As filed with the U.S. Securities and Exchange Commission on

September

2

8

, 2023

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number

811-23802

Destiny Tech100 Inc.

(Exact name of registrant as specified in charter)

1401 Lavaca Street, #144

Austin, TX 78701

(Address of principal executive offices) (Zip code)

Sohail Prasad

c/o Destiny Tech100 Inc.

1401 Lavaca Street, #144

Austin, TX 78701

(Name and address of agent for service)

(415) 639-9966

Registrant's telephone number, including area code

Date of fiscal year end:

December 31

Date of reporting period:

December 31, 2022

EXPLANATORY NOTE

This Amendment on Form N-CSR/A (this “Amendment”) amends the Form N-CSR of Destiny Tech100 Inc. (the “Fund”) for the fiscal year ended December 31, 2022, which was filed with the Securities and Exchange Commission (the “SEC”) on March 30, 2023 (the “Original Form N-CSR”).

This Amendment is being filed solely for the purpose of correcting the “

Report of Independent Registered Public Accounting Firm”

included in the Original

Form N-CSR (the “Report”) to include reference to Marcum LLP’s audit of all periods presented in the Fund’s financial statements. The changes made to the Report do not in any way change the conclusions expressed in the Report that was included in the Original Form

N-CSR.

Pursuant to Rule 12b-15 under the Securities Exchange Act of 1934, as amended, and Rule 8b-15 under the Investment Company Act of 1940, as amended (the “1940 Act”), this Amendment also contains new certifications for the Fund’s Chief Executive Officer and Chief Financial Officer pursuant to Rules 30a-2(a) and 30a-2(b) under the 1940 Act, which are attached as exhibits hereto. Pursuant to Rules 12b-15 and 8b-15 referenced above, the Fund has included the entire text of Item 1(a) in this Amendment.

Except for the amendment to correct the Report and the certifications referred to above, no other changes have been made to the Original Form N-CSR, and, accordingly, Items 1(b) through 12 thereof from the Original Form N-CSR are hereby incorporated by reference. The Original Form N-CSR continues to speak as of the date of the Original Form N-CSR and, except as described above, this Amendment does not reflect events occurring after the filing of the Original Form N-CSR, nor does it modify or update in any way the disclosures contained in the Original Form N-CSR. Accordingly, this Amendment should be read in conjunction with the Original Form N-CSR and the Fund's other filings with the SEC.

Item 1. Reports to Stockholders.

( a ) | The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1) |

Table of Contents

Destiny Tech100 Inc.

As of December 31, 2022

March 27, 2023

Dear Shareholders:

For the 12 months ended December 31, 2022, the investments held by Destiny Tech100 (the “Fund”) generated a return of -37.1%

1

. This compares to a -32.5% return for the Nasdaq Composite, a benchmark, over the same period.2022 was a challenging year for owners of both public and private assets. Many domestic and global stock indexes faced declines on the order of fifteen to twenty percent while US bonds, also down double digits, failed to backstop the drawdown in equities. In turn, the “classic” portfolio of 60% U.S. stocks and 40% bonds produced its worst annual return since 1932

2

.The tightening of monetary policy by the Federal Reserve has been particularly hard on high-growth technology businesses. With the 10-year treasury yield more than doubling amid the fastest rate-hiking cycle in four decades, once-cheap and abundant capital has evaporated, prompting a re-rating of forward-looking revenue multiples by market participants. Furthermore, as borrowing costs rise, operating losses have become a problem. The ARK Innovation ETF, AXS de-SPAC ETF, and Goldman Sachs Non Profitable Tech index - proxies for high-growth and low-profitability technology performance - returned -67.0%, -73.1%, and -62.3%, respectively, in 2022.

We believe the compression of multiples in the public markets will have a continuing impact on private company valuations. In Q4 2022, the median secondary trade price executed on the Forge platform represented an approximate 50% discount to a given company’s last fundraising round, as opposed to a 39% discount in Q3 and a 16% discount in Q2 2022

3

. Data from Pitchbook indicates that the median late-stage primary round post-money valuation declined 25.7% year-over-year4

.Adverse public and private market conditions may force private companies and shareholders with limited liquidity options to accept lower valuations moving forward, presenting more attractive risk-adjusted entry points. We believe these conditions could create great opportunities to purchase high-quality technology businesses at sensible prices. We will continue to utilize our investment targeting and screening process to identify and seek to take advantage of such opportunities in the coming year.

Thank you for your loyalty and continued support.

Sincerely,

Sohail Prasad

1. Performance represents the depreciation on investments for the one-year period of January 1, 2022 to December 31, 2022.

2. https://www.ft.com/content/c93f3660-821f-458b-ae0f-23ac05b8f03f

3. https://forgeglobal.com/insights/reports/investors-eye-next-wave-of-2023-unicorns/

4. Pitchbook data for the two-year period of January 1, 2021 to December 31, 2022

| 1 |

Destiny Tech100 Inc.

December 31, 2022

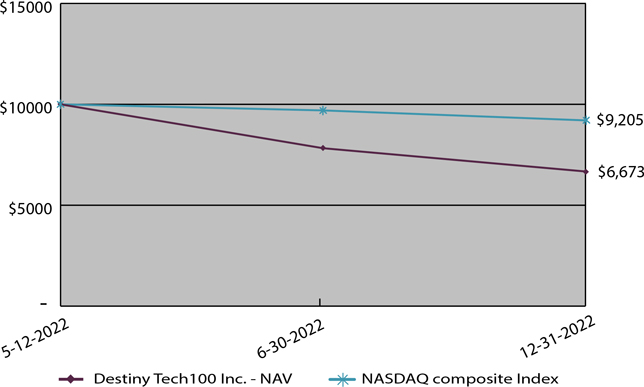

The Fund’s performance figures* for the period ended December 31, 2022 compared to its benchmark:

| Fund/Index | Since Inception (a) | |||

| Destiny Tech100 Inc. - NAV | (33.27 | )% | ||

| Fund Benchmark | ||||

NASDAQ Composite Index (b) | (7.95 | )% | ||

Comparison of Change in Value of $10,000 Initial Investment

| * | The Fund’s past performance does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when sold may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the sale of Fund shares. Current performance of the Fund may be lower or higher than the performance quoted. Returns are calculated using the traded net asset value or “NAV” on December 31, 2022. |

| (a) | The graph shown above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. All returns reflect reinvested dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. |

| (b) | The Nasdaq Composite is a market cap-weighted index, simply representing the value of all its listed stocks. The set of eligible securities includes common stocks, ordinary shares, and common equivalents such as ADRs. However, convertible debentures, warrants, Nasdaq-listed closed-end funds, exchange traded funds (ETFs), preferred stocks, and other derivative securities are excluded. |

The graph shown above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. All returns reflect reinvested dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares.

| 2 |

Destiny Tech100 Inc.

As of December 31, 2022

| Shares/ Principal | Acquisition | ||||||||||||||

| Amount | Security | Date | Cost | Fair Value | |||||||||||

Private Investments, at fair value 87.39% | |||||||||||||||

| Agreement for Future Delivery of Common Shares 3.99% | |||||||||||||||

| Financial Technology 3.99% | |||||||||||||||

| 1,540 | Plaid, Inc. (a)(b)(c)(f) | 2/15/2022 | $ | 1,110,340 | $ | 672,379 | |||||||||

| 49,075 | Stripe, Inc. (a)(b)(c)(f) | 1/10/2022 | 3,478,813 | 1,594,938 | |||||||||||

| Total Agreement for Future Delivery of Common Shares - (Cost $4,589,153) | 4,589,153 | 2,267,317 | |||||||||||||

| Common Stocks 62.55% | |||||||||||||||

| Aviation/Aerospace 27.84% | |||||||||||||||

| 63,846 | Relativity Space, LLC (a)(b)(c)(d) | 12/28/2021 | 1,659,996 | 1,329,912 | |||||||||||

| 9,100 | Space Exploration Technologies Corp., Series A (a)(b)(c)(d) | 6/9/2022 | 618,618 | 690,963 | |||||||||||

| 135,135 | Space Exploration Technologies Corp. (a)(b)(c)(g) | 6/27/2022 | 10,009,990 | 10,260,800 | |||||||||||

| 47,143 | Space Exploration Technologies Corp., Class A and Class C (a)(b)(c)(d) | 6/8/2022 | 3,390,000 | 3,521,582 | |||||||||||

| 15,678,604 | 15,803,257 | ||||||||||||||

| Education Services 4.95% | |||||||||||||||

| 106,136 | ClassDojo, Inc. (a)(b)(c) | 11/19/2021 | 3,000,018 | 2,812,604 | |||||||||||

| Enterprise Software 5.02% | |||||||||||||||

| 88,885 | Automation Anywhere, Inc. (a)(b)(c) | 12/28/2021 | 2,609,219 | 748,412 | |||||||||||

| 110,234 | SuperHuman Labs, Inc. (a)(b)(c) | 6/25/2021 | 2,999,996 | 2,099,958 | |||||||||||

| 5,609,215 | 2,848,370 | ||||||||||||||

| Financial Technology 16.13% | |||||||||||||||

| 90,952 | CElegans Labs, Inc. (a)(b)(c) | 11/23/2021 | 2,999,977 | 2,999,977 | |||||||||||

| 3,077 | Klarna Bank AB (a)(b)(c) | 3/16/2022 | 4,657,660 | 793,865 | |||||||||||

| 55,555 | Public Holdings, Inc. (a)(b)(c) | 7/22/2021 | 999,990 | 999,990 | |||||||||||

| 8,200 | Revolut Group Holdings Ltd. (a)(b)(c) | 12/8/2021 | 5,275,185 | 2,002,768 | |||||||||||

| 117,941 | Brex, Inc. (a)(b)(c)(d) | 3/2/2022 | 4,130,298 | 2,358,820 | |||||||||||

| 18,063,110 | 9,155,420 | ||||||||||||||

| Gaming/Entertainment 6.06% | |||||||||||||||

| 4,946 | Epic Games, Inc. (a)(b)(c)(d) | 1/3/2022 | 6,998,590 | 3,437,470 | |||||||||||

| Mobile Commerce 1.27% | |||||||||||||||

| 23,690 | Maplebear, Inc. (a)(b)(c) | 10/8/2021 | 3,556,000 | 718,755 | |||||||||||

| Social Media 0.70% | |||||||||||||||

| 1,069 | Discord, Inc. (a)(b)(c) | 3/1/2022 | 724,942 | 395,530 | |||||||||||

See accompanying notes to the financial statements.

| 3 |

Destiny Tech100 Inc.

Schedule of Investments (continued)

As of December 31, 2022

| Shares/ Principal | Acquisition | |||||||||||||

| Amount | Security | Date | Cost | Fair Value | ||||||||||

| Supply Chain/Logistics 0.58% | ||||||||||||||

| 26,000 | Flexport, Inc. (a)(b)(c) | 3/29/2022 | $ | 520,000 | $ | 329,160 | ||||||||

| Total Common Stocks - | ||||||||||||||

| (Cost $54,150,479) | 54,150,479 | 35,500,566 | ||||||||||||

| Convertible Notes 9.93% | ||||||||||||||

| Aviation/Aerospace 9.93% | ||||||||||||||

| $ | 3,000,000 | Axiom Space, Inc. PIK, 3.00%, 12/22/2023 (b)(c)(e) | 12/22/2021 | 3,090,000 | 3,634,867 | |||||||||

| $ | 2,000,000 | Boom Technology, Inc., 5.00% 01/09/2027 (b)(c) | 2/11/2022 | 2,000,000 | 2,000,000 | |||||||||

| Total Convertible Notes - | ||||||||||||||

| (Cost $5,090,000) | 5,090,000 | 5,634,867 | ||||||||||||

| Preferred Stocks 10.92% | ||||||||||||||

| Financial Technology 6.54% | ||||||||||||||

| 45,455 | Bolt Financial, Inc., Series C Preferred Stock (a)(b)(c)(d) | 3/7/2022 | 2,000,020 | 1,136,375 | ||||||||||

| 60,250 | Chime Financial Inc. - Series A Preferred Stock (a)(b)(c) | 12/30/2021 | 5,150,748 | 1,826,780 | ||||||||||

| 176,886 | Jeeves, Inc. - Series C Preferred Stock (a)(b)(c) | 4/5/2022 | 749,997 | 749,997 | ||||||||||

| 7,900,765 | 3,713,152 | |||||||||||||

| Food Products 2.46% | ||||||||||||||

| 52,000 | Impossible Foods, Inc. - Series A Preferred Stock (a)(b)(c) | 6/17/2022 | 1,272,986 | 538,720 | ||||||||||

| 82,781 | Impossible Foods, Inc. - Series H Preferred Stock (a)(b)(c)(d) | 11/4/2021 | 2,098,940 | 857,616 | ||||||||||

| 3,371,926 | 1,396,336 | |||||||||||||

| Mobile Commerce 1.07% | ||||||||||||||

| 20,000 | Maplebear, Inc. - Series B Preferred Stock (a)(b)(c) | 11/16/2021 | 2,863,400 | 606,800 | ||||||||||

| Social Media 0.85% | ||||||||||||||

| 1,311 | Discord, Inc. - Series G Preferred Stock (a)(b)(c) | 3/1/2022 | 889,055 | 485,070 | ||||||||||

| Total Preferred Stocks - | ||||||||||||||

| (Cost $15,025,146) | 15,025,146 | 6,201,358 | ||||||||||||

| Total Investments, at fair value – 87.39% | ||||||||||||||

| (Cost $78,854,778) | $ | 49,604,108 | ||||||||||||

Other Assets Less Liabilities - 12.61 % | 7,159,932 | |||||||||||||

| Net Assets - 100.00% | $ | 56,764,040 | ||||||||||||

See accompanying notes to the financial statements.

| 4 |

Destiny Tech100 Inc.

Schedule of Investments (continued)

As of December 31, 2022

| Shares/ Principal | Acquisition | |||||||||||||

| Amount | Security | Date | Cost | Fair Value | ||||||||||

| Securities by Country as a Percentage of Investments Fair Value | ||||||||||||||

| United States 94.36% | ||||||||||||||

| Common Stocks | $ | 44,217,634 | $ | 32,703,933 | ||||||||||

| Convertible Notes | 5,090,000 | 5,634,867 | ||||||||||||

| Preferred Stocks | 15,025,146 | 6,201,358 | ||||||||||||

| Agreement for Future Delivery of | ||||||||||||||

| Common Shares | 4,589,153 | 2,267,317 | ||||||||||||

| Total United States | $ | 68,921,933 | $ | 46,807,475 | ||||||||||

| United Kingdom 4.04% | ||||||||||||||

| Common Stocks | 5,275,185 | 2,002,768 | ||||||||||||

| Total United Kingdom | $ | 5,275,185 | $ | 2,002,768 | ||||||||||

| Sweden 1.60% | ||||||||||||||

| Common Stocks | 4,657,660 | 793,865 | ||||||||||||

| Total Sweden | $ | 4,657,660 | $ | 793,865 | ||||||||||

| (a) | Non-income producing security. |

| (b) | Level 3 securities fair valued using significant unobservable inputs. (See Note 3) |

| (c) | Restricted investments as to resale. (See Note 2) |

| (d) | These securities have been purchased through Special Purpose Vehicles (“SPVs”) in which the Fund has a direct investment of ownership units. The shares, cost basis and fair value stated are determined based on the underlying securities purchased by the SPV and the Fund’s ownership percentage. |

| (e) | Paid in kind security which may pay interest in additional par. |

| (f) | Investment is an SPV that holds multiple forward agreements that represent common shares of Stripe, Inc. and Plaid, Inc. Forward contracts involve the future delivery of shares of a portfolio company upon such securities becoming freely transferable or the removal of restrictions on transfer. The counterparties are shareholders of the portfolio company. The aggregate total of the forward contracts for each SPV represents less than 5% of theFund’s net assets . |

| (g) | These securities have been purchased through a SPV in which the Fund has a direct investment of ownership units. The shares, cost basis and fair value stated are determined based on the underlying securities purchased by the SPV and the Fund’s ownership percentage of the SPV. The SPV holds approximately 99% of Class A Common Shares and 1% of Class J Preferred Shares. |

LLC - Limited Liability Company

LP - Limited Partnership

Ltd. - Limited

See accompanying notes to the financial statements.

| 5 |

Destiny Tech100 Inc.

As of December 31, 2022

| Assets | ||||

| Investments, at fair value (Cost - $78,854,778) | $ | 49,604,108 | ||

| Cash | 12,025,800 | |||

| Deferred offering costs (See Note 2) | 72,170 | |||

| Interest Receivable | 184,250 | |||

| Total Assets | 61,886,328 | |||

| Liabilities | ||||

| Warrant liabilities, at fair value | 3,571,824 | |||

| Professional fees payable | 292,251 | |||

| Management fee payable (See Note 5) | 469,566 | |||

| Offering cost payable to Organizer (See Notes 2 and 5) | 216,510 | |||

| Fund administration fee payable | 169,458 | |||

| Payable to Shareholder | 75,000 | |||

| Organization cost payable to Organizer (See Notes 2 and 5) | 70,202 | |||

| Due to Organizer (See Note 5) | 224,824 | |||

| Other fees payable | 32,653 | |||

| Total Liabilities | 5,122,288 | |||

| Net Assets | $ | 56,764,040 | ||

| Commitments and contingencies (See Note 6) | ||||

| Net Assets Consist Of: | ||||

| Paid-in-capital (500,000,000 shares authorized, $0.00001 par value) | 64,722,000 | |||

| Total distributable losses | (7,957,960 | ) | ||

| Net Assets a ttri able to Common Shareholdersbu t | $ | 56,764,040 | ||

| Net Asset Value Per Share | ||||

| Net assets applicable to Common Shareholders | $ | 56,764,040 | ||

| Common Shares outstanding of beneficial interest outstanding, at $0.00001 par value; | 10,879,905 | |||

| 500,000,000 shares authorized, 10,879,905 shares issued and outstanding | ||||

| Net Asset Value Per Share applicable to Common Shareholders | $ | 5.22 | ||

See accompanying notes to the financial statements.

| 6 |

Destiny Tech100 Inc.

For the Year Ended December 31, 2022

| Investment Income | ||||

| Interest Income | $ | 184,250 | ||

| Total investment income | 184,250 | |||

| Expenses | ||||

| Management fees (See Note 5) | 1,847,629 | |||

| Audit and tax fees | 318,585 | |||

| Pricing fees | 275,000 | |||

| Legal fees | 217,000 | |||

| Offering costs (See Notes 2 and 5) | 144,340 | |||

| Trustee fees | 127,671 | |||

| Fund administration fees (See Note 5) | 83,332 | |||

| Chief compliance and principal financial officer fees (See Note 5) | 63,836 | |||

| Research fees | 22,653 | |||

| Custody fees | 5,233 | |||

| Other accrued expenses | 18,086 | |||

| Total Expenses | 3,123,365 | |||

| Net Investment Loss | (2,939,115 | ) | ||

| Recognition of conversion of SAFE note liabilities to Common Shares | 25,375,657 | |||

| Change in unrealized fair value on investments | (28,483,048 | ) | ||

| Change in unrealized appreciation on SAFE note liabilities | 677,092 | |||

| Change in unrealized appreciation on fair value of warrants | 1,441,461 | |||

| Net Decrease in Net Assets from Operations | $ | (3,927,953 | ) | |

See accompanying notes to the financial statements.

| 7 |

Destiny Tech100 Inc.

For the Year Ended December 31, 2022 | For the period of January 25, 2021 (commencement of operations) to December 31, 2021 | |||||||

| Operations | ||||||||

| Net investment gain/(loss) | $ | (2,939,115 | ) | $ | (3,262,384 | ) | ||

| Recognition of conversion of SAFE note liabilities to Common Shares | 25,375,657 | — | ||||||

| Net change in unrealized appreciation/depreciation on investments, SAFE note liabilities and warrants | (26,364,495 | ) | (767,623 | ) | ||||

| Increase/(Decrease) in net assets resulting from operations | (3,927,953 | ) | (4,030,007 | ) | ||||

| Distributions to Shareholders | ||||||||

| From distributable earnings | — | — | ||||||

| Total distributions to Fund shareholders | — | — | ||||||

| Capital Share Transactions | ||||||||

| Proceeds from shareholder subscriptions | — | 25,000 | (1) | |||||

| Conversion of SAFE Notes | 64,697,000 | (2) | — | |||||

| Increase/(Decrease) in net assets from capital share transactions | 64,697,000 | 25,000 | ||||||

| Total increase/(decrease) in net assets | 60,769,047 | (4,005,007 | ) | |||||

| Net Assets | ||||||||

| Beginning of period | (4,005,007 | ) | — | |||||

| End of period | $ | 56,764,040 | $ | (4,005,007 | ) | |||

| Capital Share Activity | ||||||||

| Shares sold | — | 2,500,000 | (1) | |||||

| Conversion to SAFE Notes | 9,424,629 | (2) | — | |||||

| Reverse stock split | (1,044,724 | ) | — | |||||

| Net increase in shares outstanding | 8,379,905 | 2,500,000 | ||||||

| Shares outstanding, beginning of period | 2,500,000 | — | ||||||

| Shares outstanding, end of period | 10,879,905 | 2,500,000 | ||||||

| (1) | On January 25, 2021, the Organizer purchased 2,500,000 shares of the Fund’s common stock, par value $0.00001, for $25,000. |

| (2) | On May 11, 2022, each SAFE holder received from the Fund a number of shares of common stock equal to the total amount invested by such investor in the private offering divided by $10.00. Following the SAFE Conversion and the reverse stock split, the Fund has 10,879,905 shares of common stock issued and outstanding. |

See accompanying notes to the financial statements.

| 8 |

Destiny Tech100 Inc.

For the Year Ended December 31, 2022

| Cash Flows From Operating Activities | ||||

| Net decrease in net assets from operations | $ | (3,927,953 | ) | |

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||

| Recognition of conversion of SAFE note liabilities to Common Shares | (25,375,657 | ) | ||

| Net unrealized depreciation of investments | 28,483,048 | |||

| Purchases of investments | (39,778,832 | ) | ||

| Return of capital from investments | 13,310,000 | |||

| Net unrealized appreciation on SAFE note liabilities | (677,092 | ) | ||

| Net unrealized appreciation on warrants | (1,441,461 | ) | ||

| Changes in operating assets and liabilities: | ||||

| Increase in interest receivable | (184,250 | ) | ||

| Decrease in deferred offering cost payable to Organizer | 144,340 | |||

| Increase in Due to Organzier | 204,749 | |||

| Increase in professional fees payable | 40,251 | |||

| Increase in fund administration fee payable | 169,458 | |||

| Increase in other fees payable | 32,653 | |||

| Decrease in investment fee payable | (390,028 | ) | ||

| Decrease in management fee payable | (933,731 | ) | ||

| Increase in payable to Shareholder | 75,000 | |||

| Decrease in payable for investments purchased | (6,998,590 | ) | ||

| Net cash used in operating activities | (37,248,095 | ) | ||

| Cash Flows from Financing Activities | ||||

| Proceeds from issuance of SAFE notes | 2,398,502 | |||

| Proceeds from issuance of warrants | 106,528 | |||

| Net cash provided by financing activities | 2,505,030 | |||

| Net Decrease in cash | (34,743,066 | ) | ||

| Cash, beginning of period | 46,768,865 | |||

| Cash, end of period | $ | 12,025,800 | ||

| Supplemental disclosure of cash flow information: | ||||

| Non-cash financing activities | ||||

| SAFE notes conversion to common stock | $ | 64,697,000 | ||

| Total non-cash financing activities | 64,697,000 | |||

| 9 |

Destiny Tech100 Inc.

For a Share Outstanding Throughout the Period Presented

| For the Year | ||||

| Ended December 31, | ||||

2022 (1)(2) | ||||

| Net Asset Value, Beginning of Year | $ | (1.60 | ) | |

| Income from Investment Operations | ||||

| Net investment income/(loss) (3) | (0.27 | ) | ||

| Recognition of conversion of SAFE note liabilities to Common Shares | 2.33 | |||

| Change in unrealized fair value on investments and warrants | (2.42 | ) | ||

| Total income/(loss) from investment operations and recognition of conversion of SAFE | ||||

| Note liabilities to Common Shares | (0.36 | ) | ||

| Distributions to Shareholders | ||||

| From net investment income | - | |||

| From return of capital | - | |||

| Total distributions | - | |||

| Effect of shares issued from SAFE note conversion to Common Shares | 7.18 | |||

| Increase/(Decrease) in Net Asset Value | 6.82 | |||

| Net Asset Value, End of Year | $ | 5.22 | ||

Total Return (4) | 426.08 | % (6) | ||

| Supplemental Data and Ratios | ||||

| Net assets attributable to common shares, end of period (000s) | $ | 56,764 | ||

| Ratio of expenses to average net assets (5) | (5.13 | )% | ||

| Ratio of net investment income to average net assets (5) | (4.82 | )% | ||

| Portfolio turnover rate | 0.24 | % | ||

| (1) | The Fund commenced operations on January 25, 2021. For the period from January 25, 2021 to May 11, 2022, the Organizer was the sole owner of the Fund’s shares of common stock of 2,500,000 shares. Financial Highlights were not were not presented for the Fund for the 2021 period. |

| (2) | On May 11, 2022, each SAFE holder received from the Fund a number of shares of common stock equal to the total amount invested by such investor in the private offering divided by $10.00. Following the SAFE Conversion and the reverse stock split, the Fund has 10,879,905 shares of common stock issues and outstanding. |

| (3) | Calculated using the average shares method. |

| (4) | Returns do not reflect the deduction of taxes the shareholder would pay on fund distributions or redemptions of Fund shares. |

| (5) | Ratios do not include expenses of underlying private investments in which the Fund invests. |

| (6) | Total return has been calculated using the absolute value of the initial Net Asset Value due to a negative Net Asset Value as of January 1, 2022. The total return for the fund has been calculated for shareholders owning shares for the entire period and does not represent the return for holders of SAFE notes that converted to common stock during the year ended December 31, 2022. |

| 10 |

Destiny Tech100 Inc.

December 31, 2022

(1) Organization

Destiny Tech100 Inc. (the “Fund”) was formed on November 8, 2020 as a Maryland corporation and commenced operations on January 25, 2021. On May 13, 2022, the Fund registered with the Securities and Exchange Commission as an investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund is a-diversified, closed-end management investment company. The Fund intends to apply to have the common stock listed on the New York Stock Exchange (the “NYSE”) under the symbol “DXYZ”.

Destiny Advisors LLC, a Delaware limited liability company (the “Adviser”), serves as the investment adviser to the Fund. The Adviser is responsible for the overall management and affairs of the Fund and has full discretion to invest the assets of the Fund in a manner consistent with the Fund’s investment objective.

The Fund’s investment objective is to maximize the portfolio’s total return, principally by seeking capital gains on equity and equity-related investments. The Fund invests principally in the equity and equity-linked securities of what it believes to be rapidly growing venture-capital-backed emerging companies, primarily in the United States. The Fund may also invest on an opportunistic basis in select U.S. publicly traded equity securities or certain non-U.S. companies that otherwise meet the investment criteria.

The Adviser is a wholly-owned subsidiary of Destiny XYZ Inc. (the “Organizer”). The Organizer manages and controls the Adviser.

The Fund’s board of directors (the “Board”) has overall responsibility for monitoring and overseeing the Fund’s operations and investment program. A majority of the directors of the Board are not “interested persons” (as defined by the 1940 Act) of the Fund or the Adviser.

(2)

Summary of Significant Accounting Policies

The following is a summary of the significant accounting policies followed by the Fund in the preparation of its financial statements. All accounts are stated in U.S. dollars unless otherwise noted. The accompanying financial statements have been prepared in conformity with accounting principles generally accepted in the United State of America (“U.S. GAAP”). The Fund is an investment company and follows the accounting and reporting guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946,

Financial Services - Investment Companies.

(a) Investments

Investments in securities, including through SPVs, are recorded on the trade date, the date on which the Fund agrees to purchase or sell the securities.

The Fund may invest in SPVs that hold forward contracts. Forward contracts involve the future delivery of shares of a portfolio company upon such securities becoming freely transferable or the removal of restrictions on transfer. The counterparties are shareholders of the portfolio company. The Fund does not have information as to the identities of the shareholders; however, counterparty risk is mitigated by the fact that there is not a single counterparty on the opposite side of the forward contracts.

The Fund may invest in “forward contracts” that involve shareholders (each a “counterparty”) of a potential portfolio company whereby such counterparties promise future delivery of such securities upon transferability or other removal of restrictions. This may involve counterparty promises of future performance, including among other things transferring shares to us in the future, paying costs and fees associated with maintaining and transferring the shares, not transferring or encumbering their shares, and participating in further acts required of shareholders by the counterparty and their agreement with us. Should counterparties breach their agreement inadvertently, by operation of law, intentionally, or fraudulently, it could affect the Fund’s performance. The Fund’s ability and right to enforce transfer and payment obligations, and other obligations, against counterparties could be limited by acts of fraud or breach on the part of counterparties, operation of law, or actions of third parties. Measures the Fund takes to mitigate these risks, including powers of attorney, specific performance and damages provisions, any insurance policy, and legal enforcement steps, may prove ineffective, unenforceable, or economically impractical to enact.

| 11 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

The

o

rganizer of each SPV holding forward contracts may carry an insurance policy at their own expense to protect theSPV

against certain insured risks with respect to the forward purchase contracts. Insured risks include (i) an intentional attempt by as

hareholder to deceive theo

rganizer or theSPV

, or a failure to honor an obligation under, or refusal to settle, an obligation to theSPV

; (ii) certain events of bankruptcy; and (iii) in the case of death of as

hareholder, the refusal of thes

hareholder’s heirs, beneficiary, or estate to honor the obligation.In cases where the Fund purchases a forward contract through a secondary marketplace,

it

may have no direct relationship with, or right to contact, enforce rights against, or obtain personal information or contact information concerning the counterparty. In such cases,the Fund

will not be direct beneficiaries of the portfolio company’s securities or related instruments. Instead,it

would rely on a third party to collect, settle, and enforce its rights with respect to the portfolio company’s securities. There is no guarantee that said party will be successful or effective in doing so.Realized gains or losses on dispositions of investments represent the difference between the original cost of the investment, based on the specific identification method, and the proceeds received from the sale. The Fund applies a fair value accounting policy to its investments with changes in unrealized gains and losses recognized in the statement of operations as a component of net unrealized gain (loss).

(b)

Income Taxes

For the year ended December 31, 2022,

t

he Fund did not meet the requirements to be registered under the 1940 Act as a management company for the entirety of its taxable year. As a result, the Fund does not qualify as a regulated investment company for the 2022 taxable year and will be taxed as a C corporation.The Fund accounts for income taxes under the asset and liability method, which requires the recognition of deferred tax assets and liabilities for the expected future tax consequences of events that have been included in the financial statements. Under this method, the Fund determines deferred tax assets and liabilities on the basis of the differences between the financial statement and tax bases of assets and liabilities by using enacted tax rates in effect for the year in which the differences are expected to reverse. The effect of a change in tax rates on deferred tax assets and liabilities is recognized in income in the period that includes the enactment date.

The Fund recognizes deferred tax assets to the extent that the Fund believes that these assets are more likely than not to be realized. In making such a determination, the Fund considers all available positive and negative evidence, including future reversals of existing taxable temporary differences, projected future taxable income, tax-planning strategies, and results of recent operations. If the Fund determines that it would be able to realize

its

d

eferred tax assets in the future in excess of their net recorded amount, it would make an adjustment to the deferred tax asset valuation allowance, which would reduce the provision for income taxes.

The Fund records uncertain tax positions in accordance with ASC 740 on the basis of a two-step process in which (1) it determines whether it is more likely than not that the tax positions will be sustained on the basis of the technical merits of the position and (2) for those tax positions that meet the more-likely-than-not recognition threshold, it recognizes the largest amount of tax benefit that is more than 50 percent likely to be realized upon ultimate settlement with the related tax authority.

| 12 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

The Fund recognizes interest and penalties related to unrecognized tax benefits, if any, on the income tax expense line in the accompanying statement of operations. As of December 31, 2022, no accrued interest or penalties are included on the related tax liability line in the balance sheet.

(c)

Cash and Cash Equivalents

Cash includes cash in bank accounts. Cash equivalents include short-term highly liquid investments that are readily convertible to cash and have original maturities of three months or less. The Fund maintains cash in the bank accounts which, at times, may exceed the United States Federal Deposit Insurance Corporation (FDIC) limit of $250,000.

(d)

Income and Expenses

Interest income is recognized on an accrual basis as earned. Dividend income is recorded on the ex-dividend date. Expenses are recognized on an accrual basis as incurred.

Organization costs include costs relating to the formation and incorporation of the business. These costs are expensed as incurred. From the commencement of the Fund’s operations, the Fund has incurred and expensed organization costs of $70,202, which were paid by the Organizer to be reimbursed by the Fund and are reflected as “Organizational costs payable to Organizer” on the Statement of Assets and Liabilities.

Pursuant to the terms of the investment advisory agreement while the Fund operated as a private fund (the “Prior Advisory Agreement”) entered into between the Fund and the Adviser that was in operation while the Fund operated as a private fund, the Fund is obligated to pay up to $150,000 of organizational costs and amounts in excess thereof will be borne by the Adviser. As of December 31, 2022, the Adviser has not borne any of the organizational expenses as the total amount incurred by the Fund has not historically exceeded $150,000. See note 5 for details on the reimbursable organizational costs to the Adviser.

Offering costs were accounted for as deferred costs until the Fund registered as an investment company under the 1940 Act and were then amortized to expense over twelve months on a straight-line basis. These costs consist of fees for the legal preparation and filing fees associated with the private offering. As of December 31, 2022, these costs amount to $216,510, which were paid by the Organizer to be reimbursed by the Fund. On the Statement of Assets and Liabilities, $72,170 remains as a deferred asset while $144,340 has been amortized to expense in the Statement of Operations.

Certain investments may have contractual payment-in-kind (“PIK”) interest. PIK represents accrued interest that is added to the principal of the investment on the respective interest payment dates rather than being paid in cash and generally becomes due at maturity or upon being called by the issuer. PIK is recorded as interest income.

(e)

Use of Estimates

The preparation of financial statements in conformity with GAAP requires the Fund’s management to make estimates and assumptions that affect the amounts reported in the financial statements. Because of the uncertainties associated with estimation, actual results could differ from those estimates used in preparing the accompanying financial statements.

| 13 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

(f)

Concentrations of Credit Risk

Financial instruments which potentially expose the Fund to concentrations of credit risk consist of cash and cash equivalents. The Fund maintains its cash and cash equivalents in financial institutions at levels that have historically exceeded federally-insured limits.

(g)

Risks and Uncertainties

All investments are subject to certain risks. Changes in overall market movements, interest rates, or factors affecting a particular industry, can affect the ultimate value of the Fund’s investments. Investments are subject to a number of risks, including the risk that values will fluctuate as a result of changing expectations for the economy and individual investors.

Liquidity and Valuation Risk

- Liquidity risk is the risk that securities may be difficult or impossible to sell at the time the Adviser would like or at the price it believes the security is currently worth. Liquidity risk may be increased for certain Fund investments, including those investments in funds with gating provisions or other limitations on investor withdrawals and restricted or illiquid securities. Some SPVs in which the Fund invests may impose restrictions on when an investor may withdraw its investment or limit the amounts an investor may withdraw. To the extent that the Adviser seeks to reduce or sell out of its investment at a time or in an amount that is prohibited, the Fund may not have the liquidity necessary to participate in other investment opportunities or may need to sell other investments that it may not have otherwise sold.The Fund may also invest in securities that, at the time of investment, are illiquid, as determined by using the Securities and Exchange Commission’s (the “SEC”) standard applicable to registered investment companies (i.e., securities that cannot be disposed of by the Fund within seven calendar days in the ordinary course of business at approximately the amount at which the Fund has valued the securities). Illiquid and restricted securities may be difficult to dispose of at a fair price at the times when the Fund believes it is desirable to do so. The market price of illiquid and restricted securities generally is more volatile than that of more liquid securities, which may adversely affect the price that the Fund pays for or recovers upon the sale of such securities. Investment of the Fund’s assets in illiquid and restricted securities may also restrict the Fund’s ability to take advantage of market opportunities.

Valuation risk is the risk that one or more of the securities in which the Fund invests are priced differently than the value realized upon such security’s sale. In times of market instability, valuation may be more difficult, in which case the Adviser’s judgment may play a greater role in the valuation process.

Market Disruption and Geopolitical Risk

- The Fund is subject to the risk that geopolitical events will disrupt securities markets and adversely affect global economies and markets. War, terrorism, and related geopolitical events (and their aftermath) have led, and in the future may lead, to increased short-term market volatility and may have adverse long-term effects on U.S. and world economies and markets generally. Likewise, natural and environmental disasters, such as, for example, earthquakes, fires, floods, hurricanes, tsunamis and weather-related phenomena generally, as well as the spread of infectious illness or other public health issues, including widespread epidemics or pandemics such as the COVID-19 outbreak, and systemic market dislocations can be highly disruptive to economies and markets. Those events as well as other changes in non-U.S. and domestic economic and political conditions also could adversely affect individual issuers or related groups of issuers, securities markets, interest rates, credit ratings, inflation, investor sentiment, and other factors affecting the value of Fund Investments.| 14 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

The impact of the COVID-19 outbreak and any other epidemic or pandemic that may arise in the future could adversely affect the economies of many nations or the entire global economy, the financial performance of individual issuers, borrowers and sectors and the health of capital markets and other markets generally in potentially significant and unforeseen ways. This crisis or other public health crises may also exacerbate other pre-existing political, social and economic risks in certain countries or globally. The duration of the COVID-19 outbreak and its effects cannot be determined with certainty. The foregoing could lead to a significant economic downturn or recession, increased market volatility, a greater number of market closures, higher default rates and adverse effects on the values and liquidity of securities or other assets. Such impacts, which may vary across asset classes, may adversely affect the performance of the Fund’s investments, the Fund and a Shareholder’s investment in the Fund.

(h)

Restricted securities

Restricted securities are securities of privately-held companies that may be resold only upon registration under federal securities laws or in transactions exempt from such registration. In some cases, the issuer of restricted securities has agreed to register such securities for resale, at the issuer’s expense, either upon demand by the Fund or in connection with another registered offering of the securities. Many restricted securities may be resold in the secondary market in transactions exempt from registration. Such restricted securities may be determined to be liquid under criteria established by the Adviser. The restricted securities may be valued at the price provided by dealers in the secondary market or, if no market prices are available, the fair value as determined in good faith using methods approved by the Adviser. As of the date of this report, there is no expected date for such restrictions to be removed from any of the Fund’s restricted securities.

| 15 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

Additional information on each restricted investment held by the Fund on December 31, 2022 is as follows:

| Initial | ||||||||||||||

| Acquisition | ||||||||||||||

| Investments | Date | Cost | Fair Value | % of Net Assets | ||||||||||

| Automation Anywhere, Inc. | 12/30/2021 | 2,609,219 | 748,412 | 1.32 | % | |||||||||

| Axiom Space, Inc. | 12/22/2021 | 3,090,000 | 3,634,867 | 6.41 | % | |||||||||

| Bolt Financial, Inc., Series C Preferred Stock | 3/7/2022 | 2,000,020 | 1,136,375 | 2.00 | % | |||||||||

| Boom Technology, Inc. | 2/11/2022 | 2,000,000 | 2,000,000 | 3.52 | % | |||||||||

| Brex Inc. | 3/2/2022 | 4,130,298 | 2,358,820 | 4.16 | % | |||||||||

| CElegans Labs, Inc. | 11/23/2021 | 2,999,977 | 2,999,977 | 5.28 | % | |||||||||

| Chime Financial Inc. - Series A Preferred Stock | 12/30/2021 | 5,150,748 | 1,826,780 | 3.22 | % | |||||||||

| ClassDojo, Inc. | 11/19/2021 | 3,000,018 | 2,812,604 | 4.95 | % | |||||||||

| Discord, Inc. | 3/1/2022 | 724,942 | 395,530 | 0.70 | % | |||||||||

| Discord, Inc. - Series G Preferred Stock | 3/1/2022 | 889,055 | 485,070 | 0.85 | % | |||||||||

| Epic Games, Inc. | 1/3/2022 | 6,998,590 | 3,437,470 | 6.06 | % | |||||||||

| Flexport, Inc. | 3/29/2022 | 520,000 | 329,160 | 0.58 | % | |||||||||

| Impossible Foods - Series A Preferred Stock | 6/17/2022 | 1,272,986 | 538,720 | 0.95 | % | |||||||||

| Impossible Foods, Inc. - Series H Preferred Stock | 11/4/2021 | 2,098,940 | 857,616 | 1.51 | % | |||||||||

| Jeeves, Inc. - Series C Preferred Stock | 4/5/2022 | 749,997 | 749,997 | 1.32 | % | |||||||||

| Klarna Bank AB | 3/16/2022 | 4,657,660 | 793,866 | 1.40 | % | |||||||||

| Maplebear, Inc. | 10/8/2021 | 3,556,000 | 718,755 | 1.27 | % | |||||||||

| Maplebear, Inc. - Series B Preferred Stock | 11/16/2021 | 2,863,400 | 606,800 | 1.07 | % | |||||||||

| Plaid, Inc. | 2/15/2022 | 1,110,340 | 672,379 | 1.18 | % | |||||||||

| Public Holdings, Inc. | 7/22/2021 | 999,990 | 999,990 | 1.76 | % | |||||||||

| Relativity Space, LLC | 12/28/2021 | 1,659,996 | 1,329,912 | 2.34 | % | |||||||||

| Revolut Group Holdings Ltd | 12/8/2021 | 5,275,185 | 2,002,768 | 3.53 | % | |||||||||

| Space Exploration Technologies Corp., Class A | 6/27/2022 | 10,009,990 | 10,260,801 | 18.08 | % | |||||||||

| Space Exploration Technologies Corp., Class A and Class C | 6/8/2022 | 3,390,000 | 3,521,582 | 6.20 | % | |||||||||

| Space Exploration Technologies Corp., Class A | 6/9/2022 | 618,618 | 690,963 | 1.22 | % | |||||||||

| Stripe, Inc. | 1/10/2022 | 3,478,813 | 1,594,938 | 2.81 | % | |||||||||

| Superhuman Labs, Inc. | 6/25/2021 | 2,999,996 | 2,099,958 | 3.70 | % | |||||||||

| Total Investments | $ | 78,854,778 | $ | 49,604,108 | 87.39 | % | ||||||||

(3)

Fair Value Measurements

The Fund’s Fair Valuation Procedures incorporate the principles found in Rule 2a-5 of the 1940 Act in conjunction with Topic 820 (“ASC 820”) of the Financial Accounting Standards Board (“FASB”). Rule 2a-5 was created to address valuation practices with respect to the investments of a registered investment company and the oversight role performed by the Board in the valuation process. The Board has appointed the Adviser to serve as the Valuation Designee to perform fair value determinations.

ASC 820 was created to establish a framework for measuring fair value through the use of certain methods and inputs and shall be used by the Adviser in combination with the directives of Rule 2a-5 of the 1940 Act. ASC 820 defines fair value as the price of an asset that one would observe in an orderly purchase and sale transaction between market participants at a specific point in time. Data inputs used to perform a valuation are categorized as follows:

| 16 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

Readily Available (Level I) - Investments that trade frequently, for which pricing quotations in active markets are easily accessible.

Limited Availability (Level II) - Investments lacking easily recognizable market data, but where certain other observable data points exist such as market quotes for similar investments, and other observable market conditions such as interest rates, yield curves, default rates, etc.

Unavailable (Level III) - Investments where there is virtually no market data available, with no observable market data points or inputs. Fair value may be derived from professional judgments and assumptions in the form of an analysis that considers relevant factors and criteria determined in good faith, using a methodology such as liquidation basis, present value of cash flows, income approach, etc. or an independent third-party appraisal, should the committee feel the need to engage one.

Investments in publicly traded securities are generally carried at the closing price on the last trading day of the reporting period, while private investments are carried at fair value, estimated using applicable methodologies or are valued at their NAV as a practical expedient. In instances where a public or private real estate market transaction is not sufficiently similar to the investment being valued, alternative valuation methodologies shall be utilized. The determined fair value may be discounted even further on account of factors including but not limited to capital and risk structure, restrictions on resale, and ownership structure.

The Fund is registered under the 1940 Act. The Fund’s investments will be fair valued on a monthly basis and the Fund will calculate its NAV as of the close of each business quarter. Fluctuations in an investment’s fair value may be caused by volatility in economic conditions, among other factors. Such fluctuations in the fair value are classified as unrealized gains or losses in the Fund’s statement of operations. Upon the disposition of an investment, the corresponding gain or loss is classified as realized and will also be noted in the statement of operations.

Investments in private financial instruments or securities for which no readily available pricing is available may be valued by an independent reputable third-party service provider on a quarterly basis or as needed. This includes securities for which the use of NAV as a practical expedient is permitted under U.S. GAAP because their value is not based on unadjusted quoted prices. In conjunction with input from the independent third-party valuation agent, the

Adviser, as the

Valuation Designee,

shall value each Level III Investment on a monthly basis.The methods commonly used to develop indications of value for an asset are the Income, Market, and Cost Approaches. Each valuation technique is detailed in ASC 820.

The Income Approach uses valuation techniques to convert future amounts (for example, cash flows or earnings) to a single present amount (discounted). The measurement is based on the value indicated by current market expectations about those future amounts. Those valuation techniques include present value techniques; option-pricing models, such as the Black-Scholes-Merton formula (a closed-form model) and a binomial model (a lattice model), which incorporate present value techniques.

The Market Approach uses prices and other relevant information generated by market transactions involving identical or comparable assets or liabilities (including a business). For example, valuation techniques consistent with the market approach often use market multiples derived from a set of comparables. Multiples might lie in ranges with a different multiple for each comparable. The selection of where within the range the appropriate multiple falls requires judgment, considering factors specific to the measurement (qualitative and quantitative).

The Cost Approach is based on the amount that currently would be required to replace the service capacity of an asset (often referred to as current replacement cost). From the perspective of a market participant (seller), the price that would be received for the asset is determined based on the cost to a market participant (buyer) to acquire or construct a substitute asset of comparable utility, adjusted for obsolescence. Obsolescence encompasses physical deterioration, functional (technological) obsolescence, and economic (external) obsolescence and is broader than depreciation for financial reporting purposes (an allocation of historical cost) or tax purposes (based on specified service lives).

| 17 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

At various times, the Fund may utilize Special Purpose Vehicles (“SPV”)contributions made

and similar funds

in the investment process. The Fund advances money to these SPVs for the specific purpose of investing in securities of a single private issuer (an “SPV Investment”). When the Fund makes an SPV Investment, the investment is held through the Fund’s interest in the respective SPV. The Fund presents and fair values its SPV Investments in the financial statements as if they were owned directly by the Fund andhas

disregardedthe SPVs

for presentation purposes as a result of the following: (1) an SPV Investment is the sole activity of the SPV; (2) the Fund’s underlying ownership ofan

SPVinvestment

is proportionate to theFund’s

to

the SPV; and (3) the Fund will receiveits proportionate share of the

cash proceeds as the SPV Investment is monetized and distributed. The Schedule of Investments presents the direct investment of the SPVs with material positions in the Fund. The SPVs may incur a tax liability associated with distributions made by underlying portfolio investments. If an SPV charges management fees, those fees will adjust the cost of the SPV.Investments in SPVs consist of an investment by the Fund in an entity that invests directly in the common or preferred stock of a Portfolio Company. Investments in SPVs are generally valued using the same fair value techniques for the securities held by the Fund once the investment has been made by the SPV into the underlying portfolio company and are categorized as Level 3 of the fair value hierarchy. The investments in an SPV that have yet to purchase the underlying securities are held at cost and are categorized in Level 3 of the fair value hierarchy.

The Warrants issued were fair valued by a valuation consultant. As of December 31, 2022, the valuation consultant used a valuation methodology that used a probability distribution of the common stock price at the forecast time of the public listing combined with the probability-weighted average formula for the value of a call option to value the Warrants.

The following table summarizes the levels within the fair value hierarchy for the Fund’s assets and liabilities measured at fair value as of December 31, 2022:

Assets

| Investments | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Agreement for Future Delivery of Common Shares (a) | $ | $ | $ | 2,267,317 | $ | 2,267,317 | ||||||||||

| Common Stocks | — | — | 35,500,566 | $ | 35,500,566 | |||||||||||

| Convertible Notes | — | — | 5,634,867 | 5,634,867 | ||||||||||||

| Preferred Stocks | — | — | 6,201,358 | 6,201,358 | ||||||||||||

| Total | $ | — | $ | — | $ | 49,604,108 | $ | 49,604,108 | ||||||||

| Liabilities | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Warrants | — | — | (3,571,824 | ) | (3,571,824 | ) | ||||||||||

| Total | $ | — | $ | — | $ | (3,571,824 | ) | $ | (3,571,824 | ) | ||||||

| (a) | Certain investments are held through SPV s that holds forward contracts. Forward contracts involve the future delivery of shares of a portfolio company upon such securities becoming freely transferable or the removal of restrictions on transfer. The counterparties are shareholders of the portfolio company. See Schedule of Investments. |

| 18 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

The changes in fair value of investments and liabilities for which the Fund has used Level 3 inputs to determine the fair value are as follows:

Assets

Investments | Balance as of December 31, 2021 | Purchase of Investments | Proceeds from Sale of Investments (a) | Net Realized Gain (Loss) on Investments | Net Change in Unrealized Appreciation (Depreciation) on Investments | Balance as of December 31, 2022 | ||||||||||||||||||

Agreement for Future Delivery of Common Shares (b) | $ | — | $ | 4,589,153 | $ | — | $ | — | $ | (2,321,836 | ) | $ | 2,267,317 | |||||||||||

Common Stocks | 38,727,109 | 25,208,683 | (10,280,000 | ) | — | (18,155,226 | ) | $ | 35,500,566 | |||||||||||||||

Convertible Notes | 3,000,000 | 2,000,000 | — | — | 634,867 | 5,634,867 | ||||||||||||||||||

Preferred Stocks | 9,891,214 | 7,980,997 | (3,030,000 | ) | — | (8,640,853 | ) | 6,201,358 | ||||||||||||||||

Total | $ | 51,618,323 | $ | 39,778,833 | $ | (13,310,000 | ) | $ | — | $ | (28,483,048 | ) | $ | 49,604,108 | ||||||||||

| (a) | Sale proceeds from investments is comprised entirely of returned funds held within an SPV. |

| (b) | Certain investments are held through SPV s that holds forward contracts. Forward contracts involve the future delivery of shares of a portfolio company upon such securities becoming freely transferable or the removal of restrictions on transfer. The counterparties are shareholders of the portfolio company. See Schedule of Investments. |

Liabilities

Balance as of December 31, 2021 | Issuance of Liabilities | Conversion of SAFE Notes to Common Stock | Net Realized Gain (Loss) on Conversion of Liabilities | Net Change in Unrealized Appreciation (Depreciation) on Liabilities | Balance as of December 31, 2022 | |||||||||||||||||||

SAFE Notes | $ | (88,351,247 | ) | $ | (2,398,501 | ) | $ | 64,697,000 | $ | 25,375,657 | $ | 677,091 | $ | — | ||||||||||

Warrants | (4,906,756 | ) | (106,529 | ) | — | — | 1,441,461 | (3,571,824 | ) | |||||||||||||||

Total | $ | (93,258,003 | ) | $ | (2,505,030 | ) | $ | 64,697,000 | $ | 25,375,657 | $ | 2,118,552 | $ | (3,571,824 | ) | |||||||||

The following is a summary of quantitative information about significant unobservable valuation inputs for Level 3 Fair Value Measurements for investments held as of December 31, 2022:

Level 3 Investments | Fair Value as of December 31, 2022 | Valuation Technique | Unobservable Input | Ranges of Inputs/(Average) | ||||

Assets | ||||||||

Agreement for Future Delivery of Common Shares (a) | $2,267,317 | Market Approach | Adjusted Recent Transaction Price | $436.61 | ||||

| Market Approach | Indicative Broker Quote | $32.50 | ||||||

Common Stocks | $35,500,566 | Market Approach | Recent Transaction Price | N/A | ||||

| Market Approach | Discount Factor | 30%-65%/(52%) | ||||||

| Market Approach | Volume Weighted Average Price | $6.00-15.00/($10.63) | ||||||

| Market Approach | Indicative Broker Quotes | $20.00-$26.50/($22.44) | ||||||

Convertible Notes | $5,634,867 | Market Approach | Acquisition Price | N/A | ||||

| 19 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

Level 3 Investments | Fair Value as of December 31, 2022 | Valuation Technique | Unobservable Input | Ranges of Inputs/(Average) | ||||

| Market Approach | Recent Transaction Price | N/A | ||||||

Preferred Stocks | $6,201,358 | Cost Approach | Acquisition Price | N/A | ||||

| Market Approach | Recent Transaction Price | N/A | ||||||

| Market Approach | Indicative Broker Quote | $25.00 | ||||||

| Market Approach | Volume Weighted Average Price | $9.50-$34.95/($11.75) | ||||||

| Market Approach | Discount Factor | 65% | ||||||

Total | $49,604,108 |

Liabilities | ||||||||

Warrants | (3,571,824) | Probability- Weighted Average | Monte Carlo Simulation/Time to Public Listing Black-Scholes-Merton | 0.25 Years-0.75 Years/ (0.50 Years) | ||||

| Probability- Weighted Average | Model/Estimated Volatility | 32.5% | ||||||

Total | $(3,571,824) | |||||||

| (a) | Certain investments are held through an SPV that holds forward contracts. Forward contracts involve the future delivery of shares of a portfolio company upon such securities becoming freely transferable or the removal of restrictions on transfer. The counterparties are shareholders of the portfolio company. See Schedule of Investments. |

(4)

Capital Transactions

On January 25, 2021, the Organizer purchased 2,500,000 shares of the Fund’s common stock, par value $0.00001, for $25,000.

The securities offered and sold to investors in the Fund’s private offering were simple agreements for future equity in the Fund (the “SAFEs”). A SAFE is an investment instrument similar to a convertible promissory note. The SAFE document is not a debt instrument, but rather appears on the Fund’s capitalization table like other convertible securities such as options. Unlike a convertible note, the SAFE does not have a maturity date and contains provisions for conversion into shares of the Fund’s common stock or redemption upon the occurrences set forth therein. Additionally, a SAFE does not accrue interest.

The purchasers of SAFEs are referred to as “SAFE Investors.” As additional consideration of a SAFE Investor’s purchase of the SAFE, each SAFE Investor was granted a warrant to purchase the number of shares of the Fund’s common stock equal to the purchase amount of the SAFE divided by $10.00 per share (or such amount per share established pursuant to any amendment to the terms of the SAFE) multiplied by either 40% for Tranche 1 or 30% for Tranche 2 and Tranche 3, rounded down to the nearest whole share (the “Warrant Shares”) at a purchase price of $11.50 per Warrant Share, subject to such adjustments as set forth in the terms of the SAFE (the “Warrant”).

Immediately prior to the SAFE Conversion

(defined below)

,and in accordance with the terms of the SAFE agreement, the Fund performed a reverse stock split of shares of the common stock to ensure that a sufficient amount of shares of the common stock not owned by the Organizer would be outstanding after the SAFE Conversion.

On April 27, 2022, the Fund obtained approval from a majority of the SAFE holders to amend the SAFE Agreement to provide for a mandatory conversion of the SAFEs to shares of our common stock at a conversion price of $10.00 per share (the “SAFE Conversion”). On May 11, 2022, each SAFE holder received from the Fund a number of shares of common stock equal to the total amount invested by such investor in the private offering divided by $10.00. Following the SAFE Conversion and the reverse stock split, the Fund has 10,879,905 shares of common stock issued and outstanding.

| 20 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

Selling Stockholders who acquired shares of the common stock in connection with the SAFE Conversion (the “Lock-Up Shares”) are subject to limitations on their ability to offer, sell or otherwise dispose of the Lock-Up Shares during the “Lock-Up Period”. Immediately following the date the shares are listed for trading on the NYSE, 25% of the Lock-Up Shares will be freely transferable and not subject to the lock-up provisions as defined in the Fund’s Registration Statement. The Lock-Up Period for the remaining Lock-Up Shares is:

| · | with respect to the first 33.33% of the remaining Lock-Up Shares, 60 days after the date our shares are listed for trading on the NYSE, |

| · | with respect to an additional 33.33% of the remaining Lock-Up Shares, 120 days after the date our shares are listed for trading on the NYSE, and |

| · | with respect to the last 33.33% of the remaining Lock-Up Shares, 180 days after the date our shares are listed for trading on the NYSE. |

Warrants

The Warrants may only be exercised in full at any time until 5:00 P.M., Eastern Time, on January 1, 2026 (the “Expiration Date”) by the holders of the Warrants by surrendering the Warrant and providing an exercise notice with the information set forth in the Warrant Purchaser Agreement (the “Warrant Agreement”). As a result of the listing of common stock on the NYSE, the Fund may amend the Expiration Date at its sole discretion, provided that such amended Expiration Date will not be effective for at least ten (10) days after written notice is provided to the holder of the Warrants and that any such amendment will be identical among all outstanding Warrants.

If the exercise price of the Warrants is below the opening trading price when trading commences on the NYSE, the exercise price of the Warrants will be increased to an amount equal to the opening trading price when trading commences on the NYSE.

If at any time after the listing of common stock on the NYSE, the then-outstanding shares of common stock are subdivided (by stock split, reclassification or otherwise) or converted or exchange for a certain number of shares of any class or series of capital stock of the Fund (other than the common stock) or for other securities or property, then the exercise price will be adjusted pursuant to the terms of the Warrant Agreement.

A holder of the Warrants is not entitled to any voting rights or other rights as a stockholder of the Fund. In addition, the Warrants and the rights thereunder are not transferable without the written consent of the Fund.

If the Warrant Exercise Price is more than 115% of the SAFE Price at the time of any Public Listing, the Warrant Exercise Price will be reduced by such amount as is necessary to cause the Warrant Exercise Price to equal 115% of the SAFE Price. In addition, if the Warrant Exercise Price would be below the price of common stock offered in any Public Listing, the Warrant Exercise Price will be exercised to an amount equal to the price per share of common stock in the Public Listing.

The Fund evaluated the Warrants pursuant to ASC 480 to determine whether they represent an obligation requiring the Fund to classify the instruments as a liability. Management determined the Warrants do not meet the criteria to be classified as liabilities under ASC 480 and next evaluated them under ASC 815.

| 21 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

Management then determined the Warrants do not meet the definition of a derivative. It was thus determined to next evaluate them under the guidance in ASC 815-40-15-5 through 15-8 to determine whether they meet the criteria to be considered indexed to the Fund’s own stock. Management determined the Warrants do not meet the criteria to be considered indexed to the Fund’s own stock and are a liability classified pursuant to ASC 815-40-15-7D.

(5)

Related Party Transactions

(a) Management Fee

On April 29, 2022, the Fund and the Adviser entered into an investment advisory agreement (the “Advisory Agreement”), whereby the Adviser received management fees in the amount of 2.00 percent per annum (the “Management Fee”) on the first business day of each month prior to a public listing of the Fund’s shares of common stock. The Management Fee is calculated based on the value of the invested capital. Under the Advisory Agreement, upon the listing of the Fund’s shares of common stock on a national securities exchange, the Adviser will receive a Management Fee, payable quarterly, in an amount equal to 2.50% of average gross assets, at the end of the two most recently completed calendar quarters. For purposes of the Advisory Agreement, the term “gross assets” includes assets purchased with borrowed amounts.

Prior to the execution of the Advisory Agreement, the Fund and the Adviser operated under a separate investment advisory agreement whereby the Adviser received management fees in the amount of 2.00 percent per annum on a monthly basis. Management fees under the prior investment advisory agreement were calculated based on (x) the aggregate amount of the SAFEs purchased by SAFE investors multiplied by (y) the management fee divided by (z) twelve.

Additionally, from time to time, the Fund will invest in SPVs that charge management fees in connection with the Fund’s investment. For the year ended

December 31, 2022

, the Fund paid $0 in management fees in connection with its investments in SPVs.(b)

Administrator

U.S. Bancorp Fund Services, LLC, d/b/a US Bank Global Fund Services (the “Administrator”), serves as administrator to the Fund. Under the Fund Administration Servicing Agreement and the Fund Accounting Servicing Agreement by and among the Fund and the Administrator, the Administrator maintains the Fund’s general ledger and is responsible for calculating the net asset value of the Shares, and generally managing the administrative affairs of the Fund. Under the Fund Administration Servicing Agreement, the Administrator is paid an administrative fee, computed and payable monthly at an annual rate based on the aggregate monthly total assets of the Fund.

(c)

Service Providers

U.S. Bancorp Fund Services, LLC, d/b/a US Bank Global Fund Services (“USBGFS”) serves as the Fund’s dividend paying agent, transfer agent and registrar. Under a transfer agency services agreement, USBFS is paid an administrative fee, computed and payable monthly at an annual rate based on the transactions processed.

U.S. Bank National Association (“USB N.A.”) serves as the custodian to the Fund. Under a custody agreement, USB N.A. is paid a custody fee monthly based on the average daily market value of any securities and cash held in the portfolio.

| 22 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

Employees of PINE Advisors LLC (“PINE”) serve as officers of the Fund. PINE receives a monthly fee for the services provided to the Fund. The Fund also reimburses PINE for certain out-of-pocket expenses incurred on the Fund’s behalf.

(d)

Affiliated Partners

The Organizer has made payments of the Fund’s expenses and the Fund intends to reimburse the Organizer for these expenses. As of December 31, 2022, the reimbursable balance to the Organizer is $306,787 which consists of Offering costs payable, Organizational costs payable, and Operating Expenses Due to Organizer in the amounts of $216,510, $70,202 and $224,824, respectively as reported on the Statement of Assets and Liabilities.

As of December 31, 2022, Affiliates of the Fund owned 14.75% of shares of the Fund.

(6)

Commitments and Contingencies

In the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

The Fund may be required to provide financial support in the form of investment commitments to certain investees as part of the conditions for entering into such investments. As of December 31, 2022, the Fund did not have any unfunded commitments and did not provide any financial support.

The Fund is not currently subject to any material legal proceedings, and to the Fund’s knowledge, no material legal proceedings are threatened against the Fund. From time to time, the Fund may be a party to certain legal proceedings in the ordinary course of business, including proceedings related to the enforcement of the Fund’s rights under contracts with its portfolio companies. While the outcome of any legal proceedings cannot be predicted with certainty, to the extent the Fund becomes party to such proceedings, the Fund would assess whether any such proceedings will have a material adverse effect upon its financial condition or results of operations.

(7)

Investment Transactions

The cost of purchases and the proceeds from sales of investment securities (excluding in-kind subscriptions and redemptions, US government securities, and short-term investments), for the year ended December 31, 2022, amounted to $39,778,833 and $13,310,000 respectively.

(8)

Tax

Any net operating losses arising in tax years beginning after December 31, 2017 will have an indefinite carry forward period. The TCJA also established a limitation for any net operating losses generated in tax years beginning after December 31, 2017 to the lesser of the aggregate of available net operating losses or 80% of taxable income before any net operating losses utilization.

As of December 31, 2022, the Fund had a federal net operating loss carryforward of $3,497,720

which may be carried forward indefinitely. As of December 31, 2021, the Fund had a federal and state net operating loss carryforward of

$70,622

which may be carried forward indefinitely. The net operating loss carryforward is available to offset future taxable income

and subject to 80% of taxable income limitations.

.Future realization of the tax benefits of existing temporary differences and net operating loss carryforwards ultimately depends on the existence of sufficient taxable income within the carryforward period. As of December 31, 2022, the Fund performed an evaluation to determine whether a valuation allowance was needed. The Fund considered all available evidence, both positive and negative, which included the results of operations for the current and preceding years. The Fund determined that it was not possible to reasonably quantify future taxable income and determined that it is more likely than not that all the deferred tax assets will not be realized. Accordingly, the Fund maintained a full valuation allowance as of December 31, 2022.

Under Internal Revenue Code Section 382, if a corporation undergoes an “ownership change,” the corporation’s ability to use its pre-change NOL carryforwards and other pre-change tax attributes to offset its post-change income may be limited. The Fund has not completed a study to assess whether an “ownership change” has occurred or whether there have been multiple ownership changes since the Fund became a “loss corporation” as defined in Section 382. Future changes in the Fund’s stock ownership, which may be outside of the Fund’s control, may trigger an “ownership change.” In addition, future equity offerings or acquisitions that have equity as a component of the purchase price could result in an “ownership change.” If an “ownership change” has occurred or does occur in the future, utilization of the NOL carryforwards or other tax attributes may be limited, which could potentially result in increased future tax liability to the Fund.

The calculation of the Fund’s tax liabilities involves dealing with uncertainties in the application of complex tax laws and regulations for both federal taxes and the many states in which we operate or do business in. ASC 740 states that a tax benefit from an uncertain tax position may be recognized when it is more likely than not that the position will be sustained upon examination, including resolutions of any related appeals or litigation processes, on the basis of the technical merits.

The Fund recognizes accrued interest and penalties related to unrecognized tax benefits as income tax expense. There were no unrecognized tax benefits and no amounts accrued for interest and penalties as of December 31, 2022. The Fund is currently not aware of any issues under review that could result in significant payments, accruals or material deviation from its position. The Fund is subject to income tax examinations by major taxing authorities since inception.

No current or deferred provision for federal or state income taxes has been recorded for the period ended December 31, 2022. A reconciliation of the Fund's statutory income tax rate to the Fund's effective income tax rate as of December 31, 2022 is as follows:

Income at U.S. statutory rate | 21.00 | % | ||

State taxes, net of federal benefit | 6.52 | % | ||

Permanent differences | 192.61 | % | ||

Temporary differences | 0.91 | % | ||

Valuation allowance | -221.04 | % | ||

Income tax provision/(benefit) | 0.00 | % |

The net deferred income tax asset balance as of December 31, 2022 related to the following:

Net Operating Losses | $ | 962,485 | ||

Accrued Expenses & Other | 190,409 | |||

Management Fees | 129,213 | |||

Amortization | 16,849 | |||

Unrealized losses | 8,049,055 | |||

SPV Income/Losses | 26,103 | |||

Total deferred tax assets | $ | 9,374,114 | ||

Valuation allowance | 9,374,114 | |||

Net deferred tax assets (liability) | $ | 0 |

At December 31, 2022 the tax cost basis of investments was $86,109,570 and gross unrealized depreciation was $29,345,531

.

The Company may elect to file an election to be treated for federal income tax purposes as a Regulated Investment company (“RIC”) effective for the 2023 tax year. If the Fund is unable to qualify as a RIC, the Fund will continue to be taxed as a C Corporation for the 2023 taxable year. In order to qualify as a RIC, among other things, the Fund is required to distribute to its stockholders on a timely basis at least 90% of investment company taxable income and must meet certain asset diversification requirements on a quarterly basis. As a RIC, the Fund generally will not pay corporate-level U.S. federal income taxes on any net ordinary income or capital gains that the Fund distributes to its stockholders as dividends and claims dividends paid deductions to compute taxable income. A RIC will not be eligible to utilize net operating losses. However, net operating losses may be available to offset any built in gain on the Fund’s conversion from a C Corporation to a RIC and would continue to be available if the Fund fails to qualify as a RIC for the 2023 tax year.

(9)

Recent Accounting Standards

From time to time, new accounting pronouncements are issued by the FASB or other standards setting bodies that are adopted by the Fund as of the specified effective date. The Fund believes that the impact of recently issued standards and any that are not yet effective will not have a material impact on its financial statements upon adoption.

| 23 |

Destiny Tech100 Inc.

Notes to the Financial Statements (continued)

December 31, 2022

(10)

Subsequent Events