UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

Date of Report: November 4, 2024

Commission File Number: 001-39570

TIM S.A.

(Exact name of Registrant as specified in its Charter)

João Cabral de Melo Neto Avenue, 850 – North Tower – 12th floor

22775-057 Rio de Janeiro, RJ, Brazil

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1).

Yes ☐ No ☒

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7).

Yes ☐ No ☒

TIM S.A.

QUARTERLY INFORMATION

September 30, 2024

TIM S.A.

QUARTERLY INFORMATION

September 30, 2024

Contents

| Independent auditors’ report on quarterly information | 1 |

| Quarterly information | |

| Balance sheets | 3 |

| Statements of income | 5 |

| Statements of comprehensive income | 7 |

| Statements of changes in shareholders' equity | 9 |

| Statements of cash flows | 11 |

| Statements of value added | 13 |

| Performance comment | 14 |

| Notes to the individual and consolidated quarterly information | 35 |

| Tax Council Opinion | 125 |

| Statement of the Executive Officers on the quarterly information | 126 |

| Statement of the Executive Officers on the Independent auditors' report | 127 |

| 1 |

| 2 |

| TIM S.A. | ||||

| BALANCE SHEETS | ||||

| September 30, 2024 and December 31, 2023 | ||||

| (In thousands of reais) | ||||

| Parent Company | ||||

| Note | September 2024 | December 2023 | ||

| Assets | 54,535,904 | 55,260,156 | ||

| Current assets | 11,251,213 | 11,404,293 | ||

| Cash and cash equivalents | 4 | 2,287,330 | 3,077,931 | |

| Marketable securities | 5 | 2,045,032 | 1,958,490 | |

| Trade accounts receivable | 6 | 4,437,636 | 3,709,766 | |

| Inventories | 7 | 382,256 | 331,783 | |

| Recoverable income tax and social contribution | 8.a | 274,520 | 494,382 | |

| Recoverable taxes, fees and contributions | 9 | 765,714 | 943,767 | |

| Prepaid expenses | 10 | 405,998 | 238,468 | |

| Derivative financial instruments | 37 | 327,042 | 299,539 | |

| Leases | 18 | 32,956 | 29,886 | |

| Other amounts recoverable | 17 | 44,345 | 80,963 | |

| Other assets | 13 | 248,384 | 239,318 | |

| Non-current assets | 43,284,691 | 43,855,863 | ||

| Long-term receivables | 4,504,795 | 4,368,195 | ||

| Marketable securities | 5 | 15,231 | 12,949 | |

| Trade accounts receivable | 6 | 127,637 | 199,007 | |

| Recoverable income tax and social contribution | 8.a | 212,381 | 218,897 | |

| Recoverable taxes, fees and contributions | 9 | 979,503 | 874,539 | |

| Deferred income tax and social contribution | 8.c | 1,120,370 | 1,257,494 | |

| Judicial deposits | 11 | 672,384 | 689,739 | |

| Prepaid expenses | 10 | 258,500 | 138,937 | |

| Derivative financial instruments | 37 | 526,247 | 507,873 | |

| Leases | 18 | 207,966 | 206,455 | |

| Other financial assets | 12 | 351,522 | 216,721 | |

| Other assets | 13 | 33,054 | 45,584 | |

| Investment | 14 | 1,390,695 | 1,450,812 | |

| Property, plant and equipment | 15 | 22,467,329 | 22,411,815 | |

| Intangible assets | 16 | 14,921,872 | 15,625,041 | |

See the accompanying notes to the individual and consolidated quarterly information.

| 3 |

| TIM S.A. | ||||

| BALANCE SHEETS | ||||

| September 30, 2024 and December 31, 2023 | ||||

| (In thousands of reais) | ||||

| Parent Company | ||||

| Note | September 2024 | December 2023 | ||

| Total liabilities and shareholders' equity | 54,535,904 | 55,260,156 | ||

| Total liabilities | 28,558,652 | 29,244,216 | ||

| Current liabilities | 11,625,567 | 12,882,966 | ||

| Suppliers | 19 | 3,653,624 | 4,612,112 | |

| Loans and financing | 21 | 401,306 | 1,267,237 | |

| Lease liabilities | 18 | 1,802,680 | 1,808,740 | |

| Derivative financial instruments | 37 | 185,499 | 239,714 | |

| Labor obligations | 383,420 | 386,348 | ||

| Income tax and social contribution payable | 8.b | 97,585 | 64,407 | |

| Taxes, fees and contributions payable | 22 | 3,620,484 | 3,048,115 | |

| Dividends and interest on shareholders' equity payable | 26 | 799,175 | 647,872 | |

| Authorizations payable | 20 | 289,888 | 407,747 | |

| Deferred revenues | 23 | 273,591 | 279,401 | |

| Other liabilities and provision | 25 | 118,315 | 121,273 | |

| Non-current liabilities | 16,933,085 | 16,361,250 | ||

| Loans and financing | 21 | 2,732,053 | 2,503,709 | |

| Lease liabilities | 18 | 10,706,339 | 10,448,035 | |

| Taxes, fees and contributions payable | 22 | 38,231 | 10,603 | |

| Provision for legal and administrative proceedings | 24 | 1,518,008 | 1,410,299 | |

| Pension plan and other post-employment benefits | 38 | 5,019 | 5,019 | |

| Authorizations payable | 20 | 1,220,179 | 1,117,416 | |

| Deferred revenues | 23 | 569,360 | 621,601 | |

| Other liabilities and provision | 25 | 143,896 | 244,568 | |

| Shareholders' equity | 26 | 25,977,252 | 26,015,940 | |

| Share capital | 13,477,891 | 13,477,891 | ||

| Capital reserves | 380,629 | 384,311 | ||

| Profit reserves | 10,864,364 | 12,160,035 | ||

| Equity valuation adjustments | (3,313) | (3,313) | ||

| Treasury shares | (47,988) | (2,984) | ||

| Retained earnings | 1,305,669 | - | ||

See the accompanying notes to the individual and consolidated quarterly information.

| 4 |

| TIM S.A. | |||||||||

| STATEMENTS OF INCOME | |||||||||

| Periods ended September 30, 2024 and 2023 | |||||||||

| (In thousands of reais, unless otherwise indicated) | |||||||||

| Parent Company | |||||||||

| Notes | 3Q24 | September 2024 | 3Q23 | September 2023 | |||||

| Net revenue | 28 | 6,418,943 | 18,817,012 | 6,055,319 | 17,567,847 | ||||

| Costs of services provided and goods sold | 29 | (2,959,380) | (8,827,486) | (2,838,833) | (8,826,109) | ||||

| Gross income | 3,459,563 | 9,989,526 | 3,216,486 | 8,741,738 | |||||

| Operating revenues (expenses): | |||||||||

| Selling expenses | 29 | (1,510,611) | (4,472,387) | (1,435,297) | (4,176,711) | ||||

| General and administrative expenses | 29 | (430,763) | (1,319,767) | (441,435) | (1,308,030) | ||||

| Equity in earnings | 14 | (14,531) | (60,117) | (24,740) | 86,968 | ||||

| Other revenues (expenses), net | 30 | (72,473) | (218,924) | (96,142) | (272,707) | ||||

| (2,028,378) | (6,071,195) | (1,997,614) | (5,670,480) | ||||||

| Income before financial revenues and expenses | 1,431,185 | 3,918,331 | 1,218,872 | 3,071,258 | |||||

| Financial revenues (expenses): | |||||||||

| Financial revenues | 31 | 206,888 | 616,279 | 261,525 | 932,177 | ||||

| Financial expenses | 32 | (660,699) | (2,075,930) | (674,017) | (2,103,106) | ||||

| Net foreign exchange variations | 33 | (5,501) | 25,394 | 6,176 | 2,609 | ||||

| (459,312) | (1,434,257) | (406,316) | (1,168,320) | ||||||

| Profit before income tax and social contribution | 971,873 | 2,484,074 | 812,556 | 1,902,938 | |||||

| Income tax and social contribution | 8.d | (166,847) | (378,405) | (96,551) | (148,025) | ||||

| Net profit for the period | 805,026 | 2,105,669 | 716,005 | 1,754,913 | |||||

| Earnings per share attributable to the Company’s shareholders (expressed in R$ per share) | |||||||||

| Basic earnings per share | 34 | 0.32 | 0.87 | 0.30 | 0.72 | ||||

| Diluted earnings per share | 34 | 0.32 | 0.87 | 0.30 | 0.72 | ||||

See the accompanying notes to the individual and consolidated quarterly information.

| 5 |

| TIM S.A. | |||||

| STATEMENTS OF INCOME | |||||

| Period ended September 30, 2023 | |||||

| (In thousands of reais, unless otherwise indicated) | |||||

| Consolidated | |||||

| Notes | 3Q23 | September 2023 | |||

| Net revenue | 28 | 6,055,319 | 17,558,734 | ||

| Costs of services provided and goods sold | 29 | (2,838,833) | (8,583,065) | ||

| Gross income | 3,216,486 | 8,975,669 | |||

| Operating revenues (expenses): | |||||

| Selling expenses | 29 | (1,435,297) | (4,288,090) | ||

| General and administrative expenses | 29 | (441,435) | (1,309,616) | ||

| Equity in earnings | 14 | (24,740) | (66,419) | ||

| Other revenues (expenses), net | 30 | (96,142) | (274,335) | ||

| (1,997,614) | (5,938,460) | ||||

| Income before financial revenues and expenses | 1,218,872 | 3,037,209 | |||

| Financial revenues (expenses): | |||||

| Financial revenues | 31 | 261,525 | 952,926 | ||

| Financial expenses | 32 | (674,017) | (2,011,031) | ||

| Net foreign exchange variations | 33 | 6,176 | 2,609 | ||

| (406,316) | (1,055,496) | ||||

| Profit before income tax and social contribution | 812,556 | 1,981,713 | |||

| Income tax and social contribution | 8.d | (96,551) | (226,800) | ||

| Net profit for the period | 716,005 | 1,754,913 | |||

| Earnings per share attributable to the Company’s shareholders (expressed in R$ per share) | |||||

| Basic earnings per share | 34 | 0.30 | 0.72 | ||

| Diluted earnings per share | 34 | 0.30 | 0.72 | ||

See the accompanying notes to the individual and consolidated quarterly information.

| 6 |

| TIM S.A. | ||||||||

| STATEMENTS OF COMPREHENSIVE INCOME | ||||||||

| Periods ended September 30, 2024 and 2023 | ||||||||

| (In thousands of reais) | ||||||||

| Parent Company | ||||||||

| 3Q24 | September 2024 | 3Q23 | September 2023 | |||||

| Net profit for the period | 805,026 | 2,105,669 | 716,005 | 1,754,913 | ||||

| Other components of the comprehensive income | ||||||||

| Total comprehensive income for the period | 805,026 | 2,105,669 | 716,005 | 1,754,913 | ||||

See the accompanying notes to the individual and consolidated quarterly information.

| 7 |

| TIM S.A. and TIM S.A. and SUBSIDIARY | ||||

| STATEMENTS OF COMPREHENSIVE INCOME | ||||

| Period ended September 30, 2023 | ||||

| (In thousands of reais) | ||||

| Consolidated | ||||

| 3Q23 | September 2023 | |||

| Net profit for the period | 716,005 | 1,754,913 | ||

| Other components of the comprehensive income | ||||

| Total comprehensive income for the period | 716,005 | 1,754,913 | ||

See the accompanying notes to the individual and consolidated quarterly information.

| 8 |

| TIM S.A. | ||||||||||||||||||||

| STATEMENT OF CHANGES IN SHAREHOLDERS' EQUITY | ||||||||||||||||||||

| Period ended September 30, 2024 and 2023 | ||||||||||||||||||||

| (In thousands of reais) | ||||||||||||||||||||

| Profit reserves | ||||||||||||||||||||

| Share capital | Capital reserve | Legal reserve | Expansion reserve | Additional dividends/interest on shareholders’ equity proposed | Tax incentive reserve | Treasury shares | Equity valuation adjustments | Retained earnings | Total | |||||||||||

| Balances on January 1, 2024 | 13,477,891 | 384,311 | 1,380,427 | 7,107,369 | 1,310,000 | 2,362,239 | (2,984) | (3,313) | - | 26,015,940 | ||||||||||

| Total comprehensive income for the period | ||||||||||||||||||||

| Net profit for the period | - | - | - | - | - | - | - | - | 2,105,669 | 2,105,669 | ||||||||||

| Total contribution from shareholders and distribution to shareholders | - | - | - | - | - | - | - | - | - | - | ||||||||||

| Total comprehensive income for the period | - | - | - | - | - | - | - | - | - | - | 2,105,669 | 2,105,669 | ||||||||

| Total contribution from shareholders and distribution to shareholders | ||||||||||||||||||||

| Long-term incentive plan (note 27) | - | (3,682) | - | - | - | - | - | (3,682) | ||||||||||||

| Purchase of treasury shares, net of disposals | - | - | - | - | - | (45,004) | - | - | (45,004) | |||||||||||

| Allocation of net profit for the period: | ||||||||||||||||||||

| Interest on Shareholders’ Equity (note 26) | - | - | - | - | - | (800,000) | (800,000) | |||||||||||||

| Additional dividends/interest on shareholders’ equity distributed | - | - | - | (1,310,000) | - | - | - | - | - | (1,310,000) | ||||||||||

| Distribution of reserve for expansion (Note 26) | - | - | - | 1,310,000 | (1,310,000) | - | - | - | ||||||||||||

| Unclaimed dividends (Note 26) | - | - | - | 14,329 | - | - | 14,329 | |||||||||||||

| Total contribution from shareholders and distribution to shareholders | - | (3,682) | - | 14,329 | (1,310,000) | - | (45,004) | - | (800,000) | (2,144,357) | ||||||||||

| Balances at September 30, 2024 | 13,477,891 | 380,629 | 1,380,427 | 7,121,698 | - | 2,362,239 | (47,988) | (3,313) | 1,305,669 | 25,977,252 | ||||||||||

See the accompanying notes to the individual and consolidated quarterly information.

| 9 |

| TIM S.A. and TIM S.A. and SUBSIDIARY | ||||||||||||||||||||

| STATEMENT OF CHANGES IN SHAREHOLDERS' EQUITY | ||||||||||||||||||||

| Period ended September 30, 2023 | ||||||||||||||||||||

| (In thousands of reais) | ||||||||||||||||||||

| Profit reserves | ||||||||||||||||||||

| Share capital | Capital reserve | Legal reserve | Expansion reserve | Additional dividends/interest on shareholders’ equity proposed | Tax incentive reserve | Treasury shares | Equity valuation adjustments | Retained earnings | Total | |||||||||||

| Balances on January 01, 2023 | 13,477,891 | 408,602 | 1,250,448 | 7,540,020 | 600,000 | 2,124,411 | (163) | (3,844) | - | 25,397,365 | ||||||||||

| Total comprehensive income for the period | ||||||||||||||||||||

| Net profit for the period | - | - | - | - | - | - | - | - | 1,754,913 | 1,754,913 | ||||||||||

| Total contribution from shareholders and distribution to shareholders | - | - | - | - | - | - | - | - | - | - | ||||||||||

| Total comprehensive income for the period | - | - | - | - | - | - | - | - | - | - | 1,754,913 | 1,754,913 | ||||||||

| Total contribution from shareholders and distribution to shareholders | ||||||||||||||||||||

| Long-term incentive plan | - | (30,399) | - | - | - | - | - | (30,399) | ||||||||||||

| Purchase of treasury shares, net of disposals | - | - | - | - | - | (2,821) | - | - | (2,821) | |||||||||||

| Additional dividends/interest on shareholders’ equity distributed | - | - | - | (600,000) | - | - | - | - | - | (600,000) | ||||||||||

| Distribution of expansion reserve | - | - | - | 600,000 | (600,000) | - | - | - | ||||||||||||

| Allocation of net profit for the period: | ||||||||||||||||||||

| Interest on Shareholders’ Equity | - | - | - | - | - | (945,000) | (945,000) | |||||||||||||

| Total contribution from shareholders and distribution to shareholders | - | (30,399) | - | - | (600,000) | - | (2,821) | - | (945,000) | (1,578,220) | ||||||||||

| Balances at September 30, 2023 | 13,477,891 | 378,203 | 1,250,448 | 7,540,020 | - | 2,124,411 | (2,984) | (3,844) | 809,913 | 25,574,058 | ||||||||||

See the accompanying notes to the individual and consolidated quarterly information.

| 10 |

| TIM S.A. and TIM S.A. and SUBSIDIARY | |||||||

| STATEMENT OF CASH FLOWS | |||||||

| Periods ended September 30, 2024 and 2023 | |||||||

| (In thousands of reais) | |||||||

| Parent Company | Consolidated | ||||||

| Note | September 2024 | September 2023 | September 2023 | ||||

| Operating activities | |||||||

| Profit before income tax and social contribution | 2,484,074 | 1,902,938 | 1,981,713 | ||||

| Adjustments to reconcile income to net cash generated by operating activities: | |||||||

| Depreciation and amortization | 29 | 5,300,633 | 5,147,438 | 5,367,064 | |||

| Equity in earnings | 14 | 60,117 | (86,968) | 66,419 | |||

| Residual value of written-off property, plant and equipment and intangible assets | 8,350 | 12,079 | 89,153 | ||||

| Interest on asset retirement obligation | 8,722 | 28,150 | 33,325 | ||||

| Provision for legal and administrative proceedings | 24 | 217,032 | 258,903 | 258,900 | |||

| Inflation adjustment on judicial deposits and legal and administrative proceedings | 119,229 | 164,187 | 164,187 | ||||

| Interest, monetary and exchange rate variations on loans and other financial adjustments | 572,780 | 509,335 | 436,311 | ||||

| Yield from marketable securities | (123,049) | (41,926) | (41,926) | ||||

| Interest on lease liabilities | 32 | 1,072,860 | 831,677 | 730,103 | |||

| Lease interest | 31 | (21,204) | (20,935) | (20,935) | |||

| Provision for expected credit losses | 29 | 511,780 | 448,132 | 467,157 | |||

| Long-term incentive plans | 27 | 23,181 | (30,399) | (30,399) | |||

| 10,234,505 | 9,122,611 | 9,501,072 | |||||

| Decrease (increase) in operating assets | |||||||

| Trade accounts receivable | (1,071,311) | (561,642) | (602,238) | ||||

| Recoverable taxes, fees and contributions | 272,337 | 35,148 | 29,718 | ||||

| Inventories | (50,473) | (179,255) | (179,255) | ||||

| Prepaid expenses | (287,093) | (92,290) | (108,118) | ||||

| Judicial deposits | 34,648 | 15,777 | 15,777 | ||||

| Other assets | 41,146 | (104,571) | (98,492) | ||||

| Increase (decrease) in operating liabilities | |||||||

| Labor obligations | (2,928) | 35,114 | 35,114 | ||||

| Suppliers | (990,986) | (15,308) | (398,406) | ||||

| Taxes, fees and contributions payable | 332,075 | 466,740 | 437,476 | ||||

| Authorizations payable | (101,017) | (98,572) | (98,572) | ||||

| Payments for legal and administrative proceedings | 24 | (245,847) | (274,238) | (274,238) | |||

| Deferred revenues | (58,051) | (12,886) | (41,679) | ||||

| Other liabilities | (206,943) | (383,882) | (418,310) | ||||

| Cash generated by operations | 7,900,062 | 7,952,746 | 7,799,849 | ||||

| Income tax and social contribution paid | (89,892) | (228,184) | (228,184) | ||||

| Net cash generated by operating activities | 7,810,170 | 7,724,562 | 7,571,665 | ||||

| 11 |

| TIM S.A. and TIM S.A. and SUBSIDIARY | ||||||

| STATEMENT OF CASH FLOWS | ||||||

| Periods ended September 30, 2024 and 2023 | ||||||

| (In thousands of reais) | ||||||

| Parent Company | Consolidated | |||||

| Note |

September 2024 |

September 2023 |

September 2023

| |||

| Investment activities | ||||||

| Redemptions of marketable securities | 6,061,430 | 2,357,193 | 2,357,193 | |||

| Investments on marketable securities | (6,027,204) | (962,900) | (962,900) | |||

| Capital contribution 5G Fund | (131,348) | - | - | |||

| Cash from the acquisition of Cozani (Note 1) | - | 421,835 | - | |||

| Additions to property, plant and equipment and intangible assets | (3,175,860) | (3,212,417) | (3,212,417) | |||

| Other | 16,624 | 19,896 | 19,896 | |||

| Net cash used in investment activities | (3,256,358) | (1,376,393) | (1,798,228) | |||

| Financing activities | ||||||

| Additions of loans and financing | 503,351 | - | - | |||

| Amortization of loans | (1,287,585) | (177,786) | (177,786) | |||

| Interest paid- Loans | (92,229) | (134,636) | (134,636) | |||

| Payment of lease liability | (1,267,125) | (1,261,008) | (1,377,202) | |||

| Interest paid on lease liabilities | (1,083,355) | (995,448) | (1,068,135) | |||

| Lease incentives received | 79,557 | - | - | |||

| Derivative financial instruments | (128,641) | (196,406) | (196,406) | |||

| Purchase of treasury shares, net of disposals | (71,866) | (2,821) | (2,821) | |||

| Dividends and interest on shareholders’ equity paid | 26 | (1,996,520) | (1,756,352) | (1,756,352) | ||

| Net cash used in financing activities | (5,344,413) | (4,524,457) | (4,713,338) | |||

| Increase (decrease) in cash and cash equivalents | (790,601) | 1,823,712 | 1,060,099 | |||

| Cash and cash equivalents at the beginning of the period | 3,077,931 | 1,785,100 | 2,548,713 | |||

| Cash and cash equivalents at the end of the period | 2,287,330 | 3,608,812 | 3,608,812 | |||

See the accompanying notes to the individual and consolidated quarterly information.

| 12 |

| TIM S.A. | |||||

| STATEMENT OF VALUE ADDED | |||||

| Periods ended September 30, 2024 and 2023 | |||||

| (In thousands of reais) | |||||

| Parent Company | Consolidated | ||||

| September 2024 | September 2023 | September 2023 | |||

| Revenues | |||||

| Gross operating revenue | 27,129,493 | 24,648,229 | 24,686,630 | ||

| Losses on doubtful accounts | (511,780) | (448,132) | (467,157) | ||

| Discounts granted, returns and others | (5,318,008) | (4,382,739) | (4,383,342) | ||

| 21,299,705 | 19,817,358 | 19,836,131 | |||

| Inputs acquired from third parties | |||||

| Cost of services rendered and goods sold | (3,124,326) | (3,353,160) | (2,889,746) | ||

| Materials, energy, outsourced services and other | (2,835,989) | (2,892,244) | (2,963,600) | ||

| (5,960,315) | (6,245,404) | (5,853,346) | |||

| Retentions | |||||

| Depreciation and amortization | (5,300,633) | (5,147,438) | (5,367,064) | ||

| Net added value produced | 10,038,757 | 8,424,516 | 8,615,721 | ||

| Value added received in transfer | |||||

| Equity in earnings | (60,117) | 86,968 | (66,419) | ||

| Financial revenues | 812,088 | 1,073,256 | 1,094,005 | ||

| 751,971 | 1,160,224 | 1,027,586 | |||

| Total added value payable | 10,790,728 | 9,584,740 | 9,643,307 | ||

| Distribution of added value | |||||

| Personnel and charges | |||||

| Direct remuneration | 593,582 | 577,081 | 577,081 | ||

| Benefits | 207,130 | 179,070 | 179,070 | ||

| F.G.T.S | 58,606 | 56,334 | 56,334 | ||

| Other | 46,547 | 33,264 | 33,264 | ||

| 905,865 | 845,749 | 845,749 | |||

| Taxes, fees and contributions | |||||

| Federal | 2,211,041 | 1,807,709 | 1,953,277 | ||

| State | 2,238,027 | 1,941,146 | 1,945,846 | ||

| Municipal | 78,137 | 64,052 | 63,731 | ||

| 4,527,205 | 3,812,907 | 3,962,854 | |||

| Third-party capital remuneration | |||||

| Interest | 2,241,226 | 2,238,090 | 2,146,015 | ||

| Rents | 1,004,951 | 926,408 | 927,103 | ||

| 3,246,177 | 3,164,498 | 3,073,118 | |||

| Other | |||||

| Social investment | 5,812 | 6,673 | 6,673 | ||

| 5,812 | 6,673 | 6,673 | |||

| Shareholders’ Equity Remuneration | |||||

| Dividends and interest on shareholders’ equity | 800,000 | 945,000 | 945,000 | ||

| Retained earnings | 1,305,669 | 809,913 | 809,913 | ||

| 2,105,669 | 1,754,913 | 1,754,913 | |||

See the accompanying notes to the individual and consolidated quarterly information.

| 13 |

2024 THIRD QUARTER RESULTS

|

| 14 |

2024 THIRD QUARTER RESULTS

|

| 15 |

2024 THIRD QUARTER RESULTS

|

EVENTS OF THE QUARTER AND SUBSEQUENT EVENTS

[1] Nominal value.

| 16 |

2024 THIRD QUARTER RESULTS

|

FINANCIAL PERFORMANCE

OPERATING REVENUE

REVENUE GROWING AT A HEALTHY PACE TO MEET 2024 GOALS

* Net Revenue normalized by the temporary effect from the inefficiency of PIS/COFINS arising from a contract signed between TIM S.A and Cozani (+R$41.0 million in 1Q23). The merger of Cozani into TIM S.A. became effective on April 01, 2023.

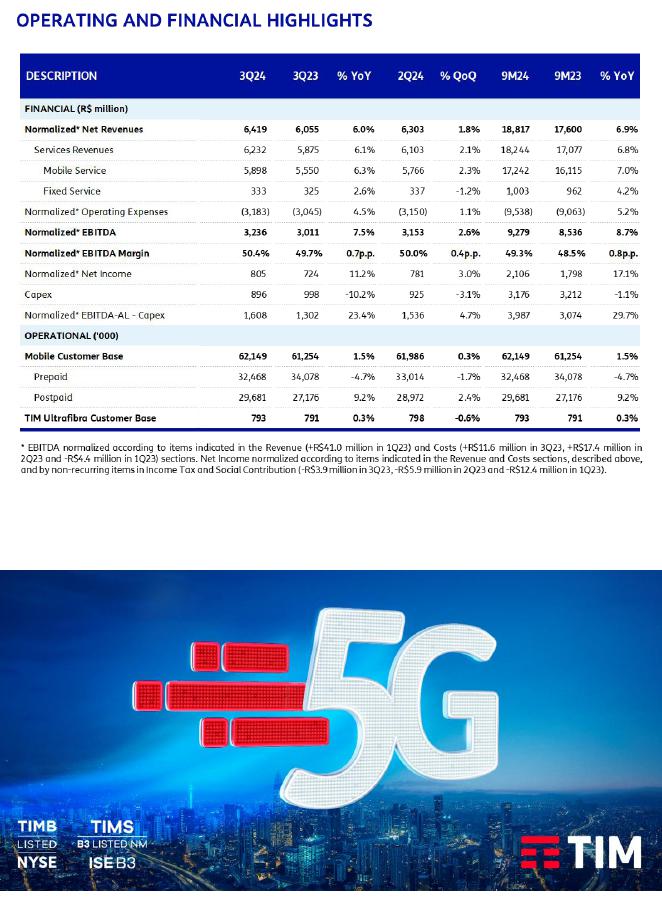

In 3Q24, Normalized Net Revenue grew by 6.0% YoY, totaling R$6,419 million. This result was mainly due to the expansion in Mobile Service Revenue, which increased by 6.3% YoY, leveraged by Postpaid, which grew by 8.3% YoY in 3Q24. In 9M24, revenue dynamics were similar, with Normalized Net Revenue increasing by 6.9% YoY and Mobile Service Revenue growing 7.0% YoY.

| 17 |

2024 THIRD QUARTER RESULTS

|

Breakdown of the Mobile Segment (net of taxes and deductions):

Normalized Mobile Service Revenue (“MSR”) amounted to R$5,898 million in 3Q24, corresponding to a 6.3% YoY expansion, benefited mainly by the positive performance in Postpaid which reflects a smarter management of the customer base amid a less pronounced annual price adjustment dynamic in 2024 compared to 2023. The following factors stand out for this performance: (i) the migration of customers to higher value-added plans (Prepaid-Postpaid and Pospaid-Postpaid); and (ii) efforts to reduce disconnection rates (Postpaid Churn ex-M2M of -0.7% in 3Q24). Normalized Mobile ARPU (average monthly revenue per user) reached R$31.7, representing an increase of 4.8% YoY. In 9M24, Normalized MSR grew by 7.0% YoY.

In 3Q24, Client Generated Revenue (MSR excluding interconnection, customer platform and other revenues) reached R$5,477 million, up by 6.5% YoY. This performance was explained by the recurring growth in revenue generated by TIM Customers and an increase in revenue from non-TIM Customers, benefited by the performance of TIM Viagem packages after the reformulation of the international roaming portfolio in September 2023. In 9M24, Client Generated Revenue grew by 7.5% YoY.

In 3Q24, Interconnection (ITX) Revenue dropped by 21.9% YoY, which was already expected and in line with the reduction in MTR (“Mobile Termination Rate”) rate and lower incoming traffic. In 9M24, this line fell by 18.6% YoY.

Customer Platform Revenue was R$40 million in 3Q24, compared to R$54 million in 3Q23, falling by 26.7% YoY. The reduction is explained by the Company's operating model which encompasses an activation fee-based model for some segments and a revenue share model for others. On the positive side, the Mobile Advertising and Data Monetization initiatives also stood out, growing robust double digits YoY for another quarter. In 9M24, the line reached R$101 million, down by 17.0% for the same reasons.

The Other Normalized[2] Revenue line increased by 21.7% YoY in 3Q24, mainly due to higher revenues from IoT projects for the agribusiness. In 9M24, this line increased by 13.0% YoY.

Below is the performance breakdown of each mobile customer profile:

| (i) | Postpaid Revenue increased by 8.3% YoY in 3Q24, with Postpaid ARPU reaching R$43.3 in the quarter (-0.9% YoY) and Postpaid ex-M2M ARPU reaching R$53.2 (+0.7% YoY). This performance is explained by: (i) the annual price adjustments for part of the Postpaid customer base, but at a lower percentage than in 2023; (ii) efforts to migrate customers to higher-value plans; and (iii) the Company’s success in reducing churn rates .. In 9M24, Postpaid Revenue increased by 8.6% YoY. |

[2] The Other Revenues line had a non-recurring impact of R$41.0 million in 1Q23, referring to the temporary effect of the inefficiency of PIS/COFINS, arising from a contract signed between TIM S.A and Cozani, which was extinguished with the merger Cozani.

| 18 |

2024 THIRD QUARTER RESULTS

|

| (ii) | Prepaid Revenue declined by 5.1% YoY in 3Q24, with Prepaid ARPU reaching R$14.9 (-0.3% YoY). Excluding Interconnection Revenue, Prepaid Revenue would have declined by 4.3% YoY. This performance in Prepaid continues to be impacted by: (i) the consecutive increases in customer migration from Prepaid to Postpaid; and (ii) lower recharging recurrences in certain customer groups. In 9M24, Prepaid Revenue fell by 2.1% YoY. |

Breakdown of the Fixed Segment (net of taxes and deductions):

In 3Q24, Fixed Service Revenue amounted to R$333 million, up by 2.6% YoY. In 9M24, Fixed Service Revenue grew by 4.2% YoY.

| TIM Ultrafibra, the main line for the fixed segment, grew by 6.0% YoY in 3Q24, with ARPU of R$99.0 (+5.9% YoY). This performance reflects the Company's strategy to carry out a more selective expansion of TIM Ultrafibra, which arrived in the state of Rio Grande do Sul, covering 28 new municipalities in 3Q24. It is worth mentioning that FTTH (Fiber-to-the-Home) already accounts for over 94% of our total broadband customer base. In 9M24, TIM Ultrafibra Revenue increased by 7.7% YoY. |  |

Details of Product Revenue (net of taxes and deductions):

Product Revenue expanded 3.5% in 3Q24 and 9.6% YoY in 9M24. In 9M24 the performance is explained by:(i) an increase in the volume of device sales; (ii) the sale of accessories (cases, screen protectors, etc.) for phones; (iii) an increase in sales of other equipment such as wearables and modules related to "B2B IoT," reinforcing the Company's portfolio diversification strategy.

| 19 |

2024 THIRD QUARTER RESULTS

|

OPERATING COSTS AND EXPENSES

EFFICIENT MANAGEMENT OF COSTS AND EXPENSES THAT CONTINUE TO GROW PRACTICALLY IN LINE WITH INFLATION IN THE PERIOD

* Operating Costs normalized by: expenses with consulting within the scope of the acquisition project of Oi Móvel and customer migration (+R$2.1 million in 3Q23, +R$16.3 million in 2Q23 and +R$12.5 million in 1Q23), PIS/COFINS credits generated in the intercompany contract with Cozani (-R$17.7 million in 1Q23), expenses with FUST/FUNTEL related to the intercompany contract with Cozani (+R$886k in 1Q23), expenses with specialized legal and administrative services (+R$1.1 million in 2Q23) and payroll expenses related to the acquisition of Oi Mobile (+R$8.4 million in 3Q23).

Normalized Operating Costs and Expenses was R$3,183 million in 3Q24, up by 4.5% YoY, practically in line with inflation in the period (in September, the accumulated 12-month IPCA was 4.42%), reflecting the Company’s efficient cost management. This line was negatively affected by these key items: (i) higher interconnection expenses, related to international roaming services and costs related to network; and (ii) higher advertising expenses due to the campaigns for TIM Pré XIP and Rock in Rio. In 9M23, Normalized Operating Costs and Expenses grew 5.2% YoY.

Breakdown of Normalized Costs and Expenses Performance:

Normalized Personnel costs[3] grew by 7.4% YoY in 3Q24, impacted by annual salary adjustments and improved benefits, which were partially offset by the drop in expenses related to long-term incentives. In 9M24, this line increased by 8.3%, also due to the salary increases and improved benefits, in addition to provisions for expenses related to employee profit-sharing in the Company's results.

The Selling and Marketing line increased by 4.0% YoY in 3Q24, mainly due to higher advertising expenses related to the launch of TIM Pré XIP and the Rock in Rio campaigns. In 9M24, this cost line increased slightly, by 1.8% YoY, reflecting the increases in advertising expenses, as previously mentioned, and was partially offset by the recognition of Fistel credits, which had a positive effect in the 9M23 results.

[3] In 3Q23, the Personnel costs line had a non-recurring impact of R$8.4 million referring to payroll expenses related to the acquisition of Oi's mobile assets.

| 20 |

2024 THIRD QUARTER RESULTS

|

The Normalized Network and Interconnection group[4] increased by 9.2% YoY in 3Q24, due to: (i) higher expenses for international roaming services, still reflecting the increase in traffic volume after the strategy to reformulate the Postpaid portfolio in September 2023; and (ii) higher spending related to network infrastructure. These amounts were partially offset by lower expenses with content providers and leased lines. In 9M24, this line grew by 10.8% YoY.

Normalized General and Administrative Expenses (G&A)[5] fell by 0.7% YoY, totaling R$214 million in 3Q24, mainly due to customer billing digitalization initiatives. This reduction was partially offset by higher software maintenance expenses related to the cloud migration project and third-party services. In 9M24, this line fell by 2.8% for the same reasons.

The Cost of Goods Sold (COGS) line declined by 2.5% YoY in 3Q24,due to more efficient inventory management. In 9M24, COGS grew by 5.6%, in line with the same growth levels for sales of devices, mainly in 2Q24.

The Bad Debt line grew by 7.6% YoY in 3Q24, due to the growth in the Postpaid revenue base. Despite this increase, the Bad Debt over Gross Revenue ratio remains healthy, corresponding to 1.9% (compared to 1.9% in 3Q23). In 9M24, this expense line increased by 9.6% YoY.

Other Normalized[6] Operating Expenses (Income) fell by 24.6% YoY in 3Q24, mainly due to lower provisions for tax contingencies and lower expenses with civil lawsuits. In 9M24, this cost line fell by 19.9% YoY, for the same reasons.

[4] The Network and Interconnection line had a non-recurring impact of R$2.1 million in 3Q23, R$16.3 million in 2Q23 and R$12.5 million in 1Q23, referring to consulting expenses within the scope of the migration project for customers arriving from Oi, and -R$17.7 million in 1Q23, referring to PIS/COFINS credits generated in the intercompany contract with Cozani.

[5] The G&A expenses line was impacted by non-recurring items, in the amount of R$1.1 million in 3Q23 and R$1.1 million in 2Q23, referring to expenses with specialized legal and administrative services for the acquisition of Oi’s assets.

[6] The Other Operating Expenses (Revenues) line had a non-recurring impact of R$886k in 1Q23, referring to expenses with FUST/FUNTEL.

| 21 |

2024 THIRD QUARTER RESULTS

|

FROM EBITDA TO NET INCOME

EBITDA AND MARGINS CONTINUE TO EVOLVE AND SUSTAIN THE NET PROFIT EXPANSION

* Normalized EBITDA according to the items described in the Revenue section (+R$41.0 million in 1Q23) and Costs (+R$11.6 million in 3Q23, +R$17.4 million in 2Q23 and -R$4.4 million in 1Q23). Normalized Net Income according to the items described in the Revenue and Costs sections, as described previously, and by non-recurring items in Income Tax and Social Contribution: tax credits related to the intercompany contract with Cozani (-R$8.2 million in 1Q23) and other tax effects (-R$3.9 million in 3Q23, -R$5.9 million in 2Q23, -R$4.2 million in 1Q23).

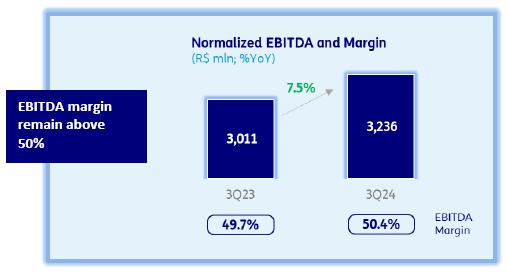

EBITDA[7] (Earnings Before Interest, Taxes, Depreciation, Amortization and Equity in Earnings)

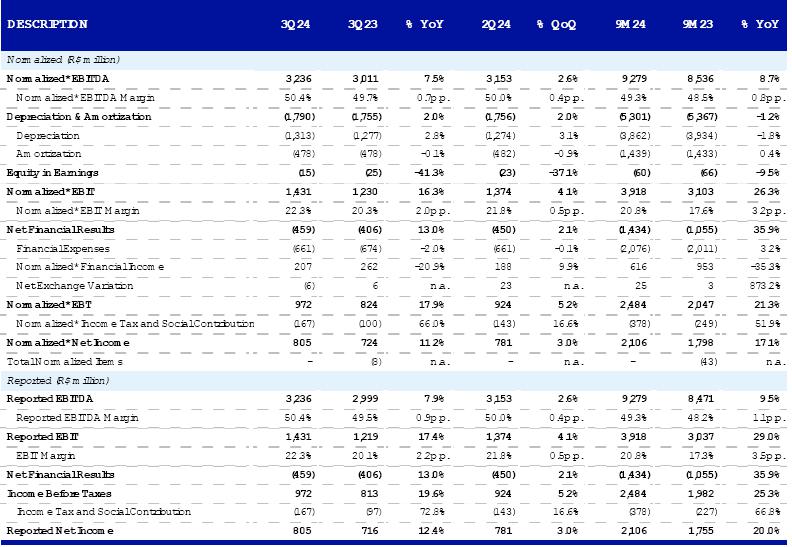

Normalized EBITDA reached R$3,236 million in 3Q24, up by 7.5% YoY, as a result of the positive Service Revenue performance and ongoing cost control initiatives. This improvement allowed the Normalized EBITDA Margin to reach higher levels, of 50.4% in the quarter, expanding by 0.7 p.p. YoY. In 9M24, Normalized EBITDA grew by 8.7% YoY, reaching a Margin of 49.3% (+0.8 p.p. YoY).

[7] EBITDA is normalized according to the items described in the “Revenue” and “Costs” sections.

| 22 |

2024 THIRD QUARTER RESULTS

|

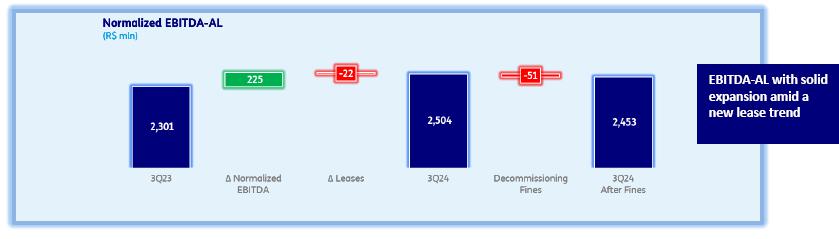

Considering the effects of the leases on EBITDA, the Normalized EBITDA-AL (“After Lease”)[8] (excluding impacts from fines related to the site decommissioning process[9]) grew by 8.8% YoY in 3Q24, totaling R$2,504 million, with a margin of 39.0%, an increase of 1.0 p.p. YoY. This growth reflects the Company's consistent operational performance, despite the increase in recurring leases QoQ, which were impacted by: (i) lower levels of incentives arising from contractual negotiations; and (ii) an expected increase in new towers and the beginning of solar plants rental. In 9M24, Normalized EBITDA-AL grew by 13.9% YoY, totaling R$7,162 million.

[8] EBITDA-AL is normalized according to items described in the “From EBITDA to Net Income” section and excludes the impact of the fines related to the decommissioning process of the sites. For additional details, access Exhibit 5 – EBITDA After Lease.

[9] Site decommissioning is the process of deactivation of towers and transmission structures through renegotiation and/or cancellation of lease contracts with tower companies. After the acquisition of Oi Mobile, the Company is working to disconnect approximately 60% of the sites that overlap or are close to sites where TIM was already present.

| 23 |

2024 THIRD QUARTER RESULTS

|

DEPRECIATION AND AMORTIZATION (D&A) / EBIT

The D&A line increased by 2.0% YoY in 3Q24, mainly driven by the combination of the following: (i) a higher depreciation for the network infrastructure and telecommunications equipment arising from investments made during the year to expand 5G; (ii) partially offset by a lower depreciation on IFRS 16 lease rights due to the sites decommissioning process. In 9M24, the D&A line fell by 1.2% YoY.

Normalized EBIT increased by 16.3% YoY in 3Q24, with a margin of 22.3%, reflecting the strong EBITDA growth in the period. In 9M24, Normalized EBIT increased by 26.3% YoY, achieving a margin of 20.8%.

NET FINANCIAL RESULT

In 3Q24, the Net Financial Result was negative by R$459 million, worsening by R$53 million from 3Q23. This result can be explained by factors that positively affect results in 3Q23, such as: (i) a negative impact from the annual comparison for interest on leases due to a more significant reduction in 3Q23, when lease contracts were renegotiated, in line with the decommissioning process for sites; (ii) lower monetary update on contingencies contributing to the performance of the other line in non-cash items; and (iii) a negative impact from non-cash items in mark-to-market for C6 due to the recognition, in 3Q23, of the achievement of a new contractual tranche of the bank’s subscription bonus. In 9M24, this line worsened by 35.9% YoY, mainly impacted by non-cash items: (i) a lower mark-to-market of derivatives; (ii) termination of capitalization on license interest; and (iii) a positive effect, in 1Q23, related to the renegotiation of lease tower contracts.

| 24 |

2024 THIRD QUARTER RESULTS

|

INCOME TAX AND SOCIAL CONTRIBUTION

Income Tax and Social Contribution (IR/CSLL), in the Normalized[10] view, was -R$167 million in 3Q24, compared to -R$100 million in 3Q23, corresponding to an effective rate of -17.2% against -12.2% in 3Q23. This variation reflects the higher amounts of Interest on Capital declared in 3Q23, totaling R$425 million, compared to R$300 million in 3Q24. In 9M24, the Income Tax and Social Contribution line was -R$378 million, reaching an effective rate of -15.2%.

NET INCOME

Normalized Net Income[11] reached R$805 million in 3Q24 (+11.2% YoY), maintaining a double-digit annual growth for the 6th consecutive quarter and reaching the highest net income level recorded by the Company in a third quarter. As a result, Normalized Earnings per Share (EPS) for the quarter reached R$0.33 vs. R$0.30 in 3Q23. In 9M24, Normalized Net Income expanded by 17.1% YoY, with an EPS of R$0.87.

INVESTMENTS, CASH FLOW AND DEBT

THE EFFICIENT ALLOCATION OF INVESTMENTS ENABLES A HEALTHY CASH GENERATION AIMING AT DELIVERING THE GUIDANCE TARGETS

CAPEX

[10] The Income Tax and Social Contribution line had a non-recurring impact of -R$ 8.2 million in 1Q23, related to tax credits with the Cozani intercompany contract, and of -R$3.9 million in 3Q23, -R$5.9 million in 2Q23 and -R$4.2 million in 1Q23, related to other tax effects.

[11] Net Income is normalized according to items in the “From EBITDA to Net Income” section.

| 25 |

2024 THIRD QUARTER RESULTS

|

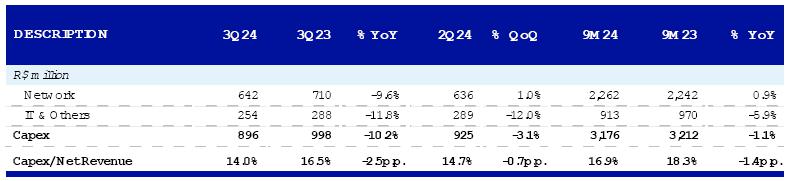

Capex amounted to R$896 million in 3Q24, a decrease of 10.2% YoY due to higher investments in network and IT infrastructure carried out by the Company in the same period of the previous year. Nevertheless, TIM continues to invest in the expansion of its 5G network, adding coverage to 142 new municipalities in the third quarter of 2024. The Total Capex over Normalized Net Revenue ratio reached 14.0% in 3Q24, compared to 16.5% in 3Q23 (falling by 2.5 p.p.). In 9M24, Capex fell by 1.1% YoY, reaching R$3,176 million. It is worth noting that the Company’s guidance for 2024 remains unchanged, with Capex guidance already disclosed between R$4.4 billion and R$4.6 billion.

CASH FLOW

Normalized EBITDA (-) Capex amounted to R$2,340 million in 3Q24, up by 16.3% YoY. Returning the effects from leases, Normalized EBITDA-AL[12] (-) Capex reached R$1,608 million, maintaining solid a double-digit growth pace (+23.4% YoY). Both results were achieved due to the consistent EBITDA growth and lower Capex levels. The Normalized EBITDA-AL (-) Capex over Normalized Net Revenue ratio reached 25.0% in the quarter. In 9M24, Normalized EBITDA (-) Capex grew by 14.6% YoY and Normalized EBITDA-AL (-) Capex increased 29.7% YoY (representing 21.2% of Normalized Net Revenue).

* The Company recognized incentives on lease payments received in line with the agreed contractual conditions, reducing the amount disbursed in the period (+R$14.1 million in 3Q24, +R$31.6 million in 3Q24, +R$31.6 million in 2Q24 and +R$33.9 million in 1Q24).

[12] EBITDA-AL is normalized according to items described in the “From EBITDA to Net Income” section and excludes the impact of the fines related to the decommissioning process of the sites. For additional details, access Exhibit 5 – EBITDA After Lease.

| 26 |

2024 THIRD QUARTER RESULTS

|

Operating Free Cash Flow (“OpFCF”) totaled R$1,743 million in 3Q24, increasing by R$288 million (+19.8% YoY) from 3Q23, primarily due to the improvement in Reported EBITDA (-) Capex, which increased by 16.9% YoY. The variation in working capital returned to a positive level, as expected by the Company, but, despite that, it declined by R$75 million from 3Q23. This performance is explained by: (i) the “Trade Accounts Receivable” line, which was impacted by new revenue lines; (ii) the “Suppliers” line, which was impacted by the mix between operating costs and Capex; (iii) partially offset by the “Other Liabilities” line, which has been reducing since last year due to payments to third parties that carried out the shutdown of towers. In 9M24, OpFCF grew by 27.2% YoY, due to the improvement in operating performance and reduction in lease payments.

It is worth highlighting that the full payment of the TFF (Operating Inspection Fee), which makes up the Fistel rate, has been suspended since 2020. The total amount registered, until September 30, 2024, was R$3.2 billion, of which R$2.5 billion was principal and R$659 million in late interest payments.

DEBT AND CASH

Debt Profile

| 27 |

2024 THIRD QUARTER RESULTS

|

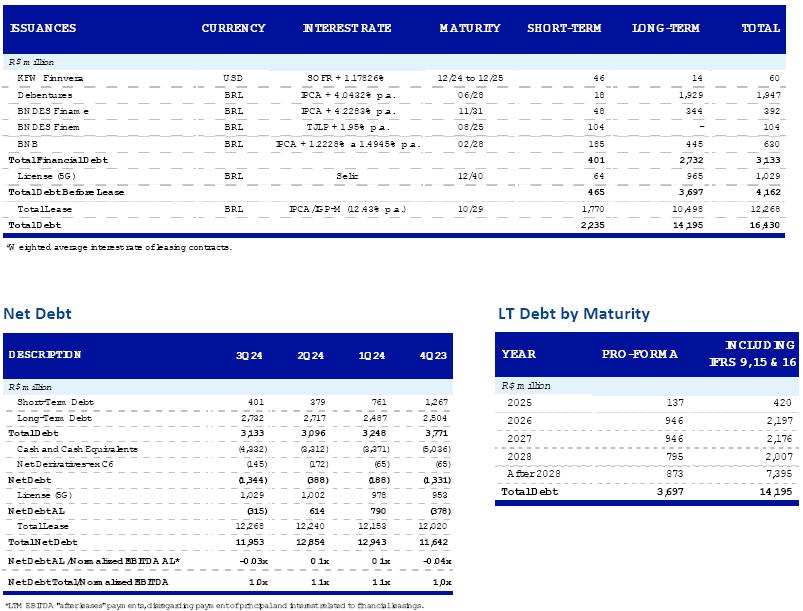

Total Debt (post-hedge) amounted to R$16,285 million at the end of September 2024, down by R$1,976 million over 3Q23. This decrease reflects mainly: (i) the settlement of a portion of the short-term financial debt; and in a lower proportion (ii) the reduction in total leases, due to the decommissioning of sites.

The Cash and Securities balance totaled R$4,332 million at the end of September 2024, representing a decrease of 2.6% YoY. The disbursements made in the last 12 months, mainly those related to the settlement of a part of the short-term financial debt, were partially offset by the Company's solid operational performance in the period.

OPERATIONAL PERFORMANCE

MOBILE SEGMENT:

In 3Q24, TIM recorded 62.1 million mobile lines, representing a net addition of 895k new lines in the last 12 months and 163k new lines in the quarter. This result was driven by the Postpaid segment, which grew 9.2% YoY, totaling 29.7 million customers, an increase of more than 2.5 million customers in the last 12 months and 709k in 3Q24. Of these, 23.9 million were in Human Postpaid (+7.6% YoY). The Prepaid segment totaled 32.5 million customers, down by 4.7% YoY, impacted by the migration of customers from the Prepaid to Postpaid.

FIXED SEGMENT:

TIM Ultrafibra’s customer base reached 793k connections in 3Q24, practically flat in the annual comparison (+0.3% YoY). This performance reflects the Company’s strategy of being more selective in its geographic expansion. Even so, the FTTH base, which represents the main portion of its broadband services, added 744k new customers in 3Q24, an increase of 7.5% YoY.

| 28 |

2024 THIRD QUARTER RESULTS

|

CUSTOMER PLATFORM

The Customer Platform aims to monetize the company's customer base and increase customer loyalty through the observation of market trends and innovative partnerships. This initiative is enabled by two business models:

| I. | Commercial Partnerships with: |

| (i) | direct remuneration for the sale of advertising and data intelligence where the main products are TIM Ads and TIM Insights. We maintained a YoY growth in 3Q24, driven by recurring campaigns from relevant advertisers and the entry of new brands. We also launched the initial campaigns for external inventories, expanding our operations in the Retail Media model; |

| (ii) | remuneration for data products, through financial scores and standardized validation/authentication products to improve the digital security of our users. In 3Q24, we maintained a recurring growth in profitability of financial scoring solutions and Open Gateway products. Additionally, we performed over 78 million queries in the quarter, demonstrating our data processing capacity. |

| II. | Strategic Partnerships. In this model, in addition to TIM Ads and TIM Insights, we use the segmentation capacity of our base, combined with the strength of the TIM brand to endorse the partner brand, encouraging consumers to adopt the products of our strategic partners with exclusive offers for TIM customers. In this case, TIM's remuneration is linked to the success of this adhesion and comprised of a CAC fee and an equity stake in partner companies. |

| II. |

Within this strategy, some verticals were listed as having a great opportunity for synergy with mobile services and a market valuation higher than those of telecom companies. Below are details of the verticals in which we are already operating:

FINANCIAL SERVICES

In 2020, the Company concluded negotiations with C6 Bank and launched exclusive offers for TIM customers who opened accounts with the bank and used its services. In this contract, TIM receives remuneration for active accounts and the option to obtain equity participation in C6 Bank as certain goals are achieved, with the number of shares received for each goal achieved varying throughout the contract.

On February 01, 2021, TIM announced, within the scope of this partnership, that it obtained the right to exercise a subscription warrant equivalent to an indirect equity stake of approximately 1.44% of Banco C6’s share capital arising from the achievement, in December 2020, of the 1st level of the agreed targets. Subsequently, the Company exercised its option to acquire and convert shares issued by Banco C6, representing 1.44% of the Bank’s capital. It is important to highlight that when said option was exercised, TIM gained a minority equity stake without a controlling position or significant influence over the management of Banco C6.

| 29 |

2024 THIRD QUARTER RESULTS

|

In addition, TIM holds stock subscription options, which represent the Company's option to subscribe for 4.62% of C6's shares on September 30, 2024. Considering what has already been exercised, plus the options, TIM's potential stake in C6 Bank could reach approximately 6.06%, subject to the ongoing arbitration dispute. More details can be found in Notes 12, 31 and 37 of the ITR.

EDUCATION SERVICES

In the Education pillar, the partnership with Descomplica has already surpassed 700k subscribers in various courses such as ENEM preparatory courses, free courses, and undergraduate and postgraduate programs. Free courses focused on technology, such as ChatGPT and Artificial Intelligence for Non-Technicians, have already reached +130k subscribers in 2024.

HEALTH SERVICES

In the Health pillar, the Company operates a partnership with Cartão de Todos, with over 193k of TIM’s customers registered in the platform as of September 2024, with more than 64k of these subscriptions from the Prepaid, Control and Postpaid plans. TIM customers are still exempt from the membership fee, and those in the Control and Postpaid segment are entitled to 3 months of free monthly payments.

ENVIRONMENTAL, SOCIAL & GOVERNANCE

3Q24 HIGHLIGHTS

| o | For the fourth consecutive year, TIM has been recognized as one of the most diverse and inclusive companies in the world, earning the 1st global Telecom position in the FTSE Russell D&I Index 2024 (formerly the Refinitiv D&I Index). The index is one of the main tools used by investors around the world to identify companies with advanced practices in this area. Another important recognition for the company was its selection, for the second year running, to make up the IDIVERSA portfolio, a B3 index that assesses the representation of black people and women in the company and in leadership and non-leadership positions in Brazil. |

| o | In line with its commitment to tackling violence against women, TIM continues to make progress, in partnership with the Positive Women platform, with the Caminho Delas project. After transforming its 158 own stores in Brazil into safe places for women in situations of risk, the initiative has now reached the operator's resellers, expanding to a further 43 points in the states of Rio de Janeiro, São Paulo, Pernambuco, Minas Gerais and Paraíba. For this expansion, 350 employees from these establishments were trained by the startup Livre de Assédio, which supports the prevention of sexual harassment, moral harassment and discrimination. |

| 30 |

2024 THIRD QUARTER RESULTS

|

| o | TIM launched the AI Academy to train its approximately 10,000 employees in Artificial Intelligence. The initiative reinforces the company's commitment to innovation and the development of new skills. Created in partnership with companies from the Education and AI ecosystem, such as: Exame, FIAP, Alura, Google, Microsoft, among others, the academy will offer a multi-format learning journey on behavioral and technical topics that will enable the use of technology to leverage business challenges. The operator has already identified more than 100 use cases that will be leveraged by AI. |

| o | Instituto TIM, in partnership with the NGO One By One, graduated the first class of 2024 from the Exponential Education program, a technological education project aimed at disabled children and young people supported by the organization and their families. Throughout the training, the 41 students of varying ages were able to develop entrepreneurial skills using a variety of tools. |

| o | Bateria do Instituto TIM, made up of children, young people and adults with and without disabilities, ended another cycle of training for its more than 50 members in September. The project offered free music and singing lessons, as well as psychological support, in 34 weekly meetings at the Centro da Música Carioca. Performances open to the public include the TIM Music Rio festival in Copacabana and the Mini Bloco pre-carnival in Tijuca. |

| o | Instituto TIM's Edital Fortalecendo Redes has shown promising results in the development of the 10 organizations selected from the Gerando Falcões Network. In the first half of 2024, significant institutional strengthening was observed, with several nonprofit organizations expanding their digital presence and improving their operations. Some actions had a direct impact on the communities served, such as the more efficient management achieved by Cores do Mará (MA), due to a better structuring of its operations and the hiring of specialized professionals. Each organization received 100,000 reais and around 9,000 people will be impacted by the organization’s actions. |

| o | For the second year in a roll, TIM was voted the best company in the Technology and Telecommunications sector in Exame's Best and Biggest 2024 awards, one of the most recognized economic and business awards in Brazil. With more than a thousand companies from different sectors taking part, only 15 were awarded, with TIM being the only one in its sector. |

| o | In the 3rd quarter, TIM incorporated eight new plants into its operation as part of the evolution of the Distributed Generation Project (DG), totaling more than 120 units. The project is responsible for promoting the supply of the network using renewable energy plants, with a predominance of solar plants. The expectation is that by the end of 2024, about 60% of the energy used by the company will come from DG, reaching a total of 134 plants, which will serve 25 states. |

| 31 |

2024 THIRD QUARTER RESULTS

|

| o | TIM ended the 1st quarter with 1,860 active biosites on its network. These structures, similar to a common pole, are a solution for densifying the mobile access network (antennas/towers) with a very low visual and urban impact, lower cost and quick installation. |

More information on TIM's ESG actions can be accessed in the Quarterly Report, available on the Investor Relations website.

| 32 |

2024 THIRD QUARTER RESULTS

|

DISCLAIMER

The consolidated financial and operating information disclosed in this document, except where otherwise indicated, is presented in accordance with the International Financial Reporting Standards (IFRS) and in Brazilian Reais (R$), in compliance with the Brazilian Corporate Law (Law 6,404/76). Comparisons refer to the third quarter of 2024 (“3Q24”) and the first nine months of 2024 (“9M24”), except when otherwise indicated.

This document may contain forward-looking statements. Such statements are not statements of historical fact and reflect the beliefs and expectations of the Company's management. The words “anticipates”, “believes”, “estimates”, “expects”, “forecasts”, “plans”, “predicts”, “projects”, “targets” and similar words are intended to identify these statements, which necessarily involve known and unknown risks and uncertainties foreseen, or not, by the Company. Therefore, the Company’s future operating results may differ from current expectations and readers of this report should not base their assumptions exclusively on the information given herein. Forward-looking statements only reflect opinions on the date on which they are made and the Company is not obliged to update them in light of new information or future developments.

Exhibits

Exhibit 1: Operating Indicators

| 33 |

2024 THIRD QUARTER RESULTS

|

EXHIBIT 1 – TIM S.A.

Operating Indicators

| 34 |

TIM S.A.

NOTES TO THE QUARTERLY INFORMATION - continued September 30, 2024 (In thousands of reais, unless otherwise indicated)

|

| 1. | Operations |

1.1. Corporate Structure

TIM S.A. (“TIM” or “Company”) is a public limited company with Registered office in the city of Rio de Janeiro, RJ, and a subsidiary of TIM Brasil Serviços e Participações S.A. (“TIM Brasil”). TIM Brasil is a subsidiary of the Telecom Italia Group that holds 66.59% of the share capital of TIM S.A on September 30, 2024 (66.59% on December 31, 2023).

The TIM group (“Group”) comprises TIM and its associated company I-Systems.

The Company holds an authorization for Landline Switched Telephone Service (“STFC”) in Local, National Long-Distance and International Long-Distance modes, as well as Personal Mobile Service (“SMP”) and Multimedia Communication Service (“SCM”), in all Brazilian states and in the Federal District.

The Company’s shares are traded on B3 – Brasil, Bolsa, Balcão (“B3”). Additionally, TIM has American Depositary Receipts (ADRs), Level II, traded on the New York Stock Exchange (NYSE) – USA. As a result, the company is subject to the rules of the Brazilian Securities and Exchange Commission (“CVM”) and the Brazilian Securities and Exchange Commission (“SEC”). In order to comply with good market practices, the company adopts as a principle the simultaneous disclosure of its financial information in both markets, in reais, in Portuguese and English.

As of September 30, 2024, TIM holds a 49% equity interest (49% as of December 31, 2023) in the company I-Systems (associated company) and held 100% on December 31, 2022 in the company Cozani RJ Infraestrutura e Rede de Telecomunicações S.A. (“Cozani”) - subsidiary. Considering that the merger by TIM, through Act 3,535/2023, which transferred the SMP grants associated with it, and its consequent extinction, for all purposes and effects, on April 1, 2023, consequently, TIM S.A., does not have equity interests in Cozani on September 30, 2024.

1.2. Corporate Reorganization

1.2.1. Business combination - Cozani

On April 20, 2022, TIM, together with other Buyer companies (Claro S.A. and Telefônica Brasil S.A.), after complying with the prior conditions established by CADE and ANATEL, concluded the acquisition transaction of Oi Móvel S.A. – Under Court-Ordered Reorganization (“Seller”, “Assignor” or “Oi Móvel”). Due to this, TIM now holds 100% of Cozani’s share capital, a company that corresponds to the part of the unit of assets, rights and obligations of Oi Móvel acquired by Company.

The total consideration recorded for the acquisition of Cozani was R$ 7,211.6 million.

TIM also paid, on April 20, 2022, on behalf of SPE Cozani, the amount of R$ 250.7 million to the Seller, as remuneration, for up to 12 months of service provision in the transition phase, recorded under “Prepaid expenses” and signed an annual contract term for the use of transport infrastructure capacity with Brasil Telecom Comunicação Multimídia S.A., involving the payment of decreasing amounts which, at present value, total approximately R$ 476 million.

| 35 |

TIM S.A.

NOTES TO THE QUARTERLY INFORMATION - continued September 30, 2024 (In thousands of reais, unless otherwise indicated)

|

Considering the agreed purchase amounts, we had the following balances recorded as contractual obligations on December 31, 2022:

| (i) | The amount of R$ 634.3 million was withheld by TIM, as provided for in the purchase agreement, mainly to meet the possible need for additional price adjustments to be made, which could be identified in the 120 days after the acquisition date. According to the material fact disclosed on September 19, 2022, as a result of the differences found in the assumptions for calculating the topics: (i) Working Capital and Net Debt, (ii) Capex and (iii) Net Additions, the amount of R$ 634.3 million remained fully retained by the Company until the date of October 4, 2022, that the preliminary decision was handed down by the 7th Business Court of the Judicial District of Rio de Janeiro determining the deposit in court by the Buyers, with TIM being responsible for depositing the updated amount up to that date of R$ 670 million in an account linked to the court-ordered reorganization process of Oi Móvel S.A. Said deposit remained in an account linked to the Court until the agreement reached between the parties in October 2023. For further details, see Note 11; |

| (ii) | The amount of R$ 77 million recognized as contingent consideration, until there was an agreement between the parties. |

On October 4, 2023, TIM S.A., through a Material Fact, communicated to its shareholders and the market in general that the Arbitration Chamber Court approved an agreement related to the Post-Closing Adjustment, celebrated, on the one hand, between TIM S.A., Telefônica Brasil S.A. and Claro S.A. and, on the other hand, Oi S.A. – Under Court-Ordered Reorganization, as a way of putting an end to the controversy and the arbitration procedure related to the Post-Closing Adjustment. The final price of the portion of UPI Ativos Móveis assigned to the Company, considering the Post-Closing Adjustment negotiated in the Agreement (except for the contract targets), was R$ 6.6 billion.

Considering the TIM Adjusted Final Price, the Company recovered a portion corresponding to half of the amount that had been deposited in court and subsequently transferred it to the Arbitration Chamber (equivalent to approximately R$ 317 million on the closing date, updated by the 100% of the CDI change until the deposit in court, plus interest and/or inflation adjustment, applicable until the date of the respective redemption), and the remaining amount was redeemed by the Seller as part of the purchase price of the UPI Ativos Móveis assigned to the Company. Mainly due to the fact that it is still a contractual debt at the date of completion of the allocation of the purchase price of the Cozani acquisition, the decrease in the consideration, corresponding to the half of the amount in court, was recorded in the income (loss) for the year on the date of approval of the agreement (October 2023), under “other operating revenues (expenses)”.

On September 30, 2024 and December 31, 2023, considering the agreement signed with Oi S.A., the Company was free from any obligations mentioned in items (i) and (ii).

| 36 |

TIM S.A.

NOTES TO THE QUARTERLY INFORMATION - continued September 30, 2024 (In thousands of reais, unless otherwise indicated)

|

Identifiable assets acquired and liabilities assumed

The fair value of the identifiable assets acquired and liabilities assumed from Cozani on the date of acquisition by TIM S.A. is finalized, according to the purchase price allocation report (“Price purchase allocation” - PPA). On the closing date of the “PPA”, on December 31, 2022, the analysis indicates the assets and liabilities presented below:

| Fair value recognized on acquisition | ||

Assets

| ||

| Cash and cash equivalents | 193,382 | |

| Trade accounts receivable | 362,379 | |

| Prepaid expenses | 165,111 | |

| Recoverable taxes | 13,535 | |

| Deferred income tax and social contribution | 705,388 | |

| Property, plant and equipment | 3,518,477 | |

| Intangible assets | 3,599,811 | |

| 8,558,083 | ||

| ||

Liabilities | ||

| Suppliers | (183,227) | |

| Lease liabilities | (2,929,449) | |

| Taxes payable | (157,595) | |

| Deferred revenues | (95,135) | |

| Other liabilities | (617,518) | |

| (3,982,924) |

| Total net identifiable assets at fair value | 4,575,159 |

| Goodwill on acquisition (Note 16) | 2,636,426 |

| Total consideration | 7,211,585 |

The assets acquired and liabilities assumed related to Cozani (“net assets”) by TIM on the acquisition date are summarized below:

| Cozani

|

| Equity interest of the acquiree | 100% |

| Shareholders’ equity of Cozani at book value on 04/30/2022 | 1,282,579 |

| Shareholders’ equity of Cozani at fair value on 04/30/2022 | 4,575,159 |

| Surplus of radio frequencies(i) | 3,038,951 |

| Surplus of customers’ portfolio(ii) | 253,629 |

| (i) | The intangible asset value refers to the adjustment in the authorizations item reflecting the fair value of the acquired grants and the spectrum assessment was carried out using the market approach, with the application of a transaction multiple. The average useful life is 17.68 years; |

| (ii) | The evaluation of the customer portfolio was conducted using the profitability approach, using the MPEEM(Multi-period excess earning method) method based on a calculation of cash flows from future economic benefits attributable to the customer base. The average useful life is 7.67 years. |

| 37 |

TIM S.A.

NOTES TO THE QUARTERLY INFORMATION - continued September 30, 2024 (In thousands of reais, unless otherwise indicated)

|

The goodwill paid of R$ 2,636,426 comprises the value of future economic benefits arising from synergies expected from the acquisition. The recognized goodwill has already been deducted for tax purposes since the date of the corporate acquisition of the company Cozani by TIM S.A., which took place on April 1, 2023.

Merger of Cozani

According to the Material Fact disclosed by the Company on February 27, 2023, the completion of the Merger would still depend on the conclusion of the operational procedures related to the systemic parameterization and obtaining prior consent from ANATEL, which took place when the Act 3535/2023 was published.

On March 31, 2023, the Board of Directors (“BoD”) acknowledged the obtaining of said consent and verified compliance with the other conditions to grant full effectiveness to the Merger. Accordingly, the BoD declared that said Merger and the consequent extinction of Cozani became effective, for all purposes and effects, on April 1, 2023. The approved Acquisition did not give rise to a capital increase, nor issue of new shares of the Company, or changes in the Company’s shareholding, therefore, there is no need to approach different topics related to the exchange of shares or right to withdraw.

The purpose of this acquisition is to streamline the corporate structure of TIM S.A., eliminate overlapping authorizations for exploring the SMP service, standardize the services provided by the Companies, and will allow the concentration of activities related to the provision of personal mobile telecommunication services in a single company, in addition to optimize operating costs and efficiently allocate investments due to the integration of acquired assets.

The changes in Cozani’s equity between the date of the report (December 31, 2022) and the merger (April 1, 2023) were incorporated into the balance sheet of TIM S.A., as set forth in the protocol of merger. As a result of the merger, all operations of Cozani were transferred to TIM S.A., which succeeded it in all its assets, rights and obligations, universally and for all purposes of law.

The net assets as of December 31, 2022, is summarized below:

| Assets | Liabilities | |||

| Current assets | 1,376,107 | Current liabilities | 1,900,283 | |

| Non-current assets | 3,987,996 | Non-current liabilities | 2,422,684 | |

| Long-term receivables | 846,823 | |||

| Property, plant and equipment | 2,885,893 | |||

| Intangible assets | 255,280 | |||

| Net assets | 1,041,136 | |||

| Total assets | 5,364,103 | Total liabilities | 5,364,103 |

| 38 |

TIM S.A.

NOTES TO THE QUARTERLY INFORMATION - continued September 30, 2024 (In thousands of reais, unless otherwise indicated)

|

| 2. | Preparation basis and presentation of individual and consolidated quarterly information |

The individual and consolidated quarterly information was prepared and is being presented according to the accounting practices adopted in Brazil, which comprises the CVM standards and pronouncements, guidance and interpretations issued by the Accounting Pronouncement Committee (“CPC”) and in compliance with the International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB).

Additionally, the Company considered the guidelines provided for in Technical Guideline OCPC 07 - Evidencing upon Disclosure of General Purpose Financial-Accounting Reports in the preparation of its quarterly information. Accordingly, relevant information of the quarterly information is being evidenced and corresponds to the information used by management when administrating.

The significant accounting policies applied in the preparation of this quarterly information are below and/or presented in its respective notes. These policies were applied consistently over the periods presented.

a. General criteria for preparation and disclosure

The individual and consolidated quarterly information was prepared considering the historical cost as value basis, except regarding the derivative financial instruments that were measured at fair value.

As a result of the merger of Cozani by TIM S.A., which occurred on April 1, 2023 (see Note 1), all Cozani's operations were transferred to TIM S.A. As a result, as of this date, there are no longer consolidated balance sheets, with only consolidated information on income and operations being presented up to the end of year 2023.

Assets and liabilities are classified according to their degree of liquidity and collectability. They are reported as current when they are likely to be realized or settled over the next 12 months. Otherwise, they are stated as non-current. The exception to this procedure involves deferred income tax and social contribution balances (assets and liabilities) and provision for lawsuits and administrative proceedings that are fully classified as non-current.

On September 30, 2024, the Company reported a net profit of R$ 2,105,669. The Company’s current liabilities exceeded total current assets by R$ 374,354 due to the payment of a debt in the amount of R$ 1,379,814 and the distribution of additional dividends in the amount of R$ 1,310,000, of which R$ 874,000 have already been paid, leaving a balance of R$ 436,000, in addition to the distribution of 3rd Tranche of interest on shareholders’ equity (not paid) for the period in the amount of R$ 300,000. The Company has been recovering its working capital position through operating cash flow. On September 30, 2024, the Company’s shareholders’ equity is positive by R$ 25,977,252.

In connection with the preparation of this quarterly information, Company’s Management made analyses which confirms that the cash generated by operations up to September 30 is positive by R$ 7.9 billion; therefore, there is no evidence of uncertainties about the going concern.

The presentation of the Statement of Value Added is required by Brazilian corporate law and the accounting practices adopted in Brazil applicable to publicly-held companies. The DVA was prepared according to the criteria set forth in CPC Technical Pronouncement No. 09 - “Statement of Value Added”.

| 39 |

TIM S.A.

NOTES TO THE QUARTERLY INFORMATION - continued September 30, 2024 (In thousands of reais, unless otherwise indicated)

|

The IFRS do not require the presentation of this statement. Consequently, according to IFRS, this statement is presented as supplementary information, without prejudice to the set of quarterly information.

Interests paid from loans and financing are classified as financing cash flow in the statement of cash flow as it represents costs of obtaining financial resources.

| b. | Functional and presentation currency |

The currency of presentation of the quarterly information is the Real (R$), which is also the functional currency of the Company and its associated company.

Transactions in foreign currency are recognized by the exchange rate on the date of transaction. Monetary items in foreign currency are translated into Brazilian reais at the foreign exchange rate prevailing on the balance sheet date, informed by the Central Bank of Brazil. Foreign exchange gains and losses linked to these items are recorded in the statement of income.

| c. | Segment information |

Operating segments are components of the entity that carry out business activities from which revenues can be obtained and expenses incurred. Its operating results are regularly reviewed by the entity's main operations manager, who makes decisions on resource allocation and evaluates segment performance. For the segment to exist, individualized financial information is required.

The main operational decision maker in the Company, responsible for the allocation of resources and periodically evaluating performance, is the Executive Board, which, along with the Board of Directors, are responsible for making the strategic decisions of the company and its management.

The Group's strategy is focused on optimizing results, and all the operating activities of the Group are concentrated in TIM. Although there are diverse activities, decision makers understand that the company represents only one business segment and do not contemplate specific strategies focused only on one service line. All decisions regarding strategic, financial planning, purchases, investments and investment of resources are made on a consolidated basis. The aim is to maximize the consolidated result obtained by operating the SMP, STFC and SCM licenses.

| d. | Consolidation procedures |

Subsidiaries are all the entities in which the Group retains control. The Group controls an entity when it is exposed to, or has a right over the variable returns arising from its involvement with the entity and has the ability to interfere in those returns due to its power over the entity. The subsidiaries are fully consolidated as of the date control is transferred to the Group. Consolidation is interrupted beginning as of the date in which the Group no longer holds control.

If the Group loses control exercised over a subsidiary, the corresponding assets (including any goodwill) and liabilities of the subsidiary are written-off at their book values on the date the control is lost, and the write-off of the book value of any non-controlling interests on the date when control is lost (including any components of other comprehensive income attributed to them) also occurs. Any resulting difference as a gain or loss is recorded in income (loss). Any retained investment is recognized at its fair value on the date control is lost.

| 40 |

TIM S.A.

NOTES TO THE QUARTERLY INFORMATION - continued September 30, 2024 (In thousands of reais, unless otherwise indicated)

|

Intercompany transactions, as well as the balances and unrealized gains and losses in those transactions, are eliminated. The base date of the financial information used for consolidation purposes is the same for all the companies in the Group.

| e. | Business combination and goodwill |

Business combinations are accounted for under the acquisition method. The cost of an acquisition is measured for the consideration amount transferred, which is valuated on fair value basis on the acquisition date, including the value of any non-controlling interest in the acquiree, regardless of their proportion. For each business combination the Acquirer must measure the non-controlling interest in the acquiree at the fair value or based on its interest in the net assets identified in the acquiree. Costs directly attributable to the acquisition are accounted for as expense when incurred.

The purchase accounting method is used to record the acquisition of subsidiaries by the Group. The acquisition cost is measured as the fair value of the assets acquired, equity instruments (i.e.: shares) and liabilities incurred or assumed by the acquirer on the date of the change of control. Identifiable assets acquired, contingencies and liabilities assumed in a business combination are initially measured at their fair value on the acquisition date, regardless of the proportion of any non-controlling interest. The portion exceeding the transferred consideration of the Company's interest in the acquired identifiable net assets, is recorded as goodwill. Should the consideration transferred be less than the fair value of the net assets of the acquired subsidiary, the difference is recognized directly in the statement of income as a gain from bargain purchase once concepts and calculations applied are reviewed.

On acquiring a business, the Group assesses the financial assets and liabilities assumed in order to rate and to allocate them in accordance with contractual terms, economic circumstances and pertinent conditions on the acquisition date, which includes segregation by the acquired entity of built-in derivatives existing in the acquired entity’s host contracts.

Any contingent payments to be transferred by the acquiree will be recognized at fair value on the acquisition date. Subsequent changes to the fair value of the contingent consideration which is deemed to be an asset or liability should be recognized in accordance with CPC 48 in the statement of income.

Initially, goodwill is initially measured as being the excess of consideration transferred in relation to net assets acquired (acquired identifiable assets and assumed liabilities) measured at fair value on acquisition date. If consideration is lower than fair value of net assets acquired, the difference must be recognized as gain in bargain purchase in the statement of income on the acquisition date.

After initial recognition, the goodwill is carried at cost less any accumulated impairment losses. For impairment testing purposes, goodwill acquired in a business combination is, from the acquisition date, allocated to each cash-generating units of the Group that are expected to benefit by the synergies of combination, regardless of other assets or liabilities of the acquiree being allocated to those units.

When the goodwill is part of a cash generating unit and a portion of this unit is disposed of, the premium associated with the disposed portion should be included in the cost of the operation when calculating gains or losses in the disposal. The goodwill disposed under these circumstances of this operation is determined based on the proportional values of the portion disposed of, in relation to the cash generating unit maintained.

| 41 |

TIM S.A.

NOTES TO THE QUARTERLY INFORMATION - continued September 30, 2024 (In thousands of reais, unless otherwise indicated)

|

| f. | Approval of quarterly information |

This individual and consolidated quarterly information was approved by the Company's Board of Directors on November 4, 2024.

| g. | New standards, amendments and interpretations of standards |

The following new standards/amendments were issued by the Accounting Pronouncement Committee (“CPC”) and International Accounting Standards Board (IASB), are effective for the period ended September 30, 2024 that may affect the Company somehow.

IFRS 17 - Insurance Contracts