UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 | ||||||||||||||||||||

| FORM 10-Q | ||||||||||||||||||||

| ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||||||||||||||

| For the quarterly period ended March 31, 2023 | ||||||||||||||||||||

| or | ||||||||||||||||||||

| ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||||||||||||||

| For the transition period from ________________to________________ | ||||||||||||||||||||

| Commission File Number: | 001-39739 | |||||||||||||||||||

| Sunlight Financial Holdings Inc. | ||||||||||||||||||||

| (Exact name of registrant as specified in its charter) | ||||||||||||||||||||

| Delaware | 85-2599566 | |||||||||||||||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||||||||

| 101 North Tryon Street, Suite 1000, Charlotte, NC | 28246 | |||||||||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||||||||

| (888) 315-0822 | ||||||||||||||||||||

| (Registrant’s telephone number, including area code) | ||||||||||||||||||||

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||||||||||||||

| Title of each class: | Trading Symbol(s): | Name of each exchange on which registered: | ||||||||||||||||||

| Class A Common Stock, par value $0.0001 per share | SUNL | New York Stock Exchange | ||||||||||||||||||

| Warrants, each whole warrant is exercisable for one share of Class A Common Stock at an exercise price of $11.50 per share | SUNL.WS | New York Stock Exchange | ||||||||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☒

Non-accelerated filer ☐ Smaller reporting company ☒ Emerging growth company ☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of May 8, 2023, 85,397,279 shares of Class A Common stock, $0.0001 par value, and 44,973,227 shares of Class C common stock, par value $0.0001 per share, were outstanding.

SUNLIGHT FINANCIAL HOLDINGS INC.

FORM 10-Q

INDEX

| PAGE | |||||

| Part I. Financial Information | |||||

| Part II. Other Information | |||||

ii

PART I

ITEM 1. FINANCIAL STATEMENTS

SUNLIGHT FINANCIAL HOLDINGS INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(dollars in thousands)

| March 31, 2023 | December 31, 2022 | ||||||||||||||||

| (Unaudited) | |||||||||||||||||

| Assets | |||||||||||||||||

| Cash and cash equivalents | $ | 75,518 | $ | 47,515 | |||||||||||||

| Restricted cash | 4,350 | 4,272 | |||||||||||||||

| Advances (net of allowance for credit losses of $2,319 and $6,736) | 18,030 | 45,393 | |||||||||||||||

| Financing receivables (net of allowance for credit losses of $151 and $102) | 3,269 | 3,532 | |||||||||||||||

| Intangible assets, net | 312,589 | 319,920 | |||||||||||||||

| Property and equipment, net | 1,383 | 1,489 | |||||||||||||||

| Other assets | 35,286 | 30,074 | |||||||||||||||

| Total assets | $ | 450,425 | $ | 452,195 | |||||||||||||

| Liabilities and Stockholders' Equity | |||||||||||||||||

| Liabilities | |||||||||||||||||

| Accounts payable and accrued expenses | $ | 51,306 | $ | 20,674 | |||||||||||||

| Funding commitments | 29,378 | 20,400 | |||||||||||||||

| Debt | 7,694 | 20,613 | |||||||||||||||

| Deferred tax liabilities | 688 | 688 | |||||||||||||||

| Warrants, at fair value | 931 | 4,297 | |||||||||||||||

| Other liabilities | 23,788 | 17,196 | |||||||||||||||

| Total liabilities | 113,785 | 83,868 | |||||||||||||||

| Commitments and Contingencies (Note 10) | |||||||||||||||||

| Stockholders' Equity | |||||||||||||||||

| Preferred stock; $0.0001 par value; 35,000,000 shares authorized; none issued and outstanding as of March 31, 2023 and December 31, 2022 | — | — | |||||||||||||||

| Class A common stock; $0.0001 par value; 420,000,000 shares authorized; 85,417,812 and 83,619,915 issued; and 85,401,353 and 82,307,760 outstanding as of March 31, 2023 and December 31, 2022, respectively | 9 | 8 | |||||||||||||||

| Class C common stock; $0.0001 par value; 65,000,000 shares authorized; 44,973,227 and 47,287,370 issued and outstanding as of March 31, 2023 and December 31, 2022, respectively | — | — | |||||||||||||||

| Additional paid-in capital | 747,064 | 761,698 | |||||||||||||||

| Accumulated deficit | (524,285) | (501,635) | |||||||||||||||

| Total capital | 222,788 | 260,071 | |||||||||||||||

| Treasury stock, at cost; 16,459 and 1,312,155 Class A shares as of March 31, 2023 and December 31, 2022, respectively | (17) | (15,307) | |||||||||||||||

| Total stockholders' equity | 222,771 | 244,764 | |||||||||||||||

| Noncontrolling interests in consolidated subsidiaries | 113,869 | 123,563 | |||||||||||||||

| Total equity | 336,640 | 368,327 | |||||||||||||||

| Total liabilities and stockholders' equity | $ | 450,425 | $ | 452,195 | |||||||||||||

See notes to unaudited condensed consolidated financial statements.

1

SUNLIGHT FINANCIAL HOLDINGS INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(dollars in thousands, except per share amounts)

| For the Three Months Ended March 31, | |||||||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | ||||||||||||||||||||||||||||||||||||||||

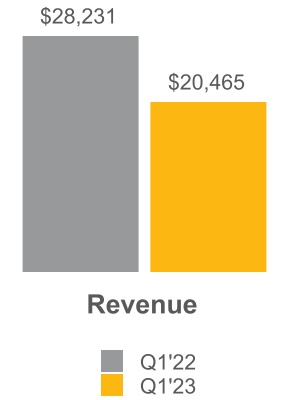

| Revenue | $ | 20,465 | $ | 28,231 | |||||||||||||||||||||||||||||||||||||

| Costs and Expenses | |||||||||||||||||||||||||||||||||||||||||

| Cost of revenues (exclusive of items shown separately below) | 18,301 | 5,229 | |||||||||||||||||||||||||||||||||||||||

| Compensation and benefits | 14,146 | 13,125 | |||||||||||||||||||||||||||||||||||||||

| Selling, general, and administrative | 12,500 | 6,472 | |||||||||||||||||||||||||||||||||||||||

| Property and technology | 1,992 | 1,928 | |||||||||||||||||||||||||||||||||||||||

| Depreciation and amortization | 8,521 | 22,447 | |||||||||||||||||||||||||||||||||||||||

| Provision for losses | 2,169 | 638 | |||||||||||||||||||||||||||||||||||||||

| 57,629 | 49,839 | ||||||||||||||||||||||||||||||||||||||||

| Operating loss | (37,164) | (21,608) | |||||||||||||||||||||||||||||||||||||||

| Other Income (Expense), Net | |||||||||||||||||||||||||||||||||||||||||

| Interest income | 5,972 | 84 | |||||||||||||||||||||||||||||||||||||||

| Interest expense | (379) | (260) | |||||||||||||||||||||||||||||||||||||||

| Change in fair value of warrant liabilities | 3,366 | (4,884) | |||||||||||||||||||||||||||||||||||||||

| Change in fair value of contract derivatives, net | (156) | (227) | |||||||||||||||||||||||||||||||||||||||

| Realized gains on contract derivatives, net | 123 | 1,909 | |||||||||||||||||||||||||||||||||||||||

| Other realized losses, net | (128) | (197) | |||||||||||||||||||||||||||||||||||||||

| Other income (expense) | (6,426) | 176 | |||||||||||||||||||||||||||||||||||||||

| 2,372 | (3,399) | ||||||||||||||||||||||||||||||||||||||||

| Net Income (Loss) Before Income Taxes | (34,792) | (25,007) | |||||||||||||||||||||||||||||||||||||||

| Income tax benefit (expense) | (17) | 2,401 | |||||||||||||||||||||||||||||||||||||||

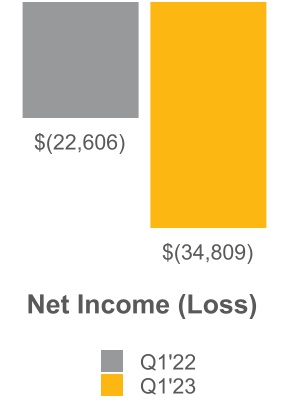

| Net Loss | (34,809) | (22,606) | |||||||||||||||||||||||||||||||||||||||

| Noncontrolling interests in loss of consolidated subsidiaries | 11,862 | 8,632 | |||||||||||||||||||||||||||||||||||||||

| Net Income (Loss) Attributable to Class A Shareholders | $ | (22,947) | $ | (13,974) | |||||||||||||||||||||||||||||||||||||

| Loss Per Class A Share | |||||||||||||||||||||||||||||||||||||||||

| Net loss per Class A share | |||||||||||||||||||||||||||||||||||||||||

| Basic | $ | (0.27) | $ | (0.16) | |||||||||||||||||||||||||||||||||||||

| Diluted | $ | (0.27) | $ | (0.16) | |||||||||||||||||||||||||||||||||||||

| Weighted average number of Class A shares outstanding | |||||||||||||||||||||||||||||||||||||||||

| Basic | 85,123,344 | 84,798,918 | |||||||||||||||||||||||||||||||||||||||

| Diluted | 85,123,344 | 84,798,918 | |||||||||||||||||||||||||||||||||||||||

See notes to unaudited condensed consolidated financial statements.

2

SUNLIGHT FINANCIAL HOLDINGS INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

(dollars in thousands)

| Shares | Preferred Stock | Common Stock | Additional Paid-in Capital | Accumulated Deficit | Treasury Stock | Total Stockholders' Equity | Noncontrolling Interests | Total Equity | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Class A | Class C | Class A | Class B | Class C | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | 83,619,915 | 47,287,370 | $ | — | $ | 8 | $ | — | $ | — | $ | 761,698 | $ | (501,635) | $ | (15,307) | $ | 244,764 | $ | 123,563 | $ | 368,327 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Equity-based compensation | 800,498 | — | — | — | — | — | 1,524 | — | — | 1,524 | 1,139 | 2,663 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares withheld related to net share settlement of equity awards | — | — | — | — | — | — | — | — | (1) | (1) | — | (1) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Class EX unit & Class C share exchange | 997,399 | (2,314,143) | — | 1 | — | — | (8,670) | — | 15,291 | 6,622 | (6,622) | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dilution | — | — | — | — | — | (7,488) | — | — | (7,488) | 7,488 | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cumulative ASC 326 adoption effect | — | — | — | — | — | — | 297 | — | 297 | 163 | 460 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | — | — | (22,947) | — | (22,947) | (11,862) | (34,809) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| March 31, 2023 | 85,417,812 | 44,973,227 | $ | — | $ | 9 | $ | — | $ | — | $ | 747,064 | $ | (524,285) | $ | (17) | $ | 222,771 | $ | 113,869 | $ | 336,640 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2021 | 86,373,596 | 47,595,455 | $ | — | $ | 9 | $ | — | $ | — | $ | 764,366 | $ | (186,022) | $ | (15,535) | $ | 562,818 | $ | 316,145 | $ | 878,963 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Equity-based compensation | — | — | — | — | — | — | 1,783 | — | — | 1,783 | 1,092 | 2,875 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares withheld related to net share settlement of equity awards | — | — | — | — | — | — | — | — | (55) | (55) | — | (55) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dilution | — | — | — | — | — | — | (394) | — | — | (394) | 394 | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Distribution | — | — | — | — | — | — | — | — | — | — | (1,373) | (1,373) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cumulative ASC 842 adoption effect | — | — | — | — | — | — | — | 238 | — | 238 | 41 | 279 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | — | — | — | (13,974) | — | (13,974) | (8,632) | (22,606) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| March 31, 2022 | 86,373,596 | 47,595,455 | $ | — | $ | 9 | $ | — | $ | — | $ | 765,755 | $ | (199,758) | $ | (15,590) | $ | 550,416 | $ | 307,667 | $ | 858,083 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

See notes to unaudited condensed consolidated financial statements.

3

SUNLIGHT FINANCIAL HOLDINGS INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(dollars in thousands)

| For the Three Months Ended March 31, | ||||||||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||||||||

| Cash Flows From Operating Activities | ||||||||||||||||||||||||||

| Net loss | $ | (34,809) | $ | (22,606) | ||||||||||||||||||||||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||||||||||||||||||||

| Depreciation and amortization | 8,521 | 22,447 | ||||||||||||||||||||||||

| Provision for losses | 2,169 | 638 | ||||||||||||||||||||||||

| Change in fair value of warrant liabilities | (3,366) | 4,884 | ||||||||||||||||||||||||

| Change in fair value of contract derivatives, net | 156 | 227 | ||||||||||||||||||||||||

| Other expense (income) | 5,807 | (176) | ||||||||||||||||||||||||

| Share-based payment arrangements | 3,555 | 3,860 | ||||||||||||||||||||||||

| Deferred income tax benefit | — | (2,401) | ||||||||||||||||||||||||

| Increase (decrease) in operating capital: | ||||||||||||||||||||||||||

| Decrease (increase) in advances | 27,862 | (19,513) | ||||||||||||||||||||||||

| Decrease (increase) in other assets | (666) | 3,949 | ||||||||||||||||||||||||

| Increase (decrease) in accounts payable and accrued expenses | 26,248 | (6,052) | ||||||||||||||||||||||||

| Increase (decrease) in funding commitments | 8,978 | (6,106) | ||||||||||||||||||||||||

| Decrease in other liabilities | (494) | (281) | ||||||||||||||||||||||||

| Net cash provided by (used in) operating activities | 43,961 | (21,130) | ||||||||||||||||||||||||

| Cash Flows From Investing Activities | ||||||||||||||||||||||||||

| Return of investments in loan pool participation and loan principal repayments | 237 | 307 | ||||||||||||||||||||||||

| Payments to acquire loans and participations in loan pools | (2,161) | (448) | ||||||||||||||||||||||||

| Payments to acquire property and equipment | (1,025) | (645) | ||||||||||||||||||||||||

| Net cash used in investing activities | (2,949) | (786) | ||||||||||||||||||||||||

| Cash Flows From Financing Activities | ||||||||||||||||||||||||||

| Repayments of borrowings under line of credit | (12,919) | — | ||||||||||||||||||||||||

| Payments for share-based payment tax withholding | (12) | (55) | ||||||||||||||||||||||||

| Net cash used in financing activities | (12,931) | (55) | ||||||||||||||||||||||||

| Net Increase (Decrease) in Cash, Cash Equivalents, and Restricted Cash | 28,081 | (21,971) | ||||||||||||||||||||||||

| Cash, Cash Equivalents, and Restricted Cash, Beginning of Period | 51,787 | 93,900 | ||||||||||||||||||||||||

| Cash, Cash Equivalents, and Restricted Cash, End of Period | $ | 79,868 | $ | 71,929 | ||||||||||||||||||||||

| Supplemental Disclosure of Cash Flow Information | ||||||||||||||||||||||||||

| Cash paid during the period for interest | $ | 373 | $ | 260 | ||||||||||||||||||||||

| Noncash Investing and Financing Activities | ||||||||||||||||||||||||||

| Distributions declared, but not paid | $ | — | $ | 1,373 | ||||||||||||||||||||||

| Capital expenditures incurred but not yet paid | 292 | 200 | ||||||||||||||||||||||||

| Deferred financing costs | 366 | — | ||||||||||||||||||||||||

See notes to unaudited condensed consolidated financial statements.

4

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(dollars in tables in thousands, except share, per share, unit, and per unit data)

Note 1. Organization and Business

Sunlight Financial Holdings Inc. (together with its consolidated subsidiaries, the “Company” or “Sunlight”) is a premier, technology-enabled point-of-sale finance company. Sunlight Financial LLC, its accounting predecessor and wholly-owned subsidiary, was organized as a Delaware limited liability company on January 23, 2014.

Business — Sunlight operates a technology-enabled financial services platform within the United States of America, using a nationwide network of contractors at the point-of-sale, to offer homeowners secured and unsecured loans (“Loans”), originated by third-party lenders, for the purchase and installation of residential solar energy systems and other home improvements. Sunlight arranges for the origination of Loans by third-party lenders in two distinct ways:

Direct Channel Loans — Sunlight arranges for certain Loans (“Direct Channel Loans”) to be originated and retained by third parties (“Direct Channel Partners”). The Direct Channel Partners originate the Direct Channel Loans directly, using their own credit criteria. These Direct Channel Partners pay for Direct Channel Loans by remitting funds to Sunlight, and Sunlight is thereafter responsible for making the appropriate payments to the relevant contractor. Sunlight earns income from the difference between the cash amount paid by a Direct Channel Partner to Sunlight for a given Direct Channel Loan and the dollar amount due to the contractor for such Direct Channel Loan. Sunlight does not participate in the ongoing economics of the Direct Channel Loans and, generally, does not retain any obligations with respect thereto except for certain ongoing fee-based administrative services and loan servicing performed by Sunlight.

Indirect Channel Loans — Sunlight arranges for other Loans (“Indirect Channel Loans”) to be originated by Cross River Bank, Sunlight’s issuing bank partner (“Bank Partner” or “CRB”). Sunlight has entered into program agreements with its Bank Partner that govern the terms and conditions with respect to originating and servicing the Indirect Channel Loans and Sunlight pays its Bank Partner a fee based on the principal balance of Loans originated by Sunlight’s Bank Partner. Sunlight’s Bank Partner funds these Loans by remitting funds to Sunlight, and Sunlight is thereafter responsible for making the appropriate payments to the relevant contractor. Sunlight arranges for the sale of certain Indirect Channel Loans, or participations therein, to third parties (“Indirect Channel Loan Purchasers”).

Liquidity and Going Concern — Sunlight has evaluated whether there are certain conditions and events, considered in the aggregate, that raised substantial doubt about its ability to continue as a going concern within one year after the date that the consolidated financial statements are issued.

As more fully described in Note 5, Sunlight borrows under a revolving credit facility with Silicon Valley Bank (“SVB”) that was due to mature on April 26, 2023. Prior to the SVB receivership and entry into a new Secured Term Loan with the Bank Partner (Note 11), Sunlight was in negotiations with SVB to extend the maturity date and to address Sunlight’s noncompliance with certain terms of the revolving credit facility. Prior to the issuance of these financial statements, these negotiations and the ability of Sunlight to amend and extend (or to replace) this revolving credit facility were uncertain, which could have had a material impact on Sunlight’s liquidity, cash and ability to attract new capital if not resolved on a timely basis.

Additionally, Sunlight’s Bank Partner holds Indirect Channel Loans on its balance sheet until directed by Sunlight in the ordinary course of its business to sell them to investors, including credit funds, insurance companies, and pension funds. While Sunlight’s Bank Partner is the owner of the loans, Sunlight retains economic exposure to them until they are sold. Sunlight profits when the price that investors pay for the Indirect Channel Loans exceeds the Bank Partner’s cost basis in the loans and incurs a loss when the price that investors pay for the Indirect Channel Loans is less than the Bank Partner’s cost basis in the loans. Prior to the execution of amendments (Note 11) to the loan agreements between Sunlight and its Bank Partner (“Bank Partner Agreements”), the Bank Partner Agreements capped the total amount of Indirect Channel Loans held by the Bank Partner at $450.0 million. However, the Indirect Channel Loans held by Sunlight’s Bank Partner included a significant amount of funded but unsold loans which were credit approved prior to certain pricing actions that Sunlight took in the third and fourth quarters of 2022 (the “Backbook Loans”). Despite the completion of the previously disclosed loan sale in December 2022, Sunlight was not in compliance with certain provisions of the Bank Partner Agreements, including the total loan cap.

5

Sunlight believes that the aforementioned conditions, considered in the aggregate, raised substantial doubt about its ability to continue as a going concern; however, on April 2, 2023, Sunlight entered into a Commitment and Transaction Support Agreement (“Commitment & Transaction Support Agreement”) with Sunlight’s Bank Partner and effective April 25, 2023 consummated the transactions agreed to under the agreement including, among other things, amendments to the Bank Partner Agreements (“Amended Bank Partner Agreements”) and entry into a Secured Term Loan with the Bank Partner (the “Secured Term Loan”), after March 31, 2023 that Sunlight believes alleviates such conditions as the Secured Term Loan, among other things, replaces the revolving credit facility with SVB with increased borrowing amounts and was used to pay off the SVB facility and the Amended Bank Partner Agreements, increasing the total amount of Indirect Channel Loans that Sunlight’s Bank Partner may hold (Note 11).

Sunlight believes such transactions, in addition to pricing actions that Sunlight took in the third and fourth quarters of 2022, provide cash and cash equivalents that will be reasonably sufficient to fund its operating expenses, capital expenditure requirements, and debt service payments through at least twelve months from the date that these consolidated financial statements were issued.

The accompanying consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty. Accordingly, the consolidated financial statements have been prepared on a basis that assumes Sunlight will continue as a going concern and which contemplates the realization of assets and satisfaction of liabilities and commitments in the ordinary course of business.

Note 2. Summary of Significant Accounting Policies

Basis of Presentation — The accompanying consolidated financial statements and related notes, prepared in accordance with U.S. generally accepted accounting principles (“GAAP”), include the accounts of Sunlight and its consolidated subsidiaries. In the opinion of management, all adjustments considered necessary for a fair presentation of Sunlight’s financial position, results of operations, and cash flows have been included and are of a normal and recurring nature. All intercompany balances and transactions have been eliminated.

Certain information and footnote disclosures normally included in financial statements prepared under GAAP may be condensed or omitted for interim financial reporting, and the operating results presented for interim periods are not necessarily indicative of the results that may be expected for any other interim period or for the entire year.

These financial statements should be read in conjunction with Sunlight’s audited financial statements for the year ended December 31, 2022 and footnotes thereto included in Sunlight's annual report on Form 10-K filed with the Securities and Exchange Commission (“SEC”) on May 4, 2023. Capitalized terms used herein, and not otherwise defined, are defined in Sunlight's consolidated financial statements for the year ended December 31, 2022.

Certain prior period amounts have been reclassified to conform to the current period's presentation.

Emerging Growth Company — The Company is an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, as amended (the “Securities Act”), as modified by the Jumpstart our Business Startups Act of 2012 (the “JOBS Act”), and it may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, reduced disclosure obligations regarding executive compensation in its periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

Further, Section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a Securities Act registration statement declared effective or do not have a class of securities registered under the Securities Exchange Act of 1934, as amended) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that an emerging growth company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies, but any such an election to opt out is irrevocable. The Company has elected not to opt out of such extended transition period, which means that when an accounting standard is issued or revised and it has different application dates for public or private companies, the Company, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard. This may make comparison of the Company’s financial statements with another public company that is neither an

6

emerging growth company nor an emerging growth company that has opted out of using the extended transition period difficult or impossible because of the potential differences in accounting standards used.

Consolidation — Sunlight consolidates those entities over which it controls significant operating, financial, and investing decisions of the entity as well as those entities deemed to be variable interest entities (“VIEs”) in which the Company is determined to be the primary beneficiary.

The analysis as to whether to consolidate an entity is subject to a significant amount of judgment. Some of the criteria considered are the determination as to the degree of control over an entity by its various equity holders, the design of the entity, how closely related the entity is to each of its equity holders, the relation of the equity holders to each other and a determination of the primary beneficiary in entities in which Sunlight has a variable interest. These analyses involve estimates, based on the assumptions of management, as well as judgments regarding significance and the design of entities.

VIEs are defined as entities in which equity investors do not have the characteristics of a controlling financial interest or do not have sufficient equity at risk for the entity to finance its activities without additional subordinated financial support from other parties. A VIE is required to be consolidated by its primary beneficiary, and only by its primary beneficiary, which is defined as the party who has the power to direct the activities of a VIE that most significantly impact its economic performance and who has the obligation to absorb losses or the right to receive benefits from the VIE that could potentially be significant to the VIE.

Sunlight monitors investments in VIEs and analyzes the potential need to consolidate the related entities pursuant to the VIE consolidation requirements. These analyses require considerable judgment in determining whether an entity is a VIE and determining the primary beneficiary of a VIE since they involve subjective determinations of significance with respect to both power and economics. The result could be the consolidation of an entity that otherwise would not have been consolidated or the deconsolidation of an entity that otherwise would have been consolidated.

A wholly-owned subsidiary of Sunlight Financial Holdings Inc. is the managing member of Sunlight Financial LLC, in which existing unitholders hold a 34.4% and 35.9% noncontrolling interest, net of unvested Class EX Units (Note 6), at March 31, 2023 and December 31, 2022, respectively.

Through its indirect managing member interest, Sunlight Financial Holdings Inc. directs substantially all of the day-to-day activities of Sunlight Financial LLC. The third-party investors in Sunlight Financial LLC do not possess substantive participating rights or the power to direct the day-to-day activities that most directly affect the operations of Sunlight Financial LLC. However, these third-party investors hold both voting, noneconomic Class C shares in Sunlight Financial Holdings Inc. on a one-for-one basis along with nonvoting, economic Class EX Units issued by Sunlight Financial LLC. No single third-party investor, or group of third-party investors, possesses the substantive ability to remove the managing member of Sunlight Financial LLC. Sunlight considers Sunlight Financial LLC a VIE for consolidation purposes and its managing member holds the controlling interest and is the primary beneficiary. Therefore, Sunlight consolidates Sunlight Financial LLC and reflects Class EX unitholder interests in Sunlight Financial LLC held by third parties as noncontrolling interests.

Sunlight conducts substantially all operations through Sunlight Financial LLC and its consolidated subsidiary.

Segments — Sunlight operates through one operating and reportable segment, which reflects how the chief operating decision maker allocates resources and assesses performance. Sunlight arranges for the origination of Loans by third-party lenders using a predominately single expense pool.

Risks and Uncertainties — In the normal course of business, Sunlight primarily encounters credit risk, which is the risk of default on Sunlight’s investments that results from a borrower’s or counterparty’s inability or unwillingness to make contractually required payments, and interest rate risk, which impacts the value of Indirect Channel Loans for which Sunlight facilitates sales.

Use of Estimates — The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenue and expenses during the reporting period. Management makes subjective estimates of: pending loan originations and sales, which significantly impacts revenues; determinations of fair value, including goodwill, derivatives, and servicing rights; estimates regarding loan performance, which impacts impairments and allowances for loan losses; project installations, which impacts guarantee obligations; and the useful lives of intangible assets. Actual results may differ from those estimates.

7

Fair Value — GAAP requires the categorization of the fair value of financial instruments into three broad levels that form a hierarchy based on the transparency of inputs to the valuation.

| Level | Measurement | |||||||

| 1 | Inputs are unadjusted, quoted prices in active markets for identical assets or liabilities at the measurement date. | |||||||

| 2 | Inputs are other than quoted prices that are observable for the asset or liability, either directly or indirectly. Level 2 inputs include quoted prices for similar instruments in active markets, and inputs other than quoted prices that are observable for the asset or liability. | |||||||

| 3 | Inputs are unobservable for the asset or liability, and include situations where there is little, if any, market activity for the asset or liability. | |||||||

Sunlight follows this hierarchy for its financial instruments, with classifications based on the lowest level of input that is significant to the fair value measurement. The following summarizes Sunlight’s financial instruments hierarchy at March 31, 2023:

| Level | Financial Instrument | Measurement | ||||||||||||

| 1 | Cash and cash equivalents and restricted cash | Estimates of fair value are measured using observable, quoted market prices, or Level 1 inputs | ||||||||||||

| Public Warrants | Estimates of fair value are measured using observable, quoted market prices of Sunlight’s warrants. | |||||||||||||

| 2 | Servicing liabilities | Estimates of fair value are measured based upon observable market data. | ||||||||||||

| 3 | Loans and loan participations, held-for-investment | Estimated fair value is generally determined by discounting the expected future cash flows using inputs such as discount rates. | ||||||||||||

| Contract derivative | Estimated fair value based upon discounted expected future cash flows arising from the contract. | |||||||||||||

| Private Placement Warrants | Estimated fair value based upon quarterly valuation estimates of warrant instruments, based upon quoted prices of Sunlight’s Class A shares and warrants thereon as well as fair value inputs provided by an independent valuation firm. | |||||||||||||

Valuation Process — On a quarterly basis, with assistance from an independent valuation firm, management estimates the fair value of Sunlight’s Level 3 financial instruments. Sunlight’s determination of fair value is based upon the best information available for a given circumstance and may incorporate assumptions that are management’s best estimates after consideration of a variety of internal and external factors. When an independent valuation firm expresses an opinion on the fair value of a financial instrument in the form of a range, management selects a value within the range provided by the independent valuation firm to assess the reasonableness of management’s estimated fair value for that financial instrument. At March 31, 2023, Sunlight’s valuation process for Level 3 measurements, as described below, was conducted internally or by an independent valuation firm and reviewed by management.

Valuation of Loans and Loan Participations — Management generally considers Sunlight's loans and loan participations Level 3 assets in the fair value hierarchy as such assets are illiquid investments that are specific to the loan product, for which there is limited market activity. On a quarterly basis, management engages an independent valuation firm to estimate the fair value of each loan or loan participation categorized as a Level 3 asset.

Valuation of Contract Derivative — Management considers Sunlight's contracts under which Sunlight (a) arranged Indirect Channel Loans for the purchase and installation of home improvement other than residential solar energy systems until December 2022 (“Contract Derivative 1”) and (b) earns income from the prepayment of certain of those Loans sold to an Indirect Channel Loan Purchaser (“Contract Derivative 2”), both considered derivatives under GAAP, as Level 3 financial instruments in the fair value hierarchy as such instruments represent bilateral, nontraded agreements for which there is limited market activity. On a quarterly basis, management engages an independent valuation firm to estimate the fair value of the contracts.

Valuation of Servicing Liabilities — Sunlight assumes an obligation to service certain loans when originated. Sunlight evaluates compensation it receives to service these loans, if any, against the servicing costs a willing market participant

8

would require to service loans with similar characteristics to service such loans. At March 31, 2023 and December 31, 2022, Sunlight determined that the compensation it receives for certain servicing agreements are less than the estimated market cost to service and recognized a liability reported within Other Liabilities in the accompanying Unaudited Condensed Consolidated Balance Sheet. Servicing liabilities are considered Level 2 financial instruments, as the primary components of the fair value are obtained from observable inputs based on market data, reasonably adjusted for assumptions that would be used by market participants to service our Bank Partner loans, for which market data is not available.

Valuation of Warrants — Management considers the Private Placement Warrants (Note 6) redeemable for Sunlight’s equity as Level 3 liabilities in the fair value hierarchy as liquid markets do not exist for such liabilities. On a quarterly basis, management engages an independent valuation firm to estimate the fair value of Sunlight’s warrants, which includes models that include estimates of volatility, contractual terms, discount rates, dividend rates, expiration dates, and risk-free rates.

Other Valuation Matters — For Level 3 financial assets acquired and financial liabilities assumed during the calendar month immediately preceding a quarter end that were conducted in an orderly transaction with an unrelated party, management generally believes that the transaction price provides the most observable indication of fair value given the illiquid nature of these financial instruments, unless management is aware of any circumstances that may cause a material change in the fair value through the remainder of the reporting period. For instance, significant changes in a counterparty’s intent or ability to make payments on a financial asset may cause material changes in the fair value of that financial asset.

See Note 7 for additional information regarding the valuation of Sunlight's financial assets and liabilities.

Sales of Financial Assets and Financing Agreements — Sunlight will, from time to time, facilitate the sale of Indirect Channel Loans. In each case, the transferred loans are legally isolated from Sunlight and control of the transferred loans passes to the transferee, who may pledge or exchange the transferred asset without constraint of Sunlight. Sunlight neither recognizes any financial assets nor incurs any liabilities as a result of the sale, but does recognize revenue based upon the difference between proceeds received from the transferee and the proceeds paid to the transferor.

Leases — Sunlight recognizes right-of-use assets and lease liabilities at the commencement date of the lease based on the present value of remaining fixed and determinable lease payments over the lease term. Sunlight calculates the present value of future payments by using an estimated incremental borrowing rate, which approximates the rate at which Sunlight would borrow on a secured basis and over a similar term, and recognizes lease expense for operating leases on a straight-line basis over the lease term. Right-of-use assets represent Sunlight’s right to control the use of an identified asset for the lease term and lease liabilities represent Sunlight’s obligation to make lease payments arising from the lease. Sunlight uses the incremental borrowing rate on the commencement date in determining the present value of the lease payments.

Balance Sheet Measurement

Cash and Cash Equivalents and Restricted Cash — Cash and cash equivalents consist of bank checking accounts and money market accounts. Sunlight considers all highly liquid investments with original maturities of three months or less at the time of purchase to be cash equivalents. Sunlight maintains cash in restricted accounts pursuant to various lending agreements and considers other cash amounts restricted under certain agreements with other counterparties. Substantially all amounts on deposit with major financial institutions exceed insured limits. Cash and cash equivalents and restricted cash are carried at cost, which approximates fair value. Sunlight reported cash and cash equivalents and restricted cash in the following line items of its Unaudited Condensed Consolidated Balance Sheets, which totals the aggregate amount presented in Sunlight’s Unaudited Condensed Consolidated Statements of Cash Flows:

| March 31, 2023 | December 31, 2022 | ||||||||||||||||

| Cash and cash equivalents | $ | 75,518 | $ | 47,515 | |||||||||||||

| Restricted cash and cash equivalents | 4,350 | 4,272 | |||||||||||||||

| Total cash, cash equivalents, and restricted cash shown in the Consolidated Statement of Cash Flows | $ | 79,868 | $ | 51,787 | |||||||||||||

Financing Receivables — Sunlight records financing receivables for (a) advances that Sunlight remits to contractors to facilitate the installation of residential solar systems and the construction or installation of other home improvement projects and (b) loans and loan participations.

9

Advances — In certain circumstances, Sunlight will provide a contractually agreed upon percentage of cash to a contractor related to a Loan that has not yet been funded by either a Direct Channel Partner or its Bank Partner as well as amounts funded to contractors in anticipation of loan funding. Such advances are generally repaid upon the earlier of (a) a specified number of days from the date of the advance outlined within the respective contractor contract or (b) the substantial installation of the residential solar system or the construction or installation of other home improvement projects. In either case, Sunlight will net such amounts advanced from payments otherwise due to the related contractor. Sunlight carries advances at the amount advanced, net of allowances for losses and charge-offs. In the first quarter of 2023, Sunlight suspended its advance program and has significantly reduced outstanding advances.

Loans and Loan Participations — Sunlight recognizes Indirect Channel Loans purchased from Sunlight’s Bank Partner as well as its 5.0% participation interests in Indirect Channel Loans as financing receivables held-for-investment based on management's intent, and Sunlight's ability, to hold those investments through the foreseeable future or contractual maturity. Financing receivables that are held‑for‑investment are carried at their aggregate outstanding face amount, net of applicable (a) unamortized acquisition premiums and discounts, (b) allowance for losses and (c) charge-offs or write-downs of impaired receivables. If management determines a loan or loan participation is impaired, management writes down the loan or loan participation through a charge to the provision for losses. See “— Impairment” for additional discussion regarding management’s determination for loan losses. Sunlight applies the interest method to amortize acquisition premiums and discounts or on a straight-line basis when it approximates the interest method. Sunlight has not acquired any material loans with deteriorated credit quality that were not charged off upon purchase.

Impairment — Sunlight holds financing receivables carried at amortized cost for which management evaluates credit quality indicators at least quarterly to establish allowance for credit losses for advances, loans, and loan participations that represent management's estimate of expected credit losses over the remaining expected life of those financial assets after considering contractual terms, expected prepayments, and cancellation features. The income statement effect of all changes in the allowance for credit losses is recognized in the provision for credit losses. Determining the appropriateness of the allowance for credit losses is complex and requires significant judgment by management about the effect of matters that are inherently uncertain. Subsequent evaluations of credit exposures, considering the macroeconomic conditions, forecasts, and other factors then prevailing, may result in significant changes in the allowance for credit losses in future periods.

To the extent Sunlight’s credit exposures share risk characteristics with other similar exposures, such credit exposure is collectively assessed for impairment, which includes Sunlight’s loan and loan participations and certain advances. If an exposure does not share risk characteristics with other exposures, Sunlight generally estimates expected credit losses on an individual basis, considering expected repayment and conditions impacting that individual credit exposure, which primarily applies to advances to certain contractors. The assessment of risk characteristics is subject to significant management judgment. Emphasizing one characteristic over another or considering additional characteristics could affect the allowance. Refer to Note 3 for risk characteristics applicable to Sunlight’s financing receivables.

Estimating the timing and amounts of future cash flows is highly judgmental as these cash flow projections rely upon estimates such as loss severities, asset valuations, default rates, the amounts and timing of interest or principal payments (including any expected prepayments) or other factors that are reflective of current and expected market conditions. These estimates are, in turn, dependent on factors such as the duration of current overall economic conditions, industry, portfolio, or borrower-specific factors as well as, in certain circumstances, other economic factors. All of these estimates and assumptions require significant management judgment and certain assumptions are highly subjective. Actual losses, if any, could materially differ from these estimates.

If management deems that it is probable that Sunlight will be unable to collect all amounts owed according to the contractual terms of a receivable, impairment of that receivable is indicated. Consistent with this definition, all receivables for which the accrual of interest has been discontinued (nonaccrual loans) are considered impaired. If management considers a receivable to be impaired, management establishes an allowance for losses through a valuation provision in earnings, which reduces the carrying value of the receivable to (a) the amounts management expects to collect, for receivables due within 90 days, or (b) the present value of expected future cash flows discounted at the receivable’s contractual effective rate. Impaired financing receivables are charged off against the allowance for losses when a financing receivable is more than 120 days past due or when management believes that collectability of the principal is remote, if earlier. Sunlight credits subsequent recoveries, if any, to the allowance when received.

Sunlight individually evaluates nonaccrual loans with contractual balances of $50,000 or more to establish specific allowances for such receivables, if required.

10

Advances — For advances made by Sunlight, management performs an evaluation of credit quality indicators using financial information obtained from its counterparties and third parties as well as historical experience. Such indicators may include the borrower’s financial wherewithal and recent operating performance as well as macroeconomic trends. Management rates the potential for advance receivables by reviewing the counterparty. The counterparty is rated by overall risk tier on a scale of “1” through “5,” from least to greatest risk, which management reviews and updates on at least an annual basis. Counterparties may be granted advance approval within any overall risk tier, however tier “5” advance approvals are approved on an exception basis. A subset category of the overall risk tier is the financial risk of the counterparty. As with the overall risk tier, counterparties may be granted advance approval within any financial risk tier; however financial risk tier “5” advance approvals are approved on an exception basis. As part of that approval, management will set an individual counterparty advance dollar limit, which cannot be exceeded prior to additional review and approval. The overall risk tiers are defined as follows:

| 1 | Low Risk | The counterparty has demonstrated low risk characteristics. The counterparty is a well-established company within the applicable industry, with low commercial credit risk, excellent reputational risk (e.g. online ratings, low complaint levels), and an excellent financial risk assessment. | ||||||||||||

| 2 | Low-to-Medium Risk | The counterparty has demonstrated low to medium risk characteristics. The counterparty is a well-established company within the applicable industry, with low to medium commercial credit risk, excellent to above average reputational risk (e.g. online ratings, lower complaint levels), and/or an excellent to above average financial risk assessment. | ||||||||||||

| 3 | Medium Risk | The counterparty has demonstrated medium risk characteristics. The counterparty may be a less established company within the applicable industry than risk tier "1" or "2", with medium commercial credit risk, excellent to average reputational risk (e.g., online ratings, average complaint levels), and/or an excellent to average financial risk assessment. | ||||||||||||

| 4 | Medium-to-High Risk | The counterparty has demonstrated medium to high risk characteristics. The counterparty is likely to be a less established company within the applicable industry than risk tiers "1" through "3," with medium to high commercial credit risk, excellent to below average reputational risk (e.g. online ratings, higher complaint levels), and/or an excellent to below average financial risk assessment. | ||||||||||||

| 5 | Higher Risk | The counterparty has demonstrated higher risk characteristics. The counterparty is a less established company within the applicable industry, with higher commercial credit risk, and/or below average reputational risk (e.g. online ratings, higher complaint levels), and/or below average financial risk assessment. Tier "5" advance approvals will be approved on an exception basis. | ||||||||||||

Loans and Loan Participations, Held-For-Investment — Sunlight aggregates performing loans and loan participations into pools for the evaluation of impairment based on like characteristics, such as loan type and acquisition date. Pools of loans are evaluated based on criteria such as an analysis of borrower performance, credit ratings of borrowers, and historical trends in defaults and loss severities for the type and seasoning of loans and loan participations under evaluation.

Goodwill — Goodwill represents the excess of the purchase price over the estimated fair values of the net tangible and intangible assets of acquired entities. Sunlight performs a goodwill impairment test annually during the fourth quarter of the fiscal year and more frequently if an event or circumstance indicates that impairment may have occurred. Triggering events that may indicate a potential impairment include, but are not limited to, significant adverse changes in customer demand or business climate and related competitive considerations. Sunlight first performs a qualitative assessment to determine whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount. If so, Sunlight performs a two-step goodwill impairment test to identify potential goodwill impairment and measure the amount of goodwill impairment loss to be recognized by the applicable reporting unit(s). If Sunlight determines that the implied fair value of a reporting unit is greater than its carrying amount, the two-step goodwill impairment test is not required. Sunlight has one reporting unit and fully impaired any remaining carrying value of goodwill at December 31, 2022.

Intangible Assets, Net — Sunlight identified the following intangible assets, recorded at fair value at the Closing Date of the Business Combination, and carried at a value net of amortization over their estimated useful lives on a straight-line basis. Sunlight’s intangible assets are evaluated for impairment on at least a quarterly basis:

11

| Estimated Useful Life (in Years) | Carrying Value | |||||||||||||||||||||||||||||||||||||

| Asset | March 31, 2023 | December 31, 2022 | ||||||||||||||||||||||||||||||||||||

Contractor relationships(a) | 11.5 | $ | 350,000 | $ | 350,000 | |||||||||||||||||||||||||||||||||

Trademarks/ trade names(b) | 10.0 | 7,900 | 7,900 | |||||||||||||||||||||||||||||||||||

Developed technology(c) | 3.0 | — | 5.0 | 12,247 | 11,163 | |||||||||||||||||||||||||||||||||

| 370,147 | 369,063 | |||||||||||||||||||||||||||||||||||||

Accumulated amortization(d)(e)(f) | (57,558) | (49,143) | ||||||||||||||||||||||||||||||||||||

| $ | 312,589 | $ | 319,920 | |||||||||||||||||||||||||||||||||||

a.Represents the value of existing contractor relationships of Sunlight estimated using a multi-period excess earnings methodology.

b.Represents the trade names that Sunlight originated or acquired and valued using a relief-from-royalty method.

c.Represents technology developed by Sunlight for the purpose of generating income for Sunlight, and valued using a replacement cost method.

d.Amounts include amortization expense of $0.4 million and $0.1 million related to capitalized internally developed software costs for the three months ended March 31, 2023 and 2022, respectively.

e.Includes amortization expense of $8.4 million and $22.3 million for the three months ended March 31, 2023 and 2022, respectively.

f.At March 31, 2023, the approximate aggregate annual amortization expense for definite-lived intangible assets, including capitalized internally developed software costs as a component of capitalized developed technology, are as follows:

| Developed Technology | Other Identified Intangible Assets | Total | ||||||||||||||||||

| April 1, through December 31, 2023 | $ | 2,175 | $ | 23,506 | $ | 25,681 | ||||||||||||||

| 2024 | 3,091 | 31,285 | 34,376 | |||||||||||||||||

| 2025 | 2,496 | 31,199 | 33,695 | |||||||||||||||||

| 2026 | 777 | 31,199 | 31,976 | |||||||||||||||||

| 2027 | — | 31,199 | 31,199 | |||||||||||||||||

| Thereafter | — | 155,662 | 155,662 | |||||||||||||||||

| $ | 8,539 | $ | 304,050 | $ | 312,589 | |||||||||||||||

Property and Equipment, Net — Property and equipment are recorded at cost, less accumulated depreciation and amortization. Depreciation and amortization are calculated using the straight-line method over the following estimated useful lives:

| Estimated Useful Life (in Years) | Carrying Value | |||||||||||||||||||||||||||||||||||||

| Asset Category | March 31, 2023 | December 31, 2022 | ||||||||||||||||||||||||||||||||||||

| Furniture, fixtures, and equipment | 5 | $ | 1,512 | $ | 1,512 | |||||||||||||||||||||||||||||||||

| Computer hardware | 5 | 1,328 | 1,328 | |||||||||||||||||||||||||||||||||||

| Computer software | 1 | — | 3 | 278 | 338 | |||||||||||||||||||||||||||||||||

| 3,118 | 3,178 | |||||||||||||||||||||||||||||||||||||

Accumulated amortization and depreciation(a) | (1,735) | (1,689) | ||||||||||||||||||||||||||||||||||||

| $ | 1,383 | $ | 1,489 | |||||||||||||||||||||||||||||||||||

a.Includes depreciation expense of $0.1 million and $0.1 million the three months ended March 31, 2023 and 2022, respectively.

Funding Commitments — Pursuant to Sunlight’s contractual arrangements with its Bank Partner, Direct Channel Partners, and contractors, each of Sunlight’s Direct Channel Partners and its Bank Partner periodically remits to Sunlight the cash related to loans the funding source has originated. Sunlight has committed to funding such amounts, less any amounts Sunlight is entitled to retain, to the relevant contractor when certain milestones relating to the installation of residential solar systems or the construction of installation of other home improvement projects underlying the consumer receivable have been reached. Sunlight presents any amounts that Sunlight retains in anticipation of a contractor completing an installation milestone as “Funding Commitments” on the accompanying Unaudited Condensed Consolidated Balance Sheets, which totaled $29.4 million and $20.4 million at March 31, 2023 and December 31, 2022, respectively.

Guarantees — Sunlight records a liability for the guarantees it makes for certain Loans if it determines that it is probable that it will have to repurchase those loans, in an amount based on the likelihood of such repurchase and the loss, if any, Sunlight expects to incur in connection with its repurchase of Loans that may have experienced credit deterioration since the time of the loan’s origination.

Warrants — The Company has public and private placement warrants classified as liabilities as well as warrants issued to a capital provider classified as equity. The Company classifies as equity any equity-linked contracts that (a) require

12

physical settlement or net-share settlement or (b) give the Company a choice of net-cash settlement or settlement in the Company’s own shares (physical settlement or net-share settlement). Warrants classified as equity are initially measured at fair value. Subsequent changes in fair value are not recognized as long as the warrants continue to be classified as equity.

The Company classifies as assets or liabilities any equity-linked contracts that (a) require net-cash settlement (including a requirement to net-cash settle the contract if an event occurs and if that event is outside the Company’s control) or (b) give the counterparty a choice of net-cash settlement or settlement in shares (physical settlement or net-share settlement). For equity-linked contracts that are classified as liabilities, the Company records the fair value of the equity-linked contracts at each balance sheet date and records the change in the statements of operations as a gain (loss) from change in fair value of warrant liability. The Company’s public warrant liability is valued using observable market prices for those public warrants. The Company’s private placement warrants are valued using a binomial lattice pricing model when the warrants are subject to the make-whole table, or otherwise are valued using a Black-Scholes pricing model. The Company’s warrants issued to a capital provider are valued using a Black-Scholes pricing model based on observable market prices for public shares and warrants. The assumptions used in preparing these models include estimates such as volatility, contractual terms, discount rates, dividend yield, expiration dates and risk-free rates.

Distributions Payable — Sunlight Financial LLC accrues estimated tax payments to holders of its members’ equity when earned in accordance with Sunlight Financial LLC’s organizational agreements. On March 31, 2022, Sunlight accrued $1.4 million, or $0.03 per Class EX Unit, to its noncontrolling interests. Ratable estimated tax payments from Sunlight Financial LLC to members consolidated by Sunlight are eliminated in consolidation. As of March 31, 2023, Sunlight Financial LLC did not generate taxable income during the year ended March 31, 2023 and expects to use tax distributions already declared during the current tax year to offset future estimated tax liability distributions, if any.

Other Assets and Accounts Payable, Accrued Expenses, and Other Liabilities — At March 31, 2023 and December 31, 2022, (a) other assets included Sunlight’s contract derivatives, right-of-use assets arising from operating leases, prepaid expenses, accounts receivable, deferred financing costs, and interest receivable, and (b) accounts payable, accrued expenses, and other liabilities included Sunlight’s guarantee liability, lease liabilities, servicing liabilities, accrued compensation, and other payables.

Noncontrolling Interests in Consolidated Subsidiaries — Noncontrolling interests represent the portion of Sunlight Financial LLC that the Company controls and consolidates but does not own. The Company recognizes each noncontrolling holder’s respective share of the estimated fair value of the net assets at the date of formation or acquisition. Noncontrolling interests are subsequently adjusted for the noncontrolling holder’s share of additional contributions, distributions, and their share of the net earnings or losses of each respective consolidated entity. The Company allocates net income or loss to noncontrolling interests based on the weighted average ownership interest during the period. The net income or loss that is not attributable to the Company is reflected in net income (loss) attributable to noncontrolling interests in the Unaudited Condensed Consolidated Statements of Operations. The Company does not recognize a gain or loss on transactions with a consolidated entity in which it does not own 100% of the equity, but the Company reflects the difference in cash received or paid from the noncontrolling interests carrying amount as additional paid-in-capital.

Class EX Units issued by Sunlight Financial LLC are exchangeable, along with the Company’s Class C shares on a one-for-one basis, into the Company’s Class A common stock. Class A common stock issued upon exchange of a holder’s noncontrolling interest is accounted for at the carrying value of the surrendered limited partnership interest and the difference between the carrying value and the fair value of the Class A common stock issued is recorded to additional paid-in-capital.

Treasury Stock — Sunlight accounts for treasury stock under the cost method. When treasury stock is re-issued at a price higher than its cost, the difference is recorded as a component of additional paid-in-capital. When treasury stock is re-issued at a price lower than its cost, the difference is recorded as a component of additional paid-in-capital to the extent that there are previously recorded gains to offset the losses. If there are no treasury stock gains in additional paid-in-capital, the losses upon re-issuance of treasury stock are recorded as a reduction of retained earnings.

13

Income Recognition

Revenue Recognition — Sunlight recognizes revenue from (a) platform fees on the Direct Channel Loans when the Direct Channel Partner funds the Loans and on the Indirect Channel Loans when the Indirect Channel Loan Purchaser buys the Loans from the balance sheet of Sunlight’s Bank Partner and (b) loan portfolio management, servicing, and administration services on a monthly basis as Sunlight provides such services for that month. Sunlight’s contracts include the following groups of similar services, which do not include any significant financing components:

| For the Three Months Ended March 31, | ||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||||||||||||||||||||||||||

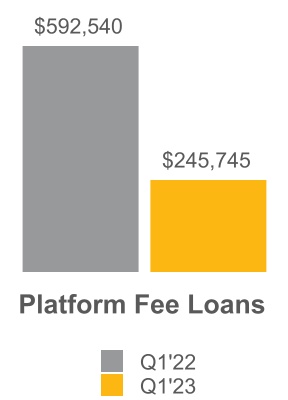

Platform fees, net(a) | $ | 17,909 | $ | 26,154 | ||||||||||||||||||||||||||||||||||||||||

Other revenues(b) | 2,556 | 2,077 | ||||||||||||||||||||||||||||||||||||||||||

| $ | 20,465 | $ | 28,231 | |||||||||||||||||||||||||||||||||||||||||

a.Amounts presented net of variable consideration in the form of rebates to certain contractors.

b.Includes loan portfolio management, administration, and other ancillary fees Sunlight earns that are incidental to its primary operations.

Platform Fees, Net — Sunlight arranges Loans for the purchase and installation of residential solar energy systems on behalf of its Direct Channel Partners, Bank Partner, and Indirect Channel Loan Purchasers. As agent, Sunlight presents platform fees on a net basis at the time that Direct Channel Partners or Indirect Channel Loan Purchasers obtain control of the service provided to facilitate their origination or purchase of a Loan, which is no earlier than when Sunlight delivers loan documentation to the customer. Sunlight wholly satisfies its performance obligation to Direct Channel Partners, Bank Partner, and Indirect Channel Loan Purchasers, as it relates to such platform fees, upon origination or purchase of a Loan. Sunlight considers rebates offered by Sunlight to certain contractors in exchange for volume commitments as variable components to transaction prices; such variability resolves upon the contractor’s satisfaction of their volume commitment.

The contracts under which Sunlight (a) arranges Indirect Channel Loans for the purchase and installation of home improvements other than residential solar energy systems until December 2022 and (b) earns income from the prepayment of certain Indirect Channel Loans for the purchase and installation of home improvements other than residential solar energy systems sold to an Indirect Channel Loan Purchaser are considered derivatives under GAAP. As such, Sunlight’s revenues exclude the platform fees that Sunlight earns in connection with these contracts. Instead, Sunlight records realized gains on the derivatives within “Realized Gains on Contract Derivative, Net” in the accompanying Unaudited Condensed Consolidated Statements of Operations. Sunlight realized gains (losses) of $0.1 million, and $1.9 million, for the three months ended March 31, 2023 and 2022, respectively (Note 4). Sunlight recognized platform fee revenue for its facilitation of Direct Channel Loans for the purchase and installation of home improvements other than residential solar energy systems of $1.6 million and $0.5 million, for the three ended March 31, 2023 and 2022, respectively.

Other Revenues — Sunlight provides monthly services in connection with the portfolio management, servicing, and administration of Loans originated by certain Direct Channel Partners, Sunlight’s Bank Partner, and an Indirect Channel Loan Purchaser. Such services may include the reporting of loan performance information, administration of servicing performed by third parties, and portfolio management services.

Interest Income — Loans where management expects to collect all contractually required principal and interest payments are considered performing loans. Sunlight accrues interest income on performing loans based on the unpaid principal balance (“UPB”) and contractual terms of the loan. Interest income also includes discounts associated with the loans purchased as a yield adjustment using the effective interest method over the loan term. Sunlight expenses direct loan acquisition costs for loans acquired by Sunlight as incurred. Sunlight does not accrue interest on loans placed on non-accrual status or on loans where the collectability of the principal or interest of the loan are deemed uncertain.

14

Loans are considered past due or delinquent if the required principal and interest payments have not been received as of the date such payments are due. Generally, loans, including impaired loans, are placed on non-accrual status when (a) either principal or interest payments are 90 days or more past due based on contractual terms or (b) an individual analysis of a borrower’s creditworthiness indicates a loan should be placed on non-accrual status. When a loan owned by Sunlight (each, a “Balance Sheet Loan”) is placed on non-accrual status, Sunlight ceases to recognize interest income on the loans and reverses previously accrued and unpaid interest, if any. Subsequent receipts on non-accrual loans are recorded as a reduction of principal, and interest income may only be recorded on a cash basis after recovery of principal is reasonably assured. Sunlight may return a loan to accrual status when repayment of principal and interest is reasonably assured under the terms of the restructured loan. Advances are created at par and do not bear, and therefore do not accrue, interest income. In addition to loans and loan participations, Sunlight recognizes interest income on a specified proportion of the contractual interest and original issue discount on Indirect Channel Loans held by Sunlight’s Bank Partner.

Expense Recognition

Cost of Revenues — Sunlight’s cost of revenues includes the aggregate costs of the services that Sunlight performs to satisfy its contractual performance obligations to customers as well as variable consideration that Sunlight pays for its fee revenue that do not meet the criteria necessary for netting against gross revenues.

Sunlight Rewards™ Program — The Sunlight Rewards™ Program is a proprietary loyalty program that Sunlight offers to salespeople selling residential solar systems for Sunlight’s network of contractors. Sunlight records a contingent liability using the estimated incremental cost of each point based upon the points earned, the redemption value, and an estimate of probability of redemption consistent with Sunlight’s historical redemption experience under the program. When a salesperson redeems points from Sunlight’s third-party loyalty program vendor, Sunlight pays the stated redemption value of the points redeemed to the vendor.

Compensation and Benefits — Management expenses salaries, benefits, and equity-based compensation as services are provided. “Compensation and Benefits” in the accompanying Unaudited Condensed Consolidated Statements of Operations includes expenses not otherwise included in Sunlight’s cost of revenues, such as compensation costs associated with information technology, sales and marketing, product management, and overhead.

Equity-Based Compensation — Sunlight granted awards of restricted stock units (“RSUs”) to employees and directors under Sunlight’s 2021 Equity Incentive Plan (“Equity Plan”). RSUs are Class A restricted share units which entitle the holder to receive Class A Shares on various future dates if the applicable service conditions, if any, are met. Sunlight expenses the grant-date fair value of awards on a straight-line basis over the requisite service period. Sunlight does not estimate forfeitures, and records actual forfeitures as they occur.

Selling, General, and Administrative — Management expenses selling, general, and administrative costs, including legal, audit, other professional service fees, travel and entertainment, and insurance premiums as incurred. Sunlight recognizes expenses associated with co-marketing agreements when earned by the counterparty.

Property and Technology — Management expenses rent, information technology and telecommunication services, and noncapitalizable costs to internally develop software as incurred.

Income Taxes — The Company accounts for income taxes under the asset and liability method. Under this method, deferred tax assets and liabilities are determined based on differences between the consolidated financial statement carrying amounts and tax bases of assets and liabilities and operating loss and tax credit carryforwards and are measured using the enacted tax rates that are expected to be in effect when the differences reverse. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the Unaudited Condensed Consolidated Statements of Operations in the period that includes the enactment date. Valuation allowances are established when necessary to reduce deferred tax assets to an amount that, in the opinion of management, is more likely than not to be realized.

The Company accounts for uncertain tax positions by reporting a liability for unrecognizable tax benefits resulting from uncertain tax positions taken or expected to be taken in a tax return. The Company recognizes interest and penalties, if any, related to unrecognized tax benefits in income tax expense.

In accordance with the operating agreement of Sunlight Financial LLC, to the extent possible without impairing its ability to continue to conduct its business and activities, and in order to permit its member to pay taxes on the taxable income allocated to those members, Sunlight Financial LLC is required to make distributions to the member in the amount equal to the estimated tax liability of the member computed as if the member paid income tax at the highest marginal federal

15

and state rate applicable to a corporate entity or individual resident in New York, New York to the extent Sunlight’s operations generate taxable income allocable to the applicable member. Sunlight Financial LLC did not declare any distributions during the three months ended March 31, 2023, and declared $1.4 million of distributions during the three months ended March 31, 2022. As of March 31, 2023, Sunlight Financial LLC does not expect to generate taxable income during the current tax year and expects to use unpaid tax distributions already declared to offset future estimated tax liability distributions, if any. Consequently, Sunlight Financial LLC did not declare any further distributions through March 31, 2023.

Recent Accounting Pronouncements Issued, But Not Yet Adopted

The Financial Accounting Standards Board (“FASB”) has issued the following Accounting Standard Updates (“ASUs”) that may materially impact Sunlight’s financial position and results of operations, or may impact the preparation of, but not materially affect, Sunlight’s consolidated financial statements.

As an “emerging growth company,” as defined in Section 2(a) of the Securities Act, as modified by the JOBS Act, Sunlight is eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies.” Section 107 of the JOBS Act provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. Unless otherwise stated, Sunlight elected to adopt recent accounting pronouncements using the extended transition period applicable to private companies.

ASU No. 2020-06 Debt — Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity — In August 2020, the FASB issued ASU No. 2020-06, which simplifies accounting for convertible instruments by removing major separation models required under current GAAP, removes certain settlement conditions that are required for equity contracts to qualify for the derivative scope exception, and simplifies the diluted earnings per share calculations. While Sunlight remains a smaller reporting company, this guidance is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2023, with early adoption permitted. Sunlight is currently evaluating the impact of the adoption of ASU 2020-06 on its consolidated financial statements.

ASU No. 2020-04 Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting — In March 2020, the FASB issued ASU No. 2020-04, which provides optional expedients for a limited period of time to ease the potential burden in accounting for, or recognizing the effects of, reference rate reform on financial reporting. ASU 2020-04 provides optional expedients and exceptions for applying GAAP to contracts, hedging relationships, and other transactions affected by reference rate reform if certain criteria are met. The standard is effective for all entities as of March 12, 2020 through December 31, 2024. An entity can elect to apply the amendments as of any date from the beginning of an interim period that includes or is subsequent to March 12, 2020, or prospectively from a date within an interim period that includes or is subsequent to March 12, 2020, up to that date that the financial statements are available to be issued. Sunlight is currently evaluating the impact of the adoption of ASU 2020-04, as updated by ASU 2021-01 Reference Rate Reform (Topic 848): Scope, and ASU 2022-06 Reference Rate Reform (Topic 848): Deferral of the Sunset Date of Topic 848 on its consolidated financial statements.

Recently Adopted Accounting Pronouncements

ASU No. 2016-13 Financial Instruments — Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments — The FASB issued ASU No. 2016-13 in June 2016. The standard amends the existing credit loss model to reflect a reporting entity’s current estimate of all expected credit losses and requires a financial asset (or a group of financial assets) measured at amortized cost basis to be presented at a net amount expected to be collected through deduction of an allowance for credit losses from the amortized cost basis of the financial asset(s).

Sunlight adopted ASU No. 2016-13, as amended, as of January 1, 2023. Sunlight’s cumulative adjustment of $0.5 million to the opening balance of retained earnings was not material and adoption of the standard did not have a material effect on the statements of operations or statements of cash flows. See Note 3 for additional information regarding Sunlight’s application of this accounting standard.

16

ASU No. 2022-02 Financial Instruments — Credit Losses (Topic 326) — Troubled Debt Restructuring and Vintage Disclosures — The FASB issued final guidance amending Topic 310 to eliminate the recognition and measurement guidance for a troubled debt restructuring for creditors that have adopted Topic 326 and requiring them to make enhanced disclosures about loan modifications for borrowers experiencing financial difficulty. The guidance also requires public business entities to present gross write-offs by year of origination in their vintage disclosures.