UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

----------------------------------------------------------------

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-23630

----------------------------------------------------------------

Cliffwater Enhanced Lending Fund

(Exact name of registrant as specified in charter)

----------------------------------------------------------------

c/o UMB Fund Services, Inc.

235 West Galena Street

Milwaukee, WI 53212

Registrant’s telephone number, including area code: (414) 299-2000

Timothy M. Bonin

235 West Galena Street

Milwaukee, WI 53212

(Name and address of agent for service)

----------------------------------------------------------------

Date of fiscal year end: March 31

Date of reporting period: March 31, 2024

Item 1. Report to Shareholders

(a) | The annual report of the registrant for the year ended March 31, 2024 transmitted to shareholders pursuant to Rule 30e-1 promulgated under the Investment Company Act of 1940, as amended (the “1940 Act”), is as follows: |

CLIFFWATER ENHANCED LENDING FUND

![]()

Annual Report

For the Year Ended March 31, 2024

Cliffwater Enhanced Lending Fund |

Table of Contents For the Year Ended March 31, 2024 |

2 | ||

4 | ||

5 | ||

6 | ||

26 | ||

27 | ||

28 | ||

29 | ||

31 | ||

33 | ||

64 | ||

66 | ||

68 |

This report is submitted for the general information of the shareholders of the Fund. It is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus, which includes information regarding the Fund’s risks, objectives, fees and expenses, experience of its management and other information.

www.cliffwaterfunds.com

1

To our shareholders:

The Cliffwater Enhanced Lending Fund (“the Fund”) recently completed its first two- and three-quarter years of operation, and we want to thank you for the trust you have placed in us.

Performance has been consistently strong relative to the Fund’s objective. The Cliffwater Enhanced Lending Fund produced a net 12.60% return from its July 1, 2021 inception, through March 31, 2024. This compares to a 6.01% return for the Morningstar LSTA Leveraged Loan Index. The Fund also reported relatively consistent monthly returns. Its annualized standard deviation measured 1.04% for the same period.

The Fund experienced strong investor inflows over the last year, with net-asset-value growing from $1.5 billion on March 31, 2023, to $2.9 billion on March 31, 2024. This asset growth has been supported by significant investment in personnel and technology to grow our platform, and the onboarding of additional strategic lending partners to access high quality private debt. Factors materially affecting the Fund’s performance during the most recently completed fiscal year include a high current cash yield and accretive discounted secondary transactions.

We remain confident in the Fund’s continued performance despite the uncertain economic environment brought by inflation and rising interest rates. We believe that, during the past year, the Fund’s 11.0% distribution rate remained attractive and the floating-rate nature of most of our loans helped mitigate interest rate risk.

We again sincerely thank you for your support.

Regards,

Stephen L. Nesbitt

Chief Investment Officer

Cliffwater LLC

2

Cliffwater Enhanced Lending Fund |

Letter to Shareholders March 31, 2024 (Unaudited) (Continued) |

The Fund’s investment program is speculative and entails substantial risks. There can be no assurance that the Fund’s investment objectives will be achieved or that its investment program will be successful. Investors should consider the Fund as a supplement to an overall investment program and should invest only if they are willing to undertake the risks involved. Investors could lose some or all of their investment.

Shares are an illiquid investment.

We do not intend to list the Fund’s shares (“Shares”) on any securities exchange and we do not expect a secondary market in the Shares to develop.

You should generally not expect to be able to sell your Shares (other than through the limited repurchase process), regardless of how we perform.

Although we are required to implement a Share repurchase program, only a limited number of Shares will be eligible for repurchase by us.

You should consider that you may not have access to the money you invest for an indefinite period of time.

An investment in the Shares is not suitable for you if you have foreseeable need to access the money you invest.

Because you will be unable to sell your Shares or have them repurchased immediately, you will find it difficult to reduce your exposure on a timely basis during a market downturn.

The Fund is a non-diversified management investment company and may be more susceptible to any single economic or regulatory occurrence than a diversified investment company. Cybersecurity risks have significantly increased in recent years and the Fund could suffer such losses in the future. One of the fundamental risks associated with the Fund’s investments is the risk that an issuer will be unable to make principal and interest payments on its outstanding debt obligations when due. Other risk factors include interest rate risk (a rise in interest rates causes a decline in the value of debt securities) and prepayment risk (the debtor may pay its obligation early, reducing the amount of interest payments).

3

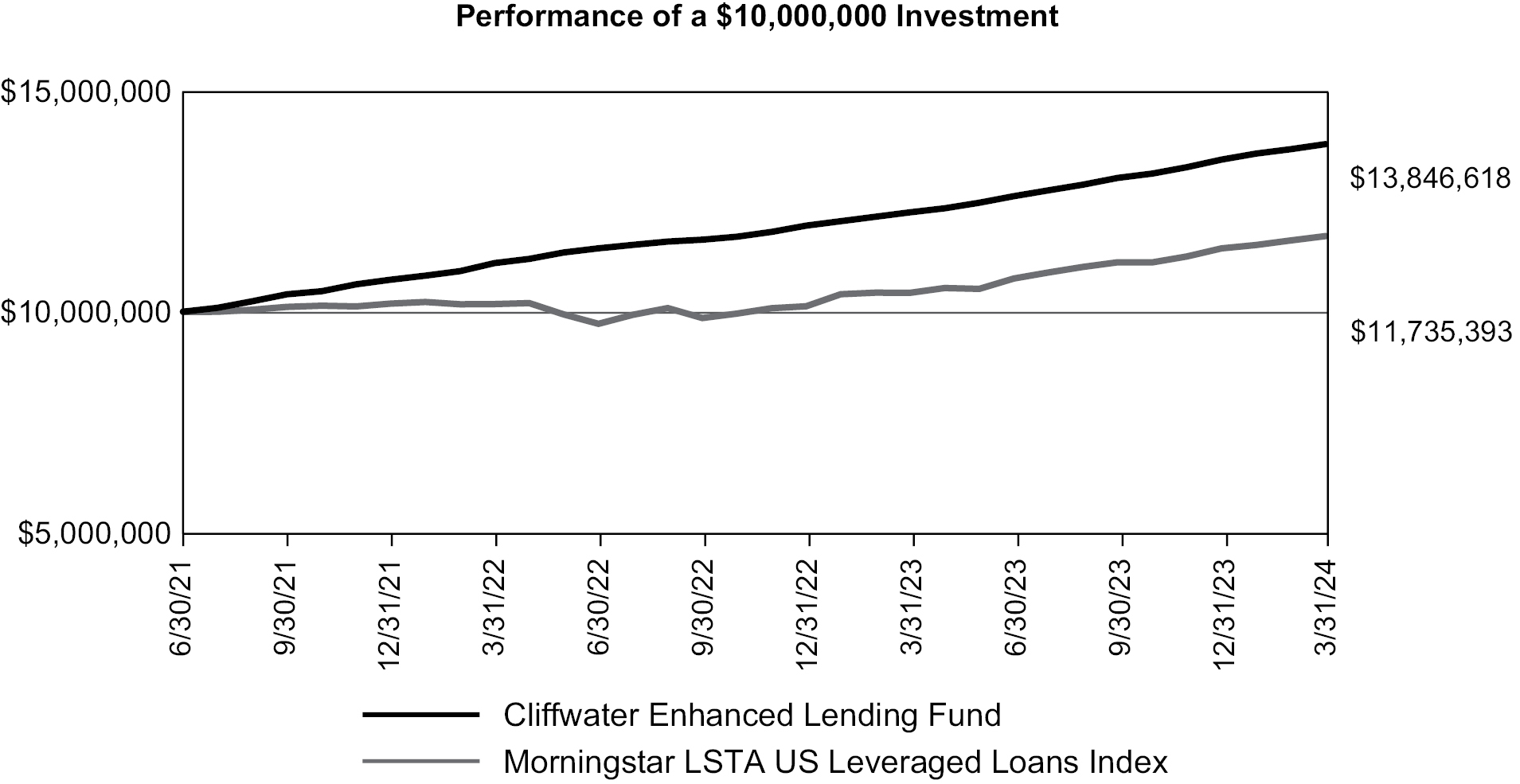

This graph compares a hypothetical $10,000,000 investment in the Fund’s Class I Shares with a similar investment in the Morningstar LSTA US Leveraged Loans Index (previously named S&P LSTA US Leveraged Loans Index). The index does not serve as a benchmark for the Fund and is shown for illustrative purposes only. The Fund does not have a designated performance benchmark. Results include the reinvestment of all dividends and capital gains. The index does not reflect expenses, fees, or sales charges, which would lower performance.

The Morningstar LSTA US Leveraged Loans Index is designed to deliver comprehensive, precise coverage of the US leveraged loan market. The Morningstar LSTA US Leveraged Loans Index is a market value weighted index tracking institutional leveraged loans in the United States based upon market weightings, spreads and interest payment, including Term Loan A, Term Loan B and Second Lien tranches. The Morningstar LSTA US Leveraged Loans Index is unmanaged and it is not available for investment.

Average Annual Total Returns as of March 31, 2024 | 1 Year | Since | ||||

Cliffwater Enhanced Lending Fund (Inception Date July 1, 2021) | 12.74 | % | 12.56 | % | ||

Morningstar LSTA US Leveraged Loans Index | 12.47 | % | 5.03 | % | ||

The performance data quoted here represents past performance and past performance is not a guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. The most recent quarter end performance may be obtained by calling 1 (888) 442-4420.

For the period from the Fund’s inception through July 31, 2022, the Investment Manager contractually waived management fees and voluntarily reimbursed expenses for the Fund (together, the “Waiver and Reimbursement”). The performance quoted above reflects the Waiver and Reimbursement in effect through July 31, 2022 and would have been lower in their absence.

For the Fund’s current expense ratios, please refer to the Consolidated Financial Highlights Section of this report.

Returns reflect the reinvestment of distributions made by the Fund, if any. The graph and the performance table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

4

To the Shareholders and Board of Trustees of

Cliffwater Enhanced Lending Fund

Opinion on the Financial Statements

We have audited the accompanying consolidated statement of assets and liabilities, including the consolidated schedules of investments and forward foreign currency exchange contracts, of Cliffwater Enhanced Lending Fund (the “Fund”) as of March 31, 2024, and the related consolidated statements of operations, cash flows, and the statements of changes in net assets, the related notes, and the consolidated financial highlights for each of the periods indicated below (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of March 31, 2024, the results of its operations, its cash flows, the changes in net assets, and the financial highlights for each of the periods indicated below in conformity with accounting principles generally accepted in the United States of America.

Fund Name | Consolidated | Consolidated Statements of | Consolidated Financial |

Cliffwater Enhanced Lending Fund | For the year ended March 31, 2024 | For the years ended March 31, 2024, and 2023 | For the years ended March 31, 2024 and 2023 and the period from July 1, 2022 (commencement of operations) to March 31, 2022 |

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of March 31, 2024, by correspondence with the custodian, brokers, agent banks, and underlying fund administrators or managers; when replies were not received, we performed other auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more investment companies advised by Cliffwater LLC since 2019.

COHEN & COMPANY, LTD.

Cleveland, Ohio

June 5, 2024

5

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||

Private Investment Vehicles — 78.4% |

|

| ||||||||||||||||||||

Investment Partnerships — 66.6% |

|

| ||||||||||||||||||||

AG Asset Based Credit Fund L.P. | USD | N/A | $ | 82,500,000 | $ | 88,644,558 | 1,2,16 | |||||||||||||||

AG Essential Housing Fund II Holdings (DE), L.P. | USD | N/A |

| 12,075,000 |

| 13,280,314 | 1,2,16 | |||||||||||||||

Ares Commercial Finance, LP | USD | N/A |

| 28,535,713 |

| 34,129,618 | 1,2,16 | |||||||||||||||

Ares Pathfinder Fund II (Offshore), LP | USD | N/A |

| 1,831,168 |

| 1,907,110 | 1,2,16 | |||||||||||||||

Ares Priority Loan Co-Invest LP | USD | N/A |

| 28,625,000 |

| 29,357,914 | 1,2,16 | |||||||||||||||

Ares Private Credit Solutions (Cayman), L.P. | USD | N/A |

| 17,429,603 |

| 21,683,661 | 1,2,16 | |||||||||||||||

Ares Special Opportunities Fund II, LP | USD | N/A |

| 17,388,406 |

| 19,343,683 | 1,2,16 | |||||||||||||||

Ares Special Opportunities Fund, LP | USD | N/A |

| 7,597,632 |

| 9,107,784 | 2,16 | |||||||||||||||

Atalaya A4 (Cayman), LP | USD | N/A |

| 29,894,850 |

| 28,121,120 | 1,2,16 | |||||||||||||||

Atalaya Asset Income Fund Evergreen, LP | USD | N/A |

| 10,550,196 |

| 10,333,522 | 1,2,16 | |||||||||||||||

Axonic Private Credit Fund I, LP | USD | N/A |

| 5,235,849 |

| 5,426,151 | 1,2,16 | |||||||||||||||

Banner Ridge DSCO Fund I, LP | USD | N/A |

| 15,480,563 |

| 23,535,766 | 2,16 | |||||||||||||||

Banner Ridge DSCO Fund II (Offshore), LP | USD | N/A |

| 9,691,695 |

| 12,661,648 | 1,2,16 | |||||||||||||||

Banner Ridge Secondary Fund IV (Offshore), LP | USD | N/A |

| 5,219,797 |

| 9,056,513 | 1,2,16 | |||||||||||||||

Banner Ridge Secondary Fund V (Offshore), LP | USD | N/A |

| 14,018,308 |

| 17,590,883 | 1,2,16 | |||||||||||||||

Benefit Street Partners Real Estate Opportunistic Debt Fund L.P. | USD | N/A |

| 54,778,195 |

| 63,004,875 | 1,2,16 | |||||||||||||||

Blue Owl First Lien Fund (Offshore), L.P. | USD | N/A |

| 4,103,056 |

| 4,823,422 | 1,2,16 | |||||||||||||||

Blue Owl Real Estate Fund VI | USD | N/A |

| 2,237,086 |

| 2,252,876 | 1,2,16 | |||||||||||||||

BPC Real Estate Debt Fund, LP | USD | N/A |

| 48,806,204 |

| 54,088,584 | 1,2,16 | |||||||||||||||

BSOF Parallel Onshore Fund L.P. (Class Absolute III Series 3 | USD | N/A |

| 5,242,498 |

| 5,240,662 | 2,16 | |||||||||||||||

BSOF Parallel Onshore Fund L.P. (Class Chestnut II Series 2) | USD | N/A |

| 20,108,879 |

| 20,740,379 | 2,16 | |||||||||||||||

BSOF Parallel Onshore Fund L.P. (Class Gnochi Series 2 Interests) | USD | N/A |

| 30,679,130 |

| 31,111,730 | 2,16 | |||||||||||||||

BSOF Parallel Onshore Fund L.P. (Class Olympic Srt Interests) | USD | N/A |

| 100,000,000 |

| 106,822,534 | 2,16 | |||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

6

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||

Private Investment Vehicles (Continued) |

|

| ||||||||||||||||||||

Investment Partnerships (Continued) |

|

| ||||||||||||||||||||

BSOF Parallel Onshore Fund L.P. (Class Colonnade 2024 Series 3) | USD | N/A | $ | 10,250,000 | $ | 10,280,469 | 2,16 | |||||||||||||||

Burford Advantage Feeder Fund A, LP | USD | N/A |

| 10,681,900 |

| 11,382,923 | 1,2,16 | |||||||||||||||

Callodine Perpetual ABL Fund, LP | USD | N/A |

| 95,526,538 |

| 93,442,869 | 1,2,16 | |||||||||||||||

Carlyle Credit Opportunities Fund (Parallel) II, SCSp | USD | N/A |

| 9,043,286 |

| 9,108,565 | 1,2,16 | |||||||||||||||

CCOF III Nexus Co-Invest Aggregator, L.P. | USD | N/A |

| 5,130,126 |

| 5,145,376 | 2,16 | |||||||||||||||

Comvest Special Opportunities Fund, | USD | N/A |

| 11,650,392 |

| 13,391,994 | 2,16 | |||||||||||||||

Contingency Capital Fund I-A, LP | USD | N/A |

| 45,851,047 |

| 54,543,148 | 1,2,16 | |||||||||||||||

Crestline PF Sentry Fund (US), LP | USD | N/A |

| 4,594,328 |

| 4,643,943 | 2,16 | |||||||||||||||

Crestline Specialty Lending III (U.S.), L.P. | USD | N/A |

| 13,778,564 |

| 15,117,937 | 1,2,16 | |||||||||||||||

D.E. Shaw Diopter International Fund, L.P. | USD | N/A |

| 50,985,204 |

| 52,029,818 | 2,16 | |||||||||||||||

Everberg Capital Partners II, L.P. | USD | N/A |

| 12,884,181 |

| 13,313,791 | 1,2,16 | |||||||||||||||

EVP II LP | USD | N/A |

| 20,173,893 |

| 29,097,716 | 2,16 | |||||||||||||||

Felicitas Secondary Fund II Offshore, | USD | N/A |

| 10,616,857 |

| 15,071,112 | 1,2,16 | |||||||||||||||

Felicitas Tactical Opportunities Fund, | USD | N/A |

| 39,860,000 |

| 56,339,335 | 1,2,16 | |||||||||||||||

Harvest Partners Structured Capital Fund III, L.P. | USD | N/A |

| 12,618,669 |

| 14,383,855 | 1,2,16 | |||||||||||||||

Hayfin Healthcare Opportunities Fund (US Parallel), LP | USD | N/A |

| 17,448,920 |

| 20,879,077 | 1,2,16 | |||||||||||||||

Hercules Private Global Venture Growth Fund I, L.P. | USD | N/A |

| 130,464,177 |

| 133,847,805 | 1,2,16 | |||||||||||||||

HPS Offshore Strategic Investment Partners V, LP | USD | N/A |

| 23,210,756 |

| 24,395,041 | 2,16 | |||||||||||||||

HPS Specialty Loan Fund V-L, L.P. | USD | N/A |

| 21,679,075 |

| 22,601,984 | 1,2,16 | |||||||||||||||

ICG LP Secondaries Fund I (Feeder) SCSp | USD | N/A |

| 9,534,782 |

| 17,691,435 | 2,16 | |||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

7

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||

Private Investment Vehicles (Continued) |

|

| ||||||||||||||||||||

Investment Partnerships (Continued) |

|

| ||||||||||||||||||||

King Street Opportunistic Credit Evergreen Fund, L.P. | USD | N/A | $ | 70,000,000 | $ | 76,574,000 | 1,2,16 | |||||||||||||||

Linden Structured Capital Fund-A, LP | USD | N/A |

| 20,535,021 |

| 26,406,708 | 1,2,16 | |||||||||||||||

Madison Realty Capital Debit Fund, IV | USD | N/A |

| 13,564,062 |

| 18,921,790 | 2,16 | |||||||||||||||

NB Credit Opportunities II Cayman Feeder, LP | USD | N/A |

| 18,685,489 |

| 21,206,341 | 1,2,16 | |||||||||||||||

OrbiMed RCO IV Offshore Feeder, LP | USD | N/A |

| 12,534,441 |

| 12,354,946 | 1,2,16 | |||||||||||||||

Pathlight Capital Evergreen Fund, LP | USD | N/A |

| 34,143,592 |

| 32,427,904 | 1,2,16 | |||||||||||||||

Pathlight Capital Fund II, LP | USD | N/A |

| 32,167,772 |

| 32,537,058 | 1,2,16 | |||||||||||||||

Pennybacker Real Estate Credit II Pacific, LLC | USD | N/A |

| 2,467,491 |

| 2,497,476 | 1,2,16 | |||||||||||||||

Pennybacker Real Estate Credit II, LP | USD | N/A |

| 18,149,241 |

| 17,517,698 | 1,2,16 | |||||||||||||||

Raven Asset-Based Credit Fund II LP | USD | N/A |

| 15,156,811 |

| 16,547,221 | 1,2,16 | |||||||||||||||

Raven Evergreen Credit Fund II, LP | USD | N/A |

| 55,052,265 |

| 65,923,640 | 1,2,16 | |||||||||||||||

Shamrock Capital Debt Opportunities Fund I, LP | USD | N/A |

| 9,992,922 |

| 10,243,492 | 2,16 | |||||||||||||||

Silver Point Specialty Credit Fund II, | USD | N/A |

| 32,200,401 |

| 29,995,814 | 1,2,16 | |||||||||||||||

Sixth Street Growth Partners II (B), | USD | N/A |

| 2,756,161 |

| 2,790,089 | 1,2,16 | |||||||||||||||

Sky Fund V Offshore, LP | USD | N/A |

| 40,764,318 |

| 46,605,538 | 1,2,16 | |||||||||||||||

Specialty Loan Institutional Fund | USD | N/A |

| 3,319,266 |

| 4,805,099 | 2,16 | |||||||||||||||

Summit Partners Credit Offshore Fund II, L.P. | USD | N/A |

| 6,919,667 |

| 5,180,285 | 2,16 | |||||||||||||||

Thompson Rivers LLC | USD | N/A |

| 1,566,992 |

| 712,225 | 1,2,16 | |||||||||||||||

Thorofare Asset Based Lending Fund V, L.P. | USD | N/A |

| 30,401,096 |

| 31,435,671 | 1,2,16 | |||||||||||||||

Tinicum L.P. | USD | N/A |

| 8,069,447 |

| 11,617,105 | 2,16 | |||||||||||||||

Tinicum Tax Exempt, L.P. | USD | N/A |

| 4,068,957 |

| 5,642,174 | 2,16 | |||||||||||||||

Vista Capital Solutions Fund-A, L.P. | USD | N/A |

| 11,768,121 |

| 11,936,250 | 1,2,16 | |||||||||||||||

VPC Asset Backed Opportunistic Credit Fund (Levered), L.P. | USD | N/A |

| 77,440,258 |

| 80,627,854 | 1,2,16 | |||||||||||||||

VPC COV, L.P. | USD | N/A |

| 1,000,000 |

| 1,267,911 | 2,16 | |||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

8

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||

Private Investment Vehicles (Continued) |

|

| ||||||||||||||||||||

Investment Partnerships (Continued) |

|

| ||||||||||||||||||||

VPC Legal Finance Fund, L.P. | USD | N/A | $ | 86,429,056 | $ | 95,683,860 | 1,2,16 | |||||||||||||||

Waccamaw River LLC | USD | N/A |

| 12,498,740 |

| 7,731,913 | 2,16 | |||||||||||||||

WhiteHawk Evergreen Fund, LP | USD | N/A |

| 50,000,000 |

| 50,837,055 | 2,16 | |||||||||||||||

| 1,779,663,110 |

| 1,949,000,617 | |||||||||||||||||||

Non-Listed Business Development Companies — 2.0% |

|

| ||||||||||||||||||||

Blue Owl Technology Finance Corp. | USD | 683,646 |

| 10,332,953 |

| 11,985,574 | 1,2,16 | |||||||||||||||

Blue Owl Technology Finance Corp. II | USD | 543,524 |

| 7,927,947 |

| 8,562,985 | 1,2,16 | |||||||||||||||

Franklin BSP Capital Corp | USD | 127,108 |

| 1,795,011 |

| 1,838,434 | 1,2,16 | |||||||||||||||

Redwood Enhanced Income Corp. | USD | 1,988,166 |

| 28,275,000 |

| 25,930,093 | 1,2,16 | |||||||||||||||

Stellus Private Credit BDC Feeder LP | USD | N/A |

| 8,558,048 |

| 8,844,964 | 1,2,16 | |||||||||||||||

| 56,888,959 |

| 57,162,050 | |||||||||||||||||||

Private Collateralized Fund Obligations — 0.1% |

|

| ||||||||||||||||||||

Archer 2023 Finance, LLC, Class B | 17.30% PIK | SOFR | 400 | 12/28/2035 | USD | 35,500,000 |

| 1,259,196 |

| 1,259,196 | 4,8,9 | |||||||||||

|

| |||||||||||||||||||||

Private Collateralized Loan Obligations — 3.4% |

|

| ||||||||||||||||||||

Guggenheim MM-C CLO | USD | N/A |

| 90,202,500 |

| 99,650,906 | 2,16 | |||||||||||||||

|

| |||||||||||||||||||||

Private Equity — 0.1% |

|

| ||||||||||||||||||||

Blue Owl Technology Holdings II, LLC, Class A | USD | N/A |

| 207,405 |

| 966,160 | 1,4 | |||||||||||||||

Stellus Private BDC Advisor, LLC | USD | N/A |

| — |

| 786,317 | 4 | |||||||||||||||

| 207,405 |

| 1,752,477 | |||||||||||||||||||

Special Purpose Vehicle for Common and Preferred Equity — 0.3% |

|

| ||||||||||||||||||||

Boost Co-Invest LP | USD | N/A |

| 6,764,671 |

| 6,764,671 | 2,16 | |||||||||||||||

Felicitas Diner Offshore, LP | USD | N/A |

| 2,625,575 |

| 3,162,356 | 1,2,16 | |||||||||||||||

| 9,390,246 |

| 9,927,027 | |||||||||||||||||||

Special Purpose Vehicle for Common Equity — 1.3% |

|

| ||||||||||||||||||||

Blackstone Tactical Opportunities Fund (Matrix Co-Invest) LP | USD | N/A |

| 4,719,266 |

| 4,743,917 | 2,16 | |||||||||||||||

KWOL Co-Invest, LP | USD | N/A |

| 2,500,000 |

| 2,585,890 | 2,16 | |||||||||||||||

Marilyn Co-Invest, L.P. | USD | N/A |

| 24,732,588 |

| 30,266,187 | 1,2,16 | |||||||||||||||

| 31,951,854 |

| 37,595,994 | |||||||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

9

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||

Private Investment Vehicles (Continued) |

|

| ||||||||||||||||||||

Special Purpose Vehicle for Consumer Credit — 0.0% |

|

| ||||||||||||||||||||

Atalaya Digithouse Opportunity Fund, LLC | USD | N/A | $ | 277,516 | $ | 1,198,838 | 1,2,3,16 | |||||||||||||||

|

| |||||||||||||||||||||

Special Purpose Vehicle for Preferred Equity — 2.1% |

|

| ||||||||||||||||||||

CCOF Alera Aggregator, L.P. | USD | N/A |

| 4,856,250 |

| 5,760,011 | 1,2,16 | |||||||||||||||

CCOF Sierra II, L.P. | USD | N/A |

| 3,906,521 |

| 4,746,690 | 1,2,16 | |||||||||||||||

Chilly HP SCF Investor, LP | USD | N/A |

| 2,970,297 |

| 3,520,955 | 1,2,16 | |||||||||||||||

CL Oliver Co-Invest I, L.P. | USD | N/A |

| 5,048,999 |

| 5,645,378 | 1,2,16 | |||||||||||||||

HPS Mint Co-Invest Fund, L.P. | USD | N/A |

| 6,473,263 |

| 8,274,266 | 2,16 | |||||||||||||||

Minerva Co-Invest, L.P. | USD | N/A |

| 12,468,490 |

| 12,850,197 | 2,16 | |||||||||||||||

NB Capital Solutions Co-Investment (Wolverine), LP | USD | N/A |

| 1,380,844 |

| 1,490,637 | 2,16 | |||||||||||||||

VCSF Co-Invest 1-A, L.P. | USD | N/A |

| 16,875,378 |

| 18,074,896 | 2,16 | |||||||||||||||

| 53,980,042 |

| 60,363,030 | |||||||||||||||||||

Special Purpose Vehicle for Real Estate Loans — 1.2% |

|

| ||||||||||||||||||||

BP Holdings RHO LLC | USD | N/A |

| 9,099,750 |

| 10,319,495 | 1,2,3,16 | |||||||||||||||

BP Holdings Tau, LLC | USD | 684,815 |

| 683,208 |

| 684,815 | 1,2,3,16 | |||||||||||||||

BP Holdings Zeta LP — Class A | USD | N/A |

| 8,609,327 |

| 8,919,263 | 2,3,16 | |||||||||||||||

BP Holdings Zeta LP — Class B | USD | N/A |

| 1,410,673 |

| 1,461,457 | 2,3,16 | |||||||||||||||

SB DOF Speedway, LLC | USD | N/A |

| 7,887,281 |

| 9,200,756 | 2,16 | |||||||||||||||

Sculptor Real Estate Science Park Fund, LP | USD | N/A |

| 5,384,068 |

| 5,373,969 | 1,2,16 | |||||||||||||||

| 33,074,307 |

| 35,959,755 | |||||||||||||||||||

Special Purpose Vehicle for Senior Secured Loans — 1.3% |

|

| ||||||||||||||||||||

17Capital Co-Invest (B) SCSp | EUR | N/A |

| 5,462,221 |

| 5,365,611 | 2,16 | |||||||||||||||

Crestline Nevermore Holdco, L.P. | USD | N/A |

| 12,916,934 |

| 8,708,902 | 2,3,16 | |||||||||||||||

Gramercy PG Holdings, LP (Common Interests) | USD | N/A |

| 8,877,594 |

| 9,465,445 | 2,16 | |||||||||||||||

Gramercy PG Holdings, LP (Preferred Interests) | USD | N/A |

| 5,450,422 |

| 5,340,350 | 2,16 | |||||||||||||||

Magenta Co-Invest L.P. | USD | N/A |

| 6,000,000 |

| 6,000,000 | 2,16 | |||||||||||||||

Symbiotic Capital EB Fund, L.P. | USD | N/A |

| 3,977,275 |

| 4,001,797 | 2,16 | |||||||||||||||

| 42,684,446 |

| 38,882,105 | |||||||||||||||||||

Total Private Investment Vehicles |

| 2,099,579,581 |

| 2,292,751,995 | ||||||||||||||||||

|

| |||||||||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

10

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | ||||||||||||||

Senior Secured Loans — 19.3% |

|

|

| ||||||||||||||||||||

Consumer Discretionary — 1.3% |

|

|

| ||||||||||||||||||||

Gateway Casinos & Entertainment Limited | First Lien Term Loan | 13.47% | LIBOR | 800 | 10/22/2027 | USD | $ | 976,104 | $ | 948,468 | $ | 973,664 | 4,7 | ||||||||||

Harbor Purchaser, Inc. | First Lien Term Loan | 13.83% | SOFR | 850 | 4/7/2030 | USD |

| 3,000,000 |

| 2,951,822 |

| 2,926,020 | 3,4,7 | ||||||||||

Houghton Mifflin Harcourt Publishing Company | Second Lien Term Loan | 13.43% | SOFR | 800 | 4/7/2028 | USD |

| 4,962,500 |

| 4,790,726 |

| 4,829,846 | 4,7 | ||||||||||

Hudson’s Bay Company | First Lien Term Loan | 13.90% | SOFR | 850 | 9/30/2026 | USD |

| 4,254,860 |

| 4,209,411 |

| 4,210,163 | 1,3,4,7 | ||||||||||

KCP Acquisitions, Inc. | First Lien Term Loan | 13.90% | SOFR | 857 | 3/16/2027 | USD |

| 7,531,146 |

| 7,562,927 |

| 7,644,113 | 3,4,7 | ||||||||||

Keller Postman, LLC | First Lien Term Loan | 17.41% | SOFR | 1,200 | 9/15/2028 | USD |

| 12,121,212 |

| 12,000,000 |

| 12,139,394 | 4,7 | ||||||||||

NKD Group GmbH | First Lien Term Loan | 11.90% | EURIBOR | 800 | 3/23/2026 | EUR |

| 1,730,769 |

| 1,800,181 |

| 1,867,266 | 4,6,7 | ||||||||||

Penney Borrower LLC | First Lien Term Loan | 11.93% | SOFR | 650 | 12/16/2026 | USD |

| 3,988,971 |

| 3,965,651 |

| 3,965,915 | 1,3,4,7 | ||||||||||

|

| 38,229,186 |

| 38,556,381 | |||||||||||||||||||

Consumer Staples — 0.6% |

|

|

| ||||||||||||||||||||

Baxters North America Holdings, Inc. | First Lien Term Loan | 12.58%, 2.00% PIK | SOFR | 725 | 5/31/2028 | USD |

| 7,256,272 |

| 7,097,429 |

| 6,892,355 | 4,7,8 | ||||||||||

GOJO Industries Holdings, Inc. | First Lien Term Loan | 10.33%, 4.50% PIK | SOFR | 500 | 10/26/2028 | USD |

| 12,186,464 |

| 11,846,205 |

| 11,960,723 | 4,7,8 | ||||||||||

|

| 18,943,634 |

| 18,853,078 | |||||||||||||||||||

Energy — 0.6% |

|

|

| ||||||||||||||||||||

Knight Energy Services LLC | First Lien Term Loan | 12.96% | SOFR | 750 | 6/1/2028 | USD |

| 3,575,498 |

| 3,526,958 |

| 3,575,497 | 4,7 | ||||||||||

Wellbore Integrity Solutions LLC | First Lien Term Loan | 12.41% | SOFR | 700 | 12/31/2025 | USD |

| 12,774,788 |

| 12,774,787 |

| 12,774,788 | 3,4,7 | ||||||||||

|

| 16,301,745 |

| 16,350,285 | |||||||||||||||||||

Financials — 0.9% |

|

|

| ||||||||||||||||||||

Clearco SPV V US LP | First Lien Term Loan | 16.35% | SOFR | 1,100 | 4/3/2027 | USD |

| 15,000,000 |

| 5,598,127 |

| 5,577,000 | 4,7,9 | ||||||||||

Cresset Asset Management, LLC | First Lien Term Loan | 12.32%, 0.50% PIK | SOFR | 700 | 4/20/2025 | USD |

| 3,548,004 |

| 3,533,087 |

| 3,505,009 | 4,7,8 | ||||||||||

Foundation Risk Partners, Corp. | Delayed Draw | 12.16% | SOFR | 675 | 10/29/2028 | USD |

| 1,265,000 |

| 1,227,262 |

| 1,276,638 | 4,7 | ||||||||||

Foundation Risk Partners, Corp. | First Lien Term Loan | 12.16% | SOFR | 675 | 10/29/2028 | USD |

| 2,706,818 |

| 2,636,586 |

| 2,731,992 | 4,7 | ||||||||||

Kensington Private Equity Fund | Delayed Draw | 12.31% PIK | SOFR | 700 | 3/28/2026 | USD |

| 3,200,000 |

| 608,044 |

| 707,040 | 3,4,8,9 | ||||||||||

Kensington Private Equity Fund | Second Lien Term Loan | 12.31% PIK | SOFR | 700 | 3/28/2026 | USD |

| 3,200,000 |

| 3,165,873 |

| 3,267,040 | 3,4,7,8 | ||||||||||

Pennybacker Real Estate Credit II Pacific, LLC | Promissory Note | 11.59% | 5/10/2031 | USD |

| 809,927 |

| 809,927 |

| 809,927 | 1,4 | ||||||||||||

Retail Services Corporation | First Lien Term Loan | 13.81% | SOFR | 835 | 5/20/2025 | USD |

| 2,679,717 |

| 2,656,813 |

| 2,656,926 | 4,7 | ||||||||||

Wealth Enhancement Group, LLC | First Lien Term Loan | 15.00% PIK | 5/26/2033 | USD |

| 4,923,647 |

| 4,788,684 |

| 5,481,988 | 4,7,8 | ||||||||||||

|

| 25,024,403 |

| 26,013,560 | |||||||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

11

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||||

Senior Secured Loans (Continued) |

|

|

|

| ||||||||||||||||||||

Health Care — 8.1% |

|

|

|

| ||||||||||||||||||||

Acclaim Midco, LLC | Delayed Draw | 1.00% | 6/13/2029 | USD | $ | 897,436 | $ | (3,904 | ) | $ | 15,167 | 4,5 | ||||||||||||

Acclaim Midco, LLC | Revolver | 0.50% | 6/13/2029 | USD |

| 358,974 |

| (6,246 | ) |

| 826 | 4,5 | ||||||||||||

Acclaim Midco, LLC | First Lien Term Loan | 11.31% | SOFR | 600 | 6/13/2029 | USD |

| 2,226,763 |

| 2,186,325 |

|

| 2,231,884 | 4,7 | ||||||||||

ADMA Biologics, Inc. | Revolver | 9.13% | SOFR | 375 | 12/18/2027 | USD |

| 1,000 |

| 988 |

|

| 988 | 3,4,7 | ||||||||||

ADMA Biologics, Inc. | First Lien Term Loan | 11.88% | SOFR | 650 | 12/18/2027 | USD |

| 10,000,000 |

| 9,882,142 |

|

| 9,875,000 | 3,4,7 | ||||||||||

Alcami Corporation | Delayed Draw | 12.47% | SOFR | 700 | 12/21/2028 | USD |

| 277,299 |

| 268,451 |

|

| 275,327 | 4,7 | ||||||||||

Alcami Corporation | Revolver | 0.50% | 12/21/2028 | USD |

| 508,806 |

| (14,158 | ) |

| (3,620 | )4,5 | ||||||||||||

Alcami Corporation | First Lien Term Loan | 12.49% | SOFR | 700 | 12/21/2028 | USD |

| 3,777,886 |

| 3,665,371 |

|

| 3,751,012 | 4,7 | ||||||||||

Artivion, Inc. | Delayed Draw | 1.00% | 1/18/2030 | USD |

| 5,172,414 |

| (127,193 | ) |

| (129,310 | )4,5 | ||||||||||||

Artivion, Inc. | Revolver | 9.30% | SOFR | 650 | 1/18/2030 | USD |

| 334 |

| 159 |

|

| 159 | 4,7,9 | ||||||||||

Artivion, Inc. | First Lien Term Loan | 11.80% | SOFR | 650 | 1/18/2030 | USD |

| 9,827,586 |

| 9,587,463 |

|

| 9,581,896 | 4,7 | ||||||||||

Bamboo U.S. Bidco EUR | First Lien Term Loan | 9.86% | EURIBOR | 675 | 9/29/2030 | EUR |

| 7,829,072 |

| 8,035,068 |

|

| 8,193,117 | 4,6,7 | ||||||||||

Bamboo U.S. Bidco USD | First Lien Term Loan | 11.32% | SOFR | 675 | 9/29/2030 | USD |

| 12,583,276 |

| 12,223,451 |

|

| 12,205,778 | 4,7 | ||||||||||

Bamboo U.S. Bidco USD | Delayed Draw | 11.35% | SOFR | 675 | 9/29/2030 | USD |

| 1,966,137 |

| 179,432 |

|

| 180,229 | 4,9 | ||||||||||

Bamboo U.S. Bidco USD | Revolver | 0.50% | 10/1/2029 | USD |

| 2,621,516 |

| (72,986 | ) |

| (78,645 | )4,5 | ||||||||||||

Bausch Receivables Funding LP | Revolver | 11.98% | SOFR | 665 | 1/28/2028 | USD |

| 8,000,000 |

| 4,236,426 |

|

| 4,185,083 | 3,4,7,9 | ||||||||||

Confluent Health, LLC | First Lien Term Loan | 12.83% | SOFR | 750 | 11/30/2028 | USD |

| 2,835,573 |

| 2,658,781 |

|

| 2,704,999 | 4,7 | ||||||||||

Exactcare Parent, Inc. | Revolver | 0.50% | 11/3/2029 | USD |

| 442,623 |

| (11,358 | ) |

| (10,649 | )4,5 | ||||||||||||

Exactcare Parent, Inc. | First Lien Term Loan | 11.77% | SOFR | 650 | 11/3/2029 | USD |

| 4,057,377 |

| 3,950,986 |

|

| 3,959,763 | 4,7 | ||||||||||

Hanger, Inc. | Delayed Draw | 11.57% | SOFR | 625 | 10/3/2028 | USD |

| 7,428,571 |

| 4,105,104 |

|

| 4,118,572 | 4,9 | ||||||||||

Hanger, Inc. | Second Lien Term Loan | 11.58% | SOFR | 625 | 10/3/2028 | USD |

| 13,565,774 |

| 13,169,793 |

|

| 13,124,815 | 4,7 | ||||||||||

Hanger, Inc. | Delayed Draw | 1.00% | 10/3/2029 | USD |

| 3,285,714 |

| (65,238 | ) |

| (73,928 | )4,5 | ||||||||||||

Hanger, Inc. | Second Lien Term Loan | 15.08% | SOFR | 975 | 10/3/2029 | USD |

| 5,714,286 |

| 5,541,772 |

|

| 5,528,571 | 4,7 | ||||||||||

Hanger, Inc. | Revolver | 9.57% | SOFR | 425 | 10/3/2027 | USD |

| 1,000 |

| 764 |

|

| 750 | 4,9 | ||||||||||

Helium Acquirer Corporation | Delayed Draw | 12.40% | SOFR | 700 | 1/5/2029 | USD |

| 1,752,690 |

| 1,321,254 |

|

| 1,318,174 | 4,7,9 | ||||||||||

Helium Acquirer Corporation | Revolver | 12.40% | SOFR | 700 | 1/5/2029 | USD |

| 293,190 |

| 202,946 |

|

| 204,030 | 4,7,9 | ||||||||||

Helium Acquirer Corporation | First Lien Term Loan | 12.40% | SOFR | 700 | 1/5/2029 | USD |

| 1,915,207 |

| 1,866,113 |

|

| 1,871,841 | 4,7 | ||||||||||

KWOL Acquisition, Inc. | Revolver | 0.50% | 12/12/2029 | USD |

| 448,296 |

| (10,685 | ) |

| (11,144 | )4,5 | ||||||||||||

KWOL Acquisition, Inc. | First Lien Term Loan | 11.43% | SOFR | 625 | 12/12/2029 | USD |

| 3,301,704 |

| 3,222,014 |

|

| 3,219,628 | 4,7 | ||||||||||

Nader Upside 2 Sarl | First Lien Term Loan | 14.14% | EURIBOR | 1,025 | 3/13/2028 | EUR |

| 4,685,610 |

| 4,968,440 |

|

| 4,953,033 | 4,6,7 | ||||||||||

Nephron Pharmaceuticals Corporation | First Lien Term Loan | 16.49% | SOFR | 1,100 | 9/11/2026 | USD |

| 14,943,750 |

| 14,560,485 |

|

| 12,937,892 | 4,7 | ||||||||||

Next HoldCo, LLC | Delayed Draw | 1.00% | 11/9/2030 | USD |

| 950,570 |

| (13,870 | ) |

| (14,259 | )4,5 | ||||||||||||

Next HoldCo, LLC | Revolver | 0.50% | 11/9/2029 | USD |

| 342,205 |

| (4,802 | ) |

| (5,133 | )4,5 | ||||||||||||

Next HoldCo, LLC | First Lien Term Loan | 11.33% | SOFR | 600 | 11/9/2030 | USD |

| 3,707,224 |

| 3,653,655 |

|

| 3,651,616 | 4,7 | ||||||||||

See accompanying Notes to Consolidated Financial Statements.

12

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||||

Senior Secured Loans (Continued) |

|

|

|

| ||||||||||||||||||||

Health Care (Continued) |

|

|

|

| ||||||||||||||||||||

Nomi Health, Inc | First Lien Term Loan | 13.64% | SOFR | 825 | 7/12/2028 | USD | $ | 23,278,373 | $ | 22,648,759 |

| $ | 22,580,021 | 4,7 | ||||||||||

OMH-Healthedge Holdings, Inc. | Revolver | 0.50% | 10/6/2029 | USD |

| 1,466,165 |

| (33,694 | ) |

| (36,654 | )4,5 | ||||||||||||

OMH-Healthedge Holdings, Inc. | First Lien Term Loan | 11.42% | SOFR | 600 | 10/6/2029 | USD |

| 13,533,835 |

| 13,214,351 |

|

| 13,195,489 | 4,7 | ||||||||||

Orthodontic Partners, LLC | Delayed Draw | 11.97% | SOFR | 650 | 10/12/2027 | USD |

| 3,542,817 |

| 3,487,921 |

|

| 3,545,651 | 4,7 | ||||||||||

Orthodontic Partners, LLC | First Lien Term Loan | 11.97% | SOFR | 650 | 10/12/2027 | USD |

| 2,406,107 |

| 2,366,977 |

|

| 2,389,231 | 4,7 | ||||||||||

Paragon 28 Inc | Delayed Draw | 0.50% | 11/2/2028 | USD |

| 7,500,000 |

| (179,855 | ) |

| (187,500 | )4,5 | ||||||||||||

Paragon 28 Inc | Revolver | 9.33% | SOFR | 675 | 11/2/2028 | USD |

| 1,000 |

| 480 |

|

| 478 | 4,5,7 | ||||||||||

Paragon 28 Inc | First Lien Term Loan | 12.08% | SOFR | 675 | 11/2/2028 | USD |

| 22,500,000 |

| 21,971,016 |

|

| 21,937,500 | 4,7 | ||||||||||

PerkinElmer U.S., LLC | First Lien Term Loan | 11.08% | SOFR | 575 | 3/13/2029 | USD |

| 5,000,000 |

| 4,904,630 |

|

| 4,900,000 | 4,7 | ||||||||||

Prolacta Bioscience | First Lien Term Loan | 14.33% | SOFR | 575 | 12/21/2029 | USD |

| 6,458,333 |

| 6,366,332 |

|

| 6,370,628 | 3,4,7 | ||||||||||

Prolacta Bioscience | First Lien Term Loan | 10.76% | SOFR | 575 | 12/21/2029 | USD |

| 2,083,333 |

| 2,053,544 |

|

| 2,055,041 | 3,4,7 | ||||||||||

Tempus Labs, Inc. | First Lien Term Loan | 13.66% | SOFR | 825 | 9/22/2027 | USD |

| 21,875,000 |

| 21,363,865 |

|

| 21,328,125 | 4,7 | ||||||||||

TerSera Therapeutics, LLC | Revolver | 0.50% | 4/4/2029 | USD |

| 227,926 |

| (5,709 | ) |

| (1,370 | )4,5 | ||||||||||||

TerSera Therapeutics, LLC | First Lien Term Loan | 12.05% | SOFR | 675 | 4/4/2029 | USD |

| 2,765,144 |

| 2,691,739 |

|

| 2,748,518 | 4,7 | ||||||||||

United Digestive MSO Parent, LLC | Delayed Draw | 1.00% | 3/30/2029 | USD |

| 595,000 |

| (7,435 | ) |

| (16,132 | )4,5 | ||||||||||||

United Digestive MSO Parent, LLC | Revolver | 12.07% | SOFR | 675 | 3/30/2029 | USD |

| 297,500 |

| 75,865 |

|

| 75,234 | 4,9 | ||||||||||

United Digestive MSO Parent, LLC | First Lien Term Loan | 12.21% | SOFR | 675 | 3/30/2029 | USD |

| 2,237,400 |

| 2,178,037 |

|

| 2,176,739 | 4,7 | ||||||||||

Vardiman Black Holdings, LLC | First Lien Term Loan | 14.43% | SOFR | 700 | 3/18/2027 | USD |

| 3,597,344 |

| 3,597,344 |

|

| 3,518,402 | 4,7 | ||||||||||

Vardiman Black Holdings, LLC | Delayed Draw | 1.00% | 3/18/2027 | USD |

| 304,997 |

| (9,150 | ) |

| (9,150 | )4,5 | ||||||||||||

WCI-BXC Purchaser, LLC | Revolver | 0.50% | 11/6/2029 | USD |

| 512,821 |

| (11,979 | ) |

| (12,821 | )4,5 | ||||||||||||

WCI-BXC Purchaser, LLC | First Lien Term Loan | 11.59% | SOFR | 625 | 11/6/2030 | USD |

| 4,487,179 |

| 4,379,110 |

|

| 4,375,000 | 4,7 | ||||||||||

Whitehawk Healthcare | First Lien Term Loan | 16.18% | PRIME | 1,275 | 12/31/2027 | USD |

| 12,293,224 |

| 12,007,913 |

|

| 12,293,224 | 3,4,7 | ||||||||||

Xeris Pharmaceuticals, Inc. | Delayed Draw | 14.33% | SOFR | 900 | 3/8/2027 | USD |

| 1,666,667 |

| 1,576,561 |

|

| 1,654,810 | 3,4,7 | ||||||||||

Xeris Pharmaceuticals, Inc. | First Lien Term Loan | 14.33% | SOFR | 900 | 3/8/2027 | USD |

| 3,333,333 |

| 3,298,363 |

|

| 3,309,621 | 1,3,4,7 | ||||||||||

|

| 237,091,928 |

|

| 235,953,547 | |||||||||||||||||||

Industrials — 2.8% |

|

|

|

| ||||||||||||||||||||

Apex Service Partners, LLC | First Lien Term Loan | 14.25% | 10/24/2028 | USD |

| 2,051,590 |

| 1,993,463 |

|

| 2,007,221 | 4 | ||||||||||||

Apex Service Partners, LLC | Delayed Draw | 14.25% PIK | 10/24/2029 | USD |

| 1,007,146 |

| 978,745 |

|

| 985,365 | 4,8 | ||||||||||||

Cobham Holdings, Inc. | Revolver | 0.50% | 1/9/2028 | USD |

| 468,750 |

| (10,745 | ) |

| (5,107 | )4,5 | ||||||||||||

Cobham Holdings, Inc. | First Lien Term Loan | 12.06% | SOFR | 675 | 1/9/2030 | USD |

| 4,485,938 |

| 4,366,820 |

|

| 4,437,068 | 4,7 | ||||||||||

DMT Solutions Global Corporation | First Lien Term Loan | 13.27% | SOFR | 800 | 8/30/2027 | USD |

| 7,757,647 |

| 7,551,597 |

|

| 7,546,021 | 4,7 | ||||||||||

FB FLL Aviation LLC | First Lien Term Loan | 12.33% | SOFR | 700 | 7/19/2028 | USD |

| 12,600,000 |

| 8,067,891 |

|

| 7,987,500 | 4,7,9 | ||||||||||

Fenix Topco, LLC | First Lien Term Loan | 11.81% | SOFR | 650 | 3/28/2029 | USD |

| 2,747,419 |

| 2,680,572 |

|

| 2,680,000 | 4,7 | ||||||||||

Fenix Topco, LLC | Delayed Draw | 1.00% | 3/28/2029 | USD |

| 1,062,537 |

| (26,605 | ) |

| (26,943 | )4,5 | ||||||||||||

Fenix Topco, LLC | Delayed Draw | 1.00% | 3/28/2029 | USD |

| 190,045 |

| 160,004 |

|

| 159,958 | 4,5 | ||||||||||||

See accompanying Notes to Consolidated Financial Statements.

13

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||||

Senior Secured Loans (Continued) |

|

|

|

| ||||||||||||||||||||

Industrials (Continued) |

|

|

|

| ||||||||||||||||||||

Florida Marine, LLC. | First Lien Term Loan | 13.44% | SOFR | 800 | 3/17/2028 | USD | $ | 4,785,600 | $ | 4,671,459 |

| $ | 4,751,556 | 4,7 | ||||||||||

Helix Acquisition Holdings, Inc. | First Lien Term Loan | 12.40% | ARR CSA | 700 | 3/31/2030 | USD |

| 5,675,461 |

| 5,545,435 |

|

| 5,632,247 | 4,7 | ||||||||||

iCIMS, Inc. | First Lien Term Loan | 12.58% | SOFR | 725 | 8/18/2028 | USD |

| 7,000,000 |

| 6,899,467 |

|

| 6,927,434 | 4,7 | ||||||||||

P20 Parent, Inc. | First Lien Term Loan | 12.81% | SOFR | 750 | 7/12/2028 | USD |

| 4,925,000 |

| 4,846,887 |

|

| 4,849,051 | 4,7 | ||||||||||

Panda Acquisition LLC | First Lien Term Loan | 11.66% | SOFR | 625 | 10/18/2028 | USD |

| 3,875,000 |

| 3,224,281 |

|

| 3,278,852 | 4,7 | ||||||||||

Penn TRGRP Holdings | Revolver | 0.50% | 9/29/2030 | USD |

| 769,167 |

| (14,276 | ) |

| (12,970 | )4,5 | ||||||||||||

Penn TRGRP Holdings | First Lien Term Loan | 7.10%, 6.00% PIK | SOFR | 175 | 9/29/2030 | USD |

| 5,151,971 |

| 5,056,337 |

|

| 5,065,099 | 4,7,8 | ||||||||||

Starlight Inventory I, LLC | First Lien Term Loan | 15.23% | SOFR | 1,000 | 9/24/2024 | USD |

| 15,000,000 |

| 15,111,901 |

|

| 15,112,500 | 3,4 | ||||||||||

TecoStar Holdings, Inc. | First Lien Term Loan | 9.32%, 4.50% PIK | SOFR | 400 | 7/7/2029 | USD |

| 5,848,637 |

| 5,717,162 |

|

| 5,720,442 | 4,7,8 | ||||||||||

The Arcticom Group, LLC | Delayed Draw | 12.33% | SOFR | 675 | 12/22/2027 | USD |

| 3,960,000 |

| 3,867,086 |

|

| 3,931,830 | 4,7 | ||||||||||

The Arcticom Group, LLC | Delayed Draw | 11.62% | SOFR | 625 | 12/22/2027 | USD |

| 169,854 |

| 149,146 |

|

| 149,121 | 4,7,9 | ||||||||||

The Arcticom Group, LLC | First Lien Term Loan | 11.57% | SOFR | 625 | 12/22/2027 | USD |

| 652,186 |

| 637,554 |

|

| 637,944 | 4,7 | ||||||||||

|

| 81,474,181 |

|

| 81,814,189 | |||||||||||||||||||

Materials — 0.3% |

|

|

|

| ||||||||||||||||||||

SintecMedia NYC, Inc. | Revolver | 12.33% | SOFR | 700 | 6/21/2029 | USD |

| 423,729 |

| 260,122 |

|

| 255,429 | 4,7,9 | ||||||||||

SintecMedia NYC, Inc. | First Lien Term Loan | 12.33% | SOFR | 700 | 6/21/2029 | USD |

| 4,564,831 |

| 4,439,979 |

|

| 4,399,299 | 4,7 | ||||||||||

Sunland Asphalt & Construction, LLC | Delayed Draw | 1.00% | 6/16/2028 | USD |

| 742,188 |

| (10,861 | ) |

| (1,566 | )4,5,8 | ||||||||||||

Sunland Asphalt & Construction, LLC | First Lien Term Loan | 11.93% | SOFR | 650 | 6/16/2028 | USD |

| 1,761,418 |

| 1,714,846 |

|

| 1,757,703 | 4,7,8 | ||||||||||

SureWerx Purchaser III, Inc. | First Lien Term Loan | 12.05% | SOFR | 675 | 12/28/2029 | USD |

| 2,264,141 |

| 2,204,073 |

|

| 2,264,141 | 4,7 | ||||||||||

SureWerx Purchaser III, Inc. | Revolver | 12.08% | SOFR | 675 | 12/28/2028 | USD |

| 250,000 |

| 106,250 |

|

| 106,250 | 4,7,9 | ||||||||||

SureWerx Purchaser III, Inc. | Delayed Draw | 1.00% | 12/28/2029 | USD |

| 468,750 |

| (7,741 | ) |

| — | 4,5 | ||||||||||||

|

| 8,706,668 |

|

| 8,781,256 | |||||||||||||||||||

Real Estate — 0.4% |

|

|

|

| ||||||||||||||||||||

Lexington Hotel Owner, LLC | Delayed Draw | 12.19% | SOFR | 675 | 7/1/2024 | USD |

| 9,018,621 |

| 8,993,334 |

|

| 9,058,044 | 4,7 | ||||||||||

Poinciana LLC | Delayed Draw | 12.00% | 5/1/2026 | USD |

| 4,848,649 |

| 3,562,031 |

|

| 3,537,788 | 4,9 | ||||||||||||

|

| 12,555,365 |

|

| 12,595,832 | |||||||||||||||||||

Technology — 4.3% |

|

|

|

| ||||||||||||||||||||

Afiniti, Inc. | First Lien Term Loan | 10.25%, 1.00% PIK | 6/13/2024 | USD |

| 2,269,211 |

| 2,266,714 |

|

| 2,253,182 | 1,3,4,7,8 | ||||||||||||

Alteryx | Delayed Draw | 1.00% | 3/19/2031 | USD |

| 645,833 |

| (9,664 | ) |

| (9,688 | )4,5 | ||||||||||||

Alteryx | Revolver | 0.50% | 3/19/2031 | USD |

| 103,333 |

| (1,542 | ) |

| (1,550 | )4,5 | ||||||||||||

Alteryx | First Lien Term Loan | 11.83% | SOFR | 650 | 3/19/2031 | USD |

| 284,167 |

| 279,917 |

|

| 279,904 | 4,7 | ||||||||||

ASG II, LLC | Delayed Draw | 11.71% | SOFR | 625 | 5/25/2028 | USD |

| 391,304 |

| 360,295 |

|

| 370,174 | 4,7,9 | ||||||||||

ASG II, LLC | First Lien Term Loan | 11.71% | SOFR | 625 | 5/25/2028 | USD |

| 2,608,696 |

| 2,568,507 |

|

| 2,615,739 | 4,7 | ||||||||||

Avalara, Inc. | Revolver | 0.50% | 10/19/2028 | USD |

| 272,727 |

| 422 |

|

| (4,861 | )4,5 | ||||||||||||

See accompanying Notes to Consolidated Financial Statements.

14

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||||

Senior Secured Loans (Continued) |

|

|

|

| ||||||||||||||||||||

Technology (Continued) |

|

|

|

| ||||||||||||||||||||

Avalara, Inc. | First Lien Term Loan | 12.56% | SOFR | 725 | 10/19/2028 | USD | $ | 2,727,273 | $ | 2,670,813 |

| $ | 2,678,658 | 4,7 | ||||||||||

Bluefin Holding, LLC | Revolver | 0.50% | 9/12/2029 | USD |

| 673,077 |

| (15,284 | ) |

| (15,496 | )4,5 | ||||||||||||

Bluefin Holding, LLC | First Lien Term Loan | 12.57% | SOFR | 725 | 9/12/2029 | USD |

| 6,826,923 |

| 6,667,070 |

|

| 6,669,746 | 4,7 | ||||||||||

Bluesight, Inc. | Revolver | 0.50% | 7/17/2029 | USD |

| 400,000 |

| (10,588 | ) |

| (10,543 | )4,5 | ||||||||||||

Bluesight, Inc. | First Lien Term Loan | 12.55% | SOFR | 725 | 7/17/2029 | USD |

| 4,600,000 |

| 4,472,949 |

|

| 4,478,758 | 4,7 | ||||||||||

Coupa Holdings, LLC | Delayed Draw | 1.00% | 2/28/2029 | USD |

| 385,633 |

| (4,089 | ) |

| (3,863 | )4,5 | ||||||||||||

Coupa Holdings, LLC | Revolver | 0.50% | 2/28/2029 | USD |

| 295,276 |

| (6,077 | ) |

| (2,958 | )4,5 | ||||||||||||

Coupa Holdings, LLC | First Lien Term Loan | 12.81% | SOFR | 750 | 2/27/2030 | USD |

| 4,319,091 |

| 4,221,646 |

|

| 4,275,830 | 4,7 | ||||||||||

Crewline Buyer, Inc. | Revolver | 0.50% | 11/8/2030 | USD |

| 870,417 |

| (20,557 | ) |

| (18,972 | )4,5 | ||||||||||||

Crewline Buyer, Inc. | First Lien Term Loan | 12.06% | SOFR | 675 | 11/8/2030 | USD |

| 8,355,999 |

| 8,154,540 |

|

| 8,173,863 | 4,7 | ||||||||||

Disco Parent, LLC | Revolver | 0.50% | 3/30/2029 | USD |

| 113,619 |

| (2,366 | ) |

| (1,746 | )4,5 | ||||||||||||

Disco Parent, LLC | First Lien Term Loan | 12.84% | SOFR | 750 | 3/30/2029 | USD |

| 1,136,195 |

| 1,111,021 |

|

| 1,118,730 | 4,7 | ||||||||||

Finastra USA, Inc. | Revolver | 0.50% | 9/13/2029 | USD |

| 936,090 |

| (17,014 | ) |

| (15,863 | )4,5 | ||||||||||||

Finastra USA, Inc. | First Lien Term Loan | 12.46% | SOFR | 725 | 9/13/2029 | USD |

| 9,023,910 |

| 8,854,529 |

|

| 8,870,935 | 4,7 | ||||||||||

Fullsteam Operations LLC | Delayed Draw | 13.73% | SOFR | 825 | 11/27/2029 | USD |

| 729,445 |

| 357,766 |

|

| 359,177 | 4,7,9 | ||||||||||

Fullsteam Operations LLC | Revolver | 0.50% | 11/27/2029 | USD |

| 89,778 |

| (2,542 | ) |

| (2,438 | )4,5 | ||||||||||||

Fullsteam Operations LLC | First Lien Term Loan | 13.73% | SOFR | 825 | 11/27/2029 | USD |

| 1,604,778 |

| 1,558,376 |

|

| 1,561,190 | 4,7 | ||||||||||

Fullsteam Operations LLC | Delayed Draw | 1.00% | 11/27/2029 | USD |

| 1,122,222 |

| (16,684 | ) |

| (16,191 | )4,5 | ||||||||||||

Infinite Bidco LLC | First Lien Term Loan | 11.83% | CME | 625 | 3/2/2028 | USD |

| 4,937,500 |

| 4,813,708 |

|

| 4,911,766 | 4,7 | ||||||||||

Mercury Bidco LLC | First Lien Term Loan | 12.31% | SOFR | 700 | 5/31/2030 | USD |

| 4,568,878 |

| 4,494,184 |

|

| 4,537,748 | 4,7 | ||||||||||

Mercury Bidco LLC | Revolver | 0.50% | 5/31/2029 | USD |

| 408,163 |

| (8,878 | ) |

| (3,067 | )4,5 | ||||||||||||

MGT Merger Target, LLC | Delayed Draw | 11.92% | SOFR | 675 | 4/10/2029 | USD |

| 225,287 |

| 224,161 |

|

| 228,554 | 4,7 | ||||||||||

MGT Merger Target, LLC | Revolver | 14.00% | PRIME | 650 | 4/10/2028 | USD |

| 496,552 |

| 248,276 |

|

| 248,276 | 4,7,9 | ||||||||||

MGT Merger Target, LLC | First Lien Term Loan | 11.92% | SOFR | 650 | 4/10/2029 | USD |

| 3,975,426 |

| 3,870,966 |

|

| 3,975,426 | 4,7 | ||||||||||

MIS Acquisition, LLC | Revolver | 0.50% | 11/17/2028 | USD |

| 533,334 |

| (14,834 | ) |

| (15,484 | )4,5 | ||||||||||||

MIS Acquisition, LLC | First Lien Term Loan | 12.07% | SOFR | 675 | 11/17/2028 | USD |

| 7,466,666 |

| 7,254,617 |

|

| 7,249,884 | 4,7 | ||||||||||

Oranje Holdco, Inc. | Revolver | 0.50% | 2/1/2029 | USD |

| 592,667 |

| (12,149 | ) |

| (3,178 | )4,5 | ||||||||||||

Oranje Holdco, Inc. | First Lien Term Loan | 12.81% | SOFR | 750 | 2/1/2029 | USD |

| 4,741,333 |

| 4,637,769 |

|

| 4,715,910 | 4,7 | ||||||||||

Polaris Newco, LLC | Second Lien Term Loan | 14.44% | SOFR | 900 | 6/4/2029 | USD |

| 14,693,001 |

| 11,563,784 |

|

| 11,626,276 | 4,7,8 | ||||||||||

PracticeTek Purchaser LLC | Delayed Draw | 1.00% | 8/30/2029 | USD |

| 6,460,385 |

| (72,871 | ) |

| (80,755 | )4,5 | ||||||||||||

PracticeTek Purchaser LLC | Revolver | 9.82% | SOFR | 450 | 8/30/2029 | USD |

| 1,000 |

| 477 |

|

| 475 | 4,9 | ||||||||||

PracticeTek Purchaser LLC | First Lien Term Loan | 11.33% | SOFR | 575 | 8/30/2029 | USD |

| 14,695,362 |

| 14,352,946 |

|

| 14,327,978 | 4,7 | ||||||||||

See accompanying Notes to Consolidated Financial Statements.

15

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | ||||||||||||||

Senior Secured Loans (Continued) |

|

|

| ||||||||||||||||||||

Technology (Continued) |

|

|

| ||||||||||||||||||||

PracticeTek Purchaser LLC | First Lien Term Loan | 14.00% | 8/30/2030 | USD | $ | 6,006,287 | $ | 5,845,606 | $ | 5,826,098 | 4,8 | ||||||||||||

PracticeTek Purchaser LLC | First Lien Term Loan | 11.33% | SOFR | 575 | 8/30/2029 | USD |

| 6,320,648 |

| 6,173,388 |

| 6,162,631 | 3,4,7 | ||||||||||

Trintech, Inc. | Revolver | 11.83% | SOFR | 650 | 7/25/2029 | USD |

| 595,752 |

| 154,379 |

| 154,021 | 4,7,9 | ||||||||||

Trintech, Inc. | First Lien Term Loan | 11.83% | SOFR | 650 | 7/25/2029 | USD |

| 7,724,574 |

| 7,510,481 |

| 7,514,607 | 4,7 | ||||||||||

User Zoom Technologies, Inc | First Lien Term Loan | 12.99% | SOFR | 750 | 4/5/2029 | USD |

| 5,000,000 |

| 4,869,726 |

| 4,924,396 | 4,7 | ||||||||||

Xactly Corporation | First Lien Term Loan | 12.69% | SOFR | 725 | 7/31/2025 | USD |

| 6,000,000 |

| 5,910,000 |

| 5,967,827 | 4,7 | ||||||||||

|

| 125,253,894 |

| 125,871,106 | |||||||||||||||||||

Total Senior Secured Loans |

|

| 563,581,004 |

| 564,789,234 | ||||||||||||||||||

|

|

| |||||||||||||||||||||

Collateralized Loan Obligations — 2.6% |

|

|

| ||||||||||||||||||||

ABPCI Direct Lending Fund CLO XII | 15.00% | SOFR | 968 | 4/29/2035 | USD |

| 7,500,000 |

| 7,208,771 |

| 7,561,176 | 7,10,11 | |||||||||||

ABPCI Direct Lending Fund CLO XV, | 14.04% | SOFR | 860 | 10/30/2035 | USD |

| 5,000,000 |

| 4,900,000 |

| 5,021,689 | 4,7,10,11 | |||||||||||

ABPCI Direct Lending Fund CLO XV, | 11.84% | SOFR | 640 | 10/30/2035 | USD |

| 8,100,000 |

| 8,100,000 |

| 8,454,347 | 4,7,10,11 | |||||||||||

Barings Middle Market CLO 2023-II | 14.00% | SOFR | 867 | 1/20/2032 | USD |

| 8,450,000 |

| 8,365,500 |

| 8,463,192 | 4,7,10,11 | |||||||||||

Barings Middle Market CLO Ltd. | 14.24% | LIBOR | 892 | 1/20/2034 | USD |

| 2,000,000 |

| 1,960,000 |

| 1,935,000 | 7,10,11 | |||||||||||

Barings Middle Market CLO Ltd. | 27.00% | 1/20/2034 | USD |

| 2,905,983 |

| 2,463,233 |

| 1,918,758 | *,4,10,11,12 | |||||||||||||

Barings Private Credit Corp. CLO | 11.66% | SOFR | 635 | 7/15/2031 | USD |

| 6,000,000 |

| 6,000,000 |

| 6,150,563 | 4,7,10,11 | |||||||||||

Deerpath Capital CLO 2020-1 Ltd. | 11.71% | SOFR | 639 | 4/17/2034 | USD |

| 3,250,000 |

| 3,185,000 |

| 3,392,190 | 4,7,10,11 | |||||||||||

Golub Capital Partners CLO | 11.41% | SOFR | 600 | 10/23/2023 | USD |

| 13,950,000 |

| 13,950,000 |

| 14,269,957 | 4,7,10,11 | |||||||||||

HPS Private Credit CLO 2023-1 LLC | 15.16% | SOFR | 985 | 7/15/2035 | USD |

| 7,500,000 |

| 7,350,000 |

| 7,527,266 | 7,10,11 | |||||||||||

Ivy Hill Middle Market Credit Fund XXI Ltd. | 13.82% | SOFR | 852 | 7/18/2035 | USD |

| 6,500,000 |

| 6,336,850 |

| 6,509,324 | 4,7,10,11 | |||||||||||

Ivy Hill Middle Market Credit Fund XXI Ltd. | 11.70% | SOFR | 640 | 7/18/2035 | USD |

| 3,500,000 |

| 3,500,000 |

| 3,656,013 | 4,7,10,11 | |||||||||||

TCP Whitney CLO Ltd. | 13.74% | LIBOR | 842 | 8/20/2033 | USD |

| 2,500,000 |

| 2,450,000 |

| 2,424,159 | 1,7,10,11 | |||||||||||

Total Collateralized Loan Obligations |

|

| 75,769,354 |

| 77,283,634 | ||||||||||||||||||

|

|

| |||||||||||||||||||||

Preferred Stocks — 1.1% |

|

|

| ||||||||||||||||||||

Energy — 0.0% |

|

|

| ||||||||||||||||||||

Service Compression Preferred Equity (JR. Preferred Shares) | 0.000% | USD |

| 40,919 |

| 135,094 |

| 139,534 | 4 | ||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

16

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||

Preferred Stocks (Continued) |

|

| ||||||||||||||||||||

Health Care — 0.3% |

|

| ||||||||||||||||||||

nThrive, Inc., Series A-2 Preferred | 11.00% PIK | USD | 3,260 | $ | 3,162,200 | $ | 3,053,371 | 1,4,8 | ||||||||||||||

Propharma, LLC | 13.00% PIK | USD | 2,500 |

| 2,425,000 |

| 2,500,000 | 1,4,8,13 | ||||||||||||||

Tempus Labs, Inc. | 0.000% | USD | 54,531 |

| 3,125,003 |

| 3,125,003 | 4 | ||||||||||||||

Vardiman Black Holdings, LLC | 0.000% | USD | 1,765,938 |

| 515,371 |

| 515,371 | 4 | ||||||||||||||

| 9,227,574 |

| 9,193,745 | |||||||||||||||||||

Industrials — 0.4% |

|

| ||||||||||||||||||||

Atomic Transport, LLC | 8.50% PIK | USD | 2,500 |

| 1,782,701 |

| 2,427,719 | 1,4,8,14 | ||||||||||||||

Atomic Transport, LLC | 15.35% PIK | USD | 875 |

| 857,500 |

| 875,000 | 1,4,8,14 | ||||||||||||||

FSG Acquisition, LLC, — Senior | 12.25% PIK | USD | 3,750,000 |

| 3,656,250 |

| 3,735,105 | 4,8 | ||||||||||||||

Pollen, Inc. Series H1 Preferred | 8.36% PIK | USD | 108,305 |

| 3,359,435 |

| 3,414,857 | 1,4,8 | ||||||||||||||

Pollen, Inc. Series H2 Preferred | 7.53% PIK | USD | 64,983 |

| 1,856,902 |

| 1,929,345 | 1,4,8 | ||||||||||||||

| 11,512,788 |

| 12,382,026 | |||||||||||||||||||

Technology — 0.4% |

|

| ||||||||||||||||||||

GS Holder, Inc. Preferred | 17.33% PIK | USD | 5,000 |

| 4,850,000 |

| 5,000,000 | 1,4,8 | ||||||||||||||

Mandolin Technology Holdings, Inc. — Series A Preferred | 10.50% PIK | USD | 3,500 |

| 3,395,000 |

| 3,444,406 | 1,4,8 | ||||||||||||||

Riskonnect Parent, LLC — Series B Preferred | 15.31% PIK | USD | 3,000 |

| 2,940,000 |

| 3,000,000 | 4,8 | ||||||||||||||

| 11,185,000 |

| 11,444,406 | |||||||||||||||||||

Total Preferred Stocks |

| 32,060,456 |

| 33,159,711 | ||||||||||||||||||

|

| |||||||||||||||||||||

Common Stocks — 0.3% |

|

| ||||||||||||||||||||

Financials — 0.0% |

|

| ||||||||||||||||||||

Barings BDC, Inc. | USD | 113,298 |

| 1,162,244 |

| 1,053,671 | 1 | |||||||||||||||

|

| |||||||||||||||||||||

Health Care — 0.2% |

|

| ||||||||||||||||||||

Prolacta Bioscience, Inc. (Class A-3) | USD | 3,958,334 |

| 3,992,815 |

| 3,992,816 | 4 | |||||||||||||||

Vardiman Black Holdings, LLC | USD | 3,639,628 |

| — |

| — | 4 | |||||||||||||||

WCI-BXC Investment Holdings LP | USD | 786,000 |

| 786,000 |

| 786,000 | 4 | |||||||||||||||

| 4,778,815 |

| 4,778,816 | |||||||||||||||||||

Industrials — 0.0% |

|

| ||||||||||||||||||||

Atomic Transport, LLC | USD | 2,188 |

| 654,496 |

| 1,163,136 | 1,4,14 | |||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

17

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||

Common Stocks (Continued) |

|

| ||||||||||||||||||||

Technology — 0.1% |

|

| ||||||||||||||||||||

GSV PracticeTek Holdings, LLC, | USD | 1,590,747 | $ | 1,740,277 | $ | 1,740,277 | 4 | |||||||||||||||

Total Common Stocks |

| 8,335,832 |

| 8,735,900 | ||||||||||||||||||

|

| |||||||||||||||||||||

Subordinated Debt — 0.1% |

|

| ||||||||||||||||||||

Financials — 0.1% |

|

| ||||||||||||||||||||

OTR Midco, LLC | 12.00% | 5/13/2026 | USD | 2,000,000 |

| 2,000,000 |

| 2,000,000 | 1,4 | |||||||||||||

|

| |||||||||||||||||||||

Materials — 0.0% |

|

| ||||||||||||||||||||

Comar Holding Company, LLC | 12.50% PIK | LIBOR | 1,075 | 6/18/2026 | USD | 1,891,682 |

| 1,891,460 |

| 1,871,185 | 1,4,7 | |||||||||||

Total Subordinated Debt |

| 3,891,460 |

| 3,871,185 | ||||||||||||||||||

|

| |||||||||||||||||||||

Warrants — 0.1% |

|

| ||||||||||||||||||||

Energy — 0.0% |

|

| ||||||||||||||||||||

Service Compression, LLC |

|

| ||||||||||||||||||||

Exercise Price: $1.35 |

|

| ||||||||||||||||||||

Expiration Date: 1/17/2031 | USD | N/A |

| — |

| 162,014 | 1,4 | |||||||||||||||

|

| |||||||||||||||||||||

Financials — 0.0% |

|

| ||||||||||||||||||||

CTF Clear Finance Technology Corp |

|

| ||||||||||||||||||||

Exercise Price: $0.01 |

|

| ||||||||||||||||||||

Expiration Date: 10/2/2035 | USD | 25,228,521** |

| — |

| — | 4 | |||||||||||||||

|

| |||||||||||||||||||||

Health Care — 0.1% |

|

| ||||||||||||||||||||

ADMA Biologics, Inc. |

|

| ||||||||||||||||||||

Exercise Price: $1.65 |

|

| ||||||||||||||||||||

Expiration Date: 3/23/2029 | USD | 260,087** |

| — |

| 1,357,427 | 4 | |||||||||||||||

ADMA Biologics, Inc. |

|

| ||||||||||||||||||||

Exercise Price: $3.26 |

|

| ||||||||||||||||||||

Expiration Date: 4/30/2030 | USD | 67,071** |

| — |

| 304,539 | 4 | |||||||||||||||

Xeris Biopharma Holdings, Inc. |

|

| ||||||||||||||||||||

Exercise Price: $2.28 |

|

| ||||||||||||||||||||

Expiration Date: 3/8/2029 | USD | 43,860** |

| — |

| 80,577 | 4 | |||||||||||||||

| — |

| 1,742,543 | |||||||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

18

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Portfolio Company | Investment | Interest | Reference | Basis | Maturity | Currency | Shares/ | Cost | Fair | |||||||||||||

Warrants (Continued) |

|

| ||||||||||||||||||||

Technology — 0.0% |

|

| ||||||||||||||||||||

Afiniti, Inc. (via a participation with VHG Investment Fund I, L.P.) |

|

| ||||||||||||||||||||

Exercise Price: $40.80 |

|

| ||||||||||||||||||||

Expiration Date: 6/13/2024 | USD | 3,246** | $ | 172,839 | $ | 65,326 | 1,4 | |||||||||||||||

Total Warrants |

| 172,839 |

| 1,969,883 | ||||||||||||||||||

|

| |||||||||||||||||||||

Short-Term Investments — 6.1% |

|

| ||||||||||||||||||||

State Street Institutional U.S. Government Money Market | 5.26% | USD | 177,281,347 |

| 177,281,347 |

| 177,281,347 | 1,15 | ||||||||||||||

Total Short-Term Investments |

| 177,281,347 |

| 177,281,347 | ||||||||||||||||||

Total Investments — 108.0% |

| 2,960,671,873 |

| 3,159,842,889 | ||||||||||||||||||

Liabilities Less Other Assets — (8.0)% |

|

| (233,934,122 | ) | ||||||||||||||||||

Net Assets — 100.0% |

| $ | 2,925,908,767 | |||||||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

19

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

ARR CSA – Alternate Reference Rate Credit Adjustment Spread

BASE – Base rate as defined in the credit agreement

BDC – Business Development Company

EUR – Euro

EURIBOR – Euro Interbank Offered Rate

LIBOR – London Interbank Offered Rate

LLC – Limited Liability Company

LP – Limited Partnership

SOFR – Secured Overnight Financiang Rate

US – United States

USD – United States Dollar

* Subordinated note position. Rate shown is the effective yield as of period end.

** Shares represent underlying security.

1 As of March 31, 2024 all or a portion of the security has been pledged as collateral for a secured revolving facility. The market value of the securities in the pledged account totaled $1,710,579,746 as of March 31, 2024. See Note 2, subsection Borrowing, Use of Leverage of the Notes to Consolidated Financial Statements for additional information.

2 Investment valued using net asset value per share as practical expedient. See Note 12 for respective investment strategies, unfunded commitments, and redemptive restrictions.

3 This investment was made through a participation. Please see Note 2 for a description of loan participations.

4 Value was determined using significant unobservable inputs.

5 Represents an unfunded loan commitment. The rate disclosed is equal to the commitment fee. The negative cost and/or fair value, if applicable, is due to the discount received in excess of the principal amount of the unfunded commitment. See Note 2 for additional information.

6 Foreign securities purchased in foreign currencies are converted to U.S. Dollars using period end spot rates.

7 Floating rate security. Rate shown is the rate effective as of period end.

8 Principal includes accumulated payment in kind (“PIK”) interest and is net of repayments, if any.

9 A portion of this holding is subject to unfunded loan commitments. The stated interest rate reflects the reference rate and spread for the funded portion. See Note 2 for additional information.

10 Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities are restricted. They may only be resold in transactions exempt from registration normally to qualified institutional buyers. The total value of these securities is $77,283,633, which represents 2.6% of total net assets of the Fund.

11 Callable.

12 Variable rate security. Rate shown is the rate in effect as of period end.

13 Jayhawk Intermediate, LLC is the holding company that owns ProPharma Group, LLC.

14 Atomic Blocker, LLC holds Class A Preferred Units and Class W Common Units in Atomic Holdings, LLC, which is the holding company that owns Atomic Transport, LLC.

15 The rate is the annualized seven-day yield at period end.

16 These securities are restricted, the total value of these securities is $2,289,740,322, which represents 77.0% of total net assets of the Fund.

See accompanying Notes to Consolidated Financial Statements.

20

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Additional information on restricted securities is as follows:

Security | First | Cost | |||

17Capital Co-Invest (B) SCSp | 9/23/2021 | $ | 5,462,221 | ||

AG Asset Based Credit Fund L.P. | 9/13/2023 |

| 82,500,000 | ||

AG Essential Housing Fund II Holdings (DE), L.P. | 3/23/2022 |

| 12,075,000 | ||

Ares Commercial Finance, LP | 6/30/2021 |

| 28,535,713 | ||

Ares Pathfinder Fund II (Offshore), LP | 8/31/2023 |

| 1,831,168 | ||

Ares Priority Loan Co-Invest LP | 1/25/2023 |

| 28,625,000 | ||

Ares Private Credit Solutions (Cayman), L.P. | 12/29/2022 |

| 17,429,603 | ||

Ares Special Opportunities Fund II, LP | 11/7/2022 |

| 17,388,406 | ||

Ares Special Opportunities Fund, LP | 12/29/2023 |

| 7,597,632 | ||

Atalaya A4 (Cayman), LP | 8/2/2021 |

| 29,894,850 | ||

Atalaya Asset Income Fund Evergreen, LP | 2/28/2022 |

| 10,550,196 | ||

Atalaya Digithouse Opportunity Fund, LLC | 12/14/2021 |

| 277,516 | ||

Axonic Private Credit Fund I, LP | 4/27/2023 |

| 5,235,849 | ||

Banner Ridge DSCO Fund I, LP | 6/30/2023 |

| 15,480,563 | ||

Banner Ridge DSCO Fund II (Offshore), LP | 10/11/2022 |

| 9,691,695 | ||

Banner Ridge Secondary Fund IV (Offshore), LP | 6/30/2021 |

| 5,219,797 | ||

Banner Ridge Secondary Fund V (Offshore), LP | 5/31/2023 |

| 14,018,308 | ||

Benefit Street Partners Real Estate Opportunistic Debt Fund L.P. | 3/2/2022 |

| 54,778,195 | ||

Blackstone Tactical Opportunities Fund (Matrix Co-Invest) LP | 9/20/2023 |

| 4,719,266 | ||

Blue Owl First Lien Fund (Offshore), L.P. | 7/1/2022 |

| 4,103,056 | ||

Blue Owl Real Estate Fund VI | 1/31/2023 |

| 2,237,086 | ||

Blue Owl Technology Finance Corp. | 6/29/2022 |

| 10,332,953 | ||

Blue Owl Technology Finance Corp. II | 12/30/2021 |

| 7,927,947 | ||

Boost Co-Invest LP | 1/25/2024 |

| 6,764,671 | ||

BP Holdings RHO LLC | 6/7/2023 |

| 9,099,750 | ||

BP Holdings Tau, LLC | 6/29/2023 |

| 683,208 | ||

BP Holdings Zeta LP – Class A | 11/29/2023 |

| 8,609,327 | ||

BP Holdings Zeta LP – Class B | 11/29/2023 |

| 1,410,673 | ||

BPC Real Estate Debt Fund, LP | 6/7/2023 |

| 48,806,204 | ||

BSOF Parallel Onshore Fund L.P. (Class Absolute III Series 3 Interests) | 9/1/2023 |

| 5,242,498 | ||

BSOF Parallel Onshore Fund L.P. (Class Chestnut II Series 2) | 12/12/2023 |

| 20,108,879 | ||

BSOF Parallel Onshore Fund L.P. (Class Gnochi Series 2 Interests) | 10/10/2023 |

| 30,679,130 | ||

BSOF Parallel Onshore Fund L.P. (Class Olympic Srt Interests) | 9/1/2023 |

| 100,000,000 | ||

BSOF Parallel Onshore Fund L.P. (Class Colonnade 2024 Series 3) | 3/22/2024 |

| 10,250,000 | ||

Burford Advantage Feeder Fund A, LP | 1/28/2022 |

| 10,681,900 | ||

Callodine Perpetual ABL Fund, LP | 10/3/2022 |

| 95,526,538 | ||

Carlyle Credit Opportunities Fund (Parallel) II, SCSp | 12/14/2021 |

| 9,043,286 | ||

CCOF Alera Aggregator, L.P. | 4/25/2023 |

| 4,856,250 | ||

CCOF III Nexus Co-Invest Aggregator, L.P. | 3/22/2024 |

| 5,130,126 | ||

CCOF Sierra II, L.P. | 7/29/2022 |

| 3,906,521 | ||

Chilly HP SCF Investor, LP | 2/9/2022 |

| 2,970,297 | ||

CL Oliver Co-Invest I, L.P. | 6/28/2023 |

| 5,048,999 | ||

See accompanying Notes to Consolidated Financial Statements.

21

Cliffwater Enhanced Lending Fund |

Consolidated Schedule of Investments As of March 31, 2024 (Continued) |

Security | First | Cost | |||

Comvest Special Opportunities Fund, L.P. | 2/3/2022 | $ | 11,650,392 | ||

Contingency Capital Fund I-A, LP | 11/28/2022 |

| 45,851,047 | ||

Crestline Nevermore Holdco, L.P. | 12/7/2023 |

| 12,916,934 | ||

Crestline PF Sentry Fund (US), LP | 8/14/2023 |

| 4,594,328 | ||

Crestline Specialty Lending III (U.S.), L.P. | 8/30/2021 |

| 13,778,564 | ||

D.E. Shaw Diopter International Fund, L.P. | 10/20/2022 |

| 50,985,204 | ||

Everberg Capital Partners II, L.P. | 10/11/2021 |

| 12,884,181 | ||

EVP II LP | 11/30/2023 |

| 20,173,893 | ||

Felicitas Diner Offshore, LP | 12/28/2022 |

| 2,625,575 | ||

Felicitas Secondary Fund II Offshore, LP | 9/10/2021 |

| 10,616,857 | ||

Felicitas Tactical Opportunities Fund, LP | 10/26/2022 |

| 39,860,000 | ||

Franklin BSP Lending Corporation | 11/30/2021 |

| 1,795,011 | ||

Gramercy PG Holdings, LP (Common Interests) | 3/22/2024 |

| 8,877,594 | ||

Gramercy PG Holdings, LP (Preferred Interests) | 3/22/2024 |

| 5,450,422 | ||

Guggenheim MM-C CLO | 7/26/2023 |

| 90,202,500 | ||

Harvest Partners Structured Capital Fund III, L.P. | 9/22/2021 |

| 12,618,669 | ||

Hayfin Healthcare Opportunities Fund (US Parallel), LP | 6/29/2022 |

| 17,448,920 | ||

Hercules Private Global Venture Growth Fund I, L.P. | 8/6/2021 |

| 130,464,177 | ||

HPS Offshore Strategic Investment Partners V, LP | 5/1/2023 |

| 23,210,756 | ||

HPS Mint Co-Invest Fund, L.P. | 5/25/2022 |

| 6,473,263 | ||

HPS Specialty Loan Fund V-L, L.P. | 7/30/2021 |

| 21,679,075 | ||

ICG LP Secondaries Fund I (Feeder) SCSp | 12/29/2023 |

| 9,534,782 | ||

King Street Opportunistic Credit Evergreen Fund, L.P. | 1/31/2023 |

| 70,000,000 | ||

KWOL Co-Invest, LP | 11/30/2023 |

| 2,500,000 | ||

Linden Structured Capital Fund-A, LP | 6/30/2021 |

| 20,535,021 | ||

Madison Realty Cap Debit Fund, IV LP | 9/29/2023 |

| 13,564,062 | ||

Magenta Co-Invest L.P. | 3/5/2024 |

| 6,000,000 | ||

Marilyn Co-Invest, L.P. | 1/14/2022 |

| 24,732,588 | ||

Minerva Co-Invest, L.P. | 2/11/2022 |

| 12,468,490 | ||

NB Capital Solutions Co-Investment (Wolverine), LP | 11/15/2023 |

| 1,380,844 | ||

NB Credit Opportunities II Cayman Feeder, LP | 8/31/2022 |

| 18,685,489 | ||

OrbiMed RCO IV Offshore Feeder, LP | 12/30/2022 |

| 12,534,441 | ||

Pathlight Capital Evergreen Fund, LP | 12/30/2022 |

| 34,143,592 | ||

Pathlight Capital Fund II, LP | 6/30/2021 |

| 32,167,772 | ||

Pennybacker Real Estate Credit II, LP | 5/6/2022 |

| 2,467,491 | ||

Pennybacker Real Estate Credit II Pacific, LLC | 5/6/2022 |

| 18,149,241 | ||

Raven Asset-Based Credit Fund II LP | 9/21/2021 |

| 15,156,811 | ||

Raven Evergreen Credit Fund II, LP | 4/22/2022 |

| 55,052,265 | ||

Redwood Enhanced Income Corp. | 6/30/2022 |

| 28,275,000 | ||

SB DOF Speedway, LLC | 3/31/2023 |

| 7,887,281 | ||

Sculptor Real Estate Science Park Fund, LP | 5/4/2022 |