MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

As of June 30, 2024, and for the six-month period then ended

Special note regarding forward-looking statements

Certain information included herein may be deemed to be “forward-looking statements”. Forward-looking statements are often characterized by the use of forward-looking terminology such as “may,” “might,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “seek,” “believe,” “estimate,” “predict,” “potential,” “continue,” “contemplate,” “possible,” “project,” or the negative of these terms or similar expressions, but are not the only way these statements are identified.

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. Forward-looking statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements, including, but not limited to:

| • | our limited operating history at our current scale; |

| • | our ability to effectively manage the scope and complexity of our business following years of rapid growth and our ability to maintain profitability; |

| • | foreign currency exchange rate fluctuations; |

| • | the fact that we continue to derive a majority of revenues from a single platform; |

| • | fluctuations in operating results; |

| • | real or perceived errors, failures, vulnerabilities or bugs or interruptions or performance problems in the technology or infrastructure underlying our platform; |

| • | risks related to artificial intelligence (“AI”) or machine learning (“ML”) in offerings; |

| • | our ability to attract customers, grow our retention rates and expand usage within organizations, including cross selling and upselling; |

| • | risks related to our subscription-based business model; |

| • | our sales efforts may require considerable time and expense or may extend sales cycles, and downturns or upturns are not immediately reflected in full in results of operations; |

| • | our ability to offer high-quality customer support and consistent sales strategies; |

| • | our ability to enhance our reputation, brand, and market awareness of our products and maintenance of corporate culture; |

| • | risks related to actions by governments to restrict access to our platform and products or to require us to disclose or provide access to our platform and products or to require us to disclose or provide access to information; |

| • | risks related to international operations and compliance with laws and regulations applicable to our global operations; |

| • | difficulties in integration of partnerships, acquisitions and alliances; |

| • | risks associated with environmental and social responsibility and climate change; |

| • | our dependence on key employees and ability to attract and retain highly skilled employees; |

| • | our ability to raise additional capital or generate cash flows necessary to grow our business; |

| • | uncertain global economic conditions and inflation; |

| • | changes and competition in the market and software categories in which we participate; |

| • | our ability to maintain adequate research and development resources and introduce new products, features, integrations, capabilities, and enhancements; |

| • | the ability of our platform to interoperate with a variety of software applications; |

| • | our reliance on third-party application stores to distribute our mobile application; |

| • | our successful strategic relationships with, and our dependence on third parties; |

| • | our reliance on traditional web search engines to direct traffic to our website; |

| • | interruption or delays in service from third parties or our inability to plan and manage interruptions; |

| • | risks related to security disruptions, unauthorized system access; |

| • | evolving privacy protection and data security laws, regulations, industry standards, policies, contractual obligations, and cross-border data transfer or localization restrictions; |

| • | new legislation and regulatory obligations regulating AI; |

| • | changes in tax law and regulations or if we were to be classified as a passive foreign investment company; |

| • | our ability to maintain, protect or enforce our intellectual property rights or risks related to claims that we infringe the intellectual property rights of others; |

| • | risks related to our use of open-source software; |

| • | risks related to our founder shares that provide certain veto rights |

| • | risks related to our status as a foreign private issuer incorporated and located in Israel, including risks related to the ongoing war between Israel and Hamas and escalations thereof; |

| • | our expectation not to pay dividends for the foreseeable future; |

| • | the novelty of our Digital Lift Initiative, and |

| • | risks related to legal and regulatory matters; |

You should not rely upon forward-looking statements as predictions of future events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that future results, levels of activity, performance and events and circumstances reflected in the forward-looking statements will be achieved or will occur. The estimates and forward-looking statements contained in this report speak only as of the date of this report. Except as required by applicable law, we undertake no obligation to publicly update or revise any estimates or forward-looking statements whether as a result of new information, future events or otherwise, or to reflect the occurrence of unanticipated events.

The foregoing list is intended to identify only certain of the principal factors that could cause actual results to differ. For a more detailed description of the risks and uncertainties affecting our company, reference is made to our Annual Report on Form 20-F for the year ended December 31, 2023, which was filed with the Securities and Exchange Commission, or the SEC, on March 14, 2024 (hereafter: “Annual Report”), and the other risk factors discussed from time to time by our company in reports filed or furnished to the SEC.

Unless indicated otherwise by the context, all references in this report to “monday.com,” “we,” “us,” or “our” are to monday.com Ltd. When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below:

| • | “dollars” or “$” means United States dollars; and |

| • | “NIS” means New Israeli Shekels. |

You should read the following discussion and analysis in conjunction with our unaudited condensed consolidated financial statements for the six months ended June 30, 2024 and notes thereto, and together with our audited consolidated financial statements for the year ended December 31, 2023 and notes thereto filed with the SEC as part of our Annual Report.

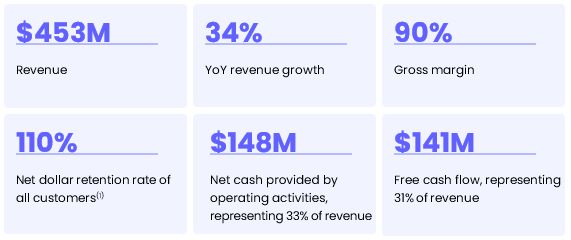

monday.com H1-24 overview in numbers

(1) For a definition of Net Dollar Retention Rate see “Key Business Metrics” below.

Hyper-growth at scale

We have experienced rapid growth since we launched our product in 2014.

| • | Revenue: Our revenue was $453.0 million and $337.9 million for the six months ended June 30, 2024, and June 30, 2023, respectively. |

| • | Year over Year Revenue Growth: An increase of 34% and 46% for the six months ended June 30, 2024, and June 30, 2023, respectively. |

| • | Net Income (loss): Our net income (loss) was $21.4 million and $(21.7) million, for the six months ended June 30, 2024, and June 30, 2023, respectively. |

| • | Net Cash Provided by Operating Activities: Our net cash provided by operating activities was $147.7 million and $90.3 million for the six months ended June 30, 2024, and June 30, 2023, respectively. |

| • | Free Cash Flow: Our free cash flow was $140.7 million, and $84.6 million for the six months ended June 30, 2024, and June 30, 2023, respectively. |

Key Business Metrics

We believe that our growth and financial performance are dependent upon many factors, including the key factors described below.

A Large and Diversified Customer Base

We are focused on expanding within our existing customers by increasing the number of users within the organization, upgrading to higher tiers and by offering additional products. Our operating results and growth opportunities depend, in part, on our ability to attract new customers and expand relationships with existing customers. We believe we have significant greenfield opportunities among addressable customers worldwide and we will continue to invest in our research and development to differentiate our platform from competitive products and services. We will also continue to invest in our sales and marketing to help us take advantage of this opportunity. To this extent, we are making significant investments in our sales and marketing efforts, including investment and expansion of our CRO teams.

We define “customer” to mean a unique web domain-based account that is on a paid subscription plan, which could include an organization, educational or government institution, or distinct business unit of an organization. We are not reliant on any specific customer, as no single customer accounts for more than 1% of our revenues, and our top 100 customers accounted for less than 10% of our revenues for the six months ended June 30, 2024, and 2023.

We see a significant opportunity to continue to add customers as we further develop our sales and marketing efforts and scale our platform, as well as add new products.

Consistent Growth of Enterprise Customers

Our ability to successfully move upmarket is demonstrated by the consistent growth in the number of our enterprise customers. We grew the number of enterprise customers, which we define as customers with more than $50,000 in Annual Recurring Revenue (“ARR”) (defined below), on our platform by 43% from 1,892 customers as of June 30, 2023, to 2,713 customers as of June 30, 2024. The ARR from such enterprise customers grew by 51% from June 30, 2023, to June 30, 2024, outpacing our overall ARR growth.

Customers with more than $100,000 in ARR grew by 49% during the 12 months ending on June 30, 2024, from 677 customers as of June 30, 2023, to 1,009 customers as of June 30, 2024. The ARR from such enterprise customers grew by 57% from June 30, 2023, to June 30, 2024.

Strong base of Customers with more than 10 users

We distinguish customers with more than 10 users from our broader customer base. The ARR from customers with more than 10 users, which include enterprise and non-enterprise customers, has outpaced the rest of the business in each of our previous years. As of June 30, 2024, and June 30, 2023, our customers with more than 10 users accounted for 78% and 77% of our ARR, respectively. “Annual Recurring Revenue” or “ARR” is defined to mean, as of the measurement date, the annualized value of our customer subscriptions plan assuming that any contract that expires during the next 12 months is renewed on its existing terms.

We believe ARR illustrate the improvements we have made to our platform to increase the value we deliver to our customers over time. We expect the percentage of ARR attributable to customers with more than 10 users to remain at similar levels.

Net Dollar Retention Rate

We expect to derive a significant portion of our revenue growth from expansion within our customer base, where we have an opportunity to expand adoption of the Work OS products across teams, departments, and organizations. We believe that our dollar-based net retention rate (“Net Dollar Retention Rate”) demonstrates our opportunity to further expand within our customer base, particularly those that generate higher levels of annual revenues.

We calculate Net Dollar Retention Rate as of a period end by starting with the ARR from customers as of the 12 months prior to such period end (“Prior Period ARR”). We then calculate the ARR from these customers as of the current period end (“Current Period ARR”). The calculation of Current Period ARR includes any upsells, contraction and attrition. We then divide the total Current Period ARR by the total Prior Period ARR to arrive at the Net Dollar Retention Rate. For the trailing 12-month calculation, we take a weighted average of this calculation of our quarterly Net Dollar Retention Rate for the four quarters ending with the most recent quarter. Our Net Dollar Retention Rate may fluctuate due to a number of factors, including the level of penetration within our customer base, expansion of products and features and our ability to retain our customers.

Our Net Dollar Retention Rate for all customers was 110% for the three months ended June 30, 2024, and 114% for the three months ended June 30, 2023. We believe that the slight slowdown in Net Dollar Retention Rate is related to a slowdown in expansion of existing customers. We see a very healthy traffic of new customers; however, macroeconomic factors are leading to slower expansion in some existing customers. We currently anticipate that overall Net Dollar Retention to remain stable throughout 2024 and start to improve at the end of the year. NDR Additionally, our Net Dollar Retention rate for customers with more than 10 users was 114% for the three months ended June 30, 2024, and 120% for the three months ended June 30, 2023.

A. Operating Results

Components of Results of Operations

The following briefly describes the components of revenue and expenses as presented in our consolidated statements of operations.

Revenue

We derive revenue mainly from monthly or annual subscription agreements with our customers for access to our cloud-based Work OS platform. Our customers do not have the ability to take possession of our software.

Cost of Revenue

Cost of revenue consists of merchant and credit card processing fees, hosting fees, amortization of capitalized software development costs, subcontractor costs, salaries and related expenses, share-based compensation, software license fees, and allocated overhead costs.

Gross Profit and Gross Margin

Gross profit, or revenue less cost of revenues, and gross margin, or gross profit as a percentage of revenue, has been, and will continue to be, affected by various factors, including the timing of our acquisition of new customers, renewals of and follow-on sales to existing customers, costs associated with operating our cloud-based platform, and the extent to which we expand our operations and customer support organizations. We expect our gross margin to remain relatively consistent over the long term.

Operating Expenses

Our operating expenses consist of research and development, sales and marketing, and general and administrative expenses. Sales and marketing expenses are the most significant component of our operating expenses and consist of marketing and advertising expenses and commission paid to our partners. In addition, personnel-related expenses are a substantial component of our operating expenses and consist of salaries, benefits, and share-based compensation expenses. Operating expenses also include an allocation of overhead costs for facilities and shared IT-related expenses, including depreciation expenses.

Research and Development Expenses

Research and development expenses include salaries and related expenses, share-based compensation, subcontractor costs and allocated overhead costs.

As we continue to focus our research and development efforts on enhancing our Work OS and existing products, as well as building new products, we expect our research and development expenses to increase in absolute dollar amounts and remain at the same level as a percentage of revenue. We foresee that such investment in research and development will contribute to our long-term growth but will also negatively impact our short-term profitability.

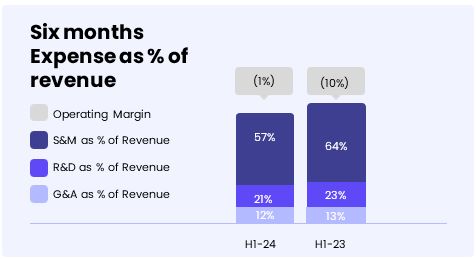

For the six months ended June 30, 2024, and June 30, 2023, our research and development expenses as a percentage of revenue were approximately 21% and 23%, respectively.

Sales and Marketing Expenses

Sales and marketing expenses consist primarily of compensation expenses for our employees, including share-based compensation, online and offline marketing and advertising expenses, channel partners’ commissions and allocated overhead costs.

Our channel partners' commissions as a percentage of revenue were approximately 5% for each of the six months ended June 30, 2024, and June 30, 2023. For the six months ended June 30, 2024, and June 30, 2023, our sales and marketing expenses as a percentage of revenue were approximately 57% and 64%, respectively.

We expect our sales and marketing expenses will increase in absolute dollar amounts, as we plan to expand our sales and marketing efforts globally, through personnel, online and offline marketing efforts and brand awareness. In the long term, as our business scales through customer expansion and market awareness, we anticipate that sales and marketing expenses as a percentage of total revenue will continue to decline.

General and Administrative Expenses

General and administrative expenses consist of salaries and related expenses, share-based compensation, professional service fees and allocated overhead costs.

We expect our general and administrative expenses to increase in absolute dollars as we continue to grow and expand our operations and operate as a public company. In the long term, we expect that general and administrative expenses as a percent of total revenue will remain at approximately the same level. For the six months ended June 30, 2024, and June 30, 2023, our general and administrative expenses as a percentage of revenue were approximately 12% and 13%, respectively.

Financial Income (Expense), Net

Financial income (expense), net, consists primarily of interest generated by our money market funds and foreign exchange gains and losses, offset by bank charges and interest expenses.

Income Tax Expenses

Income tax expenses consist primarily of income tax related to foreign jurisdictions in which we conduct business. We maintain a full valuation allowance on deferred tax assets because we have concluded that it is not more likely than not that the deferred tax assets will be realized.

Comparison of Period-to-Period Results of Operations

The following tables set forth the consolidated statements of operations in U.S. dollars and as a percentage of revenue for the period presented.

| | | Six months ended June 30, | |

| | | 2024 | | | 2023 | |

| | | (in thousands) | |

| | $ | 453,019 | | | $ | 337,935 | |

Cost of revenue (1) | | | 47,217 | | | | 36,530 | |

| Gross profit | | | 405,802 | | | | 301,405 | |

| Operating Expenses: | | | | | | | | |

Research and development (1) | | | 94,868 | | | | 76,169 | |

Sales and marketing (1) | | | 259,612 | | | | 215,123 | |

General and administrative (1) | | | 54,550 | | | | 45,032 | |

| Total operating expenses | | | 409,030 | | | | 336,324 | |

| Operating loss | | | (3,228 | ) | | | (34,919 | ) |

| Financial income (expense), net | | | 27,689 | | | | 17,495 | |

| Income (loss) before income taxes | | | 24,461 | | | | (17,424 | ) |

| Income tax expenses | | | (3,068 | ) | | | (4,278 | ) |

| Net income (loss) | | $ | 21,393 | | | $ | (21,702 | ) |

(1) Includes share-based compensation expense as follows:

| | | Six months ended June 30, | |

| | | 2024 | | | 2023 | |

| | | (in thousands) | |

| Cost of revenue | | $ | 3,116 | | | $ | 3,322 | |

| Research and development | | | 23,193 | | | | 19,742 | |

| Sales and marketing | | | 18,068 | | | | 13,640 | |

| General and administrative | | | 18,789 | | | | 14,539 | |

| Total share-based compensation | | $ | 63,166 | | | $ | 51,243 | |

| | | Six months ended June 30, | |

| | | 2024 | | | 2023 | |

| Revenue | | | 100 | % | | | 100 | % |

| Cost of revenue | | | 10 | | | | 11 | |

| Gross profit | | | 90 | | | | 89 | |

| Operating Expenses: | | | | | | | | |

| Research and development | | | 21 | | | | 23 | |

| Sales and marketing | | | 57 | | | | 64 | |

| General and administrative | | | 12 | | | | 13 | |

| Total operating expenses | | | 90 | | | | 100 | |

| Operating loss | | | (1 | ) | | | (10 | ) |

| Financial income (expense), net | | | 6 | | | | 5 | |

| Income (loss) before income taxes | | | 5 | | | | (5 | ) |

| Income tax expenses | | | (1 | ) | | | (1 | ) |

| Net income (loss) | | | 5 | % | | | (6 | )% |

Comparison of the Six Months Ended June 30, 2024 and 2023

Revenue

| | | Six months ended June 30, | | | | | | | |

| | | 2024 | | | 2023 | | | $ Change | | | % Change | |

| | | (in thousands) | | | | | | | |

| Revenues | | $ | 453,019 | | | $ | 337,935 | | | $ | 115,084 | | | | 34 | % |

Revenue was $453.0 million for the six months ended June 30, 2024, an increase of $115.1 million, or 34%, compared to $337.9 million for the six months ended June 30, 2023. This increase was driven primarily by the addition of new customers and revenues generated from our existing customers expanding their use of our products, as reflected by our dollar-based net retention rate of 110% as of June 30, 2024.

Cost of Revenue and Gross Profit

|

| Six months ended June 30, |

|

|

|

|

|

|

|

| |

|

|

| 2024 |

|

|

| 2023 |

|

|

| $ Change |

|

|

| % Change | |

| | | | (in thousands) | | | | | | | | | |

| Cost of revenue | | $ | 47,217 | | | $ | 36,530$ | | | | 10,687 | | | | 29 | % |

| Gross profit | | | 90 | % | | | 89 | % | | | | | | | | |

Cost of revenue was $47.2 million for the six months ended June 30, 2024, an increase of $10.7 million, or 29%, compared to $36.5 million for the six months ended June 30, 2023. This increase is directly related to the growth and scale of our business and was primarily driven by an increase of $4.7 million in hosting expenses, an increase of $1.9 million in processing fees, an increase of $1.5 million in third-party consulting costs, an increase of $1.2 million in salaries and related expenses, an increase of $0.9 million in indirect taxes, an increase of $0.7 million in amortization of capitalized software costs, and an increase in allocated overhead costs of $0.5 million as a result of increased overall costs to support our business growth and related infrastructure, partially offset by a decrease of $0.2 million in share-based compensation expenses.

Operating Expenses

| | | Six months ended June 30, | | | | | | | |

| | | 2024 | | | 2023 | | | Change | | | % | |

| | | (in thousands) | | | | | | | |

| Research and development | | $ | 94,868 | | | $ | 76,169 | | | $ | 18,699 | | | | 25 | % |

| Sales and marketing | | | 259,612 | | | | 215,123 | | | | 44,489 | | | | 21 | % |

| General and administrative | | | 54,550 | | | | 45,032 | | | | 9,518 | | | | 21 | % |

| Total operating expenses | | $ | 409,030 | | | $ | 336,324 | | | $ | 72,706 | | | | 22 | % |

Research and Development Expenses

Research and development expenses were $94.9 million for the six months ended June 30, 2024, an increase of $18.7 million, or 25%, compared to $76.2 million for the six months ended June 30, 2023. This increase is directly related to the growth and scale of our business and was primarily driven by an increase of $9.5 million in salaries and related expenses, and of $3.5 million in share-based compensation expenses due to an increase in the number of employees, a $1.7 million increase in hosting costs, an increase of $1.7 million in allocated overhead costs as a result of increased overall costs to support our business growth and related infrastructure, an increase of $0.7 million in software costs, and an increase of $0.6 million in third-party consulting costs.

Sales and Marketing Expenses

Sales and marketing expenses were $259.6 million for the six months ended June 30, 2024, an increase of $44.5 million, or 21%, compared to $215.1 million for the six months ended June 30, 2023. This increase is directly related to the growth and scale of our business and was primarily driven by an increase of $17.1 million in salaries and related expenses and of $4.4 million in share-based compensation expenses due to an increase in the number of employees, an increase of $7.0 million in marketing, advertising and brand costs, an increase of $6.7 million in partners commission expenses, an increase of $3.1 million in allocated overhead costs to support our business growth and related infrastructure, an increase of $1.2 million in recruitment expenses, an increase of $1.1 million in travel expenses, and an increase of $1.0 million in courses and conferences expenses.

General and Administrative Expenses

General and administrative expenses were $54.6 million for the six months ended June 30, 2024, an increase of $9.5 million, or 21%, compared to $45.0 million for the six months ended June 30, 2023. This increase is directly related to the growth and scale of our business and was primarily driven by an increase of $4.3 million in share-based compensation expenses and of $3.5 million in salaries and related expenses due to an increase in the number of employees, an increase of $3.6 million in welfare, an increase of $1.3 million in rent and related expenses, mainly due to our global office expansion, an increase of $0.6 million in depreciation, an increase of $0.5 million in software expenses, and an increase of $0.5 million in donation expenses, partially offset by a decrease of $6.3 million in overhead allocation.

Financial Income (Expense), Net

| | | Six months ended June 30, | | | | | | | |

| | | 2024 | | | 2023 | | | $ Change | | | % Change | |

| | | (in thousands) | | | | | | | |

| Financial income (expense), net | | $ | 27,689 | | | $ | 17,495 | | | $ | 10,194 | | | | 58 | % |

Financial income (expense), net, was an income of $27.7 million for the six months ended June 30, 2024, an increase of $10.2 million or 58%, compared to income of $17.5 million for the six months ended June 30, 2023. This increase was partially driven by global macroeconomic trends, such as higher interest on our money market funds of $12.5 million, partially offset by foreign currency losses.

| | | Six months ended June 30, | | | | | | | |

| | | 2024 | | | 2023 | | | $ Change | | | % Change | |

| | | (in thousands) | | | | | | | |

| Income Tax Expenses | | $ | 3,068 | | | $ | 4,278 | | | $ | (1,210 | ) | | | (28 | )% |

Income tax expenses were $3.1 million for the six months ended June 30, 2024, a decrease of $1.2 million, or 28%, compared to $4.3 million for the six months ended June 30, 2023. The decrease was primarily driven by tax benefits related to share-based compensation.

Non-GAAP Financial Measures

We regularly review several financial measures, including non-GAAP operating income (loss) and adjusted free cash flow, to evaluate our business, measure our performance, identify trends in our business, prepare financial forecasts and make strategic decisions. We believe these non-GAAP financial measures are useful in evaluating our performance in addition to our financial results prepared in accordance with GAAP. You should read these non-GAAP measures in conjunction with our unaudited condensed consolidated financial statements for the six months ended June 30, 2024, and notes thereto, and together with our audited consolidated financial statements for the year ended December 31, 2023, included in our Annual Report.

Non-GAAP financial measures have limitations as analytical tools and should not be considered in isolation or as substitutes for financial information presented under GAAP. For example, other companies in our industry may calculate these non-GAAP financial measures differently or may use other measures to evaluate their performance. Investors are encouraged to review the reconciliations of these non-GAAP financial measures to their most directly comparable GAAP financial measures and to not rely on any single financial measure to evaluate our business.

The following table sets forth our non-GAAP operating income and free cash flow for the six months ended June 30, 2024, and June 30, 2023:

| | | Six months ended June 30, | |

| | | 2024 | | | 2023 | |

| | | (in thousands) | |

| Non-GAAP operating income | | $ | 59,938 | | | $ | 16,324 | |

| Free cash flow | | $ | 140,715 | | | $ | 84,614 | |

Non-GAAP Operating income

We define non-GAAP operating income as GAAP operating loss, adjusted for certain non-cash items, such as share-based compensation expenses. We exclude these items because these are non-cash expenses, which we do not consider indicative of performance. In addition, management uses non-GAAP operating income to evaluate our financial performance and for planning and forecasting purposes. Non-GAAP operating income should not be considered as an alternative to GAAP operating loss or net income (loss) as an indicator of operating performance. The following table provides a reconciliation of non-GAAP operating income to GAAP operating loss for the periods indicated:

| | | Six months ended June 30, | |

| | | 2024 | | | 2023 | |

| | | (in thousands) | |

| Operating loss | | $ | (3,228 | ) | | $ | (34,919 | ) |

| Share-based compensation expenses | | | 63,166 | | | | 51,243 | |

| Non-GAAP operating income | | $ | 59,938 | | | $ | 16,324 | |

Free Cash Flow

We define free cash flow as net cash provided by operating activities less cash used for purchases of property and equipment and capitalized software development costs.

We believe that free cash flow is a useful indicator of liquidity that provides information to management and investors, even if negative, about the amount of cash used in our operations and for investments in property and equipment and capitalized software development costs. However, we caution that free cash flow does not reflect our future contractual commitments and the total increase or decrease of our cash balance for a given period.

The following table provides a reconciliation of free cash flow to net cash provided by operating activities for the periods indicated:

| | | Six months ended June 30, | |

| | | 2024 | | | 2023 | |

| | | (in thousands) | |

| Net cash provided by operating activities | | $ | 147,749 | | | $ | 90,317 | |

| Purchase of property and equipment | | | (5,964 | ) | | | (4,684 | ) |

| Capitalized software development costs | | | (1,070 | ) | | | (1,019 | ) |

| Free cash flow | | $ | 140,715 | | | $ | 84,614 | |

B. Liquidity and Capital Resources

As of June 30, 2024, we had $1,290.2 million in cash and cash equivalents. In the six months ended June 30, 2024, we generated net cash provided by operating activities, and we have also generated net cash provided by operating activities each year since our initial public offering in June 2021.

Excluding capital raises, our principal sources of funds are from our deferred revenue, which is included in the liabilities section of our consolidated balance sheet. Deferred revenue consists of payments received in advance of revenue recognition, excluding amounts subject to right of return, and is recognized as revenue recognition criteria are met. We generally invoice our customers in advance of services being provided. The majority of our deferred revenue is expected to be recognized as revenue during the succeeding 12-month period, provided all other revenue recognition criteria have been met. As of June 30, 2024, and December 31, 2023, we had deferred revenue of $319.7 million and $269.5 million, respectively. We have generated losses from our operations as reflected in our accumulated deficit of $563.0 million and $584.4 million as of June 30, 2024, and December 31, 2023, respectively. Our future capital requirements will depend on many factors, including revenue growth and costs incurred to support customer usage and growth in our customer base, increased research and development expenses to support the growth of our business and related infrastructure, and general and administrative expenses to support being a publicly traded company.

We assess our liquidity primarily through our cash on hand as well as the projected timing of billings under contract with our paying customers and related collection cycles. We believe that our current cash and cash equivalents will be sufficient to meet our working capital and capital expenditure requirements for at least the next 12 months and for the foreseeable future.

Cash Flows

The following table presents the summary consolidated cash flow information for the periods presented:

| | | Six months ended June 30, | |

| | | 2024 | | | 2023 | |

| | | (in thousands) | |

| Net cash provided by operating activities | | $ | 147,749 | | | $ | 90,317 | |

| Net cash used in investing activities | | $ | (7,034 | ) | | $ | (5,703 | ) |

| Net cash provided by financing activities | | $ | 33,399 | | | $ | 18,869 | |

Operating Activities

Cash provided by operating activities for the six months ended June 30, 2024, of $147.7 million was primarily related to our net income of $21.4 million, adjusted for non-cash charges of $68.6 million and net cash inflows of $57.7 million resulting from changes in our operating assets and liabilities. Non-cash charges primarily consisted of share-based compensation and depreciation and amortization of property and equipment. The main drivers of the changes in operating assets and liabilities were a $50.2 million increase in deferred revenue, resulting primarily from increased billings for subscriptions, a $2.7 million increase in accrued expenses and other liabilities, and a $21.7 million increase in accounts payable primarily driven by payments timing differences. These amounts were partially offset by a $15.2 million increase in prepaid expenses and other assets and a $1.7 million increase in accounts receivables, net.

Cash provided by operating activities for the six months ended June 30, 2023, of $90.3 million was primarily due to our net loss of $21.7 million, adjusted for non-cash charges of $55.4 million and net cash inflows of $56.6 million resulting from changes in our operating assets and liabilities. Non-cash charges primarily consisted of share-based compensation and depreciation and amortization of property and equipment. The main drivers of the changes in operating assets and liabilities were a $49.1 million increase in deferred revenue, resulting primarily from increased billings for subscriptions, a $6.0 decrease in prepaid expenses and other assets, and a $3.6 million increase in accounts payable primarily, both of which are driven by payments timing differences. These amounts were partially offset by a $1.9 million increase in accounts receivables, net, and a $0.2 million decrease in accrued expenses and other liabilities.

Investing Activities

Cash used in investing activities during the six months ended June 30, 2024, was $7.0 million, as a result of purchases of property and equipment and capitalized software development costs.

Cash used in investing activities during the six months ended June 30, 2023, was $5.7 million, as a result of purchases of property and equipment and capitalized software development costs.

Cash provided by financing activities for the six months ended June 30, 2024, was $33.4 million and was primarily as a result of proceeds of $19.3 million from exercise of share options and purchases under the employee share purchase plan and a receipt of tax advance in the amount of $14.1 million relating to exercises of share options and RSUs, net.

Cash provided by financing activities for the six months ended June 30, 2023, was $18.9 million and was primarily as a result of proceeds of $10.4 million from exercise of share options and purchases under the employee share purchase plan and a receipt of tax advance in the amount of $8.5 million relating to exercises of share options and RSUs, net.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements, as defined by applicable regulations of the SEC, that are reasonably likely to have a current or future material effect on our financial condition, results of operations, liquidity, capital expenditures or capital resources.

C. Research and development, patents and licenses, etc.

A comprehensive discussion of our research and development, patents and licenses, etc., is included in “Part 1 - Who We Are” and “Part 4 - Operating and Financial Review and Prospects - Operating Results” sections in our Annual Report.

D. Trend information

Other than as disclosed above and in our Annual Report, we are not aware of any trends, uncertainties, demands, commitments or events since June 30, 2024, that are reasonably likely to have a material adverse effect on our net revenue, income, profitability, liquidity or capital resources, or that caused the disclosed financial information to be not necessarily indicative of future operating results or financial condition.

E. Critical Accounting Estimates

We describe our significant accounting policies more fully in Note 2 to our unaudited condensed consolidated financial statements for the six months ended June 30, 2024. There have been no material changes to our critical accounting policies since we filed our Annual Report other than as described in Note 2 to our unaudited condensed consolidated financial statements for the six months ended June 30, 2024. Please see “Part 4. Operating and Financial Review and Prospects – E. Critical Accounting Estimates” section in our Annual Report.

F. Quantitative and Qualitative Disclosures About Market Risk

We are exposed to market risk in the ordinary course of our business. Market risk represents the risk of loss that may impact our financial position due to adverse changes in financial market prices and rates. Our market risk exposure is primarily a result of foreign currency exchange rates and interest rates, which are discussed in detail below.

Foreign Currency Risk

The U.S. dollar is our functional currency. The majority of our revenue was denominated in U.S. dollars for the six months ended June 30, 2024, and June 30, 2023; however certain expenses comprising our cost of revenue and operating expenses were denominated in NIS, mainly payroll and rent.

This foreign currency exposure gives rise to market risk associated with exchange rate movements of the U.S. dollar against the NIS. Furthermore, we anticipate that a material portion of our expenses will continue to be denominated in NIS.

A decrease of 5% in the U.S. dollar to NIS exchange rate would have increased our cost of revenue and operating expenses by approximately 1% during each of the six months ended June 30, 2024, and June 30, 2023. If the NIS fluctuates significantly against the U.S. dollar, it may have a negative impact on our results of operations.

To reduce the impact of foreign exchange risks associated with forecasted future cash flows and the volatility in our Consolidated Statements of Operations, we have established a hedging program as further described in Note 2 to our audited consolidated financial statements included in our Annual Report. Foreign currency contracts are generally utilized in this hedging program. Our foreign currency contracts are short-term in duration. We do not enter into derivative instruments for trading or speculative purposes.

We account for our derivative instruments as either assets or liabilities and carry them at fair value in the Consolidated Balance Sheets. The accounting for changes in the fair value of the derivative depends on the intended use of the derivative and the resulting designation. Our hedging program reduces but does not eliminate the impact of currency exchange rate movements.

Our derivatives expose us to credit risk to the extent that the counterparties may be unable to meet the terms of the agreement. We seek to mitigate such risk by limiting our counterparties to major financial institutions and by spreading the risk across a number of major financial institutions. However, failure of one or more of these financial institutions is possible and could result in incurred losses.

As of June 30, 2024, the notional amount of our outstanding foreign exchange contracts was $135.7 million, all of which met the requirements of hedge accounting.

The table below provides information regarding our derivative instruments held in order to limit the exposure to exchange rate fluctuation as of June 30, 2024 (in thousands of dollars):

| Derivatives designated as hedging instruments: | | Maturity in 2024-2025 | |

| Foreign exchange contracts: | | | |

| NIS | | $ | 135,674 | |

| Total | | $ | 135,674 | |

Interest Rate Risk

We believe that we have no significant exposure to interest rate risk, as we have no long-term loans. However, our future interest income may fall short of expectations due to changes in market interest rates.