0000018230 cat:USEquitiesMember us-gaap:FairValueInputsLevel3Member us-gaap:ForeignPlanMember 2019-12-31 0000018230 us-gaap:OperatingSegmentsMember cat:MachineryEnergyTransportationMember cat:IntercompanyReceivablesMember 2019-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

| |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

|

| |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File No. 1-768

CATERPILLAR INC.

(Exact name of Registrant as specified in its charter)

|

| | | | |

| Delaware | | | 37-0602744 |

| (State or other jurisdiction of incorporation) | | (IRS Employer I.D. No.) |

| 510 Lake Cook Road, | Suite 100, | Deerfield, | Illinois | 60015 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (224) 551-4000

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | Trading Symbol (s) | Name of each exchange on which registered |

| Common Stock ($1.00 par value) | CAT | New York Stock Exchange (1) |

| 9 3/8% Debentures due March 15, 2021 | CAT21 | New York Stock Exchange |

| 8% Debentures due February 15, 2023 | CAT23 | New York Stock Exchange |

| 5.3% Debentures due September 15, 2035 | CAT35 | New York Stock Exchange |

| |

(1) | In addition to the New York Stock Exchange, Caterpillar common stock is also listed on stock exchanges in France and Switzerland. |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | |

| Large accelerated filer | x | Accelerated filer | o |

| | | | |

| Non-accelerated filer | o | Smaller reporting company | ☐ |

| | | | |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ý

As of June 28, 2019, there were 562,589,191 shares of common stock of the Registrant outstanding, and the aggregate market value of the voting stock held by non-affiliates of the Registrant (assuming only for purposes of this computation that directors and executive officers may be affiliates) was approximately $76.8 billion.

As of December 31, 2019, there were 550,082,610 shares of common stock of the Registrant outstanding.

Documents Incorporated by Reference

Portions of the documents listed below have been incorporated by reference into the indicated parts of this Form 10-K, as specified in the responses to the item numbers involved.

|

| |

| Part III | 2020 Annual Meeting Proxy Statement (Proxy Statement) to be filed with the Securities and Exchange Commission (SEC) within 120 days after the end of the fiscal year. |

PART I

General

Originally organized as Caterpillar Tractor Co. in 1925 in the State of California, our company was reorganized as Caterpillar Inc. in 1986 in the State of Delaware. As used herein, the term “Caterpillar,” “we,” “us,” “our” or “the company” refers to Caterpillar Inc. and its subsidiaries unless designated or identified otherwise.

Overview

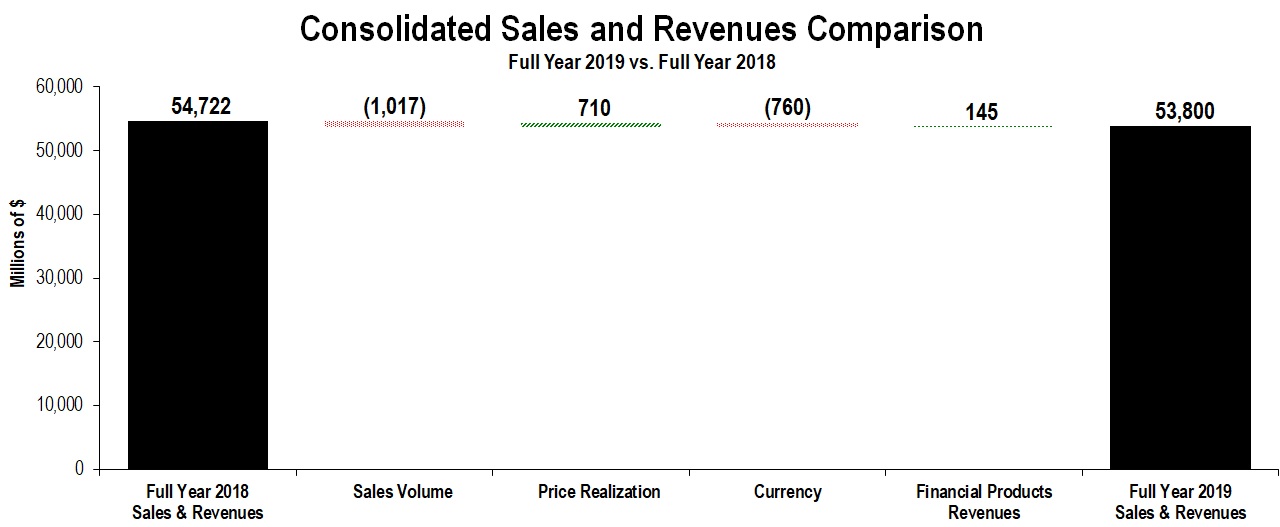

With 2019 sales and revenues of $53.800 billion, Caterpillar is the world’s leading manufacturer of construction and mining equipment, diesel and natural gas engines, industrial gas turbines and diesel-electric locomotives. The company principally operates through its three primary segments - Construction Industries, Resource Industries and Energy & Transportation - and also provides financing and related services through its Financial Products segment. Caterpillar is also a leading U.S. exporter. Through a global network of independent dealers and direct sales of certain products, Caterpillar builds long-term relationships with customers around the world.

Currently, we have five operating segments, of which four are reportable segments and are described below.

Categories of Business Organization

1. Machinery, Energy & Transportation — Represents the aggregate total of Construction Industries, Resource Industries, Energy & Transportation and All Other operating segment and related corporate items and eliminations.

2. Financial Products — Primarily includes the company’s Financial Products Segment. This category includes Caterpillar Financial Services Corporation (Cat Financial), Caterpillar Insurance Holdings Inc. (Insurance Services) and their respective subsidiaries.

Other information about our operations in 2019, including certain risks associated with our operations, is included in Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Construction Industries

Our Construction Industries segment is primarily responsible for supporting customers using machinery in infrastructure, forestry and building construction. The majority of machine sales in this segment are made in the heavy and general construction, rental, quarry and aggregates markets and mining.

The nature of customer demand for construction machinery varies around the world. Customers in developing economies often prioritize purchase price in making their investment decisions, while customers in developed economies generally weigh productivity and other performance criteria that contribute to lower owning and operating costs over the lifetime of the machine. To meet customer expectations in developing economies, Caterpillar developed differentiated product offerings that target customers in those markets, including our SEM brand machines. We believe that these customer-driven product innovations enable us to compete more effectively in developing economies. The majority of Construction Industries' research and development spending in 2019 focused on the next generation of construction machines.

The competitive environment for construction machinery is characterized by some global competitors and many regional and specialized local competitors. Examples of global competitors include CASE (part of CNH Industrial N.V.), Deere Construction & Forestry (part of Deere & Company), Doosan Infracore Co., Ltd., Hitachi Construction Machinery Co., Ltd., Hyundai Construction Equipment Co., Ltd., J.C. Bamford Excavators Ltd., Kobelco Construction Machinery (part of Kobe Steel, Ltd), Komatsu Ltd., Kubota Farm & Industrial Machinery (part of Kubota Corporation), and Volvo Construction Equipment (part of the Volvo Group). As an example of regional and local competitors, our competitors in China also include Guangxi LiuGong Machinery Co., Ltd., Longking Holdings Ltd., Sany Heavy Industry Co., Ltd., XCMG Group, Shandong Lingong Construction Machinery Co., Ltd. (SDLG, part of the Volvo Group) and Shantui Construction Machinery Co., Ltd., (part of Shandong Heavy Industry Group Co.). Each of these companies has varying product lines that compete with Caterpillar products, and each has varying degrees of regional focus.

The Construction Industries product portfolio includes the following machines and related parts and work tools:

|

| | | | |

· asphalt pavers | | · feller bunchers | | · telehandlers |

· backhoe loaders | | · harvesters | | · small and medium |

· compactors | | · knuckleboom loaders | | track-type tractors |

· cold planers | | · motorgraders | | · track-type loaders |

| · compact track and | | · pipelayers | | · wheel excavators |

multi-terrain loaders | | · road reclaimers | | · compact, small and |

· mini, small, medium | | · site prep tractors | | medium wheel loaders |

and large excavators | | · skidders | | · utility vehicles |

· forestry excavators | | · skid steer loaders | | |

Resource Industries

The Resource Industries segment is primarily responsible for supporting customers using machinery in mining, heavy construction, quarry and aggregates, waste and material handling applications. Caterpillar offers a broad product range and services to deliver comprehensive solutions for our mining customers. We manufacture high productivity equipment for both surface and underground mining operations around the world. Our equipment is used to extract and haul copper, iron ore, coal, oil sands, aggregates, gold and other minerals and ores. In addition to equipment, Resource Industries also develops and sells technology products and services to provide customers fleet management systems, equipment management analytics and autonomous machine capabilities.

Customers in most markets place an emphasis on equipment that is highly productive, reliable and provides the lowest total cost of ownership over the life of the equipment. In some developing markets, customers often prioritize purchase price in making their investment decisions. We believe our ability to control the integration and design of key machine components represents a competitive advantage. Our research and development efforts remain focused on providing customers the lowest total cost of ownership enabled through the highest quality, most productive products and services in the industry.

The competitive environment for Resource Industries consists of a few larger global competitors that compete in several of the markets that we serve and a substantial number of smaller companies that compete in a more limited range of products, applications, and regional markets. Our global surface competitors include Deere Construction & Forestry (part of Deere & Company), Epiroc AB, Hitachi Construction Machinery Co., Ltd., Komatsu Ltd., Liebherr-International AG, Sandvik AB, and Volvo Construction Equipment. Our global underground competitors include Epiroc AB, Komatsu Ltd., Sandvik AB and Zhengzhou Coal Mining Machinery Group Co., Ltd.

The Resource Industries product portfolio includes the following machines and related parts:

|

| | | | |

· electric rope shovels | | · longwall miners | | · soil compactors |

· draglines | | · large wheel loaders | | · machinery components |

· hydraulic shovels | | · off-highway trucks | | · autonomous ready vehicles and |

· rotary drills | | · articulated trucks | | solutions |

· hard rock vehicles | | · wheel tractor scrapers | | · select work tools |

· large track-type tractors | | · wheel dozers | | · hard rock continuous mining systems |

· large mining trucks | | · landfill compactors | | |

Energy & Transportation

Our Energy & Transportation segment supports customers in oil and gas, power generation, marine, rail and industrial applications, including Cat® machines. The product and services portfolio includes reciprocating engines, generator sets, marine propulsion systems, gas turbines and turbine-related services, the remanufacturing of Caterpillar engines and components and remanufacturing services for other companies, diesel-electric locomotives and other rail-related products and services and product support of on-highway vocational trucks for North America.

Regulatory emissions standards require us to continue to make investments as new products and new regulations are introduced. On-going compliance with these regulations remains a focus. Emissions compliance in developing markets is complex due to rapidly evolving and unique requirements where enforcement processes can often vary. We employ robust product development and manufacturing processes to help us comply with these regulations.

The competitive environment for reciprocating engines in marine, oil and gas, industrial and electric power generation systems along with turbines in oil and gas and electric power generation consists of a few larger global competitors that compete in a variety of markets that Caterpillar serves, and a substantial number of smaller companies that compete in a limited-size product range, geographic region and/or application. Principal global competitors include Cummins Inc., Deutz AG, INNIO, Rolls-Royce Power Systems and Wärtsilä Corp. Other competitors, such as Fiat Industrial SpA (CNHI), GE Power, Kawasaki Heavy Industries Energy System & Plant Engineering, MAN Energy Solutions (VW), Mitsubishi Heavy Industries Ltd., Siemens Power and Gas,Volvo Penta AB, Weichai Power Co., Ltd., and other emerging market competitors compete in certain markets in which Caterpillar competes. An additional set of competitors, including Aggreko plc, Baker Hughes Co., Generac Holdings, Kohler Power Systems, and others, are primarily packagers who source engines and/or other components from domestic and international suppliers and market products regionally and internationally through a variety of distribution channels. In rail-related businesses, our global competitors include Alstom SA, Bombardier Transportation, CRRC Corp., LTD., The Greenbrier Companies, Siemens Mobility, Voestalpine AG, Vossloh AG and Wabtec Freight. We also compete with other companies on a more limited range of products, services and/or geographic regions.

The Energy & Transportation portfolio includes the following products and related parts:

| |

| • | reciprocating engine powered generator sets |

| |

| • | reciprocating engines supplied to the industrial industry as well as Caterpillar machinery |

| |

| • | integrated systems used in the electric power generation industry |

| |

| • | turbines, centrifugal gas compressors and related services |

| |

| • | reciprocating engines and integrated systems and solutions for the marine and oil and gas industries |

| |

| • | remanufactured reciprocating engines and components |

| |

| • | diesel-electric locomotives and components and other rail-related products and services |

Financial Products Segment

The business of our Financial Products Segment is primarily conducted by Cat Financial, Insurance Services and their respective subsidiaries. Cat Financial is a wholly owned finance subsidiary of Caterpillar Inc. and its primary business is to provide retail and wholesale financing alternatives for Caterpillar products to customers and dealers around the world. Retail financing is primarily comprised of the financing of Caterpillar equipment, machinery and engines. Cat Financial also provides financing for vehicles, power generation facilities and marine vessels that, in most cases, incorporate Caterpillar products. In addition to retail financing, Cat Financial provides wholesale financing to Caterpillar dealers and purchases short-term trade receivables from Caterpillar. The various financing plans offered by Cat Financial are primarily designed to increase the opportunity for sales of Caterpillar products and generate financing income for Cat Financial. A significant portion of Cat Financial’s activity is conducted in North America, with additional offices and subsidiaries in Latin America, Asia/Pacific, Europe, Africa and the Middle East.

For over 35 years, Cat Financial has been providing financing in the various markets in which it participates, contributing to its knowledge of asset values, industry trends, product structuring and customer needs.

In certain instances, Cat Financial’s operations are subject to supervision and regulation by state, federal and various foreign governmental authorities, and may be subject to various laws and judicial and administrative decisions imposing various requirements and restrictions which, among other things, (i) regulate credit granting activities and the administration of loans, (ii) establish maximum interest rates, finance charges and other charges, (iii) require disclosures to customers and investors, (iv) govern secured transactions, (v) set collection, foreclosure, repossession and other trade practices and (vi) regulate the use and reporting of information related to a borrower’s credit experience. Cat Financial’s ability to comply with these and other governmental and legal requirements and restrictions affects its operations.

Cat Financial’s retail loans (totaling 49 percent*) include:

| |

| • | Loans that allow customers and dealers to use their Caterpillar equipment or other assets as collateral to obtain financing (24 percent*). |

| |

| • | Installment sale contracts, which are equipment loans that enable customers to purchase equipment with a down payment or trade-in and structure payments over time (25 percent*). |

Cat Financial's retail leases (totaling 35 percent*) include:

| |

| • | Finance (non-tax) leases, where the lessee for tax purposes is considered to be the owner of the equipment during the term of the lease, that either require or allow the customer to purchase the equipment for a fixed price at the end of the term (22 percent*). |

| |

| • | Tax leases that are classified as either operating or finance leases for financial accounting purposes, depending on the characteristics of the lease. For tax purposes, Cat Financial is considered the owner of the equipment (12 percent*). |

| |

| • | Governmental lease-purchase plans in the U.S. that offer low interest rates and flexible terms to qualified non-federal government agencies (1 percent*). |

Cat Financial also purchases short-term receivables from Caterpillar (14 percent*).

Cat Financial’s wholesale loans and leases (2 percent*) include inventory/rental programs, which provide assistance to dealers by financing their new Caterpillar inventory and rental fleets.

*Indicates the percentage of Cat Financial’s total portfolio at December 31, 2019. We define total portfolio as total finance receivables (net of unearned income and allowance for credit losses) plus equipment on operating leases, less accumulated depreciation. For more information on the above and Cat Financial’s concentration of credit risk, please refer to Note 7 — “Cat Financial Financing Activities” of Part II, Item 8 "Financial Statements and Supplementary Data."

_____________________________

Cat Financial operates in a highly competitive environment, with financing for users of Caterpillar equipment available through a variety of sources, principally commercial banks and finance and leasing companies. Cat Financial’s competitors include, Australia and New Zealand Banking Group Limited, Banc of America Leasing & Capital LLC, BNP Paribas Leasing Solutions Limited, Wells Fargo Equipment Finance Inc. and various other banks and finance companies. In addition, many of our manufacturing competitors own financial subsidiaries, such as John Deere Capital Corporation, Komatsu Financial L.P., Kubota Credit Corporation and Volvo Financial Services, which utilize below-market interest rate programs (funded by the manufacturer) to assist machine sales. Caterpillar and Cat Financial work together to provide a broad array of financial merchandising programs around the world to meet these competitive offers.

Cat Financial’s financial results are largely dependent upon the ability of Caterpillar dealers to sell equipment and customers’ willingness to enter into financing or leasing agreements. Cat Financial is also affected by, among other things, the availability of funds from its financing sources, its cost of funds relative to its competitors and general economic conditions such as inflation and market interest rates.

Cat Financial has a match-funding policy that addresses interest rate risk by aligning the interest rate profile (fixed or floating rate) of its debt portfolio with the interest rate profile of its receivables portfolio within predetermined ranges on an ongoing basis. In connection with that policy, Cat Financial uses interest rate derivative instruments to modify the debt structure to match assets within the receivables portfolio. This matched funding reduces the volatility of margins between interest-bearing assets and interest-bearing liabilities, regardless of which direction interest rates move. For more information regarding match funding, please see Note 4 — “Derivative financial instruments and risk management” of Part II, Item 8 "Financial Statements and Supplementary Data." See also the risk factors associated with our financial products business included in Item 1 A. of this Form 10-K.

In managing foreign currency risk for Cat Financial’s operations, the objective is to minimize earnings volatility resulting from conversion and the remeasurement of net foreign currency balance sheet positions, and future transactions denominated in foreign currencies. This policy allows the use of foreign currency forward, option and cross currency contracts to offset the risk of currency mismatch between the assets and liabilities, and exchange rate risk associated with future transactions denominated in foreign currencies.

Cat Financial provides financing only when certain criteria are met. Credit decisions are based on a variety of credit quality factors including prior payment experience, customer financial information, credit-rating agency ratings, loan-to-value ratios and other internal metrics. Cat Financial typically maintains a security interest in retail-financed equipment and requires physical damage insurance coverage on financed equipment. Cat Financial finances a significant portion of Caterpillar dealers’ sales and inventory of Caterpillar equipment throughout the world. Cat Financial’s competitive position is improved by marketing programs offered in conjunction with Caterpillar and/or Caterpillar dealers. Under these programs, Caterpillar, or the dealer, funds an amount at the outset of the transaction, which Cat Financial then recognizes as revenue over the term of the financing. We believe that these marketing programs provide Cat Financial a significant competitive advantage in financing Caterpillar products.

Caterpillar Insurance Company, a wholly owned subsidiary of Caterpillar Insurance Holdings Inc., is a U.S. insurance company domiciled in Missouri and primarily regulated by the Missouri Department of Insurance. Caterpillar Insurance Company is licensed to conduct property and casualty insurance business in 50 states, the District of Columbia and Guam, and as such, is also regulated in those jurisdictions. The State of Missouri acts as the lead regulatory authority and monitors Caterpillar Insurance Company’s financial status to ensure that it is in compliance with minimum solvency requirements, as well as other financial ratios prescribed by the National Association of Insurance Commissioners. Caterpillar Insurance Company is also licensed to conduct insurance business through a branch in Zurich, Switzerland and, as such, is regulated by the Swiss Financial Market Supervisory Authority.

Caterpillar Life Insurance Company, a wholly owned subsidiary of Caterpillar, is a U.S. insurance company domiciled in Missouri and primarily regulated by the Missouri Department of Insurance. Caterpillar Life Insurance Company is licensed to conduct life and accident and health insurance business in 26 states and the District of Columbia and, as such, is also regulated in those jurisdictions. The State of Missouri acts as the lead regulatory authority and it monitors the financial status to ensure that it is in compliance with minimum solvency requirements, as well as other financial ratios prescribed by the National Association of Insurance Commissioners. Caterpillar Life Insurance Company provides stop loss insurance protection to a Missouri Voluntary Employees’ Beneficiary Association (VEBA) trust used to fund medical claims of salaried retirees of Caterpillar under the VEBA.

Caterpillar Insurance Co. Ltd., a wholly owned subsidiary of Caterpillar Insurance Holdings Inc., is a captive insurance company domiciled in Bermuda and regulated by the Bermuda Monetary Authority. Caterpillar Insurance Co. Ltd. is a Class 2 insurer (as defined by the Bermuda Insurance Amendment Act of 1995), which primarily insures its parent and affiliates. The Bermuda Monetary Authority requires an Annual Financial Filing for purposes of monitoring compliance with solvency requirements.

Caterpillar Product Services Corporation (CPSC), a wholly owned subsidiary of Caterpillar, is a warranty company domiciled in Missouri. CPSC previously conducted a machine extended service contract program in Germany and France by providing machine extended warranty reimbursement protection to dealers in Germany and France. The program was discontinued effective January 1, 2013, though CPSC continues to provide extended warranty reimbursement protection under existing contracts.

Caterpillar Insurance Services Corporation, a wholly owned subsidiary of Caterpillar Insurance Holdings Inc., is a Tennessee insurance brokerage company licensed in all 50 states, the District of Columbia and Guam. It provides brokerage services for all property and casualty and life and health lines of business.

Caterpillar’s insurance group provides protection for claims under the following programs:

| |

| • | Contractual Liability Insurance to Caterpillar and its affiliates, Caterpillar dealers and original equipment manufacturers (OEMs) for extended service contracts (parts and labor) offered by Caterpillar, third party dealers and OEMs. |

| |

| • | Cargo insurance for the worldwide cargo risks of Caterpillar products. |

| |

| • | Contractors’ Equipment Physical Damage Insurance for equipment manufactured by Caterpillar or OEMs, which is leased, rented or sold by third party dealers to customers. |

| |

| • | General liability, employer’s liability, auto liability and property insurance for Caterpillar. |

| |

| • | Retiree Medical Stop Loss Insurance for medical claims under the VEBA. |

| |

| • | Brokerage services for property and casualty and life and health business. |

Acquisitions

Information related to acquisitions appears in Note 24 — “Acquisitions” of Part II, Item 8 "Financial Statements and Supplementary Data."

Competitive Environment

Caterpillar products and product support services are sold worldwide into a variety of highly competitive markets. In all markets, we compete on the basis of product performance, customer service, quality and price. From time to time, the intensity of competition results in price discounting in a particular industry or region. Such price discounting puts pressure on margins and can negatively impact operating profit. Outside the United States, certain competitors enjoy competitive advantages inherent to operating in their home countries or regions.

Raw Materials and Component Products

We source our raw materials and manufactured components from suppliers both domestically and internationally. These purchases include unformed materials and rough and finished parts. Unformed materials include a variety of steel products, which are then cut or formed to shape and machined in our facilities. Rough parts include various sized steel and iron castings and forgings, which are machined to final specification levels inside our facilities. Finished parts are ready to assemble components, which are made either to Caterpillar specifications or to supplier developed specifications. We machine and assemble some of the components used in our machines, engines and power generation units and to support our after-market dealer parts sales. We also purchase various goods and services used in production, logistics, offices and product development processes. We maintain global strategic sourcing models to meet our global facilities’ production needs while building long-term supplier relationships and leveraging enterprise spend. We expect our suppliers to maintain, at all times, industry-leading levels of quality and the ability to timely deliver raw materials and component products for our machine and engine products. However, increases in demand have led to parts and components constraints across some products. We use a variety of agreements with suppliers to protect our intellectual property and processes to monitor and mitigate risks of the supply base causing a business disruption. The risks monitored include supplier financial viability, the ability to increase or decrease production levels, business continuity, quality and delivery.

Patents and Trademarks

We own a number of patents and trademarks, which have been obtained over a period of years and relate to the products we manufacture and the services we provide. These patents and trademarks are generally considered beneficial to our business. We do not regard our business as being dependent upon any single patent or group of patents.

Order Backlog

The dollar amount of backlog believed to be firm was approximately $13.7 billion at December 31, 2019 and $16.5 billion at December 31, 2018. Compared with year-end 2018, the order backlog decreased across the three primary segments. Of the total backlog at December 31, 2019, approximately $3.8 billion was not expected to be filled in 2020.

Dealers and Distributors

Our machines are distributed principally through a worldwide organization of dealers (dealer network), 46 located in the United States and 119 located outside the United States, serving 191 countries. Reciprocating engines are sold principally through the dealer network and to other manufacturers for use in products. Some of the reciprocating engines manufactured by our subsidiary Perkins Engines Company Limited are also sold through its worldwide network of 67 distributors covering 178 countries. The FG Wilson branded electric power generation systems primarily manufactured by our subsidiary Caterpillar Northern Ireland Limited are sold through its worldwide network of 150 distributors covering 109 countries. Some of the large, medium speed reciprocating engines are also sold under the MaK brand through a worldwide network of 20 distributors covering 130 countries.

Our dealers do not deal exclusively with our products; however, in most cases sales and servicing of our products are the dealers’ principal business. Some products, primarily turbines and locomotives, are sold directly to end customers through sales forces employed by the company. At times, these employees are assisted by independent sales representatives.

While the large majority of our worldwide dealers are independently owned and operated, we own and operate a dealership in Japan that covers approximately 80% of the Japanese market: Nippon Caterpillar Division. We are currently operating this Japanese dealer directly and its results are reported in the All Other operating segment. There are also three independent dealers in the Southern Region of Japan.

For Caterpillar branded products, the company’s relationship with each of its independent dealers is memorialized in standard sales and service agreements. Pursuant to these agreements, the company grants the dealer the right to purchase and sell its products and to service the products in a specified geographic service territory. Prices to dealers are established by the company after receiving input from dealers on transactional pricing in the marketplace. The company also agrees to defend its intellectual property and to provide warranty and technical support to the dealer. The agreement further grants the dealer a non-exclusive license to use the company’s trademarks, service marks and brand names. In some instances, a separate trademark agreement exists between the company and a dealer.

In exchange for these rights, the agreement obligates the dealer to develop and promote the sale of the company’s products to current and prospective customers in the dealer’s service territory. Each dealer agrees to employ adequate sales and support personnel to market, sell and promote the company’s products, demonstrate and exhibit the products, perform the company’s product improvement programs, inform the company concerning any features that might affect the safe operation of any of the company’s products and maintain detailed books and records of the dealer’s financial condition, sales and inventories and make these books and records available at the company’s reasonable request.

These sales and service agreements are terminable at will by either party primarily upon 90 days written notice.

Employment

As of December 31, 2019, we employed about 102,300 full-time persons of whom approximately 58,700 were located outside the United States. In the United States, we employed approximately 43,600 employees, most of whom are at-will employees and, therefore, not subject to any type of employment contract or agreement. At select business units, certain highly specialized employees have been hired under employment contracts that specify a term of employment, pay and other benefits.

|

| | | | | | |

| Full-Time Employees at Year-End | | | | |

| | 2019 | | 2018 | |

| Inside U.S. | 43,600 |

| | 44,600 |

| |

| Outside U.S. | 58,700 |

| | 59,400 |

| |

| Total | 102,300 |

| | 104,000 |

| |

| | | | | |

| By Region: | |

| | |

| |

| North America | 43,900 |

| | 44,900 |

| |

| EAME | 18,400 |

| | 18,000 |

| |

| Latin America | 16,400 |

| | 17,300 |

| |

| Asia/Pacific | 23,600 |

| | 23,800 |

| |

| Total | 102,300 |

| | 104,000 |

| |

| | | | | |

As of December 31, 2019, there were approximately 8,290 U.S. hourly production employees who were covered by collective bargaining agreements with various labor unions, including The United Automobile, Aerospace and Agricultural Implement Workers of America (UAW), The International Association of Machinists and The United Steelworkers. Approximately 6,880 of such employees are covered by collective bargaining agreements with the UAW that expire on December 17, 2020 and March 1, 2023. Outside the United States, the company enters into employment contracts and agreements in those countries in which such relationships are mandatory or customary. The provisions of these agreements generally correspond in each case with the required or customary terms in the subject jurisdiction.

Environmental Matters

The company is regulated by federal, state and international environmental laws governing our use, transport and disposal of substances and control of emissions. In addition to governing our manufacturing and other operations, these laws often impact the development of our products, including, but not limited to, required compliance with air emissions standards applicable to internal combustion engines. We have made, and will continue to make, significant research and development and capital expenditures to comply with these emissions standards.

We are engaged in remedial activities at a number of locations, often with other companies, pursuant to federal and state laws. When it is probable we will pay remedial costs at a site, and those costs can be reasonably estimated, the investigation, remediation, and operating and maintenance costs of the remedial action are accrued against our earnings. Costs are accrued based on consideration of currently available data and information with respect to each individual site, including available technologies, current applicable laws and regulations, and prior remediation experience. Where no amount within a range of estimates is more likely, we accrue the minimum. Where multiple potentially responsible parties are involved, we consider our proportionate share of the probable costs. In formulating the estimate of probable costs, we do not consider amounts expected to be recovered from insurance companies or others. We reassess these accrued amounts on a quarterly basis. The amount recorded for environmental remediation is not material and is included in the line item "Accrued expenses" in Statement 3 — "Consolidated Financial Position at December 31" of Part II, Item 8 "Financial Statements and Supplementary Data." There is no more than a remote chance that a material amount for remedial activities at any individual site, or at all the sites in the aggregate, will be required.

Available Information

The company files electronically with the Securities and Exchange Commission (SEC) required reports on Form 8-K, Form 10-Q, Form 10-K and Form 11-K; proxy materials; ownership reports for insiders as required by Section 16 of the Securities Exchange Act of 1934 (Exchange Act); registration statements on Forms S-3 and S-8, as necessary; and other forms or reports as required. The SEC maintains a website (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The company maintains a website (www.Caterpillar.com) and copies of our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to these reports filed or furnished with the SEC are available free of charge through our website (www.Caterpillar.com/secfilings) as soon as reasonably practicable after filing with the SEC. Copies of our board committee charters, our board’s Guidelines on Corporate Governance Issues, Worldwide Code of Conduct and other corporate governance information are available on our website (www.Caterpillar.com/governance). The information contained on the company’s website is not included in, or incorporated by reference into, this annual report on Form 10-K.

Additional company information may be obtained as follows:

Current information -

| |

| • | view additional financial information on-line at www.Caterpillar.com/en/investors/financial-information.html |

| |

| • | request, view or download materials on-line or register for email alerts at www.Caterpillar.com/materialsrequest |

Historical information -

| |

| • | view/download on-line at www.Caterpillar.com/historical |

The statements in this section describe the most significant risks to our business and should be considered carefully in conjunction with Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the “Notes to Consolidated Financial Statements” of Part II, Item 8 “Financial Statements and Supplementary Data” to this Form 10-K. In addition, the statements in this section and other sections of this Form 10-K, including in Part II, Item 7 “Management's Discussion and Analysis of Financial Condition and Results of Operations,” include “forward-looking statements” as that term is defined in the Private Securities Litigation Reform Act of 1995 and involve uncertainties that could significantly impact results. Forward-looking statements give current expectations or forecasts of future events about the company or our outlook. You can identify forward-looking statements by the fact they do not relate to historical or current facts and by the use of words such as “believe,” “expect,” “estimate,” “anticipate,” “will be,” “should,” “plan,” “forecast,” “target,” “guide,” “project,” “intend,” “could” and similar words or expressions.

Forward-looking statements are based on assumptions and on known risks and uncertainties. Although we believe we have been prudent in our assumptions, any or all of our forward-looking statements may prove to be inaccurate, and we can make no guarantees about our future performance. Should known or unknown risks or uncertainties materialize or underlying assumptions prove inaccurate, actual results could materially differ from past results and/or those anticipated, estimated or projected.

We undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future events or otherwise. You should, however, consult any subsequent disclosures we make in our filings with the SEC on Form 10-Q or Form 8-K.

The following is a cautionary discussion of risks, uncertainties and assumptions that we believe are significant to our business. In addition to the factors discussed elsewhere in this report, the following are some of the important factors that, individually or in the aggregate, we believe could make our actual results differ materially from those described in any forward-looking statements. It is impossible to predict or identify all such factors and, as a result, you should not consider the following factors to be a complete discussion of risks, uncertainties and assumptions.

MACROECONOMIC RISKS

Our business and the industries we serve are highly sensitive to global and regional economic conditions.

Our results of operations are materially affected by economic conditions globally and regionally and in the particular industries we serve. The demand for our products and services tends to be cyclical and can be significantly reduced in periods of economic weakness characterized by lower levels of government and business investment, lower levels of business confidence, lower corporate earnings, high real interest rates, lower credit activity or tighter credit conditions, perceived or actual industry overcapacity, higher unemployment and lower consumer spending. A prolonged period of economic weakness may also result in increased expenses due to higher allowances for doubtful accounts and potential goodwill and asset impairment charges. Economic conditions vary across regions and countries, and demand for our products and services generally increases in those regions and countries experiencing economic growth and investment. Slower economic growth or a change in the global mix of regions and countries experiencing economic growth and investment could have an adverse effect on our business, results of operations and financial condition.

The energy, transportation and mining industries are major users of our products, including the coal, iron ore, gold, copper, oil and natural gas industries. Customers in these industries frequently base their decisions to purchase our products and services on the expected future performance of these industries, which in turn are dependent in part on commodity prices. Prices of commodities in these industries are frequently volatile and can change abruptly and unpredictably in response to general economic conditions and trends, government actions, regulatory actions, commodity inventories, production and consumption levels, technological innovations, commodity substitutions, market expectations and any disruptions in production or distribution or changes in consumption. Economic conditions affecting the industries we serve may in the future also lead to reduced capital expenditures by our customers. Reduced capital expenditures by our customers are likely to lead to a decrease in the demand for our products and services and may also result in a decrease in demand for aftermarket parts as customers are likely to extend preventative maintenance schedules and delay major overhauls when possible.

The rates of infrastructure spending, commercial construction and housing starts also play a significant role in our results. Our products are an integral component of these activities, and as these activities decrease, demand for our products may be significantly impacted, which could negatively impact our results.

Commodity price changes, material price increases, fluctuations in demand for our products, significant disruptions to our supply chains or significant shortages of material may adversely impact our financial results or our ability to meet commitments to customers.

We are a significant user of steel and many other commodities required for the manufacture of our products. Increases in the prices of such commodities would increase our costs, negatively impacting our business, results of operations and financial condition if we are unable to fully offset the effect of these increased costs through price increases, productivity improvements or cost reduction programs.

We rely on suppliers to produce or secure material required for the manufacture of our products. Production challenges at suppliers, a disruption in deliveries to or from suppliers or decreased availability of raw materials or commodities could have an adverse effect on our ability to meet our commitments to customers or increase our operating costs. On the other hand, in circumstances where demand for our products is less than we expect, we may experience excess inventories and be forced to incur additional costs and our profitability may suffer. Our business, competitive position, results of operations or financial condition could be negatively impacted if supply is insufficient for our operations, if we experience excess inventories or if we are unable to adjust our production schedules or our purchases from suppliers to reflect changes in customer demand and market fluctuations on a timely basis.

Changes in government monetary or fiscal policies may negatively impact our results.

Most countries where our products and services are sold have established central banks to regulate monetary systems and influence economic activities, generally by adjusting interest rates. Interest rate changes affect overall economic growth, which affects demand for residential and nonresidential structures, as well as energy and mined products, which in turn affects sales of our products and services that support these activities. Interest rate changes may also affect our customers’ ability to finance machine purchases, can change the optimal time to keep machines in a fleet and can impact the ability of our suppliers to finance the production of parts and components necessary to manufacture and support our products. Increases in interest rates could negatively impact sales and create supply chain inefficiencies.

Central banks and other policy arms of many countries may take actions to vary the amount of liquidity and credit available in an economy. The impact from a change in liquidity and credit policies could negatively affect the customers and markets we serve or our suppliers, create supply chain inefficiencies and could adversely impact our business, results of operations and financial condition.

Changes in monetary and fiscal policies, along with other factors, may cause currency exchange rates to fluctuate. Actions that lead the currency exchange rate of a country where we manufacture products to increase relative to other currencies could reduce the competitiveness of products made in that country, which could adversely affect our competitive position, results of operations and financial condition.

Government policies on taxes and spending also affect our business. Throughout the world, government spending finances a significant portion of infrastructure development, such as highways, rail systems, airports, sewer and water systems, waterways and dams. Tax regulations determine asset depreciation lives and impact the after-tax returns on business activity and investment, both of which influence investment decisions. Unfavorable developments, such as decisions to reduce public spending or to increase taxes, could negatively impact our results.

Our global operations are exposed to political and economic risks, commercial instability and events beyond our control in the countries in which we operate.

Our global operations are dependent upon products manufactured, purchased and sold in the U.S. and internationally, including in countries with political and economic instability or uncertainty. This includes, for example, the uncertainty related to the United Kingdom’s withdrawal from the European Union (commonly known as “Brexit”). Some countries have greater political and economic volatility and greater vulnerability to infrastructure and labor disruptions than others. Our business could be negatively impacted by adverse fluctuations in freight costs, limitations on shipping and receiving capacity, and other disruptions in the transportation and shipping infrastructure at important geographic points of exit and entry for our products. Operating in different regions and countries exposes us to a number of risks, including:

| |

| • | multiple and potentially conflicting laws, regulations and policies that are subject to change; |

| |

| • | imposition of currency restrictions, restrictions on repatriation of earnings or other restraints; |

| |

| • | imposition of new or additional tariffs or quotas; |

| |

| • | withdrawal from or modification of trade agreements or the negotiation of new trade agreements; |

| |

| • | imposition of new or additional trade and economic sanctions laws imposed by the U.S. or foreign governments; |

| |

| • | war or acts of terrorism; and |

| |

| • | political and economic instability or civil unrest that may severely disrupt economic activity in affected countries. |

The occurrence of one or more of these events may negatively impact our business, results of operations and financial condition.

OPERATIONAL RISKS

The success of our business depends on our ability to develop, produce and market quality products that meet our customers’ needs.

Our business relies on continued global demand for our brands and products. To achieve business goals, we must develop and sell products that appeal to our dealers, OEMs and end-user customers. This is dependent on a number of factors, including our ability to maintain key dealer relationships, our ability to produce products that meet the quality, performance and price expectations of our customers and our ability to develop effective sales, advertising and marketing programs. In addition, our continued success in selling products that appeal to our customers is dependent on leading-edge innovation, with respect to both products and operations, and on the availability and effectiveness of legal protection for our innovations. Failure to continue to deliver high quality, innovative, competitive products to the marketplace, to adequately protect our intellectual property rights, to supply products that meet applicable regulatory requirements, including engine exhaust emission requirements or to predict market demands for, or gain market acceptance of, our products, could have a negative impact on our business, results of operations and financial condition.

We operate in a highly competitive environment, which could adversely affect our sales and pricing.

We operate in a highly competitive environment. We compete on the basis of a variety of factors, including product performance, customer service, quality and price. There can be no assurance that our products will be able to compete successfully with other companies’ products. Thus, our share of industry sales could be reduced due to aggressive pricing or product strategies pursued by competitors, unanticipated product or manufacturing difficulties, our failure to price our products competitively, our failure to produce our products at a competitive cost or an unexpected buildup in competitors’ new machine or dealer-owned rental fleets, which could lead to downward pressure on machine rental rates and/or used equipment prices.

Lack of customer acceptance of price increases we announce from time to time, changes in customer requirements for price discounts, changes in our customers’ behavior or a weak pricing environment could have an adverse impact on our business, results of operations and financial condition.

In addition, our results and ability to compete may be impacted negatively by changes in our geographic and product mix of sales.

Increased information technology security threats and more sophisticated computer crime pose a risk to our systems, networks, products and services.

We rely upon information technology systems and networks, some of which are managed by third parties, in connection with a variety of business activities. Additionally, we collect and store sensitive information relating to our business, customers, dealers, suppliers and employees. Operating these information technology systems and networks and processing and maintaining this data in a secure manner, is critical to our business operations and strategy. Information technology security threats -- from user error to cybersecurity attacks designed to gain unauthorized access to our systems, networks and data -- are increasing in frequency and sophistication. Cybersecurity attacks may range from random attempts to coordinated and targeted attacks, including sophisticated computer crime and advanced persistent threats. These threats pose a risk to the security of our systems and networks and the confidentiality, availability and integrity of our data. Cybersecurity attacks could also include attacks targeting customer data or the security, integrity and/or reliability of the hardware and software installed in our products. It is possible that our information technology systems and networks, or those managed by third parties, could have vulnerabilities, which could go unnoticed for a period of time. While various procedures and controls have been and are being utilized to mitigate such risks, there can be no guarantee that the actions and controls we have implemented and are implementing, or which we cause or have caused third party service providers to implement, will be sufficient to protect our systems, information or other property.

We have experienced cyber security threats and vulnerabilities in our systems and those of our third party providers, and we have experienced viruses and attacks targeting our information technology systems and networks. Such prior events, to date, have not had a material impact on our financial condition, results of operations or liquidity. However, the potential consequences of a future material cybersecurity attack include reputational damage, litigation with third parties, government enforcement actions, penalties, disruption to systems, unauthorized release of confidential or otherwise protected information, corruption of data, diminution in the value of our investment in research, development and engineering, and increased cybersecurity protection and remediation costs, which in turn could adversely affect our competitiveness, results of operations and financial condition. Due to the evolving nature of such security threats, the potential impact of any future incident cannot be predicted. Further, the amount of insurance coverage we maintain may be inadequate to cover claims or liabilities relating to a cybersecurity attack.

In addition, data we collect, store and process is subject to a variety of U.S. and international laws and regulations, such as the European Union's General Data Protection Regulation that became effective in May 2018, which may carry significant potential penalties for noncompliance.

Our business is subject to the inventory management decisions and sourcing practices of our dealers and our OEM customers.

We sell finished products primarily through an independent dealer network and directly to OEMs and are subject to risks relating to their inventory management decisions and operational and sourcing practices. Both carry inventories of finished products as part of ongoing operations and adjust those inventories based on their assessments of future needs and market conditions, including levels of used equipment inventory and machine rental usage rates. Such adjustments may impact our results positively or negatively. If the inventory levels of our dealers and OEM customers are higher than they desire, they may postpone product purchases from us, which could cause our sales to be lower than the end-user demand for our products and negatively impact our results. Similarly, our results could be negatively impacted through the loss of time-sensitive sales if our dealers and OEM customers do not maintain inventory levels sufficient to meet customer demand.

We may not realize all of the anticipated benefits of our acquisitions, joint ventures or divestitures, or these benefits may take longer to realize than expected.

In pursuing our business strategy, we routinely evaluate targets and enter into agreements regarding possible acquisitions, divestitures and joint ventures. We often compete with others for the same opportunities. To be successful, we conduct due diligence to identify valuation issues and potential loss contingencies, negotiate transaction terms, complete complex transactions and manage post-closing matters such as the integration of acquired businesses. Further, while we seek to mitigate risks and liabilities of such transactions through due diligence, among other things, there may be risks and liabilities that our due diligence efforts fail to discover, that are not accurately or completely disclosed to us or that we inadequately assess. We may incur unanticipated costs or expenses following a completed acquisition, including post-closing asset impairment charges, expenses associated with eliminating duplicate facilities, litigation, and other liabilities. Risks associated with our past or future acquisitions also include the following:

| |

| • | the failure to achieve the acquisition's revenue or profit forecast; |

| |

| • | the business culture of the acquired business may not match well with our culture; |

| |

| • | technological and product synergies, economies of scale and cost reductions may not occur as expected; |

| |

| • | unforeseen expenses, delays or conditions may be imposed upon the acquisition, including due to required regulatory approvals or consents; |

| |

| • | we may acquire or assume unexpected liabilities or be subject to unexpected penalties or other enforcement actions; |

| |

| • | faulty assumptions may be made regarding the macroeconomic environment or the integration process; |

| |

| • | unforeseen difficulties may arise in integrating operations, processes and systems; |

| |

| • | higher than expected investments may be required to implement necessary compliance processes and related systems, including information technology systems, accounting systems and internal controls over financial reporting; |

| |

| • | we may fail to retain, motivate and integrate key management and other employees of the acquired business; |

| |

| • | higher than expected costs may arise due to unforeseen changes in tax, trade, environmental, labor, safety, payroll or pension policies in any jurisdiction in which the acquired business conducts its operations; and |

| |

| • | we may experience problems in retaining customers and integrating customer bases. |

Many of these factors will be outside of our control and any one of them could result in increased costs, decreases in the amount of expected revenues and diversion of management’s time and attention. They may also delay the realization of the benefits we anticipate when we enter into a transaction.

In order to conserve cash for operations, we may undertake acquisitions financed in part through public offerings or private placements of debt or equity securities, or other arrangements. Such acquisition financing could result in a decrease in our earnings and adversely affect other leverage measures. If we issue equity securities or equity-linked securities, the issued securities may have a dilutive effect on the interests of the holders of our common shares.

Failure to implement our acquisition strategy, including successfully integrating acquired businesses, could have an adverse effect on our business, financial condition and results of operations. Furthermore, we make strategic divestitures from time to time. In the case of divestitures, we may agree to indemnify acquiring parties for certain liabilities arising from our former businesses. These divestitures may also result in continued financial involvement in the divested businesses following the transaction, including through guarantees or other financial arrangements. Lower performance by those divested businesses could affect our future financial results.

Union disputes or other labor matters could adversely affect our operations and financial results.

Some of our employees are represented by labor unions in a number of countries under various collective bargaining agreements with varying durations and expiration dates. There can be no assurance that any current or future issues with our employees will be resolved or that we will not encounter future strikes, work stoppages or other disputes with labor unions or our employees. We may not be able to satisfactorily renegotiate collective bargaining agreements in the United States and other countries when they expire. If we fail to renegotiate our existing collective bargaining agreements, we could encounter strikes or work stoppages or other disputes with labor unions. In addition, existing collective bargaining agreements may not prevent a strike or work stoppage at our facilities in the future. We may also be subject to general country strikes or work stoppages unrelated to our business or collective bargaining agreements. A work stoppage or other limitations on production at our facilities for any reason could have an adverse effect on our business, results of operations and financial condition. In addition, many of our customers and suppliers have unionized work forces. Strikes or work stoppages experienced by our customers or suppliers could have an adverse effect on our business, results of operations and financial condition.

Unexpected events may increase our cost of doing business or disrupt our operations.

The occurrence of one or more unexpected events, including war, acts of terrorism or violence, civil unrest, fires, tornadoes, tsunamis, hurricanes, earthquakes, floods and other forms of severe weather in the United States or in other countries in which we operate or in which our suppliers are located could adversely affect our operations and financial performance. Natural disasters, pandemic illness, including the current COVID-19 outbreak, equipment failures, power outages or other unexpected events could result in physical damage to and complete or partial closure of one or more of our manufacturing facilities or distribution centers, temporary or long-term disruption in the supply of component products from some local and international suppliers, and disruption and delay in the transport of our products to dealers, end-users and distribution centers. Existing insurance coverage may not provide protection for all of the costs that may arise from such events.

FINANCIAL RISKS

Disruptions or volatility in global financial markets could limit our sources of liquidity, or the liquidity of our customers, dealers and suppliers.

Continuing to meet our cash requirements over the long-term requires substantial liquidity and access to varied sources of funds, including capital and credit markets. Global economic conditions may cause volatility and disruptions in the capital and credit markets. Market volatility, changes in counterparty credit risk, the impact of government intervention in financial markets and general economic conditions may also adversely impact our ability to access capital and credit markets to fund operating needs. Global or regional economic downturns could cause financial markets to decrease the availability of liquidity, credit and credit capacity for certain issuers, including certain customers, dealers and suppliers. An inability to access capital and credit markets may have an adverse effect on our business, results of operations, financial condition and competitive position. Furthermore, changes in global economic conditions, including material cost increases and decreases in economic activity in key markets we serve, and the success of plans to manage cost increases, inventory and other important elements of our business may significantly impact our ability to generate funds from operations.

In addition, demand for our products generally depends on customers’ ability to pay for our products, which, in turn, depends on their access to funds. Changes in global economic conditions may result in customers experiencing increased difficulty in generating funds from operations. Capital and credit market volatility and uncertainty may cause financial institutions to revise their lending standards, resulting in customers’ decreased access to capital. If capital and credit market volatility occurs, customers’ liquidity may decline which, in turn, would reduce their ability to purchase our products.

Failure to maintain our credit ratings would increase our cost of borrowing and could adversely affect our cost of funds, liquidity, competitive position and access to capital markets.

Each of Caterpillar’s and Cat Financial’s costs of borrowing and their respective ability to access the capital markets are affected not only by market conditions but also by the short- and long-term credit ratings assigned to their respective debt by the major credit rating agencies. These ratings are based, in significant part, on each of Caterpillar’s and Cat Financial’s performance as measured by financial metrics such as net worth, interest coverage and leverage ratios, as well as transparency with rating agencies and timeliness of financial reporting. There can be no assurance that Caterpillar and Cat Financial will be able to maintain their credit ratings. We receive debt ratings from the major credit rating agencies. Moody’s

long- and short-term ratings of Caterpillar and Cat Financial are A3 and Prime-2 (“low-A”), while other major credit rating agencies maintain a “mid-A” debt rating. A downgrade of our credit rating by any of the major credit rating agencies would result in increased borrowing costs and could adversely affect Caterpillar’s and Cat Financial’s liquidity, competitive position and access to the capital markets, including restricting, in whole or in part, access to the commercial paper market. There can be no assurance that the commercial paper market will continue to be a reliable source of short-term financing for Cat Financial or an available source of short-term financing for Caterpillar. An inability to access the capital markets could have an adverse effect on our cash flow, results of operations and financial condition.

Our Financial Products segment is subject to risks associated with the financial services industry.

Cat Financial is significant to our operations and provides financing support for a significant share of our global sales. The inability of Cat Financial to access funds to support its financing activities to our customers could have an adverse effect on our business, results of operations and financial condition.

Continuing to meet Cat Financial's cash requirements over the long-term could require substantial liquidity and access to sources of funds, including capital and credit markets. Cat Financial has continued to maintain access to key global medium term note and commercial paper markets, but there can be no assurance that such markets will continue to represent a reliable source of financing. If global economic conditions were to deteriorate, Cat Financial could face materially higher financing costs, become unable to access adequate funding to operate and grow its business and/or meet its debt service obligations as they mature, and be required to draw upon contractually committed lending agreements and/or seek other funding sources. However, there can be no assurance that such agreements and other funding sources would be available or sufficient under extreme market conditions. Any of these events could negatively impact Cat Financial’s business, as well as our and Cat Financial's results of operations and financial condition.

Market disruption and volatility may also lead to a number of other risks in connection with these events, including but not limited to:

| |

| • | Market developments that may affect customer confidence levels and cause declines in the demand for financing and adverse changes in payment patterns, causing increases in delinquencies and default rates, which could impact Cat Financial’s write-offs and provision for credit losses. |

| |

| • | The process Cat Financial uses to estimate losses inherent in its credit exposure requires a high degree of management’s judgment regarding numerous subjective qualitative factors, including forecasts of economic conditions and how economic predictors might impair the ability of its borrowers to repay their loans. Financial market disruption and volatility may impact the accuracy of these judgments. |

| |

| • | Cat Financial’s ability to engage in routine funding transactions or borrow from other financial institutions on acceptable terms or at all could be adversely affected by disruptions in the capital markets or other events, including actions by rating agencies and deteriorating investor expectations. |

| |

| • | As Cat Financial’s lending agreements are primarily with financial institutions, their ability to perform in accordance with any of its underlying agreements could be adversely affected by market volatility and/or disruptions in financial markets. |

Changes in interest rates or market liquidity conditions could adversely affect Cat Financial's and our earnings and/or cash flow.

Changes in interest rates and market liquidity conditions could have an adverse impact on Cat Financial's and our earnings and cash flows. Because a significant number of the loans made by Cat Financial are made at fixed interest rates, its business results are subject to fluctuations in interest rates. Certain loans made by Cat Financial and various financing extended to Cat Financial are made at variable rates that use LIBOR as a benchmark for establishing the interest rate. LIBOR is the subject of recent proposals for reform. On July 27, 2017, the United Kingdom’s Financial Conduct Authority announced that it intends to stop persuading or compelling banks to submit LIBOR rates after 2021. These reforms may cause LIBOR to cease to exist, new methods of calculating LIBOR to be established such that LIBOR continues to exist after 2021 or the establishment of an alternative reference rate(s). Several offerings of securities that include such an alternative reference rate have now been completed by other companies. The consequences of these developments cannot be entirely predicted and could have an adverse impact on the market value for or value of LIBOR-linked securities, loans, derivatives, and other financial obligations or extensions of credit held by or due to Cat Financial, as well as the revenue and expenses associated with those securities, loans and financial instruments. Cat Financial has created a cross-functional team that will assess risk across multiple categories as it relates to the use of LIBOR in securities, loans, derivatives, and other financial obligations or extensions of credit held by or due to us. The team is also closely monitoring the progress of LIBOR reform and preparing to incorporate appropriate fallback language for transitioning to an alternative reference rate(s) into new agreements with customers. The team is reviewing how to best manage those customer agreements that extend beyond 2021 and utilize LIBOR. Other changes in market interest rates may influence Cat Financial’s borrowing costs and could reduce its and our earnings and cash flows, returns on financial investments and the valuation of derivative contracts. Cat Financial manages interest rate and market liquidity risks through a variety of techniques that include a match funding strategy, the selective use of derivatives and a broadly diversified funding program. There can be no assurance, however, that fluctuations in interest rates and market liquidity conditions will not have an adverse impact on its and our earnings and cash flows. If any of the variety of instruments and strategies Cat Financial uses to hedge its exposure to these types of risk is ineffective, this may have an adverse impact on our earnings and cash flows. With respect to Insurance Services' investment activities, changes in the equity and bond markets could result in a decline in value of its investment portfolio, resulting in an unfavorable impact to earnings.

An increase in delinquencies, repossessions or net losses of Cat Financial customers could adversely affect its results.

Inherent in the operation of Cat Financial is the credit risk associated with its customers. The creditworthiness of each customer and the rate of delinquencies, repossessions and net losses on customer obligations are directly impacted by several factors, including relevant industry and economic conditions, the availability of capital, the experience and expertise of the customer's management team, commodity prices, political events and the sustained value of the underlying collateral. Any increase in delinquencies, repossessions and net losses on customer obligations could have a material adverse effect on Cat Financial's and our earnings and cash flows. In addition, although Cat Financial evaluates and adjusts its allowance for credit losses related to past due and non-performing receivables on a regular basis, adverse economic conditions or other factors that might cause deterioration of the financial health of its customers could change the timing and level of payments received and necessitate an increase in Cat Financial's estimated losses, which could also have a material adverse effect on Cat Financial's and our earnings and cash flows.

Currency exchange rate fluctuations affect our results of operations.

We conduct operations in many countries involving transactions denominated in a variety of currencies. We are subject to currency exchange rate risk to the extent that our costs are denominated in currencies other than those in which we earn revenues. Fluctuations in currency exchange rates have had, and will continue to have, an impact on our results as expressed in U.S. dollars. There can be no assurance that currency exchange rate fluctuations will not adversely affect our results of operations, financial condition and cash flows. While the use of currency hedging instruments may provide us with protection from adverse fluctuations in currency exchange rates, by utilizing these instruments we potentially forego the benefits that might result from favorable fluctuations in currency exchange rates. In addition, our outlooks do not assume fluctuations in currency exchange rates. Adverse fluctuations in currency exchange rates from the date of our outlooks could cause our actual results to differ materially from those anticipated in our outlooks and adversely impact our business, results of operations and financial condition.

We also face risks arising from the imposition of exchange controls and currency devaluations. Exchange controls may limit our ability to convert foreign currencies into U.S. dollars or to remit dividends and other payments by our foreign subsidiaries or businesses located in or conducted within a country imposing controls. Currency devaluations result in a diminished value of funds denominated in the currency of the country instituting the devaluation.

Restrictive covenants in our debt agreements could limit our financial and operating flexibility.

We maintain a number of credit facilities to support general corporate purposes (facilities) and have issued debt securities to manage liquidity and fund operations (debt securities). The agreements relating to a number of the facilities and the debt securities contain certain restrictive covenants applicable to us and certain subsidiaries, including Cat Financial. These covenants include maintaining a minimum consolidated net worth (defined as the consolidated shareholder’s equity including preferred stock but excluding the pension and other post-retirement benefits balance within accumulated other comprehensive income (loss)), limitations on the incurrence of liens and certain restrictions on consolidation and merger. Cat Financial has also agreed under certain of these agreements not to exceed a certain leverage ratio (consolidated debt to consolidated net worth, calculated (1) on a monthly basis as the average of the leverage ratios determined on the last day of each of the six preceding calendar months and (2) at each December 31), to maintain a minimum interest coverage ratio (profit excluding income taxes, interest expense and net gain/(loss) from interest rate derivatives to interest expense, calculated at the end of each calendar quarter for the rolling four quarter period then most recently ended) and not to terminate, amend or modify its support agreement with us.