioned drive material earnings and margin growth. Consistent Delivery of Revenue and Earnings Growth Proven track record of delivering Revenue and Adj. EBITDA 1 growth since the creation of the JV in 2014. 1 2 3 4 5 22 6 1. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconciliation of Adj. EBITDA to GAAP

Travel Recovery Has Strong Momentum Drew Crawley

20% 25% 30% 35% 40% 45% 50% 55% 60% 65% 70% Week Ended Nov 13, 2021 Week Ended Jan 15, 2022 Week Ended Apr 2, 2022 Continued Momentum in Business Travel Recovery Gross transactions recovery vs. 2019 1,2 24 1. Gross Transactions represents the total number of transactions, including air, hotel, car rental, rail or other travel - related t ransactions, recorded at the time of booking, on a gross basis to include cancellations, refunds and exchanges 2. Thanksgiving, Christmas and New Years’ weeks excluded There is headroom for the recovery to continue: • Businesses and employees want to travel • Key cross border routes remain subject to restrictions; some minor, some significant • GMN customers still have some policy restrictions in place • Some are still reopening offices 61%

Businesses and Employees Want to Travel 25 1. Back to Blue Skies survey, May 2021 2019 Estimated Share of GBT Trips by Purpose Sales and business development Client delivery Internal meetings 69% of travel managers believe more distributed workforces will drive more business travel (1) 85% of travel managers said business travel leads to higher revenue and profits (1) 78% of business travelers prefer to sell in person (1)

SME, Domestic Air and Hotel Volumes are Leading the Recovery Weekly gross transactions recovery compared to 2019 1. Gross Transactions represents the total number of transactions, including air, hotel, car rental, rail or other travel - related t ransactions, recorded at the time of booking, on a gross basis to include cancellations, refunds and exchanges 26 0% 10% 20% 30% 40% 50% 60% 70% 15-Jan 22-Jan 29-Jan 5-Feb 12-Feb 19-Feb 26-Feb 5-Mar 12-Mar 19-Mar 26-Mar SME GMN 13ppt Total Customer Segment 15-Jan 22-Jan 29-Jan 5-Feb 12-Feb 19-Feb 26-Feb 05-Mar 12-Mar 19-Mar 26-Mar Hotel Rail Air Booking Type 15-Jan 22-Jan 29-Jan 5-Feb 12-Feb 19-Feb 26-Feb 5-Mar 12-Mar 19-Mar 26-Mar Domestic International 9ppt Route (Air) 15-Jan 22-Jan 29-Jan 5-Feb 12-Feb 19-Feb 26-Feb 5-Mar 12-Mar 19-Mar 26-Mar EMEA Americas APAC Region of Sale

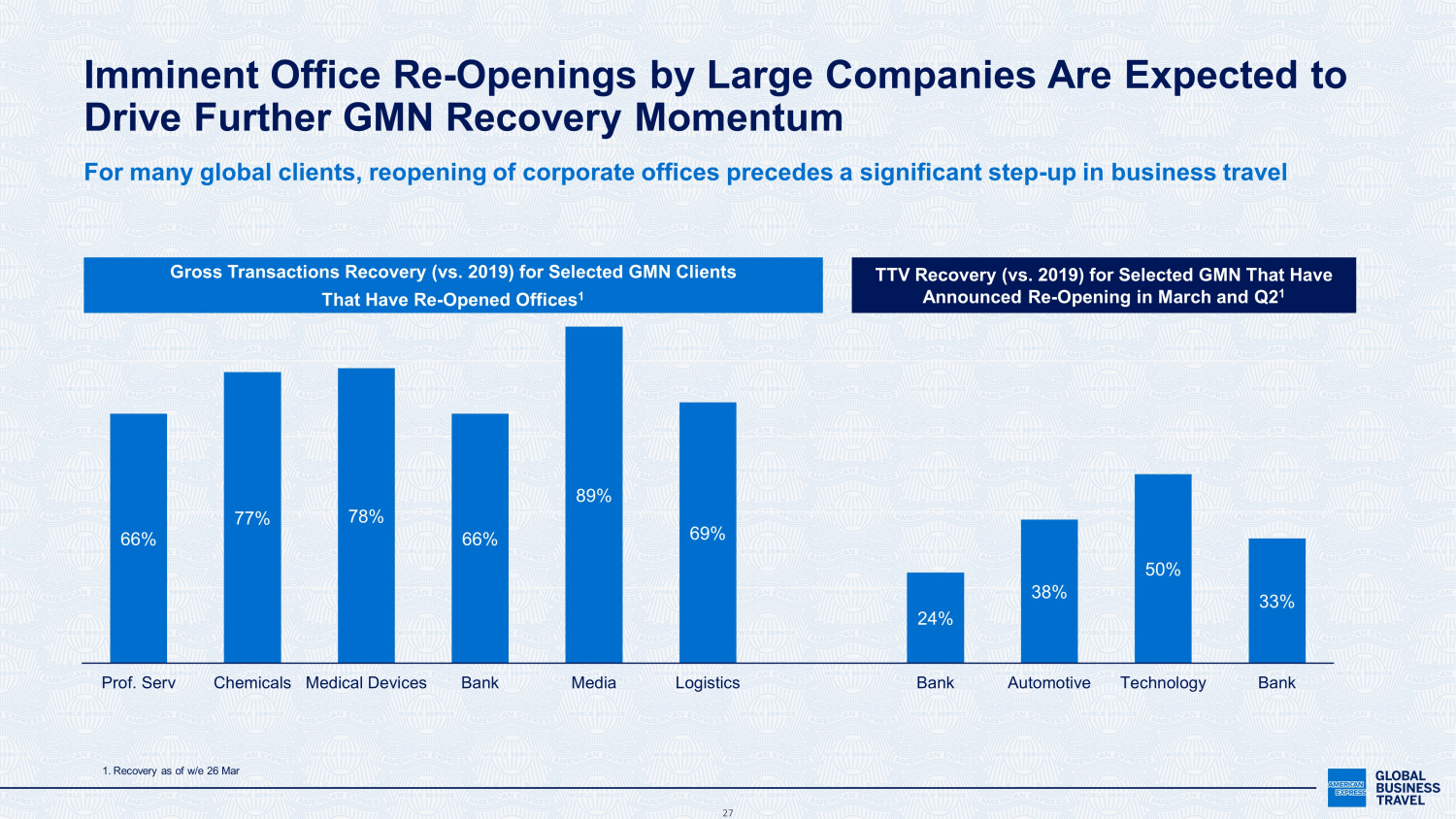

Imminent Office Re - Openings by Large Companies Will Drive Further GMN Recovery Momentum 27 For many global clients, reopening of corporate offices precedes a significant step - up in business travel 66% 77% 78% 66% 89% 69% 24% 38% 50% 33% Prof. Serv Chemicals Medical Devices Bank Media Logistics Bank Automotive Technology Bank Gross Transactions Recovery (vs. 2019) for Selected GMN Clients That Have Re - Opened Offices 1 TTV Recovery (vs. 2019) for Selected GMN That Have Announced Re - Opening in March and Q2 1 1. Recovery as of w/e 26 Mar

58% 59% 66% 64% 56% 55% 2% 19% 32% 33% 3% US - UK US - EU US - Switzerland US - Australia US - Singapore Australia - Singapore US - China/HK US - Japan US - Brazil US- South Korea France - China Strong Reasons to Believe in Further International Recovery as More Restrictions are Eased Weekly gross transactions recovery compared to 2019 w/e March 26 +8 +10 +8 +22 +26 +19 A few key routes remain closed or subject to onerous testing or quarantines 28 Pt change in last 4 weeks 1. Relaxation of restrictions announced but not come into effect at time of analysis Current state of restrictions Approximately 15 % of GBT air routes by TTV are still impacted by border closures, caps or onerous testing requirements 1 1 1 Light testing Border closed Entry capped Heavy testing Heavy testing Border closed Most key routes have opened up in the last 2 months, with recovery already at 60%+, despite some testing requirements still being in place

Key Partners See Even More Positive Trends in Forward Bookings “As we close out this quarter, we're looking at about a 65% corporate [revenue recovery]… Throughout the entire crisis [SME] has run between 5 and 10 points above corporate travel,” – GLEN HAUENSTEIN , President (March 2022) “I think there's a really good chance, on a run rate basis, that [business transient demand] will end up back at or above where we were in 2019 before the year is out , ” – CHRIS NASSETTA , President & CEO (Feb 2022) “I will go back to my point on held revenues at American and point out again how quickly business revenues are growing back right now , with the simple fact that -- of more offices opening up. That gives me a lot of confidence that this is going to come back.” – DOUG PARKER, Chairman & CEO (March 2022) “ Business traffic is booming, we still have a long way to go . But we've made so much more progress than we thought earlier in Q1 … business revenues now close to 75% versus 2019, business demand is about 70%.” – ANDREW NOCELLA , Executive VP & CCO (March 2022) 29

A Significant Runway for Growth Drew Crawley

Our Leading Customer Value Proposition 31 Unrivaled Choice ▪ Solutions designed around customer needs and powered by a modern, agile platform ▪ The leading solutions for the customer segments, needs and verticals we serve Unrivaled Experience ▪ The leading digital, self - service and agent - facilitated traveler experience, anytime, anywhere, from any device ▪ Travel manager tools that make world class travel programs easy Unrivaled Value ▪ The most valuable marketplace in travel with the most comprehensive and competitive content and savings ▪ Efficient marketplace for customers and suppliers With The Powerful Backing of American Express GBT ▪ The brand trusted to deliver the best service, reliability, safety and security ▪ Setting the standard for ESG, Privacy and Compliance unmatched in the industry

The Powerful Backing of Amex GBT 32 “…massive thank you for all your support over the weekend... trying to find accommodation for us in Lviv , Ukraine. Your hard work, commitment and partnership is much appreciated… you have done a stellar job!” & “ thanks… for all the efforts in these exceptional circumstances. We could have not done this without your help! ” “Kudos to… the entire team! It is so wonderful to have a team that is available 24/7 to assist us with these evacuations! I truly appreciate your support.” – “…thank you for your quick attention on Saturday...Amazing service!...[team] had great things to say about our Travel team…it is greatly appreciated by us all.” “Your team responded so incredibly swiftly and had such quick positive responses… [we were] able to demonstrate excellent service is great, but to do is in such challenging conditions as is currently occurring, is hugely well received and I am very thankful to you for this support” "We are SO thankful for this teams support… early morning calls… [and] late night asks. Thank you for everything you’ve done to support the teams in the field.” “Beyond thankful… in directly supporting… frightened traveler via WhatsApp communications.” “... thank you… for the herculean efforts to support [ ou r people] and their families fleeing Russia and Ukraine… we are so very appreciative of Amex GBT leadership who have truly gone above and beyond in the most challenging of circumstances.” “…thank you… your leadership along with our Amex GBT partners is what brings our values to life…”

1. Based on 100% recovery to 2019; includes Egencia for FY 2021 2. 2015 – 2021 average 3. Based on TTV; Amex GBT only (excludes Egencia) We Are the Leader in a $1.4T Industry Recent New Wins A Proven Track Record of Accelerating Net New Wins $3.7B 2021 New Wins Value 1 95% 2021 Customer Retention Rate 3 2.5x Average Win/Loss Ratio 2 33 Ferrero Hewlett Packard Enterprise Standard Chartered

A Significant Runway for Growth Mark Hollyhead Accelerating SME Growth

Clear Leader with Significant Runway in Industry’s Largest, Fastest Growing and Most Profitable Customer Segment – SME Large & Underpenetrated Segment… Unmanaged SME ~$675B 1 Managed SME ~$254B 1 GBT Share of Managed SME $16B, ~6% Total SME Opportunity of ~$945B 1 ▪ Volume recovery for SME has outpaced GMN by ~10pts ▪ Only ~30% of global SME spend is managed today ▪ We are the No. 1 managed SME player ▪ SME represents 45% of total Amex GBT revenue 2 Fastest Growing… …And Most Profitable 35 ▪ U.S. SME contribution margin 25 - 30% higher than total Amex GBT ▪ Higher revenue yield due to increased usage of GBT Preferred Extras rates ▪ Lower cost to serve due to higher digital adoption 1. Source: GBTA, JP Morgan T&E Benchmark, ARC, Phocuswright , Airlines for America, European Business Travel Barometer survey, iResearch China. Segment sizes are estimated. 2. Pro - forma for Egencia.

Our portfolio of leading solutions provide the ability to increase win rate Personalized, High Touch Traveler Care Simple, Easy to Use Self Service Platform Solve For Complex Global Travel Program How Are We Accelerating Growth? Our Solutions Lead in Each SME Customer Segment 36

The Pandemic and Existing Macro Trends Are Accelerating the Movement to Managed Travel Program Unmanaged Travel Program Managed Travel Program Savings Booking high priced published fares – missed savings Full access to GBT Preferred Extras unique rates and savings Duty of Care Traveler location unknown, support a major issue when things don’t go to plan Proactive, full 24/7 support when things don’t go to plan, with the powerful backing of Amex GBT Booking Process Travelers spending time searching different websites for fares and calling airlines High employee productivity and satisfaction. Fully integrated tools, technology and booking and expense processes Customer Service Long waits, inconsistent and unreliable service Immediate 24/7 care and support in place (phone, chat, self service) Compliance Unable to enforce T&E policy Full control, visibility and ability to enforce T&E policy 37 Egencia provides a customer - friendly, one - stop - shop technology platform that is perfect for this

Multiple Levers to Accelerate SME Revenue Growth to Double Digits ▪ Accelerate shift from unmanaged to managed ‒ Huge whitespace represents significant area of opportunity ($675B) ‒ Large potential for higher win rates in 2022/2023 ▪ Expand lead generation ‒ Full utilization of American Express’s 3M U.S. SME relationships through exclusive partnership ▪ Scale marketing ‒ Increased investments in marketing and digital acquisition ▪ Expand SME sales team ‒ Increase sales investments across all channels 7% Underlying Historical SME Annual Growth (Excluding M&A) 1 Consistent double - digit revenue growth potential Based on GBT SME, Egencia and Ovation TTV growth in 2016 – 2019. 38

Differentiated Value for Customers and Suppliers Mike Qualantone Powered by Differentiated Content

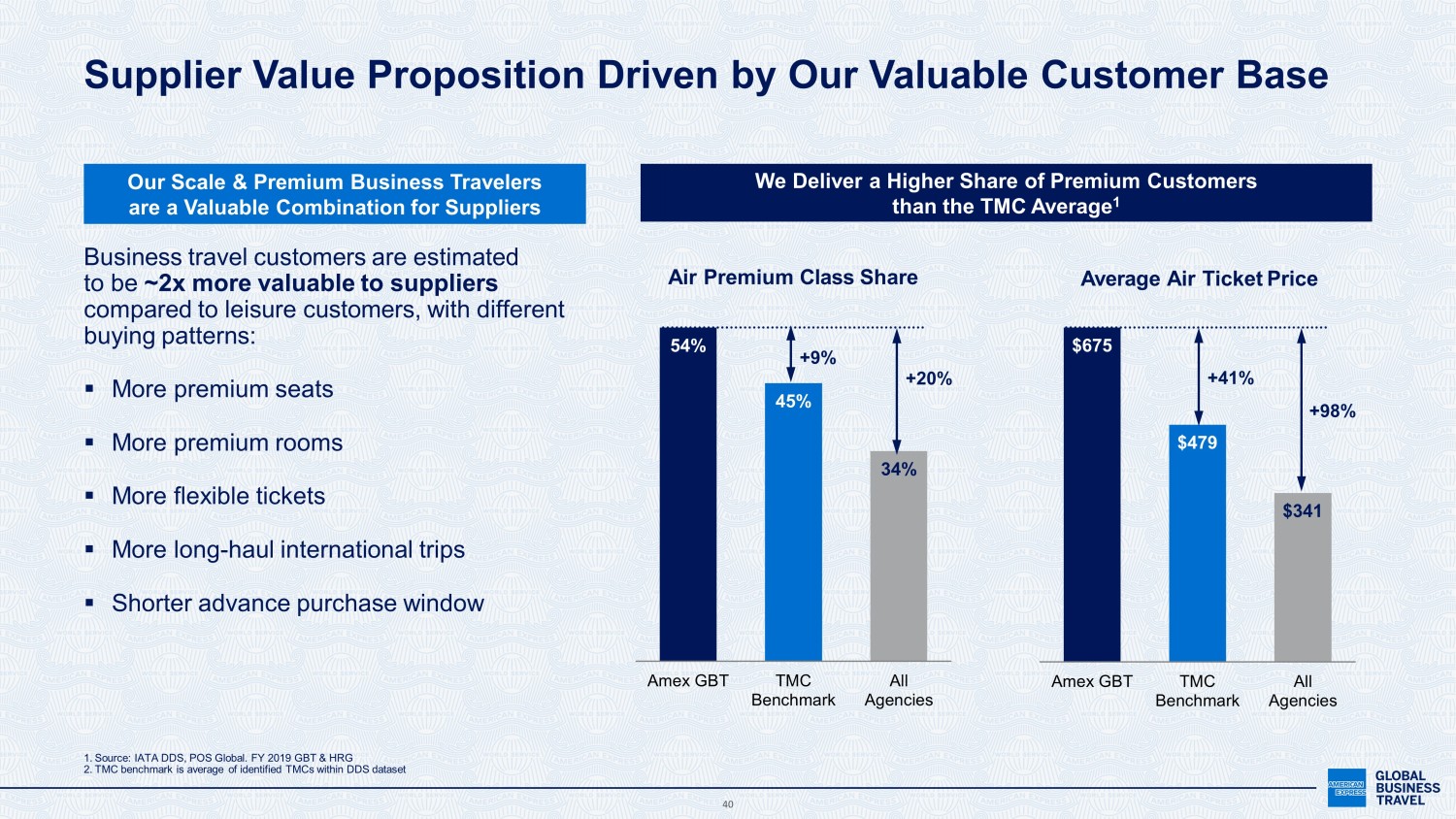

54% 45% 34% Amex GBT TMC Benchmark All Agencies Business travel customers are estimated to be ~2x more valuable to suppliers compared to leisure customers, with different buying patterns: ▪ More premium seats ▪ More premium rooms ▪ More flexible tickets ▪ More long - haul international trips ▪ Shorter advance purchase window Our Scale & Premium Business Travelers are a Valuable Combination for Suppliers Supplier Value Proposition Driven by Our Valuable Customer Base 1. Source: IATA DDS, POS Global. FY 2019 GBT & HRG 2. TMC benchmark is average of identified TMCs within DDS dataset We Deliver a Higher Share of Premium Customers than the TMC Average 1 + 9% $675 $479 $341 Amex GBT TMC Benchmark All Agencies + 41% + 98% +20% 40 Air Premium Class Share Average Air Ticket Price

Our Marketplace Strategy is Powering the Return of Business Travel 41 Most valuable portfolio of high value customers across Global and SME segments. This is t heir marketplace Partnering with Amex GBT enhances suppliers’ opportunities with the greatest aggregation of premium customers Unique ability to bring greater content, access and savings to our clients We deliver greater savings for our customers and performance for our supplier partners

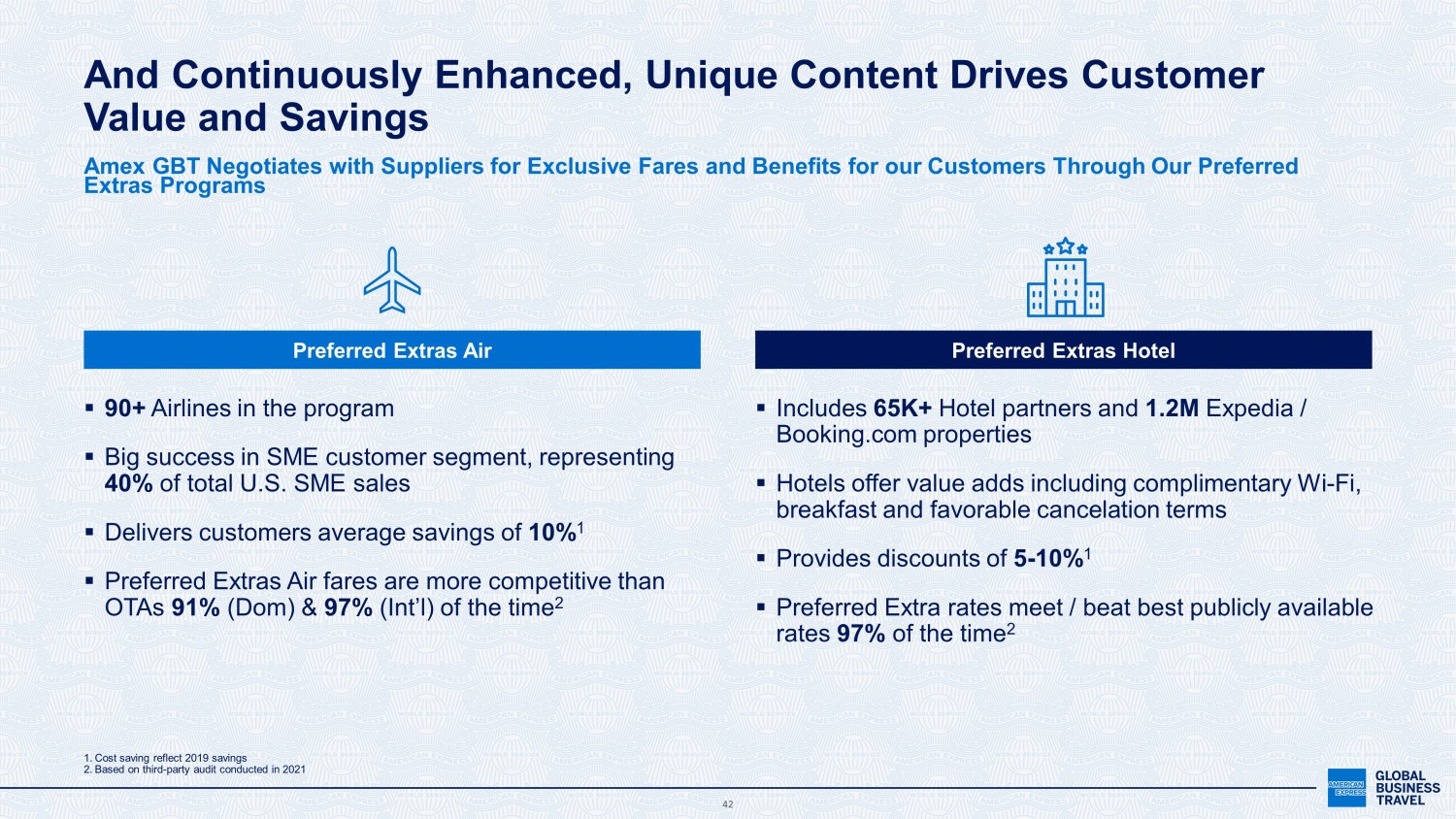

And Continuously Enhanced, Unique Content Drives Customer Value and Savings 42 Amex GBT Negotiates with Suppliers for Exclusive Fares and Benefits for our Customers Through Our Preferred Extras Programs Preferred Extras Air Preferred Extras Hotel ▪ 90+ Airlines in the program ▪ Big success in SME customer segment, representing 40% of total U.S. SME sales ▪ Delivers customers average savings of 10% 1 ▪ Preferred Extras Air fares are more competitive than OTAs 91% (Dom) & 97% (Int’l) of the time 2 ▪ Includes 65K+ Hotel partners and 1.2M Expedia / Booking.com properties ▪ Hotels offer value adds including complimentary Wi - Fi, breakfast and favorable cancelation terms ▪ Provides discounts of 5 - 10% 1 ▪ Preferred Extra rates meet / beat best publicly available rates 97% of the time 2 1. Cost saving reflect 2019 savings 2. Based on third - party audit conducted in 2021

Differentiated Value for Customers and Suppliers Evan Konwiser Enabled by Our Proprietary Technology

$1.4B+ Invested in Last 7 Years in Building Leading Technology Platform 44 Acquisition Organic / Internal Leading B2B Travel Software Platform 30 SECONDS TO FLY Travel AI Capability Infrastructure Stand - up KDS Neo, Online Booking, T&E Core Platform Launch Industry - Defining Product and Technology Strategy Priorities Digital Acceleration Cloud Migration NDC Digital & Ecommerce Hub 2015 2016 2017 2019 2020 2021 2022

Complete Proprietary Technology Platform that Leads Where it Matters Traveler Profile Supply Market Place Trip Record Travel Management Tools for Full Visibility & Control Full Ownership of Traveler Experience Proprietary Marketplace for Savings and Value ▪ Comprehensive Content ▪ Unique Content ▪ Leading Revenue Management Neo and Amex GBT Mobile Agent Desktop Egencia

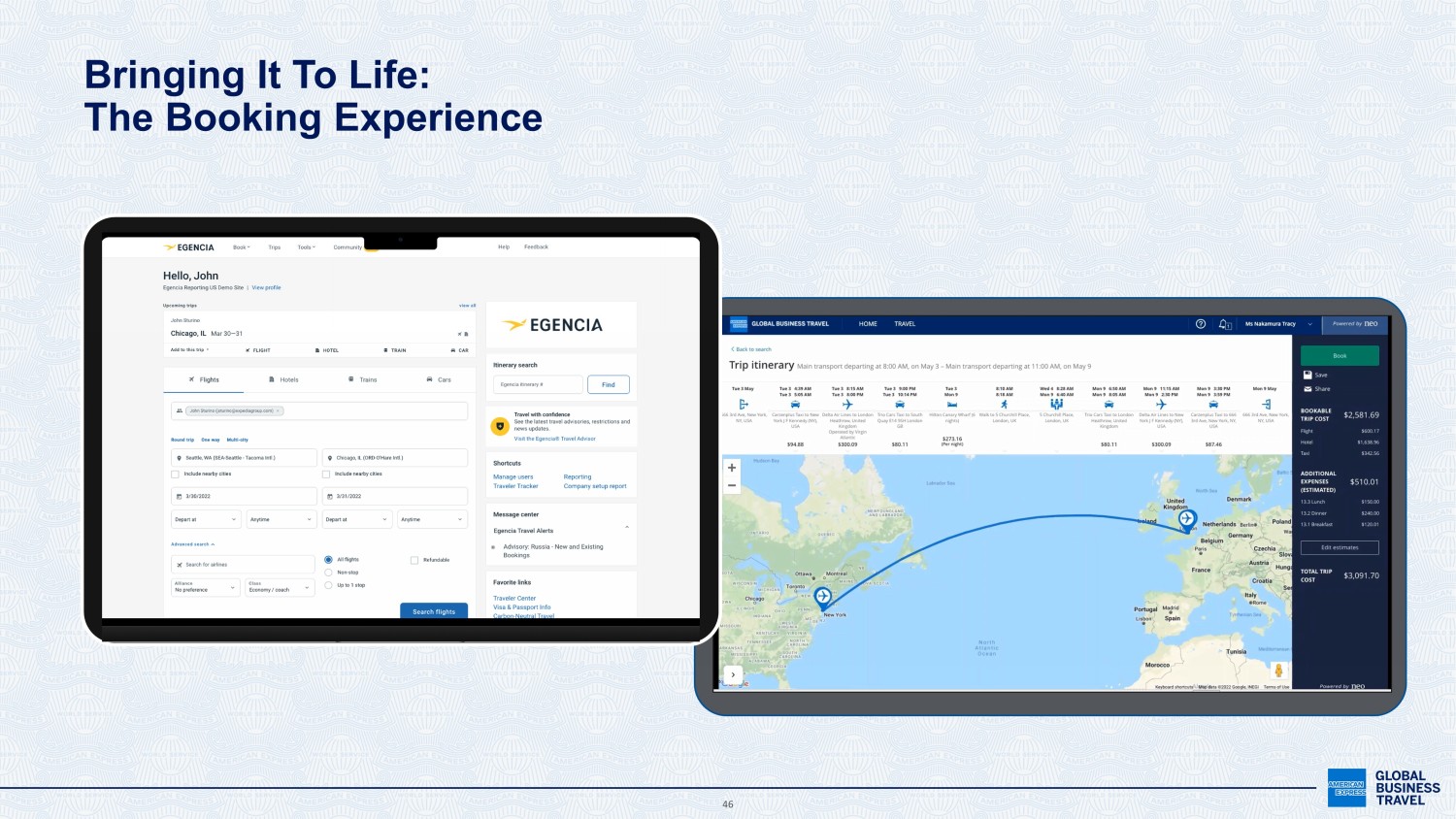

Bringing It To Life: The Booking Experience 46

Demo Video – Bringing it to life: Proactive Response to Disruption Tailored to Each Trip 47

48 Bringing It To Life: Making Travel Management Intuitive and Easy for SMEs

49 Full Ownership of Traveler Experience • Leading traveler experience • In control of our digital destiny • Ability to drive efficiency Travel Management Tools for Full Visibility & Control • Best solution for any customer • Deep integration • Flexible & globally capable Proprietary Marketplace for Savings and Value • Comprehensive and unique content • Delivering superior savings • Future proofing our model Leading & Differentiated Value Proposition Across All Segments of B2B Travel

Incremental M&A Opportunity and a Proven Track Record Eric Bock

Target Date Rationale ▪ Neo expense management solutions, travel booking technology, supplier marketplace technology and a dedicated tech development team ▪ Technology driven AI messaging capabilities ▪ High touch capability and scale in U.S. SME ▪ Leading global digital platform and scale in U.S. SME ▪ Meetings and events scale and solutions ▪ German presence and SME expansion ▪ Spanish and European expansion ▪ SME scale and Nordic presence ▪ Transformative expansion providing global and multi - national scale History of Successful M&A Execution and Integration 51 GBT Spain (Barcelo) Dec ‘17 30STF Oct ‘20 Nov ‘21 Jan ‘21 Sep ‘19 Aug ‘17 Oct ‘16 Oct ‘16 Jul ‘18 CAPABILITIES SCOPE & SCALE

Scope and Scale – Hogg Robinson Group M&A Case Studies 52 Implied TEV/EBITDA Multiple Over Time Pre-acquisition (FY'18A) Post-acquisition + synergies (FY'19A) Post-acquisition + synergies (FY'22E) $62M acquired Adj. EBITDA 1 $75M synergies / harmonization achieved $90M synergies / harmonization expected (vs. $77M budgeted) 11.4x 5.1x 4.6x • Acquired HRG, the fourth largest TMC globally, in July 2018 • Combined two advanced travel technology and development platforms • Added ~$5.5B incremental TTV and ~$400M revenue which added ~25% TTV and ~24% revenue to our business Acquisition Overview Highly Attractive Synergized Purchase Multiple • In November 2021, GBT acquired Egencia, the leading global digital B2B travel software platform • Strengthens presence in high value US SME customer segment • Added $8.3B in incremental TTV and $547M revenue, adding ~27% TTV and ~24% revenue to our business Acquisition Overview Scope and Scale & Capabilities – Egencia Purchase Multiple Synergies Synergized Multiple Synergies driven by revenue harmonization, real estate optimization and workforce rationalization $40M acquired Adj. EBITDA 1 $109M synergies 18.8x 13.8x 5.0x 1. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconciliation of Adj. EBITDA to GAAP

Priorities for M&A 53 Supported by strong balance sheet and liquidity position 1 2 3 SME Platform Growth Technology and Product Enhancements Higher Growth/Margin Regions M&A Priorities M&A Objectives ▪ Win New Business/Improve Organic Growth ▪ Efficiencies/Cost Synergy Benefits ▪ Revenue Harmonization Benefits ▪ Strengthen Global Platform Offering ▪ Value Creation Drives

Significant Opportunity for Value Creation Through M&A 54 • M&A offers significant upside • Acquisitions achieved inside our De - Spac valuation of 9.4x ‘23E Adj. EBITDA provide immediate value to our shareholders • 1x EBITDA synergy target for TMC acquisitions • Financial forecasts contemplate no acquisitions, so M&A is upside to forecast • Significant runway due to large and highly fragmented industry • $1.4 trillion industry; Amex GBT, as the industry leader, manages $40 billion • Expertise to capture M&A opportunity as evidenced by historical M&A track record • Our proven ability to drive revenue & cost synergies has resulted in attractive synergized multiples over time • We are constantly evaluating opportunities • Enhancing our service offering and portfolio of operations • Via strategically and financially compelling acquisitions

Accelerated Earnings Power with Egencia Synergies & Permanent Cost Savings Martine Gerow

On Track to Achieve $109M in Egencia Synergies Bottom - aligned footnote position. Copy and paste as needed. This is NOT part of the slide master. Expect $109M in Total Synergies With Solid Progress to Date ▪ $75M of revenue synergies driven by revenue harmonization ▪ $34M of cost synergies, primarily from real estate consolidation ▪ Revenue harmonization is on track ▪ GBT Preferred Extras live in Egencia platform ▪ 13 office moves completed, representing 50% of target real estate synergies On track to achieve forecasted $25M in total synergies in 2022

$235M of Permanent Cost Savings Enhance Margins 57 Overview of OpEx Optimization $235M of Permanent Savings Executed in 2020 & 2021 ▪ Reacted quickly to changing environment; aggregate cost reduction of ~$900M from May 2020 – April 2021, representing 48% of cost base, including volume - related savings ▪ $235M permanent cost reductions, representing 13% of pre - COVID cost base ▪ 80% of permanent cost reductions realized; remainder as volumes recover $160M $32M $24M $19M $235M Productivity & Efficiency Vendor Cost Reduction Real Estate Other Total Represents 13% of 2019 cost base

Model assumptions were to maintain supplier economics, but some recent supplier deals have improved – suggests incremental opportunity not included in current model Recently signed major supplier deals will protect our revenues and allow for future growth opportunities Improved revenue economics Expanded and strengthened SME value proposition creates capability to accelerate SME sales performance beyond what’s in forecast Additional upside potential as SME is the fastest growing segment that is also recovering from pandemic more quickly Accretive margin impact – as SME becomes a higher % of revenue, higher incremental margins on a largely fixed cost base drive upside Accelerated SME growth 18% 5% 8% 1% 2% 22% 5% 1% 28% 1. 2023 forecast based on ~70% of 2019 industry TTV recovery. 2. Opportunity to partially offset further cost inflation with increased Average Ticket Price (“ATP”) is not included in forecast, although net impact may vary by geography and supplier among other factors. Additionally, cost inflation is generally passed along to the customer in Management Fee contracts. 1 1 2 2019 PF Adj. EBITDA 2 Margin % Permanent Cost Benefits Merit / Inflation ~70% Travel Industry Recovery Egencia Synergies 100% Industry Recovery 2023 PF Mgmt. Adj. EBITDA 2 Margin % at 70% Industry Recovery PF Adj.EBITDA 2 Margin % at 100% Industry Recovery Egencia Synergies Margin Expansion Opportunity of 4 - 10pts at 70 - 100% Industry Recovery 1. Pro forma for Egencia ownership 2. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconciliation of Adj. EBITDA to GAAP Margin Expansion Drivers in the Forecast 1 Margin Expansion Levers Incremental to Forecast 58

Consistent Delivery of Revenue and Earnings Growth Martine Gerow

$462 $40 $205 $245 $292 $356 $502 2014 2015 2016 2017 2018 2019 $2,282 $547 $1,488 $1,524 $1,609 $1,899 $2,829 2014 2015 2016 2017 2018 2019 1. GBT only, excludes Egencia 2. GBT 2019 Revenue of $2,282M includes GAAP revenue of $2,119M plus pro forma impact of DER and Ovation acquisitions of $124M p lus FX normalization of $39M 3. Pro forma for Egencia ownership. 4. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconciliation of Adj. EBITDA to GAAP Proven Financial Track Record JV Formed JV Formed ~600bps in margin uplift from 2015 - 2019 1 14% 16% 18% 19% 20% Revenue ($M) 2 Adj. EBITDA & Margin ($M) 4 60 2 GBT Egencia 3 3

GDP growth Spend growth above GDP within existing customers Share gain Pre-COVID organic growth ~2% 1 - 2% 2 - 3% 6% SME: 7% annually GMN: 5% annually Organic Growth driven by Existing Customer Growth and Share Gains Installed Base of Customers Growing Above GDP, Track Record of Share Gain 61 1. 2017 – 2019 TTV growth; Includes GBT, Ovation and Egencia 1

2019 PF Adj. EBITDA Travel industry decline (21% of 2019) Permanent structural cost benefit 2021 PF Adj. EBITDA Travel industry recovery (70% of 2019 TTV) Permanent structural cost benefit Share gain Wage Inflation Egencia synergies 2023 PF Adj. EBITDA forecast ($1,210M) $188M $881M $88M ($30M) $47M $61M 2019A – 2023E Amex GBT + Egencia Adj. EBITDA Bridge Amex GBT Returns to Pre - Covid Earnings With Only ~ 70% of Travel Demand Recovered 62 $502M ($520M) $6M $527M 1 1. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconciliation of Adj. EBITDA to GAAP 2. Totals to $235M permanent cost savings 1 1 2 2

205 245 292 356 502 151 189 241 290 401 2015 2016 2017 2018 2019 PF Adj. EBITDA 3 Free Cash Flow 1 ‘15 - ’19 +$297M ’15 - ’19 +$250M Annual working capital outflow approximately ~1% of TTV growth Working Capital Cash interest of ~$90M per year $1.2B debt after $200M DDTL Long term net leverage target of 2x, with flexibility to increase by up to 3x to execute M&A Cash Interest Projecting cash taxes of 50% of accounting tax to reflect utilization of losses Assume 32% accounting tax rate Expect to become full cash taxpayer in 8 - 10 years Cash Taxes Pension contribution of $25 - 35M per year Pension Contribution 2022 Severance cash outflow - $60M Egencia integration expense - $45M in 2022, $20M in 2023 M&A fees / Restructuring envelope of ~$20 - 30M per year Other Cashflow Items Steady state Capex of $100 - 110M per year Capex Expect Significant Long Term Cash Flow Generation 1. Free Cash Flow (FCF) is a non - GAAP measure defined as Adj. EBITDA less Capex; please refer to the Supplemental Materials section for reconciliation of Free Cash Flow 2. Free Cash Flow Conversion is defined as FCF / Adj. EBITDA; 3. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconciliation of Adj. EBITDA to GAAP 4. 2019 is pro forma for Egencia ownership Adj. EBITDA and Free Cash Flow ($M) 1,2,3 Net Cash Flow Generation Drivers 63 82% 81% 80% Free Cash Flow Conversion 1 80% in 2019 4 77% 74%

Liquidity Highlights $516M $250M $335M $90M $1,011M $817M $1,828M 12/31/2021 Cash Balance Delayed Draw & Revolver PIPE Proceeds APSG Cash Held in Trust (Subject to Redemptions) PF Liquidity with APSG Cash Held in Trust 1 Business Combination Transaction Fees PF Liquidity Before APSG Cash in Trust 1. Pro Forma Liquidity is before potential preferred equity paydown of $168M ▪ Have $1.0B - $1.8B estimated pro forma liquidity under various redemption scenarios, as of 12/31/21 1 ▪ December 2021 debt refinancing provided $400M of incremental liquidity ▪ Upsized and oversubscribed fully committed PIPE investment adds $335M ▪ Pending business combination adds up to $817M cash held in trust 1 ▪ Long - term net leverage target of 2x with flexibility to increase to up to 3x to execute M&A Strong Liquidity Position After Pending Business Combination 64

2021 Financial Results Well Above Forecast 1 The following table presents full year 2021 financial results pro forma to include Egencia for the full year. These pro forma results are directly comparable to the forecast provided in the Registration Statement 1 filed with the SEC by Apollo Strategic Growth Capital. Year Ended Dec. 31, 2021 ($M; 2021 amounts are preliminary and unaudited) Pro Forma Results (incl. full year of Egencia) Registration Statement Forecast 1 Variance Total Transaction Value (TTV) 2 $7,969 $7,600 + $369 Revenue $889 $828 + $61 Adjusted EBITDA ($520) ($557) + $37 65 1. Apollo Strategic Growth Capital filed the Registration Statement with the SEC on December 21, 2021 as amended on February 4, 202 2 and March 21, 2022 (as amended from time to time, the “Registration Statement”) 2. Total Transaction Value (TTV) refers to the sum of the total price paid by travelers for air, hotel, rail, car rental and cru ise bookings, including taxes and other charges applied by suppliers at point of sale, less cancellations and refunds

2022 Guidance and 2023 Forecast 66 2022 Guidance 2023 Forecast Revenue $1.6B $2.4B % of PF 2019 1 58% 86% Adj. EBITDA 2 $7M $527M Margin % Breakeven 22% 1. Pro forma for Egencia ownership 2. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconciliation of Adj. EBITDA to GAAP

$502 $527 $626 $736 $846 9.9x 9.4x 8.0x 6.8x 5.9x 2019 2023 Business Plan at ~70% Industry Recovery 2023 at 80% Industry Recovery 2023 at 90% Industry Recovery 2023 at 100% Industry Recovery GBT Would Return to Pre - COVID Adj. EBITDA with Only ~70% Industry Recovery As Recovery Outpaces Amex GBT’s Estimate, Proposed Transaction Becomes Even More Attractive 67 Significant Upside Under Quicker Recovery Scenarios ($M, unless otherwise stated) Adj. EBITDA 1 Implied EV / EBITDA Multiple 1. Pro forma for Egencia ownership. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for re conciliation of Adj. EBITDA to GAAP

Why Amex GBT is a Compelling Investment Opportunity – APSG’s Perspective Itai Wallach, Apollo

75.8% 15.4% 6.3% 2.6% Transaction Summary GBT Existing Shareholders SPAC Public Shareholders PIPE Shareholders Sponsor Promote Pro Forma Valuation ($M, unless otherwise noted) Share Price ($) $10.00 Pro Forma Shares Outstanding (M) 3 531.6 Total Equity Value 5,316 Debt 4 1,041 Cash 4 (1,410) Total Enterprise Value $4,947 EV / 2023E Pro Forma Adj. EBITDA 9.4x Illustrative Sources ($M, unless otherwise noted) SPAC Cash in Trust $817 Sponsor Promote 5 137 PIPE 335 Equity Rollover 6 4,027 Total Sources $5,316 Illustrative Uses ($M, unless otherwise noted) Cash to Balance Sheet $894 Sponsor Promote 5 137 Equity Rollover 7 4,027 Preferred Equity Paydown 7 168 Transaction Costs 90 Total Uses $5,316 Post - Combination Ownership at Close 8 American Express Global Business Travel (“GBT”) – the world leader in B2B software and services for travel – intends to become a public company through a business combination transaction with Apollo Strategic Growth Capital (NYSE:APSG) APSG is a publicly listed Special Purpose Acquisition Company (“SPAC”) with $817M cash in trust PIPE of $335M is being raised in connection with the transaction Overview Seller earn - out of up to 15M shares, subject to vesting milestones based on share price appreciation, aligning value creation incentives 2 Deferral of 6.7M shares of the sponsor promote, with vesting conditional on the same share price appreciation milestones 2 Sponsor is committing $20M to the PIPE Incentive Alignment Pro Forma Enterprise Value of $4,947M: − 9.4x pro forma 2023E Adj. EBITDA of $527M 1 − 9.9 x pro forma 2019A Adj. EBITDA pre - cost savings and synergies of $502M 1 − 5.8x run - rate pro forma Adj. EBITDA of $846M 1 Valuation 69 1. Run - rate pro forma Adj. EBITDA of $846M calculated as 2019A pro forma Adj. EBITDA of $502M plus GBT standalone cost savings of $ 235M plus run - rate synergies from Egencia acquisition of $109M. Refer to the Supplemental Materials section for non - GAAP reconci liations 2. 50% of earn - out and deferred shares vest at $12.50 20 - day VWAP and remaining vest at $15.00 20 - day VWAP 3. Excludes any potential dilutive impact of outstanding warrants 4. Debt and cash balance of $1,041M and $516M, respectively, as of 31 - Dec - 21 5. Includes 75,000 sponsor shares held by APSG’s independent directors 6. Subject to adjustment pursuant to Business Combination Agreement if preferred equity is redeemed for equity, rather than cash 7. Assumes no shareholder redemptions. No incremental dilution at close from sponsor promote deferral of 6.7M shares and seller ear n - out of up to 15.0M shares

Apollo Strategic Growth Capital Is an Extension of Apollo’s Global Integrated Platform 15 Global Offices $472B AUM 39% IRR Since 1990 1 550+ Investment Professionals 1990 Founded High - value player at the center of the business travel ecosystem Strong, seasoned management team and exceptional strategic partners in American Express and Expedia Track record of organic growth, accretive M&A, cost reductions and free cash flow generation Attractive way to invest behind a thesis of near - term travel recovery by backing the industry leader Attractive valuation of 9.4x 2023 pro forma Adj. EBITDA 1 represents a meaningful discount to key publicly traded peers in travel and business services Attractive entry - point with significant upside from continued corporate travel recovery and other tangible growth levers (e.g., SME expansion through Egencia and Ovation acquisitions, achievement of synergies, etc.) Significant Investment Experience in Travel, Leisure and Business Services & Apollo - Sponsored De - SPACs Amex GBT fits squarely in APSG’s wheelhouse, and we believe this transaction is a rare opportunity to capitalize on an extended period of market uncertainty and invest in a market leader at a compelling valuation Apollo Strategic Growth Capital’s Investment Thesis for GBT 1 6 2 3 4 5 & Date: 16 - Mar - 2022 Transaction EV: $2,468M Total Proceeds: $161M Date: 29 - Oct - 2020 Transaction EV: $1,900M Total Proceeds: $1,040M 70 1. Represents returns of traditional Apollo private equity funds since inception in 1990 through December 31, 2021. Past perform anc e is not indicative of future results. Gross IRR represents the cumulative investment - related cash flows ( i ) for a given investment for the fund or funds which made such investment, and (ii) for a given fund, in the relevant fund it sel f (and not any one investor in the fund), in each case, on the basis of the actual timing of investment inflows and outflows (for unrealized investments ass umi ng disposition on December, 2021 or other date specified) aggregated on a gross basis quarterly, and the return is annualized an d compounded before management fees, performance fees and certain other expenses (including interest incurred by the fund its elf ) and measures the returns on the fund’s investments as a whole without regard to whether all of the returns would, if distribu ted , be payable to the fund’s investors. In addition, gross IRRs at the fund level will differ from those at the individual inve sto r level as a result of, among other factors, timing of investor - level inflows and outflows. Gross IRR does not represent the ret urn to any fund investor. Net IRR means the Gross IRR applicable to a fund, including returns for related parties which may not pay fees or p erf ormance fees, net of management fees, certain expenses (including interest incurred or earned by the fund itself) and realize d p erformance fees all offset to the extent of interest income, and measures returns at the fund level on amounts that, if distr ibu ted, would be paid to investors of the fund. The timing of cash flows applicable to investments, management fees and certain expen ses , may be adjusted for the usage of a fund’s subscription facility. To the extent that a fund exceeds all requirements detaile d w ithin the applicable fund agreement, the estimated unrealized value is adjusted such that a percentage of up to 20.0% of the unrealized gain is allocated to the general partner of such fund, thereby reducing the balance attributable to fund investors . I n addition, net IRR at the fund level will differ from that at the individual investor level as a result of, among other fact ors , timing of investor - level inflows and outflows. Net IRR does not represent the return to any fund investor .

EV / 2023E Adj. EBITDA 1 9.4x 2 21.0x 23.3x 18.3x 10.7x 13.2x 23.3x 13.3x 13.0x 16.6x EV / 2023E FCF 1 11.6x 3 22.0x 26.9x 23.9x 12.5x 18.9x 25.3x 15.5x 19.0x 21.0x Scale – Technology Capabilities – – – Organic Growth Prospects – – – – Consolidation Opportunity X X X X X X Depth of Customer Relationships End Market and Supplier Diversity X X Low Capital Intensity We Believe Amex GBT I s a Superior Investment Opportunity to Peers Business Services Amex GBT Corporate Travel & GDS 1. Market data as of 07 - Apr - 2022 2. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconciliation of Adj. EBITDA to GAAP 3. Free Cash Flow is a non - GAAP measure. Free Cash Flow is defined as Adj. EBITDA less Capex 71

9.4x 23.3x 23.3x 21.0x 18.3x 13.2x 10.7x 16.6x 13.3x 13.0x 9.9x 32.3x 32.5x 28.6x 19.0x 17.7x 13.9x 7.8x 24.4x 12.7x Amex GBT Valuation Presents an Opportunity to Invest at a Discount To Peers EV / 2019A & 2023E Adj. EBITDA $5.0 $48.7 $50.5 $102.1 $61.4 $25.4 $9.1 $7.3 $2.4 $31.0 Source: Management projections, Capital IQ, Thomson Consensus Estimates; market data as of 07 - Apr - 2022 1. Based on Adj. EBITDA for GBT. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconcil iation of Adj. EBITDA to GAAP. Adj. EBITDA may be defined different by peers and therefore may not be a relevant comparison. 2019A 2023E Enterprise Value ($B) 1 72

Wrap - Up

Highly Attractive and Differentiated Investment Opportunity What You Need to Believe Proof Points Travel Recovery Has Strong Momentum Business travel has strong momentum. Transaction recovery was 61% of 2019 the week of April 2, a 33pt recovery since mid - January. A Significant Runway for Growth Global leader in a $1.4T addressable industry, delivering consistent share gains. Differentiated Value for Customers and Suppliers Our products, capabilities and premium scale deliver compelling value. Incremental M&A Opportunity and Proven Track Record Proven track record of delivering value through M&A in a highly fragmented and consolidating sector. Accelerating Earnings Power with Egencia Synergies & Cost Savings The Egencia acquisition and cost savings already actioned drive material earnings and margin growth. Consistent Delivery of Revenue and Earnings Growth Proven track record of delivering Revenue and Adj. EBITDA 1 growth since the creation of the JV in 2014. 1 2 3 4 5 74 6 1. Adj. EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconciliation of Adj. EBITDA to GAAP

Q&A

Thank You

Supplemental Materials

EBITDA Reconciliation 78 ($M) 2015 2016 2017 2018 2019 2020 2021 GAAP operating income ($116) (33) $34 $74 $206 ($747) ($560) Depreciation & amortization 71 78 96 125 141 148 154 Share of earnings in equity method investments 3 1 4 6 5 (5) - Restructuring charges 37 27 30 21 12 206 14 Integration costs - - 0 17 36 14 22 M&A costs - 5 11 24 12 10 14 Separation costs 139 87 59 39 3 (0) - Non - cash equity plan 4 4 4 4 6 3 3 Long Term Incentive Plan - - - - - 2 15 Other - 3 0 2 8 6 6 Adjusted EBITDA 138 172 238 311 428 (363) (340) Parallel costs 48 49 36 15 1 2 TSA admin fee & premium 14 10 7 3 - - PCI - - 1 12 4 0 Board expenses 4 4 4 3 4 3 Product investments - 10 14 12 9 0 All other adjustments - - (8) - - - Ovation PF EBITDA 5 (21) DER PF EBITDA 4 - Egencia PF EBITDA 40 (248) (180) FX at constant currency 7 2 PF Adjusted EBITDA $205 $245 $292 $356 $502 ($625) ($520)

Free Cash Flow Reconciliation 79 ($M) 2015 2016 2017 2018 2019 PF Adjusted EBITDA $205 $245 $292 $356 $502 Less: Capex (54) (56) (51) (66) (101) Free Cash Flow $151 $189 241 290 401 Note : Adjusted EBITDA is a non - GAAP measure. Please refer to the Supplemental Materials section for reconciliation of Adj. EBIT DA to GAAP 2019 is pro forma for Egencia ownership