UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

(Mark One)

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2021

or

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-40493

ATAI Life Sciences N.V.

(Exact name of registrant as specified in its charter)

| The Netherlands | Not Applicable | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

ATAI Life Sciences N.V. c/o Mindspace Krausenstraße 9-10 Berlin, Germany | Not Applicable | |

| (Address of principal executive offices) | (Zip Code) | |

+49 89 2153 9035

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common shares, par value €0.10 per share | ATAI | The Nasdaq Stock Market LLC (Nasdaq Global Market) |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of August 11, 2021, the registrant had 154,819,776 common shares, par value €0.10 per share, outstanding.

FORM 10-Q

Table of Contents

| Page | ||||||

| 1 | ||||||

PART I. FINANCIAL INFORMATION | 2 | |||||

Item 1. | Financial Statements (Unaudited) | 2 | ||||

Condensed Consolidated Balance Sheets as of June 30, 2021 and December 31, 2020 | 2 | |||||

| 3 | ||||||

| 4 | ||||||

| 5 | ||||||

Condensed Consolidated Statements of Cash Flows for the Six Months Ended June 30, 2021 and 2020 | 6 | |||||

| Notes to Condensed Consolidated Financial Statements | 7 | |||||

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 51 | ||||

Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 77 | ||||

Item 4. | Controls and Procedures | 78 | ||||

PART II. OTHER INFORMATION | ||||||

Item 1. | Legal Proceedings | 80 | ||||

Item 1A. | Risk Factors | 81 | ||||

Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 82 | ||||

Item 3. | Defaults Upon Senior Securities | 83 | ||||

Item 4. | Mine Safety Disclosures | 83 | ||||

Item 5. | Other Information | 83 | ||||

Item 6. | Exhibits | 83 | ||||

| Signatures | 85 | |||||

i

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

This Quarterly Report on Form 10-Q (this “Quarterly Report”) contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements contained in this Quarterly Report other than statements of historical fact, including statements regarding our future operating results and financial position, the success, cost and timing of development of our product candidates, including the progress of preclinical and clinical trials, the commercialization of our current product candidates and any other product candidates we may identify and pursue, if approved, including our ability to successfully build a specialty sales force and commercial infrastructure to market our current product candidates and any other product candidates we may identify and pursue, the timing of and our ability to obtain and maintain regulatory approvals, our business strategy and plans, potential acquisitions, and the plans and objectives of management for future operations and capital expenditures, are forward-looking statements. The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “could,” “would,” “project,” “plan,” “potentially,” “preliminary,” “likely,” and similar expressions are intended to identify forward-looking statements.

We have based these forward-looking statements largely on our current expectations and projections about future events and trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations and objectives, and financial needs. These forward-looking statements are subject to a number of risks, uncertainties, and assumptions, including without limitation: we are a clinical-stage biopharmaceutical company and have incurred significant losses since our inception, and we anticipate that we will continue to incur significant losses for the foreseeable future; we will require substantial additional funding to achieve our business goals, and if we are unable to obtain this funding when needed and on acceptable terms, we could be forced to delay, limit or terminate our product development efforts; our limited operating history may make it difficult to evaluate the success of our business and to assess our future viability; we have never generated revenue and may never be profitable; our product candidates contain controlled substances, the use of which may generate public controversy; clinical and preclinical development is uncertain, and our preclinical programs may experience delays or may never advance to clinical trials; we currently rely on qualified therapists working at third-party clinical trial sites to administer certain of our product candidates in our clinical trials and we expect this to continue upon approval, if any, of our current or future product candidate, and if third-party sites fail to recruit and retain a sufficient number of therapists or effectively manage their therapists, our business, financial condition and results of operations would be materially harmed; we cannot give any assurance that any of our product candidates will receive regulatory approval, which is necessary before they can be commercialized; research and development of drugs targeting the central nervous system, or CNS, is particularly difficult, and it can be difficult to predict and understand why a drug has a positive effect on some patients but not others; we face significant competition in an environment of rapid technological and scientific change; third parties may claim that we are infringing, misappropriating or otherwise violating their intellectual property rights, the outcome of which would be uncertain and may prevent or delay our development and commercialization efforts; a change in our effective place of management may increase our aggregate tax burden; we identified material weaknesses in connection with our internal control over financial reporting; and a pandemic, epidemic, or outbreak of an infectious disease, such as the COVID-19 pandemic, may materially and adversely affect our business, including our preclinical studies, clinical trials, third parties on whom we rely, our supply chain, our ability to raise capital, our ability to conduct regular business and our financial results. Other risk factors include the important factors described in the section titled “Risk Factors” in our final prospectus dated June 17, 2021, filed with the Securities and Exchange Commission (“SEC”) pursuant to Rule 424(b) under the Securities Act, that may cause our actual results, performance or achievements to differ materially and adversely from those expressed or implied by the forward-looking statements.

Any forward-looking statements made herein speak only as of the date of this Quarterly Report, and you should not rely on forward-looking statements as predictions of future events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that the future results, performance, or achievements reflected in the forward-looking statements will be achieved or will occur. Except as required by applicable law, we undertake no obligation to update any of these forward-looking statements for any reason after the date of this Quarterly Report on Form 10-Q or to conform these statements to actual results or revised expectations.

GENERAL

Unless the context otherwise requires, all references in this Quarterly Report to “we,” “us,” “our,” “ATAI” or the “Company” refer to ATAI Life Sciences N.V. and its consolidated subsidiaries.

All reports we file with the SEC are available for download free of charge via the Electronic Data Gathering Analysis and Retrieval (EDGAR) System on the SEC’s website at www.sec.gov. We also make electronic copies of our reports available for download, free of charge, through our investor relations website at ir.atai.life as soon as reasonably practicable after filing such material with the SEC.

We may announce material business and financial information to our investors using our investor relations website at ir.atai.life. We therefore encourage investors and others interested in ATAI to review the information that we make available on our website, in addition to following our filings with the SEC, webcasts, press releases and conference calls. Information contained on our website is not part of this Quarterly Report.

1

PART I – FINANCIAL INFORMATION

| Item 1. | Financial Statements (Unaudited) |

CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts in thousands, except share and per share amounts)

| June 30, | December 31, | |||||||

| 2021 | 2020 | |||||||

| (unaudited) | ||||||||

Assets | ||||||||

Current assets: | ||||||||

Cash and cash equivalents | $ | 453,622 | $ | 97,246 | ||||

Prepaid expenses and other current assets | 3,964 | 2,076 | ||||||

Short term notes receivable - related party | — | 226 | ||||||

|

|

|

| |||||

Total current assets | 457,586 | 99,548 | ||||||

Property and equipment, net | 331 | 71 | ||||||

Deferred offering costs | — | 1,575 | ||||||

Equity method investments | 19,780 | — | ||||||

Other investments held at fair value | 6,886 | — | ||||||

Other investments | 16,107 | 8,044 | ||||||

Long term notes receivable | 1,388 | 911 | ||||||

Long term notes receivable - related parties | 3,194 | 1,060 | ||||||

Other assets | 689 | 339 | ||||||

|

|

|

| |||||

Total assets | $ | 505,961 | $ | 111,548 | ||||

|

|

|

| |||||

Liabilities and Stockholders’ Equity | ||||||||

Current liabilities: | ||||||||

Accounts payable | $ | 6,202 | $ | 3,083 | ||||

Accrued liabilities | 7,824 | 9,215 | ||||||

Deferred revenue | 120 | — | ||||||

Short-term notes payable | 39 | — | ||||||

|

|

|

| |||||

Total current liabilities | 14,185 | 12,298 | ||||||

Contingent consideration liability - related parties | 2,466 | 1,705 | ||||||

Convertible promissory notes - related parties, net of discounts and deferred issuance costs | 1,176 | 1,199 | ||||||

Convertible promissory notes and derivative liability (including a related party convertible promissory note and derivative liability of $0 million and $0.3 million at June 30, 2021 and December 31, 2020, respectively) | — | 978 | ||||||

Other liabilities | 3,239 | — | ||||||

|

|

|

| |||||

Total liabilities | 21,066 | 16,180 | ||||||

|

|

|

| |||||

Commitments and contingencies (Note 15) | ||||||||

Stockholders’ equity: | ||||||||

Common stock, €0.10 par value ($0.12 par value at June 30, 2021 and December 31, 2020, respectively); 750,000,000 and 173,116,704 shares authorized at June 30, 2021 and December 31, 2020, respectively; 154,819,776 and 114,735,712 shares issued and outstanding at June 30, 2021 and December 31, 2020, respectively | 17,299 | 13,372 | ||||||

Additional paid-in capital | 691,382 | 261,626 | ||||||

Accumulated other comprehensive income (loss) | 3,937 | 5,819 | ||||||

Accumulated deficit | (237,768 | ) | (189,995 | ) | ||||

|

|

|

| |||||

Total stockholders’ equity attributable to ATAI Life Sciences N.V. stockholders | 474,850 | 90,822 | ||||||

Noncontrolling interests | 10,045 | 4,546 | ||||||

|

|

|

| |||||

Total stockholders’ equity | 484,895 | 95,368 | ||||||

|

|

|

| |||||

Total liabilities and stockholders’ equity | $ | 505,961 | $ | 111,548 | ||||

|

|

|

| |||||

See accompanying notes to the unaudited condensed consolidated financial statements

2

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Amounts in thousands, except share and per share amounts)

(unaudited)

| Three Months Ended | Six Months Ended | |||||||||||||||

| June 30, | June 30, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

License revenue | $ | — | $ | — | $ | 19,880 | $ | — | ||||||||

Operating expenses: | ||||||||||||||||

Research and development | 16,026 | 2,854 | 21,611 | 4,998 | ||||||||||||

Acquisition of in-process research and development | 7,962 | 120 | 8,934 | 120 | ||||||||||||

General and administrative | 37,331 | 2,851 | 46,604 | 4,421 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total operating expenses | 61,319 | 5,825 | 77,149 | 9,539 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Loss from operations | (61,319 | ) | (5,825 | ) | (57,269 | ) | (9,539 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Other income (expense), net: | ||||||||||||||||

Interest income | 35 | 18 | 72 | 38 | ||||||||||||

Change in fair value of contingent consideration liability - related parties | (911 | ) | (42 | ) | (660 | ) | (66 | ) | ||||||||

Change in fair value of short term notes receivable - related party | — | — | — | 718 | ||||||||||||

Change in fair value of convertible promissory notes | — | (1,260 | ) | — | (133 | ) | ||||||||||

Change in fair value of derivative liability | — | — | 41 | — | ||||||||||||

Unrealized loss on other investments held at fair value | (5,460 | ) | — | (5,460 | ) | — | ||||||||||

Unrealized gain on other investments | — | — | — | 19,856 | ||||||||||||

Loss on conversion of convertible promissory notes | (513 | ) | — | (513 | ) | — | ||||||||||

Gain on consolidation of a variable interest entity | 3,543 | — | 3,543 | — | ||||||||||||

Other income (expense), net | (2,676 | ) | (37 | ) | (1,302 | ) | (119 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total other income (expense), net | (5,982 | ) | (1,321 | ) | (4,279 | ) | 20,294 | |||||||||

|

|

|

|

|

|

|

| |||||||||

Net income (loss) before income taxes | (67,301 | ) | (7,146 | ) | (61,548 | ) | 10,755 | |||||||||

Provision for income taxes | (58 | ) | — | (64 | ) | — | ||||||||||

Gain on dilution of equity method investment | 16,923 | — | 16,923 | — | ||||||||||||

Losses from investments in equity method investees, net of tax | (2,937 | ) | (9,811 | ) | (4,640 | ) | (11,831 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net loss | (53,373 | ) | (16,957 | ) | (49,329 | ) | (1,076 | ) | ||||||||

Net loss attributable to redeemable noncontrolling interests and noncontrolling interests | (4,912 | ) | (600 | ) | (1,556 | ) | (1,022 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net loss attributable to ATAI Life Sciences N.V. stockholders | $ | (48,461 | ) | $ | (16,357 | ) | $ | (47,773 | ) | $ | (54 | ) | ||||

|

|

|

|

|

|

|

| |||||||||

Net loss per share attributable to ATAI Life Sciences N.V. stockholders — basic and diluted | $ | (0.37 | ) | $ | (0.18 | ) | $ | (0.38 | ) | $ | (0.00 | ) | ||||

|

|

|

|

|

|

|

| |||||||||

Weighted average common shares outstanding attributable to ATAI Life Sciences N.V. stockholders — basic and diluted | 132,265,075 | 90,709,312 | 125,797,732 | 90,709,312 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

See accompanying notes to the unaudited condensed consolidated financial statements

3

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(Amounts in thousands)

(unaudited)

| Three Months Ended | Six Months Ended | |||||||||||||||

| June 30, | June 30, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

Net loss | $ | (53,373 | ) | $ | (16,957 | ) | $ | (49,329 | ) | $ | (1,076 | ) | ||||

Other comprehensive loss: | ||||||||||||||||

Foreign currency translation adjustments, net of tax | 2,110 | 784 | (1,916 | ) | (106 | ) | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Comprehensive income (loss) | $ | (51,263 | ) | $ | (16,173 | ) | $ | (51,245 | ) | $ | (1,182 | ) | ||||

Comprehensive income (loss) attributable to redeemable noncontrolling interests and noncontrolling interests | (4,912 | ) | (600 | ) | (1,556 | ) | (1,022 | ) | ||||||||

Foreign currency translation adjustments, net of tax attributable to noncontrolling interests | 150 | (20 | ) | (34 | ) | (7 | ) | |||||||||

|

|

|

|

|

|

|

| |||||||||

Comprehensive loss attributable to redeemable noncontrolling interests and noncontrolling interests | (4,762 | ) | (620 | ) | (1,590 | ) | (1,029 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Comprehensive income (loss) attributable to ATAI Life Sciences N.V. stockholders | $ | (46,501 | ) | $ | (15,553 | ) | $ | (49,655 | ) | $ | (153) | |||||

|

|

|

|

|

|

|

| |||||||||

See accompanying notes to the unaudited condensed consolidated financial statements

4

CONDENSED CONSOLIDATED STATEMENTS OF REDEEMABLE NONCONTROLLING

INTERESTS AND STOCKHOLDERS’ EQUITY

(Amounts in thousands, except share and per share amounts)

(unaudited)

| Accumulated | Total | |||||||||||||||||||||||||||||||||||||||

| Other | Stockholders’ | |||||||||||||||||||||||||||||||||||||||

| Redeemable | Additional | Share | Comprehensive | Equity Attributable to | Total | |||||||||||||||||||||||||||||||||||

| Noncontrolling | Common Stock | Paid-In | Subscriptions | Income | Accumulated | ATAI Life Sciences N.V. | Noncontrolling | Stockholders’ | ||||||||||||||||||||||||||||||||

| Interests | Shares | Amount | Capital | Receivable | (Loss) | Deficit | Stockholders | Interests | Equity | |||||||||||||||||||||||||||||||

Balances at December 31, 2020 | $ | — | 114,735,712 | $ | 13,372 | $ | 261,626 | $ | — | $ | 5,819 | $ | (189,995 | ) | $ | 90,822 | $ | 4,546 | $ | 95,368 | ||||||||||||||||||||

Issuance of common shares, net of issuance costs of $4.9 million | — | 15,552,688 | 1,881 | 162,497 | (140,868 | ) | — | — | 23,510 | — | 23,510 | |||||||||||||||||||||||||||||

Issuance of common shares under the Hurdle Share Option Plan (see Note 12) | — | 7,281,376 | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||

Issuance of noncontrolling interest | — | — | — | — | — | — | — | — | 885 | 885 | ||||||||||||||||||||||||||||||

Stock-based compensation expense | — | — | — | 212 | — | — | — | 212 | — | 212 | ||||||||||||||||||||||||||||||

Foreign currency translation adjustment, net of tax | — | — | — | — | — | (3,842 | ) | — | (3,842 | ) | (184 | ) | (4,026 | ) | ||||||||||||||||||||||||||

Net income | — | — | — | — | — | — | 688 | 688 | 3,356 | 4,044 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Balances as of March 31, 2021 | $ | — | 137,569,776 | $ | 15,253 | $ | 424,335 | $ | (140,868 | ) | $ | 1,977 | $ | (189,307 | ) | $ | 111,390 | $ | 8,603 | $ | 119,993 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Settlement of issuance of common shares, net of issuance costs of $4.9 million | — | — | — | — | 140,868 | — | — | 140,868 | — |

| 140,868 |

| ||||||||||||||||||||||||||||

Issuance of common shares, net of issuance costs of $9.0 million | — | 17,250,000 | 2,046 | 229,535 | — | — | — | 231,581 | — | 231,581 | ||||||||||||||||||||||||||||||

Issuance of noncontrolling interest | 2,555 | — | — | — | — | — | — | — | 3,649 | 3,649 | ||||||||||||||||||||||||||||||

Stock-based compensation expense | — | — | — | 37,512 | — | — | — | 37,512 | — | 37,512 | ||||||||||||||||||||||||||||||

Foreign currency translation adjustment, net of tax | — | — | — | — | — | 1,960 | — | 1,960 | 150 | 2,110 | ||||||||||||||||||||||||||||||

Net income | (2,555 | ) | — | — | — | — | — | (48,461 | ) | (48,461 | ) | (2,357 | ) | (50,818 | ) | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Balances as of June 30, 2021 | $ | — | 154,819,776 | $ | 17,299 | $ | 691,382 | $ | — | $ | 3,937 | $ | (237,768 | ) | $ | 474,850 | $ | 10,045 | $ | 497,032 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

| Accumulated | Total | |||||||||||||||||||||||||||||||||||

| Other | Stockholders’ | |||||||||||||||||||||||||||||||||||

| Redeemable | Additional | Comprehensive | Equity Attributable | Total | ||||||||||||||||||||||||||||||||

| Noncontrolling | Common Stock | Paid-In | Income | Accumulated | to ATAI Life Sciences N.V. | Noncontrolling | Stockholders’ | |||||||||||||||||||||||||||||

| Interests | Shares | Amount | Capital | (Loss) | Deficit | Stockholders | Interests | Equity | ||||||||||||||||||||||||||||

Balances at December 31, 2019 | $ | 142 | 90,709,312 | $ | 10,510 | $ | 69,819 | $ | (1,426 | ) | $ | (20,152 | ) | $ | 58,751 | $ | 887 | $ | 59,638 | |||||||||||||||||

Stock-based compensation expense | — | — | — | 41 | — | — | 41 | — | 41 | |||||||||||||||||||||||||||

Foreign currency translation adjustment, net of tax | — | — | — | — | (903 | ) | — | (903 | ) | 13 | (890 | ) | ||||||||||||||||||||||||

Net income (loss) | (33 | ) | — | — | — | — | 16,302 | 16,302 | (389 | ) | 15,913 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Balances as of March 31, 2020 | $ | 109 | 90,709,312 | $ | 10,510 | $ | 69,860 | $ | (2,329 | ) | $ | (3,850 | ) | $ | 74,191 | $ | 511 | $ | 74,702 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Stock-based compensation expense | — | — | — | 41 | — | — | 41 | — | 41 | |||||||||||||||||||||||||||

Issuance of subsidiary shares in connection with the Columbia stock purchase agreement (Note 16) | — | — | — | 120 | — | — | 120 | — | 120 | |||||||||||||||||||||||||||

Foreign currency translation adjustment, net of tax | — | — | — | — | 804 | 804 | (20 | ) | 777 | |||||||||||||||||||||||||||

Net income (loss) | (109 | ) | — | — | — | — | (16,357 | ) | (16,357 | ) | (491 | ) | (16,848 | ) | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Balances as of June 30, 2020 | $ | — | $ | 90,709,312 | $ | 10,510 | $ | 70,021 | $ | (1,525 | ) | $ | (20,207 | ) | $ | 58,799 | $ | — | $ | 58,800 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

See accompanying notes to the unaudited condensed consolidated financial statements

5

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amounts in thousands)

(unaudited)

| Six Months Ended | ||||||||

| June 30, | ||||||||

| 2021 | 2020 | |||||||

Cash flows from operating activities | ||||||||

Net loss | $ | (49,329 | ) | $ | (1,076 | ) | ||

Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

Depreciation and amortization expense | 25 | 5 | ||||||

Amortization of debt discount | 191 | 15 | ||||||

Change in fair value of contingent consideration liability- related parties | 660 | 66 | ||||||

Change in fair value of short term notes receivable - related parties | — | (718 | ) | |||||

Change in fair value of convertible promissory notes | — | 133 | ||||||

Change in fair value of derivative liability | (41 | ) | 12 | |||||

Change in fair value of warrant liability | 40 | — | ||||||

Unrealized loss on other investments held at fair value | 5,460 | — | ||||||

Unrealized gains on other investments | — | (19,856 | ) | |||||

Gain on dilution of equity method investment | (16,923 | ) | — | |||||

Loss on conversion of convertible notes | 513 | — | ||||||

Gain on consolidation of a variable interest entity | (3,543 | ) | — | |||||

Losses from investments in equity method investees | 4,641 | 11,831 | ||||||

In-process research and development expense | 8,934 | 120 | ||||||

Stock-based compensation expense | 37,724 | 82 | ||||||

Unrealized foreign exchange gains | — | (155 | ) | |||||

Other | 41 | (57 | ) | |||||

Changes in operating assets and liabilities: | ||||||||

Prepaid expenses and other current assets | (1,674 | ) | (513 | ) | ||||

Accounts payable | 2,380 | 252 | ||||||

Accrued liabilities | (3,846 | ) | 752 | |||||

Deferred revenue | 120 | — | ||||||

|

|

|

| |||||

Net cash used in operating activities | (14,627 | ) | (9,107 | ) | ||||

|

|

|

| |||||

Cash flows from investing activities | ||||||||

Purchases of property and equipment | (298 | ) | (8 | ) | ||||

Capitalized internal-use software development costs | (155 | ) | — | |||||

Cash acquired in asset acquisitions, net | 47 | — | ||||||

Cash paid for investments in equity method investees | (5,359 | ) | — | |||||

Cash paid for other investments | (23,445 | ) | (17,823 | ) | ||||

Purchases of long term notes receivable - related party | — | (1,198 | ) | |||||

Loans to related parties | (2,624 | ) | — | |||||

Cash paid for other assets | (195 | ) | — | |||||

|

|

|

| |||||

Net cash used in investing activities | (32,029 | ) | (19,029 | ) | ||||

|

|

|

| |||||

Cash flows from financing activities | ||||||||

Proceeds from issuance of common stock | 409,884 | — | ||||||

Cash paid for common stock issuance costs | (10,161 | ) | — | |||||

Proceeds from issuance of share option awards | 534 | — | ||||||

Proceeds from sale of investment | 2,417 | — | ||||||

Proceeds from issuance of convertible promissory notes | 1,588 | 13,011 | ||||||

|

|

|

| |||||

Net cash provided by financing activities | 404,262 | 13,011 | ||||||

|

|

|

| |||||

Effect of foreign exchange rate changes on cash | (1,230 | ) | (204 | ) | ||||

|

|

|

| |||||

Net increase (decrease) in cash and cash equivalents | 356,376 | (15,329 | ) | |||||

|

|

|

| |||||

Cash and cash equivalents – beginning of the period | 97,246 | 30,062 | ||||||

|

|

|

| |||||

Cash and cash equivalents – end of the period | $ | 453,622 | 14,733 | |||||

|

|

|

| |||||

Supplemental disclosures of non-cash investing and financing information: | ||||||||

Fair value of noncontrolling interests issued in connection with asset acquisitions | $ | 885 | $ | — | ||||

Fair value of noncontrolling interests issued in connection with consolidation of a VIE | $ | 392 | $ | — | ||||

Fair value redeemable noncontrolling interests issued in connection with consolidation of a VIE | $ | 2,555 | $ | — | ||||

Issuance of subsidiary shares in connection with the conversion of convertible notes | $ | 3,257 | $ | — | ||||

Common stock issuance costs in accounts payable | $ | 230 | $ | — | ||||

Common stock issuance costs in accrued liabilities | $ | 1,958 | $ | — | ||||

Conversion of short term notes receivable for other investments | $ | — | $ | 9,003 | ||||

Issuance of subsidiary shares in connection with a stock purchase agreement | $ | — | $ | 120 | ||||

Issuance of derivative instrument related to convertible promissory notes | $ | 646 | $ | 203 | ||||

See accompanying notes to the unaudited condensed consolidated financial statements

6

1. Organization and Description of Business

ATAI Life Sciences N.V. (“ATAI”) is the parent company of ATAI Life Sciences AG and, along with its subsidiaries, is a clinical-stage biopharmaceutical company aiming to transform the treatment of mental health disorders. ATAI was founded to address the significant unmet need and lack of innovation in the mental health treatment landscape as well as the emergence of therapies that previously may have been overlooked or underused, including psychedelic compounds and digital therapies.

Since inception, ATAI has either created wholly owned subsidiaries or has made investments in certain controlled entities, including variable interest entities (“VIEs”) for which ATAI is the primary beneficiary under the VIE model (collectively, the “Company”). ATAI is headquartered in Berlin, Germany.

Corporate Reorganization and Initial Public Offering

ATAI was incorporated pursuant to the laws of the Netherlands as a Dutch private company with limited liability on September 10, 2020 for the purposes of becoming a holding company for ATAI Life Sciences AG and for the purposes of consummating the corporate reorganization described below. ATAI has not conducted any operations prior to the corporate reorganization other than activities incidental to its formation. ATAI Life Sciences AG was formed as a separate company on February 7, 2018.

In contemplation of the consummation of ATAI’s initial public offering (“IPO”) of common shares, ATAI undertook a corporate reorganization (the “Corporate Reorganization”). The Corporate Reorganization consisted of several steps as described below:

| • | Exchange of ATAI Life Sciences AG Securities for ATAI Life Sciences B.V. Common Shares and Share Split: In April 2021, the existing shareholders of ATAI Life Sciences AG each became a party to a separate notarial deed of issue under Dutch law and (i) subscribed for new common shares in ATAI Life Sciences B.V. and (ii) transferred their respective shares in ATAI Life Sciences AG, on a 1 to 10 basis (the “Exchange Ratio”), to ATAI Life Sciences B.V. as a contribution in kind on the common shares in ATAI Life Sciences B.V. As a result of the issuance of common shares in ATAI Life Sciences B.V. to the shareholders of ATAI Life Sciences AG and the contribution and transfer of their respective shares in ATAI Life Sciences AG to ATAI Life Sciences B.V., ATAI Life Sciences AG became a wholly owned subsidiary of ATAI Life Sciences B.V. No shareholder rights or preferences changed as a result of the share for share exchange. In connection with such exchange, the common share in ATAI Life Sciences B.V. held by Apeiron was cancelled. On June 7, 2021, shares of ATAI Life Sciences B.V. were split applying a ratio of 1.6 to one, and the nominal value of the shares was reduced to €0.10, pursuant to a shareholders’ resolution and amendment to the articles of association. |

| • | Conversion of ATAI Life Sciences B.V. into ATAI Life Sciences N.V.: Immediately preceding the Company’s IPO, the legal form of ATAI Life Sciences B.V. was converted from a Dutch private company with limited liability to a Dutch public company, and the articles of association of ATAI Life Sciences N.V., became effective. Following the Corporate Reorganization, ATAI Life Sciences N.V. became the holding company of ATAI Life Sciences AG. |

The Corporate Reorganization, as described above, is considered a continuation of ATAI Life Sciences AG resulting in no change in the carrying values of assets or liabilities. As a result, the financial statements for periods prior to the Corporate Reorganization are the financial statements of ATAI Life Sciences AG as the predecessor to ATAI for accounting and reporting purposes. All share, per-share and related information presented in these condensed consolidated financial statements and corresponding disclosure notes have been retrospectively adjusted, where applicable, to reflect the impact of the share exchange and share split resulting from the Corporate Reorganization. In connection with the Corporate Reorganization, outstanding share awards and option grants of ATAI Life Sciences AG were exchanged for share awards and option grants of ATAI Life Sciences B.V. with identical restrictions.

On June 22, 2021, ATAI closed the IPO of its common stock on Nasdaq. As part of the IPO, the Company issued and sold 17,250,000 shares of its common stock, which included 2,250,000 shares sold pursuant to the exercise of the

7

underwriters’ over-allotment option, at a public offering price of $15.00 per share. The Company received net proceeds of approximately $231.6 million from the IPO, after deducting underwriters’ discounts and commissions of $18.1 million and offering costs of $9.0 million.

Impact of COVID-19 Pandemic

In December 2019, a novel strain of coronavirus, severe acute respiratory syndrome coronavirus 2, or SARS-CoV-2, was identified in Wuhan, China. On March 11, 2020, the World Health Organization designated the outbreak of COVID-19, the disease associated with SARS-CoV-2, as a global pandemic. Governments and businesses around the world have taken unprecedented actions to mitigate the spread of COVID-19, including, but not limited to, shelter-in-place orders, quarantines, significant restrictions on travel, as well as restrictions that prohibit many employees from going to work.

The Company has been actively monitoring the impact of the COVID-19 pandemic, including variants, on its employees and business. Although some research and development timelines have been impacted by delays related to the COVID-19 pandemic, the Company has not experienced material financial impacts on its business and operations as a result of the COVID-19 pandemic. The Company has undertaken a number of business continuity measures to mitigate potential disruption to its operations and in order to preserve the integrity of its research and development programs. The extent of the impact of COVID-19 on the Company’s future operational and financial performance will depend on certain developments, including the duration and spread of the pandemic, including its variants, the rate and success of vaccination roll-out efforts, impact on employees and vendors all of which are uncertain and cannot be predicted. At this point, the extent to which COVID-19 may impact the Company’s future financial condition or results of operations is uncertain.

Liquidity and Going Concern

The Company has incurred significant losses and negative cash flows from operations since its inception. As of June 30, 2021, the Company had cash and cash equivalents of $453.6 million and its accumulated deficit was $237.8 million. The Company has historically financed its operations through the sale of equity securities, sale of convertible notes and revenue generated from licensing and collaboration arrangements. The Company has not generated any revenues to date from the sale of its product candidates and does not anticipate generating any revenues from the sale of its product candidates unless and until it successfully completes development and obtains regulatory approval to market its product candidates.

The Company currently expects that its existing cash as of June 30, 2021 will be sufficient to fund its operating expenses and capital expenditure requirements for at least the next 12 months from the date the unaudited condensed consolidated financial statements are issued.

2. Basis of Presentation and Summary of Significant Accounting Policies

Basis of Presentation

The accompanying condensed consolidated financial statements, which include the accounts of ATAI, its wholly owned subsidiaries and controlled entities, are presented in accordance with generally accepted accounting principles in the United States of America (“GAAP”) and applicable rules and regulations of SEC regarding interim financial reporting. Certain information and footnote disclosures normally included in the financial statements prepared in accordance with U.S. GAAP have been condensed or omitted in accordance with such rules and regulations. All intercompany transactions and accounts have been eliminated in consolidation.

8

The unaudited interim condensed consolidated financial statements have been prepared on the same basis as the annual financial statements and, in the opinion of management, reflect all adjustments, which include only normal recurring adjustments, necessary for a fair statement of the Company’s financial position, its results of operations and comprehensive loss, and its cash flows for the periods presented. The results of operations for the three and six months ended June 30, 2021 are not necessarily indicative of the results to be expected for the year ending December 31, 2021 or for any other future annual or interim period.

These condensed consolidated financial statements should be read in conjunction with the Company’s audited consolidated financial statements included in the prospectus dated June 17, 2021 (“Prospectus”) that forms a part of the Company’s Registration Statements on Form S-1 (File Nos. 333-255383 and 333-257184), as filed with the SEC pursuant to Rule 424(b)(4) promulgated under the Securities Act of 1933, as amended.

Significant Accounting Policies

During the six months ended June 30, 2021, there were no significant changes to the Company’s significant accounting policies as described in the Company’s audited consolidated financial statement as of and for the year ended December 31, 2020 except as described below.

Use of Estimates

The preparation of condensed consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements, and the reported amounts of expenses during the reporting period. Significant estimates and assumptions made in the accompanying condensed consolidated financial statements include, but are not limited to the fair value of the Company’s short term notes receivable—related party with COMPASS Pathways plc, convertible promissory notes issued in connection with the 2020 convertible note agreement (the “2020 Convertible Notes”), contingent consideration liability—related parties, derivative liability associated with the Perception convertible promissory notes, redeemable noncontrolling interests, and IPR&D assets and noncontrolling interests recognized in acquisitions, the valuations of common shares and share-based awards, and accruals for research and development costs.

The Company bases its estimates on historical experience and on various other assumptions that are believed to be reasonable. Actual results may differ from those estimates or assumptions.

Cash and Cash Equivalents

The Company considers all highly liquid investments purchased with original maturities of three months or less from the purchase date to be cash equivalents. As of June 30, 2021 and December 31, 2020, cash and cash equivalents consisted of cash on deposit and cash held in high-yield savings accounts and money market funds.

Fair Value Measurements

Assets and liabilities recorded at fair value on a recurring basis in the consolidated balance sheets are categorized based upon the level of judgment associated with the inputs used to measure their fair values. Fair value is defined as the exchange price that would be received for an asset or an exit price that would be paid to transfer a liability in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. Valuation techniques used to measure fair value must maximize the use of observable inputs and minimize the

9

use of unobservable inputs. The authoritative guidance on fair value measurements establishes a three-tier fair value hierarchy for disclosure of fair value measurements as follows:

Level 1—Observable inputs such as unadjusted, quoted prices in active markets for identical assets or liabilities at the measurement date;

Level 2—Inputs (other than quoted prices included in Level 1) are either directly or indirectly observable for the asset or liability. These include quoted prices for similar assets or liabilities in active markets and quoted prices for identical or similar assets or liabilities in markets that are not active; and

Level 3—Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities.

To the extent that the valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised by the Company in determining fair value is greatest for instruments categorized in Level 3. A financial instrument’s level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement.

The Company’s contingent consideration liability—related parties, the 2020 Convertible Notes, derivative liability associated with the Perception convertible promissory notes, investment in Intelgenx Technologies Corp. Initial Warrants and Additional Units Warrant and warrant liability with Neuronasal Inc. are carried at fair value, determined according to Level 3 inputs in the fair value hierarchy described above (See Note 7). The carrying amount reflected in the accompanying consolidated balance sheets for cash, prepaid expenses and other current assets, accounts payable and accrued expenses approximate their fair values, due to their short-term nature.

The carrying amounts of the Company’s convertible promissory notes—related parties issued in 2018 and 2020 (collectively, the “2018 Convertible Notes”) do not approximate fair value because the fair value is driven by the underlying value of the Company’s common stock to which the notes are able to be converted. As of June 30, 2021, the carrying amount and fair value amount of the convertible promissory notes issued in 2018 was $0.2 million and $44.3 million, respectively. As of June 30, 2021, the carrying amount and fair value amount of the convertible promissory notes issued in 2020 was $1.0 million and $232.3 million, respectively. As of December 31, 2020, the carrying amount and fair value amount for convertible promissory note issued in 2018 was $0.2 million and $12.3 million, respectively. As of December 31, 2020, the carrying amount and fair value amount for convertible promissory note issued in 2020 was $1.0 million and $64.4 million, respectively.

The carrying amounts of the Perception convertible promissory notes issued during 2020, do not approximate fair value because carrying amounts are net of unamortized debt discounts. The fair value of the Perception convertible promissory notes was determined based on the changes in expectation and increase in probability of occurrence of certain conversion events, including a qualified equity financing and a licensing transaction, that would have beneficial conversion terms for the note holders. In June 2021, Perception convertible promissory notes converted into shares of Series A preferred stock of Perception pursuant to their original terms. As of June 30, 2021, there were no Perception convertible promissory notes outstanding. As of December 31, 2020, the carrying amount and fair value amount for Perception convertible promissory notes was $0.8 million and $4.6 million, respectively. See Note 10 for additional discussion.

Fair Value Option

As permitted under Accounting Standards Codification 825, Financial Instruments, or ASC 825, the Company has elected the fair value option to account for its investment in IntelGenx Technologies Corp. (“IntelGenx”) common stock which otherwise would be subject to ASC 323. In accordance with ASC 825, the Company records these common stock investments at fair value with changes in fair value recorded as a component of other income (expense), net in the consolidated statement of operations and comprehensive loss.

10

Convertible Promissory Notes and Derivative Instruments

The Company does not use derivative instruments to hedge exposures to interest rate, market, or foreign currency risks. The Company evaluates all of its financial instruments, including convertible promissory notes, to determine if such instruments contain features that meet the definition of embedded derivatives. Embedded derivatives must be separately measured from the host contract if all the requirements for bifurcation are met. The assessment of the conditions surrounding the bifurcation of embedded derivatives depends on the nature of the host contract. Bifurcated embedded derivatives are recognized at fair value, with changes in fair value recognized in the consolidated statements of operations at each reporting period. Bifurcated embedded derivatives are classified with the related host contract in the Company’s consolidated balance sheets.

On March 16, 2020, Perception entered into a convertible promissory note agreement with the Company and other investors, including related parties, which provided for the issuance of convertible notes of $3.3 million to the Company and $0.6 million to other investors. On December 1, 2020, Perception entered into an additional convertible promissory note agreement with the Company and other investors, including related parties, which provided for the issuance of convertible notes of up to $12.0 million to the Company in aggregate of which (i) $6.2 million and $0.8 million were issued in December 2020 and January 2021, respectively, under the First Tranche Funding and (ii) $5.0 million was issued under the Second Tranche Funding (See Note 10). The Perception convertible promissory notes issued to the Company represent intercompany debt and are eliminated upon consolidation.

In addition, the Perception convertible promissory notes contain certain embedded features, which are redemption features and meet the definition of derivative instruments. The Company classifies these instruments as a liability on its consolidated balance sheets as the redemption features involve substantial discounts, provide for the accelerated repayment of the notes upon the occurrence of specified events, and are not clearly and closely related to its host instrument. The derivative liability was initially recorded at fair value upon issuance of the convertible promissory notes and is subsequently remeasured to fair value at each reporting date. Both the Perception convertible promissory notes and the derivative liability have been classified as long-term and presented as convertible promissory notes and derivative liability in the Company’s consolidated balance sheets.

Changes in the fair value of the derivative asset and liability are recognized as a component of other income (expense), net in the consolidated statements of operations. Changes in the fair value of the derivative asset and liability will continue to be recognized until the warrants and convertible promissory notes are no longer outstanding.

Warrant Liability

The Company accounts for the warrants in accordance with the guidance contained in ASC 815-40 under which the warrants do not meet the criteria for equity treatment and must be recorded as liabilities and is included other liabilities in the consolidated balance sheet. Accordingly, we classify the warrants as liabilities at their fair value and adjust the warrants to fair value at each reporting period. This liability is subject to re-measurement at each balance sheet date until exercised, and any change in fair value is recognized in our statement of operations. The fair value of the warrant liability is measured using a Black Scholes pricing model. Assumptions and estimates are made in determining an appropriate risk-free interest rate, volatility, term, dividend yield, discount due to exercise restrictions, and the fair value of common stock. Any significant adjustments to the unobservable inputs would have a direct impact on the fair value of the warrant liability.

Licenses of Intellectual Property

The Company may enter into collaboration and licensing arrangements for research and development, manufacturing, and commercialization activities with counterparties for the development and commercialization of its product candidates. The agreements may have units of account within the scope of ASC 606 where the counterparties meet the definition of a customer as well as units of account within the scope of ASC 808 where both parties are determined to be active participants.

The arrangements may contain multiple components, which may include (i) licenses, or options to obtain licenses to the Company’s intellectual property or sale of the Company’s license, (ii) research and development

11

activities, (iii) participation on joint steering committees, and (iv) the manufacturing of commercial, clinical or preclinical material. Payments pursuant to these arrangements may include non-refundable, upfront payments, milestone payments upon the achievement of significant development events, research and development reimbursements, sales milestones, and royalties on product sales. The amount of variable consideration is constrained until it is probable that the revenue is not at a significant risk of reversal in a future period. The contracts into which the Company enters generally do not include significant financing components.

In determining the appropriate amount of revenue to be recognized as it fulfills its obligations under each of its collaboration and license agreements, the Company performs the following steps: (i) identification of the promised goods or services in the contract within the scope of ASC 606; (ii) determination of whether the promised goods or services are performance obligations including whether they are capable of being distinct and distinct in the context of the contract; (iii) measurement of the transaction price, including the constraint on variable consideration; (iv) allocation of the transaction price to the performance obligations; and (v) recognition of revenue when (or as) the Company satisfies each performance obligation. As part of the accounting for these arrangements, the Company must use significant judgment to determine: a) the number of performance obligations based on the determination under step (ii) above; b) the transaction price under step (iii) above; c) the stand-alone selling price for each performance obligation identified in the contract for the allocation of transaction price in step (iv) above; and d) the measure of progress in step (v) above. The Company uses judgment to determine whether milestones or other variable consideration, except for sales-based milestones and royalties on license arrangements, should be included in the transaction price as described further below.

If a license to the Company’s intellectual property is determined to be distinct from the other promises or performance obligations identified in the arrangement, the Company recognizes revenue from consideration allocated to the license when the license is transferred to the customer and the customer is able to use and benefit from the license. In assessing whether a promise or performance obligation is distinct from the other elements, the Company considers factors such as the research, development, manufacturing and commercialization capabilities of the counterparties and the availability of its associated expertise in the general marketplace. In addition, the Company considers whether the counterparties can benefit from a promise for its intended purpose without the receipt of the remaining elements, whether the value of the promise is dependent on the unsatisfied promise, whether there are other vendors that could provide the remaining promise, and whether it is separately identifiable from the remaining promise. For licenses that are combined with other promises, the Company utilizes judgment to assess the nature of the combined performance obligation to determine whether the combined performance obligation is satisfied over time or at a point in time and, if over time, the appropriate method of measuring progress for purposes of recognizing revenue. The Company evaluates the measure of progress as of each reporting period and, if necessary, adjusts the measure of performance and related revenue recognition. The measure of progress, and thereby periods over which revenue should be recognized, is subject to estimates by management and may change over the course of the arrangement. Such a change could have a material impact on the amount of revenue the Company records in future periods.

Customer Options: If an arrangement is determined to contain customer options that allow the customer to acquire additional goods or services such as research and development services or manufacturing services, the goods and services underlying the customer options are not considered to be performance obligations at the inception of the arrangement unless a material right is provided to the customer. If the customer option does not represent a material right, the obligation to provide such goods and services is contingent on exercise of the option, and the associated consideration is not included in the transaction price. If a customer option is determined to include a significant and incremental discount and, therefore, represents a material right, the material right is recognized as a separate performance obligation at the outset of the arrangement. The Company allocates the transaction price to material rights based on the relative standalone selling price.

Milestone Payments: At the inception of each arrangement that includes milestone payments, the Company evaluates whether the milestones are considered probable of being achieved and estimates the amount to be included in the transaction price using the most-likely amount method. If it is probable that a significant revenue reversal would not occur, the associated milestone value is included in the transaction price. Milestone payments that are not within the control of the Company or the licensee, such as regulatory approvals, are not considered probable of being achieved until those approvals are received. The Company evaluates factors such as the scientific, clinical, regulatory, commercial, and other risks that must be overcome to achieve the respective milestone in making this assessment. There is considerable judgment involved in determining whether it is probable that a significant revenue reversal would not occur. At the end of each subsequent reporting period, the Company reevaluates the probability

12

of achievement of all milestones subject to constraint and, if necessary, adjusts its estimate of the overall transaction price. Any such adjustments are recorded on a cumulative catch-up basis, which would affect revenues and earnings in the period of adjustment.

Royalties: For license arrangements that include sales-based royalties, including milestone payments based on a level of sales, and the license is deemed to be the predominant item to which the royalties relate, the Company recognizes revenue at the later of (i) when the related sales occur, or (ii) when the performance obligation to which some or all of the royalty has been allocated has been satisfied (or partially satisfied). To date, the Company has not recognized any royalty revenue resulting from any of its licensing arrangements.

Stock-Based Compensation

The Company accounts for all stock-based payment awards granted to employees, directors and non-employees as stock-based compensation expense based on their grant date fair value. The Company grants equity awards under its stock-based compensation programs, which may include stock options and restricted common stock. The measurement date for employee awards is the date of grant, and stock-based compensation costs are recognized as expense over the requisite service period, which is the vesting period, on a straight-line basis. Since the adoption of ASU 2018-07, the measurement date for non-employee awards is the date of grant, and stock-based compensation costs are recognized in the same period and in the same manner as if the entity had paid cash for the goods or services. Stock-based compensation expense is classified in the accompanying condensed consolidated statements of operations based on the function to which the related services are provided. The Company has elected to recognize forfeitures of stock-based compensation awards as they occur.

The Company recognizes the compensation cost of awards subject to service-based and performance-based vesting conditions using the accelerated attribution method over the requisite service period if the performance- based vesting conditions are probable of being met. Recognition of compensation cost relating to awards that vest on a “Liquidity Event” (as defined in the award or Partnership agreements) will be deferred until the consummation of such transaction.

The Company calculates the fair value of stock options granted using the Black-Scholes option-pricing model with the following assumptions:

Expected Volatility—The Company estimated volatility for option grants by evaluating the average historical volatility of a peer group of companies for the period immediately preceding the option grant for a term that is approximately equal to the options’ expected life.

Expected Term—The expected term of the Company’s options represents the period that the stock-based awards are expected to be outstanding. The Company has generally elected to use the “simplified method” by analogy for estimating the expected term of options, whereby the expected term equals the arithmetic average of the vesting term and the original contractual term of the option.

Risk-Free Interest Rate—The risk-free interest rate is based on the implied yield with an equivalent expected term at the grant date.

Dividend Yield—The Company has not declared or paid dividends to date and does not anticipate declaring dividends. As such, the dividend yield has been estimated to be zero.

As part of the valuation of stock-based compensation under the Black-Scholes option pricing model, it is necessary for the Company to estimate the fair value of its common stock. Prior to the closing of the IPO, the fair value of the Company’s common stock was estimated on each grant date. Given the absence of a public trading market, and in accordance with the American Institute of Certified Public Accountants’ Practice Guide, Valuation of Privately-Held-Company Equity Securities Issued as Compensation, the Company exercised reasonable judgment and considered numerous objective and subjective factors to determine its best estimate of the fair value of its common stock. The estimation of the fair value of the common stock considered factors including the following: the estimated present value of the Company’s future cash flows; the Company’s business, financial condition and results of operations; the Company’s forecasted operating performance; the illiquid nature of the Company’s common stock; industry information such as market size and growth; market capitalization of comparable companies and the estimated value of transactions such companies have engaged in; and macroeconomic conditions.

After the closing of the IPO, the Company’s board of directors determined the fair value of each share of common stock underlying stock-based awards based on the closing price of the Company’s common stock as reported by Nasdaq on the date of grant.

13

Net Income (Loss) per Share Attributable to Common Stockholders

The Company computed basic net income (loss) per share attributable to common stockholders by dividing net income (loss) attributable to common stockholders by the weighted-average number of common stock outstanding for the period, without consideration for potentially dilutive securities. The Company computes diluted net income (loss) per common share after giving consideration to all potentially dilutive common stock, including convertible notes and stock options, outstanding during the period determined using the if-converted and treasury-stock methods, respectively, except where the effect of including such securities would be antidilutive.

Recently Adopted Accounting Pronouncements

In August 2020, the FASB issued ASU 2020-06, “Debt—Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815—40)” (“ASU 2020-06”). ASU 2020-06 simplifies the accounting for certain financial instruments with characteristics of liabilities and equity, including convertible instruments and contracts on an entity’s own equity. The ASU is part of the FASB’s simplification initiative, which aims to reduce unnecessary complexity in U.S. GAAP. The ASU’s amendments are effective for the Company for fiscal years beginning after December 15, 2023 and interim periods within those fiscal years, with early adoption permitted. The Company early adopted this standard on January 1, 2021 applying the modified retrospective transition approach. Upon adoption of ASU 2020-06, the embedded conversion option related to the 2018 Convertible Notes is no longer separated from the host contract and recognized within additional paid-in-capital and is instead accounted for as a single liability measured at amortized cost within convertible promissory notes—related parties in the condensed consolidated balance sheets. Therefore, the unamortized debt discount of $8,000 was eliminated.

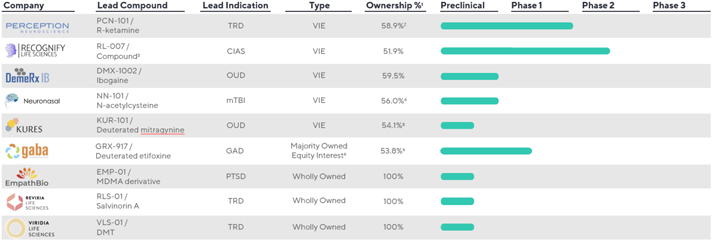

3. Acquisitions

2021 Acquisitions

PsyProtix, Inc.

In February 2021, the Company jointly formed PsyProtix with Chymia, LLC (“Chymia”). PsyProtix was created for the purpose of exploring and developing a metabolomics-based precision psychiatry approach, initially targeting the stratification and treatment of Treatment Resistant Depression (“TRD”) patients. In February 2021, pursuant to a Series A Preferred Stock Purchase Agreement (the “PsyProtix Purchase Agreement”), the Company acquired shares of PsyProtix’s Series A preferred stock in exchange for an initial payment of $0.1 million in cash. In addition, pursuant to the PsyProtix Purchase Agreement, the Company agreed to make aggregate payments to PsyProtix of up to $4.9 million upon the achievement of specified clinical milestones to complete the purchase of the shares and provide additional funding to PsyProtix. The PsyProtix Purchase Agreement resulted in the Company holding a 75.0% voting interest and Chymia holding a 25.0% voting interest in PsyProtix. In connection with the Company’s agreement for additional funding, PsyProtix issued the corresponding Series A preferred shares to the Company provided that the shares are held in an escrow account (the “PsyProtix Escrow Shares”). The PsyProtix Escrow Shares will be released, from time to time, to the Company upon PsyProtix achieving certain milestones as defined in the PsyProtix Purchase Agreement with cash payments to be made by the Company. In addition, the Company has the right, but not the obligation, to make payment for the certain PsyProtix Escrow Shares at any time, regardless of the achievement of any milestones. The PsyProtix Escrow Shares have voting and all other rights until an event of default occurs where the Company fails to make a payment within 10 days following the written notice

14

of the achievement of the relevant milestone. In the event of default, a pro rata portion of the PsyProtix Escrow Shares will automatically be surrendered and be deemed forfeited and canceled, and could result in the Company losing control of PsyProtix’s board of directors and its controlling financial interest in PsyProtix. In addition, prior to the occurrence of the earlier of a certain milestone event or reaching of the Company’s capital contribution threshold of $5.0 million, PsyProtix will issue additional shares of common stock to Chymia to maintain Chymia’s current ownership percentage. This anti-dilution right was concluded to be embedded in the common shares held by Chymia.

Immediately following the closing of the PsyProtix Purchase Agreement, PsyProtix loaned $0.1 million to Chymia in exchange for a duly executed promissory note (the “Chymia Note”). The Chymia Note shall accrue interest at a 5% rate per annum until payment in full. The aggregate principal amount of $0.1 million, together with all accrued and unpaid interest and all other amounts payable are due to be paid on the date that is the earlier of (i) five years from the promissory note agreement date or (ii) the occurrence of a liquidation event or a deemed liquidation event (as defined in the PsyProtix’s certificate of incorporation). As of June 30, 2021, the Chymia Note was $0.1 million and included as a component of long-term notes receivable—related parties on the condensed consolidated balance sheets.

The PsyProtix Purchase Agreement provided the Company unilateral rights to control all decisions related to the significant activities of PsyProtix. The Company concluded that PsyProtix was not considered a business based on its assessment under ASC 805 and accounted for the Company’s acquisition in PsyProtix as an initial consolidation of a VIE that is not a business under ASC 810 (See Note 4). The assets acquired, liabilities assumed, and noncontrolling interest in the transaction were measured based on their fair values. The Company did not recognize a gain or a loss in connection with the consolidation of PsyProtix as the fair value of the consideration paid of $0.1 million was equivalent to the fair value of the identifiable assets acquired of $0.1 million.

Psyber, Inc.

Psyber is a globally based startup focused on the development of brain-computer interface-enabled digital therapeutics for treating mental health issues. Psyber was created as a joint venture between the Company and the founders of Psyber. In February 2021, pursuant to a Series A Preferred Stock Purchase Agreement (the “Psyber Purchase Agreement”), the Company acquired shares of Psyber’s Series A preferred stock in exchange for an initial payment of $0.2 million in cash. In addition, pursuant to the Psyber Purchase Agreement, the Company agreed to make aggregate payments to Psyber of up to $1.8 million upon the achievement of specified clinical milestones to complete the purchase of the shares and provide additional funding to Psyber. The Psyber Purchase Agreement resulted in the Company holding a 75.0% voting interest and the founders of Psyber jointly holding a 25.0% voting interest in Psyber. In connection with the Company’s agreement for additional funding, Psyber issued the corresponding Series A preferred shares to the Company provided that the shares are held in an escrow account (the “Psyber Escrow Shares”). The Psyber Escrow Shares will be released, from time to time, to the Company upon Psyber achieving certain milestones as defined in the Psyber Purchase Agreement with cash payments to be made by the Company. In addition, the Company has the right, but not the obligation, to make payment for the certain Psyber Escrow Shares at any time, regardless of the achievement of any milestones. The Psyber Escrow Shares have voting and all other rights until an event of default occurs where the Company fails to make a payment within 10 days following the written notice of the achievement of the relevant milestone. In the event of default, a pro rata portion of the Psyber Escrow Shares will automatically be surrendered and be deemed forfeited and canceled, and could result in the Company losing control of Psyber’s board of directors and its controlling financial interest in Psyber. In addition, prior to the occurrence of the earlier of a certain milestone event or reaching of the Company’s capital contribution threshold of $2.0 million, Psyber will issue additional shares of common stock to the founders of Psyber to maintain the founders’ current ownership percentage. This anti-dilution right was concluded to be embedded in the common shares held by the founders of Psyber.

The Psyber Purchase Agreement provided the Company unilateral rights to control all decisions related to the significant activities of Psyber. The Company concluded that Psyber was not considered a business based on its assessment under ASC 805 and accounted for the Company’s acquisition in Psyber as an initial consolidation of a VIE that is not a business under ASC 810 (See Note 4). The assets acquired, liabilities assumed, and noncontrolling interest in the transaction were measured based on their fair values. The Company recognized a gain on consolidation of $2,000. The gain was calculated as the sum of the consideration paid of $0.2 million, less the fair value of identifiable net assets acquired of $0.2 million.

15

InnarisBio, Inc.

In February 2021, the Company jointly formed InnarisBio with UniQuest Pty Ltd (“UniQuest”) for the purpose of adding a solgel-based direct-to-brain intranasal drug delivery technology to the Company’s platform. In March 2021, pursuant to a Series A Preferred Stock Purchase Agreement (the “InnarisBio Purchase Agreement”), the Company acquired shares of InnarisBio’s Series A preferred stock in exchange for an initial payment of $1.1 million in cash. In addition, pursuant to the InnarisBio Purchase Agreement, the Company agreed to make aggregate payments to InnarisBio of up to $3.9 million upon the achievement of specified clinical milestones to complete the purchase of the shares and provide additional funding to InnarisBio. The InnarisBio Purchase Agreement resulted in the Company holding an 82.0% voting interest and UniQuest holding a 18.0% voting interest in InnarisBio. In connection with the Company’s agreement for additional funding, InnarisBio issued the corresponding Series A preferred shares to the Company provided that the shares are held in an escrow account (the “InnarisBio Escrow Shares”). The InnarisBio Escrow Shares will be released, from time to time, to the Company upon InnarisBio achieving certain milestones as defined in the InnarisBio Purchase Agreement with cash payments to be made by the Company. In addition, the Company has the right, but not the obligation, to make payment for the certain InnarisBio Escrow Shares at any time, regardless of the achievement of any milestones. The InnarisBio Escrow Shares have voting and all other rights until an event of default occurs where the Company fails to make a payment within 10 days following the written notice of the achievement of the relevant milestone. In the event of default, a pro rata portion of the InnarisBio Escrow Shares will automatically be surrendered and be deemed forfeited and cancelled and could result in the Company losing control of InnarisBio’s board of directors and its controlling financial interest in InnarisBio.

The InnarisBio Purchase Agreement provided the Company unilateral rights to control all decisions related to the significant activities of InnarisBio. The Company concluded that InnarisBio was not considered a business based on its assessment under ASC 805 and accounted for the Company’s acquisition in InnarisBio as an initial consolidation of a VIE that is not a business under ASC 810 (See Note 4). The assets acquired, liabilities assumed, and noncontrolling interest in the transaction were measured based on their fair values. The Company recognized a loss on consolidation of $7,000 for the six months ended June 30, 2021. The loss was calculated as the sum of the consideration paid of $1.1 million, the fair value of the noncontrolling interest issued of $0.9 million, less the fair value of identifiable net assets acquired of $2.0 million. The fair value of the contingent milestone payments of $0.1 million was included in the total purchase consideration for the noncontrolling interest and recognized as a liability by InnarisBio at the date of acquisition. The fair value of the IPR&D acquired of $1.0 million was reflected as acquired in-process research and development expense on the condensed consolidated statements of operations as it had no alternative future use at the time of the acquisition.

Neuronasal, Inc.

Neuronasal, Inc. (“Neuronasal”) is developing a novel intranasal formulation of N-acetylcysteine for acute mild traumatic brain injury. The Company first acquired investments in Neuronasal in December 2019 pursuant to a Preferred Stock Purchase Agreement (the “Neuronasal PSPA”). In December 2019, in connection with the original purchase of the preferred shares, Neuronasal and the Company entered into the Secondary Sale and Put Right Agreement (the “Neuronasal Secondary Sale Agreement”), whereby upon the achievement of certain contingent development milestones, existing common shareholders have the right to sell and the Company has the option but not the obligation to purchase additional shares of common stock at a price determined based on the fair market value per share on the date of exercise. These options are contingent upon the exercise of the options by Neuronasal’s common shareholders to sell shares to the Company. On March 10, 2021, pursuant to the Neuronasal PSPA, the Company purchased additional Series A preferred shares for approximately $0.8 million based on the achievement of certain development milestones. Also, pursuant to the Neuronasal Secondary Sale Agreement, the Company purchased additional common shares for approximately $0.3 million. On May 17, 2021, pursuant to the Neuronasal PSPA the Company exercised its option to purchase additional shares of Series A preferred stock of Neuronasal for an aggregate cost of $1.0 million. The additional purchase on May 17, 2021 resulted in the Company obtaining an aggregate 55.99% ownership interest in Neuronasal, including the Company’s previously acquired investments in Neuronasal’s common and preferred stock, and provided the Company with control of Neuronasal’s board of directors and the unilateral rights to control all decisions related to the significant activities of Neuronasal. Prior to May 17, 2021, the Company accounted for its investments in Neuronasal’s common stock under the equity method and Neuronasal’s preferred stock under the measurement alternative (See Note 5). Following the closing of this acquisition on May 17, 2021, the results of Neuronasal have been consolidated in the Company’s consolidated financial statements.

16