Exhibit 99.1 Analyst Day Presentation March 2021Exhibit 99.1 Analyst Day Presentation March 2021

Legal Disclaimer This presentation contains proprietary and confidential information regarding A Place for Rover, Inc. (“Rover”) and Nebula Caravel Acquisition Corporation (“NCAC”) and is being provided to assist interested parties in making their own evaluation with respect to a potential business combination between Rover and NCAC and related transactions (the “Potential Business Combination”) and for no other purpose. By reviewing or reading this presentation, you will be deemed to have agreed to the obligations and restrictions set out below. Without the express prior written consent of Rover and NCAC, this presentation and any information contained within it may not be (1) reproduced (in whole or in part), (2) copied at any time, or (3) used for any purpose other than your evaluation of Rover. This presentation supersedes and replaces all previous oral or written communications between the parties hereto relating to the subject matter hereof. This presentation and any oral statements made in connection with this presentation do not constitute an offer or invitation or solicitation of any offer to sell or purchase any securities, or the solicitation of any vote, consent or approval in any jurisdiction in connection with the Potential Business Combination or any related transactions, nor shall there be any sale, issuance or transfer of any securities in any jurisdiction where, or to any person to whom, such offer, solicitation or sale may be unlawful under the laws of such jurisdiction. This presentation does not constitute either advice or a recommendation regarding any securities. Any offer to sell securities will be made only pursuant to a definitive Subscription Agreement and will be made in reliance on an exemption from registration under the Securities Act of 1933, as amended, for offers and sales of securities that do not involve a public offering. NCAC and Rover reserve the right to withdraw or amend for any reason any offering and to reject any Subscription Agreement for any reason. The communication of this presentation is restricted by law; it is not intended for distribution to, or use by any person in, any jurisdiction where such distribution or use would be contrary to local law or regulation. No representations or warranties, express or implied are given in, or in respect of, this presentation. To the fullest extent permitted by law, in no circumstances will Rover, NCAC or any of their respective subsidiaries, stockholders, affiliates, representatives, partners, directors, officers, employees, advisers or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of this presentation, its contents, its omissions, reliance on the information contained within it, or on opinions communicated in relation thereto or otherwise arising in connection therewith. Recipients of this presentation are not to construe its contents, or any prior or subsequent communications from or with NCAC, Rover or their respective representatives as investment, legal or tax advice. In addition, this presentation does not purport to be all-inclusive or to contain all of the information that may be required to make a full analysis of Rover or the Potential Business Combination. Recipients of this presentation should each make their own evaluation of Rover and of the relevance and adequacy of the information and should make such other investigations as they deem necessary. Forward-Looking Statements Information in this presentation represents current expectations relating to transaction structure and is subject to further discussion and negotiation of definitive documentation in its entirety. All statements in this presentation other than statements of historical fact, including, but not limited to, statements regarding Rover’s future operating results, financial position, business strategy, addressable market, anticipated benefits of its technologies, and plans and objectives for future operations and offerings are “forward-looking statements” and can often be identified by the use of terminology such as “may,” “will,” “estimate,” “intend,” “continue,” “believe,” “expect,” “anticipate,” “should,” “could,” “potential,” “projection,” “forecast,” “plan,” “trend,” “assumption,” “opportunity,” “predict,” “seek,” “target,” or similar terminology, although not all forward-looking statements contain these identifying terms. These forward-looking statements include, but are not limited to, statements regarding estimates and forecasts of other financial and performance metrics, projections of market opportunity and market share, expectations and timing related to commercial product launches, potential benefits of the transaction and the potential success of Rover’s strategy, and expectations related to the terms and timing of the transaction. These forward-looking statements are based upon Rover management’s current expectations, assumptions and estimates as of the date of this presentation and are not guarantees of future results or the timing thereof. These forward-looking statements are provided for illustrative purposes only and are not intended to serve, and must not be relied on by any investor, as a guarantee, assurance, prediction or definitive statement of fact or probability. Actual results may differ materially from those contemplated in these statements due to a variety of risks and uncertainties, including, but not limited to, risks and uncertainties related to the inability of the parties to successfully or timely consummate the Potential Business Combination, including the risk that any required regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect the combined company or the expected benefits of the Potential Business Combination is not obtained, failure to realize the anticipated benefits of the Potential Business Combination, risks related to Rover’s ability to execute on its business strategy, attract and retain users, develop new offerings, enhance existing offerings, compete effectively, and manage growth and costs, the duration and global impact of COVID-19, the number of redemption requests made by NCAC’s public stockholders and the ability of NCAC’s or the combined company to issue equity or equity-linked securities in connection with the proposed business combination or in the future; and those factors discussed in documents of NCAC filed, or to be filed, with SEC. If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that neither NCAC nor Rover presently know or that NCAC and Rover currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect NCAC’s and Rover’s expectations, plans or forecasts of future events and views as of the date of this presentation. NCAC and Rover anticipate that subsequent events and developments will cause NCAC’s and Rover’s assessments to change. The information contained herein is provided only as of the date on which this presentation is made and is subject to change. However, while Rover and NCAC may elect to update these forward-looking statements in the future, each of Rover and NCAC is not under any obligation, and expressly disclaims any duty, to update or otherwise revise the information after the date of presentation, whether as a result of new information, new developments or otherwise. These forward-looking statements should not be relied upon as representing NCAC’s and Rover’s assessments as of any date subsequent to the date of this presentation. Accordingly, you should not place undue reliance on the forward-looking statements. Rover and NCAC have not independently verified the statistical and other industry data generated by independent parties and contained in this presentation and accordingly cannot guarantee their accuracy or completeness. Use of Data The data contained herein is derived from various internal and third-party industry publications and sources as well as from research reports prepared for other purposes. Neither NCAC nor Rover has independently verified the data obtained from these sources and cannot assure you of the data’s accuracy or completeness. This data is subject to change. No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any projections or modeling or any other information contained herein. Any data on past performance or modeling contained herein is not an indication as to future performance. Rover and NCAC assume no obligation to update the information in this presentation. 2Legal Disclaimer This presentation contains proprietary and confidential information regarding A Place for Rover, Inc. (“Rover”) and Nebula Caravel Acquisition Corporation (“NCAC”) and is being provided to assist interested parties in making their own evaluation with respect to a potential business combination between Rover and NCAC and related transactions (the “Potential Business Combination”) and for no other purpose. By reviewing or reading this presentation, you will be deemed to have agreed to the obligations and restrictions set out below. Without the express prior written consent of Rover and NCAC, this presentation and any information contained within it may not be (1) reproduced (in whole or in part), (2) copied at any time, or (3) used for any purpose other than your evaluation of Rover. This presentation supersedes and replaces all previous oral or written communications between the parties hereto relating to the subject matter hereof. This presentation and any oral statements made in connection with this presentation do not constitute an offer or invitation or solicitation of any offer to sell or purchase any securities, or the solicitation of any vote, consent or approval in any jurisdiction in connection with the Potential Business Combination or any related transactions, nor shall there be any sale, issuance or transfer of any securities in any jurisdiction where, or to any person to whom, such offer, solicitation or sale may be unlawful under the laws of such jurisdiction. This presentation does not constitute either advice or a recommendation regarding any securities. Any offer to sell securities will be made only pursuant to a definitive Subscription Agreement and will be made in reliance on an exemption from registration under the Securities Act of 1933, as amended, for offers and sales of securities that do not involve a public offering. NCAC and Rover reserve the right to withdraw or amend for any reason any offering and to reject any Subscription Agreement for any reason. The communication of this presentation is restricted by law; it is not intended for distribution to, or use by any person in, any jurisdiction where such distribution or use would be contrary to local law or regulation. No representations or warranties, express or implied are given in, or in respect of, this presentation. To the fullest extent permitted by law, in no circumstances will Rover, NCAC or any of their respective subsidiaries, stockholders, affiliates, representatives, partners, directors, officers, employees, advisers or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of this presentation, its contents, its omissions, reliance on the information contained within it, or on opinions communicated in relation thereto or otherwise arising in connection therewith. Recipients of this presentation are not to construe its contents, or any prior or subsequent communications from or with NCAC, Rover or their respective representatives as investment, legal or tax advice. In addition, this presentation does not purport to be all-inclusive or to contain all of the information that may be required to make a full analysis of Rover or the Potential Business Combination. Recipients of this presentation should each make their own evaluation of Rover and of the relevance and adequacy of the information and should make such other investigations as they deem necessary. Forward-Looking Statements Information in this presentation represents current expectations relating to transaction structure and is subject to further discussion and negotiation of definitive documentation in its entirety. All statements in this presentation other than statements of historical fact, including, but not limited to, statements regarding Rover’s future operating results, financial position, business strategy, addressable market, anticipated benefits of its technologies, and plans and objectives for future operations and offerings are “forward-looking statements” and can often be identified by the use of terminology such as “may,” “will,” “estimate,” “intend,” “continue,” “believe,” “expect,” “anticipate,” “should,” “could,” “potential,” “projection,” “forecast,” “plan,” “trend,” “assumption,” “opportunity,” “predict,” “seek,” “target,” or similar terminology, although not all forward-looking statements contain these identifying terms. These forward-looking statements include, but are not limited to, statements regarding estimates and forecasts of other financial and performance metrics, projections of market opportunity and market share, expectations and timing related to commercial product launches, potential benefits of the transaction and the potential success of Rover’s strategy, and expectations related to the terms and timing of the transaction. These forward-looking statements are based upon Rover management’s current expectations, assumptions and estimates as of the date of this presentation and are not guarantees of future results or the timing thereof. These forward-looking statements are provided for illustrative purposes only and are not intended to serve, and must not be relied on by any investor, as a guarantee, assurance, prediction or definitive statement of fact or probability. Actual results may differ materially from those contemplated in these statements due to a variety of risks and uncertainties, including, but not limited to, risks and uncertainties related to the inability of the parties to successfully or timely consummate the Potential Business Combination, including the risk that any required regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect the combined company or the expected benefits of the Potential Business Combination is not obtained, failure to realize the anticipated benefits of the Potential Business Combination, risks related to Rover’s ability to execute on its business strategy, attract and retain users, develop new offerings, enhance existing offerings, compete effectively, and manage growth and costs, the duration and global impact of COVID-19, the number of redemption requests made by NCAC’s public stockholders and the ability of NCAC’s or the combined company to issue equity or equity-linked securities in connection with the proposed business combination or in the future; and those factors discussed in documents of NCAC filed, or to be filed, with SEC. If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that neither NCAC nor Rover presently know or that NCAC and Rover currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect NCAC’s and Rover’s expectations, plans or forecasts of future events and views as of the date of this presentation. NCAC and Rover anticipate that subsequent events and developments will cause NCAC’s and Rover’s assessments to change. The information contained herein is provided only as of the date on which this presentation is made and is subject to change. However, while Rover and NCAC may elect to update these forward-looking statements in the future, each of Rover and NCAC is not under any obligation, and expressly disclaims any duty, to update or otherwise revise the information after the date of presentation, whether as a result of new information, new developments or otherwise. These forward-looking statements should not be relied upon as representing NCAC’s and Rover’s assessments as of any date subsequent to the date of this presentation. Accordingly, you should not place undue reliance on the forward-looking statements. Rover and NCAC have not independently verified the statistical and other industry data generated by independent parties and contained in this presentation and accordingly cannot guarantee their accuracy or completeness. Use of Data The data contained herein is derived from various internal and third-party industry publications and sources as well as from research reports prepared for other purposes. Neither NCAC nor Rover has independently verified the data obtained from these sources and cannot assure you of the data’s accuracy or completeness. This data is subject to change. No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any projections or modeling or any other information contained herein. Any data on past performance or modeling contained herein is not an indication as to future performance. Rover and NCAC assume no obligation to update the information in this presentation. 2

Legal Disclaimer Trademarks Rover and NCAC own or have rights to various trademarks, service marks and trade names that they use in connection with the operation of their respective businesses. This presentation may also contain trademarks, service marks, trade names and copyrights of third parties, which are the property of their respective owners. The use or display of third parties’ trademarks, service marks, trade names or products in this presentation is not intended to, and does not imply, a relationship with Rover or NCAC, or an endorsement or sponsorship by or of Rover or NCAC. Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in this presentation may appear without the TM, SM, ® or © symbols, but such references are not intended to indicate, in any way, that Rover or NCAC will not assert, to the fullest extent under applicable law, their rights or the right of the applicable licensor to these trademarks, service marks, trade names and copyrights. Use of Projections The projections, estimates and targets in this presentation are forward-looking statements that are based on assumptions that are inherently subject to significant uncertainties and contingencies, many of which are beyond Rover and NCAC’s control. Such projections, estimates and targets are included for illustrative purposes only and should not be relied upon as necessarily being indicative of future results. While all projections, estimates and targets are necessarily speculative, Rover and NCAC believe that the preparation of prospective financial information involves increasingly higher levels of uncertainty the further out the projection, estimate or target extends from the date of preparation. The assumptions and estimates underlying the projected, expected or target results are inherently uncertain and are subject to a wide variety of significant business, economic, regulatory and competitive risks and uncertainties that could cause actual results to differ materially from those contained in such projections, estimates and targets. The inclusion of projections, estimates and targets in this presentation should not be regarded as an indication Rover and NCAC, or their representatives, considered or consider the financial projections, estimates and targets to be a reliable prediction of future events. The independent auditors of NCAC and of Rover did not audit, review, compile or perform any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation. Financial Information; Non-GAAP Financial Measures Rover is in the process of finalizing its financial results for the fourth quarter and fiscal year 2020, and therefore its finalized and audited results and final analysis of those results are not yet available. The preliminary expectations regarding fourth quarter and full year 2020 are the responsibility of Rover management, are subject to management’s review and actual results could differ from management’s expectations. The actual results are also subject to audit by Rover’s independent registered public accounting firm and no assurance is given by its independent registered public accounting firm on such preliminary expectations. You should not draw any conclusions as to any other financial results as of and for the year ended December 31, 2020 based on the foregoing estimates. The financial information and data for the year ended December 31, 2020 are unaudited and does not conform to Regulation S-X. Accordingly, such information and data may not be included in, may be adjusted in or may be presented differently in, any proxy statement or registration statement to be filed by NCAC or Rover with the SEC. Some of the financial information and data contained in this presentation, such as Adjusted EBITDA and Adjusted EBITDA margin, have not been prepared in accordance with United States generally accepted accounting principles (“GAAP”). Adjusted EBITDA is defined as net loss adjusted for interest and taxes, depreciation and amortization, other income or expenses, stock-based compensation, restructuring costs, and M&A integration costs. Adjusted EBITDA margin is defined as Adjusted EBITDA divided by revenue. Adjusted EBITDA has been included in this presentation because it is a key measure used by Rover management and board of directors to evaluate its operating performance, generate future operating plans and make strategic decisions regarding the allocation of capital. In particular, the exclusion of certain expenses in calculating Adjusted EBITDA facilitates operating performance comparisons on a period-to-period basis and, in the case of exclusion of the impact of equity-based compensation and M&A expenses, excludes items that Rover does not consider to be indicative of its core operating performance. Accordingly, Rover and NCAC believe that the use of these non-GAAP financial measures provide useful information to investors and others in understanding and evaluating Rover’s operating results in the same manner as its management and board of directors. Non-GAAP financial measures have limitations as an analytical tool, and you should not consider them in isolation or as a substitute for analysis of our results as reported under GAAP. For example, other companies may calculate non-GAAP measures differently, or may use other measures to calculate their financial performance, and therefore Rover’s non-GAAP measures may not be directly comparable to similarly titled measures of other companies. The principal limitation of these non-GAAP financial measures is that they exclude significant expenses and income that are required by GAAP to be recorded in Rover’s financial statements. In addition, they are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. In order to compensate for these limitations, management presents non-GAAP financial measures in connection with GAAP results. A reconciliation of the non-GAAP financial measures to the corresponding GAAP measures is included in the supplemental materials at the end of the presentation. A reconciliation forward-looking non-GAAP financial measures has not been provided because the various reconciling items are difficult to predict and subject to constant change. Important Information for Investors and Stockholders NCAC and Rover and their respective directors and executive officers and other members of management and employees, under SEC rules, may be deemed to be participants in the solicitation of proxies of NCAC stockholders in connection with the Potential Business Combination. Investors and security holders may obtain more detailed information regarding the names and interests in the Potential Business Combination of NCAC’s directors and officers in NCAC’s filings with the SEC, including NCAC’s registration statement on Form S-1, which was originally filed with the SEC on September 4, 2020. To the extent that holdings of NCAC’s securities have changed from the amounts reported in NCAC’s registration statement on Form S-1, such changes have been or will be reflected on Statements of Change in Ownership on Form 4 filed with the SEC. Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of proxies to NCAC’s stockholders in connection with the Potential Business Combination will be set forth in the proxy statement/prospectus on Form S-4 for the Potential Business Combination, which is expected to be filed by NCAC with the SEC. This presentation is not a substitute for the registration statement or for any other document that NCAC may file with the SEC in connection with the Potential Business Combination. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain free copies of other documents filed with the SEC by NCAC through the website maintained by the SEC at http://www.sec.gov. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. 3Legal Disclaimer Trademarks Rover and NCAC own or have rights to various trademarks, service marks and trade names that they use in connection with the operation of their respective businesses. This presentation may also contain trademarks, service marks, trade names and copyrights of third parties, which are the property of their respective owners. The use or display of third parties’ trademarks, service marks, trade names or products in this presentation is not intended to, and does not imply, a relationship with Rover or NCAC, or an endorsement or sponsorship by or of Rover or NCAC. Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in this presentation may appear without the TM, SM, ® or © symbols, but such references are not intended to indicate, in any way, that Rover or NCAC will not assert, to the fullest extent under applicable law, their rights or the right of the applicable licensor to these trademarks, service marks, trade names and copyrights. Use of Projections The projections, estimates and targets in this presentation are forward-looking statements that are based on assumptions that are inherently subject to significant uncertainties and contingencies, many of which are beyond Rover and NCAC’s control. Such projections, estimates and targets are included for illustrative purposes only and should not be relied upon as necessarily being indicative of future results. While all projections, estimates and targets are necessarily speculative, Rover and NCAC believe that the preparation of prospective financial information involves increasingly higher levels of uncertainty the further out the projection, estimate or target extends from the date of preparation. The assumptions and estimates underlying the projected, expected or target results are inherently uncertain and are subject to a wide variety of significant business, economic, regulatory and competitive risks and uncertainties that could cause actual results to differ materially from those contained in such projections, estimates and targets. The inclusion of projections, estimates and targets in this presentation should not be regarded as an indication Rover and NCAC, or their representatives, considered or consider the financial projections, estimates and targets to be a reliable prediction of future events. The independent auditors of NCAC and of Rover did not audit, review, compile or perform any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation. Financial Information; Non-GAAP Financial Measures Rover is in the process of finalizing its financial results for the fourth quarter and fiscal year 2020, and therefore its finalized and audited results and final analysis of those results are not yet available. The preliminary expectations regarding fourth quarter and full year 2020 are the responsibility of Rover management, are subject to management’s review and actual results could differ from management’s expectations. The actual results are also subject to audit by Rover’s independent registered public accounting firm and no assurance is given by its independent registered public accounting firm on such preliminary expectations. You should not draw any conclusions as to any other financial results as of and for the year ended December 31, 2020 based on the foregoing estimates. The financial information and data for the year ended December 31, 2020 are unaudited and does not conform to Regulation S-X. Accordingly, such information and data may not be included in, may be adjusted in or may be presented differently in, any proxy statement or registration statement to be filed by NCAC or Rover with the SEC. Some of the financial information and data contained in this presentation, such as Adjusted EBITDA and Adjusted EBITDA margin, have not been prepared in accordance with United States generally accepted accounting principles (“GAAP”). Adjusted EBITDA is defined as net loss adjusted for interest and taxes, depreciation and amortization, other income or expenses, stock-based compensation, restructuring costs, and M&A integration costs. Adjusted EBITDA margin is defined as Adjusted EBITDA divided by revenue. Adjusted EBITDA has been included in this presentation because it is a key measure used by Rover management and board of directors to evaluate its operating performance, generate future operating plans and make strategic decisions regarding the allocation of capital. In particular, the exclusion of certain expenses in calculating Adjusted EBITDA facilitates operating performance comparisons on a period-to-period basis and, in the case of exclusion of the impact of equity-based compensation and M&A expenses, excludes items that Rover does not consider to be indicative of its core operating performance. Accordingly, Rover and NCAC believe that the use of these non-GAAP financial measures provide useful information to investors and others in understanding and evaluating Rover’s operating results in the same manner as its management and board of directors. Non-GAAP financial measures have limitations as an analytical tool, and you should not consider them in isolation or as a substitute for analysis of our results as reported under GAAP. For example, other companies may calculate non-GAAP measures differently, or may use other measures to calculate their financial performance, and therefore Rover’s non-GAAP measures may not be directly comparable to similarly titled measures of other companies. The principal limitation of these non-GAAP financial measures is that they exclude significant expenses and income that are required by GAAP to be recorded in Rover’s financial statements. In addition, they are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. In order to compensate for these limitations, management presents non-GAAP financial measures in connection with GAAP results. A reconciliation of the non-GAAP financial measures to the corresponding GAAP measures is included in the supplemental materials at the end of the presentation. A reconciliation forward-looking non-GAAP financial measures has not been provided because the various reconciling items are difficult to predict and subject to constant change. Important Information for Investors and Stockholders NCAC and Rover and their respective directors and executive officers and other members of management and employees, under SEC rules, may be deemed to be participants in the solicitation of proxies of NCAC stockholders in connection with the Potential Business Combination. Investors and security holders may obtain more detailed information regarding the names and interests in the Potential Business Combination of NCAC’s directors and officers in NCAC’s filings with the SEC, including NCAC’s registration statement on Form S-1, which was originally filed with the SEC on September 4, 2020. To the extent that holdings of NCAC’s securities have changed from the amounts reported in NCAC’s registration statement on Form S-1, such changes have been or will be reflected on Statements of Change in Ownership on Form 4 filed with the SEC. Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of proxies to NCAC’s stockholders in connection with the Potential Business Combination will be set forth in the proxy statement/prospectus on Form S-4 for the Potential Business Combination, which is expected to be filed by NCAC with the SEC. This presentation is not a substitute for the registration statement or for any other document that NCAC may file with the SEC in connection with the Potential Business Combination. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain free copies of other documents filed with the SEC by NCAC through the website maintained by the SEC at http://www.sec.gov. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. 3

Team and Presenters • Co-Founder and CEO of Rover • GeekWire’s 2016 CEO of the Year and a 2014 EY Entrepreneur of the Year Award winner for the Pacific Northwest Aaron Easterly Co-Founder and CEO, Rover• Previously general manager at Microsoft, where he managed advertiser marketplaces worth $3 billion • CFO of Rover Tracy Knox • Previously CFO for A Place for Mom, UIEvolution, Drugstore.com, and CFO, Rover Rightside • COO of Rover Brent Turner • Previously President of Code Fellows, a digital trade school in Seattle COO, Rover • Former Executive Vice President at aQuantive • Founding Partner of True Wind Capital Adam Clammer • Former Founder and Head of KKR Global Technology Group Founding Partner, True Wind Capital • Boards include LPRO, AVGO, GDDY, NXPI, JAZZ, AEPI, and many private companies • Previously served as an investment professional at Google Capital where Brandon Van Buren he focused on growth stage technology investments Partner, True Wind Capital • Prior to joining Google Capital, worked as an investment professional at KKR 4Team and Presenters • Co-Founder and CEO of Rover • GeekWire’s 2016 CEO of the Year and a 2014 EY Entrepreneur of the Year Award winner for the Pacific Northwest Aaron Easterly Co-Founder and CEO, Rover• Previously general manager at Microsoft, where he managed advertiser marketplaces worth $3 billion • CFO of Rover Tracy Knox • Previously CFO for A Place for Mom, UIEvolution, Drugstore.com, and CFO, Rover Rightside • COO of Rover Brent Turner • Previously President of Code Fellows, a digital trade school in Seattle COO, Rover • Former Executive Vice President at aQuantive • Founding Partner of True Wind Capital Adam Clammer • Former Founder and Head of KKR Global Technology Group Founding Partner, True Wind Capital • Boards include LPRO, AVGO, GDDY, NXPI, JAZZ, AEPI, and many private companies • Previously served as an investment professional at Google Capital where Brandon Van Buren he focused on growth stage technology investments Partner, True Wind Capital • Prior to joining Google Capital, worked as an investment professional at KKR 4

True Wind Capital Investment Highlights - Why We Are Excited • Rover is the world's largest online marketplace for pet care (~10x relative market share) in a massive and growing market • Offline to online shift within pet services is in early innings • Rover benefitting from the confluence of major secular tailwinds; pet ownership and travel recovery • Differentiated marketplace with an attractive economic model • World-class management team • Attractive valuation 5True Wind Capital Investment Highlights - Why We Are Excited • Rover is the world's largest online marketplace for pet care (~10x relative market share) in a massive and growing market • Offline to online shift within pet services is in early innings • Rover benefitting from the confluence of major secular tailwinds; pet ownership and travel recovery • Differentiated marketplace with an attractive economic model • World-class management team • Attractive valuation 5

Table of Contents 1. Business Overview 2. Investment Highlights 3. Financial Overview 4. Transaction Overview 5. Appendix 6Table of Contents 1. Business Overview 2. Investment Highlights 3. Financial Overview 4. Transaction Overview 5. Appendix 6

We believe that everyone deserves to experience the unconditional love of pets, and exists to make that possible. 7We believe that everyone deserves to experience the unconditional love of pets, and exists to make that possible. 7

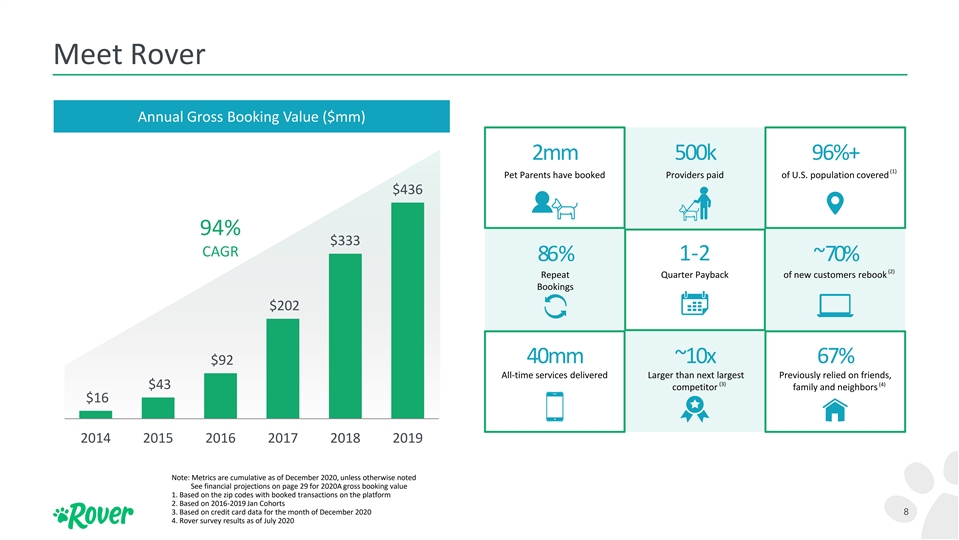

Meet Rover Annual Gross Booking Value ($mm) 2mm 500k 96%+ (1) Pet Parents have booked Providers paid of U.S. population covered $436 94% $333 CAGR 86 % 1-2 ~ 70% (2) Repeat Quarter Payback of new customers rebook Bookings $202 40mm ~10x 67% $92 All-time services delivered Larger than next largest Previously relied on friends, (3) (4) $43 competitor family and neighbors $16 2014 2015 2016 2017 2018 2019 Note: Metrics are cumulative as of December 2020, unless otherwise noted See financial projections on page 29 for 2020A gross booking value 1. Based on the zip codes with booked transactions on the platform 2. Based on 2016-2019 Jan Cohorts 3. Based on credit card data for the month of December 2020 8 4. Rover survey results as of July 2020Meet Rover Annual Gross Booking Value ($mm) 2mm 500k 96%+ (1) Pet Parents have booked Providers paid of U.S. population covered $436 94% $333 CAGR 86 % 1-2 ~ 70% (2) Repeat Quarter Payback of new customers rebook Bookings $202 40mm ~10x 67% $92 All-time services delivered Larger than next largest Previously relied on friends, (3) (4) $43 competitor family and neighbors $16 2014 2015 2016 2017 2018 2019 Note: Metrics are cumulative as of December 2020, unless otherwise noted See financial projections on page 29 for 2020A gross booking value 1. Based on the zip codes with booked transactions on the platform 2. Based on 2016-2019 Jan Cohorts 3. Based on credit card data for the month of December 2020 8 4. Rover survey results as of July 2020

Rover Overview Rover is the #1 Pet Services App Digital and Convenient • Platform connects you with high-quality pet care providers in your area • Ability to choose your pet care provider, unlike some competitors • 3.7 million reviews provide assurance on quality of care Trust and Safety • Background checks • Detailed sitter profiles • Personal information privacy • Customer reviews • 24/7 support 9Rover Overview Rover is the #1 Pet Services App Digital and Convenient • Platform connects you with high-quality pet care providers in your area • Ability to choose your pet care provider, unlike some competitors • 3.7 million reviews provide assurance on quality of care Trust and Safety • Background checks • Detailed sitter profiles • Personal information privacy • Customer reviews • 24/7 support 9

Rover Services Overview – Illustrative Booking Overnight Daytime Boarding Drop-in Dog Doggy In Home House Visits Walking Day Care Grooming Sitting Overnight pet care For potty breaks, quick Whenever your dog Daytime pet care in Full-service or just Overnight pet care or at a sitter’s pet- play dates, and litter needs a walk your sitter’s dog- a bath in your house-sitting services friendly home box cleaning friendly home home at your home Average $35 $30 $15 $20 $30 $70 price / night / night / day / walk / visit / groom per unit 68% of GBV 32% of GBV % of Testing in 54% 14% 14% 12% 5% GBV Select Markets 10 GBV and average price based on FYE December 31, 2019Rover Services Overview – Illustrative Booking Overnight Daytime Boarding Drop-in Dog Doggy In Home House Visits Walking Day Care Grooming Sitting Overnight pet care For potty breaks, quick Whenever your dog Daytime pet care in Full-service or just Overnight pet care or at a sitter’s pet- play dates, and litter needs a walk your sitter’s dog- a bath in your house-sitting services friendly home box cleaning friendly home home at your home Average $35 $30 $15 $20 $30 $70 price / night / night / day / walk / visit / groom per unit 68% of GBV 32% of GBV % of Testing in 54% 14% 14% 12% 5% GBV Select Markets 10 GBV and average price based on FYE December 31, 2019

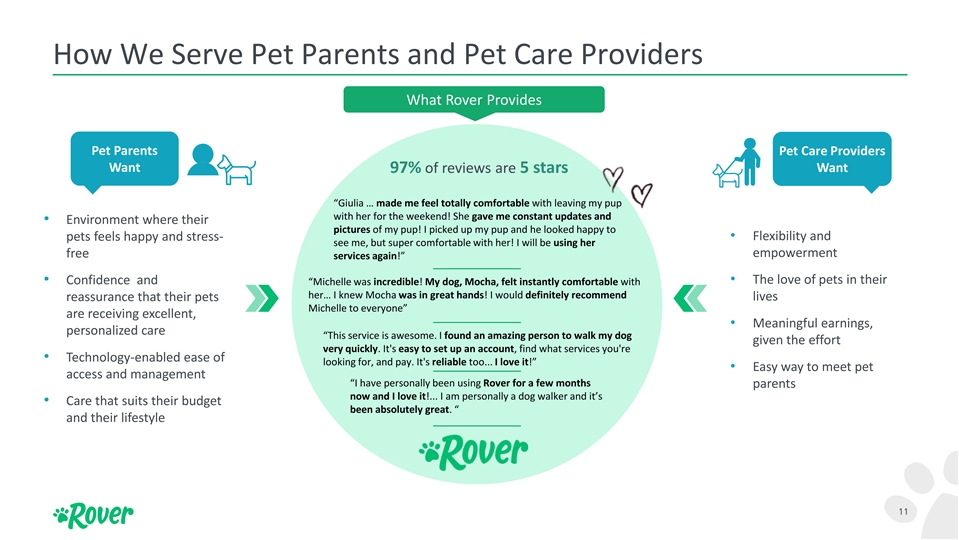

How We Serve Pet Parents and Pet Care Providers What Rover Provides Pet Parents Pet Care Providers Want Want 97% of reviews are 5 stars “Giulia … made me feel totally comfortable with leaving my pup with her for the weekend! She gave me constant updates and • Environment where their pictures of my pup! I picked up my pup and he looked happy to • Flexibility and pets feels happy and stress- see me, but super comfortable with her! I will be using her empowerment free services again!” • Confidence and • The love of pets in their “Michelle was incredible! My dog, Mocha, felt instantly comfortable with her… I knew Mocha was in great hands! I would definitely recommend reassurance that their pets lives Michelle to everyone” are receiving excellent, • Meaningful earnings, personalized care “This service is awesome. I found an amazing person to walk my dog given the effort very quickly. It's easy to set up an account, find what services you're • Technology-enabled ease of looking for, and pay. It's reliable too... I love it!” • Easy way to meet pet access and management “I have personally been using Rover for a few months parents now and I love it!... I am personally a dog walker and it’s • Care that suits their budget been absolutely great. “ and their lifestyle 11How We Serve Pet Parents and Pet Care Providers What Rover Provides Pet Parents Pet Care Providers Want Want 97% of reviews are 5 stars “Giulia … made me feel totally comfortable with leaving my pup with her for the weekend! She gave me constant updates and • Environment where their pictures of my pup! I picked up my pup and he looked happy to • Flexibility and pets feels happy and stress- see me, but super comfortable with her! I will be using her empowerment free services again!” • Confidence and • The love of pets in their “Michelle was incredible! My dog, Mocha, felt instantly comfortable with her… I knew Mocha was in great hands! I would definitely recommend reassurance that their pets lives Michelle to everyone” are receiving excellent, • Meaningful earnings, personalized care “This service is awesome. I found an amazing person to walk my dog given the effort very quickly. It's easy to set up an account, find what services you're • Technology-enabled ease of looking for, and pay. It's reliable too... I love it!” • Easy way to meet pet access and management “I have personally been using Rover for a few months parents now and I love it!... I am personally a dog walker and it’s • Care that suits their budget been absolutely great. “ and their lifestyle 11

Rover’s Users span across Geographies, Age, and Income We serve a wide age range of pet parents, while our providers tend to be younger (3) Bookings by Population Density 11% 15% Gen Z 38% Millennials 31% 41% Gen X 22% 26% Baby Boomers 43% High 23% Builders Density 51% 29% 14% 20% 5% 3% 1% Medium (1) (2) (2) APPA Rover Pet Parents Pet Care Providers Density 27% Low Density We serve a range of household incomes, but our pet parents skew more affluent 22% 30% 10% $125k+ 15% 15% $100-125k 19% $75-100k 53% < $75k 36% Note: Demographic data for U.S. only 1. APPA National Pet Owners Survey (1) (2) APPA Rover Pet Parents 2. Based on Rover survey 3. Based on 2019 Bookings Rover defines the population density as: Low Density as < 800 people per sq. mile, Medium Density as 800-4000 people per sq. mile, and High Density as >4000 people per sq. mile 12 Based on Rover definitions, Low Density constitutes ~45% of the US population, Medium Density constitutes ~39% of the US population, and High Density constitutes ~16% of the US populationRover’s Users span across Geographies, Age, and Income We serve a wide age range of pet parents, while our providers tend to be younger (3) Bookings by Population Density 11% 15% Gen Z 38% Millennials 31% 41% Gen X 22% 26% Baby Boomers 43% High 23% Builders Density 51% 29% 14% 20% 5% 3% 1% Medium (1) (2) (2) APPA Rover Pet Parents Pet Care Providers Density 27% Low Density We serve a range of household incomes, but our pet parents skew more affluent 22% 30% 10% $125k+ 15% 15% $100-125k 19% $75-100k 53% < $75k 36% Note: Demographic data for U.S. only 1. APPA National Pet Owners Survey (1) (2) APPA Rover Pet Parents 2. Based on Rover survey 3. Based on 2019 Bookings Rover defines the population density as: Low Density as < 800 people per sq. mile, Medium Density as 800-4000 people per sq. mile, and High Density as >4000 people per sq. mile 12 Based on Rover definitions, Low Density constitutes ~45% of the US population, Medium Density constitutes ~39% of the US population, and High Density constitutes ~16% of the US population

Table of Contents 1. Business Overview 2. Investment Highlights 3. Financial Overview 4. Transaction Overview 5. Appendix 13Table of Contents 1. Business Overview 2. Investment Highlights 3. Financial Overview 4. Transaction Overview 5. Appendix 13

Pets and Their Love in Our Lives 67% of U.S. Households have Pets +20% have previously owned a pet Part of the Family 95% of dog parents and 94% of cat parents consider their pet a part of the family Our Pets… decrease stress, improve heart health, and help socialize children Pet Humanization and Premiumization Driving Spend Prioritization of Pet Needs Increasing Spend Per Pet Increasing Spend on Pet Services Recession Resilience 14 Source: APPA National Pet Owners Survey, Packaged Facts, National Institutes of HealthPets and Their Love in Our Lives 67% of U.S. Households have Pets +20% have previously owned a pet Part of the Family 95% of dog parents and 94% of cat parents consider their pet a part of the family Our Pets… decrease stress, improve heart health, and help socialize children Pet Humanization and Premiumization Driving Spend Prioritization of Pet Needs Increasing Spend Per Pet Increasing Spend on Pet Services Recession Resilience 14 Source: APPA National Pet Owners Survey, Packaged Facts, National Institutes of Health

The Pet Market is Massive, with a Relatively Untapped Services Market (3) Global Buy Pet Food ~98% Pet Spend Global Dog (3) & Cat Spend Buy Treats ~90% Current U.S. (1) Pet Opportunity (3) Take Their Pet to Vet ~85% $95bn Current (4) Commercial Pay for Commercial Overnight Pet Services ~10% Pet Services (2) Market $9bn 1. Packaged Facts, 2019. Represents retail pet food/supplies, veterinary and non-medical services 2. Packaged Facts, 2019. Represents current non-medical services market of $10.33bn less the $1.4bn pet insurance market 15 3. APPA. Pet parent behavior statistics represent average for both dog and cat parents 4. Management estimate based on Packaged Facts data in footnotes 1 and 2 aboveThe Pet Market is Massive, with a Relatively Untapped Services Market (3) Global Buy Pet Food ~98% Pet Spend Global Dog (3) & Cat Spend Buy Treats ~90% Current U.S. (1) Pet Opportunity (3) Take Their Pet to Vet ~85% $95bn Current (4) Commercial Pay for Commercial Overnight Pet Services ~10% Pet Services (2) Market $9bn 1. Packaged Facts, 2019. Represents retail pet food/supplies, veterinary and non-medical services 2. Packaged Facts, 2019. Represents current non-medical services market of $10.33bn less the $1.4bn pet insurance market 15 3. APPA. Pet parent behavior statistics represent average for both dog and cat parents 4. Management estimate based on Packaged Facts data in footnotes 1 and 2 above

Rover Unlocks Latent Demand for Pet Care Services (1) (1) Overnight Daytime $3bn Unlock Unlock Opportunity Opportunity $4bn $6bn $66bn # of Pet Households in US Total Dogs in US Families x Household Travel Nights per Year x Services per Year (3) x Number of Pets per Household x Price per Household x Price per Pet per Night x Percent of Addressable Households (2) = $79bn Estimated U.S. TAM, Growing to $113bn Source: Packaged Facts, Euromonitor 1. Management estimates based on Packaged Facts and Euromonitor. See reconciliation on page 46 for details Additional market opportunity based on $ of households with pets, number of total households, number of trips nights per households, and price per pet We estimate that leisure/non-business travel represents ~85-87% of our GBV. We also estimate that domestic travel represents ~90% of all trips taken 16 2. Management estimates based on Packaged Facts and Euromonitor. International opportunity in geographies where Rover currently operates estimated to be 30% of U.S. opportunity 3. For purposes of TAM build, pet = dog or catRover Unlocks Latent Demand for Pet Care Services (1) (1) Overnight Daytime $3bn Unlock Unlock Opportunity Opportunity $4bn $6bn $66bn # of Pet Households in US Total Dogs in US Families x Household Travel Nights per Year x Services per Year (3) x Number of Pets per Household x Price per Household x Price per Pet per Night x Percent of Addressable Households (2) = $79bn Estimated U.S. TAM, Growing to $113bn Source: Packaged Facts, Euromonitor 1. Management estimates based on Packaged Facts and Euromonitor. See reconciliation on page 46 for details Additional market opportunity based on $ of households with pets, number of total households, number of trips nights per households, and price per pet We estimate that leisure/non-business travel represents ~85-87% of our GBV. We also estimate that domestic travel represents ~90% of all trips taken 16 2. Management estimates based on Packaged Facts and Euromonitor. International opportunity in geographies where Rover currently operates estimated to be 30% of U.S. opportunity 3. For purposes of TAM build, pet = dog or cat

Majority of Our Pet Parents and Pet Care Providers are New to Commercial Market Where are our pet parents coming from? Where are our providers coming from? Local Other Existing Independent / 0.5% Professionals Boutique 2% Professionals 13% New to Commercial Services Kennels / Vets 98% 20% Family / Friends / Neighbors 67% Stats based on Rover survey 17Majority of Our Pet Parents and Pet Care Providers are New to Commercial Market Where are our pet parents coming from? Where are our providers coming from? Local Other Existing Independent / 0.5% Professionals Boutique 2% Professionals 13% New to Commercial Services Kennels / Vets 98% 20% Family / Friends / Neighbors 67% Stats based on Rover survey 17

The Traditional Pet Care Services Market was not Built with Today’s Consumer in Mind The Majority of Pet Care is Done by Family and Friends Extremely fragmented Local Mom & Pet Care Independent market Family & Friends Pop Shops Chains Professionals Low online penetration Found Offline or via Online Aggregators & Directories Few pet care specialists operating at scale online 18The Traditional Pet Care Services Market was not Built with Today’s Consumer in Mind The Majority of Pet Care is Done by Family and Friends Extremely fragmented Local Mom & Pet Care Independent market Family & Friends Pop Shops Chains Professionals Low online penetration Found Offline or via Online Aggregators & Directories Few pet care specialists operating at scale online 18

Data Creates a Competitive Advantage… • 42mm services booked • Matching • 10mm pet profiles • Marketing • 18.4mm search sessions in 2019 • Operations • 6.2mm requests matched with a provider in 2019 • Safety Features • >100 attributes analyzed from each service request • Notifications • 428mm messages • Advertising on Blog • 264mm blog visits • 98mm photos (5.5 per • Adds Value to Partnerships booking) • Opportunity to Monetize via • 2mm pet parents booked Future Products and Offerings • 500k pet care providers paid Note: Metrics are cumulative as of December 2020, unless otherwise noted 19Data Creates a Competitive Advantage… • 42mm services booked • Matching • 10mm pet profiles • Marketing • 18.4mm search sessions in 2019 • Operations • 6.2mm requests matched with a provider in 2019 • Safety Features • >100 attributes analyzed from each service request • Notifications • 428mm messages • Advertising on Blog • 264mm blog visits • 98mm photos (5.5 per • Adds Value to Partnerships booking) • Opportunity to Monetize via • 2mm pet parents booked Future Products and Offerings • 500k pet care providers paid Note: Metrics are cumulative as of December 2020, unless otherwise noted 19

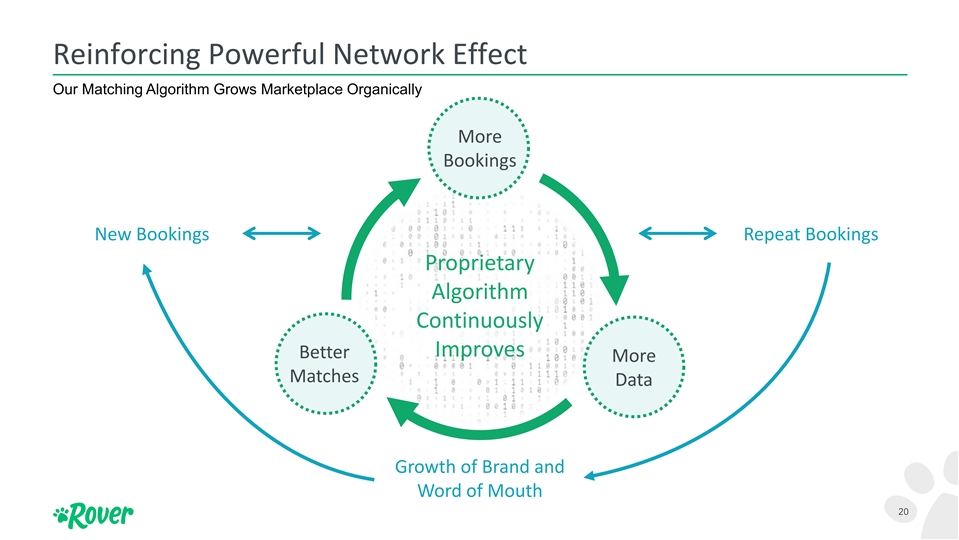

Reinforcing Powerful Network Effect Our Matching Algorithm Grows Marketplace Organically More Bookings New Bookings Repeat Bookings Proprietary Algorithm Continuously Improves Better More Matches Data Growth of Brand and Word of Mouth 20Reinforcing Powerful Network Effect Our Matching Algorithm Grows Marketplace Organically More Bookings New Bookings Repeat Bookings Proprietary Algorithm Continuously Improves Better More Matches Data Growth of Brand and Word of Mouth 20

Powerful Word of Mouth Acquisition Enhanced by Strategic Paid Marketing Drives Growth • Over time, as the strength of word of mouth customer acquisition has increased, our marketing spend as a % of GBV has decreased • In 2020, 51% new customers in Top 10 cities were acquired via word of mouth vs. 44% in the rest of the market • 1-2 quarter target payback on customer acquisition cost (1) (1) • Following initial transaction, we retain >50% of customer repeat year 1 bookings every year thereafter, growing lifetime value Note: 2020 results have not been audited. See Legal Disclaimer for additional information 21 1. 2020 Marketing as % of GBV was depressed due to impact of COVID, and is not indicator of future marketing levelsPowerful Word of Mouth Acquisition Enhanced by Strategic Paid Marketing Drives Growth • Over time, as the strength of word of mouth customer acquisition has increased, our marketing spend as a % of GBV has decreased • In 2020, 51% new customers in Top 10 cities were acquired via word of mouth vs. 44% in the rest of the market • 1-2 quarter target payback on customer acquisition cost (1) (1) • Following initial transaction, we retain >50% of customer repeat year 1 bookings every year thereafter, growing lifetime value Note: 2020 results have not been audited. See Legal Disclaimer for additional information 21 1. 2020 Marketing as % of GBV was depressed due to impact of COVID, and is not indicator of future marketing levels

Strong Retention Metrics Pet Parents Book More and More Often Average Total Bookings 10 1-2 quarter 2016 2017 payback period 9 2015 8 2018 2013 2014 7 6 2019 5 4 Net Take Retention, excluding 1st Booking Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 2013 100% 64% 52% 56% 61% 57% 3 2014 100% 67% 62% 65% 62% 2020 2015 100% 71% 66% 60% 2016 100% 64% 54% 2 2017 100% 62% 1 0 6 12 18 24 30 36 42 48 54 60 66 72 78 84 (1) Months since first booking 1. Represent cohorts from January of respective year. Cumulative through Q4’19, except for 2020 cohort 22Strong Retention Metrics Pet Parents Book More and More Often Average Total Bookings 10 1-2 quarter 2016 2017 payback period 9 2015 8 2018 2013 2014 7 6 2019 5 4 Net Take Retention, excluding 1st Booking Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 2013 100% 64% 52% 56% 61% 57% 3 2014 100% 67% 62% 65% 62% 2020 2015 100% 71% 66% 60% 2016 100% 64% 54% 2 2017 100% 62% 1 0 6 12 18 24 30 36 42 48 54 60 66 72 78 84 (1) Months since first booking 1. Represent cohorts from January of respective year. Cumulative through Q4’19, except for 2020 cohort 22

Continued Acceleration in Engagement Increased Engagement Driven By Both Higher Rebooking Rates and Higher Frequency Percentage of Cohort with Rebooking Cumulative Bookings per Repeat Customer 2016 80% 2017 12 2013 2016 2017 2014 2018 2015 2015 70% 10 2018 2019 2014 60% 2013 8 2019 50% 2020 6 40% 2020 4 30% 2 20% 0 10% 0 6 12 18 24 30 36 42 48 54 60 66 72 78 84 0 6 12 18 24 30 36 42 48 54 60 66 72 78 84 Months since first booking Months since first booking (1) Months since first booking 1. Represent cohorts from January of respective year. Cumulative through Q4’19, except for 2020 cohort 23Continued Acceleration in Engagement Increased Engagement Driven By Both Higher Rebooking Rates and Higher Frequency Percentage of Cohort with Rebooking Cumulative Bookings per Repeat Customer 2016 80% 2017 12 2013 2016 2017 2014 2018 2015 2015 70% 10 2018 2019 2014 60% 2013 8 2019 50% 2020 6 40% 2020 4 30% 2 20% 0 10% 0 6 12 18 24 30 36 42 48 54 60 66 72 78 84 0 6 12 18 24 30 36 42 48 54 60 66 72 78 84 Months since first booking Months since first booking (1) Months since first booking 1. Represent cohorts from January of respective year. Cumulative through Q4’19, except for 2020 cohort 23

Our Strong User Retention is the Result of our Value Proposition and Applied Data Science Strong Retention on Value Proposition Extends Both Sides of Platform Far Beyond Finding a Provider • 85%+ of bookings are repeat • The Rover Guarantee • >90% revenue retention for pet • 24/7 Customer support care providers • Care instructions • ~65% revenue retention for pet • In-app messaging parents • Photo sharing • Cohort retention is ~linear after • Calendaring 12-18 months (subscription-like) • Real-time mapping of walks • Cohorts have improved over time, in increasing take rate environment• Ease of paying 24 Note: Metrics are through 2019, and exclude 2020Our Strong User Retention is the Result of our Value Proposition and Applied Data Science Strong Retention on Value Proposition Extends Both Sides of Platform Far Beyond Finding a Provider • 85%+ of bookings are repeat • The Rover Guarantee • >90% revenue retention for pet • 24/7 Customer support care providers • Care instructions • ~65% revenue retention for pet • In-app messaging parents • Photo sharing • Cohort retention is ~linear after • Calendaring 12-18 months (subscription-like) • Real-time mapping of walks • Cohorts have improved over time, in increasing take rate environment• Ease of paying 24 Note: Metrics are through 2019, and exclude 2020

Ultimately Applied Data Science Drives Platform Stickiness, Increasing Loyalty Our technology identifies good providers and promotes them, driving positive experiences for pet parents Good providers rank higher in search results Provider shows positive activities on platform 25Ultimately Applied Data Science Drives Platform Stickiness, Increasing Loyalty Our technology identifies good providers and promotes them, driving positive experiences for pet parents Good providers rank higher in search results Provider shows positive activities on platform 25

COVID Recovery Story: Converging Tailwinds U.S. households got a new pet during the pandemic Vaccine progress driving expected travel recovery 11mm (1) U.S. Pet Adoption Y/Y Growth (%) Y/Y % Analyst Bookings Growth Forecast for Expedia and Booking Group 100% 80% 35% 60% 40% ~4.0x 20% 0% (20%) (40%) 9% (60%) EXPE and BKNG (as of Dec 2020) (80%) (100%) 2019 2020 2019 2020 2021 2022 2023 2024 2025 Further accelerated by shift from offline to online for pet spend categories Source: Wall Street Research; Shelteranimalscount.com, Last Chance Animal Rescue, The Wall Street Journal, APPA 26 1. Management’s estimate based on Gross Live Outcomes growth from 3.26M to 3.55M and Last Chance Pet Adoption rates in 2020COVID Recovery Story: Converging Tailwinds U.S. households got a new pet during the pandemic Vaccine progress driving expected travel recovery 11mm (1) U.S. Pet Adoption Y/Y Growth (%) Y/Y % Analyst Bookings Growth Forecast for Expedia and Booking Group 100% 80% 35% 60% 40% ~4.0x 20% 0% (20%) (40%) 9% (60%) EXPE and BKNG (as of Dec 2020) (80%) (100%) 2019 2020 2019 2020 2021 2022 2023 2024 2025 Further accelerated by shift from offline to online for pet spend categories Source: Wall Street Research; Shelteranimalscount.com, Last Chance Animal Rescue, The Wall Street Journal, APPA 26 1. Management’s estimate based on Gross Live Outcomes growth from 3.26M to 3.55M and Last Chance Pet Adoption rates in 2020

Multiple Growth Vectors Expand strategic partnerships Increase revenue from advertising and retail offerings Grow international coverage Expand service Attract and delight customers offerings and pet in existing geographies and types covered within existing services 27Multiple Growth Vectors Expand strategic partnerships Increase revenue from advertising and retail offerings Grow international coverage Expand service Attract and delight customers offerings and pet in existing geographies and types covered within existing services 27

Table of Contents 1. Business Overview 2. Investment Highlights 3. Financial Overview 4. Transaction Overview 5. Appendix 28Table of Contents 1. Business Overview 2. Investment Highlights 3. Financial Overview 4. Transaction Overview 5. Appendix 28

Financial Projections Bookings (mm) Gross Booking Value ($mm) 27% 8.1 CAGR $855 4.2 3.9 3.2 $436 $408 2.4 $333 $233 2 20 018A 18A 2 20 019A 19A 2 20 020A 20A 20 2021E 21E 20 2022E 22E 2018A 2019A 2020A 2021E 2022E 2018A 2019A 2020A 2021E 2022E 30% (43%) 63% 106% 31% (47%) 75% 109% YoY Growth % YoY Growth % (1) Adjusted EBITDA ($mm) $35 Revenue ($mm) 30% CAGR 2 2018A 018A 2 2019A 019A 2020E 2020E 2021E 2021E $201 2 20 022E 22E ($9) $97 $95 $71 ($25) $49 ($35) ($49) 2018A 2019A 2020E 2021E 2022E 2018A 2019A 2020A 2021E 2022E YoY Growth % (49%) 99% 107% Margin % (69%) (37%) (51%) (9%) 17% 33% Note: 2020 results have not been audited. See Legal Disclaimer for additional information 29 Projections assume successful COVID vaccine rollout in 2021. Projections assume the travel industry starts to recover in 2H'21. Projections assume existing pet parents gradual return to normal cohort behavior from Q2'21 through Q1’22 1. Defined as net loss adjusted for interest & taxes, depreciation & amortization, other income or expenses, stock-based compensation, restructuring costs, and acquisition-related costs. See reconciliation on page 45 for detailsFinancial Projections Bookings (mm) Gross Booking Value ($mm) 27% 8.1 CAGR $855 4.2 3.9 3.2 $436 $408 2.4 $333 $233 2 20 018A 18A 2 20 019A 19A 2 20 020A 20A 20 2021E 21E 20 2022E 22E 2018A 2019A 2020A 2021E 2022E 2018A 2019A 2020A 2021E 2022E 30% (43%) 63% 106% 31% (47%) 75% 109% YoY Growth % YoY Growth % (1) Adjusted EBITDA ($mm) $35 Revenue ($mm) 30% CAGR 2 2018A 018A 2 2019A 019A 2020E 2020E 2021E 2021E $201 2 20 022E 22E ($9) $97 $95 $71 ($25) $49 ($35) ($49) 2018A 2019A 2020E 2021E 2022E 2018A 2019A 2020A 2021E 2022E YoY Growth % (49%) 99% 107% Margin % (69%) (37%) (51%) (9%) 17% 33% Note: 2020 results have not been audited. See Legal Disclaimer for additional information 29 Projections assume successful COVID vaccine rollout in 2021. Projections assume the travel industry starts to recover in 2H'21. Projections assume existing pet parents gradual return to normal cohort behavior from Q2'21 through Q1’22 1. Defined as net loss adjusted for interest & taxes, depreciation & amortization, other income or expenses, stock-based compensation, restructuring costs, and acquisition-related costs. See reconciliation on page 45 for details

Key Model Assumptions rd • Pre-2021 cohorts make up greater than 1/3 of 2022 revenue after recovery to normalized historical cohort behavior over the next ~12-14 months • 2021 will be the tale of two halves • Normalized leisure travel volume for the full year 2022 • Technology investments continue to modestly enhance unit economics drivers Note: See page 51 for additional detail behind key model assumptions 30Key Model Assumptions rd • Pre-2021 cohorts make up greater than 1/3 of 2022 revenue after recovery to normalized historical cohort behavior over the next ~12-14 months • 2021 will be the tale of two halves • Normalized leisure travel volume for the full year 2022 • Technology investments continue to modestly enhance unit economics drivers Note: See page 51 for additional detail behind key model assumptions 30

Cohort Retention Recovery Monthly cohort retention rates are used to track incremental booking behavior Projections assume 12-month recovery of existing cohorts All Service Lines Combined January Cohorts Only (for illustration purposes) 35% 30% 25% 20% 15% Fall off due to 12 month recovery initial stay at home assumption for existing orders 10% cohorts 5% Initial recovery in early summer 0% 1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 Tenure Month Jan '17 Jan '18 Jan '19 Jan '20 Jan '21 Jan '22 Jan '23 Normal Retention curve (no COVID impact) Note: Projections assume existing pet parents gradual return to normal cohort behavior from Q2'21 through Q1’22 31 Cohort unique user retention rate: Unique users with at least one booking in the month, divided by the original cohort size (the originating new active users) Cohort Unique User Retention Rate*Cohort Retention Recovery Monthly cohort retention rates are used to track incremental booking behavior Projections assume 12-month recovery of existing cohorts All Service Lines Combined January Cohorts Only (for illustration purposes) 35% 30% 25% 20% 15% Fall off due to 12 month recovery initial stay at home assumption for existing orders 10% cohorts 5% Initial recovery in early summer 0% 1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 Tenure Month Jan '17 Jan '18 Jan '19 Jan '20 Jan '21 Jan '22 Jan '23 Normal Retention curve (no COVID impact) Note: Projections assume existing pet parents gradual return to normal cohort behavior from Q2'21 through Q1’22 31 Cohort unique user retention rate: Unique users with at least one booking in the month, divided by the original cohort size (the originating new active users) Cohort Unique User Retention Rate*

Long-Term Targets Long-Term 3 FY18 FY19 Q4’20 Targets Revenue $71.4 $95.1 $13.2 Revenue Growth 65% 33% (51%) Gross Margin (inclusive of IDS Amortization) ~70% 77% 75% 71% Service Operations 25% 21% 18% ~10% Marketing 82% 53% 18% ~25% Technology 24% 23% 34% 10%+ General and Administrative <10% 31% 26% 46% (1) Adjusted EBITDA 30%+ (69%) (37%) (23%) Note: 2020 results have not been audited. See Legal Disclaimer for additional information 1. Defined as net loss adjusted for interest & taxes, depreciation & amortization, other income or expenses, stock-based compensation, restructuring costs, and acquisition-related costs 32 % of RevenueLong-Term Targets Long-Term 3 FY18 FY19 Q4’20 Targets Revenue $71.4 $95.1 $13.2 Revenue Growth 65% 33% (51%) Gross Margin (inclusive of IDS Amortization) ~70% 77% 75% 71% Service Operations 25% 21% 18% ~10% Marketing 82% 53% 18% ~25% Technology 24% 23% 34% 10%+ General and Administrative <10% 31% 26% 46% (1) Adjusted EBITDA 30%+ (69%) (37%) (23%) Note: 2020 results have not been audited. See Legal Disclaimer for additional information 1. Defined as net loss adjusted for interest & taxes, depreciation & amortization, other income or expenses, stock-based compensation, restructuring costs, and acquisition-related costs 32 % of Revenue

Rover – Differentiated Consumer Marketplace World’s largest online marketplace for pet care Massive untapped market opportunity, supported by tailwinds of pet adoption and spend Largest supply of high-quality pet care providers, providing personalized service Strong pet parent loyalty and word-of-mouth growth Data scale and proprietary algorithm to make continuously better matches High growth financial profile with attractive customer unit economics 33Rover – Differentiated Consumer Marketplace World’s largest online marketplace for pet care Massive untapped market opportunity, supported by tailwinds of pet adoption and spend Largest supply of high-quality pet care providers, providing personalized service Strong pet parent loyalty and word-of-mouth growth Data scale and proprietary algorithm to make continuously better matches High growth financial profile with attractive customer unit economics 33

Table of Contents 1. Business Overview 2. Investment Highlights 3. Financial Overview 4. Transaction Overview 5. Appendix 34Table of Contents 1. Business Overview 2. Investment Highlights 3. Financial Overview 4. Transaction Overview 5. Appendix 34

True Wind Overview Firm Track Record Focus — San Francisco-based — Track record of excellence with — Investing in differentiated, leading TMT private equity firm managing ~$2 billion principals playing a major role in 30+ companies platform investments with $75+ billion — 75+ years of collective investing — Broad mandate across multiple in total transaction value and $15+ experience technology sectors: billion of invested equity — True Wind’s founding partners were ‒ Software — Repeat SPAC issuer: First transaction previously the founding members of ‒ Internet / Digital Media reached combination with Open KKR’s technology franchise ‒ Financial Technology Lending (NASDAQ: LPRO), resulting in — Fifteen full-time investment successful outcome for prior ‒ Healthcare IT professionals with deep technology shareholders, management, and PIPE ‒ Industrial Technology investing expertise and public market investors ‒ Hardware — Successful public company experience: ‒ IT Services GoDaddy, Avago/Broadcom, NXP, Jazz Pharma, Open Lending, Safeway, Owens Illinois, Reltec, Amphenol 35True Wind Overview Firm Track Record Focus — San Francisco-based — Track record of excellence with — Investing in differentiated, leading TMT private equity firm managing ~$2 billion principals playing a major role in 30+ companies platform investments with $75+ billion — 75+ years of collective investing — Broad mandate across multiple in total transaction value and $15+ experience technology sectors: billion of invested equity — True Wind’s founding partners were ‒ Software — Repeat SPAC issuer: First transaction previously the founding members of ‒ Internet / Digital Media reached combination with Open KKR’s technology franchise ‒ Financial Technology Lending (NASDAQ: LPRO), resulting in — Fifteen full-time investment successful outcome for prior ‒ Healthcare IT professionals with deep technology shareholders, management, and PIPE ‒ Industrial Technology investing expertise and public market investors ‒ Hardware — Successful public company experience: ‒ IT Services GoDaddy, Avago/Broadcom, NXP, Jazz Pharma, Open Lending, Safeway, Owens Illinois, Reltec, Amphenol 35

Transaction Overview Illustrative Pro Forma Capitalization Key Proposed Transaction Terms ▪ Aggregate Value: $1,355MM / Equity Value: $1,630MM ▪ Total Raise of $325MM: $275MM from SPAC and $50MM from PIPE ▪ $50MM backstop from Sponsor against potential redemptions ▪ $45MM in secondary ▪ 6.875MM shares for Sponsor Promote : 40%/40%/20% split at $12.00/$14.00/$16.00 ▪ Backstop acceleration - 3.4MM promote shares vest pro rata with $50MM backstop ▪ Promote and warrants reduced linearly from zero net redemptions in excess of backstop to minimum cash threshold (Up to $200MM of net redemptions in excess of backstop) ▪ 22.5MM shares for Seller Earnout: 10MM at $12.00; 10MM at $14.00; 2.5MM @ $16.00 Cash Sources and Uses ($MM) ▪ 3.0MM founder warrants, $18.00 conversion cap Illustrative Post-Transaction Ownership PIPE Holders, 3% SPAC Public Holders, 17% Existing Holders, 80% 36Transaction Overview Illustrative Pro Forma Capitalization Key Proposed Transaction Terms ▪ Aggregate Value: $1,355MM / Equity Value: $1,630MM ▪ Total Raise of $325MM: $275MM from SPAC and $50MM from PIPE ▪ $50MM backstop from Sponsor against potential redemptions ▪ $45MM in secondary ▪ 6.875MM shares for Sponsor Promote : 40%/40%/20% split at $12.00/$14.00/$16.00 ▪ Backstop acceleration - 3.4MM promote shares vest pro rata with $50MM backstop ▪ Promote and warrants reduced linearly from zero net redemptions in excess of backstop to minimum cash threshold (Up to $200MM of net redemptions in excess of backstop) ▪ 22.5MM shares for Seller Earnout: 10MM at $12.00; 10MM at $14.00; 2.5MM @ $16.00 Cash Sources and Uses ($MM) ▪ 3.0MM founder warrants, $18.00 conversion cap Illustrative Post-Transaction Ownership PIPE Holders, 3% SPAC Public Holders, 17% Existing Holders, 80% 36

Comparable Selection Criteria Market Differentiated Proprietary Network Leader Consumer Marketplace Data Assets Effect ✓ Undisputed sector leaders✓ Similar “take-rate” ✓ Leading data scale✓ Reinforcing network effect business models driven by more bookings, ✓ Proprietary algorithm more data, and better ✓ Inclusion of 3-sided matches marketplaces 37Comparable Selection Criteria Market Differentiated Proprietary Network Leader Consumer Marketplace Data Assets Effect ✓ Undisputed sector leaders✓ Similar “take-rate” ✓ Leading data scale✓ Reinforcing network effect business models driven by more bookings, ✓ Proprietary algorithm more data, and better ✓ Inclusion of 3-sided matches marketplaces 37

Public Comparables – Operating Metrics 1. Market Data as of 3/5/2021 2. Chewy excluded from AV / Revenue Median and Mean 38 3. Match CAGR represents CY20’-22’ growthPublic Comparables – Operating Metrics 1. Market Data as of 3/5/2021 2. Chewy excluded from AV / Revenue Median and Mean 38 3. Match CAGR represents CY20’-22’ growth

Public Comparables – Trading Metrics AV / 22E Revenue AV / 22E SS EBITDA 88.8x 22.2x 62.0x 19.2x Median: 16.3x 13.4x 32.8x 31.5x 31.4x 10.4x Median: 32.8x 22.3x 6.7x 3.3x Fetch Fiverr Airbnb Match Etsy Chewy Fetch Fiverr Airbnb Match Chewy Etsy 1. Market Data as of 3/5/2021 39 2. Chewy excluded from AV / Revenue Median Public Comparables – Trading Metrics AV / 22E Revenue AV / 22E SS EBITDA 88.8x 22.2x 62.0x 19.2x Median: 16.3x 13.4x 32.8x 31.5x 31.4x 10.4x Median: 32.8x 22.3x 6.7x 3.3x Fetch Fiverr Airbnb Match Etsy Chewy Fetch Fiverr Airbnb Match Chewy Etsy 1. Market Data as of 3/5/2021 39 2. Chewy excluded from AV / Revenue Median

Recent Bookings Performance Bookings GBV Note: See Legal Disclaimer for additional information 40 Yo2Y % calculated as simple growth rate vs. period 2-years priorRecent Bookings Performance Bookings GBV Note: See Legal Disclaimer for additional information 40 Yo2Y % calculated as simple growth rate vs. period 2-years prior

Table of Contents 1. Business Overview 2. Investment Highlights 3. Financial Overview 4. Transaction Overview 5. Appendix 41Table of Contents 1. Business Overview 2. Investment Highlights 3. Financial Overview 4. Transaction Overview 5. Appendix 41

Opportunity for Continued M&A in Existing Markets Pet-Owning Households United States (1) ● All 50 States & Territories mm 85 (2) ● 96% of U.S. population covered ● Launched 2013 Canada (3) mm 7 ● All Provinces including Quebec serviced in English and French ● Entered in March 2017 with acquisition of DogVacay Europe ● 8 Countries: Great Britain, Spain, France, Norway, Sweden, Netherlands, (4) mm Italy, Germany 35 ● 8 Languages supported by operations team based in Barcelona ● Launched in London in 2Q18; entered additional geographies in mid-2019 (5) via acquisition of DogBuddy 1. APPA National Pet Owners Survey 2019-2020 2. Based on the zip codes with booked transactions on the platform as of September 2020 3. Management estimates based on Canadian Veterinary Journal and the Canadian census reports. 56% of 12.4mm Canadian households have pets 42 4. Management estimates based on Euromonitor and Statista. 35mm dog-owning households in 2019 within the green shaded countries, where Rover operates 5. Acquired DogBuddy in late 4Q18 and integrated in Q2’19Opportunity for Continued M&A in Existing Markets Pet-Owning Households United States (1) ● All 50 States & Territories mm 85 (2) ● 96% of U.S. population covered ● Launched 2013 Canada (3) mm 7 ● All Provinces including Quebec serviced in English and French ● Entered in March 2017 with acquisition of DogVacay Europe ● 8 Countries: Great Britain, Spain, France, Norway, Sweden, Netherlands, (4) mm Italy, Germany 35 ● 8 Languages supported by operations team based in Barcelona ● Launched in London in 2Q18; entered additional geographies in mid-2019 (5) via acquisition of DogBuddy 1. APPA National Pet Owners Survey 2019-2020 2. Based on the zip codes with booked transactions on the platform as of September 2020 3. Management estimates based on Canadian Veterinary Journal and the Canadian census reports. 56% of 12.4mm Canadian households have pets 42 4. Management estimates based on Euromonitor and Statista. 35mm dog-owning households in 2019 within the green shaded countries, where Rover operates 5. Acquired DogBuddy in late 4Q18 and integrated in Q2’19

Large Greenfield Opportunity in Rest of the World Europe Canada Rest of the World ● Near term international opportunity includes continued expansion through rest of Europe Japan ● Outside of Europe includes Australia and New Zealand ● Initial expansion in Asia begins with Japan United States Australia New Zealand Near Term Markets/ Existing Markets White Space Opportunities 43Large Greenfield Opportunity in Rest of the World Europe Canada Rest of the World ● Near term international opportunity includes continued expansion through rest of Europe Japan ● Outside of Europe includes Australia and New Zealand ● Initial expansion in Asia begins with Japan United States Australia New Zealand Near Term Markets/ Existing Markets White Space Opportunities 43