UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF

THE SECURITIES EXCHANGE ACT OF 1934

(Amendment No. )

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement | |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ☐ | Definitive Proxy Statement | |

| ☐ | Definitive Additional Materials | |

| ☒ | Soliciting Material under §240.14a-12 | |

SOCIAL CAPITAL SUVRETTA HOLDINGS CORP. III

(Name of Registrant as Specified in Its Charter)

N/A

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. | |||

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ☐ | Fee paid previously with preliminary materials. | |||

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

-1-

-2-

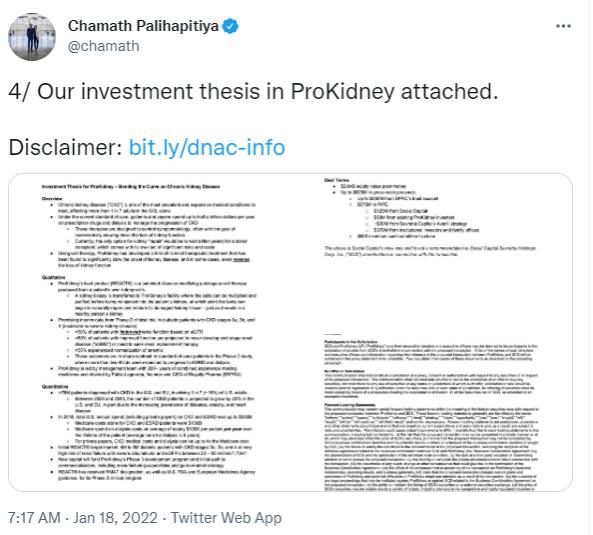

Investment Thesis for ProKidney – Bending the Curve on Chronic Kidney Disease

Overview

| • | Chronic kidney disease (“CKD”) is one of the most prevalent and expensive medical conditions to treat, affecting more than 1 in 7 adults in the U.S. alone |

| • | Under the current standard of care, patients and payers spend up to half a trillion dollars per year on prescription drugs and dialysis to manage the progression of CKD |

| • | These therapies are designed to control symptomatology, often with the goal of incrementally slowing down the loss of kidney function |

| • | Currently, the only option for kidney “repair” would be to wait (often years) for a donor transplant, which comes with its own set of significant risks and costs |

| • | Using cell therapy, ProKidney has developed a first-of-its-kind therapeutic treatment that has been found to significantly slow the onset of kidney disease, and in some cases, even reverse the loss of kidney function |

Qualitative

| • | ProKidney’s lead product (REACT®) is a patented disease-modifying autologous cell therapy produced from a patient’s own kidney cells |

| • | A kidney biopsy is transferred to ProKidney’s facility where the cells can be multiplied and purified before being reinjected into the patient’s kidney, at which point the body can begin to naturally repair and restore its damaged kidney tissue – just as it would in a healthy person’s kidney |

| • | Promising interim data from Phase 2 clinical trial in diabetic patients with CKD stages 3a, 3b, and 4 (moderate-to-severe kidney disease): |

| • | >50% of patients with improved renal function based on eGFR |

| • | >80% of patients with improved function are projected to never develop end-stage renal disease (“ESRD”) or need to seek renal replacement therapy |

| • | >55% experienced normalization of anemia |

| • | These outcomes are in sharp contrast to standard-of-care patients in the Phase 2 study, where more than two-thirds were expected to progress to ESRD and dialysis |

| • | ProKidney is led by management team with 200+ years of combined experience making medicines and chaired by Pablo Legorreta, founder and CEO of Royalty Pharma ($RPRX) |

Quantitative

| • | >75M patients diagnosed with CKD in the U.S. and EU, involving 1 in 7 (~15%) of U.S. adults |

| • | Between 2020 and 2040, the number of CKD patients is projected to grow by 22% in the U.S. and EU, in part due to the increasing prevalence of diabetes, obesity, and heart disease |

| • | In 2018, total U.S. annual spend (including private payers) on CKD and ESRD was up to $500B |

| • | Medicare costs alone for CKD and ESRD patients were $130B |

| • | Medicare spend on dialysis costs an average of nearly $100K per patient per year over the lifetime of the patient (average term for dialysis is 5 years) |

| • | For private payers, CKD medical costs and dialysis can be up to 4x the Medicare cost |

| • | Initial REACT® target market: 4M to 5M diabetic patients with CKD stages 3a, 3b, and 4 at very high risk of renal failure with severe albuminuria and eGFR’s between 20 – 50 ml/min/1.73m2 |

| • | New capital will fund ProKidney’s Phase 3 development program and initial path to commercialization, including manufacturing capabilities and go-to-market strategy |

| • | REACT® has received RMAT designation, as well as U.S. FDA and European Medicines Agency guidance, for its Phase 3 clinical program |

| • | The Phase 3 trial launched in the United States on schedule in January 2022 and may enroll up to 1,500 participants for a primary analysis projected to occur in 2025 |

-3-

| • | While conducting the Phase 3 development program, ProKidney will build a launch facility equipped to serve up to 20K patients per year |

| • | Post launch (targeting 2025), ProKidney plans to build additional manufacturing facilities to serve an additional 40K to 45K patients per year |

| • | Over time, and subject to receipt of regulatory approvals, ProKidney intends to expand to the EU and additional markets, including China, Japan, South Korea, the Middle East, Latin America, Australia, and New Zealand, as well as into additional indications, including congenital anomalies of the kidney, polycystic kidney disease, and other genetically based kidney diseases |

Deal Terms

| • | $2.64B equity value post-money |

| • | Up to $825M in gross cash proceeds |

| • | Up to $250M from SPAC’s trust account |

| • | $575M in PIPE |

| • | $125M from Social Capital |

| • | $50M from existing ProKidney investors |

| • | ~$30M from Suvretta Capital’s Averill strategy |

| • | $370M from institutional investors and family offices |

| • | $500 minimum cash condition to close |

The above is Social Capital’s view only and is not a recommendation to Social Capital Suvretta Holdings Corp. Inc. (“SCS”) shareholders in connection with the transaction.

-4-

BLOOMBERG NEWS

Jan 18, 2022 05:30:00

Palihapitiya’s SPAC to Merge With ProKidney in $2.6 Billion Deal

Medical technology firm will receive up to $825 million

cash ProKidney treats chronic kidney disease using patient’s cells

By Crystal Tse

(Bloomberg) — A blank-check firm started by serial dealmaker Chamath Palihapitiya and Suvretta Capital is merging with medical technology company ProKidney, according to a statement, confirming a Bloomberg News report earlier this month.

Social Capital Suvretta Holdings Corp. III and ProKidney will have a combined equity value of $2.64 billion, the companies said. The transaction also includes a $575 million equity placement that will provide ProKidney with as much as $825 million in cash proceeds, assuming investors in the special purpose acquisition company don’t redeem their shares.

The $575 million private investment in public equity is led by a $125 million investment from Palihapitiya’s Social Capital, and includes $50 million from ProKidney’s existing investors, about $30 million from Suvretta Capital’s Averill strategy and the remainder from institutional investors and family offices, the statement shows.

ProKidney is developing a technology to treat chronic kidney disease by using the patient’s own cells to restore kidney function, according to its website. The company was started by a group of investors led by Pablo Legorreta, the founder and chief executive officer of Royalty Pharma Plc.

Proceeds from the transaction will fund the phase three development of the company’s lead product candidate, accelerate manufacturing build-out and ultimately prepare for a global commercial launch.

“ProKidney can help usher in a new era of better health for millions of chronic kidney disease patients living with the fear of kidney failure and a life on dialysis,” Tim Bertram, founder and CEO of ProKidney, said according to the statement.

The partnership between Palihapitiya and Suvretta Capital has so far resulted in four SPACs that have each raised $250 million. The SPACs are each targeting a different subsector within biotechnology: neurology, oncology, organs and immunology.

Their Social Capital Suvretta Holdings Corp. I SPAC is in talks to merge with Akili Interactive, a startup that specializes in technology-based cognitive therapies, Bloomberg News reported this month.

“For decades, health-care providers have been limited to addressing the symptoms of chronic kidney disease—largely through burdensome regimens like dialysis—with no cure for the underlying disease,” Palihapitiya said in the statement. “ProKidney has the opportunity to change the way we approach and treat chronic kidney disease.”

Related tickers:

1692472D US (ProKidney LLC)

DNAC US (Social Capital Suvretta Holdings Corp III)

To contact the reporter on s story :

Crystal Tse in New York at ctse44@bloomberg.net

To contact the editors responsible for this story:

Liana Baker at lbaker75@bloomberg.net

David Morris, Sam Nagarajan

© 2022 Bloomberg L.P. All rights rese rved .

January 18, 2022

Corporate Speakers:

| • | Chamath Palihapitiya; Founder & CEO; Social Capital Suvretta Holding Corp. III |

| • | Pablo Legorreta; Board Chairman; ProKidney |

| • | Kishen Mehta; President; Social Capital Suvretta Holdings Corp. III |

| • | Tim Bertram; Chief Executive Officer; ProKidney |

PRESENTATION

Operator: Welcome to today’s conference call announcing the business combination of Social Capital Suvretta Holdings Corp. III and ProKidney LP.

Joining us on the call are Chamath Palihapitiya, Chairman and Chief Executive Officer of Social Capital Suvretta Holdings Corp. III and Founder and Chief Executive Officer at Social Capital. Kishen Mehta, President of Social Capital Suvretta Holdings Corp. III and Portfolio Manager of the Averill Strategy at Suvretta Capital Management.

Pablo Legorreta, Founder of Royalty Pharma and Chairman of the ProKidney board and Tim Bertram, Chief Executive Officer of ProKidney.

We would first like to remind everyone that this call contains forward-looking statements including but not limited to Social Capital Suvretta Holding Corp. III and ProKidney’s expectations of predictions of financial and business performance and conditions.

The timing of development milestones, competitive and industry outlook and the timing and completion of the transaction. Forward-looking statements are inherently subject to risks, uncertainties and assumptions and they are not guarantees of performance.

We encourage you to read the press release issued today. The accompanying presentation and Social Capital Suvretta Holding Corp. III’s public filings with the SEC for a discussion of the risks that can affect the transaction, Social Capital Suvretta Holding Corp. III’s and ProKidney’s businesses and the outlook of the combined company.

Social Capital Suvretta Holding Corp. III and ProKidney are under no obligation and expressly disclaim any obligation to update, alter or otherwise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by law.

This conference call is for informational purposes only and shall not constitute an offer to buy any securities or a solicitation of any vote in any jurisdiction pursuant to the proposed business combination or otherwise. Nor shall there be any sale of the securities at any jurisdiction in which the offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities law of any such jurisdiction.

With that, I’ll turn the call over to Chamath Palihapitiya.

Chamath Palihapitiya: Welcome everybody to the merger of DNAC and ProKidney. Thank you for taking the time to learn about this company and this transaction.

But, before we go into any further details what I would really to do is introduce my partner in this, Pablo Legorreta. Pablo is the founder and CEO of Royalty Pharma and is the largest shareholder and chairman of ProKidney and before we really talk about the company I’d love for everybody to hear his perspectives, not only on this transaction but also on the space and what he thinks about the long-term commercial opportunity of providing a really meaningful solution for chronic kidney disease.

Pablo Legorreta: Thanks Chamath. Hello, I’m Pablo Legorreta, founder and CEO of Royalty Pharma as well as chairman and shareholder of ProKidney.

Given the challenging environment we’re all living in we’re particularly appreciative of the time you’re spending to get to know ProKidney. I will begin by providing briefly a bit of background on myself and the 25 years of experience I have gained in funding innovation in life sciences for Royalty Pharma and building biotech companies like ProKidney as a private investor.

Since I founded Royalty Pharma in 1996 we have pioneered the life sciences royalty market and have been at the forefront developing royalties as an asset class.

The idea behind Royalty Pharma was simple. Innovation has been the driving force behind the profound transformation of the life sciences R&D ecosystem. Consistence in growing medical research funding over many decades by world government and more recently by the [C-specific] Research Foundation led to a better understanding of human biology, transformed drug discovery and importantly launched the vibrant biotechnology industry.

The United States government through the National Institutes of Health funds medical research by providing over $50 billion in grants to science and academic institutions and research (inaudible).

This consistent funding over many decades has resulted in an enormous number of discoveries and patents, as well as royalties owned by this institution. So, how does Royalty Pharma fit and, in fact, help accelerate the innovation that takes place in the R&D ecosystem?

We fund innovation both directly and indirectly. Directly when we partner with companies to co-fund late-stage clinical trials and new product launches in exchange for future royalties.

And indirectly when we acquire assisting royalties from universities, research hospitals, foundations and inventors. As the business Royalty Pharma captures and offers investors the best attributes of biopharma without exposure to the common industry challenges. We collect royalties in many of the most attractive biopharma products, which are marketed by the top biopharma companies. The royalties we own allow us to share in the top-line, the sales of biopharma products.

So, importantly from a top line revenue perspective we’re no different than any biopharma company. When we benefit from strong I.T. protection as well as the product upside often derived from new indications.

At the same time we have no or substantially lower exposure to many common industry challenges, like early-stage development risks, [serve] (inaudible) constraints, high research and development costs and high fixed manufacturing and marketing costs.

This results in Royalty Pharma’s unusually high EBITDA margin of over 90% and net margin of over 70%. Historically, we’ve been able to consistently grow a double-digits, both our top line and bottom line. For more than two decades we have been able to compound growth and when compared to the biopharma companies our growth dynamics stand out on, one, magnitude of growth which is severe to most companies.

Two, diversity of growth which makes our growth more consistent and predictable because it is less reliant of your products and like most companies. And three, duration of growth given the very long I.P. duration of our portfolio, twice as long as many large pharmas.

We took Royalty Pharma public in June of 2020 and we trade on Nasdaq with a ticker RPRX. Royalty Pharma’s core focus is to provide capital to those at the forefront of discovering life-saving therapies and enable institutions to reinvest capital back into the biopharma ecosystem to accelerate future innovation. This is a powerful and enduring value proposition that is necessary for the success of innovators and life sciences.

Turning over to ProKidney, I have had a personal interest in therapies that have the potential to improve long-term outcomes in people with chronic kidney disease, CKD, because my son was born with urinary reflux.

I became aware of the cutting-edge science behind ProKidney’s REACT because at Boston Children’s Hospital where my son had surgery shortly after birth a team led by Tony Atala did the basic early research behind ProKidney cell therapy. In 2014, I was approached by Tony Atala and Tim Bertram, who asked if I would be interested in an investment to fund REACT.

At the time REACT had not yet started human clinical trials, so I declined. By 2017, my son’s renal function was declining and around that time in inRegen, ProKidney’s predecessor, had concluded a phase I trial in diabetic CKD patients.

So I reached out to Tim and I asked if they could consider running a clinical trial in patients with impaired kidney function caused by urinary conditions, not diabetes.

inRegen and I agreed to collaborate and split the cost of the trial, about $3 million, on a 50/50 basis. I’ve worked with Tim and the nephrology team at Children’s Hospital of Philadelphia and Mount Sinai to design a trial. We filed it with FDA.

FDA approved the trial and I went back to the — to inRegen to discuss the launch of the trial. inRegen declined. I offered to pay for 100% of the cost of the trial. And Tim indicated that the owner of inRegen had become very negative about biopharma given the incoming Trump administration and its negative position on the pharma industry.

I pushed back with no success and eventually they asked if I would be willing to acquire the company. So, I said I would at cost, indicating I would not be willing to pay a premium. I reached out to [Carlos Leem] and his family who I knew well, who had expressed an interest in kidney research given a genetic predisposition to kidney issues in the [Leem] family. He said if you ever see something interesting in kidney give me a call.

So, we partnered and acquired the company and changed its name to ProKidney. When we acquired the company they were launching a fully-patient phase II trial in diabetics with phase III and phase IV CKD. I felt uncomfortable investing in a rather small trial that I felt could yield inconclusive data.

So, I asked him to check with statisticians and based on their feedback we decided to double the size of the trial to 80 patients and make it randomized, multi-centered and to follow our patients for much longer, up to three years after being treated with REACT to get a better feel for the duration of clinical benefits.

So, we ran the trial, an 80-patient trial that was randomized one-to-one and ran it in 15 hospitals. And that allowed us to randomly create an active cohort of about 40 patients that had been injected with REACT, their own presented their self and started to improve their kidney function.

And another 40 patients that were enrolled in a deferred cohort that were not treated for a year. These patients were maintained on best standard of care and followed for 12 months before being offered the possibility to cross over and be injected.

The superior design created two groups, around 40 patients each with similar characteristics. One group that was treated and improved and another one that was not treated for a year and continued to decline. In this design then allowed us to measure the magnitude of difference in renal function between the two groups as well as the duration of benefits.

Many phase I and phase II companies have data from smaller single-arm trials that were run in a single or a few centers and the data rarely exceeds a year of follow-up. ProKidney has generated unprecedented clinical data running a randomized trial that enrolled 81 patients from 15 hospitals and we have up to 24 months of follow-up data.

This is somewhat rare and should meaningfully reduce the remaining clinical development risks. In a disease in which kidney function progressively declines in patients inevitably reach dialysis. The stabilization of kidney function would be enough for REACT to achieve the status of a disease-modifying (inaudible) product, likely making it a widely successful product from a patient off-take and commercial perspective.

Our data today unprecedented in CKD appears to meaningfully improve renal function in many patients, improvement that has been sustained for up to 24 months. We are seeing improvements in one, gaining renal function; two, stabilization to slightly decline in albuminuria and proteinuria. And three, improvements in other CKD comorbidities such as anemia and bone and mineral dysfunction.

Importantly, REACT’s clinical data impacts a wide range of a patient’s clinical parameters because it has the potential to repair the organ. In contrast to most other products that impact only one clinical parameter.

Notably, ProKidney’s REACT was awarded the covenant RMAT designation by FDA, the equivalent of breakthrough designation for small molecules and biologics. Which materially the risks, the remaining clinical developments and FDA approval process. To achieve this result ProKidney shareholders, the [Leem] family and myself have supported the company, investing around $200 million to date.

ProKidney has also benefitted from an additional $200 million that was invested before the existing shareholders, the [Leem] family and myself acquired the company. This capital was invested in the science and in the developments of the manufacturing process of the cell admix and the delivery of the product safely into the kidney with a minimally invasive procedure.

Existing shareholders, the [Leem] family and myself are also committed to invest an additional $50 million in the pipe. Finally, if approved ProKidney’s REACT will address one of the largest unmet medical needs in human health, potentially delaying dialysis, the medical treatment that represents the number one category of expenditure by most healthcare systems.

Further, from a pharmaeconomic perspective it is extremely rare for a new treatment to have the potential to reduce existing costs already being born by healthcare systems around the world. In fact, the launch of the vast majority of novel disease modifying medicines, many that treat rare diseases afflicting small patient populations, many of which I know well since we have invested in them through Royalty Pharma. This rare disease product generally, at significant cost to already stretched healthcare budgets.

What is so unique and exciting about ProKidney’s REACT is its ability to benefit patients by delaying dialysis while reducing significant cost that’s already in the system.

Thank you. Back to you Chamath.

Chamath Palihapitiya: Thanks Pablo. So let’s jump in. I think it’s important, starting on page 4, to really understand what we’re dealing with. And in most cases in biotech currently, we don’t really get the chance to work on large disease categories. And there’s a lot of reasons why that is. But, without belaboring them the point here is that chronic kidney disease is a condition with a very large patient population.

In fact, if you start looking on page 5, what you can see is that the chronic kidney disease market is really quite substantial. And, unfortunately, in the United States, as of 2020, approximately 38.5 million Americans suffered from the disease. When you include Western Europe that population almost doubles to almost 75 million total people.

And over the course of the next decades what we see just in the United States and Western Europe is that this disease is estimated to touch more than 90 million people by 2040.

And when you deal with population sizes that big the thing that we can also expect is that there is an enormous amount of money that is spent treating CKD all around the world.

On page 7, what we’ve done is we’ve broken out the United States population and we’ve started to look at the actual costs. And inside of Medicare there is some transparency that they give us in terms of how much they spend in supporting this disease. And the answer is that there is an enormous amount of money that’s spent to support these 38.5 million people. Just inside of Medicare around $80 billion a year is spent on chronic kidney disease.

Now that’s just unfortunately the beginning of this disease burden, because at the end of chronic kidney disease when your kidneys have effectively failed you are then put on end-stage renal disease or dialysis. That is yet another $50 billion that are spent. And so when you add these two things together on a kidney disease begins a journey that costs Americans around $130 billion a year just in public insurance.

If you then extrapolate that to include the cost of CKD and end-stage renal failure for private insurers the cost increased between two and four X. And so what that means is on a yearly basis in America we’ve spent somewhere between a quarter of $1 trillion and half $1 trillion a year dealing with this disease.

If you take a big step back the real thing that I was surprised by is that CKD has no known cure. And that the current standard of care nearly just slows down your expected eventual loss of kidney function. So if you’re an individual, and many of us know these people, in fact, in my own family my father suffered from chronic kidney disease brought on by diabetes. He then spent 10 years on dialysis. Unfortunately, he passed away six years ago. It’s a disease that we all understand as a slow motion train wreck in many ways.

And essentially what happens is patients continue to slowly lose kidney function on whatever existing therapies exist. And despite the fact that these therapies are not that efficacious, those therapies still exhibit multi-million dollars worth of sales.

In fact, what you can see here on this slide, on page 9, is essentially the performance both physiologically as well as financially of the three most prevalent drugs that are prescribed for patients suffering from CKD.

I think this is a good opportunity to reintroduce Pablo and have him talk to you about his view about these drugs from the context of Royalty Pharma when he underwrote one of these drugs and bought one of these drugs.

Pablo Legorreta: Thank you Chamath. So what we see here is the clinical data from three large well-run trials on SGLT-2s. This is interesting for me because at Royalty Pharma over the last 10-ish years we have invested close to $2 billion in patients in CKD. We actually invested close to $1 billion in DPP4 inhibitors, which are approved and became a $10 billion plus category, drugs like Januvia/Janumet from Merck, Onglyza, Tradjenta from Lilly. And these are drugs that are used to treat CKD patients.

But what we see here is SGLT-2s and at Royalty Pharma we actually at some point many years ago considered funding the phase III trial on canagliflozin the drug on the left. We had discussions with the developer J&J. It did not happen, but eventually we did invest in canagliflozin and today we collect the royalty on INVOKANA. So this is a drug that I’m very familiar with. And what’s interesting to note here is that what you see is on each one of these cases you have placebo-controlled trials with about 4,000 to 7,000 depending on the trial — 4,000 to 7,000 patients.

And you can see that the patients have the very typical decline that you see in phase III, IV CKD patients where they’re losing between eight and 10 points of function per year and that’s the grey lines that you see in each one of these graphs. These patients continue to decline over time.

And what you then see is the effect of the SGLT2s. When patients get on these drugs what we can see here is that all that happens is that the slopes of decline attenuated a bit. And that it is between 1mL and 2mLs, this is merely just per minutes of eGFR over a 24-month period.

Highly beneficial for these patients, it delays a little bit dialysis but this is the best of today’s — best drugs can do. Also noteworthy is the fact that these drugs are all approved, generating significant sales, and are forecasted to get to 10 billion plus in sales by the middle of this decade.

And it’s important also to keep this drug in mind because when we look at the effect of ProKidney’s REACT it is obviously more significant improvement than function. Stability to — actually a gain in kidney function versus and [automation] of the loss of kidney function. Thank you, back to you, Chamath.

Chamath Palihapitiya: Great, thanks, Pablo. If you take a big step back knowing that these drugs are not that affected the real opportunity for us is to answer the holy grail question in medicine, which is how can you find a solution that is ultimately disease-modifying?

And the economic reason for doing that sits in a very complimentary way with the human and ethical reason, obviously. Which is that economically they are enormous payoffs. So, on page 11 what you can see is just a study of six very meaningful breakthroughs in medicine over the last number of years.

And in each of these cases what we see are drugs that have been proven to be disease-modifying in a very conclusive way in their own category. Whether that’s cystic fibrosis, or SMA, Graves’ disease, et cetera. And in all of these cases what’s interesting to note is that being diseased modifying two things happen.

The first is that you have these really large competitive [nodes] based on how unique you are to build a large revenue stream and a very predictable revenue stream. The second is that because of your uniqueness you also tend to get enormous amount of pricing power that you inherit.

And this is a — quite a unique relationship that happens specifically in this class of drug. So, that opportunity for us was to diligence ProKidney and to try to figure out whether their early data was directionally trending towards one of these very unique and special disease-modifying solutions for, again, what is an enormously large diseased population.

Because if we could show that their solution, which is called REACT is not just stopping the progression of CKD but also drives meaningful improvement and that we could see that scaling into a phase III trial and hopefully an eventual FDA approval. It really would be a first-of-its-kind and quite a revolution in science.

And so, starting on page 13 what we can start to do now is give you a very high-level readout of some of the clinical data that allowed us to really get comfortable, excited, and then eventually underwrite this deal. To do that I’d like to introduce Kishen Mehta, who is my partner in the Social Capital Suvretta biotech SPAC business. And he’ll give you a sense of his readout from this perspective.

Kishen Mehta: Thanks, Chamath. As part of our diligence, we focused on three questions. Is the REACT product safe? Is it clinically active and impacting chronic kidney disease progression? And is the benefit seen to date relevant for patients given the existing standard of care?

From a safety perspective, we believe the question has to a large degree been answered through large phase I and phase II programs, which include multi-year follow-up. The REACT product has been safe and well-tolerated to date with a profile in line with or even a little better than standard biopsy.

As Tim will walk you through later in the presentation over 100 patients have been treated with REACT with follow-up in some cases of more than two years post the last cell injection. The cells once in place do not seem to cause any reaction in the patient. The next question was is it clinically active?

Thanks to Pablo, Tim, and the ProKidney team, we have a well-designed phase II randomized controlled data-set, which we believe points to the clinical activity of REACT.

As you see in the graph on the slide the REACT treated or active patients demonstrate a meaningful and statistically significant different eGFR trend than the untreated standard of care patients. In addition, active patients demonstrate a compelling change in the slope of their eGFR graph from pretreatment.

We view these relative trends on eGFR, which include good long-term follow-up for a phase II study as substantial. On the next slide, we see the eGFR trends for the entire treated phase II population. This included patients randomized to receive REACT upfront and those that crossed over after one year to receive REACT.

When looking at these data, which is the broadest way to evaluate the phase II the average eGFR trend is upwards looking. While this is an average and not all patients will benefit from the treatment we do believe that on average this represents a trend that suggests a potential — a multi-year delay in the need for end-stage renal care and dialysis.

Which gets to the last question, is the benefit seen to date relevant for patients in light of existing standard of care? We believe that if these data are replicated in phase III that REACT will represent a major step-change in the treatment of advanced CKD.

And meaningfully impact how the medical community and patients think about kidney disease progression. As Pablo walked you through previously, around the SGLT2s CKD is a slowly progressive disease where the best outcome to date has been to tilt the slip of decline and potentially delay the progression to dialysis by a few months or longer.

We do not diminish these contributions as we, patients, and physicians agree in the high value of every month of benefit that can be obtained. However, we believe that more can be done to help CKD patients live with better kidney function and will look to the phase III REACT data to confirm the work done to date.

With that, I would like to turn it back over to Chamath, who will walk you through the revenue opportunity in more detail.

Chamath Palihapitiya: Thanks, Kishen. So, as Kishen said, this data starts to show this really disruptive ability to not just slow the progression of the disease but in many cases to improve kidney function even in an all-comers kind of situation.

So, what we wanted to do though was take a step back and say well, if the disease-modifying capability is proven in a phase III clinical trial how would we size the population? How would we think about an initial go-to-market? Who would be the patients that would be the first — at the front of the line to be able to use this solution?

And the way that we thought about that was in the following way. As we talked about earlier, there’s about 38.5 million Americans with CKD, about 15% of the entire United States adult population. Of that, we sub-segmented to individuals specifically with CKD end-stage 3 and 4.

And of that we further sub-segmented that to those who suffer from CKD end-stage 3 and 4 specifically because of diabetes or hypertension. And we think that ultimately that is the initial population pool. Within that, there’s about 8.3 million people who suffer CKD because of diabetes and 5.1 million people who suffer it because of hypertension.

We believe that within that diabetic population and specifically, if you have eGFR between 20 and 50, that is likely where the most value exists initially for ProKidney and REACT. And so, what does that 4.4 million person population represent in terms of potential long-term revenue.

Well, one way to think about it is to sensitize these 4.4 million people for every 1% of that market that we acquire. That is to say around 44,000 patients. And if you think about the pricing power that we would have if we are disease-modifying one way to think about the revenue potential is by looking at those other six drugs that we looked at previously.

Again, just to remind in those six examples when you were a disease-modifying solution, not only did you have the ability to have very little competition, you also had tremendous pricing power. And in those six examples the median price there was $360,000 a patient.

Now, if we apply that same metric here, as a — as a thought experiment what that would mean is that for every 1% of the population we acquire at that same median price point that would result in around $16 billion of revenue per 1% of the market that we attract.

That being said, I think there’s a very good argument to made that it’s not clear whether we would have the ability nor should be price at that upper bound. Because it could be deemed relatively arbitrary.

We could also consider how much money we save the system because we could make a very good claim that we should be able to capture some percentage of these savings in a value-based care model. And this slide on page 17 starts to demonstrate that. If you think about what happens when somebody gets to the end of chronic kidney disease as we indicated before they start dialysis or ESRD.

When you do that if you’re on public Medicare the cost to Medicare is around $100,000 per year and the average patient is on dialysis for about five years. Which means the lower bound of cost is about $0.5 million.

If you’re on private insurance, however, the cost can be up to $400,000 and over that same five years what that means is the cost can be upwards of $2 million. So, the point is that if we can actually take CKD patients in stage 3 and 4, stop the progression of (inaudible) kidney loss, stabilize, and in some cases improve what we actually do is we have the ability to defray up to $2 million of costs in the system.

And so, that, again, is a different way of backing into how we could price and so we think that pricing in the hundreds of thousands could be quite reasonable upon approval. Now, all of that revenue potential and market sensitivity, which really focused on the United States but the bigger point is much more important.

Which is that this is a global disease. And wherever you see large middle-classes, large growing GDP, poor eating habits you have chronic kidney disease, you have diabetes and hypertension, and you have end-stage renal failure.

And so, if we can find a solution that works meaningfully in a compelling way in the United States the obvious markets are not just expanded to Western Europe but into markets like China, Latin America, the Middle East, Japan, et cetera.

And on page 18 what you see is that when you add up these populations we’re talking about hundreds of millions of people all around the world that could be a potential patient of ProKidney and REACT.

So, to summarize our investment thesis and how we came to this conclusion, what does ProKidney represent? It represents a very novel solution to a high acuity, large global unmet medical need where the diseased population is measured in the hundreds of millions of people.

As you will hear it’s a very novel platform with broad potential in kidney disease, which uses your own self to help heal you. Third, what you will also hear is that there are some very strong scientific underpinnings, this is 17 years of research. And broad phase II clinical trials that have been funded internally by the principals in order to get to this stage.

And based on that compelling proof of concept phase II data we were able to receive this very unique designation called RMAT from the FDA, which is essentially form of breakthrough and fast track innovation. But also gives us the ability for an accelerated approval specifically designed to these kinds of molecular therapies.

And the last thing is that we have a comprehensive plan to achieve the goal that we would need in order to build the capacity to be able to manufacture our REACT solution at scale to our patient population. And then the last thing I’ll say is that we’ve also spent a lot of time with the team, you have just heard from Pablo.

Pablo is an incredible executive who’s had a multi-decade career in identifying very compelling and disruptive solutions in biotechnology, underwriting them from first principles from both a scientific and financial perspective. Which he’s done at scale and in success.

I’ve found it quite compelling that he essentially did that for ProKidney off of his own balance sheet. And has supported this thing for both ethical and societal and financial reasons for the last many number of years. You will now meet Tim Bertram, who is the CEO and has really been the pioneer of finding a meaningful solution to CKD.

Tim is an incredible scientist and really deeply understands the physiology of the kidney and the mechanism of action here. And has really been doing this for almost two decades incredibly.

And I think that what we’ve brought together with ProKidney and Social Capital Suvretta is a very good balance of deep science underwriting, deep financial underwriting, and a very credible go-to-market team that has had a track record of finding these kids of compelling solutions.

So, with that, I’d like to introduce Tim Bertram, the CEO of ProKidney to walk you through the mechanism of action and our clinical trial results, and to go into the REACT solution in more meaningful detail.

Tim Bertram: Thank you, Chamath. REACT is a new generation of disease-modifying treatments for chronic kidney disease. I would like to introduce you to REACT by covering the mechanism of action, clinical and regulatory developments, and how we make REACT.

REACT starts with a standard biopsy conducted in an outpatient procedure. In the United States, over 100,000 kidney biopsies are performed each year. Once a biopsy is taken it is shipped to ProKidney’s manufacturing facility in North Carolina where we use a proprietary process to grow the kidney’s progenitor cells from each patient’s biopsy.

We then select the active cells involved in the normal repair and restorative healing processes of the kidney. Once these cells have been grown and processed, they are formulated into a final product and frozen. Only one biopsy is needed to make five to 10 REACT doses prepared for each patient.

This entire process takes approximately 10 weeks from biopsy to injection. Once the doses have been tested for identity, purity, and potency it can be shipped frozen to the clinical site for injection. After thawing the product is injected back into the patient’s kidney using a small 35 gauge non-cutting needle.

Up to 800 million progenitor cells are injected into a kidney. Injection is a simple procedure done under conscious sedation on an outpatient basis. Injection procedure takes about 45 minutes with recovery from sedation in about two hours. The kidney is composed of approximately 26 different cell types.

Many of these cells form the nephron, which is the functional unit of the kidney. The nephron is composed of a filtering portion called the glomerulus and a tubular segment that is evolved in the metabolic functions of the kidney.

Some cells are involved in maintenance, repair, and restoration of damage that can incurred from diseases such as diabetes and hypertension. After more than a decade of research, our scientists were able to identify three cell progenitors that could restore and repair nephrons damaged by disease.

These cells were combined upon REACT, a cellular [ad] mixture that can reactivate the kidney’s natural healing processes. These progenitor cells form the mechanistic basis for the stabilization and improvement of kidney function in chronically diseased kidneys.

To understand the mechanism of this repair we look to see where the progenitor cells localize after being injected into diseased kidneys. Cells were labeled to allow microscopic visualization. You can see in the images in the lower right the blue labeled REACT cells go to damaged regions of a nephron.

When they integrate into the damaged areas of the glomerulus and tubules they replace the damaged cells and remain there for up to six months guiding the repair and restoration of the diseased nephrons and downregulating the inflammation and remodeling the scarring process.

Once we knew that the three progenitors could repair damaged nephrons we looked at the potential of REACT to repair other areas of kidney damage. We used four different animal models of chronic kidney disease caused by diabetes, hypertension, and acute or chronic injury.

If the chronic kidney disease was untreated in these models the disease progresses to renal failure. When REACT was injected after the animals developed severe chronic kidney disease we saw that the REACT treated animals would live while most of the untreated control animals would die of kidney failure.

REACT treated animals had many structural improvements of the kidney, including repair of damaged nephrons, reduced scarring, reduced inflammation, and multiple functional improvements including the ability to control blood pressure, and maintain phosphorus and calcium metabolism.

These effects could be attributed to the repair of the damaged nephron resulting in restoration of glomerular filtration, tubular metabolism, vitamin D3 production, and release of erythropoietin to control erythroid homeostasis.

Let’s now consider the effects of REACT in patients with chronic kidney disease caused by type 2 diabetes. CKD can be caused by many diseases, including diabetes, hypertension, and congenital anomalies.

ProKidney is currently evaluating REACT in the United States as part of a global phase III trial of chronic kidney disease caused by type 2 diabetes. We are also conducting phase II trial with patients that have congenital anomalies of the kidney and urinary tract.

For our discussion today I will focus on ProKidney’s lead indication for patients with diabetic kidney disease stages 3 and 4. I would now like to share with you the effects of REACT from the O2 phase II trial in patients that have diabetic kidney disease stage 3, 4 and are at very high risk of progressing to kidney failure.

This trial is a multicenter one to one randomized study of type 2 diabetic patients with chronic kidney disease stage 3, 4 that have lost between 50% and 80% of their kidney function. Function is measured by estimated (inaudible) filtration rate levels and covered estimated glomerular filtration rate ranges from 20 to 50 [ml] per minute.

Eighty-one patients were enrolled and placed on maximally tolerated standard of care medications including angiotensin receptor blockers, sodium glucose transport protein 2 or SGLT2 inhibitors and other medications to control their diabetes and hypertension.

The average EGFR for all patients was 33 ml per minute and 40% of the patients in this study had CKD Stage 4. After meeting the key entry criteria a routine biopsy was taken from the kidney and the patients were randomly assigned to one of two groups.

If assigned to an acting group they were injected with two REACT doses six months apart in the same kidney of the biopsy. Alternatively, if they were assigned the placebo control cohort they [remained] on best standard care for one year. At the end of that one year standard of care therapy time period they were crossed over and injected with two doses of REACT six months apart in the same kidney that was biopsied.

Both patient groups were followed for two years after the second injection of REACT. REACT is demonstrating a robust efficacy and safety profile in this interim analysis of the phase II trial, 50% of REACT injected patients had improve renal function of which 80% were projected to never go on to end-stage renal disease.

This estimate of risk to progress onto kidney failure is based on two independent models evaluating its changes in estimated glomerular filtration rate, gender, age, and clinical outcomes based on the rate of kidney function decline. Using the same predictive models that assess the risk of progressing to renal failure a majority of patients in the placebo controlled group were projected to progress to end-stage kidney disease even though they were maintained on maximal standard of care for one year.

Other kidney improvements in the REACT injected patients included reduction of anemia and hyperphosphatemia. REACT was also shown to have a robust safety profile and the injection procedure was shown to have fewer side effects than a standard biopsy.

Kidney function in both cohorts was measured by estimated glomerular filtration rate from screening to last scheduled follow-up examination available for this interim analysis. In the REACT treated patients you can see the improvement in renal function after both REACT injections. REACT injected patients are observed in the blue line.

The average EGFR for the REACT treated patients improved from 32.8 at injection to over 38 ml per minute at the 18-month follow-up. In sharp contrast patients in the placebo control cohort being maintained on best standard of care including SGLT2 had a progressively declining kidney function from an average of 32.5 to 28.2 ml per minute at the one-year follow-up.

The results from the placebo control patients are shown in the purple line. It can be seen in the gray boxes between the lines there are substantial differences in the average estimated glomerular filtration rate between the REACT and placebo control patients are each time sampling beginning at the time of the second injection REACT and progressing to the last reported follow-up.

The REACT effects on kidney function as measured by estimate glomerular filtration rate and estimates of kidney damage seen as protein in the urine and measured by a urine albumin-to-creatinine ratio also called uACR per demonstrated. EGFR is shown in the red and blue lines and urine protein levels are the numbers placed above the gold bars.

At the time of injection patients had an average estimate glomerular filtration rate of 32.5 ml per minute and severe proteinuria of over 300 milligrams per gram as measured by the uACR [asset]. As the average EGFR increased over time the proteinuria stabilized or decreased to an average of under 200 milligram per gram.

This suggest the improved renal function is linked to the effects of REACT on the kidney including the stabilization or reduction of proteinuria which is a [surrogate] marker of kidney damage such as inflammation and scarring.

If we now consider other kidney functions such as the production of the Vitamin D3 and (inaudible) we can see that REACT stabilizes, restores and may repair co-morbidities of diabetic kidney disease including the anemia and hyperphosphatemia observed commonly in these patients.

Patients can be seen to have a progressive decrease in their hemoglobin prior to REACT injection and a progressive improvement after injection. Similarly, phosphorus can be seen to have a slow but steady increase before REACT injection followed by a decrease after injection. These observations are consistent with the mechanism of action for REACT as was defined in the animal models.

To evaluate the potential of REACT in patients with very severe chronic kidney disease and risk of kidney failure leading to the need for dialysis ProKidney conducted a study in patients with chronic kidney disease stage 4 having estimated glomerular filtration rates of 15 to 20 ml per minute. This group of patients had an average EGFR of 17.5 ml per minute.

It is generally considered that patients with a EGFR of 15 ml per minute or less are progressing to renal failure and can be referred onto dialysis. Notice that these very sick patients also had quite high levels of proteinuria as shown by uACR levels that were over 2,500 milligrams per gram at the time of injection.

Even with this lower kidney function and extent of kidney damage REACT reduced the decline of renal function by almost 50% potentially adding months of dialysis free living and stabilizing the amount of protein being lost in the urine.

For over seven years ProKidney has evaluated REACT’s affect on diabetic patients with chronic kidney disease stage 3, 4. We have completed over 150 injections. In this time period we have provided 100% of the REACT doses to each patient and there have been no product related adverse events. Adverse events that were observed have been typical for patients suffering from type 2 diabetes (inaudible) and diabetic kidney disease stages 3 and four.

In these studies the REACT injection procedure has been shown to have fewer related side effects than a standard kidney biopsy. This highlights the robust safety profile of REACT and these significant safety findings have recently published in the journal “Kidney International Report”.

Clinical outcomes from this study have been shared with both the Food and Drug Administration and the European Medicines Agency. Based on these results, the Food and Drug Administration awarded ProKidney’s REACT the Regenerative Medicine Advanced Therapy or RMAT designation. This assignment for a cell therapy is equivalent to breakthrough designation awarded for drugs advancing against severe diseases with a few other standards of care available.

Also ProKidney has worked with both agencies to define a phase III program. This [registrationaly] program will include the randomized control trials in a patient population at very high risk for end-stage kidney disease that is caused by type 2 diabetes. These trials will be [sham] controlled and involve up to 1,500 patients.

Treated patients will have a REACT injection in both kidneys. These patients will be followed for two years and then rolled over into a long-term follow-up study to evaluate safety and durability and the support of a premium pricing of this product.

We launched the phase III program in the U.S. in January of this year. We are planning for an interim analysis in 2024, commercial launch to follow after regulatory review. During the two year period while we conduct the blinded sham-controlled trials in the U.S. and around the world we will be conducting four other phase II clinical trials. We plan to progress the current trial in CKD 3, 4 patients and enroll in open label extension of the OO2 study to establish long-term characterization of REACT’s durability and safety.

We will also complete two other studies, the OO3 trial in late-stage CKD 4 patients in estimated glomerular filtration rates of 15 to 20 ml per minute and the OO4 trial in patients with congenital anomalies of the kidney and urinary tract.

Additionally, we will complete enrollment and report out results of another trial in diabetic kidney disease patients which will evaluate the effects of a REACT injection in both kidneys and define a REACT redosing based upon EGFR and uACR triggers. We anticipate this last study to be a [surrogate] for the outcomes we might expect with the phase III program that is being done by injecting REACT into each kidney.

After review of interim OO2 clinical trial outcomes, FDA guided ProKidney to conduct a timed to event randomized sham-controlled registrational program. The phase III program would be conducted in type 2 diabetic patients with diabetic kidney disease stage 3, 4.

The primary end-point for the program would be a [four comp] point composite evaluating the 40% reduction in estimated glomerular filtration rate. And EGFR of less 15 ml per minute or chronic dialysis and increased uACR of 30% and greater than 30 milligram per gram and mortality caused by kidney or cardiovascular failure.

Because OO2 is your randomized controlled trial being conducted in a similar patient population that will be studied in the phase III program we conducted an ad hoc [tying two] event statistical analysis of the OO2 results obtained at this interim analysis.

In the Kaplan-Meier graph to the left placebo controlled patients receiving the best standard of care for diabetic kidney disease are shown on the black line. These patients are gathering adverse events at a greater rate and more frequently than REACT treated patients shown in the blue line.

That can be seen in the lower right REACT reduced the risk of triggering the component from the primary end-point by 60% in patients with an average EGFR of 33 ml per minute resulting in a [hazard] ratio of 0.4 with a low [P] value. It is noteworthy to compare the [hazard] ratio for REACT using patients at high-risk of end-stage renal disease who recently reported EGLT2 use in healthier patients with average EGFRs of 43 to 56 ml per minute also using a composite end-point.

ProKidney controls the REACT supply chain from biopsy to injection to ensure the highest quality product all manufacturing is conducted in ProKidney’s manufacturing facilities. ProKidney’s bio process and quality manufacturing procedures have been developed over the past 15 years using patented processes that have been reviewed by both the FDA and the European Medicines Agency.

Over the past seven years 100% of REACT doses have been manufactured, shipped and injected in all REACT clinical trials. ProKidney’s manufacturing facilities have been inspected by the European Medicines Agency and considered phase III commercial ready. We are conducting advanced bioprocess research and development for the manufacturing process to ensure commercial cost of goods support a robust business model.

The manufacturing process starts with the biopsy and ends with an injection into the patient’s kidney. The entire process from biopsy to injection takes a total of 10 weeks. Five to ten doses are manufactured from each patient’s biopsy. All manufacturing is conducted to the highest quality and regulatory standards to ensure the best product is provided for each patient. Our manufacturing facility has been inspected by regulatory agencies from the U.S. and E.U. and is approved for phase III and commercial manufacturing of REACT.

ProKidney has a staged manufacturing strategy to ensure we can deliver all products for the phase III program can be prepared for early commercial launch. In preparation for commercialization and market ramp we are initiating plans for a launch facility that would be production ready after phase III registration. Additional plants will be planned and developed after launch to address up to 65,000 patients with CKD per year.

Commercial facilities will be designed to optimize cost of goods and large scale supply chain efficiencies.

Proceeds from this capital raise will be used to support the Company to registration. Our current funding requirements include capital for continuing the phase III program planned and ongoing phase II programs, commercial readiness and capital expenses. Financial needs are approximately 450 million which will take us to mid-2024 for the interim analysis of the phase III program.

An upsized capital raise of 700 million will allow for increasing manufacturing capacity, and expanding sales and marketing.

Thank you for your attention and interest in the ProKidney story. I will now turn it back to Chamath to discuss with you the transaction overview. Chamath.

Chamath Palihapitiya: Thanks, Tim. So, to summarize what do we know the problem to be? Well, again, just to recap 75 million people suffer from CKD and ESRD in the United States and EU. More than 12 million people develop CKD in the United States and Europe every year.

What is our goal? Our goal is to find a solution that, obviously, slows and stabilizes but ideally reverses the decline of kidney function so that we can delay or prevent dialysis and renal transplantation. Tim and his team have built a solution called REACT, which utilizes these proprietary autologous cell therapy taken from the patient’s own kidney.

Ultimately what that results in three specific cell types that helps promote the re-growth of all kidney function. What you’ve heard is that we are building a financing plan and a capital plan that allows us to scale a very large phase III clinical program, monitor it very closely, obviously, in a partnership with the FDA and the EMA.

We have conditional approval potential based on this interim data analysis that could be possible in 2024. But realistically we’re targeting commercial launch in 2025. And the goal is to ultimately treat millions of diabetic CKD patients worldwide and meaningfully reduce the number of people on dialysis or that require transplantation each year.

Specifically, in terms of the transaction, the pre-money equity value of this business is $1.75 billion. The pro-formatic re-value is around 2.64 billion with all the capital that comes in. There is up to 250 million in the SPAC’s trust account. There’s also a $575 million pipe that we have raised.

Affiliates of DNAC, including myself have committed approximately 155 million and existing ProKidney investors have committed at least 50 million. And then existing ProKidney equity holders will roll over 100% of exiting consisting equity. And they will hold around 66% of the pro forma equity in the combined company.

Around 12% of the pro forma equity will be held by DNAC’s sponsors and public shareholders, and 22% of the pro forma equity will be held by the pipe investors. And then lastly, is that there is an earn-out for ProKidney’s existing management and equity holders of 17.5 million shares that will trigger in three installments of 5.8 million share increments at $15, $20, and $25 per share.

Which is to say that as they perform and create equity value for everybody then they will be able to participate in those gains as well. And then lastly as Tim has said but to reiterate the point of all of the capital right now is to make sure that we fully fund this phase III trial of REACT.

That we can make some early progress in manufacturing and commercial build-out, and have some money as well for some other general corporate purposes so that on the presumption of a successful phase III trial and approval in 2025 or thereabouts we can hit the ground running and really bring this solution to as many millions of patients as possible.

And with that, I would like to thank you for tuning in and your support.

ProKidney CEO Memo

Subject: Exciting News to Share about ProKidney’s Future

Dear Colleagues,

We have all been working tirelessly to develop REACT and prepare for our first ever Phase 3 development program, a critical next step in ProKidney’s mission to bring transformational care to CKD patients around the world.

I am pleased to share that this morning we announced a major milestone toward making this mission a reality: ProKidney will become a publicly traded company via a business combination with Social Capital Suvretta III (SCS), a special purpose acquisition company (SPAC). This business combination will provide ProKidney up to $825 million to fund REACT’s Phase 3 development program, accelerate our manufacturing buildout, and be even better capitalized as we prepare for REACT’s anticipated global commercial launch in late 2025 to mid-2026. You can read the news release [here – insert link].

We will hold an all-employee gathering today, January 18, 2022 at 12 PM EST, to discuss this announcement in greater detail and answer some of your questions (calendar invitation to follow).

I want to share some background on why we chose this path forward, why we think it is best for ProKidney, and what it means for you.

For those of you who may not be familiar with these types of transactions, SPACs are companies that raise money from public market investors and then merge with a private operating company, such as ProKidney. The result is the private company – in this case ProKidney – becomes publicly traded. In our case, we will trade on the Nasdaq under the symbol “PROK.”

This is a significant step, and we are thrilled about the opportunities that the additional capital and benefits of being a public company will create for us over the near and long term.

Importantly, we are doing this with SCS because they are the perfect partner for us at such a key inflection point in our company’s trajectory. As you all know, a successfully executed Phase 3 trial will be critical for our path ahead and plans to bring REACT to patients around the world – and we look forward to benefiting from SCS’s track record of working with innovative companies like ProKidney.

For a bit of background, SCS is a partnership between leading investment firm Social Capital (led by Chamath Palihapitiya) and Suvretta Capital (led by Kishen Mehta). SCS was created to partner with innovative, agile biotech companies like ProKidney to help them realize their full potential at critical business junctures.

Page 1 of 2

Now many of you might be wondering: What does it mean to be publicly traded? Will SCS “own” or “operate” ProKidney? And ultimately what does this mean for me? For the vast majority of you, your day-to-day responsibilities will not change. Our executive leadership team and board of directors will work closely with SCS on our business execution and growth strategy and, ultimately, this transaction will enable us to continue the good work we already have in progress.

Further, this announcement is just the first step in going public. We expect the transaction to close in the third quarter of 2022, following approval by SCS’s shareholders and other customary closing requirements. In the meantime, ProKidney will continue to operate as we always have.

While this is an exciting moment, becoming a public company means we are all more restricted in what we can say about ProKidney and this transaction. To that end, if you receive any inquiries from external parties, we ask that you refer them to our announcement press release. For those of you in regular contact with outside parties, we will share specific instructions for how to handle those conversations. We ask that you do not discuss anything beyond what’s included in those guidelines.

If you are approached by any media or investors, please do not respond and instead forward their inquiries to Janet Bridge (janet.bridge@prokidney.com).

You should all be incredibly proud of what we’ve accomplished to get to this milestone – but the journey is just beginning! As we continue to work toward realizing our mission, we must remain diligent, humble, and grounded in our work – focused delivery is more critical now than ever.

On behalf of the executive leadership team, I want to extend our immense gratitude for your continued dedication and hard work. Without you, none of this would be possible, and I am as proud and excited as ever to be on this journey with all of you.

Best,

Tim Bertram

Page 2 of 2

All Hands Meeting – Company Update January 2022 Tim Bertram, Chief Executive Officer

Announcement Overview What is a SPAC & Why Social Capital Suvretta? What’s Next? What this Means for You Important Communications Guidelines Closing Remarks Q&A Today’s Agenda 3

Announcement Overview ProKidney will become a publicly traded company via a business combination with a special purpose acquisition company – or SPAC – called Social Capital Suvretta, or SCS. This transaction is expected to provide ProKidney with up to $825 million to fund REACT’s Phase 3 development program, accelerate our manufacturing buildout, and even better capitalize us as we prepare for REACT’s anticipated global commercial launch in late 2025 to mid-2026. We will trade on the Nasdaq under the symbol “PROK.”

Rationale At ProKidney, we are on the forefront of something monumental. Now is the right time for us to take this crucial step. Raising capital through the public markets will provide us access to additional funding and resources, supporting REACT’s Phase 3 development program as well as our eventual global launch. Chronic kidney disease (CKD) is one of the most prevalent and expensive medical conditions to treat. For the first time, there is a disease-modifying cell therapy with the potential to not only slow the progression of CKD, but in some cases drive meaningful improvement in kidney function. We are distinguished by: Our promising Phase 2 clinical trial results; The opportunity to make a difference for millions of patients globally; Our robust manufacturing capabilities and clear go-to-market strategy; and Our experienced, dedicated team.

What is a SPAC? Opportunity to vastly improve the quality of life for more than 75M people with CKD in the U.S. and EU, as well as millions of other people around the world SPACs are companies that raise money from public market investors and then merge with a private operating company – in this case ProKidney – and in the process, the private company becomes a public company. Being a public company will create additional capital and benefits for ProKidney over the near and long term. A number of other prominent and successful companies have chosen to go public through SPAC transactions, including several in the biotech industry, such as:

Why Social Capital Suvretta? Management Team Chamath Palihapitiya Founder and CEO, Social Capital Chamath Palihapitiya is Founder and CEO of Social Capital, whose mission is to advance humanity by solving the world’s hardest problems. Kishen Mehta Portfolio Manager of the Averill strategy, Suvretta Capital Management Kishen Mehta is currently responsible for Suvretta’s healthcare-focused investment strategy, Averill, which attempts to identify companies that are disruptive to the healthcare industry. SCS is the perfect partner for us at such a critical next stage of our journey. SCS is a partnership between leading investment firm Social Capital and Suvretta Capital. Formed to partner with innovative, agile biotechnology companies and help them realize their full potential at critical business junctures. Has a deep track record of working with innovative companies like ours and extensive investor relationships. Team has deep respect and admiration for the work we have done.

What’s Next? Transaction will close in the third quarter of 2022, subject to approval by SCS’s shareholders and other customary closing conditions.

What this Means for You For the vast majority of you, your day-to-day responsibilities will not change. Everything remains business as usual – our executive leadership team, your roles, and managers will all remain the same. Our executive leadership team and Board of Directors will work closely with SCS on our business execution and growth strategy. Our dedication to our company mission – to change the lives of tens of millions of CKD patients through a first-of-its-kind disease-modifying autologous cellular therapy – remains the same.

Important Communications Guidelines As a public company, we may receive more attention than we have previously, and we are all more restricted in what we can say about ProKidney and this transaction than we were before. If you receive any inquiries from external parties, please refer them to our announcement press release. For those of you in regular contact with outside parties as part of your job, we have shared specific instructions for how to handle those conversations. Please do not discuss anything beyond what’s included in those guidelines. If you are approached by any media or investors, please do not respond and instead forward any inquiries to Janet Bridge (janet.bridge@prokidney.com).

Thank You

Q&A

Additional Information and Where to Find It In connection with the proposed transaction, Social Capital Suvretta Holdings Corp. III (“SCS”) intends to file a preliminary proxy statement and a definitive proxy statement with the U.S. Securities and Exchange Commission (the “SEC”). SHAREHOLDERS OF SCS ARE ADVISED TO READ, WHEN AVAILABLE, THE PRELIMINARY PROXY STATEMENT, ANY AMENDMENTS THERETO, THE DEFINITIVE PROXY STATEMENT AND ALL OTHER RELEVANT DOCUMENTS FILED OR THAT WILL BE FILED WITH THE SEC IN CONNECTION WITH THE PROPOSED TRANSACTION AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. HOWEVER, THIS DOCUMENT WILL NOT CONTAIN ALL THE INFORMATION THAT SHOULD BE CONSIDERED CONCERNING THE PROPOSED TRANSACTION. IT IS ALSO NOT INTENDED TO FORM THE BASIS OF ANY INVESTMENT DECISION OR ANY OTHER DECISION IN RESPECT OF THE PROPOSED TRANSACTION. When available, the definitive proxy statement will be mailed to the shareholders of SCS as of a record date to be established for voting on the proposed transaction. Shareholders will also be able to obtain copies of the preliminary proxy statement, the definitive proxy statement and other documents filed with the SEC that will be incorporated by reference therein, without charge, once available, at the SEC’s website at http://www.sec.gov. The documents filed by SCS with the SEC also may be obtained free of charge at SCS’s website at https://socialcapitalsuvrettaholdings.com/dnac or upon written request to 2850 W. Horizon Ridge Parkway, Suite 200, Henderson, NV 89052. Participants in the Solicitation SCS and ProKidney, LP (“ProKidney”) and their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from SCS’s shareholders in connection with the proposed transaction. A list of the names of such directors and executive officers and information regarding their interests in the proposed transaction between ProKidney and SCS will be contained in the proxy statement when available. You may obtain free copies of these documents as described in the preceding paragraph. No Offer or Solicitation This communication shall not constitute a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the proposed transaction. This communication shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any states or jurisdictions in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such state or jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended or an exemption therefrom.