As filed with the Securities and Exchange Commission on February 12, 2021.

Registration Statement No. 333-252036

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

GOLD ROYALTY CORP.

(Exact name of registrant as specified in its charter)

| Canada | 1040 | Not Applicable | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

1030 West Georgia Street, Suite 1830

Vancouver, BC V6E 2Y3

(604) 396-3066

(Address, including zip code and telephone number, including area code, of registrant’s principal executive offices)

C T Corporation System

28 Liberty Street

New York, New York 10005

(212) 894-8940

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Rick A. Werner, Esq. | Rod Talaifar, Esq. | Joseph A. Smith, Esq. | Steven D. Bennett, Esq. | |||

| Haynes and Boone, LLP | Sangra Moller LLP | Ellenoff Grossman & Schole LLP | Stikeman Elliott LLP | |||

| 30 Rockefeller Plaza | 1000 Cathedral Place | 1345 Avenue of the Americas | 5300 Commerce Court West | |||

| 26th Floor | 925 West Georgia Street | 11th Floor | 199 Bay Street | |||

| New York, New York 10112 | Vancouver, BC, Canada V6C 3L2 | New, York, New York 10105 | Toronto, Ontario Canada, M5L 1B9 | |||

| Tel: +1 212 659-7300 | Tel: +1 604 662-8808 | Tel: +1 212 370-7889 | Tel: +1 416 869-5205 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. [X]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non-accelerated filer | [X] | Smaller reporting company | [X] |

| Emerging growth company | [X] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. [ ]

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities To Be Registered | Proposed Maximum Offering Price(1)(2)(3) | Amount of Registration Fee | ||||||

| Units, each consisting of one common share, no par value, and one-half warrant | $ | 34,500,000 | $ | 3,763.95 | ||||

| (1) Common shares included as part of the Units | — | — | (4) | |||||

| (2) Warrants included as part of the Units | — | — | (4) | |||||

| Common shares issuable upon exercise of the warrants | $ | 25,875,000 | $ | 2,822.96 | ||||

| Total | $ | 60,375,000 | $ | 6,586.91 | (5) |

| (1) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended, referred to as the “Securities Act.” |

| (2) | Includes the aggregate offering price of additional common shares and/or warrants to purchase common shares that the underwriters have the option to purchase, if any. |

| (3) | Pursuant to Rule 416, there are also being registered an indeterminable number of additional securities as may be issued to prevent dilution resulting from stock splits, stock dividends or similar transactions. |

| (4) | No additional registration fee is payable pursuant to Rule 457(i) under the Securities Act. |

(5) | A filing fee of $3,763,95 was previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED FEBRUARY 12, 2021 |

Units, each consisting of one Common Share and

one-half of one Warrant to purchase one Common Share

$30,000,000

6,000,000 Units

GOLD ROYALTY CORP.

This is the initial public offering of our securities in the United States. We are offering 6,000,000 units, or the “units,” with each unit having an offering price of $5.00 and consisting of (i) one common share, no par value per share, and (ii) one-half (1/2) warrant to purchase a common share, or the “warrants.” Each whole warrant entitles the holder thereof to purchase one common share at a price of $7.50 per share, subject to adjustment as described in this prospectus. Only whole warrants are exercisable.

Prior to this offering, no public market has existed for our common shares or warrants. We have applied to list our common shares and warrants on the NYSE American under the symbols “GROY” and “GROY WS,” respectively.

We are an “emerging growth company” as that term is defined in the Jumpstart Our Business Startups Act of 2012 and, as such, will be subject to reduced public company reporting requirements for this prospectus and future filings.

GoldMining Inc., our parent company and majority shareholder, controls approximately 88% of the voting power of our common shares, and we are therefore a “controlled company” as defined in the NYSE American Company Guide. However, even if we qualify as a “controlled company,” we do not intend to rely on the controlled company exemptions provided in the NYSE American Company Guide.

Investing in our securities is speculative and involves a high degree of risk. See “Risk Factors” beginning on page 14 for a discussion of information that you should consider before investing in our securities.

| Per unit | Total | |||||||

| Initial public offering price(1) | $ | 5.00 | $ | 30,0000,000 | ||||

| Underwriting discounts and commissions(2) | $ | 0.35 | $ | 2,100,000 | ||||

| Proceeds to us, before expenses | $ | 4.65 | $ | 27,900,000 |

| (1) | The initial public offering price and underwriting discount corresponds to an initial public offering price per unit of $5.00. |

| (2) | Represents underwriting discount and commissions equal to 7.0% of the aggregate purchase price paid by the underwriters to us per unit. A reduced underwriting discount of 2.0% will be payable on the gross proceeds of up to $9,900,000 of the offering sold to certain purchasers and thereafter the full 7.0% discount will apply. We have also agreed to reimburse the representatives of the underwriters for certain of their expenses. See “Underwriting” for additional information regarding total underwriter compensation. |

We have granted the underwriters the right to purchase up to an additional 900,000 common shares and/or warrants to purchase up to 450,000 common shares to cover over-allotments, if any. The underwriters can exercise this right at any time within 30 days after the date of this prospectus. If the underwriters exercise the option in full, the total underwriting discounts and commissions payable by us will be $2,415,000, and the total proceeds to us, before expenses, will be $32,085,000.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the units against payment in New York, New York on or about , 2021 .

| H.C. Wainwright & Co. | BMO Capital Markets |

Prospectus dated , 2021

TABLE OF CONTENTS

Neither we nor the underwriters have authorized anyone to provide you with information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give to you. The information contained in this prospectus or any free writing prospectus is accurate only as of the date of this prospectus or such free writing prospectus, regardless of the time of delivery of this prospectus or any free writing prospectus.

We are offering to sell, and seeking offers to buy, units only in jurisdictions where offers and sales are permitted. Neither we nor the underwriters have taken any action to permit a public offering of our units or the possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

We are also offering units in Canada by way of a separate Canadian prospectus. The Canadian prospectus, which will be filed with the securities regulators in all of the provinces and territories of Canada, other than Quebec, has the same date as this prospectus and contains substantially the same information but has a different format and is not considered part of this prospectus. The offering being made in the United States is being made solely on the basis of the information contained in this prospectus. Investors should take this into account when making investment decisions.

| i |

BASIS OF PRESENTATION

Unless otherwise indicated, references in this prospectus to “Gold Royalty,” “GRC,” “the Company,” “we,” “us” and “our” refer to Gold Royalty Corp., a company incorporated under the laws of Canada.

We express all amounts in this prospectus in U.S. dollars, except where otherwise indicated. References to “$” and “US$” are to U.S. dollars and references to “C$” are to Canadian dollars. Except as otherwise noted, conversions from Canadian dollars into U.S. dollars were made at the rate of C$1,2686 to $1.00, which was the rate in effect on February 11, 2021 as published by the Bank of Canada.

We have made rounding adjustments to some of the figures included in this prospectus. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

PRESENTATION OF FINANCIAL INFORMATION

We report under International Financial Reporting Standards as issued by the International Accounting Standards Board, referred to as “IFRS.” None of the financial statements were prepared in accordance with generally accepted accounting principles in the United States. We present our financial statements in U.S. dollars.

MARKET, INDUSTRY AND OTHER DATA

Unless otherwise indicated, information contained in this prospectus concerning our industry and the market in which we operate, including our market position, market opportunity and market size, is based on information from various sources such as industry publications, on assumptions that we have made based on such data and other similar sources and on our knowledge of the markets for our products. These data involve a number of assumptions and limitations. We have not independently verified any third-party information.

In addition, projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate is necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the sections entitled “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements,” and elsewhere in this prospectus. These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

TECHNICAL AND THIRD PARTY INFORMATION

Except where otherwise stated, the disclosure herein relating to the properties underlying our royalty and other interests in the sections entitled “Prospectus Summary – Asset Overview ,” “Business” and “Annex B – Summaries of Material Royalty Properties” is based on information publicly disclosed by the owners and operators of such properties, including GoldMining Inc., referred to as “GoldMining,” our parent company and the parent company of the owners and operators of such properties. Specifically, as a royalty holder, we have limited, if any, access to properties included in our asset portfolio. Additionally, we may from time to time receive operating information from the owners and operators of the properties, which we are not permitted to disclose to the public. We are dependent on the operators of the properties and their qualified persons to provide information to us or on publicly available information to prepare disclosure pertaining to properties and operations on the properties on which we hold interests and generally will have limited or no ability to independently verify such information. Although we do not have any knowledge that such information may not be accurate, there can be no assurance that such third-party information is complete or accurate.

We currently consider our royalty interests in the: (a) Whistler Project, located in Alaska, USA; (b) Yellowknife Project, located in the Northwest Territories, Canada; (c) Titiribi Project, located in the department of Antioquia, Colombia; (d) La Mina Project, located in the department of Antioquia, Colombia; and (e) São Jorge Project, located in the state of Para, Brazil to be our only material properties for the purposes of National Instrument 43-101—Standards of Disclosure for Mineral Projects, referred to as “NI 43-101.” We will continue to assess the materiality of our assets, including as new assets are acquired or as existing assets are further explored and developed.

| ii |

Information contained herein with respect to each of such projects has been prepared in accordance with the exemption set forth in section 9.2 of NI 43-101. Accordingly, unless otherwise noted, the disclosure contained herein of a scientific or technical nature for the: (a) Whistler Project, is based upon the technical report titled “NI 43-101 Resource Estimate for the Whistler Project” dated effective May 24, 2016 (re-stated May 30, 2016), prepared for GoldMining and filed under its profile on the Canadian System for Electronic Document Analysis and Retrieval, or “SEDAR,” at www.sedar.com, referred to as the “Whistler Technical Report”; (b) Yellowknife Project, is based upon the technical report titled “Independent Technical Report for the Yellowknife Gold Project, Northwest Territories, Canada” dated effective March 1, 2019, prepared for GoldMining and filed under its profile on SEDAR, referred to as the “Yellowknife Technical Report”; (c) Titiribi Project, is based upon the technical report titled “Technical Report on the Titiribi Project Department of Antioquia, Colombia” dated effective October 28, 2016, prepared for GoldMining and filed under its profile on SEDAR, referred to as the “Titiribi Technical Report”; (d) La Mina Project, is based upon the technical report titled “NI 43-101 Technical Report, Bellhaven Copper & Gold Inc., La Mina Project, Antioquia, Republic of Colombia” dated effective October 24, 2016, prepared for Bellhaven Copper & Gold Inc., which was acquired by, and is now a wholly-owned subsidiary of, GoldMining, and filed under its profile on SEDAR, referred to as the “La Mina Technical Report”; and (e) São Jorge Project, is based upon the technical report titled “São Jorge Gold Project, Para State, Brazil: Independent Technical Report on Mineral Resources” dated effective November 22, 2013, prepared for GoldMining and filed under its profile on SEDAR, referred to as the “São Jorge Technical Report.”

The technical and scientific information contained herein relating to our royalties and other interests has been reviewed and approved by Paulo Pereira, the President of our parent company, GoldMining, a qualified person as such term is defined under NI 43-101 and a member of the Association of Professional Geoscientists of Ontario.

For the meanings of certain technical terms used in this prospectus, see Annex A of this prospectus.

CAUTIONARY NOTE TO U.S. INVESTORS REGARDING MINERAL RESOURCE AND MINERAL RESERVE ESTIMATES

The disclosure of Mineral Resources in this prospectus has been prepared in accordance with the requirements of securities laws in effect in Canada, which differ from the requirements of United States securities laws. In Canada, an issuer is required to provide technical information with respect to mineralization, including Mineral Resources, if any, on its mineral exploration properties in accordance with Canadian requirements, which differ significantly from the requirements of the United States Securities and Exchange Commission, referred to as the “SEC,” pursuant to SEC Industry Guide 7 applicable to registration statements and reports filed by United States companies pursuant to the Securities Act or Securities Exchange Act of 1934, as amended, referred to as the “Exchange Act.” As such, information contained in this prospectus concerning descriptions of mineralization under Canadian standards may not be comparable to similar information made public by United States companies subject to the reporting and disclosure requirements of the SEC pursuant to Industry Guide 7.

Mineral Resource estimates included in this prospectus have been prepared in accordance with NI 43-101 and the CIM Definition Standards, as required by Canadian securities regulatory authorities. In particular, this prospectus, includes the terms “Measured Mineral Resource,” “Indicated Mineral Resource” and “Inferred Mineral Resource.” While these terms are recognized and required by Canadian regulations (under NI 43-101), SEC Industry Guide 7 does not recognize them. In addition, this prospectus may include disclosure of “contained ounces” of mineralization. Although such disclosure is permitted under Canadian regulations, SEC Industry Guide 7 only permits issuers to report mineralization as in place tonnage and grade without reference to unit measures.

United States investors are cautioned not to assume that any part or all of the mineral deposits identified as a “Measured Mineral Resource,” “Indicated Mineral Resource” or “Inferred Mineral Resource” will ever be converted to reserves as defined in NI 43-101 or SEC Industry Guide 7. “Inferred Mineral Resources” have a lower level of confidence than an “Indicated Mineral Resource” and must not be converted to a mineral “reserve.” The quantity and grade of reported “Inferred Mineral Resources” in this estimation are uncertain in nature and there has been insufficient exploration to define these “Inferred Mineral Resources” as an “Indicated Mineral Resource” or “Measured Mineral Resource” and it is uncertain if further exploration will result in upgrading them as such. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases.

Accordingly, information contained in this prospectus and the exhibits filed herewith contain descriptions of our mineral deposits that may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under U.S. federal securities laws and the rules and regulations promulgated thereunder.

| iii |

The following summary highlights certain information in this prospectus and should be read together with the more detailed information and financial data and statements contained elsewhere in this prospectus. This summary does not contain all of the information that may be important to you. You should read and carefully consider the following summary together with the entire prospectus, especially the “Risk Factors” section of this prospectus and our financial statements and the notes thereto appearing elsewhere in this prospectus before deciding to invest in our units. For more information on our business, refer to the “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operation” sections of this prospectus. Some of the statements in this prospectus constitute forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in such forward-looking statements as a result of certain factors, including those discussed in the “Risk Factors” and other sections of this prospectus. See “Cautionary Note Regarding Forward-Looking Statements.”

Overview

We are a precious metals-focused royalty and streaming company offering creative financing solutions to the metals and mining industry. Our mission is to acquire royalties, streams and similar interests at varying stages of the mine life cycle to build a balanced portfolio offering near, medium and longer-term attractive returns for our investors.

Our diversified portfolio currently consists of net smelter return, referred to as “NSR,” royalties ranging from 0.5% to 2.0% on 18 gold properties covering 12 projects located in the Americas, of which 17 properties are owned by subsidiaries of our parent, GoldMining. We have additional rights to acquire nine royalty interests from third parties holding royalties on certain of such properties. See “Business.”

We were incorporated under the Canada Business Corporations Act, or the “CBCA,” as a subsidiary of GoldMining on June 23, 2020. GoldMining is a Toronto Stock Exchange and NYSE American listed precious metals exploration and development company that was incorporated in 2009 and whose disclosed strategy is to expand its property portfolio through accretive transactions of resource stage gold projects and to advance its properties towards development.

Our office is located at 1030 West Georgia Street, Suite 1830, Vancouver, British Columbia V6E 2Y3 and our telephone number is +1 (604) 396-3066. Our website address is www.goldroyalty.com. The information contained on, or that can be accessed through, our website is not a part of this prospectus.

Our Strategy

Our strategy is to build a diversified asset base, with a focus on gold and other precious metals, by being a preferred partner to operating companies in the global mining industry. In doing so, our goal is to grow our net asset value per share and to generate value for all of our stakeholders over time. Our current long-term strategy is to build upon our significant existing resource base, which we believe offers substantial growth potential through future development of the underlying properties.

We plan to focus on acquiring royalties, streams and similar interests on mines and projects at varying stages of the mine life cycle to build a balanced portfolio offering near, medium, and longer-term growth in underlying net asset value per share. We intend to diversify our existing portfolio by adding additional assets across a range of precious metals mines and projects in the Americas and other jurisdictions around the world as opportunities arise.

Our management team, board of directors and advisory board have in excess of 250 years of combined mining sector experience, including exploration, development, operating and capital markets experience. We intend to capitalize on our significant collective knowledge, experience, and contacts to add value to the owners and operators of existing and prospective mines we partner with.

We believe our core team has the experience and capability to provide creative solutions to prospective partners thereby enhancing our ability to acquire attractive growth assets, whether in competitive auction processes or as a result of bilateral discussions.

| 1 |

As part of our strategy, we expect to utilize a cost-efficient business model by operating with a small, but highly experienced team and calling upon third-party resources to supplement our skill set as opportunities may arise. This strategy should enable us to maintain a high degree of flexibility in our cost structure. We believe it will also help to ensure that our business model is scalable and should allow us to seek new growth opportunities in a cost effective and value enhancing manner.

Royalties and Streams Generally

A royalty is a payment to a royalty holder that is typically based on a percentage of the minerals produced or the revenues or profits generated from the underlying project. With a stream, the holder makes an upfront payment or deposit to purchase a pre-agreed percentage of a mine’s production at a defined or pre-determined price. Royalties and streams are typically for the life of a mine, but streams can also be structured over a specified period or production interval. Royalties and streams are non-operating interests in the underlying project and therefore, the holder is generally not responsible for contributing additional funds for any purpose, including capital and operating costs.

Royalties and streams limit the holder’s exposure, in most instances, to exploration, development, operating, sustaining or reclamation expenditures typically associated with an operating interest in a mine. While they have limited operating exposure, royalty and stream holders do however benefit from any resource expansion or upside generated by exploration success, mine life extensions and operational expansions within the areas covered by the interest. A royalty and streaming business model provides greater diversification than typical mining companies. Royalty and streaming companies typically hold a portfolio of diversified assets, whereas mining companies generally depend on one or few key mines. Royalty and streaming companies therefore generally offer a relatively lower risk investment when compared to operating companies, while still offering potential upside to resource expansion and underlying commodity prices. We do not currently hold any stream interests but may acquire them in the future.

Asset Overview

The following is a summary of our royalties and other interests as of the date hereof:

| Type of Interest | Description |

| Royalties | We hold the following royalty interests: |

| ● | a 1.0% NSR on the Whistler Project, located in Alaska, USA, including each of the Whistler, Raintree West and Island Mountain properties; | |

| ● | a 1.0% NSR on the Yellowknife Project, located in the Northwest Territories, Canada, including each of the Nicholas Lake, Ormsby-Bruce, Goodwin Lake, Clan Lake and Big Sky properties; | |

| ● | a 2.0% NSR on the Titiribi Project, located Colombia; | |

| ● | a 2.0% NSR on the La Mina Project, located in Colombia; | |

| ● | a 1.0% NSR on the São Jorge Project, located in Brazil; | |

| ● | a 1.0% NSR on the Batistão Project, located in Brazil; | |

| ● | a 0.5% NSR on the Almaden Project, located in Idaho, USA; | |

| ● | a 1.0% NSR on the Cachoeira Project, located in Brazil; | |

| ● | a 1.0% NSR on the Crucero Project, located in Peru; | |

| ● | a 1.0% NSR on the Surubim Project, located in Brazil, including the Surubim and Rio Novo areas; | |

| ● | a 1.0% NSR on the Yarumalito Project, located in Colombia; and | |

| ● | a 1.0% NSR on a portion of the Quartz Mountain Project, located in Oregon, USA. |

See “Business – Property, Plants and Equipment – Royalty Interests.”

| 2 |

| Type of Interest | Description |

| Buyback Rights | We hold the rights to acquire additional royalties pursuant to buyback rights under existing royalty agreements between subsidiaries of GoldMining and third parties: |

| ● | a 2.0% NSR on the Batistão Project for $1,000,000; | |

| ● | a 0.5% NSR on the Surubim area of the Surubim Project for $1,000,000, which royalty is payable after production at the project has exceeded two million ounces; | |

| ● | a 1.5% NSR on the Surubim area of the Surubim Project for $1,000,000; | |

| ● | a 0.65% NSR on the Rio Novo area of the Surubim Project for $1,500,000; | |

| ● | a 0.75% NSR on the Whistler Project (including an area of interest) for $5,000,000; | |

| ● | a 1.0% NSR on the Yarumalito Project for C$1,000,000; | |

| ● | a 1.0% NSR on the Goodwin Lake property at the Yellowknife Project for C$1,000,000; | |

| ● | a 1.0% NSR on certain portions of the Big Sky property at the Yellowknife Project for C$500,000; and | |

| ● | a 0.25% NSR on the Narrow Lake property at the Yellowknife Project for C$250,000, in cash or common shares of GoldMining at any time until the fifth anniversary of commercial production. |

See “Business – Property, Plants and Equipment – Buyback Rights.”

The properties underlying our royalty interests are at the Exploration and Development stage and none are currently in production or host Mineral Reserves as of the date hereof. A project is considered to be in the “Exploration” stage when there is no current or historic Mineral Resource or Mineral Reserve defined for the project and is considered to be in the “Development” stage when the project has a current or historic Mineral Resource or Mineral Reserve defined for the project, but there is no current Preliminary Economic Assessment, Pre-Feasibility Study or Feasibility Study completed by the operator thereof to support the potential economic viability of such resource or reserve.

| 3 |

The following map sets forth the location of each of our royalty interests:

| 4 |

The following table sets forth summary information regarding each of our royalty interests, including existing Mineral Resource estimates for each deposit underlying such interests:

| Area | Gold Equivalent Ounces(1) | Attributable Gold Equivalent Ounces(1)(2) | ||||||||||||||||

| Project (Property) | Country | (ha) | Measured & Indicated | Inferred | Royalty Interest | Metal | Property Stage | Measured & Indicated | Inferred | |||||||||

| Whistler Project | USA | 17,159 | 1% NSR | Gold, Silver, Copper | ||||||||||||||

| Whistler | 2,250,000 | 3,350,000 | Development | 22,500 | 33,500 | |||||||||||||

| Raintree West | - | 1,991,000 | Development | - | 19,910 | |||||||||||||

| Island Mountain | 547,000 | 1,390,000 | Development | 5,470 | 13,900 | |||||||||||||

| Yellowknife | Canada | 12,239 | 1% NSR | Gold | ||||||||||||||

| Nicholas Lake | 138,000 | 154,000 | Development | 1,380 | 1,540 | |||||||||||||

| Ormsby-Bruce | 921,000 | 353,000 | Development | 9,210 | 3,530 | |||||||||||||

| Goodwin Lake | - | 33,000 | Development | - | 330 | |||||||||||||

| Clan Lake | - | 199,000 | Development | - | 1,990 | |||||||||||||

| Big Sky | - | - | Exploration | - | - | |||||||||||||

| Titiribi | Colombia | 3,919 | 6,220,000 | 3,440,000 | 2% NSR | Gold, Copper | Development | 124,400 | 68,800 | |||||||||

| La Mina | Colombia | 3,208 | 1,013,185 | 427,408 | 2% NSR | Gold, Silver, Copper | Development | 20,264 | 8,548 | |||||||||

| São Jorge | Brazil | 45,997 | 715,000 | 1,035,000 | 1% NSR | Gold | Development | 7,150 | 10,350 | |||||||||

| Almaden | USA | 1,895 | 910,000 | 160,000 | 0.5% NSR | Gold | Development | 4,550 | 800 | |||||||||

| Batistão | Brazil | 5,108 | - | - | 1% NSR | Gold | Exploration | |||||||||||

| Cachoeira | Brazil | 5,677 | 691,676 | 537,756 | 1% NSR | Gold | Development | 6,917 | 5,378 | |||||||||

| Crucero | Peru | 4,600 | 993,000 | 1,147,000 | 1% NSR | Gold | Development | 9,930 | 11,470 | |||||||||

| Surubim | Brazil | 14,611 | 1% NSR | Gold | ||||||||||||||

| Rio Novo | - | 503,000 | Development | - | 5,030 | |||||||||||||

| Surubim | - | - | Exploration | - | - | |||||||||||||

| Yarumalito | Colombia | 1,453 | - | 1,502,000 | 1% NSR | Gold, Copper | Development | - | 15,020 | |||||||||

| Quartz Mountain (3) | USA | 1,952 | 339,000 | 1,147,000 | 1% NSR | Gold | Development | 3,390 | 11,470 | |||||||||

| Total(4) | 117,818 | 14,738,861 | 17,369,164 | 215,161 | 211,566 | |||||||||||||

| 5 |

Notes:

| (1) | See “Business – Property, Plants and Equipment – Resource Estimates” for further information regarding the resource estimates included herein, including individual metal grades underlying gold equivalent resource calculations. | |

| (2) | Attributable Mineral Resources are calculated as gold equivalent ounces reported under Mineral Resource estimates reported by the operators in the applicable technical reports multiplied by the applicable rate under the royalty we hold. This figure is provided for illustrative purposes and is not intended to represent any actual ownership by us of the underlying Mineral Resource or minerals. | |

| (3) | Our royalty interest does not apply to the entirety of the project. However, we believe it applies to the areas under the existing Mineral Resource estimates for the project. | |

| (4) | The aggregated resource figure is provided for informational purposes only and are not intended to represent the viability of any project on a standalone or aggregated basis. The exploration and development of each project, project geology and the assumptions and other factors underlying each estimate, are not uniform and will vary from project to project. |

Our Business Model

Our business model is focused on managing and growing our portfolio of precious metals interests through the acquisition of additional royalties, streams and similar interests. We do not operate mines, develop projects or conduct exploration. We believe that the advantages of this business model include the following:

| ● | Lower volatility through diversification. By investing in precious metals interests across a spectrum of geographies, we reduce our dependency on any one asset, project or location. |

| ● | Exploration upside with less risk. We have limited direct financial exposure to exploration, development, operating and sustaining capital expenditures typically associated with mining projects, while generally maintaining exposure to potential upside attributable to mine life extensions, operational expansions and exploration success associated with the assets underlying our interests. As our interests are non-operational, we are not required to satisfy cash calls to maintain our interests in such projects. |

| ● | Focus and scalability. As our management team and directors are not encumbered with making and implementing operational decisions and tasks associated with mining projects, they are free to focus on executing our growth strategy. We expect that this will allow us to leverage our business model by establishing a larger and more diversified portfolio of precious metals interests than would be typical in an operating company. |

The table below provides a comparison of royalty companies, mining companies, exchange traded funds and funds that hold physical commodities:

| Royalty Companies | Operating Companies | Precious Metals ETFs | Physical Funds | |||||

| Exposure to Commodity Prices |  | | | | ||||

| Fixed Operating Costs | |  | | | ||||

| No Development or Sustaining Capital Costs | | | | | ||||

Exploration and Expansion Upside Without the Associated Costs | | | | | ||||

| Diversified Asset Portfolio | | | | | ||||

| Ability to Grow Without Increased Management | | | | |

| 6 |

Competitive Strengths

We believe that our competitive strengths include, among other things:

| ● | Significant Resource Base with Meaningful Attributable Ounces. We believe that our significant attributable resource base is a key competitive strength, as it provides us with the opportunity to experience success in the future, subject to the success of the properties underlying our royalty interests. |

| ● | Experienced Team with a Proven Track Record in Mining. Led by our Chairman and Chief Executive Officer, David Garofalo, our management team, board of directors and advisory board have over 250 years of combined experience in the mining sector, including key expertise in exploration, development and operational areas, along with important capital markets acumen and extensive networks. We believe this enhances our ability to execute on opportunities and makes us an attractive partner to potential royalty and stream counterparties where our collective knowledge and experience could add value to their business. In addition, we believe our team’s collective experience and network provide us with many of the capabilities of much larger companies, while allowing us to maintain a lean cost structure and a strong entrepreneurial culture. |

| ● | Lean but Scalable Operating Structure. Our lean operating profile allows us to operate with a low-cost structure, while maintaining the flexibility to rapidly assess and respond to new investment opportunities. We intend to leverage external expertise when appropriate, which should give us the ability to expand our technical and geographic footprint well outside of our internal resources and maintain a high level of confidence that a comprehensive range of opportunities are evaluated to meet our objectives and long-term strategy. |

| ● | Positioned to Execute on our Growth-Oriented Strategy. The net proceeds of the offering will provide us with total liquidity of $28.5 million, assuming the maximum amount under the offering is raised. This liquidity combined with our ability to issue shares as consideration for acquisitions, will allow us to pursue accretive acquisitions. Furthermore, we expect that our experienced management team and extensive relationships coupled with our strong technical skills and execution capabilities, will position us to source and pursue new growth opportunities across the asset spectrum. |

| ● | Diversified Royalty Portfolio and Growth Strategy. We hold royalties ranging from 0.5% to 2.0% on 18 pre-production gold properties covering 12 projects located in five countries across the Americas. This provides us a relatively geopolitically stable resource base with significant future upside potential. |

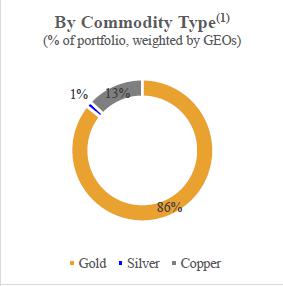

The following charts illustrate the composition of our existing portfolio by region and by metal type.

|  |

Note:

| 1. | Based on long term street consensus prices of $1,600/oz Au, $20.00/oz Ag, and $3.00/lb Cu. Please see “Business – Property, Plants and Equipment – Resource Estimates” for information regarding each Mineral Resource estimate and equivalent metal grades. |

| 7 |

Our Evaluation Process

Upon completion of the offering, we plan to aggressively pursue additional accretive royalty and stream transactions, targeting near-term production and complementary development and exploration projects worldwide. We believe we offer potential counterparties added value, by virtue of, among other things, our:

| ● | ability to provide non-dilutive project development financing; |

| ● | capital markets presence, which provides counterparties with expanded visibility; |

| ● | ability to leverage the experience of our team to offer market and development insights to the management and boards of counterparties; and |

| ● | due diligence and selection process, which provides a potential third-party endorsement to the projects underlying our precious metals interests. |

In evaluating potential transactions, we intend to utilize a disciplined approach to manage our fiscal profile. We expect to maintain low overhead costs by operating with a small but highly experienced team and calling upon third-party resources to supplement our skill set if required, thereby maintaining a high degree of flexibility in our cost structure. We believe this strategy will help to ensure that our business model is scalable and should allow us to seek new growth opportunities in a cost effective and value enhancing manner. We also seek to partner with operators who are committed to leading responsible mining, environmental, social and governance practices, including through their participation in transparent reporting initiatives.

We believe our core team has the experience and capability to provide creative solutions to prospective partners thereby enhancing our ability to acquire attractive growth assets, whether in a competitive auction process or as a result of bilateral discussions.

We believe that the extensive contacts within the mining industry of our collective management team, advisory board and board of directors give us enhanced access to a meaningful number of potential investment opportunities. These opportunities include identifying and acquiring existing royalties or streams from operating companies who deem these assets to be non-core to their operating philosophy or where there is potential for the operating company to highlight value for hidden assets. Furthermore, we engage with operating companies that are seeking to raise capital by selling a royalty or stream on one or more underlying asset.

Our focus is on seeking accretive precious metals assets that we believe will enhance our overall portfolio and increase our net asset value per share. Once a potential opportunity is identified, we seek to employ a disciplined approach to evaluating it and assessing whether such opportunity aligns with our strategic growth plans. As part of our evaluation process, we have, and intend to continue to, prioritize ensuring that appropriate due diligence is completed. We also rely on our own internal data and the extensive knowledge base and experience of our management team, advisory board and board of directors. Where we believe it is appropriate, we may engage the services of third-party experts to assist in our due diligence and evaluations process.

Acquisition opportunities are initially screened through a process involving an assessment of the technical merits and risks of the underlying asset, and a financial analysis that includes potential acquisition terms. If the initial screening indicates that further evaluation is warranted, then a more fulsome due diligence review is conducted. Such process may include, among other things, site visits and legal and technical due diligence. If a decision is made by management to proceed with a proposed acquisition, the transaction is then presented to our board of directors for final review and approval. Certain of the factors that our board of directors and management may evaluate in assessing proposed opportunities include the following:

| ● | project resources and/or reserves; | |

| ● | estimated life of mine including the potential for mine expansions and/or mine life extensions; | |

| ● | exploration potential and resource expansion; | |

| ● | identification and evaluation of relevant operational and technical risks; | |

| ● | historical and forecasted operational data; | |

| ● | project location, including jurisdiction-specific considerations such as mining regulations, history of mining related activities and permitting requirements; | |

| ● | environmental, social and governance considerations regarding the operator and the project; | |

| ● | project capital requirements; |

| 8 |

| ● | project stage and development timeline; | |

| ● | transaction structure considerations; | |

| ● | operational and financial track records of potential counterparties and their ability to develop and operate underlying precious metals projects; | |

| ● | tax planning and transaction tax considerations; and | |

| ● | ability to generate value enhancing returns. |

Recent Developments

The following are key developments in our business since our incorporation on June 23, 2020:

| ● | On November 27, 2020 we entered into a royalty purchase agreement, referred to as the “Royalty Purchase Agreement,” with our parent company, GoldMining, pursuant to which GoldMining caused its applicable subsidiaries to create and issue to us royalty interests and transfer to us certain buyback rights held by its subsidiaries in consideration for 15,000,000 of our common shares. See “Business – Property, Plants and Equipment” for further information regarding such royalty and other interests. |

| ● | On December 4, 2020, we completed a private placement, pursuant to which we issued 1,325,000 of our common shares at a subscription price of $2.15 per share for gross proceeds of $2,848,750. See “Business – Recent Developments.” | |

| ● | On February 3, 2021, we completed the acquisition of a 1.0% NSR on a portion of the Quartz Mountain Project, located in Oregon, USA in consideration for $150,000. See “Business – Property, Plants and Equipment”. |

Summary Risk Factors

Investing in our securities is speculative and involves substantial risk. You should carefully consider all of the information in this prospectus prior to investing in our securities. There are numerous risk factors related to our business that are described under “Risk Factors” and elsewhere in this prospectus. These risks could materially and adversely impact our business, results of operations, financial condition and future prospects, which could cause the trading price of our securities to decline and could result in a loss of your investment. Among these important risks are the following:

| ● | we own passive interests in mining properties, and it is difficult or impossible for us to ensure properties are developed or operated in our best interest; | |

| ● | none of our royalty and other interests are on producing properties and these and any future royalty, streaming or similar interests we acquire, particularly on development stage properties, are subject to the risk that they may never achieve production; | |

| ● | all of our existing royalties and other interests are on properties owned and operated by GoldMining; | |

| ● | we entered into the Royalty Purchase Agreement with our parent company, under which we acquired the substantial majority of our existing royalties, and we may in the future enter into additional transactions with related parties and such transactions present possible conflicts of interest; | |

| ● | we have limited or no access to data or the operations underlying our royalty and other interests; | |

| ● | we are subject to many of the risks faced by the owners and operators of our royalty and other interests; | |

| ● | we may enter into acquisitions or other material transactions at any time; | |

| ● | the volatility in gold and other commodity prices may have an adverse impact on the value of our royalty interests; | |

| ● | our future growth is to a large extent dependent on our acquisition strategy; |

| 9 |

| ● | estimates of Mineral Resources on the projects in which we have royalty interests are subject to significant revision; | |

| ● | impacts of COVID-19; | |

| ● | counterparty risks relating to our royalty interests; | |

| ● | federal, state and foreign legislation governing us or the operators of properties where we hold royalty interests; | |

| ● | risks associated with conducting business in foreign countries, including application of foreign laws to contract and other disputes, validity of security interests, governmental consents for granting interests in exploration and exploitation licenses, application and enforcement of real estate, mineral tenure, contract, safety, environmental and permitting laws, currency fluctuations, expropriation of property, repatriation of earnings, taxation, price controls, inflation, import and export regulations, community unrest and labor disputes, endemic health issues, corruption, enforcement and uncertain political and economic environments; | |

| ● | changes in laws governing us, the properties where we hold royalty interests or the operators of such properties; | |

| ● | changes in management and key employees; and | |

| ● | we will be a “passive foreign investment company” or “PFIC,” which could have material adverse federal income tax effects on United States shareholders. |

As a result of these risks and other risks described under “Risk Factors,” there is no guarantee that we will experience growth or profitability in the future.

Implications of Being an Emerging Growth Company, a Foreign Private Issuer and a Controlled Company

We qualify as an “emerging growth company” pursuant to the Jumpstart Our Business Startups Act, or the JOBS Act. An emerging growth company may take advantage of specified exemptions from various requirements that are otherwise applicable generally to public companies in the United States. These exceptions include:

| ● | an exemption to include in an initial public offering registration statement less than five years of selected financial data; | |

| ● | an exemption from the auditor attestation requirement in the assessment of the emerging growth company’s internal control over financial reporting; and | |

| ● | reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements and registration statements. |

The JOBS Act also permits an emerging growth company such as us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We have elected not to avail ourselves of the exemption that allows emerging growth companies to extend the transition period for complying with new or revised financial accounting standards. This election is irrevocable.

We will remain an emerging growth company until the earliest of:

| ● | the last day of our fiscal year during which we have total annual gross revenues of at least $1.07 billion; | |

| ● | the last day of our fiscal year following the fifth anniversary of the completion of this offering; | |

| ● | the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible debt securities; or | |

| ● | the date on which we are deemed to be a “large accelerated filer” under the Exchange Act, which would occur if the market value of our common shares that are held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter. |

| 10 |

We have availed ourselves in this prospectus of the reduced reporting requirements described above with respect to selected financial data. As a result, the information that we are providing to you may be less comprehensive than what you might receive from other public companies. When we are no longer deemed to be an emerging growth company, we will not be entitled to the exemptions provided in the JOBS Act discussed above.

Upon consummation of this offering, we will report under the Exchange Act as a non-U.S. company with foreign private issuer, or “FPI,” status. Even after we no longer qualify as an emerging growth company, as long as we qualify as an FPI under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| ● | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; | |

| ● | the sections of the Exchange Act requiring insiders to file public reports of their share ownership and trading activities and liability for insiders who profit from trades made in a short period of time; | |

| ● | the rules under the Exchange Act requiring the filing with the SEC of quarterly reports on Form 10-Q containing unaudited financial and other specified information, or current reports on Form 8-K, upon the occurrence of specified significant events; and | |

| ● | Regulation Fair Disclosure, or “Regulation FD,” which regulates selective disclosures of material information by issuers. |

Upon consummation of this offering, we will be a “controlled company” as defined in the NYSE American Company Guide because GoldMining beneficially owns 20,000,000 common shares, representing approximately 69% of our total voting power after completion of this offering. Pursuant to the NYSE American Company Guide, a “controlled company” may elect not to comply with certain corporate governance requirements. Currently, we do not plan to utilize the “controlled company” exemptions with respect to our corporate governance practices after we complete this offering.

Organizational Structure

The following chart sets forth our current corporate organization as of the date hereof and prior to completion of this offering.

Company Information

We were incorporated on June 23, 2020, under the CBCA. Our principal executive offices are located at 1030 West Georgia Street, Suite 1830, Vancouver, British Columbia V6E 2Y3 and our telephone number is +1 (604) 396-3066. Our website address is www.goldroyalty.com. The information contained on, or that can be accessed through, our website is not a part of this prospectus.

| 11 |

The Offering

| Securities offered by us | 6,000,0000 units, with each unit consisting of one (1) common share and one-half (1/2) warrant to purchase a common share. The units will not be certificated, and the common share and one-half (1/2) warrant comprising each unit are immediately separable and will be issued separately in this offering.

This prospectus also relates to the offering of common shares issuable upon the exercise of the warrants included in the units. |

| Warrants | Each whole warrant entitles the holder thereof to purchase one common share at a price of $7.50 per share. Only whole warrants are exercisable. The warrants are exercisable at any time for a period of three years from the date on which such warrants were issued. |

| Over-allotment option | We have granted the underwriters an option, exercisable within 30 days of the date of this prospectus, to purchase up to an additional 900,000 common shares and/or warrants to purchase up to 450,000 common shares to cover over-allotments, if any, in connection with this offering. |

| Common shares to be outstanding after this offering | 28,825,000 common shares (29,725,000 common shares if the over-allotment option is exercised in full). |

| Use of proceeds | We estimate that we will receive net proceeds from this offering of approximately $26.5 million, or approximately $30.6 million if the underwriters exercise their option to purchase additional common shares and/or warrants from us in full, based on an initial public offering price of $5.00 per unit, after deducting underwriting discounts and commissions and estimated offering expenses payable by us. We intend to use the net proceeds of this offering to implement our growth and acquisition strategy, and for other general working capital purposes. See “Use of Proceeds.” |

| Proposed NYSE American symbol | “GROY” (common shares); “GROY WS” (warrants) |

| Voting Rights | Holders of our common shares are entitled to one vote per share. See “Description of Share Capital.” |

| Dividend Policy | We have never paid or declared any dividends on our common shares or any of our other securities. We currently intend to retain any future earnings to finance the growth and development of our business, and we do not anticipate that we will declare or pay any cash dividends in the foreseeable future. See “Dividend Policy.” |

| Risk factors | See “Risk Factors” and the other information included in this prospectus for a discussion of factors you should consider carefully before investing in our securities. |

| Lock-ups | We and our directors, officers and principal shareholders of our common shares have agreed with the underwriters not to offer for sale, issue, sell, contract to sell, pledge or otherwise dispose of any of our common shares for a period of 180 days after the date of this prospectus. See “Underwriting” on page 111. |

The number of common shares to be outstanding after this offering is based on 22,825,000 common shares outstanding as of the date hereof and excludes:

| ● | 2,882,500 common shares reserved for future issuance under our share-based compensation plans based on the number of shares outstanding upon completion of the offering; and |

| ● | 3,000,0000 common shares issuable upon the exercise of the warrants to be issued in this offering at an exercise price of $7.50 per share. |

Unless otherwise indicated, all information in this prospectus reflects and assumes:

| ● | no exercise of the warrants issued in this offering; | |

| ● | no exercise by the underwriters of their option to purchase up to an additional 900,000 common shares and/or warrants to purchase up to 450,000 common shares from us to cover over-allotments, if any, in connection with this offering; and | |

| ● | no issuance or exercise of options after February 12, 2021. |

| 12 |

Summary Historical Financial Data

The following tables set forth a summary of our historical financial data at, and for the period ended on, the date indicated. We have derived the statement of loss and other comprehensive loss data for the period from June 23, 2020, being the date of our incorporation, to September 30, 2020 and the statement of financial position data as at September 30, 2020 from our audited financial statements included in this prospectus. The statement of loss and other comprehensive loss data for the three months ended December 31, 2020 and the statement of financial position data as at December 31, 2020 are derived from our condensed interim consolidated financial statements for the three months ended December 31, 2020 included in this prospectus. Our financial statements for the period from incorporation to September 30, 2020 have been prepared in accordance with IFRS and our interim financial statements for the three months ended December 31, 2020 have been prepared in accordance with IFRS as applicable to the preparation of interim financial statements including International Accounting Standard 34, Interim Financial Reporting. Our financial statements are presented in U.S. dollars except where otherwise indicated. We maintain our books and records in and have a functional currency of Canadian dollars. Our historical results for any prior period are not necessarily indicative of results to be expected in any future period. You should read this data together with our financial statements and related notes appearing elsewhere in this prospectus and the sections in this prospectus entitled “Capitalization,” “Selected Historical Financial Data,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Statement of Loss and Other Comprehensive Loss Data

Period from incorporation to September 30, 2020 | Three months ended December 31, 2020 | |||||||

| Expenses | ||||||||

| Depreciation | $ | 45 | 139 | |||||

| Management fees and salaries | 15,698 | 34,536 | ||||||

| General and administrative | 5,106 | 34,048 | ||||||

| Professional fees | 119,782 | 283,059 | ||||||

| Share-based compensation | - | 78,700 | ||||||

| Operating loss for the period | $ | (140,631 | ) | (430,482 | ) | |||

| Other items | ||||||||

| Foreign exchange loss | - | (69,321 | ) | |||||

| Net loss for the period | $ | (140,631 | ) | (499,803 | ) | |||

| Net loss per share, basic and diluted | $ | (140,631 | ) | (0.04 | ) | |||

Statement of Financial Position Data

As at September 30, 2020 | As at December 31, 2020 | |||||||

| Cash | $ | 37,539 | 2,509,704 | |||||

| Other receivables | $ | 241 | 14,189 | |||||

| Prepaids and other receivables | $ | 16,089 | 19,792 | |||||

| Current assets | $ | 53,869 | 2,543,685 | |||||

| Total assets | $ | 55,456 | 15,928,449 | |||||

| Total liabilities | $ | 196,382 | 182,979 | |||||

| Total shareholder’s equity (deficit) | $ | (140,926 | ) | 15,745,470 | ||||

| 13 |

Investing in our securities is speculative and involves a high degree of risk. You should consider carefully the following risk factors, as well as the other information in this prospectus, including our financial statements and notes thereto, before you decide to purchase our securities. If any of the following risks actually occur, our business, financial conditions, results of operations and prospects could be materially adversely affected, the value of our securities could decline, and you may lose all or part of your investment. This prospectus also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements as a result of a number of factors, including the risks described below. See “Cautionary Note Regarding Forward-Looking Statements.”

Risks Relating to our Business

We own passive interests in mining properties, and it is difficult or impossible for us to ensure properties are developed or operated in our best interest.

We are not and will not be directly involved in the exploration, development and production of minerals from, or the continued operation of, the mineral projects underlying the royalties, streams and similar interests that are or may be held by us. A substantial number of our royalty interests are owned and operated by subsidiaries of GoldMining. The exploration, development and operation of such properties is determined and carried out by third party owners and operators thereof and any revenue that may be derived from our asset portfolio will be based on any production by such owners and operators. Third party owners and operators will generally have the power to determine the manner in which the properties are exploited, including decisions regarding feasibility, exploration and development of such properties or decisions to commence, continue or reduce, or suspend or discontinue production from a property.

The interests of third party owners and operators and our interests may not always be aligned. As an example, it will usually be in our interest to advance development and production on properties as rapidly as possible, in order to maximize near-term cash flow, while third party owners and operators may take a more cautious approach to development, as they are exposed to risk on the cost of exploration, development and operations. Likewise, it may be in the interest of owners and operators to invest in the development of, and emphasize production from, projects or areas of a project that are not subject to royalties, streams or similar interests that are or may be held by us.

Our inability to control or influence the exploration, development or operations for the properties in which we hold or may hold royalties, streams and similar interests may have a material adverse effect on our business, results of operations and financial condition. In addition, the owners or operators may take action contrary to our policies or objectives; be unable or unwilling to fulfill their obligations under their agreements with us; or experience financial, operational or other difficulties, including insolvency, which could limit the owner or operator’s ability to advance such properties or perform its obligations under arrangements with us.

We may not be entitled to any compensation if the properties in which we hold or may hold royalties, streams and similar interests discontinue exploration, development or operations on a temporary or permanent basis.

The owners or operators of the projects in which we hold interests may, from time to time, announce transactions, including the sale or transfer of the projects or of the operator itself, over which we have little or no control. If such transactions are completed, it may result in a new operator, which may or may not explore, develop or operate the project in a similar manner to the current operator, which may have a material adverse effect on our business, results of operations and financial condition. The effect of any such transaction on us may be difficult or impossible to predict.

None of our royalty and other interests are on producing properties and these and any future royalty, streaming or similar interests we acquire, particularly on development stage properties, are subject to the risk that they may never achieve production.

None of the properties underlying our royalty and other interests are in production nor do they have established Mineral Reserves. These and any future royalty, streaming or similar interests we acquire may not achieve production or produce any revenues. While the discovery of gold deposits may result in substantial rewards, few properties that are explored are ultimately developed into producing mines. Major expenditures may be required to locate and establish Mineral Reserves, to develop metallurgical processes and to construct mining and processing facilities at a particular site. It is impossible to ensure that exploration or development programs planned by the owners or operators of the properties underlying royalties, streams and similar interests that are or may be held by us will result in profitable commercial mining operations. Whether a mineral deposit will be commercially viable depends on a number of factors, including cash costs associated with extraction and processing; the particular attributes of the deposit, such as size, grade and proximity to infrastructure; mineral prices, which are highly cyclical; government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use and environmental protection; and political stability. The exact effect of these factors cannot be accurately predicted but the combination of these factors may result in one or more of the properties underlying our current or future interests not receiving an adequate return on invested capital. Accordingly, there can be no assurance the properties underlying our current or future interests will be brought into a state of commercial production.

| 14 |

The failure of any of the properties underlying our interests to achieve production on schedule or at all would have a material adverse effect on our asset carrying values or the other benefits we expect to realize from our royalties and other interests or the acquisition of royalty interests, and potentially our business, results of operations, cash flows and financial condition.

A substantial majority of our existing royalties and other interests are on properties owned and operated by subsidiaries of GoldMining.

A substantial majority of our existing royalties are on projects owned and operated by subsidiaries of our parent company, GoldMining. Accordingly, the advancement and development of the projects underlying our royalties and other interests are largely dependent on the exploration and development strategy of GoldMining and its ability to advance such projects. In the event that GoldMining determines not to, or otherwise fails to, progress any such projects, our ability to achieve future revenues and the value of our existing assets, will be materially adversely affected.

In addition, due to counterparty concentration of our existing portfolio, the development and viability of the underlying projects are dependent on the financial condition of GoldMining and its ability to obtain necessary financing to maintain in good standing and develop such projects. Any material adverse change in the business, operations and financial condition of GoldMining may adversely affect our business, results of operations and financial condition and the maintenance and advancement of the projects underlying our interests.

GoldMining is not obligated to enter into any additional royalty agreements with us following this offering. In addition, GoldMining is not limited in its ability to compete against us.

We entered into the Royalty Purchase Agreement with our parent company, under which we acquired the substantial majority of our existing royalties, and we may in the future enter into additional transactions with related parties and such transactions present possible conflicts of interest.

The Royalty Purchase Agreement and the acquisition of a substantial majority of our existing royalty and other interests were entered into with our parent company. See “Related Party Transactions.” Transactions entered into with our parent company or any other entity in which a related party has an interest may not align with the interests of our security holders. There can be no assurance that we may have been able to achieve more favorable terms, including as to value and other key terms, if such transaction had not been with a related party. Any discrepancy between market perception of value of our royalties and other interests and the consideration under the Royalty Purchase Agreement may have a material adverse effect on the market value of our securities.

We may in the future enter into additional transactions with entities in which our board of directors and other related parties hold ownership interests. We expect that material transactions with related parties after this offering, if any, will be reviewed and approved by our nominating and corporate governance committee or our audit committee, each of which will be comprised solely of independent directors upon the completion of this offering. Nevertheless, there can be no assurance that any such transactions will result in terms that are more favorable to us than if such transactions are not entered into with related parties. Furthermore, we may achieve more favorable terms if such transactions had not been entered into with related parties and, in such case, these transactions, individually or in the aggregate, may have an adverse effect on our business, financial position and results of operations.

We have limited or no access to data or the operations underlying our existing or future royalty and other interests.

We are not, and will not be, the owner or operator of any of the properties underlying our existing or future royalties, streams and similar interests and have no input in the exploration, development or operation of such properties. Consequently, we have limited or no access to related exploration, development or operational data or to the properties themselves. This could affect our ability to assess the value of such interest. This could also result in delays in cash flow from that anticipated by us, based on the stage of development of the properties underlying our existing or future royalties and similar interests. Our entitlement to payments in relation to such interests may be calculated by the royalty payors in a manner different from our projections and we may not have rights of audit with respect to such interests. In addition, some royalties, streams or similar interests may be subject to confidentiality arrangements that govern the disclosure of information with regard to such interests and, as a result, we may not be in a position to publicly disclose related non-public information. The limited access to data and disclosure regarding the exploration, development and production of minerals from, or the continued operation of, the properties in which we have an interest may restrict our ability to assess value, which may have a material adverse effect on our business, results of operations and financial condition. We attempt to mitigate this risk by building relationships with various owners, operators and counterparties, in order to encourage information sharing.

| 15 |

We are subject to many of the risks faced by the owners and operators of our existing or future royalty and other interests.

To the extent that they relate to the exploration, development and production of minerals from, or the continued operation of, the properties in which we hold or may hold royalties, streams or similar interests, we will be subject to the risk factors applicable to the owners and operators of such mines or projects.

Mineral exploration, development and production generally involves a high degree of risk. Such operations are subject to all of the hazards and risks normally encountered in the exploration, development and production of metals, including weather related events, unusual and unexpected geology formations, seismic activity, environmental hazards and the discharge of toxic chemicals, explosions and other conditions involved in the drilling, blasting and removal of material, any of which could result in damage to, or destruction of, mines and other producing facilities, damage to property, injury or loss of life, environmental damage, work stoppages, delays in exploration, development and production, increased production costs and possible legal liability. Any of these hazards and risks and other acts of God could shut down such activities temporarily or permanently. Mineral exploration, development and production is subject to hazards such as equipment failure or failure of retaining dams around tailings disposal areas, which may result in environmental pollution and consequent liability for the owners or operators thereof. The exploration for, and development, mining and processing of, mineral deposits involves significant risks that even a combination of careful evaluation, experience and knowledge may not eliminate.

We may enter into acquisitions or other material transactions at any time.

In the ordinary course of business, we engage in a continual review of opportunities to acquire royalties, streams or similar interests, to establish new royalties, streams or similar interests on operating mines, to create new royalties, streams or similar interests through financing mine development or exploration, or to acquire companies that hold royalty interests. We currently, and generally at any time, have acquisition opportunities in various stages of active review, including, for example, our engagement of consultants and advisors to analyze particular opportunities, analysis of technical, financial, legal and other confidential information, submission of indications of interest and term sheets, participation in preliminary discussions and negotiations and involvement as a bidder in competitive processes. We may consider obtaining debt commitments for acquisition financing. In the event that we choose to raise debt capital to finance any acquisition, our leverage may be increased. We also could issue common shares to fund acquisitions. Issuances of common shares could dilute existing shareholders and may reduce some or all of our per share financial measures.

Any such acquisition could be material to us. All transactions include risks associated with our ability to negotiate acceptable terms with counterparties. In addition, any such acquisition or other transaction may have other transaction-specific risks associated with it, including risks related to the completion of the transaction, the project, its operators, or the jurisdictions in which the project is located, and other risks discussed in this prospectus. There can be no assurance that any acquisitions completed will ultimately benefit us.

The volatility in gold and other commodity prices may have an adverse impact on the value of our royalty interests.

The value of our royalty interests and the potential future development of the projects underlying our interests are directly related to the market price of gold and other commodity prices. Market prices may fluctuate widely and are affected by numerous factors beyond our control or that of any mining company, including metal supply, industrial and jewelry fabrication, investment demand, central banking economic policy, expectations with respect to the rate of inflation, the relative strength of the dollar and other currencies, interest rates, gold purchases, sales and loans by central banks, forward sales by metal producers, global or regional political, trade, economic or banking conditions, and a number of other factors.

Volatility in gold prices is demonstrated by its annual high and low prices over the past decade as reported by the London Bullion Market Association:

| Gold | |||||||

| ($/ounce) | |||||||

| Calendar Year | High | Low | |||||

| 2012 - 2013 | $ | 1,792 | $ | 1,192 | |||

| 2014 - 2015 | $ | 1,385 | $ | 1,049 | |||

| 2016 - 2017 | $ | 1,366 | $ | 1,077 | |||

| 2018 - 2019 | $ | 1,355 | $ | 1,178 | |||

| 2019 - 2020 | $ | 1,536 | $ | 1,287 | |||

| 2020 - 2021 | $ | 2,067 | $ | 1,472 | |||

Declines in market prices could cause an operator to cease or slowdown exploration and development activities, reduce, suspend or terminate production from an operating project or construction work at a development project which would negatively impact our ability to obtain revenues from our interests in the future. A price decline may result in a material and adverse effect on our business, results of operations and financial condition.

| 16 |

Our future growth is to a large extent dependent on our acquisition strategy.