UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

10-K

(Mark One)

☒

Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

for the

fiscal year

December 31, 2023

or

☐

Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

for the transition period from to .

Commission File Number

001-41058

VAXXINITY, INC.

(Exact name of registrant as specified in its charter)

Delaware

86-2083865

(State or other jurisdiction of incorporation or organization)

(IRS Employer Identification No.)

505 Odyssey Way

Merritt Island

,

FL

32953

(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code:

(

254

)

244-5739

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbol

Name of exchange on which registered

Class A Common Stock, par value $0.0001 per

share

VAXX

The

Nasdaq

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes

☐

No

☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes

☐

No

☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of

1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days.

Yes

☒

☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405

of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such

files).

Yes

☒

☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or

an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth

company" in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer

☐

Accelerated Filer

☐

Non-Accelerated Filer

☒

Smaller Reporting Company

☒

Emerging Growth Company

☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any

new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal

control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that

prepared or issued its audit report.

☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in

the filing reflect the correction of an error to previously issued financial statements.

☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

☐

No

☒

The aggregate market value of registrant’s voting and non-voting outstanding common stock held by non-affiliates was approximately $

155.6

based upon the closing stock price of issuer’s common stock on June 30,

2023

, the last business day of the registrant’s most recently completed second

fiscal quarter. Shares of common stock held by each officer and director and by each person who may be deemed to be affiliates of the Company. This

determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of March 25, 2024, the registrant had

112,873,552

13,874,132

par value Class B common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following document are incorporated by reference in Part III of this Report: the registrant’s definitive proxy statement relating to its

2024 Annual Meeting of Shareholders. We currently anticipate that our definitive proxy statement will be filed with the SEC no later than 120 days

after December 31, 2023, pursuant to Regulation 14A of the Securities Exchange Act of 1934, as amended.

1

TABLE OF CONTENTS

3

44

92

92

93

93

93

94

94

94

104

106

134

134

134

134

134

134

134

134

134

Item 15.

135

137

138

2

PART I

Unless otherwise indicated in this report, “Vaxxinity ,” “we,” “us,” “our,” and similar terms refer to Vaxxinity, Inc. and our consolidated

subsidiaries.

SPECIAL NOTE REGARDING FORWARD -LOOKING STATEMENTS

This Annual Report on Form 10-K for the year ended December 31, 2023 (“Report”) contains forward-looking statements. Forward-

looking statements are neither historical facts nor assurances of future performance. Instead, they are based on our current beliefs,

expectations and assumptions regarding the future of our business, future plans and strategies and other future conditions. In some cases,

you can identify forward-looking statements because they contain words such as “anticipate,” “believe,” “estimate,” “expect,” “intend,”

“may,” “predict,” “project,” “target,” “potential,” “seek,” “will,” “would,” “could,” “should,” “continue,” “contemplate,” “plan,” other

words and terms of similar meaning and the negative of these words or similar terms.

Forward-looking statements are subject to known and unknown risks and uncertainties, many of which may be beyond our control. We

caution you that forward-looking statements are not guarantees of future performance or outcomes and that actual performance and

outcomes may differ materially from those made in or suggested by the forward-looking statements contained in this Report. In addition,

even if our results of operations, financial condition and cash flows, and the development of the markets in which we operate, are

consistent with the forward-looking statements contained in this Report, those results or developments may not be indicative of results

or developments in subsequent periods. New factors emerge from time to time that may cause our business not to develop as we expect,

and it is not possible for us to predict all of them. Factors that could cause actual results and outcomes to differ from those reflected in

forward-looking statements include, among others, the following:

• the prospects of UB-612 and other product candidates, including the timing of data from our clinical trials and our

ability to obtain and maintain regulatory approval for our product candidates;

• our ability to develop and commercialize new products and product candidates;

• our substantial doubt about our ability to continue as a going concern;

• our ability to leverage our AIM Platform (defined below);

• the rate and degree of market acceptance of our products and product candidates;

• decreased demand for our COVID-19 product candidate, if and when such product candidate is approved;

• our status as a clinical-stage company and estimates of our addressable market, market growth, future revenue,

expenses, capital requirements and our needs for additional financing;

• our ability to comply with multiple legal and regulatory systems relating to privacy, tax, anti-corruption and other

applicable laws;

• our ability to hire and retain key personnel and to manage our future growth effectively;

• competitive companies and technologies, including existing third party approved and market accepted products in our

industry and our ability to compete;

• our and our collaborators’, including United Biomedical’s (“UBI”), ability and willingness to obtain, maintain, defend

and enforce our intellectual property protection for our proprietary and collaborative product candidates, and the scope

of such protection;

• the performance of third-party suppliers and manufacturers and our ability to find additional suppliers and

manufacturers;

• our ability and the potential to successfully manufacture our product candidates for pre-clinical use, for clinical trials

and on a larger scale for commercial use, if approved;

• the ability and willingness of our third-party collaborators to continue research and development activities relating to

our product candidates;

• general economic, political, demographic and business conditions in the United States, Taiwan and other jurisdictions;

3

• the potential effects of government regulation, including regulatory developments in the United States and other

jurisdictions;

• our ability to obtain additional financing in future offerings;

• our ability to maintain our listing on The Nasdaq Global Market;

• expectations about market trends; and

• the effects of the ongoing conflicts between Russia and Ukraine or Israel and Hamas and increased tension between

Taiwan and China on business operations, the initiation, development and operation of our clinical trials and patient

enrollment of our clinical trials.

We discuss many of these factors in greater detail under Item 1A. “Risk Factors.” These risk factors are not exhaustive and other sections

of this report may include additional factors which could adversely impact our business and financial performance. Given these

uncertainties, you should not place undue reliance on these forward-looking statements.

You should read this Report and the documents that we reference in this Report and have filed as exhibits completely and with the

understanding that our actual future results may be materially different from what we expect. We qualify all of the forward- looking

statements in this Report by these cautionary statements. Except as required by law, we undertake no obligation to publicly update any

forward-looking statements, whether as a result of new information, future events or otherwise.

Item 1. Business.

Overview

We are a purpose-driven biotechnology company committed to positively impacting humanity by democratizing healthcare across the

globe. Our metric for success is simple: amount of human suffering alleviated. We doggedly pursue this as our north star, and aim to be

number one in the world at this metric. Our vision is to redefine the paradigm for tackling the global epidemic of chronic diseases, and

provide cheaper, safer, more convenient and effective medicines to all.

There are many inventions that have served thousands of lives, and some that have benefited a million lives, but only a select few that

have saved billions lives. These include the innovations of fertilizer of the green revolution to feed an exponentially growing population,

hygienic plumbing to control cholera and typhoid, and vaccines to prevent over 20 dangerous or deadly diseases. We believe that we

have a technological innovation in medicine with the potential for a billion-person impact within the chronic disease epidemic.

Today’s approach to treating patients suffering from chronic disease is focused on and increasingly dominated by drugs, particularly

monoclonal antibodies (“mAbs”), which can be highly efficacious but remain limited by prohibitive costs, cumbersome administration,

and restricted scale. We believe our synthetic peptide-based Active Immunotherapy Medicines Platform (“AIM Platform” formerly

called the Vaxxine Platform) has the potential to enable a new class of medicines that will improve the quality and convenience of care,

reduce costs and increase access to treatments for a wide range of indications. Moreover, we believe that due to the unique features of

our AIM Platform, these new medicines can enable an expansion from treating sick patients to prevention of illness in healthy people.

Medicine is only as effective as its access, and we believe there is a path to increasing the number of people who have access to

immunotherapies from less than 1% of the world today to nearly anyone that could benefit.

Our AIM Platform is designed to harness the immune system to convert the body into its own “mAb drug factory,” stimulating the

production of antibodies with a therapeutic or protective effect. While traditional vaccines have been able to leverage this approach

against infectious diseases, they have historically been unable to resolve key challenges in the fight against chronic diseases. We believe

our AIM Platform has the potential to overcome these challenges and to bring the efficiency of vaccines to a whole new class of medical

conditions. Our technology has been commercialized independently in billions of doses of animal health vaccines, tested in over four

thousand human subjects across multiple candidates and clinical trials, including the company’s first completed Phase 3 study. Our

current pipeline consists of five chronic disease product candidates from early to late-stage development across multiple therapeutic

areas, including Alzheimer’s Disease (“AD”), Parkinson’s disease (“PD”), migraine and hypercholesterolemia, diseases that collectively

affect billions of people in the world today and of which hundreds of millions more are at high risk of contracting. Additionally, we

believe our AIM Platform may be used to disrupt the treatment paradigm for a wide range of other chronic diseases, including any that

are or could potentially be successfully treated by mAbs. We have assembled an industry-leading team with extensive experience

developing successful drugs that is committed to realizing our mission of alleviating the greatest amount of suffering we can in the

world. Our website address is www.vaxxinity.com. The information contained on, or that can be accessed through, our website is not

part of, and is not incorporated into, this Report.

4

The Chronic Disease Epidemic

More people today are suffering from a chronic disease than ever before. Chronic diseases kill 41 million people each year, or 74% of

all deaths globally. These diseases are ongoing, generally incurable illnesses or conditions that gradually onset and tend to be of long

duration such as heart disease, cancer and AD.

Less than a century ago, the chronic disease and disability prevalence was about 7.5% in adults in the U.S. By 2000, the proportion of

Americans with at least one chronic disease had grown to 45%, and today, only two decades later, it has grown to 60% of all adults. The

proportion with multiple chronic diseases has similarly skyrocketed to 40% of adults in the U.S. today. Overall, chronic disease accounts

for 70% of deaths and nearly 90% of overall healthcare expenditure in the U.S.

The epidemic is not limited to the U.S. or the developed world. To the contrary, chronic diseases disproportionately affect low- and

middle-income countries (LMICs) where 77% of all chronic disease deaths occur. Each year, 17 million people die of a chronic disease

before age 70, and 86% of these premature deaths occur in LMICs. According to the World Health Organization (“WHO”), chronic

disease is closely linked with poverty in what can become a vicious cycle. More limited access to health services by socially

disadvantaged people underlies increased incidence of chronic disease. Meanwhile, healthcare costs for treatment of these diseases,

which often become lengthy and expensive, can quickly drain household resources. The WHO estimates millions of people are forced

into poverty annually due to chronic disease.

Limitations of the Current Healthcare Paradigm

Since 2000, there have been over 700 new medicines approved by the FDA, mostly to treat chronic illnesses, and yet the chronic disease

epidemic continues to grow.

We believe that medicine is only as effective as its access, and many of the newest medicines are limited to less than 1% of the world’s

patient population. The current healthcare paradigm favors the development of drugs that are primarily intended for the U.S. market, for

niche indications and for treatment of disease rather than prevention. Furthermore, these drugs are expected to be sold at price points

that are only accessible to healthcare systems in developed countries, and even within those systems, to a small subset of patients.

One class of drugs in particular exemplifies the current environment: biologics, especially mAbs. In 2022, biologics represented seven

of the fifteen top selling drugs, of which six were mAbs. The global market for mAbs totaled approximately $202 billion in 2022,

representing over 60% of the total sales for all biopharmaceutical products. While mAbs can provide life-altering care with generally

favorable safety characteristics and significant health benefits for the patients who receive them, regular in-office transfusions and annual

treatment costs, which can exceed hundreds of thousands of dollars, present challenges to both patients and payors. These price and

administration hurdles cause mAb treatments to be available to only a fraction of the population who could benefit from them.

Furthermore, mAbs are often restricted to moderate to severe disease and to later lines of treatment due to their high cost, rather than

prevention or early intervention in disease.

Thus, due to their cost and administrative burden, mAbs account for less than 2% of all prescriptions in the U.S., and, based on internal

estimates, less than 1% worldwide. Meanwhile, the alternative to mAb treatments tends to be small molecules, which are sometimes

more accessible to patients, but are often comparatively less effective with more significant side effects. Collectively, this perpetuates a

profound inequity in healthcare access, domestically but even more so globally, that we believe represents a tremendous social and

market opportunity.

Our Scalable AIM Platform Solution

Our vision is to disrupt the existing paradigm of chronic disease treatment with a new class of active immunotherapeutic medicines that

can potentially improve the health of more people, more conveniently, for less money.

Our AIM Platform is designed to harness the immune system to convert the body into its own “drug factory,” to stimulate the production

of antibodies with a therapeutic or protective effect, and to be scaled to supply millions or even billions of persons. In contrast,

monoclonal antibodies are developed, produced and purified outside the body and then transfused into the patient on a regular basis, as

frequently as bi-weekly. Therefore, mAbs are inherently less efficient than active immunotherapies, or vaccines, which instead stimulate

antibody production within the patient’s immune system, requiring both less active material and less frequent treatments. However,

while traditional vaccines have historically been successful at addressing infectious diseases, previous attempts to utilize vaccines to

address chronic disease have not achieved both acceptable safety and efficacy. Our AIM Platform technology contains modular

components that can be rapidly custom-designed to mimic select biology and activate the immune system, enabling our product

candidates to break immune tolerance when targeting self-antigens, a property observed across multiple clinical and pre-clinical studies.

Our AIM Platform depends heavily on intellectual property licensed from UBI and its affiliates, a related party and a commercial partner

for us, who first developed the synthetic peptide vaccine technology utilized by our AIM Platform. The formulation of our peptide-

based product candidates relies on contract manufacturers at this time, including both related parties as well as third-party manufacturers.

5

We believe our AIM Platform has the potential to generate product candidates with attributes that collectively offer significant

advantages over both mAbs and small molecule therapeutics, and that some of these advantages may allow for use in a first-line or a

prevention setting for population health level diseases:

•

Cost and Scalability

: Whereas monoclonal antibodies require costly and complex biological manufacturing

processes, our manufacturing process is chemically based and highly scalable, and requires lower capital expenditures. Our AIM

Platform has been designed and tested to produce on a scale of hundreds of millions of doses of GMP manufactured material. In addition,

we design our product candidates to generate antibody production in the body, thus requiring meaningfully less drug substance relative

to mAbs, leading to commensurately lower costs.

•

Administration and Convenience

: Our product candidates are designed to be injected in quarterly or longer

intervals via intramuscular injection similar to a flu shot. We believe this offers considerable convenience compared to mAbs, which

can require up to bi-weekly dosing via intravenous infusion or subcutaneous injections, and small molecules, which often require daily

dosing. We are also in the early stages of exploring additional modes of administration, including intradermal delivery that may be

administered in an at-home setting, potentially offering enhanced convenience to patients.

•

Efficacy

: In our clinical trials conducted to date, our product candidates have yielded high response rates

(90% or above at target dose levels for UB-311, UB-312, UB-313, and UB-612), high target-specific antibodies against self-antigens

(as seen in UB-311, UB-312, and UB-313 clinical trials) and long durations of action (for UB-311 based on titer levels remaining

elevated between doses, and UB-612 based on half-life). We have observed target engagement in patient CSF in a Phase 1 clinical trial

of our UB-312 program. See our descriptions of these clinical trials under “—Our Product Candidates.” Our AIM Platform also enables

the combining of multiple target antigens into a single formulation. For indications that could be treated more effectively with a

multivalent approach, we believe our AIM Platform would have an advantage over other modalities. Further, because our AIM Platform

is designed to elicit endogenous antibodies, we believe our product candidates may lessen or avoid altogether the phenomenon of anti-

drug antibodies which has limited the efficacy of certain mAbs over time. Finally, we believe that the improved convenience of our

product candidates as compared to mAbs has the potential to lead to increased adherence by patients and therefore improve overall

effectiveness of our candidates.

•

Safety

: Based on our clinical trials to date, our product candidates have been well tolerated. We aim to offer

product candidates with safety profiles at least comparable to the relevant mAb or small molecule alternative for the relevant disease.

Our Targeted Impact

Our current pipeline addresses leading areas of unmet medical need, from AD to heart disease, impacting nearly 3.5 billion persons

worldwide, and resulting in over 8 million annual deaths and $4 trillion dollars in economic impact globally. The following table depicts

our R&D pipeline.

As used in the chart above, “IND” signifies a program has begun investigational new drug (“IND”)-enabling studies.

Our pipeline consists of five lead programs focused on chronic disease, particularly neurodegenerative disorders, in addition to other

neurology and cardiovascular indications. For each candidate, we believe the targeted biology has been validated or de-risked either

through published genetic evidence or by a successfully licensed mAb against the same target.

6

Neurodegenerative Disease Programs:

•

UB-311

: Targets toxic forms of aggregated amyloid-beta (“Aβ”) in the brain to fight AD, a disease

affecting 44 million people worldwide, resulting in 1.6 million annual deaths and over $3 trillion in estimated economic cost. Phase 1,

Phase 2a and Phase 2a Long Term Extension (“LTE”) trials have shown UB-311 to be well tolerated in mild-to-moderate AD subjects

over three years of repeat dosing, with a safety profile comparable to placebo, with no cases of amyloid-related imaging

abnormalities-edema (“ARIA-E”) observed in the main Phase 2a trial, and only one case of ARIA-E in the LTE trial, which was

clinically not significant according to the study investigator. UB-311 was also shown to be immunogenic, with a high responder rate

and antibodies that bind to the desired target. Although not powered for statistical significance, the Phase 2a trial showed dose-

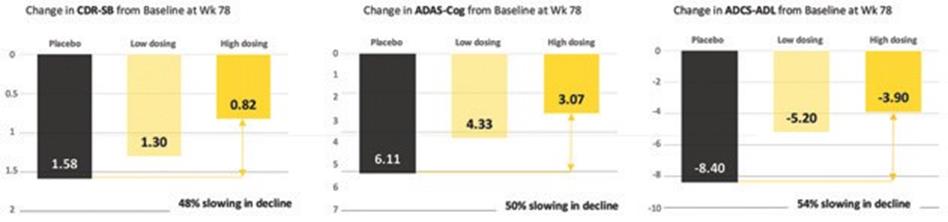

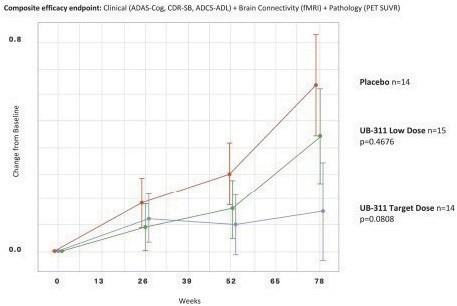

dependent trends of slowing of cognitive decline by 48% versus placebo, as measured by CDR-SB. We held an End of Phase 2

meeting with the U.S. Food and Drug Administration (“FDA”) and have aligned upon a large scale efficacy trial, which, pending data,

could potentially support initial licensure of UB-311 for the treatment of early AD. The FDA granted UB-311 Fast Track Designation

in the second quarter of 2022. The expected timing of the next clinical trial will be determined based upon the timing of additional

financing or a strategic partnership.

•

UB-312

: Targets toxic forms of aggregated α-synuclein (“aSyn”) in the brain and peripheral tissues to fight

PD and other synucleinopathies, such as Lewy body dementia (“LBD”) and multiple system atrophy (“MSA”), diseases together

affecting 16 million people worldwide, resulting in 400,000 annual deaths and over $80 billion in estimated economic cost. Part A and

Part B of a Phase 1 trial in healthy volunteers and Parkinson’s patients, respectively, have been completed and have shown UB-312 to

be well tolerated, with no significant safety findings, and immunogenic, with a high responder rate and antibodies that cross the blood-

brain barrier (“BBB”). UB-312-induced antibodies were observed in the serum and CSF of both healthy volunteers and PD patients,

and showed preferential binding to aggregated aSyn and almost no binding to normal monomeric aSyn. Two exploratory biomarkers

were evaluated as measures of target engagement: aggregated aSyn as measured by a semi-quantitative seed amplification assay

(“SAA”), and phosphorylated aSyn (pS129 aSyn). PD patients with UB-312-induced antibodies in the CSF showed a significant

reduction from baseline in pathological aSyn in the CSF compared to the placebo group as measured by both SAA and pS129 aSyn.

A

post hoc

daily living versus placebo, as measured by the MDS-UPDRS II clinical scale. We believe UB-312 is the first immunotherapy

candidate to show data of reduction of pathological aSyn in CSF of PD patients. The next step will be to conduct a Phase 2 trial to

optimize a dose regimen and to confirm target engagement in PD patients.

•

VXX-301

: We are developing an anti-tau product candidate that has the potential to address multiple

neurodegenerative conditions, including AD, traumatic brain injury (“TBI”) and chronic traumatic encephalopathy (“CTE”) by targeting

abnormal tau proteins alone and in potential combination with other pathological proteins such as Aβ to address multiple pathological

processes at once. TBI is estimated to affect 56 million people worldwide and is attributed to approximately 2 million deaths annually.

Our lead candidate targets multiple epitopes of tau and has been shown in preclinical studies to reduce tau spreading and improve

survival in animal models. In an effort to focus internal resources, we have decided to continue the development of VXX-301 only

through a preclinical research collaboration with the University of Florida, which has received a grant from the state of Florida in support

of this project.

Next Wave Chronic Disease Programs:

•

VXX-401

: Targets proprotein convertase subtilisin/kexin type 9 serine protease (“PCSK9”) to lower low-

density lipoprotein (“LDL”) cholesterol and reduce the risk of cardiac events. Today, cardiovascular disease is the leading killer in the

world, accounting for over 18 million annual deaths, affecting both developed and developing countries. Over 2 billion people have

high cholesterol globally. As of October 2023, we have expanded the ongoing first-in-human clinical trial of VXX-401 in Australia to

include two higher dose cohorts due to its favorable safety and tolerability profile to that point, for a total of six cohorts. In the first

quarter of 2024, we submitted a protocol amendment to add a booster dose to these two higher dose cohorts. We expect to report initial

topline data from this trial in mid-2024, with results from the booster dose later in the second half of 2024.

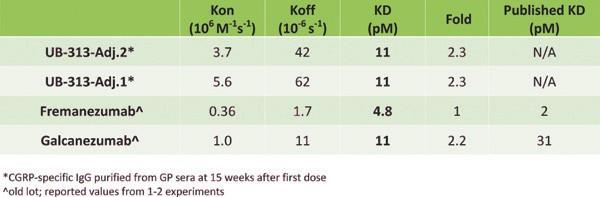

•

UB-313

: Targets Calcitonin Gene-Related Peptide (“CGRP”) to fight migraines, a disease affecting over 1

billion people worldwide, resulting in an estimated over 45 million years lived with disability annually. In 2023, we completed a first-

in-human Phase 1 clinical trial in healthy volunteers in which UB-313 was generally well tolerated and immunogenic: all subjects who

received three doses of UB-313 (31 out of 31) developed anti-CGRP antibodies; however, serum antibody titers were lower than

expected, and due to this lower immunogenicity, UB-313 did not meet the trial’s secondary objective of capsaicin-induced dermal blood

flow inhibition. We believe this was the result of a suboptimal drug product made by a new contract manufacturer, and we have identified

the necessary steps to manufacture a more immunogenic product consistent with prior lots and the known immunogenic potential of our

platform candidates. In an effort to focus internal resources, we have deprioritized this program and are not currently planning on running

another Phase 1 at this time.

Given the global COVID-19 pandemic and our AIM Platform’s applicability to infectious disease, we also have advanced a product

candidate that addresses SARS-CoV-2.

7

COVID-19

•

UB-612

: Employs a “multitope” subunit protein-peptide approach to neutralizing the SARS-CoV-2 virus,

meaning the product candidate is designed to activate both antibody and cellular immunity against multiple viral epitopes. A Phase 3

trial evaluating UB-612 as a heterologous boost against SARS-CoV-2, head-to-head versus homologous boosts of VNT162b2

(mRNA), ChAdOx1-S (adenovirus), and BIBP (inactivated virus), was initiated in the first half of 2022 with funding support from the

Coalition of Epidemic Preparedness Innovations (“CEPI”). In December 2022, we announced positive topline data: UB-612 met

primary and key secondary endpoints, eliciting non-inferior neutralizing antibody titers and seroconversion rates (“SCR(s)”), defined

as a 4-fold or greater increase in neutralizing antibodies from baseline, against both Wuhan and Omicron BA.5 variants as compared

to BNT162b2, and superior neutralizing antibody titers and SCRs against both variants as compared to ChAdOx1-S and BIBP. UB-

612 was well tolerated with balanced reactogenicity and no additional safety risks evoked over the licensed COVID-19 comparators.

There were no serious adverse events (“SAEs”) related to UB-612 reported through 12 months of safety follow-up. Phase 1 and Phase

2 trials of UB-612 have also shown UB-612 to be well tolerated, with over 7,500 doses administered to over 3,750 subjects. In March

2023 we completed rolling submissions for conditional/provisional authorization with regulatory authorities in the United Kingdom

and Australia, who are reviewing under their established work share agreement. In November 2023, the MHRA conducted GMP

inspections of our overseas CMO facilities responsible for UB-612 manufacture. We believe a decision on authorization will be made

in 2024.

We believe our AIM Platform has application across a multitude of chronic and infectious disease indications beyond our existing

pipeline. We are developing additional product candidates that we believe may address significant unmet needs both within and beyond

our current pipeline’s therapeutic areas.

Our Team

We have assembled an experienced group of executives with deep scientific, business and leadership expertise in pharmaceutical and

vaccine discovery and development, manufacturing, regulatory and commercialization. Mei Mei Hu, our co-founder and Chief

Executive Officer, has been a member of the executive committee of UBI since 2010. Our board of directors is chaired by our co-

founder Louis Reese, who has been a member of the executive committee of UBI since 2014. Our research efforts are guided by

highly experienced scientists and physicians on our leadership team including Dr. Jean-Cosme Dodart, our Senior Vice President of

Research. Our leadership team contributes a diverse range of experiences from leading companies including AstraZeneca, Eli Lilly,

Genentech, Merck, and Pharmacyclics, and were executives in multiple successful mAb and vaccine launches.

As of December 31,

2023, we have assembled an exceptional team of 53 employees, the majority of whom hold Ph.D., M.D., J.D. or Master’s degrees. We

also have a highly experienced scientific advisory board consisting of leading doctors and scientists in relevant therapeutic areas.

Our Strategy

Our mission is to alleviate the most human suffering possible by developing active immunotherapy product candidates that improve the

quality of care for chronic diseases and are accessible to all patients across the globe. In order to achieve this mission, we seek to:

•

Advance our chronic disease pipeline through clinical stage development

: We plan to advance UB-311,

UB-312, and VXX-401 through clinical stage development for the treatment or prevention of chronic diseases, either ourselves or with

a strategic partner. We believe that our differentiated AIM Platform will enable our product candidates, if approved and successfully

commercialized, to potentially disrupt the current treatment paradigm for their respective indications. However, there can be no

guarantee that we will obtain regulatory approval or commercialize of any such product candidates.

•

Expand our pipeline of product candidates

: Chronic diseases are prevalent globally and expected to worsen

over the next several decades. In furtherance of our mission, we plan to expand our pipeline by developing new product candidates that

address additional indications. In expanding our pipeline, we rely on our proprietary filtering methodology, which evaluates potential

product candidates across five principal criteria – (i) probability of technical and regulatory success, (ii) addressable market, (iii)

development cost, (iv) competitive dynamics and (v) disruptive potential.

•

Continue to improve our AIM Platform

: In addition to, and in conjunction with, our product candidate

development efforts, we are continuously working to improve and enhance the richness, breadth and effectiveness of our AIM Platform.

As our AIM Platform further develops, we believe that we can both increase the speed and efficiency of developing product candidates,

improve the probability of technical success of our product candidates, and increase the number of product candidates in concurrent

development.

•

Maximize the value of our product candidates through potential partnerships

: We currently retain worldwide

rights for all of our product candidates and will consider entering into development and commercialization partnerships with third parties

that align with our mission on an opportunistic basis.

8

Background and Limitations of Traditional Vaccines and Monoclonal Antibodies

The immune system, the body’s mechanism for fighting off potential threats, is comprised of cells that form the innate and adaptive

immune responses. The main purpose of the innate immune system is to immediately prevent the spread and movement of foreign

pathogens throughout the body. The adaptive immune response is specific to the pathogen presented to T-cells and B lymphocytes (“B-

cells”) and leads to an enhanced response upon future encounters with those antigens. Antibodies represent an important tool within the

adaptive immune system’s arsenal. Upon detection of a potential threat, B-cells produce antibodies that recognize, bind to and eliminate

the threatening pathogen. Over time, the immune system develops the ability to produce countless types of antibodies, each finely tuned

against a specific threat.

Generally, the immune system is able to function effectively by neutralizing viruses, bacteria and even self-generated cells and proteins

from within our own bodies that could cause harm if unchecked. However, as powerful as the immune system is, there are threats that

it cannot overcome on its own, generating the need for medicine. Conventional forms of medicine include small molecules (e.g.,

antibiotics), which can inhibit or promote action within the body by, for instance, binding to a receptor on the surface of a cell, or directly

inducing toxic effects upon bacteria. These medicines do not necessarily modulate the immune system directly in order to work. Instead,

they work alongside it. While small molecules have provided substantial benefits to human health, they are typically not designed to

interact with the immune system. They may also have limited efficacy in cases where an immune response to a target can be used against

a chronic condition.

Vaccines

In the first part of the twentieth century, vaccines revolutionized healthcare by directly interacting with, and modulating, the immune

system — training it to recognize a dangerous pathogen by introducing the immune system to a relatively harmless form of the pathogen,

its toxins or one of its surface proteins, thereby promoting the body’s own production of binding antibodies. Once immunized to a

specific pathogen, the immune system can recognize it and generate the antibodies to fight it more quickly and robustly.

Traditional vaccine technologies have generally focused on the prevention of bacterial and viral infections and not on chronic disease.

In chronic disease settings, the disease-causing agents frequently come from within the body. These self-antigens are proteins that

become too abundant, misfolded or aggregated such that they can no longer perform their healthy function and even may induce toxic

effects. The body can sometimes produce antibodies against such proteins, but this often falls short of providing the right types of

antibodies in the right concentrations to ward off disease. Historically, vaccine technologies developed to target these proteins have been

unable to break immune tolerance — that is, the immune system’s general avoidance of reactivity towards self-antigens — with an

acceptable level of reactogenicity. The challenges faced by prior efforts to advance vaccine technologies for chronic diseases included

low response rates, low titer levels, off- target responses and other safety concerns such as T-cell mediated inflammation.

Monoclonal Antibodies

The first mAbs were developed in the later part of the twentieth century. In contrast to vaccines, which prompt the body to produce

antibodies, mAbs are antibodies manufactured outside of the patient’s body and then injected or infused into the body to recognize and

eliminate harmful targets. Monoclonal antibodies have revolutionized the standard-of-care treatment for many chronic diseases.

However, manufacturing mAbs is often an expensive and complex process and administering mAbs is cumbersome, sometimes requiring

infusions as frequently as bi-weekly. These factors have generally limited mAbs’ availability to moderate-to-severe disease, to later

lines of therapy and to wealthier geographies, thus denying access to a substantial portion of the patients who could benefit from them.

Finally, patients on mAbs often experience a loss of effectiveness over time due to a phenomenon known as anti-drug antibodies,

whereby the immune system begins to recognize therapeutic mAbs as foreign, and mounts a response against them, eventually mitigating

their efficacy.

Our AIM Platform

Our AIM Platform is designed to stimulate the patient’s own immune system to generate antibodies and overcome the limitations of

traditional vaccines to target self-antigens safely and effectively in chronic diseases. Our product candidates have broken immune

tolerance against self-antigens consistently. As described in the section titled “Our Product Candidates” below, across seven clinical

trials, we have consistently observed that our product candidates have stimulated the development of antibodies against the desired

target at relevant doses in clinical trial subjects, including the elderly. We have observed favorable tolerability and reactogenicity of our

product candidates across studies of UB-311, UB-312, UB-313, and UB-612, with no significant safety findings to date. We aim to

develop product candidates that are more convenient, more cost-effective and more accessible to large patient populations, with safety

profiles at least comparable to relevant mAbs and small molecule treatments. We believe our product candidates have the potential to

eventually not only capture meaningful market share from mAbs and small molecules, but more importantly, to provide therapeutic

benefit to large patient populations who currently receive neither form of treatment and thereby open up the broadest access to patients.

This would represent an unprecedented shift in the treatment paradigm, potentially providing better global access to treatments that have

been previously limited to the wealthiest nations. In particular, we believe our treatments for chronic disease could reflect the following

benefits as compared with the relevant mAbs and small molecule alternatives:

9

Characteristics of our Product Candidates versus Monoclonal Antibodies and Small Molecules

History and Design

Our AIM Platform utilizes a peptide vaccine technology first developed by UBI and subsequently refined over the last two decades,

with more than three billion doses of animal vaccines commercialized to date. UBI initiated the development of this technology for

human use; the business focused on human use was then separated from UBI through two separate transactions: a spin-out from UBI in

2014 of operations focused on developing chronic disease product candidates that resulted in United Neuroscience, a Cayman Islands

exempted company (“UNS”), and a second spin-out from UBI in 2020 of operations focused on the development of a COVID-19 vaccine

that resulted in C19 Corp., a Delaware corporation (“COVAXX”). Our current company, Vaxxinity, Inc., was incorporated under the

laws of the State of Delaware on February 2, 2021 for the purpose of acquiring UNS and COVAXX in March of 2021.

On March 2, 2021, in accordance with a contribution and exchange agreement among Vaxxinity, UNS, COVAXX and the UNS and

COVAXX stockholders party thereto (the “Contribution and Exchange Agreement”), the existing equity holders of UNS and COVAXX

contributed their equity interests in each of UNS and COVAXX in exchange for equity interests in Vaxxinity (the “Reorganization”).

In connection with the Reorganization, (i) all outstanding shares of UNS and COVAXX preferred stock and common stock were

contributed to Vaxxinity and exchanged for like shares of stock in Vaxxinity, (ii) the outstanding options to purchase shares of UNS

and COVAXX common stock were terminated and substituted with options to purchase shares of Class A common stock in Vaxxinity,

(iii) the outstanding warrant to purchase shares of COVAXX common stock was cancelled and exchanged for a warrant to acquire

Class A common stock in Vaxxinity, and (iv) the outstanding convertible notes and a related party not payable were contributed to

Vaxxinity and the former holders of such notes received Series A preferred stock in Vaxxinity. On December 31, 2022, COVAXX was

merged into Vaxxinity in order to simplify the corporate structure.

UBI has used its capabilities in peptide technology for innovations across an array of business endeavors: antibody testing for human

diagnostics, animal health vaccines and the manufacture of medical products. Its innovative products include one of the first approved

peptide-based blood antibody tests in the world (for HIV), one of the first approved peptide vaccines against an infectious disease in the

world in animal health (for a food-and-mouth disease virus) and one of the first approved peptide vaccines against a self-antigen in the

world in animal health (an anti-luteinizing hormone-releasing hormone (“LHRH”) vaccine used for the immunocastration of swine).

Grant funding from the National Institutes of Health supported some of UBI’s work in the fields of vaccines and antibody testing. To

commercialize its animal health vaccine business, UBI and its affiliates scaled up GMP vaccine manufacturing to over 500 million doses

per year and partnered with a top-ten animal health company for commercialization of its anti-LHRH vaccine; all together, UBI’s

technology platform is utilized for the vaccination of approximately 25% of the global swine population annually.

We are advancing our peptide-based AIM Platform to develop product candidates that target chronic diseases and COVID-19. Our AIM

Platform comprises a proprietary, custom, rationally designed antigen capable of evoking an immune response (an “immunogen”)

formulated with a proprietary CpG oligonucleotide. The immunogen contains several advanced synthetic peptide domains, including B-

cell epitopes, T-helper (“Th”) peptide carrier constructs and peptide linkers. This composition enables us to achieve a highly specific

immune response to the target antigen, with limited inflammation and off-target effects that could cause reactogenicity. This design

process has evolved into a repeatable series of well-defined steps, which has enabled the development of our current pipeline of product

candidates.

10

Key Elements of our AIM Platform Constructs and Formulations

When developing a product candidate, we use publicly available information and sophisticated bioinformatics tools to investigate the

entire protein structure of a target in a comprehensive manner to identify functional B-cell epitopes that may provide optimal antigens.

We then synthesize peptides that mimic these identified antigens to elicit highly specific antibodies against these B-cell epitopes. To

yield favorable tolerability profiles, we screen our product candidates for lack of toxicity as well as reactogenicity, and design them not

to elicit T-cell mediated inflammation. To enhance effectiveness, we seek to optimize the size and sequence of our custom peptides to

elicit a robust, specific antibody response when linked to a carrier molecule.

We then attach a proprietary carrier molecule, an artificial Th carrier peptide that delivers the synthetic peptide into cells. Traditional

vaccines have faced challenges in achieving specific responses because they rely on conjugating an antigen to a large toxoid carrier

molecule, to which most of the antibody response is directed, causing off-target effects such as inflammation. In our pre-clinical trials

and clinical trials to date, our product candidates have displayed specific immunogenicity, or the ability to stimulate a targeted immune

response, thereby greatly reducing potential off-target effects and increasing the potential for our product candidates to be well tolerated

and efficacious. We have observed that our carrier molecules have produced consistent results across multiple species and against

multiple targets in seven human clinical trials to date.

11

Our Product Candidate Does Not Induce an Antibody Response against its Carrier Molecule

The graph above illustrates that our peptide carriers induce a strong immune response against the target antigen, and a minimal immune

response against themselves, as compared to traditional vaccines formulated with other types of carrier molecules.

Our peptide carriers have short sequence lengths; we design them with the aim that they are not antigenic on their own and do not

stimulate cytotoxic T-cells. The carriers’ sequences model those found in natural pathogens, so they are recognized by T-helper cells.

This encourages robust T-helper cell exposure and promotes activation of other immune cells. In turn, B-cells are exposed to the B-

cell antigen and begin antibody production against the antigen, while avoiding an antibody response to the carrier.

Our library of peptide carriers enables the use of different carrier molecules or different combinations of carrier molecules, which

allows us to potentially regulate the speed of immune response onset as well as the magnitude and duration of that response. For

example, a longer duration of response would allow for less frequent dosing. In the case of vaccines for infectious diseases, where T-

cell mediated activity is desirable, our AIM Platform also affords the flexibility to design immunogen constructs that specifically

promote cytotoxic T-cell activity when warranted.

We utilize proprietary linker constructs to fuse our peptide carriers with our custom peptide antigens. These linkers are designed to

promote binding of both B-cell and T-helper epitopes to their respective receptors, contributing to a B-cell response. They may enhance

the immune response by enabling conformational changes to optimize presentation of the B-cell epitope to antigen-presenting cells

(“APCs”), such as dendritic cells (“DCs”).

Our AIM Platform also enables the construction of candidates that target multiple epitopes in a single formulation, whether on multiple

targets or a single target. In certain cases, targeting multiple epitopes of a single target could promote increased target engagement.

Combinations of therapies targeting different molecular mechanisms are common in treating neurologic, cardiovascular, psychiatric,

metabolic, respiratory, infectious and oncologic disease. Our AIM Platform’s favorable cost of goods and efficient manufacturing

process could allow for viable multi-target therapies in a single formulation. This concept could be applied in an array of potential

therapeutic areas. Our current pipeline has candidates against amyloid-β, α-synuclein and tau; targeting of two or more of these at the

same time might prove more effective than any single-target therapy in some patients. Pre-clinical data to date suggests that we can

elicit antibody titers against all three targets in a single formulation. In contrast, multi-target therapy with mAbs would compound the

cost and administration burdens as compared to single-target mAb therapy.

12

Immunogenicity of Single- Versus Multi-Target Formulations in Guinea Pigs

Guinea pigs (three per dose) were immunized with either single-target or multi-target formulations, then serum was drawn and antibody

titers compared via enzyme immunoassays (“EIA”). Multi-target formulations elicited similar titer levels against each target as their

corresponding single-target formulations. This suggests we can create product candidates with multiple neurodegenerative targets in a

single formulation and achieve sustainable titer levels.

Product Candidate Formulations

In addition to our immunogen construct, each product candidate formulation includes custom CpG oligonucleotides and adjuvant

selection. CpG oligonucleotides are negatively charged, and we utilize proprietary CpG configurations to stabilize the positively charged

peptides. This stabilization acts to optimize display of the B-cell epitope to the immune system. In this way, the primary function of

CpG oligonucleotides in our formulations is that of an excipient.

A potential secondary function of CpG is that of an adjuvant. Certain CpG configurations are known to act as immunostimulants and

promote direct cytotoxic T-cell activity, while others do not. Accordingly, our selection of the specific CpG modality is highly dependent

on the target indication. For infectious disease indications, the T-cell response generated by the CpG configuration is independent and

in addition to that of the T-cell response generated by the peptide carrier.

The final formulation includes the addition of an adjuvant, such as a well-recognized, alum-derived Adju-Phos or Alhydrogel to further

enhance the immunogenicity of our product candidate. Alum-derived adjuvants are commonly used in vaccines to promote an immune

response. This is not the same adjuvant used in other companies’ failed neurodegenerative vaccine candidates.

How our Product Candidates are Designed to Function

Our immunogens stimulate the body’s adaptive immune system to produce antibodies against a variety of antigen targets, including

secreted peptides or proteins, degenerative or dysfunctional proteins and membrane proteins, as well as infectious pathogens. The

mechanism of action involves the following sequence of steps:

1. The immunogen is taken up by an APC, such as a DC. Antigen uptake leads to DC maturation and migration

to the draining lymph nodes where the DCs interact with CD4+ T-helper cells.

2. DCs engulf and process the antigen internally and present the T-helper epitope on major histocompatibility

complex (“MHC”) Class II molecules. The presentation activates immunogen-specific CD4+ T-helper cells causing them to mature,

proliferate and promote B-cell stimulatory activity.

3. B-cells with receptors that recognize the target B-cell epitope bind, internalize and process the immunogen.

The binding of the B-cell receptor to the immunogen provides the first activation signal to the B-cells.

4. When B-cells function as APCs and present the T-helper epitope on MHC Class II molecules, interaction

with immunogen-specific CD4+ T-helper cells provides a second activation signal to B-cells, which causes them to differentiate into

plasma cells.

5. B-cell epitope-specific plasma cells produce high affinity antibodies against the target B-cell epitope. Of

particular importance for targets located in the central nervous system (“CNS”), these antibodies are produced in sufficient

concentrations to cross the BBB.

13

Overview of How our Product Candidates Function

Importantly, from both clinical trials and pre-clinical studies, we have observed the rapid expansion of antibodies upon administration

of a booster of our product candidates. Based on the available data to date, we can infer that while antibody titers decline with time after

administration, a small number of memory B-cells and antibody secreting cells are maintained in the lymphoid organs, spleen or bone

marrow. We believe this is important because if a patient misses a dose of our product candidate, they may be able to recall the antibody

response, and therefore the therapeutic effect of the antibodies, with a single booster, even after a long period of time has passed.

AIM Platform Immunogenicity upon Re-dosing

As shown in the above graph, a rapid antibody response is elicited by a booster dose of UB-311 given 72 weeks after the priming

regimen.

Furthermore, the antibodies elicited by our product candidates have different properties than those of mAbs targeting similar pathology.

In general, we aim to achieve binding affinity, specificity and functionality similar or improved compared to mAbs targeting similar

pathology. We use Bio-Layer Interferometry (ForteBio

®

) to compare the binding kinetics (K

ON

, K

OFF

, and K

D

) of antibodies elicited by

14

our product candidates versus mAbs. We also use Western blot or slot blot to evaluate the binding specificity of antibodies elicited by

our product candidates against the normal, toxic, misfolded or aggregated forms of the target protein. We use immunohistochemical

analyses to observe the binding of antibodies to pathological inclusions on tissue sections, such as brain sections of patients. Moreover,

we use cell-based models and animal models to measure the induced antibodies’ functionality. Additionally, a major challenge in mAb

drug discovery is that mAbs are prone to induce an immune response against themselves, resulting in a potential

inactivation/neutralization of the mAb by the host (i.e., the patient). This is not a concern with our vaccine approach as each patient will

produce its own antibodies against the target. Finally, mAbs have a potential for off-target binding, which could result in non-specific

binding leading to safety and toxicity issues. We believe that this is unlikely to happen using our technology since antibodies elicited

by our product candidates are designed to break immune tolerance against specific targets and should not trigger an immune response

against other self-peptides or proteins.

Product Candidate Selection Process

Because our AIM Platform may have applicability across a range of chronic diseases, we employ a proprietary filtering methodology to

best identify new product candidates for development. We evaluate potential product candidates across five principal criteria:

•

Probability of technical and regulatory success

: We examine the probability of success for a product

candidate based on stage of development and therapeutic area, and then make target-specific adjustments for design difficulty, industry

knowledge and clarity of biological mechanism, general safety risk and estimated titer level required for therapeutic effect. This criterion

accounts for the known validity of a given target in the relevant disease context.

•

Market opportunity

: We account for the prevalence, unmet need and drug market size for each likely

indication associated with a given target, as well as the number of potential indications.

•

Development cost

: We estimate the cost of development through BLA submission, the time to submission

and the number of patient-years to proof-of-concept.

•

Competitive advantages

: We evaluate the extent to which the advantages of our AIM Platform compare to

the current and potential future standard of care, including convenience, dosing, safety, efficacy and cost.

•

Disruptive opportunities

: We evaluate the extent to which the potential disruptive properties of our AIM

Platform may play a role in treatment paradigms, including the ability to “leap-frog” mAbs and treat patients in earlier lines of treatment,

to be used as a prophylactic, to include multiple targets in a single formulation and to be used as an adjuvant therapy.

After assigning values to each criterion for a given product candidate, we weight each criterion according to a confidential algorithm,

and thereby prioritize product candidates for development. We update these values on a regular basis based on new scientific literature,

trial results and our AIM Platform advancements.

As an example, in light of these criteria, AD and other neurodegenerative diseases that involve misfolded proteins are an attractive area

for development. First, as the field has gained knowledge and clinical experience around the biology of targeting aberrant proteins with

antibodies, the relative technical, safety and regulatory risk has decreased. For instance, with two FDA-approved products targeting Aβ

for AD, Aβ has been validated as a target. Both AD and PD have high prevalence worldwide, and large unmet need with limited or no

disease-modifying products readily available to patients. Moreover, the underlying pathologies often begin years or decades before

symptoms may appear and as a result, early intervention in the disease state, as well as prevention or delay of onset strategies, may be

optimal and more practically achievable with a vaccine approach. While mAbs can target the pathology, they face the limitations of

high cost, cumbersome and inefficient administration and limited access, and are not suited for early treatment or prevention, which we

believe provides a disruptive opportunity for our AIM Platform.

We believe that our AIM Platform, and our strategy more generally, will create a significant opportunity for drug development well

beyond our current pipeline of clinical and pre-clinical indications, in therapeutic areas including allergy (e.g., atopic dermatitis, chronic

rhinosinusitis, , food allergy), autoimmune disease (e.g., psoriasis, psoriatic arthritis, Crohn’s disease), pain (e.g., peripheral neuropathy,

diabetic neuropathy) and bone and muscle atrophy (e.g., sarcopenia, osteoporosis, osteopenia).

Underlying Drivers of Our Platform Advantages

Our AIM Platform’s properties drive the unique combination of attributes that we believe will be reflected in our product candidates:

•

Cost and Scalability

: Whereas monoclonal antibodies require costly and complex biological manufacturing

processes, our manufacturing process is chemically based and highly scalable, and requires lower capital expenditures. Our AIM

Platform has been designed and tested to produce on a scale of hundreds of millions of doses of GMP manufactured material. In addition,

we design our product candidates to generate antibody production in the body, thus requiring meaningfully less drug substance relative

to mAbs, leading to commensurately lower costs.

15

•

Administration and Convenience

: Our product candidates are designed to be injected in quarterly or longer

intervals via intramuscular injection similar to a flu shot. We believe this offers considerable convenience compared to mAbs, which

can require up to bi-weekly dosing via intravenous infusion or subcutaneous injections, and small molecules, which often require daily

dosing. We are also exploring additional modes of administration, including intradermal delivery that may be administered in an at-

home setting, potentially offering enhanced convenience to patients.

•

Efficacy

: In our clinical trials conducted to date, our product candidates have yielded high response rates

(90% or above at target dose levels for UB-311, UB-312, UB-313, and UB-612), high target-specific antibodies against self-antigens

(as seen in UB-311, UB-312, and UB-313 clinical trials) and long durations of action (for UB-311 based on titer levels remaining

elevated between doses, and UB-612 based on half-life). We have observed target engagement in patient CSF in a Phase 1 clinical trial

of our UB-312 program. See our descriptions of these clinical trials under “—Our Product Candidates.” Our AIM Platform also enables

the combining of multiple target antigens into a single formulation. For indications that could be treated more effectively with a

multivalent approach, we believe our AIM Platform would have an advantage over other modalities. Further, because our AIM Platform

is designed to elicit endogenous antibodies, we believe our product candidates may lessen or avoid altogether the phenomenon of anti-

drug antibodies which has limited the efficacy of certain mAbs over time. Finally, we believe that the improved convenience of our

product candidates as compared to mAbs has the potential to lead to increased adherence by patients and therefore improve overall

effectiveness of our candidates.

•

Safety

: Based on our clinical trials to date, our product candidates have been well tolerated. We aim to offer

product candidates with safety profiles at least comparable to the relevant mAb or small molecule alternative for the relevant disease.

Additionally, we believe our AIM Platform possesses important benefits reflected at the platform level, as opposed to the product

candidate level:

•

Product Candidate Discovery

: Our AIM Platform enables the efficient iteration of product candidates in the

discovery phase through rapid, rational design and formulation. We are able to screen in high throughput rapidly and at low cost. Upon

nominating a target for drug discovery, we can formulate several dozen product candidate compounds for preliminary in vivo

immunogenicity and cross-reactivity screening within 2 to 3 months. This process allows nonviable product candidates to “fail fast” and

allows us to carry top product candidates forward through subsequent pre-clinical development to lead identification. In contrast,

biologics require the maintenance and adjustment of living cultures to design, formulate and iterate, and therefore discovery and early

development is inherently less efficient.

•

Process Development

: Scaling the formulation of a drug product from research grade to clinical grade, then

to commercial grade, typically consumes a great deal of resources. This, together with the development of assays for quality control and

quality assurance, comprise process development. We leverage our manufacturing expertise, originally developed alongside UBI and

certain of its affiliates, to enable rapid scale-up of the manufacture of both clinical and commercial compounds that use our AIM Platform

technology. Unlike process development for mAbs, which has inherent challenges such as risk of contamination in cell culture or

bioreactors and time-consuming adjustments to cell lines for any formulation adjustment, our peptide platform relies on synthetic peptide

chemistry, which is more reproducible and scalable, and relatively quick to manipulate for any modifications.

Our Product Candidates

Neurodegenerative Disease Programs

Neurodegenerative diseases are a collection of conditions defined by progressive nervous system dysfunction, degeneration or death of

neurons, which can cause cognitive decline, functional impairment and eventually death. Neurodegeneration represents one of the most

significant unmet medical needs of our time due to an aging population and lack of effective therapeutic options.

Two of the most common neurodegenerative diseases are AD and PD. In the United States, currently more than six million people suffer

from AD, and approximately one million people suffer from PD according to estimates from the Alzheimer’s Association and the

Parkinson’s Disease Foundation, respectively. As a result, AD and PD bring a heavy burden on our society’s cost of care. The direct

costs of AD treatment in the United States were estimated at $321 billion in 2022 according to a study published by the American

Journal of Managed Care, and are projected to exceed $1 trillion by 2050. The financial burden of PD exceeded $50 billion in the United

States in 2019. Many more people around the world suffer from these two diseases and their related social and economic implications.

UB-311

An Overview of Alzheimer’s Disease

Alzheimer’s disease is a progressive neurodegenerative disorder that slowly affects memory and cognitive skills and eventually the

ability to carry out simple tasks. Its symptoms include cognitive dysfunction, memory abnormalities, progressive impairment in activities

16

of daily living and a host of other behavioral and neuropsychiatric symptoms. The exact cause of AD is unknown, but genetic and

environmental factors are established contributors. AD affects more than six million people in the United States and 44 million

worldwide. The global economic burden of AD is expected to surpass $2.8 trillion by 2030.

Many molecular and cellular changes take place in the brain of a person with AD. Aβ plaques and neurofibrillary tangles of tau protein

in the brain are the pathological hallmarks of the disease. Several pathological or toxic forms of Aβ and tau seem implicated in the

disease process, leading to loss of neurons and neuronal connectivity underlying the signs and symptoms of AD.

The Aβ protein involved in AD comes in several different pathological forms that accumulate in the brain parenchyma. Soluble species

of Aβ (e.g., oligomers) can directly disrupt normal synaptic and neuronal functions. They may also contribute to tau pathology.

Research is ongoing to better understand how, and at what stage of the disease, the various forms of Aβ influence AD.

Neurofibrillary tangles are abnormal accumulations of a protein called tau that collect inside neurons. Healthy neurons are supported

internally, in part, by structures called microtubules, which help to guide nutrients and molecules from the cell body to the axon and

dendrites. In healthy neurons, tau normally binds to and stabilizes microtubules. In AD, abnormal chemical changes cause tau to detach

from microtubules and to stick to other tau molecules, forming threads that eventually join to form tangles. These tangles block the

neuron’s transport system, which harms the synaptic communication between neurons.

Converging lines of evidence suggest that AD-related brain changes may result from a complex interplay among Aβ proteins, abnormal

tau, and several other factors. It appears that abnormal tau accumulates in specific brain regions involved in memory. Concurrently, Aβ

clumps into plaques between neurons. As the level of Aβ reaches a tipping point, tau rapidly spreads throughout the brain. In addition

to the spread of Aβ and tau, chronic inflammation and its effect on the cellular functions of microglia and astrocytes, as well as changes

to the vasculature, are thought to be involved in AD’s pathology and progression.

In the last three years, the FDA has approved two different mAbs that target Aβ for the treatment of AD.

Limitations of Current Therapies

Two classes of small molecules approved for the treatment of AD’s symptoms are acetylcholinesterase inhibitors (“AChEIs”) and

glutamatergic modulators. AChEIs are designed to slow the degradation of the neurotransmitter acetylcholine, temporarily compensating

for cholinergic deficits. Glutamatergic modulators are designed to block sustained, low-level activation of the N-methyl-D-aspartate

(“NMDA”) receptor, without inhibiting the normal function of the receptor in memory and cognition. However, these therapeutic

products only address the symptoms of AD and do not modify or alter the progression of the underlying disease.

Aducanumab, marketed under the trade name Aduhelm, is a mAb developed by Biogen, Inc. (“Biogen”) that targets aggregated forms

of Aß. The FDA approved aducanumab in June 2021, making it the first approved immunotherapy for AD, the first new FDA-approved

treatment since 2003 and, importantly, the first to receive accelerated approval based on a biomarker. By approving aducanumab on the

basis of biomarker evidence, we believe the FDA set a precedent for developers of neurodegeneration immunotherapies.

Despite the milestone in the treatment of AD that aducanumab’s approval represents, the drug has several limitations, and Biogen

announced its discontinuation in 2024. Approximately one-third of patients experience ARIA-E related adverse events, which can

manifest as symptoms ranging from headaches to confusion to coma. In addition, the drug must be administered monthly via intravenous

infusion in healthcare facilities specifically configured to support an hour-long infusion process with healthcare professionals trained to

administer infusion therapies, creating a burden for patients and additional costs resulting from the complex administration process.

Because of the risk of developing ARIA-E, physicians who prescribe aducanumab must titrate dosing and carefully monitor each patient

using magnetic resonance imaging (“MRI”). This process is costly and burdensome The combination of price, side effects, extra costs,

and extra administration burden highlight the challenges of mAbs. The Center for Medicare & Medicaid Services (“CMS”) decided not

to cover aducanumab, leading to its commercial failure.

Soon after the FDA’s approval of aducanumab, Eli Lilly and Company (“Lilly”) announced that it would file for approval of its anti-Aβ

mAb, donanemab, in 2022 on the basis of Phase 2 data. In January 2023, the FDA declined accelerated approval of donanemab due to

an insufficiently sized safety database in its Phase 2 trial; however, Lilly filed for approval later in 2023 on the basis of Phase 3 data.

In January 2023, the FDA granted accelerated approval to lecanemab, another mAb targeting Aβ, jointly developed by Biogen and Eisai

Co., Ltd. (“Eisai”). Over 12.5% of patients on lecanemab experience ARIA-E, and physicians who prescribe lecanemab must monitor

each patient using MRI. Lecanemab must be administered every two weeks as an intravenous infusion in healthcare facilities specifically

configured to support an hour-long infusion process with healthcare professionals trained to administer infusion therapies, creating a

burden for patients and additional costs resulting from the complex administration process. Biogen and Eisai have set the wholesale

acquisition cost (“WAC”) price of lecanemab in the U.S. at $26,500 for the drug product only, which does not include administration

and ongoing monitoring costs. CMS has decided to cover lecanemab under Medicare Part B with a 20% coinsurance after a patient has

met their Part B deductible.

17

We believe the above examples signify not only the validity of targeting toxic forms of Aβ as a target in AD, but also the practical

limitations of mAbs, which so far despite approval have remained unable to serve a population with high unmet need.

Our Product Candidate: UB-311

We are developing a novel product candidate, UB-311, as a potential disease-modifying therapy for the treatment of AD. We completed

a Phase 1 open label trial (V118-AD) and a Phase 2a randomized, double-blinded, placebo-controlled trial (the “Phase 2a Main Trial”).

We believe that UB-311 may offer several differentiators versus the approved mAbs, including the preferential targeting of aggregated

Aβ oligomers over monomers, longer durability suggesting greater overall exposure, or area under the curve (“AUC”), improved

convenience in dosing and administration, a safety and tolerability profile comparable to placebo with potentially limited ARIA-E, and

an ability to broaden patient access with greater cost-effectiveness and scalability. No signs of ARIA-E related adverse events were

reported in the Phase 2a Main Trial despite more than two-thirds of the study participants being APOE4 carriers.

Post hoc

analyses of UB-311’s Phase 2a clinical data also suggest that quarterly dosing of UB-311 might slow cognitive decline in some subjects

by up to 50% when compared to placebo, as measured by Clinical Dementia Rating Sum of Boxes (“CDR-SB”), Alzheimer’s Disease

Assessment Scale – Cognitive Subscale (“ADAS-Cog”), Alzheimer’s Disease Cooperative Study – Activities of Daily Living (“ADCS-

ADL”) and Mini-Mental State Examination (“MMSE”) scores, all clinically validated measures of cognition or function in AD. In this

small Phase 2a study, these were secondary measures, as the study was not designed to assess cognitive decline. Although our Phase 2a

trial was a proof-of-concept study, not powered to demonstrate significant changes in any endpoint, we believe the data are suggestive

of potential therapeutic efficacy and may lead to clinical benefit.

UB-311 is formulated for intramuscular administration on a dosing schedule of every three or six months. In addition, manufacturing

costs lower than those of mAbs may support meaningfully lower pricing and access to larger patient populations. We believe such

advantages of UB-311, if ever approved for use, could position it not only to disrupt the emerging mAb-based treatment for early AD