UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-23654

MAINSTAY CBRE GLOBAL

INFRASTRUCTURE MEGATRENDS

FUND

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

30 Hudson Street

Jersey City, New Jersey 07302

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 576-7000

Date of fiscal year end: May 31

Date of reporting period: May 31, 2022

| Item 1. | Reports to Stockholders. |

MainStay CBRE Global Infrastructure Megatrends Fund

Message from the President and Annual Report

May 31, 2022 | NYSE Symbol MEGI

Sign up for e-delivery of your shareholder reports. For full details on e-delivery, including who can participate and what you can receive via e-delivery,

please log in to www.computershare.com/investor.

| Not FDIC/NCUA Insured | Not a Deposit | May Lose Value | No Bank Guarantee | Not Insured by Any Government Agency |

The Fund has adopted a managed distribution policy (the “Distribution Policy”), pursuant to a Securities and Exchange Commission exemptive order, with the goal of providing shareholders with a consistent, although not guaranteed, monthly distribution. In accordance with the Distribution Policy, the Fund currently expects to make monthly distributions to Common shareholders at a distribution rate per share of $0.1083. You should not draw any conclusions about the Fund’s investment performance from the amount of this distribution or from the terms of the Fund's Distribution Policy. The Distribution Policy provides that the Board of Trustees of the Fund may amend or terminate the Distribution Policy at any time without prior notice to Fund shareholders. The Fund does not believe there are any reasonably foreseeable circumstances that would cause the termination of the Distribution Policy. The amendment or termination of the Distribution Policy could have an adverse effect on the market price of the Fund’s shares.

Message from the President

The reporting period from October 27, 2021, through May 31, 2022, began on an optimistic note, with markets buoyed by economic growth and gradual commercial reopening despite a new wave of COVID-19 infections. However, sharply rising inflation, increasing interest rates, mounting geopolitical uncertainty related to Russia’s war in Ukraine and the lingering effects of the pandemic weighed heavily on confidence and drove increasingly turbulent market conditions as the period progressed.

Even before the reporting period began, inflation started to rise in response to government stimulus and accommodative monetary policies. Rising prices were further aggravated by wage increases, pandemic-related supply-chain bottlenecks and commodity price spikes. Market sentiment turned negative in January and February 2022 as aggressive Russian rhetoric regarding Ukraine culminated in Russia’s invasion of its neighbor, a development that exacerbated global inflationary pressures while increasing investor uncertainty. Domestic supply shortages, international trade imbalances and rising inflation caused U.S. GDP (gross domestic product) to contract for the first time since the height of the pandemic, although consumer spending, a primary driver of U.S. economic growth, remained strong. Prices for petroleum surged to multi-year highs and natural gas prices soared, while many key agricultural chemicals and industrial metals reached record levels. The U.S. Federal Reserve responded by raising interest rates 0.25% in March, and followed with a 0.50% increase in May– the largest rate hike in more than two decades.

Although most equity sectors struggled in this environment, the underlying conditions created a favorable backdrop for the MainStay CBRE Global Infrastructure Megatrends Fund. In particular, rising energy prices bolstered returns for companies engaged in the energy transition and electrification of the energy grid, while strong demand for infrastructure assets prompted attractive buyout bids from private infrastructure companies for investments across a wide range of infrastructure areas.

Today, despite the continuing impact of COVID-19, much of the world appears intent on a return to post-pandemic normalcy. Instead, the focus of global political and economic attention has increasingly turned to the war in Ukraine and the impact of rising inflation. Together, Russia and Ukraine account for a substantial share of the world’s supply of food, fossil fuels and raw materials production. Accordingly, the timing and outcome of this conflict will undoubtedly play a major role in global economic developments over the coming months and, possibly, years. The actions of central banks, as they raise interest rates to fight inflation while trying to limit the risks of recession, are likely to further affect global markets and economies.

However these forces impact financial markets in the immediate future, the secular trends on which MainStay CBRE Global Infrastructure Megatrends Fund focuses—decarbonization, asset modernization and digital transformation—are likely to continue playing a major role in shaping the global investment environment over the longer term. We believe that MainStay CBRE Global Infrastructure Megatrends Fund leverages the capabilities of the CBRE Investment Management team’s industry-leading real asset investment expertise, and their unmatched global network and research platform, to provide you with an investment vehicle specifically targeted toward these key trends. It’s one way that New York Life Investments’ multi-boutique approach offers relevant and innovative approaches to help achieve your financial goals.

Kirk C. Lehneis

President

The opinions expressed are as of the date of this report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. Past performance is no guarantee of future results.

Not part of the Annual Report

Certain material in this report may include statements that constitute “forward-looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates and information about possible or future results or events related to the Fund, market or regulatory developments. The views expressed herein are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed herein are subject to change at any time based upon economic, market, or other conditions and the Fund undertakes no obligation to update the views expressed herein.

Fund Performance and Statistics (Unaudited)

Performance data quoted represents past performance of Common shares of the Fund. Past performance is no guarantee of future results. Because of market volatility and other factors, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate. For performance information current to the most recent month-end, please visit newyorklifeinvestments.com/megi.

The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on distributions or the sale of Fund shares.

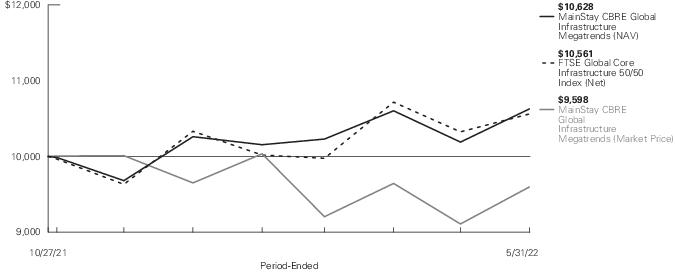

| Cumulative Total Returns for the Period-Ended May 31, 2022 |

| | Since Inception1 |

| Net Asset Value (“NAV”)2 | 6.28 % |

| Market Price2 | (4.02) |

| FTSE Global Core Infrastructure 50/50 Index (Net)3 | 5.61 |

| 1. | The Fund commenced operations on October 27, 2021. |

| 2. | Total returns assume dividends and capital gains distributions are reinvested. For periods of less than one year, total return is not annualized. |

| 3. | The FTSE Global Core Infrastructure 50/50 Index (Net) is the Fund’s primary broad-based securities market index for comparison purposes. The FTSE Global Core Infrastructure 50/50 Index (Net) gives participants an industry-defined interpretation of infrastructure and adjusts the exposure to certain infrastructure sub-sectors. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

Fund Statistics as of May 31, 2022

| NYSE Symbol | MEGI | Premium/Discount 1 | (9.90)% |

| CUSIP | 56064Q107 | Total Net Assets (millions) | $1,077.3 |

| Commencement of Operations | 10/27/2021 | Total Managed Assets (millions)2 | $1,505.2 |

| Market Price | $18.65 | Leverage 3 | 28.43% |

| NAV | $20.70 | | |

| 1. | Premium/Discount is the percentage (%) difference between the market price and the NAV. When the market price exceeds the NAV, the Fund is trading at a premium. When the market price is less than the NAV, the Fund is trading at a discount. |

| 2. | "Managed Assets" is defined as the Fund’s total assets, including assets attributable to any form of leverage minus liabilities (other than debt representing leverage and the aggregate liquidation preference of any preferred shares that may be outstanding). |

| 3. | Leverage is based on the use of funds borrowed from banks or other financial institutions, expressed as a percentage of Managed Assets. |

Portfolio Composition as of May 31, 2022†(Unaudited)

| United States | 39.8% |

| United Kingdom | 11.2 |

| Spain | 9.1 |

| Italy | 6.7 |

| Canada | 6.3 |

| France | 5.9 |

| China | 5.0 |

| Australia | 4.6 |

| Singapore | 4.2% |

| Hong Kong | 3.6 |

| Guernsey | 1.8 |

| Ireland | 0.7 |

| Jersey, C.I. | 0.3 |

| Other Assets, Less Liabilities | 0.8 |

| | 100.0% |

| † | As a percentage of Managed Assets. |

See Portfolio of Investments beginning on page 9 for specific holdings within these categories. The Fund's holdings are subject to change.

Top Ten Holdings and/or Issuers Held as of May 31, 2022 (excluding short-term investments) (Unaudited)

| 1. | National Grid plc |

| 2. | Enel SpA |

| 3. | ONEOK, Inc. |

| 4. | Williams Cos., Inc. (The) |

| 5. | Enagas SA |

| 6. | Enbridge, Inc. |

| 7. | Eutelsat Communications SA |

| 8. | Atlantica Sustainable Infrastructure plc |

| 9. | Edison International |

| 10. | Guangdong Investment Ltd. |

| 6 | MainStay CBRE Global Infrastructure Megatrends Fund |

Portfolio Management Discussion and Analysis (Unaudited)

Questions answered by portfolio managers Jeremy Anagnos, CFA, Daniel Foley, CFA, Hinds Howard and Joseph Smith, CFA, of CBRE Investment Management Listed Real Assets LLC, the Fund’s Subadvisor.

How did MainStay CBRE Global Infrastructure Megatrends Fund perform during the period October 27, 2021 (commencement of operations) through May 31, 2022?

During the reporting period, MainStay CBRE Global Infrastructure Megatrends Fund returned 6.28% at NAV (net asset value) and −4.02% at market price.1

What factors affected the Fund’s performance during the reporting period?

The Fund is exposed to three megatrend themes: decarbonization, asset modernization and digital transformation. During the reporting period, rising energy prices significantly affected the performance of companies in the decarbonization theme, as well as the performance of companies in the asset modernization theme that are part of the energy transition, such as midstream/pipeline companies. Higher energy prices resulted from increased global demand as the world recovered from the depressed COVID-19 economic cycle, in addition to the impact of the Russia/Ukraine war on energy supply. Europe responded to the war by moving toward less reliance on Russian energy, including an acceleration of renewable energy investment. Companies engaged in the energy transition and electrification of the energy grid were beneficiaries of these developments.

Another significant factor affecting performance was the bidding for listed infrastructure companies by large, private infrastructure funds at a significant premium to their share prices. The Fund had three investments receive offers to acquire all outstanding shares by private funds. These investments covered a range of sectors, including data centers, toll roads and utilities. There remains significant capital in the private market seeking core infrastructure assets, and the listed market is a large, liquid pool of high-quality assets trading at a 20-30% discount to the value of those assets in the private market.

What was the impact of the Fund’s distribution policies during the reporting period?

The Fund's managed distribution policy had no effect on the Fund's investment strategy during the reporting period. In December 2021, the Fund announced its inaugural distribution, setting the distribution at a rate that is consistent with the underlying income and expected return of the investments. The distribution policy was set at $1.30/share on an annual basis. Current distribution estimates, as disclosed in recent 19(a) Notices, suggest that the fiscal year-to-date distributions are comprised of net investment income as well as short-term and long-term capital gains. At this time, it is not anticipated that any of the distributions made during the reporting period will be classified as a return of capital. In general, the fixed monthly distribution policy does not affect the Fund's investment strategy. However, the Fund may occasionally need to raise cash to fund the distributions through the sale of portfolio securities at less-than-opportune times. In addition, distributions reduce the net assets of the Fund, which in turn could increase the Fund's expense ratio.

How was the Fund’s leverage strategy implemented during the reporting period?

The Fund established a line of credit with a large financial institution. We monitor the line of credit daily, seeking to optimize the use of this credit facility. The target level of leverage is 30% of the Fund’s managed assets; during the reporting period, the Fund remained close to, but did not exceed, this level.

During the reporting period, which sectors were the strongest positive contributors to the Fund’s performance and which sectors were particularly weak?

Common stock securities generated the bulk of the Fund’s return during the reporting period. The strongest contributions to the Fund’s performance came from investments in the asset modernization theme – specifically shares in companies in the midstream sector classified in the energy transition sub-theme. (Contributions take weightings and total returns into account.) Rising energy prices drove investor interest in the traditional energy market, as the need for energy security, diversity and safety was highlighted by Russia/Ukraine war. In addition, shares in electric utilities in the decarbonization theme that are supporting the electrification of the grid contributed positive returns. These companies offer stable earnings, buoyed by regulation that is relatively unaffected by the macroeconomic challenges weighing on the broad equity market.

The weakest contributors to performance were preferred/convertible preferred and other securities. While this group delivered a positive return of 1.5%, it lagged the return of the Fund’s common stocks, as the majority of the securities in this group offer fixed-income payments, thus making them more interest-rate sensitive.

Among the Fund’s megatrend themes, the digital transformation theme was the weakest, generating a negative 1.0% return. The weak performance in the reporting period reflected a shift in investor sentiment away from growth stocks. The data center, tower, satellite and fiber network owners in this group tend to have higher growth rates and more contracted cash flows, as opposed to regulation that is more demand sensitive.

What were some of the Fund’s largest purchases and sales during the reporting period?

After the initial investment period, the Fund’s largest purchases were shares in Clearway Energy and Mapletree Industrial Trust. Clearway Energy is an owner of contracted renewable generation assets, which falls in the renewable leadership sub-group of the decarbonization megatrend theme. In our opinion, the company is well positioned to continue to grow its portfolio, and the recent addition of TotalEnergies as a major shareholder provides another strong sponsor of renewable projects for the company to acquire in the future. Mapletree Industrial Trust is a Singapore-based real estate investment trust increasingly active in data center investment in Singapore. The company offers an interesting value option in the growing data center market as we believe it has yet to be fully valued based on those assets.

The largest sales during the reporting period included France-based gas utility Engie and Spain-based electric utility Red

| 1. | See page 5 for more information on Fund returns. |

Eléctrica. The Russia/Ukraine war impacted energy markets, particularly in Europe. Rising energy prices led to political pressures to socialize those costs. The Fund sought to limit its exposure to the increasing political risk by reducing its position in Engie; the company procures 30% of its gas volumes from Russia and was an investor in the Nord Stream 2 natural gas pipeline from Russia to Germany, which was denied certification by Germany in the run-up to Russia’s invasion of Ukraine. The Fund continued to retain a smaller position in Engie as the company has a growing renewable generation portfolio and appears well positioned to earn higher cash flows on its fossil-fuel generation assets. The Fund sold its entire position in Red Eléctrica. While the company offered exposure to the electrification theme in Europe, we saw limited growth options and its valuation had risen relative to other opportunities in the region.

How did the Fund’s sector weightings change during the reporting period?

There were no material changes to the Fund’s megatrend theme weightings during the reporting period.

How was the Fund positioned at the end of the reporting period?

As of May 31, 2022, the Fund has allocated 52% of its managed assets to the decarbonization megatrend theme, 34% to asset modernization and 13% to digital transformation. These allocations represent significant exposure to companies playing a role in the decarbonization of the energy market, including companies—such as regulated electric utilities and integrated electric utilities—that are renewable development leaders. Within the asset modernization theme, the Fund holds diversified exposure to companies continuing to underpin the clean energy transition in the midstream sector, as well as companies promoting investment in clean water and transport mobility. Digital transformation remains a key, long-term secular theme in the infrastructure market, reflecting the growing need for new assets to support the storage, processing and transmission of data. We believe the Fund is also well positioned with a mix of 84% of its managed assets in common stock securities and 15% preferred/convertible preferred and other securities.

The opinions expressed are those of the portfolio managers as of the date of this report and are subject to change. There is no guarantee that any forecasts will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

| 8 | MainStay CBRE Global Infrastructure Megatrends Fund |

Portfolio of Investments May 31, 2022†

| | Shares | Value |

| Closed-End Funds 6.0% |

| Guernsey 2.6% (1.8% of Managed Assets) |

| Bluefield Solar Income Fund Ltd. (Decarbonization) | 4,785,487 | $ 7,840,097 |

| Renewables Infrastructure Group Ltd. (The) (Decarbonization) | 11,865,304 | 19,947,115 |

| | | 27,787,212 |

| Jersey, C.I. 0.4% (0.3% of Managed Assets) |

| GCP Asset-Backed Income Fund Ltd. (Asset Modernization) | 3,391,651 | 4,197,428 |

| United Kingdom 3.0% (2.1% of Managed Assets) |

| Foresight Solar Fund Ltd. (Decarbonization) | 5,213,000 | 7,806,305 |

| Greencoat UK Wind plc (Decarbonization) | 9,030,000 | 17,070,188 |

| HICL Infrastructure plc (Asset Modernization) | 3,340,514 | 7,452,185 |

| | | 32,328,678 |

Total Closed-End Funds

(Cost $64,033,379) | | 64,313,318 |

| Common Stocks 111.7% |

| Australia 6.4% (4.6% of Managed Assets) |

| APA Group (Asset Modernization) | 1,797,000 | 14,633,590 |

| Atlas Arteria Ltd. (Asset Modernization) | 7,628,000 | 39,330,067 |

| Aurizon Holdings Ltd. (Asset Modernization) | 5,340,000 | 15,369,553 |

| | | 69,333,210 |

| Canada 7.0% (5.0% of Managed Assets) |

| Enbridge, Inc. (Asset Modernization) | 998,200 | 46,112,050 |

| Pembina Pipeline Corp. (Asset Modernization) | 576,500 | 23,245,049 |

| TransAlta Renewables, Inc. (Decarbonization) | 413,800 | 5,672,840 |

| | | 75,029,939 |

| China 6.9% (5.0% of Managed Assets) |

| Beijing Enterprises Water Group Ltd. (Asset Modernization) | 33,170,000 | 10,982,030 |

| Guangdong Investment Ltd. (Asset Modernization) | 38,701,728 | 48,798,622 |

| Jiangsu Expressway Co. Ltd. Class H (Asset Modernization) | 5,064,000 | 5,233,183 |

| | Shares | Value |

| |

| China (continued) |

| Zhejiang Expressway Co. Ltd. Class H (Asset Modernization) | 10,800,000 | $ 9,510,296 |

| | | 74,524,131 |

| France 8.2% (5.9% of Managed Assets) |

| Engie SA (Decarbonization) | 2,769,985 | 37,246,563 |

| Eutelsat Communications SA (Digital Transformation) | 4,320,677 | 51,303,860 |

| | | 88,550,423 |

| Hong Kong 5.0% (3.6% of Managed Assets) |

| CK Infrastructure Holdings Ltd. (Decarbonization) | 4,329,500 | 29,008,191 |

| Power Assets Holdings Ltd. (Decarbonization) | 3,833,000 | 25,039,676 |

| | | 54,047,867 |

| Ireland 1.0% (0.7% of Managed Assets) |

| Greencoat Renewables plc (Decarbonization) | 8,495,490 | 10,490,156 |

| Italy 9.4% (6.7% of Managed Assets) |

| Atlantia SpA (Asset Modernization) | 362,239 | 8,786,355 |

| Enel SpA (Decarbonization) | 11,479,084 | 74,566,021 |

| Infrastrutture Wireless Italiane SpA (Digital Transformation) | 450,000 | 5,009,904 |

| Terna - Rete Elettrica Nazionale (Decarbonization) | 1,555,497 | 13,181,404 |

| | | 101,543,684 |

| Singapore 5.9% (4.2% of Managed Assets) |

| Keppel Infrastructure Trust (Asset Modernization) | 29,000,000 | 11,949,551 |

| Mapletree Industrial Trust (Digital Transformation) | 4,812,000 | 8,701,031 |

| NetLink NBN Trust (Digital Transformation) | 60,860,000 | 43,073,831 |

| | | 63,724,413 |

| Spain 12.7% (9.1% of Managed Assets) |

| Atlantica Sustainable Infrastructure plc (Decarbonization) | 1,517,400 | 49,543,110 |

| Enagas SA (Asset Modernization) | 2,466,351 | 56,452,465 |

| Endesa SA (Decarbonization) | 1,411,697 | 31,277,616 |

| | | 137,273,191 |

| United Kingdom 12.8% (9.1% of Managed Assets) |

| National Grid plc (Decarbonization) | 5,481,098 | 81,127,172 |

| SSE plc (Decarbonization) | 1,635,607 | 36,549,618 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

9

Portfolio of Investments May 31, 2022† (continued)

| | Shares | Value |

| Common Stocks (continued) |

| United Kingdom (continued) |

| United Utilities Group plc (Asset Modernization) | 1,485,384 | $ 19,813,226 |

| | | 137,490,016 |

| United States 36.4% (26.0% of Managed Assets) |

| American Electric Power Co., Inc. (Decarbonization) | 81,259 | 8,290,855 |

| Clearway Energy, Inc. Class C (Decarbonization) | 453,300 | 15,888,165 |

| Crown Castle International Corp. (Digital Transformation) | 182,529 | 34,616,625 |

| Edison International (Decarbonization) | 705,700 | 49,335,487 |

| FirstEnergy Corp. (Decarbonization) | 596,100 | 25,608,456 |

| Iron Mountain, Inc. (Digital Transformation) | 543,000 | 29,267,700 |

| Kinder Morgan, Inc. (Asset Modernization) | 534,400 | 10,522,336 |

| Medical Properties Trust, Inc. (Asset Modernization) | 466,500 | 8,667,570 |

| OGE Energy Corp. (Decarbonization) | 1,024,500 | 42,311,850 |

| ONEOK, Inc. (Asset Modernization) | 970,000 | 63,874,500 |

| South Jersey Industries, Inc. (Asset Modernization) | 349,100 | 12,166,135 |

| Southern Co. (The) (Decarbonization) | 162,000 | 12,256,920 |

| Uniti Group, Inc. (Digital Transformation) | 1,374,800 | 15,590,232 |

| Williams Cos., Inc. (The) (Asset Modernization) | 1,707,200 | 63,268,832 |

| | | 391,665,663 |

Total Common Stocks

(Cost $1,170,231,485) | | 1,203,672,693 |

| Convertible Preferred Stocks 10.8% |

| United States 10.8% (7.7% of Managed Assets) |

| AES Corp. (The) (Decarbonization) | | |

| 6.875% | 364,900 | 32,695,040 |

| American Electric Power Co., Inc. (Decarbonization) | | |

| 6.125% | 79,107 | 4,499,606 |

| Dominion Energy, Inc. (Decarbonization) | | |

| Series A | | |

| 7.25% | 377,000 | 38,306,970 |

| South Jersey Industries, Inc. (Asset Modernization) | | |

| 8.75% | 1,811 | 126,770 |

| | Shares | Value |

| |

| United States (continued) |

| Southern Co. (The) (Decarbonization) | | |

| Series 2019 | | |

| 6.75% | 560,514 | $ 31,612,990 |

| Spire, Inc. (Asset Modernization) | | |

| Series A | | |

| 7.50% | 169,000 | 9,203,740 |

Total Convertible Preferred Stocks

(Cost $114,361,804) | | 116,445,116 |

| |

| | Principal

Amount | |

| Corporate Bonds 3.6% |

| United States 3.6% (2.6% of Managed Assets) |

| Vistra Corp. (Decarbonization) (a)(b) | | |

| 7.00% (5 Year Treasury Constant Maturity Rate + 5.74%), due 12/15/26 | $ 29,000,000 | 27,810,130 |

| 8.00% (5 Year Treasury Constant Maturity Rate + 6.93%), due 10/15/26 | 11,000,000 | 10,917,500 |

Total Corporate Bonds

(Cost $40,618,001) | | 38,727,630 |

| |

| | Shares | |

| Preferred Stocks 6.7% |

| Canada 1.8% (1.3% of Managed Assets) |

| Algonquin Power & Utilities Corp. (Decarbonization) (b) | | |

| 5.091% | 54,200 | 1,074,273 |

| 5.162% | 62,900 | 1,195,988 |

| AltaGas Ltd. (Asset Modernization) | | |

| 5.393% (b) | 66,300 | 1,294,707 |

| Brookfield BRP Holdings Canada, Inc. (Decarbonization) | | |

| 4.875% (b) | 451,794 | 9,203,044 |

| Enbridge, Inc. (Asset Modernization) (b) | | |

| 4.376% | 244,400 | 3,588,179 |

| 4.46% | 221,400 | 3,345,024 |

| | | 19,701,215 |

| United States 4.9% (3.5% of Managed Assets) |

| CMS Energy Corp. (Decarbonization) | | |

| 5.875% | 377,994 | 9,649,986 |

| Digital Realty Trust, Inc. (Digital Transformation) (b) | | |

| 5.20% | 172,388 | 4,268,327 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

| 10 | MainStay CBRE Global Infrastructure Megatrends Fund |

| | Shares | | Value |

| Preferred Stocks (continued) |

| United States (continued) |

| Digital Realty Trust, Inc. (Digital Transformation) (b) (continued) | | | |

| 5.25% | 161,791 | | $ 3,988,148 |

| 5.85% | 170,000 | | 4,460,800 |

| DTE Energy Co. (Asset Modernization) | | | |

| 5.25% | 145,000 | | 3,548,150 |

| Duke Energy Corp. (Decarbonization) | | | |

| 5.75% (b) | 287,000 | | 7,441,910 |

| NextEra Energy Capital Holdings, Inc. (Decarbonization) | | | |

| 5.65% | 140,000 | | 3,596,600 |

| NiSource, Inc. (Asset Modernization) | | | |

| 6.50% (b) | 286,000 | | 7,418,840 |

| Sempra Energy (Asset Modernization) | | | |

| 5.75% | 148,000 | | 3,707,400 |

| Spire, Inc. (Asset Modernization) | | | |

| 5.90% (b) | 159,620 | | 4,014,443 |

| | | | 52,094,604 |

Total Preferred Stocks

(Cost $77,042,515) | | | 71,795,819 |

Total Investments

(Cost $1,466,287,184) | 138.8% | | 1,494,954,576 |

| Line of Credit Borrowing | (39.6) | | (427,000,000) |

| Other Assets, Less Liabilities | 0.8 | | 9,296,833 |

| Net Assets | 100.0% | | $ 1,077,251,409 |

| † | Percentages indicated are based on Fund net assets applicable to Common Shares. |

| (a) | Floating rate—Rate shown was the rate in effect as of May 31, 2022. |

| (b) | Security is perpetual and, thus, does not have a predetermined maturity date. The date shown, if applicable, reflects the next call date. |

"Managed Assets" is defined as the Fund’s total assets, including assets attributable to any form of leverage minus liabilities (other than debt representing leverage and the aggregate liquidation preference of any preferred shares that may be outstanding), which was $1,505,195,071 as of May 31, 2022.

Investments in Affiliates (in 000's)

Investments in issuers considered to be affiliate(s) of the Fund during the period October 27, 2021 (commencement of operations) through May 31, 2022 for purposes of Section 2(a)(3) of the Investment Company Act of 1940, as amended, were as follows:

| Affiliated Investment Companies | Value,

Beginning

of Period | Purchases

at Cost | Proceeds

from

Sales | Net

Realized

Gain/(Loss)

on Sales | Change in

Unrealized

Appreciation/

(Depreciation) | Value,

End of

Period | Dividend

Income | Other

Distributions | Shares

End of

Period |

| MainStay U.S. Government Liquidity Fund | $ — | $ 944,993 | $ (944,993) | $ — | $ — | $ — | $ 3 | $ — | — |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

11

Portfolio of Investments May 31, 2022† (continued)

The following is a summary of the fair valuations according to the inputs used as of May 31, 2022, for valuing the Fund’s assets:

| Description | Quoted

Prices in

Active

Markets for

Identical

Assets

(Level 1) | | Significant

Other

Observable

Inputs

(Level 2) | | Significant

Unobservable

Inputs

(Level 3) | | Total |

| Asset Valuation Inputs | | | | | | | |

| Investments in Securities (a) | | | | | | | |

| Closed-End Funds | $ — | | $ 64,313,318 | | $ — | | $ 64,313,318 |

| Common Stocks | | | | | | | |

| Australia | — | | 69,333,210 | | — | | 69,333,210 |

| China | — | | 74,524,131 | | — | | 74,524,131 |

| France | — | | 88,550,423 | | — | | 88,550,423 |

| Hong Kong | — | | 54,047,867 | | — | | 54,047,867 |

| Ireland | — | | 10,490,156 | | — | | 10,490,156 |

| Italy | — | | 101,543,684 | | — | | 101,543,684 |

| Singapore | — | | 63,724,413 | | — | | 63,724,413 |

| Spain | 49,543,110 | | 87,730,081 | | — | | 137,273,191 |

| United Kingdom | — | | 137,490,016 | | — | | 137,490,016 |

| All Other Countries | 466,695,602 | | — | | — | | 466,695,602 |

| Total Common Stocks | 516,238,712 | | 687,433,981 | | — | | 1,203,672,693 |

| Convertible Preferred Stocks | 116,445,116 | | — | | — | | 116,445,116 |

| Corporate Bonds | — | | 38,727,630 | | — | | 38,727,630 |

| Preferred Stocks | 71,795,819 | | — | | — | | 71,795,819 |

| Total Investments in Securities | $ 704,479,647 | | $ 790,474,929 | | $ — | | $ 1,494,954,576 |

| (a) | For a complete listing of investments and their industries, see the Portfolio of Investments. |

The table below sets forth the diversification of the Fund’s investments by Megatrend Themes.

Megatrend Themes

| | Value | | Percent |

| Decarbonization | $ 778,061,842 | | 72.2% |

| Asset Modernization | 516,612,276 | | 48.0 |

| Digital Transformation | 200,280,458 | | 18.6 |

| | 1,494,954,576 | | 138.8 |

| Line of Credit Borrowing | (427,000,000) | | (39.6) |

| Other Assets, Less Liabilities | 9,296,833 | | 0.8 |

| Net Assets | $1,077,251,409 | | 100.0% |

| † Percentages indicated are based on Fund net assets applicable to Common Shares |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

| 12 | MainStay CBRE Global Infrastructure Megatrends Fund |

Statement of Assets and Liabilities as of May 31, 2022

| Assets |

Investment in securities, at value

(identified cost $1,466,287,184) | $1,494,954,576 |

| Cash | 314,276 |

Cash denominated in foreign currencies

(identified cost $101,082) | 101,101 |

| Receivables: | |

| Dividends and interest | 9,131,148 |

| Investment securities sold | 3,691,867 |

| Other assets | 38,986 |

| Total assets | 1,508,231,954 |

| Liabilities |

| Payable for Line of Credit | 427,000,000 |

| Payables: | |

| Investment securities purchased | 1,332,571 |

| Manager (See Note 3) | 1,248,140 |

| Shareholder communication | 289,805 |

| Custodian | 73,265 |

| Professional fees | 47,400 |

| Transfer agent | 5,701 |

| Trustees | 396 |

| Accrued expenses | 39,605 |

| Interest expense and fees payable | 943,662 |

| Total liabilities | 430,980,545 |

| Net assets applicable to Common shares | $1,077,251,409 |

| Common shares outstanding | 52,047,534 |

| Net asset value per Common share (Net assets applicable to Common shares divided by Common shares outstanding) | $ 20.70 |

| Net Assets Applicable to Common Shares Consist of |

| Common shares, $0.001 par value per share, unlimited number of shares authorized | $ 52,048 |

| Additional paid-in-capital | 1,040,557,027 |

| | 1,040,609,075 |

| Total distributable earnings (loss) | 36,642,334 |

| Net assets applicable to Common shares | $1,077,251,409 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

13

Statement of Operations for the period October 27, 2021 (commencement of operations) through May 31, 2022

| Investment Income (Loss) |

| Income | |

| Dividends-unaffiliated (net of foreign tax withholding of $2,857,635) | $40,083,705 |

| Interest | 1,321,426 |

| Dividends-affiliated | 2,557 |

| Total income | 41,407,688 |

| Expenses | |

| Manager (See Note 3) | 8,317,624 |

| Interest expense and fees | 2,198,776 |

| Excise tax | 341,605 |

| Professional fees | 315,180 |

| Shareholder communication | 309,423 |

| Trustees | 131,189 |

| Custodian | 105,436 |

| Transfer agent | 18,868 |

| Miscellaneous | 110,062 |

| Total expenses | 11,848,163 |

| Net investment income (loss) | 29,559,525 |

| Realized and Unrealized Gain (Loss) |

| Net realized gain (loss) on: | |

| Unaffiliated investment transactions | 6,631,492 |

| Foreign currency transactions | (393,351) |

| Net realized gain (loss) | 6,238,141 |

| Net change in unrealized appreciation (depreciation) on: | |

| Unaffiliated investments | 28,667,392 |

| Translation of other assets and liabilities in foreign currencies | 19,411 |

| Net change in unrealized appreciation (depreciation) | 28,686,803 |

| Net realized and unrealized gain (loss) | 34,924,944 |

Net increase (decrease) in net assets to Common shares

resulting from operations | $64,484,469 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

| 14 | MainStay CBRE Global Infrastructure Megatrends Fund |

Statement of Changes in Net Assets

for the period October 27, 2021 (commencement of operations) through May 31, 2022

| | 2022 |

| Increase (Decrease) in Net Assets Applicable to Common Shares |

| Operations: | |

| Net investment income (loss) | $ 29,559,525 |

| Net realized gain (loss) | 6,238,141 |

| Net change in unrealized appreciation (depreciation) | 28,686,803 |

| Net increase (decrease) in net assets applicable to Common shares resulting from operations | 64,484,469 |

| Distributions to Common shareholders | (28,183,740) |

Capital share transactions

(Common shares): | |

| Net proceeds from sales of shares | 1,040,850,680 |

| Net increase (decrease) in net assets applicable to Common shares | 1,077,151,409 |

| Net Assets Applicable to Common Shares |

| Beginning of period | 100,000 |

| End of period | $1,077,251,409 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

15

Statement of Cash Flows

for the period October 27, 2021 (commencement of operations) through May 31, 2022

| Cash Flows From (Used in) Operating Activities: |

| Net increase in net assets resulting from operations | $ 64,484,469 |

| Adjustments to reconcile net increase in net assets resulting from operations to net cash used in operating activities: | |

| Long term investments purchased | (1,614,041,463) |

| Long term investments sold | 152,281,763 |

| Amortization (accretion) of discount and premium, net | 2,103,989 |

| Increase in investment securities sold receivable | (3,691,867) |

| Increase in dividends and interest receivable | (9,131,148) |

| Increase in other assets | (38,986) |

| Increase in investment securities purchased payable | 1,332,571 |

| Increase in professional fees payable | 47,400 |

| Increase in custodian payable | 73,265 |

| Increase in shareholder communication payable | 289,805 |

| Increase in due to Trustees | 396 |

| Increase in due to manager | 1,248,140 |

| Increase in due to transfer agent | 5,701 |

| Increase in accrued expenses | 39,605 |

| Increase in interest expense and fees payable | 943,662 |

| Net realized gain from investments | (6,631,492) |

| Net change in unrealized (appreciation) depreciation on unaffiliated investments | (28,667,392) |

| Net cash used in operating activities | (1,439,351,582) |

| Cash Flows From (Used in) Financing Activities: |

| Proceeds from shares sold | 1,040,850,680 |

| Proceeds from line of credit | 535,500,000 |

| Payments on line of credit | (108,500,000) |

| Cash distributions paid, net of change in Common share dividend payable | (28,183,740) |

| Net cash from financing activities | 1,439,666,940 |

| Effect of exchange rate changes on cash | 19 |

| Net increase in cash | 315,377 |

| Cash at beginning of period | 100,000 |

| Cash at end of period | $ 415,377 |

| Supplemental disclosure of cash flow information: |

| |

| Cash | $314,276 |

| Cash denominated in foreign currencies | 101,101 |

| Total cash shown in the Statement of Cash Flows | $415,377 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

| 16 | MainStay CBRE Global Infrastructure Megatrends Fund |

Financial Highlights selected per share data and ratios

| | October 27, 2021^ through

May 31, |

| | 2022 |

| Net asset value at beginning of period applicable to Common shares | $ 20.00 |

| Net investment income (loss) (a) | 0.58 |

| Net realized and unrealized gain (loss) | 0.66 |

| Total from investment operations | 1.24 |

| Dividends and distributions to Common shareholders | (0.54) |

| Dilution effect on net asset value from overallotment issuance | 0.00‡ |

| Net asset value at end of period applicable to Common shares | $ 20.70 |

| Market price at end of period applicable to Common shares | $ 18.65 |

| Total investment return on market price (b) | (4.02)% |

| Total investment return on net asset value (b) | 6.28% |

Ratios (to average net assets of Common shareholders)/

Supplemental Data: | |

| Net investment income (loss) | 4.78%†† |

| Net expenses (including interest expense and fees) (c)(d)(e) | 1.92%†† |

| Interest expense and fees (f) | 0.36%†† |

| Portfolio Turnover Rate | 12% |

| Net assets applicable to Common shareholders at end of period (in 000’s) | $ 1,077,251 |

| ^ | Commencement of Operations |

| ‡ | Less than one cent per share. |

| †† | Annualized. |

| (a) | Per share data based on average shares outstanding during the year. |

| (b) | Total investment return on market price is calculated assuming a purchase of a Common share at the market price on the first day and a sale on the last day business day of each month. Dividends and distributions are assumed to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment return on net asset value reflects the changes in net asset value during each period and assumes the reinvestment of dividends and distributions at net asset value on the last business day of each month. This percentage may be different from the total investment return on market price, due to differences between the market price and the net asset value. For periods less than one year, total investment return is not annualized. |

| (c) | Net of Excise tax expense of 0.06%. |

| (d) | In addition to the fees and expenses which the Fund bears directly, it also indirectly bears a pro-rata share of the fees and expenses of the underlying funds in which it invests. Such indirect expenses are not included in the above expense ratios. |

| (e) | The expense ratio is higher than the Fund anticipates for a typical fiscal year due to the short fiscal period and the annualization of all expenses, some of which are fixed or non-recurring. |

| (f) | Interest expense and fees relate to the Line of Credit borrowing (See Note 6). |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

17

Notes to Financial Statements

Note 1–Organization and Business

MainStay CBRE Global Infrastructure Megatrends Fund (the “Fund”) was organized as a Delaware statutory trust on March 30, 2021, and is governed by an agreement and declaration of trust (“Declaration of Trust’’). The Fund is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a “non-diversified”, closed-end management investment company, as those terms are defined in the 1940 Act, as interpreted or modified by regulatory authorities having jurisdiction, from time to time. The Fund first offered Common shares through an initial public offering on October 27, 2021.

Prior to commencement of operations on October 27, 2021, the Fund had no operations other than those relating to organizational matters and the sale of 5,000 common shares on September 17, 2021, to New York Life Investment Management Holdings LLC, the parent company of New York Life Investment Management LLC, for $100,000. Investment operations for the Fund commenced on October 27, 2021.

Pursuant to the terms of the Declaration of Trust, the Fund will commence the process of liquidation and dissolution at the close of business on December 15, 2033 (the “Termination Date”) unless otherwise extended by a majority of the Board of Trustees (the “Board”) (as discussed in further detail below). Upon liquidation and termination of the Fund, shareholders will receive an amount equal to the Fund’s net asset value (���NAV”) at that time, which may be greater or less than the price at which Common shares were issued. The Fund’s investment objectives and policies are not designed to return to investors who purchased Common shares in the initial offering of such shares their initial investment on the Termination Date and such initial investors may receive more or less than their original investment upon termination.

Prior to the commencement of the twelve-month period preceding the Termination Date, a majority of the Board may, without shareholder approval unless such approval is required by the 1940 Act, extend the Termination Date (i) once for up to one year and (ii) once for up to an additional six months (the “Extended Termination Date”), upon a determination that winding up the affairs of and liquidating the Fund would not, given prevailing market conditions, be in the best interests of the Fund’s shareholders. Additionally, if the Fund completes an Eligible Tender Offer (as defined below), a majority of the Board may, without shareholder approval unless such approval is required by the 1940 Act, eliminate the Termination Date and cause the Fund to have a perpetual existence as a closed-end fund. An “Eligible Tender Offer” is defined as a tender offer by the Fund to purchase 100% of the then outstanding Common shares of the Fund at a price equal to the NAV per Common share on the expiration date of the tender offer, which shall be as of a date within twelve months preceding the Termination Date.

If the payment for properly tendered Common shares would result in the Fund’s net assets totaling less than $200 million (the “Termination Threshold”), the Eligible Tender Offer shall be canceled, no Common shares will be repurchased pursuant to the Eligible Tender Offer, and the Fund would dissolve as set forth above. If an Eligible Tender Offer is

conducted and the payment for properly tendered Common shares would result in the Fund’s net assets totaling greater than or equal to the Termination Threshold, all Common shares properly tendered and not withdrawn will be purchased by the Fund pursuant to the terms of the Eligible Tender Offer. The Fund may conduct an Eligible Tender Offer upon the affirmative vote of a majority of the Board - or by an instrument signed by a majority of the Board - without a vote of the shareholders.

The Fund's investment objective is to seek a high level of total return with an emphasis on current income.

Note 2–Significant Accounting Policies

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic 946 Financial Services—Investment Companies. The Fund prepares its financial statements in accordance with generally accepted accounting principles (“GAAP”) in the United States of America and follows the significant accounting policies described below.

(A) Securities Valuation. Investments are usually valued as of the close of regular trading on the New York Stock Exchange (the "Exchange") (usually 4:00 p.m. Eastern time) on each day the Fund is open for business ("valuation date").

The Board adopted procedures establishing methodologies for the valuation of the Fund's securities and other assets and delegated the responsibility for valuation determinations under those procedures to the Valuation Committee of the Fund (the “Valuation Committee”). The procedures state that, subject to the oversight of the Board and unless otherwise noted, the responsibility for the day-to-day valuation of portfolio assets (including fair value measurements for the Fund's assets and liabilities) rests with New York Life Investment Management LLC (“New York Life Investments” or the "Manager") aided to whatever extent necessary by the Subadvisor (as defined in Note 3(A)). To assess the appropriateness of security valuations, the Manager, the Subadvisor or the Fund's third-party service provider, who is subject to oversight by the Manager, regularly compares prior day prices, prices on comparable securities and the sale prices to the prior and current day prices and challenges prices with changes exceeding certain tolerance levels with third-party pricing services or broker sources.

The Board authorized the Valuation Committee to appoint a Valuation Subcommittee (the “Subcommittee”) to establish the prices of securities for which market quotations are not readily available or the prices of which are not otherwise readily determinable under the procedures. The Subcommittee meets (in person, via electronic mail or via teleconference) on an as-needed basis. The Valuation Committee meets to ensure that actions taken by the Subcommittee were appropriate.

For those securities valued through either a standardized fair valuation methodology or a fair valuation measurement, the Subcommittee deals with such valuation and the Valuation Committee reviews and affirms, if appropriate, the reasonableness of the valuation based on such

| 18 | MainStay CBRE Global Infrastructure Megatrends Fund |

methodologies and measurements on a regular basis after considering information that is reasonably available and deemed relevant by the Valuation Committee. Any action taken by the Subcommittee with respect to the valuation of a portfolio security or other asset is submitted for review and ratification (if appropriate) to the Valuation Committee and the Board at the next regularly scheduled meeting.

"Fair value" is defined as the price the Fund would reasonably expect to receive upon selling an asset or liability in an orderly transaction to an independent buyer in the principal or most advantageous market for the asset or liability. Fair value measurements are determined within a framework that establishes a three-tier hierarchy that maximizes the use of observable market data and minimizes the use of unobservable inputs to establish a classification of fair value measurements for disclosure purposes. "Inputs" refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, such as the risk inherent in a particular valuation technique used to measure fair value using a pricing model and/or the risk inherent in the inputs for the valuation technique. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s own assumptions about the assumptions market participants would use in pricing the asset or liability based on the information available. The inputs or methodology used for valuing assets or liabilities may not be an indication of the risks associated with investing in those assets or liabilities. The three-tier hierarchy of inputs is summarized below.

| • | Level 1—quoted prices in active markets for an identical asset or liability |

| • | Level 2—other significant observable inputs (including quoted prices for a similar asset or liability in active markets, interest rates and yield curves, prepayment speeds, credit risk, etc.) |

| • | Level 3—significant unobservable inputs (including the Fund's own assumptions about the assumptions that market participants would use in measuring fair value of an asset or liability) |

The level of an asset or liability within the fair value hierarchy is based on the lowest level of an input, both individually and in the aggregate, that is significant to the fair value measurement. The aggregate value by input level of the Fund’s assets and liabilities as of May 31, 2022, is included at the end of the Portfolio of Investments.

The Fund may use third-party vendor evaluations, whose prices may be derived from one or more of the following standard inputs, among others:

| • Broker/dealer quotes | • Benchmark securities |

| • Two-sided markets | • Reference data (corporate actions or material event notices) |

| • Bids/offers | • Monthly payment information |

| • Industry and economic events | • Reported trades |

An asset or liability for which market values cannot be measured using the methodologies described above is valued by methods deemed reasonable in good faith by the Valuation Committee, following the procedures established by the Board, to represent fair value. Under these procedures, the Fund generally uses a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values and other relevant information. The Fund may also use an income-based valuation approach in which the anticipated future cash flows of the asset or liability are discounted to calculate fair value. Discounts may also be applied due to the nature and/or duration of any restrictions on the disposition of the asset or liability. Fair value represents a good faith approximation of the value of a security. Fair value determinations involve the consideration of a number of subjective factors, an analysis of applicable facts and circumstances and the exercise of judgment. As a result, it is possible that the fair value for a security determined in good faith in accordance with the Fund's valuation procedures may differ from valuations for the same security determined by other funds using their own valuation procedures. Although the Fund's valuation procedures are designed to value a security at the price the Fund may reasonably expect to receive upon the security's sale in an orderly transaction, there can be no assurance that any fair value determination thereunder would, in fact, approximate the amount that the Fund would actually realize upon the sale of the security or the price at which the security would trade if a reliable market price were readily available. During the period October 27, 2021 (commencement of operations) through May 31, 2022, there were no material changes to the fair value methodologies.

Securities which may be valued in this manner include, but are not limited to: (i) a security for which trading has been halted or suspended; (ii) a debt security that has recently gone into default and for which there is not a current market quotation; (iii) a security of an issuer that has entered into a restructuring; (iv) a security that has been delisted from a national exchange; (v) a security for which the market price is not readily available from a third-party pricing source or, if so provided, does not, in the opinion of the Manager or the Subadvisor, reflect the security's market value; (vi) a security subject to trading collars for which no or limited trading takes place; and (vii) a security whose principal market has been temporarily closed at a time when, under normal conditions, it would be open. Securities valued in this manner are generally categorized as Level 3 in the hierarchy. No securities held by the Fund as of May 31, 2022, were fair valued in such a manner.

Certain securities and closed-end funds held by the Fund may principally trade in foreign markets. Events may occur between the time the foreign markets close and the time at which the Fund's NAVs are calculated. These events may include, but are not limited to, situations relating to a single issuer in a market sector, significant fluctuations in U.S. or foreign markets, natural disasters, armed conflicts, governmental actions or other developments not tied directly to the securities markets. Should the Manager or the Subadvisor conclude that such events may have affected the accuracy of the last price of such securities reported on the local foreign market, the Subcommittee may, pursuant to procedures adopted

Notes to Financial Statements (continued)

by the Board, adjust the value of the local price to reflect the estimated impact on the price of such securities as a result of such events. In this instance, securities are generally categorized as Level 3 in the hierarchy. Additionally, certain foreign equity securities are also fair valued whenever the movement of a particular index exceeds certain thresholds. In such cases, the securities are fair valued by applying factors provided by a third-party vendor in accordance with valuation procedures adopted by the Board and are generally categorized as Level 2 in the hierarchy. Securities that were fair valued in such a manner as of May 31, 2022, are shown in the Portfolio of Investments.

If the principal market of certain foreign equity securities is closed in observance of a local foreign holiday, these securities are valued using the last closing price of regular trading on the relevant exchange and fair valued by applying factors provided by a third-party vendor in accordance with valuation procedures adopted by the Board. These securities are generally categorized as Level 2 in the hierarchy. No securities held by the Fund as of May 31, 2022, were fair valued in such a manner.

Equity securities are valued at the last quoted sales prices as of the close of regular trading on the relevant exchange on each valuation date. Securities that are not traded on the valuation date are valued at the mean of the last quoted bid and ask prices. Prices are normally taken from the principal market in which each security trades. These securities are generally categorized as Level 1 in the hierarchy.

Debt securities (other than convertible and municipal bonds) are valued at the evaluated bid prices (evaluated mean prices in the case of convertible and municipal bonds) supplied by a pricing agent or broker selected by the Manager, in consultation with the Subadvisor. The evaluations are market-based measurements processed through a pricing application and represents the pricing agent’s good faith determination as to what a holder may receive in an orderly transaction under market conditions. The rules-based logic utilizes valuation techniques that reflect participants’ assumptions and vary by asset class and per methodology, maximizing the use of relevant observable data including quoted prices for similar assets, benchmark yield curves and market corroborated inputs. The evaluated bid or mean prices are deemed by the Manager, in consultation with the Subadvisor, to be representative of market values at the regular close of trading of the Exchange on each valuation date. Debt securities purchased on a delayed delivery basis are marked to market daily until settlement at the forward settlement date. Debt securities, including corporate bonds, U.S. government and federal agency bonds, municipal bonds, foreign bonds, convertible bonds, asset-backed securities and mortgage-backed securities are generally categorized as Level 2 in the hierarchy.

In calculating NAV, each closed-end fund is valued at market value, which will generally be determined using the last reported official closing or last trading price on the exchange or market on which the security is primarily traded at the time of valuation. Price information on closed-end funds is taken from the exchange where the security is primarily traded. In addition, because closed-end funds and exchange-traded funds trade on a secondary market, their shares may trade at a premium or discount to

the actual net asset value of their portfolio securities and their shares may have greater volatility because of the potential lack of liquidity. These closed-end funds are generally categorized as Level 1 in the hierarchy.

The information above is not intended to reflect an exhaustive list of the methodologies that may be used to value portfolio investments. The valuation procedures permit the use of a variety of valuation methodologies in connection with valuing portfolio investments. The methodology used for a specific type of investment may vary based on the market data available or other considerations. The methodologies summarized above may not represent the specific means by which portfolio investments are valued on any particular business day.

(B) Income Taxes. The Fund's policy is to comply with the requirements of the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), applicable to regulated investment companies and to distribute all of its taxable income to the shareholders of the Fund within the allowable time limits.

The Manager evaluates the Fund’s tax positions to determine if the tax positions taken meet the minimum recognition threshold in connection with accounting for uncertainties in income tax positions taken or expected to be taken for the purposes of measuring and recognizing tax liabilities in the financial statements. Recognition of tax benefits of an uncertain tax position is permitted only to the extent the position is “more likely than not” to be sustained assuming examination by taxing authorities. The Manager analyzed the Fund's tax positions taken on federal, state and local income tax returns for all open tax years (for up to three tax years) and has concluded that no provisions for federal, state and local income tax are required in the Fund's financial statements. The Fund's federal, state and local income tax and federal excise tax returns for tax years for which the applicable statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state and local departments of revenue.

(C) Foreign Taxes. The Fund may be subject to foreign taxes on income and other transaction-based taxes imposed by certain countries in which it invests. A portion of the taxes on gains on investments or currency purchases/repatriation may be reclaimable. The Fund will accrue such taxes and reclaims as applicable, based upon its current interpretation of tax rules and regulations that exist in the markets in which it invests.

The Fund may be subject to taxation on realized capital gains, repatriation proceeds and other transaction-based taxes imposed by certain countries in which it invests. The Fund will accrue such taxes as applicable based upon its current interpretation of tax rules and regulations that exist in the market in which it invests. Capital gains taxes relating to positions still held are reflected as a liability in the Statement of Assets and Liabilities, as well as an adjustment to the Fund's net unrealized appreciation (depreciation). Taxes related to capital gains realized, if any, are reflected as part of net realized gain (loss) in the Statement of Operations. Changes in tax liabilities related to capital gains taxes on unrealized investment gains, if any, are reflected as part of the change in net unrealized

| 20 | MainStay CBRE Global Infrastructure Megatrends Fund |

appreciation (depreciation) on investments in the Statement of Operations. Transaction-based charges are generally assessed as a percentage of the transaction amount.

(D) Dividends and Distributions to Common Shareholders. Dividends and distributions are recorded on the ex-dividend date. Subject to its managed distribution policy, the Fund intends to distribute monthly all or a portion of its net investment income, including current net realized capital gains, to Common shareholders. The Fund’s monthly distributions may include return of capital, which represents a return of a shareholder’s original investment in the Fund. Dividends and distributions are determined in accordance with federal income tax regulations and may differ from determinations using GAAP. Unless a Common shareholder elects otherwise, all dividends and distributions are reinvested pursuant to the Fund's dividend reinvestment plan. For information on the Fund’s dividend reinvestment plan, please see page 26.

(E) Security Transactions and Investment Income. The Fund records security transactions on the trade date. Realized gains and losses on security transactions are determined using the identified cost method. Dividend income is recognized on the ex-dividend date, net of any foreign tax withheld at the source, and interest income is accrued as earned using the effective interest rate method. Distributions received from real estate investment trusts may be classified as dividends, capital gains and/or return of capital. Discounts and premiums on securities purchased by the Fund, other than temporary cash investments that mature in 60 days or less at the time of purchase, are accreted and amortized, respectively, using the effective interest rate method.

(F) Expenses. The expenses borne by the Fund, including those of related parties to the Fund, are shown in the Statement of Operations. Certain expenses of the Fund are allocated in proportion to other funds within the MainStay Group of Funds.

Additionally, the Fund may invest in other funds, which are subject to management fees and other fees that may cause the costs of investing in other funds to be greater than the costs of owning the underlying securities directly. These indirect expenses of other funds are not included in the amounts shown as expenses in the Statement of Operations or in the expense ratios included in the Financial Highlights.

(G) Organizational Expenses and Offering Costs. Prior to the commencement of operations, organizational expenses associated with the establishment of the Fund and offering costs of the Fund with respect to the issuance of shares in the amounts of $458,151 and $437,128, respectively, were shared equally by the Manager and Subadvisor. The Fund is not obligated to repay any such organizational expenses or offering costs paid by the Manager and Subadvisor.

(H) Use of Estimates. In preparing financial statements in conformity with GAAP, the Manager makes estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates and assumptions.

(I) Foreign Currency Transactions. The Fund's books and records are maintained in U.S. dollars. Prices of securities denominated in foreign currency amounts are translated into U.S. dollars at the mean between the buying and selling rates last quoted by any major U.S. bank at the following dates:

(i) market value of investment securities, other assets and liabilities— at the valuation date; and

(ii) purchases and sales of investment securities, income and expenses—at the date of such transactions.

The assets and liabilities that are denominated in foreign currency amounts are presented at the exchange rates and market values at the close of the period. The realized and unrealized changes in net assets arising from fluctuations in exchange rates and market prices of securities are not separately presented.

Net realized gain (loss) on foreign currency transactions represents net currency gains or losses realized as a result of differences between the amounts of securities sale proceeds or purchase cost, dividends, interest and withholding taxes as recorded on the Fund's books, and the U.S. dollar equivalent amount actually received or paid. Net currency gains or losses from valuing such foreign currency denominated assets and liabilities, other than investments at valuation date exchange rates, are reflected in unrealized foreign exchange gains or losses.

(J) Statement of Cash Flows. The cash amount shown in the Fund’s Statement of Cash Flows is the amount included in the Fund’s Statement of Assets and Liabilities and represents the cash on hand at its custodian and restricted cash, if any, as of May 31, 2022.

(K) Foreign Securities Risk. The Fund invests in foreign securities, which carry certain risks that are in addition to the usual risks inherent in domestic securities. These risks include those resulting from currency fluctuations, future adverse political or economic developments and possible imposition of currency exchange blockages or other foreign governmental laws or restrictions. These risks are likely to be greater in emerging markets than in developed markets. The ability of issuers of debt securities held by the Fund to meet their obligations may be affected by, among other things, economic or political developments in a specific country, industry or region.

(L) Indemnifications. Under the Fund’s organizational documents, its officers and trustees are indemnified against certain liabilities that may arise out of performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts with third-party service providers that contain a variety of representations and warranties and that may provide general indemnifications. The Fund's maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. The Manager believes that the risk of loss in connection with these potential indemnification obligations is remote. However, there can be no assurance that material liabilities related to such obligations will not arise in the future, which could adversely impact the Fund.

Notes to Financial Statements (continued)

Note 3–Fees and Related Party Transactions

(A) Manager and Subadvisor. New York Life Investments, a registered investment adviser and an indirect, wholly-owned subsidiary of New York Life Insurance Company ("New York Life"), serves as the Fund's Manager pursuant to a Management Agreement ("Management Agreement"). The Manager provides offices, conducts clerical, recordkeeping and bookkeeping services and keeps most of the financial and accounting records required to be maintained by the Fund. Except for the portion of salaries and expenses that are the responsibility of the Fund, the Manager pays the salaries and expenses of all personnel affiliated with the Fund and certain operational expenses of the Fund. CBRE Investment Management Listed Real Assets LLC ("CBRE" or the "Subadvisor") a registered investment adviser, serves as Subadvisor to the Fund and is responsible for the day-to-day portfolio management of the Fund. Pursuant to the terms of a Subadvisory Agreement ("Subadvisory Agreement") between New York Life Investments and CBRE, New York Life Investments pays for the services of the Subadvisor.

Under the Management Agreement, the Fund pays the Manager a monthly fee for the services performed and the facilities furnished at an annual rate of 1.00% of the “Managed Assets”. "Managed Assets" is defined as the Fund's total assets, including assets attributable to any form of leverage minus liabilities (other than debt representing leverage and the aggregate liquidation preference of any preferred shares that may be outstanding).

During the period October 27, 2021 (commencement of operations) through May 31, 2022, New York Life Investments earned fees from the Fund in the amount of $8,317,624 and paid the Subadvisor in the amount of $4,158,815.

JPMorgan Chase Bank, N.A. ("JPMorgan") provides sub-administration and sub-accounting services to the Fund pursuant to an agreement with New York Life Investments. These services include calculating the daily NAVs of the Fund, maintaining the general ledger and sub-ledger accounts for the calculation of the Fund's NAVs, and assisting New York Life Investments in conducting various aspects of the Fund's administrative operations. For providing these services to the Fund, JPMorgan is compensated by New York Life Investments.

Pursuant to an agreement between the Fund and New York Life Investments, New York Life Investments is responsible for providing or procuring certain regulatory reporting services for the Fund. The Fund will reimburse New York Life Investments for the actual costs incurred by New York Life Investments in connection with providing or procuring these services for the Fund.

(B) Transfer, Dividend Disbursing and Shareholder Servicing Agent. Computershare Trust Company, N.A. (“Computershare”), 150 Royall Street, Canton, Massachusetts, 02021, is the Fund’s transfer, dividend disbursing and shareholder servicing agent pursuant to an agreement between the Fund and Computershare.

Note 4–Federal Income Tax

As of May 31, 2022, the cost and unrealized appreciation (depreciation) of the Fund’s investment portfolio, including applicable derivative contracts and other financial instruments, as determined on a federal income tax basis, were as follows:

| | Federal Tax

Cost | Gross

Unrealized

Appreciation | Gross

Unrealized

(Depreciation) | Net

Unrealized

Appreciation/

(Depreciation) |

| Investments in Securities | $1,469,142,284 | $86,652,432 | $(60,840,140) | $25,812,292 |

As of May 31, 2022, the components of accumulated gain (loss) on a tax basis were as follows:

Ordinary

income | Accumulated

Capital

and Other

Gain (Loss) | Other

Temporary

Differences | Unrealized

Appreciation

(Depreciation) | Total

Accumulated

Gain (Loss) |

| $10,810,632 | $— | $— | $25,831,702 | $36,642,334 |

The difference between book-basis and tax-basis unrealized appreciation (depreciation) is primarily due to wash sales, a debt security treated as equity for tax, and Passive Foreign Investment Company (“PFIC”) adjustments.

The following table discloses the current year reclassifications between total distributable earnings (loss) and additional paid-in capital arising from permanent differences; net assets as of May 31, 2022 were not affected.

| | Total

Distributable

Earnings (Loss) | Additional

Paid-In

Capital |

| | $341,605 | $(341,605) |

The reclassifications for the Fund are primarily due to excise tax paid.

During the year ended May 31, 2022, the tax character of distributions paid as reflected in the Statements of Changes in Net Assets was as follows:

| | 2022 |

| Distributions paid from: | |

| Ordinary Income | $28,183,740 |

Note 5–Custodian

JPMorgan is the custodian of cash and securities held by the Fund. Custodial fees are charged to the Fund based on the Fund's net assets and/or the market value of securities held by the Fund and the number of certain transactions incurred by the Fund.

| 22 | MainStay CBRE Global Infrastructure Megatrends Fund |

Note 6–Line of Credit

The Fund maintains a line of credit under a credit agreement with The Bank of New York Mellon ("BNY Mellon") dated November 4, 2021 (the "Credit Agreement") in order to achieve its investment objective. The aggregate commitment amount is $500,000,000. Under the Credit Agreement, the Fund is subject to (i) a financing charge of the Overnight Bank Funding Rate plus 0.75% on drawn assets and (ii) a commitment fee at an annual rate of 0.25% of undrawn portions of the credit facility to the extent the credit facility utilization rate is less than 80%. The Credit Agreement expires on May 3, 2023. During the period November 4, 2021 through May 31, 2022, the Fund utilized the line of credit for 197 days, maintained an average daily balance of $404,375,635 at a weighted average interest rate of 0.99% and incurred interest expense in the amount of $2,198,776. As of May 31, 2022, borrowings outstanding with respect to the Fund under the Credit Agreement were $427,000,000. Prior to November 30, 2021, the Fund's aggregate commitment amount was $350,000,000.

Note 7–Purchases and Sales of Securities (in 000’s)

During the period October 27, 2021 (commencement of operations) through May 31, 2022, purchases and sales of securities, other than short-term securities, were $1,614,041 and $152,282, respectively.

Note 8–Capital Share Transactions

Transactions in capital shares for the period October 27, 2021 (commencement of operations) through May 31, 2022, were as follows:

| Common Shares | Shares | Amount |

| Period October 27, 2021 (commencement of operations) through May 31, 2022: | | |

| Shares sold | 52,042,534 | $1,040,850,680 |

Note 9–Other Matters

An outbreak of COVID-19, first detected in December 2019, has developed into a global pandemic and has resulted in travel restrictions, closure of international borders, certain businesses and securities markets, restrictions on securities trading activities, prolonged quarantines, supply chain disruptions, and lower consumer demand, as well as general concern and uncertainty. The continued impact of COVID-19 and related variants is uncertain and could further adversely affect the global economy, national economies, individual issuers and capital markets in unforeseeable ways and result in a substantial and extended economic downturn. Developments that disrupt global economies and financial markets, such as COVID-19, may magnify factors that affect the Fund's performance.

Note 10–Subsequent Events

In connection with the preparation of the financial statements of the Fund as of and for the period October 27, 2021 (commencement of operations) through May 31, 2022, events and transactions subsequent to May 31, 2022, through the date the financial statements were issued have been evaluated by the Manager for possible adjustment and/or disclosure. No subsequent events requiring financial statement adjustment or disclosure have been identified, other than the following:

On July 15, 2022, the Fund declared a dividend in the amount of $0.1083 per Common share, payable July 29, 2022, to shareholders of record on July 25, 2022.

Report of Independent Registered Public Accounting Firm

To the Shareholders of the Fund and Board of Trustees

MainStay CBRE Global Infrastructure Megatrends Fund:

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of MainStay CBRE Global Infrastructure Megatrends Fund (the Fund), including the portfolio of investments, as of May 31, 2022, the related statements of operations, changes in net assets, and cash flows for the period from October 27, 2021 (commencement of operations) through May 31, 2022, and the related notes (collectively, the financial statements) and the financial highlights for the period from October 27, 2021 through May 31,2022. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Fund as of May 31, 2022, the results of its operations, changes in its net assets, cash flows, and the financial highlights for the period from October 27, 2021 through May 31,2022, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion