Exhibit 99.6

| ANNUAL REPORT 2020 |

| All financial amounts in this Annual Report are in Canadian dollars unless stated otherwise. |

| About CI Financial 2 2020 At a Glance 5 Financial Highlights 5 Operating Highlights 5 Letter to Shareholders 6 Subsidiary Profiles 14 Asset Management 14 Wealth Management 17 Corporate Social Responsibility Report 24 TABLE OF CONTENTS |

| CI Financial Corp. is an independent, diversified global asset and wealth management company operating in Canada, the United States and Australia. Since 1965, we have been driven by a commitment to provide our clients with the highest-quality investments and advice. We have $139 billion in assets under management and $102 billion in wealth management assets for total assets of $241 billion (as at March 31, 2021). We are guided by our core beliefs that active management adds value to clients’ portfolios and that investors benefit from working with professional financial advisors. CI has been listed on the Toronto Stock Exchange under the symbol CIX since June 1994 and on the New York Stock Exchange under the symbol CIXX since November 2020. ABOUT CI FINANCIAL |

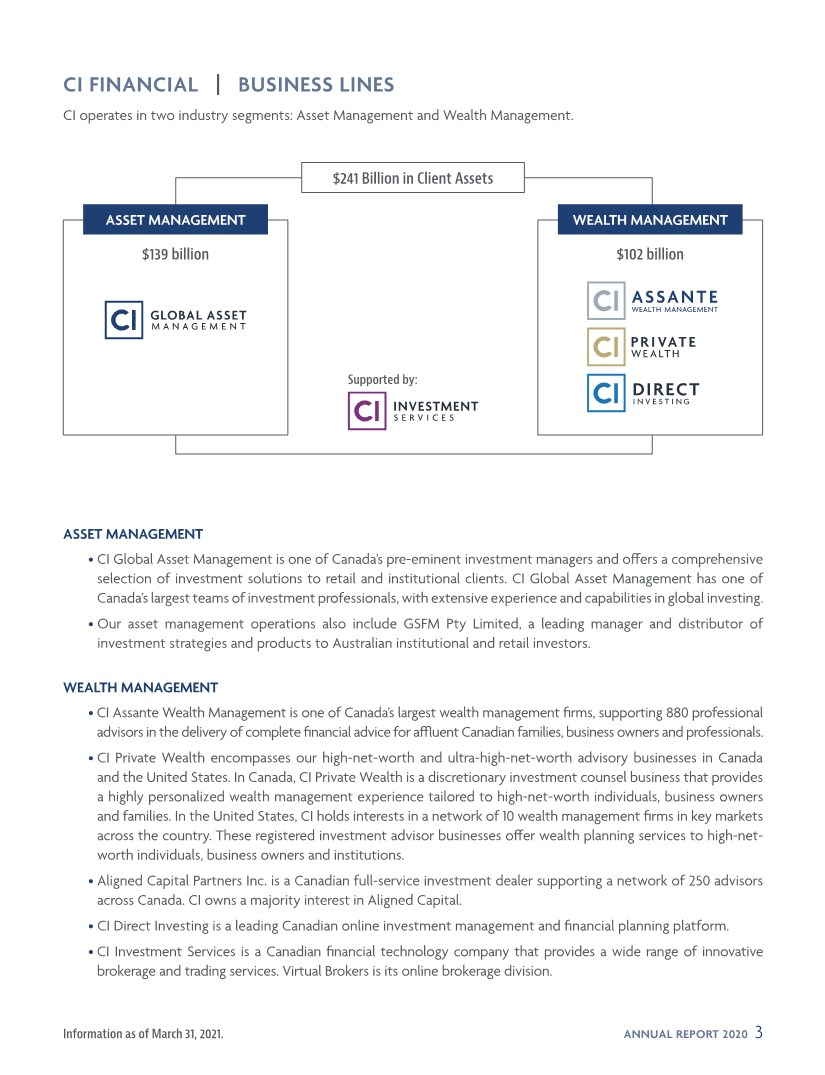

| ANNUAL REPORT 2020 3 ASSET MANAGEMENT • CI Global Asset Management is one of Canada’s pre-eminent investment managers and offers a comprehensive selection of investment solutions to retail and institutional clients. CI Global Asset Management has one of Canada’s largest teams of investment professionals, with extensive experience and capabilities in global investing. • Our asset management operations also include GSFM Pty Limited, a leading manager and distributor of investment strategies and products to Australian institutional and retail investors. WEALTH MANAGEMENT • CI Assante Wealth Management is one of Canada’s largest wealth management firms, supporting 880 professional advisors in the delivery of complete financial advice for affluent Canadian families, business owners and professionals. • CI Private Wealth encompasses our high-net-worth and ultra-high-net-worth advisory businesses in Canada and the United States. In Canada, CI Private Wealth is a discretionary investment counsel business that provides a highly personalized wealth management experience tailored to high-net-worth individuals, business owners and families. In the United States, CI holds interests in a network of 10 wealth management firms in key markets across the country. These registered investment advisor businesses offer wealth planning services to high-net- worth individuals, business owners and institutions. • Aligned Capital Partners Inc. is a Canadian full-service investment dealer supporting a network of 250 advisors across Canada. CI owns a majority interest in Aligned Capital. • CI Direct Investing is a leading Canadian online investment management and financial planning platform. • CI Investment Services is a Canadian financial technology company that provides a wide range of innovative brokerage and trading services. Virtual Brokers is its online brokerage division. CI FINANCIAL | BUSINESS LINES CI operates in two industry segments: Asset Management and Wealth Management. $102 billion $139 billion $241 Billion in Client Assets WEALTH MANAGEMENT ASSET MANAGEMENT Supported by: Information as of March 31, 2021. |

| 4 ANNUAL REPORT 2020 CI FINANCIAL DIRECTORS Kurt MacAlpine Chief Executive Officer and Director David P. Miller Director William T. Holland Chairman of the Board Tom P. Muir Director William (Bill) Butt Director Sheila A. Murray Director Brigette Chang-Addorisio Director Paul J. Perrow Director |

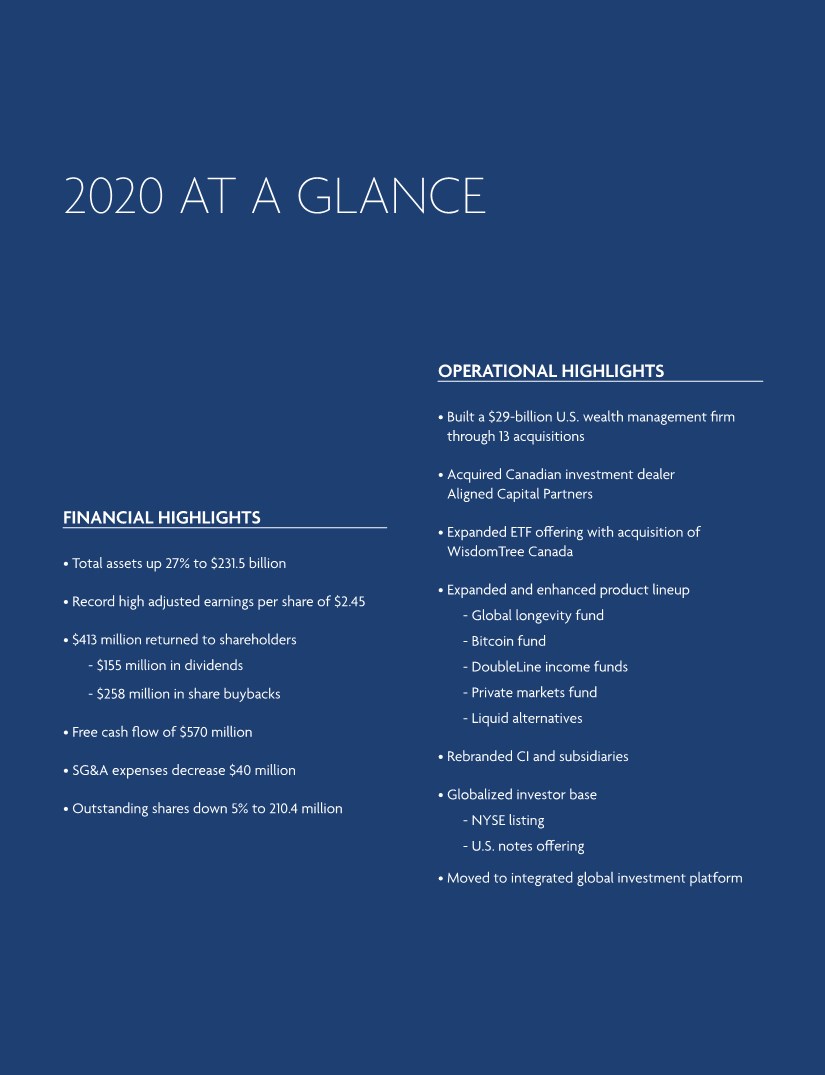

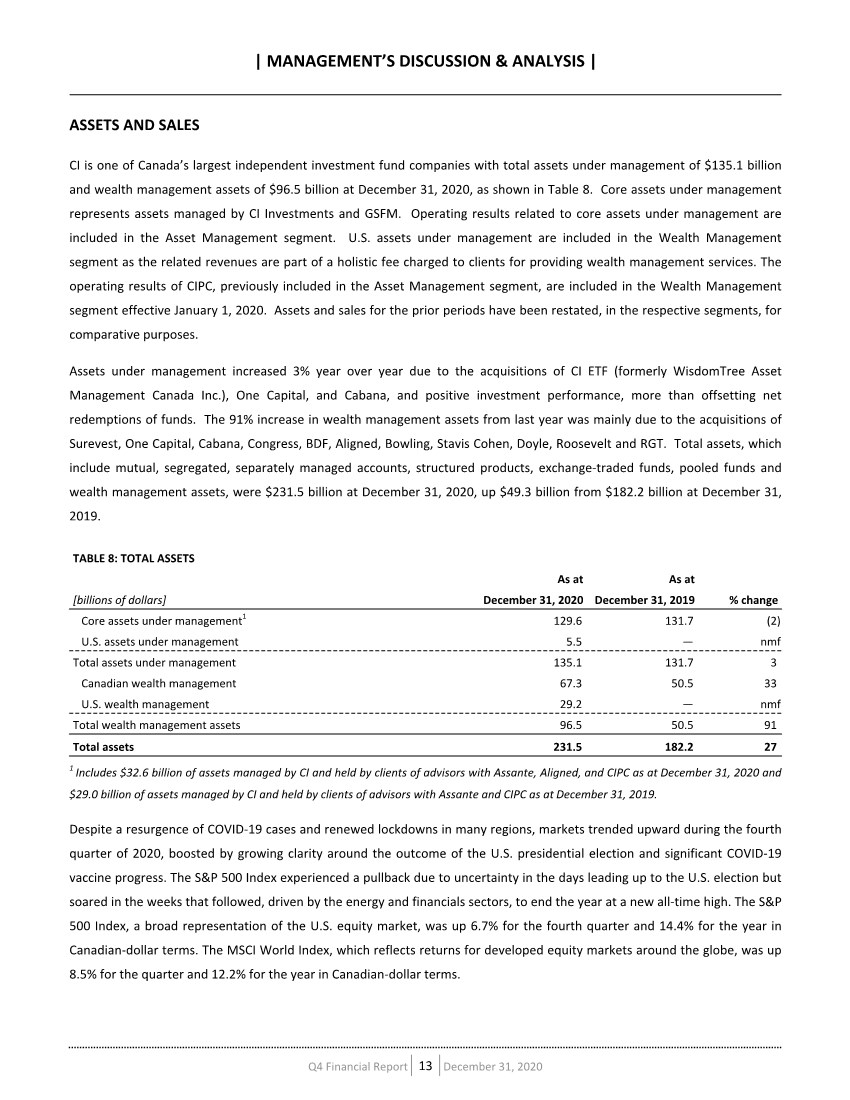

| 2020 AT A GLANCE FINANCIAL HIGHLIGHTS • Total assets up 27% to $231.5 billion • Record high adjusted earnings per share of $2.45 • $413 million returned to shareholders - $155 million in dividends - $258 million in share buybacks • Free cash flow of $570 million • SG&A expenses decrease $40 million • Outstanding shares down 5% to 210.4 million OPERATIONAL HIGHLIGHTS • Built a $29-billion U.S. wealth management firm through 13 acquisitions • Acquired Canadian investment dealer Aligned Capital Partners • Expanded ETF offering with acquisition of WisdomTree Canada • Expanded and enhanced product lineup - Global longevity fund - Bitcoin fund - DoubleLine income funds - Private markets fund - Liquid alternatives • Rebranded CI and subsidiaries • Globalized investor base - NYSE listing - U.S. notes offering • Moved to integrated global investment platform |

| 6 ANNUAL REPORT 2020 LETTER TO SHAREHOLDERS Dear Shareholders, It was truly a year unlike any other. In 2020, we faced both a global health crisis and an economic crisis, as the pandemic shuttered many companies and profoundly changed how we live and do business. Increasing political polarization and anger over racial inequality also roiled society. To say it was a challenging year is an understatement. However, you can be proud of the performance of CI Financial and its employees during this difficult period. Not only did we adapt quickly and efficiently to a work-from-home environment and continue to provide an exceptional level of service to our clients, but we made tremendous progress in executing against our strategic priorities. In fact, 2020 was transformative for CI. The company is larger, stronger, more diversified and more global than it was just a year ago. And while we are still in the early stages of our strategic transformation, I believe CI is exceptionally well positioned for continued success given the advances we’ve made over the past year. In this letter, I will reprise our strategic priorities and discuss the achievements of 2020, as well as touch on other key concerns for shareholders, including our financial results and capital allocation. |

| ANNUAL REPORT 2020 7 OUR STRATEGIC PRIORITIES We introduced a new strategic direction for the company in November 2019 centred on three strategic priorities: These priorities leverage CI’s many strengths and capabilities to extend our industry leadership and take advantage of opportunities for growth in a rapidly changing environment. Every initiative we undertake supports one or more of these priorities. For example, the buildout of our U.S. business, described below, both expands our wealth management business and globalizes the company. Before reviewing each strategic priority in more detail, I would like to mention two projects that support all three priorities — the rebranding of our firm and our digital transformation. REBRANDING THE FIRM In 2020, we initiated a company-wide rebrand, which includes newly designed logos and the renaming of several subsidiaries, accompanied by new signage and a crucial update of our websites. This process is being completed in the first half of this year and, as our company grows, all of our operations will eventually adopt branding that’s consistent with the rest of CI. Prior to these changes, we had approximately 20 brands, most of which had no obvious association with CI. This created confusion for advisors, clients and anyone else doing business with us. Having so many unrelated brands reduced the effectiveness and increased the cost of our marketing. You will have seen all of the new logos at the start of this report, but let’s briefly review the naming changes: • CI Global Asset Management represents our investment management business, with the legacy boutique brands (such as Signature Global Asset Management) to be phased out. • CI Assante Wealth Management is the new name for Assante Wealth Management, which provides a connection to CI while maintaining the positive brand equity of the Assante name. • CI Private Wealth represents our high-net-worth advisory business. Stonegate Private Counsel adopted this brand in the first quarter of 2021 and it will also represent our U.S. advisory businesses. • CI Direct Investing is the new business name for WealthBar and will eventually include Virtual Brokers, so that CI Direct Investing becomes CI’s integrated digital wealth platform. • CI Investment Services is the former BBS Securities, and is a name that better represents the firm’s product offerings. What we have created is a streamlined group of brands with a consistent look and a relationship to CI. We have improved the client experience while enhancing our marketing return on investment, as marketing for any one brand will support the whole. Most importantly, this new approach more effectively communicates the breadth and depth of CI’s capabilities and scale and supports our continued development as a diversified global asset and wealth management company. MODERNIZE ASSET MANAGEMENT EXPAND WEALTH MANAGEMENT GLOBALIZE THE COMPANY |

| 8 ANNUAL REPORT 2020 DIGITAL TRANSFORMATION When I introduced our new strategic direction, I said it was important that we drive advanced technology into everything we do. This sustained effort, which we call our “digital transformation,” underpins the execution of our entire strategy. I am pleased to report that we have made great strides in harnessing new technologies and processes to enhance our capabilities and efficiency in all aspects of our work, from sales and marketing to operations to client services. For more detail on this important undertaking, please see the following section, “CI’s Digital Transformation: Innovating to Lead in an Agile, Competitive Marketplace.” MODERNIZING ASSET MANAGEMENT Our strategic priority of modernizing asset management addresses a number of developments within our industry, including evolving demographics, shifting investor preferences and needs, increased expectations for service and support among both investors and advisors, and a changing regulatory regime. The high levels of volatility and rapid shifts in market dynamics that accompanied the pandemic over the past year underscore the need to be agile and forward-looking. There were many accomplishments in this area in 2020; however, I am going to focus on two key areas: the restructuring of our portfolio management function and the upgrading of our product lineup with the introduction of a number of innovative and relevant new products. In portfolio management, as I explained above, we rebranded CI Investments to CI Global Asset Management and made the decision to phase out the brands for our in-house investment boutiques. In conjunction with this, we also began to integrate the boutiques themselves into one team operating under the CI Global Asset Management (“CI GAM”) name. By moving from a multi-boutique model to an integrated platform, we are reducing complexity and fostering improved communication and collaboration across the entire group, leading to the increased sharing of research and insights. As a result, we are delivering to our clients in all of our mandates the full benefits of CI GAM’s scale and expertise, not just what was available within that boutique. To date, these changes have been well received. It’s important to note that the individuals managing each mandate and their investment approaches did not change as a result of the integration, minimizing the disruption to clients. The implementation of this model will continue this year as we review the naming conventions within our fund lineup. We are confident that this structure will lead to better investment outcomes and an improved experience for our clients. In the area of product innovation, we launched an ambitious number of new mandates to meet the evolving needs of investors and help them achieve their objectives in a challenging investment environment. In several cases, we teamed with outside firms to harness globally leading expertise that was not available in-house. |

| ANNUAL REPORT 2020 9 Notable product initiatives included: • The launch of three income funds sub-advised by DoubleLine Capital, which is led by the legendary Jeffrey Gundlach, one of the world’s best-known and most successful income investors. These mandates, exclusive to CI in Canada, bolster our lineup of income products, which are so crucial as increasing numbers of retirees seek reliable cash flow in a time of low interest rates. • A strategic relationship with Adams Street Partners, a global leader in private markets investing, to develop the CI Adams Street Global Private Markets Fund, which was launched in January 2021. This fund is just one step in expanding our lineup of alternative investments, which offer strong diversification and other benefits to investors and are particularly well suited for our high-net-worth and ultra-high-net-worth clients. • The launch of the CI Global Longevity Economy Fund, which draws on the research and insights of Dr. Joseph Coughlin, a global expert on demographic change and Founder and Director of the Massachusetts Institute of Technology AgeLab. The fund focuses on companies benefiting from changes resulting from the trend towards longer, healthier lifespans. • In December 2020, we launched the CI Galaxy Bitcoin Fund, a closed-end fund that provides secure and convenient exposure to bitcoin. This was followed in the new year by the launch of a bitcoin ETF and mutual fund, as well as an Ethereum ETF and mutual fund, giving CI an industry-leading suite of digital asset mandates. Our sub-advisor on these funds is Galaxy Digital, a well-established firm in this sector. • The launch of several mandates to meet the demand for investments in real assets — infrastructure and real estate — as well as the expansion of our lineup of liquid alternative mutual funds and ETFs. CI has established an industry-leading presence in liquid alternatives, with $3.8 billion in assets under management as at March 31, 2021. It’s worth noting that many mandates are offered in multiple product structures, including mutual funds, private pools and ETFs, allowing our clients to access our investment expertise in the structure they prefer — an advantage of our scale and diversity that few competitors can match. Also in 2020, we completed the acquisition of WisdomTree Asset Management Canada, Inc., adding approximately $1 billion in assets and new capabilities to our ETF lineup. Our ETF business is experiencing strong growth and has a significant presence in the Canadian market, with over $12 billion in assets under management and a comprehensive lineup of 70 ETFs (as at March 31, 2021), with a focus on actively managed and factor-based mandates. I would like to reiterate that the process of modernizing our asset management is advancing on many fronts. Other initiatives include: adopting a radically different approach to marketing, with a focus on digital and data; the introduction of a new model for our sales and distribution team; and the hiring of a new head of institutional sales to revitalize that group. EXPANDING WEALTH MANAGEMENT At CI, we firmly believe in the value of advice and the future of the wealth management industry. This view underlies our strategic priority of expanding our wealth management platform in both Canada and the U.S. The role of the financial advisor is more important now than ever, and likely to remain so for years to come, as clients’ lives become increasingly complex. |

| 10 ANNUAL REPORT 2020 CI also has considerable experience in wealth management, with our Canadian advisory businesses — Assante and Stonegate, which is now CI Private Wealth — earning exceptional reputations for service and quality. For many years, our firms have put forth a comprehensive approach to wealth management as their value proposition. We have a high level of credibility in this area, given the experience of our advisors and the high level of support we provide to them and their clients through a diverse group of in-house experts in wealth planning. This approach represents the future of the wealth management business, in our view, given the increasing complexity of our clients’ lives. It is also crucial in attracting the coveted high-net-worth and ultra-high-net-worth clientele, and we have been very successful on that front. It is on this solid foundation that we built a dramatic expansion of our wealth management business in 2020. Wealth management assets almost doubled during the year — to $96.5 billion from $50.5 billion — through impressive organic growth and onboarding $38.7 billion in new client assets in Canada and the United States. In contrast, we onboarded $1 billion in new client assets in each of the previous two years. In Canada, we continued to make significant investments in Assante and CI Private Wealth, including the extensive use of technology to add efficiency to our operations and provide enhanced tools and services for advisors and clients. In particular, Assante continued the development of its discretionary platform, which will launch this year. It will provide an attractive new service option for existing advisors and for advisors we are seeking to recruit. Assante has also made a concerted effort in recent years to assist its advisors in moving “up market,” and one sign of that campaign’s success in 2020 was a 70% increase in net sales at Assante Private Client, a high-net-worth program exclusive to Assante and managed by CI Private Counsel. A significant boost to our Canadian wealth management business came through the October acquisition of Aligned Capital Partners, a fast-growing, profitable investment dealer with 250 advisors across Canada and $13.5 billion in assets (March 31, 2021). In the United States, CI went from being an unknown to one of the fastest-growing firms in the market in a very short time. In 2020, we completed 13 acquisitions of registered investment advisor firms (which includes three transactions by affiliates) to establish a significant presence in U.S. wealth management with total assets of $29 billion at the end of the year. Let’s step back for a moment to review why we entered this market, which supports the strategic priorities of expanding our wealth management platform and globalizing the firm. First, the U.S. is a logical market for global expansion, given its size, proximity, similarity in business practices, and shared language. While competition is high, barriers to entry are low. Second, the registered investment advisor, or RIA, sector is the fastest-growing segment of U.S. wealth management with a strong focus on financial planning for clients. However, the sector is highly fragmented, offering the potential for an acquiror such as CI to realize the benefits of economies of scale. CI is also a natural owner of these businesses, given our own long experience in wealth management and our emphasis on complete wealth planning for clients. Our vision is to create the leading private wealth platform in the United States and provide a comprehensive and unrivalled client experience. This vision, our experience, and our long-term commitment to the industry resonated strongly with RIA owners who were seeking a larger partner. The RIAs we have acquired are very high-quality, profitable and growing firms, in locations across the United States. (A list and description of each firm can be found in the Subsidiary Profiles section of this report.) |

| ANNUAL REPORT 2020 11 In the first quarter of 2021, we signed agreements to acquire another three RIAs — Segall, Bryant & Hamill, LLC (“SBH”) of Chicago, Barret Asset Management, LLC of New York and Brightworth, LLC of Atlanta. SBH, our largest U.S. acquisition to date, also has a $22-billion institutional money management business in addition to about $8 billion in wealth management assets. Combined, these transactions will add $38 billion to our U.S. assets, bringing the total to approximately $69 billion, based on asset levels as of March 31, 2021. Our RIA firms are already contributing to our revenues and profitability even before the achievement of any synergies. And we intend to continue to scale our U.S. wealth platform through acquisitions and organic growth. Even with our success to date, we are just at the beginning of building this business, which we believe holds tremendous potential. GLOBALIZING THE COMPANY As you can see from the previous section, we have made excellent progress in globalizing the company, having added approximately $69 billion in U.S.-based assets once our most recent transactions close. Further global diversification is the key to growth for various reasons. Achieving scale is critical today in asset and wealth management, and this is difficult to achieve in Canada, a smaller and more concentrated market. We were very pleased to acquire Aligned Capital, but opportunities to purchase such a quality business in Canada are few and far between. Additionally, clients today want to be serviced and supported globally, given that many of them work or have residences in more than one country. In 2020, we launched a referral program between our Canadian advisors and our U.S. RIAs, to provide such support to our clients. Globalization also means that we are accessing expertise that we may not have in-house and examples of that include our relationships with DoubleLine, Adams Street, Galaxy Digital and Dr. Joseph Coughlin of MIT. There were two other important initiatives in 2020 promoting the globalization of our firm in addition to our entry into the RIA business — listing our common shares on the New York Stock Exchange (“NYSE”) and issuing debt into the U.S. Our NYSE listing, which occurred in November, has helped to broaden our shareholder base and increase our profile in the United States. It also gives us the option to offer shares as part of the purchase price in any U.S. transaction. Our U.S. bond offering also diversified our investor base and, in fact, shifted the majority of our creditors from Canada to the U.S. The offering and a subsequent re-opening in early 2021 were so well received that we raised a total principal amount of US$960 million at an attractive rate of 3.2% and a favourable term of 10 years. This allowed us to proceed with the early redemption of bond issues due this year and in 2023, reducing costs and extending the overall maturity of our debt. FINANCIAL RESULTS I am going to touch on a few important highlights in this section, and I refer you to the Management Discussion & Analysis section of this report for a detailed look at our results in 2020. Despite the market volatility stemming from the pandemic and the accompanying lockdowns around the world, CI registered strong results for the year. Our adjusted earnings per share were a record $2.45 and our free cash flow was $570.2 million. As mentioned earlier, our wealth management assets grew by 91% during the year to an all-time high of $96.5 billion. Our assets under management increased 3% year over year to $135.1 billion. As a result, our total assets were up by $49.3 billion or 27% to $231.5 billion. |

| 12 ANNUAL REPORT 2020 Redemptions were still present in our Canadian asset management business, but we believe that the many changes we are making to modernize that business and its operations — including the launch of a number of innovative and relevant products and the move to an integrated global investment management platform — should lead to improved net sales. We believe it’s important that as we grow our business, we maintain cost discipline. In 2020, we reduced selling, general and administrative (“SG&A”) expenses by $40 million or 8%, even as we took on the expenses of acquired businesses. Excluding acquisitions, we reduced expenses by 11% — savings that will benefit the company on an ongoing basis. In realizing these efficiencies, we are aligning our company’s resources with our strategic priorities and the opportunities we see in the marketplace. CAPITAL ALLOCATION CI’s ability to generate significant cash flow allows us to finance our M&A strategy while continuing to return money to our shareholders through dividends and share repurchases. In 2020, we maintained our quarterly dividend at $0.18 per share, and paid total dividends of $155.3 million. We also believe that our share price remains undervalued by the market and during the year we repurchased 14.0 million shares for a total cost of $257.9 million. However, we will continue to take a dynamic approach to capital allocation by varying our share repurchases according to market conditions and our corporate priorities. LOOKING FORWARD It’s incredible that we were able to accomplish so much in the space of year — especially during a year when our work lives and our entire society were disrupted. I continue to be impressed by the high level of engagement, resilience and adaptability shown by our employees, advisors and associates in Canada and around the world during this most challenging of times. I thank all of you for your work and dedication. I would also like to thank our shareholders for their continued support. As I said at the start of this letter, 2020 was a transformative year for CI. We are continuing to build on this progress, guided by our strategic priorities. As we look forward to an economic recovery and the return to a more normal environment, there are many reasons to be excited about the coming year and the future of CI. Sincerely, Kurt MacAlpine Chief Executive Officer March 31, 2021 |

| ANNUAL REPORT 2020 13 The vital role that technology plays in our business was underscored in 2020 with the sudden shift to a distanced world of remote work, virtual meetings, online apps, and digital transactions, making “Digital Transformation” an imperative. When the pandemic was declared we were ready, with more than 95% of CI’s workforce successfully making the shift to working from home just weeks later. As we continue to modernize our business, we are emphasizing Digital Transformation across several key operational areas, work that will fundamentally change our business practices and our corporate culture for years to come. Our goal is to be an industry leader and innovator by adopting emerging technologies designed to optimize our resources, improve our efficiencies, and enhance how we engage with our clients and partners as the business grows. Throughout 2020 we finalized our long-term Digital Transformation roadmap and executed in several targeted areas, focusing on implementing technologies to eliminate or reduce manual tasks, enhance and scale our operational capacity, reduce human error rates and improve our employee and client experiences. Some of the notable developments include: • Introducing ICR (Intelligent Character Recognition) and OCR (Optical Character Recognition) technologies to automatically digitize input data from paper forms or email. • Applying RPA (Robotic Process Automation) technology to replace manual data entry for a number of back- office and operational functions. We launched automated solutions in key areas such as new account setups, account transactions, new fund set-up and B2B loan records, saving time and improving accuracy to nearly 100%. • Implementing Amazon Connect, an enhanced cloud- based communications system featuring voice and chat functions to support a more streamlined, personalized client service experience in our call centre. • Creating an easily searchable digital knowledge management database to serve as a single source of product information for sales, operations, and client service personnel. • Leveraging the power of artificial intelligence and data analytics to assist our sales team in prioritizing and targeting outreach to advisors, streamlining and optimizing their interactions. • Emphasizing digital literacy and agile methodology throughout the organization and through the employee recruitment process. • Implementing DevOps and CI/CD methodologies and tools in our IT environment, allowing for faster and more efficient delivery of IT applications across the organization. The process of Digital Transformation will continue throughout 2021 on a greater scale as we build on this strong foundation, and we expect this work to be an important competitive advantage. CI’S DIGITAL TRANSFORMATION: INNOVATING TO LEAD IN AN AGILE, COMPETITIVE MARKETPLACE |

| ASSET MANAGEMENT As a global investment manager, CI Financial is committed to providing innovative and effective solutions for retail and institutional clients, and to helping a broad range of investors meet their financial goals. As part of our larger strategic priority to modernize our asset management business, we made significant advancements in 2020, responding to evolving investor needs amid an increasingly complex environment. CI operates in this segment primarily through CI Global Asset Management (the business name of CI Investments Inc.) in Canada and GFSM Pty in Australia. CI also owns a majority stake in Marret Asset Management Inc., a Toronto-based fixed- income investment manager, and minority interests in Altrinsic Global Advisors, LLC, a global asset manager based in Greenwich, Connecticut, and Lawrence Park Capital Partners Ltd. of Toronto, which specializes in alternative fixed-income strategies. (In 2021, CI and Lawrence Park reached an agreement under which CI will purchase full ownership of the company.) SUBSIDIARY PROFILES |

| ANNUAL REPORT 2020 15 CI GLOBAL ASSET MANAGEMENT CI Global Asset Management (“CI GAM”) is one of Canada’s largest investment management companies. We are proud to partner with financial advisors to serve approximately 1.4 million investors across the country. We also provide investment services to pension funds, foundations and other institutional investors through a dedicated institutional group. We offer a wide range of innovative and effective investment solutions, including mutual funds, exchange-traded funds, segregated funds, managed solutions and alternative investments. Our product lineup spans a wide range of investment disciplines and mandates covering various geographic regions, asset classes and industries. As part of CI Financial’s strategic priority of modernizing its asset management business, we rebranded CI Investments as CI Global Asset Management in 2020, unveiling the new name and modern logo as part of a broader corporate update. At CI GAM, we believe that the key to delivering the best possible outcomes for our clients lies in gathering highly talented people who bring a diverse range of thoughts and ideas to the investment process. To truly leverage the depth of talent within our in-house portfolio management teams, we took the bold step of transforming our asset management structure, beginning to phase out our legacy in-house investment management boutique brands in favour of an integrated global investment management platform in November 2020. The new CI Global Asset Management model promotes efficiency and enhances the solutions we offer our clients by aligning investment professionals according to their areas of specialization. It encourages them to effectively channel our common technology-based platforms and resources for greater collaboration and improved communication. At the same time, it allows for a cohesive marketing message, simplifying the investment selection process for advisors and their clients. We are confident that this development will support enhanced portfolio results and allow investors to benefit from the full spectrum of capabilities within CI GAM over the coming years. 2020 OPERATING HIGHLIGHTS • CI GAM teamed up with DoubleLine Capital LP, led by legendary U.S. bond investor Jeffrey Gundlach, to launch three exclusive income mandates to the Canadian marketplace in May 2020. Available in both mutual fund and ETF series, the CI DoubleLine Funds provide investors with access to the unique structured products segment of the U.S. fixed-income market. • Throughout a turbulent year, CI GAM continued to show leadership in key areas of the business, building on earlier successes in the ETF and liquid alternatives spaces. Our ETF business experienced strong inflows and annual growth of about 35%, finishing the year at $11.6 billion in AUM. In February, CI completed the acquisition of WisdomTree’s Canadian ETF business and several new ETFs were launched in 2020, including a well-received suite of liquid alternative ETFs with similar mandates to the popular CI Liquid Alternatives™ mutual funds. • CI GAM launched its first mandate based on the research and insights of Dr. Joseph Coughlin, a global expert on demographic change and Founder and Director of the Massachusetts Institute of Technology AgeLab. CI Global Longevity Economy Fund focuses on companies benefiting from the trend towards longer lifespans. |

| 16 ANNUAL REPORT 2020 • To meet investor demand for access to the cryptocurrency space, CI GAM launched CI Galaxy Bitcoin Fund in December, a closed-end fund listed on the Toronto Stock Exchange. The success of this initial offering set the stage for further collaboration with Galaxy Digital Capital Management LLP to offer ETFs and mutual funds investing in bitcoin and Ether in early 2021. • In April 2020, we announced plans to collaborate with private equity fund manager Adams Street Partners to develop a private equity offering for accredited high-net-worth clients. This fund was launched in January 2021. • Our sales team leveraged a combination of artificial intelligence and sales best practices to launch the Advisor Smart List program, a tool designed to improve the effectiveness of the sales process. By identifying advisor preferences and sales trends, the custom-built lists provide guidance to the CI GAM sales team on how and when to contact advisors with specific product recommendations, resulting in enhanced sales coverage and improved market penetration. GFSM PTY LIMITED GSFM is a leading manager and distributor of investment funds to institutional and retail investors in Australia. The firm was founded in 2007 and today manages approximately $7.1 billion in assets (as at March 31, 2021). GSFM partners with high-calibre investment managers in Australia and globally to offer unique investment strategies to the Australian market. We have formed relationships with eight investment managers — New York-based Epoch Investment Partners, Los Angeles-based Payden & Rygel, London-based Man Group, Toronto-based CI Global Asset Management, and Australian-based managers Munro Partners, Redpoint Investment Management, Tribeca Investment Partners and Triple3 Partners. Each offers a differentiated investment strategy in their specialist asset classes. These mandates span Australian equities, global equities, fixed income, infrastructure, alternatives and volatility. CI Financial owns 84% of GSFM, and GSFM executives hold a 16% equity stake. 2020 OPERATING HIGHLIGHTS • Munro Partners was named winner of a Zenith Fund Award for International Equities, Alternative Strategies. The awards recognize excellence in funds management. • Munro Global Growth Fund was named best long/short equity fund at the 2020 Hedge Funds Rock + Australian Alternative Investment Awards. These awards were established in 2005 to recognize and honour the industry’s top performers. • We launched our first actively managed ETF, the Munro Global Growth Fund, a hedge fund (ASX: MAET). • GFSM was awarded new institutional fixed-income mandates totalling $590 million. |

| WEALTH MANAGEMENT CI provides a wide range of wealth management services focused on protecting and enhancing our clients’ wealth. When the pandemic began, many people were understandably concerned about the safety of their investments and their future financial security, and our advisors were there to support their clients through a difficult time. As part of our strategic priority to expand our wealth management platform, CI made significant strategic investments in this area of our business in 2020, particularly within the growing high-net-worth and ultra-high-net-worth segments. In addition to strong results at Assante and CI Private Wealth, we acquired a majority interest in Aligned Capital Partners Inc., one of the fastest-growing wealth firms in Canada by revenues, and accelerated our expansion into the U.S. registered investment advisor (“RIA”) market with 13 acquisitions, including 10 direct acquisitions and three indirect transactions. At the same time, we directed investment toward digitally transforming our business to improve efficiencies and expand our range of product and service offerings. |

| 18 ANNUAL REPORT 2020 CI ASSANTE WEALTH MANAGEMENT CI Assante Wealth Management (“Assante”) is one of Canada’s largest wealth management firms, supporting 880 advisors in the delivery of complete financial advice for affluent Canadian families, business owners and professionals. Assante’s services are offered through Assante Capital Management, an investment dealer, and Assante Financial Management, a mutual fund dealer. Assante advisors also have exclusive access to Assante Private Client, a division of CI Private Counsel, for high-net-worth investment management and holistic advice services. Despite the onset of the global pandemic and heightened market volatility, Assante ended the year with record assets under advisement (“AUA”) of $46 billion, highlighting the strength of client relationships and the value of trusted advice. Our success is closely linked to the strong partnerships we have developed with our advisor network and our goal of delivering an industry-leading advisor and client experience. Across our lines of business, we support our advisors by providing comprehensive investment and wealth planning capability through Evolution Private Managed Accounts and Assante Private Client. Backed by a wealth of resources, including investment analysts, portfolio managers, tax lawyers, accountants, estate planning and insurance specialists and wealth planners, our advisors provide a comprehensive and integrated approach to wealth management. 2020 OPERATING HIGHLIGHTS • Assante ended the year with a record $46 billion in AUA, reflecting organic net client growth, market gains and advisor recruiting. • We rolled out the new, sophisticated CI Assante Wealth Management branding to showcase and reinforce the strength, scale and stability of CI Financial standing behind Assante advisors and their clients. • We launched the volunteer-led Be Well-Advised program to support individuals and families through the depths of the global pandemic with free financial advice. • We continued to digitally transform our business to improve the client and advisor experience by introducing further efficiencies into our back-office capability. Highlights include digital onboarding, the introduction of robotic process automation, an app for Assante Investor Online and the growth of Assante Connect, our digital advice platform powered by CI Direct Investing. • We implemented new platform functionalities to add more services for clients and advisors, including on-book margin capability and U.S.-dollar registered accounts. • The high-net-worth segment represents a significant area of growth, and 2020 brought a 70% increase in net sales for Assante Private Client, with assets standing at $3.1 billion. • Assante ranked #1 in the 2020 Investment Executive Dealer Report Card for full-service and mutual fund dealers, and #2 in the 2020 J.D. Power Full-Service Investor Satisfaction Study. • Development of Assante’s discretionary platform, powered by d1g1t Inc.’s enterprise wealth management platform with institutional-grade analytics and risk management tools, continued in 2020. With completion expected in early 2021, this capability will augment the firm’s recruiting pipeline and foster continued growth in the affluent segments. |

| ANNUAL REPORT 2020 19 ALIGNED CAPITAL PARTNERS CI acquired a majority interest in Aligned Capital Partners Inc. (“ACPI”) of Burlington, Ontario in October 2020. The firm supports a network of 250 advisors servicing over 41,000 clients with total assets of $13.5 billion (as at March 31, 2021). ACPI is one of the fastest-growing, progressive securities dealers in the country. The reason: a strong solid foundation and an adaptive digital platform. Unique to the industry, ACPI was founded on the principle that Canadian financial advisors should have the freedom to run their businesses independently while being supported by an unconflicted dealer platform. The end goal for both: a better, more customized investor experience and ultimately a better outcome for investors. In its evolution, ACPI has become an industry leader on several fronts. First by recognizing the need for change and challenging the status quo, then by inciting that change not just on a platform level, but also on a wider industry level. Innovation is at the core of the ACPI initiative. A large part of that is developing a fully integrated digital ecosystem designed to grow and support both the company’s business and our advisor partners’ businesses, while at the same time remaining flexible enough to meet the demands of technological advancements as they come into play. The Aligned 360 Digital Platform is the sum of many inter-related digital components through which data is flowing live 24/7. ACPI continues to push the boundaries by working collaboratively within the industry itself, and by forging strategic partnerships with other like-minded companies all interested in one common goal — to build a better Canadian wealth management landscape. 2020 OPERATING HIGHLIGHTS • We added 43 new advisor teams with approximately $1.5 billion in assets. • Our assets under administration ended the year at $12 billion, an increase of more than 26% year over year. • We completed our Data Lake Historical Transaction Project, which serves as the core source of data for the firm and allows for greater flexibility in upgrading technology platforms. • We launched our new Compliance Supervision system. |

| 20 ANNUAL REPORT 2020 CI PRIVATE WEALTH — CANADA CI Private Wealth (“CI PW”) is a full-service wealth management firm that offers a highly personalized experience tailored to the financial goals, unique needs and evolving priorities of high-net-worth individuals, business owners and families. It combines the benefits of a boutique client experience, one guided by the fiduciary standard and principle of always placing client interests first, supported by the strength, size and scale of being part of CI Financial. CI PW offers an unrivalled experience that combines discretionary investment management and comprehensive wealth planning, including sophisticated financial planning, retirement planning, estate and legacy planning, and tax strategies for individuals, businesses and multi-generational families. Supporting our advisory teams across Canada in the delivery of an integrated client experience is a robust, multi- disciplinary team of experts — including lawyers, accountants, Certified Financial Planners, Certified Financial Analysts, MBAs and other professionals. They are all part of a dedicated client service team that is available to help plan, provide guidance, and answer technical questions that may impact our clients — be they business owners contemplating transition, professionals and executives looking to mitigate tax, individuals working through a divorce, who’ve inherited money or dealing with other life events. Despite the challenges of 2020, CI PW continued to see great success, especially among ultra-high-net-worth investors. We’ve also seen an increase in liquidity from business and real estate sales this year, furthering our growth opportunities through prospecting as well supporting existing clients. CI PW is a division of CI Private Counsel LP, which also manages the Assante Private Client Program. 2020 OPERATING HIGHLIGHTS • Our assets reached a record high at year-end of $7.8 billion, consisting of assets in Assante Private Client and those managed by advisors with Stonegate Private Counsel. • In 2020, we began the rebranding of Stonegate to CI Private Wealth, which was completed in the first quarter of 2021. • We accelerated our efforts to modernize our firm through digital automation, increasingly specialized investment management expertise, and enhancing our client and advisor experiences. • The d1g1t wealth management platform launched with a rollout to all investment counsellors and Stonegate advisors. The next phase will focus on improving the service experience by introducing client and advisor portals. • We continued to focus on providing a diverse lineup of alternative investment strategies for accredited investors, including CI Global Private Real Estate Fund and launching CI Adams Street Global Private Markets Fund. • In the fourth quarter of 2020, we welcomed our first Assante Private Client household to CI Investment Services Inc., rolling out a new custodial relationship that will allow us to better control the end-to-end experience for our high-net-worth clients, offer custodial optionality and streamline the onboarding process. • Our financial planning team completed its shift to NaviPlan Online, improving our abilities in NaviPlan file sharing between our Wealth Planning Group and advisors, and furthering our digital transformation goals. |

| ANNUAL REPORT 2020 21 CI PRIVATE WEALTH — UNITED STATES A major element supporting CI’s corporate strategy to globalize the firm and expand its wealth management platform has been its expanding presence in the U.S. RIA industry. As a well-capitalized company with extensive experience in wealth management and a unique value proposition relative to other firms, CI’s competitive advantages have supported the acquisition of several leading RIAs located in key U.S. markets. At December 31, 2020, CI’s U.S. wealth management holdings comprised 10 firms with aggregate assets of $29 billion. They include: BDF LLC (“BDF”), Itasca, IL — The BDF team of 62 people provides customized wealth management services to individuals and families, business owners and institutions and non-profit organizations from offices in the Chicago area. The firm advises on approximately $6.7 billion in assets. BDF was ranked Number 30 on the RIA Channel Top 100 Wealth Managers for 2020, and was listed on the 2020 FT300: Top Registered Investment Advisors and the Barron’s Top RIAs for 2020. CI owns 100% of BDF. Bowling Portfolio Management LLC (“Bowling”), Cincinnati, OH — Bowling provides customized financial planning and investment management services to high-net-worth clients. The firm, which advises on approximately $600 million in assets, has been a stalwart in the Cincinnati market since its founding in 1982. CI owns 100% of Bowling. The Cabana Group LLC (“Cabana”), Fayetteville, AR — Cabana oversees approximately $2.2 billion in assets from offices in Fayetteville and Plano, TX. Cabana also manages the Cabana Target Drawdown series of ETFs and separately managed portfolios. CI owns a minority interest in Cabana. Congress Wealth Management LLC (“Congress”), Boston, MA — Congress advises on approximately $3.6 billion in assets from offices in Boston, Westport, CT, Scottsdale, AZ, and Orange City and Avila Beach, CA. Congress provides wealth management and family office services to high-net-worth individuals, families, foundations, and endowments, with an emphasis on comprehensive and customized client plans. The firm was named to the Financial Times 300 Top Registered Investment Advisors list of 2019, the third time in four years it has received the award. CI owns a minority interest in Congress. Doyle Wealth Management LLC (“DWM”), St. Petersburg, FL — DWM advises on approximately $1.6 billion in assets, providing a wide range of wealth management services to high-net-worth individuals in the Tampa Bay region. The firm’s accolades include being named to the Barron’s magazine list of Florida’s Top Financial Advisors from 2015-2020, ranking No. 3 in North Florida on the 2020 Forbes list of America’s Best in State Wealth Advisors, and appearing on the Forbes list of America’s Top Wealth Advisors from 2016-2019. CI owns 100% of DWM. One Capital Management LLC (“OCM”), Westlake Village, CA — OCM advises on approximately $3.3 billion in assets. The firm features well-developed expertise in advanced wealth planning, including specializations in family office services and a division focused on the needs of professional athletes and entertainers. It also has a robust cross-border servicing capability. CI owns a majority interest in OCM. |

| 22 ANNUAL REPORT 2020 RGT Wealth Advisors, LLC (“RGT”), Dallas, TX — RGT, with $6.1 billion in assets, offers a fully integrated approach to investment management and wealth management, with specializations in wealth management and planning for corporate executives, business owners, multi-generational families, and current and retired professional athletes. The firm’s accolades include being recognized by Barron’s magazine as one of America’s Best Registered Investment Advisor Firms in 2019 and 2020. CI owns a majority interest in RGT. Roosevelt Investment Group, LLC (“Roosevelt”), New York, NY — Roosevelt advises on approximately $3.8 billion, specializing in providing financial planning and wealth management services to high-net-worth families in the greater New York area. CI owns 100% of Roosevelt. Stavis & Cohen Private Wealth LLC (“Stavis”), Houston, TX — Stavis is a leading Houston-based wealth management firm advising on approximately $800 million in assets. Its service offerings include retirement planning, investment management, risk management, estate planning and business succession, as well as specializations in serving energy industry executives, business owners and financially independent women. CI owns a majority interest in Stavis. Surevest Private Wealth LLC (“Surevest”), Los Angeles, CA — Surevest advises on approximately $600 million in assets from offices in Los Angeles and Phoenix. It specializes in providing a wide range of fee-only financial planning and investment management services to high-net-worth individuals through a concierge approach to wealth management. CI owns a majority interest in Surevest. CI DIRECT INVESTING CI Direct Investing, the operating name of WealthBar Financial Services Inc., exists to give Canadians an easy and affordable way to build a brighter financial future, whether they’re starting with $1,000 or $1 million. We make it easy to build one’s financial future with convenient online savings and investing tools, and financial advice. CI Direct Investing has approximately $562 million in assets under management, as at March 31, 2021. Our “hybrid model” combines technology with professional advice for a personalized experience. Through our online platform, investors can access a mix of investment portfolios. The firm operates two advisor channels, including Assante Connect, which launched in 2019 exclusively for clients of Assante advisors. This digital wealth management platform pairs seasoned portfolio managers with digital advice services to help advisors scale their business and augment their offerings. The other is PPI Valet, which delivers a far- ranging suite of investment options for PPI advisors and their clients. 2020 OPERATING HIGHLIGHTS • CI Financial extended its ownership of CI Direct Investing to 100%. • We adopted the CI Direct Investing brand as part of a first step in creating in an integrated online investment platform. • Our total AUM grew by 29% to approximately $518 million. |

| ANNUAL REPORT 2020 23 CI INVESTMENT SERVICES AND VIRTUAL BROKERS CI Investment Services (“CIIS”), formerly BBS Securities Inc., is a Canadian financial technology company and a registered investment dealer that provides a wide range of innovative brokerage, trading and investment services to a diverse client base of portfolio managers, broker dealers, institutional and retail investors. Through our online brokerage division, Virtual Brokers, CIIS provides services using a proprietary system that offers innovative trading platforms to the retail Canadian market. CIIS offers a wide range of brokerage services, including clearing, custody, settlement and trade execution services for all investment types, multiple trading platforms, access to new issues and risk monitoring to a wide range of customers (from registered portfolio managers to retail clients). We leverage our technological capability to provide online brokerage and trade execution services to individual investors, active traders and institutions. 2020 OPERATING HIGHLIGHTS • Our total assets grew to $4.2 billion. • We rebranded to CI Investment Services from BBS Securities, as part of CI Financial’s overall corporate rebrand. • We modernized the firm’s proprietary books and records system. • Virtual Brokers was recognized by the Globe and Mail as one of the top discount brokerages in Canada for 2020. • CIIS implemented a digital client portal for CI’s high-net-worth client base based on the d1g1t technology platform. |

| CI Financial (“CI”) strives to operate with responsibility and integrity, from the management of our funds to the conduct of all aspects of our business. We are committed to treating our employees and business partners with respect and consideration, to supporting communities across Canada, and to reducing our impact on the environment. This section highlights some of CI’s efforts and achievements in these areas. CORPORATE SOCIAL RESPONSIBILITY |

| ANNUAL REPORT 2020 25 MEMBERSHIPS & RECOGNITION SIGNATORY TO THE UNPRI The United Nations Principles for Responsible Investment (UNPRI) is the world’s leading proponent of responsible investment. It encourages investors to use responsible investment to enhance returns and better manage risks. ASSOCIATE MEMBER OF THE RIA The Responsible Investment Association (RIA) is Canada’s membership association for responsible investment. RIA members believe that the integration of environmental, social and governance (ESG) factors into the selection and management of investments can provide superior risk-adjusted returns while contributing to positive societal change. GREAT PLACE TO WORK CI Financial was certified as a Great Place to Work, a Canada-wide survey program that recognizes companies where employees exhibit a high level of trust in their employer, pride in their work and camaraderie with colleagues. COMMITMENT TO CORPORATE GOVERNANCE AND INTEGRITY • CI’s Board of Directors and management are committed to maintaining a high standard of governance consistent with the governance guidelines of the Canadian Securities Administrators and best practices recommendations of the Canadian Coalition for Good Governance. • All directors, officers, and employees of CI Financial and its subsidiaries and affiliates are governed by the CI Code of Business Conduct and Ethics, which requires them to follow prescribed standards of integrity and ethical business conduct. • The Board of Directors oversees risk management through the board’s Audit and Risk Committee, and governance through its Governance, Human Resources, and Compensation Committee. • CI upholds principles, policies, and procedures that promote integrity and ensure compliance with applicable laws and regulations in specialized areas of the company. These include policies addressing money laundering, bribery and corruption, personal trading by portfolio managers and other employees, as well as sales practices. • We are dedicated to respecting and protecting the privacy and confidentiality of the information entrusted to us. Our Privacy Notice outlines our principles and practices. • CI has established formal Ethical Reporting Procedures through which employees can anonymously report questionable conduct and concerns to the Board’s Lead Director. • CI employees are required to complete annual Security Awareness Training and acknowledgement of key corporate policies. • In recognition of our increased efforts to enhance the quality of our disclosure on environmental, social and governance (“ESG”) factors and to improve our overall performance, CI established a multi-departmental ESG committee. The committee includes members from finance, legal, investor relations and our ESG team. |

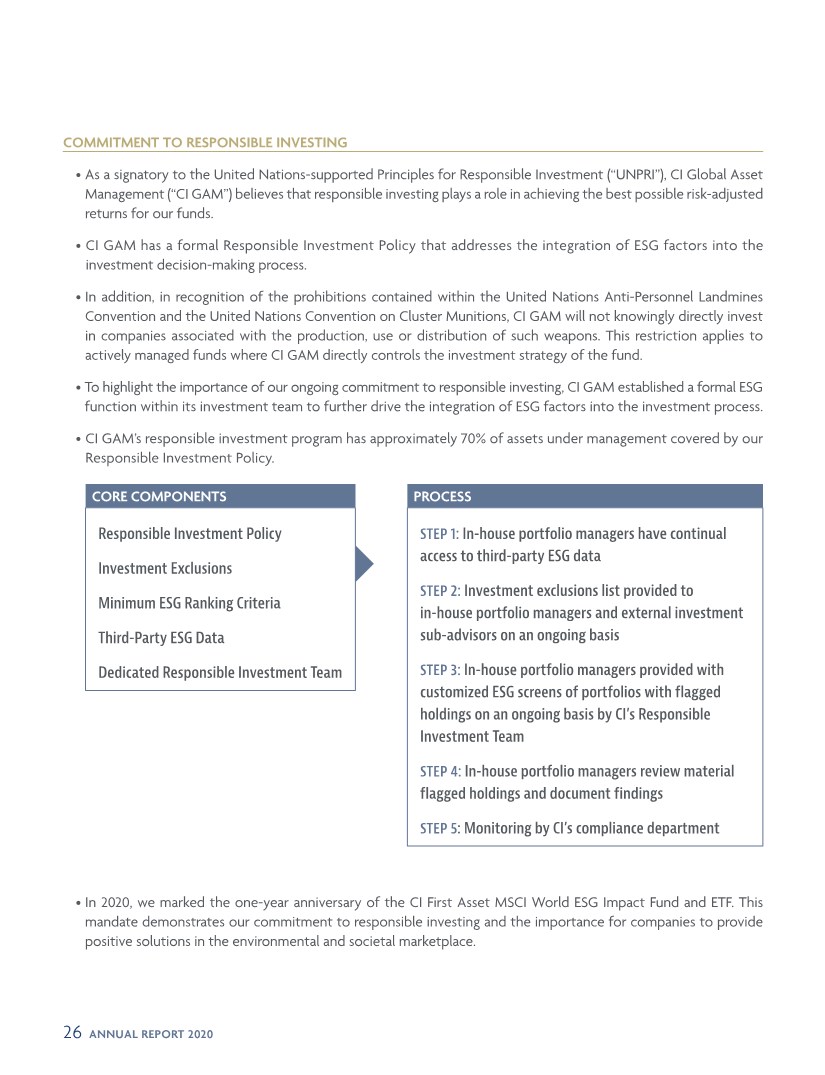

| 26 ANNUAL REPORT 2020 COMMITMENT TO RESPONSIBLE INVESTING • As a signatory to the United Nations-supported Principles for Responsible Investment (“UNPRI”), CI Global Asset Management (“CI GAM”) believes that responsible investing plays a role in achieving the best possible risk-adjusted returns for our funds. • CI GAM has a formal Responsible Investment Policy that addresses the integration of ESG factors into the investment decision-making process. • In addition, in recognition of the prohibitions contained within the United Nations Anti-Personnel Landmines Convention and the United Nations Convention on Cluster Munitions, CI GAM will not knowingly directly invest in companies associated with the production, use or distribution of such weapons. This restriction applies to actively managed funds where CI GAM directly controls the investment strategy of the fund. • To highlight the importance of our ongoing commitment to responsible investing, CI GAM established a formal ESG function within its investment team to further drive the integration of ESG factors into the investment process. • CI GAM’s responsible investment program has approximately 70% of assets under management covered by our Responsible Investment Policy. • In 2020, we marked the one-year anniversary of the CI First Asset MSCI World ESG Impact Fund and ETF. This mandate demonstrates our commitment to responsible investing and the importance for companies to provide positive solutions in the environmental and societal marketplace. CORE COMPONENTS Responsible Investment Policy Investment Exclusions Minimum ESG Ranking Criteria Third-Party ESG Data Dedicated Responsible Investment Team PROCESS STEP 1: In-house portfolio managers have continual access to third-party ESG data STEP 2: Investment exclusions list provided to in-house portfolio managers and external investment sub-advisors on an ongoing basis STEP 3: In-house portfolio managers provided with customized ESG screens of portfolios with flagged holdings on an ongoing basis by CI’s Responsible Investment Team STEP 4: In-house portfolio managers review material flagged holdings and document findings STEP 5: Monitoring by CI’s compliance department |

| ANNUAL REPORT 2020 27 COMMITMENT TO EMPLOYEES • In 2020, we were Great Place to Work® certified, with an 85% employee participation rate in the survey. CI was also named one of Canada’s Best Workplaces in Financial Services & Insurance for 2020 by the Great Place to Work organization. • CI believes that to be competitive in a global environment, we must create a culture of trust where people know their differences are valued as they strive to be innovative without barriers. Diversity will strengthen our collective success and potential by enabling CI to attract and retain the best talent, bringing innovation and different perspectives to the table. CI is committed to a diverse and inclusive culture where all employees feel: Valued — They are appreciated and respected for their unique perspectives and talents. Trusted — They make meaningful contributions and are influential in decision-making. Authentic — They can bring their full selves to work and express aspects of themselves that may be different from their peers. Psychologically Safe — They feel free to hold differing views and make mistakes without being penalized and secure enough to address tough issues or take risks. • In 2020, CI launched a Diversity and Inclusion Committee made up of volunteer employees, people managers and leaders to further the important work of creating an inclusive culture and workplace environment. • CI provides extensive training and learning opportunities for employees, giving them access to a variety of tools and resources to support skill development, including eLearning courses and classroom-based workshops. CI also supports those who pursue education and training on their own initiative through tuition reimbursement and other recognition. • To support our strategic imperative of modernizing our business through digital automation, we implemented Learning Paths to provide development content for employees to build their digital competencies, as well as their skills in agile methodologies, critical thinking, embracing change and fostering innovation. • CI’s successful Women’s Mentoring Program has been supporting female employees since 2012. The newly redesigned MentorHub is a virtual cross-country mentoring program for top talent with consideration for inclusive representation. About 70% of participants identified as members of a designated group. • Despite the global pandemic, CI offered important learning opportunities and work experience to 85 students through summer and co-op placements. |

| 28 ANNUAL REPORT 2020 SPOTLIGHT: COVID-19 RESPONSE • As a result of investments in technology and crisis planning, CI was well prepared to respond to the COVID-19 pandemic. In March 2020, CI created a COVID-19 Response Team which oversaw a quick and efficient transition to a work-from-home environment for most employees. The team has supplied regular company-wide updates of the ever-changing pandemic conditions, including a Wellness Check-in Survey for employees to provide feedback on CI’s response. • By mid-March 2020, more than 95% of employees were successfully working from home. For staff members whose duties require them to be in the office, CI has taken extraordinary measures to help ensure their safety, including providing them with private transportation, parking and meals. • Due to the growing mental health challenges presented by the pandemic, CI expanded employee wellness benefits, including doubling benefit coverage for psychological services. Throughout the year, virtual mental health resources were offered, including coping mechanisms, strategies for well-being, and access to mental health professionals. In November 2020, CI hosted a Virtual Wellness Day to provide fitness and wellness workshops for employees. • In response to the pandemic, CI took steps to respond to our communities’ most urgent needs. We made donations to Second Harvest to help Canada’s most food-insecure communities, while Assante launched the Be Well-Advised program, in which Assante advisors volunteer to provide free financial advice to Canadians experiencing financial hardship. COMMITMENT TO COMMUNITIES • CI is committed to supporting communities across Canada and to being a good corporate citizen. In addition to making significant donations to charitable and community causes, we provide employees with one paid day off per year, known as a Ray Day, to volunteer with a community organization or charity of their choice. This program was named in memory of CI’s former Chairman and Chief Executive Officer Ray Chang, who was well known for his commitment to philanthropy. |

| ANNUAL REPORT 2020 29 HIGHLIGHTS OF CI’S CHARITABLE GIVING: • CI made donations to organizations that are focused on improving the lives of the Black community, including the: CEE Centre for Young Black Professionals — Focused on youth workforce development, education and advocacy to influence systems and policy. Black Business and Profession Association — Facilitates the delivery of programs that support business and professional excellence, higher education and economic development. Black Health Alliance — Supports the health and well-being of Black communities in Canada. • SickKids GetLoud — CI was a Premier Sponsor of SickKids GetLoud, a campaign to help build a new SickKids hospital in Toronto, and donated over $150,000. • Second Harvest — In 2020, CI was a premium sponsor of Second Harvest’s mission to feed families, support communities and protect the environment. • SAAAC Autism Centre — CI’s donation supported culturally responsive autism practices and accessible programming • The Arthritis Society — CI has been a supporter of the Arthritis Society since 2008, with funds contributing to cutting-edge research, proactive advocacy and innovative solutions that will deliver better health outcomes for people affected by arthritis. • Wilfrid Laurier University — CI is proud to partner with Wilfrid Laurier University in preparing Canada’s next generation of financial managers and to provide support for the “Building Canada’s Best Business School” fundraising campaign. In 2020, CI donated $50,000 as part of a larger $500,000 commitment to supporting the finance program at the Lazaridis School of Business and Economics and the CI Financial Finance Lab, which opened in 2017. SPOTLIGHT: AUSTRALIA WILDFIRES RELIEF EFFORTS • In January 2020, CI launched a campaign to raise funds for Australia wildfire relief efforts through the Canadian Red Cross, raising over $40,000. The proceeds helped send Australian Red Cross staff and volunteers to communities affected by the fires and provided support for displaced persons. |

| 30 ANNUAL REPORT 2020 COMMITMENT TO ENVIRONMENTAL SUSTAINABILITY • We continue to use paper certified under the Sustainable Forestry Initiative. This standard sets mandatory practice requirements for the responsible procurement of all fibre sourced directly from forests. • In support of our ongoing effort to reduce CI’s environmental footprint, we have launched several waste reduction initiatives, including introducing composting and eliminating the provision of disposable plates, cups, cutlery and water bottles at certain Toronto locations. SPOTLIGHT: E-DELIVERY INITIATIVE • In support of our mission to modernize our asset management business and reduce our environmental footprint, CI decided in 2020 to deliver client documents primarily through online tools. This successful initiative saw a 57% decline in printed statements year over year, with 83% of CI statements being delivered electronically. |

| QUARTERLY FINANCIAL REPORT Q4 | 2020 DECEMBER 31, 2020 |

| TABLE OF CONTENTS 01 — Financial Highlights 02 — Management’s Discussion and Analysis 38 — Consolidated Financial Statements 46 — Notes to Consolidated Financial Statements |

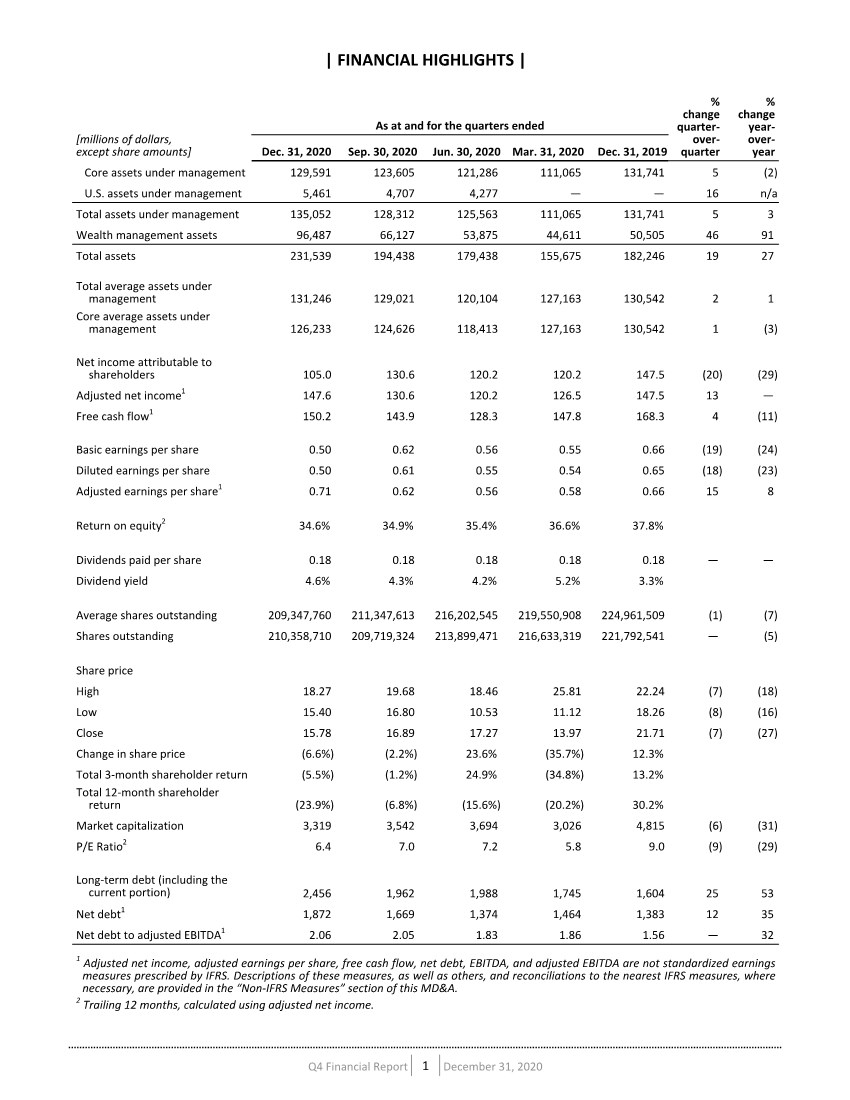

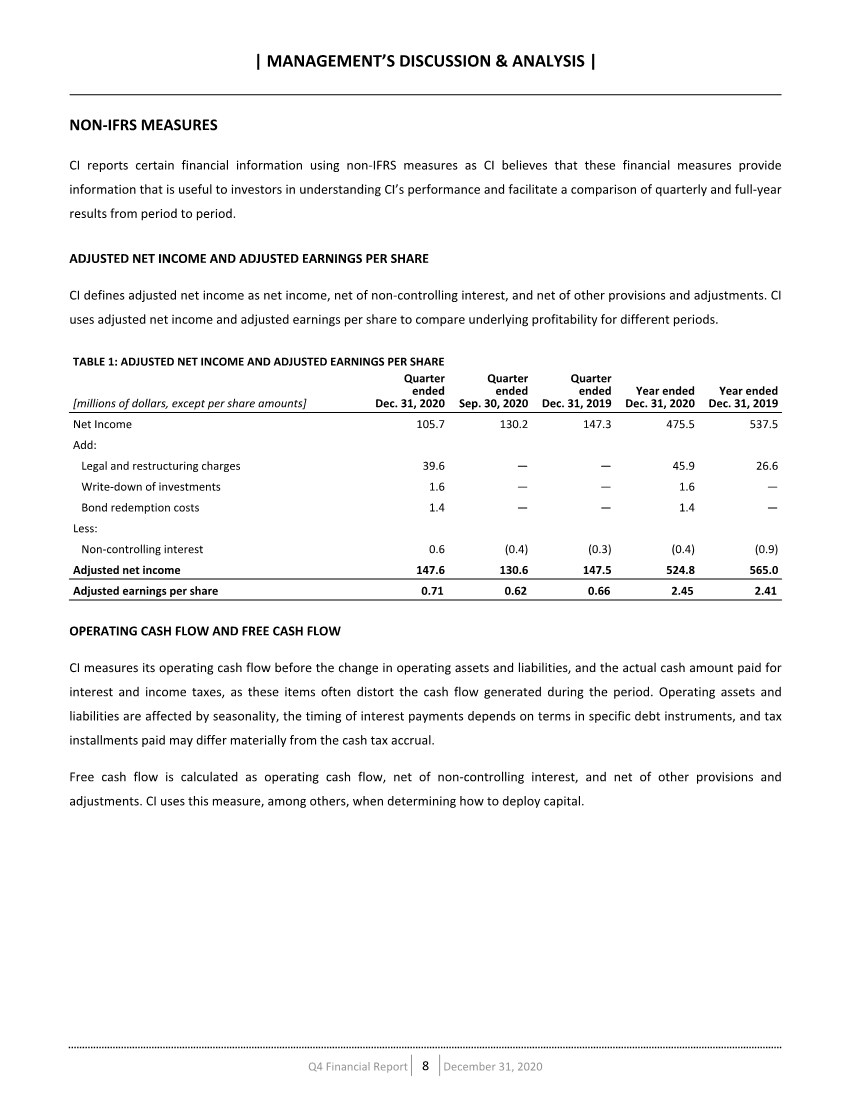

| | FINANCIAL HIGHLIGHTS | [millions of dollars, except share amounts] As at and for the quarters ended % change quarter- over- quarter % change year- over- year Dec. 31, 2020 Sep. 30, 2020 Jun. 30, 2020 Mar. 31, 2020 Dec. 31, 2019 Core assets under management 129,591 123,605 121,286 111,065 131,741 5 (2) U.S. assets under management 5,461 4,707 4,277 — — 16 n/a Total assets under management 135,052 128,312 125,563 111,065 131,741 5 3 Wealth management assets 96,487 66,127 53,875 44,611 50,505 46 91 Total assets 231,539 194,438 179,438 155,675 182,246 19 27 Total average assets under management 131,246 129,021 120,104 127,163 130,542 2 1 Core average assets under management 126,233 124,626 118,413 127,163 130,542 1 (3) Net income attributable to shareholders 105.0 130.6 120.2 120.2 147.5 (20) (29) Adjusted net income1 147.6 130.6 120.2 126.5 147.5 13 — Free cash flow1 150.2 143.9 128.3 147.8 168.3 4 (11) Basic earnings per share 0.50 0.62 0.56 0.55 0.66 (19) (24) Diluted earnings per share 0.50 0.61 0.55 0.54 0.65 (18) (23) Adjusted earnings per share1 0.71 0.62 0.56 0.58 0.66 15 8 Return on equity2 34.6% 34.9% 35.4% 36.6% 37.8% Dividends paid per share 0.18 0.18 0.18 0.18 0.18 — — Dividend yield 4.6% 4.3% 4.2% 5.2% 3.3% Average shares outstanding 209,347,760 211,347,613 216,202,545 219,550,908 224,961,509 (1) (7) Shares outstanding 210,358,710 209,719,324 213,899,471 216,633,319 221,792,541 — (5) Share price High 18.27 19.68 18.46 25.81 22.24 (7) (18) Low 15.40 16.80 10.53 11.12 18.26 (8) (16) Close 15.78 16.89 17.27 13.97 21.71 (7) (27) Change in share price (6.6%) (2.2%) 23.6% (35.7%) 12.3% Total 3-month shareholder return (5.5%) (1.2%) 24.9% (34.8%) 13.2% Total 12-month shareholder return (23.9%) (6.8%) (15.6%) (20.2%) 30.2% Market capitalization 3,319 3,542 3,694 3,026 4,815 (6) (31) P/E Ratio2 6.4 7.0 7.2 5.8 9.0 (9) (29) Long-term debt (including the current portion) 2,456 1,962 1,988 1,745 1,604 25 53 Net debt1 1,872 1,669 1,374 1,464 1,383 12 35 Net debt to adjusted EBITDA1 2.06 2.05 1.83 1.86 1.56 — 32 1 Adjusted net income, adjusted earnings per share, free cash flow, net debt, EBITDA, and adjusted EBITDA are not standardized earnings measures prescribed by IFRS. Descriptions of these measures, as well as others, and reconciliations to the nearest IFRS measures, where necessary, are provided in the “Non-IFRS Measures” section of this MD&A. 2 Trailing 12 months, calculated using adjusted net income. Q4 Financial Report 1 December 31, 2020 |

| Management’s Discussion and Analysis DECEMBER 31, 2020 CI FINANCIAL CORP. |

| This Management’s Discussion and Analysis (“MD&A”) dated February 11, 2021 presents an analysis of the financial position of CI Financial Corp. and its subsidiaries (“CI”) as at December 31, 2020, compared with December 31, 2019, and the results of operations for the quarter and year ended December 31, 2020, compared with the quarter and year ended December 31, 2019 and the quarter ended September 30, 2020. CI’s Consolidated Financial Statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board. Amounts are expressed in Canadian dollars. The principal subsidiaries referenced herein include CI Investments Inc. (“CI Investments”) and Assante Wealth Management (Canada) Ltd. (“AWM” or “Assante”). CI has two reportable segments: Asset Management and Wealth Management (formerly Asset Administration). These segments reflect CI’s current internal financial reporting, performance measurement, and strategic priorities. The Asset Management segment of the business includes the operating results and financial position of CI Investments and its subsidiaries, as well as the operating results and financial position of GSFM Pty Limited (“GSFM”). First Asset Investment Management Inc., formerly a subsidiary of CI Investments, was amalgamated on July 1, 2019. CI ETF Investment Management Inc. (“CI ETF”), formerly WisdomTree Asset Management Canada, Inc. and a subsidiary of CI Investments, was amalgamated on July 1, 2020. The Wealth Management segment includes the operating results and financial position of AWM and its subsidiaries, including Assante Capital Management Ltd. (“ACM”) and Assante Financial Management Ltd. (“AFM”), as well as the operating results and financial position of CI Investment Services Inc. (“CI Investment Services”, formerly BBS Securities Inc.), WealthBar Financial Services Inc., operating as CI Direct Investing (“CI Direct Investing”), Aligned Capital (“Aligned”), Surevest LLC (“Surevest”), OCM Capital Partners LLC (“One Capital”), The Cabana Group LLC (“Cabana”), Congress Wealth Management LLC (“Congress”), Balasa Dinverno Foltz LLC (“BDF”), Bowling Portfolio Management LLC (“Bowling”), Stavis & Cohen Private Wealth LLC (“Stavis Cohen”), Doyle Wealth Management LLC (“Doyle”), The Roosevelt Investment Group LLC (“Roosevelt”), and RGT Wealth Advisors LLC (“RGT”). CI Private Counsel LP (“CIPC”), previously included in the Asset Management segment, is included in the Wealth Management segment effective January 1, 2020. The impact of this change was to move revenue of approximately $69.0 million and related expenses to the Wealth Management segment in the year ended December 31, 2020. The operating results of prior periods have been restated for comparative purposes. | MANAGEMENT’S DISCUSSION & ANALYSIS | Q4 Financial Report 3 December 31, 2020 |

| This MD&A contains forward-looking statements concerning anticipated future events, results, circumstances, performance or expectations with respect to CI Financial Corp. and its products and services, including its business operations, strategy and financial performance and condition. Forward-looking statements are typically identified by words such as “believe”, “expect”, “foresee”, “forecast”, “anticipate”, “intend”, “estimate”, “goal”, “plan” and “project” and similar references to future periods, or conditional verbs such as “will”, “may”, “should”, “could” or “would”. These statements are not historical facts but instead represent management beliefs regarding future events, many of which by their nature are inherently uncertain and beyond management’s control. Although management believes that the expectations reflected in such forward-looking statements are based on reasonable assumptions, such statements involve risks and uncertainties. The material factors and assumptions applied in reaching the conclusions contained in these forward-looking statements include that the investment fund industry will remain stable and that interest rates will remain relatively stable. Factors that could cause actual results to differ materially from expectations include, among other things, general economic and market conditions, including interest and foreign exchange rates, global financial markets, the impact of the coronavirus pandemic, changes in government regulations or in tax laws, industry competition, technological developments and other factors described or discussed in CI’s disclosure materials filed with applicable securities regulatory authorities from time to time. The foregoing list is not exhaustive and the reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Other than as specifically required by applicable law, CI undertakes no obligation to update or alter any forward-looking statement after the date on which it is made, whether to reflect new information, future events or otherwise. This MD&A includes several non-IFRS financial measures that do not have any standardized meaning prescribed by IFRS and may not be comparable to similar measures presented by other companies. CI believes that these financial measures provide information that is useful to investors in understanding CI’s performance and facilitate a comparison of quarterly and full year results from period to period. Descriptions of these non-IFRS measures and reconciliations to the nearest IFRS measure, where necessary, are provided in the “Non-IFRS Measures” section of this MD&A. Note that figures in tables may not add due to rounding. | MANAGEMENT’S DISCUSSION & ANALYSIS | Q4 Financial Report 4 December 31, 2020 |

| BUSINESS OVERVIEW CI is a diversified wealth management firm and one of Canada’s largest independent asset management companies. CI’s principal business is the management, marketing, distribution and administration of investment products for Canadian investors. CI also provides financial advice, tax, retirement, estate and wealth planning services in Canada through Assante, CIPC, CI Direct Investing, Aligned, and in the United States through Surevest, One Capital, Cabana, Congress, BDF, Bowling, Stavis Cohen, Doyle, Roosevelt, and RGT. In addition, CI has asset management operations in Australia through its subsidiary GSFM. CI’s products are distributed primarily through brokers, independent financial planners and insurance advisors, including ACM, AFM, and Aligned financial advisors. CI operates through two business segments, Asset Management and Wealth Management. The Asset Management segment provides the majority of CI’s income and derives its revenue principally from the fees earned on the management of investment funds and other fee-earning investment products. CI uses in-house teams and external investment managers to provide portfolio management services. These investment managers typically have long careers in the industry as well as extensive track records with CI. This lineup of investment managers provides a wide selection of styles and areas of expertise for CI’s funds and ETFs. The Wealth Management segment (previously called Asset Administration) was renamed to better reflect CI’s performance measurement and business strategy, and now includes the results of operations of CIPC (previously in Asset Management). The Wealth Management segment derives its revenue principally from fees and commissions for providing financial planning and advice (which may include investment management services), and on the sale of investment funds and other financial products. Prior results have been restated for comparative purposes. BUSINESS STRATEGY In the fourth quarter of 2019, CI Financial announced a new strategic direction for the company, with the introduction of three strategic priorities: • Modernize the asset management business • Expand the wealth management platform • Globalize the company In establishing these priorities, CI sought input from a series of critical sources, including employees, clients, shareholders and industry analysts, and incorporated insights from observing market dynamics and industry trends. Each strategic priority builds on CI’s existing extensive capabilities to take advantage of opportunities in the marketplace. A key factor in CI’s focus on modernizing its asset management business is that the rate and pace of change in the industry is at an all-time high, due to changes in demographics and investor preferences, changing client expectations for service and support, and ongoing regulatory change. This environment requires new services, new products and new approaches to meet investors’ changing needs. | MANAGEMENT’S DISCUSSION & ANALYSIS | Q4 Financial Report 5 December 31, 2020 |