Exhibit 99.1

Synovus®

BARCLAYS

Global Financial Services Conference

September 9, 2013

Forward-looking statements

This slide presentation and certain of our other filings with the Securities and Exchange Commission contain statements that constitute “forward-looking statements” within the meaning of, and subject to the protections of, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements other than statements of historical fact are forward-looking statements. You can identify these forward-looking statements through Synovus” use of words such as “believes,” “anticipates,” “expects,” “may,” “will,” “assumes,” “should,” “predicts,” “could,” “should,” “would,” “intends,” “targets,” “estimates,” “projects,” “plans,” “potential” and other similar words and expressions of the future or otherwise regarding the outlook for Synovus’ future business and financial performance and/or the performance of the commercial banking industry and economy in general. These forward-looking statements include, among others, (1) our expectations on credit trends and key credit metrics for the remainder of 2013; (2) expectations on future loan growth; (3) expectations on net interest margin; (4) expectations on mortgage banking and other fee income; (5) expectations regarding the impact of redemption of our obligations under TARP; (6) expectations regarding the impact of our ongoing efficiency initiatives and further cost savings; (7) expectations regarding future growth opportunities; and (8) the assumptions underlying our expectations. Prospective investors are cautioned that any such forward-looking statements are not guarantees of future performance and involve known and unknown risks and uncertainties which may cause the actual results, performance or achievements of Synovus to be materially different from the future results, performance or achievements expressed or implied by such forward-looking statements. Forward-looking statements are based on the information known to, and current beliefs and expectations of, Synovus’ management and are subject to significant risks and uncertainties. Actual results may differ materially from those contemplated by such forward-looking statements. A number of factors could cause actual results to differ materially from those contemplated by the forward-looking statements in this report. Many of these factors are beyond Synovus’ ability to control or predict.

These forward-looking statements are based upon information presently known to Synovus” management and are inherently subjective, uncertain and subject to change due to any number of risks and uncertainties, including, without limitation, the risks and other factors set forth in Synovus’ filings with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended December 31, 2012 under the captions “Cautionary Notice Regarding Forward-Looking Statements” and “Risk Factors” and in Synovus” quarterly reports on Form 10-Q and current reports on Form 8-K. We believe these forward-looking statements are reasonable; however, undue reliance should not be placed on any forward-looking statements, which are based on current expectations and speak only as of the date that they are made. We do not assume any obligation to update any forward-looking statements as a result of new information, future developments or otherwise, except as otherwise may be required by law.

2

Use of non-GAAP financial measures

This slide presentation contains certain non-GAAP financial measures determined by methods other than in accordance with generally accepted accounting principles. Such non-GAAP financial measures include the following: adjusted non-interest expense, core deposits, the Tier 1 common equity ratio; and the tangible common equity to tangible assets ratio. The most comparable GAAP measures to these measures are total non-interest expense, total deposits; and the ratio of total equity to total assets, respectively. Management uses these non-GAAP financial measures to assess the performance of Synovus’ core business and the strength of its capital position. Synovus believes that these non-GAAP financial measures provide meaningful additional information about Synovus to assist investors in evaluating Synovus’ operating results, financial strength and capitalization. The non-GAAP financial measures should be considered as additional views of the way our financial measures are affected by significant charges for credit costs and other factors. Adjusted non-interest expense is a measure utilized by management to measure the success of expense management initiatives focused on reducing recurring controllable operating costs. Core deposits is a measure used by management to evaluate organic growth of deposits and the quality of deposits as a funding source. The Tier 1 common equity ratio and the tangible common equity to tangible assets ratio are used by management to assess the strength of our capital position. These non-GAAP financial measures should not be considered as a substitute for operating results determined in accordance with GAAP and may not be comparable to other similarly titled measures of other companies. The computations of the non-GAAP financial measures used in this slide presentation are set forth in the appendix to this slide presentation.

3

The road from 2008

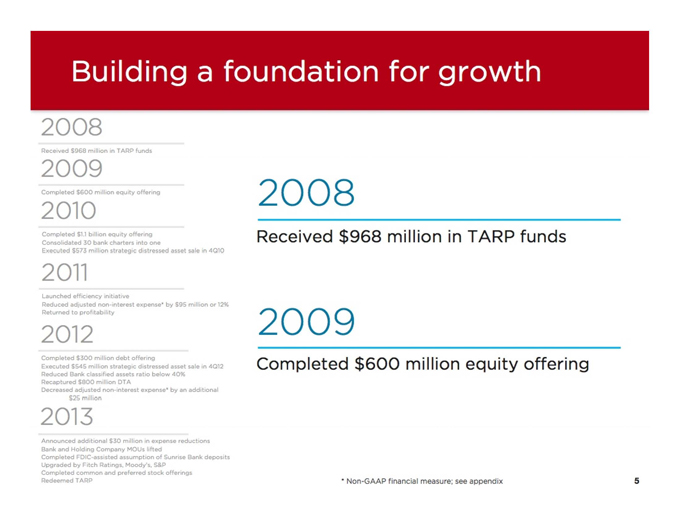

Building a foundation for growth

2008

Received $968 million in TARP funds

2009

Completed $600 million equity offering

2010

2008

Completed $1.1 billion equity offering Consolidated 30 bank charters into one

Received $968 million in TARP funds

Executed $573 million strategic distressed asset sale in 4Q10

2011

Launched efficiency initiative

Reduced adjusted non-interest expense* by $95 million or 12%

Returned to profitability

2012

2009

Completed $300 million debt offering

Executed $545 million strategic distressed asset sale in 4Q12

Reduced Bank classified assets ratio below 40%

Recaptured $800 million DTA

Decreased adjusted non-interest expense* by an additional $25 million

2013

Announced additional $30 million in expense reductions Bank and Holding Company MOUs lifted

Completed FDIC-assisted assumption of Sunrise Bank deposits

Upgraded by Fitch Ratings, Moody’s, S&P Completed common and preferred stock offerings Redeemed TARP

Completed $600 million equity offering

* Non-GAAP financial measure; see appendix

5

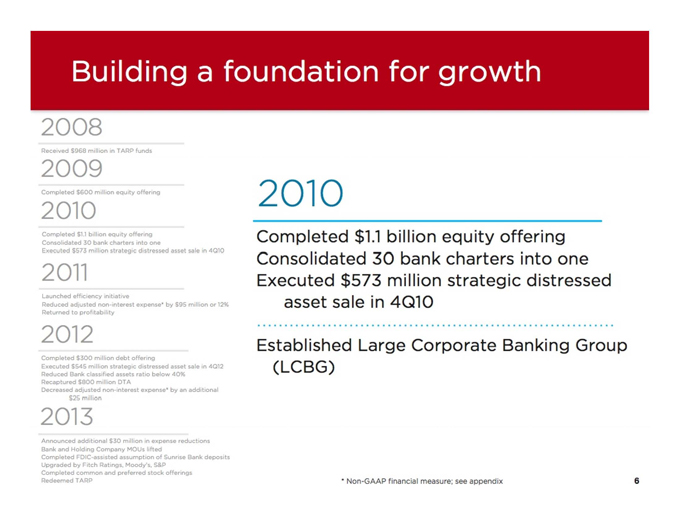

Building a foundation for growth

2008

Received $968 million in TARP funds

2009

Completed $600 million equity offering

2010

2010

Completed $1.1 billion equity offering Consolidated 30 bank charters into one

Executed $573 million strategic distressed asset sale in 4Q10

2011

Launched efficiency initiative

Reduced adjusted non-interest expense* by $95 million or 12% Returned to profitability

2012

Completed $300 million debt offering

Executed $545 million strategic distressed asset sale in 4Q12

Reduced Bank classified assets ratio below 40%

Recaptured $800 million DTA

Decreased adjusted non-interest expense* by an additional $25& million

Completed $1.1 billion equity offering Consolidated 30 bank charters into one Executed $573 million strategic distressed asset sale in 4Q10

Established Large Corporate Banking Group (LCBG)

2013

Announced additional $30 million in expense reductions Bank and Holding Company MOUs lifted

Completed FDIC-assisted assumption of Sunrise Bank deposits Upgraded by Fitch Ratings, Moody’s, S&P Completed common and preferred stock offerings Redeemed TARP

* Non-GAAP financial measure; see appendix

6

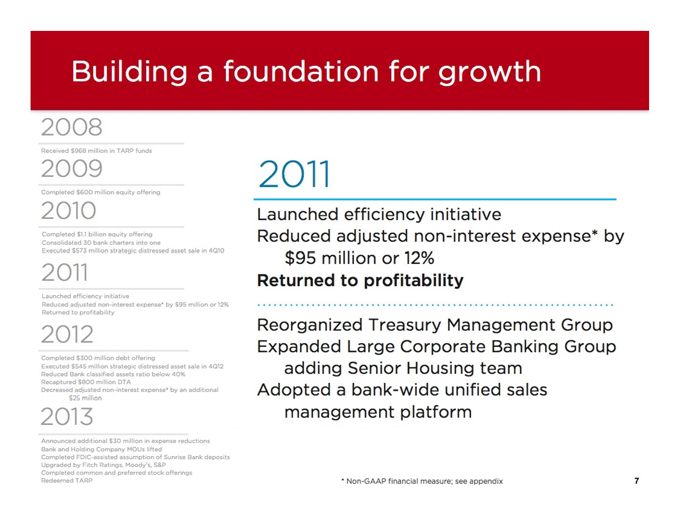

Building a foundation for growth

2008

Received $968 million in TARP funds.

2009

2011

Completed $600 million equity offering

2010

Completed $1.1 billion equity offering Consolidated 30 bank charters into one

Executed $573 million strategic distressed asset sale in 4Q10

2011

Launched efficiency initiative

Reduced adjusted non-interest expense* by $95 million or 12%

Returned to profitability

2012

Completed $300 million debt offering

Executed $545 million strategic distressed asset sale in 4Q12 Reduced Bank classified assets ratio below 40% Recaptured $800 million DTA

Decreased adjusted non-interest expense* by an additional S25 million

2013

Launched efficiency initiative

Reduced adjusted non-interest expense* by

$95 million or 12% Returned to profitability

Reorganized Treasury Management Group Expanded Large Corporate Banking Group

adding Senior Housing team Adopted a bank-wide unified sales

management platform

Announced additional $30 million in expense reductions Bank and Holding Company MOUs lifted

Completed FDIC-assisted assumption of Sunrise Bank deposits Upgraded by Fitch Ratings, Moody’s, S&P Completed common and preferred stock offerings Redeemed TARP

* Non-GAAP financial measure; see appendix

7

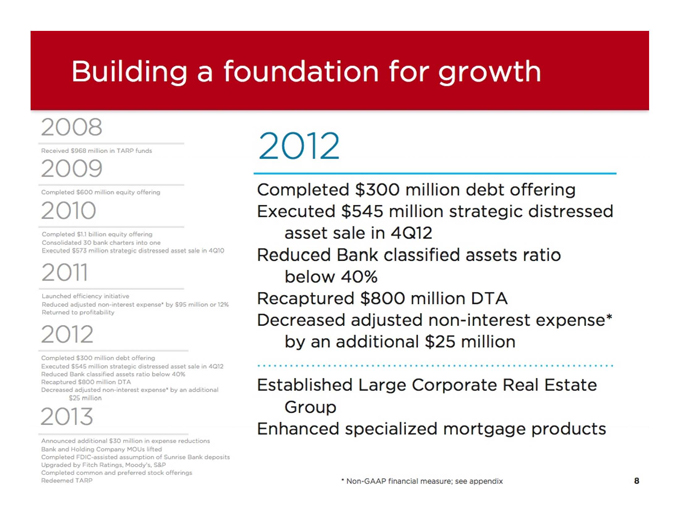

Building a foundation for growth

2008

Received $968 million in TARP funds.

2009

2012

Completed $600 million equity offering

2010

Completed $1.1 billion equity offering Consolidated 30 bank charters into one

Executed $573 million strategic distressed asset sale in 4Q10

2011

Launched efficiency initiative

Reduced adjusted non-interest expense* by $95 million or 12% Returned to profitability

2012

Completed $300 million debt offering

Executed $545 million strategic distressed asset sale in 4Q12 Reduced Bank classified assets ratio below 40% Recaptured $800 million DTA

Decreased adjusted non-interest expense* by an additional S25 million

2013

Completed $300 million debt offering Executed $545 million strategic distressed

asset sale in 4Q12 Reduced Bank classified assets ratio

below 40% Recaptured $800 million DTA Decreased adjusted non-interest expense*

by an additional $25 million

Established Large Corporate Real Estate Group

Enhanced specialized mortgage products

Announced additional $30 million in expense reductions Bank and Holding Company MOUs lifted

Completed FDIC-assisted assumption of Sunrise Bank deposits Upgraded by Fitch Ratings, Moody’s, S&P Completed common and preferred stock offerings Redeemed TARP

* Non-GAAP financial measure; see appendix

8

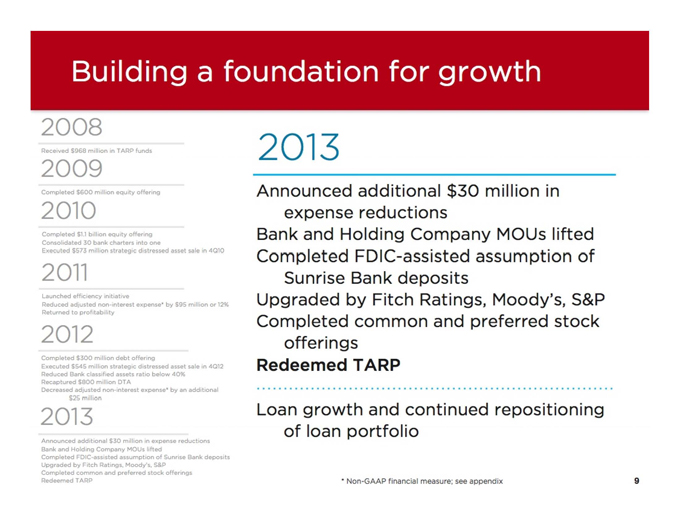

Building a foundation for growth

2008

Received $968 million in TARP funds

2009

2013

Completed $600 million equity offering

2010

Completed $1.1 billion equity offering Consolidated 30 bank charters into one

Executed $573 million strategic distressed asset sale in 4Q10

2011

Launched efficiency initiative

Reduced adjusted non-interest expense* by $95 million or 12% Returned to profitability

2012

Completed $300 million debt offering

Executed $545 million strategic distressed asset sale in 4Q12 Reduced Bank classified assets ratio below 40% Recaptured $800 million DTA

Decreased adjusted non-interest expense* by an additional $25 million

2013

Announced additional $30 million in expense reductions Bank and Holding Company MOUs lifted

Completed FDIC-assisted assumption of Sunrise Bank deposits Upgraded by Fitch Ratings, Moody’s, S&P Completed common and preferred stock offerings Redeemed TARP

Announced additional $30 million in

expense reductions Bank and Holding Company MOUs lifted Completed FDIC-assisted assumption of

Sunrise Bank deposits Upgraded by Fitch Ratings, Moody’s, S&P Completed common and preferred stock

offerings

Redeemed TARP

Loan growth and continued repositioning of loan portfolio

* Non-GAAP financial measure; see appendix

9

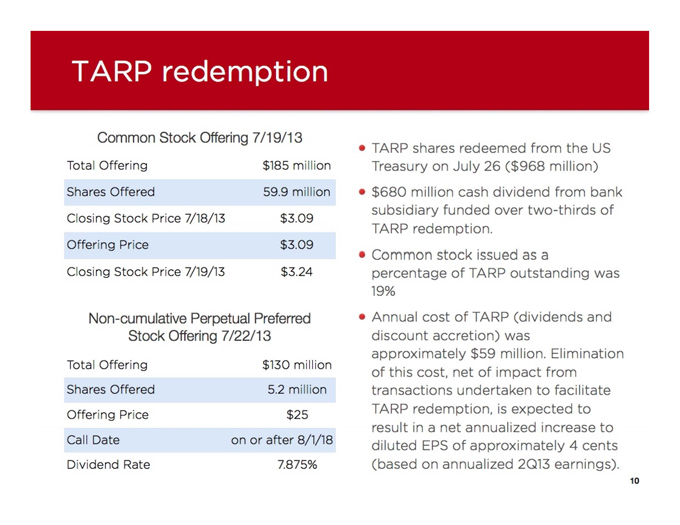

TARP redemption

Common Stock Offering 7/19/13

Total Offering $185 million

Shares Offered 59.9 million

Closing Stock Price 7/18/13 $3.09

Offering Price $3.09

Closing Stock Price 7/19/13 $3.24

Non-cumulative Perpetual Preferred Stock Offering 7/22/13

Total Offering $130 million

Shares Offered 5.2 million

Offering Price $25

Call Date on or after 8/1/18

Dividend Rate 7.875%

TARP shares redeemed from the US Treasury on July 26 ($968 million)

$680 million cash dividend from bank subsidiary funded over two-thirds of TARP redemption.

Common stock issued as a percentage of TARP outstanding was 19%

Annual cost of TARP (dividends and discount accretion) was approximately $59 million. Elimination of this cost net of impact from transactions undertaken to facilitate TARP redemption, is expected to result in a net annualized increase to diluted EPS of approximately 4 cents (based on annualized 2Q13 earnings).

10

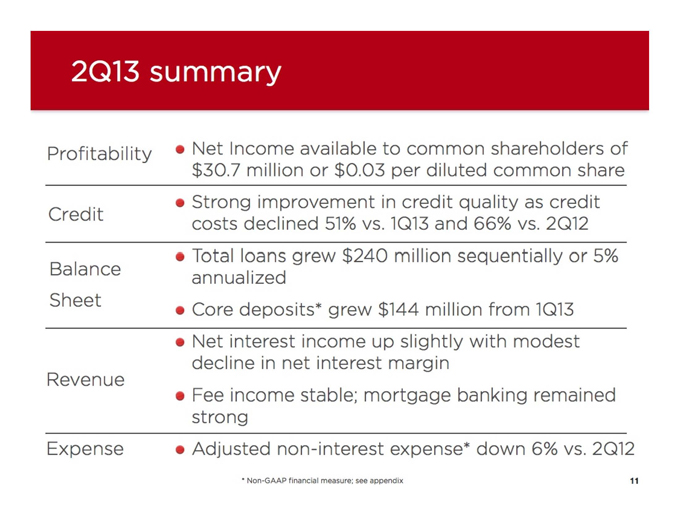

2Q13 summary

Profitability

Credit

Balance Sheet

Revenue

Expense

Net Income available to common shareholders of $30.7 million or $0.03 per diluted common share

Strong improvement in credit quality as credit costs declined 51% vs. 1Q13 and 66% vs. 2Q12

Total loans grew $240 million sequentially or 5% annualized

Core deposits* grew $144 million from 1Q13

Net interest income up slightly with modest decline in net interest margin

Fee income stable; mortgage banking remained strong

Adjusted non-interest expense* down 6% vs. 2Q12

* Non-GAAP financial measure; see appendix

11

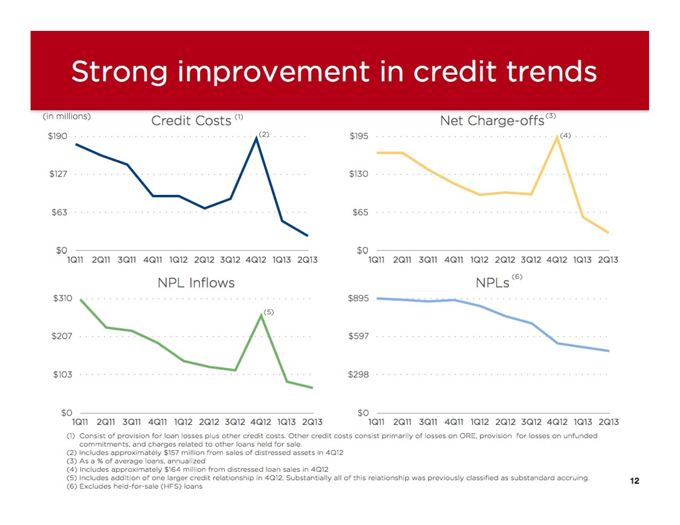

strong improvement in credit trends

(in millions) Credit Costs(1) Net charge-offs(3)

$190 $195 (2) (4)

$127 $130

$63 $65

$0

$0

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

(5)

NPL Inflows

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

(6)

NPLs

$310

$895

$207

$597

$103

$298

$0

$0

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

(1) Consist of provision for loan losses plus other credit costs. Other credit costs consist primarily of losses on ORE, provision for losses on unfunded commitments, and charges related to other loans held for sale.

(2) Includes approximately $157 million from sales of distressed assets in 4Q12

(3) As a % of average loans, annualized

(4) Includes approximately $164 million from distressed loan sales in 4Q12

(5) Includes addition of one larger credit relationship in 4Q12. Substantially all of this relationship was previously classified as substandard accruing.

(6) Excludes held-for-sale (HFS) loans

12

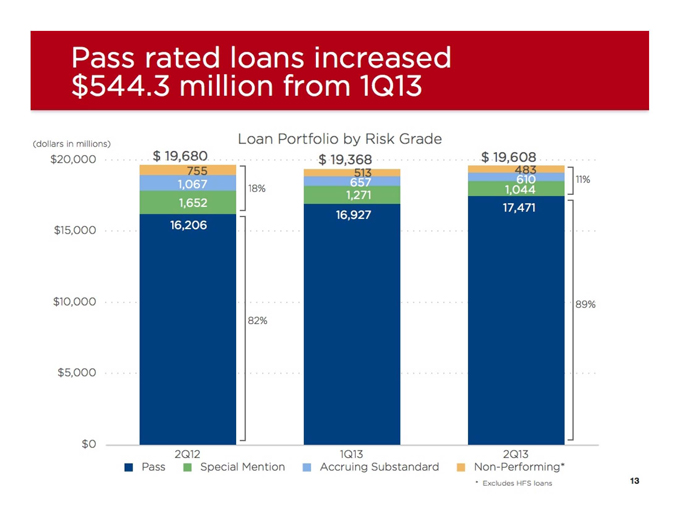

Pass rated loans increased $544.3 million from 1Q13

(dollars in millions) $20,000

$ 19,680 755

Loan Portfolio by Risk Grade

$19,368

513

$ 19,608 483

1,067

18%

1,271

16,927

$15,000

$10,000

89%

82%

$5,000

2Q13 Non-Performing*

* Excludes HFS loans

657

11%

1,652

610

17,471

1,044

16,206

2Q12

Pass Special Mention

1Q13

Accruing Substandard

13

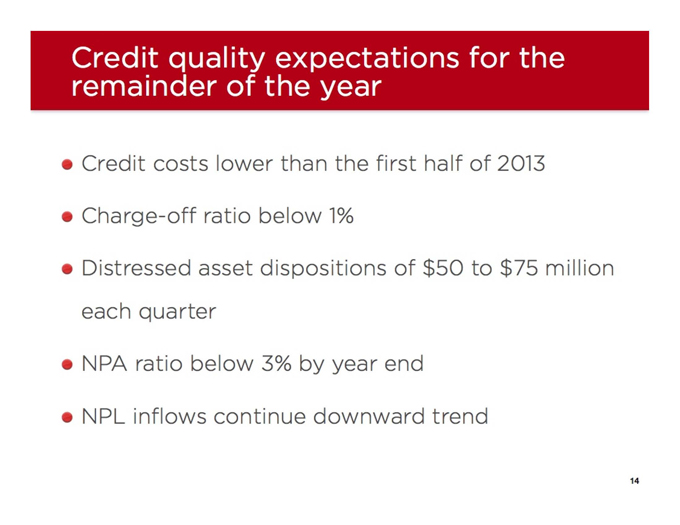

Credit quality expectations for the remainder of the year

Credit costs lower than the first half of 2013

Charge-off ratio below 1%

Distressed asset dispositions of $50 to $75 million each quarter

NPA ratio below 3% by year end

NPL inflows continue downward trend

14

The road ahead

Current banking environment

Expense management is a way of life for the industry

Small business activity remains sluggish

Large corporate borrowers are active

Mid- and large-sized businesses expect more value-added services, not just loans

Pricing pressure continues

Fee income generation is under pressure

Mortgage lending impacted by rising interest rates

Branch utilization is changing and other channel use is expanding

16

Synovus is well-positioned for the future

A strong banking franchise in an improving economy

A strengthened balance sheet and solid operating foundation

A roadmap focused on execution

17

Synovus is well-positioned for the future

A strong banking franchise in an improving economy

Targeting high-potential consumer, business, and larger corporate borrowers who value our relationship-based delivery model

Consistently recognized for customer service excellence in retail, small business, and middle market banking

Synovus Family Asset Management again listed in Bloomberg’s 2013 ranking as one of the top 50 family offices in the world

Committed to retention and expansion of market share in attractive Southeastern footprint

-Always evaluating current bank market potential for continued growth and financial performance

Strategic new market and business line additions

18

Recently launched initiatives demonstrate our strategic focus on footprint opportunities

Metro Orlando, Florida Market Expansion

Metro Orlando among top locations for business growth

Logical next-step expansion market for Synovus in Florida, complementing existing franchise in Tampa, Jacksonville and panhandle

Added team of experienced Commercial, Private, and CRE bankers

Equipment Finance

Hired strong, proven, in market leadership

Large manufacturing presence in Southeast - big users of heavy equipment

Opportunity for more than $1 billion in loan growth over the next five years

19

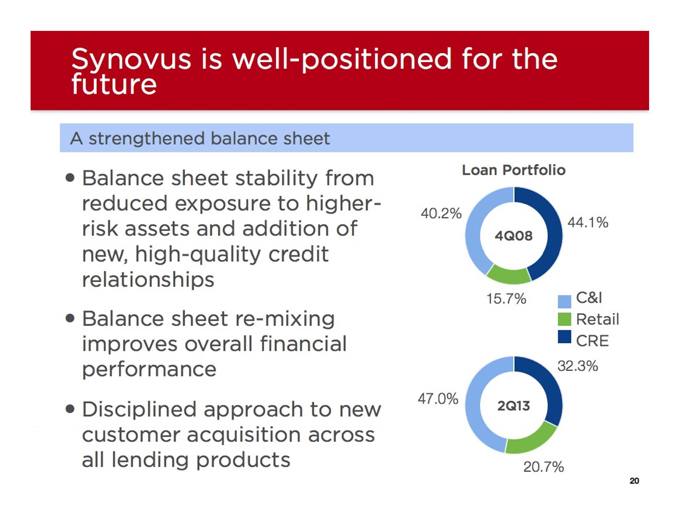

Synovus is well-positioned for the future

A strengthened balance sheet

Loan Portfolio

Balance sheet stability from reduced exposure to higher-risk assets and addition of new, high-quality credit

40.2%

4Q08

44.1%

15.7% C&I

Retail CRE

32.3%

relationships

Balance sheet re-mixing improves overall financial performance

Disciplined approach to new customer acquisition across all lending products

47.0%

2Q13

20.7%

20

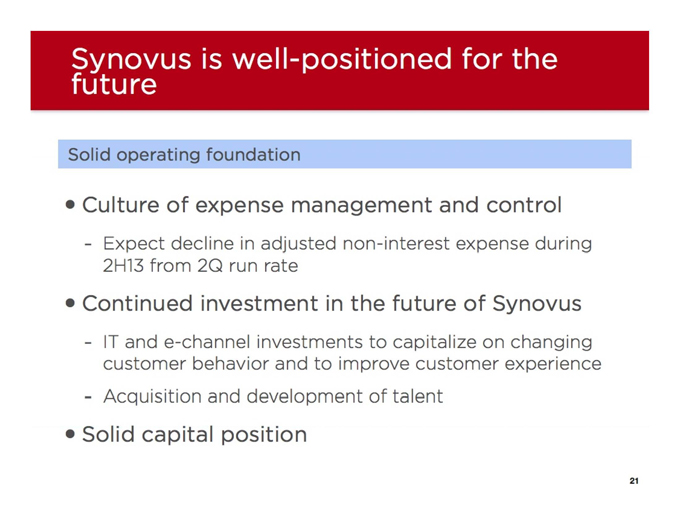

Synovus is well-positioned for the future

Solid operating foundation

Culture of expense management and control

- Expect decline in adjusted non-interest expense during 2H13 from 2Q run rate

Continued investment in the future of Synovus

-IT and e-channel investments to capitalize on changing customer behavior and to improve customer experience

-Acquisition and development of talent

Solid capital position

21

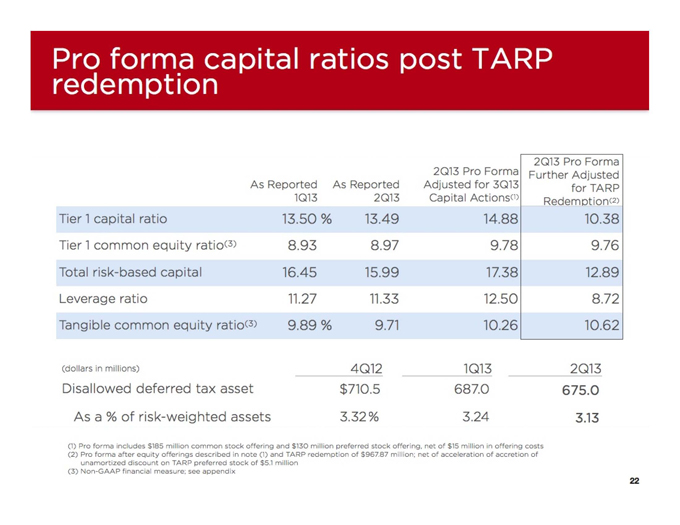

Pro forma capital ratios post TARP redemption

As Reported 1Q13 As Reported 2Q13 2Q13 Pro Forma Adjusted for 3Q13 Capital Actions(1) 2Q13 Pro Forma Further Adjusted for TARP Redemption(2)

Tier 1 capital ratio 13.50% 13.49 14.88 10.38

Tier 1 common equity ratio(3) 8.93 8.97 9.78 9.76

Total risk-based capital 16.45 15.99 17.38 12.89

Leverage ratio 11.27 11.33 12.50 8.72

Tangible common equity ratio(3) 9.89% 9.71 10.26 10.62

(dollars in millions) 4Q12 1Q13 2Q13

Disallowed deferred tax asset $710.5 687.0 675.0

As a % of risk-weighted assets 3.32% 3.24 3.13

(l) Pro forma includes $185 million common stock offering and $130 million preferred stock offering, net of $15 million in offering costs (2) Pro forma after equity offerings described in note (1) and TARP redemption of $967.87 million; net of acceleration of accretion of

unamortized discount on TARP preferred stock of $5.1 million (3) Non-GAAP financial measure; see appendix

22

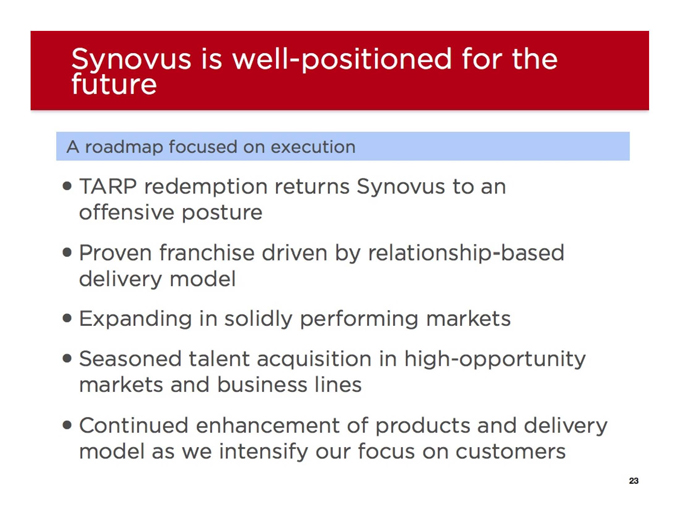

Synovus is well-positioned for the future

A roadmap focused on execution

TARP redemption returns Synovus to an offensive posture

Proven franchise driven by relationship-based delivery model

Expanding in solidly performing markets

Seasoned talent acquisition in high-opportunity markets and business lines

Continued enhancement of products and delivery model as we intensify our focus on customers

23

Synovus is well-positioned for the future

A strong banking franchise in an improving economy

A strengthened balance sheet and solid operating foundation

A roadmap focused on execution

24

APPENDIX

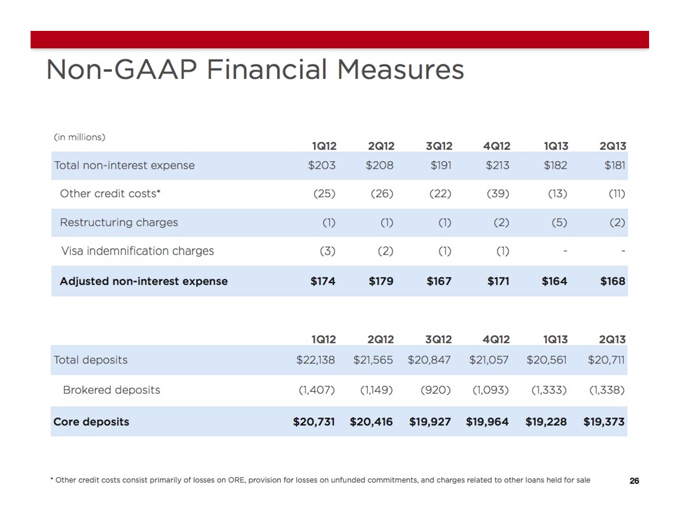

Non-GAAP Financial Measures

(in millions)

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Total non-interest expense $203 $208 $191 $213 $182 $181

Other credit costs* (25) (26) (22) (39) (13) (11)

Restructuring charges (1) (1) (1) (2) (5) (2)

Visa indemnification charges (3) (2) (1) (1) - -

Adjusted non-interest expense $174 $179 $167 $171 $164 $168

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Total deposits $22,138 $21,565 $20,847 $21,057 $20,561 $20,711

Brokered deposits (1,407) (1,149) (920) (1,093) (1,333) (1,338)

Core deposits $20,731 $20,416 $19,927 $19,964 $19,228 $19,373

* Other credit costs consist primarily of losses on ORE, provision for losses on unfunded commitments, and charges related to other loans held for sale

26

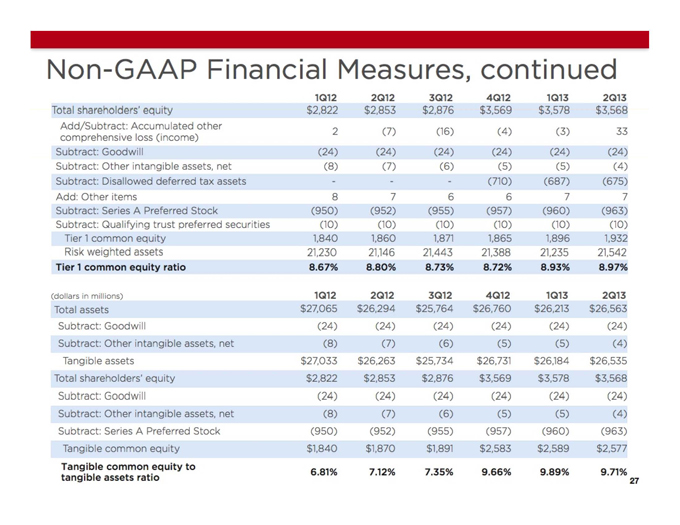

Non-GAAP Financial Measures, continued

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Total shareholders’ equity $2,822 $2,853 $2,876 $3,569 $3,578 $3,568

Add/Subtract: Accumulated other comprehensive loss (income) 2 (7) (16) (4) (3) 33

Subtract: Goodwill (24) (24) (24) (24) (24) (24)

Subtract: Other intangible assets, net (8) (7) (6) (5) (5) (4)

Subtract: Disallowed deferred tax assets - - - (710) (687) (675)

Add: Other items 8 7 6 6 7 7

Subtract: Series A Preferred Stock (950) (952) (955) (957) (960) (963)

Subtract: Qualifying trust preferred securities (10) (10) (10) (10) (10) (10)

Tier 1 common equity 1,840 1,860 1,871 1,865 1,896 1,932

Risk weighted assets 21,230 21,146 21,443 21,388 21,235 21,542

Tier 1 common equity ratio 8.67% 8.80% 8.73% 8.72% 8.93% 8.97%

(dollars in millions) 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Total assets $27,065 $26,294 $25,764 $26,760 $26,213 $26,563

Subtract: Goodwill (24) (24) (24) (24) (24) (24)

Subtract: Other intangible assets, net (8) (7) (6) (5) (5) (4)

Tangible assets $27,033 $26,263 $25,734 $26,731 $26,184 $26,535

Total shareholders’ equity $2,822 $2,853 $2,876 $3,569 $3,578 $3,568

Subtract: Goodwill (24) (24) (24) (24) (24) (24)

Subtract: Other intangible assets, net (8) (7) (6) (5) (5) (4)

Subtract: Series A Preferred Stock (950) (952) (955) (957) (960) (963)

Tangible common equity $1,840 $1,870 $1,891 $2,583 $2,589 $2,577

Tangible common equity to tangible assets ratio 6.81% 7.12% 7.35% 9.66% 9.89% 9.71%

27