Exhibit 99.2

Starton Therapeutics Proprietary Continuous Delivery Platform To Improve Patient Outcomes In Oncology Investor Presentation April 2023

Disclaimer (1 of 4) IMPORTANT LEGAL INFORMATION Additional Information and Where to Find It In connection with the proposed transaction (the “ Proposed Transaction ”), a newly formed parent company (“ Pubco ”) intends to file a registration statement on Form S - 4 (as may be amended or supplemented from time to time, the “ Registration Statement ”) with the U . S . Securities and Exchange Commission (the “ SEC ”), which will include a preliminary proxy statement and a prospectus in connection with the Proposed Transaction . STOCKHOLDERS OF HEALTHWELL ACQUISITION CORP . I (“ HEALTHWELL ”) ARE ADVISED TO READ, WHEN AVAILABLE, THE PRELIMINARY PROXY STATEMENT, ANY AMENDMENTS THERETO, THE DEFINITIVE PROXY STATEMENT, THE PROSPECTUS AND ALL OTHER RELEVANT DOCUMENTS FILED OR THAT WILL BE FILED WITH THE SEC IN CONNECTION WITH THE PROPOSED TRANSACTION AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION . THIS DOCUMENT WILL NOT CONTAIN ALL THE INFORMATION THAT SHOULD BE CONSIDERED CONCERNING THE PROPOSED TRANSACTION . IT IS ALSO NOT INTENDED TO FORM THE BASIS OF ANY INVESTMENT DECISION OR ANY OTHER DECISION IN RESPECT OF THE PROPOSED TRANSACTION . When available, the definitive proxy statement and other relevant documents will be mailed to the stockholders of Healthwell as of a record date to be established for voting on the Proposed Transaction . Stockholders and other interested persons will also be able to obtain copies of the preliminary proxy statement, the definitive proxy statement, the Registration Statement and other documents filed the SEC that will be incorporated by reference therein, without charge, once available, at the SEC’s website at www . sec . gov . Healthwell’s stockholders will also be able to obtain a copy of such documents, without charge, by directing a request to : Healthwell Acquisition Corp . , 1001 Green Bay Rd, # 227 Winnetka, IL 60093 ; e - mail : healthwell . management@healthwellspac . com . 2

Disclaimer (2 of 4) Forward - Looking Statements This communication contains forward - looking statements for purposes of the “safe harbor” provisions under the United States Private Securities Litigation Reform Act of 1995 . Any statements other than statements of historical fact contained herein are forward - looking statements . Such forward - looking statements include, but are not limited to, expectations, hopes, beliefs, intentions, plans, prospects, financial results or strategies regarding Starton Therapeutics, Inc . (“ Starton ”) and the Proposed Transaction and the future held by the respective management teams of Healthwell or Starton, the anticipated benefits and the anticipated timing of the Proposed Transaction, future financial condition and performance of Starton and expected financial impacts of the Proposed Transaction (including future revenue, pro forma enterprise value and cash balance), the satisfaction of closing conditions to the Proposed Transaction, financing transactions, if any, related to the Proposed Transaction, the level of redemptions of Healthwell’s public stockholders and the products and markets and expected future performance and market opportunities of Starton . These forward - looking statements generally are identified by the words “anticipate,” “believe,” “could,” “expect,” “estimate,” “future,” “intend,” “may,” “might,” “strategy,” “opportunity,” “plan,” “project,” “possible,” “potential,” “project,” “predict,” “scales,” “representative of,” “valuation,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions, but the absence of these words does not mean that a statement is not forward - looking . Forward - looking statements are predictions, projections and other statements about future events that are based on current expectations and assumptions and, as a result, are subject to risks and uncertainties . Many factors could cause actual future events to differ materially from the forward - looking statements in this communication, including, without limitation : (i) the risk that the Proposed Transaction may not be completed in a timely manner or at all, which may adversely affect the price of Healthwell’s securities ; (ii) the risk that the Proposed Transaction may not be completed by Healthwell’s business combination deadline and the potential failure to obtain an extension of the business combination deadline if sought by Healthwell ; (iii) the failure to satisfy the conditions to the consummation of the Proposed Transaction, including, among others, the condition that Healthwell has cash or cash equivalents of at least $ 15 million, and the requirement that the definitive agreement related to the Proposed Transaction (the “ Merger Agreement ”) and the transactions contemplated thereby be approved by the stockholders of each of Healthwell and Starton ; (iv) the failure to obtain any applicable regulatory approvals required to consummate the Proposed Transaction ; (v) the occurrence of any event, change or other circumstance that could give rise to the termination of the Merger Agreement ; (vi) the effect of the announcement or pendency of the Proposed Transaction on Starton's business relationships, operating results, and business generally ; (vii) risks that the Proposed Transaction disrupts current plans and operations of Starton ; (viii) the risk that Pubco may not be able to raise funds in a PIPE financing or may not be able to raise as much as anticipated ; (ix) the outcome of any legal proceedings that may be instituted against Starton or Healthwell related to the Merger Agreement or the Proposed Transaction ; (x) the ability to maintain the listing of Healthwell’s securities on a national securities exchange or failure of Pubco to meet initial listing standards in connection with the consummation of the Proposed Transaction ; (xi) uncertainty regarding outcomes of Starton’s ongoing clinical trials, particularly as they relate to regulatory review and potential approval for its product candidates ; (xii) risks associated with Starton’s efforts to commercialize a product candidate ; (xiii) Starton’s ability to negotiate and enter into definitive agreements for supply, sales, marketing, and/or distribution on favorable terms, if at all ; (xiv) the impact of competing product candidates on Starton’s business ; (xv) intellectual property - related claims ; and (xvi) Starton’s ability to attract and retain qualified personnel ; and (xvii) Starton’s ability to continue to source the raw materials for its product candidates . 3

Disclaimer (3 of 4) The foregoing list of factors is not exhaustive . Recipients should carefully consider such factors and the other risks and uncertainties described and to be described in the “Risk Factors” section of Healthwell’s initial public offering (“ IPO ”) prospectus filed with the SEC on August 4 , 2021 , Healthwell’s Annual Report on Form 10 - K filed for the year ended December 31 , 2022 filed with the SEC on March 3 , 2023 and subsequent periodic reports filed by Healthwell with the SEC, the Registration Statement and other documents filed or to be filed by Healthwell from time to time with the SEC . These filings identify and address other important risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward - looking statements . Forward - looking statements speak only as of the date they are made . Recipients are cautioned not to put undue reliance on forward - looking statements, and neither Starton, Healthwell nor Pubco assume any obligation to, nor intend to, update or revise these forward - looking statements, whether as a result of new information, future events, or otherwise, except as required by law . Neither Starton, Healthwell nor Pubco gives any assurance that either Starton or Healthwell, or the combined company, will achieve its expectations . Information Sources; No Representations The communication furnished herewith has been prepared for use by Healthwell and Starton in connection with the Proposed Transaction . The information therein does not purport to be all - inclusive . The information therein is derived from various internal and external sources, with all information relating to the business, past performance, results of operations and financial condition of Healthwell derived entirely from Healthwell and all information relating to the business, past performance, results of operations and financial condition of Starton derived entirely from Starton . No representation is made as to the reasonableness of the assumptions made with respect to the information therein, or to the accuracy or completeness of any projections or modeling or any other information contained therein . Any data on past performance or modeling contained therein is not an indication as to future performance . No representations or warranties, express or implied, are given in respect of the communication or any other information (whether written or oral) that has been or will be provided to you or publicly available . To the fullest extent permitted by law in no circumstances will Healthwell, Starton or Pubco, or any of their respective subsidiaries, affiliates, shareholders, representatives, partners, directors, officers, employees, advisors or agents, be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of the this communication (including without limitation any projections or models), any omissions, reliance on information contained within it, or on opinions communicated in relation thereto or otherwise arising in connection therewith, which information relating in any way to the operations of Starton has been derived, directly or indirectly, exclusively from Starton and has not been independently verified by Healthwell . Neither the independent auditors of Healthwell nor the independent auditors of or Starton audited, reviewed, compiled or performed any procedures with respect to any projections or models for the purpose of their inclusion in the communication and, accordingly, neither of them expressed any opinion or provided any other form of assurances with respect thereto for the purposes of the communication . Prior Disclosures Starton is aware that its CEO appeared on the television program “Unicorn Hunters” on June 7 , 2021 . During that appearance, the CEO made a number of representations as to Starton’s approach to reformulating drug products to improve efficacy, tolerability and patients’ quality of life . As part of these representations, the CEO raised the specific example of Starton’s investigational reformulation of Revlimid Œ . While Starton believes in the value of its product, it understands that any clinical superiority claims cannot be made absent specific findings from rigorous clinical studies which Starton has not undertaken . The CEO’s comments on the television program were not intended to suggest Starton has conducted such studies ; Starton does not have data to support these specific representations and disclaims any representations or purported representations by its CEO which either stated or implied the contrary . Trademarks and Tradenames This communication includes trademarks of Starton, which are protected under applicable intellectual property laws and are the property of Starton or its subsidiaries . This communication also includes other trademarks, trade names and service marks that are the property of their respective owners . We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies . 4

Disclaimer (4 of 4) Participants in the Solicitation Healthwell, Starton, Pubco and their respective directors and executive officers may be deemed participants in the solicitation of proxies of Healthwell’s stockholders in connection with the Proposed Transaction . Healthwell’s stockholders and other interested persons may obtain more detailed information regarding the names, affiliations, and interests of certain of Healthwell executive officers and directors in the solicitation by reading Healthwell’s final prospectus filed with the SEC on August 4 , 2021 in connection with Healthwell’s IPO, Healthwell’s Annual Report on Form 10 - K for the year ended December 31 , 2022 filed with the SEC on March 3 , 2023 and Healthwell’s other filings with the SEC . A list of the names of such directors and executive officers and information regarding their interests in the Proposed Transaction, which may, in some cases, be different from those of stockholders generally, will be set forth in the Registration Statement relating to the Proposed Transaction when it becomes available . These documents can be obtained free of charge from the source indicated above . No Offer or Solicitation This communication shall not constitute a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the Proposed Transaction . This communication shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any states or jurisdictions in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such state or jurisdiction . No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933 , as amended, or an exemption therefrom . 5

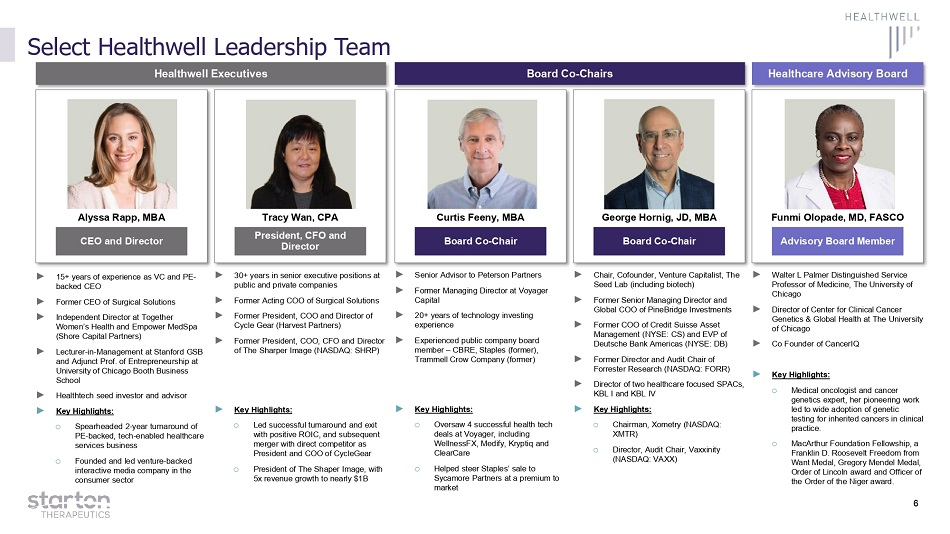

Select Healthwell Leadership Team ► 30+ years in senior executive positions at public and private companies ► Former Acting COO of Surgical Solutions ► Former President, COO and Director of Cycle Gear (Harvest Partners) ► Former President, COO, CFO and Director of The Sharper Image (NASDAQ: SHRP) ► Key Highlights: o Led successful turnaround and exit with positive ROIC, and subsequent merger with direct competitor as President and COO of CycleGear o President of The Shaper Image, with 5x revenue growth to nearly $1B President, CFO and Director Tracy Wan, CPA CEO and Director Alyssa Rapp, MBA ► 15+ years of experience as VC and PE - backed CEO ► Former CEO of Surgical Solutions ► Independent Director at Together Women’s Health and Empower MedSpa (Shore Capital Partners) ► Lecturer - in - Management at Stanford GSB and Adjunct Prof. of Entrepreneurship at University of Chicago Booth Business School ► Healthtech seed investor and advisor ► Key Highlights: o Spearheaded 2 - year turnaround of PE - backed, tech - enabled healthcare services business o Founded and led venture - backed interactive media company in the consumer sector Healthwell Executives Healthcare Advisory Board Advisory Board Member Funmi Olopade, MD, FASCO ► Walter L Palmer Distinguished Service Professor of Medicine, The University of Chicago ► Director of Center for Clinical Cancer Genetics & Global Health at The University of Chicago ► Co Founder of CancerIQ ► Key Highlights: o Medical oncologist and cancer genetics expert, her pioneering work led to wide adoption of genetic testing for inherited cancers in clinical practice. o MacArthur Foundation Fellowship, a Franklin D . Roosevelt Freedom from Want Medal, Gregory Mendel Medal, Order of Lincoln award and Officer of the Order of the Niger award . Board Co - Chair Curtis Feeny, MBA ► Senior Advisor to Peterson Partners ► Former Managing Director at Voyager Capital ► 20+ years of technology investing experience ► Experienced public company board member – CBRE, Staples (former), Trammell Crow Company (former) ► Key Highlights: o Oversaw 4 successful health tech deals at Voyager, including WellnessFX, Medify, Kryptiq and ClearCare o Helped steer Staples’ sale to Sycamore Partners at a premium to market Board Co - Chairs Board Co - Chair George Hornig, JD, MBA ► Chair, Cofounder, Venture Capitalist, The Seed Lab (including biotech) ► Former Senior Managing Director and Global COO of PineBridge Investments ► Former COO of Credit Suisse Asset Management (NYSE: CS) and EVP of Deutsche Bank Americas (NYSE: DB) ► Former Director and Audit Chair of Forrester Research (NASDAQ: FORR) ► Director of two healthcare focused SPACs, KBL I and KBL IV ► Key Highlights: o Chairman, Xometry (NASDAQ: XMTR) o Director, Audit Chair, Vaxxinity (NASDAQ: VAXX) 6

Investment Highlights Enhanced Proprietary Delivery System Leveraging Proven Continuous Delivery Technology Across a Wide Range of Indications Blockbuster Potential With a Groundbreaking Approach to Treating Multiple Myeloma and Other Hematological - Malignancies Superior PK/PD Profile Versus the Current Standard - Of - Care, Leading to Improved Drug Tolerability and Superior Outcomes Significant Opportunity to Expand Total Addressable Market by Capturing Revlimid Intolerant Patients De - Risked Opportunity by Leveraging FDA - Approved Blockbuster Products With Proven Active Ingredients Strong Cadence of Upcoming Catalysts With Defined Pathway Into Clinic and Clear Path Forward to Potential Approval Substantial Expansion Opportunities With the Potential to Leverage the Existing Technology in Other Approved Blockbuster Molecules 1 2 3 4 5 6 7 7

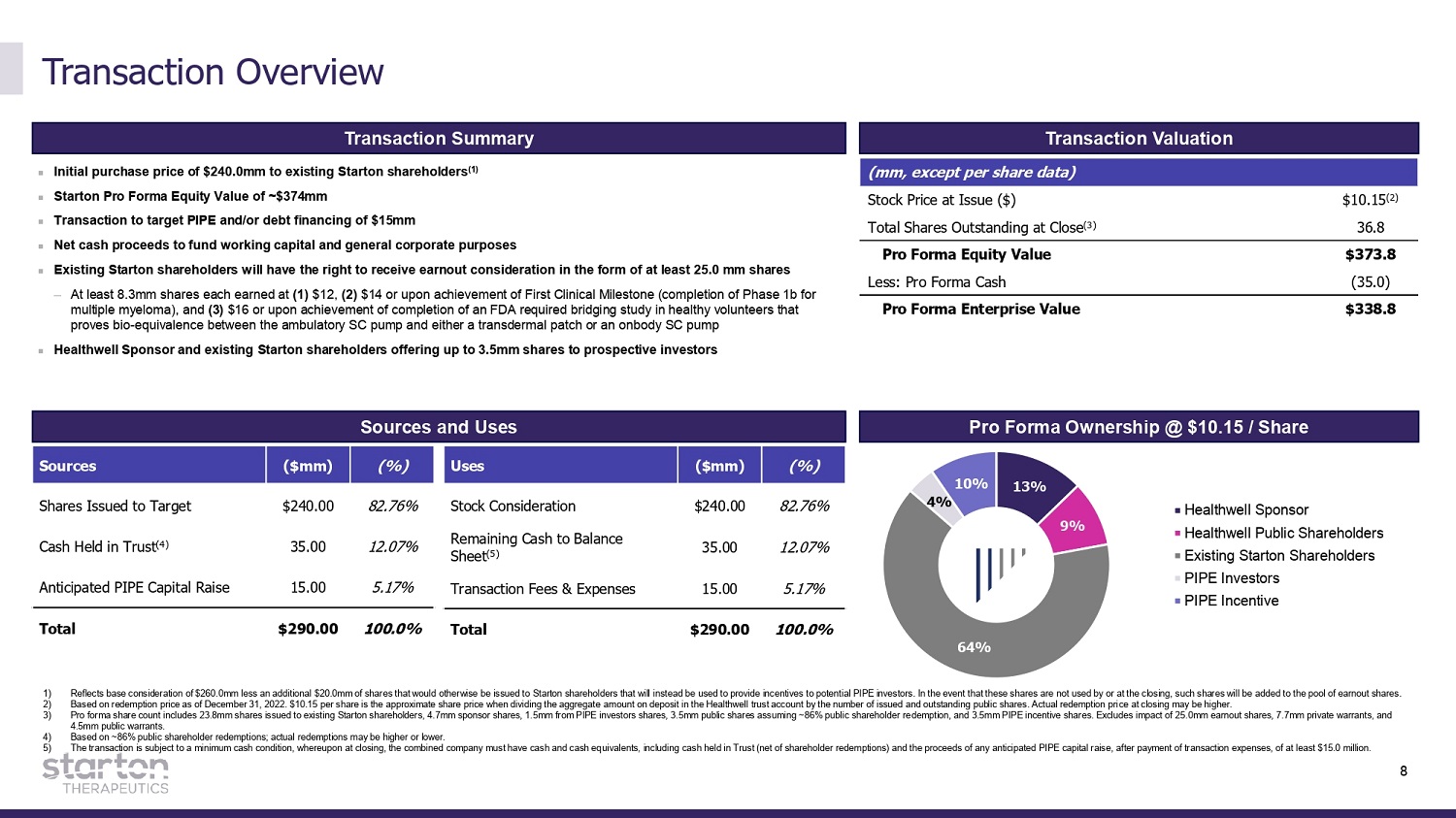

Transaction Overview 1) 2) 3) 4) 5) Reflects base consideration of $260.0mm less an additional $20.0mm of shares that would otherwise be issued to Starton shareholders that will instead be used to provide incentives to potential PIPE investors. In the event that these shares are not used by or at the closing, such shares will be added to the pool of earnout shares. Based on redemption price as of December 31, 2022. $10.15 per share is the approximate share price when dividing the aggregate amount on deposit in the Healthwell trust account by the number of issued and outstanding public shares. Actual redemption price at closing may be higher. Pro forma share count includes 23.8mm shares issued to existing Starton shareholders, 4.7mm sponsor shares, 1.5mm from PIPE investors shares, 3.5mm public shares assuming ~86% public shareholder redemption, and 3.5mm PIPE incentive shares. Excludes impact of 25.0mm earnout shares, 7.7mm private warrants, and 4.5mm public warrants. Based on ~86% public shareholder redemptions; actual redemptions may be higher or lower. The transaction is subject to a minimum cash condition, whereupon at closing, the combined company must have cash and cash equivalents, including cash held in Trust (net of shareholder redemptions) and the proceeds of any anticipated PIPE capital raise, after payment of transaction expenses, of at least $15.0 million. Transaction Summary Transaction Valuation (mm, except per share data) Stock Price at Issue ($) $10.15 (2) Total Shares Outstanding at Close (3) 36.8 Pro Forma Equity Value $373.8 Less: Pro Forma Cash ( 3 5 .0) Pro Forma Enterprise Value $338 . 8 Initial purchase price of $240.0mm to existing Starton shareholders (1) Starton Pro Forma Equity Value of ~$374mm Transaction to target PIPE and/or debt financing of $15mm Net cash proceeds to fund working capital and general corporate purposes Existing Starton shareholders will have the right to receive earnout consideration in the form of at least 25.0 mm shares — At least 8.3mm shares each earned at (1) $12, (2) $14 or upon achievement of First Clinical Milestone (completion of Phase 1b for multiple myeloma), and (3) $16 or upon achievement of completion of an FDA required bridging study in healthy volunteers that proves bio - equivalence between the ambulatory SC pump and either a transdermal patch or an onbody SC pump Healthwell Sponsor and existing Starton shareholders offering up to 3.5mm shares to prospective investors Sources and Uses Sources ($mm) (%) Uses ($mm) (%) Shares Issued to Target $240.00 82.76% Stock Consideration $240.00 82.76% Cash Held in Trust (4) 35.00 12.07% Remaining Cash to Balance Sheet (5) 35.00 12.07% Anticipated PIPE Capital Raise 15.00 5.17% Transaction Fees & Expenses 15.00 5.17% Total $290.00 100.0% Total $290.00 100.0% Pro Forma Ownership @ $10.15 / Share 13% 9% 64% 4% 10% Healthwell Sponsor Healthwell Public Shareholders Existing Starton Shareholders PIPE Investors PIPE Incentive 8

Starton Overview 9

Established Starton Leadership Team With Clinical, Operational, and Financial Expertise Chief Financial Officer Scott Kahn, CPA, CGMA, MBA CEO, Co - founder Chairman Pedro Lichtinger, MBA Chief Medical Officer Dr. Jamie Oliver, PharmD ► 35+ years of experience. Prior to joining Starton Therapeutics, Mr. Kahn was CFO and Vice President of Diopsys for approximately fifteen years where he was responsible for all accounting, finance, human resources and investor relations. ► Prior to joining Diopsys, Mr. Kahn served as CFO at Diamond Chemical Co., Inc., a privately held chemical manufacturer. ► Previously, Mr. Kahn held various finance, strategy and operational leadership roles. received a B.A. in Accounting from Franklin and Marshall College and an M.B.A. in International Business from Rutgers University. ► 37 - year career in biotechnology and a proven track record of developing turnaround and financing strategies, executing strategic alliances, and building commercial and R&D capabilities. ► Former President and CEO of Asterias Biotherapeutics and Optimer Pharmaceuticals with 16 years’ experience at Pfizer Inc as President of Global Primary Care and President of Europe. ► He currently sits on the Board of Applied Biological Laboratories, Inc. and Zero Gravity. He holds an MBA degree from Wharton School of Business and an engineering degree from the National University of Mexico. ► 12 years in academia and 29 years in both the public and private sectors of the biopharma industry and contract research organizations. ► He served in numerous clinical development operations roles including COO, SVP Clinical Research and Regulatory Affairs, CSO, and Medical Officer. ► Dr. Oliver has significant FDA experience with both the Drug and Biologic divisions, having prepared more than 50 INDs and participated in seven successful NDA submissions for U.S./Global pharmaceutical companies. ► Participated in several series of successful fund raisings, as well as served in - licensing negotiations and out - licensing of several oncology assets. ► 30+ years of operational experience including 13 years in transdermal development and manufacturing. Mr. Rensink is the former President and COO of Tapemark, where he led development, strategy implementation for pharmaceutical COMO developing and manufacturing Transdermal Patches and Oral Thin Film products. ► Currently sits on the Board of Advisors for HydraFlex chemical dispensing systems. ► Holds a Masters in Engineering from Marquette University, BSME from University of Wisconsin and completed the GE Manufacturing Management Program. Chief Manufactu r ing Officer Andy Rensink, MSE 10

Renowned Scientific Committee with Significant Experience in Relevant Therapy Areas Mohamad Hussein, MD Chair, Scientific Committee Instrumental in REVLIMID® approval in MM and the body of literature supporting its use in CLL Kenneth Anderson, MD Multiple Myeloma (MM) Lead Have contributed to the body of literature supporting the use of Asher Chanan - Khan, MD lenalidomide in MM and Chronic Lymphocytic Leukemia (CLL) Lead CLL Starton Scientific Committee Members 11 Source: Published scientific literature and public websites.

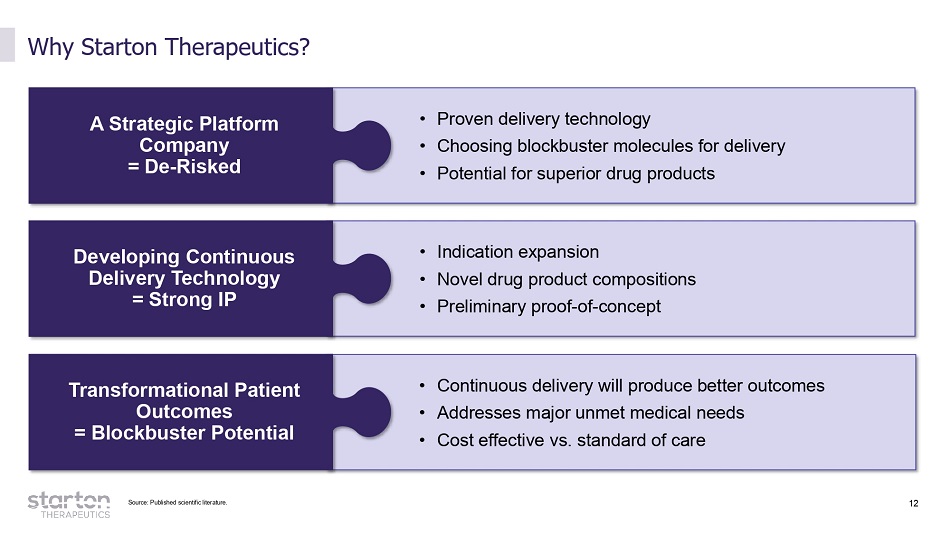

12 • Proven delivery technology • Choosing blockbuster molecules for delivery • Potential for superior drug products • Continuous delivery will produce better outcomes • Addresses major unmet medical needs • Cost effective vs. standard of care • Indication expansion • Novel drug product compositions • Preliminary proof - of - concept Why Starton Therapeutics? A Strategic Platform Company = De - Risked Developing Continuous Delivery Technology = Strong IP Transformational Patient Outcomes = Blockbuster Potential Source: Published scientific literature.

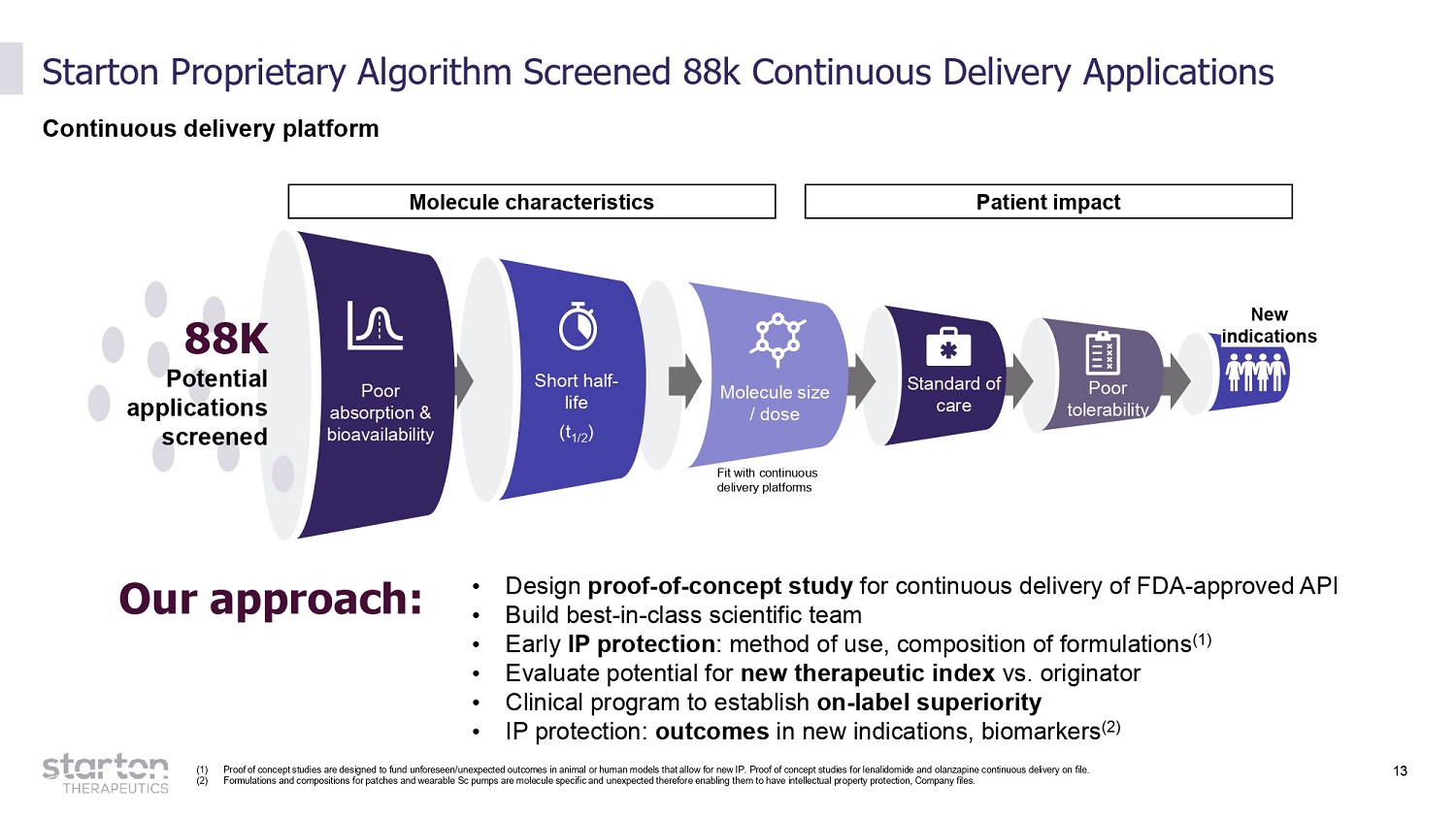

13 Starton Proprietary Algorithm Screened 88k Continuous Delivery Applications Continuous delivery platform Poor absorption & b i oav a i l a b i l ity Short half - life (t 1/2 ) Molecule size / dose 88K Potent i al app l ic a tions screened Fit with continuous delivery platforms Molecule characteristics Patient impact Standard of care Poor tolerab i l i ty New indicatio ns Our approach: • Design proof - of - concept study for continuous delivery of FDA - approved API • Build best - in - class scientific team • Early IP protection : method of use, composition of formulations (1) • Evaluate potential for new therapeutic index vs. originator • Clinical program to establish on - label superiority • IP protection: outcomes in new indications, biomarkers (2) (1) Proof of concept studies are designed to fund unforeseen/unexpected outcomes in animal or human models that allow for new IP. Proof of concept studies for lenalidomide and olanzapine continuous delivery on file. (2) Formulations and compositions for patches and wearable Sc pumps are molecule specific and unexpected therefore enabling them to have intellectual property protection, Company files.

14 Continuous Delivery Platform & Market Opportunity Overview

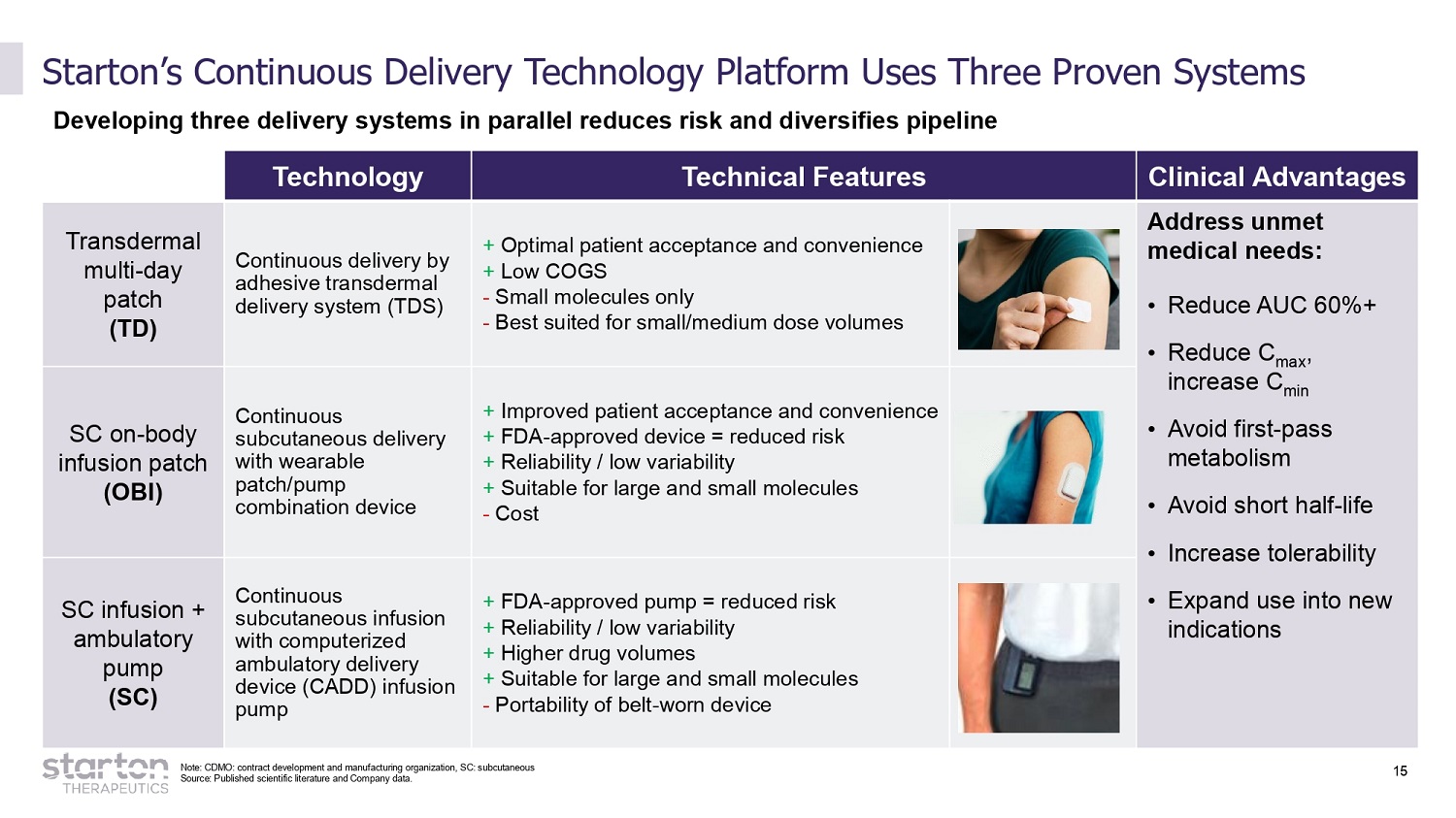

15 Starton’s Continuous Delivery Technology Platform Uses Three Proven Systems Developing three delivery systems in parallel reduces risk and diversifies pipeline Note: CDMO: contract development and manufacturing organization, SC: subcutaneous Source: Published scientific literature and Company data. Technology Technical Features Clinical Advantages T ra n sderm a l multi - day patch (TD) Continuous delivery by adhesive transdermal delivery system (TDS) + Optimal patient acceptance and convenience + Low COGS - Small molecules only - Best suited for small/medium dose volumes Address unmet medical needs: • Red u ce AUC 6 0 %+ • Reduce C max , increase C min • Avoid first - pass metabolism • Avoid short half - life • Increase tolerability • Expand use into new indications SC on - body infusion patch (OBI) Continuous subcutaneous delivery with wearable patch/pump combination device + Improved patient acceptance and convenience + FDA - approved device = reduced risk + Reliability / low variability + Suitable for large and small molecules - Cost SC infusion + ambulatory pump (SC) Continuous subcutaneous infusion with computerized ambulatory delivery device (CADD) infusion pump + FDA - approved pump = reduced risk + Reliability / low variability + Higher drug volumes + Suitable for large and small molecules - Portability of belt - worn device

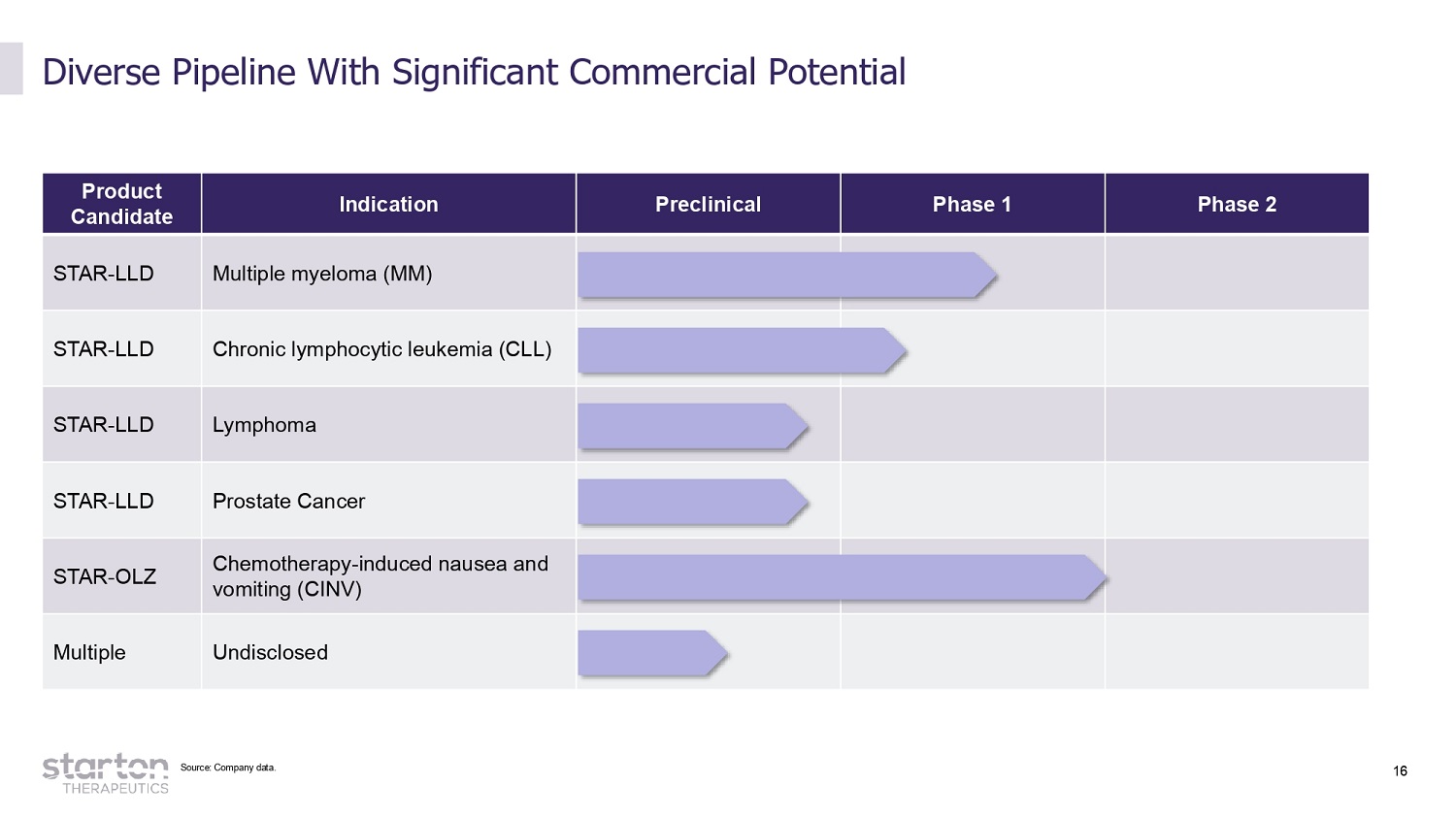

16 Product Candidate Indication Preclinical Phase 1 Phase 2 STAR - LLD Multiple myeloma (MM) STAR - LLD Chronic lymphocytic leukemia (CLL) STAR - LLD Lymphoma STAR - LLD Prostate Cancer STAR - OLZ Chemotherapy - induced nausea and vomiting (CINV) Multiple Undisclosed Diverse Pipeline With Significant Commercial Potential Source: Company data.

17 S T A R - LLD

18 Significant Market Opportunity For STAR - LLD, A Continuous Delivery Lenalidomide Multiple Myeloma (MM) Opportunity Revlimid Peak Revenues in US Additional Potential Indications: • In combination with CAR - T cell and bi - specifics • Smoldering Myeloma $6. 5 B Chronic Lymphocytic Leukemia (CLL) Opportunity CLL Global Market Opportunity $5. 3 B Target Indications Clinical Stage Near - Term Catalysts Multiple myeloma (MM), Chronic lymphocytic leukemia (CLL) Phase 1 Bioavailability complete Phase 1b MM, Phase 2 CLL Projected CAGR 4.6% - 15% • Leading product Ibrutinib $3.4B • Only 3 MoAs Used in Treatment • No IMiDs Available • No maintenance First IMiD available Phase 3 Revlimid Trial • Highly effective • First maintenance indication • Well tolerated at 5 - 10mgs Source: Public filings and third - party market research.

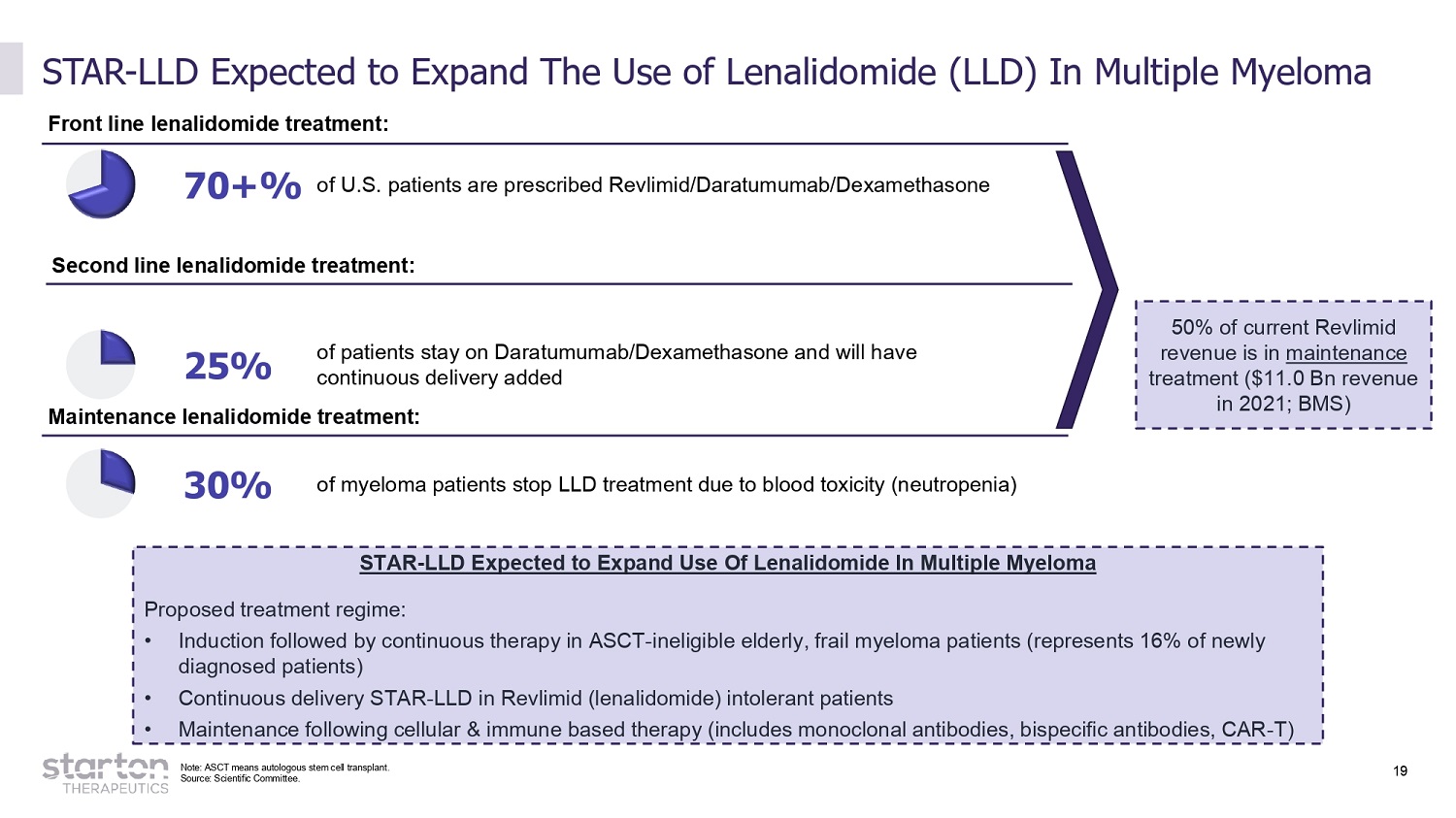

19 STAR - LLD Expected to Expand The Use of Lenalidomide (LLD) In Multiple Myeloma 70+% of U.S. patients are prescribed Revlimid/Daratumumab/Dexamethasone 30% of myeloma patients stop LLD treatment due to blood toxicity (neutropenia) Front line lenalidomide treatment: Maintenance lenalidomide treatment: 25% of patients stay on Daratumumab/Dexamethasone and will have continuous delivery added 50% of current Revlimid revenue is in maintenance treatment ($11.0 Bn revenue in 2021; BMS) STAR - LLD Expected to Expand Use Of Lenalidomide In Multiple Myeloma Proposed treatment regime: • Induction followed by continuous therapy in ASCT - ineligible elderly, frail myeloma patients (represents 16% of newly diagnosed patients) • Continuous delivery STAR - LLD in Revlimid (lenalidomide) intolerant patients • Maintenance following cellular & immune based therapy (includes monoclonal antibodies, bispecific antibodies, CAR - T) Second line lenalidomide treatment: Note: ASCT means autologous stem cell transplant. Source: Scientific Committee.

20 Multiple Myeloma Development Plans Phase 1b/2/3 – 2 nd line STAR - LLD in combination with a Proteasome Inhibitor and Dex in transplant ineligible patients 1,2 Phase 2/3 – 1 st line STAR - LLD in combination with Daratumumab and Dex in transplant ineligible patients 1,2 Phase 3 – Maintenance monotherapy following SCT 1,2 Phase 2 – Combination with CAR - T to improve the depth of response 1,3 1 = superiority in outcomes and/or tolerability 2 = single pivotal study Source: Company data. 3 = phase 2 pivotal study

21 Chronic Lymphocytic Leukemia Development Plans Phase 2/3 – 2 nd line in combination with venetoclax 1,2 Phase 2/3 – 1 st line in combination with a BTK inhibitor 1,2 Phase 3 – Maintenance monotherapy in MRD - patients following six months of venetoclax 1,2 1 = superiority in outcomes 2 = single pivotal study Note: MRD means minimal residual disease. Source: Company data.

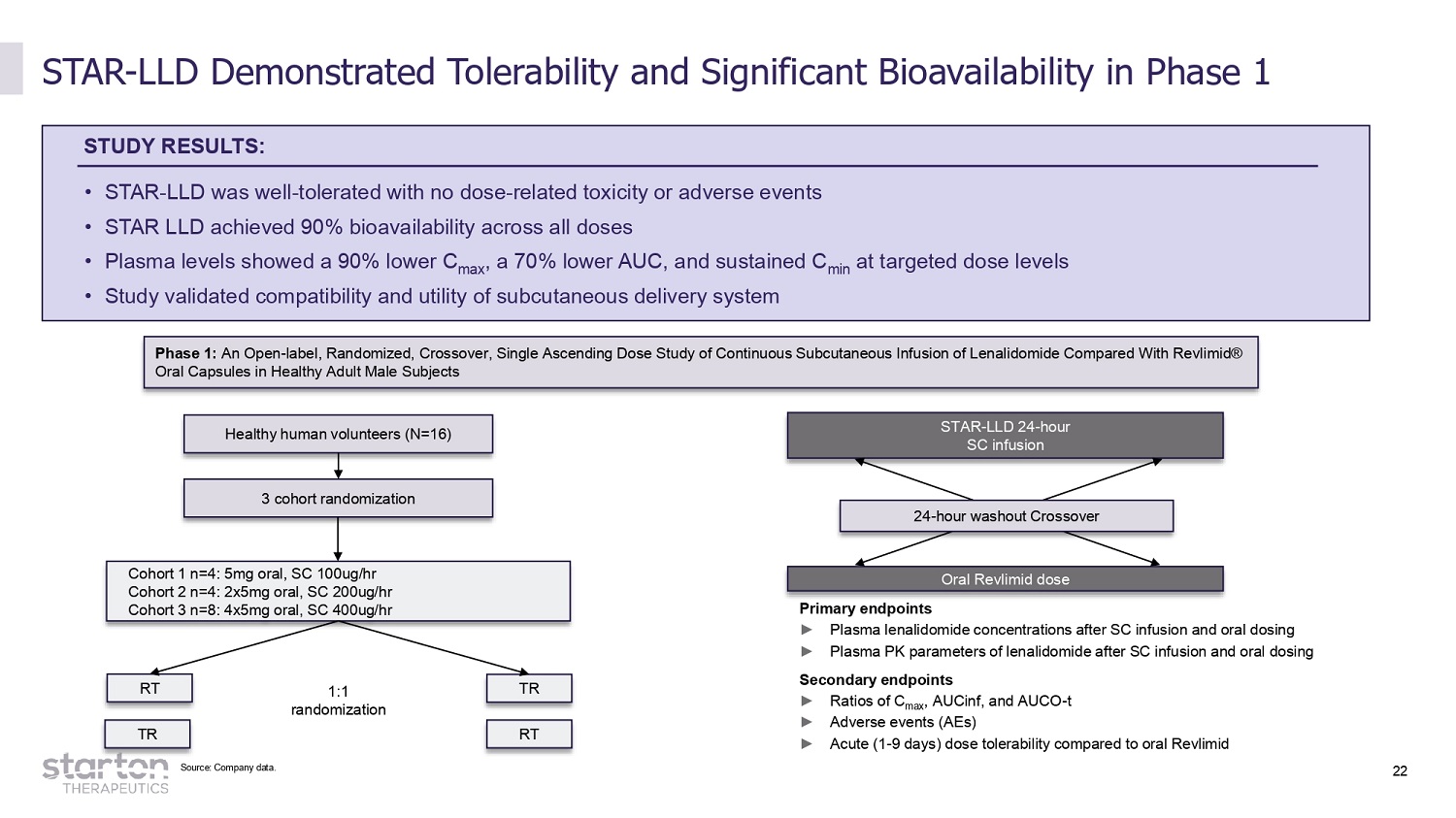

22 STAR - LLD Demonstrated Tolerability and Significant Bioavailability in Phase 1 STUDY RESULTS: • STAR - LLD was well - tolerated with no dose - related toxicity or adverse events • STAR LLD achieved 90% bioavailability across all doses • Plasma levels showed a 90% lower C max , a 70% lower AUC, and sustained C min at targeted dose levels • Study validated compatibility and utility of subcutaneous delivery system Phase 1: An Open - label, Randomized, Crossover, Single Ascending Dose Study of Continuous Subcutaneous Infusion of Lenalidomide Compared With Revlimid® Oral Capsules in Healthy Adult Male Subjects 3 cohort randomization Healthy human volunteers (N=16) STAR - LLD 24 - hour SC infusion Cohort 1 n=4: 5mg oral, SC 100ug/hr Cohort 2 n=4: 2x5mg oral, SC 200ug/hr Cohort 3 n=8: 4x5mg oral, SC 400ug/hr RT TR Oral Revlimid dose 1:1 randomization Primary endpoints ► Plasma lenalidomide concentrations after SC infusion and oral dosing ► Plasma PK parameters of lenalidomide after SC infusion and oral dosing Secondary endpoints ► Ratios of C max , AUCinf, and AUCO - t ► Adverse events (AEs) ► Acute (1 - 9 days) dose tolerability compared to oral Revlimid 24 - hour washout Crossover TR RT Source: Company data.

23 STAR - LLD Is Currently Being Evaluated In A Phase 1b Study In Multiple Myeloma • 2 nd line MM patients receiving a proteasome inhibitor and dex with lenalidomide • Allows for Phase 2 studies in MM and CLL STAR - LLD continuous administration Open - label study, objectives: • Safety and tolerability of continuous LLD • Immunologic activity of NK cells and T cells for innate and humoral immunity • Changes in efficacy indicators including MRD status, PFS, DOR Open - label Study With Multiple Opportunities To Report On Tolerability, Complete And Partial Responses (CR/PR). Potential For Breakthrough Designation Phase 1b: Study Locations: US, 6 sites Duration: 12 months + interim reports throughout study Safety and PD: 9.6 mg/day or 400 mcg/hr Phase 1b: n=6 Multiple myeloma patients Note: DOR means duration of response, PFS means progression - free survival. Source: Company data.

24 STAR - LLD Demonstrated Durable and Deep Responses in Preclinical Work STAR - LLD preclinical program Superior efficacy: durability and depth of response • 40% Complete Response, 60% Partial Response at 144 mcg continuous LLD vs. 0% daily pulsatile LLD • 20% of animals at 144 mcg/d cured with no evidence of disease at 100 days Safety and tolerability • Chronic (28 day) treatment produced no hematologic or local toxicity • No drug - related macro/micro histopathologic toxicity • Similar weight changes in all animals (placebo and lenalidomide) Four preclinical studies • 10 - day dose - finding of STAR - LLD continuous SC in healthy CB17 mice • 29 - day efficacy/safety of STAR - LLD continuous SC versus ip lenalidomide in SCID mice • 28 - day GLP toxicity study of STAR - LLD continuous SC versus vehicle in healthy mice • 27 - day efficacy study of STAR - LLD continuous SC versus ip lenalidomide in IMiD - resistant RPMI CB.17 SCID mice Source: Company data.

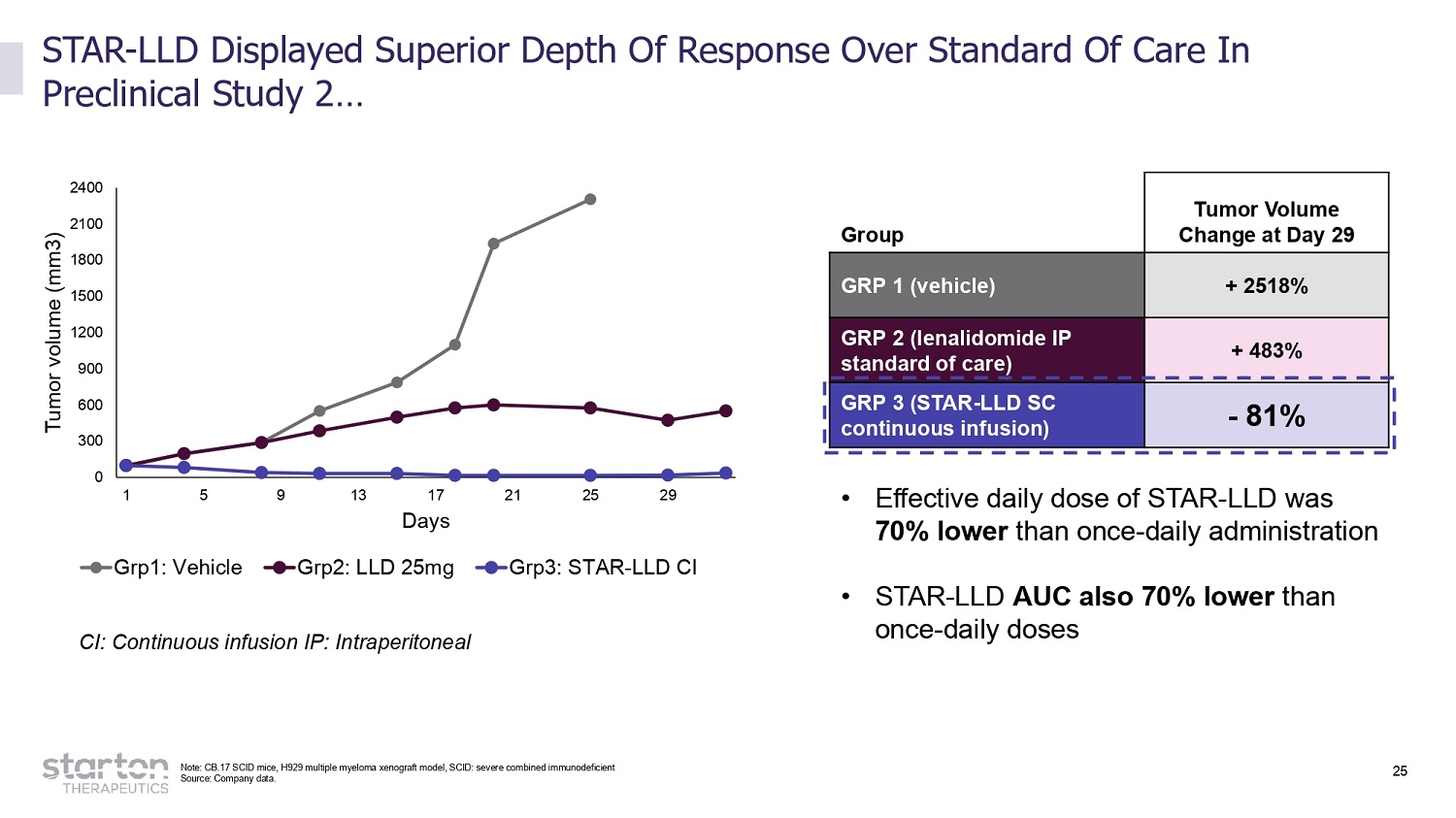

25 CI: Continuous infusion IP: Intraperitoneal 2 4 00 2 1 00 1 8 00 1 5 00 1 2 00 900 600 300 0 1 5 9 13 17 Days 21 25 29 Tumor volume (mm3) Grp1: Vehicle Grp2: LLD 25mg Grp3: STAR - LLD CI Source: Company data. Group Tumor Volume Change at Day 29 GRP 1 (vehicle) + 2518% GRP 2 (lenalidomide IP standard of care) + 483% GRP 3 (STAR - LLD SC continuous infusion) - 81% STAR - LLD Displayed Superior Depth Of Response Over Standard Of Care In Preclinical Study 2… • Effective daily dose of STAR - LLD was 70% lower than once - daily administration • STAR - LLD AUC also 70% lower than once - daily doses Note: CB.17 SCID mice, H929 multiple myeloma xenograft model, SCID: severe combined immunodeficient

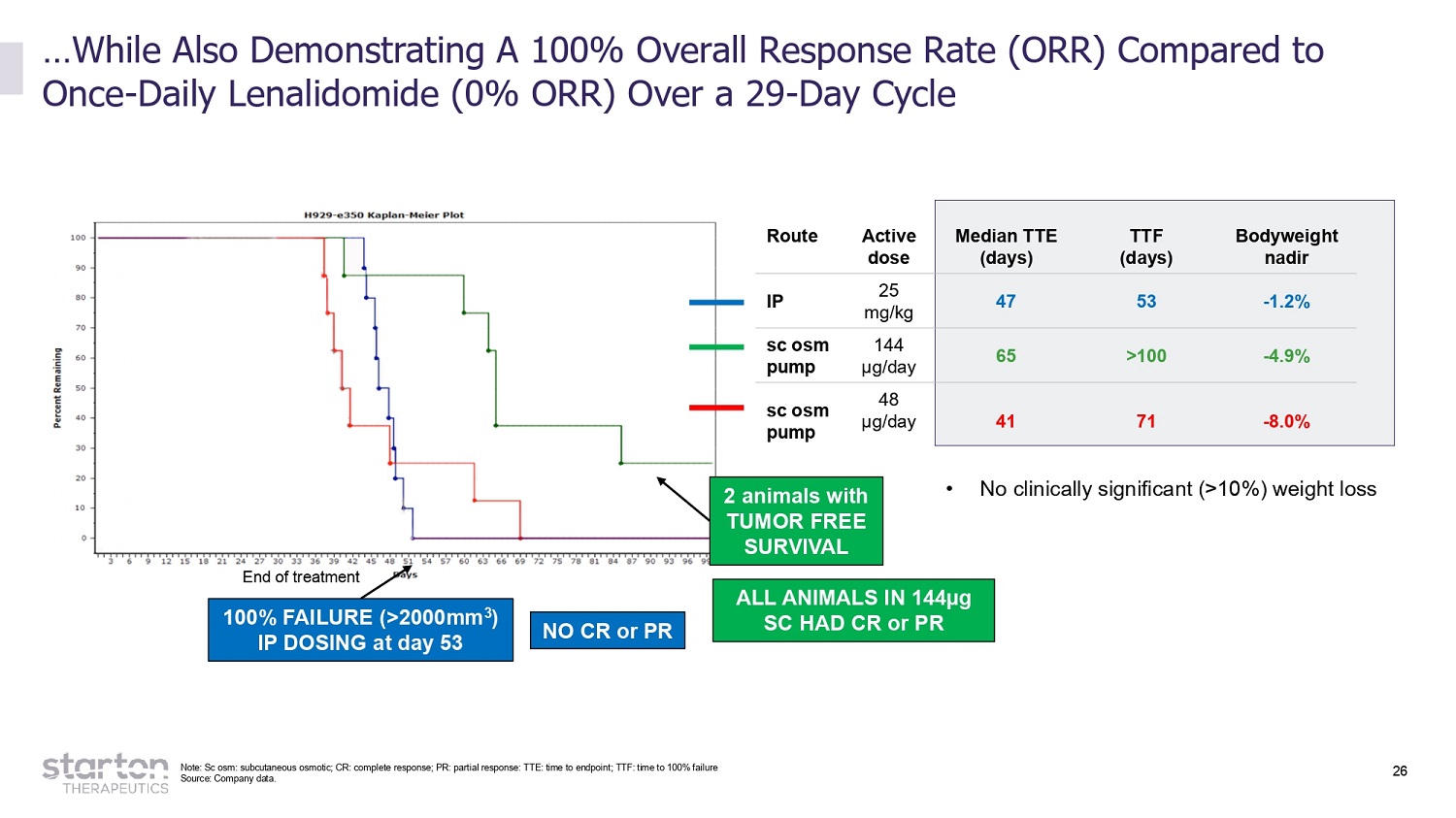

26 …While Also Demonstrating A 100% Overall Response Rate (ORR) Compared to Once - Daily Lenalidomide (0% ORR) Over a 29 - Day Cycle End of treatment 100% FAILURE (>2000mm 3 ) IP DOSING at day 53 2 animals with TUMOR FREE SURVIVAL Route A c tive dose Median TTE (days) TTF (days) B o d y w eight nadir IP 25 mg/kg 47 53 - 1.2% sc osm pump 144 µg/day 65 >100 - 4.9% sc osm pump 48 µg/day 41 71 - 8.0% NO CR or PR Source: Company data. ALL ANIMA L S IN 1 4 4µg SC HAD CR or PR • No clinically significant (>10%) weight loss Note: Sc osm: subcutaneous osmotic; CR: complete response; PR: partial response: TTE: time to endpoint; TTF: time to 100% failure

27 4.00 3.50 3.00 2.50 2.00 1.50 1.00 0.50 0.00 WBC (10 3/uL) NEUT (10 3/uL) PLT (10 6/uL) Mean 28 - day hematologic parameters: male mice (n=5/dose strength) 0 mcg /d ay 48 m cg/d a y 144 mcg/day 0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 WBC (10 3/uL) NEUT (10 3/uL) PLT (10 6/uL) Mean 28 - day hematologic parameters: female mice (n=5/dose strength) 0 mcg/day 48 mcg/day 144 mcg/day In Preclinical Studies, STAR - LLD Showed No Hem - Toxicity In Chronic Treatment - Preclinical Rodent Study 3 x No neutropenia x No reduction in platelets (thrombocytope nia) x No local infusion site toxicity STAR - LLD vs. sham Healthy CD20 mice Animals were split into 3 treatment groups, each group receiving a different drug dosage n=20 animals per dosage (10 males and 10 females); 5 per dose sacrificed on Day 8 (1) and 5 per dose sacrificed on Day 28 Study evaluated effect of chronic subcutaneous (SC) administration of continuous lenalidomide on tolerability, histopathology, and key hematologic parameters at 28 days of treatment > > > > > > Source: Company data. (1) Day 8 data is not shown here.

28 CD - 17 lenalidomide refractory: Preclinical Rodent Study 4 A Continuous Subcutaneous Infusion Improves Tumor Control (TTF) And Tumor Volume Versus Pulsatile Dosing In Lenalidomide - resistant Tumors STUDY RESULTS: • Continuous delivery of lenalidomide resulted in significant improvements (p<0.05) in the mean time to treatment failure (TTF) in the 216 mcg/day (42 days) and 288 mcg/day (43 days) groups compared to both vehicle and IP arms. • Mean TV at the end of the 27 day cycle ~40% greater in the vehicle and IP - treated animals (1096 and 1042 mm 3 ) compared to continuous doses of 144 mcg/day (742 mm 3 ), 216 mcg/day (707 mm 3 ), and 288 mcg/day (702 mm 3 ). (p<0.05). High - level Data Subject To Final Analysis And Quality Check • No significant difference in mean time to treatment failure (TTF) between vehicle and IP lenalidomide treated animals. CB.17 SCID mice RPMI - 8226 multiple myeloma xenograft model – lenalidomide - resistant human myeloma strain N=10 animals per group, 5 groups Route Active Dose Schedule IP 25 mg/kg 500 µg/day Once daily for 13 days / 1 day off / once daily for 13 days sc osm pump 144 µg/day Continuous for 13 days / 1 day off / continuous for 13 days sc osm pump 216 µg/day sc osm pump 288 µg/day sc osm pump vehicle Source: Company data.

29 STAR - LLD Positioned To Deliver Multiple Catalysts In Near - term Catalyst Timing S T A R - LLD SC subcutaneous Multiple myeloma (MM) Initiate Phase 1b Q2 2023 First patient dosed 2H 2023 6 - month safety/efficacy results 1H 2024 Initiate Phase 2/3 trial 2H 2024 Poten t ial FDA Approval 2027 Chronic lymphocyti c leukemia (CLL) Initiate Phase 2 2H 2024 Initiate Phase 3 2025 STAR - LLD TD transdermal Bridge to MM and CLL indications Select final transdermal formulation Q1 2024 IND filed 2024 Poten t ial FDA Approval 2027 STAR - LLD OBI on - body SC infusion Partnership with major OBI manufacturer announced 2H 2023 Poten t ial FDA Approval 2027 Source: Company files.

30 Significant Intellectual Property (IP) With Patent Protection Through 2040/41 + additional formulation and process patents in draft form • Starton owns global rights to full product portfolio • IP Protection through 2040/41 • Expect to expand IP with unexpected clinical findings • Starton IP strategy led by Roy Waldron, Ph.D., former Global VP of Intellectual Property at Pfizer and current Starton Board member No. Status Commentary US11197852 Granted on 12/14/2021 Continuous Delivery of Lenalidomide and Other Immunomodulatory Agents PCT/US2022/ 032090 PCT Publication Number WO2022 - 260940 17/518930 Continuation in Part Publication Number US2022 - 0054473 17/831603 Converted from Provisional Publication Number US2022 - 0395468 Transdermal Drug Delivery Systems for Administration of a Therapeutically Effective Amount of Lenalidomide and Other Immunomodulatory Agents 17/570463 Converted from Provisional Publication Number US2022 - 0218687 Stable Solution of Immunomodulatory Drugs (IMiD) for Parenteral Use US2022/0115 72 PCT Publication Number WO2022/150561 17/148262 Converted from Provisional Publication Number US2021 - 0244679 Treatment of Vomiting and Nausea with Minimum Dose of Olanzapine 18/246190 PCT Treatment of Vomiting and Nausea with Minimum Dose of Olanzapine US2022 - 0395468 Published Use of Olanzapine for Treatment of PARP - Inhibitor Induced Nausea 17/415279 Converted from Provisional Publication Number US2022 - 0040194 Use of Olanzapine for Treatment of PARP - Inhibitor Induced Nausea Source: Company files and U.S. Patent Office.

Potential Partners Can Benefit From Access to Starton’s Continuous Delivery Platform Continuous Delivery Technology platform can help establish new patent estates for existing blockbuster products, expanding their reach 31 Starton can create de - risked and capital efficient research & development programs, with smaller studies and shorter path to market Starton’s Continuous Delivery platform has been sufficiently developed so that new molecules can be developed on each of the SC, OBI, and TD technologies, providing easy access for partners

Enhanced Proprietary Delivery System Leveraging Proven Continuous Delivery Technology Across a Wide Range of Indications Blockbuster Potential With a Groundbreaking Approach to Treating Multiple Myeloma and Other Hematological - Malignancies Superior PK/PD Profile Versus the Current Standard - Of - Care, Leading to Improved Drug Tolerability and Superior Outcomes Significant Opportunity to Expand Total Addressable Market by Capturing Revlimid Intolerant Patients De - Risked Opportunity by Leveraging FDA - Approved Blockbuster Products With Proven Active Ingredients Strong Cadence of Upcoming Catalysts With Defined Pathway Into Clinic and Clear Path Forward to Potential Approval Substantial Expansion Opportunities With the Potential to Leverage the Existing Technology in Other Approved Blockbuster Molecules 1 2 3 4 5 6 7 Investment Highlights 32

Appendix 33

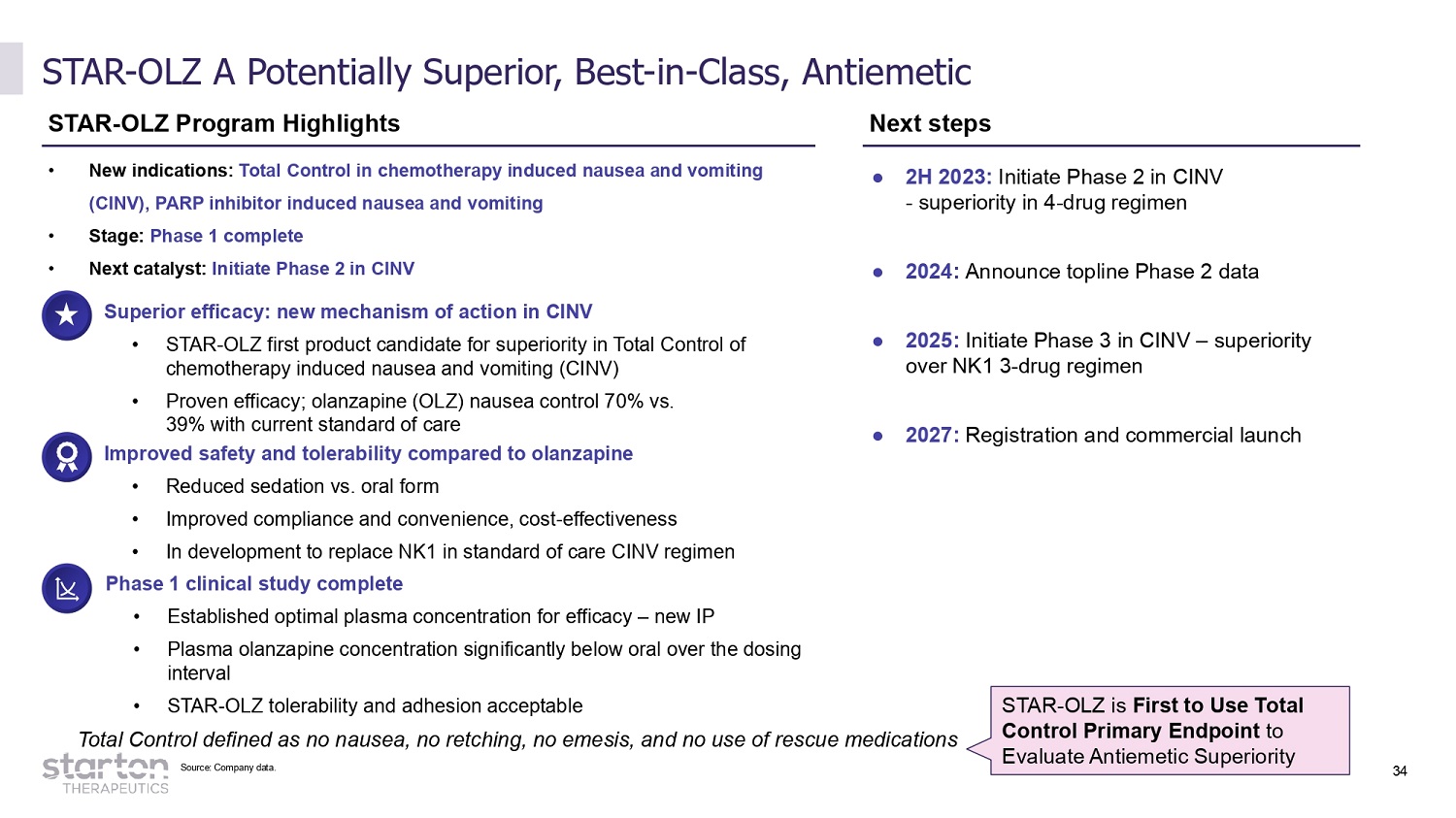

STAR - OLZ A Potentially Superior, Best - in - Class, Antiemetic STAR - OLZ Program Highlights Next steps Superior efficacy: new mechanism of action in CINV • STAR - OLZ first product candidate for superiority in Total Control of chemotherapy induced nausea and vomiting (CINV) • Proven efficacy; olanzapine (OLZ) nausea control 70% vs. 39% with current standard of care Improved safety and tolerability compared to olanzapine • Reduced sedation vs. oral form • Improved compliance and convenience, cost - effectiveness • In development to replace NK1 in standard of care CINV regimen Phase 1 clinical study complete • Established optimal plasma concentration for efficacy – new IP • Plasma olanzapine concentration significantly below oral over the dosing interval • STAR - OLZ tolerability and adhesion acceptable ● 2H 2023: Initiate Phase 2 in CINV - superiority in 4 - drug regimen ● 2024: Announce topline Phase 2 data ● 2025: Initiate Phase 3 in CINV – superiority over NK1 3 - drug regimen ● 2027: Registration and commercial launch • New indications: Total Control in chemotherapy induced nausea and vomiting (CINV), PARP inhibitor induced nausea and vomiting • Stage: Phase 1 complete • Next catalyst: Initiate Phase 2 in CINV Total Control defined as no nausea, no retching, no emesis, and no use of rescue medications STAR - OLZ is First to Use Total Control Primary Endpoint to Evaluate Antiemetic Superiority Source: Company data. 34

Phase 2: A prospective, randomized, placebo - controlled, double - blind, multicenter trial of STAR - OLZ TDS vs. Standard of Care for the prevention of nausea and vomiting STAR - OLZ Phase 2 Study in CINV Prophylaxis (TROPIC - I) 80 subjects 1 st cycle of chemo, randomized 1:1 by HEC regimen STAR - OLZ TD applied + Standard of care triple regimen (NK1 + 5HT3 + dexamethasone) Placebo TD applied + Standard of care triple regimen (NK1 + 5HT3 + dexamethasone) Day 1 Days 2 - 5 • 20 sites • US only • Fast 7 - month enrollment • 2 patch sizes (strengths) PRIMARY OBJEC T IVE: Superiority of STAR - OLZ - based antiemetic regimen in Total Control vs aprepitant - based antiemetic regimen + Dose - finding for Phase 3 study Wear STAR - OLZ day 2 - 5 + Standard delayed stage prophylaxis (NK1 + dexamethasone) Wear Placebo TD day 2 - 5 + Standard delayed stage prophylaxis (NK1 + dexamethasone) HEC stratification 1:1 AC regimens / non - AC regimens. N=80 patients Phase 2 N=235 patients Phase 3 Phase 3 regimen removes NK1 4 CYCLES HEC: highly emetogenic chemotherapy PO: oral TDS: transdermal delivery system AC: Adriamycin - cyclophosphamide Source: Company data. 35

36 STAR - OLZ In CINV Patients per year, US only, 2026 Competitive Pricing in US Chemotherapy patients in United States, 2020 960,000 Average chemotherapy cycles per patient per year 6 STAR - OLZ price: $40 - 70 / patch vs. NK1 price of $100 STAR - OLZ offers meaningful price reduction in a price - sensitive treatment setting Haisco Pharmaceutical Group (China) ▪ Exclusive License to STAR - OLZ in Mainland China ▪ Starton to receive upfront , development milestones , and high single - digit to low double - digit royalties ▪ Starton retains rights ROW Partnership in Asian Market Note: ROW: rest of world Sources: Company forecast, DRG, SEER

Starton is subject to numerous risks factors, including but not limited to the following: • Risks Related to Starton’s Business – Starton is a clinical stage biotechnology company with a limited operating history – Starton expends a significant amount of resources on research and development, which may not lead to successful product introductions – Starton has historically operated subject to a going concern qualification in its financial statements – Starton may incur operating losses in the future – Failures of or delays in clinical trials could result in increased costs to Starton and could prevent or delay Starton’s ability to obtain regulatory approval and commence product sales for new products. Starton may also find it difficult to enroll patients in its clinical trials, which could delay or prevent development of its product candidates – The testing required for the regulatory approval of Starton’s products is conducted primarily by independent third parties and any failure by any of these third parties to perform this testing properly and in a timely manner may have an adverse effect upon Starton’s ability to obtain regulatory approvals – Starton’s products or product candidates may cause adverse effects or have other properties that could delay or prevent their regulatory approval or limit the scope of any approved package insert or market acceptance, or result in significant negative consequences following marketing approval – If Starton’s products or product candidates do not produce the effects intended or if they cause undesirable side effects, its business may suffer – Starton’s branded pharmaceutical expenditures may not result in commercially successful products – Starton is subject to extensive governmental regulation and faces significant uncertainties and potentially significant costs associated with its efforts to comply with applicable regulations – The drug regulatory approval processes of the FDA and comparable foreign authorities are lengthy, time consuming and inherently unpredictable • Risks Related to Development, Clinical Testing, Manufacturing, and Regulatory Approval – Starton faces risks related to health epidemics and outbreaks, including the COVID - 19 pandemic, which could significantly disrupt its preclinical studies and clinical trials, and therefore its receipt of necessary regulatory approvals could be delayed or prevented – Results of preclinical studies, early clinical trials, or analyses may not be indicative of results obtained in later trials – The market opportunities for STAR - LLD and STAR - OLZ may be smaller than Starton anticipates – Potential product liability lawsuits against Starton could cause it to incur substantial liabilities and limit commercialization of any products that it may develop 37 Starton Selected Risk Factors

• Risks Related to Commercialization – The successful commercialization of STAR - LLD, STAR - OLZ, and/or any other product candidate Starton may develop will depend in part on the extent to which governmental authorities and health insurers establish adequate coverage, reimbursement levels, and pricing policies. Failure to obtain or maintain coverage and adequate reimbursement for Starton’s product candidates, if approved, could limit its ability to market those products and decrease its ability to generate revenue – Even if STAR - LLD, STAR - OLZ, and/or any product candidate Starton may develop receives marketing approval, it may fail to achieve market acceptance by physicians, patients, third - party payors or others in the medical community necessary for commercial success – If Starton is unable to establish sales, marketing, and distribution capabilities either on its own or in collaboration with third parties, it may not be successful in commercializing STAR - LLD and/or STAR - OLZ • Risks Related to Healthcare Laws and Other Legal Compliance Matters, including the following: – Enacted and future healthcare legislation may increase the difficulty and cost for Starton to obtain marketing approval of and commercialize its product candidates, if approved, and may affect the prices it may set – Starton’s business operations and current and future relationships with investigators, healthcare professionals, consultants, third - party payors, patient organizations, and customers will be subject to applicable healthcare regulatory laws, which could expose Starton to penalties – Environmental, health and safety laws and regulations may cause Starton to incur substantial costs or subject it to potential liabilities • Risks Related to Starton’s Intellectual Property – Starton depends on its ability to protect its intellectual property and proprietary rights. Starton may not be able to keep its intellectual property and proprietary rights confidential and protect such rights – If Starton is unable to obtain and maintain patent protection for its technology, products, and product candidates or if the scope of the patent protection obtained is not sufficiently broad, Starton may not be able to compete effectively in its markets – Starton may become subject to third parties’ claims alleging infringement of their patents and proprietary rights, or Starton may need to become involved in lawsuits to protect or enforce its patents – Starton’s business may be materially harmed if it does not obtain patent term extension in the U.S. under the Hatch - Waxman Act and in foreign countries under similar legislation • Those other factors discussed in Healthwell’s filings with the SEC and that will be contained in Pubco’s registration statement relating to the business combination 38 Starton Selected Risk Factors (Cont’d.)

Healthwell is subject to numerous risks, including but not limited to the following: • The risk that the business combination may not be completed in a timely manner or at all, which may adversely affect the price of Healthwell’s securities • The risk that the business combination may not be completed by Healthwell’s business combination deadline and the potential failure to obtain an extension of the business combination deadline if sought by Healthwell • The failure to satisfy the conditions to the consummation of the business combination, including the approval of the business combination agreement by the stockholders of Healthwell • The occurrence of any event, change or other circumstance that could give rise to the termination of the business combination agreement • The ability to maintain the listing of Healthwell’s securities on a national securities exchange • The risk that Pubco may not be able to raise funds in a PIPE financing or may not be able to raise as much as anticipated • Costs related to the business combination and the failure to realize anticipated benefits of the business combination or to realize underlying assumptions, including with respect to estimated stockholder redemptions • Healthwell is not required to obtain and has not obtained a fairness opinion from an independent third party in connection with the Proposed Transaction • Those factors discussed in Healthwell’s filings with the SEC and that will be contained in Pubco’s registration statement relating to the business combination 39 Healthwell Selected Risk Factors