Exhibit 99.2

ADAGIO MEDICAL Investor Presentation | February 2024

DISCLAIMER 2 This investor presentation (together with the oral statements made in connection herewith, this “Presentation”) is for informational purposes only to assist interested parties in making their own evaluation with respect to the proposed business combination and any related transaction, including with the PIPE financing described herein (collectively, the “Business Combination”), by and among ARYA Sciences Acquisition Corp IV (NASDAQ: ARYD) (“ARYA”), Adagio Medical, Inc. (the “Company”) and Aja Holdco, Inc., of which the Company will become a subsidiary following the consummation of the Business Combination (“ListCo”), and for no other purpose. The information contained herein is subject to change, and any such change could be material, and does not purport to be all-inclusive and none of ARYA, the Company, ListCo, Jefferies LLC (“Jefferies”) or Chardan Capital Markets, LLC (“Chardan”) or any of their respective affiliates (including, without limitation, control persons, directors, officers, employees, shareholders, representatives, legal counsel or advisors) makes any representation or warranty, express or implied, as to the accuracy, completeness or reliability of the information contained in this Presentation or any other written or oral communication communicated to the recipient in the course of the recipient’s evaluation of ARYA, the Company and ListCo. Please refer to the definitive merger agreement and other related transaction documents, when available, for the full terms of the Business Combination. This Presentation does not constitute (i) a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the Business Combination or (ii) an offer to sell, a solicitation of an offer to buy, or a recommendation to purchase any security of ARYA, the Company, ListCo or any of their respective affiliates. You should not construe the contents of this Presentation as legal, tax, accounting or investment advice or a recommendation. You should consult your own counsel and tax and financial advisors as to legal and related matters concerning the matters described herein, and, by accepting this Presentation, you confirm that you are not relying upon the information contained herein to make any investment decision. The reader shall not rely upon any statement, representation or warranty made by any other person, firm or corporation (including, without limitation, Jefferies, Chardan and any of their affiliates or control persons, officers, directors and employees) in making its investment or decision to invest in ARYA, the Company or ListCo. To the fullest extent permitted by law, none of ARYA, the Company, ListCo, Jefferies and Chardan nor any of their respective affiliates nor any of its or their control persons, officers, directors, employees or representatives, shall be responsible or liable to the reader for any information set forth herein or any action taken or not taken by any reader, including any investment in ARYA, the Company or ListCo. The distribution of this Presentation may also be restricted by law and persons into whose possession this Presentation comes should inform themselves about and observe any such restrictions. The recipient acknowledges that it is (a) aware that the United States securities laws prohibit any person who has material, non-public information concerning a company from purchasing or selling securities of such company or from communicating such information to any other person under circumstances in which it is reasonably foreseeable that such person is likely to purchase or sell such securities, and (b) familiar with the Securities Exchange Act of 1934, as amended, and the rules and regulations promulgated thereunder (collectively, the “Exchange Act”), and that the recipient will neither use, nor cause any third party to use, this Presentation or any information contained herein in contravention of the Exchange Act, including, without limitation, Rule 10b-5 thereunder. This Presentation and information contained herein constitutes confidential information and is provided to you on the condition that you agree that you will hold it in strict confidence and not use, discuss, reproduce, disclose, forward or distribute it in whole or in part without the prior written consent of ARYA, the Company and ListCo and is intended for the recipient hereof only. No securities commission or securities regulatory authority in the United States or any other jurisdiction has in any way passed upon the merits of the Business Combination or the accuracy or adequacy of this Presentation. Certain monetary amounts, percentages and other figures included in this Presentation have been subject to rounding adjustments. Certain amounts that appear in this Presentation may not sum due to rounding. Management's Estimates The Company has based its estimates of the total addressable market and growth forecasts on a number of internal and third-party estimates and resources, including, without limitation, third party reports and the experience of the management team across the industries. While the Company believes its assumptions and the data underlying its estimates are reasonable, these assumptions and estimates may not be correct and the conditions supporting such assumptions or estimates may change at any time, thereby reducing the predictive accuracy of these underlying factors. In addition, the novelty of the markets for the Company’s products may make its assumptions and estimates more uncertain. As a result, the Company's estimates of the total addressable market and growth forecasts for its products are subject to significant uncertainty and may prove to be incorrect. If third-party or internally generated data prove to be inaccurate or the Company makes errors in its assumptions based on that data, the total addressable market for the Company's products may be smaller than it has estimated, its future growth opportunities and sales growth may be impaired, any of which could have a material adverse effect on the Company's business, financial condition and results of operations. Forward-Looking Statements Certain statements in this Presentation may be considered “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements generally relate to future events or ARYA’s, the Company’s or ListCo’s future financial or operating performance. For example, any statements that refer to expectations, projections or other characterizations of future events or circumstances, including post-Business Combination fully diluted equity value, the anticipated enterprise value of ListCo, expected ownership in ListCo, projections of market opportunity and market share, the capability of the Company’s or ListCo’s business plans including its plans to expand, the sources and uses of cash from the Business Combination, any benefits of the Company’s partnerships, strategies or plans as they relate to the Business Combination, anticipated benefits of the Business Combination and expectations related to the terms and timing of the Business Combination, the Company’s expected pro forma cash at announcement, the Company’s or ListCo’s expected cash runway through 2025 or statements related to the Company’s or ListCo’s funding gap, funded business plan or use of proceeds, or other metrics or statements derived therefrom, are forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “forecast,” “future,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “propose,” “seek,” “should,” “strive,” “will,” or “would” or the negatives of these terms or variations of them or similar terminology. Such forward-looking statements are subject to risks, uncertainties, and other factors which may be beyond the control of ARYA, the Company or ListCo and could cause actual results to differ materially from those expressed or implied by such forward-looking statements. These forward-looking statements are based upon estimates and assumptions that, while considered reasonable by ARYA and its management, the Company and its management and ListCo and its management, as the case may be, are inherently uncertain. Each of ARYA, the Company and ListCo caution you that these statements are based on a combination of facts and factors currently known and projections of the future, which are inherently uncertain. There will be risks and uncertainties described in the proxy statement/prospectus included in the registration statement on Form S-4 (the “Registration Statement”) relating to the Business Combination, which is expected to be filed by ListCo with the U.S. Securities and Exchange Commission (the “SEC”), and described in other documents filed by ARYA or ListCo from time to time with the SEC. These filings may identify and address other important risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward-looking statements. Neither ARYA nor the Company can assure you that the forward-looking statements in this presentation will prove to be accurate. In addition, new risks and uncertainties may emerge from time to time, and it may not be possible to identify and accurately predict the potential impacts of any such risks and uncertainties that may arise in the future. Factors that may cause actual results to differ materially from current expectations include, but are not limited to: (1) the occurrence of any event, change or other circumstances that could give rise to the termination of negotiations and any subsequent definitive agreements with respect to the Business Combination; (2) the outcome of any potential litigation, government or regulatory proceedings that may be instituted against ARYA, the Company, ListCo or others following the announcement of the Business Combination and any definitive agreements with respect thereto; (3) the inability to complete the Business Combination due to the failure to obtain approval of the shareholders of ARYA, to obtain financing to complete the Business Combination or to satisfy other conditions to closing; (4) the amount of redemption requests made by ARYA’s public shareholders; (5) changes to the proposed structure of the Business Combination that may be required or appropriate as a result of applicable laws or regulations or as a condition to obtaining regulatory approval of the Business

DISCLAIMER (CONT.) 3 Combination; (6) delays in obtaining, adverse conditions in, or the inability to obtain regulatory approvals, or delays in completing regulatory reviews, required to complete the Business Combination; (7) the ability to meet stock exchange listing standards prior to or following the consummation of the Business Combination; (8) the risk that the Business Combination disrupts current plans and operations of the Company or ListCo as a result of the announcement and consummation of the Business Combination; (9) Adagio’s ability to remain compliant with the covenants of its existing debt, including any convertible or bridge financing notes; (10) ListCo’s ability to remain compliant with the covenants of the senior secured convertible notes that will be issued in connection with the closing of the Business Combination; (11) the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition, the ability of ListCo to grow and manage growth profitably, maintain relationships with customers and suppliers and retain its management and key employees; (12) costs related to the Business Combination; (13) risks associated with changes in applicable laws or regulations and the Company’s or ListCo’s international operations and operations in a regulated industry; (14) the possibility that the Company or ListCo may be adversely affected by other economic, business, and/or competitive factors; (15) the Company’s or ListCo’s use of proceeds, post-Business Combination fully diluted equity value or fully diluted enterprise value, expected pro forma cash at announcement, expected cash runway or funding gap, estimates of expenses and profitability; and (16) the risks described in the “Risk Factor Summary” included in this Presentation, and other risks and uncertainties set forth in the section entitled “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements” in ARYA’s Annual Report on Form 10-K for the year ended December 31, 2022, its Quarterly Reports on Form 10-Q, and other documents filed, or to be filed, with the SEC. There may be additional risks that ARYA, the Company or ListCo do not presently know or that ARYA, the Company or ListCo currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. Actual events and circumstances are difficult or impossible to predict and may materially differ from assumptions. Many actual events and circumstances are beyond the control of ARYA, the Company and ListCo. Nothing in this Presentation should be regarded as a representation or warranty by any person that the forward-looking statements set forth herein will be achieved or that any of the contemplated results of such forward-looking statements will be achieved in any specified time frame or at all. You should not place undue reliance on forward-looking statements, which speak only as of the date they are made in this Presentation. Subsequent events and developments may cause those views to change. Neither ARYA, the Company nor ListCo undertakes any duty to update these forward-looking statements. Use of Projections This Presentation contains forecasts with respect to the Company’s minimum total pro forma cash after expenses at announcement of the Business Combination and ListCo’s expected cash runway through 2025, based on current plans and estimates of the Company. Neither ARYA’s, the Company’s nor ListCo’s independent auditors have audited, reviewed, compiled or performed any procedures with respect to such projected or forecasted information included in this Presentation and, accordingly, they did not express an opinion or provide any other form of assurance with respect thereto for the purpose of this Presentation. The inclusion of the forecasted information should not be relied upon as being necessarily indicative of future results and should not be regarded as an indication that ARYA, the Company, ListCo or any other person considered, or now considers, the projections to be a reliable prediction of future events, and does not constitute an admission or representation by any person that the expectations, beliefs, opinions, and assumptions that underlie such forecasts remain the same following the date of this Presentation, and readers are cautioned not to place undue reliance on any prospective information. The assumptions and estimates underlying the prospective financial information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual cash or cash needs to differ materially from those contained in the prospective financial information. Accordingly, there can be no assurance that the prospective cash or cash needs are indicative of the future performance of the Company or ListCo or that actual cash or cash needs will not differ materially from those presented in the prospective financial information. ARYA, the Company and ListCo do not assume any obligation to update the projected information or any other information in this Presentation, and do not expect to continue to disclose detailed prospective financial information going forward. Actual cash or cash needs may differ as a result of the completion of the Company’s or ListCo’s applicable financial reporting period closing procedures, review adjustments and other developments that may arise between now and the time such financial information for the presented or projected periods is finalized. As a result, these estimates are preliminary, may change and constitute forward-looking information, and are subject to significant risks and uncertainties. See “Forward-Looking Statements” above. Any such forecasted information presented herein was not prepared with a view towards compliance with the published guidelines of the SEC, Regulation S-X promulgated under the Securities Act of 1933, as amended (the “Securities Act”) or any guidelines established by the American Institute of Certified Public Accountants for the presentation and preparation of “prospective financial information.” Accordingly, the information and data presented in this Presentation may not be included, may be adjusted, or may be presented differently, in any proxy statement or registration statement that may be filed in connection with a Business Combination. Industry and Market Data; Trademarks Certain information contained in the Presentation relates to or is based on studies, publications, statistics and surveys from third-party sources, and on ARYA’s and the Company’s own internal estimates and research. In addition, all of the market data included in this Presentation involves a number of assumptions and limitations, and there can be no guarantee as to the accuracy or reliability of such assumptions. While ARYA and the Company believe that the third-party sources and ARYA’s and the Company’s internal research are reliable, such sources and research have not been verified by any independent source. Any data on past performance or modeling contained herein is not an indication as to future performance. This information involves many assumptions and limitations, and you are cautioned not to give undue weight to such industry and market data. The information contained in the third party citations referenced in this presentation is not incorporated by reference into this presentation. This Presentation may include trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners. The inclusion of particular trademarks, service marks, trade names and copyrights of other companies is not intended to, and does not, imply a relationship with ARYA, the Company or ListCo or an endorsement or sponsorship by or of ARYA, the Company or ListCo. ARYA, the Company and ListCo own or have rights to various trademarks, service marks, trade names and copyrights in connection with the operation of their respective businesses which are also included in this Presentation. Solely for convenience, some of the trademarks, service marks, trade names and copyrights referred to in this Presentation may be listed without the ™, ℠, ©, or ® symbols, but the Company, ARYA and ListCo will assert, to the fullest extent under applicable law, the right of the applicable owners, if any, to these trademarks, service marks, trade names and copyrights. Additional Information In connection with the Business Combination, ListCo intends to file with the SEC a registration statement on Form S-4 containing a preliminary proxy statement and a preliminary prospectus of ARYA, and after the Registration Statement is declared effective, ARYA expects to mail a definitive proxy statement/prospectus related to the Business Combination to its shareholders. The proxy statement/prospectus will contain important information about the Business Combination and the other matters to be voted upon at ARYA’s shareholder meeting to be held to approve the Business Combination. ARYA and ListCo may also file other documents with the SEC regarding the Business Combination. This Presentation does not contain all the information that should be considered concerning the Business Combination and is not intended to form the basis of any investment decision or any other decision in respect of the Business Combination. Before making any voting or other investment decisions, shareholders of ARYA and other interested persons are advised to read, when available, the preliminary proxy statement/prospectus and any amendments thereto, the definitive proxy statement/prospectus and other documents filed in connection with the Business Combination, as these materials will contain important information about ARYA, the Company and the Business Combination. After the Registration Statement becomes effective, the definitive proxy statement/prospectus and other relevant materials for the Business Combination will be mailed to shareholders of ARYA as of a record date to be established for voting on the Business Combination. Shareholders will also be able to obtain copies of the definitive proxy statement/prospectus and other documents filed with the SEC, without charge, once available, at the SEC’s website at www.sec.gov, or by directing a request to: ARYA Sciences Acquisition Corp IV, 51 Astor Place, 10th Floor, New York, New York, Attention: Secretary, ARYA4@perceptivelife.com. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

DISCLAIMER (CONT.) 4 Participants in the Solicitation ARYA, the Company, ListCo and their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from ARYA’s shareholders with respect to the Business Combination. A list of the names of ARYA’s directors and executive officers and a description of their interests in ARYA is contained in ARYA’s Annual Report on Form 10-K, which was filed with the SEC and is available free of charge at the SEC’s web site at www.sec.gov, or by directing a request to ARYA Sciences Acquisition Corp IV, 51 Astor Place, 10th Floor, New York, New York, Attention: Secretary, ARYA4@perceptivelife.com. Additional information regarding the interests of such participants will be contained in the proxy statement/prospectus for the Business Combination when available. Investors, security holders and other interested person of ARYA, the Company and ListCo are urged to carefully read in their entirety the proxy statement/prospectus and other relevant documents that will be filed with the SEC, when they become available, because they will contain important information about the Business Combination. Also see above under the heading “Additional Information.” The Company and ListCo, and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from the shareholders of ARYA in connection with the proposed Business Combination. A list of the names of such directors and executive officers and information regarding their interests in the proposed Business Combination will be included in the proxy statement/prospectus for the proposed Business Combination when available. No Offer and Non-Solicitation This Presentation does not constitute (i) a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the Business Combination or (ii) an offer to sell, a solicitation of an offer to buy, or a recommendation to purchase any security of ARYA, the Company, ListCo or any of their respective affiliates. No such offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act, or an exemption therefrom. The offering and resale of the securities issuable in connection with the PIPE financing described herein has not been and will not be registered under the Securities Act or any applicable state securities laws. If the proposed Business Combination is entered into, the PIPE financing will be offered and sold only to “qualified institutional buyers” (as defined in Rule 144A under the Securities Act) and institutional “accredited investors” (as defined in Rule 501(a)(1), (2), (3) or (7) promulgated under the Securities Act) upon the consummation of the proposed Business Combination. Notice to investors in the European Economic Area / Prohibition of sales to EEA retail investors In member states of the European Economic Area (the “EEA”), this Presentation and any offer if made subsequently is directed exclusively at persons who are “qualified investors” within the meaning of Article 2(e) of Regulation (EU) 2017/1129 (the “Prospectus Regulation”). The securities are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the EEA. For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of Directive 2014/65/EU (as amended, “MiFID II”); (ii) a customer within the meaning of Directive 2002/92/EC (as amended, the “Insurance Mediation Directive”), where that customer would not qualify as a professional client as defined in point (10) of Article 4(1) of MiFID II; or (iii) not a qualified investor as defined in the Prospectus Regulation. Consequently, no key information document required by Regulation (EU) No 1286/2014 (as amended the “PRIIPs Regulation”) for offering or selling the securities or otherwise making them available to retail investors in the EEA has been prepared and therefore offering or selling the securities or otherwise making them available to any retail investor in the EEA may be unlawful under the PRIIPs Regulation. Notice to investors in the UK / Prohibition of sales to UK retail investors In the United Kingdom (“UK”), any offer of the securities will be made pursuant to an exemption under Regulation (EU) 2017/1129 as it forms part of domestic law by virtue of the European Union (Withdrawal) Act 2018 (the “EUWA”) (the “UK Prospectus Regulation”) from a requirement to publish a prospectus for offers of securities. This Presentation is for distribution in the UK only to (i) investment professionals falling within article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”); or (ii) high net worth entities and other persons to whom it may lawfully be communicated, falling within article 49(2)(a) to (d) of the Order; and (iii) “qualified investors” within the meaning of article 2(e) of the UK Prospectus Regulation. The securities are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the UK. For these purposes, a “retail investor” means a person who is one (or more) of: (i) a retail client, as defined in Directive (EU) 2014/65/EU on markets in financial instruments (as amended) and implemented in the UK as it forms part of the domestic law of the United Kingdom by virtue of the EUWA (“UK MIFID II”); (ii) a customer within the meaning of Directive (EU) 2016/97 (as amended) as it forms part of the domestic law of the UK by virtue of the EUWA, where that customer would not qualify as a professional client as defined in UK MIFID II; or (iii) not a “qualified investor” as defined in Article 2(e) of the UK Prospectus Regulation. Consequently, no key information document required by Regulation (EU) No 1286/2014 as it forms part of the domestic law of the UK by virtue of the EUWA (the “UK PRIIPs Regulation”) for offering or selling the securities or otherwise making them available to retail investors in the UK has been prepared and, therefore, offering or selling the securities or otherwise making them available to any retail investor in the UK may be unlawful under the UK PRIIPs Regulation.

WHY INVEST: ADAGIO MEDICAL OPPORTUNITY IN A NUTSHELL 5 Highly differentiated technology with focus on improved ablation outcomes Comprehensive portfolio of solutions for atrial and ventricular arrhythmias Extensive pipeline of clinical investigations Investor Validation Near-term value drivers Q4 2023: Cryocure-VT chronic data and vCLAS™ CE-Mark Q3 2024: iCLAS™ US IDE data US PMA in Q1 20205 Q1 2025: PARALELL study data Cryopulse™ CE-Mark in 2025 Currently ~$3 billion catheter market; advanced catheter revenue (75% of total) experienced historical double-digit growth1 ✔ Target clinical indications (VT and Afib ablations) are highly underpenetrated due to limited effectiveness ✔ Adagio’s breakthrough technology demonstrating improved outcomes in VT and persistent AF segments: ~$1bn ~$3bn combined growth potential2 ✔ Value inflection expected from catalysts through the next 18 months ✔ Leading investors including Perceptive Advisors, RA Capital, and Arrowmark ✔ Note: Management's analysis and estimates which are subject to significant uncertainty and may prove to be incorrect. Please see Disclaimer - Management's Estimates on slide 2. The historical market growth is based on management's analysis and calculations using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 63-66 which are part of Appendix II - Market Sources & Analysis for further details. The combined growth potential is based on management's analysis and projections using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 63-66 which are part of Appendix II - Market Sources & Analysis for further details.

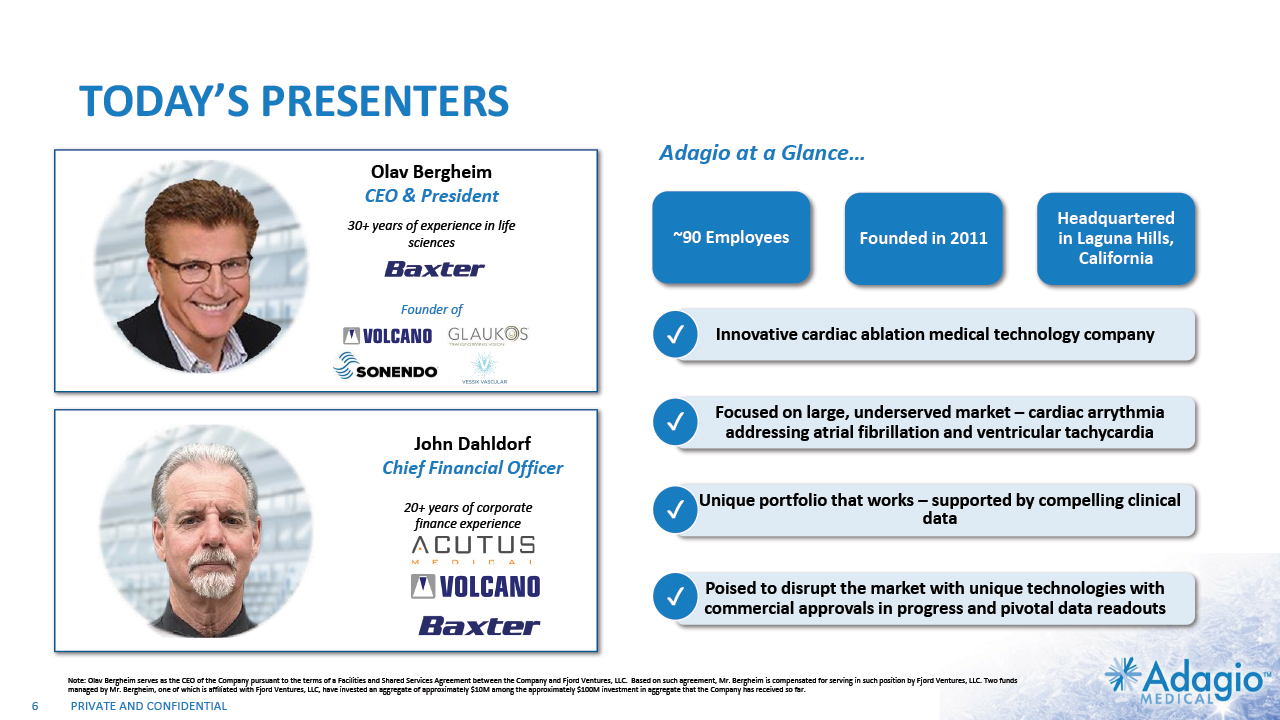

TODAY’S PRESENTERS 6 Olav Bergheim CEO & President John Dahldorf Chief Financial Officer 20+ years of corporate finance experience 30+ years of experience in life sciences Founder of Innovative cardiac ablation medical technology company ✔ Focused on large, underserved market – cardiac arrythmia addressing atrial fibrillation and ventricular tachycardia ✔ Unique portfolio that works – supported by compelling clinical data ✔ Poised to disrupt the market with unique technologies with commercial approvals in progress and pivotal data readouts ✔ ~90 Employees Founded in 2011 Headquartered in Laguna Hills, California Adagio at a Glance… Note: Olav Bergheim serves as the CEO of the Company pursuant to the terms of a Facilities and Shared Services Agreement between the Company and Fjord Ventures, LLC. Based on such agreement, Mr. Bergheim is compensated for serving in such position by Fjord Ventures, LLC. Two funds managed by Mr. Bergheim, one of which is affiliated with Fjord Ventures, LLC, have invested an aggregate of approximately $10M among the approximately $100M investment in aggregate that the Company has received so far.

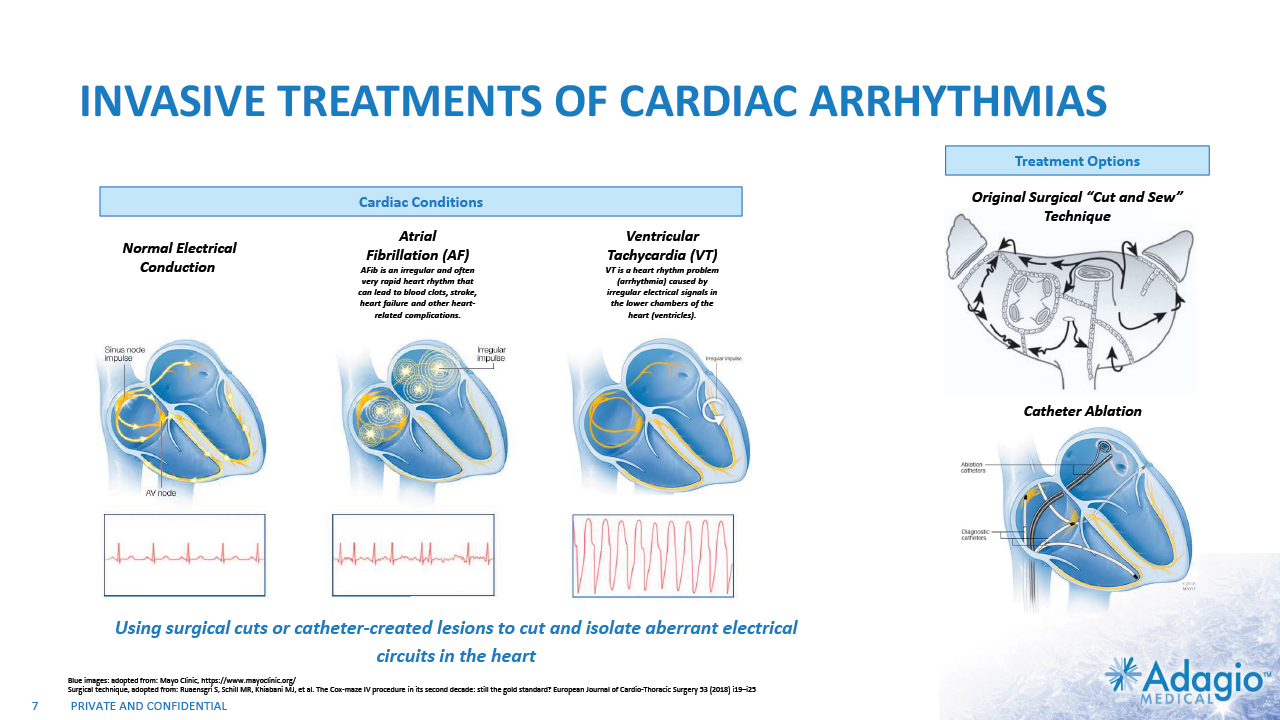

INVASIVE TREATMENTS OF CARDIAC ARRHYTHMIAS Using surgical cuts or catheter-created lesions to cut and isolate aberrant electrical circuits in the heart 7 Normal Electrical Conduction Ventricular Tachycardia (VT) VT is a heart rhythm problem (arrhythmia) caused by irregular electrical signals in the lower chambers of the heart (ventricles). Original Surgical “Cut and Sew” Technique Atrial Fibrillation (AF) AFib is an irregular and often very rapid heart rhythm that can lead to blood clots, stroke, heart failure and other heart-related complications. Catheter Ablation Treatment Options Cardiac Conditions Blue images: adopted from: Mayo Clinic, https://www.mayoclinic.org/ Surgical technique, adopted from: Ruaensgri S, Schill MR, Khiabani MJ, et al. The Cox-maze IV procedure in its second decade: still the gold standard? European Journal of Cardio-Thoracic Surgery 53 (2018) i19–i25

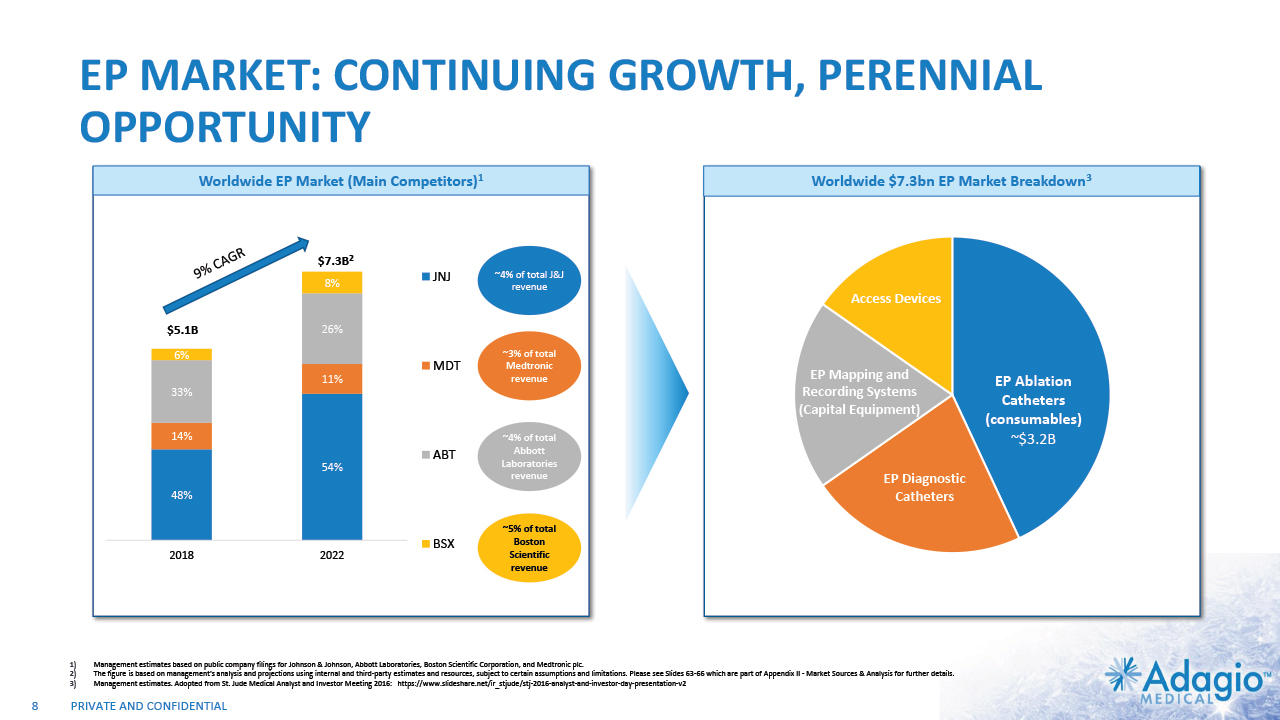

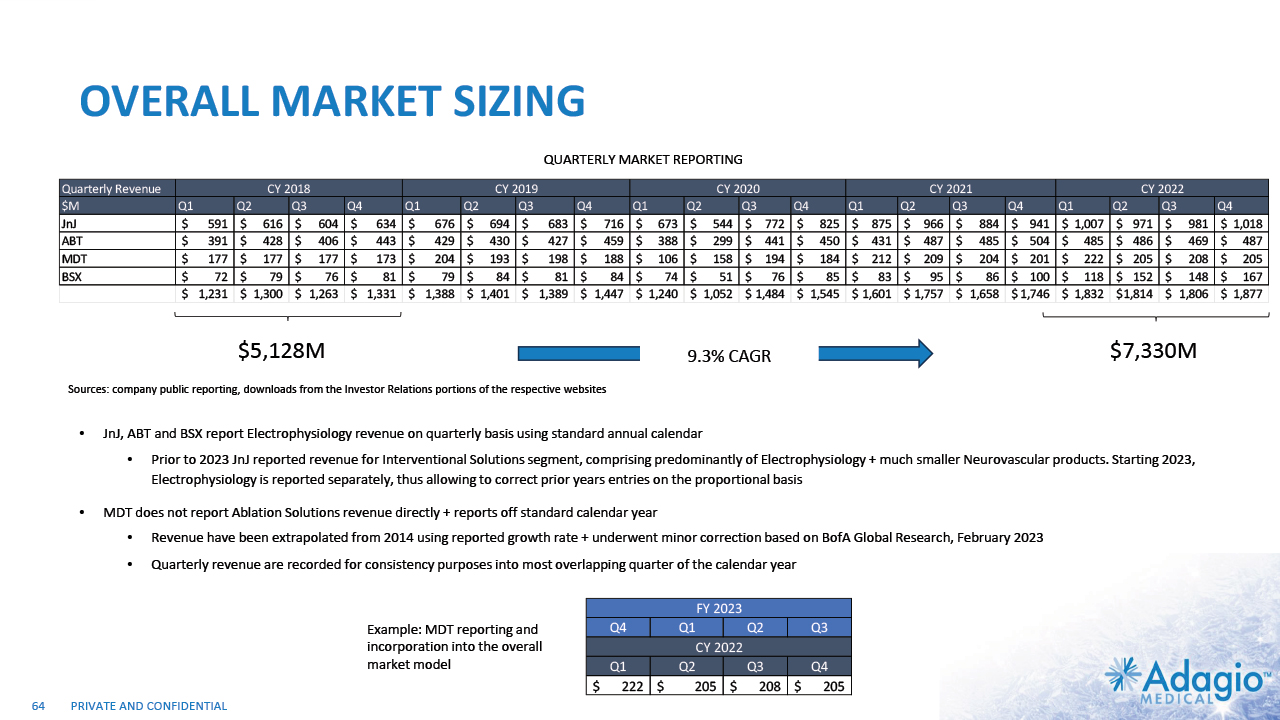

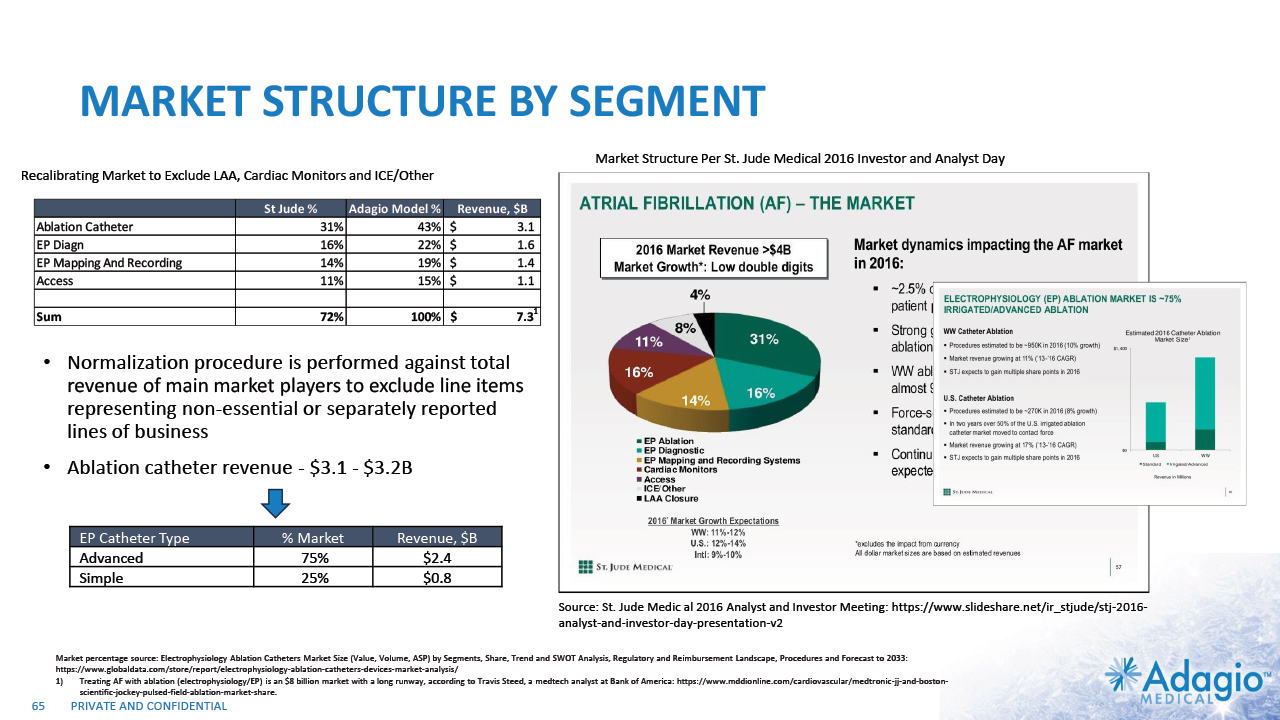

EP MARKET: CONTINUING GROWTH, PERENNIAL OPPORTUNITY 9% CAGR Worldwide EP Market (Main Competitors)1 Worldwide $7.3bn EP Market Breakdown3 $5.1B $7.3B2 EP Ablation Catheters (consumables) ~$3.2B ~4% of total J&J revenue ~3% of total Medtronic revenue ~4% of total Abbott Laboratories revenue ~5% of total Boston Scientific revenue 8 EP Diagnostic Catheters Access Devices EP Mapping and Recording Systems (Capital Equipment) Management estimates based on public company filings for Johnson & Johnson, Abbott Laboratories, Boston Scientific Corporation, and Medtronic plc. The figure is based on management's analysis and projections using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 63-66 which are part of Appendix II - Market Sources & Analysis for further details. Management estimates. Adopted from St. Jude Medical Analyst and Investor Meeting 2016: https://www.slideshare.net/ir_stjude/stj-2016-analyst-and-investor-day-presentation-v2

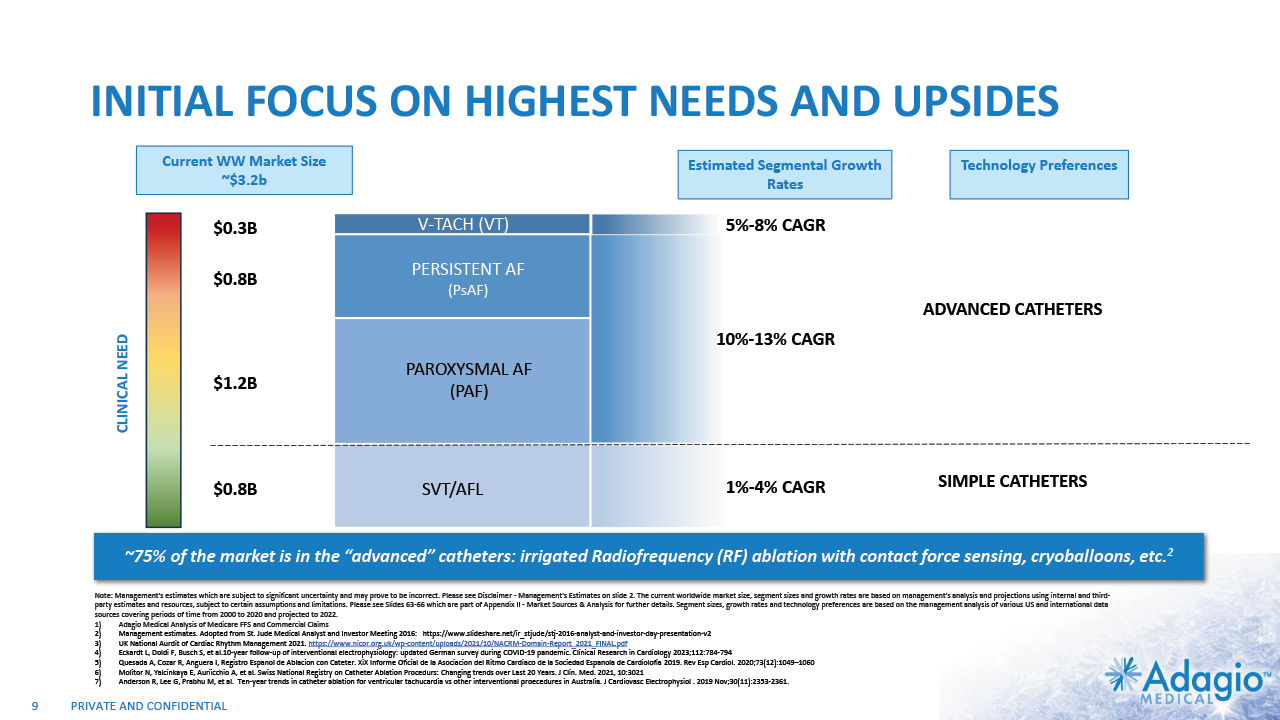

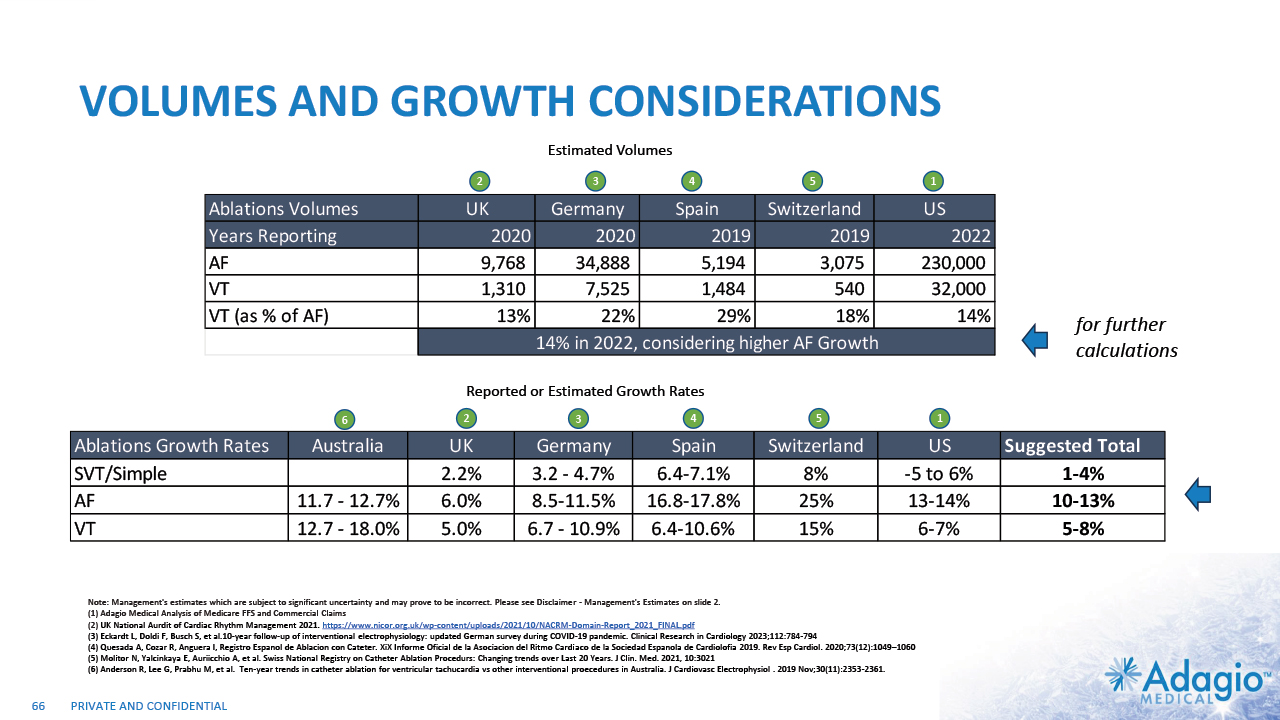

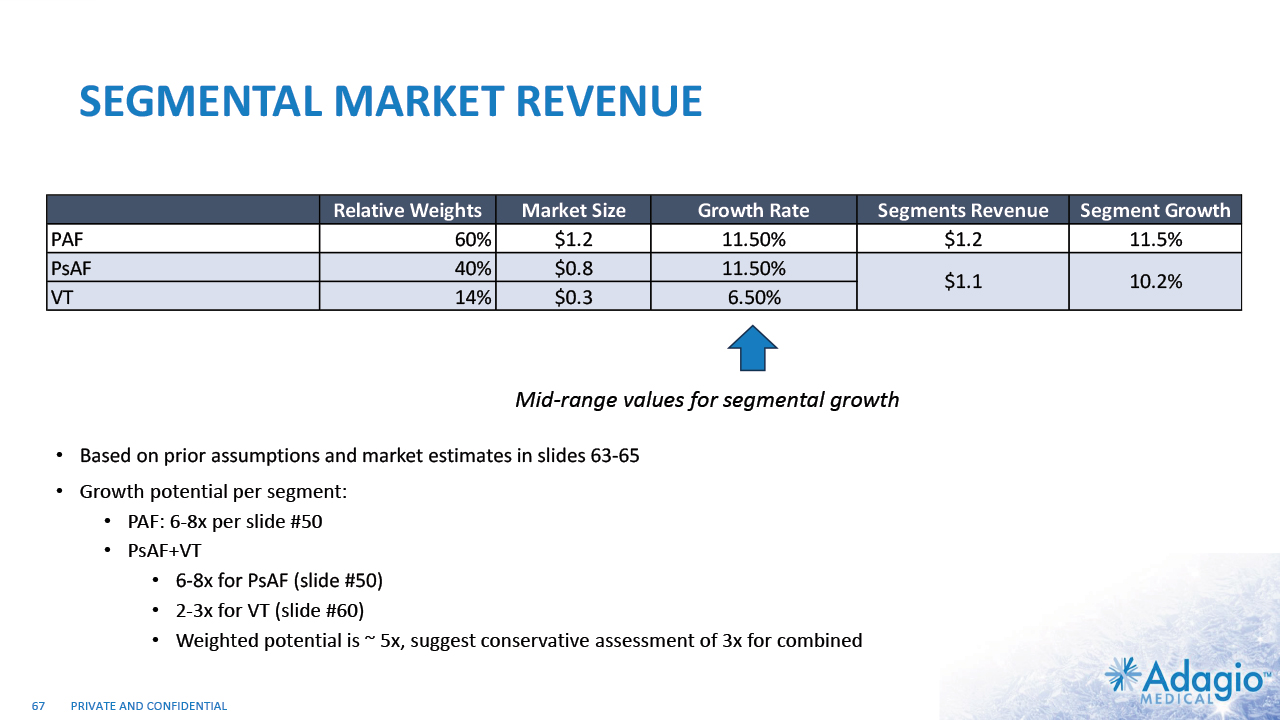

INITIAL FOCUS ON HIGHEST NEEDS AND UPSIDES 9 PAROXYSMAL AF (PAF) SVT/AFL PERSISTENT AF (PsAF) V-TACH (VT) 1%-4% CAGR 10%-13% CAGR 5%-8% CAGR $0.8B $0.8B $1.2B $0.3B SIMPLE CATHETERS ADVANCED CATHETERS ~75% of the market is in the “advanced” catheters: irrigated Radiofrequency (RF) ablation with contact force sensing, cryoballoons, etc.2 CLINICAL NEED Current WW Market Size ~$3.2b Estimated Segmental Growth Rates Technology Preferences Note: Management's estimates which are subject to significant uncertainty and may prove to be incorrect. Please see Disclaimer - Management's Estimates on slide 2. The current worldwide market size, segment sizes and growth rates are based on management's analysis and projections using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 63-66 which are part of Appendix II - Market Sources & Analysis for further details. Segment sizes, growth rates and technology preferences are based on the management analysis of various US and international data sources covering periods of time from 2000 to 2020 and projected to 2022. Adagio Medical Analysis of Medicare FFS and Commercial Claims Management estimates. Adopted from St. Jude Medical Analyst and Investor Meeting 2016: https://www.slideshare.net/ir_stjude/stj-2016-analyst-and-investor-day-presentation-v2 UK National Aurdit of Cardiac Rhythm Management 2021. https://www.nicor.org.uk/wp-content/uploads/2021/10/NACRM-Domain-Report_2021_FINAL.pdf Eckardt L, Doldi F, Busch S, et al.10-year follow-up of interventional electrophysiology: updated German survey during COVID-19 pandemic. Clinical Research in Cardiology 2023;112:784-794 Quesada A, Cozar R, Anguera I, Registro Espanol de Ablacion con Cateter. XiX Informe Oficial de la Asociacion del Ritmo Cardiaco de la Sociedad Espanola de Cardiolofia 2019. Rev Esp Cardiol. 2020;73(12):1049–1060 Molitor N, Yalcinkaya E, Auriicchio A, et al. Swiss National Registry on Catheter Ablation Procedurs: Changing trends over Last 20 Years. J Clin. Med. 2021, 10:3021 Anderson R, Lee G, Prabhu M, et al. Ten-year trends in catheter ablation for ventricular tachucardia vs other interventional proecedures in Australia. J Cardiovasc Electrophysiol . 2019 Nov;30(11):2353-2361.

ATRIAL FIBRILLATION MARKET: OPPORTUNITY, DRIVERS AND INHIBITORS

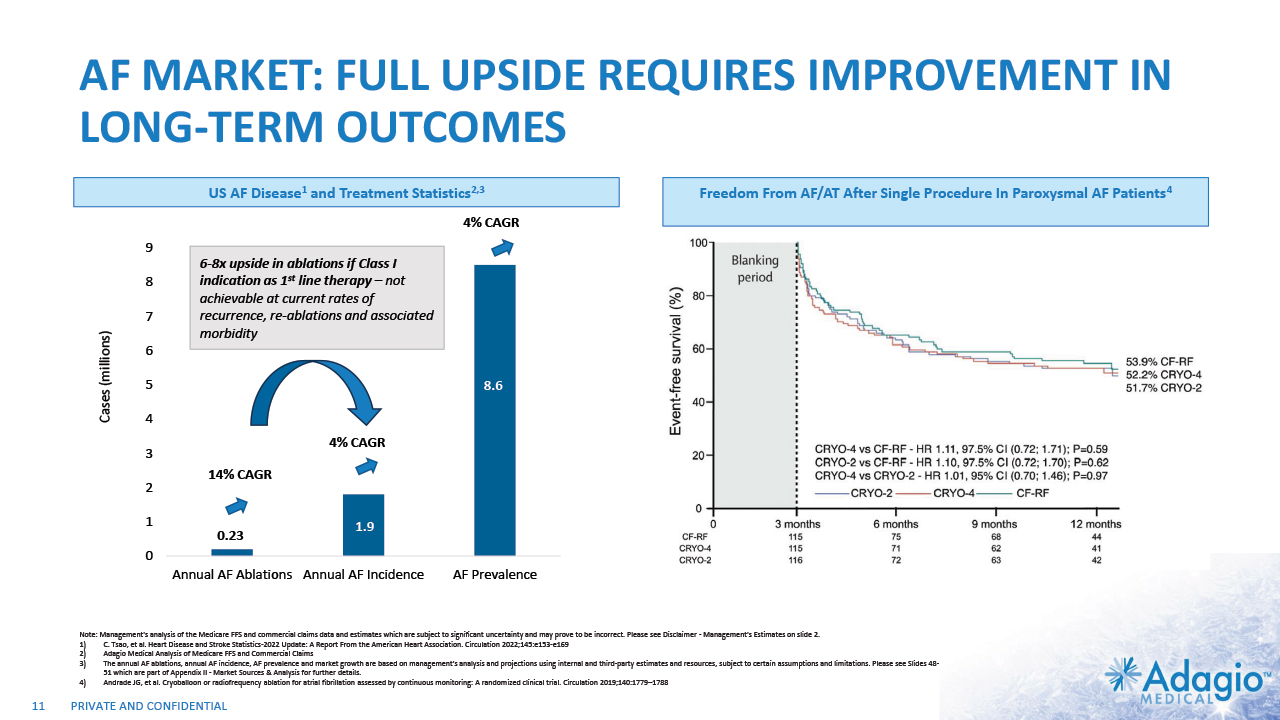

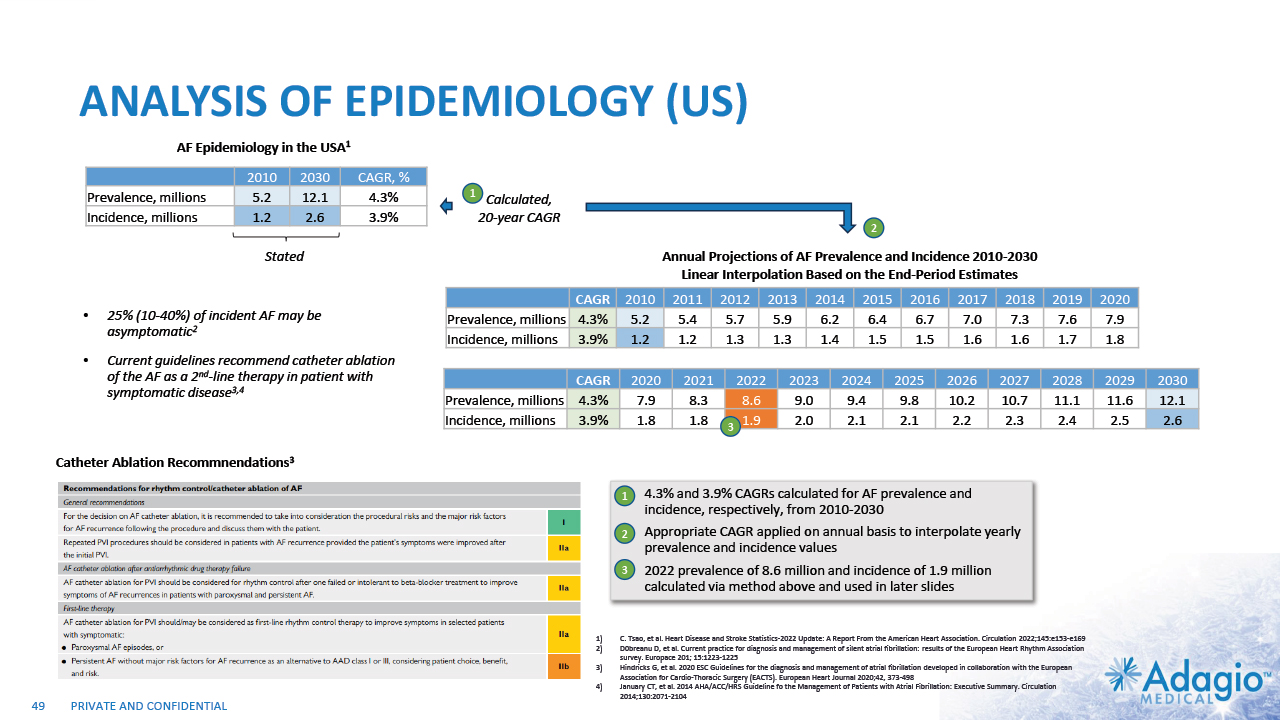

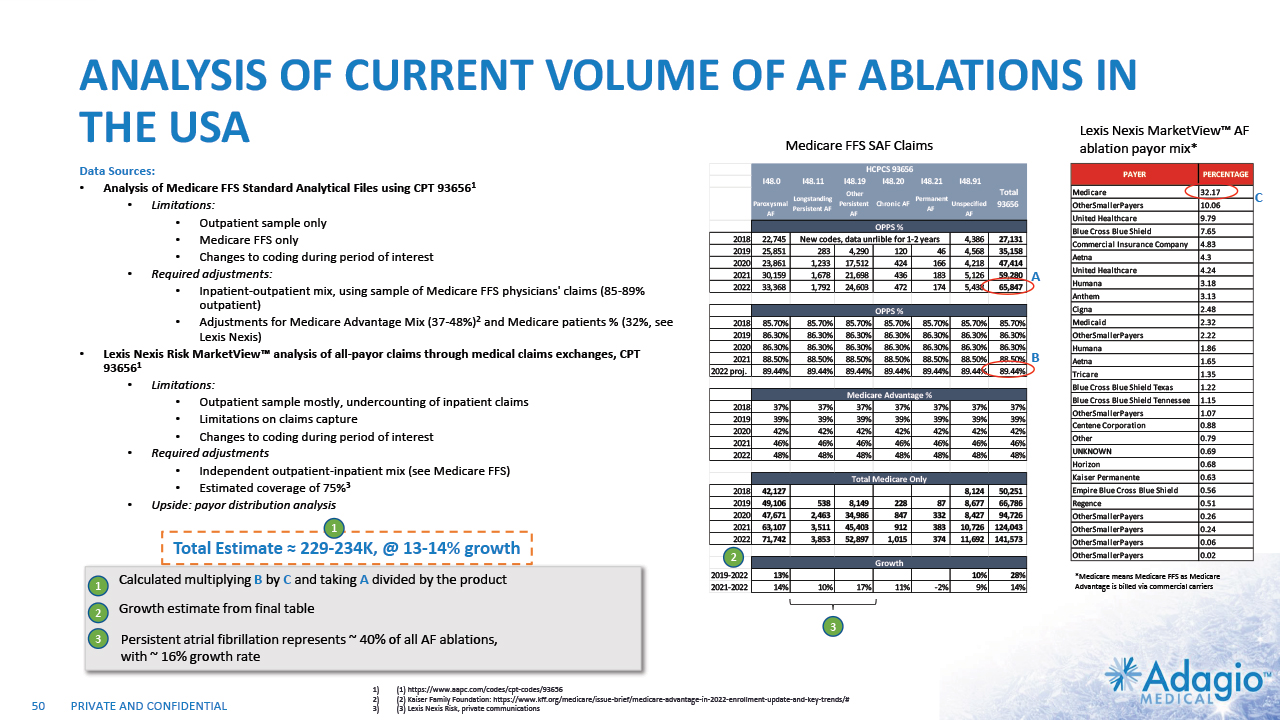

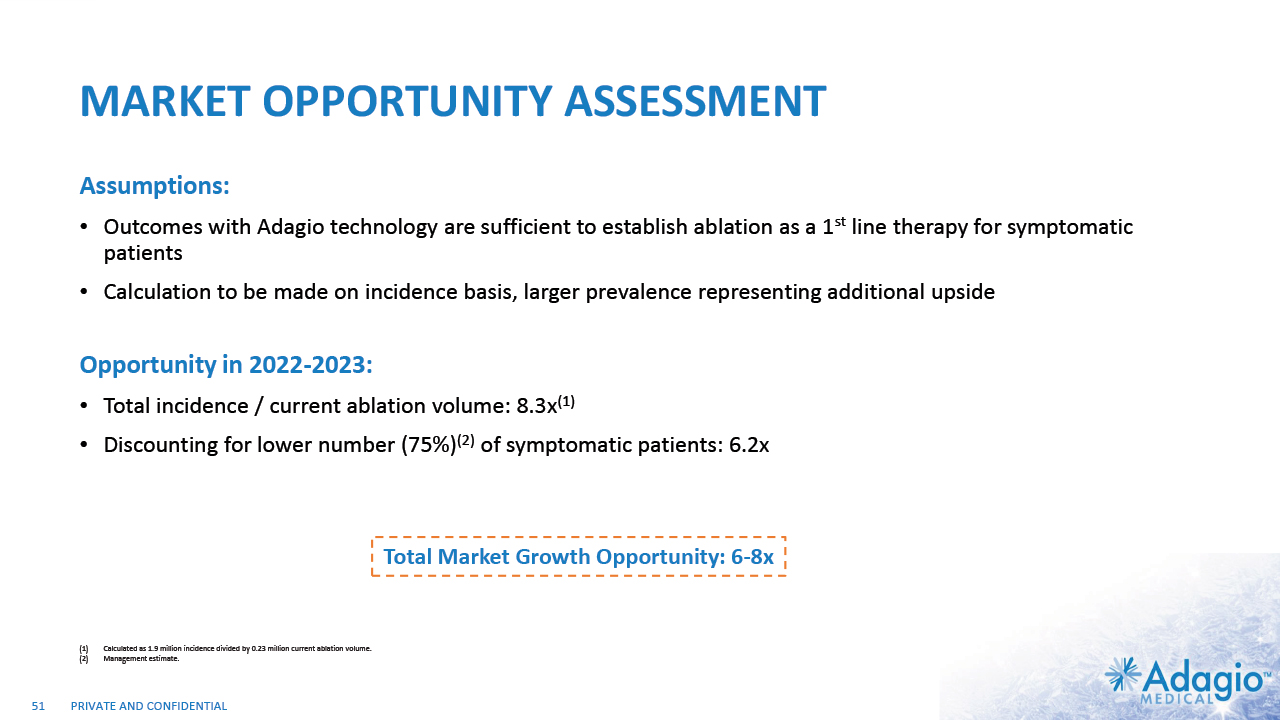

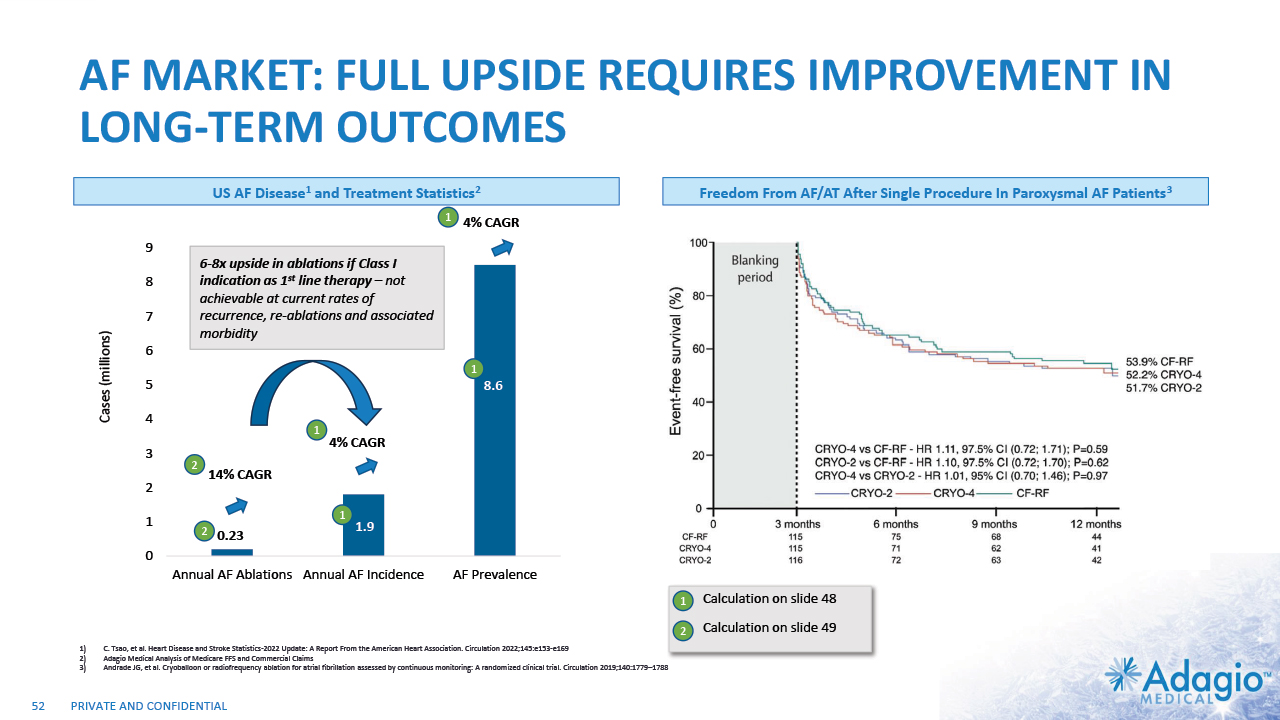

AF MARKET: FULL UPSIDE REQUIRES IMPROVEMENT IN LONG-TERM OUTCOMES Cases (millions) 0.23 1.9 8.6 4% CAGR 4% CAGR 14% CAGR 11 6-8x upside in ablations if Class I indication as 1st line therapy – not achievable at current rates of recurrence, re-ablations and associated morbidity US AF Disease1 and Treatment Statistics2,3 Freedom From AF/AT After Single Procedure In Paroxysmal AF Patients4 Note: Management's analysis of the Medicare FFS and commercial claims data and estimates which are subject to significant uncertainty and may prove to be incorrect. Please see Disclaimer - Management's Estimates on slide 2. C. Tsao, et al. Heart Disease and Stroke Statistics-2022 Update: A Report From the American Heart Association. Circulation 2022;145:e153-e169 Adagio Medical Analysis of Medicare FFS and Commercial Claims The annual AF ablations, annual AF incidence, AF prevalence and market growth are based on management's analysis and projections using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 48-51 which are part of Appendix II - Market Sources & Analysis for further details. Andrade JG, et al. Cryoballoon or radiofrequency ablation for atrial fibrillation assessed by continuous monitoring: A randomized clinical trial. Circulation 2019;140:1779–1788

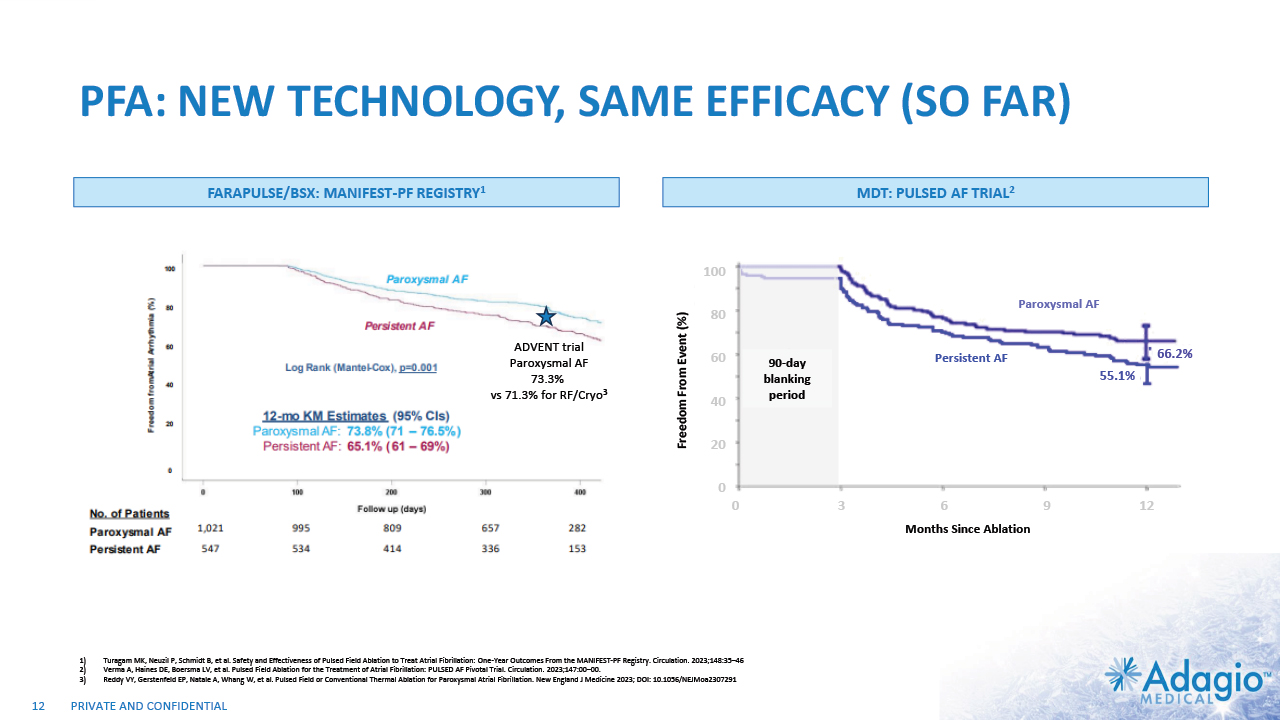

PFA: NEW TECHNOLOGY, SAME EFFICACY (SO FAR) 12 FARAPULSE/BSX: MANIFEST-PF REGISTRY1 MDT: PULSED AF TRIAL2 Turagam MK, Neuzil P, Schmidt B, et al. Safety and Effectiveness of Pulsed Field Ablation to Treat Atrial Fibrillation: One-Year Outcomes From the MANIFEST-PF Registry. Circulation. 2023;148:35–46 Verma A, Haines DE, Boersma LV, et al. Pulsed Field Ablation for the Treatment of Atrial Fibrillation: PULSED AF Pivotal Trial. Circulation. 2023;147:00–00. Reddy VY, Gerstenfeld EP, Natale A, Whang W, et al. Pulsed Field or Conventional Thermal Ablation for Paroxysmal Atrial Fibrillation. New England J Medicine 2023; DOI: 10.1056/NEJMoa2307291 Persistent AF Paroxysmal AF Months Since Ablation Freedom From Event (%) 90-day blanking period 100 80 60 40 20 0 0 3 6 9 12 55.1% 66.2% ADVENT trial Paroxysmal AF 73.3% vs 71.3% for RF/Cryo3

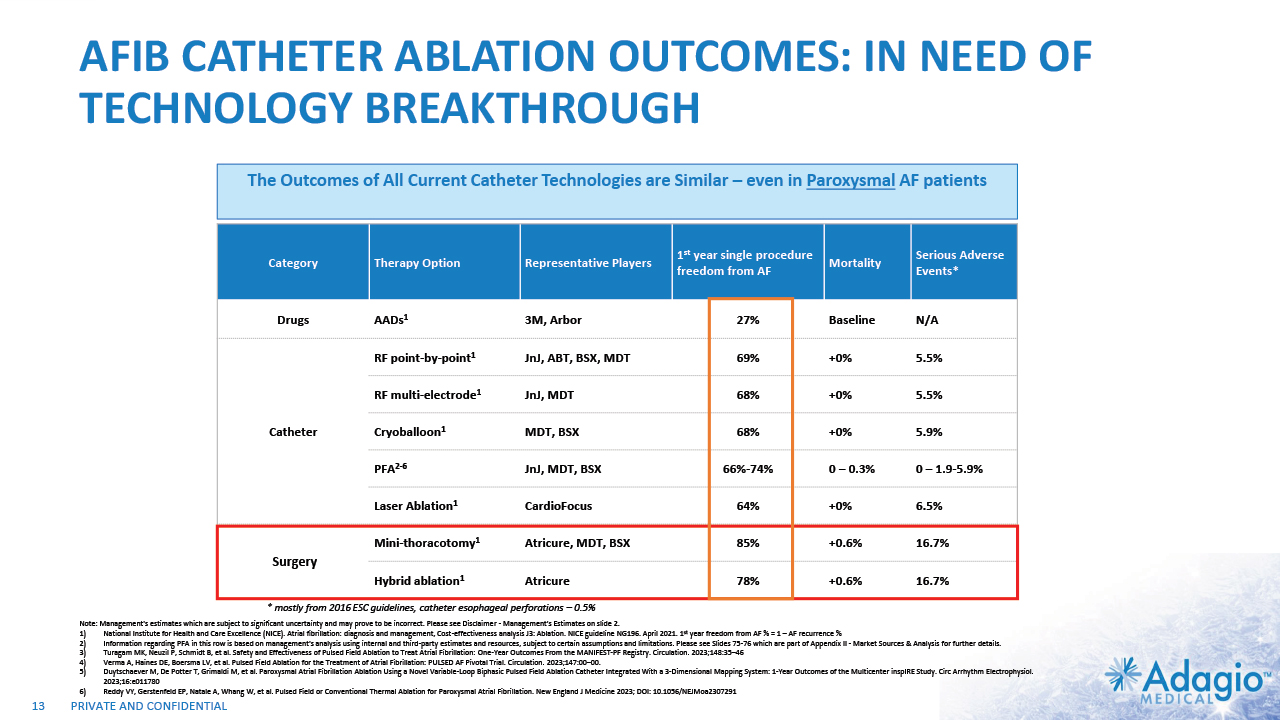

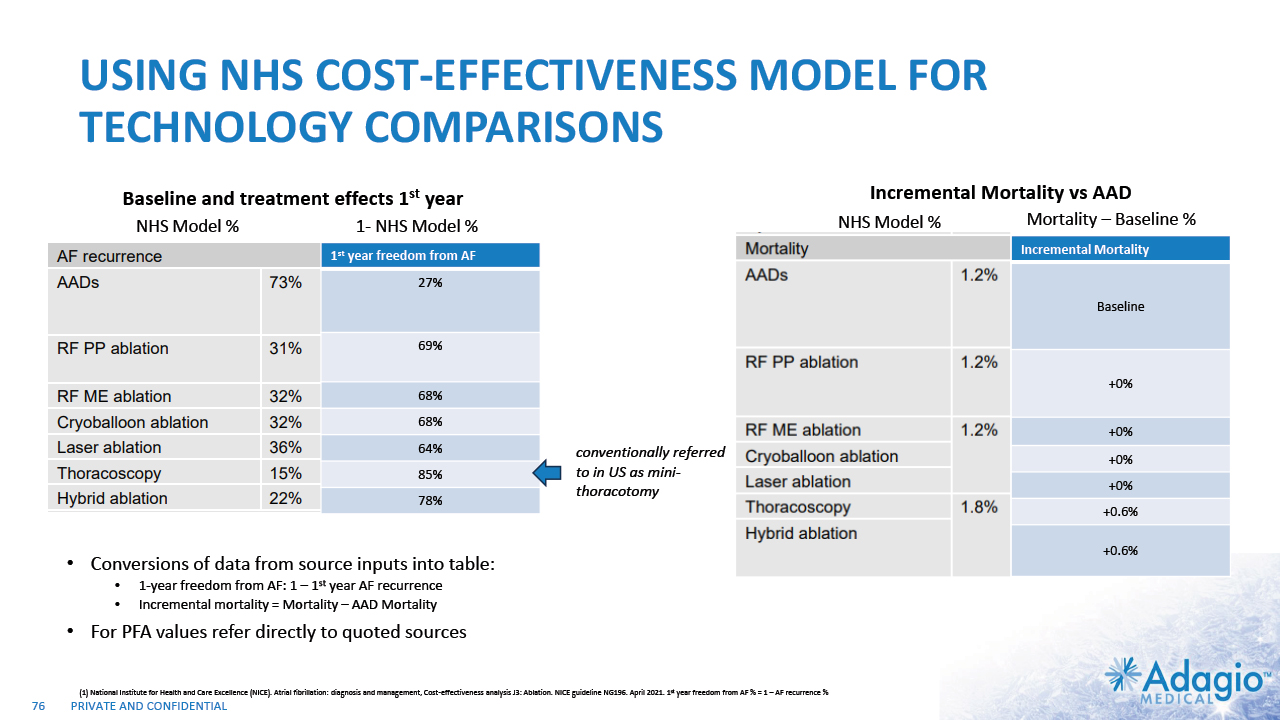

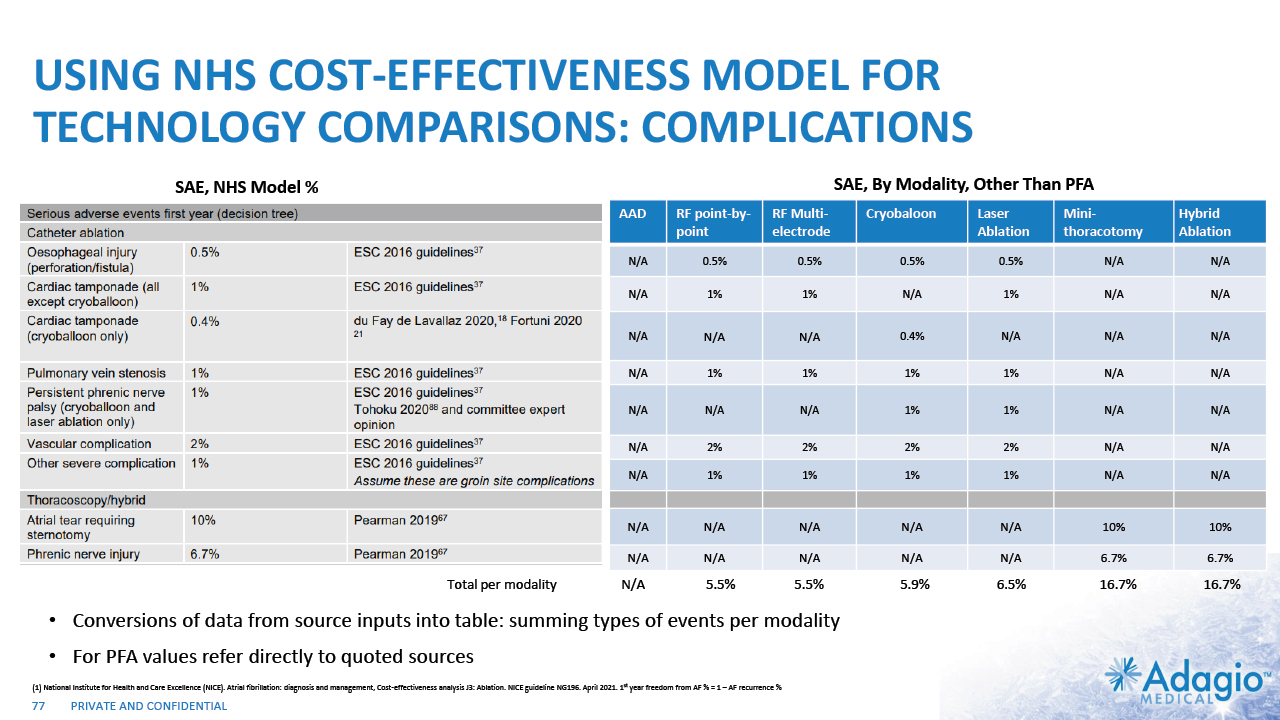

AFIB CATHETER ABLATION OUTCOMES: IN NEED OF TECHNOLOGY BREAKTHROUGH 13 Category Therapy Option Representative Players 1st year single procedure freedom from AF Mortality Serious Adverse Events* Drugs AADs1 3M, Arbor 27% Baseline N/A Catheter RF point-by-point1 JnJ, ABT, BSX, MDT 69% +0% 5.5% Catheter RF multi-electrode1 JnJ, MDT 68% +0% 5.5% Catheter Cryoballoon1 MDT, BSX 68% +0% 5.9% Catheter PFA2-6 JnJ, MDT, BSX 66%-74% 0 – 0.3% 0 – 1.9-5.9% Laser Ablation1 CardioFocus 64% +0% 6.5% Surgery Mini-thoracotomy1 Atricure, MDT, BSX 85% +0.6% 16.7% Open-Heart Surgery Hybrid ablation1 Atricure 78% +0.6% 16.7% * mostly from 2016 ESC guidelines, catheter esophageal perforations – 0.5% Note: Management's estimates which are subject to significant uncertainty and may prove to be incorrect. Please see Disclaimer - Management's Estimates on slide 2. National Institute for Health and Care Excellence (NICE). Atrial fibrillation: diagnosis and management, Cost-effectiveness analysis J3: Ablation. NICE guideline NG196. April 2021. 1st year freedom from AF % = 1 – AF recurrence % Information regarding PFA in this row is based on management's analysis using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 75-76 which are part of Appendix II - Market Sources & Analysis for further details. Turagam MK, Neuzil P, Schmidt B, et al. Safety and Effectiveness of Pulsed Field Ablation to Treat Atrial Fibrillation: One-Year Outcomes From the MANIFEST-PF Registry. Circulation. 2023;148:35–46 Verma A, Haines DE, Boersma LV, et al. Pulsed Field Ablation for the Treatment of Atrial Fibrillation: PULSED AF Pivotal Trial. Circulation. 2023;147:00–00. Duytschaever M, De Potter T, Grimaldi M, et al. Paroxysmal Atrial Fibrillation Ablation Using a Novel Variable-Loop Biphasic Pulsed Field Ablation Catheter Integrated With a 3-Dimensional Mapping System: 1-Year Outcomes of the Multicenter inspIRE Study. Circ Arrhythm Electrophysiol. 2023;16:e011780 Reddy VY, Gerstenfeld EP, Natale A, Whang W, et al. Pulsed Field or Conventional Thermal Ablation for Paroxysmal Atrial Fibrillation. New England J Medicine 2023; DOI: 10.1056/NEJMoa2307291 The Outcomes of All Current Catheter Technologies are Similar – even in Paroxysmal AF patients

VENTRICULAR TACHYCARDIA ABLATIONS MARKET: OPPORTUNITY, DRIVERS AND INHIBITORS

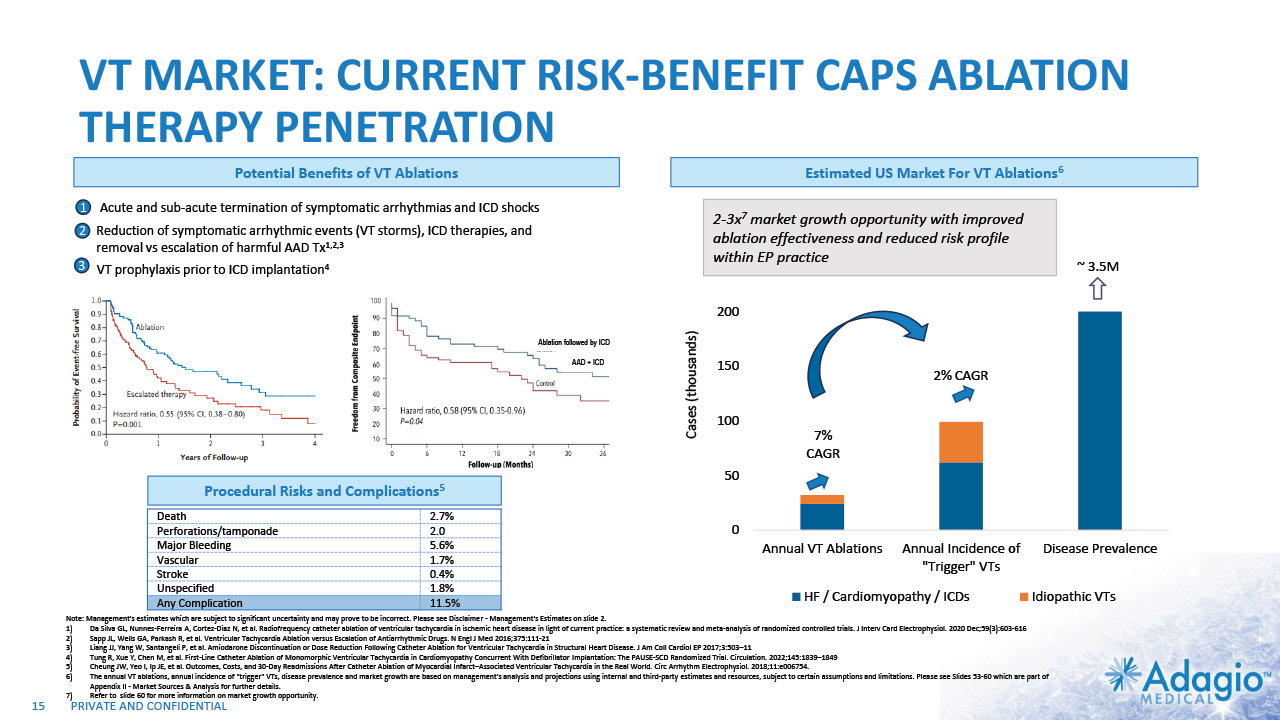

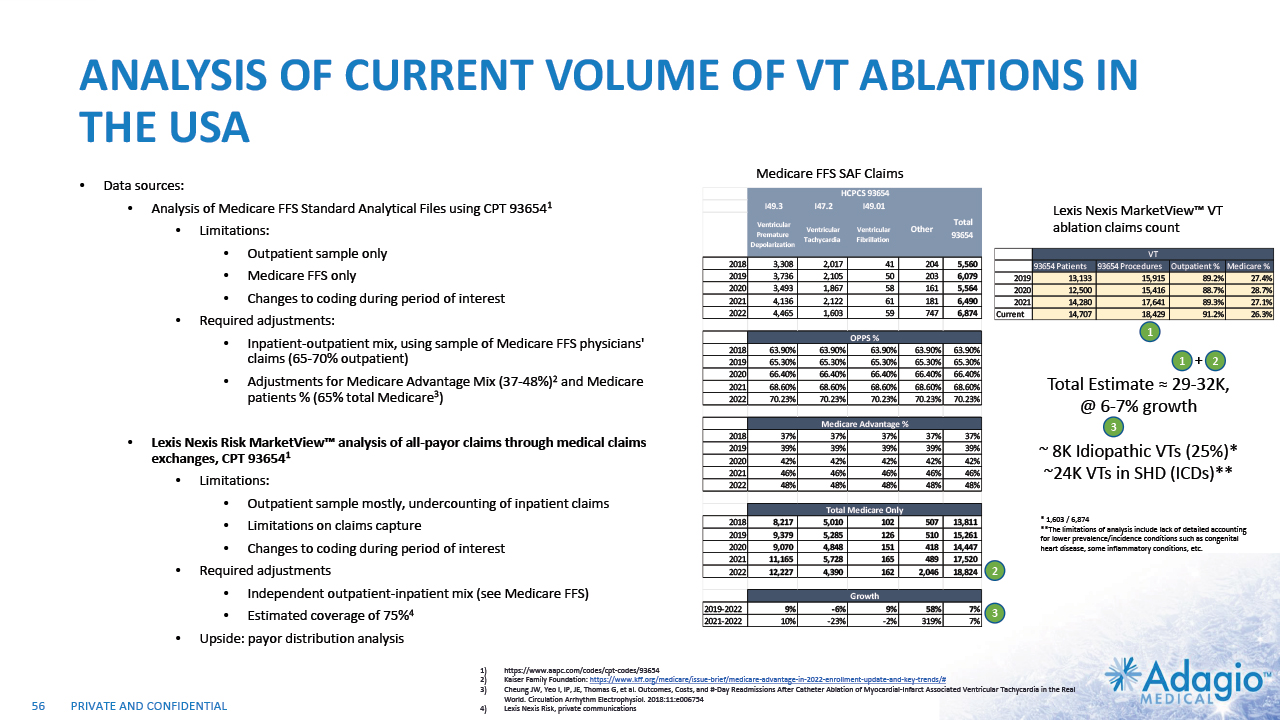

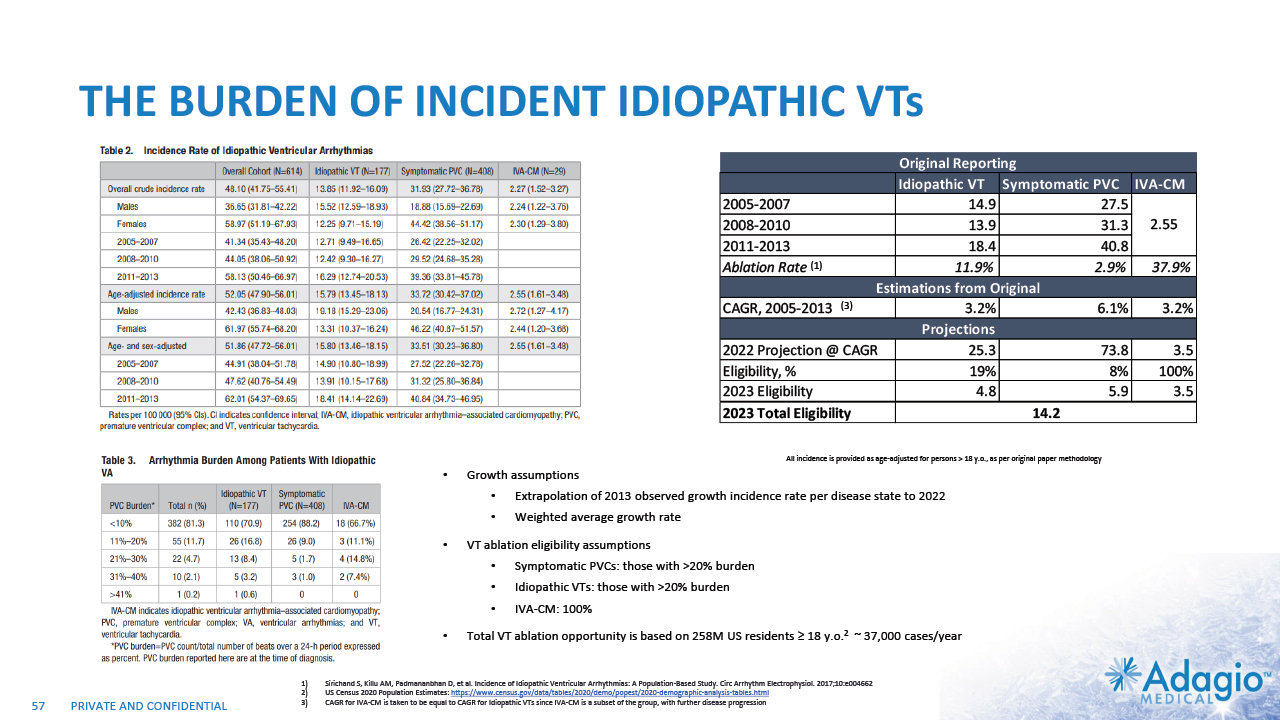

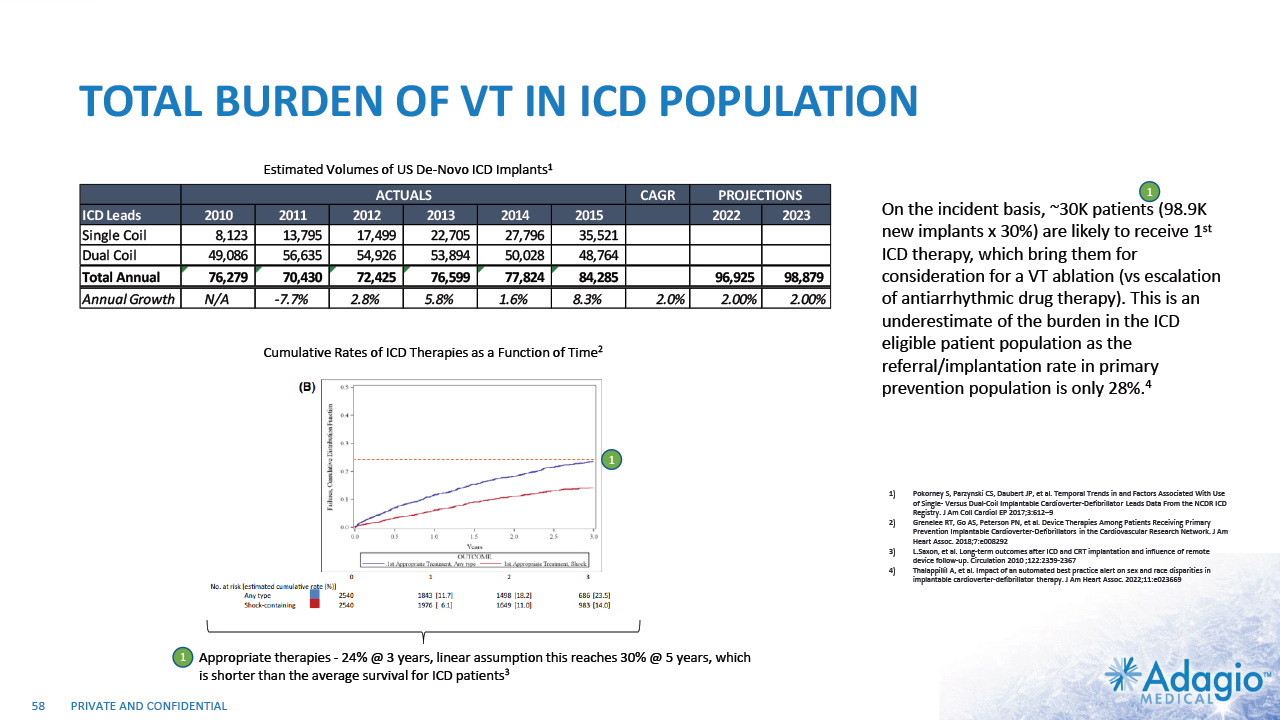

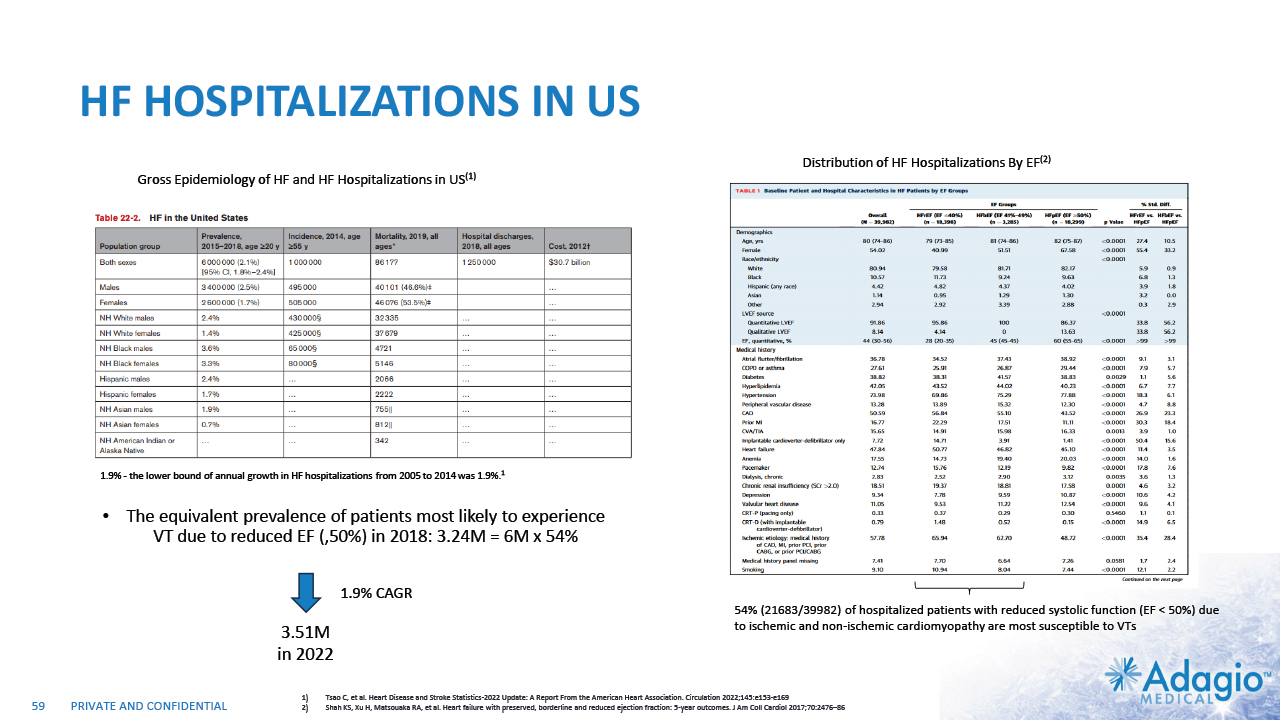

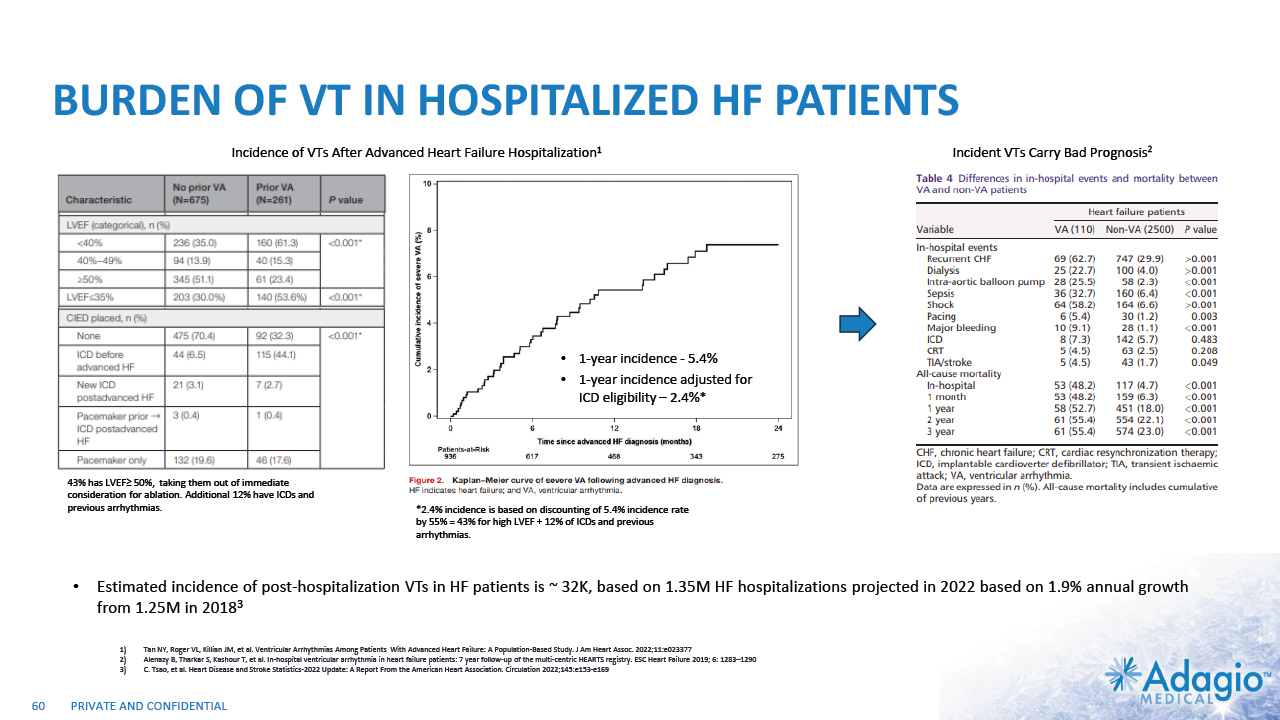

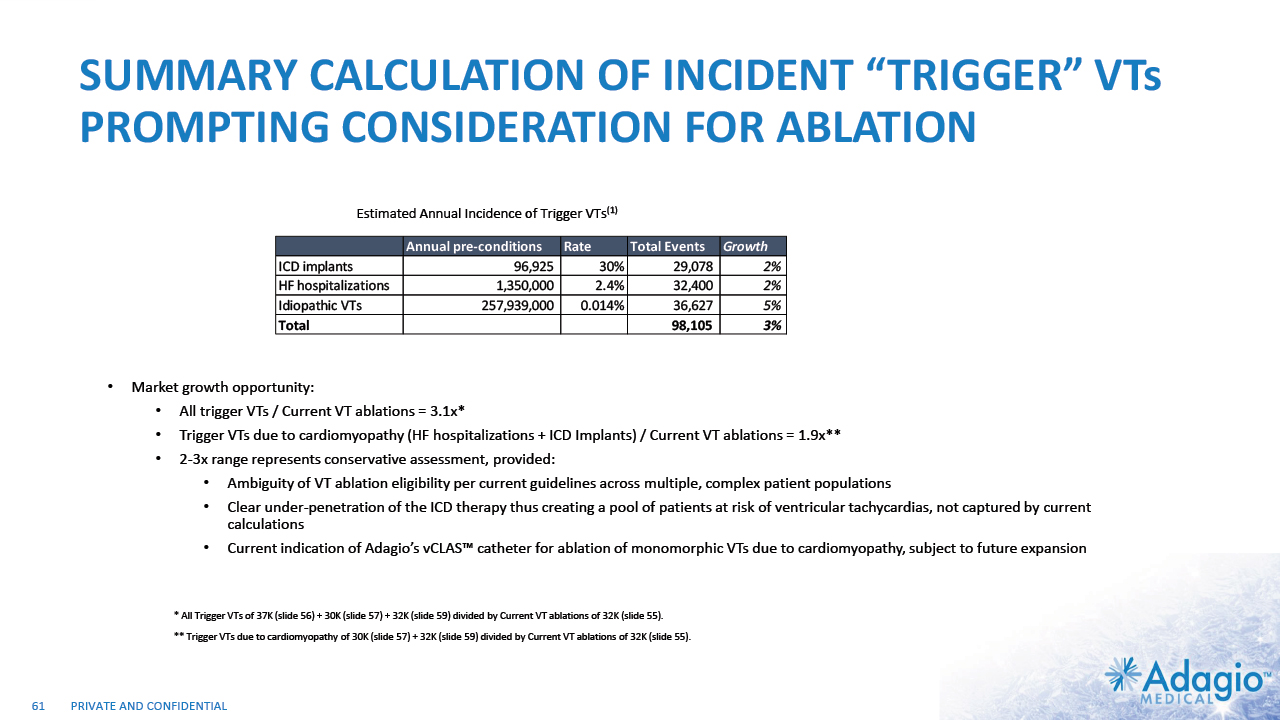

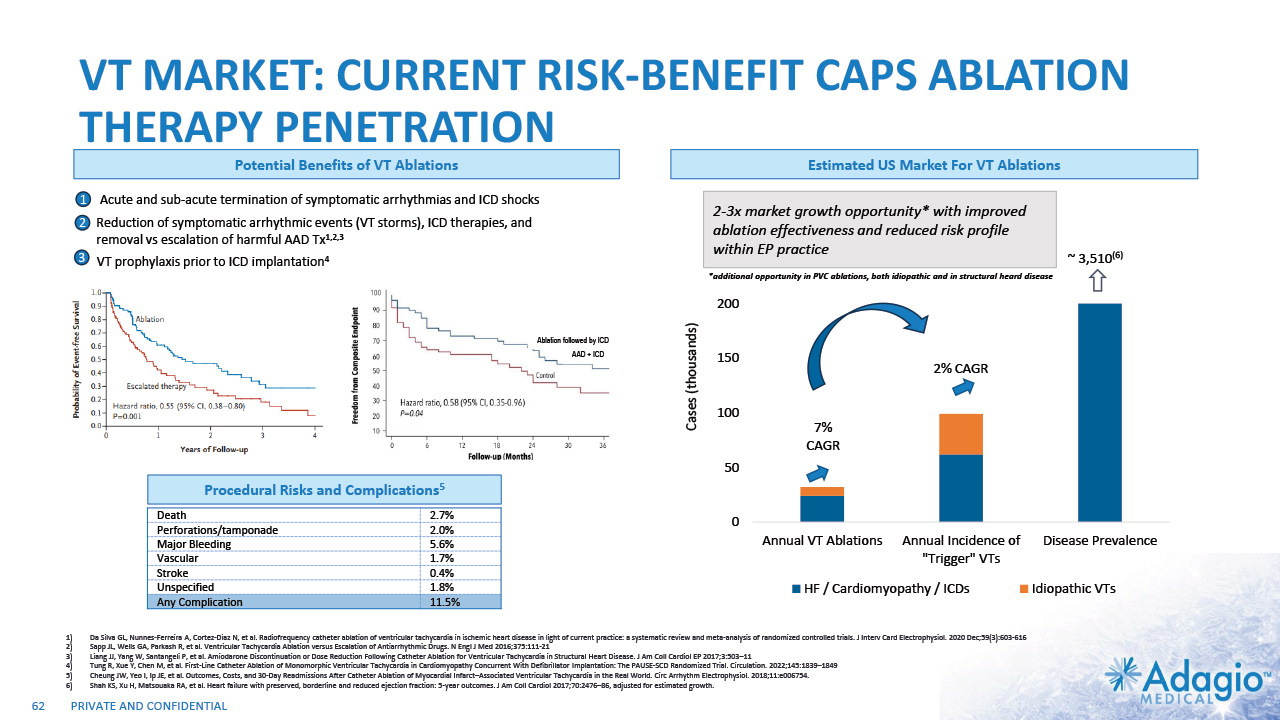

VT MARKET: CURRENT RISK-BENEFIT CAPS ABLATION THERAPY PENETRATION 2% CAGR 7% CAGR 2-3x7 market growth opportunity with improved ablation effectiveness and reduced risk profile within EP practice ~ 3.5M Reduction of symptomatic arrhythmic events (VT storms), ICD therapies, and removal vs escalation of harmful AAD Tx1,2,3 VT prophylaxis prior to ICD implantation4 2 3 1 Acute and sub-acute termination of symptomatic arrhythmias and ICD shocks Ablation followed by ICD AAD + ICD Estimated US Market For VT Ablations6 Potential Benefits of VT Ablations Death 2.7% Perforations/tamponade 2.0 Major Bleeding 5.6% Vascular 1.7% Stroke 0.4% Unspecified 1.8% Any Complication 11.5% Procedural Risks and Complications5 Note: Management's estimates which are subject to significant uncertainty and may prove to be incorrect. Please see Disclaimer - Management's Estimates on slide 2. Da Silva GL, Nunnes-Ferreira A, Cortez-Diaz N, et al. Radiofrequency catheter ablation of ventricular tachycardia in ischemic heart disease in light of current practice: a systematic review and meta-analysis of randomized controlled trials. J Interv Card Electrophysiol. 2020 Dec;59(3):603-616 Sapp JL, Wells GA, Parkash R, et al. Ventricular Tachycardia Ablation versus Escalation of Antiarrhythmic Drugs. N Engl J Med 2016;375:111-21 Liang JJ, Yang W, Santangeli P, et al. Amiodarone Discontinuation or Dose Reduction Following Catheter Ablation for Ventricular Tachycardia in Structural Heart Disease. J Am Coll Cardiol EP 2017;3:503–11 Tung R, Xue Y, Chen M, et al. First-Line Catheter Ablation of Monomorphic Ventricular Tachycardia in Cardiomyopathy Concurrent With Defibrillator Implantation: The PAUSE-SCD Randomized Trial. Circulation. 2022;145:1839–1849 Cheung JW, Yeo I, Ip JE, et al. Outcomes, Costs, and 30-Day Readmissions After Catheter Ablation of Myocardial Infarct–Associated Ventricular Tachycardia in the Real World. Circ Arrhythm Electrophysiol. 2018;11:e006754. The annual VT ablations, annual incidence of "trigger" VTs, disease prevalence and market growth are based on management's analysis and projections using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 53-60 which are part of Appendix II - Market Sources & Analysis for further details. Refer to slide 60 for more information on market growth opportunity. 15

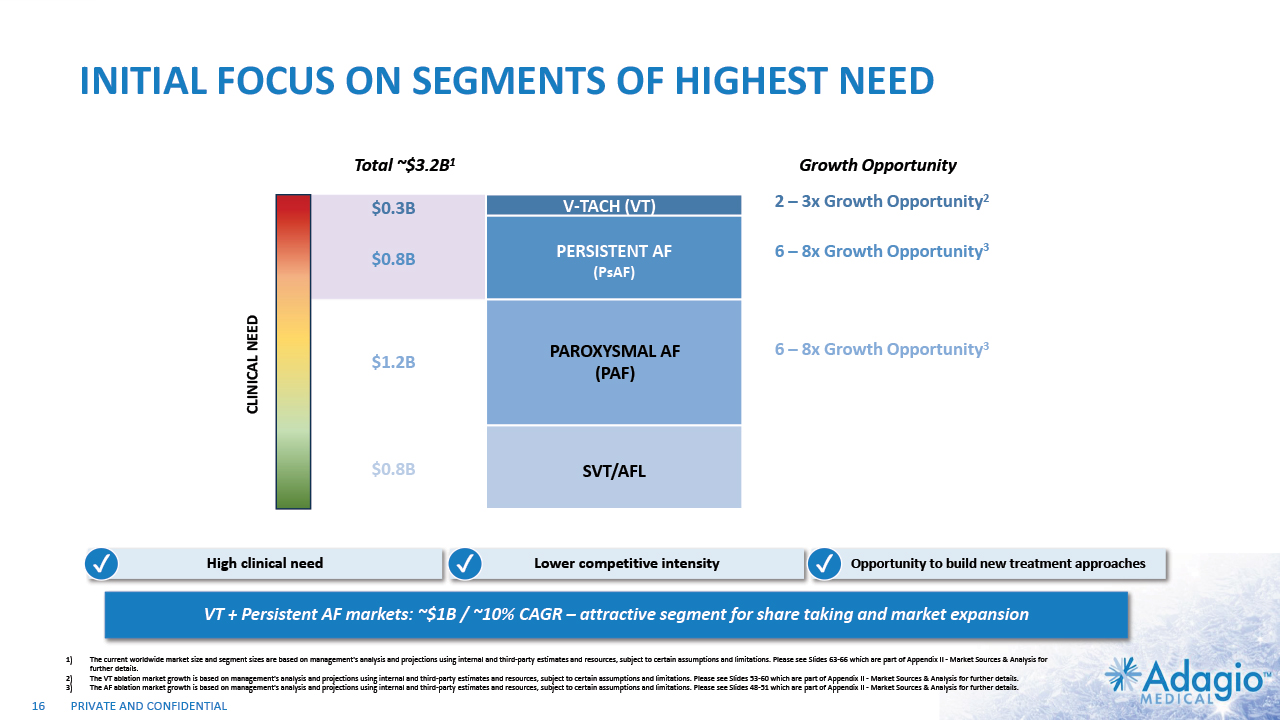

INITIAL FOCUS ON SEGMENTS OF HIGHEST NEED VT + Persistent AF markets: ~$1B / ~10% CAGR – attractive segment for share taking and market expansion PAROXYSMAL AF (PAF) SVT/AFL PERSISTENT AF (PsAF) V-TACH (VT) Highly effective and safe Low clinical need Strong indications Growth in line with population $0.8B $0.8B $1.2B $0.3B CLINICAL NEED Total ~$3.2B1 2 – 3x Growth Opportunity2 High clinical need TBU Remove bullets and incorporate growth 6 – 8x Growth Opportunity3 6 – 8x Growth Opportunity3 Growth Opportunity Lower competitive intensity Opportunity to build new treatment approaches ✔ ✔ ✔ 16 The current worldwide market size and segment sizes are based on management's analysis and projections using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 63-66 which are part of Appendix II - Market Sources & Analysis for further details. The VT ablation market growth is based on management's analysis and projections using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 53-60 which are part of Appendix II - Market Sources & Analysis for further details. The AF ablation market growth is based on management's analysis and projections using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 48-51 which are part of Appendix II - Market Sources & Analysis for further details.

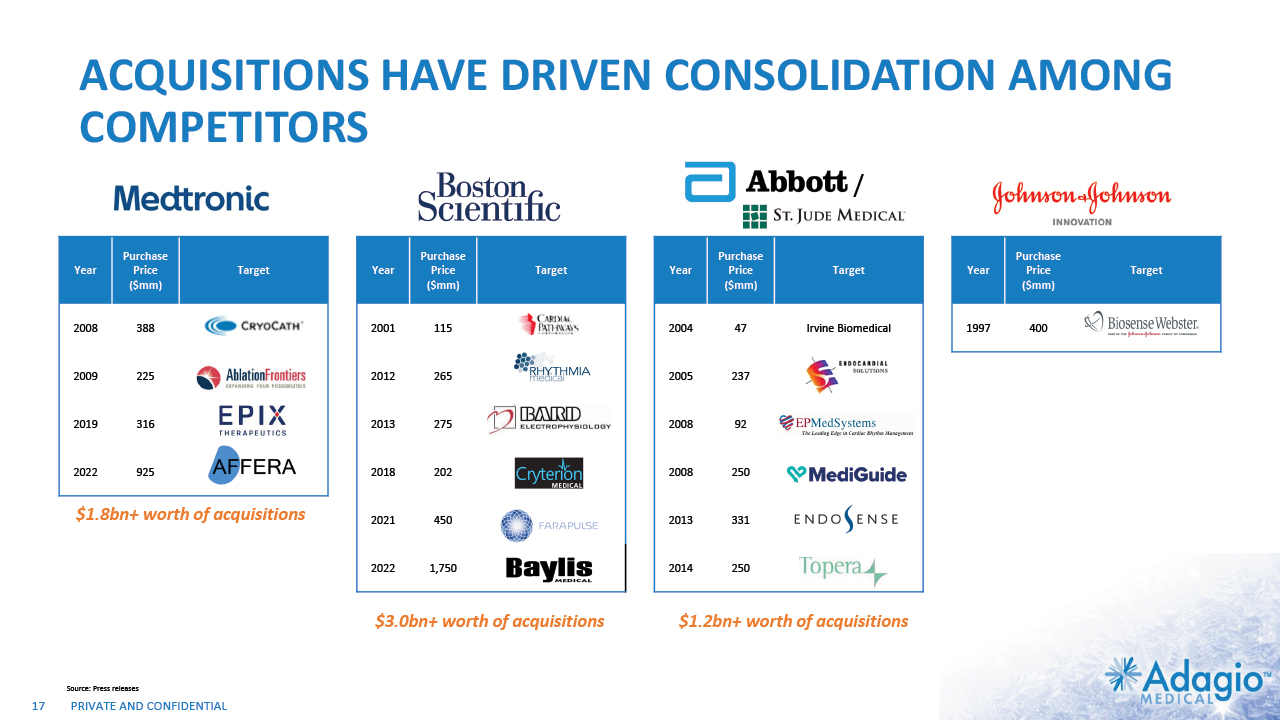

Year Purchase Price ($mm) Target Year Purchase Price ($mm) Target Year Purchase Price ($mm) Target Year Purchase Price ($mm) Target 2008 388 2001 115 2004 47 Irvine Biomedical 1997 400 2009 225 2012 265 2005 237 2019 316 2013 275 2008 92 2022 925 2018 202 2008 250 2021 450 2013 331 2022 1,750 2014 250 ACQUISITIONS HAVE DRIVEN CONSOLIDATION AMONG COMPETITORS 17 / Source: Press releases $1.8bn+ worth of acquisitions $3.0bn+ worth of acquisitions $1.2bn+ worth of acquisitions

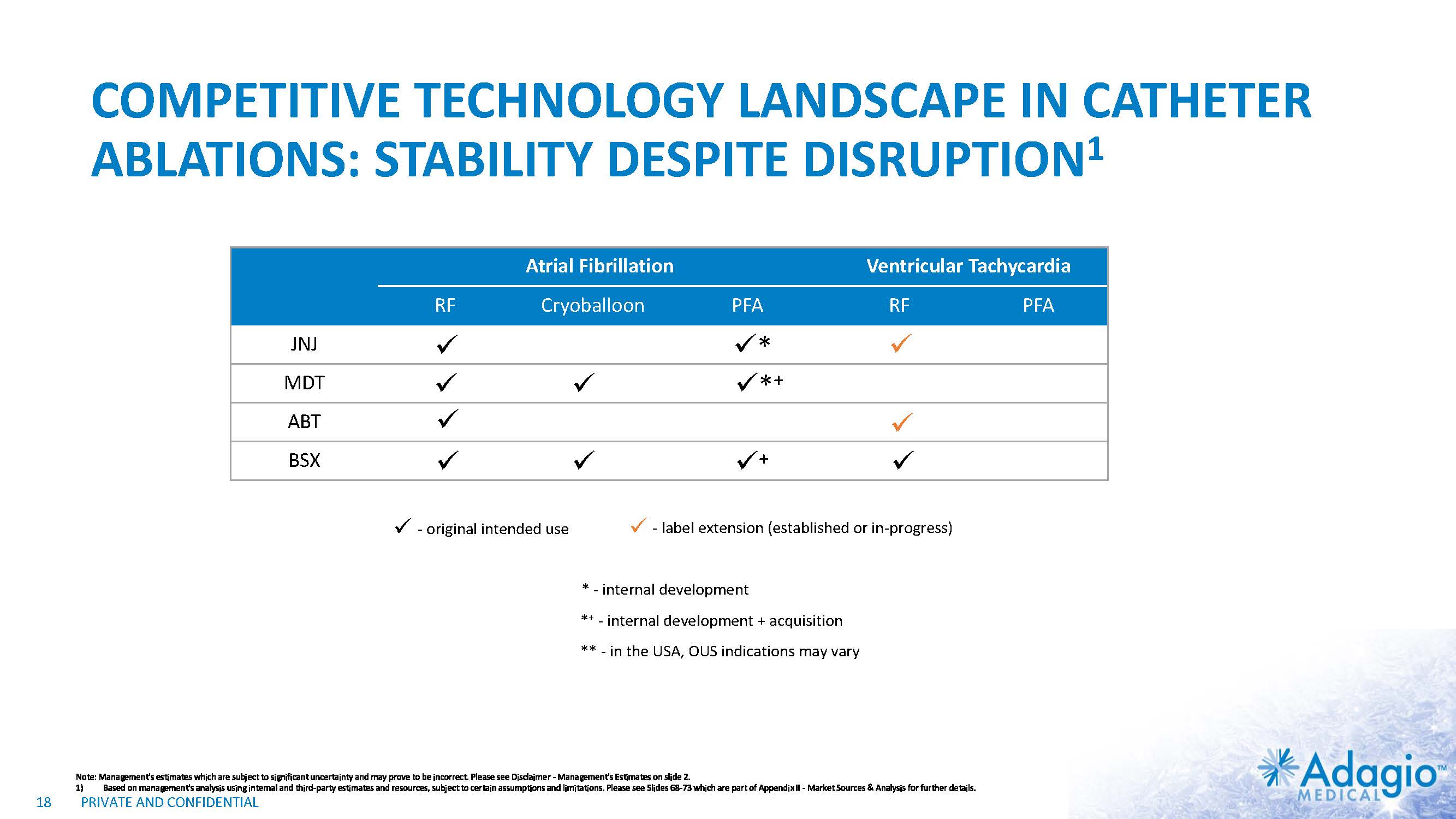

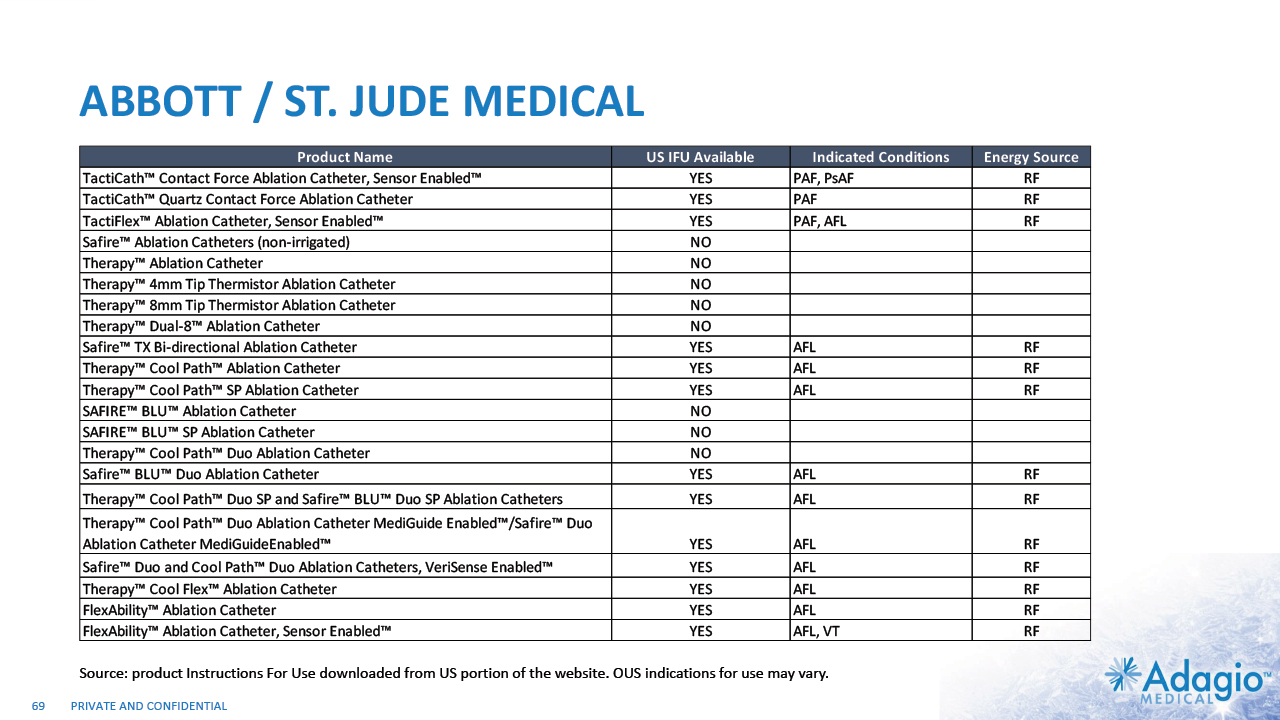

COMPETITIVE TECHNOLOGY LANDSCAPE IN CATHETER ABLATIONS: STABILITY DESPITE DISRUPTION1 18 Atrial Fibrillation Ventricular Tachycardia RF Cryoballoon PFA RF PFA JNJ MDT ABT BSX * - original intended use - label extension (established or in-progress) *+ + * - internal development ** - in the USA, OUS indications may vary *+ - internal development + acquisition Note: Management's estimates which are subject to significant uncertainty and may prove to be incorrect. Please see Disclaimer - Management's Estimates on slide 2. Based on management's analysis using internal and third-party estimates and resources, subject to certain assumptions and limitations. Please see Slides 68-73 which are part of Appendix II - Market Sources & Analysis for further details.

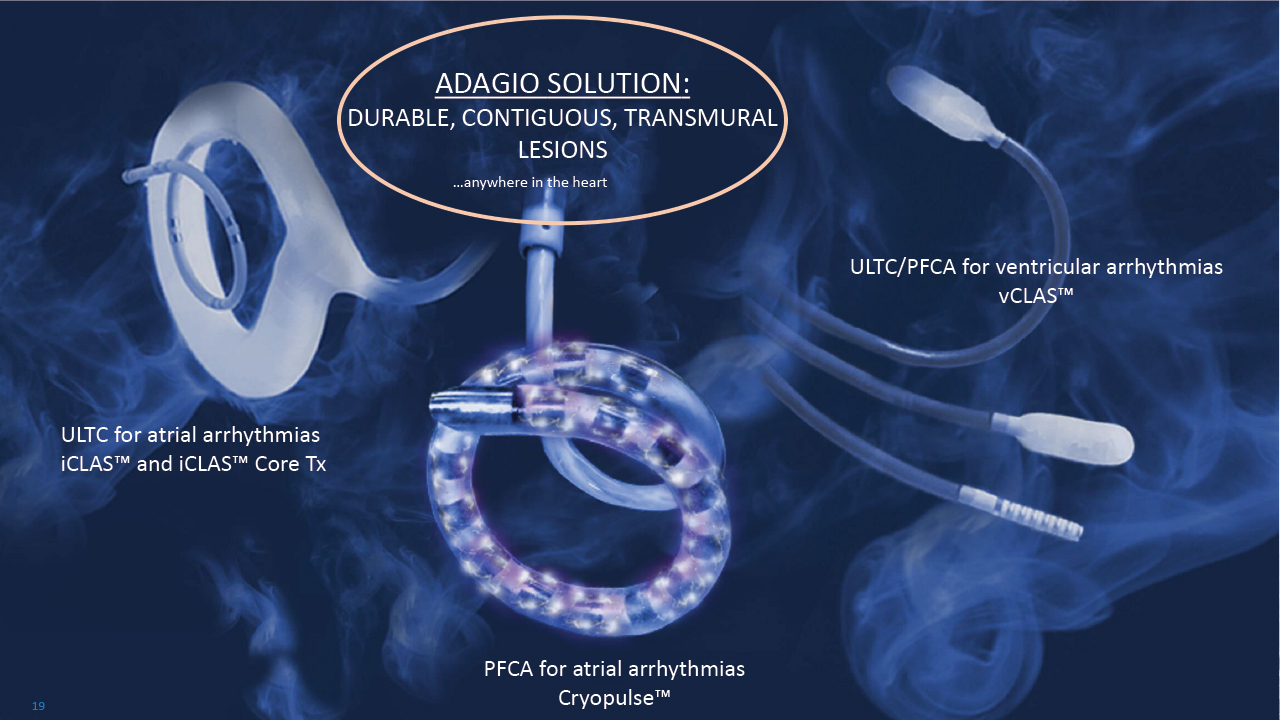

ADAGIO SOLUTION: DURABLE, CONTIGUOUS, TRANSMURAL LESIONS …anywhere in the heart PFCA for atrial arrhythmias Cryopulse™ ULTC for atrial arrhythmias iCLAS™ and iCLAS™ Core Tx ULTC/PFCA for ventricular arrhythmias vCLAS™ 19

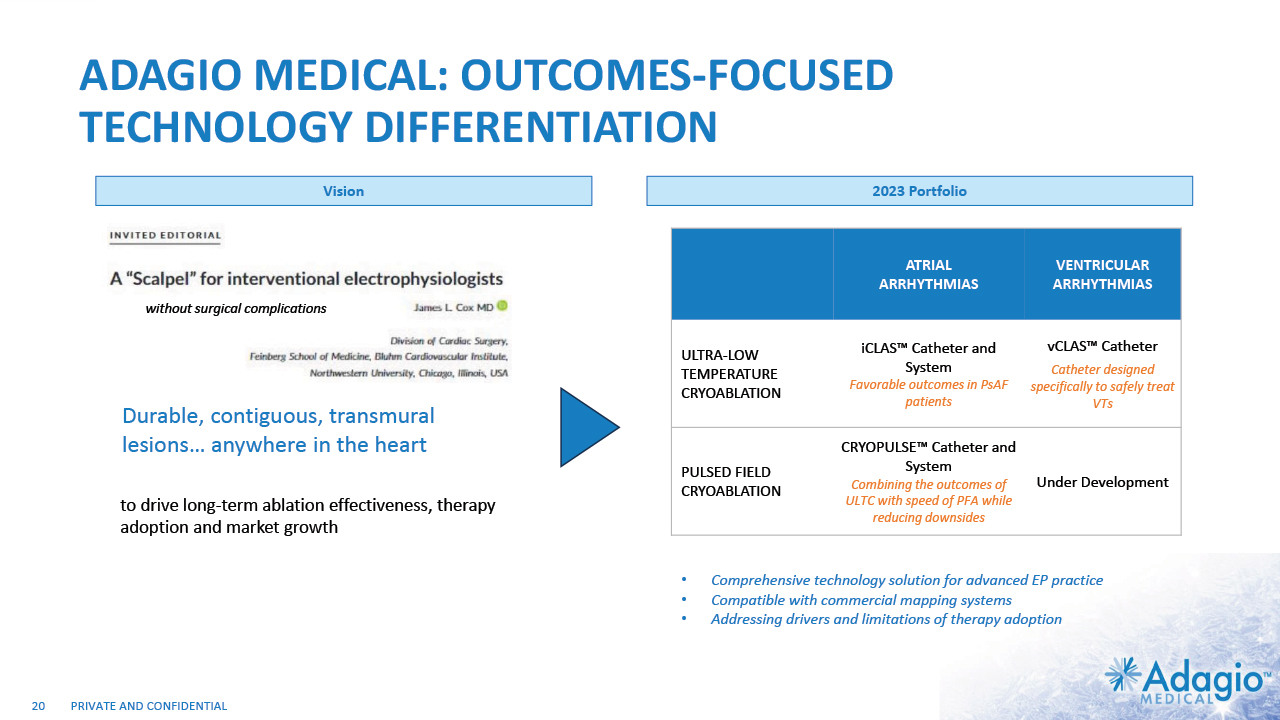

ADAGIO MEDICAL: OUTCOMES-FOCUSEDTECHNOLOGY DIFFERENTIATION 20 Durable, contiguous, transmural lesions… anywhere in the heart Comprehensive technology solution for advanced EP practice Compatible with commercial mapping systems Addressing drivers and limitations of therapy adoption to drive long-term ablation effectiveness, therapy adoption and market growth ATRIAL ARRHYTHMIAS VENTRICULAR ARRHYTHMIAS ULTRA-LOW TEMPERATURE CRYOABLATION iCLAS™ Catheter and System Favorable outcomes in PsAF patients vCLAS™ Catheter Catheter designed specifically to safely treat VTs PULSED FIELD CRYOABLATION CRYOPULSE™ Catheter and System Combining the outcomes of ULTC with speed of PFA while reducing downsides Under Development without surgical complications Vision 2023 Portfolio

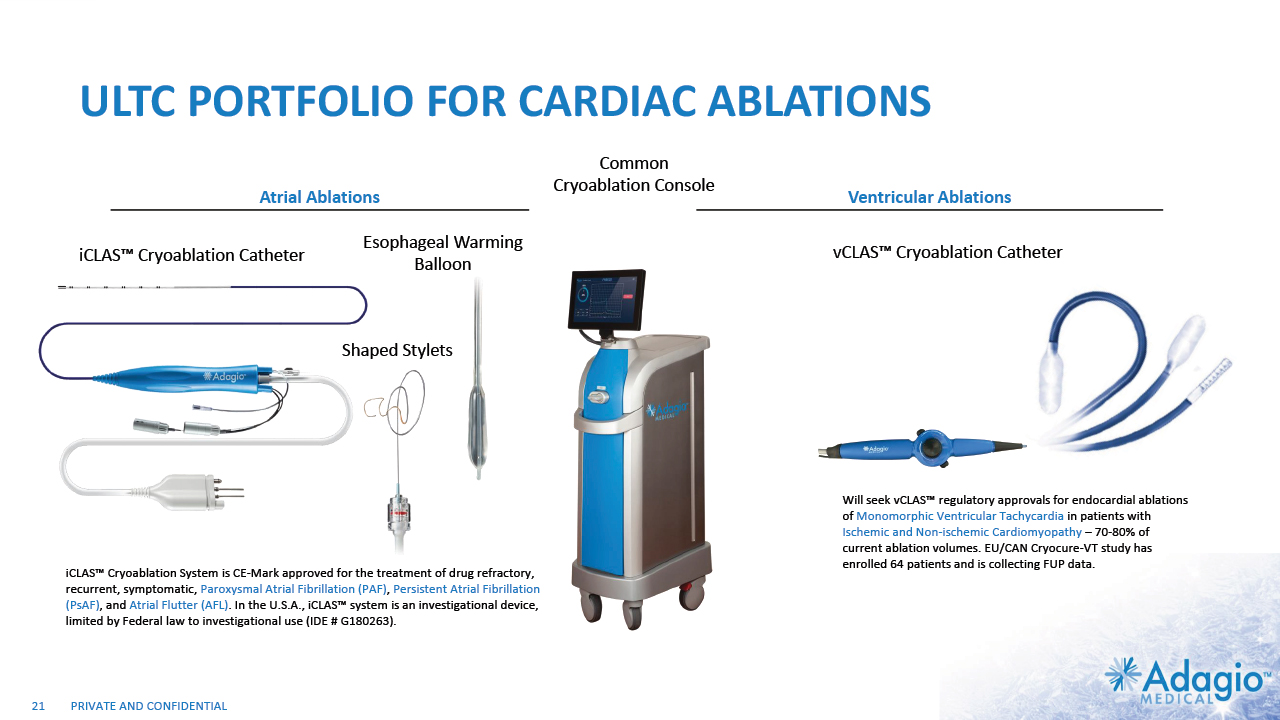

ULTC PORTFOLIO FOR CARDIAC ABLATIONS 21 Shaped Stylets Esophageal Warming Balloon iCLAS™ Cryoablation System is CE-Mark approved for the treatment of drug refractory, recurrent, symptomatic, Paroxysmal Atrial Fibrillation (PAF), Persistent Atrial Fibrillation (PsAF), and Atrial Flutter (AFL). In the U.S.A., iCLAS™ system is an investigational device, limited by Federal law to investigational use (IDE # G180263). iCLAS™ Cryoablation Catheter vCLAS™ Cryoablation Catheter Will seek vCLAS™ regulatory approvals for endocardial ablations of Monomorphic Ventricular Tachycardia in patients with Ischemic and Non-ischemic Cardiomyopathy – 70-80% of current ablation volumes. EU/CAN Cryocure-VT study has enrolled 64 patients and is collecting FUP data. Atrial Ablations Ventricular Ablations Common Cryoablation Console

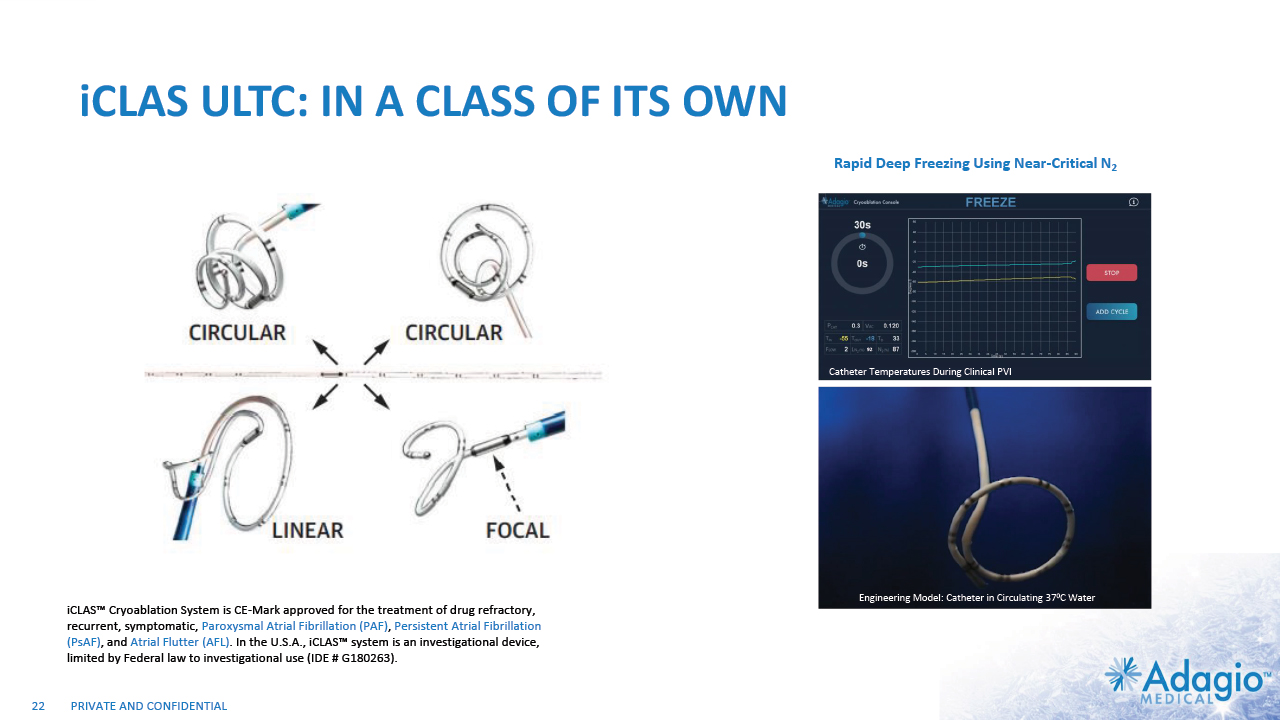

iCLAS ULTC: IN A CLASS OF ITS OWN iCLAS™ Cryoablation System is CE-Mark approved for the treatment of drug refractory, recurrent, symptomatic, Paroxysmal Atrial Fibrillation (PAF), Persistent Atrial Fibrillation (PsAF), and Atrial Flutter (AFL). In the U.S.A., iCLAS™ system is an investigational device, limited by Federal law to investigational use (IDE # G180263). 22 92 Catheter Temperatures During Clinical PVI Engineering Model: Catheter in Circulating 370C Water Rapid Deep Freezing Using Near-Critical N2

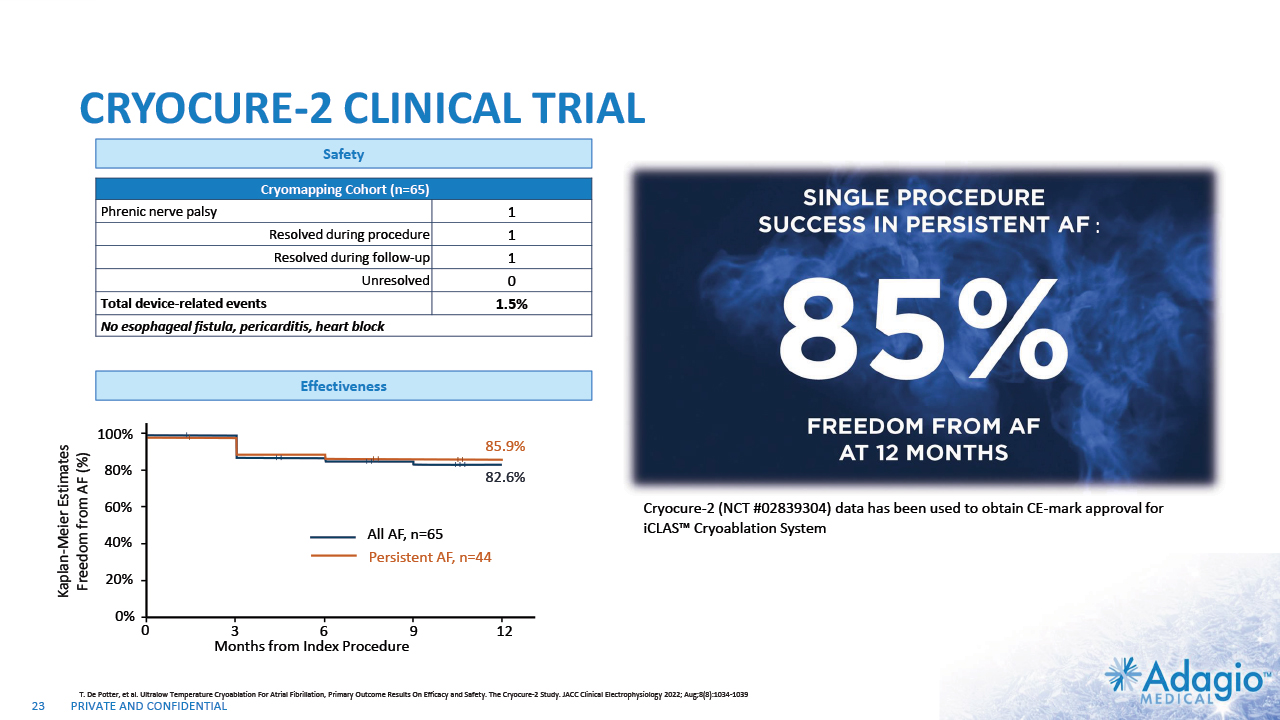

CRYOCURE-2 CLINICAL TRIAL Cryomapping Cohort (n=65) Cryomapping Cohort Phrenic nerve palsy 1 Resolved during procedure 1 Resolved during follow-up 1 Unresolved 0 Total device-related events 1.5% No esophageal fistula, pericarditis, heart block 1.5% T. De Potter, et al. Ultralow Temperature Cryoablation For Atrial Fibrillation, Primary Outcome Results On Efficacy and Safety. The Cryocure-2 Study. JACC Clinical Electrophysiology 2022; Aug;8(8):1034-1039 Cryocure-2 (NCT #02839304) data has been used to obtain CE-mark approval for iCLAS™ Cryoablation System CRYOCURE-2 NCT #02839304 : 82.6% 85.9% 0 All AF, n=65 3 6 9 12 20% 40% 60% 80% 100% Kaplan-Meier Estimates Freedom from AF (%) 0% Months from Index Procedure Persistent AF, n=44 84% (37/44) of PsAF patients had PVI+ ablations 86% (18/21) of Paroxysmal AF patients had PVI Only ablations 23 Safety Effectiveness

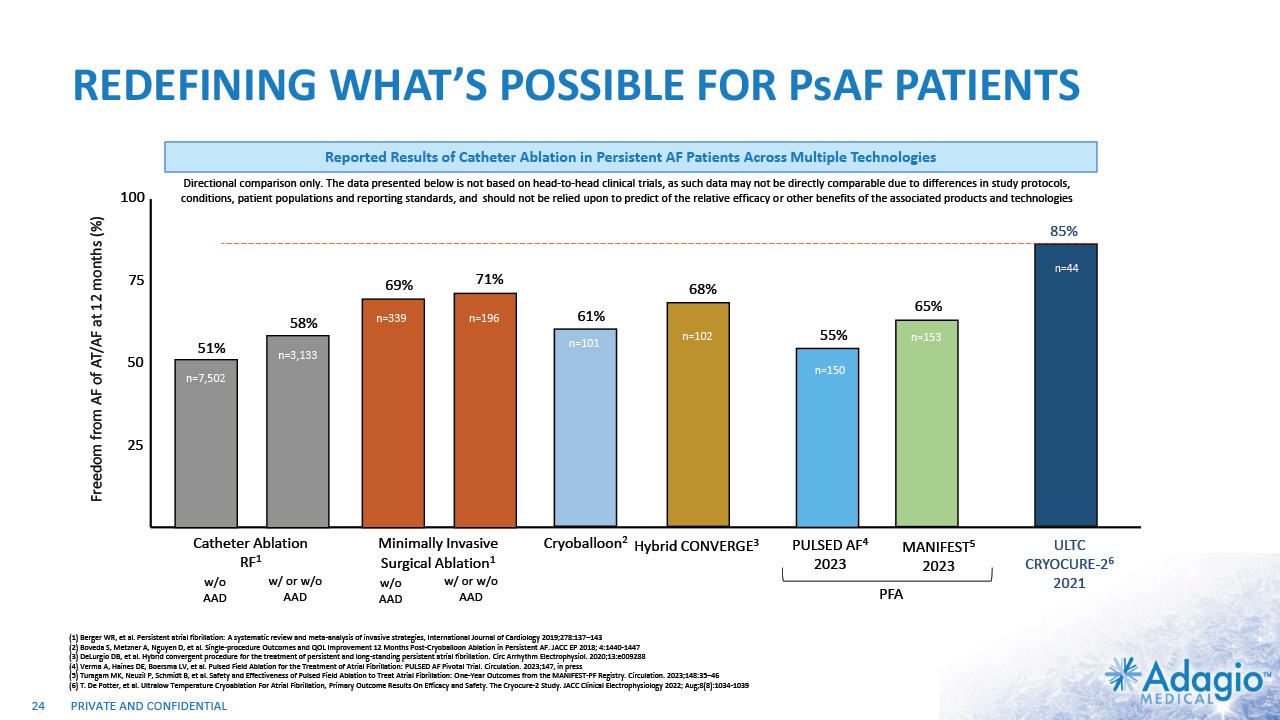

REDEFINING WHAT’S POSSIBLE FOR PsAF PATIENTS 25 50 75 100 Freedom from AF of AT/AF at 12 months (%) 68% n=102 Hybrid CONVERGE3 n=102 n=102 MANIFEST5 2023 85% n=44 ULTC CRYOCURE-26 2021 51% 58% 69% 71% n=196 n=3,133 n=339 n=7,502 Catheter Ablation RF1 Minimally Invasive Surgical Ablation1 w/o AAD w/ or w/o AAD w/o AAD w/ or w/o AAD 65% PULSED AF4 2023 55% n=150 n=44 n=153 PFA n=101 Cryoballoon2 61% Reported Results of Catheter Ablation in Persistent AF Patients Across Multiple Technologies 24 (1) Berger WR, et al. Persistent atrial fibrillation: A systematic review and meta-analysis of invasive strategies, International Journal of Cardiology 2019;278:137–143 (2) Boveda S, Metzner A, Nguyen D, et al. Single-procedure Outcomes and QOL Improvement 12 Months Post-Cryoballoon Ablation in Persistent AF. JACC EP 2018; 4:1440-1447 (3) DeLurgio DB, et al. Hybrid convergent procedure for the treatment of persistent and long-standing persistent atrial fibrillation. Circ Arrhythm Electrophysiol. 2020;13:e009288 (4) Verma A, Haines DE, Boersma LV, et al. Pulsed Field Ablation for the Treatment of Atrial Fibrillation: PULSED AF Pivotal Trial. Circulation. 2023;147, in press (5) Turagam MK, Neuzil P, Schmidt B, et al. Safety and Effectiveness of Pulsed Field Ablation to Treat Atrial Fibrillation: One-Year Outcomes from the MANIFEST-PF Registry. Circulation. 2023;148:35–46 (6) T. De Potter, et al. Ultralow Temperature Cryoablation For Atrial Fibrillation, Primary Outcome Results On Efficacy and Safety. The Cryocure-2 Study. JACC Clinical Electrophysiology 2022; Aug;8(8):1034-1039 Directional comparison only. The data presented below is not based on head-to-head clinical trials, as such data may not be directly comparable due to differences in study protocols, conditions, patient populations and reporting standards, and should not be relied upon to predict of the relative efficacy or other benefits of the associated products and technologies

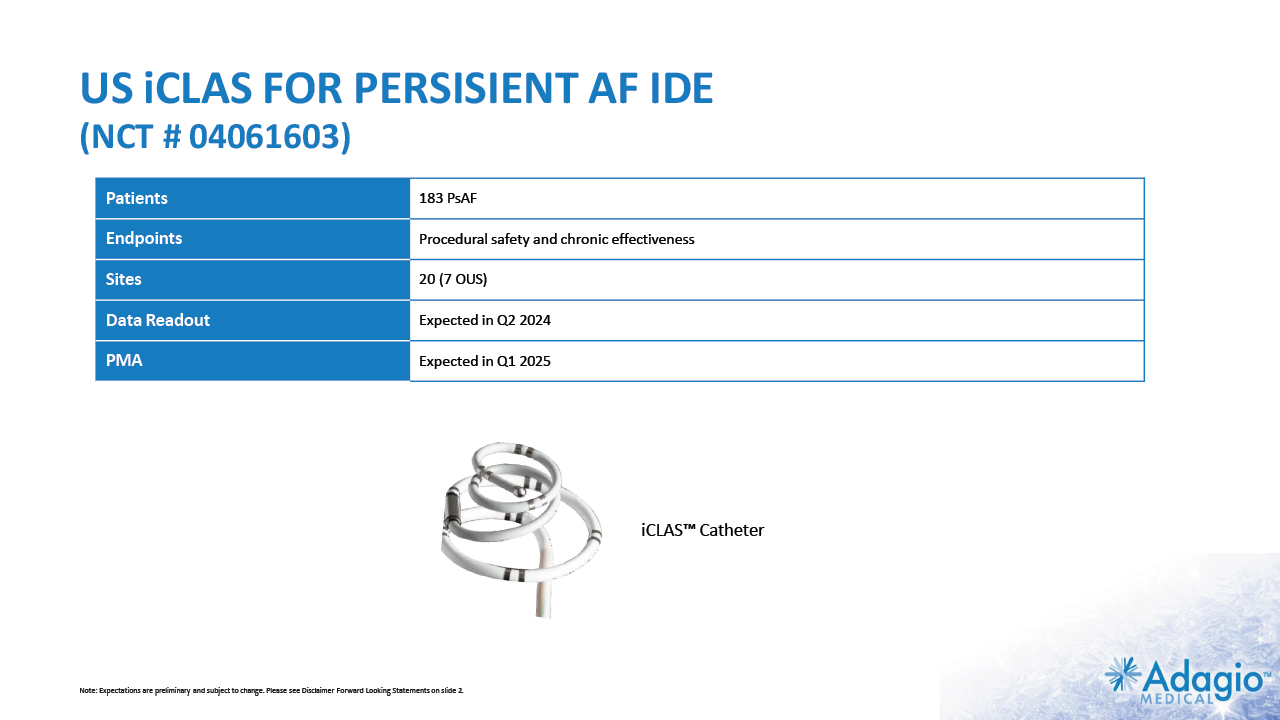

US iCLAS FOR PERSISIENT AF IDE (NCT # 04061603) iCLAS™ Catheter Patients 183 PsAF Endpoints Procedural safety and chronic effectiveness Sites 20 (7 OUS) Data Readout Expected in Q2 2024 PMA Expected in Q1 2025 Note: Expectations are preliminary and subject to change. Please see Disclaimer Forward Looking Statements on slide 2.

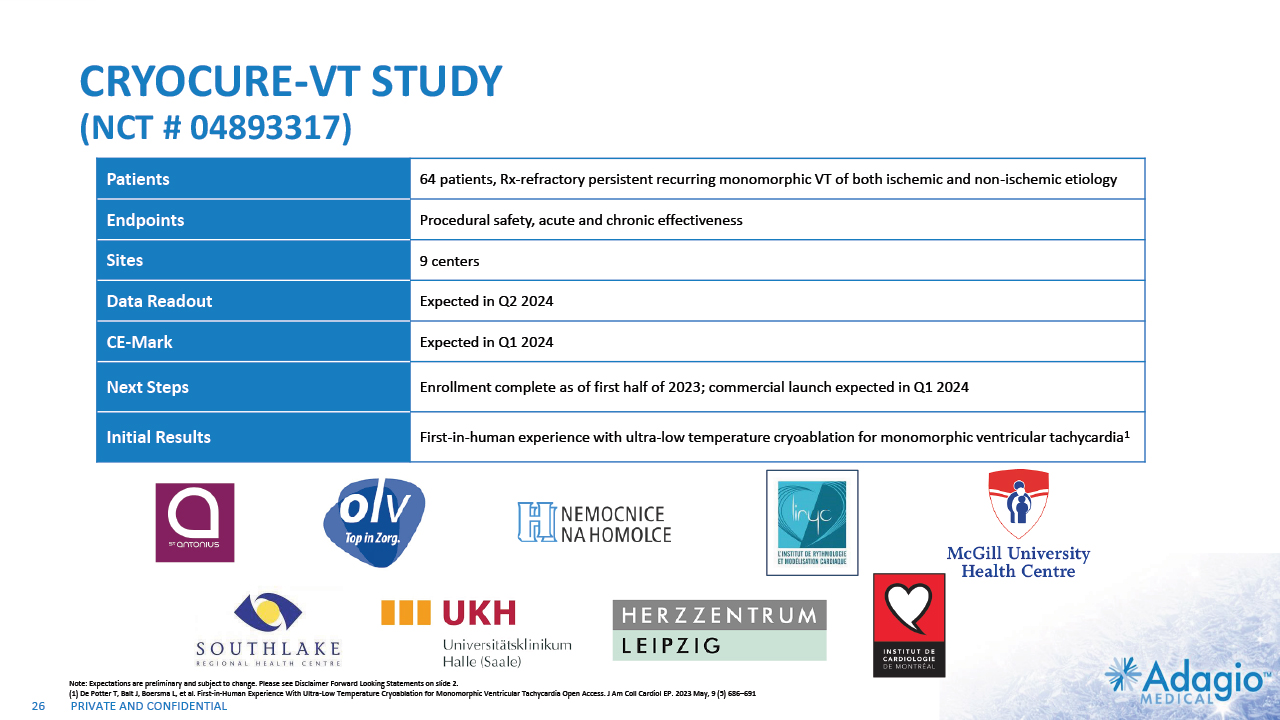

CRYOCURE-VT STUDY(NCT # 04893317) Patients 64 patients, Rx-refractory persistent recurring monomorphic VT of both ischemic and non-ischemic etiology Endpoints Procedural safety, acute and chronic effectiveness Sites 9 centers Data Readout Expected in Q2 2024 CE-Mark Expected in Q1 2024 Next Steps Enrollment complete as of first half of 2023; commercial launch expected in Q1 2024 Initial Results First-in-human experience with ultra-low temperature cryoablation for monomorphic ventricular tachycardia1 Note: Expectations are preliminary and subject to change. Please see Disclaimer Forward Looking Statements on slide 2. (1) De Potter T, Balt J, Boersma L, et al. First-in-Human Experience With Ultra-Low Temperature Cryoablation for Monomorphic Ventricular Tachycardia Open Access. J Am Coll Cardiol EP. 2023 May, 9 (5) 686–691 26

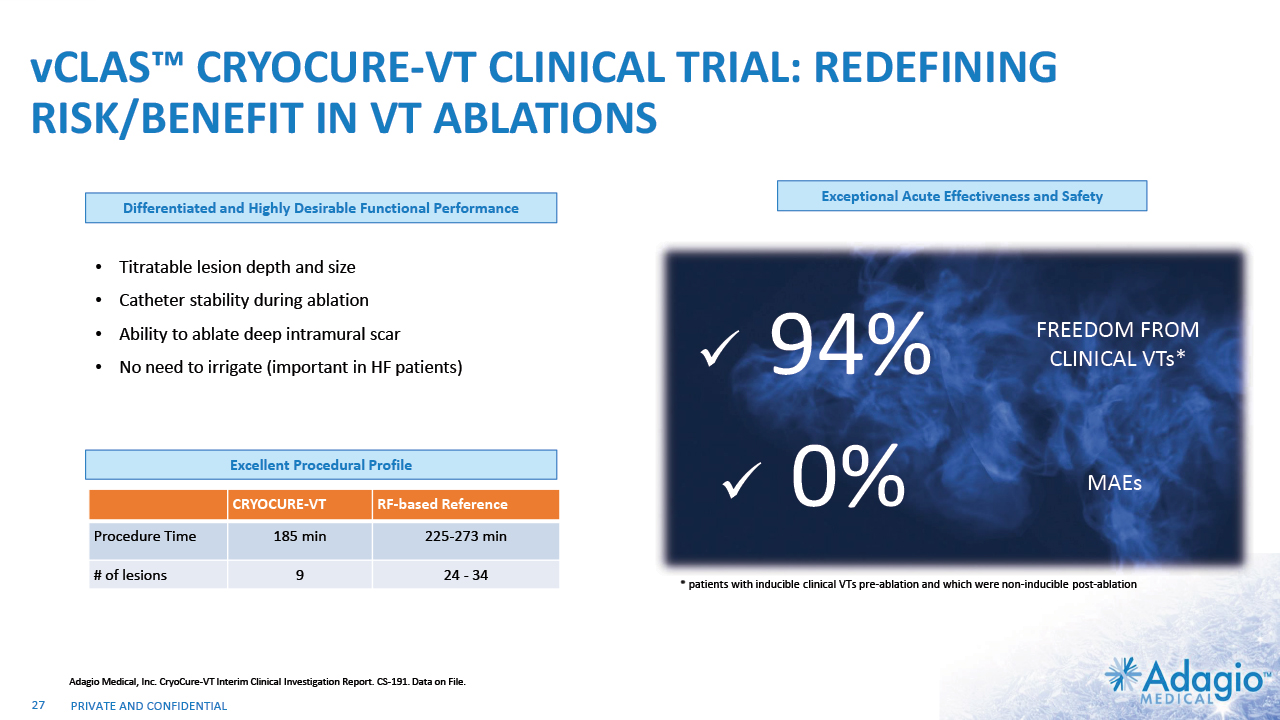

vCLAS™ CRYOCURE-VT CLINICAL TRIAL: REDEFINING RISK/BENEFIT IN VT ABLATIONS Titratable lesion depth and size Catheter stability during ablation Ability to ablate deep intramural scar No need to irrigate (important in HF patients) Differentiated and Highly Desirable Functional Performance Exceptional Acute Effectiveness and Safety Excellent Procedural Profile CRYOCURE-VT RF-based Reference Procedure Time 185 min 225-273 min # of lesions 9 24 - 34 Adagio Medical, Inc. CryoCure-VT Interim Clinical Investigation Report. CS-191. Data on File. 94% FREEDOM FROM CLINICAL VTs* 0% MAEs * patients with inducible clinical VTs pre-ablation and which were non-inducible post-ablation 27

WHAT IS PULSED FIELD CRYOABLATION?

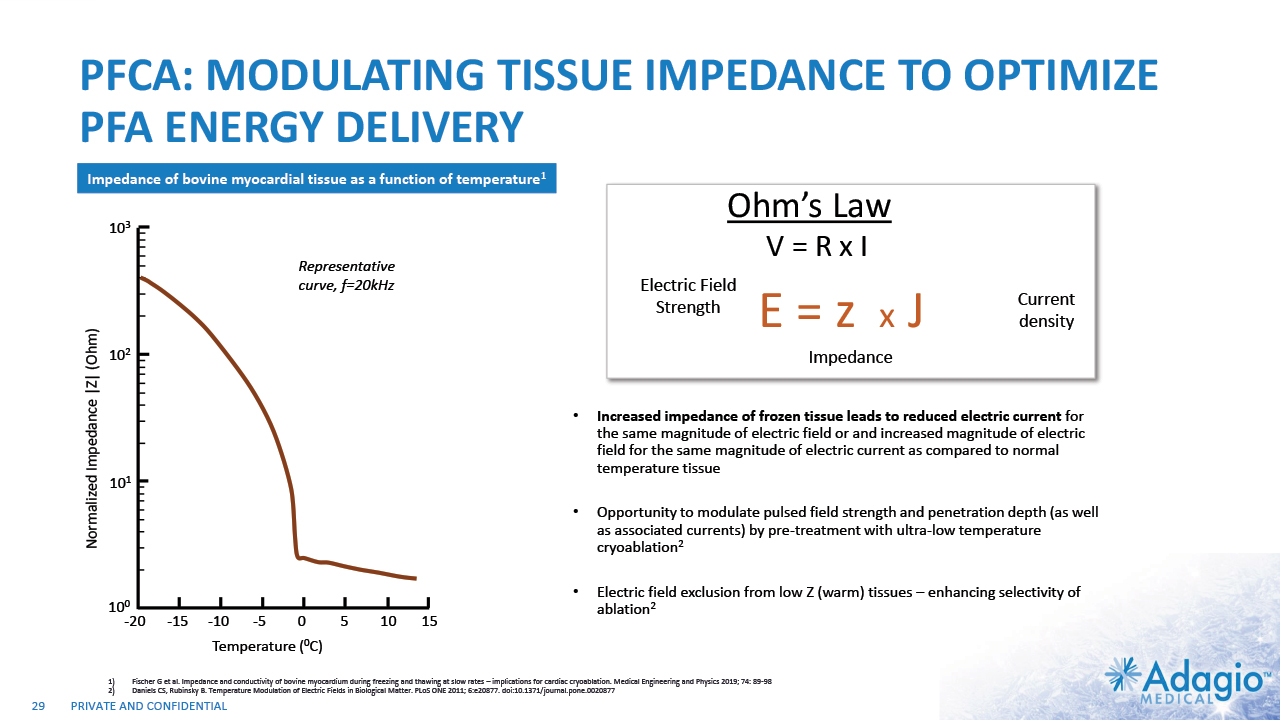

PFCA: MODULATING TISSUE IMPEDANCE TO OPTIMIZE PFA ENERGY DELIVERY Increased impedance of frozen tissue leads to reduced electric current for the same magnitude of electric field or and increased magnitude of electric field for the same magnitude of electric current as compared to normal temperature tissue Opportunity to modulate pulsed field strength and penetration depth (as well as associated currents) by pre-treatment with ultra-low temperature cryoablation2 Electric field exclusion from low Z (warm) tissues – enhancing selectivity of ablation2 Fischer G et al. Impedance and conductivity of bovine myocardium during freezing and thawing at slow rates – implications for cardiac cryoablation. Medical Engineering and Physics 2019; 74: 89-98 Daniels CS, Rubinsky B. Temperature Modulation of Electric Fields in Biological Matter. PLoS ONE 2011; 6:e20877. doi:10.1371/journal.pone.0020877 Impedance of bovine myocardial tissue as a function of temperature1 -20 -15 -10 -5 0 5 10 15 100 101 102 103 Temperature (0C) Normalized Impedance |Z| (Ohm) Representative curve, f=20kHz 29 E = z x J Ohm’s Law V = R x I Electric Field Strength Current density Impedance

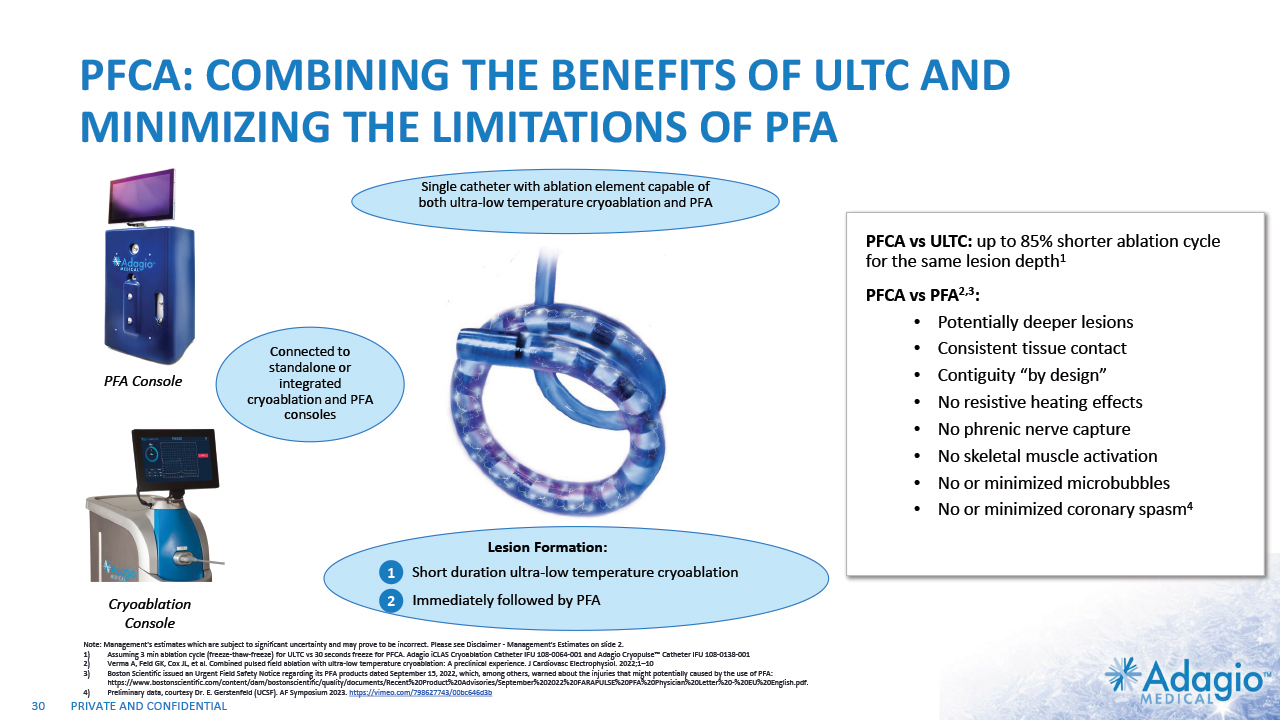

PFCA: COMBINING THE BENEFITS OF ULTC AND MINIMIZING THE LIMITATIONS OF PFA PFCA vs ULTC: up to 85% shorter ablation cycle for the same lesion depth1 PFCA vs PFA2,3: Potentially deeper lesions Consistent tissue contact Contiguity “by design” No resistive heating effects No phrenic nerve capture No skeletal muscle activation No or minimized microbubbles No or minimized coronary spasm4 30 PFA Console Cryoablation Console Single catheter with ablation element capable of both ultra-low temperature cryoablation and PFA Connected to standalone or integrated cryoablation and PFA consoles The best of both… for the price of one Note: Management's estimates which are subject to significant uncertainty and may prove to be incorrect. Please see Disclaimer - Management's Estimates on slide 2. Assuming 3 min ablation cycle (freeze-thaw-freeze) for ULTC vs 30 seconds freeze for PFCA. Adagio iCLAS Cryoablation Catheter IFU 108-0064-001 and Adagio Cryopulse™ Catheter IFU 108-0138-001 Verma A, Feld GK, Cox JL, et al. Combined pulsed field ablation with ultra-low temperature cryoablation: A preclinical experience. J Cardiovasc Electrophysiol. 2022;1–10 Boston Scientific issued an Urgent Field Safety Notice regarding its PFA products dated September 15, 2022, which, among others, warned about the injuries that might potentially caused by the use of PFA: https://www.bostonscientific.com/content/dam/bostonscientific/quality/documents/Recent%20Product%20Advisories/September%202022%20FARAPULSE%20PFA%20Physician%20Letter%20-%20EU%20English.pdf. Preliminary data, courtesy Dr. E. Gerstenfeld (UCSF). AF Symposium 2023. https://vimeo.com/798627743/00bc646d3b Lesion Formation: Short duration ultra-low temperature cryoablation 1 Immediately followed by PFA 2

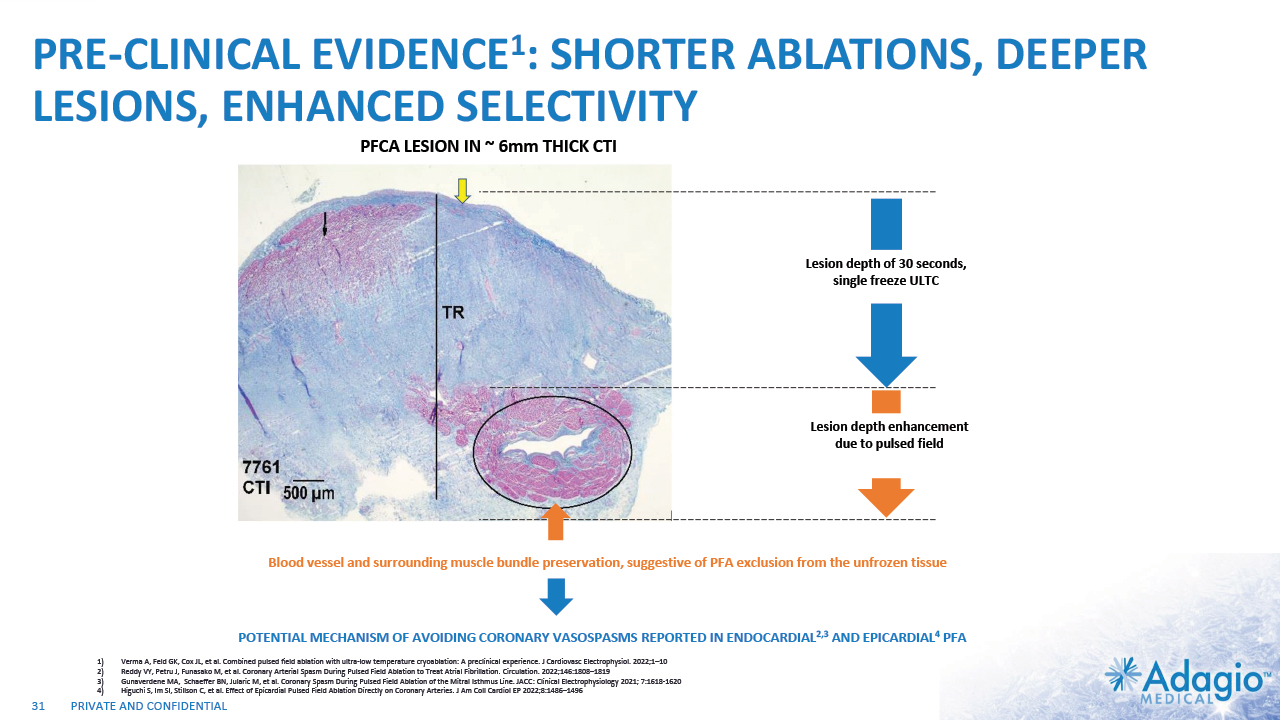

PRE-CLINICAL EVIDENCE1: SHORTER ABLATIONS, DEEPER LESIONS, ENHANCED SELECTIVITY 31 PFCA LESION IN ~ 6mm THICK CTI LESION SIZE COMPARISON: PFCA vs PFA Δ=0.8 mm (n.s.) Δ=1.7 mm (n.s.) 92% TM* 100%TM* * transmurality Lesion depth enhancement due to pulsed field Lesion depth of 30 seconds, single freeze ULTC POTENTIAL MECHANISM OF AVOIDING CORONARY VASOSPASMS REPORTED IN ENDOCARDIAL2,3 AND EPICARDIAL4 PFA Δ=2.0 mm (n.s.) Δ=6.0 mm (p=0.045) CTI LESIONS: INITIAL vs OPTIMIZED PFCA 100%TM* 100%TM* Lesion Dimension (mm) Blood vessel and surrounding muscle bundle preservation, suggestive of PFA exclusion from the unfrozen tissue 31 Verma A, Feld GK, Cox JL, et al. Combined pulsed field ablation with ultra-low temperature cryoablation: A preclinical experience. J Cardiovasc Electrophysiol. 2022;1–10 Reddy VY, Petru J, Funasako M, et al. Coronary Arterial Spasm During Pulsed Field Ablation to Treat Atrial Fibrillation. Circulation. 2022;146:1808–1819 Gunaverdene MA, Schaeffer BN, Jularic M, et al. Coronary Spasm During Pulsed Field Ablation of the Mitral Isthmus Line. JACC: Clinical Electrophysiology 2021; 7:1618-1620 Higuchi S, Im SI, Stillson C, et al. Effect of Epicardial Pulsed Field Ablation Directly on Coronary Arteries. J Am Coll Cardiol EP 2022;8:1486–1496

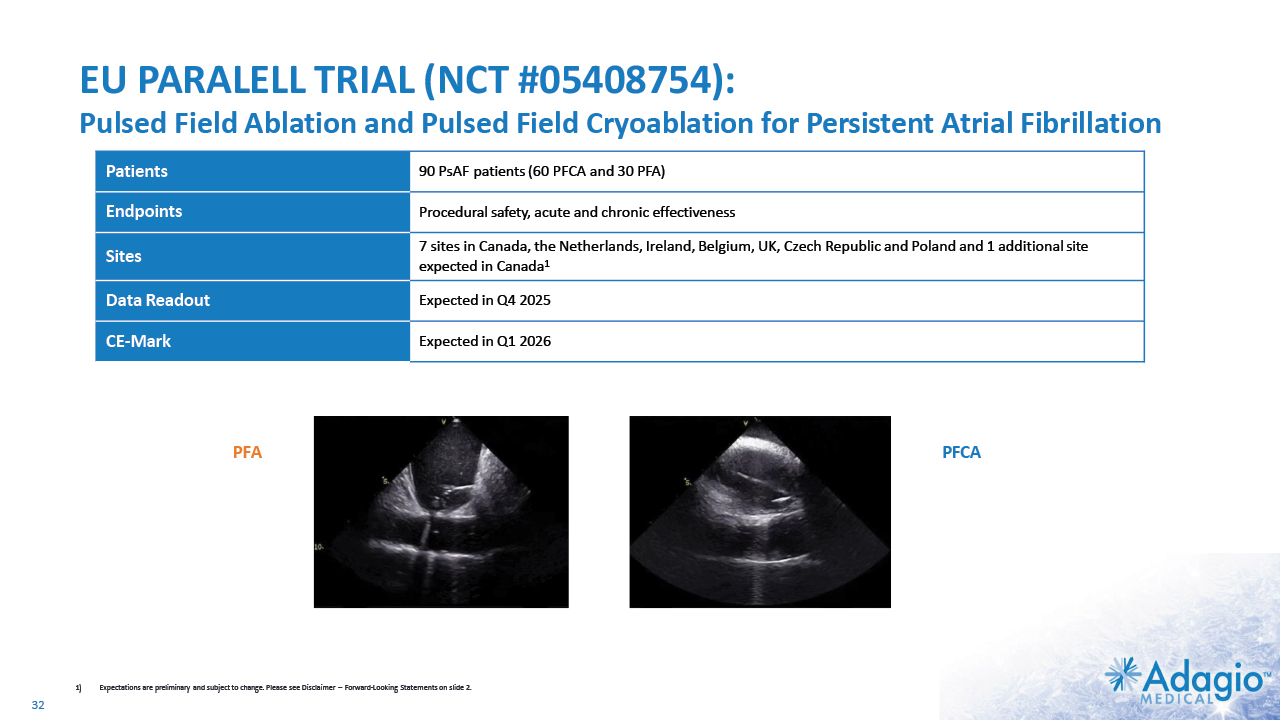

EU PARALELL TRIAL (NCT #05408754): Pulsed Field Ablation and Pulsed Field Cryoablation for Persistent Atrial Fibrillation PFA 1) Expectations are preliminary and subject to change. Please see Disclaimer -- Forward-Looking Statements on slide 2. 32 PFCA Patients 90 PsAF patients (60 PFCA and 30 PFA) Endpoints Procedural safety, acute and chronic effectiveness Sites 7 sites in Canada, the Netherlands, Ireland, Belgium, UK, Czech Republic and Poland and 1 additional site expected in Canada1 Data Readout Expected in Q4 2025 CE-Mark Expected in Q1 2026

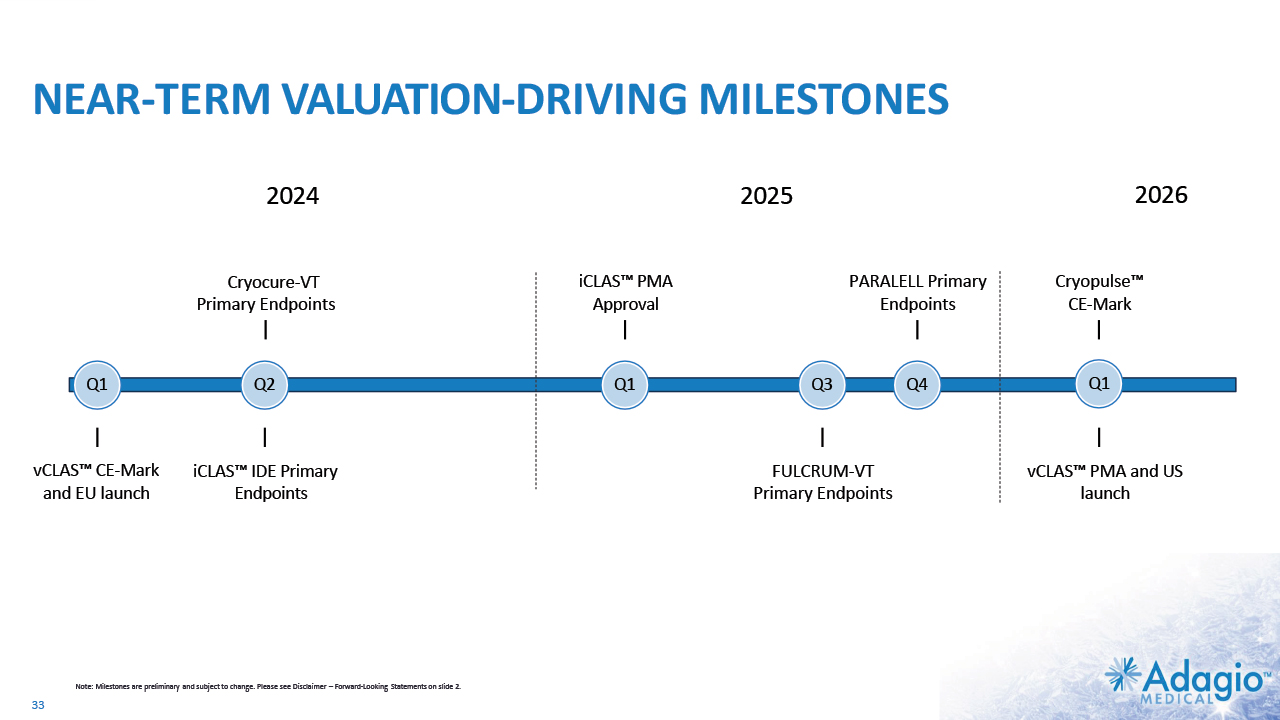

NEAR-TERM VALUATION-DRIVING MILESTONES Q1 Q2 Cryocure-VT Primary Endpoints Q1 vCLAS™ CE-Mark and EU launch 2024 iCLAS™ IDE Primary Endpoints iCLAS™ PMA Approval Q3 Cryopulse™ CE-Mark vCLAS™ PMA and US launch Note: Milestones are preliminary and subject to change. Please see Disclaimer – Forward-Looking Statements on slide 2. Q4 2026 33 Q1 2025 PARALELL Primary Endpoints FULCRUM-VT Primary Endpoints

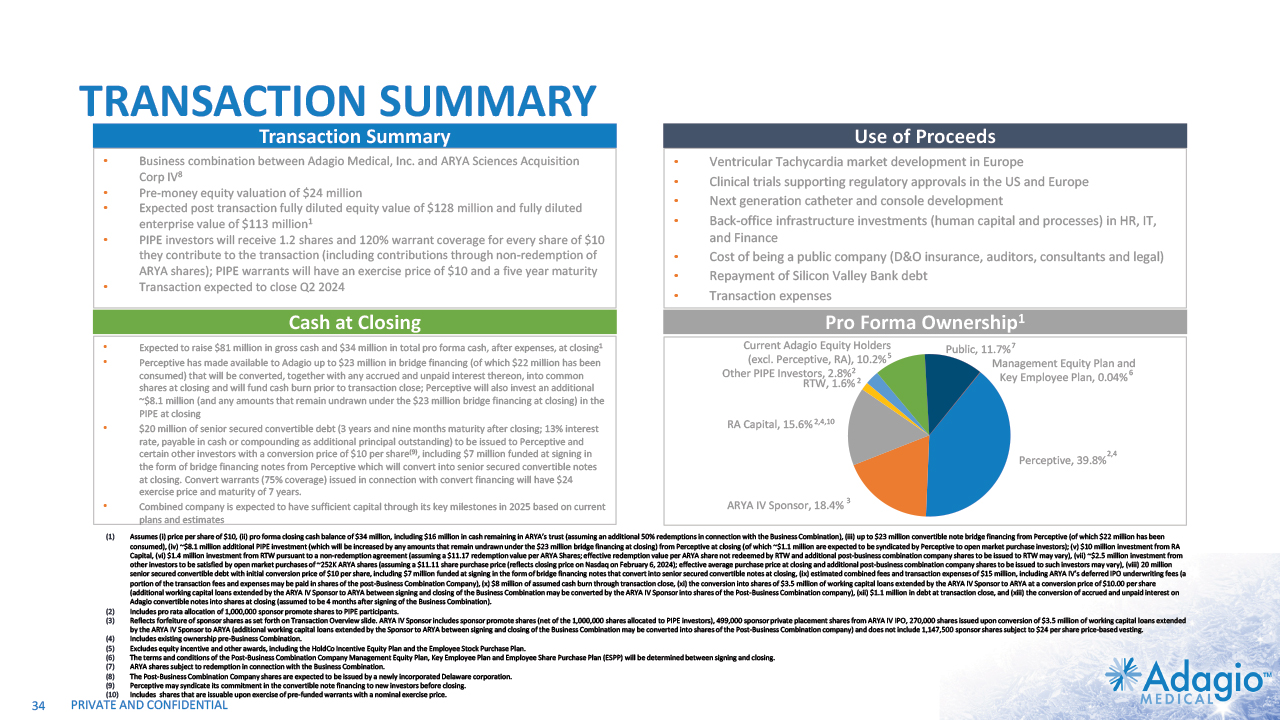

34 TRANSACTION SUMMARY Assumes (i) price per share of $10, (ii) pro forma closing cash balance of $34 million, including $15 million in cash remaining in ARYA’s trust (assuming an additional 50% redemptions in connection with the Business Combination), (iii) $23 million convertible note bridge financing from Perceptive (of which $22 million has been consumed), (iv) $7 million additional investment from Perceptive, (v) $10 million investment from RA Capital, (vi) $1.4 million investment from RTW pursuant to a non-redemption agreement (assuming a $11.17 redemption value per ARYA Shares; effective redemption value per ARYA share not redeemed by RTW and additional post-business combination company shares to be issued to RTW may vary), (vii) $3.6 million investment from other investors to be satisfied by open market purchases of ~321K ARYA shares (assuming a $11.11 share purchase price (reflects closing price on Nasdaq on February 6, 2024); effective average purchase price at closing and additional post-business combination company shares to be issued to such investors may vary), (viii) $20mm convertible debt financing with strike price of $10, (ix) estimated combined fees and transaction expenses of $15 million, including ARYA IV’s deferred IPO underwriting fees (a portion of the transaction fees and expenses may be paid in shares of the post-Business Combination Company), (x) $8 million of assumed cash burn through transaction close, (xi) the conversion into shares of $3.5 million of working capital loans extended by the ARYA IV Sponsor to ARYA at a conversion price of $10.00 per share (additional working capital loans extended by the ARYA IV Sponsor to ARYA between signing and closing of the Business Combination may be converted by the ARYA IV Sponsor into shares of the Post-Business Combination company), (xii) $1.1 million in debt at transaction close, and (xiii) the conversion of accrued and unpaid interest on Adagio convertible notes into shares at closing (assumed to be 4 months after signing of the Business Combination). Includes pro rata allocation of 1,000,000 sponsor promote shares to PIPE participants. Reflects forfeiture of sponsor shares as set forth on Transaction Overview slide. ARYA IV Sponsor includes sponsor promote shares (net of the 1,000,000 shares allocated to PIPE investors), 499,000 sponsor private placement shares from ARYA IV IPO, 270,000 shares issued upon conversion of $3.5 million of working capital loans extended by the ARYA IV Sponsor to ARYA (additional working capital loans extended by the Sponsor to ARYA between signing and closing of the Business Combination may be converted into shares of the Post-Business Combination company) and does not include 1,147,500 sponsor shares subject to $24 per share price-based vesting. Includes existing ownership pre-Business Combination. Excludes equity incentive and other awards, including the HoldCo Incentive Equity Plan and the Employee Stock Purchase Plan. Reflects management equity incentive awards assumed to be exercised immediately post-closing at a $10.00 post-Business Combination company per share price. Does not consider annual increase of incentive pool under any evergreen provision of the to be adopted equity incentive plan. ARYA shares subject to redemption in connection with the Business Combination. The Post-Business Combination Company shares are expected to be issued by a newly incorporated Delaware corporation. Perceptive may syndicate its commitment in the convertible note financing to new investors before closing. Use of Proceeds Ventricular Tachycardia market development in Europe Clinical trials supporting regulatory approvals in the US and Europe Next generation catheter and console development Back-office infrastructure investments (human capital and processes) in HR, IT, and Finance Cost of being a public company (D&O insurance, auditors, consultants and legal) Repayment of Silicon Valley Bank debt Transaction expenses Transaction Summary Business combination between Adagio Medical, Inc. and ARYA Sciences Acquisition Corp IV8 Pre-money equity valuation of $24 million Expected post transaction fully diluted equity value of $127 million and fully diluted enterprise value of $113 million1 PIPE investors will receive 1.2 shares and 120% warrant coverage for every share of $10 they contribute to the transaction (including contributions through non-redemption of ARYA shares); PIPE warrants will have an exercise price of $10 and a five year maturity Transaction expected to close Q2 2024 Cash at Closing Expected to raise $80 million in gross cash and $34 million in total pro forma cash, after expenses, at closing1 Perceptive has made available to Adagio up to $23 million in bridge financing (of which $22 million has been consumed) that will be converted, together with any accrued and unpaid interest thereon, into common shares at closing and will fund cash burn prior to transaction close; Perceptive will also invest an additional $7 million (and any amounts that remain undrawn under the $23 million bridge financing at closing) in the PIPE at closing $20 million of senior secured convertible debt (3 years and nine months maturity after closing) to be issued to Perceptive and certain other investors with a conversion price of $10 per share(9), including $12.5 million funded at signing in the form of bridge financing notes from Perceptive which will convert into senior secured convertible notes at closing. Convert warrants (75% coverage) issued in connection with convert financing will have $24 exercise price and maturity of 7 years. Combined company is expected to have sufficient capital through its key milestones in 2025 based on current plans and estimates Pro Forma Ownership1 5 2,4 2,4 6 3 7 2 2

SUMMARY: PURE-PLAY OPPORTUNITY IN CARDIAC ABLATIONS MARKET Unique technology poised to take significant market share in the Afib segment Highly differentiated product for VT A completely underserved market Muiltiple catalysts for the next several years in clinical data and product launches Pure-play electrophysiology segment investment opportunity 35 Currently ~$3 billion catheter market; advanced catheter revenue (75% of total) experienced historical double-digit growth Differentiated technology portfolio with best-in-class outcomes to drive both market expansion and share capture in ~$1bn ~$3bn VT and persistent AF market segment Key pivotal trial data and product launches in the next 18 months to drive increased valuation ✔ ✔ ✔

APPENDIX I

38 TRANSACTION OVERVIEW Transaction Summary Adagio Medical, Inc. and ARYA Sciences Acquisition Corp IV (“ARYA”, Nasdaq: ARYD) propose to enter into a definitive business combination agreement ARYA is a special purpose acquisition company sponsored by Perceptive Advisors LLC The Post-Business Combination Company shares are expected to be issued by a newly incorporated Delaware corporation and to trade under the ticker “ADGM” Pre-money equity valuation of $24 million. Expected post transaction fully diluted equity value of $127 million and fully diluted enterprise value of $113 million1 Transaction expected to close Q2 2024 Bridge, PIPE Financing, and Convertible Debt Deal structured to raise $80 million in gross cash and $34 million in total pro forma cash, after expenses, at closing1 from ARYA’s trust, PIPE financing, Perceptive bridge financing, and convertible debt PIPE investors will receive 1.2 shares and 120% warrant coverage for every share of $10 they contribute to the transaction (including contributions through non-redemption of ARYA shares); PIPE warrants will have an exercise price of $10 and a five year maturity Perceptive has made available to Adagio up to $23 million in bridge financing (of which $22 million has been consumed) that will be converted, together with any accrued and unpaid interest thereon, into common shares at closing and will fund cash burn prior to transaction close; Perceptive will also invest an additional $7 million (and any amounts that remain undrawn under the $23 million bridge financing at closing) in the PIPE at closing Bridge financing to be used to support expected $8 million cash burn prior to transaction close $20 million of senior secured convertible debt (3 years and nine months maturity after closing) to be issued to Perceptive and other investors with a conversion price of $10 per share, including $12.5 million funded at signing in the form of bridge financing notes from Perceptive which will convert into senior secured convertible notes at closing; convert warrants (75% coverage) issued in connection with convert financing will have $24 exercise price and maturity of 7 years(2) Sponsor Shares and Private Placement Shares 1,500,000 of the founder shares and 499,000 private placement shares held by ARYA Sponsor will be retained by ARYA Sponsor and not be subject to adjustment in connection with the transaction Up to 1,000,000 of the founder shares held by ARYA Sponsor will be forfeited in connection with the transaction; participants in the PIPE financing will separately receive a pro rata amount of such forfeited shares as additional consideration for the PIPE financing and bridge financing Perceptive will receive a proportionate amount of the 1,000,000 ARYA founder shares to be forfeited by ARYA Sponsor based on the portion of the aggregate financing funded by Perceptive in the bridge financing and the PIPE financing 1,147,500 of the founder shares held by ARYA Sponsor will become subject to share trigger price vesting and vest if the post-closing share price exceeds $24.00 per share Cash at Closing Adagio Medical, Inc. expected to have a minimum total pro forma cash of $34 million1, after expenses, at closing The combined company is expected to have sufficient capital through 2025 based on current plans and estimates Assumes (i) price per share of $10, (ii) pro forma closing cash balance of $34 million, including $15 million in cash remaining in ARYA’s trust (assuming an additional 50% redemptions in connection with the Business Combination), (iii) $23 million convertible note bridge financing from Perceptive (of which $22 million has been consumed), (iv) $7 million additional investment from Perceptive; (v) $10 million investment from RA Capital, (vi) $1.4 million investment from RTW pursuant to a non-redemption agreement (assuming a $11.17 redemption value per ARYA Shares; effective redemption value per ARYA share not redeemed by RTW and additional post-business combination company shares to be issued to RTW may vary), (vii) $3.6 million investment from other investors to be satisfied by open market purchases of ~321K ARYA shares (assuming a $11.11 share purchase price (reflects closing price on Nasdaq on February 6, 2024); effective average purchase price at closing and additional post-business combination company shares to be issued to such investors may vary), (viii) $20mm convertible debt financing with strike price of $10, (ix) estimated combined fees and transaction expenses of $15 million, including ARYA IV’s deferred IPO underwriting fees (a portion of the transaction fees and expenses may be paid in shares of the post-Business Combination Company), (x) $8 million of assumed cash burn through transaction close, (xi) the conversion into shares of $3.5 million of working capital loans extended by the ARYA IV Sponsor to ARYA at a conversion price of $10.00 per share (additional working capital loans extended by the ARYA IV Sponsor to ARYA between signing and closing of the Business Combination may be converted by the ARYA IV Sponsor into shares of the Post-Business Combination company), (xii) $1.1 million in debt at transaction close, and (xiii) the conversion of accrued and unpaid interest on Adagio convertible notes into shares at closing (assumed to be 4 months after signing of the Business Combination). Perceptive may syndicate its commitment in the convertible note financing to new investors before closing.

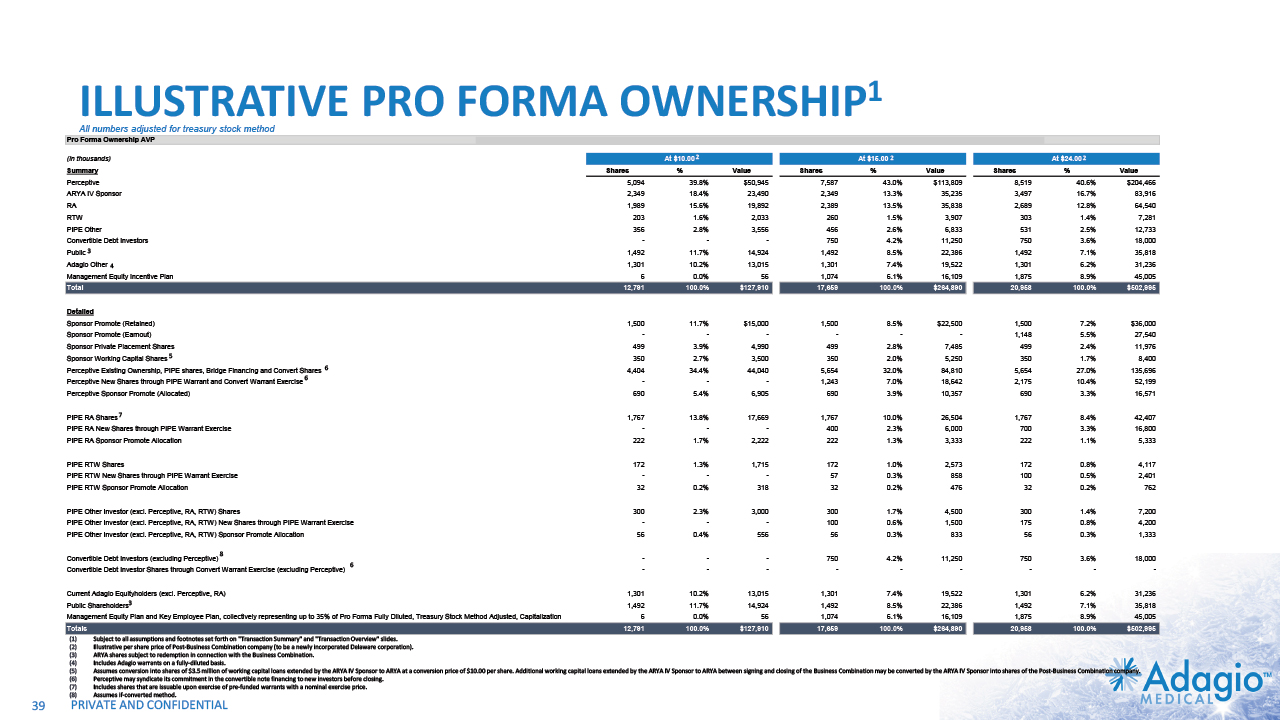

ILLUSTRATIVE PRO FORMA OWNERSHIP1 39 All numbers adjusted for treasury stock method Subject to all assumptions and footnotes set forth on "Transaction Summary" and "Transaction Overview" slides. Illustrative per share price of Post-Business Combination company (to be a newly incorporated Delaware corporation). ARYA shares subject to redemption in connection with the Business Combination. Includes Adagio warrants on a fully-diluted basis (other than Perceptive 2023 Bridge). Assumes conversion into shares of $3.5 million of working capital loans extended by the ARYA IV Sponsor to ARYA at a conversion price of $10.00 per share. Additional working capital loans extended by the ARYA IV Sponsor to ARYA between signing and closing of the Business Combination may be converted by the ARYA IV Sponsor into shares of the Post-Business Combination company. Perceptive may syndicate its commitment in the convertible note financing to new investors before closing. Assumes if-converted method. 4 2 2 2 3 3 5 6 6 6 7

40 HIGHLY ACCOMPLISHED EXECUTIVE TEAM Olav Bergheim CEO & President Hakon Bergheim Chief Operating Officer John Dahldorf Chief Financial Officer Nabil Jubran Chief Compliance Officer Tim Glynn VP of Global Sales Ilya Grigorov Vice President, Global Marketing and Product Management Doug Kurschinski Vice President of Clinical Affairs 10+ years of experience in medical devices 20+ years of corporate finance experience 20+ years of medical device experience 25+ years of medical experience 20+ years of medical device experience 30+ years of medical device experience 30+ years of experience in life sciences Founder of 3F Therapeutics Prelude Corporation Note: Olav Bergheim serves as the CEO of the Company pursuant to the terms of a Facilities and Shared Services Agreement between the Company and Fjord Ventures, LLC. Based on such agreement, Mr. Bergheim is compensated for serving in such position by Fjord Ventures, LLC. Two funds managed by Mr. Bergheim, one of which is affiliated with Fjord Ventures, LLC, have invested an aggregate of approximately $10M among the approximately $100M investment in aggregate that the Company has received so far. Volcano Corporation was acquired by Royal Philips in 2015. 1 1 1

SELECTED RISK FACTORS 41 No representation or warranty (whether express or implied) has been made by ARYA, the Company, ListCo or any of their respective directors, officers, employees, affiliates, agents, advisors or representatives with respect to the proposed PIPE financing or Business Combination or the manner in which the proposed PIPE financing or Business Combination is conducted, and the recipient hereby disclaims any such representation or warranty. The recipient of this Presentation acknowledges that ARYA, the Company, ListCo and their respective directors, officers, employees, affiliates, agents, advisors or representatives are under no obligation to accept any offer or proposal by any person or entity regarding the PIPE financing and the Business Combination. None of ARYA, the Company, ListCo or any of their respective directors, officers, employees, affiliates, agents, advisors or representatives has any legal, fiduciary or other duty to any recipient of this Presentation with respect to the manner in which the proposed PIPE financing or Business Combination is conducted. Unless the context otherwise requires, all reference in this subsection to the “Company,” “Adagio,” “we,” “us” or “our” refer to Adagio Medical, Inc. and its subsidiaries, prior to, or following, the consummation of the Business Combination, as the context requires. The risks presented below are some of the general risks to the business and operations of Adagio, ARYA Sciences Acquisition Corp IV (“ARYA”) and Aja Holdco, Inc., of which Adagio will become a subsidiary following the consummation of the Business Combination (the “Post-Combination Company”), and such risks are not exhaustive. The list below is qualified in its entirety by disclosures that will be contained in the future filings by ARYA and the Post-Combination Company, or of each of their respective affiliates or by third parties with the U.S. Securities and Exchange Commission (the “SEC”), including any documents filed in connection with the proposed transaction. The risks presented in such filings may differ significantly from and may be more extensive than those presented below. The list below is not exhaustive, and you are encouraged to perform your own investigation with respect to the business, financial condition and prospects of Adagio or the Post-Combination Company. You should carefully consider the following risk factors in addition to the information included in this presentation. Adagio or the Post-Combination Company may face additional risks and uncertainties that are not presently known to it or that it currently deems immaterial, which may also impair Adagio’s or the Post-Combination Company’s business or its financial condition. These risks speak only as of the date of this presentation, and neither the Company, ARYA nor the Post-Combination Company undertake any obligation to update the disclosure contained herein. In making any investment decision, you should rely solely upon independent investigation made by you. You acknowledge that you are not relying upon, and have not relied upon, any of the summary of risks or any other statement, representation or warranty made by any person or entity other than the statements, representations and warranties of the Company, ARYA or the Post-Combination Company explicitly contained in any definitive agreement you enter into. You acknowledge that you have such knowledge and experience in financial and business matters as to be capable of evaluating the merits and risks of an investment in the Company or the Post-Combination Company and you have sought such accounting, legal and tax advice from your own advisors as you have considered necessary to make an informed decision.

SELECTED RISK FACTORS (CONT.) 42 The consummation of the Business Combination is subject to a number of conditions, and if those conditions are not satisfied or waived, the Business Combination may not be completed; Some of ARYA’s, the Company’s or the Post-Combination Company’s officers and directors may have conflicts of interest that may influence them to approve the Business Combination without regard to your interests; ARYA’s directors and officers may have interests in the Business Combination different from the interests of ARYA, the Company, the Post-Combination Company or their respective shareholders; If ARYA is unable to close certain financing transactions and sufficient shareholders exercise their redemption rights in connection with the Business Combination such that there is less than $60 million of cash proceeds available from ARYA’s trust account and the financing transactions, then ARYA may lack sufficient funds to consummate the Business Combination; A portion of the total outstanding shares of the Post-Business Combination Company is expected to be restricted from immediate resale but may be sold into the market in the near future; Sales of a substantial number of shares of the Post-Business Combination Company’s common stock in the public market by existing stockholders could cause the Post-Business Combination Company’s share price to decline, even if our business is doing well; ARYA’s shareholders will experience dilution due to (i) the issuance to existing Company security holders and investors in the financing transactions in connection with the Business Combination of securities, and (ii) additional sources of dilution upon exercise or conversion of securities that will be issued in connection with or following the Business Combination (for instance, any earn-out shares, the PIPE Warrants, the Convert Warrants, the New Adagio Convertible Notes, securities issued in connection with the post-Business Combination Company equity plan or employee share purchase plan), in each case potentially entitling recipients of such securities to a significant voting stake in the Post-Business Combination Company; If ARYA does not consummated an initial business combination within the required time period, as may be extended at the option of ARYA Sciences Holdings IV (the “Sponsor”)), its public shareholders may receive only their pro rata portion of the funds in the ARYA’s trust account that are available for distribution its public shareholders; There are no assurances that ARYA will be able to complete the Business Combination prior to its expiration date or that the Sponsor will continue to exercise its monthly options to extend the time period ARYA has in order to consummate an initial business combination; The Company or Post-Business Combination Company stockholders cannot be certain of the value of the merger consideration they will receive until the closing of the Business Combination; Because there are no current plans to pay cash dividends on the common stock of the Post-Business Combination Company for the foreseeable future, you may not receive any return on investment unless you sell your ARYA ordinary shares or the Post-Business Combination Company common stock at a price greater than what you paid for it; ARYA, the Company and the Post-Business Combination Company expect to incur substantial transaction fees and costs in connection with the Business Combination and the integration of their businesses; The costs related to the Business Combination could be significantly higher than currently anticipated; ARYA’s, the Company’s or the Post-Business Combination Company’s business and operations could be negatively affected, or the Business Combination may be delayed or prevented from being completed, if they become subject to any securities litigation or shareholder activism; In connection with the Business Combination, the Sponsor and ARYA’s directors, executive officers, advisors and their affiliates may elect to purchase Class A ordinary shares of ARYA from public shareholders, which may reduce the public “float” of ARYA’s Class A ordinary shares;