As submitted to the Securities and Exchange Commission on January 27, 2021

PART II INFORMATION REQUIRED IN THE OFFERING CIRCULAR

Preliminary Offering Circular dated January 27, 2021

An offering statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted prior to the time an offering circular that is not designated as a Preliminary Offering Circular is delivered and the offering statement filed with the Commission becomes qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a Final Offering Circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the Final Offering Circular or the offering statement in which such Final Offering Circular was filed may be obtained.

GATEWAY GARAGE PARTNERS LLC

181 HIGH STREET LLC

Units of Limited Liability Company Interest

$650,000 Minimum Offering Amount

$1,000,000 Maximum Offering Amount

Gateway Garage Partners LLC (“Gateway”) is a newly formed Delaware limited liability company organized for the sole purpose of acquiring a membership interest (the “Interest”) in 181 High Street, LLC, a Maine limited liability company (“OpCo” and, together with Gateway, the “Issuers”). OpCo’s sole asset is a 208,375 square foot parking garage containing approximately 600 parking spaces located at 181 High Street, Portland, Maine (the “Property”). For additional information regarding the Property, see “Description of the Property” beginning on page 17.

Gateway is managed by Noyack Medical Partners LLC (the “Manager”), which is also the manager of OpCo. For additional information regarding the Manager, see “Management” beginning on page 27.

Gateway intends to qualify to be treated as a partnership for U.S. federal income tax purposes. See “Material U.S. Federal Income Tax Considerations” beginning on page 38. The mailing address of the principal executive offices of the Issuers is 6 West 20th Street, 5th Floor, New York, New York 10011 and their telephone number is (813) 438-6452.

The Issuers are offering a minimum of $650,000 of units of limited liability company units, or Units, of Gateway and a maximum of $1,000,000 of Units at an initial offering price of $250 per Unit. This offering is being made on a “best efforts” basis which means that no one is committed to purchasing any Units in this offering. OpCo has engaged Independent Brokerage Solutions LLC, formerly known as SDDco Brokerage Advisors LLC, and LEX Markets LLC (the “Placement Agents”), to act as the exclusive placement agents in connection with this offering. The Placement Agents are not obligated to purchase any Units or sell a specific amount of Units, but will use its commercially reasonable “best efforts” to solicit purchases of the Units. OpCo will pay the Placement Agents a placement fee equal to 4% of the gross proceeds of the Units sold in this offering.

The minimum aggregate investment in the Units is $650,000, based on the initial public offering price of $250.00 per Unit. We expect to commence the offering of the Units promptly following the qualification of the offering statement of which this offering circular forms a part and to continue this offering until August 31, 2021, or the Termination Date. We reserve the right to extend the Termination Date in our sole discretion. Subscription proceeds will be held in escrow until closing and will not bear interest. If we do not receive subscriptions for the total minimum offering amount set forth herein by the Termination Date, we will cancel this offering and return promptly all subscription amounts, without interest, in compliance with Rule 10b-9 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). See “Plan of Distribution—Subscription Process” beginning on page 50. We reserve the right to terminate this offering for any reason at any time.

The Company will receive 100% of the proceeds from this offering. The Placement Agents have agreed to pay the expenses of this offering, other than the placement fee payable to the Placement Agent. As a result, this is a “no load” offering, and the investors will not be required to pay any organization or offering expenses. Gateway will pay LEX Markets LLC an annual platform fee equal to 1.0% of the value of the public float of the Units, which will be initially based on the $250 offering price per Unit. The price per Unit will remain the same for the throughout the term of the offering. Following the completion of the offering, the value of the public float will be based on the average price per Unit for the last 90 calendar days of the immediately preceding calendar year. See “LEX Markets Trading Platform” beginning on page 37.

Gateway intends to use all the proceeds of this offering to acquire the Interest. See “Use of Proceeds” beginning on page 15. The Issuers expect that the sole source of funds for any distributions paid in respect of the Units will be distributions from OpCo resulting from our ownership of the Interest. See “Our Distribution Policy” beginning on page 16.

This offering is intended to qualify as a “Tier 2” offering pursuant to Regulation A promulgated under the Securities Act of 1933, as amended, or the Securities Act. In preparing this offering circular, the Issuers have elected to comply with the offering circular disclosure requirements specified in Form 1-A under Regulation A.

Because this offering is being conducted pursuant to Regulation A under the Securities Act, the Issuers are subject to reduced reporting requirements. Consequently, investors in this offering will have less information about the Issuers than would be available regarding an issuer of registered securities. This lack of information may make it more difficult for an investor to evaluate an investment in the Units. See “Risk Factors — We are subject to reduced reporting requirements which may make it more difficult for investors to evaluate an investment in the Units.”

In connection with this offering, the Issuers intend to seek to have the Units admitted to trading on an “alternative trading system” (the “ATS”) to be maintained by LEX Markets LLC. See “LEX Markets Trading Platform” beginning on page 37. However, there can be no assurance that an active trading market for the Units will be established or, if established, maintained. As a result, the liquidity of your investment in the Units may be limited.

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

Investing in the Units involves a high degree of risk, including material income tax risks and risks arising from potential conflicts of interest between the Manager, OpCo and Gateway. See “Risk Factors” beginning on page 6 for risks you should consider before buying the Units. You should purchase these securities only if you can afford a complete loss of your investment.

NEITHER THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES REGULATOR HAS PASSED UPON THE MERITS OF OR GIVEN ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THIS OFFERING, NOR DO ANY OF THEM PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SELLING LITERATURE. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION. ANY REPRESENTATION TO THE CONTRARY IS UNLAWFUL.

| | | Price to public | | Placement agent fees | | Proceeds to us (1) |

| Per unit | | $250 | | (1) | | $250.00 |

| Total minimum | | $650,000 | | (1) | | $650,000 |

| Total maximum | | $1,000,000 | | (1) | | $1,000,000 |

| (1) | OpCo has agreed to pay the Placement Agents a placement fee equal to 4% of the gross proceeds of the Units sold in this offering and to reimburse the Placement Agents for certain expenses. The Placement Agents have agreed to pay the expenses of this offering up to the extent of the 4% placement fee received. LEX Markets Corp. is responsible for any expenses in excess of the total placement fee and has already paid certain additional expenses of the Placement Agents totaling $38,569, the details of which are described under the heading “Plan of Distribution” beginning on page 50. We are not obligated to reimburse the Placement Agents for such expenses. Accordingly, the Company will receive 100% of the proceeds of the offering, all of which will be used by us to acquire the Interest in OpCo. See “Use of Proceeds” and “Plan of Distribution.” |

This Offering Circular follows the Offering Circular disclosure format.

| INDEPENDENT BROKERAGE SOLUTIONS LLC | LEX MARKETS LLC |

The date of this offering circular is January __, 2021

IMPORTANT INFORMATION ABOUT THIS OFFERING CIRCULAR

In this offering circular, Gateway Garage Partners LLC is referred to as “Gateway” or the “Company.” The co-issuer of this offering, 181 High Street, is referred to as “OpCo.” Gateway and OpCo are referred to together as the “Issuers,” “we,” “us” or “our.” Noyack Medical Partners LLC, in its capacity as the managing member of the Company, is referred to as the “Manager” and in its capacity as the manager of OpCo, is referred to as the “OpCo Manager.”

Please carefully read the information in this offering circular and any accompanying offering circular amendments and supplements, which we refer to collectively as the offering circular. You should rely only on the information contained in this offering circular. We have not authorized anyone to provide you with different information. This offering circular may only be used where it is legal to sell these securities. You should not assume that the information contained in this offering circular is accurate as of any date later than the date hereof or such other dates as are stated herein or as of the respective dates of any documents or other information incorporated herein by reference.

This offering circular is part of an offering statement that we filed with the Securities and Exchange Commission (the “SEC”), using a continuous offering process. The offering statement we filed with the SEC includes exhibits that provide more detailed descriptions of the matters discussed in this offering circular. You should read this offering circular and the related exhibits filed with the SEC and any offering circular supplement, together with additional information contained in our annual reports, semi-annual reports and other reports and information statements that we will file periodically with the SEC. See the section entitled “Additional Information” below for more details.

We are offering to sell, and seeking offers to buy, the Units only in jurisdictions where such offers and sales are permitted. You should rely only on the information contained in this offering circular. We have not and the Placement Agents have not authorized anyone to provide you with any information other than the information contained in this offering circular. The information contained in this offering circular is accurate only as of its date, regardless of the time of its delivery or of any sale or delivery of our securities. Neither the delivery of this offering circular nor any sale or delivery of the Units shall, under any circumstances, imply that there has been no change in our affairs since the date of this offering circular. This offering circular will be updated and made available for delivery to the extent required by the federal securities laws.

The offering circular and all supplements and reports that we have filed or will file in the future can be read at the SEC website, www.sec.gov, or on the LEX Markets Platform website, www.LEX-markets.com. The contents of the LEX Markets Platform website (other than the offering statement, this offering circular and the appendices and exhibits thereto) are not incorporated by reference in or otherwise a part of this offering circular.

The Manager and the Placement Agents will be permitted to make a determination that a purchaser of Units in this offering is a “qualified purchaser” in reliance on the information and representations provided by the investor regarding the investor’s financial situation. Before making any representation that an investment does not exceed applicable thresholds, we encourage investors to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage investors to refer to www.investor.gov.

TABLE OF CONTENTS

STATEMENTS REGARDING FORWARD-LOOKING INFORMATION

Some of the statements in this offering circular constitute forward-looking statements, including, without limitation, the disclosure under the caption “Description of the Property—Five-Year Financial Projections” beginning on page 22. These statements relate to future events or our future financial performance, plans and objectives. In some cases, you can identify forward-looking statements by terminology such as “may,” “should,” “expect,” “intend,” “plans,” “assumes,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue,” “will,” and similar words or phrases or the negative or other variations thereof or comparable terminology. All forward-looking statements are predictions or projections and involve known and unknown risks, estimates, assumptions, uncertainties and other factors that may cause our actual transactions, results, performance, achievements and outcomes to differ adversely from those expressed or implied by such forward-looking statements.

You should not place undue reliance on forward-looking statements. The cautionary statements set forth in this offering circular, including in “Risk Factors” and elsewhere, identify important factors that you should consider in evaluating our forward-looking statements.

Although we believe that the expectations reflected in our forward-looking statements are reasonable, we cannot guarantee future results, performance, achievements or outcomes. No assurance can be made to any investor by anyone that the expectations reflected in our forward-looking statements will be attained or that deviations from them will not be material and adverse. We undertake no obligation, other than as may be required by law, to re-issue this offering circular or otherwise make public statements in order to update our forward-looking statements beyond the date of this offering circular.

SUMMARY

This offering summary highlights information contained elsewhere and does not contain all of the information that investors should consider in making their investment decisions. Before investing in the Units, investors should carefully read this entire offering circular, including the financial statements and related notes included herein. Investors should also consider, among other information, the matters described under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

The Issuers

Overview

Gateway Garage Partners LLC is a newly formed Delaware limited liability company organized for the sole purpose of acquiring a membership interest, or the Interest, in 181 High Street LLC, or OpCo, a Maine limited liability company. OpCo is a limited liability company that was formed in 2008 and its sole asset is a 208,375 square feet parking garage containing approximately 600 parking spaces located at 181 High Street, Portland, Maine (the “Property”).

Upon the completion of this offering, Gateway will acquire the Interest in exchange for a capital contribution equal to the proceeds of this offering. The Interest will entitle Gateway to receive up to a 10 % share of the profits and losses of OpCo, with the exact amount being determined by dividing the gross proceeds of this offering by approximately $10.03 million, which is the market value of OpCo’s equity in the Property as determined by the OpCo Manager. For additional information regarding the Property valuation, see “Description of the Property—Property Valuation” beginning on page 19. If we sell Units equal to the total minimum offering amount set forth on the cover of this offering circular, we estimate Gateway’s proportionate share will be 6.5 %. If we sell Units equal to the total maximum offering amount set forth on the cover of this offering circular, we estimate that Gateway’s proportionate share will be 10 %.

Gateway intends to qualify to be treated as a partnership for U.S. federal income tax purposes. See “Material U.S. Federal Income Tax Considerations” beginning on page 40. As members of a limited liability company that will elect to be taxed as a partnership, the holders of Units will receive annual Schedule K-1s following the end of each taxable year. Schedule K-1s are usually complex and may require investors to retain sophisticated tax experts to assist the taxpayer in preparing its tax return. See “Risk Factors—Risks Related to Tax Considerations” beginning on page 14. The mailing address of our principal executive offices is 6 West 20th Street, 5th Floor, New York, New York 10011 and our telephone number is (813) 438-6452.

The Manager

Noyack Medical Partners LLC is the Manager and is responsible for directing the management of Gateway’s business and affairs and implementing its investment strategy. The Manager and its officers and managers are not required to devote all of their time to Gateway’s business and are only required to devote such time to Gateway’s affairs as their duties require. The Manager performs its duties and responsibilities to Gateway pursuant to the terms of Gateway’s limited liability company agreement, or the Operating Agreement. The Manager will not receive any compensation for serving as the managing member of the Company. The OpCo Manager will be paid an asset management fee equal to two percent (2%) of OpCo’s annual gross income, subject to a five percent (5%) cap on the aggregate management fee payable by OpCo to the Property manager and the OpCo Manager. For additional information regarding the Manager, see “Management” beginning on page 28.

The Property

The Property consists of a five-story parking garage located at 181 High Street, Portland, Maine. The parking garage has 208,375 square feet of parking space consisting of approximately 600 parking spaces and two elevators. The garage is open 24 hours a day, seven days a week and 52 weeks a year. There are multiple security cameras on the Property, and multiple daily live patrols are conducted by a third-party security vendor. The parking garage was originally built in 1987 and went through an upgrade in 2011 in order to accommodate customers from one of its lessees. OpCo intends to use approximately $300,000 of the proceeds of this offering to replace one of the four façade sides of the parking garage and to reimburse a portion of the $2.5 million for capital expenses already completed at the Property. See “OpCo Business and Growth Plan” beginning on page 24 for more details.

The Property Leases

The parking garage is currently subject to three lease/license agreements pursuant to which substantially all of the spaces are reserved for or guaranteed for use by the lessees; however, the general public also has access to a number of the spaces on an as-available basis. The average monthly rental/license rates payable by the licensees is $139 per parking space. The rates for the general public are currently $4 per hour ($5.00 for the first hour), with a maximum of eight hours a day, and $185 per month. See “Description of the Property—The Parking Leases” beginning on page 18.

Contribution Transaction

Gateway will enter into a Contribution Agreement, or the Contribution Agreement, with OpCo. Pursuant to the terms of the Contribution Agreement, Gateway will contribute the proceeds of this offering to OpCo in exchange for the Interest. The Interest will entitle Gateway to receive a proportionate share of the profits and losses of OpCo of up to 10%, with the exact amount being determined by dividing the gross proceeds of this offering by approximately $10.03 million, which is the market value of OpCo’s equity in the Property as established by the OpCo Manager. If we sell Units equal to the total minimum offering amount set forth on the cover page of this offering circular, we estimate that Gateway’s proportionate share will be 6.5%. If we sell Units equal to the total maximum offering amount set forth on the cover of this offering circular, we estimate that Gateway’s proportionate share will be 10 %. For additional information, see “Contribution Agreement” beginning on page 30.

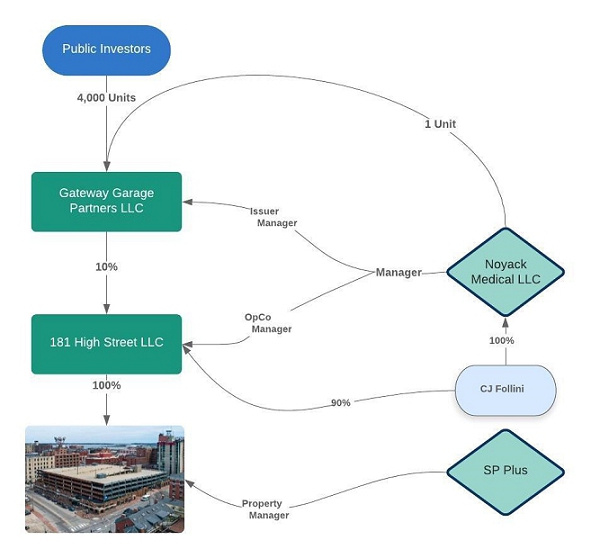

Organizational Chart

The organizational chart set forth below sets forth the ownership structure of OpCo after giving effect to the Contribution Transaction, assuming the total maximum offering amount has been raised in this offering.

Contribution Transaction

(assumes Maximum Offering Amount)

The Offering

| Issuers | | Gateway Garage Partners LLC and 181 High Street LLC |

| | | |

| Securities offered | | Units of Limited Liability Company Interest (“Units”). The Units will have the terms described under “Description of Units.” |

| | | |

| Distributions | | We expect that the sole source of funds for any distributions paid in respect of the Units will be distributions from OpCo resulting from Gateway’s ownership of the Interest. The Manager will distribute all funds received from OpCo, net of expense, principally the Platform Fee payable to LEX Markets, to the holders of the Units within ten (10) business days following receipt. See “Distribution Policy” on page 16. |

| | | |

| Price per Unit | | $250.00 |

| | | |

| Offering Type | | This offering is being made on a “best efforts” basis and is intended to qualify as a “Tier 2” offering pursuant to Regulation A promulgated under the Securities Act. |

| | | |

| Total Minimum Offering Amount/Total Maximum Offering Amount | | We are offering a minimum amount of $650,000 of the Units (the “Total Minimum Offering Amount”) and a maximum of up to $1,000,000 of the Units (the “Total Maximum Offering Amount”). |

| | | |

| Minimum and Maximum Investment | | There is a $250 minimum investment requirement, and the maximum amount that each investor can purchase is subject to the investment threshold described under “Plan of Distribution—Investment Threshold” on page 50. We can waive the minimum and maximum purchase requirements on a case-by-case basis in our sole discretion. Subscriptions, once received, are irrevocable by the investors but can be rejected by us. |

| | | |

| Placement Agents | | We have engaged Independent Brokerage Solutions LLC, formerly known as SDDco Brokerage Advisors LLC, and LEX Markets LLC (the “Placement Agents”), to act as our exclusive placement agents in connection with this offering. The Placement Agents are not obligated to purchase any Units or sell a specific amount of Units, but will use its commercially reasonable “best efforts” to solicit purchases of the Units. |

| | | |

| Payment for Units | | After the qualification by the SEC of the offering statement of which this offering circular is a part, investors can make payment of the purchase price (i) for investors holding or opening brokerage accounts with LEX Markets LLC, by funding that account by automated clearing house (ACH) debit transfer and following the subscription instructions on the LEX Markets website or (ii) for investors investing more than $50,000 through the manual subscription process, who desire to hold their Units at another U.S. brokerage firm, by wiring funds into a segregated non-interest bearing account at Bank of America, N.A. held by Computershares Trust Company until the initial closing date of this offering, which shall occur on the date that the Total Minimum Offering Amount has been raised. See “Plan of Distribution—Subscription Process” On the closing date, the funds in the account will be released to Gateway and the associated Units will be issued to the investors in this offering. If there is no closing of this offering, the funds deposited in the escrow account will be returned promptly to the investors, without interest, in compliance with Rule 10b-9 under the Exchange Act. |

| The Platform | | LEX Markets LLC operates the LEX Markets Platform located at www.LEX-markets.com that enables investors to become equity holders in companies that own real estate properties. Through the LEX Markets Platform, investors can browse and screen potential property investments, view details of an investment and sign contractual documents online. After the qualification by the SEC of the offering statement of which this offering circular is a part, the offering will be conducted through the facilities of the LEX Markets Platform, whereby investors will receive, review, execute and deliver subscription agreements electronically. The Company will pay LEX Markets LLC an annual platform fee equal to 1.0% of the value of the public float of the Units (the “Platform Fee”), which will initially be based on the $250 offering price per Unit. The price per Unit will remain the same throughout the term of the offering. Following completion of the offering, the public float will be based on the average price per Unit for the last 90 calendar days of the immediately preceding calendar year. For additional information, see “Plan of Distribution – Procedures for Subscribing” and “LEX Markets Trading Platform” on pages 50 and 37, respectively. |

| | | |

| Termination Date | | August 31, 2021 (the “Termination Date”). We reserve the right to extend the Termination Date in our sole discretion. If we do not receive subscriptions for the Total Minimum Offering Amount by the Termination Date, we will cancel this offering and return promptly all subscription amounts, without interest, in compliance with Rule 10b-9 under the Exchange Act. We reserve the right to terminate this offering for any reason at any time. See “Plan of Distribution” on page 50. |

| | | |

| Use of Proceeds | | Upon the completion of this offering, Gateway will acquire the Interest in exchange for a capital contribution equal to the proceeds of this offering. Gateway will contribute all of the proceeds from this offering to OpCo in exchange for the Interest. The Interest will entitle Gateway to receive a proportionate share of the profits and losses of OpCo of up to 10%, with the exact amount being determined by dividing the gross proceeds of this offering by approximately $10.03 million, which is the market value of OpCo’s equity in the Property as determined by OpCo Manager. If we sell Units equal to the Total Minimum Offering Amount, we estimate that Gateway’s proportionate share will be 6.5%. If we sell Units equal to the Total Maximum Offering Amount, we estimate that Gateway’s proportionate share will be 10%. See “Contribution Agreement” beginning on page 30. OpCo will use a portion of the amount contributed by Gateway pursuant to the Contribution Agreement to fund certain capital improvements to the Property, with the remainder being used to redeem a portion of the outstanding membership interests in OpCo. |

| | | |

| Servicing and Paying Agent | | We may engage a third party to act as a servicing and paying agent. We expect that the fee for any such servicing and paying agent will be paid by LEX Markets LLC. See “Distribution Policy” on page 16. |

| | | |

| Limitation on Your Investment Amount | | Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or your net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A, which states that no sale of securities may be made: In a Tier 2 offering of securities that are not listed on a registered national securities exchange upon qualification, unless the purchaser is either an accredited investor (as defined in Rule 501 (§230.501)) or the aggregate purchase price to be paid by the purchaser for the securities (including the actual or maximum estimated conversion, exercise, or exchange price for any underlying securities that have been qualified) is no more than ten percent (10%) of the greater of such purchaser’s: (1) Annual income or net worth if a natural person (with annual income and net worth for such natural person purchasers determined as provided in Rule 501 (§230.501)); or (2) Revenue or net assets for such purchaser’s most recently completed fiscal year end if a non-natural person. |

| | | |

| Trading Market | | In connection with this offering, we intend to seek to have the Units admitted to trading on an “alternative trading system” or, ATS, maintained by LEX Markets LLC. See “LEX Markets Trading Platform” beginning on page 37. However, there can be no assurance that an active trading market for the Units will be established or, if established, maintained. As a result, the liquidity of your investment in the Units may be limited. |

| Information Requirements | | Under the terms of the Contribution Agreement, OpCo and Gateway will enter into an issuer servicing agreement with Largo Real Estate Advisors, Inc. (“Largo”), an independent service provider, pursuant to which OpCo will provide certain information regarding its ongoing business operations to Largo so that the Largo can ensure Gateway complies with its periodic reporting obligations under Regulation A. The failure by OpCo to provide the required information to Largo will constitute an event of default by OpCo under the Contribution Agreement, which will result in each holder of Units having the right to put its Units to OpCo. See “Contribution Agreement – Information Rights” on page 30. LEX Markets LLC will pay Largo an annual fee equal to 0.15% of the value of the public float of the Units. |

| | | |

| Material U.S. Federal Income Tax Considerations | | Gateway intends to qualify to be treated as a partnership for U.S. federal income tax purposes. See “Material U.S. Federal Income Tax Considerations” beginning on page 38. |

| | | |

| Summary Risk Factors | | ● Gateway will be dependent on the Manager to operate our business. ● The Operating Agreement provides that the assets, affairs and business of Gateway will be managed under the direction of the Manager. Holders of the Units will not have the right to elect or remove the Manager, and, unlike the holders of common shares in a corporation, will have only limited voting rights on matters affecting our business, and therefore limited ability to influence decisions regarding our business. Notwithstanding the foregoing, the authority of the Manager is restricted in the manner described in “Contribution Agreement--Management of OpCo” on page 30. ● The parking leases are subject to termination upon the occurrence of certain events of default. If the parking leases are terminated as a result of an event of default, the value of your investment could be substantially reduced. ● Gateway has no operating history, and as of the date of this offering circular, its total assets consist of a nominal amount of cash. There is no assurance that it will achieve its business objectives. ● The only source of funds for any distributions payable in respect of the Units will be distributions from OpCo relating to Gateway’s ownership of the Interest. ● There is no guarantee that any secondary market for the Units will be established or, if established, maintained. ● Real estate investments are subject to general downturns in the industry as well as downturns in specific geographic areas. We cannot predict what the lease rate or performance will be for the Property. We also cannot predict the future value of the Property. ● OpCo’s ownership of the Property will be subject to risks relating to the volatility in the value of the underlying real estate, default on underlying income streams, fluctuations in interest rates, and other risks associated with the operation of real estate generally. ● Your investment in the Units will not be diversified. ● There is no assurance that you will be treated as a partners for U.S. federal income tax purposes. |

RISK FACTORS

An investment in the Units involves substantial risks. You should carefully consider the following risk factors in conjunction with the other information contained in this offering circular before purchasing the Units. The risks discussed in this offering circular could materially and adversely affect our business, operating results, prospects and financial condition. This could cause the value of the Units to decline and could cause you to lose all or part of your investment. The risks and uncertainties described below represent those risks and uncertainties that we believe are material to our business, operating results, prospects and financial condition as of the date of this offering circular.

Risks Related to an Investment in the Units

The Company previously published and filed testing the waters communication in reliance on Rule 255 under the Securities Act which we have determined should no longer be relied upon. You should rely only on statements made in this offering circular in determining whether to purchase our shares.

We previously disseminated testing the waters communications that contained, among other things, gross and net cash yields projections that we have determined may be confusing to investors and viewed by them as a projection of current returns which was not the intention when the communications were originally disseminated. To avoid any such confusion, we urge investors to disregard the projections in making their investment decisions. You should rely only on the information contained in this offering circular, including the risks and uncertainties described in this section, in making your investment decision. We encourage you to carefully evaluate all of the information included in this offering circular.

Gateway is a recently-formed company with no prior operating history and its business model is untested.

Gateway was formed in May 2020 and has no operating history as of the date of this offering circular. We cannot make any assurance that Gateway’s business model can be successful. Since inception, the scope of Gateway’s operations has been limited to our formation and conducting this offering. It is difficult to predict whether its business model will succeed or if there will ever be any value in the Units.

Investors purchasing the Units will not be purchasing an interest in a diversified portfolio of real estate assets.

The sole source of funds for any distributions paid in respect of the Units will be distributions from OpCo relating to Gateway’s ownership of the Interest in OpCo. Investors purchasing the Units will not have the benefit of a diversified portfolio of real estate assets. A consequence of limiting our scope of operations to an investment in a single property is that the aggregate value of the Units is expected to correlate to the value of the Property, which may fluctuate significantly.

Distributions Gateway receives from OpCo may be less than estimated, and Gateway may experience a decline in realized revenues from time to time, which could adversely affect the value of the Units and the distributions you may receive.

The Property may not achieve the revenues that we anticipate based on its prior performance. Revenues are tied to the parking rates for the Property. If the distributions Gateway receives from OpCo are less than estimated, the value of the Units and the distributions you may receive could decline. The potential factors leading to reduced revenues include competitive pricing pressure in the local market as well as general economic downturn and the changes in the desirability of the Property compared to other properties. Depending on market rental rates at any given time as compared to expiring leases on the Property, from time to time rental rates for expiring leases may be higher than starting rental rates for new leases. If OpCo is unable to obtain sufficient rental rates for the Property, the cash distributions to investors may be materially and adversely affected.

The performance of the Property will fluctuate with general and local economic conditions.

The successful operation of any real estate asset is significantly related to general and local economic conditions. Periods of economic slowdown or recession, significantly rising interest rates, declining employment levels and other economic events may decrease demand for real estate, which can result in lower rent and lower occupancy levels. As a result, these factors may adversely affect the value of the Property, the value of the Units and distributions paid to holders of the Units from the operation of the Property.

Investment in the Units is speculative, and each investor assumes the risk of losing his, her or its entire investment.

Investment in the Units is speculative and, by investing, you assume the risk of losing your entire investment. Gateway has limited operations as of the date of this offering circular and will be solely dependent upon the efforts of the Manager and the operating results of the Property, all of which are subject to the risks described herein.

Accordingly, only investors who are able to bear the loss of their entire investment and who otherwise meet the investor suitability standards should consider purchasing the Units.

The valuation of the Property may not reflect the price at which the Property could be sold to a third-party buyer.

The determination of the fair value of real estate assets involves significant judgment. The valuation of the Property is based, in part, on an appraisal, which is an estimate of the value based on a professional’s opinion and may not be an accurate predictor of the amount OpCo would actually receive if it sold the Property. Appraisals can be subjective in certain respects and rely on a variety of assumptions and conditions at a property or in the market in which the property is located, which may change materially after the appraisal is conducted. Among other things, market prices for comparable real estate may be volatile, particularly if there has been a lack of recent transactions in such market. Any resulting lack of observable transaction data may make it more difficult for a property appraiser to determine the fair value of a property. In addition, a portion of the data used by appraisers is based on historical information at the time the appraisal is conducted and subsequent changes to such data may not be adequately captured in the appraised value. Further, implicit in the determination of the market value of a property is a principal assumption that there will be a reasonable time to market the property. As a result, the market value may not reflect the actual realizable value that would be obtained in a rushed sale where time was of the essence.

Risks Related to the Property

Defaults or terminations of OpCo’s license/parking agreements could materially and adversely affect the distributions to be paid to the Company.

The amount of distributions payable by OpCo materially depends on the financial stability of the other parties to OpCo’s license and parking agreements. A default or termination under any of these agreements would cause the Property to lose the revenue associated with such agreement and may require OpCo to find an alternative source of revenue in order to generate income available for distribution to its members, including Gateway. In the event of a default, consisting of a payment or covenant default that is not remedied within the requisite cure period, or bankruptcy of the other party, OpCo may experience delays in enforcing its rights under these agreements and may incur substantial costs re-renting the parking spaces. If the other party defaults under or terminates its agreement with OpCo, OpCo may be unable to rent the parking spaces at the rates previously received. These events could materially and adversely affect the distributions to be paid from the operation of the Property to the Company. See “Description of the Property--The Property Leases.”

OpCo’s reliance on a small number of licensees may adversely affect the distributions to be paid to the Company.

The three license/parking agreements on the Property, currently license or guarantee substantially all of the available parking spaces (with spaces available for the use by the general public on an as-available basis) and provide approximately 63% of OpCo’s annual revenues, for the fiscal year ending December 31, 2019. A deterioration in the financial condition or a change in the plan of operations of the other parties to these agreements could have a particularly significant effect on the net operating income generated by the Property and the amount available for distribution to the Company and the holders of the Units.

In addition, any of these other parties may become insolvent, may suffer a downturn in business and default on or terminate its agreement with OpCo, or may decide not to renew its agreement. Any of these events would result in a reduction or cessation in rent payments to OpCo from that lessee and would adversely affect the value of Property and the distributions payable to the Company and the holders of the Units.

Competition in the real estate market where the Property is located and other risks may affect the value of the Property, the value of the Units and the distributions payable to the Company.

The market for parking lots and parking spaces is highly competitive and there can be no assurance that the Property will be able to compete effectively for customers in its market. In addition, the low cost of entry into the parking lot business could lead to increased competition for the Property, in particular the new parking facility being developed by one the Company’s major lessees, Maine Medical Center, may have a negative impact on the Company’s cash from operations when the facility is completed in 2022. See “Description of the Property—OpCo Business and Growth.” These risks may affect the value of the Property, the value of the Units and the distributions payable to holders of the Units.

Litigation at the Property may reduce the value of the Property, the value of the Units and the amount of distributions to holders of the Units.

The operation of the Property carries certain specific litigation risks. Litigation may be commenced with respect to the Property in relation to activities that took place prior to OpCo’s investment in the Property. Litigation involving the Property could cause a disruption of operations of the Property and may reduce the value of the Property, the value of the Units and the amount of distributions to holders of the Units.

An increase in property taxes may reduce the value of the Property, the value of the Units and the amount of distributions to holders of the Units.

The Property is subject to real property taxes and, in some instances, personal property taxes. Such real and personal property taxes may increase as property tax rates change and as the properties are assessed or reassessed by taxing authorities. An increase in property taxes on the Property could adversely affect OpCo’s results from operations and may reduce the value of the Property, the value of t Units and hethe amount of distributions to holders of the Units.

Because OpCo’s business is affected by weather-related trends, typically in the first and fourth quarters of each year, its results may fluctuate from period to period, which could impact the timing and amount of distributions made to the Company.

Weather conditions, including fluctuations in temperatures, snow or severe weather storms, heavy flooding or natural disasters, can negatively impact the use of the Property. OpCo has periodically experienced fluctuations in its quarterly results arising from a number of factors, including: (1) reduced levels of travel to and from work during and as a result of severe weather conditions and (2) increased costs of services, such as snow removal. These factors have typically had negative impacts on OpCo’s revenues and could cause revenue reductions in the future. As a result of these seasonal effects, OpCo’s revenues can fluctuate from quarter to quarter. Accordingly, OpCo may not be able to make, or only able to make reduced, distributions to the Company from time to time.

Changing consumer preferences and legislation may lead to a decline in parking demand, which would have a material adverse impact on OpCo’s results of operations and its ability to make distributions to the Company.

Ride sharing services, such as Uber and Lyft, and car sharing services like Zipcar may lead to a decline in the demand for parking spaces at the Property. In addition, state and local laws that have been or may be passed encouraging carpooling and the use of mass transit systems may negatively impact the demand for parking at the Property and the price that a customer would be willing to pay. In the future, local, state and federal environmental regulatory authorities may pursue or continue to pursue measures related to climate control and greenhouse gas emissions which may have the effect of decreasing the number of cars being driven. Such laws or regulations could adversely impact the demand for parking at the Property.

Uncertain economic conditions resulting from terrorism, natural disasters or pandemics could result in decreased demand for parking space.

An unstable geopolitical environment and continued threats of terrorism could have a material adverse effect on general economic conditions. Additionally, a serious pandemic or natural disaster could adversely disrupt global, national and/or regional economies. The outbreak of a novel and highly contagious form of coronavirus (COVID-19) has resulted in an approximately 15% reduction in the Company’s total revenue for the second quarter of 2020 as compared to the second quarter of 2019 due to reduced transient usage of the Property. The coronavirus has resulted, and renewed outbreaks of other epidemics or the outbreak of a new epidemic could result, in health or other government authorities requiring the closure of offices and other businesses, including office buildings, retail stores and other commercial venues and has resulted in a general economic decline. We are not able to predict the ultimate impact of this economic downturn on the operating results of the Property, but a long term economic decline could materially reduce OpCo’s net revenue and substantially reduce its ability to make distributions to its members, including the Company.

Costs associated with any latent environmental issues on the Property could reduce OpCo’s cash available for distribution to the Company.

If the Property is found to contain hazardous or toxic substances, OpCo might be required to expend considerable resources remediating the issues. If that were to occur, OpCo’s net distributable income available for distribution to its members, including the Company, could be reduced and the value of the Property could decrease below the amount paid for the Interest.

Risks Related to the LEX Markets Platform

LEX Markets is a development stage company with limited operating history. As a company in the early stages of development, LEX Markets faces increased risks, uncertainties, expenses and difficulties.

LEX Markets LLC (together with its parent LEX Markets Corp., “LEX Markets”) has a limited operating history. LEX Markets intends for current information about offerings and the performance of properties, including this offering and the Property, to be available on the LEX Markets Platform. LEX Markets and its contractors will be responsible for maintaining and expanding the LEX Markets Platform. If LEX Markets is unable to increase the capacity of the LEX Markets Platform and maintain the necessary infrastructure, or if LEX Markets is unable to make significant investments in the LEX Markets Platform on a timely basis or at reasonable costs, investors may not have access to the liquidity expected to be provided by the LEX Markets Platform.

If LEX Markets were to enter bankruptcy proceedings or cease operations, the operation of the LEX Markets Platform would be interrupted.

If LEX Markets were to enter bankruptcy proceedings or were to cease operations, we would need to find an alternative to the LEX Markets Platform as a mechanism to provide liquidity for secondary trading.

Any significant disruption in service on the LEX Markets Platform or in its computer systems could reduce the attractiveness of the online platform and result in a loss of users.

If a catastrophic event resulted in a platform outage and physical data loss, the LEX Markets Platform’s ability to perform its obligations would be materially and adversely affected. The satisfactory performance, reliability, and availability of the LEX Markets Platform technology and its underlying hosting services infrastructure are critical to our ability to share information, provide customer service, positive reputation and ability to attract new investment opportunities, new investors, and retain existing investors.

Risks Related to Conflicts of Interest

General

The Manager is also the OpCo Manager. There may be circumstances under which OpCo wishes to take or refrain from taking certain actions that are not in Gateway’s best interest. In those circumstances, the Manager may have a conflict of interest between Gateway’s interests and the interests of OpCo. There is no assurance that the Manager will resolve any such conflict of interest in Gateway’s favor.

Gateway has agreed to limit remedies available to it and its investors for actions by the Manager that might otherwise constitute a breach of duty.

The Manager maintains a contractual, as opposed to a fiduciary relationship, with Gateway and its investors. Accordingly, Gateway and its investors will only have recourse and be able to seek remedies against the Manager to the extent it breaches its obligations under the Operating Agreement. Furthermore, Gateway will agree in the Operating Agreement to limit the liability of the Manager and to indemnify the Manager against certain liabilities. These provisions may be detrimental to investors because they restrict the remedies available to them for actions that without those limitations might constitute breaches of duty, including fiduciary duties. In connection with purchasing the Units, investors will execute subscription documents including signature pages to the Operating Agreement pursuant to which they will become members of the Company and become subject to the provisions set forth in the Operating Agreement.

Risks Related to Investments in Real Estate

OpCo’s performance and the value of the Property are subject to risks associated with real estate investments and the real estate industry generally.

Deterioration of U.S. real estate fundamentals could negatively impact the performance of the Property. Furthermore, because real estate, like many other long-term investments, historically has experienced significant fluctuation and cycles in value, specific market conditions may result in occasional or permanent reductions in the value of the Property. Accordingly, the cash flow of the Property and thus the distributions to be paid to Unit holders will depend on many factors beyond the control of the Company, OpCo and the Manager, including: fluctuations in the average use and rental rates for the Property, changes in the availability of debt financing which may render the sale or refinancing of the Property difficult or impracticable, increases in property taxes and operating expenses, changes in environmental building and zoning laws, casualty or condemnation losses, changes in neighborhood values, changes in the appeal of the Property to those seeking parking space, various uninsured or uninsurable risks, increases in interest rates and the availability of mortgage funds which may render the sale or refinancing of the Property difficult or impracticable, environmental liabilities, acts of God, terrorist attacks, war and other factors.

The distributions to be received from the Property may be affected by the risks typically associated with the operation and management of real estate properties.

Distributions from the Property may be adversely affected by a number of additional risks, including:

| ● | natural disasters such as hurricanes, earthquakes and floods and other unexpected environmental conditions; |

| ● | acts of war or terrorism, including the consequences of terrorist attacks; |

| ● | adverse changes in national and local economic and real estate conditions; |

| ● | epidemics or pandemics (including COVID-19) or any escalation or worsening thereof; |

| ● | an oversupply of (or a reduction in demand for) parking space in the area where the Property is located and the attractiveness of the Property to prospective customers; |

| ● | changes in governmental laws and regulations, fiscal policies and zoning ordinances and the related costs of compliance therewith and the potential for liability under applicable laws; |

| ● | costs of remediation and liabilities associated with environmental conditions affecting properties; and |

| ● | the potential for uninsured or underinsured property losses. |

The value of a commercial real estate property is directly related to its ability to generate cash flow and net income, which in turn depends on the amount of rental or other income that can be generated net of expenses required to be incurred with respect to the Property. Many expenditures associated with properties (such as operating expenses and capital expenditures) cannot be reduced when there is a reduction in income from the properties. Any decrease in OpCo’s net distributable income would result in an immediate decrease in distributions payable to holders of the Units.

If the Property experiences significant unused spaces, the value of the Property will decline which would significantly impact the value of the Units and the distributions you may receive.

The Property may experience reduced usage of the parking space either by the expiration of parking leases or the reduced use of the parking garage by the general public. If reduced usages continue for a long period of time, OpCo may suffer reduced revenues resulting in less cash available for distribution to the investors. In addition, the value of the Property could be diminished because that value will depend principally upon the amount of the cash flow generated by rental of the parking spaces at the Property. Such a reduction in value would significantly impact the price of the Units and the distributions to be paid to investors.

Further, a decline in general economic conditions in the market in which the Property is located or in the United States generally could lead to lower rental rates and less demand for parking space in that market. As a result of these trends, new lessees may require lower rates which could result in reduced revenue and a lower value of the Property, which could materially and adversely affect the value of the Units and the distributions to be paid to investors.

The costs of defending against claims of environmental liability, of complying with environmental regulatory requirements, of remediating any contaminated property or of paying personal injury or other damage claims could reduce the amounts available for distribution to the Company.

Under various federal, state and local environmental laws, ordinances and regulations, a current or previous real property owner or operator may be liable for the cost of removing or remediating hazardous or toxic substances on, under or in such property. These costs could be substantial. Such laws often impose liability whether or not the owner or operator knew of, or was responsible for, the presence of such hazardous or toxic substances. Environmental laws also may impose liens on property or restrictions on the manner in which property may be used or businesses may be operated, and these restrictions may require substantial expenditures or prevent OpCo from entering into leases with prospective subtenants that may be impacted by such laws. Environmental laws provide for sanctions for noncompliance and may be enforced by governmental agencies or, in certain circumstances, by private parties. Certain environmental laws and common law principles could be used to impose liability for the release of and exposure to hazardous substances, including asbestos-containing materials and lead-based paint. Third parties may seek recovery from real property owners or operators for personal injury or property damage associated with exposure to released hazardous substances and governments may seek recovery for natural resource damage. The costs of defending against claims of environmental liability, of complying with environmental regulatory requirements, of remediating any contaminated property, or of paying personal injury, property damage or natural resource damage claims could reduce the amounts available for distribution to you.

Uninsured losses relating to real property or excessively expensive premiums for insurance coverage could reduce the value of the Property and the distributions to be paid to the Company.

Certain losses, generally catastrophic in nature, such as losses due to wars, acts of terrorism, earthquakes, floods, hurricanes, pollution or environmental matters, are uninsurable or not economically insurable, or may be insured subject to limitations, such as large deductibles or co-payments. Insurance risks associated with potential acts of terrorism could sharply increase the premiums we pay for coverage against property and casualty claims. Additionally, mortgage lenders in some cases insist that commercial property owners purchase coverage against terrorism as a condition for providing mortgage loans. Such insurance policies may not be available at reasonable costs, if at all. OpCo may not maintain adequate coverage for such losses. If the Property incurs a casualty loss that is not fully insured, the value of the Property will be reduced by such uninsured loss, which could reduce the value of the Units and the distributions paid to holders of the Units. In addition, other than any working capital reserve or other reserves that may be established, no source of funding will exist to repair or reconstruct any uninsured damage.

Risks Related to Our Organization and Structure

Holders of the Units will not have the right to elect or remove the Manager and, unlike the holders of common shares in a corporation, will only have limited voting rights on matters affecting the Company’s business, and therefore limited ability to influence decisions regarding its business.

The Operating Agreement provides that the assets, affairs and business of the Company will be managed exclusively under the direction of the Manager. The Manager, which is controlled by Mr. Charles Follini, has the authority to make decisions on behalf of the Company and, in its capacity as the OpCo Manager, to make decisions on behalf of OpCo regarding (1) whether to issue additional units in either entity, (2) employment decisions, including the fees payable to the Manager and the OpCo Manager, and (3) whether to enter into material transactions with third parties, subject to the approval of the “independent representative,” as described under the heading “Contribution Agreement—Actions Requiring Representative Approval.” Investors do not have the right to elect or remove the Manager even if the Manager commits, among other things, fraud or other criminal misconduct, unless such conduct would be deemed to be a “disqualification event” under Regulation A. See “Contribution Agreement—Management of OpCo.” In addition, unlike the holders of common shares in a corporation, the holders of the Units have only limited voting rights on matters affecting the Company’s business, and therefore limited ability to influence decisions regarding its business.

Investors in the Units will have limited voting rights.

Holders of the Units will have voting rights only with respect to matters for which a vote is required under Delaware law, primarily relating to amendments to the Operating Agreement that would adversely change the rights of the Units and the liquidation of the Company.

Risks Related to Employee Benefit Plans and Individual Retirement Accounts

In some cases, if investors fail to meet the fiduciary and other standards under ERISA, the Internal Revenue Code of 1986, as amended, or common law as a result of an investment in the Units, investors could be subject to liability for losses as well as civil penalties.

There are special considerations that apply to investing in the Units on behalf of pension, profit sharing or 401(k) plans, health or welfare plans, individual retirement accounts or Keogh plans. If an investor is making an investment of the assets of any of the entities identified in the prior sentence in the Units, the investor should satisfy itself that:

| ● | the investment is consistent with your fiduciary obligations under applicable law, including common law, ERISA and the Internal Revenue Code of 1986, as amended (the “Code”); |

| ● | the investment is made in accordance with the documents and instruments governing the trust, plan or IRA, including a plan’s investment policy; |

| ● | the investment satisfies the prudence and diversification requirements of Sections 404(a)(1)(B) and 404(a)(1)(C) of ERISA, if applicable, and other applicable provisions of ERISA and the Code; |

| ● | the investment will not impair the liquidity of the trust, plan or IRA; |

| ● | the investment will not produce “unrelated business taxable income” for the plan or IRA; |

| ● | it will be able to value the assets of the plan annually in accordance with ERISA requirements and applicable provisions of the applicable trust, plan or IRA document; and |

| ● | the investment will not constitute a prohibited transaction under Section 406 of ERISA or Section 4975 of the Code. |

Failure to satisfy the fiduciary standards of conduct and other applicable requirements of ERISA, the Code, or other applicable statutory or common law may result in the imposition of civil penalties, and can subject the fiduciary to liability for any resulting losses as well as equitable remedies. In addition, if an investment in the Units constitutes a prohibited transaction under the Code, the “disqualified person” that engaged in the transaction may be subject to the imposition of excise taxes with respect to the amount invested.

Risks Related to this Offering

If there is no active secondary market for the Units, you may have to hold your investment for an indefinite period.

The LEX Markets Platform intends to create a secondary market for the Units, but the LEX Markets Platform must first be approved by FINRA and the SEC and, even if approved, must attract sufficient liquidity for secondary trading to be possible. There can be no assurance that the LEX Markets Platform will achieve these objectives. There is currently no secondary market for the Units, and no secondary market may be established or, if established, maintained. If there is no active secondary market for the Units, investors may not be able to liquidate their investment. The Company is not obligated to redeem or liquidate the Units.

The requirements of complying on an ongoing basis with Regulation A of the Securities Act may strain our resources and divert management’s attention.

Because we are conducting an offering pursuant to Regulation A of the Securities Act, we will be subject to certain ongoing reporting requirements. Compliance with these rules and regulations may increase our legal and financial compliance costs, make some activities more difficult, time-consuming or costly and increase demand on our resources. The requirements of Regulation A may also make it more expensive for us to obtain manager liability insurance and we may be required to accept reduced coverage or incur substantially higher costs to obtain coverage. Moreover, as a result of the disclosure of information in this offering circular and in other public filings we make, our business operations, operating results and financial condition will become more visible, including to competitors and other third parties.

If we become subject to regulations governing investment companies, broker-dealers or investment advisers, our ability to conduct business could be adversely affected.

The SEC regulates to a substantial degree the manner in which “investment companies,” “broker-dealers” and “investment advisers” are permitted to conduct their business activities. We believe we will conduct our business in a manner that does not make us an investment company, broker-dealer or investment adviser, and we intend to continue to conduct our business to avoid any such characterizations. If, however, we are deemed to be an investment company, broker-dealer or investment adviser, we may be required to institute burdensome compliance requirements and our activities may be restricted, which would adversely affect our business and our ability to pay distributions to holders of the Units.

No market or other independent valuation of the Company or any of our equity capital has been used to set the public offering price of the Units.

The public offering price of the Units has been determined solely by us, based on a number of factors, some of which bear no relation to established, formal valuation criteria such as assets, earnings, net worth or book value. We make no representations, whether express or implied, as to the value of the Units and there can be no assurance that the offering price of the Units represents the fair value thereof.

The projections contained in this offering circular should be considered speculative and no assurance can be given as to their accuracy.

The projections included in this offering statement should be considered speculative and are qualified in their entirety by the assumptions, information and risks disclosed in this offering statement. The assumptions and facts upon which the projections are based are subject to variations that may arise as future events actually occur. No representation or warranty can be given that the projections made herein will prove to be accurate. There is no assurance that actual events will correspond with the assumptions. Potential investors are advised to consult with their tax and business advisors concerning the validity and reasonableness of the factual and accounting assumptions. Neither the Manager nor any other person or entity makes any representation or warranty as to the future profitability of the Issuers.

No advisor to the Issuers has compiled, examined or applied agreed-upon procedures to the projections or assessed the assumptions on which they are based or expressed any opinion or any form of assurance with respect thereto. The projections were based upon management’s judgments utilizing a number of internal sources, including historical financial information, annual plans, strategic plans and other business plans and include various estimates and assumptions that are inherently subject to significant political, economic, business and competitive uncertainties, contingencies and risks, all of which are difficult to quantify and many of which are beyond the control of the Issuers.

Changes in the assumptions underlying the projections or changes in the economic, political, legal or other conditions affecting investments in the real estate industry or the economy as a whole, including, without limitation: (i) the uncertainty surrounding the social and economic impact of the current COVID-19 pandemic; (ii) the competitive environment in which the Issuers operate; (iii) the potential of natural disasters such as earthquakes, floods and wild fires; (iv) potential changes in the laws or governmental regulations that affect us; (v) financing risks, including the risk that OpCo will not be able to make its debt service payments; and (vi) the lack of or insufficient amount of insurance, could materially and adversely affect the OpCo’s actual results. Accordingly, OpCo’s future financial performance may vary from the projections, possibly by material amounts. Although the projected financial information has been prepared in good faith and is based upon assumptions believed by the management to be reasonable, the projections should not be regarded as a representation by any person that these results will be achieved. Accordingly, the projections reflect the Issuers’ judgment of the expected conditions and its expected course of action through 2025. The assumptions are those that the Issuers believe are significant to the projections. However, some assumptions may not materialize and unanticipated events and circumstances may occur; therefore, the actual results achieved during the forecast period may vary from the projections and the variations may be material.

Risks Related to Tax Considerations

In addition to reading the following risk factors, you should read “Material U.S. Federal Income Tax Consequences” for a full discussion of the expected material U.S. federal income tax consequences of owning and disposing of Units.

Our tax treatment depends on each Issuer’s status as a partnership for U.S. federal income tax purposes, as well as our not being subject to entity-level taxation by individual states. If the IRS treats either Issuer as a corporation or it becomes subject to entity-level taxation, it would reduce the amount of cash available for distribution to you.

The after-tax economic benefit of an investment in the Units depends largely on each Issuer being treated as a partnership for U.S. federal income tax purposes. We have not requested, and do not plan to request, a ruling from the IRS on this or any other tax matter affecting us.

If either Issuer were treated as a corporation for U.S. federal income tax purposes, it would pay tax on its income at the corporate tax rate (which, at the federal level, is currently 21%). If Gateway were treated as a corporation, distributions to you would generally be taxed again as corporate distributions, and no income, gains, losses or deductions would flow through to you. Because a tax would be imposed on Gateway as a corporation, its cash available for distribution to you would be substantially reduced. Therefore, its treatment as a corporation would result in a material reduction in the after-tax return to the unitholders, likely causing a substantial reduction in the value of the Units.

Current law may change so as to cause either Issuer to be treated as a corporation for U.S. federal income tax purposes or otherwise subject us to entity-level taxation. In addition, because of widespread state budget deficits, several states are evaluating ways to subject partnerships to entity-level taxation through the imposition of state income, franchise and other forms of taxation. If any of these states were to impose a tax on us, the cash available for distribution to you would be reduced.

Holders of Units will receive partner information tax returns on Schedule K-1, which could increase the complexity of tax returns.

As members of a limited liability company that will elect to be taxed as a partnership, the holders of Units will receive annual Schedule K-1s following the end of each taxable year. The partner information tax returns on Schedule K-1 will contain information regarding the income items and expense items of Company and will allocate a portion of those items to you based on your percentage ownership in the Company. The preparation of annual tax returns for owners of real estate involve a complex series of calculations, and as a result, your Schedule K-1 may be more complicated that others you may have received. Additionally, if you have not received Schedule K-1s from other investments, you may find that preparing your tax return may require additional time, or it may be necessary for you to retain an accountant or other tax preparer, at an additional expense to you, to assist you in the preparation of your return.

A successful IRS contest of the U.S. federal income tax positions we take may adversely affect the market for the Units, and the cost of any IRS contest will be borne by the unitholders.

Neither Issuer has requested a ruling from the IRS with respect to its treatment as a partnership for U.S. federal income tax purposes or any other matter affecting it. The IRS may adopt positions that differ from the positions we take. It may be necessary to resort to administrative or court proceedings to sustain some or all of the positions we take. A court may not agree with all of the positions we take. Any contest with the IRS may materially and adversely impact the market for the Units and the price at which they trade. In addition, the costs of any contest with the IRS will be borne indirectly by the unitholders because the costs will reduce cash available for distribution.

You may be required to pay taxes on income from the Company even if you do not receive any cash distributions from the Company.

You will be required to pay any U.S. federal income taxes and, in some cases, state and local income taxes on your share of the Company’s taxable income even if you receive no cash distributions from it. Although the Operating Agreement and the OpCo operating agreement require OpCo us to pay certain tax-related distributions, you may not receive sufficient cash distributions from Gateway equal to your share of its taxable income or even the tax liability that results from that income.

Tax gain or loss on a disposition of Units could be more or less than expected.

If you sell your Units, you will recognize a gain or loss equal to the difference between the amount realized and your tax basis in those Units. A substantial portion of the amount realized, whether or not representing gain, may be ordinary income. In addition, if you sell your Units, you may incur a tax liability in excess of the amount of cash you receive from the sale.

Tax-exempt entities and regulated investment companies face unique tax issues from owning Units that may result in adverse tax consequences to them.

Investments in Units by tax-exempt entities, such as individual retirement accounts (known as IRAs), and regulated investment companies (known as mutual funds) raise issues unique to them. For example, some of Gateway’s income allocated to organizations that are exempt from federal income tax, including individual retirement accounts and other retirement plans, may be unrelated business taxable income and may be taxable to them. It is not anticipated that any significant amount of Gateway’s gross income will be qualifying income to a regulated investment company. If you are a tax-exempt entity or a regulated investment company, you should consult your tax advisor before investing in the Units.

The Company will treat each purchaser of Units as having the same tax benefits without regard to the actual Units purchased. The IRS may challenge this treatment, which could adversely affect the value of the Units.

Because, among other reasons, the Company cannot match transferors and transferees of Units, it will take depreciation and amortization positions that may not conform to all aspects of the Treasury Regulations. A successful IRS challenge to those positions could adversely affect the amount of tax benefit available to you. It also could affect the timing of these tax benefits or the amount of gain from the sale of Units and could have a negative impact on the value of the Units or result in audit adjustments to your tax returns.

USE OF PROCEEDS

We are offering a minimum of $650,000 of Units and a maximum of $1,000,000 of Units. This offering is being made on a “best efforts” basis which means that no one is committed to purchasing any Units in this offering. Accordingly, no assurance can be given as to the amount of Units sold in this offering. OpCo has agreed to pay the Placement Agents a placement fee equal to 4% of the gross proceeds of the Units sold in this offering. The Placement Agents have agreed to pay the expenses of this offering, other than the placement fee payable to the Placement Agents, up to the extent of the 4% placement fee received. LEX Markets LLC is responsible for any expenses in excess of the total placement fee. We are not obligated to reimburse the Placement Agents for such expenses. As a result, this is a “no load” offering, and the investors will not be required to pay any organization or offering expenses. The Company will contribute 100% of the gross proceeds of this offering to OpCo to acquire the Interest.

The amount paid by us for the Interest will be used for capital expenditures and reimbursement for capital expenses already completed at the Property as follows:

| Description | | Amount | |

| Facade Replacement | | $ | 300,000 | |

| Reimbursement Capex | | $ | 700,000 | |

DISTRIBUTION POLICY