EXHIBIT 99.3

www.electrovaya.com

ELECTROVAYA INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

FOR THE YEAR ENDED SEPTEMBER 30, 2023

January 2, 2024

ELECTROVAYA INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

1. | OUR BUSINESS |

| 1 |

|

2. | OUR STRATEGY |

| 2 |

|

3. | RECENT DEVELOPMENTS |

| 3 |

|

4. | SELECTED ANNUAL FINANCIAL INFORMATION |

| 7 |

|

5. | LIQUIDITY AND CAPITAL RESOURCES |

| 16 |

|

6. | OUTSTANDING SHARE DATA |

| 18 |

|

7. | OFF-BALANCE SHEET ARRANGEMENTS |

| 20 |

|

8. | RELATED PARTY TRANSACTIONS |

| 20 |

|

9. | CRITICAL ACCOUNTING ESTIMATES |

| 20 |

|

10. | CHANGES IN ACCOUNTING POLICIES AND RECENT ACCOUNTING PRONOUNCEMENTS |

| 21 |

|

11. | FINANCIAL AND OTHER INSTRUMENTS |

| 21 |

|

12. | DISCLOSURE CONTROLS |

| 22 |

|

13. | INTERNAL CONTROL OVER FINANCIAL REPORTING |

| 22 |

|

14. | QUALITATIVE AND QUANTITATIVE DISCLOSURES ABOUT RISKS AND UNCERTAINTIES |

| 23 |

|

15. | OTHER RISKS |

| 28 |

|

● Introduction

Management’s discussion and analysis (“MD&A”) provides our viewpoint on our Company, performance and strategy. “We,” “us,” “our,” “Company” and “Electrovaya” include Electrovaya Inc. and its wholly-owned or controlled subsidiaries, as the context requires.

Our Board of Directors, on the recommendation of its Audit Committee, approved the content of this MD&A on January 2, 2024 and it is, therefore, dated as at that date. This MD&A includes the operating and financial results for the years ending September 30, 2023 and 2022, and should be read in conjunction with our consolidated financial statements. It includes comments that we believe are relevant to an assessment of and understanding of the Company’s consolidated results of operations and financial condition. The financial information herein is presented in thousands of US dollars unless otherwise noted (except per share amounts, which are presented in US dollars unless otherwise noted), in accordance with International Financial Reporting Standards (“IFRS”). Additional information about the Company, including Electrovaya’s current annual information form, can be found on the SEDAR website for Canadian regulatory filings at www.sedar.com.

● Forward-looking statements

This MD&A contains forward-looking statements including statements with respect factors impacting revenue, the competitive position of the Company’s products, global trends in technology supply chains, the Company’s current and prospective Original Equipment Manufacturer (OEM) relationships, the Company’s strategic objectives and financial plans, including the operations and strategic direction of Electrovaya Labs, expectations with respect to increasing predictability of customer sales cycles in the future, the Company’s products, including electric bus, high voltages and electric lift truck and robotic applications and the potential for revenue from new applications , market conditions being favourable for the use of the Company’s shelf prospectus; the ability to draw on the Company’s shelf prospectus and favourable market conditions therefor, cost implications, continually increasing the Company’s intellectual property portfolio, additional capital raising activities, the adequacy of financial resources to continue as a going concern, and also with respect to the Company’s markets, objectives, goals, strategies, intentions, beliefs, expectations and estimates generally. Forward-looking statements can generally be identified by the use of words such as “may”, “will”, “could”, “should”, “would”, “likely”, “possible”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “plan”, “objective” and “continue” (or the negatives thereof) and words and expressions of similar import. Readers and investors should note that any announced estimated and forecasted orders and volumes provided by customers and potential customers to Electrovaya also constitute forward-looking information and Electrovaya does not have (a) knowledge of the material factors or assumptions used by the customers or potential customers to develop the estimates or forecasts or as to their reliability and (b) the ability to monitor the performance of the business its customers and potential customers in order to confirm that the forecasts and estimates initially represented by them to Electrovaya remain valid. If such forecasts and estimates do not remain valid, or if firm irrevocable orders are not obtained, the potential estimated revenues of Electrovaya could be materially and adversely impacted.

| 2 | Page |

Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, the outcome of such statements involve and are dependent on risks and uncertainties, and undue reliance should not be placed on such statements. Certain material factors or assumptions are applied in making forward-looking statements, and actual results may differ materially from those expressed or implied in such statements. Material assumptions used to develop forward-looking information in this MD&A include, among other things, that current customers will continue to make and increase orders for the Company’s products; that the Company’s alternate supply chain will be adequate to replace material supply and manufacturing; that the Company’s products will remain competitive with currently-available alternatives in the market; that the alternative energy market will continue to grow and the impact of that market on the Company; the purchase orders actually placed by customers of Electrovaya; customers not terminating or renewing agreements; general business and economic conditions (including but not limited to currency rates and creditworthiness of customers); the relative effect of the global pandemics, geopolitics and supply chains on the Company’s business, its customers, and the economy generally; the Company’s liquidity and capital resources, including the availability of additional capital resources to fund its activities; the Company’s ability to raise sufficient non-dilutive capital to start up its US cell manufacturing operations; industry competition; changes in laws and regulations; legal and regulatory proceedings; the ability to adapt products and services to changes in markets; the ability to retain existing customers and attract new ones; the ability to attract and retain key executives and key employees; the granting of additional intellectual property protection; and the ability to execute strategic plans. Information about risks that could cause actual results to differ materially from expectations and about material factors or assumptions applied in making forward-looking statements may be found herein under the heading “Qualitative and Quantitative Disclosures About Risks and Uncertainties”, in the Company’s Annual Information Form (“AIF”) for the year ended September 30, 2023 under the heading “Risk Factors”, and in other public disclosure documents filed with Canadian securities regulatory authorities. The Company does not undertake any obligation to update publicly or to revise any of the forward-looking statements contained or incorporated by reference in this document, whether as a result of new information, future events or otherwise, except as required by law.

Revenue forecasts herein constitute future‐oriented financial information and financial outlooks (collectively, “FOFI”), and generally, are, without limitation, based on the assumptions and subject to the risks set out above under “Forward‐Looking Statements”. Although management believes such assumptions to be reasonable, a number of such assumptions are beyond the Company’s control and there can be no assurance that the assumptions made in preparing the FOFI will prove accurate. FOFI is provided for the purpose of providing information about management’s current expectations and plans relating to the Company’s future performance, and may not be appropriate for other purposes.

The FOFI does not purport to present the Company’s financial condition in accordance with IFRS, and it is expected that there may be differences between actual and forecasted results, and the differences may be material. The inclusion of the FOFI in this MD&A should not be regarded as an indication that the Company considers the FOFI to be a reliable prediction of future events, and the FOFI should not be relied upon as such.

| 3 | Page |

ELECTROVAYA INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

1. OUR BUSINESS

Electrovaya Inc. designs, develops and manufactures directly or through out-sourced manufacturing lithium ion batteries for Material Handling Electric Vehicles (“MHEV”), robotic applications and high voltage battery systems for use in electrified bus, truck, energy storage and defense applications. Our main businesses include:

| (a) | lithium ion battery systems to power MHEV including fork-lifts as well as accessories such as battery chargers to charge the batteries; |

|

|

|

| (b) | lithium ion batteries for robotic applications; and, |

|

|

|

| (c) | high voltage battery systems for electric bus, truck and defense applications |

|

|

|

| (d) | industrial products for energy storage. |

The Company has a battery and battery systems research and manufacturing facility in Mississauga, Ontario. In December 2019, Electrovaya moved its corporate head office to 6688 Kitimat Road in Mississauga, Ontario. The location, which comprises approximately 62,000 square feet, is designed to enhance the Company’s productivity and efficiency. The Company also owns a 52 acre site including a 137,000 square foot manufacturing site at 1 Precision Way in Jamestown New York. This site is intended to be Electrovaya’s US headquarters and a key manufacturing hub. For further information, see “Liquidity and Capital Resources”. The Company has operating personnel in both Canada and the USA..

Electrovaya has a team of mechanical, electrical, electronic, battery, electrochemical, materials and system engineers able to give clients a “complete solution” for their energy and power requirements. Electrovaya also has substantial intellectual property in the lithium ion battery sector.

Management believes that our battery and battery systems contain a unique combination of characteristics that enable us to offer battery solutions that are competitive with currently available advanced lithium ion and non-lithium ion battery technologies. These characteristics include:

● | Scalability and pouch cell geometry: We believe that large-format pouched prismatic (flat) cells represent the best long-term battery technology for use in large electro-motive and energy storage systems. |

|

|

● | Safety: We believe our battery technologies provide a high level of safety benefits for lithium ion batteries. Safety in lithium ion batteries is becoming an important performance factor and Original Equipment Manufacturers (“OEMs”) and users of lithium ion batteries prefer to have the highest level of safety possible in lithium ion batteries. |

| 4 | Page |

● | Cycle-life: Our cells are in the forefront of battery manufacturers with respect to cycle-life, with excellent rate capabilities. Cycle-life is generally controlled by the parasitic reactions inside the cell and these reactions have to be reduced in order to deliver industry leading cycle-life. Higher cycle-life is of importance in many intensive applications of lithium ion batteries. |

|

|

● | Energy and Power: Our batteries give industry leading combination of energy and power and can be application specific. |

|

|

● | Battery Management System: Our Battery Management System (“BMS”) has developed over the years, and provides excellent control and monitoring of the battery with advanced features as well as communication to many chargers, electric vehicles and other devices. |

2. OUR STRATEGY

We have developed a highly proprietary and specialized lithium ion technology that provides superior cycle life and safety. Given these advantages, the Company is focused on applications where those two performance differentiators provide the greatest benefits which has led to a focus on heavy duty and mission critical applications. These often require battery systems to provide around the clock operational capability, longer life and better safety and include material handling, robotics, transit, aerospace and other intensive electrified applications. We developed cells, modules, battery management systems, software and firmware necessary to deliver systems for these intensive applications. We also developed supply chains which can produce needed components including separators, electrolytes with appropriate additives, cells and cell assembly, modules, electronic boards, electrical and mechanical components as needed for our battery systems. Our goal is to utilize our battery and systems technology to develop and commercialize mass-production levels of battery systems for our targeted end markets.

To achieve these strategic objectives, we intend to:

● | Establish global strategic relationships in order to broaden the market potential of our products and services; |

|

|

● | Develop and commercialize leading-edge technology for heavy duty and mission critical electrified applications, as well as partnering with key large organizations to bring them to market; |

|

|

● | Invest in research and development initiatives related to new technologies that reduce the costs of our products, but enhance the operating performance, of our current and future products; and, |

|

|

● | Focus our products and sales efforts on intensive use and mission critical applications such as the logistics and e-commerce industry, automated guided vehicles, electric buses, defense, energy storage and other heavy duty applications. |

| 5 | Page |

3. RECENT DEVELOPMENTS

On October 3, 2022, the Company announced that it has selected New York State as the location for its first U.S. gigafactory (“the Gigafactory”), for the production of cells and batteries. The Company will set up operations at a 135,000 square foot plant on a 52-acre campus near Jamestown, NY. The Company is developing the Gigafactory due to rising demand for its lithium-ion batteries, which provide superior safety and longevity in demanding applications for e-forklifts, e-trucks, e-robots, e-buses and more. Empire State Development (ESD) is assisting the project by providing up to $4 million of tax credits through the performance-based Excelsior Jobs Program, and $2.5 million of funding through the Regional Council Capital Fund Program. The Gigafactory will be located in a former electronics manufacturing facility and is expected to create approximately 250 new jobs, with expected production of more than one GWh of battery and energy storage systems over the next five years. The Company will also be eligible for other New York State funds, as well as U.S. federal funding from various agencies and programs. In July, the New York Power Authority Board of Trustees approved an allocation of more than 1.5 megawatts of low-cost hydropower under the Power Authority’s Industrial Economic Development program to meet the increased electric load resulting from the Gigafactory. The final capital cost of the facility is estimated at approximately $75 million, and it is expected to open in phases starting late 2023.

On November 9, 2022, the Company completed a private placement with existing institutional investors, new institutional investors and insiders, (the “Offering”) of 17,543,402 units (“Units”) at a price of $0.8461 per Unit for aggregate gross proceeds of approximately C$14.8 million. Each Unit comprises one common share of the Company (a “Common Share”) and one-half of one common share purchase warrant (each whole warrant, a “Warrant”). Each Warrant entitles the holder thereof to acquire one Common Share at a price of C$1.06 until November 9, 2025, subject to adjustment in accordance with the terms and conditions of the Warrants. The Company covenanted with the purchasers of Units to undertake best efforts to list on NASDAQ by April 30, 2023, failing which the exercise price of the Warrants would be adjusted to C$0.94 per Common Share after that date, subject to adjustment in accordance with the terms and conditions of the Warrants. proceeds of the Offering were used for working capital to service purchase orders, for general corporate purposes, Jamestown startup costs, for debt repayment and restructuring.

On December 29, 2022, the Company announced that it had amended its loan agreement with its lender to extend the current term by six months with the option of a further six months under the same terms. The fees for the six month extension are 0.5% of the facility and were paid in shares. The Company also announced that it had repaid and closed its C$6 million promissory note with the same lender.

On February 9, 2023, the Company announced the receipt of a battery purchase order through its OEM sales channel valued at approximately $3.4 million. The batteries will be used by a leading Fortune 100 retailer to power Material Handling Electric Vehicles in the United States. Delivery will be made during the 2023 fiscal year.

| 6 | Page |

On March 6, 2023, the Company announced the receipt of a battery purchase order through its OEM sales channel valued at approximately $14 million. The batteries will be used by a leading Fortune 500 company in the United States.

On March 27, 2023, the Company announced that all of the resolutions that shareholders were asked to consider at its 2023 Annual and Special Meeting held on March 24, 2023 in Toronto, Ontario, were approved. The five directors named in the management information circular of the Company, being Dr. Sankar Das Gupta, Dr. Raj Das Gupta, Dr. James Jacobs, Dr. Carolyn Hansson and Mr. Kartick Kumar, were each elected as directors by over 98% of the votes cast. Goodman & Associates LLP were re-appointed as auditors of the Company. A special resolution to approve the consolidation of the Common Shares at the board’s discretion at a ratio of up to 5:1 was passed with 98.92% in favour.

On April 3, 2023, the Company announced that it had closed the previously announced purchase of its planned manufacturing site in Jamestown, New York as of March 31 2023. The site includes 52 acres of land, including a building previously utilized for the manufacturing of electronic components.

The purchase price was paid by way of a $1.05 million promissory note payable to the members of Sustainable Energy Jamestown LLC with a term of 365 days bearing interest at 7.5% per annum payable at maturity and the assumption of a $4.4 million vendor promissory note (“VPN”) issued on July 1, 2022 with a 2 year term bearing interest at 2% per annum and secured against the property. At the time of the transaction, the balance of the VPN was $3.95 million with a payment due on maturity of $2.4 million. As part of the security interests granted to the Company’s existing lender for its consent to the transaction, Dr. Sankar Das Gupta pledged 7,000,000 Common Shares of the Company.

On April 30, 2023, the Company entered into an agreement with the purchasers of the private placement of units consisting of common shares and warrants with an automatic price adjustment mechanism tied to listing the Common Shares on a major US exchange (“Warrants”) completed in November 2022, to extend the deadline for the automatic adjustment from April 30, 2023 to June 9, 2023 in exchange for certain limits on the issuance of new Common Shares by the Company, subject to certain customary exceptions. All other terms and conditions remained unchanged.

On June 13, 2023, the Company completed a reverse split of its issued and outstanding common stock at a ratio of 1 consolidated for 5 pre-consolidated shares. The Company initiated the reverse stock split in connection with its intention to meet the minimum bid price requirement and list the Common Shares for trading on the Nasdaq Capital Market. As a result of the reverse stock split, every five outstanding Common Shares were consolidated into one Common Share without any action from stockholders, reducing the number of outstanding Common Shares from approximately 164.86 million to approximately 32.97 million.

On June 30, 2023, the Company renewed its revolving facility and extended the term of the facility by three months to September 29, 2023, with the aim to refinance the facility by the end of Q4 FY2023. The Company retains the option to extend the existing facility by a further three months to December 31, 2023.

On September 29 2023, the Company engaged MNP LLP to replace Goodmans and Associates as the Company’s auditors.

| 7 | Page |

3.1 Business Highlights, Subsequent Events and 2024 Outlook

Business Highlights – Q4 FY2023:

On July 3, 2023, the Company announced that the Nasdaq Stock Market LLC approved the listing of the Common Shares on the Nasdaq Capital Market (“Nasdaq”). The Company commenced trading on Nasdaq under the symbol “ELVA” at the opening of trading on Thursday, July 6, 2023 and will continue to trade on the Toronto Stock Exchange under the symbol “TSX:ELVA”.

Between July 19 and July 31, 2023, a portion of the warrants issued during the November 9, 2022, private placement was exercised, resulting in cash received of approximately $3 million. This investment was used for general working capital and will be reflected in the Q4 FY2023 financial statements.

On July 20, 2023, the Company announced the launch of its Infinity-HV battery systems. The Infinity-HV systems target heavy-duty, high-voltage applications including buses, delivery trucks, construction trucks, hybrid-fuel cell/battery systems and stationary energy storage systems. Electrovaya’s Infinity-HV systems will offer industry-leading safety and longevity for these applications, ultimately providing users with lower liability costs, better warranty coverage and an overall lower cost of ownership.

On August 2, 2023, the Company provided the following business update on the planned New York gigafactory. The first phase of construction is expected to take place within the existing 135,000 square foot manufacturing facility for the production of cells and batteries, with an estimated capital expenditure of approximately US$48 million. The planned Gigafactory, we believe, provides significant benefits for Electrovaya:

| ● | Domestic manufacturing and supply chain security; |

|

|

|

| ● | Inflation Reduction Act incentives of up to US$45 million for every 1GWh of plant output; |

|

|

|

| ● | Improved gross margins; and |

|

|

|

| ● | Enhanced ability to make more rapid implementation of new battery technologies. |

On September 29, 2023, the Company engaged MNP LLP to carry out the audit for the 2023 fiscal year. The audit for the Fiscal Year 2023 was carried out in line with PCAOB auditing standards as opposed to Canadian Accounting Standards for Fiscal Year 2022.

| 8 | Page |

Subsequent Events

On October 3, 2023, announced preliminary unaudited Q4 and Fiscal Year 2023 revenue. (“Q4 FY2023” and “FY2023”, respectively)

| ● | Preliminary unaudited Q4 FY 2023 revenue of US$13.4 million (C$18.1 million) for the quarter ending September 30, 2023, an increase of 35% compared with Q4 FY 2022 |

|

|

|

| ● | Preliminary unaudited FY 2023 revenue of US$42.2 million (C$56.9 million), an increase of 113% compared with $19.8 million (C$26.7 million) in FY 2022; and an increase of 264% compared to $11.6 million (C$15.6 million) in FY 2021; a CAGR of 100% over 2 years. |

In October 2023, the Company established a relationship with one of the four largest Japanese trading houses or “sogo shosha”. Through this partnership, Electrovaya products are being marketed to a host of Japanese and international OEMs representing a significant boost to the Company’s sales reach.

On October 21, 2023, the Company announced the appointment of Steven Berkenfeld to the Company’s board of directors.

On November 2, 2023, the Company announced that it had executed a strategic supply agreement with two leading affiliated OEM partners for material handling vehicles and other affiliates for the supply of battery systems. The new agreement supersedes a preceding agreement from December 2020 with just one of the OEM partners and includes a longer term with larger minimum purchases to maintain exclusivity.

On November 7, 2023, the Company announced the receipt of a battery purchase order through one of its OEM sales channels valued at over US$8 million. The batteries will be used by a leading Fortune 100 company in the United States for material handling electric vehicles.

On December 20, 2023 the Company renewed its revolving facility and extended the term of the facility by three months to March 29, 2024, with the aim to refinance the facility by the end of Q2 FY2024. The Company retains the option to extend the existing facility by a further three months to June 29, 2024.

Positive Financial Outlook:

In Q1 FY2023, the Company announced its revenue guidance for FY2023 of $42 million. The Company continued to reiterate its guidance and confirmed in October, 2023 that it had met its guidance. Upon release of the financial statements, this figure was adjusted to $44.4 million for FY2023.

The Company anticipates revenue of between $65-75 million for the fiscal year ending September 30, 2024 (“FY 2024”), an increase of between 47-70% over the revenue generated in FY2023 of $44 million. The revenue forecast takes into consideration the Company’s existing purchase order backlog, anticipated pipeline, additional demand from its key OEM partners and new products designed for new sectors. This guidance is subject to change and is made barring any unforeseen circumstances. See “Forward-Looking Statements”.

| 9 | Page |

4. SELECTED ANNUAL FINANCIAL INFORMATION

4.1 Selected Annual Financial Information for the Years ended September 30, 2023, 2022 and 2021

Results of Operations

(Expressed in thousands of U.S. dollars)

Operating Segments

The Company has reviewed its operations and determined that it operates in one business segment and has only one reporting unit. The Company develops, manufactures and markets power technology products.

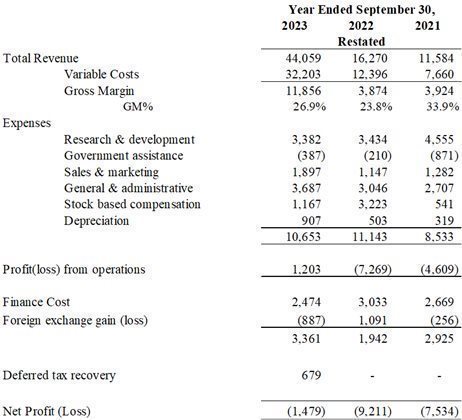

Revenue

Revenue increased to $44.1 million, compared to $16.3 million for the years ended September 30, 2023 and restated 2022 respectively, an increase of $27.8 million or 171%. The 171% increase in year-over-year revenue was due to increased order volume and ramp up in production to meet the demand.

| 10 | Page |

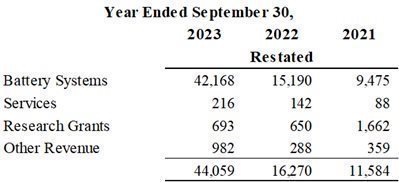

Revenue was predominantly from the sale of batteries and battery systems for MHEVs. Batteries and battery systems accounted for $42.2 million or 95.7% of revenue for FY 2023 and $15.2 million or 93.4% for FY2022. Sale of engineering services, research grants, and other sources of revenue, including Government assistance, accounted for the remaining $1.9 million or 4.3% in FY 2023 and $1.1 million or 6.8% in FY 2022.

For the year ended September 30, 2023 revenue attributable to the United States accounted for $42.4 million or 96.1% of total revenue while revenue attributed to Canada and other countries accounted for the remaining $1.7 million or 3.9%. For the year ended September 30, 2022 revenue attributable to the United States accounted for $14.3 million or 87.7% and Canada and other countries accounted for the remaining $2.0 million or 12.3%. This reflects the growing level of interest in our material handling batteries and an increased direct and indirect sales presence in the United States.

Direct Manufacturing Costs (variable costs) and Gross Margin

Direct manufacturing costs are comprised of materials, labour and manufacturing overhead, excluding amortization, associated with the production of batteries and battery packs for Electric Vehicles, stationary grid applications and research and engineering service revenues.

| 11 | Page |

The gross margin increased to $11.9 million, compared to $3.9 million for the year ended September 30, 2023 and restated 2022 respectively, an increase of $8.0 million or 206%. The gross margin percentage was 26.9% for the year ended September 30, 2023, compared to 23.8% for the prior year. When reviewing gross margin by revenue stream, the main driver of revenue, Battery Systems, shows a gross margin of 27.7% for the year.

Our margin varies from period to period due to a number of factors including the product mix, special customer pricing, material cost, shipping costs and foreign exchange movement. In the current fiscal year, we have seen some significant increases in prices due to inflationary pressures. The company has offset this by increasing sales prices and continues to work to improve gross margins going forward. The Company continues to monitor gross margin closely and has implemented measures to increase it for fiscal year 2024.

Operating Expenses

Operating expenses include:

| ● | Research and Development (“R&D”) Research and development expenses consist primarily of compensation and premises costs for research and development personnel and activities, including independent contractors and consultants, and direct materials; |

|

|

|

| ● | Government Assistance The company applied for and received funding from the Industrial Research Assistance Program during the year; |

|

|

|

| ● | Sales and Marketing Sales and marketing expenses are comprised of the salaries and benefits of sales and marketing personnel, marketing activities, advertising and other costs associated with the sales of Electrovaya’s product lines; |

|

|

|

| ● | General and Administrative General and administrative expenses include salaries and benefits for corporate personnel, insurance, professional fees, reserves for bad debts and facilities expenses. The Company’s corporate administrative staff includes its executive officers and employees engaged in business development, financial planning and control, legal affairs, human resources and information technology; |

|

|

|

| ● | Stock based compensation Recognizes the value based on Black-Scholes option pricing model of stock based compensation expensed over the relevant vesting period; stock based compensation that carries market conditions is fair valued using the Monte Carlo method and expensed over the calculated vesting period. |

|

|

|

| ● | Financing costs Financing costs includes the cost of debt, equity or other financing. This includes cash and non-cash interest, legal costs of financing, commissions and fees; and, |

|

|

|

| ● | Patent and trademark costs Patent and trademark expense recognizes the cost of maintaining the Company’s patent and trademark portfolio. |

| 12 | Page |

Total operating expenses decreased to $10.7 million compared to $11.1 million for the years ended September 30, 2023 and restated 2022 respectively, a decrease of $0.4 million or 4%. Within this movement, Sales & Marketing expenses increased by $0.7 million, being the costs associated with expanding into new sales verticals, and General & Administrative costs increased $0.6 million, being primarily the increase in headcount and Jamestown plant startup costs. Stock based compensation increased significantly in both 2023 and 2022 due to the recognition of options granted with special market conditions. Although these market conditions have yet to be met, the options are recognised based on the valuation under the Monte Carlo option pricing model. As a result of this calculation, an additional $0.7 million was recognised in 2023 and $3.4 million in 2022.

Net Profit/(Loss)

The net loss decreased to $1.5 million million from a net loss of $9.2 million for the years ended September 30, 2023 and restated 2022 respectively, a decrease of $7.7 million. This decrease in the net loss was due in a large part to the increase in revenue during the year of 171%, decrease in operating expenses of 4% and the recognition of a deferred tax recovery relating to the US operations. The Company also experienced unfavourable movements in exchange rates and recognised a foreign exchange loss of $0.9 million, compared to the gain of $1.1 million in the prior year.

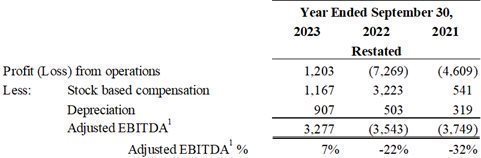

Key Performance Indicators

In addition to operating results and financial information described above, management reviews the following measures (which are not measures defined under IFRS):

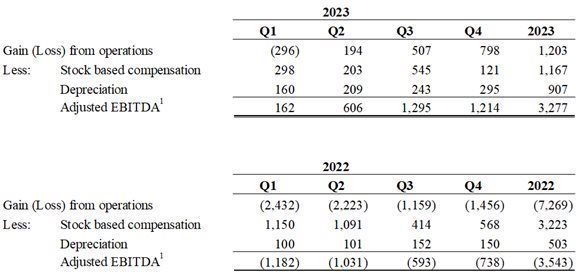

Adjusted EBITDA1

(Expressed in thousands of U.S. dollars)

1 Non-IFRS Measure: Adjusted EBITDA is defined as profit(loss) from operations, plus stock-based compensation costs and depreciation. Adjusted EBITDA does not have a standardized meaning under IFRS. We believe that certain investors and analysts use Adjusted EBITDA to measure the performance of the business and is an accepted measure of financial performance in our industry. It is not a measure of financial performance under IFRS, and may not be defined and calculated in the same manner by other companies and should not be considered in isolation or as an alternative to Income (loss) from operations.

Adjusted EBITDA1 increased by $6.8 million from the restated 2022 figure, and $7.0 million from the 2021 figure. The main driver of the improvement is the 171% increase in revenue and the 4% decrease in operating expenses during the year. Adjusted EBITDA for Q4 was $1.2 million and Management is focused on maintaining this trend in 2024.

| 13 | Page |

Adjusted EBITDA1 will improve primarily through increased sales, maintaining or improving gross margin percentage and controlling operating expenses. We continue our efforts for sales growth, control of manufacturing costs and reduction operating expenses.

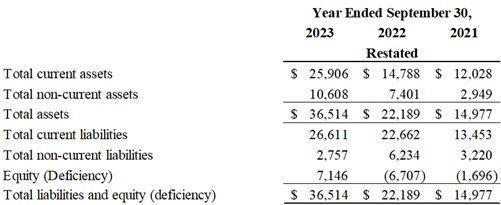

Summary Financial Position

(Expressed in thousands of U.S. dollars)

In the three year period commencing September 30, 2021 and ending September 30, 2023 current assets have increased by $13.8 million, current liabilities have increased by $13.1 million and the equity deficiency has decreased by $8.8 million.

Management is focused on continuing to improve the company’s financial position through the prudent use of debt and equity but most importantly achieving a profitable position and strong working capital management.

| 14 | Page |

Summary Cash Flow

(Expressed in thousands of U.S. dollars)

The Company ended September 30, 2023 with $1 million of cash as compared to $0.6 million and $4.2 million for September 30, 2022 and 2021, respectively. The Company showed a positive cash generated from operations of $2.9m compared to a cash used in operations of $2.5 million and $5.5 million for September 2022 and 2021 respectively. This is a significant milestone for the Company as we move towards positive cash flow from operations. The Company had a negative change in working capital of $7.7 million compared to $6.4 million for September 2022 and $2.6 million for September 2021.

Further details of the restatements made to FY2022 can be found in note 27 of the financial statements.

| 15 | Page |

4.2 Quarterly Financial Results

Results of Operations

(Expressed in thousands of U.S. dollars)

| 16 | Page |

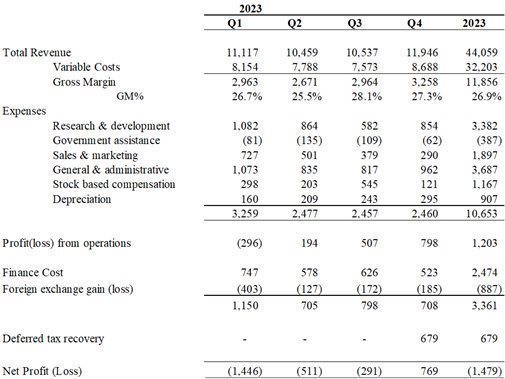

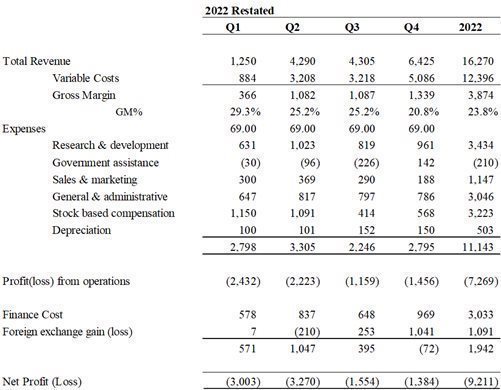

For the three month period ended September 30, 2023, total revenue was $11.9 million. This quarterly revenue was $5.5 million higher than restated Q4 FY2022. The increase is a direct result of increased orders and deliveries.

Gross margin increased by $1.9 million to $3.3 million for Q4 2023 from $1.3 million for Q4 2022. The gross margin percentage increased to 27.3% in Q4 2023 as compared to restated 20.8% in Q4 2022. As described earlier, gross margin is affected by a number of factors including the product mix, special customer pricing, material cost, shipping costs and foreign exchange movement. During Q4 2023, the company saw a significant increase in its shipping and storage costs due to the multi-week port strike in Vancouver. This had a direct impact on the gross margin. The Company is targeting returning to an improved gross margin for fiscal year 2024.

Total operating expenses for Q4 2023 decreased to $2.5 million as compared to $2.8 million for Q4 2022, a decrease of $0.3 million. Both fiscal years were affected by additional costs as a result of changes to the accounting treatment of certain items on the income statement. Stock Based Compensation decreased by $0.4. General & Administrative and Sales & Marketing costs increased by $0.2 million and $0.1 million respectively.

Quarterly Adjusted EBITDA1

Quarterly Adjusted EBITDA shows a significant increase from fiscal 2022 to fiscal 2023.

| 17 | Page |

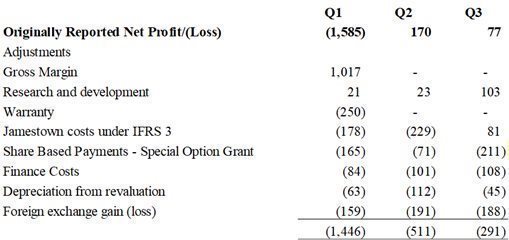

Comparison to Previously Reported

Changes were made to the accounting treatment for 2023 when compared to the treatment during the year.

The total impact of the adjustments to the first three quarters of the year is an increase in the loss of $0.3 million. The majority of the adjustments came in the first quarter of 2023, The effect of which was offset by an increase to the gross margin of $1.0 million from prior year revenue being reallocated to Q1 2023. The negative adjustments came from an addition to the warranty provision of $0.2 million, the inclusion of $0.3 million of costs and $0.2 million of depreciation associated with the Jamestown facility, prior to the Company’s purchase of Sustainable Energy Jamestown, as a result of a change in treatment of the asset under IFRS 3 common control business combinations, $0.3 million from fair value adjustments to finance costs and $0.4 million related to options with market conditions that have not vested and may never vest (the overall impact for this adjustment was $0.7 million in fiscal 2023 and $3.4 million in fiscal 2022). Of the total increase to costs to the first three quarters, $1.4 million related to non-cash adjustments.

Quarterly Comparative Summaries

Quarterly revenue from continued operations are as follows:

(USD $ thousands) | Q1 | Q2 | Q3 | Q4 |

2023 | $11,117 | $10,459 | $10,537 | $11,946 |

2022 | $1,250 | $4,290 | $4,305 | $6,425 |

2021 | $2,583 | $2,927 | $1,918 | $4,156 |

| 18 | Page |

Quarterly net profits/(losses) from continued operations are as follows:

(USD $ thousands) | Q1 | Q2 | Q3 | Q4 |

2023 | $(1,446) | $(511) | $(291) | $769 |

2022 | $(3,003) | $(3,270) | $(1,554) | $(1,384) |

2021 | $(1,844) | $(1,866) | $(1,792) | $(2,032) |

Quarterly net gains (losses) per common share from continued operations are as follows:

| Q1 | Q2 | Q3 | Q4 |

2023 | $(0.04) | $(0.01) | $(0.00) | $0.02 |

2022 | $(0.10) | $(0.11) | $(0.05) | $(0.05) |

2021 | $(0.01) | $(0.02) | $(0.01) | $(0.01) |

Revenue Seasonality

In recent periods, revenue has been relatively low in the fiscal first quarter, which management believes reflects material handling customers’ preference to defer product delivery past the holiday season and into the New Year. This is due to an increasing e-commerce demand and the need to minimize changes or disruptions at high-volume distribution centers during their peak season.

The lithium ion forklift battery has a long sales cycle as many customers are large companies, the technology is relatively new to the forklift market, and customers need time to familiarize themselves with and validate the benefits as compared to the incumbent technology of lead acid batteries. In some cases, the process involves receiving a demonstrator battery for testing and trial. This causes a somewhat long and “lumpy”, or uneven, sales cycle. As customers become more comfortable with the product and place repeat orders it is management’s view that the sales will grow in a more predictable and consistent fashion.

5. LIQUIDITY AND CAPITAL RESOURCES

During the year ended September 30, 2023, the Company generated negative cash from operations of $5.3 million (September 30, 2022: $8.8 million). As of September 30, 2023, the Company had negative working capital of $7.7 million (September 30, 2022: $6.4 million) and a net loss of $1.4 million (2022: $9.2 million). The Company’s equity was a surplus of $7.1 million (September 30, 2022: deficiency of $6.7 million). As of September 30, 2023, the Company had cash and cash equivalents of $1.0 million (September 30, 2022: $0.6 million). The Company is also anticipating the planned construction of its gigafactory in Jamestown, New York (the “Gigafactory”), which will need additional financing.

| 19 | Page |

The first phase of construction is expected to take place within the existing 137,000 square foot manufacturing facility for the production of cells and batteries, with an estimated capital expenditure of approximately US$38 million. These material uncertainties raise significant doubt upon the Company’s ability to continue as a going concern.

In assessing whether the going concern assumption was appropriate, management took into account all relevant information available about the future, which was at least, but not limited to, the twelve month period following September 30, 2023. The Company and its Board of Directors have implemented various operating and financing strategies.

Subsequent to year-end, the Company renewed its revolving credit facility and extended it to June 30, 2024 with capability to refinance earlier. Despite this, it expects to refinance this facility with a different lender in Q2 fiscal year 2024, providing additional working capital to support the increase in revenue expected for fiscal year 2024.

The Company plans on pursuing large scale investments in its planned Jamestown gigafactory only in the event that it closes a government backed debt facility that includes advantageous terms with minimal impacts to operating cash flow and equity dilution. If the Company is unable to secure such financing, it will delay or cancel these expansion plans with limited financial impact as the main investment made thus far is the land and building which can be sold at a profit.

The Company has made improvements to its manufacturing process, equipment, and facilities over the last several months that have led to increased capacity and efficiency. The Company has witnessed a significantly increased order backlog year over year with an expanding product platform that now encompasses additional revenue streams. Furthermore, the Company also anticipates gross margins to improve in fiscal year 2024 due to decreasing costs of key materials including but not limited to cell materials, separators, and other high value items. These anticipated improved margins, when combined with expected overall sales growth should result in improved overall financial performance.

Finally, the Company has multiple methods at its disposal for attracting additional working capital including debt and issuing new shares. Since the Company listed on Nasdaq in July 2023, it has further increased liquidity and overall financing capabilities.

Given the Company’s improved revenue levels, accounts receivable level, anticipated additional working capital from a planned new financial lender, strong relationship with our OEM partners and end users, a strong backlog and sales pipeline, and availability to draw on $100 million shelf prospectus, we are confident in our ability to continue operations for at least twelve months.

| 20 | Page |

At September 30, 2023, we had the following contractual obligations:

Year of Payment Obligation |

| Debt Repayment |

| |

|

|

|

| |

2024 |

|

| 15,334 |

|

2025 |

|

| 56 |

|

2026 |

|

| 57 |

|

2027 and thereafter |

|

| 84 |

|

Total |

| $ | 15,531 |

|

6. OUTSTANDING SHARE DATA

The authorized and issued capital stock of the Company consists of an unlimited authorized number of common shares as follows:

| 21 | Page |

On February 17, 2021 at a Special Meeting of the Shareholders, a resolution was passed to amend the articles of the Corporation to change the number of issued and outstanding common shares of the Corporation by consolidating the issued and outstanding common shares on the basis of one new common share for every 5 existing common shares (or such lower consolidation ratio as may be determined by the Board). Such consolidation would ultimately only become effective at a future date determined by the Board if the Board determined it was in the best interests of the Corporation to implement a consolidation.

On March 25, 2022 at a Special Meeting of the Shareholders, a resolution was passed to (i) authorize amendments to the company’s Stock Option Plan to increase the maximum number of common shares issuable upon the exercise of stock options thereunder from 4,600,000 to 6,000,000.

On March 24, 2023 at a Special Meeting of Shareholders, the resolution to amend the articles of the Corporation to change the number of issued and outstanding common shares of the Corporation by consolidating the issued and outstanding common shares on the basis of one new common share for every 5 existing common shares (or such lower consolidation ratio as may be determined by the Board) was re-presented and passed.

On June 13, 2023, the Company completed a reverse split of its issued and outstanding common stock at a ratio of 1 consolidated for 5 pre-consolidated shares. The Company initiated the reverse stock split in connection with its intention to meet the minimum bid price requirement and list the Common Shares for trading on the Nasdaq Capital Market. As a result of the reverse stock split, every five outstanding Common Shares were consolidated into one Common Share without any action from stockholders, reducing the number of outstanding Common Shares from approximately 164.86 million to approximately 32.97 million. The following table reflects the quarterly stock option activities for the period from October 1, 2021 to September 30, 2023:

The following table reflects the outstanding warrant and Broker Compensation Option activities for the period from October 1, 2021 to September 30, 2023:

| 22 | Page |

Details of share warrants

Details of Compensation Options to Brokers

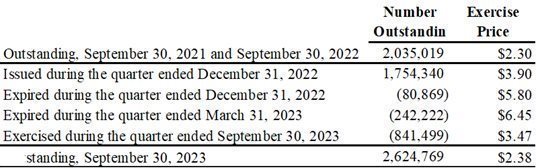

As of September 30, 2023, the Company had 33,832,784 common shares outstanding, 4,714,388 options to purchase common shares outstanding, 17,522 compensation options outstanding and 2,624,769 warrants to purchase common shares outstanding.

7. OFF-BALANCE SHEET ARRANGEMENTS

The Company does not have any off-balance sheet arrangements for the year ended September 30, 2022.

8. RELATED PARTY TRANSACTIONS

Please refer to note 17 to the 2023 Annual Financial Statements for details on related party transactions

| 23 | Page |

9. CRITICAL ACCOUNTING ESTIMATES

The Company’s management makes judgments in the process of applying the Company’s accounting policies in the preparation of its consolidated financial statements. In addition, the preparation of financial information requires that the Company’s management make assumptions and estimates of effects of uncertain future events on the carrying amounts of the Company’s assets and liabilities at the end of the reporting period and the reported amounts of revenue and expenses during the reporting period. Actual results may differ from those estimates as the estimation process is inherently uncertain. Estimates are reviewed on an ongoing basis based on historical experience and other factors that are considered to be relevant under the circumstances. Revisions to estimates and the resulting effects on the carrying amounts of the Company’s assets and liabilities are accounted for prospectively.

The critical judgments, estimates and assumptions applied in the preparation of Company’s financial information are reflected in Note 3 of the Company’s September 30, 2023 consolidated financial statements.

10. CHANGES IN ACCOUNTING POLICIES AND RECENT ACCOUNTING PRONOUNCEMENTS

Our accounting policies and information on the adoption and impact of new and revised accounting standards the Company was required to adopt effective January 1, 2015 are disclosed in Note 3 of our consolidated financial statements and their related notes for the year ended September 30, 2023.

11. FINANCIAL AND OTHER INSTRUMENTS

Derivative Liabilities

Warrants as a derivative liability are fair valued using the Black Scholes Model (BSM). Using this approach, the fair value of the warrants on 09 November 2022 was determined to be $3.3 million. Key valuation inputs and assumptions used in the BSM are stock price of CAD $4.55, expected life of 3 years, annualized volatility of 85.58%, annual risk-free rate of 3.87%, and annual dividend yield of 0.0%. Key valuation inputs and assumptions used in the BSM when valuing the warrants as at September 30, 2023 were, stock price $3.75, expected life of 2.1 years, annualized volatility of 76.8%, annual risk-free rate of 3.92%, and dividend yield of 0.0%.

Under the provisions of IFRS 9, the initial value of the warrant is reduced from equity and booked as derivative liability net off of the allocated issuance cost.

The company incurred total issuance costs of $459. The Company allocated proportionally to the derivative liability and expensed $134 as a finance cost in the statement of earnings, and the balance portion of the issuance cost reduced from equity for the amount of $325 respectively.

Warrants are fair valued at each reporting date and the gain / (loss) is charged to the other comprehensive income.

| 24 | Page |

12. DISCLOSURE CONTROLS

We have established disclosure controls and procedures that are designed to ensure that the information required to be disclosed by the Company in the reports that it files or submits under securities legislation is recorded, processed, summarized, and reported within the time periods specified in such rules and forms and that such information is accumulated and communicated to management, including our principal executive officer and principal financial officer (who are our Chief Executive Officer and Chief Financial Officer, respectively) as appropriate to allow timely decisions regarding required disclosure. In designing and evaluating our disclosure controls and procedures, management recognized that disclosure controls and procedures can provide only reasonable, not absolute, assurance that the objectives of the disclosure controls and procedures are met.

Our management, including our Chief Executive Officer and Chief Financial Officer, evaluated the effectiveness of our disclosure controls and procedures. Based on this evaluation and as described below under “Internal Control over Financial Reporting”, our Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures were not effective as of September 30, 2023.

13. INTERNAL CONTROL OVER FINANCIAL REPORTING

Our management is responsible for establishing and maintaining adequate internal control over financial reporting. Internal control over financial reporting is a process designed by, or under the supervision of, the CEO and the CFO and effected by the Board of Directors, management and other personnel to provide reasonable assurance regarding the reliability of financial reporting and the preparation of consolidated financial statements for external purposes in accordance with IFRS.

Our management, including our CEO and CFO, believes that any disclosure controls and procedures or internal control over financial reporting, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of the inherent limitations in all control systems, they cannot provide absolute assurance that all control issues and instances of fraud, if any, have been prevented or detected. These inherent limitations include the realities that judgments in decision-making can be faulty, and that breakdowns can occur because of a simple error or mistake. Additionally, controls can be circumvented by the individual acts of some persons, by collusion of two or more people, or by unauthorized override of the control. The design of any system of controls is based in part on certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Accordingly, because of the inherent limitations in a cost-effective control system, misstatements due to error or fraud might occur and not be detected.

Management assessed the effectiveness of the Company’s internal control over financial reporting on September 30, 2023, based on the criteria set forth in Internal Control – Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission as published in 2013. Based on this evaluation and due to the material weakness described below, management believes, as of September 30, 2023, the Company’s internal control over financial reporting was not effective in respect of the analysis and evaluation of certain technical accounting matters.

| 25 | Page |

Identification of material weakness in internal control over financial reporting

During the reporting period presented, management did not maintain effective control over the interpretation and application of technical IFRS matters. This deficiency required the Company to make adjustments in connection with the issuance of the September 30, 2022 consolidated financial statements.

A material weakness is a deficiency, or combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the Company’s annual or interim financial statements will not be prevented or detected on a timely basis. Management has determined there is a material weakness in internal control over financial reporting.

Remediation of material weakness in internal control over financial reporting

In light of the material weakness, management has commenced a plan to add additional technical accounting resources to the financial reporting process. Management is committed to the implementation of remediation efforts to address the material weakness. Remediation is continuing and intended to address the material weakness and enhance the overall financial control environment, including steps to address the evaluation, applicability, and documentation of the impact of technical accounting matters on an ongoing basis. The material weakness will only be considered as remediated when the applicable control operates for a sufficient period of time and management has concluded through testing, that the control is operating effectively.

No assurance can be provided at this time that the actions and remediation efforts of the Company will effectively remediate the material weakness or prevent the occurrence of other significant deficiencies or material weaknesses in the Company’s internal controls over financial reporting in the future.

14. QUALITATIVE AND QUANTITATIVE DISCLOSURES ABOUT RISKS AND UNCERTAINTIES

The Company may be exposed to risks of varying degrees of significance which could affect its ability to achieve its strategic objectives. The main objectives of the Company’s risk management processes are to ensure that the risks are properly identified and that the capital base is adequate in relation to those risks. The principal risks to which the Company is exposed are described below.

Capital risk

The Company manages its capital to ensure that there are adequate capital resources for the Company to maintain and develop its products. The capital structure of the Company consists of shareholders’ equity and depends on the underlying profitability of the Company’s operations.

| 26 | Page |

The Company manages its capital structure and makes adjustments to it, based on the funds available to the Company, in order to support the development, manufacture and marketing of its products. The Board of Directors does not establish quantitative return on capital criteria for management, but rather relies on the expertise of the Company’s management to sustain future development of the business.

The Company’s capital management objectives are:

| ● | to ensure the Company’s ability to continue as a going concern. |

|

|

|

| ● | to provide an adequate return to shareholders by pricing products and services commensurately with the level of risk. |

The Company monitors capital on the basis of the carrying amount of equity plus its short-term debt comprising the revolving facility, promissory note, less cash and cash equivalents as presented on the face of the statement of financial position.

The Company sets the amount of capital in proportion to its overall financing structure, comprising equity and long-term debt. The Company manages the capital structure and makes adjustments to it in the light of changes in economic conditions and the risk characteristics of the underlying assets. In order to maintain or adjust the capital structure, the Company issues new shares or increases its long-term debt.

Capital for the reporting periods under review is summarized as follows:

| 27 | Page |

Credit risk

Credit risk is the risk that the counterparty fails to discharge an obligation to the Company. The Company is exposed to this risk for various financial instruments, for example, by granting loans and receivables to customers, placing deposits, etc. The Company’s maximum exposure to credit risk is limited to the carrying amount of financial assets recognized at the reporting date, as summarized below:

|

| September 30, |

| |||||

|

| 2023 |

|

| 2022 |

| ||

Cash and cash equivalents |

| $ | 1,032 |

|

| $ | 626 |

|

Trade and other receivables |

|

| 10,611 |

|

|

| 2,913 |

|

Carrying amount |

| $ | 11,643 |

|

| $ | 3,539 |

|

Cash and cash equivalents are comprised of the following:

|

| September 30, |

| |||||

|

| 2023 |

|

| 2022 |

| ||

Cash |

| $ | 1,032 |

|

| $ | 626 |

|

Cash equivalents |

|

| - |

|

|

| - |

|

|

| $ | 1,032 |

|

| $ | 626 |

|

The Company’s current portfolio consists of certain banker’s acceptance and high interest yielding savings accounts deposits. The majority of cash and cash equivalents are held with financial institutions, each of which had at September 30, 2023 a rating of R-1 mid or above.

The Company manages its credit risk by establishing procedures to establish credit limits and approval policies. The balance in trade and other receivables is primarily attributable to trade accounts receivables. In the opinion of management, the credit risk is moderate as some receivables are falling into arrears. Management is taking appropriate action to mitigate this risk by adjusting credit terms.

Liquidity risk

Liquidity risk is the risk that we may not have cash available to satisfy our financial obligations as they come due. The majority of our financial liabilities recorded in accounts payable, accrued and other current liabilities and provisions are due within 90 days. We manage liquidity risk by maintaining a portfolio of liquid funds and having access to a revolving credit facility. We believe that cash flow from operating activities, together with cash on hand, cash from our A/R, and borrowings available under the revolving facility are sufficient to fund our currently anticipated financial obligations and will remain available in the current environment.

| 28 | Page |

The following are the undiscounted contractual maturities of significant financial liabilities and the total contractual obligations of the Company as at September 30, 2023.

|

| 2024 |

|

| 2025 |

|

| 2026 |

|

| 2027 |

|

| 2028 & beyond |

|

| Total |

| ||||||

Trade and other payables |

|

| 8,429 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 8,429 |

|

Lease liability |

|

| 929 |

|

|

| 950 |

|

|

| 789 |

|

|

| 745 |

|

|

| 1,737 |

|

|

| 5,150 |

|

Promissory notes |

|

| 3,500 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 3,500 |

|

Short term loans |

|

| 1,026 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 1,026 |

|

Working capital facility |

|

| 11,821 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 11,821 |

|

Other payable |

|

| 1,365 |

|

|

| 490 |

|

|

| 215 |

|

|

| 56 |

|

|

| 38 |

|

|

| 2,164 |

|

|

|

| 27,070 |

|

|

| 1,440 |

|

|

| 1,004 |

|

|

| 801 |

|

|

| 1,775 |

|

|

| 32,090 |

|

Market risk

Market risk incorporates a range of risks. Movement in risk factors, such as market price risk and currency risk, affect the fair value of financial assets and liabilities. The Company is exposed to these risks as the ability of the Company to develop or market its products and the future profitability of the Company is related to the market price of its primary competitors for similar products.

Interest rate risk

The Company has floating and fixed interest-bearing debt ranging from prime plus 7.05%. The Company’s current policy is to invest excess cash in investment-grade short-term deposit certificates issued by its banking institutions.

Foreign currency risk

The Company is exposed to foreign currency risk. The Company’s functional currency is the Canadian dollar and a majority of its revenue is derived in US dollars. Purchases are transacted in Canadian dollars, United States dollars and Euro. Management believes the foreign exchange risk derived from any currency conversions may have a material effect on the results of its operations. The financial instruments impacted by a change in exchange rates include our exposures to the above financial assets or liabilities denominated in non-functional currencies.

| 29 | Page |

Price risk

The Company is exposed to price risk. Price risk is the risk that the commodity prices that the Company charges are significantly influenced by its competitors and the commodity prices that the Company must charge to meet its competitors may not be sufficient to meet its expenses. The Company reduces the price risk by ensuring that it obtains information regarding the prices set by its competitors to ensure that its prices are appropriate to the unique attributes of our product. In the opinion of management, the price risk is low and is not material.

Disclosure control risks

The Company’s management, with the participation of the Chief Executive Officer and Chief Financial Officer of the Company, have designed disclosure controls and procedures (“DC&P”), or caused them to be designed under their supervision, to provide reasonable assurance that material information relating to the issuer, including its consolidated subsidiaries, is made known, particularly during the period in which interim or annual filings are being prepared, and information required to be disclosed by the Company in its annual filings, interim filings or other reports filed or submitted by it under securities legislation is recorded, processed, summarized and reported within the time periods specified in securities legislation. Although certain weaknesses have been identified, these items do not constitute a material weakness or a weakness in DC&P that are significant. A control system, no matter how well conceived or operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. DC&P are reviewed on an ongoing basis.

Internal control risks

The Company’s management, with the participation of the Chief Executive Officer and Chief Financial Officer of the Company, have designed such internal control over financial reporting (“ICFR”), or caused it to be designed under their supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with IFRS. Such design also uses the framework and criteria established in Internal Control over Financial Reporting - Guidance for Smaller Public Companies, issued by The Committee of Sponsoring Organizations of the Treadway Commission. The Company relies on entity-wide controls and programs including written codes of conduct and controls over initiating, recording, processing and reporting significant account balances and classes of transactions. Other controls include centralized processing controls, including a shared services environment and monitoring of operating results.

Based on the evaluation of the design and operating effectiveness of the Company’s ICFR, the CEO and CFO concluded that the company’s ICFR was not effective as at September 30, 2023.

Other than the material weakness mentioned in section 13, control deficiencies have been identified within the Company’s accounting and finance departments and its financial information systems over segregation of duties and user access respectively. Specifically, certain duties within the accounting and finance departments were not properly segregated due to the small number of individuals employed in these areas. To our knowledge, none of the control deficiencies has resulted in a misstatement to the financial statements. However, these deficiencies may be considered a material weakness resulting in a more-than remote likelihood that a material misstatement of the Company’s annual or interim financial statements would not be prevented or detected.

| 30 | Page |

As the Company incurs future growth, we plan to expand the number of individuals involved in the accounting function. At the present time, the CEO and CFO oversee all material transactions and related accounting records. In addition, the Audit Committee reviews on a quarterly basis the financial statements and key risks of the Company and queries management about significant transactions, there is a quarterly review of the company’s condensed interim unaudited financial statements by the Company’s auditors and daily oversight by the senior management of the Company.

15. OTHER RISKS

Other Risk Factors

The risks described above are not the only risks and uncertainties that we face. Additional risks the Company faces are described under the heading “Risk Factors” in the Company’s AIF for the year ended September 30, 2023.

Other additional risks and uncertainties not presently known to us or that we currently consider immaterial may also impair our business operations. These risk factors could materially affect our future operating results and could cause actual events to differ materially from those described in our forward-looking statements.

Additional information relating to the Company, including our AIF for the year ended September 30, 2023, is available on SEDAR and EDGAR.

| 31 | Page |