Exhibit 99.2

GLOBAL CONSUMER ACQUISITION CORP 1

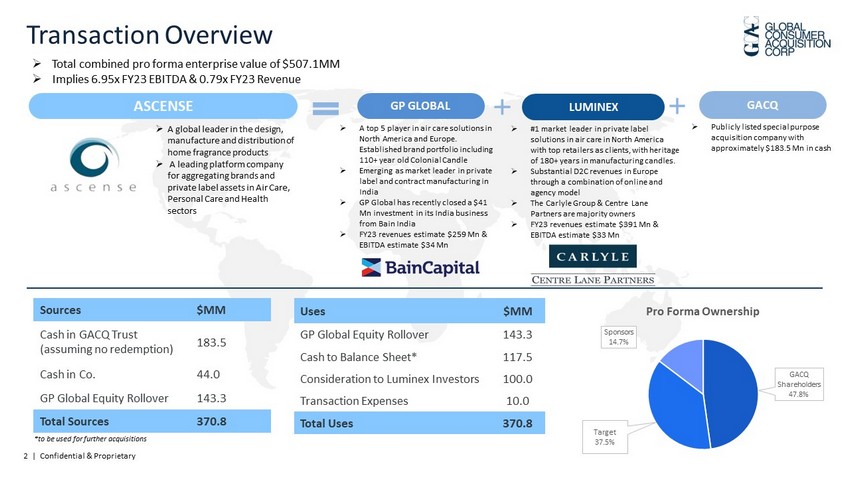

2 | Confidential & Proprietary » Total combined pro forma enterprise value of $507.1MM » Implies 6.95 x FY23 EBITDA & 0.79x FY23 Revenue GACQ Transaction Overview » Publicly listed special purpose acquisition company with approximately $183.5 Mn in cash » A global leader in the design, manufacture and distribution of home fragrance products » A leading platform company for aggregating brands and private label assets in Air Care, Personal Care and Health sectors GACQ *to be used for further acquisitions ASCENSE Sources $MM Cash in GACQ Trust (assuming no redemption) 183.5 Cash in Co. 44.0 GP Global Equity Rollover 143.3 Total Sources 370.8 Uses $MM GP Global Equity Rollover 143.3 Cash to Balance Sheet* 117.5 Consideration to Luminex Investors 100.0 Transaction Expenses 10.0 Total Uses 370.8 GP GLOBAL » A top 5 player in air care solutions in North America and Europe. Established brand portfolio including 110+ year old Colonial Candle » Emerging as market leader in private label and contract manufacturing in India » GP Global has recently closed a $41 Mn investment in its India business from Bain India » FY23 revenues estimate $259 Mn & EBITDA estimate $34 Mn » #1 market leader in private label solutions in air care in North America with top retailers as clients, with heritage of 180+ years in manufacturing candles. » Substantial D2C revenues in Europe through a combination of online and agency model » The Carlyle Group & Centre Lane Partners are majority owners » FY23 revenues estimate $391 Mn & EBITDA estimate $33 Mn LUMINEX GACQ Shareholders 47.8% Target 37.5% Sponsors 14.7% Pro Forma Ownership

3 | Confidential & Proprietary Led By Experienced Operators & Investors Rohan Ajila CEO & Co - Chairman » 20+ years of investment experience with US$1.2 Bn invested in 120+ funds and companies globally » Expertise in cross - border acquisitions and joint ventures to Asia » Focus in designing growth strategies for companies and leading business transformation through digitalization and manufacturing translocation T. Gautham Pai Co - Chairman » Chairman and Managing Director of The Manipal Group with >US$750 Mn in annual turnover » Expertise in cross - border acquisition and formulating strategic joint ventures » Proven track record of value creation through quick adoption of new technologies, building global supply chains and expanding businesses globally

4 | Confidential & Proprietary Guided by Independent Directors with Rich Experience 4 Tom Clausen » 30 years of direct investment and private equity investment experience » Co - founder and Managing Partner at Capvent , a private equity manager (with Unilever as strategic investor) which he helped build to over US $ 1 . 2 Bn AUM with offices in Switzerland, India, China and US, invested in 120 + PE funds across strategies and geographic regions » Managing Partner at FIDES Business Partner AG based in Zurich, an asset manager in Zurich, Switzerland » Early active investor & director in FlowGen Development & Management AG, a Swiss renewable energy company Denis Tse » Extensive experience in private equity and cross - border investments » CEO of ACE Equity Partners International and founder of its affiliate, Asia - IO Advisors » Head of Private Investments – Asia with Lockheed Martin Investment Management Company » “ 40 under 40 ” – Chief Investment Officer award ( 2014 ) ; Asia’s Most Influential People in Private Equity” – Asian Investor ( 2013 ) » Founding team member of the SPAC – ACE Convergence Acquisition Corp, that has recently entered into a definitive merger agreement with Tempo Automation Inc . , a Leading Software - Accelerated Electronics Manufacturer » Current board responsibility with HMD Global Oy and board advisor to Northwestern University School » Previous board experience with Maxnerva Technology Services and Hongkong Science & Technology Parks Corp Art Drogue » CPG industry veteran with over 30 years of experience at CPG majors » Board of Ruiz Foods, the largest Mexican frozen foods brand, Demers Foods, Nutrishus Brands, Atlas Bars and as Chairman of Little Bean, US » Served on the board of SPAR Group, as Chairman of Yasso until its sale in 2017 , on the board of JM Global Holdings, on the board of TABS, a CPG analytics company, and as an Operating Partner at Raptor Consumer Fund investing in early stage CPG brands » Sr . Vice President of US $ 18 Bn U . S . , Canada, and Latin America region for Unilever . Led US $ 12 Bn U . S . Foods and Personal Care business for Unilever » Various corporate roles in sales & marketing at Nabisco and General Mills

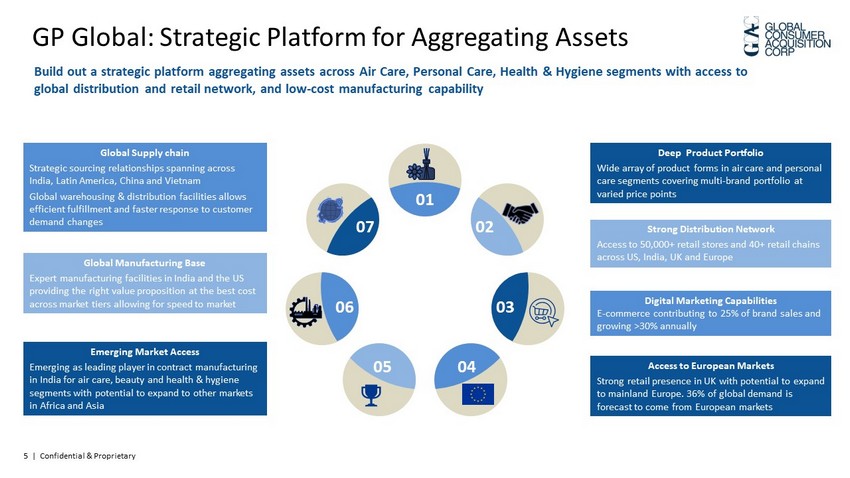

5 | Confidential & Proprietary Global Manufacturing Base Expert manufacturing facilities in India and the US providing the right value proposition at the best cost across market tiers allowing for speed to market Access to European Markets Strong retail presence in UK with potential to expand to mainland Europe. 36% of global demand is forecast to come from European markets Deep Product Portfolio Wide array of product forms in air care and personal care segments covering multi - brand portfolio at varied price points Build out a strategic platform aggregating assets across Air Care, Personal Care, Health & Hygiene segments with access to global distribution and retail network, and low - cost manufacturing capability Digital Marketing Capabilities E - commerce contributing to 25% of brand sales and growing >30% annually 01 07 02 06 03 05 04 Global Supply chain Strategic sourcing relationships spanning across India, Latin America, China and Vietnam Global warehousing & distribution facilities allows efficient fulfillment and faster response to customer demand changes Strong Distribution Network Access to 50,000+ retail stores and 4 0+ retail chains across US, India, UK and Europe Emerging Market Access Emerging as leading player in contract manufacturing in India for air care, beauty and health & hygiene segments with potential to expand to other markets in Africa and Asia GP Global: Strategic Platform for Aggregating Assets

6 | Confidential & Proprietary 183 191 166 159 179 259 329 376 419 - 100 200 300 400 500 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 FY26 Net Revenue from Operations ($ Mn) 26 28 3 16 20 34 48 58 67 0% 2% 4% 6% 8% 10% 12% 14% 16% 18% - 10 20 30 40 50 60 70 80 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 FY26 EBITDA ($ Mn) GP Global: Centres of Excellence Driving High Growth Attractive industry dynamics Strong brands with loyal customer base Large scale, multi - location manufacturing capabilities In - house digital center of excellence In - house product development expertise Deep entrenched customer relationships Global supply chain Expanding customer base in existing markets Acquiring market share in emerging markets Accelerating growth through e - commerce and digital marketing Diversifying brand offering into new product categories to address consumer needs » The company after restructuring in FY20 - 21 is poised for growth by leveraging on attractive industry dynamics and in - house cente rs of excellence » GP Global has recently closed a $41 Mn investment in its Indian business from Bain India affiliate Business was restructured in FY20 & FY21 GP Global’s financial year period is Apr - Mar

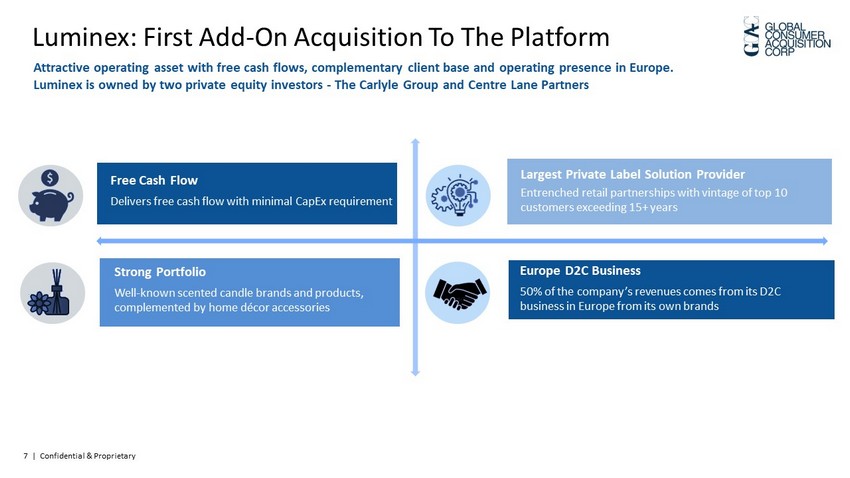

7 | Confidential & Proprietary Attractive operating asset with free cash flows, complementary client base and operating presence in Europe. Luminex is owned by two private equity investors - The Carlyle Group and Centre Lane Partners Strong Portfolio Well - known scented candle brands and products, complemented by home décor accessories Largest Private L abel Solution P rovider Entrenched retail partnerships with vintage of top 10 customers exceeding 15+ years Europe D2C Business 50% of the company’s revenues comes from its D2C business in Europe from its own brands Free Cash Flow Delivers free cash flow with minimal CapEx requirement Luminex: First Add - On Acquisition To The Platform

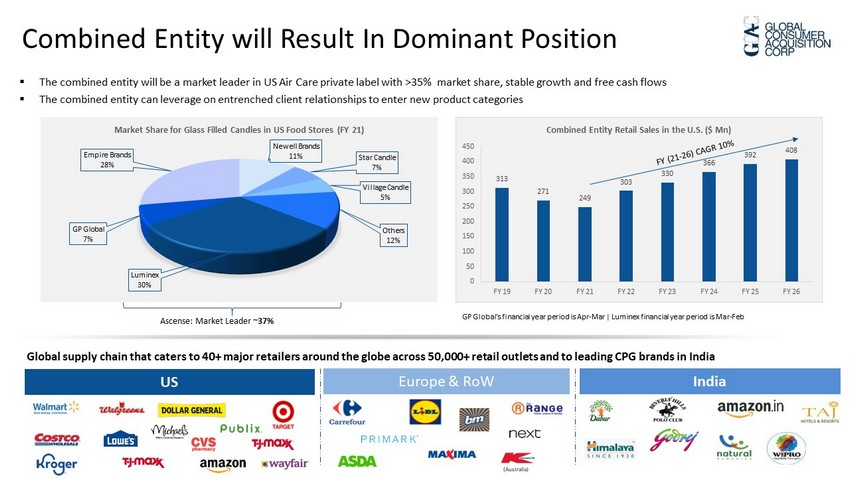

8 Combined Entity will Result In Dominant Position ▪ The combined entity will be a market leader in US Air Care private label with >35% market share, stable growth and free cash fl ows ▪ The combined entity can leverage on entrenched client relationships to enter new product categories 313 271 249 303 330 366 392 408 0 50 100 150 200 250 300 350 400 450 FY 19 FY 20 FY 21 FY 22 FY 23 FY 24 FY 25 FY 26 Combined Entity Retail Sales in the U.S. ($ Mn) Ascense: Market Leader ~37% Newell Brands 11% Star Candle 7% Village Candle 5% Others 12% Luminex 30% GP Global 7% Empire Brands 28% Market Share for Glass Filled Candles in US Food Stores (FY 21) GP Global’s financial year period is Apr - Mar | Luminex financial year period is Mar - Feb US Europe & RoW India 8 (Australia) Global supply chain that caters to 40+ major retailers around the globe across 50,000+ retail outlets and to leading CPG bran ds in India

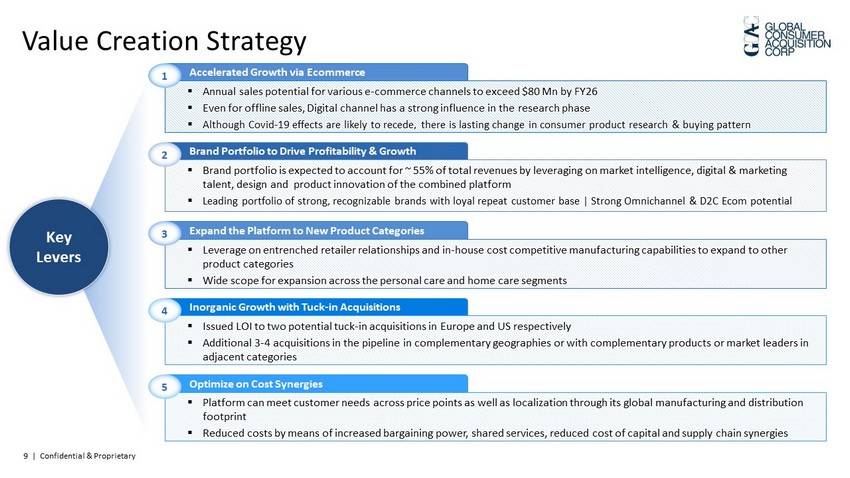

9 | Confidential & Proprietary Value Creation Strategy Key Levers Accelerated Growth via Ecommerce ▪ Annual sales potential for various e - commerce channels to exceed $80 Mn by FY26 ▪ Even for offline sales, Digital channel has a strong influence in the research phase ▪ Although Covid - 19 effects are likely to recede, there is lasting change in consumer product research & buying pattern 1 Brand Portfolio to Drive Profitability & Growth ▪ Brand portfolio is expected to account for ~ 55% of total revenues by leveraging on market intelligence, digital & marketing talent, design and product innovation of the combined platform ▪ Leading portfolio of strong, recognizable brands with loyal repeat customer base | Strong Omnichannel & D2C Ecom potential 2 Expand the Platform to New Product Categories ▪ Leverage on entrenched retailer relationships and in - house cost competitive manufacturing capabilities to expand to other product categories ▪ Wide scope for expansion across the personal care and home care segments 3 Inorganic Growth with Tuck - in Acquisitions ▪ Issued LOI to two potential tuck - in acquisitions in Europe and US respectively ▪ Additional 3 - 4 acquisitions in the pipeline in complementary geographies or with complementary products or market leaders in adjacent categories 4 Optimize on Cost Synergies ▪ Platform can meet customer needs across price points as well as localization through its global manufacturing and distributio n footprint ▪ Reduced costs by means of increased bargaining power, shared services, reduced cost of capital and supply chain synergies 5

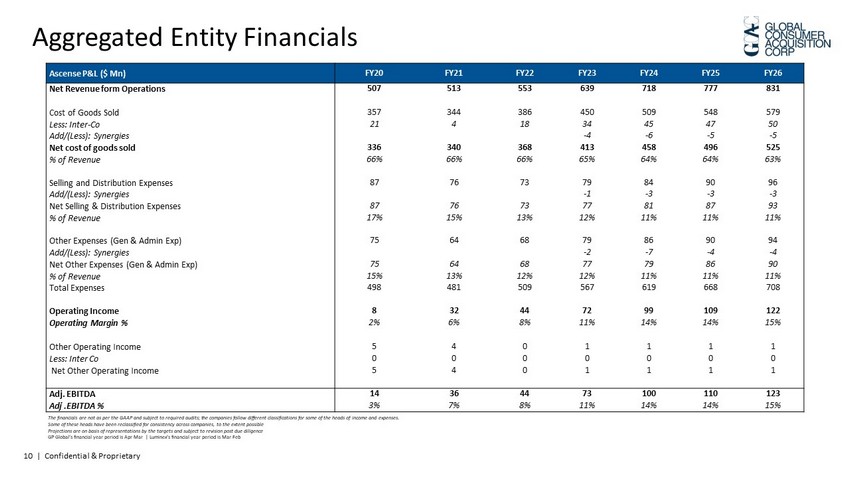

10 | Confidential & Proprietary The financials are not as per the GAAP and subject to required audits; the companies follow different classifications for som e o f the heads of income and expenses. Some of these heads have been reclassified for consistency across companies, to the extent possible Projections are on basis of representations by the targets and subject to revision post due diligence GP Global’s financial year period is Apr - Mar | Luminex’s financial year period is Mar - Feb Aggregated Entity Financials Ascense P&L ($ Mn) FY20 FY21 FY22 FY23 FY24 FY25 FY26 Net Revenue form Operations 507 513 553 639 718 777 831 Cost of Goods Sold 357 344 386 450 509 548 579 Less: Inter - Co 21 4 18 34 45 47 50 Add/(Less): Synergies - 4 - 6 - 5 - 5 Net cost of goods sold 336 340 368 413 458 496 525 % of Revenue 66% 66% 66% 65% 64% 64% 63% Selling and Distribution Expenses 87 76 73 79 84 90 96 Add/(Less): Synergies - 1 - 3 - 3 - 3 Net Selling & Distribution Expenses 87 76 73 77 81 87 93 % of Revenue 17% 15% 13% 12% 11% 11% 11% Other Expenses (Gen & Admin Exp) 75 64 68 79 86 90 94 Add/(Less): Synergies - 2 - 7 - 4 - 4 Net Other Expenses (Gen & Admin Exp) 75 64 68 77 79 86 90 % of Revenue 15% 13% 12% 12% 11% 11% 11% Total Expenses 498 481 509 567 619 668 708 Operating Income 8 32 44 72 99 109 122 Operating Margin % 2% 6% 8% 11% 14% 14% 15% Other Operating Income 5 4 0 1 1 1 1 Less: Inter Co 0 0 0 0 0 0 0 Net Other Operating Income 5 4 0 1 1 1 1 Adj. EBITDA 14 36 44 73 100 110 123 Adj .EBITDA % 3% 7% 8% 11% 14% 14% 15%

11 | Confidential & Proprietary 8,037M Total Uses 8,437M $7,387M ILLUSTRATIVE PRO FORMA VALUATION Share Price $10 Pro Forma Shares Outstanding 3 8.2 Mn Implied Equity Value $3 82.0 Mn Pro Forma Net Debt $125.1 Mn Enterprise Value $507.1 Mn ILLUSTRATIVE PRO FORMA OWNERSHIP Transaction Overview Global Consumer IPO cash $183.5 Mn GP Global equity rollover $143.3 Mn Cash from Target $44.0 Mn ESTIMATED SOURCES Total Sources $3 70.8 Mn Total Uses $370.8 Mn ESTIMATED USES Consideration to Luminex Investors $ 100.0 Mn GP Global equity rollover $143.3 Mn Cash to Balance Sheet* $ 117.5 Mn Estimated Payment of Transaction Expenses $10 Mn GACQ Shareholders 47.8% Target 37.5% Sponsors 14.7%

12 | Confidential & Proprietary Enterprise Value / EBITDA Enterprise Value / Sales Enterprise Value Benchmark Multiples are based on TTM EBITDA and revenue. Data source of comparable companies: Yahoo finance FY23 multiple for Ascense Brands 10.7x 9.7x 11.4x 16.2x 14.1x 13.9x Leifheit AG Ontex Group Treehouse Foods Primo Water Corp Post Holdings Compass Diversified Holdings 1.0x 0.7x 0.9x 2.2x 2.1x 1.8x Leifheit AG Ontex Group Treehouse Foods Primo Water Corp Post Holdings Compass Diversified Holdings FY23 multiple for Ascense Brands 12.7x 12.6x 7.0x Mean Median Ascense Brands 1.4x 1.4x 0.8x Mean Median Ascense Brands

13 Thank you!