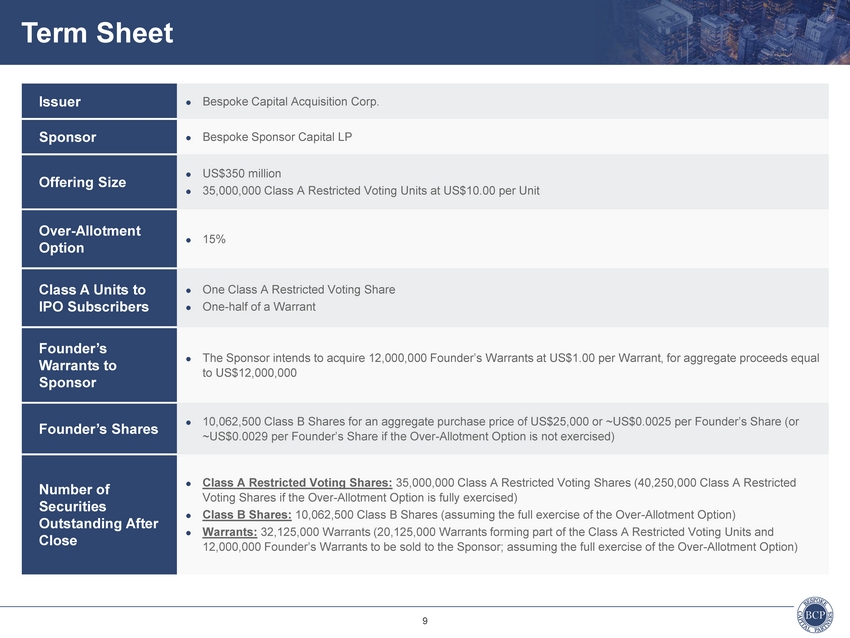

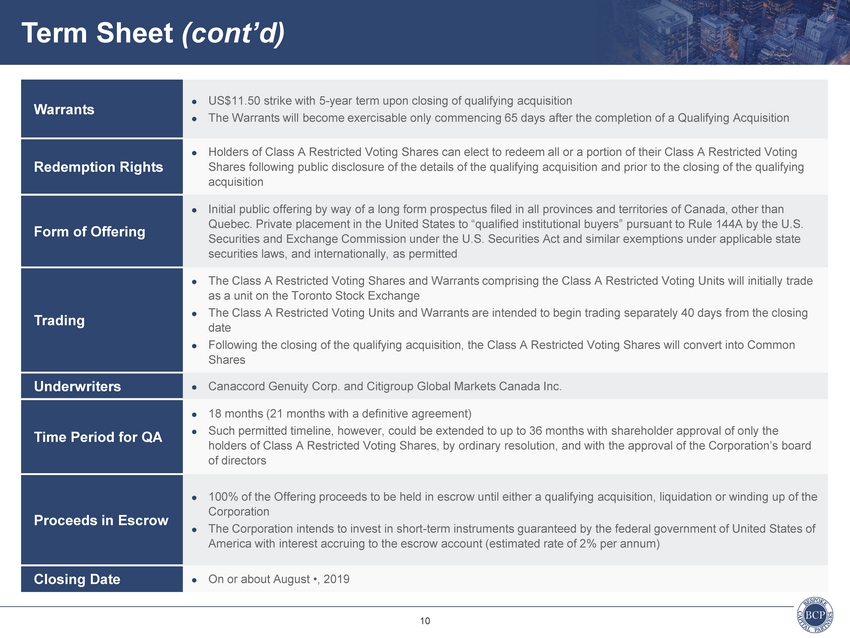

Exhibit 99.7

| Bespoke Capital Acquisition Corp. IPO Investor Presentation July 17, 2019 This document is for information purposes only and should not be considered a recommendation to purchase, sell or hold a security. This document does not constitute an offering memorandum or an offer or solicitation in any province or territory in Canada or other jurisdiction in which an offer or solicitation is not authorized. A copy of the preliminary prospectus dated July 17, 2019 containing important information relating to the securities described in this document has been filed with the securities regulatory authorities in each of the provinces and territories of Canada, except Québec. A copy of the preliminary prospectus, and any amendment, is required to be delivered with this document. The preliminary prospectus is still subject to completion. Copies of the preliminary prospectus may be obtained from ecm@cgf.com. There will not be any sale or any acceptance of an offer to buy the securities until a receipt for the final prospectus has been issued. No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. The preliminary prospectus constitutes a public offering of the securities only in those jurisdictions where they may be lawfully offered for sale and, in such jurisdictions, only by persons permitted to sell such securities. This document does not provide full disclosure of all material facts relating to the securities offered. Investors should read the preliminary prospectus, the final prospectus and any amendment for disclosure of those facts, especially risk factors relating to the securities offered, before making an investment decision. This presentation has been prepared in connection with an offering of Class A Restricted Voting Units (the “Securities”) of Bespoke Capital Acquisition Corp. (“Bespoke” or the “Corporation”). |

| Non-IFRS Financial Measures This presentation refers to certain financial measures, such as EBITDA and Total Enterprise Value, which are not measures recognized under IFRS and do not have a standardized meaning prescribed by IFRS. As a result, these measures may not be comparable to similar measures reported by other corporations. These measures are intended to provide additional information to the user and should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. “EBITDA” is defined as net income adjusted to exclude interest, income taxes, depreciation and amortization. “Total Enterprise Value” is defined as market capitalization plus total debt outstanding less cash on hand. Forward-Looking Statements Certain information in this presentation may constitute “forward-looking information” within the meaning of applicable securities legislation. Forward-looking information may relate to Bespoke’s future outlook and anticipated events or results and may include statements regarding the financial position, business strategy, growth strategy, budgets, operations, financial results, taxes, dividends, plans and objectives of Bespoke, as the case may be. Particularly, statements regarding future results, performance, achievements, prospects or opportunities of Bespoke are forward-looking statements. The forward-looking information in this presentation is based on certain assumptions, including, without limitation, the closing of Bespoke’s initial public offering, the receipt of all required regulatory approvals, and the expected timing related thereto, Bespoke’s future objectives and strategies to achieve those objectives, including the completion of a qualifying acquisition, as well as other statements with respect to management’s beliefs, plans, estimates and intentions, and similar statements concerning anticipated future events, results, circumstances, performance or expectations that are not historical facts. Generally, forward-looking information can be identified by use of words such as “outlook”, “objective”, “may”, “could”, “would”, “will”, “expect”, “intend”, “estimate”, “forecasts”, “project”, “seek”, “anticipate”, “believes”, “should”, “plans” or “continue”, and other similar terminology. Forward-looking statements are based on the opinions and estimates of management of Bespoke, as of the date such statements are made, and they are subject to known and unknown risks, uncertainties, assumptions and other factors that may cause the actual results, level of activity, performance or achievements of Bespoke to be materially different from those expressed or implied by such forward-looking statements. Although management of Bespoke believes the assumptions and analysis underlying such statements are reasonable as of the date hereof, you are cautioned not to place undue reliance on these statements. Although management the has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. The Sponsor does not undertake to update any forward-looking statements that are contained herein, except as required by applicable securities laws. See “Risk Factors” attached as Schedule “A” hereto for a description of the risk factors faced by Bespoke. Disclaimer Cautionary Note Regarding United States Securities Laws This presentation does not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the securities of Bespoke, in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such jurisdiction. The securities of Bespoke have not been and will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”), or any state securities laws and may not be offered or sold within the United States or to, or for the account or benefit of, “U.S. persons,” as such term is defined in Regulation S under the U.S. Securities Act, unless an exemption from such registration is available. Cautionary Note to Investors in the United Kingdom European laws, regulations and their enforcement, particularly those pertaining to anti-money laundering, relating to making and/or holding investments in cannabis-related practices or activities are in flux and vary dramatically from jurisdiction to jurisdiction. The enforcement of these laws – some of which carry criminal liability - and their effect on shareholders are uncertain and involve considerable risk. Accordingly, all potential investors located in the United Kingdom should take their own, independent legal advice based on their own circumstances prior to making any investment into the Corporation (whether directly or indirectly, or acting on an agency or principal basis). Risk Factor Risk Factors Relating to the Legality of Cannabis United Kingdom Anti-Money Laundering Laws and Regulation In the United Kingdom, in the event that we consummate a qualifying acquisition with a target business whose business, despite being in compliance with local laws, would not be, if operated in the U.K., in compliance with U.K. laws, the sale of their securities of the Corporation or the receipt of dividends therefrom following the consummation of the qualifying acquisition may be in violation of U.K. domestic anti-money laundering legislation. |

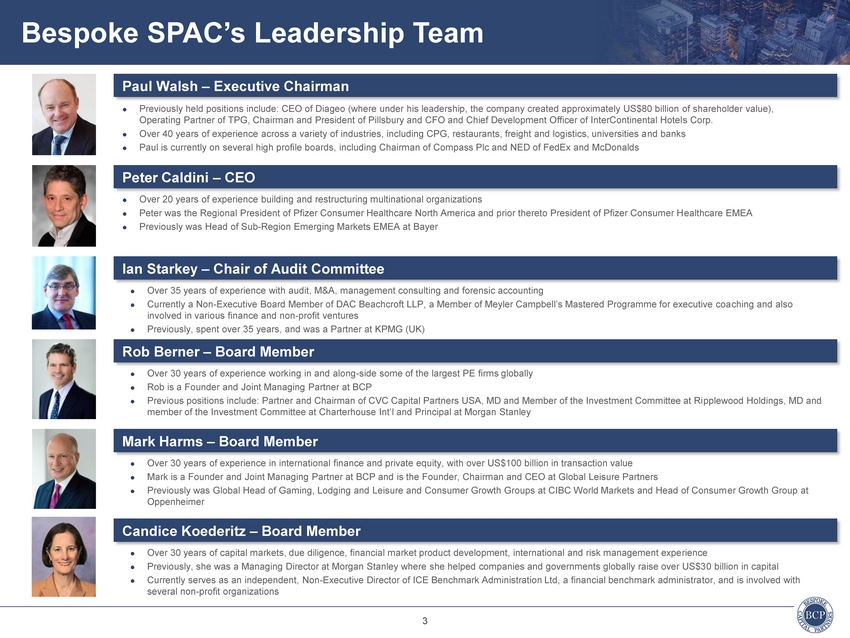

| Paul Walsh – Executive Chairman ⚫Previously held positions include: CEO of Diageo (where under his leadership, the company created approximately US$80 billion of shareholder value), Operating Partner of TPG, Chairman and President of Pillsbury and CFO and Chief Development Officer of InterContinental Hotels Corp. ⚫Over 40 years of experience across a variety of industries, including CPG, restaurants, freight and logistics, universities and banks ⚫Paul is currently on several high profile boards, including Chairman of Compass Plc and NED of FedEx and McDonalds Peter Caldini – CEO ⚫Over 20 years of experience building and restructuring multinational organizations ⚫Peter was the Regional President of Pfizer Consumer Healthcare North America and prior thereto President of Pfizer Consumer Healthcare EMEA ⚫Previously was Head of Sub-Region Emerging Markets EMEA at Bayer Ian Starkey – Chair of Audit Committee ⚫Over 35 years of experience with audit, M&A, management consulting and forensic accounting ⚫Currently a Non-Executive Board Member of DAC Beachcroft LLP, a Member of Meyler Campbell’s Mastered Programme for executive coaching and also involved in various finance and non-profit ventures ⚫Previously, spent over 35 years, and was a Partner at KPMG (UK) Rob Berner – Board Member ⚫Over 30 years of experience working in and along-side some of the largest PE firms globally ⚫Rob is a Founder and Joint Managing Partner at BCP ⚫Previous positions include: Partner and Chairman of CVC Capital Partners USA, MD and Member of the Investment Committee at Ripplewood Holdings, MD and member of the Investment Committee at Charterhouse Int’l and Principal at Morgan Stanley Mark Harms – Board Member ⚫Over 30 years of experience in international finance and private equity, with over US$100 billion in transaction value ⚫Mark is a Founder and Joint Managing Partner at BCP and is the Founder, Chairman and CEO at Global Leisure Partners ⚫Previously was Global Head of Gaming, Lodging and Leisure and Consumer Growth Groups at CIBC World Markets and Head of Consum er Growth Group at Oppenheimer Candice Koederitz – Board Member ⚫Over 30 years of capital markets, due diligence, financial market product development, international and risk management experience ⚫Previously, she was a Managing Director at Morgan Stanley where she helped companies and governments globally raise over US$30 billion in capital ⚫Currently serves as an independent, Non-Executive Director of ICE Benchmark Administration Ltd, a financial benchmark administrator, and is involved with several non-profit organizations |

| Paul Walsh – Executive Chairman ⚫ Previously held positions include: CEO of Diageo (where under his leadership, the company created approximately US$80 billion of shareholder value), Operating Partner of TPG, Chairman and President of Pillsbury and CFO and Chief Development Officer of InterContinental Hotels Corp. ⚫ Over 40 years of experience across a variety of industries, including CPG, restaurants, freight and logistics, universities and banks ⚫ Paul is currently on several high profile boards, including Chairman of Compass Plc and NED of FedEx and McDonalds Diageo Shareholder Value Creation Under Paul Walsh’s Leadership US$108 bn Market cap plus buybacks and dividends during tenure Market Cap: US$29 bn Sept 1, 2000 May 7, 2013 |

| Founded by Entrepreneurs and Business Builders ⚫ Bespoke Capital Partners, LLC (“BCP”) was founded in 2014 by experienced private equity veterans Rob Berner and Mark Harms ⚫ Paul Walsh, former CEO of Diageo, is BCP’s lead Operating Partner ⚫ Since inception, BCP has invested in deals with a combined EV of over US$2.5bn ⚫ A tailored approach to investment structure to strongly align with partners and counterparties BCP Solutions ⚫ Flexibility in control or minority positions and type of investment ⚫ Large stable of accomplished operating partners Proprietary Deal Sourcing ⚫ Proven proprietary “off-market” deal sourcing capabilities from long term relationships ⚫ All BCP investments have been proprietary bilateral negotiations, away from auction processes ⚫ Tend to be partner of choice given reputation as a “good partner” and our structuring flexibility Portfolio Overview ⚫ Privately owned and operated fitness center chain operating 440 clubs across 13 U.S. states ⚫ Provider of over 3 billion closures annually to the global wine industry ⚫ Leading Asian fitness center with 65 clubs in Taiwan ⚫ European provider of gaming services, operating a portfolio of 115 casinos |

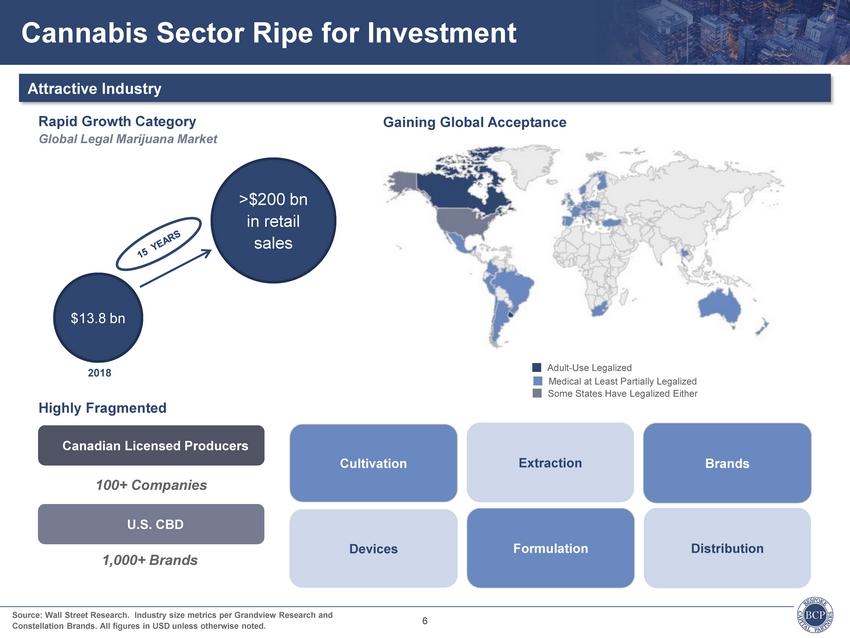

| Attractive Industry Rapid Growth Category Global Legal Marijuana Market $13.8 bn 2018 Highly Fragmented >$200 bn in retail sales Gaining Global Acceptance Adult-Use Legalized Medical at Least Partially Legalized Some States Have Legalized Either Canadian Licensed Producers 100+ Companies CultivationExtractionBrands U.S. CBD 1,000+ Brands DevicesFormulationDistribution |

| Highly Differentiated Structure Creates Strong Shareholder Alignment ⚫ Structure is intended to allow us to rapidly create an industry-leading, vertically-integrated operator with capital to accelerate growth plans ⚫ Target of US$400m+ in cash for growth, including capex, marketing and brand development Outstanding Corporate Management Team & Sponsor Group ⚫ Brings together a team of experienced investment professionals with deep capabilities and an extensive network ⚫ Paul Walsh, former CEO of Diageo, to provide best-in-class oversight and guidance as Executive Chairman ⚫ CEO, Peter Caldini, brings a strong consumer health background with extensive management experience at Pfizer, Bayer and Wyeth Excellent Operating Team ⚫ Aim to bring together founder-led businesses with expertise across the cannabis spectrum ⚫ Focused on teams that have a shared vision, underpinned by strong R&D and new product development Global Reach ⚫ Plan to become one of the only truly global legalized branded cannabis businesses, with established presence in Europe and North America, and the objective to enter other international markets in the near-term Full Value Chain Solution from “Land-to-Brand” ⚫ Vertical integration will allow for synergistic benefits and scale economies ⚫ Focus on a global brand strategy enabled by plant genetics, high quality low-cost cultivation and extraction Best-in-Class Practices ⚫ Highest regulatory and compliance standards; only doing business in federally legal frameworks ⚫ Combines large cap institutional and private equity disciplines and support frameworks |

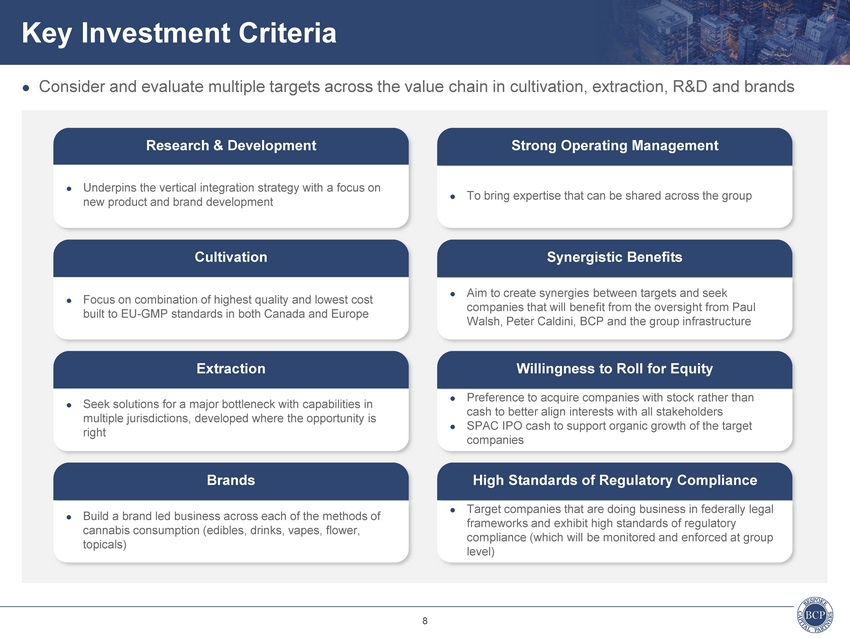

| ⚫ Consider and evaluate multiple targets across the value chain in cultivation, extraction, R&D and brands Research & Development Strong Operating Management ⚫ Underpins the vertical integration strategy with a focus on new product and brand development ⚫ To bring expertise that can be shared across the group Cultivation Synergistic Benefits ⚫ Focus on combination of highest quality and lowest cost built to EU-GMP standards in both Canada and Europe ⚫ Aim to create synergies between targets and seek companies that will benefit from the oversight from Paul Walsh, Peter Caldini, BCP and the group infrastructure Extraction ⚫ Seek solutions for a major bottleneck with capabilities in multiple jurisdictions, developed where the opportunity is right Willingness to Roll for Equity ⚫ Preference to acquire companies with stock rather than cash to better align interests with all stakeholders ⚫ SPAC IPO cash to support organic growth of the target companies Brands High Standards of Regulatory Compliance ⚫ Build a brand led business across each of the methods of cannabis consumption (edibles, drinks, vapes, flower, topicals) ⚫ Target companies that are doing business in federally legal frameworks and exhibit high standards of regulatory compliance (which will be monitored and enforced at group level) |

| [LOGO] |

| [LOGO] |

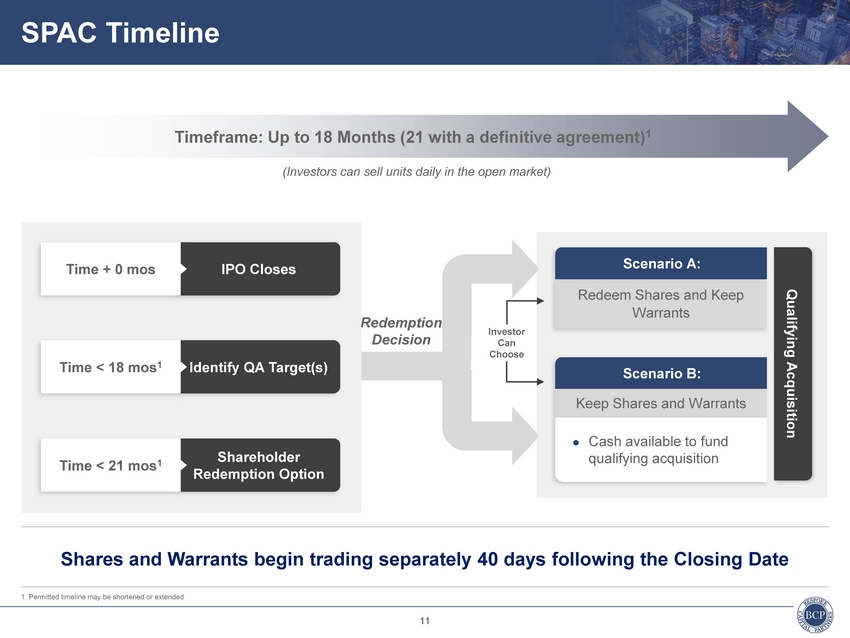

| Timeframe: Up to 18 Months (21 with a definitive agreement)1 (Investors can sell units daily in the open market) Time + 0 mos Time < 18 mos1 IPO Closes `Identify QA Target(s) Redemption Decision Investor Can Choose Scenario A: Qualifying Acquisition Warrants Scenario`B: Keep Shares and Warrants Time < 21 mos1 Shareholder Redemption Option ⚫ Cash available to fund qualifying acquisition Shares and Warrants begin trading separately 40 days following the Closing Date 1. Permitted timeline may be shortened or extended |

| In accordance with Section 13.7(4)(b) of National Instrument 41-101 - General Prospectus Requirements, all the information relating to comparables and any disclosure relating to the comparables, which is contained in the presentation to be provided to potential investors, has been removed from this template version for purposes of filing on the System for Electronic Document Analysis and Retrieval (SEDAR). |

| In accordance with Section 13.7(4)(b) of National Instrument 41-101 - General Prospectus Requirements, all the information relating to comparables and any disclosure relating to the comparables, which is contained in the presentation to be provided to potential investors, has been removed from this template version for purposes of filing on the System for Electronic Document Analysis and Retrieval (SEDAR). |

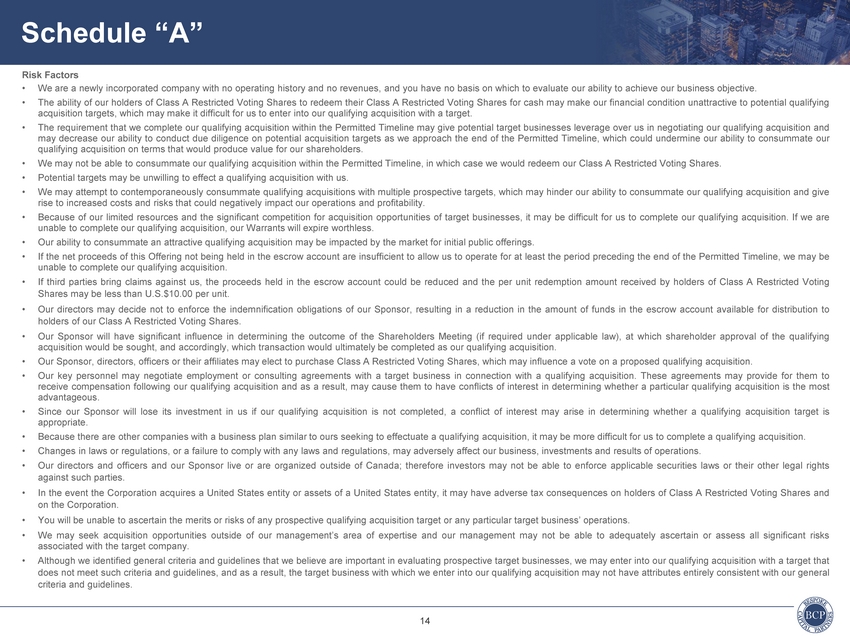

| Schedule “A” Risk Factors •We are a newly incorporated company with no operating history and no revenues, and you have no basis on which to evaluate our ability to achieve our business objective. •The ability of our holders of Class A Restricted Voting Shares to redeem their Class A Restricted Voting Shares for cash may make our financial condition unattractive to potential qualifying acquisition targets, which may make it difficult for us to enter into our qualifying acquisition with a target. •The requirement that we complete our qualifying acquisition within the Permitted Timeline may give potential target businesses leverage over us in negotiating our qualifying acquisition and may decrease our ability to conduct due diligence on potential acquisition targets as we approach the end of the Permitted Timeline, which could undermine our ability to consummate our qualifying acquisition on terms that would produce value for our shareholders. •We may not be able to consummate our qualifying acquisition within the Permitted Timeline, in which case we would redeem our Class A Restricted Voting Shares. •Potential targets may be unwilling to effect a qualifying acquisition with us. •We may attempt to contemporaneously consummate qualifying acquisitions with multiple prospective targets, which may hinder our ability to consummate our qualifying acquisition and give rise to increased costs and risks that could negatively impact our operations and profitability. •Because of our limited resources and the significant competition for acquisition opportunities of target businesses, it may be difficult for us to complete our qualifying acquisition. If we are unable to complete our qualifying acquisition, our Warrants will expire worthless. •Our ability to consummate an attractive qualifying acquisition may be impacted by the market for initial public offerings. •If the net proceeds of this Offering not being held in the escrow account are insufficient to allow us to operate for at least the period preceding the end of the Permitted Timeline, we may be unable to complete our qualifying acquisition. •If third parties bring claims against us, the proceeds held in the escrow account could be reduced and the per unit redemption amount received by holders of Class A Restricted Voting Shares may be less than U.S.$10.00 per unit. •Our directors may decide not to enforce the indemnification obligations of our Sponsor, resulting in a reduction in the amount of funds in the escrow account available for distribution to holders of our Class A Restricted Voting Shares. •Our Sponsor will have significant influence in determining the outcome of the Shareholders Meeting (if required under applicable law), at which shareholder approval of the qualifying acquisition would be sought, and accordingly, which transaction would ultimately be completed as our qualifying acquisition. •Our Sponsor, directors, officers or their affiliates may elect to purchase Class A Restricted Voting Shares, which may influence a vote on a proposed qualifying acquisition. •Our key personnel may negotiate employment or consulting agreements with a target business in connection with a qualifying acquisition. These agreements may provide for them to receive compensation following our qualifying acquisition and as a result, may cause them to have conflicts of interest in determining whether a particular qualifying acquisition is the most advantageous. •Since our Sponsor will lose its investment in us if our qualifying acquisition is not completed, a conflict of interest may arise in determining whether a qualifying acquisition target is appropriate. •Because there are other companies with a business plan similar to ours seeking to effectuate a qualifying acquisition, it may be more difficult for us to complete a qualifying acquisition. •Changes in laws or regulations, or a failure to comply with any laws and regulations, may adversely affect our business, investments and results of operations. •Our directors and officers and our Sponsor live or are organized outside of Canada; therefore investors may not be able to enforce applicable securities laws or their other legal rights against such parties. •In the event the Corporation acquires a United States entity or assets of a United States entity, it may have adverse tax consequences on holders of Class A Restricted Voting Shares and on the Corporation. •You will be unable to ascertain the merits or risks of any prospective qualifying acquisition target or any particular target business’ operations. •We may seek acquisition opportunities outside of our management’s area of expertise and our management may not be able to adequately ascertain or assess all significant risks associated with the target company. •Although we identified general criteria and guidelines that we believe are important in evaluating prospective target businesses, we may enter into our qualifying acquisition with a target that does not meet such criteria and guidelines, and as a result, the target business with which we enter into our qualifying acquisition may not have attributes entirely consistent with our general criteria and guidelines. |

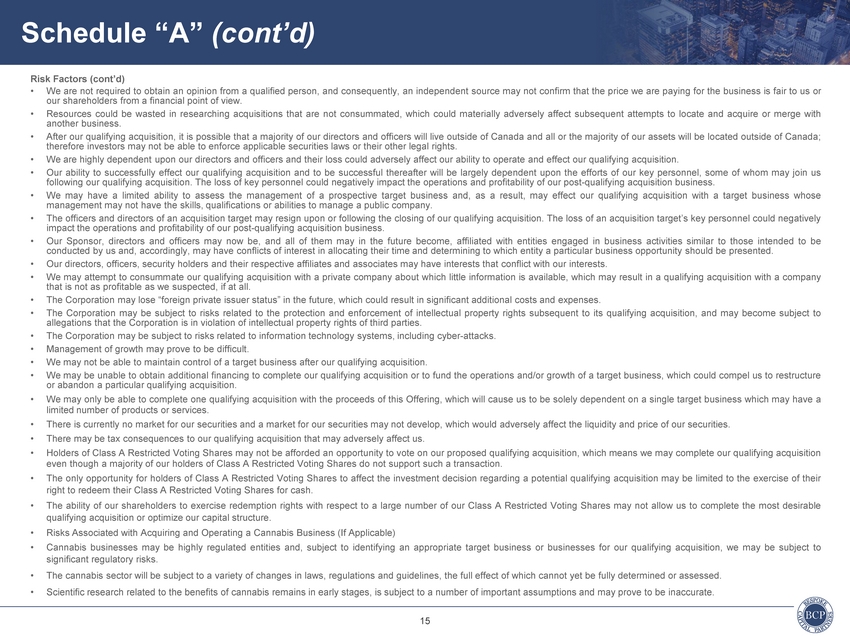

| Risk Factors (cont’d) •We are not required to obtain an opinion from a qualified person, and consequently, an independent source may not confirm that the price we are paying for the business is fair to us or our shareholders from a financial point of view. •Resources could be wasted in researching acquisitions that are not consummated, which could materially adversely affect subsequent attempts to locate and acquire or merge with another business. •After our qualifying acquisition, it is possible that a majority of our directors and officers will live outside of Canada and all or the majority of our assets will be located outside of Canada; therefore investors may not be able to enforce applicable securities laws or their other legal rights. •We are highly dependent upon our directors and officers and their loss could adversely affect our ability to operate and effect our qualifying acquisition. •Our ability to successfully effect our qualifying acquisition and to be successful thereafter will be largely dependent upon the efforts of our key personnel, some of whom may join us following our qualifying acquisition. The loss of key personnel could negatively impact the operations and profitability of our post-qualifying acquisition business. •We may have a limited ability to assess the management of a prospective target business and, as a result, may effect our qualifying acquisition with a target business whose management may not have the skills, qualifications or abilities to manage a public company. •The officers and directors of an acquisition target may resign upon or following the closing of our qualifying acquisition. The loss of an acquisition target’s key personnel could negatively impact the operations and profitability of our post-qualifying acquisition business. •Our Sponsor, directors and officers may now be, and all of them may in the future become, affiliated with entities engaged in business activities similar to those intended to be conducted by us and, accordingly, may have conflicts of interest in allocating their time and determining to which entity a particular business opportunity should be presented. •Our directors, officers, security holders and their respective affiliates and associates may have interests that conflict with our interests. •We may attempt to consummate our qualifying acquisition with a private company about which little information is available, which may result in a qualifying acquisition with a company that is not as profitable as we suspected, if at all. •The Corporation may lose “foreign private issuer status” in the future, which could result in significant additional costs and expenses. •The Corporation may be subject to risks related to the protection and enforcement of intellectual property rights subsequent to its qualifying acquisition, and may become subject to allegations that the Corporation is in violation of intellectual property rights of third parties. •The Corporation may be subject to risks related to information technology systems, including cyber-attacks. •Management of growth may prove to be difficult. •We may not be able to maintain control of a target business after our qualifying acquisition. •We may be unable to obtain additional financing to complete our qualifying acquisition or to fund the operations and/or growth of a target business, which could compel us to restructure or abandon a particular qualifying acquisition. •We may only be able to complete one qualifying acquisition with the proceeds of this Offering, which will cause us to be solely dependent on a single target business which may have a limited number of products or services. •There is currently no market for our securities and a market for our securities may not develop, which would adversely affect the liquidity and price of our securities. •There may be tax consequences to our qualifying acquisition that may adversely affect us. •Holders of Class A Restricted Voting Shares may not be afforded an opportunity to vote on our proposed qualifying acquisition, which means we may complete our qualifying acquisition even though a majority of our holders of Class A Restricted Voting Shares do not support such a transaction. •The only opportunity for holders of Class A Restricted Voting Shares to affect the investment decision regarding a potential qualifying acquisition may be limited to the exercise of their right to redeem their Class A Restricted Voting Shares for cash. •The ability of our shareholders to exercise redemption rights with respect to a large number of our Class A Restricted Voting Shares may not allow us to complete the most desirable qualifying acquisition or optimize our capital structure. •Risks Associated with Acquiring and Operating a Cannabis Business (If Applicable) •Cannabis businesses may be highly regulated entities and, subject to identifying an appropriate target business or businesses for our qualifying acquisition, we may be subject to significant regulatory risks. •The cannabis sector will be subject to a variety of changes in laws, regulations and guidelines, the full effect of which cannot yet be fully determined or assessed. •Scientific research related to the benefits of cannabis remains in early stages, is subject to a number of important assumptions and may prove to be inaccurate. |

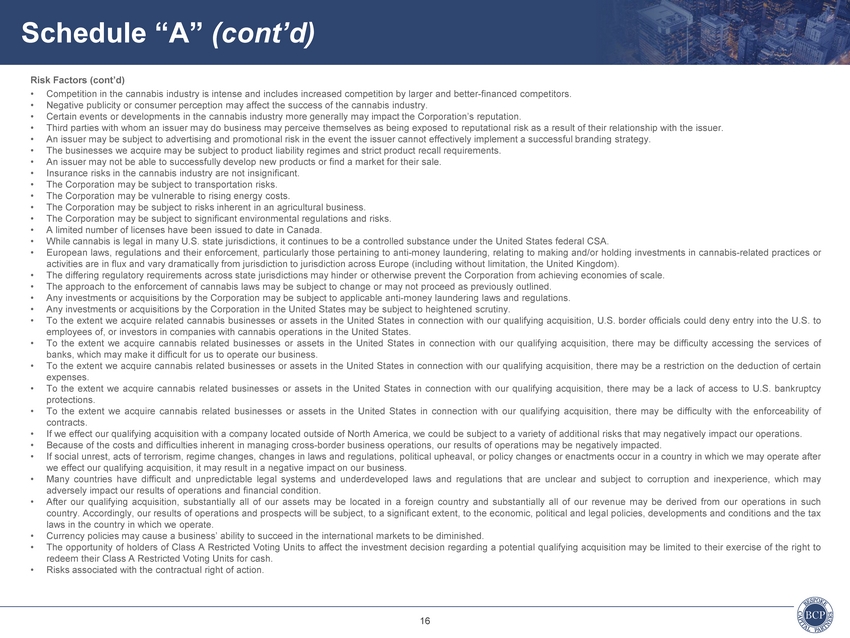

| Risk Factors (cont’d) •Competition in the cannabis industry is intense and includes increased competition by larger and better-financed competitors. •Negative publicity or consumer perception may affect the success of the cannabis industry. •Certain events or developments in the cannabis industry more generally may impact the Corporation’s reputation. •Third parties with whom an issuer may do business may perceive themselves as being exposed to reputational risk as a result of their relationship with the issuer. •An issuer may be subject to advertising and promotional risk in the event the issuer cannot effectively implement a successful branding strategy. •The businesses we acquire may be subject to product liability regimes and strict product recall requirements. •An issuer may not be able to successfully develop new products or find a market for their sale. •Insurance risks in the cannabis industry are not insignificant. •The Corporation may be subject to transportation risks. •The Corporation may be vulnerable to rising energy costs. •The Corporation may be subject to risks inherent in an agricultural business. •The Corporation may be subject to significant environmental regulations and risks. •A limited number of licenses have been issued to date in Canada. •While cannabis is legal in many U.S. state jurisdictions, it continues to be a controlled substance under the United States federal CSA. •European laws, regulations and their enforcement, particularly those pertaining to anti-money laundering, relating to making and/or holding investments in cannabis-related practices or activities are in flux and vary dramatically from jurisdiction to jurisdiction across Europe (including without limitation, the United Kingdom). •The differing regulatory requirements across state jurisdictions may hinder or otherwise prevent the Corporation from achieving economies of scale. •The approach to the enforcement of cannabis laws may be subject to change or may not proceed as previously outlined. •Any investments or acquisitions by the Corporation may be subject to applicable anti-money laundering laws and regulations. •Any investments or acquisitions by the Corporation in the United States may be subject to heightened scrutiny. •To the extent we acquire related cannabis businesses or assets in the United States in connection with our qualifying acquisition, U.S. border officials could deny entry into the U.S. to employees of, or investors in companies with cannabis operations in the United States. •To the extent we acquire cannabis related businesses or assets in the United States in connection with our qualifying acquisition, there may be difficulty accessing the services of banks, which may make it difficult for us to operate our business. •To the extent we acquire cannabis related businesses or assets in the United States in connection with our qualifying acquisition, there may be a restriction on the deduction of certain expenses. •To the extent we acquire cannabis related businesses or assets in the United States in connection with our qualifying acquisition, there may be a lack of access to U.S. bankruptcy protections. •To the extent we acquire cannabis related businesses or assets in the United States in connection with our qualifying acquisition, there may be difficulty with the enforceability of contracts. •If we effect our qualifying acquisition with a company located outside of North America, we could be subject to a variety of additional risks that may negatively impact our operations. •Because of the costs and difficulties inherent in managing cross-border business operations, our results of operations may be negatively impacted. •If social unrest, acts of terrorism, regime changes, changes in laws and regulations, political upheaval, or policy changes or enactments occur in a country in which we may operate after we effect our qualifying acquisition, it may result in a negative impact on our business. •Many countries have difficult and unpredictable legal systems and underdeveloped laws and regulations that are unclear and subject to corruption and inexperience, which may adversely impact our results of operations and financial condition. •After our qualifying acquisition, substantially all of our assets may be located in a foreign country and substantially all of our revenue may be derived from our operations in such country. Accordingly, our results of operations and prospects will be subject, to a significant extent, to the economic, political and legal policies, developments and conditions and the tax laws in the country in which we operate. •Currency policies may cause a business’ ability to succeed in the international markets to be diminished. •The opportunity of holders of Class A Restricted Voting Units to affect the investment decision regarding a potential qualifying acquisition may be limited to their exercise of the right to redeem their Class A Restricted Voting Units for cash. •Risks associated with the contractual right of action. |